Abstract

This study examines the circumstances under which public organizations establish easy performance goals, analyzing nationwide data collected from cabinet departments in central and local government agencies in South Korea. Several factors have been identified as contributing to the tendency of public organizations to set easily achievable goals. Firstly, local governments tend to establish less challenging performance standards compared to central government agencies. Secondly, public organizations with higher financial resources per employee ratios are inclined to set easy performance goals. Lastly, the presence of a strong innovation-oriented culture or transparency requirements decreases the likelihood of setting easy performance goals.

Introduction

Goal setting is important to ensure the success of performance-based management, which has now become widespread in the public sector. It is the first step in a performance management process that embodies an organization’s mission with measurable indicators and determines the degree of progress or improvement it aims for (Fortuin, 1988; Star et al., 2016). Performance targets as outcomes of this process should be specific enough to instruct employees on what kinds of work efforts to make and difficult enough to stimulate them to put significant effort into their work. Specific and challenging goalsi increase worker motivation of (Locke & Latham, 1990) thereby reducing employee’s turnover intentions (Jung, 2014) as well as boosting the chance of team (Van der Hoek et al., 2018) and organizational (K. G. Smith et al., 1990) success.

Nevertheless, performance targets often fall short of optimality. Stakeholder theory suggests that organizational decision making is a political process in which various stakeholders inside and outside the organization strive to exert influence (Freeman, 1984). From this perspective, performance goal setting in public organizations is a dynamic process marked by competition among various expectations and demands, rather than a static, organized, and rational decision-making process (Erridge et al., 1998; Modell, 2005). Which stakeholder’s agenda will most likely be reflected in the outcome depends on the numerous factors that affect the power landscape among stakeholders (Brignall & Modell, 2000).

According to the classification of Mitchell et al. (1997), a public bureaucrat is “dangerous stakeholder” who has power and urgency in setting performance goals in the public sector, whereas citizens or the overseeing agency on their behalf are “discretionary stakeholders,” who only have legitimacy.. The information asymmetry between the two actors engenders a power imbalance (Duff & Wohlstetter, 2019). At lower organizational levels, officials can justify their choice of performance goals by, for example, using unfavorable policy circumstances as a justification. This power discrepancy may be heightened when public organizations take the initiative by submitting performance plans based on management by objectives (MBO) that encourages bottom-up participation (Thompson et al., 1981). They also are stakeholders with urgency. Compared to oversight from the central government, lower-level government units (e.g., bureau) have greater information on pressing needs that require immediate intervention in their specific policy areas than do higher level officials. Likewise, local governments have more information on their jurisdictions, and their voice is likely to have greater influence over their performance goals.

Agency theory suggests that public organizations will game performance management unless there is an adequate alignment between public bureaucrats’ and citizen interests;yet, the sectoral characteristics of public organizations often make this alignment difficult. Rule-based bureaucratic control serves to discourage innovation necessary for performance improvement (Lee & Moon, 2017) and public organization’s response to this accountability conflict likely results choosing easy performance objectives. In doing so, public bureaucrats can avoid public criticism with less effort (Power, 2004; Propper & Wilson, 2003). Increased competition due to NPM (New Public Management) can add to this opportunistic motivation.

Public organizations can set easy performance targets in several ways. A considerable part of performance indexes include increases over previous performance. In this case, a “ratchet effect” likely takes pace: public organizations tend to lower the target amount of increase in a given year to avoid excessive burden for additional improvement in the following year (Casas-Arce et al., 2018). Another example is the “tunnel vision effect” in which public organizations choose performance indicators that benefit themselves and focus only on these indicators, regardless of how important these indicators are (P. Smith, 1995).

These unintended consequences indeed have been reported. Van Thiel and Leeuw (2002) pointed out that there was a disproportionate emphasis on narrow local objectives and performance measures that are easily quantifiable, irrespective of organizational mission accomplishment. Hood (2002) similarly maintained that public managers often evade control by colluding with politicians, developing phony performance standards, and even fabricating performance data. Bischoff and Blaeschke (2016) described these dysfunctional practices as “window dressing,” meaning that public organizations tend to focus on legitimating rather than improving their performance.

However, the equilibria among stakeholders are dynamic rather than static, as organizational, political, and environmental conditions interact to enhance or undermine individual stakeholder’s relative power (Brignall & Modell, 2000). It is in this vein that Murphy and Cleveland (1995) suggested a model for examining setting performance goals that includes variety of socio-political factors.. Nevertheless, the effects of these factors on performance goal setting in the public sector have not been sufficiently studied. Rather, performance goal setting typically has been examined in light of motivational or performance effects (Locke & Latham, 1990). For instance, scholars have explored whether and how goal clarity (Jung, 2014; Van der Hoek et al., 2018), goal difficulty (Jong, 2019), and goal measurability (Verbeeten, 2008) are related to positive outcomes to individuals, teams, and organization. Similarly, Jung and Ritz (2014) examined whether the collaborative nature of goal setting affects employees’ organizational commitment. Ayers (2015) found that the extent to which performance goals align with employee’s understanding of organizational goals significantly affects performance measured by PART program scores.

With this background, this study examined the effects of several factors in allowing public officials to set easier performance objectives than they can achieve. We did this with data obtained from a nationwide survey of South Korean government employees. South Korean performance evaluation consists of two parts: self-evaluation and tspecific evaluation. The self-evaluation is performed by the agencies or departments being evaluated evaluation: they not only propose their performance targets, but also assess their own performance results. The specific evaluation also utilizes the performance index agencies and departments developed (Yang & Torneo, 2016). The major target of criticism is the self-evaluation (Rah, 2003; Park, 2004), which provides considerable room for the agent (i.e., the target of evaluation) to act opportunistically. The selection of performance indicators has also been criticized (Rah, 2017; Shin, 2010).

In what follows, we first will describe and provide the rationale for factors affecting goal easiness and suggest relevant hypotheses. Next, we discuss the methods for exploring the hypotheses, before turning to the results. . We believe that the results of this study will have implications for both the theory and practice of performance management in the public sector.

Theory and Hypotheses

Theoretical Foundations

The discrepancy between organizational mission and performance indicators is observed in both the private and public sectors. Yet sectoral features make it more common and more frequent in the public sector, for several reasons.First, the missions of public organization refect diverse public values that frequently contradict each other. Employees can justify their performance improvement proposal by appealing to an eclectic set of public values, whereas those in a private organization doing the equivalent task must convince shareholders that their proposal can increase “profit.” Second, the missions of most public organizations are articlated as abstract and equivocal values (Chun & Rainey, 2005), providing public agencies with greater leeway to translate them into specific performance indicators (Fukuda-Parr & McNeill, 2019). Third, public organizations serve multiple principals, such as service users, taxpayers, and politicians at different levels of government (Dixit, 2002), which also provides public organizations with more diverse targets to appeal to gain political support for their choice at typically low risk.

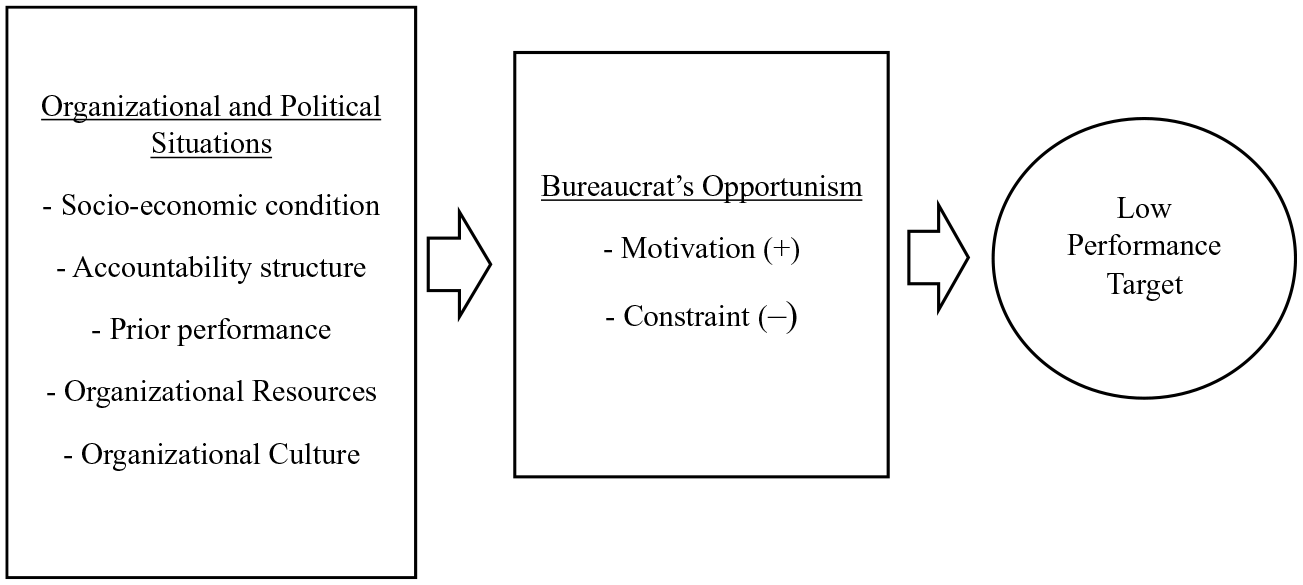

A variety of factors may influence an agent’s opportunism (Bodrov, 2014; Paswan et al., 2017; Pletnev & Kozlova, 2022). The interactions among organizational, political, and environmental conditions can provide the agent (i.e., a public bureaucrat) with advantages or disadvantages in proposing easier performance goals (Murphy & Cleveland, 1995). These conditions do so by either strengthening the motivations to make a choice enhancing the agent’s own interests (e.g., lack of incentives) or weakening the constraints to do so (e.g., monitoring efficiency). The hypotheses here consider either or both of these factors. See Figure 1.

Research framework.

Hypotheses

Municipal agencies are more likely to set easy performance goals than central government agencies. This can be the case for at least three reasons. First, the nature of their tasks differs. The major tasks of local governments are to deliver public services to their constituents, while that of the central government mainly is to plan and design national policies. Although some important decisions are devolved to municipalities, much of the work local governments undertake is devoted to implementing public service programs. Enhancing performance implementatimg programs tends to require increasing inputs, that is increasing personnel and financial resources. Accordingly, “input” (e.g., the total extra working hours of employees) and “output” (e.g., the number of the events participating citizens) measures take up a considerable portion of South Korean local government performance index (J. Lee, 2008). To the contrary, the performance index for the central government consists of a greater number of “outcome” indicators such as citizen satisfaction, corruption index, and reduced processing time for import and export cargo (Korean Institute of Public Administration, 2006). In order to enhance performance in planning and designing a program, the central government employees are under greater pressure to come up with novel ideas, which need not require greater input of organizational resources. For this reason, municipalities will feel more burdened by pressure to improve performance and thus be more inclined to set easier performance goals.

Second, local governments usually face greater competition with other government agencies than the central government. Local governments compete with other similar cities and provinces to attract residents (Hoyt, 1990). The decline in the population of younger residents has been a major challenge for many local governments, especially since one-quarter of the national population lives in the metropolitan area around Seoul and Kyeong-gi province. Considerable variance in demographic composition and population density gives other local agencies with convincing grounds for setting lower goals than the central government that spans the whole country.

The South Korean local government system consists of eight metropolitan cities and nine provinces, and a much greater number of younger residents, who have different needs and demands for governmental services from the older, lives in cities than provinces, and the population density is also much higher in cities than provinces. These differences are taken into consideration developing performance index: some performance indexes are standardized, but only across cities and across provinces. However, individual cities and provinces are still significantly different from one another depending on how close they are to major cities, which are not usually taken into consideration. Many local governments may use this unconsidered difference in their favor and make an excuse for setting low performance standards.

Third, the quality of public service is easily observable by the public as it has a direct impact on their life. Moreover, being closer to residents, local governments are likely to be held more accountable to their constituents (Seabright, 1996). In this vein, elections are more effective accountability mechanisms for local government (Hong, 2017). In contrast, the central government has departments with discrete functions that work in often quite different fields and operate in considerably different environments. The public may not be able to tell with confidence whether declining performance of one cabinet department was due to its inefficiency or to societal and economic changes that affected the field as a whole. Given this, such units are relatively free from political pressure from citizens. As a result, the central government agencies are is less pressured to increase performance compared to those in local governments, and hence, have relatively weaker incentivesto lower performance standards.

Hypothesis 1. Municipal government agencies are more likely to set easy goals than the central government agencies.

Prior performance also may explain inclinations toward easier goals. Hong (2019) did informative research on this topic. He found that the performance goals of those receiving poor performance grades in the previous two years were affected. Although the implications of his findings need to be interpreted in context, a key takeaway is that those who received poor performance grades have a stronger motivation to be more defensive. It could be that they lower standards to reduce the risk of receiving low performance grades again. This is all the more likely if they think their low grades in previous years were because their performance goals were too ambitious. In addition, many performance indicators measure the degree of improvement against previous years. Hence, lowering performance standards provide an additional advantage in the following year.

Hypothesis 2. Those government agencies that received low performance grades in the previous year are more likely to set easy goals than those that did not.

The barriers to improving performance may induce organizations to lower standards. Public organizations are viewed as being more bureaucratic than private organizations (Boyne, 2002). Public organizations tend to be constrained by more requirements to adhere to rules and regulations than their private sector counterparts. As a result, for example, street level officials in social services have been to view accountability and performance improvement as two distinct concepts (Hwang & Han, 2020), implying that the two sometimes contradict each other (Chan & Gao, 2009). This type of conflict may produce frustration among individual employees who are willing to improve their performance.

In this vein, scholars frequently have argued that public sector adoption of performance management systems should be accompanied by reforming their work processes. Ammons and Roenigk (2015), for instance, contend that successful performance management depends on devolution of authority. Behn (2002) similarly observes that the lack of flexibility is a major hurdle that makes performance management unsuccessful. More often than not, however, the pressure to improve performance is not accompanied by relaxed bureaucratic requirements. As Behn (1998) puts it, procedural rigor is the single most important “golden rule” for public organizations. According to Ammons and Roenigk (2015), only 30.3% of field supervisors had decision-making discretion as to decision making in implementing performance management. Therefore, those managers who feel pressured to improve performance without necessary provision of discretion may react by lowering performance standards.

Hypothesis 3. Those organizations faced with institutional barriers to improving performance are more likely to set easy goals than those are not.

Another source of barriers involves the lack of financial resources. The distribution of financial resources in public organizations is inherently a political process. Many departments in public organizations or agencies in the central government compete for securing greater shares of the budget (Schick, 2008). Those who lose this competition and are left with insufficient financial resources put in a disadvantageous situation ; they may be likely to respond by lowering performance standards. Huizinga and de Bree (2021) similarly note that regulatory agencies that experienced serious budget cuts tended to “produce numbers but poor outcomes” (p. 891).

Hypothesis 4. Those organizations suffering insufficient financial resources are more likely to set easy goals.

Organizational characteristics also can affect performance goal setting. Culture and institutional arrangement may lead to easy performance goals. An organization with a culture of innovation-seeking will set goals that are challenging enough to motivate its employees to propose new ideas, since such goals often cannot be accomplished with current work methods. This will not only push employees not willing to seek innovation, but also stimulate those who hope to innovate and who may see the challenge as an opportunity to show others that their worth (VandeWalle et al., 1999). Challenging goals also may induce some employees to work harder and to persist even in when facing difficulty (Locke & Latham, 1990); continuous efforts to innovate also may facilitate learning (Payne et al., 2007).

A culture of innovation tends to vary with agency mission. Public organizations in which research and development is critical for accomplishing their missions, for instance, tend to emphasize innovation. At the same time, culture may depend as well on the managerial philosophy of top management personnel. Some managers tend to set challenging goals to invigorate organizations. Crossley et al. (2013), for instance, found that proactive managers who pursue innovation and better achievement tend to set challenging goals. Thus, those organizations with innovation cultures or with innovation-oriented managers trying to build such a culture will tend to seek challenging performance goals.

Hypothesis 5. Organizations with innovation cultures are less likely to set easy goals.

In contemporary public organizations, transparency is a key mechanism of ensuring accountability to the public. Allowing citizens to look closely into the work process encourages public officials to perform their tasks more responsively. Organizations may differ the degree of transparency of setting performance goals settings. In South Korea, all government agencies must have committees responsible for overseeing the performance evaluation process that include citizens as members. In practice, however, only about 80% of municipalities have such committee in place, and on average they hold 1.4 meetings each year (Park, 2004). In addition, levels of transparency also depend on how active citizens on such committees are i monitoring goal setting. Often participants lack expertise to oversee bureaucrats; moreover, terms of committee service often are limited due to concerns about possible collusion. In sum, committee activities may be perfunctory in some local governments.

Another way to ensure transparency is through disclosure of public information. South Korean laws mandate that every government agency post online annually certain types of public data, with other data provided upon citizen request. Such requests, however, are reviewed by an internal committee, and they are not always approved. Lack of approval can be justified, for instance, by the inherent duality of missions in public organizations; public agencies can use other important public interests that they also must protect as a reason for refusing to disclose public information. For instance, if a citizen requests documents detaling the procedures for performance goal setting, lack of approval may be easily justified on confidentiality grounds, particularly when citizen representatives took part in the relevant committee meetings. In addition, those agencies with highly professional tasks that the general public does not have appropriate technical knowledge to interpret or evaluate may be relatively free from public scrutiny. In this context, some public organizations can be more or less free to choose easier performance goals, in effect taking advantage of technicality and protection of public interests, and better able to set easy performance goals.

Hypothesis 6. Organizations with greater transparency requirements are less likely to set easy goals.

Methods

Data and Samples

To examine these hypotheses, we relied on a survey of public employees in South Korea. The survey was administered by Hankook Research, one of the largest survey research agencies in South Korea, commissioned by the Public Performance Management Research Center (PPMRC) at Seoul National University. The survey contains a series of questions related to performance management in South Korean government agencies. This survey was conducted twice, in 2016 and 2017, and we combine the data from both surveys. The 2016 survey was conducted from November 2016 to January 2017, and the 2017 survey from November 2017 to February 2018.

Participants were selected randomly and proportionately using a stratified sampling framework based on agency size and paygrade. The sample is representative of the population on the size and pagrade criteria. In order to ensure that the final sample closely aligned with the stratified framework and minimized non-respondents, we contacted randomly selected respondents before mailing the questionnaires. Virtually all responded positively.

A total of 1,669 public employees from 47 government agencies participated in the survey in 2016, including those from 16 (of 18) cabinet departments, 14 bureaus (out of 27) under their jurisdiction, and 17 regional governments. The number of participants from central government entities was 1,014, while 655 worked in regional governments. The number of participants per agency ranged from 9 to 31. In 2017, 2,766 public employees participated, representing 231 different agencies. This included 509 participants from 17 regional governments and 2,257 participants from 214 municipalities. The number of participants per agency ranged from 8 to 31. Seventeen regional governments participated in both the 2016 and the 2017 surveys.

For this study, the unit of analysis is the organization, while the unit of measurement is the individual. We employed the average responses of individuals in each organization to tap the organization’s characteristics, assuming that their perceptions accurately reflected these attributes. This may not pose a major problem, primarily because the majority of the questionnaire items used inquire about the characteristics of the respondents’ organizations rather than about the individuals. For example, the item used to tap the dependent variable, ease of performance goals, asked about “performance management within your organization.” Moreover, it is important to highlight that we employed a stratified sampling method as opposed to a convenience sampling method to help ensure that participants were representative of their organization. We also included only those agencies where there was high level of consistency in individual responses. After examining intra-class correlations, we excluded agencies with notably lower coefficients.

In the 2016 and 2017 surveys, different employees from the same agencies may have participated. However, we do not believe that this introduced important selection bias for two main reasons. Firstly, we used identical questionnaire items in both the 2016 and 2017 surveys, ensuring consistency. Secondly, given the consistency observed in individual responses, utilizing the average score as a variable helped mitigate any potential selection bias resulting from different employees participating in the survey.

Table 1 summarizes the sample characteristics.

Sample Characteristics.

Measurement

Our measurement strategy was twofold. First, some of the variables are measured using questionnaire items selected from PPMRC survey questions. All questions were originally asked in Korean and then translated into English for presentation here, using Papago, a web-based translation service based on AI technology. We made minor revisions when necessary for greater clarity.

Since our target is organization-level variables, we averaged individual participants’ answers to obtain mean values for each government agency. As noted earlier, after assessing the degree of agreement among respondents, we included only those agencies with intraclass-correlation coefficients above .75 (Cicchetti, 1994). In the 2016 sample, 46 of 47 agencies are included, with 197 out of 231 municipal agencies from the 2017 sample, creating a final sample of 243 agencies. The average intraclass-correlation before we excluded agencies was .835 and .887 after.

Second, a number of other variables were based on published statistics from the South Korean government website. The sufficiency of financial resources is measured using these statistics. A control variable, partisan affiliation (of mayors in municipalities and the president in the central government), was measured based on online searches.

The unit of analysis is agency (i.e., organization), and responses were tapped using 5-point Likert scales unless otherwise noted.

The dependent variable – easiness of performance goals in an organization – signals the degree to which a public organization acted on opportunism rather than to best serve citizens. This variable might be measured in several ways. One way would be to use a quantifiable measure of the annual increase in achievement of an organizational goal, such as a 10% increase in the number of recipients of services. However, given possible variations in the socio-political circumstances of local governments or of central departments, this type measure cannot capture the actual ease of attainment. That in turn should be evaluated considering a range of relevant factors. Agency mployees would be better positioned to assess the easiness of their organization’s performance standard. In addition, South Korean public organizations confront different performance evaluations, using diverse types of performance indicators. Thus, it is difficult to develop measures to capture performance goal easiness effectively other than asking employees how easy their organizational performance goals are. As result, we posed the following question: “there is a tendency (in [your] organization) to set low performance targets?”

The first independent variable (in H1) is a binary variable tapping whether the given agency is or is not a municipality (yes=1, part of central government=0) .

The second hypothesis includes the second independent variable: the performance grade an agency received in the previous year. We used this to ask about the results of performance reviews conducted in the previous year (2015 for the 2016 survey, 2016 for the 2017 survey). We were not able to obtain specific data about the previous year’s organizational performance, so instead we used perceptions of both individual and department (or team) performance as proxies. Individual poor performance often has a spillover effect that undermines team performance (LePine & Van Dyne, 2001). In addition, an organization is a group of individuals responsible for interconnected functions necessary for organizational success. Hence, performance at the individual or team level eventually will affect organizational performance (Taggar & Neubert, 2004). Two items asked: “In the internal performance review of the previous year, (1) the performance grade of my department or team was. . .; (2) my performance grade was. . .” Responses were measured using a 7-point scale.

In H3, the independent variable focuses on institutional barriers to improving performance. Participants responded to an item about “The level of unnecessary administrative regulations and procedures [in their organization] that lead to organizational inefficiency,” with possible responses ranging from “very low” to “very high.’’

The fourth independent variable (in H4) tapped the sufficiency of financial resources available. We obtained the budget for each agency included in the sample and transformed it in two ways. First, we divided the funds by the number of public officials in the agency to obtain the proportion of the budget available for each government employee. Second, we divided it by the jurisdiction’s population to calculate the amount of public money per capita. These two variables were included as independent variables related to Hypothesis 4.

In the fifth hypothesis (H5), the independent variable is the level of organizational culture for innovation. To measuee this, we relied on three items: “Creative and innovative work performance is rewarded”; “I am encouraged to devise a new or better way of doing things”; “In our organization, it is possible to use resources to implement new plans.” Additive indexes created with these items using individual level data yielded Cronbach’s alpha of .861 and .853 for the 2016 and the 2017 surveys, respectively.

The sixth independent variable (in H6) is the degree to which public employees are required to be transparent about their work. This was tapped by levels of agreement with the statement: “we are required to disclose the process and results of our work.”

The partisan affiliation of the top elected official relevant to an organization (i.e., mayor for municipalities, the president for central government agencies) is included as a control variable to examine the prediction that partisanship (or ideology) may influence the process of goal setting. Traditionally, leftist politicians have tended to pursue a larger government that engages in changing citizens’ lives more proactively. Hence, they are more likely to set ambitious performance goals. Here, we measured partisan affiliation using a binary variable coded 1 for right-wing officials and 0 otherwise.

Analysis Strategy

We created the dataset combining data from the 2016 and 2017 surveys, and the data have a nested structure. Since the organizational characteristics we examined can be related to socio-political factors, time between the two surveys may have affected these variables or their impact. In particular, a notable political change occurred in South Korea between 2016 and 2017: the incumbent president of the right-wing party was impeached in late 2016 and a new president from the left-wing party took over in early 2017. This may have changed government employees’ perceptions of their agencies. Furthermore, it is worth noting that 17 government agencies participated in the surveys in both years. The potential effects of the period between surveys may have been particularly important for these organizations. In sum, analyzing the data using Hierarchical Linear Modeling techniques with data collection year as a grouping variable appears appropriate.

Results

Descriptive Statistics and Correlation Matrix

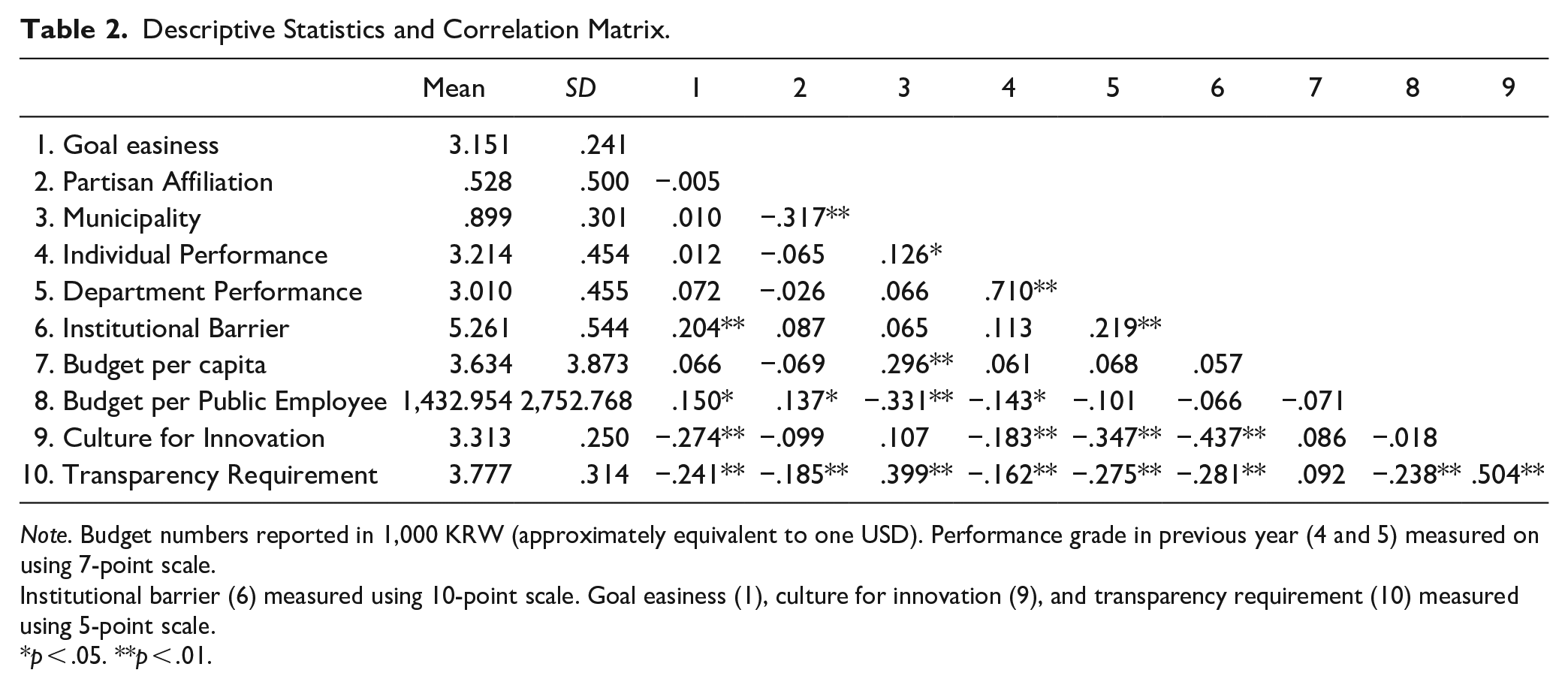

Descriptive statistics and a correlation matrix obtained from analyzing the final data from respondents in 243 agencies are provided in Table 2. Examining the correlation matrix, we found that the most of the correlation coefficients remained in the acceptable range, with the highest coefficient of .710. The second highest coefficient was .510. Despite the slightly high value of the coefficient, values of the Variation Inflation Factor (VIF) were relatively low: 2.141 and 2.284. Thus, we can reasonably argue that correlations between pairs of variables did not preclude use of regression analysis.

Descriptive Statistics and Correlation Matrix.

Note. Budget numbers reported in 1,000 KRW (approximately equivalent to one USD). Performance grade in previous year (4 and 5) measured on using 7-point scale.

Institutional barrier (6) measured using 10-point scale. Goal easiness (1), culture for innovation (9), and transparency requirement (10) measured using 5-point scale.

p < .05. **p < .01.

Hierarchical Linear Modeling Analysis

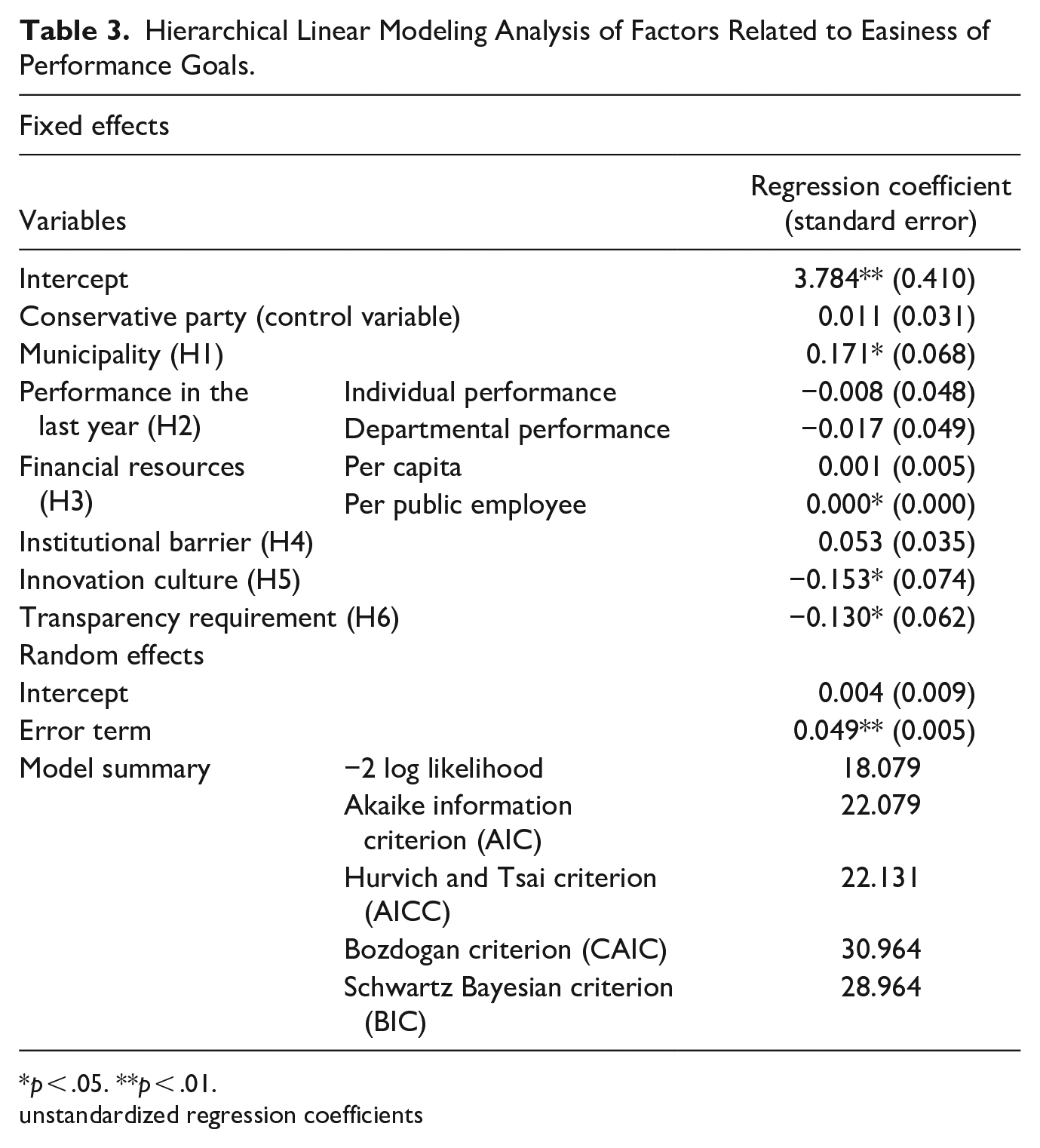

As mentioned earlier, we used HLM to test the hypotheses. The results are reported in Table 3.

Hierarchical Linear Modeling Analysis of Factors Related to Easiness of Performance Goals.

p < .05. **p < .01.

unstandardized regression coefficients

In the random effects model, the intercept was not significantly different between the 2016 sample and 2017 samples. Yet the error term did differ between the two samples. This implies that even though the time gap between the surveys was not associated with a ststistically significant change in levels of the dependent variable, performance goal easiness, it was associated with the variance of the DV. This suggests that HLM was an appropriate choice of analytic technique. In the fixed effects model, four independent variables were significantly related to easiness of performance goals. Among the six hypotheses we proposed, four were at least partially confirmed. since the regression coefficients are unstandardized, the lower magnitude of the coefficient for budget per employee compared with those of the other three statistically significant variables does not indicate that the effect size of budget/employee is smaller than the others; rather the budget variable has a much greater range than the other variables (see Table 2).

Hypothesis 1 was confirmed, showing that municipal agencies tend to set easy performance goals (t = 2.046, p = .042). Although support was found for the relationship in Hypothesis 3, its direction was reversed: agencies with greater budgets per public employee tended to set easy goals rather than to more challenging goals as initially predicted (t = 2.509, p = .013). Both hypotheses 5 and 6 were confirmed; organizations characterized by strong innovation cultures tended not to prefer easy performance standards (t = −2.016, p = .045); agencies that had stronger transparency requirements tended not to have easy performance goals (t = −2.483, p = .014).

Discussion and Conclusion

Public organizations may choose goals that are easier to attain out of self-interest motives without considering the public interest. This study examined the conditions under which public organizations might be more likely to choose easy performance goals. A major strength of the analysis is its reliance on both perceptual and archival data, seeking to reduce biases typically observed in studies with a single data source (George & Pandey, 2017). It also yielded results that have meaningful implications for public managers and scholars of public administration.

Interpretation of Findings

Several results need to be further discussed more fully. First, municipalities tend to choose to set easier goals than agencies in the central government. This is consistent with the primary responsibility of municipal agencies to implement public service programs, which often need increased staffing, workihours, and financial resources in order to improve performance. The finding may indicate as well that, as proposed, local government agencies are exposed to greater competition with agencies in other localities; as localities try to keep current residents and attract others to live in their cities and counties, local agencies may try to receive excellent performance ratings with lesser effort. Since such performance easily quantifiable (e.g., customer satisfaction rates), they may be more sensitive to the risk of getting a low performance grade.

This result may appear to be inconsistent with the belief that upper-level government agencies intervene in the process of goal setting of lower-level entities to foster goal alignment.Ma (2016), for instance, examined the performance goals of Chinese provincial governments and found this was the case. Yet, this study found otherwise. If central governments had intervened in local governments’ goal setting processes, there would have been little difference in the easiness of their goals. The discrepancy may be explained by highligtingthe differences in government structure between the two countries. South Korea emphasizes local autonomy, while the Chinese central government has greater authority over lower levels. Moreover, residents elect the mayors in South Korean cities, but the executives in Chinese provincial governments are politically appointed. Hence, South Korean local government agencies appear to have greater discretion over performance goal setting than Chinese provincial agencies. This in turn sets conditions for the generalizability of Ma’s (2016) work, suggesting that the vertical adjustment of performance goals may not happen in countries in which local governments retain considerable discretion.

Second, we failed to find suport for Hypothesis 2 on possible effects of past agency performance. This may indicate that an agency’s performance grade in the previous year does not matter for the ease of its performance goals. Yet, several factors make us reluctant to draw that conclusion. First, there is a theoretically sound basis for the hypothesized effect, which similar studies have confirmed (Hong, 2019; Ma, 2016). Second, as pointed out earlier, we were not able to obtain data on organizational past performance. The possible effects that we examined instead focused on past individual and departmental performance. Third, the signs of the regression coefficients are consistent with the directions of the hypothesized relationships. In addition, the effect size of past departmental performance is greater than that of past individual performance. Hence, we would speculate that if we had had data on past organizational performance, we could have obtained statistically significant coefficients. Future researchmight probe this possibility.

Third, those agencies with greater more financial resources at their disposal tended to set easier goals than those without sufficient funds, which was contrary to what we hypothesized. Initially, we argued that the sufficiency of financial resources would be negatively related to the easiness of performance goals. One possible explanation may be how we measured the variable. We utilized the actual annual budget of a given agency rather than directly asking respondents about the sufficiency of financial resources (or the lack thereof). Had we used primary survey data, we might have found a different result.

Nevertheless, the present finding may indicate that the underlying mechanism that motivates easy goal setting may differ from what we predicted. We initially argued that public employees seek easier ways to meet performance standards in the face of inadequate financial resources. In contrast, the unexpected opposite result might be explained by a clue from H. W. Lee’s (2019) study where he examined performance management practices from the perspective of political dynamics. The motivational effect of performance management became weaker when public employees had higher levels of job autonomy and when they had sufficient organizational resources. He interpreted his results using the term “achievement syndrome” (Rosen, 1956): where those with outstanding achievements in previous years tend to be pressured to continue to achieve at high levels. Perhaps similarly, agencies with sufficient resources may believe they need to produce performances that continue to justify their abundance and may be induced to choose easy performance goals.

This speculation is reinforced by another finding. The relationship between budget size per capita and easiness of performance goals was not stistically significant. An agency’s budget per citizen may indicate whether the agency is given financial resources to “serve” its constituents, but the budget per employee suggests that the given agency has “an advantageous status” in the politics of budget allocation. That we only found that the latter was significantly related to ease of performance goals supports the speculation that those with sufficient financial resources may be encouraged to set easy goals to maintain their superior position in the next round of budget politics.

Implications

This study has several important theoretical implications. Early scholars viewed organizations entities in which each part cooperated with other parts to accomplish the missions of the entire organization (Handel, 2003). Yet more recent scholars tend to view organizations as political arenas in which of a large organizational entity competes with others to maximize interests (Tjosvold, 1988; Tsai, 2002). A performance management system in which multiple “agencies” at various levels pursue their interests is not an exception. Individual and organizational choices are not independent; behavioral tendencies of individuals also may be observed at the organizational level (Hong, 2019). Organizations are led by key decision makers with stronger motivations than employees to act opportunistically since performance failure will be attributed to the lack of manager competence (Welter & Ensslin, 2022). We verified this using data from national and local government agencies. We call for more investigation to further understanding of the political dynamics associated with performance outcomes.

This study’s findings also provide some clues about mitigating the dysfunctional practice of setting easy performance goals. It may not be simple for upper-tier agencies to put lower-level units under tight control in democratic countries in which local governments are entitled to considerable autonomy. However, we find that better alignments of interest are necessary. For instance, Capaldo et al. (2018) report that opportunism at the goal setting stage decreased when the particular circumstances of an organization are taken into consideration at the evaluation stage. Those agencies setting challenging goals may be compensated (“rewarded”) for their risk taking at the evaluation stage.

We can induce public agencies to themselves set challenging performance goals if we can cultivate cultures of innovation within organizations. Leadership is critical. Promoting self-leadership, for instance, enhances creativity, which in turn positively affects innovation (Pratoom & Savatsomboon, 2012). Transformational leadership also can help create organizational cultures for innovation (Muchtar & Qamariah, 2014) and climates for creativity (Kim & Yoon, 2015). In addition, transformational leaders have been found to choose difficult goals, which in turn elevate employee’s work motivation (Bronkhorst et al., 2015). Thus, public managers need to be encouraged to exert leadership to foster and sustain innovative culture.

We also found that organizations that require employees to be transparent not only about their performance results, but also about their work processes tend not to set easy goals. Strengthening requirements for transparency may induce public organizations to pursue more reasonable goals. This might be done, for example, by mandating the use of grassroot committees with participation by civic experts to oversee annual strategic planningand review the legitimacy of annual performance targets. Requiring local governments to offer rationales for annual goal setting each year or opening the process of goal setting to the public also may help.

Limitations and Suggestions for Future Research

Although this study made meaningful suggestions on how to encourage public organizations to set reasonable performance targets, it also has several limitations that future researchers might address. Because it focuses on South Korea, its generalizability may be limited. The environment for South Korean performance management is somewhat distinctive. First, likely in part because South Korea was an early and enthusiastic proponent of performance management, its performance management system is quite complex, which significantly limits the monitoring capacity of overseeing entities. Its complexity reflects the many different performance evaluations undertaken for different purposes. The heavy workloads of organizations under evaluation may well further motivate them to treat evaluation as perfunctory, procedure rather than seeing it as an opportunity to improve performance (Brown & Benson, 2005). This study’s results may not apply in countries where the performance management process is simpler.

The complexity of South Korean performance management practice and workloads of most government organizations also has meant that the central government’s overseeing entity has devolved considerable discretion over performance evaluation to lower-levels. This has created an environment that reduces the costs associated with gaming in the performance evaluation regime. This study, then, may not be applicable in other governmental contexts.

Yet governments in other countries have similar weaknesses in performance-based control. In the U.K., for example, adoption of a risk management paradigm motivates public organizations to act defensively (). The Dutch government also faces limitations on performance accountability due to the lack of coherent performance indexes (Van Hengel et al., 2014). These instances suggest that public officials in many settings also may have room for opportunism. Conducting similar research can help us understand how factors related to setting easier performance goals setting may differ with country political context.

Additionally, there are several data limitations. First, we used some data collected before this study was designed. Particularly for testing examining Hypothesis 2, we did not have data on how well given organizations performed in the previous year. As a result, we relied on respondents’ perceptions of their departments’ and their own performance levels as proxies. We cannot tell with confidence if the unconfirmed hypothesis is due to the the quality of the data or whether the association we expected was not present. Future researchers are encouraged to confirm the hypothesized relationship using a sound dataset.

Second, although we took steps to reduce common source bias by utilizing the mean scores of variables for each agency, it may not have been possible to such bias fully, given our reliance on perceptual data. The use of a survey method was hard to avoid, because the key variables involve perceptions, such as the ease of achieving performance goals and cultural factors.. Nonetheless, it is crucial to exercise caution when interpreting our research findings. Specifically, for hypotheses 4 (institutional barriers) and 6 (transparency requirements), it would be advisable to incorporate more objective data whenever feasible. We hope that future researchers will undertake similar analyses of these issues using objective measures to tap the effects of institutional inefficiencies and transparency requirements on the ease of performance goals.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Public Performance Management Research Center at Graduate School of Public Administration, Seoul National University.

Data Availability Statement

Data may be provided upon request.