Abstract

To what extent did the PT governments follow developmentalist policies? A critical assessment reveals that they combined two varieties of developmentalism in different ways over time, with a surprisingly high frequency of policy changes, and that orthodox policies played a prominent role in part of this time span.

Até que ponto os governos do PT seguiram políticas desenvolvimentistas? Uma avaliação crítica revela que eles combinaram duas variedades de desenvolvimentismo de maneiras diferentes ao longo do tempo, com uma frequência surpreendentemente alta de mudanças de políticas, e que as políticas ortodoxas tiveram um papel de destaque em parte desse período.

Brazil received considerable attention in the 2000s for combining growth with equity, but its deep crisis in recent years has raised the question whether both this success and its implosion were the result of a deliberate strategy or of changes in the international context (mainly the boom-and-bust of commodities prices and capital flows) or domestic policy failures. This debate involves supporters and opponents of the strategy adopted by successive Brazilian governments led by the Partido dos Trabalhadores (Workers’ Party—PT) over more than a decade, which many have labeled (though with different prefixes) “developmentalist” (Ban, 2012; Bielschowsky, 2015) or (by analogy with “varieties of capitalism”) “varieties of neoliberalism” (Saad-Filho in this issue). 1 Following Fonseca (2014), the concept of developmentalism is ambiguous by definition, nurtured both by theory and by experiences with economic policy. Indeed, a common denominator for academics and the Brazilian governments of this period (Ministério de Planejamento, 2003) was the aim of combining sustained economic growth with the restructuring of production and income distribution by giving the state an active role.

We ask whether and to what extent the PT governments (2003 to mid-2016) adopted a developmentalist approach and, if so, what kind. To address our research question, we offer three main hypotheses: (1) that there is a set of conceptual approaches that can be labeled “developmentalist”; (2) that the policies developed during this period represented different kinds of developmentalism and even encompassed elements that we classify as “orthodox”; and (3) that the significant changes of the policy mix over time were conditioned both by the international context and by domestic factors. With this we address a lacuna in the literature on the Brazilian case by attempting to shed light on the policies applied and to bring out the differences between the PT governments and the starkly orthodox government of President Michel Temer, who took office with the impeachment of President Dilma Rousseff in August 2016.

The following section presents the different varieties of developmentalism. The next presents stylized facts of the external context and summarizes the macroeconomic features of the Brazilian economy in the period under review. The next lists the economic and social policies applied from 2003 to mid-2016, and the next proposes a periodization and typology of PT government policies in terms of the distinction between different developmentalist and other approaches. The final section offers conclusions.

Varieties of Developmentalism

“Developmentalism” involves two intertwined perspectives, that of a phenomenon of the material world (economic practices) and that of a phenomenon of the world of ideas (concepts or views of the world). The former is also expressed as political discourse, while the latter seeks to form a school of thought (Fonseca, 2014: 30). Developmentalism emerged from the development studies of the 1950s and the Latin American structuralist approach, which sought to understand the specificities of underdevelopment and how to overcome it. Classic developmentalism departed from the idea that the typical division of labor between developed and developing economies created a structural balance-of-payments constraint and impaired domestic growth. As a phenomenon of the material world, it translated into national-developmentalist strategies for promoting industrial development on the assumption that it was the most efficient way of achieving an increase in productivity and in national income. It used the “center-periphery” metaphor to translate the productive and technological asymmetries of the international order and saw industrialization as the only way for the peripheral economies to gain access to some of the technical progress of the developed economies and gradually raise living standards (Ocampo, 2001; Prebisch, 1950).

The current debate has been intertwined with policy discourse and policy making, especially in the many Latin American countries where until recently leftist parties dominated governments. Updated concepts of developmentalism attracted attention in semimature economies of the continent such as those of Argentina and Brazil, 2 which featured more diversified structures of production and ran the risk of premature deindustrialization, because of profound discontent with orthodox policies based on the neoliberal recommendations of the so-called Washington Consensus. Indeed, the region with the most economic inequality in the world experienced stagnation or even worsening of inequality throughout the period of liberalization. In the course of a critical assessment of the neoliberal agenda of domestic market liberalization, trade and financial openness, and reduction of the role of the state, income distribution emerged at the center of debate.

Within this renewed and multidisciplinary debate in Brazil, we identify two new concepts in the economic field, social developmentalism and new developmentalism, 3 that updated classic developmentalism and added new dimensions. Both rejected the neoclassical idea of welfare maximization by specializing in comparative advantage at the global level (much as did classic developmentalism), seeing structural external constraints caused by incorporation of peripheral economies into the global market as the cause of the lack of economic dynamism at the domestic level. Thus, they supported a national strategy of economic development with the state playing an active role in promoting structural change toward (re-)industrialization, resulting in social transformation (Bielschowsky, 2015; Fonseca, 2014: 41). While the concept of new developmentalism is rather well developed and clearly defined in paradigmatic terms in various papers mainly by Bresser-Pereira (2011; 2015), social developmentalism is treated less coherently by a number of writers. Although the two are rather similar in their policy aims, seeking to achieve change in production with income redistribution, they clearly differ regarding most of their targets and tools.

Social developmentalism is closer to the classic developmentalist approach, continuing to focus on the shortage of domestic demand to push investment into productive diversification, but it gives the aim of equal income distribution a more prominent role and stresses increasing domestic mass consumption to drive economic growth and increase production. The structural balance-of-payments constraint is expected to be mitigated by export growth induced by scale effects and industrialization and by domestic demand, given the complementarity of the domestic and foreign markets. Growth may also be supplemented, at least temporarily, by the expansion of the natural-resource-intensive sector and its supply chains (Biancarelli, Rosa, and Vergnhanini, 2017; Bielschowsky, 2012). New developmentalism takes a predominantly macroeconomic approach inspired by the development path of the emerging Asian markets, with their strategy of strategy of export-led growth. It sees two obstacles to development: the tendency toward currency overvaluation as a result, mainly, of specialization in commodities exports (the “Dutch disease”) and the net flows of foreign capital stimulated by the policy of growth-cum-foreign-savings and the tendency of wages to increase less than productivity because of the unlimited supply of labor. Here the aim of (re-)industrialization is directly linked to the target of an export surplus of manufactured goods, pushing for further investment in this sector that will enable the country to avoid incurring foreign debt. In this view, the exchange rate plays the key role in influencing both imports and exports. Improvement in income distribution will result from (formal) job creation in the manufacturing sector and increases in wages alongside productivity gains (Bresser-Pereira, 2011).

Regarding the policy tools attached to each of these approaches, Carneiro (2012) notes that reflections on social developmentalism are rather fragmented, especially in the first generation of papers (Bastos, 2012; Bielschowsky, 2012; Carneiro, 2012), in which the focus is on policies oriented toward redistribution and shifting production patterns, as follows: (1) wage policies, the minimum wage being a powerful policy instrument for fostering wage increases in real terms, especially in the lower income range; (2) income transfers targeted at the poor; (3) consumer credit and subsidized financing by public banks; (4) public investment, especially in infrastructure, seen as crucial for creating demand but especially as an incentive for private investment; and (5) industrial policies to stimulate private investment.

Macroeconomic considerations appear mainly in the second generation of publications. Rossi (2014) argues that macroeconomic policy consistent with social developmentalism should maintain economic growth through countercyclical fiscal policies. Fostering investment in production would require low interest rates and a nonappreciated and nonvolatile exchange rate, which could be pursued along with a more flexible execution of the current orthodox framework, the so-called macroeconomic tripod of inflation targeting, a floating exchange rate, and a primary-surplus target. He does not explain, however, how to make these macroeconomic tools compatible with the main pillar of social developmentalist policies, wage increases in real terms, without jeopardizing price stability or a competitive exchange rate.

For new developmentalism, Bresser-Pereira (2011) describes the necessary tools: currency devaluation (if necessary, supported by capital controls) and the subsequent maintenance of the exchange rate at a level where domestic industry becomes internationally competitive; other macroeconomic instruments for maintaining price stability, supported by the combination of a low interest rate and a balanced public budget with room for countercyclical fiscal policies over the cycle (meaning an austerity bias during a boom); and industrial policy that is secondary and targeted at exports until the economy catches up with the advanced economies. Wages may lose purchasing power in the short term as a consequence of currency devaluation, but in the medium term they should grow along with productivity to prevent their spurring inflation. Income redistribution is expected to stem from additional job creation in the manufacturing sector. Redistributive policies are included as an addendum in later publications (Bresser-Pereira, 2015), reacting to the heated debate around redistributional issues’ not being vital to the new developmentalist strategy.

Thus the new varieties of developmentalism substantially diverge in terms of the priority given to targets and tools (Table 1). This results in sharply different modes of policy coordination.

Varieties of Developmentalism and the Orthodox Approach Compared

To facilitate the analysis of policy coordination, we analytically disaggregate the two varieties of developmentalism into three different layers of policy aims, targets, and tools. 4 We also refer in this table to the orthodox approach to sharpen the understanding of the differences between the body of developmentalist concepts and the orthodox approach that has globally dominated the formulation of development strategies at least since the 1990s. For our purposes, we find the label “orthodox” to differentiate macroeconomic and social policies more precise than the more general label “neoliberal.” 5 Yet, since the orthodox concept is well established, in the following we detail only the two developmentalist approaches.

Empirical Outcomes

Over the period under consideration, the international context underwent important changes. Three phases can be identified: (1) from 2003 to the global financial crisis, which was benign for emerging economies in terms of trade (high commodities prices and external demand) and capital flows; (2) from September 2008 to 2010, including the crisis, the rapid recovery, and the new “twin boom” of commodities prices and capital flows; and (3) from 2011 to mid-2016, characterized by a deterioration of international conditions (Figure 1; for details, see Biancarelli, Rosa, and Vergnhanini, 2017).

World trade (annual change in percent) and capital flows (US$ billions), 2003–2016 (data from IMF, 2017).

During the first phase (specifically, from 2004 to mid-2008), the Brazilian economy experienced unprecedented growth compared with the 1980s and 1990s, an average of 4.8 percent per year. During this precrisis boom, the main engine of growth was household consumption (around 60 percent of the GDP). Another novelty of this period was the continuous growth of credit to households and firms. In line with the situations of other emerging economies, the recession caused by the contagion effect of the global financial crisis was brief, mainly because household consumption mitigated the adverse effects of the crisis. The economy recovered quickly, and in 2010 GDP recorded a growth rate of 7.5 percent; both consumption and investment contributed to that healthy recovery.

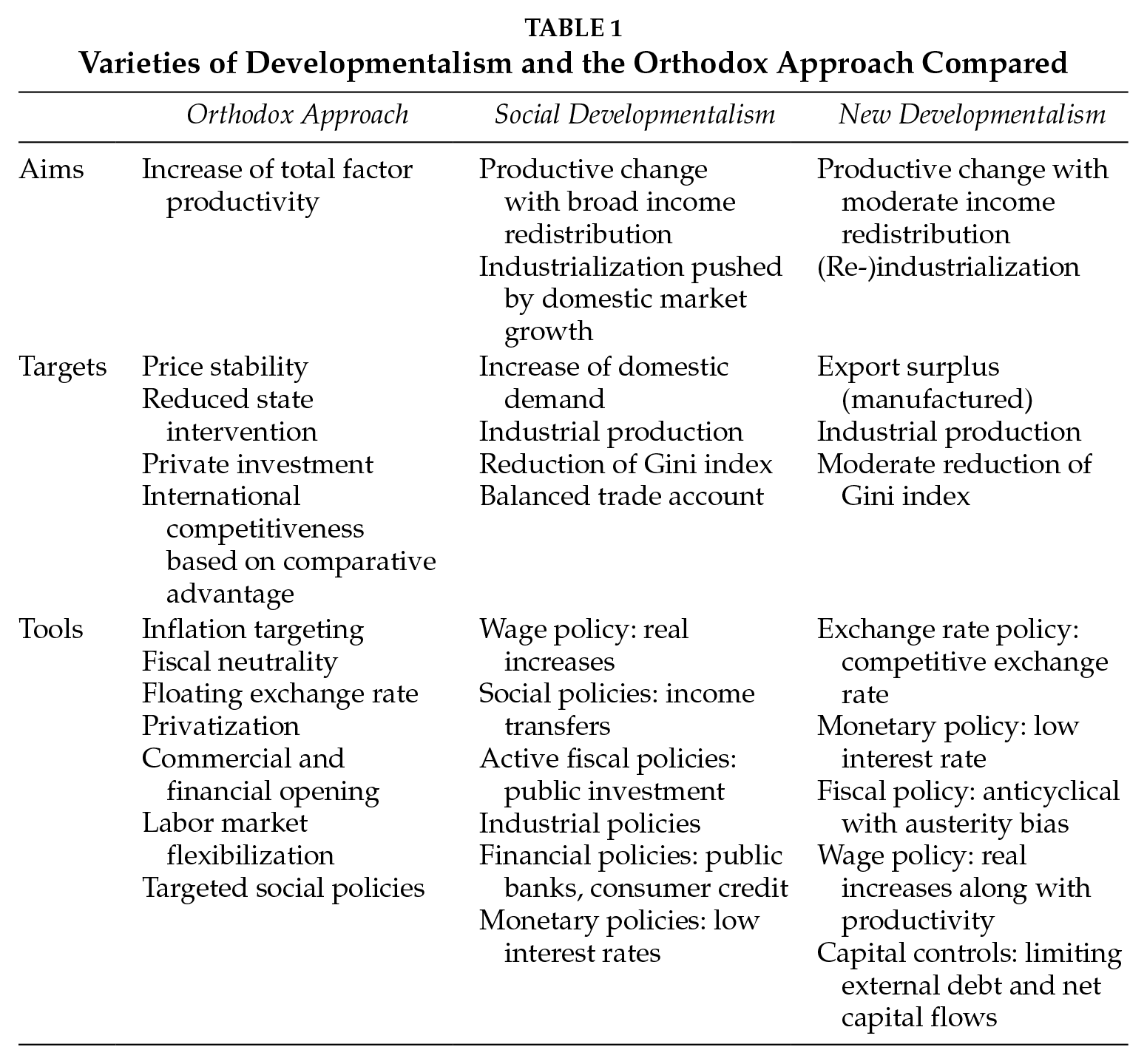

Growth began to slow down again in late 2010, however, further decelerating in 2012 and turning into the worst economic recession since at least that of the 1930s (Banco Central do Brasil, 2017). A set of shocks contributed to this crisis, among them a deterioration of the terms of trade, accelerated inflation due to a de-freezing of monitored service prices and strong currency devaluation, plus a water shortage. The recession, fueled by a tightening of monetary and fiscal policies from 2015 on, produced declining wages and profits, and this caused a huge slowdown in the supply of credit (Figure 2) and a deterioration of the financial situation of nonfinancial corporations, further delaying the recovery of the economy (Paula and Pires, 2017).

Credit supply by ownership (growth rate in percent compared with previous year in real values deflated by Consumer Price Index), 2003–2016 (data from Banco Central do Brasil, 2017).

Economic growth in 2003–2013 was accompanied by a sharp reduction in the unemployment rate, from 12.4 percent in 2003 to 5.1 percent in 2013 (this rate increased to 8 percent in 2015 because of the recession). The combination of low unemployment and real wage increases contributed to an improvement in social indicators, especially economic inequality—a trend also observed in other Latin America countries (Fritz and Lavinas, 2015). In the case of Brazil, the poverty rate fell sharply, from 35.8 percent in 2003 to 13.3 percent in 2014 (IPEA, 2017). The process of income redistribution encompassed both the personal dimension, with a reduction of the Gini index, and the functional one, with an increase of the wage share of total income.

However, studies using personal income tax records (e.g., Gobetti and Orair, 2015; Morgan, 2017) show a different picture of Brazilian personal inequality, revealing that the Gini index, which is based on household survey data, overestimates the improvements in the personal income distribution under the PT governments mainly because of the underestimation of the level of incomes at the top of the distribution. These studies confirm that poverty and inequality of income from labor registered a decline, but the exceptionally large concentration of income at the top did not change. As a result, the bottom made gains at the expense of the “squeezed middle” of income earners. 6

Besides growth and income redistribution, the third aim of developmentalism is to achieve a reallocation of productive resources from the traditional sector (especially agriculture) to the manufacturing sector (mainly its higher-tech segments), but in 2008–2015 the decline of this sector’s share of the GDP gained momentum (Figure 3).

Manufacturing sector (% of GDP), 1994–2015 (IBGE, 2017).

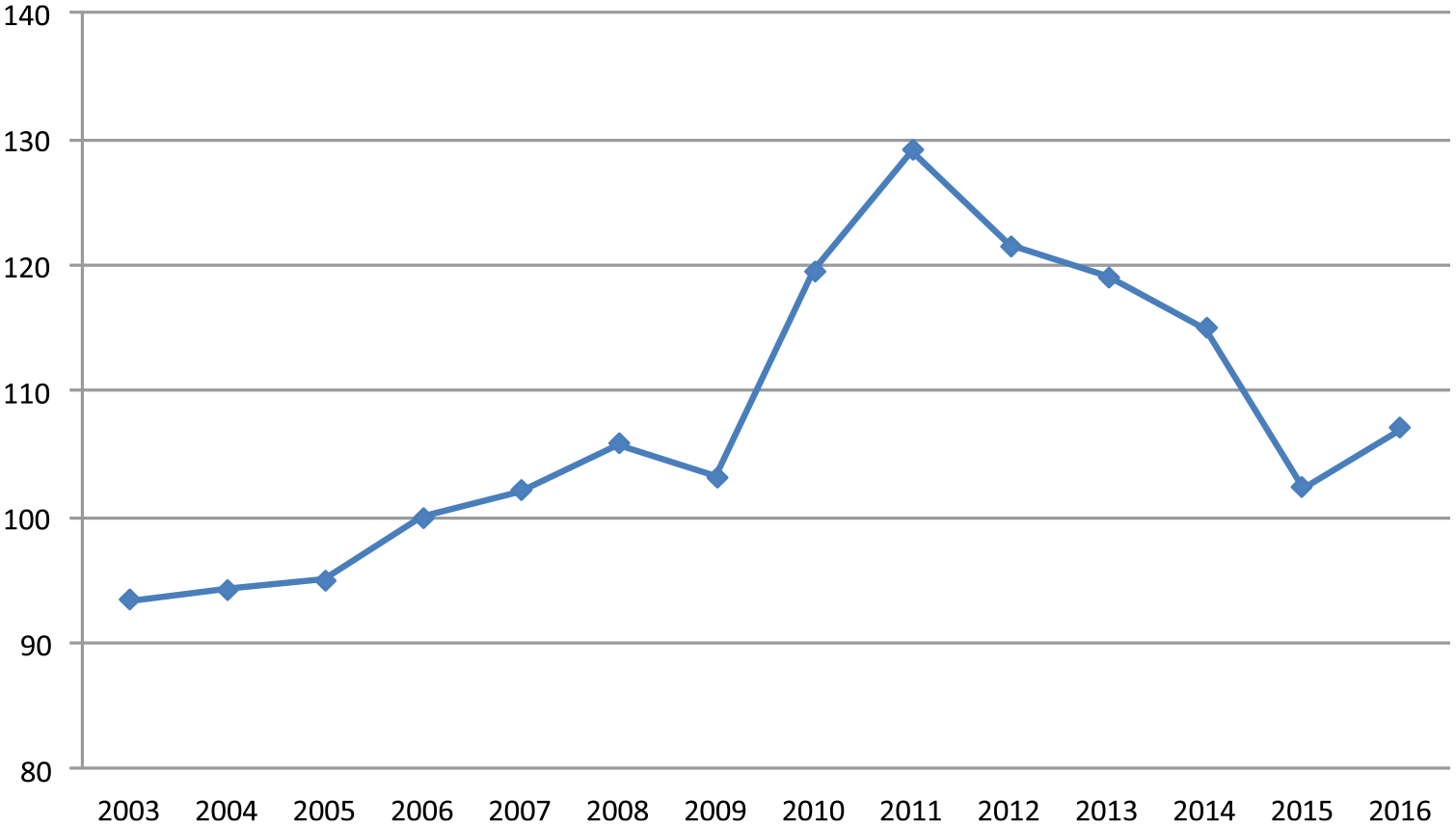

Moreover, this descending trajectory was accompanied by increasing deficits in the balance of trade in manufacturing goods, certainly fostered by the appreciation of the currency in real terms until 2012 and the surplus of nonmanufactured goods favored by the increasing terms of trade (Figure 4).

Terms of trade (average 2006 = 100), 2003–2016 (data from Banco Central do Brasil, 2017).

Even with a subsequent reverse in the appreciation trend, the profitability of exports increased only slightly. In this setting, industrial output first stagnated and, from 2013, began to fall. Meanwhile, retail sales and the import coefficient of industry inputs kept growing, indicating a replacement of domestic production by imports both in final and intermediary manufacturing goods (Paula, Modenesi, and Pires, 2015).

The negative results regarding structural change were apparent in a deterioration of external solvency in the medium and long term, since the growth rate of net foreign debt was higher than that of exports. The situation was worse with regard to exports of manufactured products, which are characterized by lower price volatility and higher income-elasticity than commodities. From this perspective, the country’s capacity for generating foreign currency to serve its foreign debt decreased during the period under analysis. In contrast, external liquidity—vulnerability in the short term—improved not only because of the policy of accumulating foreign exchange reserves but also because of the reduction of the currency mismatch associated with a change in the composition of short-term gross foreign debt. This change stemmed from two simultaneous trends: a decrease in foreign debt and an increase in foreign portfolio investment in the domestic market (Biancarelli, Rosa, and Vergnhanini, 2017). Further, the increasing current-account deficit between 2009 and 2014 was financed almost fully by foreign direct investment, which in 2015 and 2016 was higher than the foreign deficit. Thus, in the short term, Brazil did not face external constraints, which explains, along with the dirty floating exchange-rate regime, why a balance-of-payments crisis did not break out despite the huge outflow of foreign portfolio investment amid a deep economic and political crisis (Banco Central do Brasil, 2017).

Economic and Social Policies Under the PT Governments

Macroeconomic Policies

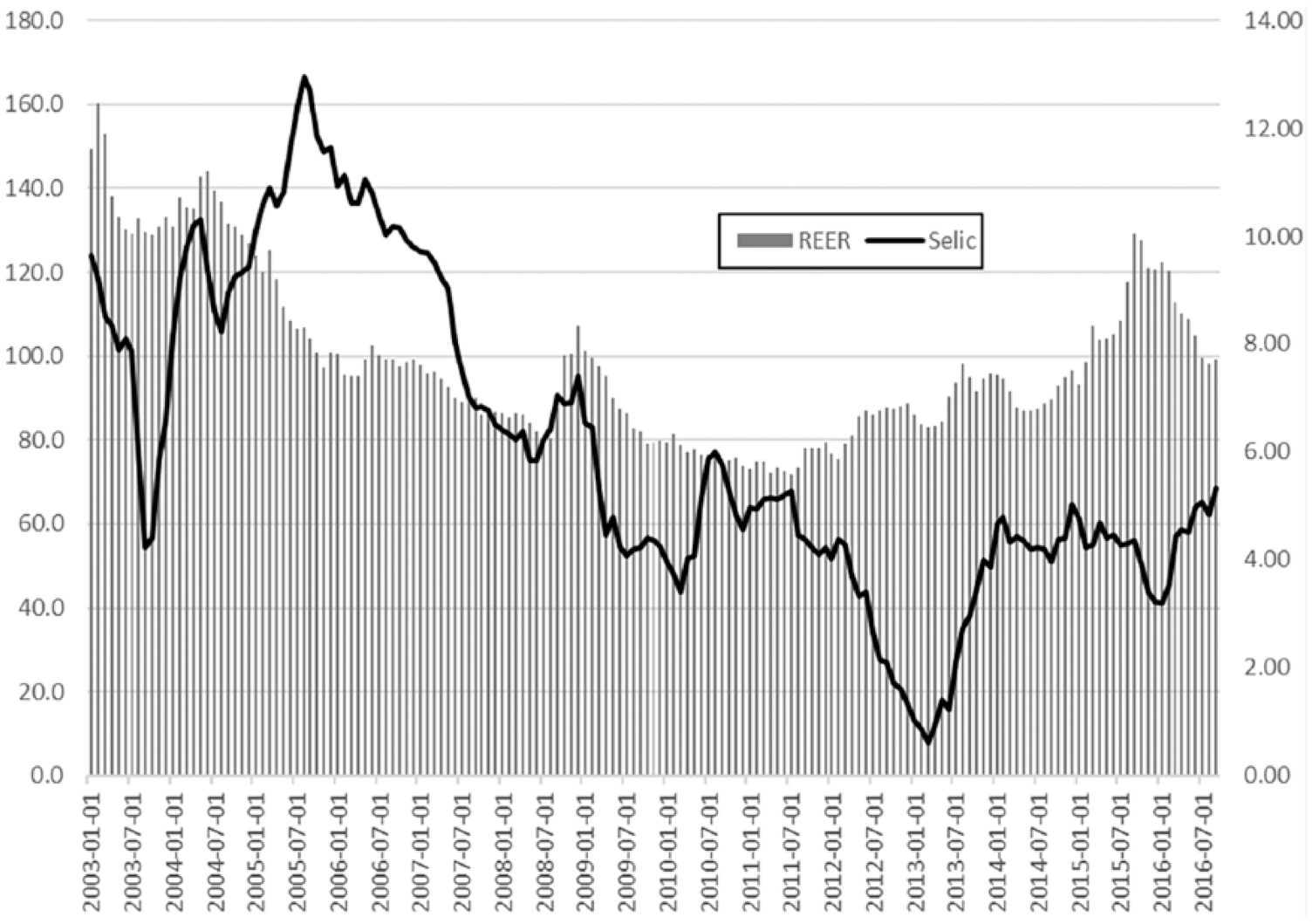

The first term of Lula da Silva’s government (2003–2006), following a confidence crisis in 2002 with a massive speculative attack on the currency, was characterized by the continuity of the tripod of macroeconomic policies adopted after the 1999 currency crisis (inflation targeting, primary-surplus targets, and a dirty floating exchange-rate regime). Within this framework, fiscal and monetary policies remained mostly orthodox, characterized by a large primary surplus and the maintenance of a high (albeit decreasing) real interest rate, while the currency appreciated gradually (Figures 5 and 6).

Policy rate (SELIC interest rate [percent annually]) and real effective exchange rate (June 1994 = 100) (data from Banco Central do Brasil, 2017).

Exchange rate (R$/US$), January 1999–August 2016 (data from Banco Central do Brasil, 2017).

In a positive external environment in terms of trade and capital flows (see Figure 4) the high interest rate stimulated speculative operations through portfolio investment and foreign exchange derivatives. These operations along with the current-account surplus resulted in significant currency appreciation. The interventions in the foreign exchange market of the monetary authority in 2005 did not curb this appreciation but resulted in the buildup of foreign exchange reserves. The so-called precautionary demand for reserves contributed to the decrease of net public foreign debt and improvement in the country’s eternal liquidity. Moreover, in this period bank credit to the private sector recorded significant growth, stimulated, among other factors, by the implementation of payroll-deductible credit operations, which reduced bank risk and, consequently, the cost of loans to households. From 2006 on, credit from public banks to corporations also gained momentum, especially when in 2007, the first year of Lula’s second term, a huge program of public investment in infrastructure called the Programa de Aceleração do Crescimento (Growth Acceleration Program) was launched. Thus, even before the contagion effect of the global financial crisis, this term was characterized by greater state activism (Singer, 2015).

The Brazilian authorities responded to the global financial crisis by adopting a number of countercyclical measures (Barbosa, 2010; Paula, Modenesi, and Pires, 2015): (1) to avoid the spread of the credit crunch, the Central Bank of Brazil adopted a series of liquidity-enhancing measures and intervened in the foreign exchange markets; (2) the state-owned banks were encouraged to expand their credit operations to compensate for the deceleration in the credit supply by private banks (see Figure 2); and (3) the Ministry of Finance undertook fiscal measures to stimulate aggregate demand. The countercyclical reaction was possible, to a large extent, because of the policy space created by the government’s shift toward a net creditor position in foreign currency. Consequently, the currency devaluation favored public finance.

In the context of the quick recovery of the economy and a new “twin boom,” Brazil again faced huge short-term inflows boosted by a still high differential between domestic and foreign interest rates. As the Central Bank resumed the exchange-rate policy adopted before the crisis, Brazil’s currency recorded a huge appreciation in 2009 (see Figure 5) and, the Ministry of Finance started imposing regulations on capital flows, starting with a tiny financial transaction tax on foreign portfolio investments in October 2009. Soon these regulations were strengthened with the first measure targeting foreign exchange derivative operations and administrative controls. Moreover, the Central Bank of Brazil adopted macroprudential regulations to curb the domestic credit boom (Paula, Modenesi, and Pires, 2015; Prates and Fritz, 2016).

In mid-2011, during Rousseff’s first term, a gradual change was introduced for what the government itself called the “new macroeconomic matrix,” a set of countercyclical measures for boosting growth in the context of the worsening of the euro crisis and increasing the competitiveness of a Brazilian industry damaged by years of currency appreciation and increased competition in the foreign markets after the global financial crisis. The regulatory toolkit for the spot and derivatives foreign exchange markets was broadened because the previous measures had only mitigated the currency appreciation trend underlying the deterioration in competitiveness of Brazil’s manufacturing sector in both foreign and domestic markets (Prates and Fritz, 2016). It was completed by a progressive reduction of the policy rate. At the same time, as a precondition for changing exchange-rate and monetary policy without jeopardizing price stability, fiscal policy was tightened in the first half of 2011 (Cagnin et al., 2013). The interplay of the new foreign exchange regulations, the relaxation of monetary policy, and the increase in the risk aversion of global investors resulted in the intended depreciation of the Brazilian currency (see Figure 6). Besides the change in the interest and the exchange rate, the government launched a wide range of instruments that favored the domestic manufacturing sector and were intended to dampen inflationary pressures in face of the currency depreciation: a nominal freeze of relevant public tariffs (such as on energy and gasoline), the use of state-owned banks to reduce bank spreads, and tax exemptions. It is worth mentionng that in the first year these measures did not change the overall fiscal policy stance (Mello and Rossi, 2017; Paula and Pires, 2017). In April 2013, however, because of an increasing inflation rate, the Central Bank began gradually increasing the policy rate (see Figure 5) and removed regulations on foreign exchange operations as a result of signaling by the Federal Reserve that its quantitative easing policy would soon be withdrawn. At the same time, the Brazilian government further increased tax exemptions and tried to intensify investment in infrastructure. Moreover, affected by the decline of oil prices and the first effects of Operation Car Wash, 7 Petrobras reduced its investments, and this had a strong impact on overall investment (Mello and Rossi, 2017). Compared with the policies launched to counter the contagion effect of the global financial crisis, the countercyclical fiscal policies implemented in 2012–2014, with the use of tax exemptions instead of public expenditures, were very limited and had little aggregate impact on production and employment. The same holds for public investment, which had been significantly higher in 2006–2010.

In 2015, after the reelection of Dilma Rousseff, the government shifted its economic policy somewhat radically toward a more orthodox stance. The main aim was fiscal adjustment mainly in public expenditures, which was understood as fundamental for restoring actors’ confidence as a precondition for economic recovery. For this purpose, the government committed itself to a primary fiscal surplus of 1.2 percent of the GDP, implementing a set of measures to reduce public expenditures (mainly through the budget), and readjusted monitored prices (energy and oil), while the Central Bank further increased its policy rate from 10.92 percent annually in October 2014 to 14.14 percent in August 2015. As a result of the severe devaluation in 2015, the bank had to intervene in the foreign exchange market to reduce exchange-rate volatility and offer exchange-rate hedging to private actors through swap operations (Carneiro, 2017; Paula and Pires, 2017).

These efforts at fiscal adjustment failed. Fiscal revenues dropped dramatically in 2015, and the Ministry of Finance had to revise its fiscal targets. As a result of the recession and increasing payments, the nominal public deficit increased even further in 2015. Net public debt over GDP, which had recorded its lowest level during the period under analysis in 2013 with 30.5 percent, again increased steeply (to 46 percent of GDP in 2016). Gross debt increased even more, from 51.5 percent to 69.6 percent over GDP in the same period. This means that the government’s assets (mainly foreign reserves and loans to public banks) shrank in relative terms, in contrast to the situation in 2010–2014, when they rose significantly. At the beginning of 2016, Nelson Barbosa, the new finance minister, announced his strategy of fiscal consolidation, which, among other things, was expected to reverse the upward trend of public spending that, contradictorily, compromised the capacity of the Brazilian state to implement public policies in the long term (Paula and Pires, 2017). The spread of the political crisis virtually paralyzed the government, making impossible the adoption of any economic policy agenda until the impeachment of President Rousseff in 2016.

Industrial Policies

After a long period of almost complete absence of industrial policies, three programs of industrial policy were launched during the period analyzed here. Industrial policy oscillated between two types of strategies: (1) prioritizing high-tech sectors and selecting “national champions” in industries with comparative international advantages such as agribusiness, steel, and mining and (2) favoring the sectors damaged by strong foreign competition (see Almeida and Novais, 2014; Kupfer, 2013).

The first program, the Industrial, Technology, and Foreign Trade Policy, launched in 2004, aimed to address Brazil’s vulnerability, emphasizing an active policy of adding to exports value based on innovation. To this end, three areas were identified: (1) incentives for strategic sectors (capital goods, software, semiconductors, and pharmaceuticals; (2) horizontal actions to stimulate innovation and technological development, international integration via exports, and modernization of the institutional environment; and (3) priority for biotechnology, nanotechnology, and renewable energy.

With the rapid and intensive improvement of Brazilian terms of trade from 2004 on, which resulted in substantial surpluses in the trade balance, priorities for industrial policy changed. The Productive Development Policy was launched in May 2008 in a context in which Brazil had received investment grade because of its sound economic fundamentals (low inflation, fiscal surplus, etc.). The main objective was to foster growth and productive investment in the domestic market. For this purpose, the program set ambitious investment goals (from 17.6 percent of GDP in 2007 to 21.0 percent in 2010) and an increased participation of Brazilian exports in world trade.

The changing global scenario led to the launch in August 2011 of a third program, the Greater Brazil Plan, which was continuously modified in the following years in view of the worsening global economic conditions. The initial objective of the plan was the productive and technological consolidation of value chains, but the intensification of foreign competition in domestic and foreign markets forced its direction toward the defense of the domestic market and the recovery of systemic competitiveness conditions. In line with the “new macroeconomic matrix,” the government adopted compensatory measures to minimize the impact on domestic manufacturing output of the increasing penetration of imported goods into Brazil, including the expansion of subsidized credit by the Brazilian Development Bank and further tax and social security payment exemptions, causing significant fiscal costs with limited effects on industrial production.

In his assessment of industrial policies in the period analyzed, Kupfer (2013) concludes that these remained an auxiliary element of macroeconomic policy that was often in conflict with it, its effectiveness reduced by the strong currency appreciation until 2011 and very high interest rates.

Social Policies

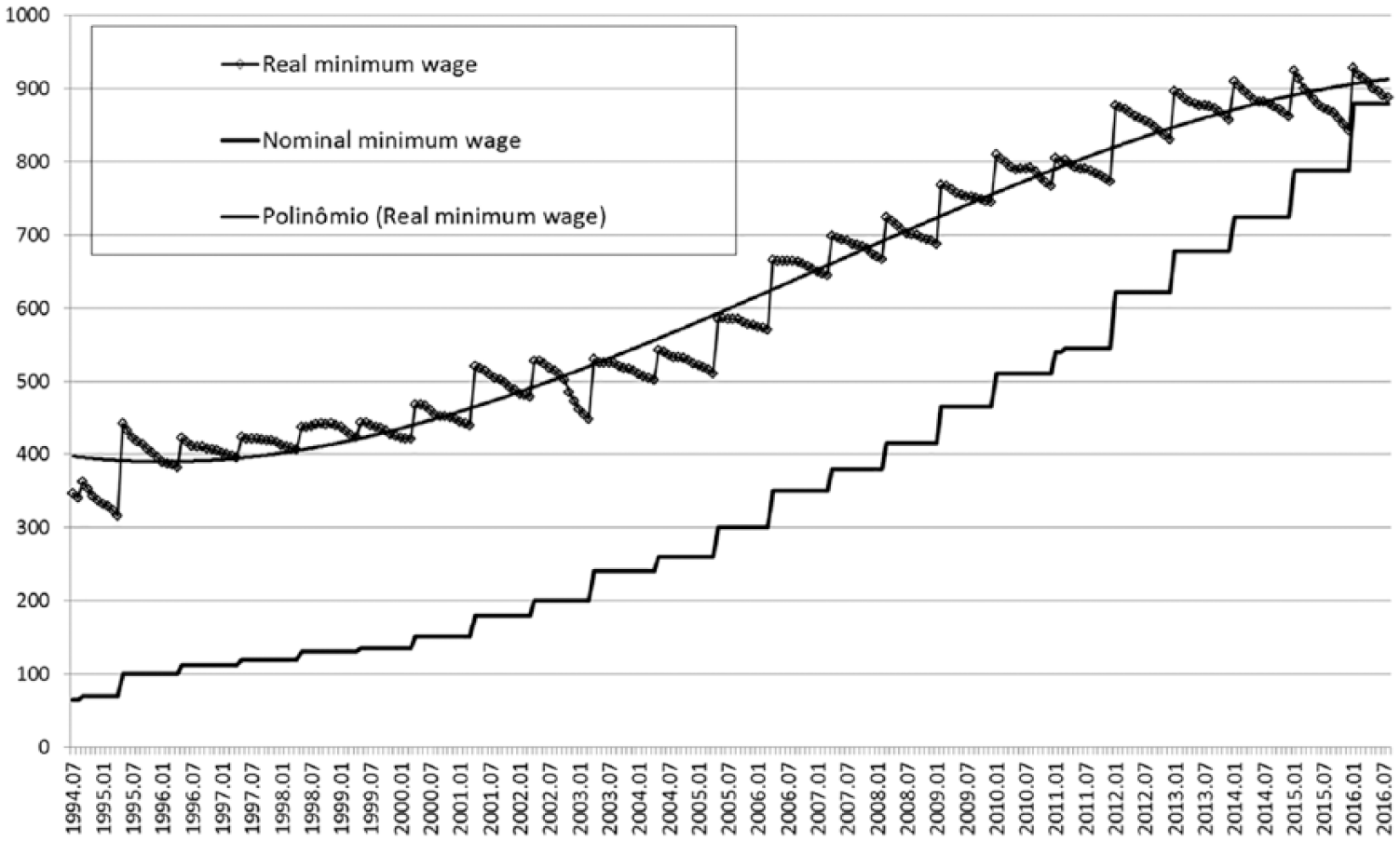

Highly active social policies were one of the major features of policy orientation during the period examined. These policies were crucial for achieving the aim of the income redistribution, which was to foster domestic consumption. The two main factors that contributed to improving income distribution were the huge increase in the minimum wage (66.9 percent in real terms from December 2003 to December 2014) and income transfers in the form of an increase in pension benefits and the Bolsa Familia program (Figure 7).

Minimum wage, nominal and real, deflated by national price index (IPEA, 2017).

The most important instrument was certainly the increase in the minimum wage. The rule for adjusting that wage adopted during this period was to add the inflation of the previous year and the GDP growth rate of the year before that. In this way, high economic growth resulted in high real wage increases, since the wages of low-skilled workers (both public and private, formal and informal) and public pension payments were linked to the minimum wage. 8 In this institutional setting, minimum wage policy turned into a powerful redistributional tool. Another social policy instrument that gained high national and international visibility was the conditional cash transfer program Bolsa Família. It was designed to combat extreme poverty and achieved almost complete coverage of very poor families with children of school age at very low cost.

Tax reform was completely absent in the area of redistribution policies. While in the Organization for Economic Cooperation and Development countries taxes are responsible for the bulk of public redistribution, in Brazil the tax system even had a slightly regressive effect (Lustig, Pessino, and Scott, 2014).

Varieties of Developmentalism Under the PT Governments

Assessing the policies adopted during the four PT governments, we find significant changes over time. Although for some aspects exact and uniform periodization is rather difficult, we also find that these changes were largely associated with the external context. We have earlier identified three phases in that context, and we use them here in developing a typology of the policies that helps to uncover the fundamental flaws of the macroeconomic foundation of redistributive policies for most of the period analyzed (Table 2).

Typology of Policies by Phase

Note: ORT, orthodox; SD, social developmentalist; ND, new developmentalist. Parentheses indicate that the policy does not entirely follow a particular strategy, only being influenced by it.

The last phase (2011 to mid-2016) is split into two subperiods in view of the changes in economic policies in Rousseff’s second term. These were largely shaped by domestic factors, especially the political confidence initiated in her first term with the street protests of June 2013 and fostered in her second term by a mix of economic crisis and corruption scandal. Operation Car Wash contributed to the loss of a political majority and of voters’ backing, leaving the government with little support to fend off a power grab by political rivals who impeached President Rousseff not on charges of corruption but on charges of manipulating the federal budget (the so-called creative accounting that also took place in former governments).

The first phase, from 2003 to September 2008, was marked by an orthodox macroeconomic policy. Moreover, following the path of other emerging economies, from 2005 on the favorable international context had enabled Brazil to adopt the precautionary strategy of accumulating foreign exchange reserves, which had a key role in reducing its vulnerability, being consistent with both varieties of developmentalism. This policy stance was mixed with increasing elements of social developmentalism, in particular the formation of a market of mass consumption that was boosted by increasing the minimum wage in real terms, stimulating private credit, and increasing households’ purchasing power in a setting of lower prices of imported goods due to currency appreciation. However, since industrial policy was mostly oriented toward strengthening exports, this policy field can be characterized as new developmentalist.

A second phase, from October 2008 to 2010, was the time when “we were all Keynesians.” In the context of the contagion effect of the global financial crisis, the Lula government in its second term launched a more flexible fiscal policy, including an increase in public investment that started in 2007 with the Growth Acceleration Program, promoted a countercyclical role of state-owned banks, and boosted social policies. These measures, consistent with social developmentalism, were taken with some pragmatism and departed from what we have called orthodox policies before the crisis. Once the economy had recovered, the government adopted price-based capital controls and macroprudential regulations on the credit market to curb, respectively, currency appreciation and the credit boom. Although these two types of financial regulation (Ocampo, 2012) were to some degree part of the conventional toolkit of macroeconomic recommendations after the 2008 global crisis (Blanchard, Dell’Ariccia, and Mauro, 2010), they fit within both new and social developmentalism (e.g., Rossi, 2014).

The third phase was characterized by strong oscillation in macroeconomic policy between orthodoxy and developmentalism, and classification becomes especially difficult. One could interpret the so-called new macroeconomic matrix as influenced by new-developmentalist prescriptions because of the initial currency devaluation and the decreasing policy rate backed by fiscal austerity, but other elements of this approach were absent, especially with regard to fiscal policy in 2013–2014. This policy was not only increasingly expansive but also supply-side-oriented instead of focusing on the public demand side. Indeed, public investment decreased in 2010–2014. Then, they were even criticized by social developmentalists (Bastos, 2015). However, from 2013 on, a more orthodox approach in terms of monetary and exchange-rate policies aimed at inflation stabilization was resumed. At the same time, in the first Rousseff government, the pillars of social developmentalism of the first two phases—minimum wage increases, stimulus to private credit, and an active role of public banks and of industrial policies—were maintained. Thus this period was characterized by a mix of social and new developmentalism, as Singer (2015) also suggests. 9

As we have pointed out, the second Rousseff government (2015–2016) was marked by a radical shift, with the implementation of orthodoxy mainly in the field of fiscal and monetary policies. The Central Bank implemented a strategy for reducing volatility and providing a hedge against exchange-rate risk but did not intend to be involved with the determination of the exchange rate. In terms of social policies there were no significant changes. As we have seen, the rule for minimum-wage readjustment remained in place, although high inflation in 2015–2016 and low growth in the years before limited real wage increases.

Conclusions

Our assessment of the policies of the PT-led governments in Brazil shows that we cannot label this period either completely orthodox or neoliberal or entirely developmentalist. Indeed, we find our first hypothesis confirmed: already at the conceptual level we can identify more than one recent variety of developmentalism, the two most relevant to the economic debate being the social and the new. They share the aim of combining sustained economic growth with productive restructuring and income distribution by giving the state an active role. However, they diverge with regard to the priority given to policies for achieving this aim. The new-developmentalist approach centers on the management of a competitive exchange rate to achieve an export surplus in manufactured goods and job creation in the industrial sector. The social developmentalist variety favors redistributional policies to foster domestic demand and diversified domestic investment. Thus, answering the question whether the PT governments were developmentalist requires consideration of which variety of developmentalism is involved.

Our second hypothesis is also confirmed. Some of the policies applied were more explicitly social developmentalist, among them the social policies and such economic policies as public investment and such financial policies as access to credit for lower-income households and the outstanding role given to public banks. The core of new developmentalist policies—an undervalued currency supported by fiscal austerity, low interest rates, and capital controls—was applied only for a rather limited period of time during the first Rousseff government. Yet the macroeconomic policies applied followed the current orthodox prescription during the first phase. There is no clear pattern of macroeconomic policies’ shifting toward a more developmentalist stance. Rather, the reaction to the spillovers of the global financial crisis was shaped by countercyclical policies that were the global standard in this context, and the third phase was characterized by a mixture of all types of policies. This, for instance, applies to monetary policy from the second half of 2012 on and especially to the policies of Rousseff’s second term, which in its struggle against a widening and mutually nurturing economic and political crisis was dominated by orthodox policies.

This makes our third hypothesis more significant than we had expected. We encountered a number of difficulties in finding clear criteria in terms of both periodization and classification, since the changes especially in macroeconomic policies were very frequent. Certainly, policies should not be expected to be a simple result of theoretical considerations, but they are highly dependent on institutional path-dependency and concrete circumstances in interplay with specific interests. It is clear, however, that the international context shaped policy options over the period. In the third phase, the swift macroeconomic policy shifts certainly had to do with necessary adjustments to a volatile international environment. Beyond this, however, they may also reflect accumulating domestic conflicts among dominant economic actors over redistributional aims and outcomes of public policies, which grew acute with the growth of the political corruption scandal involving the governing parties.

Footnotes

Notes

Daniela Magalhães Prates is an associate professor of economics at the University of Campinas and a researcher with Brazil’s National Council for Scientific Development. Barbara Fritz is a professor of economics at the Institute for Latin American Studies of the Freie Universität Berlin. Luiz Fernando de Paula is a professor of economics at the Federal University of Rio de Janeiro, a National Council for Scientific Development and Foundation for Research Support of the State of Rio de Janeiro researcher.