Abstract

This study examines the role of corporate social responsibility (CSR) in the investment preferences of tour operators through a discrete choice experiment conducted among tour operator managers worldwide. Stakeholder theory is used as a theoretical platform for explaining the role of CSR within the tour operators’ investment preferences. The findings indicate that, when making investment decisions, tour operators generally tend to balance the interests of the local community, employees and businesses, and to consider the effects of their investments on the local economy and the environment. However, empirical evidence indicates that tour operator’s investment preferences are moderated by three factors, namely: local government pressure, size of the investment, and tour operator profile. In particular, greater attention should be paid to high-scale investments, and to investments made by generalist tour operators if destinations want to preserve their distinctive sociocultural and natural assets and provide well-being to local communities.

Keywords

Introduction

Corporate social responsibility (CSR) has a long-standing history in management literature (Freeman and Hasnaoui 2011), and it has emerged as a key issue especially in the last four decades. CSR includes a number of actions that companies can undertake to contribute to a better society (Porter, Kramer, and Zadek 2007). Hence, this concept has gradually become part of academic business discussions. One of the most pressing issues is the impact of CSR on firms’ competitiveness. According to Friedman (1970), the engagement of firms in socially responsible practices and activities results in more costs than benefits, thus causing lower net financial performance. This theory is in stark contrast with the stakeholder view proposed by Freeman (1984), who supported the existence of a positive relationship between CSR and performance, thus recognizing that the aim of a business is to create value for all stakeholders. Additional schools of thought concerning this relationship and the role of CSR in modern business and society have also been developed.

Following the growing interest on the topic of CSR, this study explores the nexus between CSR and investment preferences in the tour-operating sector. A tour operator commonly combines other suppliers’ services in a form of a vacation package and charges a premium for it. It conceives the vacation, designs products and organizes tourism services, which generally include accommodation, transportation, transfers, and travel insurance, among others. A tour operator normally makes a variety of investments in both new destinations and in destinations where they are already operating; these investments comprise, for instance, tourism facilities, businesses, infrastructures, transportation services, as well as other interventions that can strengthen and diversify local economies.

Although the topic of CSR has been increasingly investigated in tourism and hospitality (Farrington et al. 2017; Font and Lynes 2018; Ibarnia, Garay, and Guevara 2020), little research has emerged in connection with the tour-operating business. Few studies about tour operators (TOs) have only recently concentrated on such topic (Araña and León 2021; Baniya, Thapa, and Kim 2019; Goffi, Masiero, and Pencarelli 2018, 2021; Kamanga and Bello 2018; Lin, Yu, and Chang 2018; Milwood 2020; Zapata Campos, Hall, and Backlund 2018) without addressing the influence of CSR on their investment preferences. TOs play a significant role in the marketing and distribution of tourism products (Tveteraas, Asche, and Lien 2014). As crucial intermediaries, they can influence consumer preferences, supplier behavior, and government tourism policies (Andriotis 2003). TOs are connected with a very large number of tourists and several suppliers, such as travel agencies, accommodation, restaurants, travel guides, and local transports, representing a powerful actor for the conservation of nature and for local empowerment (Budeanu 2005). Van Wijk and Persoon (2006) claimed that the future sustainability of the tourism industry depends largely on TOs, being key players in the tourism sector. As pointed out by Zapata Campos, Hall, and Backlund (2018), TOs have a noteworthy impact on the future move toward more responsible forms of the tourism industry as a whole, as they influence suppliers, business partners, and consumers. TOs’ investment decisions have a direct influence not only on their supply chain but also on many local communities.

Opportunities offered by considerable effort on CSR have not yet been fully exploited in the tour operating business (Dodds and Kuehnel 2010). Until the 90s, TOs have had few motivations to invest in CSR practices within the context of low demand for sustainable products and little regulatory pressure (Curtin and Busby 1999). In the last two decades, the package tourism industry has undergone tumultuous changes. The bankruptcy of numerous TOs, particularly the recent collapse of Thomas Cook, the second-largest tour operator worldwide with more than 600,000 tourists stranded around the world (The Economist 2020), has placed this issue in the spotlight, thus also raising the question of what drives TOs’ investments. Increased competitive pressure, evolving tourists’ preferences, digital innovations, and new distributions channels have resulted in changes in package tourism. The market was characterized by the entrance of new competitors, such as online TOs and low-cost airline companies, the expanding number of independent travelers, and the intense price competition (Falzon 2012). TOs have attempted to respond to these changes through several strategies, such as improving the quality of the products, exploiting niche markets, selling new destinations, and adapting price strategies (Alegre and Sard 2017; Picazo and Moreno-Gil 2018), with no clear evidence of investments in CSR as a way to react to such changes. As the tourism industry deeply depends on local sociocultural and natural resources, responsible business practices are vital for a more sustainable sector (Sheldon and Park 2011). This dependence is particularly relevant in current times, as the COVID-19 pandemic has hardly hit those economies that rely on inbound package tourism.

TOs are facing growing pressure and higher expectations in terms of CSR activities (Richards and Font 2019), which might lead to an increased effort to invest resources in environmentally and socially responsible activities. Such pressure comes from the provisions of different national legislations in the destinations in which they operate. TOs are also influenced by a multitude of local stakeholders, including small and medium enterprises, nongovernmental organizations, employees, infrastructure administrators, host communities, destination marketing organizations, education and training systems, academia, tourism services providers, cultural environment, tourist attractions administrators, tourism and hospitality associations, and local media. Furthermore, TOs aim to fulfill the expectations of their stakeholders in the residence country of their corporate headquarters. In addition, the progressive detriment of natural resource conditions in several package destinations (Escudero-Castillo et al. 2018; Gössling 2001) and package tourists’ growing interest toward sustainability (Goffi, Cladera, and Pencarelli 2019) are pushing TOs to increase their CSR engagement. Moreover, some destinations might further focus on local sustainability, thus requiring TOs to invest in CSR activities to help local economies counteract the negative effects of the COVID-19 pandemic (Hall, Scott, and Gössling 2020). Such trends call for gleaning further insight into the role of CSR in TOs’ investment preferences.

While a wealth of research has investigated the relationship between CSR and firms’ performance in management (Endrikat, Guenther, and Hoppe 2014; Friede, Busch, and Bassen 2015; Hang, Geyer-Klingeberg, and Rathgeber 2019; Margolis and Walsh 2003; Wang, Dou, and Jia 2016) as well as in tourism and hospitality literature (Franco et al. 2020; Theodoulidis et al. 2017), to the best of the authors’ knowledge, the influence of CSR on investment preferences has not been discussed yet. The present work aims to address such gap by proposing the results of a discrete choice experiment conducted among a sample of international TOs. Our model is anchored on stakeholder theory, which stresses the central role played by a variety of stakeholders for the firm’s survival and long-term success. Freeman et al. (2010) emphasized that stakeholder theory has influenced several fields, including marketing, strategic management, finance, and accounting. Given that business investments determine the company’s future financial performance, the factors that drive investment preferences are worth to be investigated and identified.

In light of the foregoing discussion, the study investigates whether different CSR attributes affect the investment preferences of TOs in addition to the classic determinants of investment preferences. Specifically, this study aims to analyze the influence of a set of CSR attributes in the investment preferences of different TOs.

Theoretical Framework

Corporate Social Responsibility Theories and Approaches

CSR has been the subject of much attention. It has been recognized as a multidimensional concept, including economic, social, environmental, ethical, philanthropic, and legal aspects (Carroll 1999). CSR is recognized as “a concept whereby companies integrate social and environmental concerns in their business operations and in their interaction with their stakeholders on a voluntary basis” (European Commission 2001, p. 8). This quote is the most cited definition of CSR (Dahlsrud 2008) and stands out for its simplicity and clarity. Three aspects are worth noting. First, the integration of social and environmental concern moves the concept a step forward from mere philanthropy. Second, the interaction with stakeholders recognizes the relevance of all the parties that can either affect or be affected by the business. Third, the “voluntary basis” recommendation emphasizes that measures over and above of those required by law should be adopted. A further step forward is made by the European Commission, which advises companies to incorporate socioeconomic, ethical, and environmental concerns in their strategies and aim at creating a shared value for their owners and stakeholders (European Commission 2019). Such recommendation integrates Porter and Kramer’s (2011) shared value concept by connecting firm success and social progress, with the idea that a business should concurrently advance its competitiveness and the socioeconomic environment in which it operates.

CSR perceptions diverge extensively within management literature. This circumstance hinders an adequate assessment of the main dimensions of CSR (Lindgreen and Swaen 2010). The notion of CSR has suffered from a proliferation of definitions, that have prevented the concept from being developed and implemented effectively (Freeman and Hasnaoui 2011; van Marrewijk 2003). Most of the definitions of CSR can be classified into five main dimensions (Dahlsrud 2008), namely, environmental, social, economic, stakeholder, and voluntariness.

Research in CSR has been conducted from several management perspectives, including the most popular stakeholder theory and other theories, such as agency theory, institutional theory, resource-based view, and reputation theory. According to stakeholder theory, companies should be socially and environmentally responsible, and they should simultaneously pursue their financial goals (Freeman 1984). Companies should take into account the interests of all stakeholders, balancing their needs, and hence improving not only financial performance but also the wellbeing of the society. Stakeholders have also been argued to play a key role for the survival and the success of a firm. Instrumental stakeholder theory suggests that profit maximization is achieved through the engagement in ethical relationship with stakeholders. It further assumes the firm as a nexus of contracts and recognizes that by minimizing the cost of contracting, it will enhance its competitive advantage (Jones 1995). Accordingly, through CSR engagement, a firm can preserve good relationship with stakeholders and foster mutual trust (Wicks, Berman, and Jones 1999), thus increasing financial performance (Jones 1995) and returns to shareholders (Berman et al. 1999).

According to Brammer, Jackson, and Matten (2012), the multifaceted and evolving nature of CSR can be better understood by using the institutional theory as a conceptual framework. Such theory, which has received a relatively recent but growing attention by CSR scholars, argues that CSR should not be grounded in the voluntary behavior of the firms, but that should be regarded as the result of the society’s expectations that are embodied in institutions. Hence, the social responsibility of companies is the product of the different formal (e.g., national laws, trade unions, business associations) and informal (e.g., cultural and religious norms) institutional factors that characterize regions and countries (Doh and Guay 2006). This interpretation helps explain why multinational companies are faced with different requirements for social and environmental responsibilities, depending on the place in which they operate. To address this issue, several initiatives have been made by international institutions with the aim of institutionalizing CSR at the global level through the creation of procedures and rules, such as the ISO 14001 and the ISO 26000 standards (Schwartz and Tilling 2009).

Drawing aspects from the resource-based view approach and reputation theory, CSR is considered capable of providing internal and external benefits. Under the resource-based view, Wernerfelt (1984) argued that firms can obtain certain internal benefits in developing close relationships with stakeholders in terms of innovation and organizational culture (Howard-Grenville, Hoffman, and Wirtenberg 2003; Russo and Harrison 2005). Indeed, according to such theory, the firm’s control of valuable, rare, and costly-to-imitate resources can lead to a sustained competitive advantage (Barney 1991). However, organizational capabilities are necessary for resources to be assembled and become productive (Eisenhardt and Martin 2000). From this perspective, investing in CSR may develop new resources capable of building a sustainable competitive advantage (Branco and Rodrigues 2006). Under reputation theory, investments in CSR are associated with the development of trustworthy and valuable relationship with stakeholders, which eventually lead to positive external effects in terms of corporate reputation (Roberts and Dowling 2002). Godfrey, Merrill, and Hansen (2009) focused on the link between CSR and corporate reputation, advocating that firms with good CSR reputation will better preserve their value, especially when negative events, such as crises, occur.

The favorable consideration of CSR is questioned by agency theory. On the basis of the principal–agent relationship, agency theory argues that a business should only be orientated to pursue the interest of its owner (Friedman 1970). According to such theory, management should only fulfill its obligations toward its shareholders. Hence, a business should have only one corporate responsibility, which is to make profit. If resources are used for socially responsible activities, they are diverted from the company’s main objective, which is to increase shareholders’ wealth.

The measurement of the impact of CSR activities on firms’ performances has attracted a long line of research. Margolis and Walsh (2003) examined more than 100 papers published from the 70s to the 90s and found that only seven studies showed a negative relationship between CSR and performance, whereas the majority revealed a positive relationship and, in some cases, non-significant relationships or mixed results. Similar conclusions were found in previous review studies (Pava and Krausz 1996; Ullmann 1985). Wang, Dou, and Jia (2016) conducted a meta-analytic review of 42 studies and provided evidence in support of stakeholder theory. Other meta-analytic studies, such as those of Endrikat, Guenther, and Hoppe (2014), Friede, Busch, and Bassen (2015), and Hang, Geyer-Klingeberg, and Rathgeber (2019) focused on the environmental perspective and revealed that the vast majority of the published works confirm the positive relationship between CSR and financial performance, thus supporting stakeholder theory.

Rangan, Chase, and Karim (2015) maintained that companies from different sectors and societal environments cannot engage in the same kind of CSR activities. Thus, it is important to adapt the concept to the specific sector under consideration. A re-examination of the CSR concept in tourism and hospitality appears necessary, especially recognizing the key role played by local communities and the environment in supporting tourism businesses (Farrington et al. 2017). The recognition of such interdependence could also translate into concrete progress toward achieving a more sustainable business configuration.

According to stakeholder theory, CSR is an important way to establish solid relationships with stakeholders not only to enhance mutual trust but also, under some conditions, to increase market opportunities (Barnett and Salomon 2012). As emphasized by Porter and Kramer (2011), a healthy community and environment are paramount to a successful business. By contrast, Clarkson et al. (2011) warned that even if wide evidence supports a positive relationship between environmental efforts and firms’ performances, not every company should adopt such practices if they take resources away from their core functions. Aragón-Correa and Sharma (2003) cautioned that in the case of some firms, investing in environmental practices can deplete resources diminishing their competitiveness. However, different from other sectors, natural and sociocultural resources are part of the tourism product sold to tourists and are thus critical assets of the company active in the tour operating business (Goffi, Masiero, and Pencarelli 2018). The creation of linkages with the local community, natural assets, and sociocultural assets can help TOs in gaining competitive advantage in generating new market opportunities (Erskine and Meyer 2012). Drawing on stakeholder theory, which serves as a background for the proposed model, the objective of this study is to investigate the role of CSR in the TOs’ investment preferences.

Corporate Social Responsibility in the Tour Operating Industry

CSR research in hospitality has had relevant growth in the last few years. Font and Lynes (2018) found 366 articles published in tourism and hospitality about CSR and environmental responsibility with over 70% published after 2013. However, Ibarnia, Garay, and Guevara (2020) noted that the vast majority of CSR studies in tourism are related to the hospitality sector. Farrington et al. (2017) reviewed 81 papers published in tourism and hospitality from 2004 to 2014 about CSR in tourism. The reviewed papers focused on the analysis of CSR impacts, both internal (such as the impact of CSR on tourists’ loyalty, firms’ performances, and employee retention) and external (such as the impact of CSR on local communities and environment), and on the conceptualization, implementation, and reporting of CSR. The relationship between CSR and tourism firms’ performances has also attracted research interest. Summing up the applied studies identified by Goffi, Masiero, and Pencarelli (2021) in their literature review scheme, more than 30 articles were published about CSR impact on tourism firms’ performances from 2007 to 2021.

The first studies investigating sustainability in the tour operating business recognized that most TOs did not acknowledge sustainability as a key component of their activity (Carey, Gountas, and Gilbert 1997; Klemm and Parkinson 2001; Tapper 2001). TOs generally perceived a lack of demand for sustainable products and underestimated their role in promoting sustainable tourism (Curtin and Busby 1999; Forsyth 1995; Holden and Kealy 1996; Miller 2001). Later studies focused on the role of TOs on different aspects related to sustainability, including poverty reduction (Erskine and Meyer 2012), tourism development (Cloquet 2013), and the development of rural and isolated area communities (Wearing and McDonald 2002). The literature has also scrutinized the barriers to the TOs’ implementation of sustainability practices and the opportunities for more sustainability products (Richards and Font 2019).

Nevertheless, the understanding of CSR in the tour operating business is still limited. To encourage the adoption of CSR initiatives in the tour operating sector, international organizations and institutions have developed several programs in the last two decades, such as the “Travelife Sustainability System for Tour Operators and Travel Agencies,” introduced in 2007, and the “Tour Operators Initiative for Sustainable Tourism Development”-TOI (UNEP 2003). The TOI, established in 2000, in 2014 merged with the “Global Sustainable Tourism Council” and proposed a set of indicators of sustainable performance for TOs (GSTC 2016).

Some studies have investigated the topic by adopting the qualitative research approach. Dodds and Kuehnel (2010) argued that even if the level of concern about CSR is rather high among Canadian mass TOs, participation in CSR-related activities is neither evident nor systematic. Similarly, Kamanga and Bello (2018) recognized that Malawian TOs have not fully and systematically implemented CSR initiatives. Milwood (2020) observed that although small Caribbean TOs have high CSR awareness, they show different implementation of CSR activities. Zapata Campos, Hall, and Backlund (2018) illustrated the efforts of one of the largest Scandinavian TOs concerning inclusive tourism, which is a part of the broader CSR agenda in tourism.

Few recent quantitative studies have been carried out concerning CSR in the tour operating business. Baniya, Thapa, and Kim (2019) showed that the perceived demand, expected benefits, and economic opportunities related to CSR affect the participation and the future engagement of Nepalese TOs on CSR initiatives using linear regressions. Two contributions assessed the behavior of TOs with respect to the environmental dimension of CSR Lozano, Arbulú, and Rey-Maquieira (2016) using a game-theoretic framework, focused on the greening role of TOs, while Lin, Yu, and Chang (2018) used a structural equation modeling to explore CSR and environmental initiatives implemented by Taiwanese travel agencies and TOs to reduce greenhouse gas emissions. A study on a sample of TOs worldwide showed that the profile of TOs is associated with different levels of CSR commitment (Goffi, Masiero, and Pencarelli 2018); the statistical comparison was performed through t-test and one-way ANOVA. Using a regression model, an analysis carried out on the same sample of TOs found a positive relationship between CSR engagement and TOs’ performances (Goffi, Masiero, and Pencarelli 2021). Additionally, Araña and León (2021) resorted to a discrete choice experiment to assess tourists’ preferences for the CSR initiatives implemented by hotels. Using the same discrete choice experiment, the authors also asked TOs to indicate the potential preference of their average customer. They reported a relatively high willingness to pay for the environmental and labor components of CSR; moreover, a rather large segment of highly CSR conscious package tourists was detected. This is in line with Goffi, Cladera, and Pencarelli (2019), who also found large segments of package tourists interested in sustainability. Package tourists’ interest in CSR/sustainability practices provide a primary motivation for the tour operating business to adopt CSR initiatives. In this research direction, this study explores the role of CSR in shaping TOs’ investment preferences through the implementation of discrete choice experiment and modeling techniques. Specifically, tour operator managers were asked to indicate a preference concerning two hypothetical investment prospects made up of a mix of standard indicators of investment performance and attributes related to CSR.

Conceptual Background

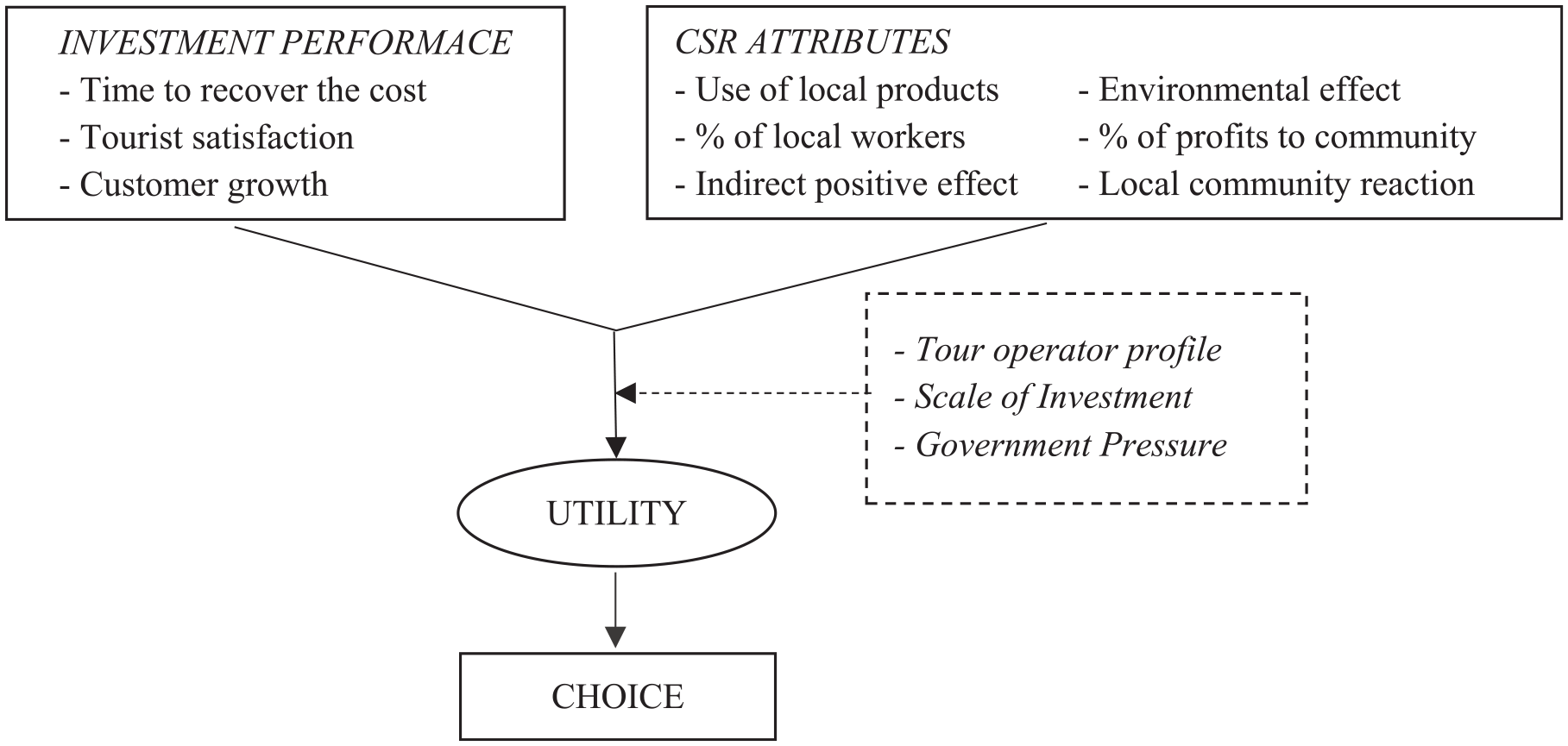

The choice of an investment is based on the evaluation of a number of relevant factors that affect the firm’s future performance and competitiveness. The predominant theme that emerges from the theoretical framework outlined in the previous section is that CSR is becoming increasingly important in shaping investment decisions in the tour operating business. Therefore, the study aims at investigating the role of different CSR attributes in the investment preferences of different TOs. In particular, tour operator managers’ assessment of alternative investment prospects is assumed to be influenced by standard measures of investment performance as well as by CSR aspects.

Regarding investment performance, the current research focuses on three indicators that are considered important for investment decisions and appraisal. The first indicator refers to the “time to recover the cost,” that is, the period necessary to recoup the funds spent in the investment. The payback period is one of the most widely applied metrics in the decision to proceed with investment techniques (Lefley 1996). Research in accounting has long advocated that non-financial measures, such as customer satisfaction, are suitable indicators of firm performance (Ittner and Larcker 1998). “Tourist satisfaction,” the second indicator in the model, has been widely recognized to have a significant and positive impact on tourists’ loyalty to destinations (Alegre and Cladera 2006), hotels (El-Adly 2019), and TOs (Hsu 2000). Moreover, the popularity of review websites attracting millions of users daily has changed the travel industry (Jeacle and Carter 2011) and amplified the importance of tourist satisfaction. “Customer growth” has also been considered one of the most relevant factors for TOs and an important indicator of TOs’ performance (Curtin and Busby 1999). Carey, Gountas, and Gilbert (1997) recognized that TOs operate under the “economies of scale” approach and are essentially concerned with customers’ growth. Indeed, when asked about the implementation of CSR initiatives, some TOs responded that CSR was not a priority, as they were too busy attempting to maximize the number of visitors (van der Duim and van Marwijk 2006).

Regarding CSR aspects, the analysis of the role played by CSR in shaping TOs’ investment preferences should take into consideration the complexity of the CSR concept. The latter has been recognized as being multidimensional, including economic, social, environmental, ethical, philanthropic, and legal aspects (Carroll 1999). Most of the definitions of CSR can be classified into five main dimensions (Dahlsrud 2008), namely: environmental, social, economic, stakeholder, and voluntariness. Hence, after a review of the pertinent literature of CSR in tour operating industry, six attributes related to the five main dimensions of CSR were included in the model: “use of local products/services, percentage of local workers employed, indirect positive effect on local economy, environmental effect of the investment, environmental effect of the investment, local community reaction.”

The stakeholder dimension in relation to TOs’ investment preferences is captured by the attribute, “local community reaction.” Local communities’ attitudes and their reaction to tourism have also received abundant consideration in the tourism literature (Hadinejad et al. 2019). Li et al. (2019) demonstrated that CSR is a key driver of local communities’ attitudes toward a new tourism project. They argued that for the success of the investment, an effective relationship must be established with the local communities. However, the stakeholder dimension permeates the whole set of the CSR attributes considered in the model. Indeed, the attributes are focused on the complex relationship between the tour operating business and the local suppliers, employees, community, economy, and environment.

Three attributes are used to represent the social and the economic dimensions of the CSR concept. The attributes “use of local products/services” and the “percentage of local workers employed” measure the direct effect on the local economy. CSR engagement means maximizing the economic impact that TOs have on local communities by purchasing local goods, using local services, and employing local workers. A wide range of practices are intended to foster local economies, such as buying locally produced goods and food produced by local agriculture, using locally owned accommodations and restaurants, and collaborating with local travel agencies and local tour guides (Dodds and Kuehnel 2010; Goffi, Masiero, and Pencarelli 2018). We further consider an attribute related to the “indirect positive effect on local economy.” The activity of TOs might generate an indirect positive effect on the local economy by stimulating a whole range of tourism-related sectors (Budeanu 2005). Such indirect effect can be stronger in developing countries affecting their economic development (Cloquet 2013; Erskine and Meyer 2012).

The environmental dimension of CSR is represented by the “environmental effect of the investment.” The key role of the tour operating business in promoting environmental sustainability has been widely recognized in tourism literature (Kamanga and Bello 2018; Otoo, Senbeto, and Demssie 2022), as well as in international programs aimed at encouraging the adoption of environmental initiatives by the tour operating sector, such as the “Tour Operators Initiative for Sustainable Tourism Development” (TOI) and the “Travelife Sustainability System for Tour Operators and Travel Agencies.” TOs have expressed interest in adopting and promoting green initiatives and practices (Baniya, Thapa, and Kim 2019; Budeanu 2005; Lin, Yu, and Chang 2018; Schwartz, Tapper, and Font 2008; Tepelus 2005), which could lead to the management of environmental actions along the supply chain (Lozano, Arbulú, and Rey-Maquieira 2016).

The attribute associated with the “percentage of profits devoted to socio-environmental initiatives” reflecting the voluntary nature of the CSR activities is related to the voluntary dimension of CSR. CSR stimulates companies to exceed legal requirements that set the minimum standard of performance toward society and environment (European Commission 2011), thus enabling TOs to demonstrate a responsible behavior (Dodds and Kuehnel 2010). Ultimately, through their voluntary engagement for the benefit of society, companies increase their reputation among consumers and stakeholders in general (Lin-Hi and Blumberg 2018). Indeed, companies have dedicated increasing efforts in philanthropic donations as a way to manage their reputation and to increase their corporate social performance (Gardberg et al. 2019) and their financial performance (Hogarth, Hutchinson, and Scaife 2018). Therefore, we anticipate an increasing interest of TOs toward reasonable proportions of profit sharing.

Figure 1 illustrates the conceptual model proposed in the present study in which performance and CSR attributes are assumed to affect the investment decision-making of TOs. Following the literature on the heterogeneity of TOs’ preferences toward sustainable practices, the study further investigates the moderating effect of three specific factors on TOs’ investment preferences, namely the profile of the tour operator, the scale of the investment, and the institutional pressure experienced by the tour operator at the local level.

The conceptual model.

Tour operator profile

TOs’ investment preferences can be influenced by several factors. Factors related to both to the tour operator profile and to the investment size were considered. Concerning tour operator profile, several characteristics of the TOs were taken into consideration, such as the primary target, the company size, the accommodation ownership, and the geographical location. In particular, Goffi, Masiero, and Pencarelli (2018) showed that TOs focused on sun and sand tourism present lower sustainability engagement than TOs focused on cultural and nature tourism, and that large TOs exhibit lower sustainability engagement than small TOs. Schwartz, Tapper, and Font (2008) also found that such mass-market TOs have a rather low sustainability orientation. Such TOs, operating under the “economies of scale” principle, have long neglected sustainability issues, but their primary concern has been to maximize the number of tourists in their resorts (Curtin and Busby 1999). As a result, coastal areas in many destinations worldwide have been extensively harmed by large-scale package tourism (El Mrini et al. 2012).

Scale of the investment

The monetary size of the investment is an internal aspect that a company can control. Companies’ decisions on investment size have a great impact on the future of businesses (Song 2022). The size of the investments can be considered an important factor in determining investments preferences (Shleifer and Vishny 1997).

Institutional pressure

There are external situational factors especially in the tour operating business, such as the pressure that TOs received from institutions at local level that might have a relevance in determining investment preferences. In particular, government pressure can affect investment preferences toward the adoption of CSR practices (Yu and Choi 2016), proactive environmental strategies (Buysse and Verbeke 2003), and sustainable supply chains (Meehan and Bryde 2011).

Empirical Analysis and Methodology

Survey Instrument

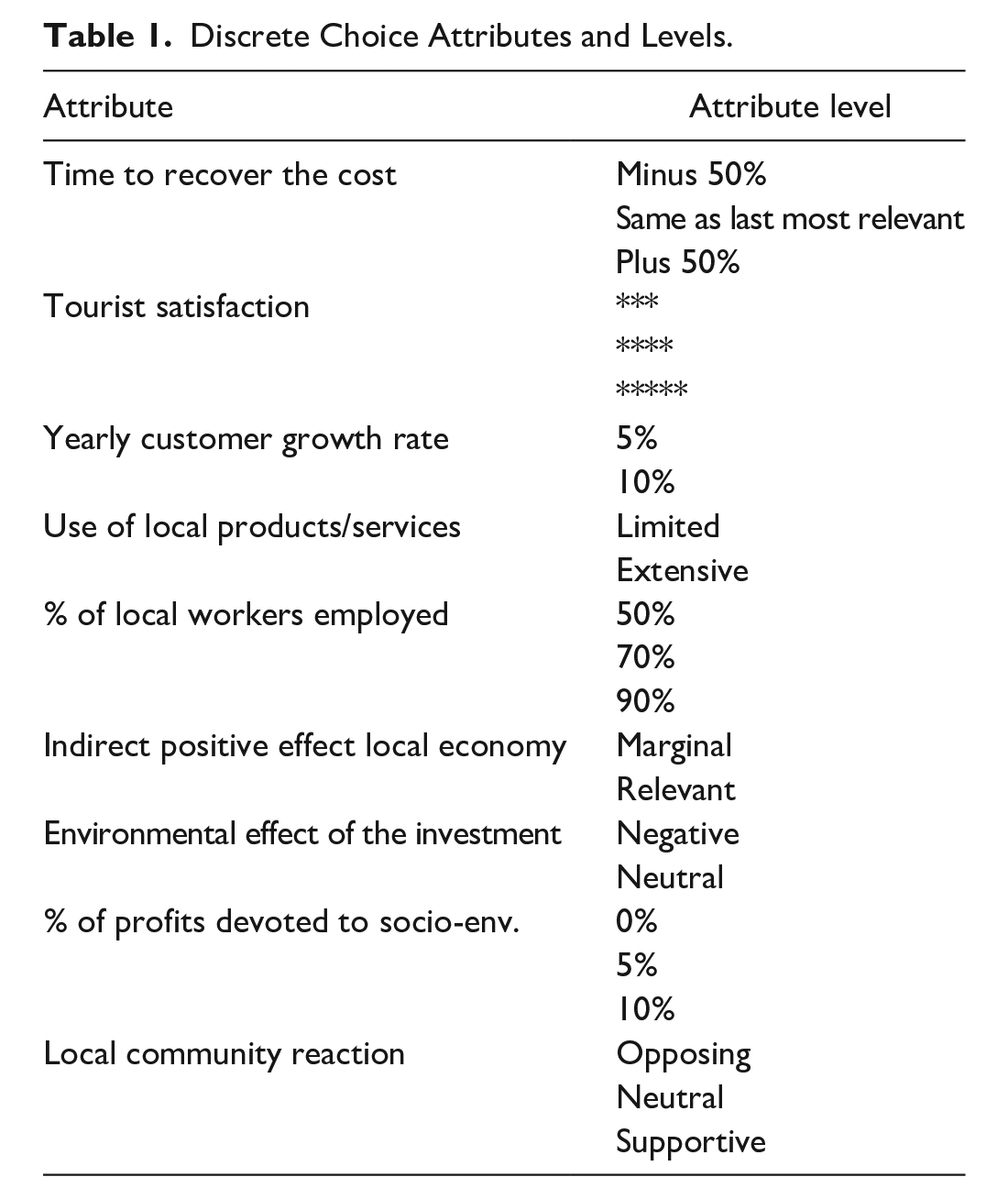

The empirical application is based on a web survey conducted among managers of TOs worldwide during the early months of 2019. The survey included few introductory questions to identify the profile of the TOs. The core part of the survey comprised a discrete choice experiment aimed to assess the relevance of CSR attributes in affecting the investment preferences of tour operator managers and investigate the trade-off with attributes reflecting standard financial and market performance. Tour operator managers were asked to imagine the possibility of a new business investment opportunity in their main destination country and state their preference for a set of hypothetical investment pairs. In line with the model background introduced in Section 3, Table 1 reports the nine attributes that were used to describe the hypothetical investments in terms of investment performance (three attributes) and CSR aspects (six attributes). The decision to characterize CSR with six attributes in the design was motivated by the need to represent the different dimensions of CSR. In fact, the use of single attribute to proxy a multidimensional attribute creates bias (Daziano and Chiew 2012). In an experimental application investigating the effect of CSR on consumer’s evaluation of town shopping centers, Oppewal, Alexander, and Sullivan (2006) concluded that the inclusion in the design of a variety of CSR attributes provides insight into the differentiated effect of detailed CSR aspects.

Discrete Choice Attributes and Levels.

The range of levels for the attribute “time to recover the cost” was decided by taking into consideration the importance to define a wide range in attribute levels (Hensher, Rose, and Greene 2005), whereas a medium to high performance was prospected for the attributes “tourist satisfaction” and “customer growth.” Regarding the CSR aspects, due to documented adverse environmental impact of tourism, such as resources and energy consumption, emissions of greenhouse gases, freshwater and land use (Gössling and Peeters 2015), the attribute “environmental effect of the investment” assumed either a neutral or a negative environmental impact of the investment. Similar discrete choice experiment applications have been used in previous studies to investigate investment preferences at the corporate level. For example, Buckley, Devinney, and Louviere (2007) investigated managers’ preferences for foreign direct investment through a discrete choice experiment with hypothetical alternatives described by 12 attributes. Chassot, Hampl, and Wüstenhagen (2014) analyzed the preferences of venture capitalists for investments in the clean energy industry using four attributes to describe the alternatives. Blondiau and Reuter (2019) used seven attributes to describe the alternatives in a choice experiment aimed at investigating the investment decisions of investors from large private and institutional corporations.

The empirical application relies on a factorial experiment design for the generation of 12 sets of hypothetical investment pairs which were selected by ensuring the absence of dominant alternatives and maximizing the attribute level balance. In studying the effect of number of choice sets in discrete choice experiments, Hensher, Stopher, and Louviere (2001) tested different solutions and concluded that around 16 tasks can represent a good compromise. Further, Caussade et al. (2005) suggested an optimum number choice tasks (i.e., around 9–10) and concluded that the dimension of the choice set represents a relatively minor problem. Furthermore, the experiment did not include an opt-out option, thereby forcing tour operator managers to state a preference between the two hypothetical investment prospects. Although the opt-out option better reflects the market conditions in real life, it implies a loss of preference information whenever it is selected by respondents (Mochon 2013) and might represent the best solution in certain contexts (Zijlstra et al. 2015). In light of the difficulty to achieve large sample sizes in a survey conducted among business managers, the experiment in this study proposed a setting without opt-out option in order to maximize the preference information collected from each respondent. A similar setting was adopted in several previous discrete choice experiment applications in the tourism literature (e.g., Crouch, Del Chiappa, and Perdue 2019; Fleischer, Tchetchik, and Toledo 2012; Keshavarzian and Wu 2021).

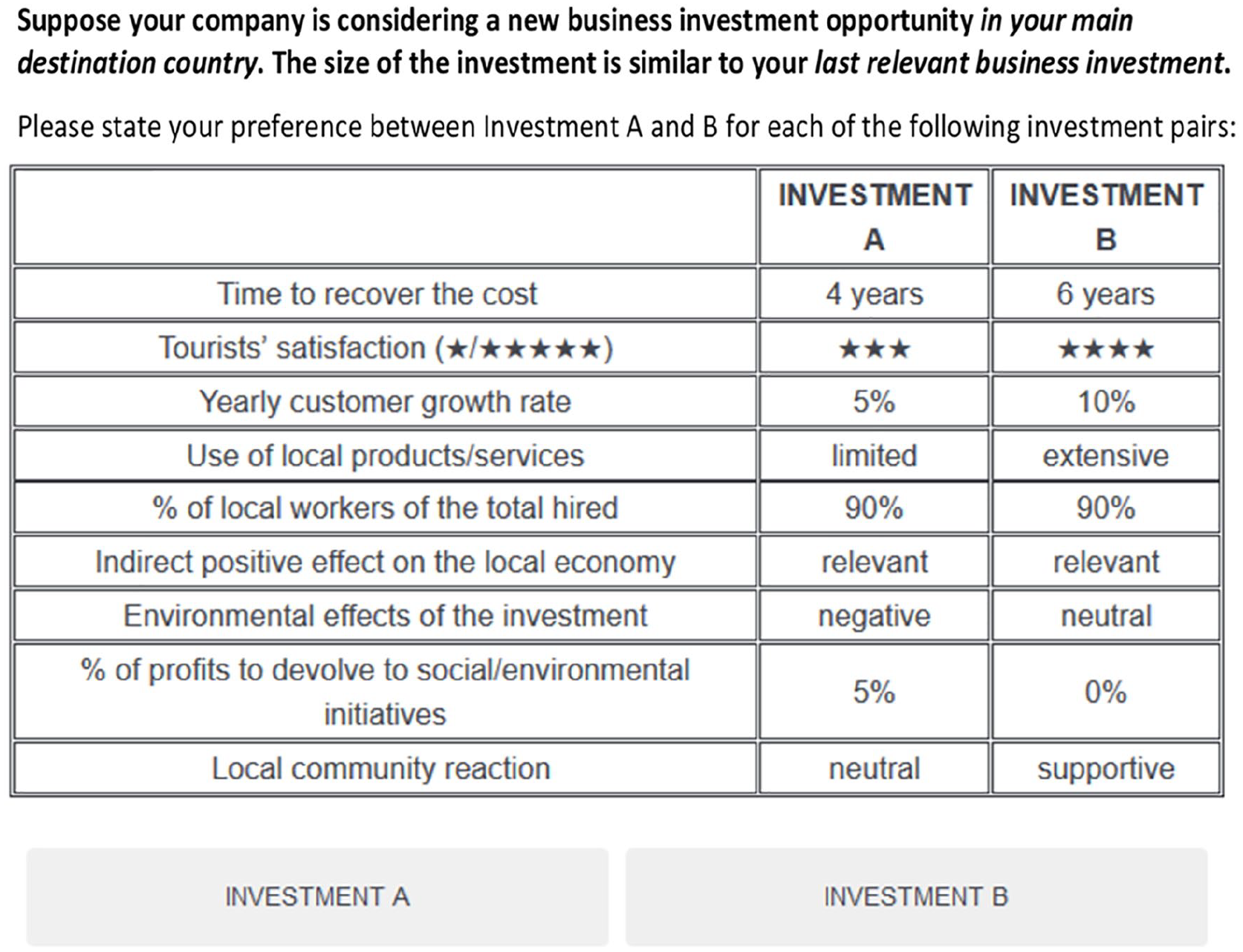

The first draft of the questionnaire was screened by two academics with expertise in the subject area. The final draft was pre-tested with eight managers of TOs and travel agencies through in-depth interviews. In particular, the structure of the interview aimed to validate the selection of the attributes, to assess whether the range of the attribute levels was realistic, and to verify the length and clarity of the choice exercise. Given the positive feedback obtained from the participants to the qualitative interviews, no changes were integrated to the design of the survey. The order of the 12 choice tasks produced by the experimental design was randomized and presented to tour operator managers with the instruction to state their preference for each of the choice tasks by assuming a size of the investment similar to their last relevant business investment (an example of choice card appears in Figure 2). To avoid influencing the respondent, the experiment, and the survey in general, did not introduce any specific information about CSR.

Example of choice card.

Sampling and Respondents’ Profile

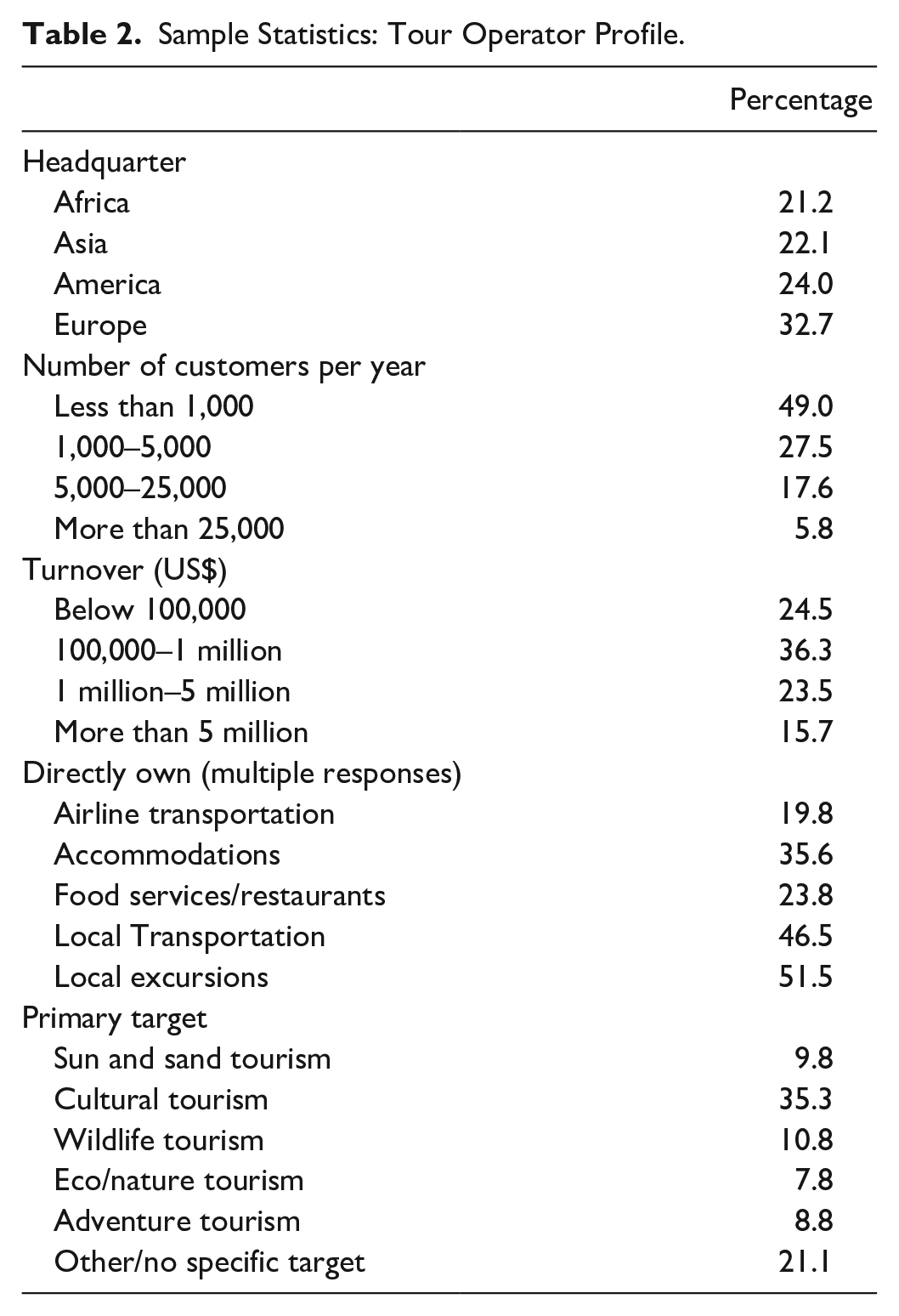

The email contacts of TOs were collected from the major international associations of TOs and used to distribute the web survey. After the first invitation to answer the survey, two reminders were sent to increase the participation rate. The final data set is composed of 104 TOs worldwide. Previous applied studies were mostly conducted on small samples of TOs (less than 50 TOs) at national level. To the best of the authors’ knowledge, an assessment of a large sample of TOs evenly distributed across the four main continents, namely, Africa, America, Asia, and Europe (Table 2) has never been conducted. The sample size, although relatively small, satisfies the rule of thumb for the estimation of a discrete choice model from a discrete choice experiment. According to Orme (1998), the estimation of a model with main effects from an experiment with sample size n, a given number of alternatives (a), choice tasks per respondent (t) and highest number of attribute levels (c) provides robust estimates if the result of the expression nta/c (being equal to 832 in the current application) is greater than 500. The majority of the TOs (49.0%) served less than 1,000 customers per year. However, a considerable proportion (23.4%) counted more than 5,000 customers per year. Approximately 39% of the TOs reported a turnover greater than US$1 million, and most of the sample directly provided local excursions (51.5%), local transportation (46.5%), and lodging (35.6%). Cultural tourism is the main target for 35.3% of the TOs, followed by wildlife tourism (10.8%), sun and sand tourism (9.8%), and adventure tourism (8.8%).

Sample Statistics: Tour Operator Profile.

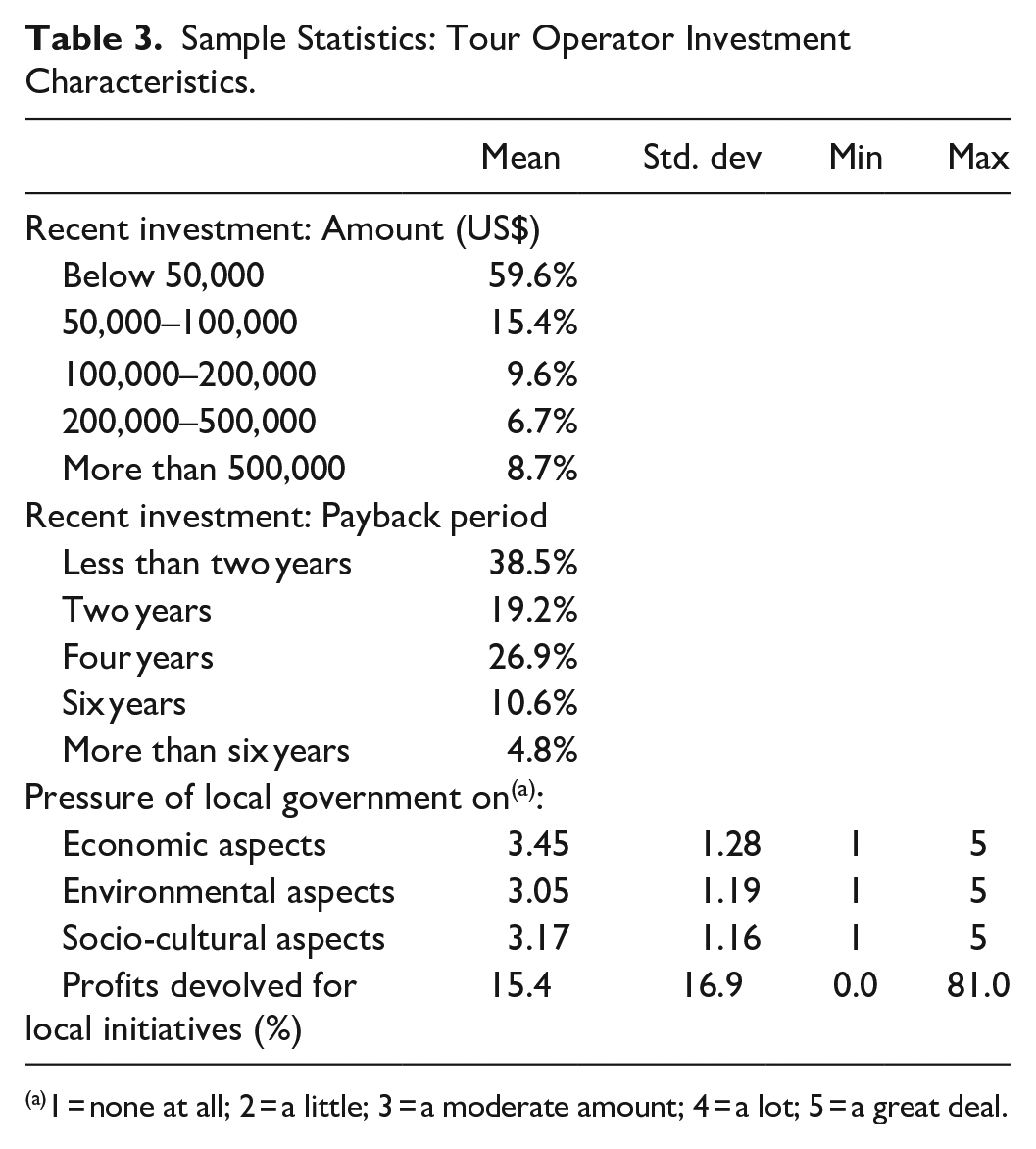

Focusing on previous investment experience (Table 3), the majority of the TOs (59.6%) had recently engaged in a relatively small investment (below US$50,000), and approximately 58% of the sample recovered the initial cost in two years or less. A smaller portion of the sample (8.7%) faced a bigger scale investment (more than US$500,000), and approximately 15% of the TOs reported a payback period of six or more years. When asked about the involvement of local institutions during the agreement phase of the described investment, TOs indicated moderate pressure on environmental aspects (3.05) and socio-cultural (3.17) aspects, and moderate to large pressure on economic aspects (3.45). TOs contributed to social and environmental initiatives at the destination by devolving, on average, 15% of their profits. However, the high value of the standard deviation (16.9) indicates a high degree of heterogeneity across the sample.

Sample Statistics: Tour Operator Investment Characteristics.

1 = none at all; 2 = a little; 3 = a moderate amount; 4 = a lot; 5 = a great deal.

Methodology

The investment preferences stated by tour operator managers in the choice exercise are modeled according to the random utility model framework (McFadden 1974). In particular, individuals are assumed to assess the attributes of each alternative in the choice set and select the alternative associated with the greatest utility. In this context, the utility (Unjs) derived by tour operator manager n for the hypothetical investment j in choice task s is defined as follows:

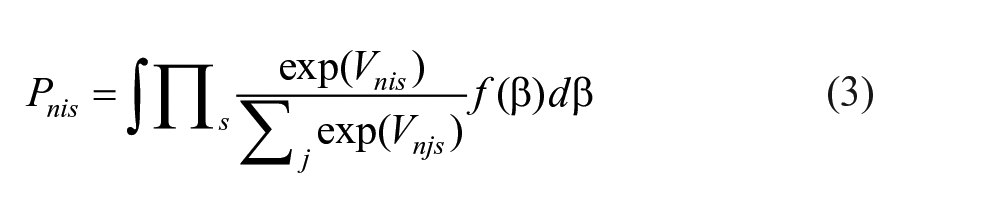

where Vnjs is the systematic utility that identifies the observed part of the utility and εnjs is the random component that identifies the unobserved part of the utility. We specify the systematic utility as a linear combination of coefficients βk associated with k attributes xks. Furthermore, we assume the random component to be independent and identically distributed (iid) following the extreme value distribution. The presence of the random component implies that probabilistic statements are made about choice outcomes (Train 2009). Hence, the probability (Pnis) that tour operator manager n selects the investment i in choice task s requires that

The coefficients βk represent the weights that the tour operator managers attach to each attribute describing the hypothetical investment. The mixed logit (MXL) class of models allows the specification of random preference heterogeneity by defining a continuous density of βk, f(βk) (Train 2009). Different distributions (i.e., normal, triangular, and uniform) were tested in the modeling phase of the study, resulting in largely consistent results. Given that the normal distribution is typically used in empirical applications (McFadden and Train 2000), the normal distribution was used to specify the density function of the random coefficients βk, that is, βk ~ N(bk, σk). Both the mean (bk) and standard deviation (σk) of the random coefficients are estimated by the model through maximum-likelihood estimation. We further introduced interactions between the mean estimates of the random coefficients and a set of tour operator characteristics in an attempt to capture sources of preference heterogeneity (Hensher and Greene 2003). Therefore, the mean estimate of the random coefficient is specified as:

The specification of the random coefficients implies the extension of the logit formula for the computation of the MXL choice probabilities, which can also accommodate for repeated choices across respondents by letting the coefficient vary over respondents while keeping it constant over choice tasks for each respondent (Hensher and Greene 2003; Train 2009). The MXL choice probability associated with tour operator manager n for investment i in choice task s is as follows:

The integral in equation (3) does not have a closed form and is approximated through simulations. In this article, we used the Halton sequence (Train 2009) and based the estimation on 1,000 draws.

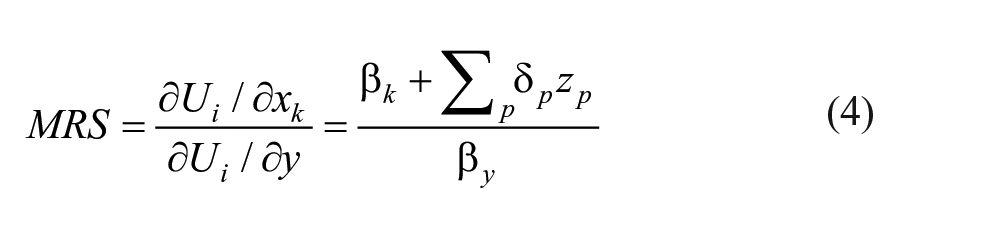

The estimates of a discrete choice model represent marginal utilities and can be used to derive the marginal rate of substitution (MRS) as the ratio of two marginal utilities. In particular, we were interested in understanding how much cost recovery time would be traded by tour operator managers to acquire a better outcome in any of the CSR attributes associated with the investment. The computation of the MRS for the second model is obtained as follows:

where, βy is the coefficient associated with the attribute “time to recover the cost.” To avoid the inconvenience of the MRS being distributed as the ratio of two random distributions, a common solution is represented by specifying the coefficient βy as non-random (Revelt and Train 1998) so that the distribution of the marginal rate of substitution resembles the distribution of the random parameter at the numerator. Individual-specific estimates were then derived through individual choice probabilities generated by using the Bayes rule (Hensher and Greene 2003). These estimates were used to compute individual-specific marginal rates of substitution between the cost recovery time and the CSR attributes of the hypothetical investment.

Model Results

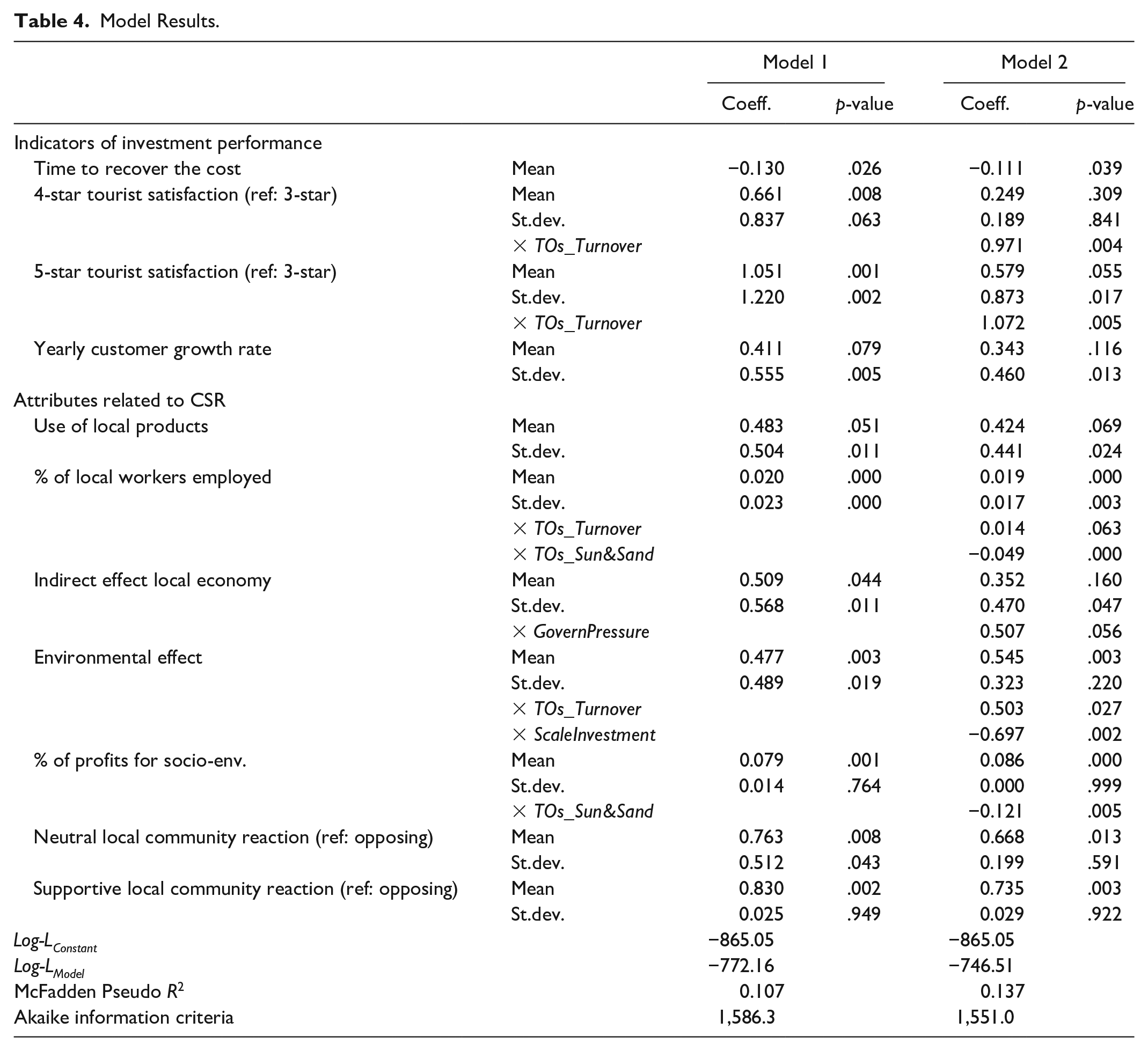

The results for the two estimated mixed logit models are reported in Table 4. The first model (model 1) estimates a random coefficient for each attribute describing the hypothetical investment, except for the coefficient associated with the attribute “time to recover the cost,” which is specified as non-random. The three-level attributes associated with tourist satisfaction and local community reaction were dummy coded. The second model (model 2) extends model 1 by introducing the interaction between the mean of the random coefficients and a set of tour operator characteristics. Four binary variables are considered in model 2 to capture heterogeneity around the mean. In particular, two indicators refer to the recent investment described by the TOs in the survey, and distinguish TOs with a recent investment greater than US$50,000 (ScaleInvestment) and those who received either a lot or a great deal of pressure from local institutions on economic aspects (GovernPressure). The other two indicators are related to the profile of the TOs and were selected after a preliminary analysis on the wider set of tour operator characteristics collected in the survey. The selected binary indicators distinguish TOs with a turnover greater than one million (Turnover) and those with a focus on sun and sand tourism (Sun&Sand). To achieve model parsimony, only significant interactions (p < .10) are included in model 2. The existence of correlation in TOs’ preferences across performance indicators and CSR aspects was investigated by allowing correlation between the coefficients associated with the attributes “tourist satisfaction” and “customer growth,” and those associated with “local community reaction” and “% of profits to devolve to social/env initiatives.” Model estimates (available upon request) indicate the absence of a statistically significant correlation between the random parameters. The model performance is assessed through the McFadden Pseudo R2 calculated as

Model Results.

Looking at model 1, the results for the indicators of investment performance indicate that the time to recover the cost of the investment has a negative impact on the utility. This outcome indicates, as expected, lower preference for investments with a longer cost recovery time. We further observe a positive impact of the attributes “tourist satisfaction” and “customer growth,” both characterized by a consistent preference heterogeneity as suggested by the statistically significant standard deviation estimates. The six attributes related to CSR are all associated with statistically significant and positive mean coefficients, providing evidence of the importance of these attributes in the investment preferences of tour operator managers. The positive sign of the mean coefficients associated with the attribute “percentage of profits for socio-environmental initiatives” is in line with our original expectation. As reported in Table 3, TOs devolve, on average, approximately 15% of their profits. Considering that the attribute “percentage of profits for socio-environmental initiatives” was defined in the range of 0%–10%, the result confirms the increasing preference of TOs toward reasonable proportions of profit sharing. The results of model 1 suggest that the dimensions of CSR considered in this study are all associated with a general increase in the utility of investment alternatives. Hence, these results indicate that tour operator managers consider CSR aspects when assessing different investment prospects. However, the statistical significance registered for the standard deviations of the random parameters associated with CSR attributes indicates a considerable amount of heterogeneity among investment preferences of tour operator managers. Thus, the next objective is to test whether sources of random heterogeneity are explained by observable variables related to the profile of the TOs and the characteristics of their recent investment. This is performed through the specification of model 2.

The introduction of the moderating variables in model 2 allows to capture part of the preference heterogeneity as confirmed by the considerable improvement of the McFadden Pseudo R2, which increased from 0.107 for model 1 to 0.137 for model 2. The low value of the Akaike information criteria further indicates the higher likelihood of model 2 to fit the data in comparison to model 1. Looking at the results, we observe that the interaction of the mean coefficients with the selected tour operator profile and investment characteristics shows several significant relationships. The sales volume of TOs moderates the impact of the attributes associated with the investment performance. In particular, in comparison with TOs with a turnover below US$1 million, managers of TOs with a turnover greater than US$1 million attach greater weight to the outcome of the investment in terms of tourist satisfaction, as indicated by the positive interaction for both four-star and five-star tourist satisfaction.

Tour operator profile and investment characteristics diversely affect the impact of the attributes related to CSR on the investment preferences. The pressure of local institutions on economic aspects influences the perception that tour operator managers have about the indirect effect local economy. The percentage of local workers employed as a result of the investment is weighed more by TOs with high turnover, whereas TOs that mainly target sun and sand tourism exhibit a negative preference (−0.032) for local workers. Furthermore, TOs with high turnover attach greater utility to the environmental impact of the investment, whereas a negative weight to environmental effect is attached by TOs involved in bigger scale investments (−0.152).

Regarding the sharing of profit with the local community, we observe that TOs that target sun and sand tourism attach negative weight to it (−0.035). The results of model 2 indicate that the interaction of mean coefficients with the tour operator’s profile and investment characteristics allow the explanation of the sources of preference heterogeneity, especially for attributes related to CSR. The findings complement the results obtained from model 1 by providing further details on the impact of the aspects of CSR on investment preferences. The socio-economic dimension of CSR related to the indirect effect on the local economy is of particular interest to TOs that used to receive institutional pressure on economic aspects. Instead, TOs that focus on sun and sand tourism exhibit a negative inclination toward CSR related to the employability of local workers and the financial support to socio-environmental initiatives at local level.

Furthermore, the scale of the investment reduces the importance of the environmental CSR dimension, especially for TOs with turnovers below US$ 1 million. Therefore, the findings show the moderating role of the tour operator profile and previous investment characteristics in the relationship between a specific set of CSR aspects and investment preferences. In particular, the moderating effect of tour operator profile is confirmed for CSR dimensions related to the employability of local workers, financial support to local initiatives, and environment. The moderating effect of the size of the investment is confirmed for the CSR dimension related to the environment, whereas the moderating effect of the pressure received from local institutions is supported for the CSR dimension related to the local economy. What is further relevant to emphasize is the low inclination of TOs active in the major segment of sun and sand tourism toward the local markets, both in terms of the employability and socio-environmental initiatives. Similarly, a low involvement to environmental aspects is registered for TOs embarking on large scale investments.

Trade-Off Between Investment Recovery Time and CSR Attributes

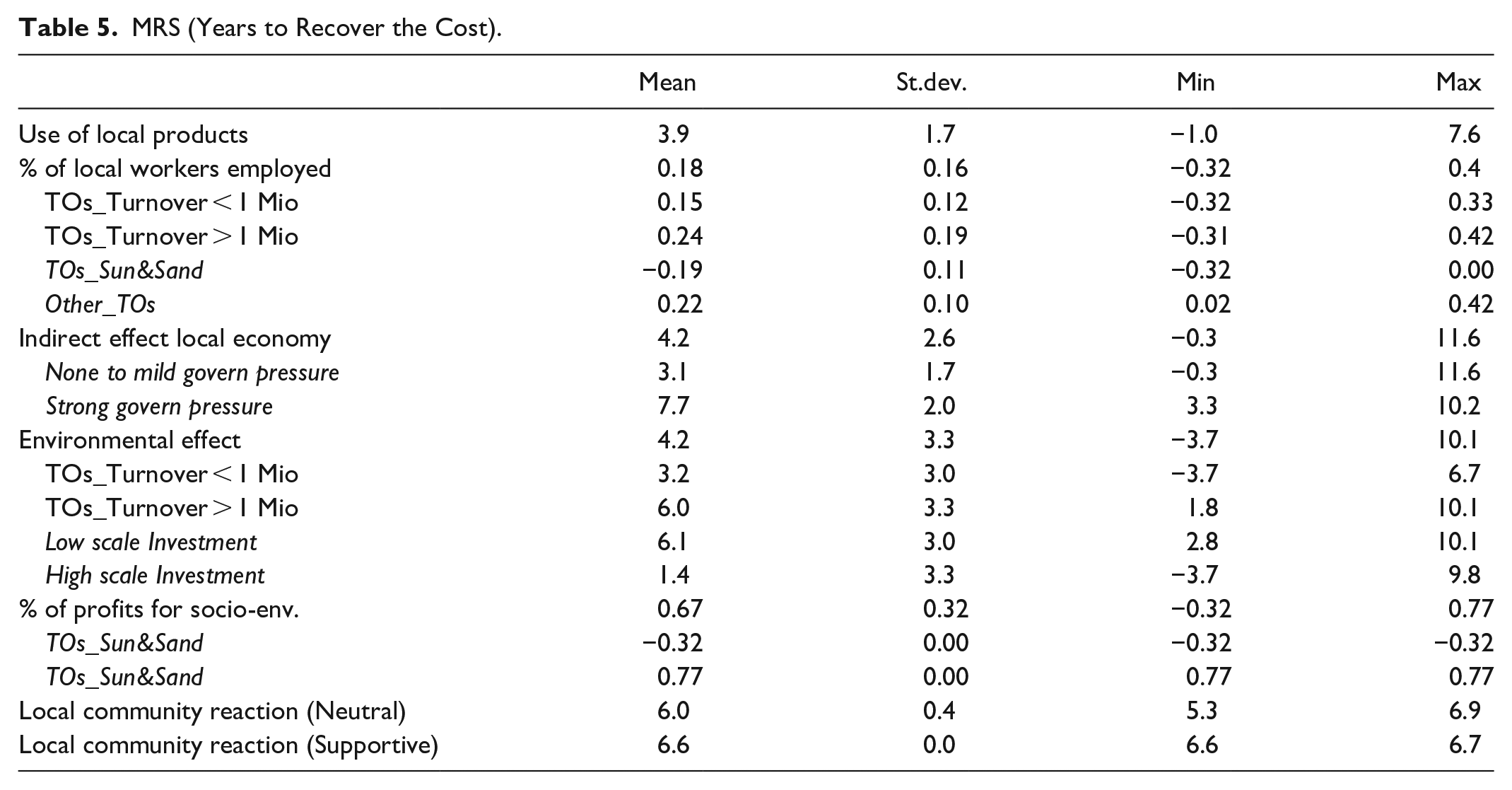

The individual-specific estimates from model 2 were used to derive the marginal rates of substitution between the cost recovery time and CSR attributes (Table 5). In particular, TOs would accept a longer payback period of 3.9 years on average for an investment that makes a “relevant” (instead of “marginal”) use of local products. On average, TOs would consider a 1.8-year longer payback period for an investment that employs a 10% higher share of local workers. This figure increases to 2.4 years of payback for TOs with a turnover above US$1 million. Instead, TOs targeting mainly sun and sand tourism would require a 1.9-year shorter payback period to consider hiring 10% more local workers.

MRS (Years to Recover the Cost).

The willingness to trade payback period with the indirect positive effect on the local economy varies considerably depending on the level of pressure placed by local institutions on the economic aspects. In particular, TOs that received a strong pressure during the agreement phase of their previous investment would consider a 7.7-year longer payback period for an investment that generates “relevant” (instead of “marginal”) effects. This figure drops to 3.1 years for TOs that experienced little to no pressure from the local institution. Both the turnover and scale of the investment affect the increase in the payback period that TOs would consider to avoid negative environmental impacts associated with the investment. This period varies from 3.2 years to 6.0 years for TOs with turnovers below and above US$1 million, respectively, and from 6.1 years and 1.4 years for TOs engaging in low- and high-scale investments, respectively.

Regarding the percentage of profits devolved to socio-environmental local initiatives, TOs engaged mainly in sun and sand tourism would require a compensation of 0.3 years in the payback period to devolve an extra 2% of their profits to local initiatives. Furthermore, TOs would be willing to consider a longer payback period of 6.0 and 6.6 years for an investment that generates, respectively, neutral and supportive reactions by the local community, instead of opposing reaction.

Discussion and Concluding Remarks

The major changes occurring in the tourism sector and the increasing competitive pressure have put on the spotlight the need to properly understand which aspects drive TOs’ investments preferences. This study contributes to the literature on CSR in the tour operating business by developing a discrete choice model that sheds light on the role of CSR in TOs’ investments preferences.

The findings, in line with previous literature, stress the importance of the payback period in investment decisions and appraisal (Lefley 1996). After recognizing the relevance of this variable, we analyzed the tradeoff between payback period and the attributes describing the implications of the investment on CSR aspects. Moreover, the results show that tourists’ satisfaction and yearly customer growth rate play a relevant role in explaining investment preferences.

Empirical evidence shows that the combination of social, environmental, and ethical aspects receives TOs’ attention when making investment choices. TOs generally take into account the interest of the local community when making investment decisions. Local communities are indeed a key part of the product assembled and sold by TOs, and a deeper connection with the local communities not only can provide a supportive environment but also allows TOs to bring local culture closer to tourists, thus selling more authentic and personalized vacations. Three further attributes related to the local stakeholder component, namely the “use of local products,” “the percentage of local workers employed,” and the “indirect positive effects on local economy,” led to positive utilities. Local employees, producers and businesses are key local stakeholders engaged in the package tourism business that can benefit from tourism development. They should be involved and motivated in order to offer less standardized and more uplifting tourism packages. Package tourism can enhance local skills and provide different livelihood options, thus fostering local empowerment (Cloquet 2013).

Moreover, an attribute related to the environmental effect had a positive influence on TOs’ investment preferences. Even if package tourists do not explicitly demand sustainable products, they tend not to return to unsustainable destinations (Goffi, Cladera, and Pencarelli 2019). TOs should realize that not only their success, but also their survival, is determined by the preservation of the natural assets of the destinations they sell. Negotiations between local governments and TOs frequently include a percentage of profits for social and environmental initiatives at the local level (Dodds and Kuehnel 2010). The findings indicate a general positive inclination of TOs to devolve reasonable proportions of their profits providing supporting evidence to the relation between corporate philanthropy and reputation (Gardberg et al. 2019).

These results suggest that TOs generally tend to balance the interest of the local community, employees and producers, and to consider the effects of their investments on local economy and environment. This seems to indicate that TOs are more than just concentrated on shareholders’ benefits. They are to a certain extent focused on the interconnected relationship between their business and the local suppliers, employees and communities. Thus, stakeholder theory can provide a theoretical platform for explaining the role of CSR in TOs’ investment preferences. Indeed, according to such theory, companies should achieve their financial goals, being at the same time committed to a social and environmental responsibility approach (Freeman 1984). However, empirical evidence shows that three factors can influence this approach.

TOs exhibited differentiated preferences for attributes related to investment performance and CSR aspects. Part of the preference heterogeneity was captured by three types of moderating factors. A first moderating factor influencing the impact of CSR aspects on TOs’ investment preferences is represented by government pressure. Empirical evidence shows that TOs who face strong local government pressure are willing to consider longer payback periods if the investment provides the opportunity to generate positive indirect effects on the local economy. Therefore, the activity of local governments should attempt to maximize the positive economic impacts that may arise from a new investment. Zapata Campos, Hall, and Backlund (2018) cautioned about the risk of a very mild adoption of CSR initiatives among TOs in the absence of institutional pressure. When local governments lack the institutional capacity to exert pressure on tour operating companies a key driver in the implementation of CSR initiatives is missing (Miller 2001). Negotiations between local governments and investors generally occur in the case of large TOs’ investments. Local governments should set up the legal framework underlying investments and develop strategies to minimize tourism leakages and maximize local employment and overall local benefits.

A second moderating factor affecting the impact of CSR aspects on TOs’ investment preferences is represented by the size of the investment. Particular consideration should be given to high-scale investments, in which TOs’ willingness to trade payback period to avoid negative environmental effects is four times lower compared with low-scale ones. In such case, local government pressure plays a key role in avoiding irreversible environmental damages that new investments might cause. On one hand, such investments are able to provide local communities an important source of employment and economic growth. On the other hand, if they are poorly planned and regulated, these investments might have negative irreversible impacts on the local environment. Coastal zones in several developing countries have severely suffered from the degradation of natural resources led by large-scale tourism investments (Escudero-Castillo et al. 2018; Gössling 2001; Shaalan 2005). Before converting empty lands into bustling building sites and tourism areas, local governments should address urgent concerns requiring careful monitoring and regulation, such as land zoning rules; project design; the protection of environmentally sensitive areas; and the use of water, drainage, and sewage systems.

A third moderating factor is represented by the tour operator profile. Our findings underscore that greater attention should be paid to investments made by generalist TOs, such as sun and sand focused TOs, if destinations want to preserve their distinctive sociocultural and natural assets and provide well-being to local communities. The results also show that TOs focused on sun and sand tourism are reluctant to devolve a percentage of their profits and hire a great amount of local work. Schwartz, Tapper, and Font (2008) and Tixier (2009) showed that sustainability is a secondary issue for generalist mass-market TOs. This kind of TOs have been embroiled in a price-cutting game and are facing a decline in profitability (van der Duim and van Marwijk 2006). We further find that larger TOs are willing to consider a longer payback period than smaller ones to mitigate the environmental impacts of the investment. A plausible explanation is that larger TOs might have greater financial solidity that allows them a longer period to repay investments in sustainability (Budeanu 2009). Furthermore, for larger TOs, this aspect is a way to increase company reputation, which is one of the key motivators in adopting sustainability strategies (Khairat and Maher 2012). Company reputation has received growing attention in recent years in tourism, especially for larger TOs, due to the key role of online review platforms in determining booking and conversion rates (Cezar and Ögüt 2016; Vermeulen and Seegers 2009).

We encourage future studies to investigate additional CSR aspects and focus on alternative methods to present them in choice experiments as well as on the estimation of interaction effects. In particular, it would be interesting to test if, and to what extent, placing the emphasis on CSR aspects when presenting prospective investments to TOs would influence their investment choices. Experimental settings that include an opt-out alternative are particularly encouraged in order to confirm the study findings in a choice context that better reflects the actual market. We also acknowledge the limitation of the sample size and recommend the use of larger samples in future studies. Although the survey was addressed to companies with different dimensions, most respondents represented small and medium TOs. Thus, we invite future research to conduct single case studies focused on multinational TOs, as they could play an influential role in the transformation of the tourism industry into a more sustainable one. The uncertainty brought by the coronavirus pandemic offers to TOs the opportunity to reconsider the positioning of the own business (Do et al. 2022). The current pandemic situation is pushing the businesses toward more authentic CSR by addressing social and environmental challenges (He and Harris 2020). As pointed out by Benjamin, Dillette, and Alderman (2020), Covid-19 pandemic offers the opportunity to shift to a more sustainable tourism industry. Therefore, future research might investigate whether the engagement of TOs in CSR activities has changed as a consequence of the global pandemic crisis, in several aspects: first, whether a more collaborative and supportive approach was developed with key tourism stakeholders; second, whether a strategic response to the Covid-19 crisis was implemented through the involvement of local businesses; third, whether social and environmental issues were more effectively integrated into TOs’ driving philosophies.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.