Abstract

The paper explains antecedents and consequences of news during the BP oil spill crisis by analyzing newspaper and internet coverage as well as financial indicators. The study establishes the roles of routines in financial journalism and of BP’s public relations efforts in building the U.S. media agenda. The U.S. media agenda in turn bears a classic agenda-setting effect on public awareness, an intermedia agenda-setting effect on foreign media, and a stakeholder agenda-setting effect on financial markets. A second-level attribute agenda-setting post-hoc study reveals that these first-order agenda setting effects depend on the resonance of specific problems and solutions with specific interests and a specific frame of mind. Financial stakeholders, for example, reacted negatively to news about judicial accountability, but positively to press releases about BP’s skills in implementing solutions. The findings contradict research which states that the news in classic media merely mirrors share prices.

Organizational crises render organizations newsworthy, because they threaten an organization’s reputation and financial performance (Huang, 2006, Seeger, Sellnow, & Ulmer, 2003), with stakeholders calling for an immediate repair of the disrupted order (Patriotta, Gond, & Schultz, 2011). In such crises, it may be the news which propagates the crisis rather than the incident itself, thereby affecting the corporation, its publics, and its stakeholders. In the BP oil spill crisis, for example, according to Haley Barbour, the governor of Mississippi, the news coverage had been more devastating for tourism in the region than the actual amount of oil washed on the shores.

Communication research has focused on the processes, antecedents, and consequences of news media in a broad range of societal systems. The impact of the issue agenda in the media on the salience of issues for publics (McCombs, 2004; McCombs & Shaw, 1972), the impact of the political agenda on the media agenda (Walgrave & Van Aelst, 2006), and the impact of corporate communication on news media (Chang, 1989; Kiousis, Popescu, & Mitrook, 2007) have been studied in depth. Although new corporate issues often emerge in crisis situations, remarkably little research has been conducted to arrive at a full picture of the interplay between corporate communication, the media, stakeholders, and mass publics during a crisis. Most studies concentrate on media and publics by means of experimental research (e.g., de Vreese, Boomgaarden, & Semetko, 2011) or by combining media content analysis data with panel survey data (e.g., Matthes, 2012). Public relations studies analyze the effects of organizations’ crisis communication on publics or individuals (e.g., situational crisis communication theory [SCCT], see Coombs, 2007; Jin, Liu, & Austin, 2011) mainly through experiments, but studies that take the mediating role of media into account are sparse (but see Huang, 2006; Kiousis et al., 2007). Comprehensive studies that also take other business-relevant factors such as stock prices and foreign news media into account are lacking. This motivates our research question on the antecedents and the effects of the news in a long-standing crisis.

The BP oil spill crisis was the most serious corporate crisis in the oil industry after Exxon (1989) and Shell (1995). It started on April 20, 2010, 9:45 p.m., when gas, oil, and concrete from the Deepwater Horizon exploded up the wellbore onto the deck, killing 11 platform workers. On the morning of April 22, the Deepwater Horizon sank. On April 24, BP reported that 1,000 barrels were being spilled each day, but on April 28 the leak was estimated at 5,000 barrels per day by the National Oceanic and Atmospheric Administration. The price of BP shares dropped dramatically in May and June during the ensuing debate on the amount of damage and clean-up costs involved, as well as the judicial accountability for this. When President Obama entered the debate by flying to Louisiana on May 3, the media attention reached new peaks. Obama attributed the responsibility for the crisis to BP, but did not impose specific solutions. Political trust in President Obama declined during the crisis, whereas a series of BP announcements proposed ever new technological solutions with appealing labels to shut the leak (e.g., “top hat,” “junk shot”). In July, the BP share price recovered. At the end of July, BP finally succeeded in sealing the cap after 4.9 million barrels (185 million gallons of oil; 53,000 barrels per day) had leaked into the ocean. On July 27, the BP board announced that Bob Dudley was to replace Tony Hayward as CEO. In the months thereafter, BP disappeared from the news headlines, although the “environmental trial of the century” to determine how much BP would be required to pay for environmental destruction only started in 2013, after new reports were published on the toxicity of the oil dispersant Corexit (Rico-Martínez, Snell, & Shearer, 2013) that BP used to limit environmental damage.

To answer the research question, we investigate whether and how journalists react to actual financial performance indicators (Castelló, 2010) and public relation efforts (Kiousis et al., 2007). Second, we analyze the effects of the U.S. news on public awareness (classic agenda-setting; for example, McCombs, 2004; McCombs & Shaw, 1972), on foreign news media (intermedia agenda-setting; for example, Farnsworth, Soroka, & Young, 2010; Vliegenthart & Walgrave, 2008), and on stock prices (stakeholder-agenda-setting, for example, Scheufele, Haas, & Brosius, 2011; Tetlock, 2007). We will also test whether expressions of public awareness on the internet influence the stock price, as indicated by Bollen, Mao, and Zeng (2010). We do not have access to a representative compilation of statements of the U.S. government and of environmental pressure groups, but we will test whether attention for them in BP press releases, U.S. news, and foreign news had a special impact.

Antecedents of News in an Organizational Crisis

An almost trivial assumption is that news channels will report on major organizational crises in a negative way. Journalism scholars (Castelló, 2010; Tambini, 2010) and economists (Stiglitz, 2011) contend that the news about risky industries is largely positive, as long as economic performance is satisfactory, because, among other things, the time available to professional financial journalists in the cost-saving media industry decreased, while corporate investments in public relations increased (Tambini, 2010). Risky industries such as the petrochemical industry are framed in the news in economic terms, just as every other industry (Castelló, 2010).

An organizational crisis, however, gives the news a negative quality. Nevertheless, the literature suggests that variations in the amount of news about the crisis remain dependent on the news-gathering routines of journalists, and thus on indicators of financial performance (H1) and public relations efforts (H2). Recent studies document that changes in the amount of news will be preceded by changes in trade volume (Scheufele et al., 2011) and in PR efforts (Kiousis et al. 2007). For journalists, trade volume and press releases become signals of crisis severity.

Hypothesis 1 (H1): The amount of news on BP in U.S. media will increase due to an increase in the trade volume of BP stocks.

Hypothesis 2 (H2): The amount of news on BP in U.S. media will increase due to BP press releases.

Consequences of News in an Organizational Crisis

Classic Agenda-Setting

The main argument in agenda-setting research is that issues on the media agenda raise public awareness (McCombs, 2004). The transfer of issues from the media agenda to the public agenda is a robust media effect in the domains of political communication (e.g., Sheafer & Weimann, 2005) and corporate communication (e.g., Carroll, 2011). Furthermore, although new media (e.g., blogs, social networks) have enabled the public to express its agenda directly, research results thus far point in the direction of a top–down agenda-setting process in which opinion leaders alter the agenda of their followers in blogs and web forums (Himelboim, 2008; Kiousis et al., 2007; Miller, 2010). H3 is based on research findings on the classical agenda-setting effect. We use the number of Google searches for BP as an unobtrusive proxy for public awareness because it offers a daily behavioral measure that is not affected by social desirability or cognitive biases.

Hypothesis 3 (H3): An increase in the amount of news on BP in U.S. media results in an increase in public awareness.

Intermedia Agenda-Setting

Intermedia agenda-setting is concerned with the transfer of issues from leading media to other media (e.g., McCombs, 2004; Vliegenthart & Walgrave, 2008). Due to the fact that the US environment was at risk, and because the news in Europe usually lags 1 day behind the news that occurred during working hours in the United States, it is expected that U.S. media will set the agenda of U.K. media, even though BP is a British firm with a stock market quotation in London.

Hypothesis 4 (H4): An increase in the amount of news on BP in U.S. media will result in an increase in the amount of news on BP in U.K. media.

Stakeholder Agenda-Setting

In recent decades, the number of financial transactions has increased tremendously. The total number of shares traded during the entire 1960s is far exceeded by the number of shares traded during a single average week in 2013. As a side effect, the number of risky network dependencies has increased as well (e.g., who lends to whom, who securitizes whom, who brings whom to court). Investors only gradually become aware of these dependencies through potentially incomplete or biased financial, economic, and political news provided by relatively slow media such as newspapers, radio, and television (Stiglitz, 2011), for example, about judicial procedures that could threaten BP’s survival. Financial stakeholders may wait until a broader picture emerges in relatively slow media. By contrast, the Efficient Market Hypothesis (Fama, 1965; Frank, Bernanke, & Kaufman, 2007) posits that the news will either have no effect or an immediate effect. Shares would be sold immediately in the case of “reliable” news of a downfall the next week, thereby giving rise to a self-denying prophecy. Existing research appears to indicate that in relatively good times the news has hardly any effect on markets (Wu, Stevenson, Chen, and Guner, 2002; Schuster, 2006). Scheufele et al. (2011) analyzed the effects of newspaper and TV coverage on the stock prices of eight German companies during the summer months in which these companies were not involved in high news peaks. Instead of molding the share price, the media mirrored actual stock developments. Other studies based on an automated content analysis of the news with the General Inquirer (Stone, Dunphy, Smith, & Ogilvie, 1966) did find effects, however (Loughran & McDonald, 2011; Tetlock, 2007). Kleinnijenhuis, Schultz, Oegema, & Van Atteveldt (2013) found that in the financial crisis of 2007 to 2009, negative news exacerbated the fall in the share prices of banks. Negative news during the recent financial crisis affected not only market volatility, but also the co-movement of national stock markets (Casarin & Squazzoni, 2013). Many high-frequency traders use automated algorithms that incorporate an automated sentiment analysis of the news (Groß-Klußmann & Hautsch, 2011). We expect therefore that a large amount of crisis news will exert a downward pressure on share prices (H5).

Hypothesis 5 (H5): An increase in the amount of news on BP in U.S. media will lead to a decrease in the BP share price.

Research findings of Bollen et al. (2010) show that public awareness, as measured by tweets collected from Twitter, also predict the value of the Dow Jones Industrial Average. In line with these findings, H6 predicts that public awareness as measured by searches for BP on the internet will influence share prices. In contrast to Bollen et al. (2010), we will test explicitly whether the correlation between public awareness as measured by internet activity and future share prices is actually a spurious correlation as a result of increased attention in the mass media, that is, an artifact of H3 and H5.

Hypothesis 6 (H6): An increase in public awareness of the BP oil crisis will give rise to a decrease in the BP share price.

Dependency of PR and Impact of PR on the Share Price

We expect also a direct effect on the share price. Coombs (2007), for example, argued in his SCCT that reputational threat is highest in intentional crises like the BP crisis in which the corporation is perceived as being responsible, but accommodative communication strategies and acceptance of responsibility minimize the loss of reputation in these cases (see also Huang, 2006). Lamin and Zaheer (2012) found indeed that investors react positively to an accommodation strategy. Kiousis et al. (2007) examined the relationship between press releases, media coverage, and financial performance of companies. The topics of the press releases were reflected to some degree in the news coverage, which—at least in some of the studied newspapers—predicted the profits of companies. We will test here whether the BP press releases also exerted a positive direct effect on the share price.

Hypothesis 7 (H7): BP press releases will result in an increase in the BP share price.

Figure 1 combines the hypotheses in a path diagram of the research model. The test of the research model will show not only whether the hypotheses hold, but also whether omitted relationships and reverse relationships are significant, thereby revealing who leads and who follows in the publicity about the BP crisis.

The research model as a path diagram.

Post Hoc Analysis to Explore Second-Level Agenda-Setting

H1 to H7 are “first-level” agenda-setting hypotheses, in that they assume that attention for BP increases the accessibility of BP in the minds of audiences, media, and stakeholders, almost regardless of selective perception due to their specific interests and specific frames of mind. The second level of attribute agenda-setting, or “emphasis framing,” assumes that attributes of the news that receive a lot of attention will become salient in the minds of publics as well (McCombs, 2004). Second-level agenda-setting resembles emphasis framing, but in the case of framing, an additional hypothesis is that specific attributes of the news (in this case about BP) will make it more or less likely that an audience with a specific frame of mind will process, or even apply, this specific news (D.A. Scheufele & Iyengar, forthcoming).

To investigate the role of second-level attribute agenda-setting and framing in the BP crisis, we will analyze which content attributes accounted specifically for the first-level influence of the agenda of X on the agenda of Y. The post hoc analysis starts out from Entman’s definition of framing (1993) as a combination of “a particular problem definition, causal interpretation, moral evaluation, and/or treatment recommendation.” Accordingly, we expect that second-level agenda-setting in the BP publicity process is based on attribute agenda-setting with respect to threats for the environment, threats for the survival of BP, judicial accountability of BP, moral condemnations of BP, solutions for the oil spill, and treatments for the environment. We may expect, for example, that information about BP’s judicial accountability and the threats to BP’s survival will resonate with the interests and the frame of mind of financial stakeholders, whereas threats and solutions for the environment will resonate more with the frame of mind of the general public.

Method

Data and Operationalization

BP trade volume and BP share price

Daily data about the BP share price at the close of the trading day, and the trade volume of BP shares were obtained from DataStream®.

News coverage

The data on the BP oil spill extend over a period of 4 months, starting with the first news on the oil spill on April 22 until August 27, 2010. By this time, the leakage had already been stopped, but it took some time for it to be officially declared closed. Saturdays, Sundays, and public holidays, when the stock markets were not open for trade, were excluded from the data analysis. The amount of news on weekends and public holidays was assigned to the subsequent trading day. This results in n = 92 days for data analysis. Data on the news about BP were extracted from LexisNexis®, with “BP” and “British Petroleum” as search strings. To tap the U.S. news on BP, a financial newspaper, and two quality newspapers were analyzed. We opted for The Wall Street Journal’s abstracts (n = 371 articles), The New York Times (n = 774 articles), and USA Today (n = 257 articles), respectively. As a control we also analyzed U.K. news, with the Financial Times (n = 1,117 articles), the Times (n = 1,053 articles), the Independent (n = 343 articles), and the Sunday Times (n = 346 articles). Thus, the U.K.-based Financial Times paid the highest amount of attention to the British company BP, followed by The New York Times.

BP press releases

We collected BP press releases in the research period from the BP website. Compared with the newspaper coverage, the number of BP press releases appears to be limited at first sight (n = 126 press releases, 53,542 words), but this number still exceeds the number of days in the research period.

Public awareness

Public awareness of the crisis was measured by the number of daily Google searches for BP in the United States via GoogleTrends®. Daily variations in GoogleTrends searches for BP were used to measure daily changes in public awareness of the BP crisis of involved internet users who want to learn more about the crisis. Obviously this behavioral measure excludes citizens who do not use the internet, or do not use the internet to obtain news. Other instruments to tap public awareness, most notably survey studies based on random samples with questions about the salience of the BP crisis, were not available, but would not have resulted in daily measurements.

Modeling Strategy

Vector Autoregression applied to news attention

A Vector Autoregression (VAR) model was estimated in line with the seminal research of Wu, Stevenson, Chen, and Guner (2002) and Tetlock (2007). VAR models enable a test on Granger causality: Cross-lagged causal influences are plausible only if a process cannot be explained from autoregressive forces. The current values of a set of variables is regressed on their previous values, on previous values of the dependent variable (autoregression) and on cross-lagged influences of the other variables, as in Equation 1 with two variables x and y and one time lag only.

It should be noted that a VAR model including BP press releases, the amount of U.S. news, U.K. news, and Google searches, BP trading volume, and the BP share price also generates tests of the absence of reverse relationships (e.g., from U.K. news to U.S. news, from share price to U.S. news, and so on). Preliminary tests guided the precise specification of the VAR model.

General Inquirer to explore second-level agenda-setting

To explore which content attributes underlie specific first-level agenda-setting relationships in the VAR model, we measured for each press release and each news item the attention for relevant actors in the BP oil spill crisis, including the U.S. government and environmental pressure groups by means of Solr/Lucene® search queries, which are available from the authors. To measure the attention for attributes, word counts for the categories of the General Inquirer were used. The General Inquirer (Stone et al., 1966) is a word categorization dictionary similar to Linguistic Inquiry and Word Count (LIWC; Pennebaker, Francis, & Booth, 2001) to analyze political, organizational (Kleinnijenhuis, van den Hooff, Utz, Vermeulen, & Huysman, 2011), and financial discourse (Tetlock, 2007). 1 Categories include a variety of positive and negative categories, active and passive categories, and various policy orientations and power relations. The automated content analysis was accomplished with the Amsterdam Content Analysis Toolkit (AMCAT; Van Atteveldt, 2008).

When the multivariate VAR model showed a significant influence of the BP agenda of X at time t −1 on a dependent variable Y at time t, an exploratory multiple regression analysis was applied with the same dependent variable Y at time t, but as independent variables in addition to the other variables from the VAR-model, also variables that measured the attention given to specific actors and to specific attributes by X at t −1. The latter variables were counts that were based, respectively, on Solr/Lucene queries and General Inquirer categories. To reduce the number of independent variables in the multiple regression equation, only actors and attributes were included that bivariately showed significant cross-lagged positive correlation coefficients with the dependent variable Y.

Results

Data Description

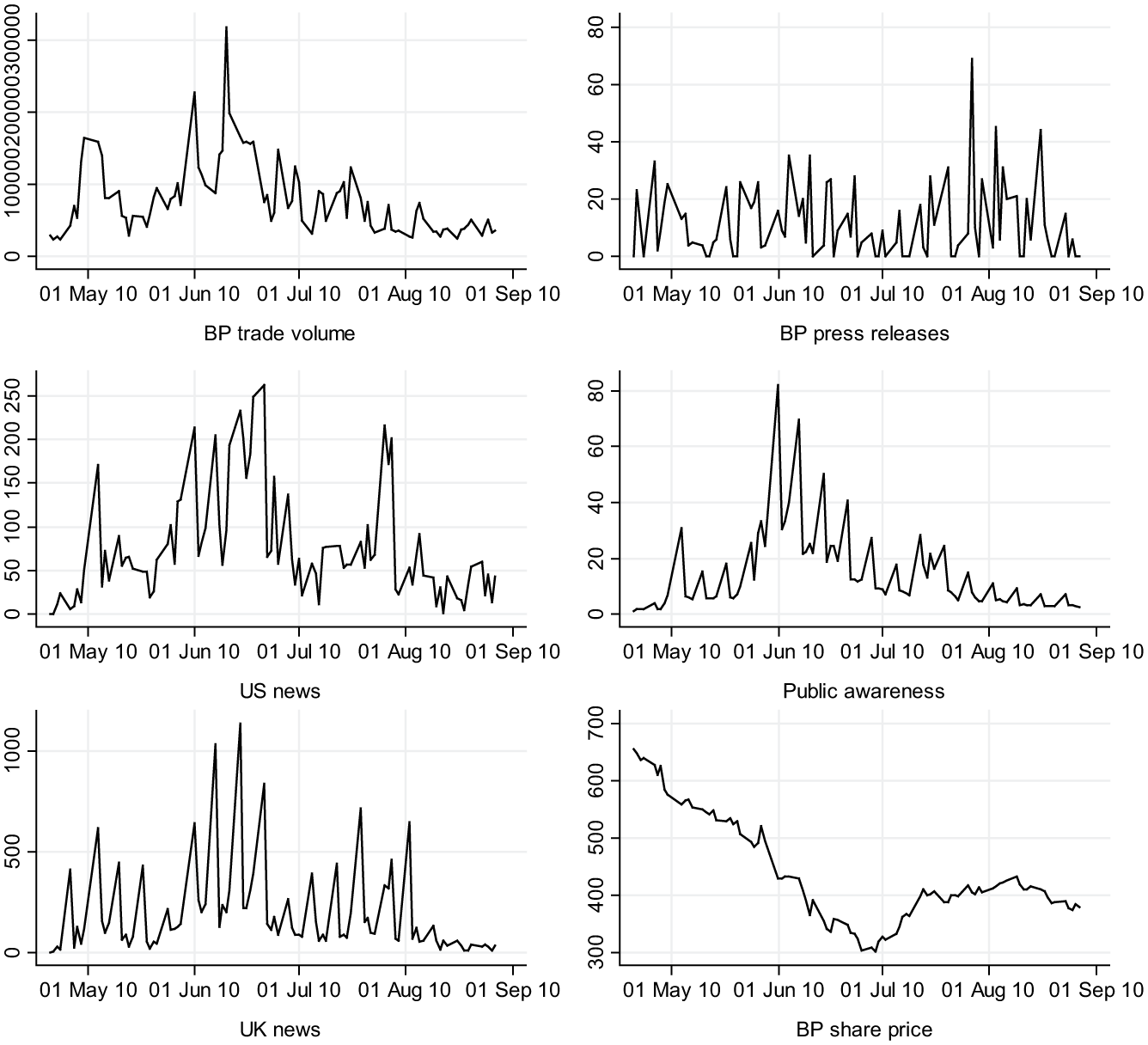

Figure 2 shows the time series for the variables that will be included in the research model. With the exception of the BP press releases, the variables show clear peaks at specific points in time. BP press releases were distributed fairly uniformly over time, but although on average more than one press release was published per day, there were also days without BP press releases and days with exceptional activity, such as June 10. On that day BP responded to earlier falls in the share price as well as announcing the provision to the State of Alabama of an additional $25 million grant for the implementation of the State’s Area Contingency Plan.

Time series for six variables that were included in the research model.

The trade volume reached its highest value on June 14, while attention for BP in the US media peaked on June 21 and again at the end of July. Figure 2 shows that the stock exchange rate of BP halved during the first 2 months of the crisis, from 655 on April 20 down to 303 on June 29, rising to 416 on August 13. In the weeks thereafter, the level of August 13 could not be sustained. Apparently, the general public and the U.K. media lost their interest in the BP crisis somewhat earlier than the U.S. media, since the attention peaks for BP in public attention (June 1) and in U.K. news (June 10) preceded the attention peak in U.S. media (June 21).

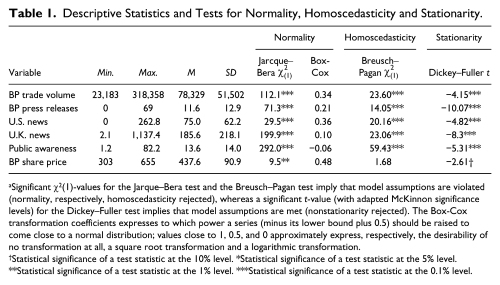

Table 1 presents the minimum, maximum, mean, and standard deviation for each variable to be included in the causal model. The differences in mean values for news variables simply reflect sampling size, which was small in the case of BP press releases, compared with the sample of U.K. news. Due to peak news events during the crisis, the standard deviation exceeds the mean for BP press releases, U.K. news, and public awareness.

Descriptive Statistics and Tests for Normality, Homoscedasticity and Stationarity.

Significant χ2(1)-values for the Jarque–Bera test and the Breusch–Pagan test imply that model assumptions are violated (normality, respectively, homoscedasticity rejected), whereas a significant t-value (with adapted McKinnon significance levels) for the Dickey–Fuller test implies that model assumptions are met (nonstationarity rejected). The Box-Cox transformation coefficients expresses to which power a series (minus its lower bound plus 0.5) should be raised to come close to a normal distribution; values close to 1, 0.5, and 0 approximately express, respectively, the desirability of no transformation at all, a square root transformation and a logarithmic transformation.

Statistical significance of a test statistic at the 10% level. *Statistical significance of a test statistic at the 5% level. **Statistical significance of a test statistic at the 1% level. ***Statistical significance of a test statistic at the 0.1% level.

Preliminary Tests on Stationarity, Homoscedasticity, and Normality

The VAR model assumes independent deviations from its predictions (normal distributed residuals) across different values of the independent variables (homoscedasticity) and across different points in time (stationarity).

Normality tests show that none of the variables exhibits a perfectly normal distribution; cf. Table 1, column labeled Jarque-Bera χ2(1). The column next to it shows that according to the Box-Cox nonlinearity test, different nonlinear transformations should be applied to the variables to render them approximately normal (e.g., roughly a square root transformation to the BP share price [0.48 ≈ ½], but roughly a fifth root transformation to BP press releases [0.21 ≈

Since homoscedasticity was violated for almost all variables according to Breusch–Pagan tests (cf. Table 1), heteroscedasticity robust estimates (HC1 type) will be used.

Stationarity means that a time series reverts back to its mean after a random shock. It took 1 day only for the variables in the VAR model to revert to their mean according to Schwarz’s Bayesian Information Criterion. This means that the link between the past and the current is mediated completely by the state on the previous day, and that the optimal lag length for the VAR model is one lag only. Nonstationarity increases the risk of drawing causal inferences from spurious correlations. Augmented Dickey–Fuller tests showed that the null hypothesis that the series were nonstationary (p < .05) could be rejected, albeit for the BP share price only marginally (p < .10). To minimize the risk of spurious correlations, it is therefore not necessary to use first-level differences of the variables, but we included a linear time index as an independent variable in the VAR model to reduce the risk of spurious correlations due to a similar time trend in the variables.

Antecedents and Effects of News Attention for BP: VAR model

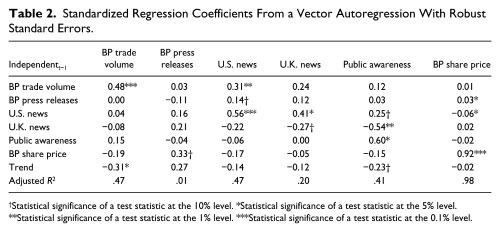

Table 2 shows the reciprocal effect estimates of the VAR with the contemporary values of the variables as dependent variables (in the columns) and the lagged values of the dependent variables as independent variables (in the rows). To interpret the relative size of the regression coefficients, standardized regression coefficients 3 are included in Table 2, as well as t-values based on heteroscedasticity robust estimates of standard errors.

Standardized Regression Coefficients From a Vector Autoregression With Robust Standard Errors.

Statistical significance of a test statistic at the 10% level. *Statistical significance of a test statistic at the 5% level. **Statistical significance of a test statistic at the 1% level. ***Statistical significance of a test statistic at the 0.1% level.

To simplify Table 2 one step further, Figure 3 presents the significant regression coefficients as a path diagram.

A Vector Autoregression model for the BP oil spill crisis.

The path diagram shows at a glance the relationships between the concepts that are also displayed in Table 2. The curved arrows within the same concept reflect the strength of autoregression. Autoregression is high for the BP share price, public awareness, U.S. news, and BP trade volume, insignificant for BP press releases, and negative for U.K. news (suggesting that U.K. newspapers report about BP in attention waves as can be seen from Figure 2). The arrows without an origin that point toward a concept represent the unexplained variance, or the “innovations.” The innovations give a new impetus to the dynamic system. BP press releases, BP trade volume, and U.S. news—which are the three variables that influence public awareness and stock prices directly or indirectly—are all characterized by a high level of innovations (+0.99, +0.73, and +0.73, respectively). Stock prices, which have a reputation of being volatile as compared with other economic indicators, actually exhibit limited volatility as compared with the communication indicators in the model.

With regard to the antecedents of news, Figure 3 shows that U.S. news is not only influenced by previous U.S. news (+0.56), but also by BP trade volume (+0.31) and BP press releases (+0.14), which is in accordance with H1 and H2. This is a first sign that the PR efforts of BP have been successful.

With regard to the effects of news, in line with H3, we see that U.S. news influences public awareness (+0.25), while public awareness did not have a reverse effect on the news. U.K. news follows the U.S. News (+0.41) in accordance with H4. As expected, the relationship between BP press releases and U.K. news is completely mediated by U.S. news.

The BP stock exchange rate depends almost perfectly on its own past (+0.92). In accordance with H5 and H7, respectively, the amount of U.S. news has a small but significantly negative impact on the share price (−0.06), whereas BP Press Releases exerted a small but significantly positive effect (+0.03). Thus, the results of the VAR model clearly violate the efficient market hypothesis (Fama, 1965; Malkiel, 2003), which maintains that apparently trustworthy predictions of share prices, such as predictions on the basis of U.S. News and BP Press Releases, will turn out to be self-denying prophecies.

An unexpected finding is that BP obviously releases its press releases after an improvement of the stock exchange price for BP (+0.33). In combination with the fact that BP press releases exhibited the largest number of innovations, which is to say that they are not predicted very well by any other variable in the model, this may indicate that BP strategically chooses opportune moments to publish its press releases. Recent research in public relations documents that BP reported on its own problem solution strategies (Harlow, Brantley, & Harlow, 2011). BP did its best to become the solution owner rather than merely the problem owner (Schultz, Kleinnijenhuis, Oegema, & Van Atteveldt, 2012).

Another unexpected finding is the rejection of H6, which maintains that public awareness of the BP crisis—as measured by browsing behavior according to Google-Trends to which financial stakeholders have access—affects the share price. The relationship between the two appears to be a spurious correlation as a result of the amount of BP news in U.S. media as their common cause. It should be noted that absent arrows in a VAR path model, unlike in a SEM model, indicate also the absence of reverse relationships. For example, a direct agenda-setting influence of BP press releases on U.K. news is not discernible, nor an effect, reversed or otherwise, of either U.K. news or U.S. news on BP press releases.

Elaboration of the Relation Between U.S. News and BP Share Price

As the VAR model contradicts recent findings of communication scholars that the news usually mirrors rather than molds financial markets (Scheufele et al., 2011), additional evidence will be presented to underpin the effect of U.S. News on the BP share price.

First, we replicated the procedure of Scheufele et al. (2011), who took the residuals from Auto Regressive Integrated Moving Average (ARIMA) models for the news and the share price to obtain white noise as the basis for a cross-lagged correlation comparison. In the case of the BP oil spill crisis, yesterday’s news did predict today’s share price rather than the other way round. 4

The VAR model assumes stationary variables, but the alternative hypothesis of nonstationarity was only marginally rejected for the BP share price (p = .09). Therefore, we also applied a Vector Error Correction (VEC) model that allows for co-integrated nonstationary variables that tend to move together in time. The regression estimates for the VEC model show that changes in the BP share price depend significantly on previous changes in the amount of U.S. news, and on deviations from the equilibrium. The latter entails that a huge amount of BP news amounted to a negative pressure on the BP share price especially when the share price was higher than could have been expected on the basis of the previous amount of BP crisis news. 5 Thus, the VEC model shows a comparable causal effect, albeit a more sophisticated one.

Post Hoc Exploratory Analysis of Second-Level Agenda-Setting

For each significant influence according to the VAR model (cf. Figure 3) of the agenda of X on Y, we will explore which specific attributes and actors in the news supply of X contributed to the influence on Y. The question to be answered is whether the specific frame of mind of U.S. journalists, U.K. journalists, the general public, and financial stakeholders makes them especially susceptible for specific problems, causes, moral evaluations, and treatments in the news supply of X.

The VAR model showed that the number of BP press releases affected the amount of U.S. news. 24 General Inquirer content categories from lagged press releases show bivariately the expected cross-lagged impact on the amount of U.S. news. Three categories stand out in a multivariate regression analysis. U.S. newspapers adopted the BP press releases especially when they explained how BP exerted influence, raised new policies, and how BP furthered well-being. 6 The latter news category in U.S. news also prompted public awareness. Thus, BP solutions for the oil spill made BP press releases newsworthy. This is in line with Huang (2006), who documented that positive media coverage in crises is increased by specific strategies, such as justification in a standard situation, and concession in an agreement situation, in which the corporation was in control of the situation and applied appropriate standards of assessment.

One hundred thirty-one content categories from lagged U.S. news show bivariately a cross-lagged impact on the amount of U.K. news. One category stands out in a multivariate test: British newspapers adopt especially U.S. news if the U.S. news deals with the morality to hold up virtues and principles. 7

The VAR model showed that the BP share price is affected positively by BP press releases, but negatively by the amount of U.S. news. Lagged BP press releases with skill-related words stating that goals have been achieved especially supported the BP share price. 8 Thus, BP press releases showing BP’s skills in offering solutions were helpful, while lagged press releases with attention for the mental process of problem-solving did not have this effect. One hundred fifty-five categories in the lagged U.S. news showed bivariately the expected negative cross-lagged impact on the BP share price. In a multivariate context, the foremost devastating news appears to be that BP got trapped in a political power game (politics, claims, demands, leadership, recommendations, etc.). 9 Thus, BP was hurt by news about the political turmoil.

We tested whether attention for specific actors and specific issues as measured by Solr/Lucene search queries improved the explanations. The explanatory power was improved only in a few exceptional cases. Public awareness depended also on the involvement of Obama in the BP crisis according to U.S. news. Share prices also reacted negatively to news about judicial claims against BP, which suggests that responsibility for the oil spill problem played a major role.

All in all the outcomes of these exploratory post hoc analyses support the interpretative expectation that influential news deals with problem definitions, causal interpretations, moral evaluations, and problem treatment recommendations. Apparently, financial stakeholders, U.S. newspapers, U.K. newspapers, and the general public reacted partly on the basis of their specific frame of mind. BP influenced the U.S. news with its solutions, and the financial stakeholders with news about its skills in implementing solutions. U.S. news exerted an influence on U.K. news due to moral issues, an influence on public awareness by showing Obama’s involvement, and an influence on shareholders with news about political turmoil and judicial claims against BP. Both BP in its press releases and the U.S. media in their news coverage paid attention to a broad variety of attributes and actors, that enabled first-level agenda-setting effects of news about BP, in spite of partly differential effects of specific news attributes on U.S. media, U.K. media, the general public, and financial stakeholders.

Discussion

We tested a model that documented the mediating role of U.S. news in the BP oil spill crisis by assessing its antecedents and its consequences. Classic, intermedia, and stakeholder agenda-setting, as well as public relations efforts and financial performance that were hitherto studied in isolation, were able to be included in a single study. To assess causality, a VAR model was applied to time series data. This enables a strong test of reciprocal causality compared with cross-sectional studies, which are poor in assessing causality, and experimental studies, which enable very strong tests of unidirectional causality, but tend to ignore reciprocal causality.

The daily amount of U.S. news about BP followed public relations (BP press releases) and financial indicators (the trade volume of BP shares), whereas the news amounted to classic agenda-setting effects on public awareness, intermedia agenda-setting effects on foreign news, and stakeholder agenda-setting effects on the BP stock rate. Post hoc analyses suggested that influence in the BP publicity was exerted by BP press releases that proposed new skillful solutions, and by U.S. news about the political turmoil, judicial claims, and moral virtues that characterized the BP oil spill crisis.

The current study confirms earlier research findings on financial journalism. Even during a crisis, business news depends heavily on indicators of business performance (Castelló, 2010). The public relations efforts of BP succeeded in getting across the message that BP was the issue owner that would offer skillful solutions that could stop the oil spill, although the variety of different solutions to stop the oil spill offered by BP may have seemed clumsy at first sight (Schultz et al., 2012). The data revealed the tendency of BP to speak when success was already imminent, in line with the finding from advertising research that it is impossible to overrule negative publicity through advertisements (Meijer & Kleinnijenhuis, 2007) and with the SCCT theory in public relations (Coombs, 2007) that accommodative strategies pay off.

A unidirectional intermedia agenda-setting effect of U.S. news on U.K. news was observed. U.S. news also results in a classic agenda-setting effect on public awareness as measured by Google searches. In contrast to earlier studies, which found that the news did not mold the financial markets but rather mirrored them (Scheufele et al., 2011), we showed that during an organizational crisis stakeholder agenda-setting occurs, since the sheer amount of news had a negative effect on the share price. This study also documents that press releases had a positive direct effect on the share price. Earlier research concentrated on effects that were mediated by the news (Kiousis et al., 2007).

This study shows that agenda-setting effects partly depend on the resonance of specific second-level news attributes (McCombs, 2004) with the frame of mind of specific audiences (D. A. Scheufele & Iyengar, forthcoming). Financial stakeholders, for example, reacted negatively to US news about political turmoil and judicial claims against BP, but positively to BP press releases discussing the skills of BP in implementing a solution for the oil spill. Due to the broad attribute agenda of BP and the U.S. media, they were both able to exert a first-level agenda-setting influence on others in spite of divergent frames of mind of financial stakeholders, foreign media, and the U.S. public.

The research results are relevant for public relations officers as they indeed can maintain legitimacy in crises by strategically communicating corporate crisis solutions (Patriotta et al., 2011). The research results also show the importance of watchdog journalism in the public interest. Whereas the BP press releases listed the skillful employment of “dispersants” to protect the environment without naming negative side effects, the press at least disclosed that the toxic dispersant Corexit was used by BP. But the press moved its attention away from BP almost completely shortly after BP imposed its final solution to the problem as defined by BP, that is to seal the oil well.

Comparative crisis research is called for to see whether the findings about the BP crisis also apply in crises with other responsibility attributions and other organizational responses (Huang, 2006). Agenda-setting effects can be observed for Western countries, but evidence for non-Western countries, such as China, is still sparse (Zhang, Shao, & Bowman, 2012). Research is also needed to test whether comparable agenda-setting mechanisms occur in newsworthy organizational processes such as mergers and takeovers about which the tone of the news is not as negative as about organizational crises.

Footnotes

Acknowledgements

The authors are grateful to Wouter van Atteveldt for his support and to the anonymous reviewers of Communication Research for their valuable comments on an earlier version.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.