Abstract

What can we learn from “minimal” economic models? I argue that learning from such models is not limited to conceptual explorations—which show how something could be the case—but may extend to explanations of real economic phenomena—which show how something is the case. A model may be minimal qua certain world-linking properties, and yet “not-so-minimal” qua learning, provided it is externally valid. This, in turn, depends on using the right principles for model building and not necessarily “isolating” principles. My argument is buttressed by a case study from computational economics, namely, two agent-based models of asset pricing.

Can so-called “minimal” economic models teach us something about real economic systems? If so, what and how? A debate on the epistemic virtues of highly idealized economic models was triggered by Sugden (2000). Sugden claimed that idealized models can, if credible, grant conclusions about the real world. More recently, Grüne-Yanoff (2009) has objected that, although learning from such models is possible, it is also very limited. The models can undermine our confidence in the truth of certain necessity or impossibility hypotheses by showing how something could be the case. However, since they are not isomorphic to their target, do not make use of laws, or isolate any real factor—that is, since they are minimal—they cannot prove that something is the case.

Here, I argue that minimal economic models can support positive conclusions about their targets, more precisely explanations. Thus, my claim resonates with, and elaborates on, Sugden’s views. A model may be minimal qua certain world-linking properties, and yet “not-so-minimal” qua learning, provided it is externally valid. This, in turn, depends on using the right principles for model building, and not necessarily “isolating” principles. My argument is buttressed by a case study from computational economics, namely, two agent-based models (ABMs) of asset pricing. Many other economic models are minimal in Grüne-Yanoff’s sense. My conclusion generalizes to them, too. Thus, I urge, caution is needed when evaluating their status: although they might all seem to deal with purely speculative matters, on closer inspection some may offer important insights into the mechanisms behind real economic phenomena.

I proceed as follows. In section 1, I introduce the debate on minimal models. In section 2, I present the ABMs of asset pricing and claim that they explain important facts involving the statistical properties of the financial time series of prices. One may object to my reading along two lines. First, on the assumption that the ABMs explain, one may question their minimality. Second, granted their minimality, one may question that they really explain. In sections 3 and 4, I rebut both objections and argue that the ABMs are, in fact, both minimal and explanatory.

1. Minimal Models, Minimal Learning?

Consider a highly idealized economic model such as Schelling’s checkerboard model (Schelling 1978, chap. 4). This model is designed to study the unintended emergence of housing segregation patterns out of uncoordinated individual actions. The phenomenon is studied on an artificial grid. Each cell in the grid corresponds to a space, which an artificial agent can occupy. Agents, belonging to two racial groups, are represented by pennies and dimes. They aim to satisfy just one preference, namely, they want to live in a cell whose neighborhood comprises at least a certain proportion of their own group. At each time step, they can either stay where they are, if their preference is satisfied, or move to a free cell whose neighborhood satisfies their preference. As a result of simulating the agent’s moves, segregation obtains across many initial distributions of agents on the grid and preference strengths.

There are two main positions on the epistemic role of theoretical models in economics, namely, fictionalism and isolationism. In the fictionalist camp, Sugden (2000, 2009) argues that idealized economic models are like fictions, or stories: they are believable depending on how the bits of the story fit together relative to the story’s environment. Yet, their function is not limited to merely conceptual explorations of what could happen but extends to validating hypotheses on what actually happens. In the case of Schelling’s model, each run of the simulation describes what happens in a world parallel to the actual world (in a city which could be real), thereby providing support to a hypothesis concerning the real world (real cities).

In a recent article, Grüne-Yanoff (2009) has argued for an opposite conclusion, appealing to broadly isolationist arguments. He notices that there are a number of world-linking conditions—among which the “isolation” of real causal factors

1

—on which learning from models depends, but that idealized economic models do not justify whether, or specify how, such conditions are fulfilled. For instance, in the case of Schelling’s model: Although calling the symbols and coins neighbours, and their patterns neighbourhoods, and attributing preferences to them, [Schelling] makes no effort to justify these labels by pointing out any resemblance to concrete real-world situations, or by citing regularities about the real world. Of course, some very general features—such as the distinguishability of tokens and the spatiality of patterns—resemble features of real-world neighbourhoods. Yet he does not justify the way in which the model specifies all these features—neighbours’ preferences, how neighbours are distinguished, the structure of the neighbourhood, or how discontented neighbours move—with reference to the real world at all. (Grüne-Yanoff 2009, 88-89)

Grüne-Yanoff proposes the following negative characterization of “minimal models,” in terms of their failure to satisfy specific world-linking conditions

2

: [Minimal models are] assumed to lack any similarity, isomorphism or resemblance relation to the world, to be unconstrained by natural laws or structural identity, and not to isolate any real factors. (Grüne-Yanoff 2009, 83)

The question then arises as to whether it is possible to learn something about the world from them. Grüne-Yanoff claims that learning is possible but—contra Sugden—limited to conceptual explorations. For both Sugden and Grüne-Yanoff, learning depends on the models’ credibility. However, differently from Sugden, and in line with his own definition of minimal model, Grüne-Yanoff construes the credibility of minimal models as fully dependent on internal coherence and not on world-linking properties such as coherence with one’s knowledge of causal processes. Learning from minimal models obtains because credibility at the microlevel extends to surprising or counterintuitive macrolevel results. Thus, minimal models can tell us how the world could be. However, they cannot tell us how the world really is. They grant negative conclusions, by undermining impossibility and necessity hypotheses, for instance, Schelling’s model shows that racism is not necessary to segregation. However, they do not grant positive conclusions, whether about general facts or about specific events. So, minimal models only grant minimal learning. Do they?

In the following, I argue that this need not be the case. Minimal models may grant positive conclusions, in particular explanations. They may be minimal qua certain world-linking properties and yet “not-so-minimal” qua learning.

Before moving on, it is important to consider why Grüne-Yanoff maintains that minimal models have limited explanatory power. In short, the relevant contrast for understanding what prevents (most) models from granting non-minimal learning about their targets is “models vs experiments” (Grüne-Yanoff 2011b). Experiments “isolate” explanatory factors (e.g., causes) from a “base” of other factors. Models don’t—whence their epistemic inferiority.

Suppose one wants to use an experiment to test the explanatory role of some factor in some target system. One will first test the contribution to the phenomenon made by the factor in experimental conditions. To this end, one will ensure that the factor is present and operating. Then, assuming that its modes of interaction with the other factors are known, one will control for such interactions. 2 If the factor makes a difference to the phenomenon, one will conclude that the factor partially explains the phenomenon. One will then export the result to the real system based on the material similarity between the experimental system and the real system. The more robust the difference across experimental variation in controlled factors, the stronger the conclusion with respect to the behavior of the target in non-controlled conditions.

If instead of an experimental system, one can only manipulate a theoretical model, a positive conclusion will only be granted in very special circumstances, and will only be as good as the background knowledge used to build the model. One must start with a faithful model of the target, such that its potentially explanatory components are clearly mapped onto real features of the target and are distinguishable from the non-explanatory ones (e.g.: idealized factors, factors that are in the formal model only to guarantee its tractability, etc.). Then, a successful isolation of the factor’s contribution to the phenomenon will depend on omitting or idealizing away the interactions with the other factors—without introducing any idealization in the explanatory factor itself—and then calculating the (theoretical) effect of the isolated factor. But this procedure cannot be successfully carried out in the case of minimal models. Minimal models are not interpreted with respect to their targets, let alone faithful representations of them. So, they cannot be used to identify explanatory factors, isolate them from the other factors, and calculate their effects. Minimal models are only good for conceptual exploration: [T]he construction process of theoretical models cannot reveal any actual constraints of the real world, but only discovers the implications of the model’s assumptions. Hence, modelling does not offer the same opportunities of learning as experimenting. (Grüne-Yanoff 2011b, 12)

For instance, minimal models grant weaker explanations than experiments (Grüne-Yanoff 2011a). They only grant potential explanations of the form: some functional capacity would suffice to produce the phenomenon if such-and-such a mechanism were present. But they grant neither full explanations, which presuppose that the model tells “the whole truth” about some target mechanism, nor partial explanations, which presuppose that the model tells “nothing but the truth” about at least some feature of the mechanism common to both the model and the target.

In the rest of the article, I take issue with the last claim. I argue that isolation is not the only means to partial explanation, and I illustrate an alternative procedure with reference to two ABMs of asset pricing. This, in turn, implies that minimal models may grant not-so-minimal learning.

2. Asset Pricing

2.1. The Neoclassical Model

The motivation for building ABMs of asset pricing lies in a discomfort with mainstream, “neoclassical” macroeconomics, both with its unrealistic assumptions and its inability to account for certain empirical facts.

A fundamental assumption of neoclassical macroeconomics is the so-called “rational expectation hypothesis” (REH): when agents formulate predictions, they use all available information and do not make systematic forecasting mistakes. This hypothesis is usually held in conjunction with the assumption that agents choose rationally, that is, their preferences among outcomes obey certain axioms (e.g., completeness, transitivity), and their choices among alternative courses of action, which aim to bring about those outcomes, maximize expected utility. Since agents are homogeneous in the above respects, the sum of their choices (e.g., their demands for some asset) is equivalent to the choice of one “representative” agent.

The REH entails a general hypothesis about market behavior, namely, the “efficient market hypothesis” (EMH). In financial markets, the price of an asset (e.g., a stock, a bond) is a “rational expectation equilibrium” (REE). This is the solution to an agent maximization problem, namely, the price that satisfies best the utility of the representative agent. Since the price always reflects all available information, the current price is the best estimate of the future price. Prices follow a “random walk.” They randomly fluctuate around the assets’ “fundamental values” 3 so that the distribution of returns, or relative price changes, is Gaussian: any deviation from the equilibrium is due to an exogenous shock (i.e., a new piece of information on, say, a technological innovation) that changes the price unpredictably; but this is immediately interpreted as an arbitrage opportunity and exploited by the agents so that the price quickly reverts to its fundamental value.

Neoclassical macroeconomics is, however, unable to account for most of the so-called “stylized facts” of finance, that is, for special statistical properties of the time series of prices (LeBaron 2006, 1191-92; Rickles 2011, §6; Ross 2003, chap. 12; Samanidou et al. 2007, 411). In agreement with the neoclassical model, unconditional distributions of returns at high frequencies (one day or so) are roughly Gaussian, which entails that the direction of returns is generally unpredictable. However, contrary to the neoclassical model, unconditional distributions of returns at lower frequencies (one month or less) are fat-tailed, that is, have too many observations near the mean, too few in the mid-range, and too many in the tails to be normally distributed. Among the alternative distributions that have been proposed to describe fat tails are power laws, which are scale-invariant. 4 Further stylized facts not predicted by the neoclassical model are volatility clustering and volatility persistence. Large (respectively, small) price changes tend to follow large (respectively, small) price changes, instead of being uniformly distributed. Relatedly, asset returns at different times show a dependency (“long memory”): although the autocorrelation of returns 5 decays quickly to zero, in agreement with the random walk hypothesis, the autocorrelation of squared returns decays more much slowly, which is evidence of some predictability at longer horizons.

Notice that the stylized facts are general facts about the statistical properties of the time series of prices. The ABMs of asset pricing are designed to reproduce such facts—and not particular historical time series—by simulating the pricing mechanism. Here, I present and discuss two such ABMs, namely, the one in (Lux and Marchesi, 1999, 2000) and the one in (Arthur et al., 1997; LeBaron, Arthur and Palmer, 1999). Their novelty with respect to the neoclassical model is that, contrary to the REH, agents are heterogeneous. Heterogeneity depends on a non-ideal, or more realistic, kind of rationality, which may be realized in various ways: agents may differ with respect to their information, computational ability, behavioral rules, learning strategies, and so forth. Representing price formation as a result of aggregating the demands of heterogeneous agents is viewed as an improvement over the representative agent model. As we shall see, heterogeneity is the engine of a self-reinforcing mechanism that produces the boom–bust pattern observed in real financial time series. In both models, the stylized facts obtain as a result of the endogenous pricing mechanism and in the absence of exogenous shocks. I will now present the two models in more detail.

2.2. A Phase-Transition Model

The first model, presented in (Lux and Marchesi 1999, 2000), is inspired by the phenomenon of phase transition in physics. Traders are divided into two main groups: fundamentalists, who sell (respectively, buy) when the price is above (respectively, below) the fundamental value, and chartists (or “noise traders”), who buy or sell depending on whether optimism or pessimism prevails. Chartists, in turn, are subdivided into optimists and pessimists. Traders can switch between different groups, like particles would switch between different states. The number of individuals in these groups determines the aggregate excess demand, which results in changes in actual price, which in turn affect the agents’ trading strategy. Changes in fundamental value are governed by a random process. Switching between groups is governed by time-varying probability functions: the fundamentalist–chartist switch depends on a comparison of the respective profits (realized profits for the chartists, expected profits for the fundamentalists); the optimist–pessimist switch depends on an opinion index (representing the average opinion among chartists) and the price trend.

The system is at equilibrium when the price is on average at its fundamental value; there is a balanced proportion of optimists and pessimists, and an arbitrary proportion of chartists. This steady state is repelling—that is, the system is unstable—when either certain parameters are larger than some critical value or when the proportion of chartists exceeds a critical value, in which case, the system suddenly undergoes a tranquil-to-turbulent phase switch.

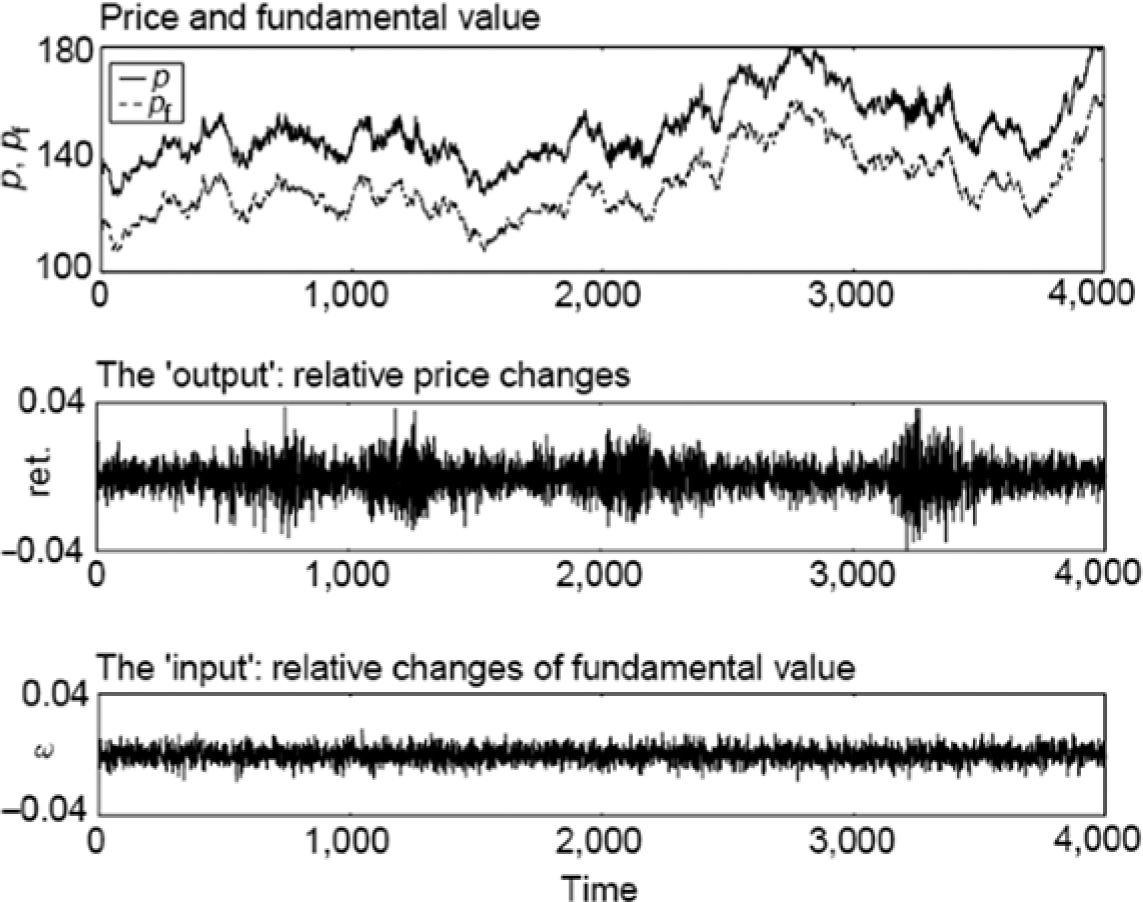

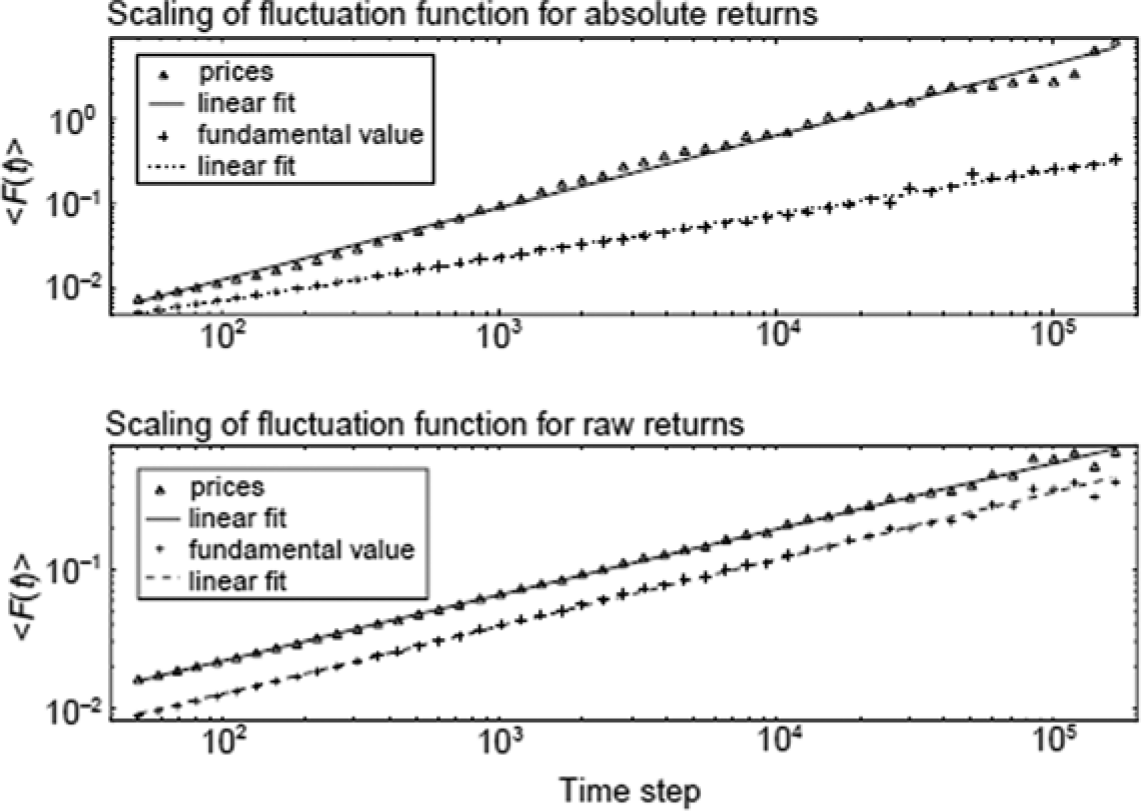

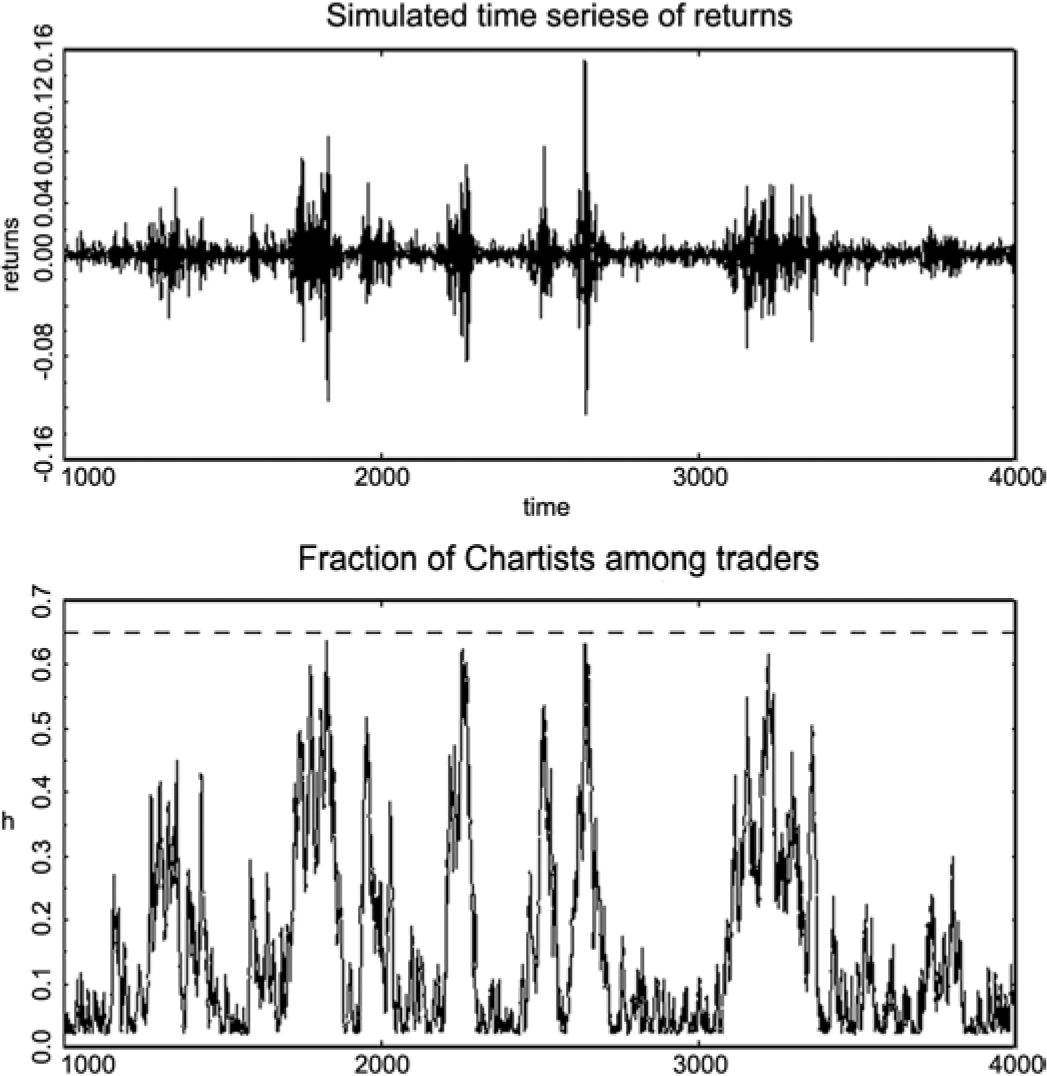

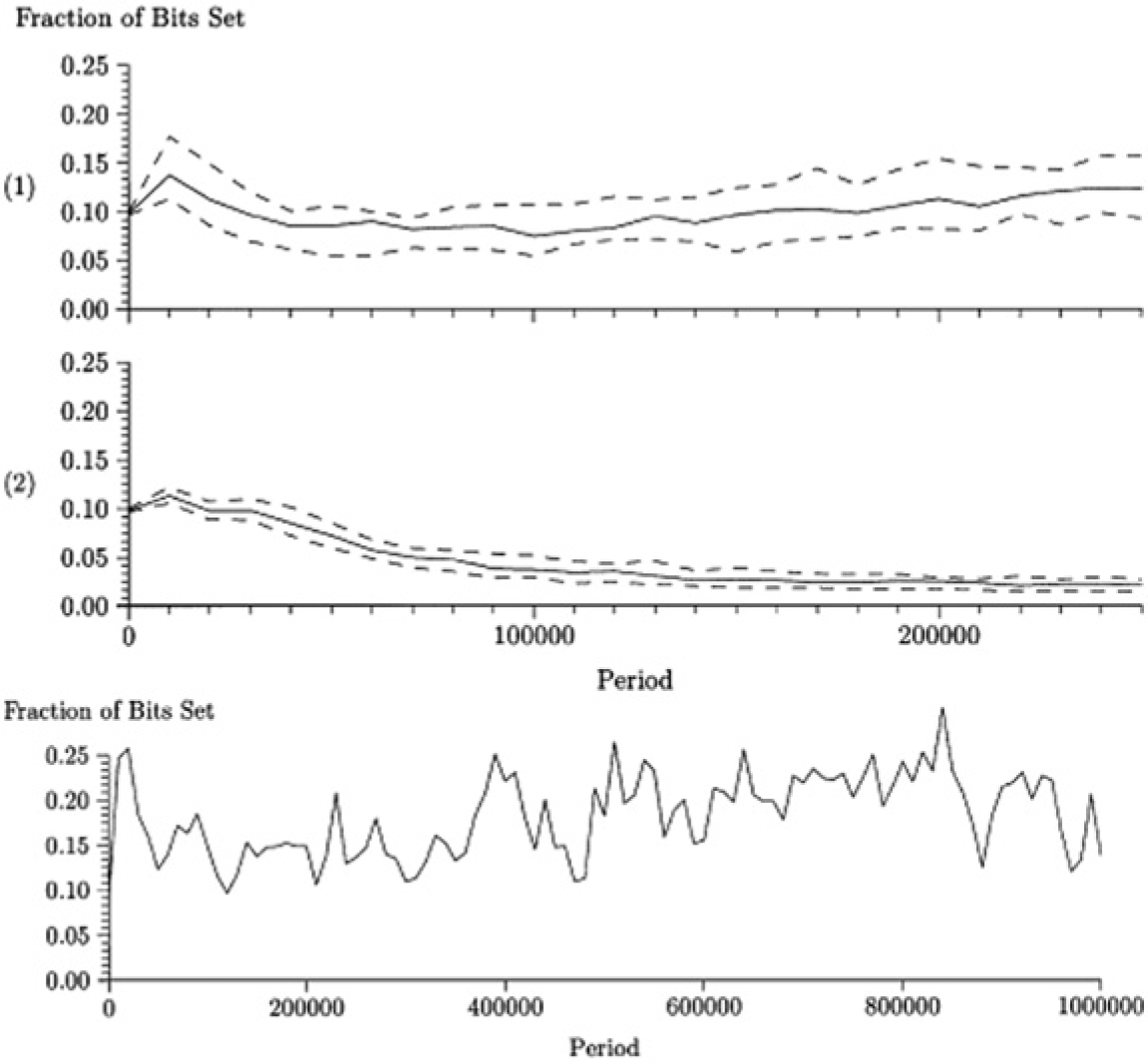

Simulation of the system in this steady state generates the aforementioned stylized facts. For instance, the time series of the market price stays close to the time series of the fundamental value, in agreement with the hypothesis that price variations are unpredictable (Figure 1, top). However, random changes in fundamental value (and the absence of exogenous shocks) (Figure 1, bottom) do not result in similarly normally distributed returns, the time series of returns exhibiting a higher-than-normal frequency of extreme events and volatility clustering (Figure 1, middle). In particular, the modelers show that the stylized facts depend on the endogenous switching mechanism rather than on the behavior of the exogenous force, that is, the changes in fundamental value. They use “detrended fluctuation analysis” to study the scaling properties of the average fluctuations F(t) of fundamental values, raw and absolute returns as a function of the time interval t, and to calculate the exponents of the corresponding power laws (Figure 2). 6 The analysis reveals that the slope of the power law of changes in fundamental price is similar to the slope of the power law of raw returns but smaller than the slope of the power law of absolute returns. This is a sign of strong persistence in volatility. And since the scaling properties of absolute returns are different from those of fundamental value changes, the former cannot depend on the latter. The authors also notice that for a wide range of parameter values, the volatility bursts robustly depend on whether the proportion of chartists in the market exceeds a critical value (Figure 3). Hence, they conclude that the volatility bursts are explained by the switches between groups driven by chartist behavior (see Lux and Marchesi 1999, 500; 2000, 679).

Volatility clustering.

Scaling of fundamental value changes, compared with that of raw returns (bottom) and absolute returns (top).

Dependence of return fluctuations (top) on the fraction of chartists in the market (bottom).

2.3. An Evolutionary Model

The second model, presented in (Arthur et al. 1997; LeBaron, Arthur and Palmer 1999), is inspired by the phenomenon of natural selection in evolutionary biology. Each agent in a population is a “theory” of trading rules. Each theory is like a genotype, made of 100 strategies, or rules. Each rule is like a chromosome, and consists in a set of predictors, comprising a condition part (a bit string of market descriptors) and a forecast part (a parameter vector). The condition part of a predictor is a string of 1s or 0s, which can be interpreted as the current price, respectively, fulfilling a market condition and not fulfilling the condition. Each bit represents either fundamental information (dividend price ratios) or chartist information (price moving averages). The forecast part contains parameters of a linear forecasting model of price and dividend. At the start of the time period, the current dividend is posted and observed by all agents. Each agent checks which of his predictors are “active,” that is, match the current state of the market. He then forecasts future price and dividend based on the most accurate of his active predictors and makes the appropriate bid or offer. The price is calculated by aggregating over the agents’ demands. At the end of the time period, the new price and dividend are revealed and the accuracies of the active predictors are updated, based on what should have been predicted in the presence of homogeneous REE. At regular intervals, but asynchronously, agents engage in a learning process for updating their theories. When learning takes place, the worst performing rules are eliminated and replaced by new rules formed by means of a genetic algorithm with uniform crossover (i.e., an interchange of subsequences of two chromosomes that creates two offspring) and mutation (i.e., a random flip of bits in the strings of 0s and 1s), which mimics the process of natural selection.

Simulations were run under a variety of conditions. Most importantly, different parameter values ensuing in different rates of the learning process were used. Statistical analyses were then performed to study the properties of the resulting time series (e.g., predictability, volatility) and the features of the learning process that determine them (condition bits used, convergence of forecast parameters). The general conclusion was that with slow learning, the price series are indistinguishable from what should be produced in the case of homogeneous REE, whereas with fast learning, the stylized facts are endogenously produced.

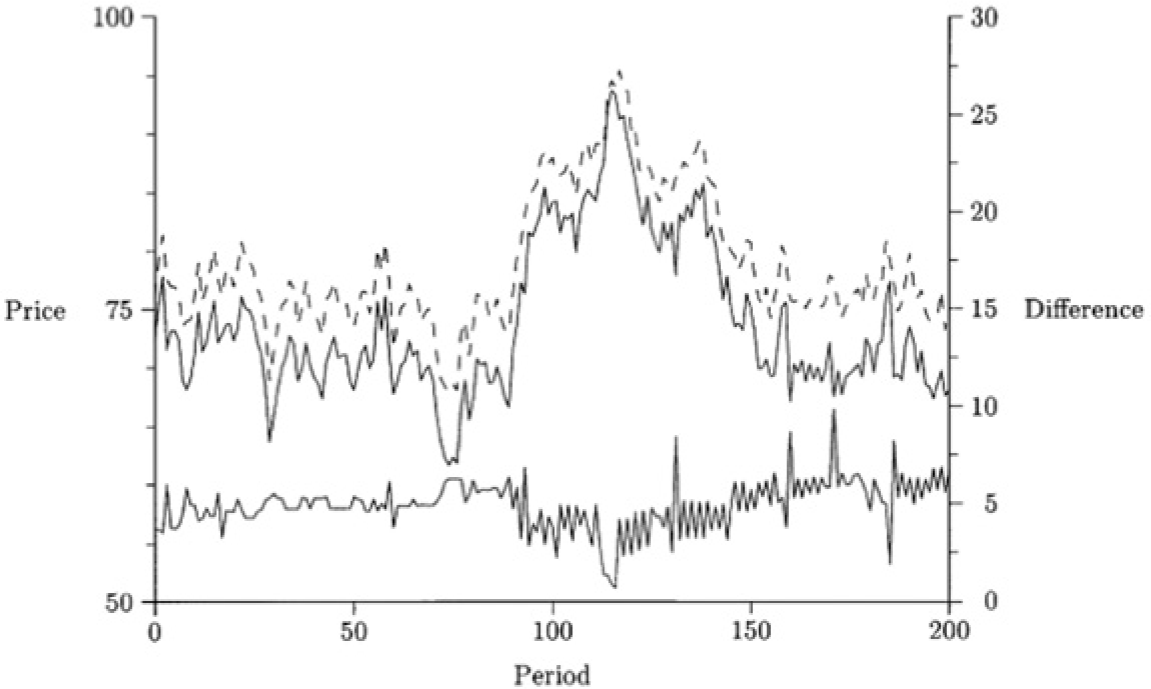

For instance, the price series, calculated by letting every agent adjust his demand according to his own forecasting rules, tracks very closely the fundamental value series, where market prices are calculated assuming homogeneous agents. Still, as was the case with the phase-transition model, the time series of differences between prices and fundamental values shows the presence of both tranquil periods and wild fluctuations (Figure 4). A study of the evolution in the use of the condition bits shows that with slow learning, the traders learn that chartist bits are of no use and as time advances tend to eliminate them from their trading strategy (Figure 5, top, 2). With fast learning, instead, the average use of chartist bits does not decay (top, 1) and in the long run keeps oscillating (Figure 5, bottom). The modelers take these results to show that complex regimes may arise even under neoclassical conditions (the benchmark used to calculate the rules’ accuracy is the homogeneous REE) and in the absence of exogenous shocks, because of the learning mechanism.

Volatility clustering.

Evolution in the use of chartist bits as a function of learning speed.

2.4. Learning from the ABMs

The ABMs in sections 2.2 and 2.3 show that minimal models may grant not only minimal learning but also not-so-minimal learning. They do show that something need not be the case: contrary to the EMH, big price changes are not necessarily driven by external shocks. But they also show that something is the case: asset pricing phenomena depend on an endogenous mechanism (the fundamentalist–chartist switch in one case, the use of chartist strategies in the other) responsible for the self-reinforcing process that drives prices up or down, and ultimately on the agents’ heterogeneity (the chartist behavior of some agents in one case, the inductive and adaptive behavior of all agents in the other case). This conclusion seems supported by an analysis of the modelers’ intentions. They interpret their own model not only as undermining a necessity hypothesis but also as explaining the stylized facts, by identifying the mechanism responsible for them. For instance, Lux and Marchesi state that their model proves not only that input signals are unnecessary to big price changes, which contradicts EMH, but also that switching determines the stylized facts: Financial prices have been found to exhibit some universal characteristics that resemble the scaling laws characterizing physical systems in which large numbers of units interact. This raises the question of whether scaling in finance emerges in a similar way from the interactions of a large ensemble of market participants. However, such an explanation is in contradiction to the prevalent “efficient market hypothesis” in economics, which assumes that the movements of financial prices are an immediate and unbiased reflection of incoming news about future earning prospects. Within this hypothesis, scaling in price changes would simply reflect similar scaling in the “input” signals that influence them. Here we describe a multi-agent model of financial markets which supports the idea that scaling arises from mutual interactions of participants. Although the ‘news arrival process’ in our model lacks both power-law scaling and any temporal dependence in volatility, we find that it generates such behaviour as a result of interactions between agents. (Lux and Marchesi 1999, 498, emphases mine)

Arthur et al. express similar remarks. For them, EMH was already sufficiently questioned by previous evidence. Not only does their model confirm this conclusion, but it also uncovers the mechanism responsible for the stylized facts: By now, enough statistical evidence has accumulated to question efficient-market theories and to show that the traders’ viewpoint cannot be entirely dismissed. As a result, the modern finance literature has been searching for alternative theories that can explain these market realities. (Arthur et al. 1997, §1, emphasis added) We conjecture a simple evolutionary explanation. Both in real markets and in our artificial market, agents are constantly exploring and testing new expectations. Once in a while, randomly, more successful expectations will be discovered. Such expectations will change the market, and trigger further changes in expectations, so that small and large “avalanches” of change will cascade through the system. (Arthur et al. 1997, §5, emphasis added)

I anticipate two obvious objections to my reconstruction. First, the ABMs are not minimal. Second, contrary to the authors’ intentions, they do not explain. I reply to these objections in, respectively, sections 3 and 4.

3. Minimality Defended

Recall the features of minimal models as defined by Grüne-Yanoff: minimal models are not similar (let alone isomorphic) to the world, they are not built based on laws, and they do not to isolate any real factors. The ABMs of asset pricing are prima facie minimal.

First, the ABMs have no strong similarity to their target, nor is there any clear specification of a concrete target. The models do not aim to approximate, say, the time series of IBM stocks in some specific time interval. They only contain fictional individual traders and ignore the role played by real entities such as firms, banks, financial, and regulatory institutions. Furthermore, the models misrepresent in clear respects. In the phase-transition model, it is obviously a fiction to represent agents as neatly belonging to either one or the other category. Also, it is in a sense unrealistic to postulate the existence of “unintelligent” noise traders switching into “intelligent” traders and back, but being otherwise unable to learn in any other way. Likewise, in the evolutionary model, it is a fiction to represent the agents’ trading strategies as binary strings of conditions and a linear forecast. Another unrealistic element is that learning agents are incapable of adjusting their learning pace by means of a coordination process. Also unrealistic is that there is no “social” learning between agents, and all learning goes via the observation of prices. Finally, the learning speed parameter—on which the stylized facts depend—has no clear interpretation in terms of real market mechanisms.

Second, the ABMs do not encode laws. There are few, if any, laws in the social sciences. Some would perhaps take REH as being one such law. The ABMs, however, do not rely on REH—they actually assume that REH is false. Or one could interpret the functions that figure in the models as describing the operation of real capacities or dispositions—the disposition to change one’s mood, or to learn by trial and error. But whatever the link between such capacities and their role in the model, the generalizations that describe them do not certainly count as laws in any strong sense—they are not universal, necessary, or the like.

Finally, the models do not—strictly speaking—isolate any real factors. 7 Variables and parameters (groups’ size, switching functions, genotypes, learning speed, etc.) are hard to interpret—their world-linking properties are unjustified or undetermined—hence they do not lend themselves to the isolation procedure. One might think that what is isolated is the agents’ heterogeneity. However, this is not the case. First, isolation presupposes that interactions with other factors are omitted or idealized away. But it is at least unclear what factors “interact” with heterogeneity and how such interactions are controlled for. Second, no idealization should be introduced in the isolated factor itself, which should be represented as it is. However, the ABMs’ representation of heterogeneity is the result of obvious idealizations.

Still, one may object that, contrary to appearances, the ABMs do not count as minimal models in Grüne-Yanoff’s sense because they do bear some similarity to their targets. As I mentioned, a key feature of minimal models is that they be credible based on their coherence rather than on similarity considerations. In contrast, the ABMs get at least some credibility from similarity. The modelers do justify the models’ role as surrogates for something vaguely resembling a real market. For instance, the two artificial markets get some credibility from analogies. In one case, the market is analogous to a system undergoing phase transition (cf. Rickles 2011, §7.3). In the other case, the market is analogous to a population undergoing natural selection. Also, the artificial markets are credible because they make (more) plausible psychological assumptions by giving up the homogeneity assumption. Heterogeneous agents are more similar to real agents than the homogeneous agents of the neoclassical model.

But then the question is, if the ABMs are not minimal on these grounds, what models are? Lack of any similarity makes it implausible for a model to represent anything. And if it were impossible to draw any connection between the model and the world, it would be a mystery how the model can tell something—even negatively so—about the world. Some similarity is usually presupposed for learning from economic models. This seems true even of the Schelling’s model cited by Grüne-Yanoff. Schelling does after all interpret coins as agents, cells as households, and so forth. And if a model gets some credibility from its similarity, is it thereby non-minimal? Arguably, not. I would argue that the ABMs must be considered minimal after all, in the sense that they approximate very closely the specific conditions laid out by Grüne-Yanoff.

Similarity comes in degrees and in various ways. Grüne-Yanoff’s definition picks out “literally minimal” models, namely, models that bear no similarity to their targets. Very few, if any, economic models belong to this class—surely neither the ABMs nor Schelling’s model. At the other end of the spectrum are models that are similar to their targets in the sense that they are isomorphic to them, describe laws of nature, isolate natural kind properties, and so forth. Again, very few models, whether in economics or in other disciplines, qualify as similar in this sense. The majority of scientific models lie somewhere in between these extremes. Toward the non-minimal end of the spectrum, one finds models that approximate more closely Grüne-Yanoff’s conditions. Causal models, for instance, are typically built out of ceteris paribus generalizations describing dependences among higher-level properties that resemble dependences in real structures; the generalizations can be studied in isolation and, according to many, they hold (or fail to hold) depending on more fundamental laws describing relations among natural kind properties. Toward the minimal end of the spectrum, one finds models such as Schelling’s model and the ABMs of asset pricing, which bear weak similarity relations to their targets. Calling them “minimal” seems fully legitimate, in agreement with both philosophical intuition and scientific practice. 8 In the next section, I consider whether and how they can, in spite of their weak similarity, function as surrogates for their targets and teach something about them.

4. Explanation Defended

As mentioned in section 1, Grüne-Yanoff holds that (partial) explanation depends on isolating the effect of some real factors. Clearly, if the ABMs explain at all, this is not because they isolate something. From this, Grüne-Yanoff would argue that they grant only potential explanations. In contrast, I believe one should draw a different conclusion: the ABMs show that minimal models may explain without relying on isolation. It is not the modelers’ intention to offer a realistic model, which allows for the isolation of explanatory factors (see Arthur et al. 1997, §6). Rather, the aim is to build a model, which is credible as a whole, and not in virtue of the credibility of the individual components. Several kinds of credibility should be distinguished, which are left undistinguished by Sugden and Grüne-Yanoff, if one is to assess the merits of the corresponding explanations in their own right. 9

On the one hand, “credibility-with-respect-to-intuitions” differs from “credibility-with-respect-to-the-target.” As mentioned, Grüne-Yanoff proposes that the credibility of minimal models is analyzed in terms of intuitions and coherence considerations. I think this is all very well, but it leaves out a part of the story, namely, the issue of assessing the credibility-with-respect-to-the-target, if any, of minimal models. Economists always construct models as models of something. It seems undesirable to build into the definition itself of minimal models that they be credible with respect to intuitions only. This would by fiat prevent the models from allowing more than merely potential explanations. If one does not impose this, the possibility remains that one learns from minimal models because they are credible with respect to their targets, too, and not just intuitions. Whether they are credible with respect to their target despite not being isomorphic to it, not adhering to laws, and so forth is a contingent issue—orthogonal to, and not necessitated by, whether they are minimal.

On the other hand, credibility-with-respect-to-the-target should not be reduced to “realisticness,” that is, the kind of credibility that depends on isomorphisms, adherence to laws, isolation of causal factors, and so forth. The two kinds of credibility are different and grant different kinds of (actual) explanation. 10 Realisticness is a stricter condition, which depends on the credibility that individual components of the model get from isolation (cf. Mäki 1992, §3). Credibility-with-respect-to-the-target is a weaker condition, which depends on the credibility of the model as a whole. When Sugden talks of credibility being aided by judgments of coherence with one’s knowledge of causal processes, he seems to have in mind the latter kind of credibility, not the former. However, the fact that he does not clearly distinguish between the two weakens his case. One could, in fact, read him as holding the somewhat inconsistent claim that idealized economic models are credible because they mimic real causal processes, in the sense that they are isomorphic with them, or isolate them, or represent causal laws. And I conjecture that Grüne-Yanoff’s dichotomous distinction between minimal and unrealistic models and non-minimal and realistic ones is a reaction to precisely this latter interpretation of Sugden’s claim.

I think the ABMs case illustrates well the rationale for building credible-with-respect-to-the-target (minimal) models that are neither realistic, in the sense of allowing isolation, nor merely credible-with-respect-to-intuitions, in the sense of allowing conceptual exploration only. I propose that credibility-with-respect-to-the-target is analyzed in terms of the procedures that justify a model’s external validity. Once one knows whether the model can generate externally valid results, one also has a justification for believing such results, that is, for learning from the model.

I draw here on Winsberg’s (1999, 2009) account of “sanctioning” a model’s external validity. For Winsberg, experiments are not intrinsically better than models. Only, their external validity depends on different kinds of justification and on—one might say—different kinds of credibility. The external validity of an experiment depends on realisticness, that is, on some factor in the experimental system being successfully isolated and on the target system being materially similar to it in the relevant respect. Instead, the external validity of a model depends on credibility-with-respect-to-the-target, that is, on making good use of the right “principles for model building,” namely, principles that tell how to build a good model of the target. 11 Importantly, good principles are not necessarily isolating principles but may vary depending on the model’s target.

In the ABMs case, the following combination of principles make the model credible-with-respect-to-the-target and sanction the validity of the explanation: (1) the soundness of theoretical principles, psychological assumptions, and functional analogies; (2) the robustness of the results across changes in initial conditions and parameter values; and (3) the robustness across changes in modeling assumptions. Principles in (1) make the model credible-with-respect-to-the-target and not just intuitions. Principles in (2) and (3) make the model credible-with-respect-to-the-target although not realistic.

Let us start with (1). Phenomena such as scaling laws and time series with complex textures are observed in mechanisms studied by other sciences, too, from physics (phase transition) to biology (natural selection). There, they are brought about by dishomogeneities in the constituents of the system (states of the particles, genetic codes of individuals) that generate self-reinforcing feedbacks (phase transitions catalyzing themselves, genetic traits becoming more and more entrenched). In spite of the obvious diversity among the various systems, the explanandum is known to require certain key conditions, namely, heterogeneous components and non-linearities. So, theoretical principles suggest that these conditions must be instantiated in the asset pricing case too. The way the heterogeneity is represented in the market depends on the analogy that guides the construction of the model: it is as if agents switched or evolved, and as a result transition—or evolution-cascades obtained. In one case, the heterogeneity is realized by different dispositions, in the other case by different expectations. In both cases, the analogy contributes to the credibility of the model as a whole because the new psychological assumptions are more plausible than the neoclassical assumptions. This analogical reasoning is illustrated by the way Lux and Marchesi motivate their model: [ . . . ] an elementary requirement for any adequate analytical approach is that it must have the potential for bringing about the required behaviour in theoretical time series. Therefore, it seems rather obvious that one has to go beyond linear deterministic dynamics, which of course is insufficient to account for the phenomena under study. Furthermore, allowing for homogeneous (white) noise in some economic variables will also not achieve our goals simply because . . . we are dealing with time-varying statistical behaviour. In fact, the situation one faces is more often encountered by natural scientists. What one wishes to explain is a feature of the empirical time series as a whole. In the natural sciences, such characteristics of the data are often described by scaling laws [ . . . ]. (Lux and Marchesi 2000, 678)

The modelers include the stylized facts in a broader class of phenomena and hypothesize that there is some common feature in the mechanisms that generate such phenomena. The stylized facts do not depend on the contribution of linearly independent factors. The isolation of one factor (e.g., the attitude of a group, or the effect of a trading rule) would eliminate the nonlinear character of the interactions, and hence destroy the self-reinforcing mechanism that generates the stylized facts. So, credibility is a property of the whole mechanism rather than isolated portions of it.

The credibility-with-respect-to-the-target is enhanced by the robustness tests performed on the results, that is, by using principles (2) and (3).

First, the robustness of the results is tested by sensitivity analyses on all factors for which no clear interpretation or calibration to realistic values is possible. This involves systematically varying many factors that regulate the internal working of the mechanism, namely, initial conditions (e.g.: initial distributions of agents in the various groups; initial structure of the trading rules in the various theories) and parameter values (e.g.: parameters that regulate the frequency of reevaluation of opinion and the weight exerted on the switch by the majority’s opinion, the price trend and the profit differential; the parameter that regulates the learning speed). Since the results are robust across such variations, one can exclude that they are an artifact of the model design, that is, that they depend on assumptions that have no representational value or that involve unrealistic (mis)representations.

Second, the interpretation of the results of the two models shows that the results are robust in yet another sense—they are robust across variation in modeling assumptions with regard to the exact nature of their key explanatory factors, namely, the agents’ heterogeneity and the self-reinforcing mechanism generated by it. It is as if the modelers employing the aforementioned principles also subscribed to the following meta-principle: the external validity of an explanation increases if it is possible to show that an entire class of models reproduce the same phenomenon, 12 and the mechanisms represented by the models in the class are different “tokens” of the same “type,” each one occupying the same functional role and carrying some credibility with respect to its target. In the asset pricing case, the two ABM explanations instantiate the same type of explanatory pattern, although in different ways. The phase-transition model explains in terms of different attitudes resulting in a switching feedback, such that at sometimes large proportions of chartists are in the market. The evolutionary model explains in terms of different expectations resulting in a learning feedback, such that at sometimes certain chartist strategies become useful. Both models explain by postulating a mechanism where the heterogeneity of the agents produces an endogenous, self-reinforcing, and destabilizing feedback.

The rationale for testing the two kinds of robustness (across initial conditions and parameter values, and across different “modalities,” or model designs) to validate the conclusions of simulations is nicely described by Muldoon: Rather than finding the single simulation that uses the appropriate parameter set to generate the phenomenon, we look for the class of simulations that generate the phenomenon. One simulation can be a fluke. A class of simulations that vary by both parameters and across modalities suggests a robust phenomenon. (Muldoon 2007, 881)

It is instructive to contrast the role of robustness in Schelling’s model and in the ABMs. The obtaining of the segregation patterns in Schelling’s model is less robust than the obtaining of the stylized facts in the ABMs. Schelling represents only one simple type of grid, only two groups of agents, only agents that aim to satisfy one preference, and so forth. Schelling does declare that his results will hold true if other representations are explored (e.g., if square cells are replaced by triangular cells). But do they? Sugden claims that Schelling’s model grants knowledge about the world based on an inductive procedure: segregation is observed in many real cities and is reproduced by simulating what could happen in many artificial cities that could be real. However, for this inductive step to be justified, there seems to be too little variation among the fictional instances. The result is tested only across different initial distributions of agents on the same grid and different preference strengths. We have no evidence that, say, certain housing preferences operate in all cities and are always responsible for segregation. Different kinds of preferences and other institutional or material constraints may be at work. Since underlying seemingly similar segregation patterns there might be very different mechanisms, no one of them can be invoked without further evidence as “the” explanation of segregation patterns. 13 I believe that the lack of robustness across different modeling assumptions may explain why Grüne-Yanoff, who generalizes from this exemplary case, holds that learning from minimal models is limited to undermining necessity and impossibility hypotheses.

However, things are clearly different in the ABMs case. Each ABM taken separately allows for a broader exploration of the space of possibilities because it controls for many aspects of the postulated mechanisms. And the two ABMs taken together also offer evidence that the phenomenon is robust across different designs of the mechanism. Thus, learning from the ABMs goes beyond undermining necessity and impossibility hypotheses. Although we have no evidence that in all markets the stylized facts depend on switching, or that in all markets they depend on learning, and so forth, we do have reasonably strong evidence that in all markets they depend on heterogeneity. So, it seems legitimate to say that heterogeneity explains the stylized facts.14,15 This explanation has, to my mind, two key features. First, heterogeneity does not figure as a factor that may or may not be present but rather as the same factor which can be variously realized. This makes the explanation general, in the sense that it does not rely on the truth of any fine-grain hypothesis on the nature of heterogeneity. 16 Second, the explanation is partial, in the sense that it only tells nothing-but-the-truth on one factor responsible for the stylized facts, the whole truth arguably comprising the role of other factors such as the exogenous changes in fundamental value. In general, distinct factors or mechanisms may positively interact with one another, by amplifying or overdetermining their effect on the target phenomenon, or they may negatively interact, by decreasing their effect or pre-empting each other (cf. Ylikoski and Aydinonat 2013, 28). In the asset pricing case, arguably non-random changes in fundamental value do not pre-empt the operation of heterogeneity but rather positively interact with it. At the same time, such changes are not as explanatory of the stylized facts as heterogeneity: one or more non-random shocks may trigger a bubble or a crash but cannot determine the statistical features of volatility as a whole.

One may then wonder whether this sort of explanation is deep enough. As I said, the two ABMs cannot prove what precise fact about the heterogeneity of the agents is responsible for the stylized facts. Differences in dispositions or expectations are not the only ways in which agents may be heterogeneous. Other models of asset pricing exist, which represent the heterogeneity as dependent on, say, a disagreement on the time required for the price to converge to the fundamental value, or an asymmetry of knowledge about the fundamental value, or a difference in the investment horizon for different investors, and so forth (cf. Markose, Arifovic, and Sunder 2007). The variety in the possible realizations of heterogeneity makes the identified mechanism hard to pin down and put to use. What do the parameters measure exactly? How can they be used to predict or intervene? Yet, the generality of the explanation suggests that models leading to more concrete interpretations, whatever their fine-grain details, will be structurally similar. For instance, more realistic models (see Schleifer 2000, chap. 4; Thurner, Farmer, and Geanakoplos 2012), which also represent entities with different roles (private investors, professional arbitrageurs, funds, banks, etc.) and non-symmetric interactions among them, hold on to the key feature identified by their cognate minimal models: the stylized facts are explained by some fact or other about the heterogeneity among the economic agents.

5. Conclusion

Many economic models are “minimal,” in the intuitive sense that they are not meant to be realistic representations of their targets. Still, they stand in for such targets. So the question arises: What, if at all, can we learn from them?

In this article, I have shown that learning from minimal models depends on the principles for model building that are used in their construction and make them externally valid. In particular, learning from minimal models need not be limited to conceptual explorations of what could be the case, and to negative conclusions, namely, to undermining impossibility or necessity hypotheses. If the right principles are used, minimal models can grant positive conclusions about what is the case, even if the models are not isomorphic to their targets, do not make use of laws, and do not isolate real factors. For instance, ABMs of asset pricing explain the stylized facts of finance in terms of the agents’ heterogeneity, even if the way the heterogeneity is represented and the mechanisms the heterogeneity gives rise to are not realistic. The explanation depends on the identification of a credible pattern through which the heterogeneity generates the stylized facts via a self-reinforcing feedback mechanism. The credibility of this pattern is enhanced by the robustness of the results across changes in initial conditions and parameter values as well as general design principles.

Minimality is orthogonal to external validity: one cannot draw conclusions about the external validity of a model from the mere fact that it is minimal. We should not be too quick in generalizing from the scarce external validity of some minimal models (e.g., Schelling’s model) to the lack of external validity of the others (e.g., ABMs of asset pricing). Rather, we should evaluate them one by one to find out if they grant just so-stories or something more.

Footnotes

Acknowledgements

I am grateful to Roberto Ganau, Catherine Herfeld, Gianluca Manzo, Alessio Moneta, and two anonymous referees for valuable comments on previous versions of this article. I also wish to thank the audiences of INEM, Rotterdam, June 13-15, 2013; and ENPOSS, Venice, September 3-4, 2013, where this article was presented.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Alexander von Humboldt Foundation.

1

For a brief explication of the isolation procedure, see below. For a thorough presentation of the method of isolation in economics, see Mäki (1992). Notice, however, the different role of isolation for Mäki and Grüne-Yanoff: whereas for Mäki, isolation (better: the attempt to isolate) constitutes the nature of representation (cf. Mäki 2005), for Grüne-Yanoff, it is the (success) criterion a model should meet if it is to represent, a criterion that idealized models fail to meet (see below; also see ![]() ).

).

2

Alternatively, one may randomize to ensure that lack of knowledge about the other factors’ interaction with the tested factor does not affect the significance of the experiment.

3

The fundamental value is defined as the “discounted sum of future earnings,” and calculated by summing the future income generated by the asset (interests), and discounting it to the present value to take into account the delay in receipt.

4

Power laws are distributions characterized by a cumulative distribution function

5

This is the correlation between values of returns at different times, as a function of their time difference.

7

On the lack of isolation in idealized economic models, both Sugden and Grüne-Yanoff agree. (See Grüne-Yanoff 2009, §7; 2011b; ![]() , §4.)

, §4.)

8

Not only is reference to similarity do no useful job in the definition of minimal models, it is actually misleading. It seems, thus, sensible to modify the definition by-at least-dropping mention of similarity, namely, “minimal models are assumed to lack any isomorphism or resemblance relation to the world, to be unconstrained by natural laws or structural identity, and not to isolate any real factors.” This allows one to (minimally) specify the ways in which minimal models are not similar, but otherwise leave it open that they may be similar in some other, weaker sense.

9

10

But I am skeptical that there is any context-independent way of measuring credibility or explanatory strength.

11

Winsberg is directly concerned with modeling phenomena for which a background of sound theories is available. However, his take-home message generalizes to other sorts of background knowledge. Trust in the external validity of the model comes “from a history of past successes” (![]() , 587); although Winsberg lists three kinds of background knowledge (theory, intuitive or speculative acquaintance with the system, and reliable computational methods) that warrant such a trust in one case (viz., physics), he leaves it open that “there may very well be other, similar ones” (Winsberg 2009, 587) that are relevant to other cases.

, 587); although Winsberg lists three kinds of background knowledge (theory, intuitive or speculative acquaintance with the system, and reliable computational methods) that warrant such a trust in one case (viz., physics), he leaves it open that “there may very well be other, similar ones” (Winsberg 2009, 587) that are relevant to other cases.

12

13

14

It would seem that this kind of explanation is causal. However, discussing whether or not this is so would require an argument that goes beyond the scope of this paper.

15

Obviously, one may still want to dispute that this evidence is actually sufficient to explanation. However, this would run contrary not only to my argument (which might be flawed) but also, and more importantly, to the scientists’ own interpretation (cf. §2.4), and one would be left with the task of explaining why their intuition is mistaken.

16

Among other things, this has the advantage of compensating for the lack of “empirical calibration” of the models (Fagiolo, Moneta, and Windrum 2007).