Abstract

In the final 15 years of the Punto Fijo era (1958–1998), as state institutions and socioeconomic conditions deteriorated, the executive class of Petróleos de Venezuela S.A. broke free from state control. In his 15 years as president of Venezuela, Hugo Chávez reasserted the state’s control over the company and reestablished a fiscal regime that brought the country enormous financial benefits. It is a legacy, however, that has an uncertain future.

En los últimos 15 años de la era del Punto Fijo (1958–1998), mientras las instituciones estatales y las condiciones socioeconómicas se deterioraban, los ejecutivos de Petróleos de Venezuela S.A. se independizaron del control estatal. Durante sus 15 años como presidente de Venezuela, Hugo Chávez reafirmó el control del estado sobre esta compañía y reestableció un régimen fiscal que le rindió grandes beneficios económicos al país. Se trata, sin embargo, de un legado que tiene un futuro incierto.

Detractors and admirers of Hugo Chávez coincide in seeing the battle to control Petróleos de Venezuela S.A. (PDVSA), the state oil company, as crucial to the Bolivarian project. Too often this is seen simply as a battle to control the company’s profits and assets rather than as a fundamental struggle between capital and landed property over the terms of access to the subsoil. This article illuminates this struggle by setting it within the classical theory of ground rent.

Against unremittingly hostile and disloyal opposition from the executives of PDVSA, the Chávez administration took the diplomatic lead in the reinvigoration of the Organization of Petroleum Exporting Countries (OPEC), reformed fiscal policies to ensure full capture of extraordinary profits (rents), reasserted majority control over joint ventures, and introduced other measures to reassert national sovereignty over the natural resources of the subsoil. However, as with several other aspects of the Chávez legacy, these accomplishments were insufficiently institutionalized. They are also in jeopardy today because insufficient attention was paid to maintaining and developing the productive capacity of PDVSA, increasing the country’s dependence on debt and foreign investment in recent years.

The first part of this study reviews the concept of international ground rent before applying it to the Venezuelan case. I first examine the growing capacity of the Venezuelan state to appropriate international ground rent in the concessions era, from the early 1900s until 1976, as it developed consciousness and administrative ability to deal with foreign oil companies. Next I show how nationalization contributed to the decline of this consciousness and ability, paving the way for the implementation of the neoliberal apertura petrolera (oil opening) of the late 1980s and the 1990s. This historical context provides the basis for an examination of policy in the Chávez era, which saw the return of natural resource nationalism in the form of restoring sovereignty and control over access to the subsoil, accomplishments that restored the state’s capacity to appropriate international ground rent. Finally, I consider contemporary debates within the left about extractivism and development and threats to the Chávez legacy in oil policy.

Appropriation of Ground Rent, Development, And Capital Accumulation

“Ground rent” (Marx, 1959: 614–813; Ricardo, 1817) in the international system refers to the portion of earnings from primary commodity exports that exceeds production costs plus the average rate of profit for transnational capital. In the capitalist world system, for Third World states heavily dependent upon the export of primary commodities the claim of sovereign ownership over natural resources constitutes the assertion of the nation’s right to appropriate extraordinary profits (ground rent). These states are “landlord states” in the sense that, much like landowners in a single nation-state, they use the principle of territorial sovereignty to assert a collective property “right” to appropriate extraordinary profits and demand compensation for access to the “wealth” 1 of the subsoil.

Within a system of simple production for exchange, differential ground rents are the result of varying levels of natural productivity. The most marginal lands put into production in a simple system of commodity exchange are those for which the cost of production permits realization of an average rate of profit under the most adverse natural conditions. Production on more naturally advantageous lands yields an extraordinary profit. This is but one source of rent. Absolute rent arises when landed property demands a rent even on the least naturally productive lands to satisfy demand and generate an average rate of profit (Marx, 1959: 748–772). Absolute rent is a barrier to investment, drives up the cost of reproduction of labor, and increases the cost of inputs into the industrial process. When landlords cooperate not only to appropriate a larger share of differential rent but also to increase rents by limiting access to the land, the antagonism between landed property and capitalism is heightened. We can see this antagonism in the recurring tensions between transnational capital and the OPEC “cartel” when the latter seeks to regulate supply.

Bernard Mommer (1990: 418), who served (starting January 2005) as a vice minister for oil and greatly influenced oil reform legislation in the Chávez years, characterizes the country’s economy as “rent capitalism”:

In normal capitalist conditions, production and distribution make up one single process of cooperation and confrontation between labor and capital, as well as land, in the case of primary production. However, land has historically reduced its participation in national income to a minimum, a trend that has been furthered by state intervention through legislation. In rent capitalism, on the contrary, the state appears as the national landlord who seeks to maximize ground rent of a natural resource which is subject to an international exploitation, thereby fostering concomitantly the national development of capitalism. Thus, an income appears which is completely external to the national production process and which, entering the national budget, is distributed by a process parallel and without relation to the distribution of true national income.

From capital’s vantage point, landed property has undertaken neither the risk nor the investment necessary to generate production from the land. 2 It is not difficult to discern this attitude in the view of transnational oil companies in the consuming capitalist states or in that of First World consumers who stereotype the rulers of oil-rich states as greedy tyrants. It may be surprising to find it in the attitude of the so-called meritocracy, the Venezuelan executives who directed PDVSA, but that is just how they viewed the late–Punto Fijo political class.

Ground rent has not figured as prominently as one might expect in the political economic literature on Venezuela. In his modern classic The Magical State, Fernando Coronil (1997: 57) observed that most Marxists “have devoted themselves to solving the mystery of capital/labor relations, [so] it is no surprise that the mystery of Madame la Terre still remains to be deciphered. Few thinkers have noted that Marx’s binary system clashes with his ‘trinity formula.’” Nonetheless, Coronil devotes more attention to the deployment of rents than to the way they are conjured up—a very material process that Marx himself elaborates in Volume 3 of Capital, though mostly with regard to agriculture within national circuits of capital accumulation.

Analysis of the neoliberal impact on Venezuelan politics during the decline of the Punto Fijo regime (1958–1998) tends to focus more on fiscal austerity and the privatization of heavy industries than on the neoliberal opening and the return of foreign capital to the oil sector, and much of the orthodox view of oil policies is that they were not generous enough to extractive industries. This view is well represented by Osmel Manzano (2014), who has argued that the changes introduced between 1986 and 1998 failed to provide stability for foreign investors and to make the country competitive with other oil-producing countries. This type of critique implies an even more unfavorable view of the changes introduced in the Chávez years, when the terms of the opening were significantly modified to the benefit of the state. By contrast, I will show that the changes in the fiscal regime left plenty of opportunity for foreign investment to profit. Combined with the spectacular increase of Venezuelan reserves and of global demand, the policies made sense.

From The Concessions Era To Nationalization

Chávez’s legacy in oil policy is the reassertion of sovereign control over the terms of access to the subsoil. I say “reassertion” because his policies were a return to the nationalist policies that matured toward the end of the concessions era. This era began with the Juan Vicente Gómez dictatorship (1908–1935) and culminated in the nationalization of the oil companies in 1976. This section briefly reviews this historical process so that we can better put the opening and Chávez’s anti-opening reforms in context.

From the earliest era, some important representatives of the Venezuelan bourgeoisie questioned the fiscal terms of the early concessions granted to oil companies. Gómez’s minister for development, Gumersindo Torres, and the country’s most important banker, Vicente Lecuna, took note that in the United States it was customary for landowners to collect a royalty of 12 to 16 percent for drilling (Mommer, 1988: 61–84). This gave impetus in 1922 to a reform of hydrocarbon law. Although the terms were very generous, no longer would oil be treated simply as a free gift of nature to capital. Six years later Torres would argue that “the nation, as a participant in the product extracted, is intimately interested; even more so as the owner of the mineral before its extraction” (quoted in Mommer, 1988: 74–75).

Regardless of the character of the political regime, the period between 1922 and 1975 saw steady advances in Venezuela’s capacity to capture rents. The most important occurred in 1943, when President (General) Isías Medina Angarita, taking advantage of the favorable context (World War II and the Mexican nationalization of the oil industry in 1938), passed an oil law with a reformed fiscal regime under which the country’s share of profits reached 60 percent in 1945 (the last war year). The reform established a royalty of 18.5 percent as a floor, superseding lower rates from the Gómez era, and required bidding for subsequent concessions. Some brought a royalty as high as one-third the value of production (Comisión Ideológica de Ruptura, 1977: 111–161; Mommer, 1988: 61–96). Just as important, the foreign companies were forced to recognize the distinction between royalty (a contractually fixed payment) and taxation (a sovereign power of the landowner state, subject to change by law and therefore a tool for appropriating rents when price changes lowered the state’s share). 3

Indeed, after the war prices fell, and so did Venezuela’s share of profits. A military coup had ousted Medina and brought Rómulo Betancourt and his Acción Democrática (Democratic Action—AD) to power for three years (1945–1948, known as the trienio), and it fell to the new government to respond to the decline. Betancourt had made a reputation as a nationalist in the 1930s, and his rhetoric about imperialismo petrolero could be incendiary at times. By this time, however, his views had moderated; he had even developed a friendship with Nelson Rockefeller, whose father had founded Standard Oil, the most important of the three major foreign companies. Betancourt and AD negotiated an agreement with Standard and the other companies by which they would split profits 50/50 with the understanding (not contractual) that the government would not raise taxes without prior consultation. The agreement came to light in 1959, when the interim government between the fall of the Pérez Jiménez dictatorship (which had come to power after a coup in 1948 ousted AD and Betancourt) raised taxes over the protests of the oil companies, which complained that the 50/50 understanding had been violated.

During the Medina years and the trienio, Salvador de la Plaza, a maverick communist, articulated a nationalist position on oil that would influence the architects of Chávez’s oil policies in the 2000s. De la Plaza (1996, Vol. 1: 43–52) harshly criticized the 50/50 agreement, which he considered not a nationalist triumph but a retreat from Medina’s achievement of sovereignty on matters of taxation. He argued as well that royalty payments should be counted toward the company’s share. He differentiated them from taxes, considering them compensation for “capital extracted from the subsoil, belonging to the nation” (1996: 135). Royalty payments take on added importance because they are easy to calculate and collect. Appropriation of rents through taxation rather than royalty payments poses other problems. Establishing a royalty has other advantages for the landlord state. It requires little more than monitoring the flow of resources at the wellhead, in transport, or at the port of embarkation. The quantity produced can then be multiplied by the world price to establish the basis on which the royalty is levied. Auditing and collecting from foreign investors are more complex tasks, especially for a state lacking an effective bureaucracy and specialized knowledge of an industry (Mommer, 1988: 168-169).

By 1959, when Betancourt and AD returned to office (though with some power sharing), the circumstances had changed. Middle Eastern producers, led by Saudi Arabia, were threatening Venezuela’s principal export market, the United States. In 1960, after failing to get Washington’s consent to a new trade treaty guaranteeing access to the U.S. market, Betancourt sent Venezuela’s oil minister, Juan Pérez Alfonzo, to the Middle East, and there he won the support of his counterpart in Saudi Arabia in founding OPEC.

OPEC is a cartel not of producing nations but of landlord states. These states used territorial sovereignty to collect royalties and taxes based on a price that they gave rather than took. OPEC nations sought not only to appropriate the extraordinary profits arising from the natural advantages inherent in their geology (differential rents) but also to defend prices by limiting production (absolute rent). Although global markets certainly limit the reach of OPEC’s power, the new regime that it created should be seen as a new stage of an old reality—that the price of oil is higher than that of most other commodities whose prices are set by political arrangements. Until OPEC, seven major transnational oil companies, the famed “Seven Sisters,” controlled production and prices in the middle decades of the twentieth century. In the late 1960s and early 1970s, its success was becoming visible as member countries began to impose reference prices for purposes of taxation, whether or not these prices corresponded to market rates or discounts offered by companies to buyers. When the Arab members implemented a boycott of Western nations for their support of Israel during the October 1973 War (Venezuela maintained production and exports), the full potential of the landlord states for cooperating in limiting supply became evident.

Having lost control over crucial decisions on production levels and pricing, the oil majors embraced rather than resisted nationalization in Venezuela in the 1970s—at least for the time being. They also had incentive because the large concessions they had obtained or renewed during the Medina administration were due to expire in 1983. The companies would have to make new investments to maintain the flow from fields past their peak natural productivity, and the closer they were to the end of the lease the less willing they were to recapitalize. After the 1973 presidential election, the three major foreign companies approached outgoing president Rafael Caldera about initiating talks on nationalization. Caldera’s successor, Carlos Andres Pérez, followed through with the nationalization law of 1975, and in 1976 PDVSA was created as a holding company with three major subsidiaries corresponding to the three major foreign companies (Standard, Shell, and Gulf). Venezuelans already occupied the top executive positions in these subsidiaries, each of which would mainly market production to its former owner.

Mesmerized by nationalization, Venezuela’s political class abandoned plans to develop the productive capacity of a fledgling state-owned company, the Corporación Venezolana Petróleo (Venezuela Petroleum Corporation—CVP). The original idea was that the CVP would participate in the exploitation of the concessions due to expire in 1983, giving the country a window on the global industry and the prospect of developing its own productive capacity. Suddenly the question of what constituted a “just” share of profits between capital and the landlord state seemed moot. Nationalization took place at a moment of highly favorable international political and economic conditions; the influx of rents in the boom years of 1973 to 1983 was misunderstood as a company success, not a success of the state’s oil policy.

PDVSA’s “success” masked the failure of the state to adjust to changing global market conditions, just as the rent-fueled surge in consumption masked the mismanagement of the disposition of appropriated rents. These twin failures lay behind the economic crash that began after the devaluation of February 1983. Only months before, President Luis Herrera Campíns had forced PDVSA to repatriate its overseas reserves of US$5.5 billion. By the time the devaluation had run its course, he might have simply burned it all in a bonfire. PDVSA’s executives were never enthusiastic about nationalization—after all, they had built their careers by climbing the managerial ladders of subsidiaries of the three major foreign companies, now controlled by the state holding company. Now they had extra incentive and a favorable political environment to break away from state control.

The Neoliberal Opening of the Venezuelan Subsoil to Foreign Capital

The collapse of oil prices in 1986 helped move the balance of power toward the company and away from the parties, Congress, and the oil ministry. Low prices had resuscitated global demand. OPEC sought to support price levels through quotas, but already by 1985 PDVSA was increasing production. In 1985 production was 1.68 million barrels per day; by 1997 it had reached 3.28 million barrels per day. Meanwhile, the profligate spending, corruption, and moral failures of the Jaime Lusinchi era (1984–1988) eroded the image of partidocracia and the capacity of oil nationalists within AD and other parties to resist company initiatives. The government seemed in control of policy, but the oil ministry increasingly found itself acting ex post facto in matters of pricing, which fell increasingly to the companies, guided by professional managers ostensibly standing above the unsightly political debacle.

PDVSA’s first efforts to break away from state control took the form of “internationalization,” which began with the purchase of a 50 percent stake in the German company Veba Oil in 1983. The AD administration of Jaime Lusinchi temporarily brought purchases to a halt, but in 1986, in the midst of a deepening economic crisis and scandals that severely tarnished Lusinchi, PDVSA was able to buy a controlling interest in the North American refining and distribution company Citgo. In 1989 it acquired the rest of the shares.

PDVSA could not change the rules of the game all at once, but it stealthily and steadily gained space for the opening. Despite his reputation for embracing neoliberal fiscal policies, President Carlos Andrés Pérez (in his second term, 1989–1993) was hesitant to embrace PDVSA’s plans to bring foreign investment back into upstream operations. The Caracazo of 1989 severely wounded Pérez’s ability to confront the companies, which made steady headway promoting their policies to Congress. Thus the rebellion against a neoliberal structural adjustment program effectively aided the neoliberal offensive in the sector that counted most—oil—as nervous political leaders of AD and COPEI (the Social Christian Party) desperately looked to the oil company’s plan as the only way to put the country back on track.

In this political environment, PDVSA executives began to dismantle obstacles to implementing the opening, beginning with certain provisions in the 1975 nationalization law. Article 5 of the law provided two ways (envisioned as primarily relevant to foreign companies) for private capital to participate in oil production: operating agreements that “in no case affect the essential conduct of activities attributed” to the state company and joint ventures, allowable “in special cases” with permission of Congress and guarantees of state control. Critics of Article 5 always feared that it would be the “nose of the camel” for the return of foreign capital; they never fully appreciated how stealthily the animal would enter the tent. The company began with service contracts that were ostensibly for extending the lives of older fields but as structured virtually amounted to concessions, spilling into the “essential activities” reserved to the state. 4 Neither in the media nor in Congress was there much serious debate about oil policy. Pro-opening commentary dominated the media (López, Canino, and Vessuri, 2006). After all, the issue seemed to be managerial and technological, and PDVSA was still state-owned, was it not? The daily headlines were dominated by corruption scandals, stories on oil policy being mostly buried in the economic sections of the prestige press.

Next PDVSA executives moved to create legal and fiscal structures to permit joint ventures with transnational oil companies. The key legal obstacles were in the oil reform of 1967. This reform had actually anticipated the possibility of joint ventures involving the CVP and private capital after the reversion of concessions in 1983. It had specified, however, that such ventures could be undertaken only where the terms of contracts for them complied with the requirements of the 1943 law, which included the resolution of disputes in national courts (known in international law as the Calvo clause), restriction of agreements to 30 years, and the possibility that as many as 80 percent of the lots conceded might revert to national control. The nationalization law said nothing about invalidating the earlier laws. The meritocracy’s solution was to obtain a Supreme Court judgment doing just that.

The vehicle was a Supreme Court case brought by the company in 1990 seeking court approval of a joint venture to develop the Cristóbal Cólon Project for producing liquid gas. An obscure case dealing with gas, not oil, it was well suited to PDVSA’s purposes. Going far beyond the boundaries of the specific project (which never went forward), the court declared all provisions of the 1967 law superseded by the nationalization law’s Article 5. Writing for the court was Ramón Duque Corredor, a former lawyer for the oil companies who left the court only four months later and who had declared in his doctoral thesis of 1978 that the entire 1943 law was superseded by the nationalization law. His view required ignoring that the nationalization law itself expressly provided for derogation only of aspects of earlier legislation inconsistent with it (Duque, 1978: 9, cited in Mommer, 1998: 14; Vallenilla, 1998). The nose of the privatization camel was now deep inside the government’s tent.

The executives encountered some resistance to part of their plan when Pérez appointed an outsider, Andrés Sosa Pietri, president of the company. Sosa took an intermediary position on the company’s opening plans. On the one hand, he aligned himself with company executives on forming joint ventures to develop liquid gas projects and extra-heavy crudes, both requiring massive new investments and technologies that were new for the company. In his mind, these were “strategic projects” for expansion of the industry. They would require fiscal adjustments to account for investment costs and risks. He also promoted Venezuela’s leaving OPEC and instead joining the International Energy Agency, whose origins lay in the organized response of consumer countries to OPEC (see Sosa, 1993). On the other hand, Sosa resisted the meritocracy’s plan to enter into operating agreements for production in marginal fields. More than mere “service contracts,” these agreements turned over extraction wholesale to foreign companies. He was concerned that the plans of the PDVSA career executives would turn the company into “a small, weak corporation, a government agency that really carried out the responsibilities of the [oil ministry]” (1993: 149). The company would not be producing in cooperation with foreign investors but merely collecting a portion of their earnings. Sosa maintained that the company had adequate resources to develop these fields itself. The political class, however, was desperate for foreign exchange to pay Venezuelan’s international debt. Indeed, the oil ministry was in agreement with PDVSA. Sosa and Celestino Armas, the oil minister, were no longer on speaking terms (Oil and Gas Journal, August 26, 1991). Congress allowed the operating agreements to go forward.

PDVSA’s increased production coincided fortuitously, from the executive’s perspective, with favorable market conditions, especially the plunge in Iraq’s exports from 2.5 barrels per day to almost nothing as a consequence of the Gulf War of 1990–1991. PDVSA was producing for the first time in years at full capacity, exceeding OPEC quotas routinely. In 1992 the opening gained additional momentum with operating contracts whereby foreign companies would reactivate dormant and marginal fields and with agreements for the first joint ventures in extraction and processing of heavy crudes and liquefied natural gas. These ventures were encouraged, if not made necessary, by pressure from the International Monetary Fund, which insisted that any money borrowed by the company to undertake such projects on its own would be counted as part of the public sector debt that Venezuela was obligated to reduce (Mommer, 1994: 21–23). In 1993, with Pérez conveniently out of the way after Congress forced his resignation, a weak interim government did away with the ministry’s authority and phased out reference prices, an important tool by which the landlord state could adjust taxation and royalties to adjust to market circumstances. In 1993 additional joint ventures were signed for projects involving heavy crudes and liquefied natural gas. These proposals needed approval by Congress. The legislature agreed to lower royalties and changes in taxation favorable to joint ventures—but only for the foreign partner. The state would tax its own enterprise at more than twice the rate applied to foreign producers. The legislation put the company at a competitive disadvantage for carrying out basic functions within the state’s own national boundaries.

The return of Rafael Caldera to the presidency in 1994 seemed briefly to check neoliberalism’s advance into the Venezuelan subsoil, but almost immediately a banking crisis that absorbed government expenditures equivalent to 10 percent of the gross domestic product (GDP) induced him to retreat. The patriarch became convinced by Luis Giusti, a prominent PDVSA executive, that the opening would bring needed capital and technology and that opponents of this policy were simply irrational nationalists. Caldera appointed Giusti as the new president of PDVSA. Giusti’s career had begun in the Shell subsidiary, and he was emblematic of the petroleum executives who had never fully embraced nationalization. He and other products of the old foreign subsidiaries, who became known as the “Generation of Shell” (Arrioja, 1998), would lead the revolt against Chávez’s attempt to recover control over oil policy between 2001 and 2004.

In late 1994 Caldera asked Congress to approve model contracts, as required by Article 5, permitting so-called joint ventures in the heart of the oil industry: exploration and production of light and medium-grade crudes. In assessing these model contracts, it is worth keeping in mind that the Venezuelan state oil company was technologically equipped to undertake exploration and production of new fields on its own and that, in contrast to its Mexican counterpart, PEMEX, it had an international reputation for sound management. At the time Patrick Crow (1994: 34) wrote in the Oil and Gas Journal, “PDVSA has always been one of the best managed state oil companies in the world, capable of finding oil without foreign help.”

Mommer (1995), then an adviser to the congressional committee with jurisdiction over the proposed legislation and after 2005 an architect of Chávez’s policies, pointed out that the terms of the new ventures were less favorable than those found in petroleum laws predating the nationalization of the industry in 1976. The opening required no payments for rights to explore territories, nor did it require the return of explored but unexploited lands to the nation as national reserves—provisions upon which Venezuelan governments had insisted since the very first law on hydrocarbons of 1920 and that the current agreements appear to violate. Reversion would have facilitated the growth of the two (of three) major subsidiaries of PDVSA that already were critically short of proven reserves. The exploration contracts granted foreign companies access to 17,600 square kilometers and were on average 10 times larger than those granted in 1971. No lots would revert to the state for longer-term reserves, production by PDVSA, or sales to other potential producers.

The opening did attract some opposition from nationalists in the major parties, especially AD, still the largest party in Congress. President Caldera controlled only one of five factions in a divided Congress, but Giusti got most of what he wanted through an alliance with the secretary general of AD, Álfaro Ucero, who kept the oil nationalists in his party under control. Speculation arose that Giusti would be AD’s presidential candidate in 1998 (Arrioja, 1998: 211–224).

The model contract legislation approved in 1995 practically ensured that Venezuelan capital would enter joint ventures only on subaltern terms, sharing profits but having little control over management and production. The royalty was ostensibly fixed at 16.67 percent, but in the case of extra-heavy crude it could be reduced to 1 percent. A form of excess profits tax called the participación del estado en las ganancias (state participation in profits—PEG) would be levied but would apply only after costs had been deducted. Furthermore, it was designed to be flexible but only downwardly. After royalty and PEG, joint ventures would be taxed at the corporate rate for other than hydrocarbons, then 30 percent. Costs are higher (and therefore profit margins lower) for extraction and upgrading of extra-heavy oil. However, it is notable that foreign companies formed these joint ventures with PDVSA at a time when the export price for such crudes was less than US$9 a barrel. Neither side anticipated that prices would surge to well past US$50 by the middle of the decade and then beyond. Inevitably there would be a struggle between them to retain the extraordinary surplus, all rents, thereby generated (see Boué, 2014).

The model contract provided only that PDVSA had the option to buy a 35 percent (or less) stake in the new enterprise, an apparent violation of Article 5’s clear requirement of “control” by the state in any such ventures. This obstacle was overcome through the device of preferred shares, by which PDVSA’s affiliates were granted 50 percent plus one of voting rights not over management of the enterprise but only over a committee with the authority to review management decisions made by the joint venture. Jurisdiction over disputes would be through international arbitration, not the Venezuelan courts.

Was the opening merely a prologue to the privatization of PDVSA? Giusti once proposed that PDVSA sell shares of the company and may have had privatization as his ultimate goal (see Márquez, 1996). However, for foreign investors there were advantages in maintaining PDVSA as a state-owned holding company. Contracts for operating agreements, profit-sharing agreements, and services typically contained clauses that (1) made the company liable for any changes in terms subsequently introduced by the government and (2) provided for contractual disputes to be resolved in international arbitration tribunals. PDVSA assets abroad could be subject to seizure in disputes, which Exxon-Mobil and Conoco-Phillips have attempted to do as part of their resistance to Chávez’s “renationalization” of joint ventures and operational contracts.

For more than a decade PDVSA executives worked systematically to tear down the legal and bureaucratic structures that Venezuelan governments had built up over 50 years of dealing with foreign oil companies. The demolition was abetted by the fact that most Venezuelans had come to share the view that their native political class had mismanaged the oil sector and thrown more than half of them into poverty. PDVSA executives had successfully presented themselves as an island of efficiency and success, a “meritocracy,” in a system wracked by major corruption scandals. PDVSA was gradually relinquishing its role in the exploration, production, and marketing of oil. The opening was on course to link Venezuela’s future to the interests of consuming nations and away from those of other landlord states. Then came Chávez.

The Chávez Factor

The immediate issue that crystallized Hugo Chávez’s successful election campaign of 1998 was his call for a constituent assembly to write a new constitution, but oil policy contributed significantly to his victory. Throughout the opening years, the meritocracy had said that oil prices would turn up. In 1998, however, PDVSA executives suffered an erosion of their standing when oil prices plummeted in the wake of a global economic crisis (the “Asian Contagion”); the basket price for Venezuelan oil plunged by fully one-third. The government had anticipated revenue and budgeted for 1998 based on a basket price of US$15.50; by the end of the year it had lowered its expectations to US$11.50.

Chávez, however, maintained his priority of rewriting the constitution; he was suspicious of the meritocracy but did not launch a frontal assault on the opening. Still, his nationalist attitude toward oil became clear in his decision to launch a diplomatic offensive to strengthen OPEC. In September 2000 he hosted in Caracas what was only the second summit of OPEC heads of state in that organization’s history. The speeches and final declaration by leaders of the 11 member countries made reference to the “unequal terms of trade” and spoke nobly of the need to address poverty and global inequality. More important, the conference proved to be a resounding success in restoring cooperation among landlord states to limit production in defense of prices (OPEC, n.d.: 19–22).

The OPEC summit threatened PDVSA’s emphasis on production, but it did not threaten foreign participation in oil production. Neither did the 1999 Bolivarian Constitution. That may seem surprising given that Article 302 states, “The State reserves to itself, through the pertinent organic law, and for reasons of national expediency, the petroleum industry.” The very next article (303) says, “For reasons of economic and political sovereignty and national strategy, the State shall retain all shares of Petróleos de Venezuela, S.A. or the organ created to manage the petroleum industry,” but it continues, “ with the exception of subsidiaries, strategic joint ventures, business enterprises, and any other venture established or coming in the future to be established as a consequence of the carrying on of the business of Petróleos de Venezuela, S.A.” (my italics).

The meritocracy remained powerful within the company, but the new minister of oil was no friend of PDVSA executives. Alí Rodríguez Araque, a former guerrilla, had been a member of the small circle of intellectuals at the Universidad de los Andes who had been influenced by the ideas of de la Plaza. This group had significant influence within the ranks of Causa R, whose candidate, Andrés Velásquez, ran a strong race for president in 1993 on a platform that called for measures to strengthen the company’s productive capacity. When Causa R divided, Rodríguez aligned himself with the faction that became the Patria para Todos (Fatherland for Everyone—PPT). As part of the Polo Patriótico (Patriotic Pole) alliance behind the election of Chávez, several of the party’s members and friends, including Rodríguez, took up important positions in the government.

As a congressional deputy and president of the Commission on Energy and Mines during the Caldera years, Rodríguez had been a thorn in the side of Giusti. The commission could not stop the opening, but it put the company’s plans under public scrutiny. As minister, Rodríguez found himself facing a fait accompli. He promised to respect all existing agreements but to seek a revision of the opening. Rather than simply recreate a state monopoly, he proposed to widen opportunities for domestic capitalists to compete with foreign capital for contracts and partnerships with PDVSA (Mommer, 1995; Rodríguez, 1997). The idea was stillborn. Leftist Chavistas were suspicious of anything that smacked of support for domestic capitalism. The meritocracy had little interest in sharing extraction with domestic capital; it always envisioned the “opening” as to the outside, not the inside.

Chávez’s Movimiento Quinta República (Fifth Republic Movement—MVR) regarded the opening as a “contemporary chapter in a policy of concentration of wealth, concentration of power, and concentration of population” (MVR, 1999). It called for a reevaluation of internationalization, recommitment to OPEC, reform of hydrocarbon tax laws and strengthening of the expertise of the tax service in such matters, correction of the generous provisions of the opening vis-à-vis foreign investors, and stimulation of private national capital in the petroleum industry. But Chávez himself did not immediately prioritize changes in fiscal matters and industry control, and his early appointments to the PDVSA presidency reflected his uncertainty. Rodríguez was the minister of oil, but oil policy remained mostly in PDVSA hands.

Roberto Mandini, the first PDVSA president, was unenthusiastic about the opening, but as the former head of Venezuelan-owned Citgo he stonewalled Chávez’s goal of selling foreign assets. Mandini’s replacement, Hector Ciavaldini, brought about the departure of several high executives who were architects of the opening (Alexander’s, November 5, 1999), but the former general’s main credential was his close relationship with the president, dating back to visits to the imprisoned Chávez after the 1992 failed coup. Running an oil company was not his path to heading PDVSA; much of the meritocracy remained in place.

In many areas of policy in the Chávez era, power really lay in the hands of the popular president, not his ministers. Rodríguez Araque’s political base did not extend far beyond the PPT, but he had long-standing ties with Chávez’s older brother, Adnán, another member of the Universidad de los Andes circle. Rodríguez Araque gained influence as Mandini and Ciavaldini failed to march with the president on internationalization. The decisive turn came in November 2001, when Chávez used powers granted by the Congress to decree a new oil law that dramatically revised the terms on which capital, mostly foreign, could henceforth reenter the subsoil. Two key provisions changed the fiscal regime and insisted on majority ownership (not just control of a management committee) of joint ventures. These were frontal assaults on the opening. So was restoration of the Calvo clause.

Violent street protests broke out in middle-class areas of Caracas after the decree laws—not for the first time, but now oil was at the center of the conflict. The demonstration that at the last minute marched on the presidential palace and precipitated (intentionally) the short-lived coup of 2002 started as a march on PDVSA headquarters to protest “politicization” of the company. Company executives were not themselves instigators of the coup, but they were clearly visible with the next opposition gambit—a paro (work stoppage) that nearly shut down the oil industry for three months beginning in December 2002 (Lander, 2004: 16–19). 5 Though a clash between capital and labor on the surface, the struggle was between capital and landed property (the landlord state). The work stoppage or (as the Chavistas label it) “sabotage” brought PDVSA into direct confrontation with the state’s sovereign ownership of the subsoil. As Rodríguez Araque, who had been appointed president of PDVSA after the coup, put it, the government was defending the nation’s “legitimate right to obtain a benefit from exploitation of the resource” based on the state’s right as “owner of the natural resource.” The PDVSA executives, he said, were aligned with “international authors who represent perfectly identifiable interests” and advance the view of “oil as a natural resource and a common good of humanity that should be freely available to it” (PDVSA, 2004: 3).

After the work stoppage, Chávez spoke to oil workers in emotional terms about his earlier meetings with PDVSA executives: “One felt fear in the air, the cold. It was like entering refrigerator for freezing blood. One felt there the looks of rejection. One felt the attitude that never was in truth PDVSA, because Petróleos de Venezuela never was of Venezuela.” Now, he said, PDVSA would be the “beginning of a new country” (patría nueva). In 2006 he would up the ante, ordering existing ventures to “migrate” to the 2001 oil law and further requiring that Venezuelan shares be minimally 60 percent. All the foreign companies except Conoco-Phillips and Exxon-Mobil reached an agreement, including compensation, to complete the migration. These two companies took Venezuela to international arbitration, but early arbitration results indicate that they were themselves in violation of key contract provisions (see Boué, 2014). 6

Impact of Chávez’s Oil Policy

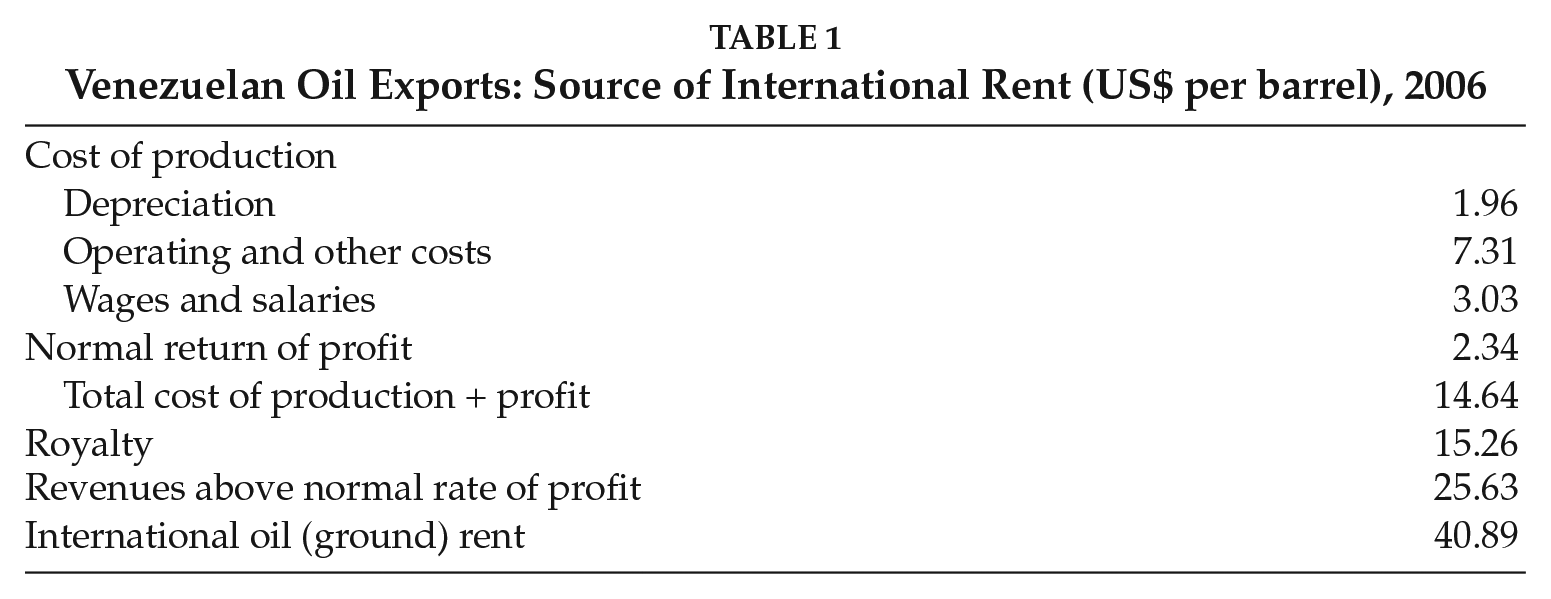

Several Venezuelan oil economists, most notably Mommer (personal communication, 2010) and Asdrubal Baptista (2010 [1997]), 7 have advocated changing national accounts systems to distinguish between the contributions made by international ground rent generated by oil and the value of actual production. Using national accounts data for 2006, Mommer first calculated the cost of production per barrel of foreign oil exports—the total of depreciation, salaries and wages, and other operating costs. Excluded from costs are royalties; these are regarded by the industry as a cost but by the nation as an income, “the patrimonial compensation by the foreigner for the natural resource owned by the nation.” For 2006, total income from oil exports was US$55.54 per barrel on total exports of 2.975 million barrels. The normal rate of return to capital and labor in Venezuela outside of the oil sector is 47 % however, the global rate of profit has been estimated as only a third of the Venezuelan rate (Li, Xiao, and Zhu, 2007: 10). Following Mommer, I apply this 47 percent rate to the cost of production to arrive at estimates of profit versus that portion of the total surplus value that constitutes an international ground rent (Table 1). In 2006, international oil rent was 2.8 times the value of production (cost of production + normal profit) and 17.5 times profit. The average price per barrel in 2006 was, as we have seen, only US$55.54, US$40–US$50 less than average prices in 2012 and 2013, and US$70 less than prices at their peak in 2014. Assuming that the average cost of production has not escalated wildly, we can reasonably estimate that all of this economic surplus generated by the post-2006 boom years falls into the category of rent, not profit.

Venezuelan Oil Exports: Source of International Rent (US$ per barrel), 2006

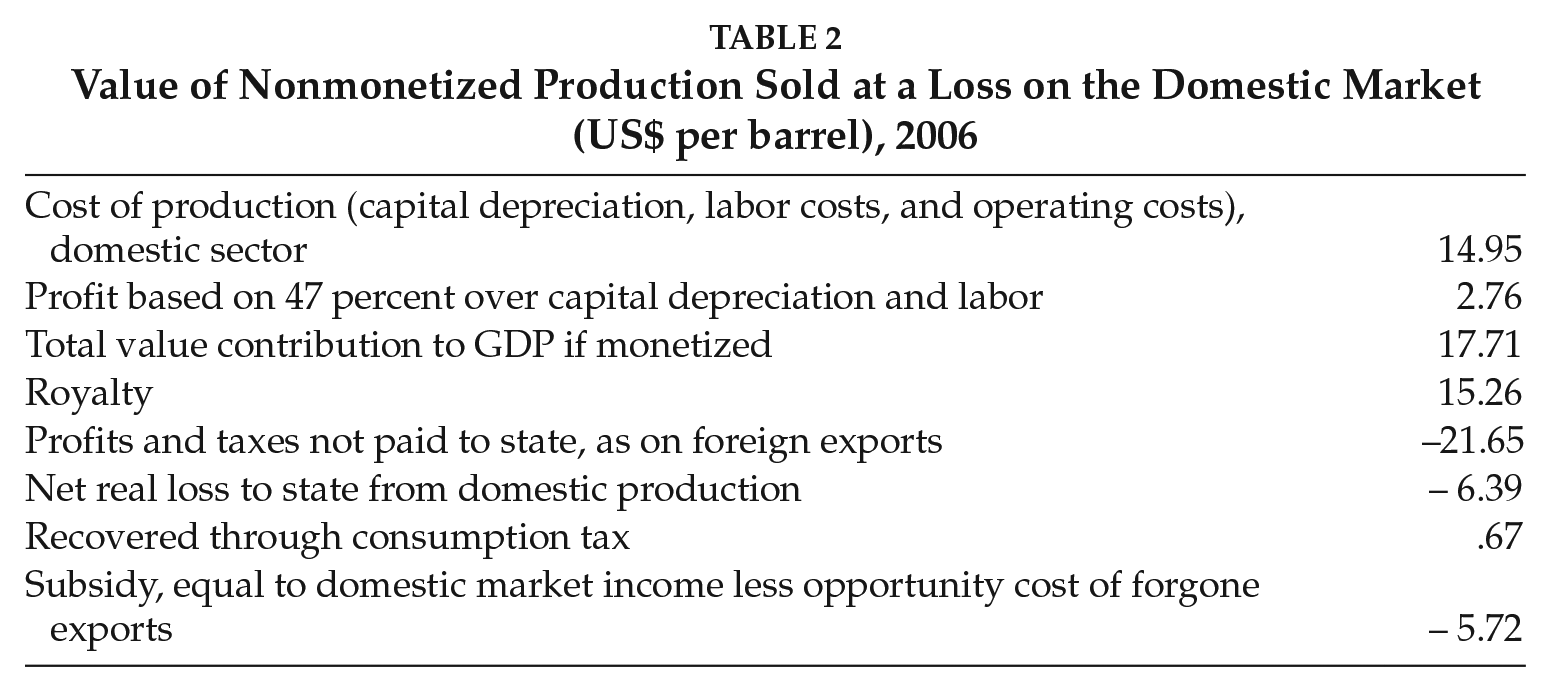

Table 1 measures the proportions of rent and profit that PDVSA’s exports contribute to the Venezuelan economy, but it does not take into account the nonmonetized value of the production of oil sold at prices below the cost of production on the domestic market. The matter of domestic prices had been central to the popular grievances that led to the Caracazo of 1989, and no government, including Chávez’s, had dared raise the issue again. The failure to address this issue must be counted as a negative legacy of the late president to his successor, President Nicolás Maduro, because the fiscal burden has become onerous as domestic consumption has increased. Using the “normal” rates of return to capital and labor in Venezuela, the true subsidy (the difference between net domestic revenues and normal returns to capital and labor) in 2006 was US$1.44 billion (Table 2). Over the next seven years, domestic consumption quadrupled, from 200 million to 800 million barrels per year. The resulting losses constituted a significant opportunity cost, especially since oil priced between US$90 and US$100 could not be placed on the global market. Here, too, I am not considering externalities such as environmental impact in my calculations.

Value of Nonmonetized Production Sold at a Loss on the Domestic Market (US$ per barrel), 2006

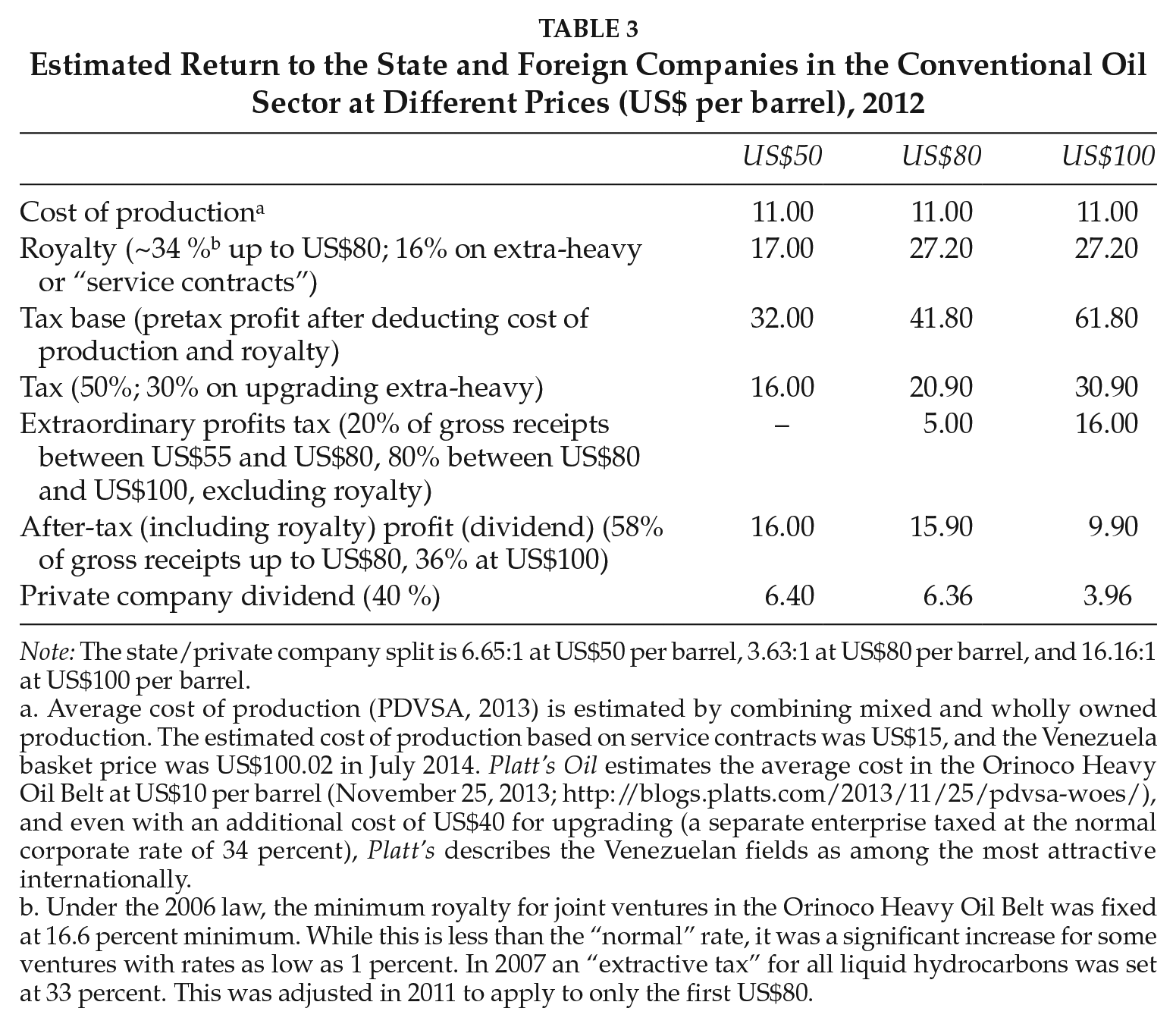

I have distinguished rent from normal profit in the Venezuelan economy in 2006. Turning now to the way fiscal policy and ownership rules affect the proportions of surplus value accruing to the state d foreign capital, I present the distribution of surplus between a foreign investor and the state under the terms of the reforms enacted by Chávez by decree in 2001 and the reform of 2006, which raised the required percentage of ownership for PDVSA to 60 percent and required firms operating under existing service agreements to “migrate” to the new fiscal regime (Table 3). Firms operating under joint ventures in heavy crude were forced to do so, beginning in 2007. In recognition of the cost of upgrading extra-heavy oil, the royalty was reduced to 16 percent, but under the opening royalties had been as low as 1 percent. Finally, as price began to soar in 2010, an “extraordinary profits” tax was added, to be applied in increased percentages as prices rose. 8

Estimated Return to the State and Foreign Companies in the Conventional Oil Sector at Different Prices (US$ per barrel), 2012

Note: The state/private company split is 6.65:1 at US$50 per barrel, 3.63:1 at US$80 per barrel, and 16.16:1 at US$100 per barrel.

Average cost of production (PDVSA, 2013) is estimated by combining mixed and wholly owned production. The estimated cost of production based on service contracts was US$15, and the Venezuela basket price was US$100.02 in July 2014. Platt’s Oil estimates the average cost in the Orinoco Heavy Oil Belt at US$10 per barrel (November 25, 2013; http://blogs.platts.com/2013/11/25/pdvsa-woes/), and even with an additional cost of US$40 for upgrading (a separate enterprise taxed at the normal corporate rate of 34 percent), Platt’s describes the Venezuelan fields as among the most attractive internationally.

Under the 2006 law, the minimum royalty for joint ventures in the Orinoco Heavy Oil Belt was fixed at 16.6 percent minimum. While this is less than the “normal” rate, it was a significant increase for some ventures with rates as low as 1 percent. In 2007 an “extractive tax” for all liquid hydrocarbons was set at 33 percent. This was adjusted in 2011 to apply to only the first US$80.

The relative share of profit per exported barrel of oil allocated to the state and to the companies under this fiscal regime varies considerably according to the movement of prices. It might seem that the landlord state reaps profit while contributing nothing to production (that is, extraction), but the rates of return to foreign companies are above Venezuelan rates at lower prices and above typical international rates at higher prices. Certainly, investors might migrate to countries offering more advantageous terms, but Venezuela’s huge reserves, location, and infrastructure have made most companies decide to remain. And, of course, there is the possibility that a future government will move back toward the opening arrangements.

While these results call into question company complaints of unfair treatment, the profit ratios also suggest that oil may have no intrinsic value tied to actual prices comparable to that of water, shampoo, or soft drinks. Consider that in 2006 Chávez offered to negotiate a stable market price of US$50 per barrel (Palast, 2006), which he envisioned at the time as a guarantee that Venezuela could economically develop its extra-heavy oil deposits. In 1999, his first year in office, the price had reached a nadir of approximately US$6. Also, one can argue that in an unstable environment a fiscal policy that maximizes capture of ground rent is just as important as one that permits the state to capture differential rents in times of high prices. However much the plunge of oil prices from US$130 to US$30 between 2014 and 2015 has impacted both the lives of Venezuelans and the political fortunes of Chavismo, without the fiscal reform of 2001 and the increased ownership of joint ventures Venezuelans would be forgoing collection of much of the rent still available at US$40.

Unfortunately, it is difficult to assess the return on investment to capital overall in the extra-heavy oil sector; production costs vary greatly from field to field and in many government and company reports are not disaggregated. Costs of early stages of refining for heavy oil are often aggregated into costs and taken into account in fiscal policy. Trade journals have at times estimated that the cost of typical upgrading operations in heavy oil after extraction is US$30 per barrel, and the Venezuelan government allows that phase of production to be taxed at the normal corporate rate; it also charges a lower royalty. Yet there are reasons to doubt that lower royalty and tax rates are justified even in the heavy oil sector. Wikileaks transcripts of conversations between oil executives and U.S. embassy officials referred to a break-even point of about US$9 for some heavy oil in the early Chávez years, though it is not clear whether this included upgrading. 9 Even at US$30, much less at US$90 to US$130 during the peak boom years, there seems to have been plenty of room for high profit margins (Boué, 2014).

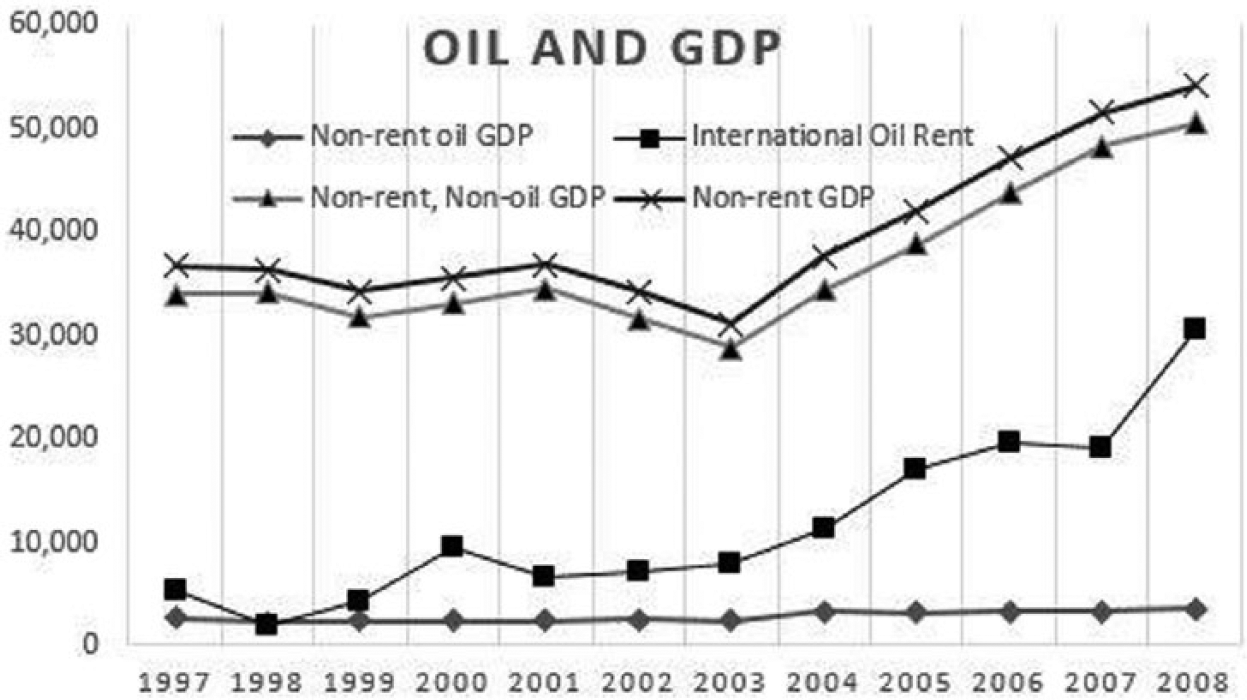

The opening virtually eliminated much of the compensation to the resource owner (the Venezuelan nation) for capital’s extraction of the resource. Even if profits were split 50/50 between the Venezuelan state and investors, this would merely bring the state’s share to the level that prevailed between 1945 and 1957 and much lower than the 64/36 split achieved by a reform in 1958 (Mommer, 1988: 145). In some circumstances, under the opening fiscal regime and low prices, the state received very little compensation. Regnault (2013; see Figure 1) used a methodology similar to Mommer’s to separate ground rent from normal profit over time and found that in 1998 the nation received virtually no compensation for extraction of this exhaustible natural resource. Regnault’s trend lines show the rising importance of ground rent versus value realized through production in extraction. The ratio of oil rent to total nonrent GDP was approximately 1:2 in 2008, when the average global price was US$91.48 per barrel. Prices remained high, above US$100 most of the time, through the middle of 2014, but actual production in the Venezuelan oil sector remained largely flat. This fact takes on importance once we realize that oil for Venezuela is an industry, not just a source of rent. The oil sector is not an enclave; it has important forward and backward linkages, and these could be expanded. While the opening radically cost Venezuelans by abjuring rent, PDVSA in the Chávez years stagnated as a productive entity, with consequences that are becoming more evident today.

International oil rent and GDP in 1997 bolivars, 1997–2008 (adapted from Regnault, 2013).

The fiscal reforms that Chávez introduced via decree law authorized by the National Assembly did not remove economic incentives for capital to produce in Venezuela. Certainly the transnational oil companies were not pleased to lose the extraordinary profits available to them in the opening era, but their profit margins remained more than healthy. Those that decided, in contrast to Exxon-Mobil and Conoco-Phillips, to bargain rather than resort to domestic and international legal resistance had their eye on a longer-run bargaining game. They accepted lower profits and chose to position themselves to continue to get access to the country’s burgeoning reserves. They could not easily make credible the threat of withdrawal when the large national oil companies from Europe and Asia were entering the competition for access to Venezuela’s hydrocarbon resources. The real loser in the game was the PDVSA meritocracy, which chose to engage in a fierce political battle to overthrow Chávez rather than accept the new regime in oil.

Sustainability of the Chávez Oil Reforms

During the opening the PDVSA meritocracy achieved nearly the ideal situation for capital and consumers—elimination of any compensation to the resource owner for extraction of an exhaustible natural resource. The production increase undermined OPEC discipline and contributed to oversupply; the fiscal terms encouraged increased production and ensured that the state’s share of profit would be less. The collapse of bureaucratic and administrative control over oil had built up over more than a half century. By 1998 the country may have been receiving no contribution at all of international rent. No doubt the post-1998 recovery can be attributed in part to a global economic recovery and economic expansion of the BRICS and other newly industrializing states, but it also has much to do with the policies of President Hugo Chávez Frías.

The political opposition in Venezuela has portrayed oil policy and the PDVSA record in the Bolivarian era as total failures. In part the charge rests on exaggerated depictions of production tendencies since the work stoppage of 2002. In reality, production has declined only slightly, from about 3.1 million to 2.9 million barrels per day (PDVSA, 2013). Claims of declines below 2.5 barrels per day are reached by not including extra-heavy production in totals, but international audits and the fact that PDVSA is paying a royalty on the higher production estimates lend veracity to the Venezuelan figures. However, the opposition criticism is not to be entirely dismissed. Under Chávez and Maduro, the government policy has been to seek production increases, but in fact goals have been missed. Whereas production levels were planned to rise from 2.9 million to 5.5 million barrels per day from 2012 to 2016, levels in 2013 actually slightly declined from the baseline figure. Furthermore, PDVSA has continued to rely solely on foreign investment for expansion. In other words, while fiscal terms and ownership issues have been addressed, the company has not shown any significant development as a productive enterprise. It has depended heavily on debt to finance development, with Chinese investors in the lead. Loans have been contracted not only to finance oil exploration and development but also to fund the social and economic missions. Production devoted to repayment of loans is not renunciation of rents, but it does represent a different kind of threat, that of mortgaging future rents. This latter practice bears some similarity to a key mistake of the first Carlos Andrés Pérez administration (1974–1978), which unwisely borrowed heavily against future earnings during the OPEC decade.

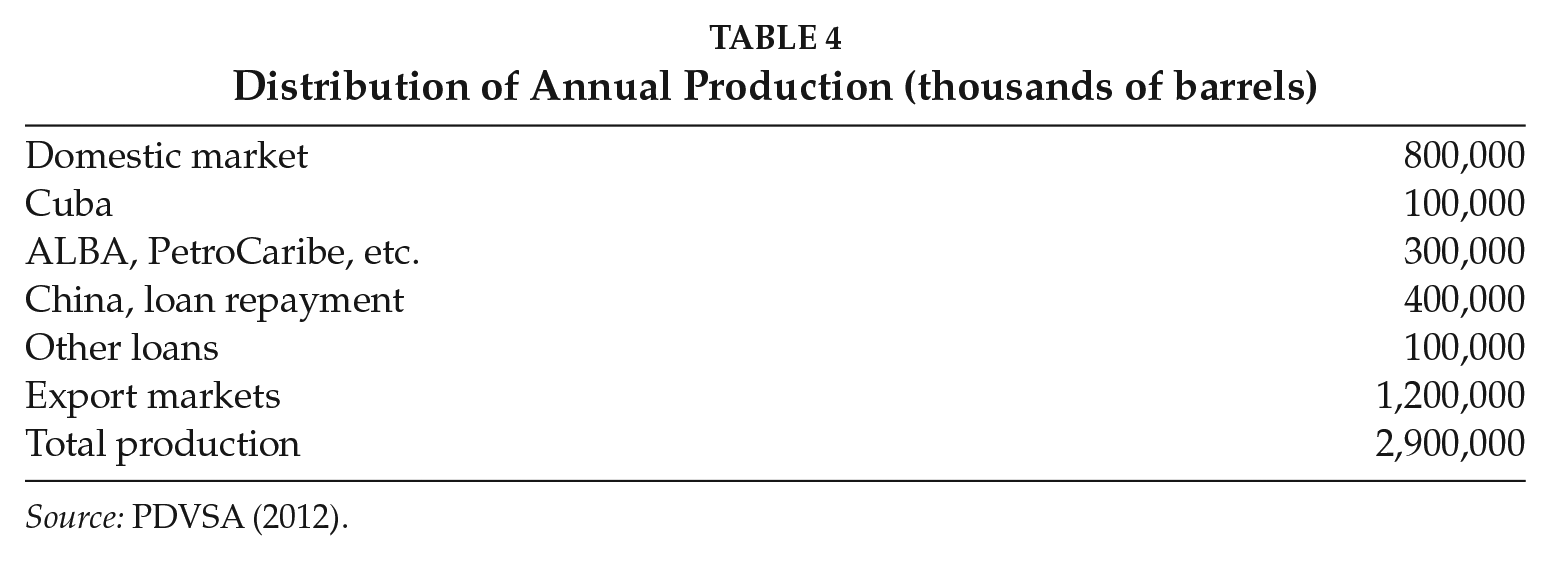

By 2014 PDVSA debt had reached US$40 billion. Much of the borrowed money has been used to shore up the overvalued bolivar and to sustain the company’s role in social and economic programs. Since 2012 PDVSA has fallen into arrears on payments to service providers, but this has less to do with its burden than with its difficulty in obtaining funds to make payments from the Central Bank. Together these forces inevitably increase pressure to expand production, but it will be hard to reconcile this goal with falling prices and cooperation with OPEC. Some of the burden on PDVSA could be eased if the burden of subsidizing the domestic market were eased, and finally a modest rise in domestic gasoline prices was implemented in 2016. Rising consumption at home is also a direct threat to the sustainability of the international solidarity projects and financial support to the countries of the Alianza Bolivariana para los Pueblos de Nuestra América (Bolivarian Alliance for the Americas—ALBA). The proportion of Venezuelan hydrocarbon production devoted to the most lucrative export market is now only about 41 percent of total production (Table 4). Cuba’s share is remunerated by services (e.g., medical, security, coaches), and the oil sold under ALBA, PetroCaribe, etc. is discounted (through financial terms) rather than sold at a loss or at cost. Barter arrangements make it difficult to assess how much Venezuela is giving up through special aid and trade programs.

Distribution of Annual Production (thousands of barrels)

Source: PDVSA (2012).

PDVSA workers may have heroically maintained production levels after the 2002 work stoppage, but many company fields have been in operation for more than 50 years, and the country’s largest reserves are in extra-heavy oil, requiring large amounts of capital and technology. The company has failed to meet production goals set in its own annual reports. Its associates are more likely to be state-owned national oil companies such as the Chinese National Offshore Oil Corporation than the major private transnationals, but most of these companies are owned by the governments of consuming nations; their goals are not necessarily any more compatible with those of the landlord state than are those of the private international oil companies. And PDVSA continues, as in the opening era, to rely on foreign investment to maintain production in aging fields and develop new ones.

What of the century-old dream of “sowing the oil” in economic development outside the oil sector? This question is beyond any exploration in depth here, but there are troubling signs that Chávez’s missions to promote “endogenous development” are struggling. Thomas Purcell (2013: 163) argues that weak oversight, both within the communal councils and in the state bureaucracy, has facilitated corruption and inefficiency at the grassroots level. He concludes that the Bolivarian Revolution must shift strategy toward the “transformation of state resources (ground rent)” into “normal, productive capital.” Such a shift, he argues, would require radical steps such as the abolition of private property (including cooperatives and micro-enterprises) and would pose “new challenges to the forms of mass participatory organization.” But even at the peak of Chávez’s popularity Venezuelans, including those living in the strongholds of Chavismo in urban areas, showed little inclination to abolish private property or the liberal state (Hellinger, 2011). Even Chávez could not induce them to vote in the majority (in the referendums of December 2007) for modification of the system of property rights that was well short of abolition.

The work of radical political economists studying the influence of ground rent on development in Argentina and Brazil echoes Purcell’s finding for Venezuela. Especially influential has been the work of Juan Iñigo Carrera (2008a; 2008b), which parses Argentina’s GDP as conventionally divided into agrarian ground rent and nonrent and concludes that Argentina’s international natural resource rents, most of which are agricultural, have failed to advance the country’s economic development of capital because they have effectively subsidized the bourgeoisie and failed to incentivize production. Nicolas Grinberg (2011; 2013) applies a similar methodology to the calculation of natural resource rents in Brazil and arrives at a similar diagnosis. According to Grinberg (2010: 188),

Import-substituting policies and the populist regimes associated with them in their nationalist and developmentalist variants did not constitute a model of development implemented to solve an external problem (i.e., decreasing terms of trade) or as a response to the emerging power of the urban working classes, as is argued by structuralist and orthodox writers respectively. On the contrary, they were the political expression of a form of capital accumulation based on the appropriation/recovery by industrial capital of a portion of the ground rent available in these national economies.

He points out (193–194) that in both Chile and Venezuela, despite their very disparate developmental paths, ground rents appropriated as a result of the commodity boom of the past 20 years were used to pay down the international debt, and this was justified in both cases by the claim that payment would allow for more autonomous development. But reduction in dependency is illusory, he says. Chile is not becoming an advanced liberal state nor Venezuela a twenty-first-century socialist state. Failing a change in any of the region’s developmental strategies, it was predictable that a decline in commodity prices would once again produce a widespread decline of real wages and an increase in poverty there and in the rest of the region (198). President Maduro has found himself in the unfortunate position of testing this proposition since oil prices began to tumble in late 2014.

Grinberg, without specifying the necessity of a working-class-led strategy, emphasizes the need for Latin America to pursue “the concentration of industrial capital in every branch of production on the scale necessary to compete in the world market through the vanguard development of technology, using the extraordinary social wealth available in the form of ground rent to enhance rather than to retard it” (2010: 199). As does Purcell, he doubts that development can be achieved through small-scale enterprises. His view is also consistent with Di John’s (2009) appraisal that appropriation of ground rents need not obstruct development; what is lacking is a state capable of disciplining the native bourgeoisie to industrialize competitively. 10

It is not hard to see that a victory via election or otherwise by the Venezuelan opposition would put the Chávez legacy in oil policy at risk. Its candidate for president in 2012 and 2013, Henrique Capriles, stated in his platform that he was committed to “guaranteeing the managerial, financial, and operational autonomy of PDVSA” and “respecting compliance with the legal framework governing current contracts.” Regardless of Capriles’s intentions, this most likely would mean a modified version of the opening. And of course an opposition government would very likely eliminate much of framework of oil discount programs, especially arrangements with Cuba. However, there may be geopolitical imperatives that prevent a retreat from PetroCaribe.

The production goals of the government and those outlined by the opposition leader Capriles in his 2012 platform differ little, both seeking to double production to reach 6 billion barrels within a very short time frame. Capriles pointed out, accurately, that Chávez’s oil plan in 2005 envisioned 5.8 million barrels per day production by 2011 and production had in fact declined to 2.9 million (using the government’s own figures). Capriles spoke of increasing Venezuelan involvement in production, which would include the return of many workers discharged after the 2002–2003 work stoppage. The government, however, has already allowed some professional and technical workers to return. The troubling reality is that the accumulating pressures on PDVSA could undermine the positive legacy of the Chávez reforms even without a return of the opposition to power.

Conclusion: The Chávez Oil Legacy

The question whether pursuit of natural resource rents is ultimately compatible with socialism has arisen in certain critiques emanating from indigenous and environmental movements (e.g., “Es pro-capitalista,” 2012) and from left academic critics (e.g., Petras and Veltmeyer, 2014). Issues of indigenous control over autonomous territory, the environmental consequences of hydrocarbon exploitation, the cultural imperialism and consumerism fostered by the foreign oil companies (see Tinker Salas, 2009), and the compatibility of extractive activities with the construction of socialism are certainly of no small consequence for an evaluation of the legacy of Hugo Chávez. My focus in this study, however, has been narrower. Chávez’s oil policies ran counter to the project of PDVSA executives, who sought maximization of production rather than maximization of rent.

Nationalization of the oil sector put an end to the concessions era, in which the conflicting interests of extractive capital and the landlord state were relatively clearly defined. Nationalization, while a victory for the Venezuelan nation, obscured this conflict. The boom years following nationalization also obscured the fact that the “success” was more in appropriating international ground rent than in the efficiency of PDVSA executives whose careers were built rising through the managerial bureaucracy of the expropriated companies. As the political regime decayed, the PDVSA meritocracy gained prestige and seized control of oil policy, implementing internationalization and the oil opening.

Hugo Chávez restored state control over PDVSA, took the diplomatic lead in resuscitating OPEC, and sought to capitalize a socialist development strategy with appropriated ground rents. His achievement was restoring national sovereignty over Venezuela’s subsoil. That legacy is threatened not only by the political opposition to the Chavistas but by institutional weakness, increasing debt, faltering economic progress, and falling oil prices. Still, Chávez directed rents to the socially and economically excluded of his country and through his international policies attempted to reduce the burden of high oil prices on those least able to afford it. He confronted and rolled back the neoliberal dream of making the natural resources of the Global South a free gift of nature to transnational capital, and this is a legacy worth defending.

Footnotes

Notes

Daniel Hellinger is a professor of international relations at Webster University.