Abstract

This article investigates the effect of different economic and financial crises, such as inflation crisis, stock market crash, debt crisis, and banking crisis on international tourism flows using a panel gravity data set of 200 countries over the period 1995 to 2010. The results show that the inflation crisis has a dampening effect on international tourism flows in both the host and origin countries. The results also show that domestic debt crisis encourages international tourism arrivals in the host countries, whereas its impact on international tourism services in originating countries is negative. Further, the impact of these crises on tourism is region dependent. In particular, banking crisis depresses international tourism flows in host countries situated in regions such as America and Latin America and Caribbean, whereas its impact on originating countries located in regions such as Asia and the Middle East is insignificant.

Introduction

Economic and financial crises often have persistent and devastating macroeconomic impacts. For instance, they usually result in lower GDP growth and rising unemployment (Reinhart and Rogoff 2009, 2011; Andersson 2016). Crises originating in one sector of the economy tend to spread across to different economic sectors. However, the impact crises have on the respective sectors of an economy is unique (Andersson and Karpestam 2014; Dell’Ariccia, Detragiache, and Rajan 2008). Tourism is one sector that is often adversely hit by economic and financial crises.

In recent times, the major crises to hit the tourism sector include the Asian Financial Crisis (AFC) in 1997 and the Global Financial Crisis (GFC) in 2007–2008 (Papatheodorou, Rosselló, and Xiao 2010). The effect of these crises on the tourism sector is still under investigation in the literature. Some studies report the crippling effects of crises on tourism (Dwyer et al. 2006; Papatheodorou, Rosselló, and Xiao 2010; Wang 2009). However, some, such as Hall (2010), question how crises are conceptualized and measured, such as conflating economic and financial crises with other events such as terrorist attacks, oil crises, and climate change. As such, the validity of such findings has been called into question. In contrast, others, including Sheldon and Dwyer (2010), believe that crises are opportunities for the tourism sector to shape up and become more competitive.

One possible explanation for the less convincing results in the empirical literature that relates to crises and tourism is that most studies focus only on a few major financial crises such as the AFC or GFC without disentangling these major events into different types of crises (Prideaux 1999; Ritchie, Amaya Molinar, and Frechtling 2010). Reinhart and Rogoff (2011) distinguish economic and financial crises into different types, namely inflation crises, sovereign debt crises, banking crises, and stock market crashes. In some cases, a crisis relates only to one of these categories, however, in most cases, it relates to more than one category. For instance, a sovereign debt crisis is often triggered by a banking crisis, forcing the national government to take over debts in the banking sector (Reinhart and Rogoff 2011; Velasco 1987). Similarly, a debt crisis may result in the depreciation of the local currency and spillover into an inflation crisis as a country facing insolvency tend to engage in expansionary monetary policies to reduce the debt burden (Lában and Sturzenegger 1994).

Consequently, the impact of an economic or a financial crisis on international tourism will eventually depend on the nature of the crisis, such as whether it is a stock market crash, inflation, debt or banking crisis, or a mixture of crises. Arguably, some types of economic or financial crises can have more severe or even stimulating effect on international tourism than others. The debt crisis, for instance, may result in the devaluation of the currency, making tourism services cheaper and hence increasing tourism flows. In contrast, an inflation crisis may make tourism services more expensive, resulting in lower tourism flows. Therefore, it is crucial to distinguish between various types of crises.

Further, past studies only focus on a certain crisis that is global in nature, such as AFC or GFC, while completely ignoring the localized crises that may have affected a particular country or region. An example of such a crisis was the hyperinflation crisis in Zimbabwe in 2008 or a prolonged sovereign debt crisis in Russia in the 1990s. Besides, many of the existing studies focus on analyzing the impact of the crisis on tourism from the perspective of either origin or destination countries or on one country or a region. For example, Li, Blake, and Cooper (2010) and Page, Song, and Wu (2012) explore the effect of the GFC on China and United Kingdom, respectively.

Considering these gaps in the literature, this study explores the effects of different economic and financial crises, such as inflation crisis, stock market crash, and domestic and external sovereign debt crisis and banking crisis on international tourism using a panel gravity data set of 200 countries from 1995 to 2010. This article contributes to the literature that relates to crisis and tourism in a number of ways. First, while previous studies focus on one particular global crisis, we distinguish between different types of economic and financial crises, such as inflation crisis, sovereign debt crisis, stock market crash, and banking crisis inter alia. Second, by utilizing a comprehensive crises data set from Reinhart and Rogoff (2011), this article captures crises that have both global and local ramifications. Third, we use a gravity model to capture the effect of crises on both inbound and outbound tourism demand of the country-pairs. More specifically, we analyze to what extent different types of crises affect international tourism flows from the perspective of both the origin and destination countries rather than the extant literature that focuses on the crisis in either origin or destination countries.

Our results show that the inflation crisis has a depressing effect on inbound and outbound international tourism. In the presence of inflation crisis, the demand for tourism service and spending decline as high levels of inflation lead to the erosion of consumers’ purchasing power. Further, stock market crash dampens international tourism flows in destination countries, whereas its impact in the originating countries is not significant. During the period of stock market turmoil, businesses cut back on travel expenses, thereby reducing demand for high-end hotel rooms. Moreover, domestic debt crisis leads to an increase in international tourism arrivals in the destination countries, whereas the demand for international tourism services declines in the originating countries in the presence of a domestic debt crisis. During the period of the domestic debt crisis, domestic currency usually loses significant value relative to a basket of international currencies. The destination country is thus more attractive for international tourists as the overall costs of international tourism services fall. In contrast, when the domestic currency devalues substantially in the originating countries, potential tourists have less purchasing power, and as a result, the demand for international tourism declines.

The results also show that the effects of different crises on international tourism are region dependent. For instance, inflation crisis has a strong negative impact on international tourism flows in destination countries situated in regions such as America, Latin America and Caribbean (LATCA), whereas its impact in destination countries located in Europe and Sub-Saharan Africa (SSA) is statistically insignificant. On the one hand, inflation crisis is accompanied by a sharp drop in consumer purchasing power, thus, explaining the negative link between inflation crisis and international tourism. On the other hand, in general, the demand for international tourism services in Africa is quite low, while European countries are close to one another in terms of distance. Therefore, low demand and distance could help to explain why inflation crisis is not a strong deriving factor in these regions.

The rest of the article is organized as follows. The next section presents a literature review on the crises–tourism nexus. The third section discusses the data and methodology used in the article followed by the discussion of the results. The final section concludes the article.

Literature Review

There is an emerging, albeit short, list of studies that try to understand the effects of crises on the tourism sector. The early “crisis literature” focus on assessing the effect of the AFC on Asia-Pacific countries, such as Malaysia and Thailand. The methodologies used in this type of studies involved a qualitative analysis of secondary data. For instance, Kontogeorgopoulos (1999) explored the interplay between sustainable development and sustainable tourism in Thailand in the face of the AFC. Because of the crisis, Thailand was forced to forego the long-term ecological sustainability of tourism and, thus, encouraged rapid growth in tourism to earn much needed foreign currency.

Prideaux (1999) examined the impact of the Asian Financial Crisis on tourism in East Asia and concluded that the effects of the crisis were not as harmful as anticipated. This, according to the author, was evidence that tourism was more resilient than previously thought. The need for further and more comprehensive analysis of the impacts of crises on tourism was also stressed. De Sausmarez (2004) explored the Malaysian tourism industry’s response to the Asian Financial Crisis and crisis management capability. The author identified Malaysia’s most successful response to the AFC as international marketing campaigns and policies aimed at boosting domestic tourism as well as encouraging arrivals from new markets.

B. A. Anderson (2006) assessed the preparedness of the Australian tourism industry to shocks and crises, including AFC and the Bali terrorist attack. The analysis concluded that the tourism industry in Australia was unprepared to handle such shocks and crises and learned little from these events. Ritchie, Amaya Molinar, and Frechtling (2010) tried to determine the impact of the economic crises—the GFC and other crises—on tourism in North America. They conducted this “backgrounder” analysis by considering the descriptive statistics on tourism in North American countries. Results showed that tourism in Canada and the USA were substantially affected by the GFC, and the effect is expected to linger. In Mexico, however, the effects of economic crises initiated by the swine flu pandemic, exchange rates, and the weather conditions were more prevalent than the GFC.

The literature then evolved to Computable General Equilibrium (CGE) modeling, which involves quantitative simulation, using sectoral input-output analysis, of the effect of shocks and crises on the economies studied. However, CGE studies are often limited in numbers because of the requirement of extensive sectoral-level data. Sufficient data on tourism to conduct quantitative analysis are usually hard to come by. Blake and Sinclair (2003) evaluated the policy response of the US tourism industry to the 9/11 terrorist attacks. Their study found targeted sector-specific subsidies and tax reductions to be the most effective means of crisis management in the tourism sector.

Dwyer et al. (2006) explored the economic effects of crises in 2003—the US invasion of Iraq and Severe Acute Respiratory Syndrome (SARS)—on the Australian tourism industry. These crises negatively affected both inbound and outbound tourism. However, the net effect was not as severe because postponement of outbound travel led to higher allocation toward savings, domestic tourism, or the purchases of other goods and services. Li, Blake, and Cooper (2010) conducted tests for the effect of the GFC on tourism in China. Results indicate that tourism expenditure declined in 2008–2009 in China because of the GFC.

Later, as tourism data became more abundant, econometric modeling of tourism demand and forecasting started to become more popular. Wang (2009) assessed the impact of economic crises and macroeconomic activities on international inbound tourism demand in Taiwan. Using the autoregressive distributive lag bounds tests, the study found a negative impact of crises on international tourism demand in Taiwan. The author found that crises related to safety—that is, natural disasters, disease outbreaks, and terrorist attacks—had a more significant effect than those related to the economy. Page, Song, and Wu (2012) estimated the effect of the GFC (which they dubbed an economic crisis) and the Swine Flu epidemic on inbound tourism in the United Kingdom. Findings revealed that the GFC and Swine Flu epidemic had a significant adverse effect on tourist arrivals in the United Kingdom.

Eugenio-Martin and Campos-Soria (2014) assessed the impact of the GFC on the expenditure of tourists from the different regions of Europe. Their methodology included Simultaneous Semi-Ordered Bivariate Probit model as well as GIS and nonparametric analysis. Results indicated that the cutback of tourism expenditure depended heavily on the tourist place of origin’s as well as the origin’s GDP and GDP growth. Perles-Ribes et al. (2016) explored the effect of business cycles and economic crises on the tourism competitiveness in Spain. The methodology incorporated tests for unit roots in Spain share in the world tourism market. Breakpoint unit root tests indicated that the market shares are stationary, and the breakpoints corresponded to major crises. In addition, highly intensive crises were found to have a persistent negative effect on Spanish tourism competitiveness.

Further, other studies implemented forecasting techniques to simulate the effect of crises on tourism. Smeral (2009) tried to decipher the effect of macroeconomic variables on outbound tourism demand for 15 EU countries. Using data on real “tourism imports” and exchange rates, the author projected outbound travel demand in 2009 and 2010—the aftermath of the GFC. Two scenarios were considered: one optimistic and the other pessimistic; tourism declined, albeit to varying extents, in both scenarios for the 15 EU member states. Later, Smeral (2010) modeled and forecasted outbound tourism demand in Australia, Canada, the United States, Japan, and the EU-15 countries over the period 2009–2010—the aftermath of the GFC. The forecasting exercise showed a decline in aggregate demand for foreign travel in 2009. However, the situation was uncertain for 2010; whether the tourism sector would face decline or stagnation. Song and Lin (2010) attempted to forecast inbound and outbound tourism to and from Asia against the backdrop of contemporary financial and economic crisis (mainly the GFC). The forecasting exercise revealed that the crisis was expected to have a negative impact on inbound and outbound Asian tourism, but the effect would dampen by 2010.

The literature also saw the advent of interviews and questionnaire surveys as well as case studies designed to ascertain the impact of crises on tourism. Okumus, Altinay, and Arasli (2005) examined the effects of the political and economic crises occurring in 2001 on tourism demand in Northern Cyprus and Turkey. Their study conducted surveys and interviews to gather information on the impact of the crisis on hotels and their preparedness in anticipating and countering the effects of the crisis. The results show that most hotels in Northern Cyprus were found to be unable to anticipate the crisis and unprepared to handle its aftermath. De Sausmarez (2007) explored how crisis indicators could be used to minimize the negative impacts of crises on the tourism sector and thus ensure sustainable tourism development. Their methodology involved interviewing private and public stakeholders in the Malaysian tourism sector. The article proposed a new crisis indicator—travel trade—and argued that it held the key to observing market trends and minimizing risk to the tourism sector.

Song et al. (2011) conducted a case study on the demand for hotel rooms in Hong Kong against the backdrop of global financial and economic crises. Their findings indicated that the most important factors determining demand are the income of the tourist place of origin and relative price levels. Boukas and Ziakas (2013) tested the effect of the GFC on tourism in Cyprus. The methodology involves “semi-structured” interviews with the parties involved in the tourism service industry. Their study identified the following as the main impacts on tourism in Cyprus: loss of competitiveness, lower number of visitors and decreased revenue, the decline in quality, and increased costs.

Alegre, Mateo, and Pou (2013) examined the Spanish household’s tourism consumption model in the face of the business cycle during the 2006–2010 period using data from the Spanish Household Budget Survey. Their results indicated that unemployment and a higher risk of a job loss substantially reduced tourism “participation and expenditure.” Stylidis and Terzidou (2014) derived a model to survey local residents’ attitude toward tourism in Kavala, Greece. The survey, conducted on 317 citizens, revealed their concerns about their direct (personal) benefit from tourism as well as its impact on the state of the economy.

In view of the above review, only a handful of empirical studies assessed the impact of crises—economic and financial—on tourism. Those that did suffer from a range of weaknesses. Generally, the extant literature examined individual countries or a specific group of countries. Specifically, the early studies relied on descriptive statistics to understand the impact crises had on tourism. However, these studies are incapable of establishing causation between crises and tourism. Later CGE modeling studies involved a more thorough quantitative analysis of the causal links between crises and tourism. However, CGE models “simulate” (a form of projection) the potential effects of crises on tourism. Thus, CGE studies often show what is the “expected effect” rather than estimate the “actual effect” using postcrisis data.

The more recent econometric and forecasting studies offered valuable insights into the issue. However, these studies tended to focus on either inbound or outbound tourism demand model or estimate them separately. In addition, forecasting studies suffer from the same “actual versus expected” effect problem faced by CGE modeling papers. Further, the case studies, interviews, and surveys were very limited in scope as they are conducted on narrow groups of people as well as specific cities and countries. This restricts their ability to decipher the effect of crises on tourism and establish causality that is applicable in general. In general, no study to date has explored the effects of different economic and financial crises, such as inflation crisis, stock market crash, domestic sovereign debt crisis, external sovereign debt crisis, and banking crisis on tourism using gravity approach and cross-country data.

Thus, our review of the literature identifies a significant gap in the discussion relating to the impact of crises on tourism. It is therefore pertinent to adopt a comprehensive and rigorous approach that analyses, using actual data, how different economic and financial crises influence tourists’ behavior in both origin and destination countries in various parts of the globe.

Data and Methodology

Empirical Strategy

The gravity models have been extensively used to explain international trade flows, migration, and foreign direct investment. For instance, gravity model is applied to estimate the determinants of international trade flows (J. E. Anderson and van Wincoop 2003; McCallum 1995; Rose 2000), determinants of migration (Gil-Pareja, Llorca-Vivero, and Martínez-Serrano 2007; Karemera, Oguledo, and Davis 2000), determinants of bilateral foreign direct investment (Bergstrand and Egger 2007; Eichengreen and Tong 2007; Head and Ries 2008), and estimating the openness of a country (Frankel and Romer 1999; Khalid 2017).

As international tourism is a major component of international trade in services, an augmented gravity model, therefore, can be used to explore the determinants and the patterns of international tourism (Khadaroo and Seetanah 2008; Morley, Rosselló, and Santana-Gallego 2014; Santana-Gallego, Ledesma-Rodríguez, and Pérez-Rodríguez 2016). Morley, Rosselló, and Santana-Gallego (2014) provide a theoretical foundation for using a gravity equation to model tourism demand based on individual utility theory. Further, numerous articles have used a gravity equation to empirically model tourism demand (Fourie and Santana-Gallego 2013; Khadaroo and Seetanah 2008; Santana-Gallego, Ledesma-Rodríguez, and Pérez-Rodríguez 2016; Okafor, Khalid, and Then 2018; Vietze 2012).

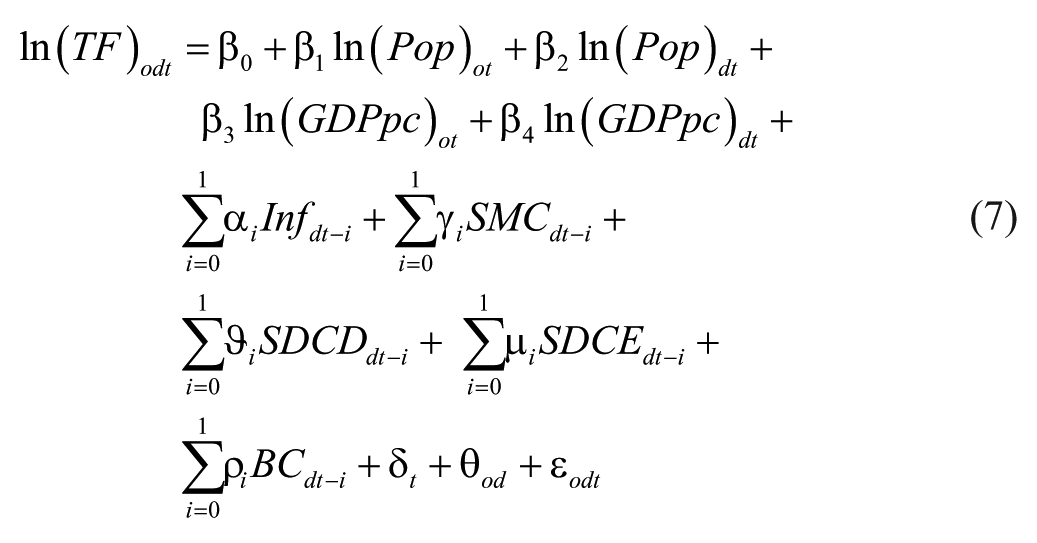

We specify the gravity models for estimating the effects of different crises on tourist flows in line with extant literature. The general tourism demand model from the literature—including Smeral (2009, 2010), Wang (2009), Song and Lin (2010), Song et al. (2011), Page, Song, and Wu (2012), and Shafiullah, Okafor, and Khalid (2018), inter alia—often expresses the tourism/travel as a function of income as well as dummies that represent exceptional events such as festivals, sporting events, and crises: economic and financial as well as those categorized as natural disasters. Accordingly, we specify and estimate a reduced-form baseline augmented panel gravity model in which tourist flows in the destination countries is a function of population, income, and a range of crisis dummies. Equation (1) presents the model for crises in destination countries and is estimated using the fixed effects (FE) approach 1 :

where the “ln” prefix denotes natural logarithm transformation;

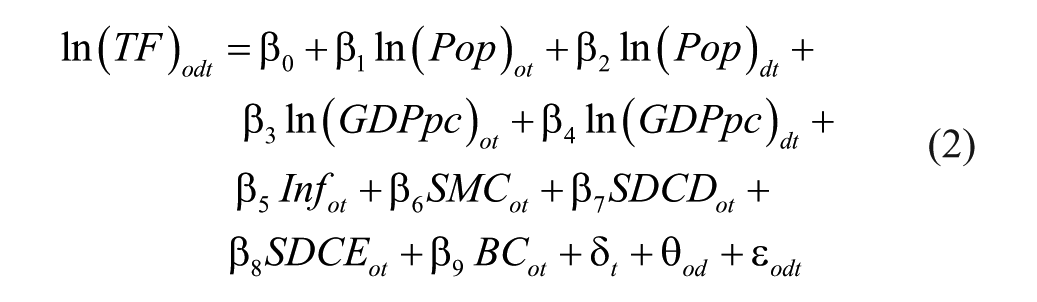

We also assess the impact of different types of crises on international tourist flows when the crises take place in the origin countries. This baseline gravity model is specified as equation (2) and estimated by the FE approach as follows:

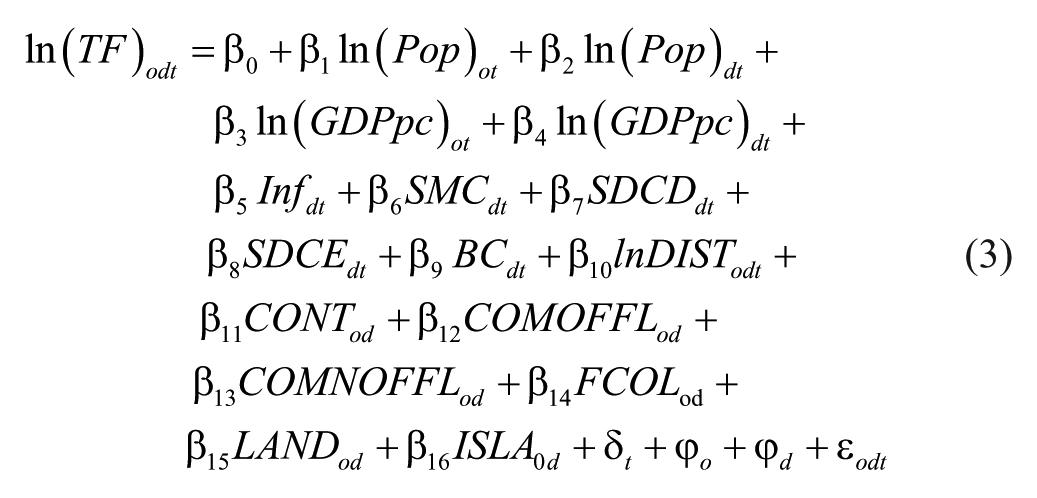

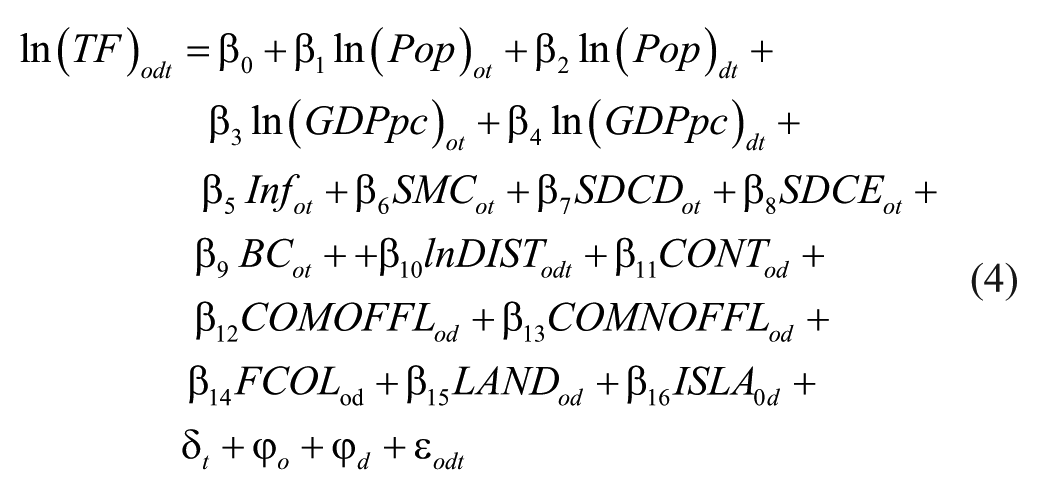

Estimating the gravity model using the FE approach, however, does not allow us to include traditional gravity variables such as geographical features that do not vary over time. Therefore, an alternative specification using the OLS approach is used to check the robustness of the results. The OLS approach allows us to control for gravity variables that do not change over time. The alternative model for exploring the impact of different types of economic and financial crises on tourist flows in the destination countries using an OLS approach is specified as follows:

Similarly, the alternative model for examining the impact of different kinds of economic and financial crises on tourist flows in the origin countries using an OLS approach is specified as follows:

where

Further, in order to check if the results are region dependent, the sample of the study was divided into four subsamples by geographical locations of the destination and origin countries. The sensitivity of the results to geographical locations was tested by reestimating the FE specifications. The four different regions used for the classifications are Europe; North America, Latin American and Caribbean; Asia, Oceania, Middle East, and North Africa; and Sub-Saharan Africa.

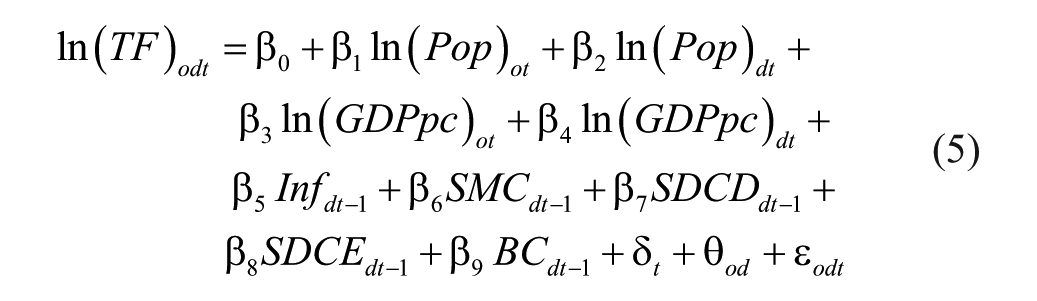

We check the robustness of our results by introducing dynamics in the model. This is achieved using two different approaches. First, instead of using contemporaneous values of the crisis variables in the model, we use the first lag and estimate the following model using FE for the crisis in the destination countries.

Similarly, for the crisis in the origin countries, the following model is estimated using FE:

Second, we estimate the model by adding both the contemporaneous and one-year lagged values of the crisis variables. This model will provide information on whether the effects of different types of crises on international tourism are temporary and short-lived or persists over time. The model for the crisis in the destination is given by the following equation and is estimated using FE.

Similarly, for the origin countries, the following model is estimated using FE.

Overview of Data and Description of Variables

The empirical model is estimated using a panel gravity data set consisting of 200 countries and covering the period 1995 to 2010. Countries and time period are chosen based on data availability. The data on different types of crises were made available by Reinhart and Rogoff (2011). The data have been widely used in previous studies on crises and their economic impact, including Agnello and Sousa (2012), Andersson (2016), Andersson and Karpestam (2014), Furceri and Zdzienicka (2012), inter alia.

The data on variables such as Gross Domestic Product, GDP per capita at PPP, and land area are collected from the World Bank Development Indicators (World Bank 2017). The data pertaining to the flow of visitors distinguished by the country of origin and destination are collected from the UNWTO database (World Tourism Organisation 2017). The data on contiguity, colonial link, and language are obtained from the Gravity database from Head, Mayer, and Ries (2010). A further description of the data and their sources can be found in Table A2 in the Appendix.

Dependent variable

Following most previous studies, we use tourist arrivals to capture tourism demand (Gil-Pareja, Llorca-Vivero, and Martínez-Serrano 2007; Khadaroo and Seetanah 2008; Okafor, Khalid, and Then 2018). Tourist arrivals are a robust measure of tourist flows as it is relatively easier to ascertain the number of individuals entering a country. Tourist expenditures are sometimes used as a measure of tourist flows. However, tourist expenditures are not easily accessible, as they have to be estimated.

Data on tourism receipts included in the balance of payments tend to be limited because of the problem of inaccuracy (Sinclair 1998). However, tourist arrivals and tourism receipts are highly correlated (Neumayer 2004). Given the above submissions, tourist arrival is used as the dependent variable in the empirical analysis.

Explanatory variables

The main variables of interest in the present study are the measures of different types of crises as made available by Reinhart and Rogoff (2011). An inflation crisis is set to 1 when the annual rate of inflation exceeds 20% in time

A banking crisis is measured by a dummy variable that is set to 1 when a bank run leads to bank closure, merger or government takeover or when a bank needs for assistance has a contagious effect on other banking institutions and zero otherwise. As highlighted by Reinhart and Rogoff (2011), due to data limitations, banking crises are measured by the events mentioned above. For instance, the time series on the relative price of bank stocks or financial institutions relative to the market would be a good candidate for capturing banking crisis, however, the time series are not easily accessible, particularly for developing countries.

Domestic debt deals with national debts issued under domestic law. In general, domestic debts are mainly held by residents and also designated in local currency. Domestic debt crises seldom attract widespread attention as the creditors are often not external agents. Further, incidences of domestic defaults are in most cases reported in the footnotes. It also attracts less attention as some domestic defaults that resulted in the conversion of foreign currency into local currency under duress occurred during the periods of hyperinflations or banking crises or a combination of the two crises (Reinhart and Rogoff 2011). A domestic debt crisis therefore takes the value 1 when a country defaults on its domestic debt and zero otherwise. Unlike domestic debt crises, external debt crises that deal with the inability of sovereign governments to pay their debts when due attract a lot of attention. External debt defaults could result from nonpayment or refusal to pay debt obligations or debt restructuring. External debt crisis is therefore set to 1 when a country defaults on its external debt and zero otherwise.

Further, stock market crashes tend to serve as a signal for macroeconomic depressions. Empirical evidence suggests that the likelihood of minor depression is 31%, while that of major depression is 10% following a stock market crash (Barro and Ursúa 2017). In the presence of a stock market crash, investment and consumption are more likely to decline similar to the period of macroeconomic depression. The demand for tourism services and investment in the tourism sector during the period of a stock market crash are more likely to be negatively impacted. To capture the impact of stock market collapse on international tourism flows, a stock market crash is measured by a dummy that is set to 1 when a country’s primary stock market experiences a cumulated multiyear real return of −25% or less and zero otherwise.

To find out the overall effect of different crises on international tourism, an overall crisis indicator destination is set to 1 if a destination experiences any type of economic or financial crisis covered in this study at time

Control variables

Following the literature on the determinants of tourist flows, we control for variables that potentially affect international tourism flows (Gil-Pareja, Llorca-Vivero, and Martínez-Serrano 2007; Khadaroo and Seetanah 2008). In this study, tourist flows are measured by the number of tourists arriving at destination

We also control for the distance between the country of origin and destination. Distance is used as a proxy to capture the cost of travel between the origin and the destination countries. This is in line with the notion of the gravity model, which suggests that tourist flows between country-pair would be higher the closer the distance between them. The closer the distance, the lower the transportation cost, which in turn would lead to an increase in international tourist flows and vice versa. As pointed out by Khadaroo and Seetanah (2008), air travel is the dominant mode of transportation for international tourism. However, the prevalence of price discrimination in the sale of air tickets makes it difficult for one to estimate the cost of travel between pairs of countries.

Similar to extant literature, indicator variables that potentially capture other factors that either increase or decrease the transaction costs of international tourism are controlled for, such as sharing a common official or unofficial language, sharing a common border, having colonial linkage, or being an island or a landlocked country (Okafor, Khalid, and Then 2018; Gil-Pareja, Llorca-Vivero, and Martínez-Serrano 2007). More specifically, cultural and language proximity plays a crucial role in international tourism. We control for the influence of official language on international tourism by including a dummy variable that is set to 1 if the country of origin and destination shares a common official language, and zero otherwise

Further, tourist preferences are more likely to influence international tourism flows. We capture tourist preferences with contiguity and colonial linkage dummies. Contiguity dummy takes the value 1 if the destination and origin countries share a border and 0 otherwise. Colonial linkages are captured using a dummy variable that is set to 1 if the origin country is a former colony of the destination country or the destination country is a former colony of the origin country and zero otherwise.

In addition, we also include an island dummy, which takes the value 1 if the origin country and destination country are an island and 0 otherwise, and a landlocked dummy, which is set to 1 if the origin and destination country are landlocked and zero otherwise. Island nations tend to attract more tourists than landlocked countries. Tourists have the option of traveling by sea if a nation is an Island, which is not a possibility if a country is landlocked. However, the expected link between Island or landlocked variable and international tourism may not hold if most tourists travel by air.

Some variables, such as trade ties, weather and climate, and political instability are excluded from the model. For instance, strong trade ties could develop as a result of the origin and destination countries sharing membership in a regional trade agreement, which in turn can lead to the construction of advanced transport networks and greater promotion of tourism between the two parties, thereby improving international tourism flows. Further, weather and climate can also influence the destination choice of tourists. In addition, political instability potentially has an effect on tourism flows. If there is a high likelihood that a government will be ousted or undermined by force or unconstitutional means, the less likely it is that tourists would like to visit such a country, just like if the probability of terrorism or violence is high (Chasapopoulos, Den Butter, and Mihaylov 2014). Given that, our preferred model is an FE specification; the exclusion of these time-invariant indicators or variables does not introduce any bias in the parameter estimates.

Summary statistics

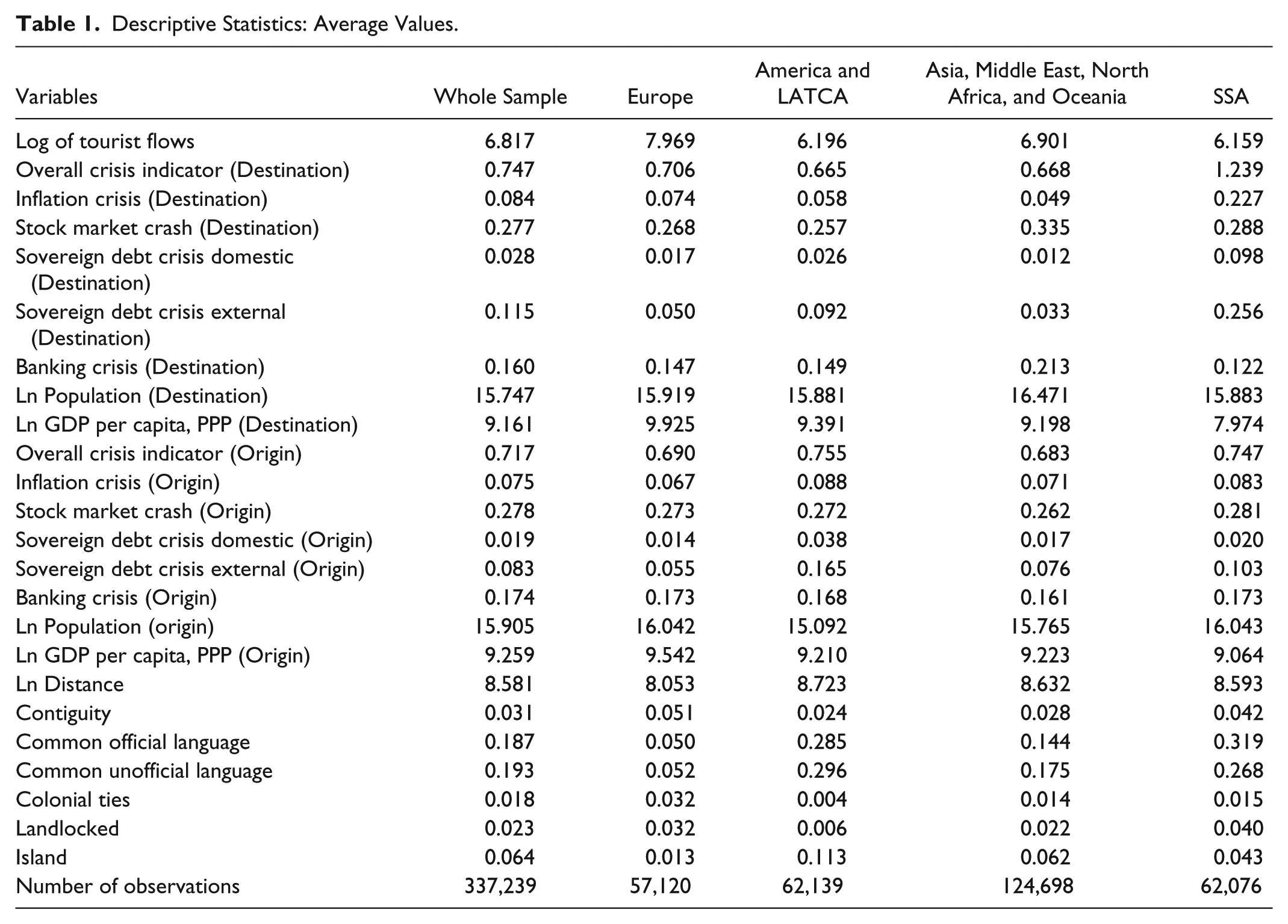

Table 1 presents the summary statistics of the data used in the empirical analysis. Column 1 reports the mean for the whole sample. On average, the probability of occurrence of a financial or economic crisis is 0.74 and 0.71 per year in the destination and origin countries, respectively. With reference to the destination countries, the most commonly occurring crisis is the stock market crash, which has a probability of occurrence of 0.277 per year, followed by the banking crisis and external sovereign debt crisis with probabilities of 0.16 and 0.11 per year, respectively. Similar to destination countries, the leading crisis is stock market crash, followed by banking crisis and external debt crisis.

Descriptive Statistics: Average Values.

On average, destination countries in North America, Latin American, and the Caribbean (America and LATCA) countries experienced a fewer number of crises than other countries (0.665 per year), whereas for Sub-Saharan African (SSA) countries, the average is 1.239 per year. On the contrary, the America and LATCA countries are more likely to experience crises compared to countries in other regions (0.755 per year) followed by SSA countries with crises probability of 0.747 per year.

Stock market crashes are the most prevalent type of crisis in all four regions, both in destination and origin countries. Destination countries in Asia, Middle East, North Africa & Oceania regions are more prone to it with a probability of occurrence of 0.335 per year, followed by destination countries in the SSA. On the other hand, origin countries in the SSA are most likely to experience a stock market crash with a probability of 0.281 per year, followed by origin countries in Europe (0.273 per year).

A banking crisis is the second most prevalent type of crisis in all the regions in terms of both origin and destination countries apart from destination countries in SSA. The probability of a banking crisis for origin countries varies between 0.161 per year in Asia, the Middle East, North Africa, and Oceania to 0.173 per year in Europe and SSA. Similarly, with respect to destination countries, the probability of a banking crisis varies between 0.122 per year in SSA to 0.213 in Asia, Middle East, North Africa, and Oceania. It is important to highlight the pattern of occurrence of crises in SSA countries, where an external debt crisis (0.256 per year) and inflation crisis (0.227 per year) are the most common types of crises behind stock market crashes.

In general, the likely influence of key determinants of international tourism such as distance, language, colonial linkage, landlocked dummy, and the island dummy also differs across regions. For instance, European countries tend to be closer to each other and are more likely to share a common border compared to countries in other regions. On the other hand, Sub-Saharan African countries are more likely to share a common official language than others, whereas America, Latin American and Caribbean countries are more likely to share a common unofficial language than their counterparts.

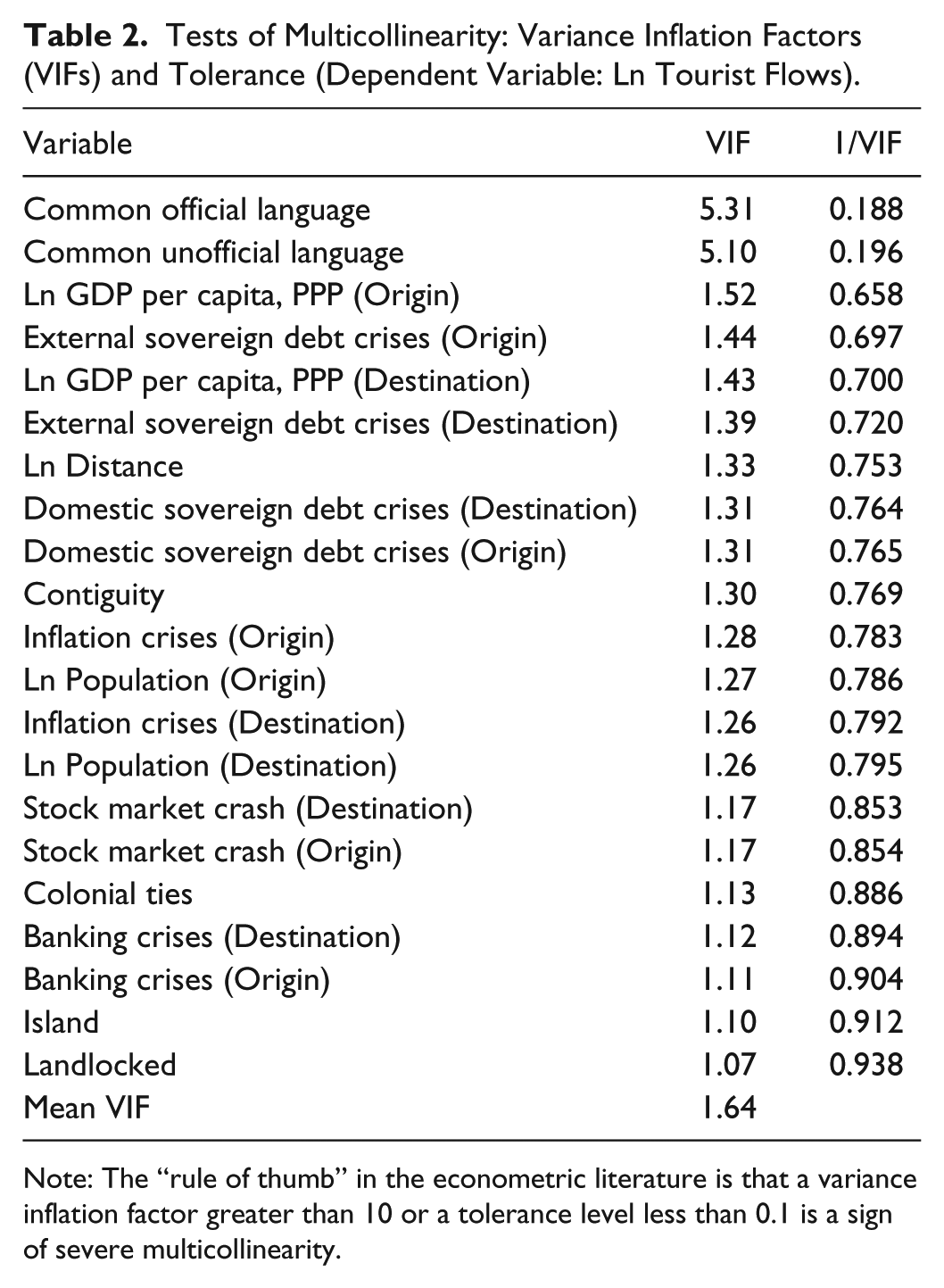

Table 2 reports the test for multicollinearity. The “rule of thumb” in the econometric literature is that a tolerance level of less than 0.1 or variance inflation factors larger than 10 is a sign of a serious multicollinearity problem. As shown in Table 2, there is no strong evidence suggesting the presence of multicollinearity problem.

Tests of Multicollinearity: Variance Inflation Factors (VIFs) and Tolerance (Dependent Variable: Ln Tourist Flows).

Note: The “rule of thumb” in the econometric literature is that a variance inflation factor greater than 10 or a tolerance level less than 0.1 is a sign of severe multicollinearity.

Empirical Results

The Link between Different Types of Crises and International Tourism in the Originating and Destination Countries

The parameter estimates obtained using OLS and FE estimators are presented in Table 3. Columns 1, 2, 4, and 5 report parameter estimates obtained using FE estimator. Columns 3 and 6 report parameter estimates obtained using OLS estimator. As shown in columns 1 and 2, in general, crises broadly measured have a negative effect on international tourism flows in both the originating and destination countries. The parameter estimate from column 1 suggests that destination countries experiencing different types of crises face a reduction in international tourism flows by about 4.40% compared to destination countries that did not experience different types of crises. Similarly, the demand for international tourism decreases by about 1.30% for originating countries experiencing different kinds of crises compared to their counterparts with no such crises.

Link between International Tourism and Crises.

Note: OLS = ordinary least squares; FE = fixed effects estimator. The dependent variable is log of tourist flows; Ln denotes natural logarithms. The numbers in parentheses in columns are robust standard errors. All regressions include constant but they are not reported. Significance at the 1%, 5%, and 10% levels is indicated by ***, **, and *.

The finding that crises dampen international tourism is consistent with the notion that most tourists spend discretionary income on tourism services. Discretionary spending is more susceptible to economic uncertainty and volatility (Papatheodorou, Rosselló, and Xiao 2010). In the presence of different types of economic and financial crises, a significant share of individuals potentially prefers to spend on essentials only and increase savings. A sharp drop in discretionary spending during the period of crisis tends to depress both outbound and inbound international tourist flows.

As reported in columns 1 and 4, population and GDP per capita at purchasing power parity have a significant positive impact on international tourism for both destination and originating countries. This suggests that populous or wealthier destination countries can afford to supply a more significant share of tourism services, whereas the demand for international tourism services is larger for populous or more affluent countries. These findings are consistent with the ones reported by Okafor, Khalid, and Then (2018).

As reported in columns 2, 3, 5, and 6, the effects of economic and financial crises on international tourism tend to vary by destination and originating countries. We discuss the effects of different crises on international tourism focusing on the parameter estimates reported in columns 2 and 5 for three reasons. First, the parameter estimates obtained using FE and OLS estimators are relatively similar in terms of signs. Second, estimates obtained using FE are robust to potential endogeneity issues arising from permanent country-pair specific effects. Third, OLS is used as a robust check.

As shown in columns 2 and 5, the inflation crisis has a significant negative impact on international tourist flows in both destination and originating countries. The coefficient from column 2 indicates that destination countries experiencing inflation crisis face a drop in international tourist arrivals of about 12.89% compared to their counterparts not experiencing such a crisis. In contrast, parameter estimate from column 5 suggests that in the presence of inflation crisis, originating countries’ demand for international tourism services fall by about 13.15% compared to originating countries not experiencing inflation crisis.

During the period of inflation crisis, the rate of inflation exceeds at least 20%. A sharp rise in the general price level corresponds to a sharp drop in consumers’ purchasing power. As a result, the demand for tourism services and spending decline during the period of inflation crisis. As reported by the World Tourism Organisation (2013), the rate of inflation in the Maldives peaked at 17% between 2008 and 2009. As a result, the purchasing power of low-skilled employees was eroded. Further, during the 2008 Global Financial Crisis, a sharp drop in tourists’ spending led to a substantial decrease in the service charge, which constitutes a major source of income for low-skilled workers in the Maldives. The income loss resulting from the decline in demand for tourism services affected 20% to 30% of about 7,000 Maldivian low-skilled tourism employees. In general, about 19% of the Maldivian population, consisting mainly of low-income workers and vulnerable groups were negatively affected in terms of job losses or income declines in the tourism industry.

As shown in columns 2 and 5, the stock market crash has a significant negative impact on international tourist flows in the destination countries, whereas its impact in the originating countries is not statistically significant. A destination country experiencing major multi-year stock market turmoil faces a 2.66% drop in international tourist arrivals compared to a destination country not experiencing such stock market downturns. During the period of stock market crashes, businesses cut back on travel expenses. As a result, the demand for high-end hotel rooms tends to decline sharply following a stock market crash. As pointed out by Murgoci et al. (2009), following the 2008 Global Financial Crisis accompanied with the stock market turmoil, the demand for tourism services from affluent international leisure and business travelers declined sharply as the world economy slowed down.

The parameter estimates in columns 2 and 5 indicate that the effect of the domestic debt crisis on international tourism differs for the destination and originating countries. In the presence of a domestic debt crisis, international tourism arrivals in the destination countries increase by about 11.74% compared to destination countries experiencing no domestic debt crisis. In contrast, when an originating country experiences a domestic debt crisis, the demand for international tourism falls by about 6.85% compared to an originating country that does not experience such a crisis.

In the presence of a domestic debt crisis in a destination country, the domestic currency usually loses substantial value relative to international currencies. The host country becomes attractive for international tourists as the overall costs of international tourism services decline. In contrast, in the presence of a domestic debt crisis in an originating country, the domestic currency devalues relative to international currencies. Consumers have less purchasing power, and as a result, the demand for international tourism services decrease.

The parameter estimates in columns 2 and 5 suggest that external debt crisis has a significant positive impact on the demand for international tourism services in the originating countries, whereas its impact is statistically insignificant in the destination countries. An originating country experiencing an external debt crisis faces an increase of about 8.33% in demand for international tourism services compared to an originating country not experiencing such a crisis. Perhaps, with the advent of the external debt crisis, the demand for tourism services from business travelers and affluent investors increase sharply as they seek opportunities for alternative investments abroad. External debt crisis is accompanied by the economic uncertainty at home, and investors would prefer to invest abroad in this kind of situation.

In general, this result suggests that tourism acts as a life jacket for economies facing a debt crisis. Greece provides a real-life example of the potential interplay between debt crisis and international tourism. As reported by Helena (2017), amid the debt crisis, the tourism industry in Greece accounted for 8 of every 10 new job openings in 2016. In 2015, figures from the Bank of Greece suggest that close to 23.5 million tourists visited, yielding about 24% of the gross domestic product. In 2016, the figure from the country’s tourism confederation indicated that approximately 27.5 million tourists visited. In 2017, approximately 30 million tourists were expected to visit Greece, which is approximately ten times its population. The booming tourism industry helps to mitigate the negative impacts of the debt crisis and economic turmoil.

As reported in columns 2 and 5, the banking crisis has a significant negative impact on international tourism in both the destination and originating countries. International tourist flows fall by about 5.07% in a destination country experiencing a banking crisis compared to a destination country not experiencing such a crisis. Similarly, the demand for international tourism services declines by about 2.50% in an originating country facing a banking crisis compared to an originating country not experiencing such a crisis.

Banking crisis usually leads to the credit crunch, fall in investor confidence, decrease in consumer spending and a heightened level of economic uncertainty. In the presence of banking crisis, consumers decrease discretionary spending. Investment also decreases as firms and investors have little access to external capital. This suggests that the demand for international tourism services falls in the originating countries. Similarly, a destination country facing a banking crisis is less attractive to tourists. For instance, tourists may face difficulty withdrawing money from ATMs during the period of the banking crisis.

Overall, the standard gravity variables have their expected signs as shown in columns 3 and 6. For instance, distance has a significant negative impact on international tourism in both the destination and originating countries. Distance could be considered as a proxy for transportation costs. Higher transportation costs tend to dampen international tourism. Sharing a border or sharing an official language or an unofficial language or having colonial ties has a strong positive impact on international tourism in both the destination and originating countries. These results are expected as these factors act to lower the transaction costs of international tourism.

Further, landlocked destination countries attract less international tourists, whereas the impact of the landlocked variable on the originating countries is statistically insignificant. As expected, Island destination countries attract more international tourists, while, island originating countries demand more international tourism services. The presence of coastline tends to promote international tourism as it lowers transaction costs, provides an alternative transport route, and presents extraordinary attractions for tourists that are not available in landlocked destination countries.

The Link between Different Types of Crises and International Tourism in the Originating and Destination Countries by Regions

Table 4 presents parameter estimates of the link between different crisis events and international tourism by regions. As shown in columns 2 and 3, the parameter estimates suggest that inflation crisis has a significant negative impact on international tourist flows in the destination countries situated in regions, such as America and Latin America and the Caribbean (LATCA). This implies that international tourist flows fall around 27.10% to 34.03% when the destination countries in these regions are experiencing inflation crisis relative to their counterparts that are not. There is no strong evidence that inflation crisis has a statistically significant impact on international tourism in the destination countries located in Europe and Sub-Saharan Africa (SSA).

Link between International Tourism and Crises by Regions.

Note: LATCA = Latin America and the Caribbean. The table reports fixed effects estimates. The dependent variable is log of tourist flows; Ln denotes natural logarithms. The numbers in parentheses in columns are robust standard errors. All regressions include constants but they are not reported. Significance at the 1%, 5%, and 10% levels is indicated by ***, ** and *.

Similarly, as reported in columns 5 to 7, in the presence of inflation crisis, the demand for international tourism services drop by around 9.61% to 14.53% in originating countries situated in regions such as Europe, America and LATCA, Asia, Middle East, North Africa, and Oceania compared to their counterparts experiencing no inflation crisis. The impact of inflation crisis on the demand for international tourism services in originating countries situated in SSA is insignificantly different from zero.

These findings suggest that the impact of the inflation crisis on international tourism is region dependent. In general, the inflation crisis tends to dampen international tourism in some regions, while not having any significant impact in some regions. On the one hand, as discussed earlier, the inflation crisis is associated with a decline in consumer’s purchasing power, thus, explaining the negative link between inflation crisis and international tourism. On the other hand, the demand for international tourism services in countries situated in SSA is quite low, and this might explain why the effect of the inflation crisis is statistically insignificant.

As presented in columns 1 to 8, the impact of the stock market crash on international tourism is region dependent. As shown in column 2, a destination country in America and LATCA experiencing a stock market crash faces a drop in international tourist flows of about 4.21% compared to a destination country not experiencing such a crisis. As pointed out earlier, in the presence of a stock market crash accompanied by economic uncertainty resulting from it, businesses cut back on travel expenses. International tourism attractiveness of the destination countries in America and LATCA decreases as a result of economic uncertainty resulting from the stock market crash.

Further, as reported in columns 3 and 7, in the presence of stock market crash, a destination or originating country located in Asia, Middle East, North Africa, and Oceania experiences an increase in international tourist flows or the demand for international tourism services ranging from 2.94% to 5.02% compared to countries in the regions with no such crisis. Perhaps, a stock market crash in these regions tends to create arbitrage or other business opportunities for both international and local investors. The potential existence of business opportunities following a stock market crash might help to explain the finding that a stock market crash tends to promote international tourism in Asia, Middle East, North Africa, and Oceania.

The parameter estimates reported in columns 1 to 8 indicate that the effect of the domestic debt crisis is also region dependent. In the presence of domestic debt crisis in destination countries situated in America, LATCA, Asia, Middle East, North Africa, and Oceania, international tourist flows increase by around 20.32% to 21.05% compared to destination countries not experiencing such crisis. As noted earlier, the domestic debt crisis is accompanied by the devaluation of the domestic currency, thus, increasing the international attractiveness of destination countries in these regions. In contrast, when a destination country situated in SSA, suffers from the domestic debt crisis, international tourist arrivals drop by around 13.24% compared to their counterparts that are not debt-stricken. In general, SSA remains a region where tourism competitiveness is the least developed (Crotti and Misrahi 2017). As a result, a domestic debt crisis accompanied by a low level of international attractiveness of countries in SSA in general acts to dampen international tourist flows.

Further, originating countries in America and LATCA faces around 20.78% drop in the demand for international tourism services if they are experiencing a domestic debt crisis compared to their counterparts that are not. As discussed earlier, in the presence of a domestic debt crisis, domestic currency depreciates relative to international currencies. As a result, the demand for international tourism services falls because a significant fraction of potential tourists have less purchasing power.

As reported in columns 1 to 8, the impact of the external debt crisis is region dependent. International tourist flows fall by about 11.40% in destination countries in America and LATCA experiencing external debt crisis. Similarly, in the presence of an external debt crisis in SSA, international tourist flows drop by 12.28% compared to destination countries that are not debt-stricken. In contrast, an originating country in Europe that is embroiled in external debt crisis faces an increase in demand for international tourism services by about 26.74% relative to their counterparts that are not facing such external debt crisis.

In the presence of an external debt crisis, wealthy investors and business travelers in the rich European originating countries might demand more international tourism services as they seek for investment opportunities abroad. In contrast, in the presence of external debt crisis accompanied with a heightened level of economic uncertainty, the international attractiveness of destination countries in America, LATCA and SSA falls, and thus, international tourist flows decline.

As shown in columns 1 to 8, the effect of the banking crisis on international tourism is region dependent. In the presence of a banking crisis, a destination country in America and LATCA faces a drop in international tourist arrivals of about 4.60%. A destination country in Asia, Middle East, North Africa, and Oceania attracts about 4.69% lower international tourists, and a destination country in SSA faces a drop in international tourist flows of about 17.14% compared to their counterparts that are not facing a banking crisis. There is no strong evidence suggesting that a banking crisis dampens international tourism in destination countries in Europe.

Similarly, during the period of the banking crisis, the demand for international tourism services declines by around 4.11% in originating countries in Europe, whereas originating countries in the America and LATCA lower demand for international tourism services by about 6.95% relative to their counterparts that are not facing a banking crisis. There is no strong evidence indicating that a banking crisis in the originating countries in Asia, Middle East, North Africa, Oceania, and SSA inhibits international tourism.

In the event of a banking crisis, less efficient banks are more likely to collapse, and interest rates on loans increase sharply as risk premium rises. As a result of the economic uncertainty resulting from a banking crisis, discretionary spending declines as consumers decrease spending and investment falls as firms face a higher level of financial constraints. In general, the banking crisis depresses international flows in countries in different regions as noted above. The negative impact of a banking crisis on international tourism is, however, more severe in destination countries in SSA judging from the magnitudes of the parameter estimates. Limited tourism infrastructure and a low level of tourism competitiveness in destination countries in SSA relative to destination countries in other regions might help to explain why the negative impact of the banking crisis on international tourism is more acute in destination countries in SSA.

Robustness Checks

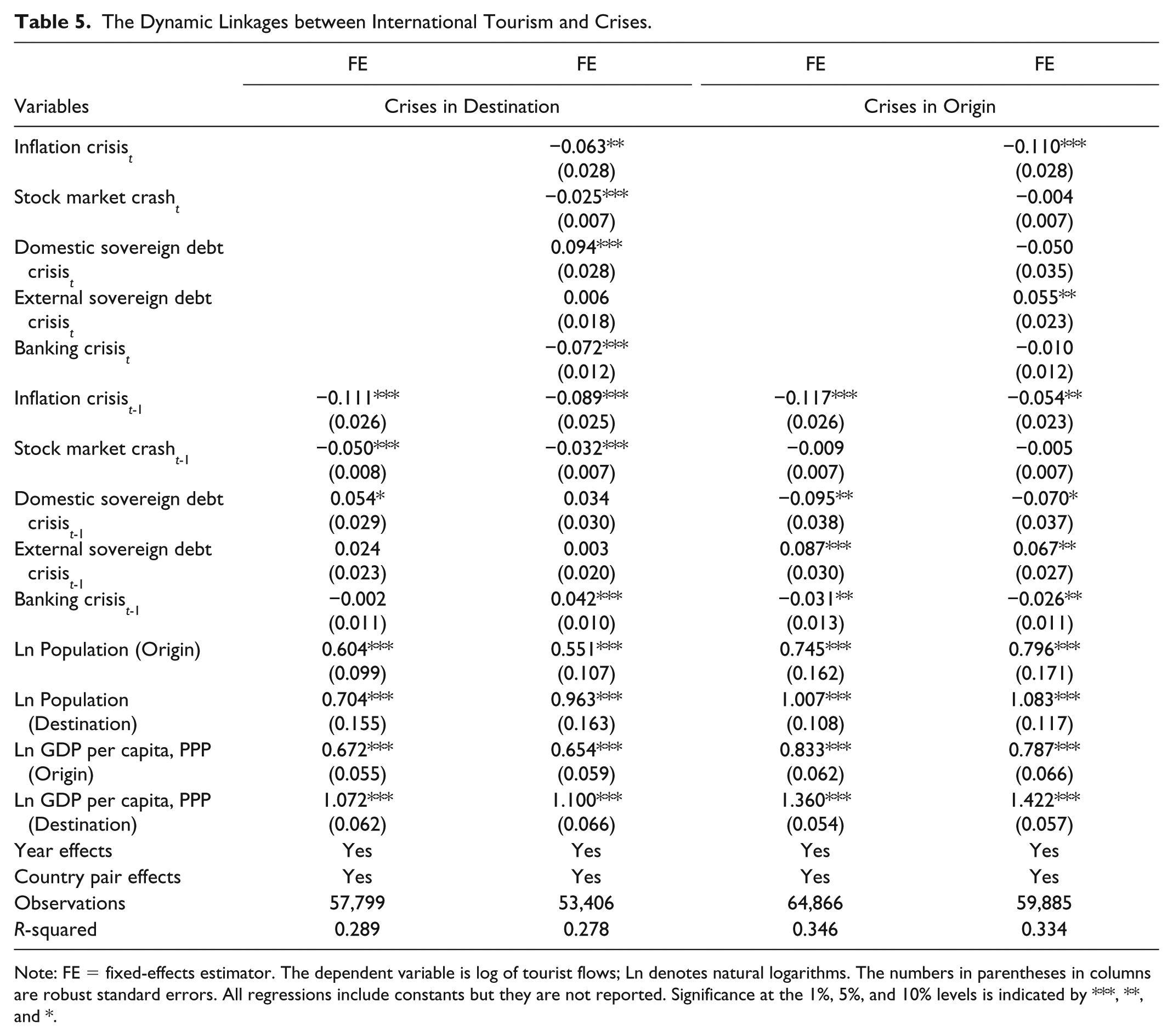

We carry out a number of robustness checks. It may be argued that the dynamic model is more appropriate compared to the static model. To address this issue, we estimated two types of dynamic models. Table 5 presents the results of the dynamic models. Overall, the findings are similar to those reported in Table 3. Columns 1 and 3 present the results when the one-year lag of the crisis variables are used in lieu of the contemporaneous values. As expected, an inflation crisis in the destination country would lead to a reduction in international tourist arrivals. Similarly, a stock market crash also significantly reduces international tourism flows to the destination country. On the other hand, a debt crisis in the destination is positively related to international tourist flows as in most cases it leads to a devaluation of local currency making the destination more attractive. Inflation crisis, domestic sovereign debt crises, and banking crisis in the origin country, on the other hand, leads to significantly lower tourist flows to the destination country.

The Dynamic Linkages between International Tourism and Crises.

Note: FE = fixed-effects estimator. The dependent variable is log of tourist flows; Ln denotes natural logarithms. The numbers in parentheses in columns are robust standard errors. All regressions include constants but they are not reported. Significance at the 1%, 5%, and 10% levels is indicated by ***, **, and *.

Further, the parameter estimates are qualitatively similar, if the contemporaneous and lagged values of the crisis variables are controlled for simultaneously. The results are reported in columns 2 and 4 of Table 5. As expected, inflation crisis in destination and origin countries significantly reduces tourist flows to destination countries in period t and t − 1. Similarly, stock market crash in the origin and destination also reduces tourist flows; however, the effect is only significant for a crash in destination countries. A domestic sovereign debt crisis in the destination countries, on the other hand, significantly increases tourism flows to destination countries; however, this effect is short-lived and disappears after one year.

A banking crisis in the destination country, on the other hand, significantly reduces tourist flows in the first period; however, after one year, the banking crisis has a significant positive effect on tourism flows. One possible explanation for this could be the fact that a banking crisis is likely to trigger institutional reforms, which would, in turn, lead to an improvement in the quality of domestic economic and political institutions (Andersson 2016). This, in turn, can improve the attractiveness of the destination country for tourism as tourists feel safe and secure as the quality of institutions improves.

An external debt crisis in the origin countries significantly increases tourist flows to destination countries in period t and t − 1. This result also corroborates our earlier findings as presented in Table 3. Nonetheless, a banking crisis in the origin country reduces tourist flows; however, this effect is only significant after one year. Overall, the findings from dynamic models provide further support to the findings from our main model and suggest that, for most types of crisis, the impact on tourism is contemporaneous.

We also check if the results are particularly vulnerable to the issue of double counting. It could be argued that a crisis has a negative effect on income, but this effect is not one to one. For instance, the impacts of crises on tourism demand are not clear-cut. First, crisis results in a reduction in tourists’ current income, which in turn leads to a reduction in expenditure devoted to tourism activities but not necessarily cancellation of travel altogether. In addition, a reduction in income would make a typical tourist to be more responsive to price/expense of destinations and tourism services. Third, in general, the cutback decisions of tourists rely not only on income but also on other personal considerations such as security, economic confidence, concerns for socioeconomic issues, the environment, etc. (Boulding 1991; Hall 2010; Papatheodorou and Arvanitis 2014).

In view of the potential that each crisis likely has a negative real income effect, if crisis variables and GDP per capita are included together in the regression, it could lead to the issue of double counting. To show that our findings are not particularly susceptible to double counting problem, we employ the procedure of generated regressors proposed by Gomanee, Girma, and Morrissey (2005). This approach consists of constructing a new regressor from the residuals of an auxiliary regression of the log of GDP per capita on the crisis indicators and use the new generated regressor in the main regression in lieu of GDP per capita. This approach allows us to identify the effect of changes in GDP per capita on international tourism that are not related to the occurrence of a crisis. 2

The parameter estimates of the robustness check are reported in Table 6. Overall, the conclusions drawn from the new estimates are similar to the ones reported earlier. In fact, after controlling for the problem of double counting, the coefficients of the indicators of interest have increased in terms of magnitude, and they are in general more statistically significant relative to prior parameter estimates, thus reinforcing the conclusions of the study. For instance, the inflation crisis, stock market crash, external sovereign debt crisis, and banking crisis in both destination and origin countries significantly reduces tourism flows to the destination. Domestic sovereign debt crisis, on the other hand, leads to an increase in tourist flows.

Link between International Tourism and Crises Using Generated Regressors for GDP per Capita.

Note: FE = fixed-effects estimator. The dependent variable is log of tourist flows; Ln denotes natural logarithms. The numbers in parentheses in columns are robust standard errors. All regressions include constants but they are not reported. Significance at the 1%, 5%, and 10% levels is indicated by ***, **, and *.

Conclusion

Economic and financial crises present challenges and, occasionally, opportunities for the tourism industry. With regard to challenges, in the presence of economic and financial crises, consumers reduce their discretionary spending, which is expected to lower the demand for international tourism services. In addition, as investor confidence falls, tourism investment plummets. Compouned by these effects, the tourism sector is likely to face stagnation as well as job losses. However, the tourism sector could provide opportunities for economies experiencing some types of crises. During the period of some economic and financial crises, the tourism industry tends to be resilient and robust, while many sectors tend to be adversely impacted. In such instances, the tourism sector might help an economy to mitigate the negative effects of some economic and financial crises.

This study attempts an in-depth analysis of the impact of crises on tourism. We are the first to explore the effects of different economic and financial crises, namely inflation crisis, stock market crash, domestic and external debt crisis, and banking crisis on international tourism using a panel gravity data set. Our results indicate that some economic and financial crises adversely affect international tourism, wheras other types of crises increase internaitonal tourism or have no effect. This is particularly evident when the findings are considered in the context of different regions of the world. For instance, the results show that an inflation crisis discourages international tourism in both the destination and origin countries. Inflation crisis erodes consumers’ purchasing power as real incomes of potential tourists are substantially reduced. Consequently, the demand for tourism services decreases as consumers reduce discretionary spending. A sharp drop in discretionary spending translates into a sharp decline in tourism spending.

Furthermore, our findings indicate that a domestic debt crisis encourages international tourism in the destination countries, whereas its impact on demand for tourism services is negative in the origin countries. A devaluation of domestic currency usually accompanies a domestic debt crisis. The devaluation of domestic currency makes the destination countries more attractive for tourists, while it lowers the spending power of tourists in the originating countries.

The findings of this study have important policy implications for the tourism sector. Policymakers should develop macroprudential policy measures to prevent and/or minimize systemwide risks in the economy in general and the financial sector in particular. For example, a wide range of system risk indicators could be used to monitor and predict wide systemic risks. However, in the event that a crisis is irreversible, policymakers should implement policies that create an enabling environment for the tourism sector to take advantage of any opportunities. An enabling environment may include, but not be limited to, avoiding visa restrictions and higher taxes on travel- and tourism-related services in the wake of domestic crises, budget shortfalls, etc.

It is essential that tourism thrive because when a host country faces a domestic crisis, it often becomes more attractive to international tourists because of an increase in their purchasing power. The tourism sector will, thus, be able to help mitigate the adverse effects of the crisis on the host economy through tourism receipts and employment generation. If the tourism sector is able to seize the opportunities left behind because of some domestic crises, the host economy would quickly correct itself with the least amount of government intervention and the associated market distortions. Consequently, government policy should be “proactive” instead of “reactive” and must be formulated with the participation of the relevant stakeholders as well as to be suitable for the particular situation/region/country.

Footnotes

Appendix

Definitions and Sources of Model Variables.

| Variable | Definition | Source |

|---|---|---|

| Tourist flows (TF) | Tourist flows are the dependent variable in the specified models. Tourist flows are measured by the number of tourists arriving at destination from originating country . They are distinguished by the country of origin and destination. | UNWTO database (World Tourism Organization 2017) |

| Population (Pop) | This variable controls for the effect of population on tourist flows. It is one of the variables used to control for the economic size of the originating and destination countries. Population data is distinguished by the country of origin and destination. | World Bank Development Indicators (World Bank 2017) |

| GDP per capita at PPP (GDPpc) | GDP per capita controls for the effect of income on tourist flows. It is one of the variables used to account for the influence of economic size in the underlying relationship. It is measured at purchasing power parity distinguished by the country of origin and destination. | World Bank Development Indicators (World Bank 2017) |

| Overall crisis indicator (origin) | The overall crisis indicator (origin) accounts for any economic and financial crisis occurring in the origin country. It is set to 1 if an origin experiences any type of economic or financial crisis covered in this study at time t and 0 otherwise. | Author’s own calculation based on the Reinhart and Rogoff (2011) data set |

| Overall crisis indicator (destination) | The overall crisis indicator (destination) accounts for any economic and financial crisis occurring in the destination country. The variable is set to 1 if a destination experiences any type of economic or financial crisis covered in this study at time t and 0 otherwise. | Author’s own calculation based on the Reinhart and Rogoff (2011) data set |

| Inflation crisis (Inf) | This is a dummy (indicator) variable accounting for the influence of inflation crisis in either the destination or origin country in the underlying relationship. The dummy is set to 1 when the annual rate of inflation exceeds 20% in time t and 0 otherwise. | Reinhart and Rogoff (2011) |

| Stock market crash (SMC) | This dummy variable is used to capture the effect of stock market crash in either the origin or destination. A stock market crash is measured by setting dummy to 1 when a country’s primary stock market experiences a cumulated multiyear real return of −25% or less and 0 otherwise. | Reinhart and Rogoff (2011) |

| Sovereign domestic debt crisis (SDCD) | This indicator accounts for domestic sovereign debt crises in either the origin or destination countries. The variable takes the value 1 when a country defaults on its domestic debt and 0 otherwise. | Reinhart and Rogoff (2011) |

| Sovereign external debt crisis (SDCE) | This is the dummy for external sovereign debt crises in either the destination or origin countries. The external debt crisis dummy is set to 1 when a country defaults on its external debt and 0 otherwise. | Reinhart and Rogoff (2011) |

| Banking crisis (BC) | A banking crisis, in either the origin or destination, is denoted by the BC dummy. The dummy is set to 1 when a bank run leads to bank closure, merger, or government takeover or when a bank’s need for assistance has a contagious effect on other banking institutions and zero otherwise. | Reinhart and Rogoff (2011) |

| Distance (DIST) | This variable controls for the effect of distance between the origin and destination countries on r tourist flows. It is measured as the number of kilometers between the destination and origin countries. | Gravity database from Head, Mayer, and Ries (2010) |

| Contiguity (CONT) | This dummy variable controls for the effect of contiguity of the origin and destination countries on tourist flows. The contiguity dummy takes the value of 1 if the destination and origin countries share a border and 0 otherwise | Gravity database from Head, Mayer, and Ries (2010) |

| Common official language (COMOFFL) | This variable is an indicator for the effect of a common official language between the origin and destination countries on tourist flows. It is set to 1 if the country of origin and destination shares a common official language, and 0 otherwise. | Gravity database from Head, Mayer, and Ries (2010) |

| Common unofficial language (COMNOFFL) | This dummy variable controls for the effect of a common unofficial language on tourist flows between the destination and origin. This dummy takes the value of 1 if the origin and destination countries share a common unofficial language that is spoken by at least 9% of the population and 0 otherwise. | Gravity database from Head, Mayer, and Ries (2010) |

| Former colony dummy (FCOL) | The former colony dummy accounts for the effect of colonial-era ties on tourist flows in the origin and destination countries. It takes the value of 1 if the origin country is a former colony of the destination country or the destination country is a former colony of the origin country and 0 otherwise. | Gravity database from Head, Mayer, and Ries (2010) |

| Landlocked (LAND) | The effect of being landlocked on tourist flows is captured by landlocked dummy. It is set to 1 if the origin and destination country are landlocked and 0 otherwise. | Gravity database from Head, Mayer, and Ries (2010) |

| Island (ISLA) | The effect of being an island on tourist flows is captured by island dummy. This dummy takes the value of 1 if the origin country and destination country are an island and 0 otherwise | Gravity database from Head, Mayer, and Ries (2010) |

Acknowledgements

The authors would like to thank Mahnoor Shahid for her assistance in data collection. The authors would like to thank three anonymous reviewers for their helpful and constructive comments that greatly contributed to improving the final version of the article.

Authors’ Note

Usman Khalid is now affiliated with Department of Innovation in Government and Society, College of Business and Economics, United Arab Emirates University.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.