Abstract

This study aimed to identify factors affecting the financial behavior of overseas Filipino workers. Responses from a survey of 116 Filipino workers in Korea were analyzed using descriptive statistics and hierarchical regression. The results revealed that some Filipino workers showed sound financial behavior only for simple financial activities; many were not equipped with complex financial management skills. Migrant workers with high financial self-efficacy in the Philippines were likely to have more positive financial behavior. However, this was not significantly associated with financial literacy or attendance in financial education programs. Implications for the development of financial education for migrant workers are discussed.

Keywords

Introduction

International migrant workers are a vital labor force in most developed countries. In 2019, there were over 560,000 migrant workers in South Korea (Korea hereafter), that accounted for approximately 2 percent of the country’s working population. The number was decreased to 406,669 in 2021 due to the spread of the COVID-19 (Ministry of Justice, 2020, 2022). As the Korean migration scheme regulating low-skilled workers generally does not encourage migrant workers to settle permanently in Korea, most of them must be prepared to return to their home country. Failing to meet their financial goals could lead to migrant workers to extend (or overstay and become irregular migrant workers) their time in Korea or to consider serial labor migrations elsewhere (Jang et al., 2019). However, it is unknown whether being equipped with adequate financial capabilities helps them achieve their financial goals (Jang et al., 2019).

Many migrant workers send a substantial part of their income to their families back in their home country while saving some money in Korea. Remittances from migrant workers could make a significant contribution to their family’s finances and the economy of their country of origin (International Labour Organization, 2009). The families of migrant workers in the home country use the remitted money for daily expenses, schooling of their children, and savings (Ashraf et al., 2015; Atkinson and Messy, 2015). In addition, in many developing countries, migrant remittances are a critical component of the national income (Karunarathne and Gibson, 2014); the amount of remittances sent to developing countries was estimated at USD 589 billion in 2021, a 6.3 percent increase from 2019 (Ratha, 2021; World Bank, 2020). For example, remittances sent by overseas Filipino workers (OFWs) in 2018 were over USD 32 billion, which accounted for more than 8 percent of the Philippines’ gross national income (Caraballo, 2019).

Migrants often have lower levels of financial literacy than natives (Nam et al., 2015). Often, migrant workers find it difficult to manage and transfer their income efficiently because of differences in financial systems between their home and host countries (Gibson et al., 2014). A lack of knowledge of the host country’s banking services combined with the home country’s underdeveloped financial systems could hinder the transfer of money through secure, low-cost channels, resulting in increased risks and costs and lesser money for migrant workers to remit (Atkinson and Messy, 2015). In addition, factors such as distrust in financial institutions, lack of experience in using financial services and low financial literacy could jeopardize migrant workers’ financial well-being, especially considering the language barrier they often experience when accessing financial services (Atkinson and Messy, 2015; Karunarathne and Gibson, 2014). Empowering migrant workers’ financial capability, i.e., the ability to manage financial matters catering to one’s best financial interests under the given socioeconomic conditions (World Bank, 2013), is critical for them to achieve their financial goals for working abroad (Lacsina and Opiniano, 2018).

There has been a growing interest in promoting migrant workers’ financial capabilities. The Philippines advocates the importance of its overseas workers’ financial literacy by providing financial education programs through various institutions including government organizations in the Philippines and abroad (Atkinson and Messy, 2015; Jang et al., 2019; Kim et al., 2017). Many financial education programs are sponsored by the Philippine government, while others are sponsored by financial institutes from the pre-departure to the post-arrival phases (Jang et al., 2019). Many Filipino workers in Korea aim to accumulate enough assets to launch a business or make an investment in the Philippines (Jang et al., 2019). Being equipped with sufficient financial capability is critical for achieving these goals. This study aimed to explore the characteristics of OFWs’ financial capabilities in Korea, focusing on the relationship between financial behavior and literacy, financial attitudes, self-efficacy and attendance in financial education programs.

Literature review

Characteristics of OFWs’ financial management

The Philippines was the fourth-highest remittance-recipient country after India, China and Mexico in 2019 (World Bank, 2020). Considering that the number of Filipino migrants is relatively smaller than that of migrants from the top three countries (International Organization for Migration, 2019), the migrant workers’ contribution to the economy of the Philippines seems prominent. Remittances from migrant workers are a large source of foreign exchange and they act as a buffer against external financial crises (Ang, 2007; Bayangos and Jansen, 2010). From a microeconomic perspective, remittances used to cover household expenditure are equivalent to approximately 60 percent of the gross domestic product (Business World, 2020).

The destination countries of OFWs are varied. According to the Bangko Sentral ng Pilipinas (Central Bank of the Philippines), in 2021, remittances from the US accounted for the highest proportion of total remittances (40.5 percent), followed by Singapore, Saudi Arabia and Japan (Bangko Sentral ng Pilipinas, 2022). There were about 49,800 Filipino migrants in Korea in 2020 (Ministry of Justice, 2021), and the total amount of remittances sent from Korea to the Philippines exceeded USD 707 million (Bangko Sentral ng Pilipinas, 2022). The majority of OFWs in Korea are men working in manufacturing (Lee et al., 2018). 1 Most OFWs in Korea are in their 20s and 30s. About half of OFWs earned two to three million Korean Won or KRW (approximately USD 1600 to 2400), and the rest made less than KRW two million, according to the 2017 Survey on Immigrants’ Living Conditions and Labour Force (Jang et al., 2019).

Compared to East Asian and Pacific countries, financial inclusion in the Philippines is lower (World Bank, 2015). The Financial Capability Survey 2014 conducted by the World Bank revealed that about 41 percent of Filipinos did not use formal financial services, and 22 percent relied on informal sources for borrowing money (World Bank, 2015). Individuals in the low-income level are less likely to use formal financial services; only 42 percent of them reported using a formal financial product. The most frequent reason was limited financial resources (20 percent); other reasons include not seeing the need to have a bank account and lack of trust and access to formal financial services (World Bank, 2015).

The level of educational attainment in the Philippines is relatively higher than in other countries. About 29 percent of the population is educated at the college level and 43 percent have a high school diploma. However, the average level of financial literacy of Filipinos is not very high; the mean score was 3.2 out of 7 points in the 2014 Philippines Financial Capability Survey (World Bank, 2015). Only about half of the survey participants were able to calculate inflation and simple interest rates and to understand the main purpose of insurance products. For financial behavior, respondents scored lower on budgeting and financial planning compared to other behavior.

According to the 2017 Survey on Immigrants’ Living Conditions and Labor Force in Korea, OFWs remitted more than half of their income; however, only about 10 percent of their income was saved in Korean bank accounts (Jang et al., 2019). Jang et al. (2019) found that although most OFWs in Korea were planning to start a business after returning to the Philippines, few of them had specific strategies to save enough money to launch a business. Previous studies show that bank accounts were not necessarily used by OFWs as savings accounts (Jang et al., 2019; Lim and Visaria, 2020). OFWs in Korea did not have much information on using their Korean bank accounts for asset management as bank accounts were mainly opened for use as salary accounts (Jang et al., 2019). Lim and Visaria (2020) found that Filipino workers in Hong Kong tended to take loans rather than use savings for investment because accessing loans was easier than saving voluntarily. They argued that this was due to Filipino migrants’ financial attitudes and not a lack of financial literacy regarding cost evaluation. However, Barua et al. (2020) found that the influence of initiating a saving club to encourage saving behavior was not effective for OFWs with low financial literacy in Singapore.

Financial inclusion and education of migrant workers

The financial inclusion of migrant workers can be achieved by guaranteeing availability and access to financial services and opportunities, which is also essential for migrants to fully benefit from their migratory experience (Centre for Studies in International Politics, 2019). Financial inclusion empowers migrant workers to plan their financial future by utilizing their limited income efficiently (Prandini and Rowena, 2020).

Financial capability is defined as one’s ability to assess and manage finances (Lusardi, 2013). Atkinson et al. (2007) posited that financial capability has four different domains: money management, planning, choosing products and staying informed. Therefore, to be financially capable, it is essential to possess financial literacy, skills, motivation and confidence in making adequate financial decision-making (Zakaria and Sabri, 2013). This suggests that there are multiple factors that affect individuals’ financial behavior, such as sociocultural contexts, financial resources, psychological and behavioral characteristics, and family financial socialization. Thus, it is necessary to explore how migrant workers’ financial circumstances, literacy, attitudes and self-efficacy affect their financial behavior.

Limited access to formal financial services could decrease financial self-efficacy (Rostamkalaei and Riding, 2020) and hinder optimal financial behavior (Birkenmaier and Fu, 2019). Multiple factors could discourage migrant workers from accessing formal financial services (Atkinson and Messy, 2013). First, underdeveloped financial infrastructure, such as a lack of financial services in the home country or difficulty in physically accessing financial services in the host country, could impede migrants’ access to formal services. High transaction costs or lack of adequate financial products for migrant workers are other barriers. In addition, undocumented migrant workers could be excluded from formal financial services (Karunarathne and Gibson, 2014). Second, different financial systems and cultures across countries could affect migrant workers’ financial attitudes and financial market participation (Osili and Paulson, 2008), and reduce confidence in seeking financial advice (Atkinson and Messy, 2013). Third, migrant workers might struggle to understand financial services in the host country due to limited language proficiency and low levels of financial literacy, especially if financial education tailored to migrant workers’ needs is unavailable (Atkinson and Messy, 2013).

The financial literacy of immigrants tends to be lower than that of the natives because of language barriers and inequality of access to education in addition to the differences in financial systems between the home and host countries (Barcellos et al., 2016; Karunarathne and Gibson, 2014; Nam et al., 2015; Rostamkalaei and Riding, 2020). Using data from the Program for International Student Assessment (PISA) across 18 countries, Gramatki (2017) found an existing gap in financial literacy scores between native and immigrant students, especially those belonging to the first generations. In addition, immigrant students are likely to have lower math and reading scores on the PISA, which are fundamental skills in acquiring financial literacy (Atkinson and Messy, 2015; Gramatki, 2017). However, migrants’ financial self-efficacy – i.e., “an individual’s self-perceived ability in managing their finances” (Nguyen, 2019: 143) – did not significantly differ from those of natives (Barcellos et al., 2016).

Migrant workers may not be able to maximize the positive economic outcomes of migration without sufficient financial literacy. For example, if migrant workers and their families do not understand the importance of savings and investments, they are more likely to spend income and remittances than to save them for the future (International Labour Organization, 2016). Therefore, it is necessary to offer them quality financial education programs and promote their financial inclusion to strengthen the financial stability of immigrant families.

Migrant workers’ financial conditions may change according to the migration stage. For instance, at the initial stage of migration, there are travel costs and settling expenses, and these costs often incur debts (Lim and Visaria, 2020). Once settled, migrants need to navigate ways on how to budget their new income and manage daily expenses and remittances. Return migration also requires advanced planning. These varying financial circumstances lead to the diverse financial education needs of migrant workers (Cohen and Nelson, 2011). Lack of clear migration planning or family agreement on managing remittances could result in serial labor migrations (Diaz, 2009, as cited in Cohen and Nelson, 2011).

Having sufficient financial literacy and sound financial attitudes are prerequisites for migrant workers to achieve their goals through sound financial behavior (Rostamkalaei and Riding, 2020; World Bank, 2015). Studies have shown that identifying the purpose of a remittance as a target for financial action can lead to positive behavioral changes. In their study, De Arcangelis et al. (2015) found that migrants who specifically set aside and marked part of the remittance for education tend to send more remittances for this purpose. Furthermore, it is important to foster sound financial behavior for the families of migrant workers as well because many families tend to have high consumption and low savings (Seshan and Yang, 2012). It is also reported that in some countries migrant workers and their families may not agree on how to manage family finances, particularly spending and savings (Ashraf et al., 2015; Lim and Visaria, 2020; Murata and Sioson, 2018). Migrant workers may have less control over their savings if they share access to savings accounts with their families (Ashraf et al., 2015).

The financial inclusion of migrants can be promoted in several ways. Policy interventions are required to lower the cost of remittances and increase opportunities for migration. The reduction in transaction fees is among the goals and targets of the Global Compact for Migration and Sustainable Development Goals (United Nations Development Program, 2019). Increasing access to small personal loans and advanced financial technologies, such as fintech or blockchain, could be an example of such interventions. In addition, empowering migrant workers through financial education is critical. At the Association of Southeast Asian Nations (ASEAN) Literacy Conference in 2013, Stephen P. Groff, vice-president of the Asian Development Bank, stated the importance of promoting formal remittance transfer channels and offering financial education to migrant workers in his keynote speech (Asian Development Bank, 2013).

Financial education for migrant workers may include basic skills such as calculating the currency exchange rate, financial budgeting, keeping books, and comparing savings and credit products. The Organization for Economic Co-operation and Development (OECD) and the International Network on Financial Education (INFE) emphasized that financial understanding can promote financial inclusion and is essential for money management and long-term financial planning, which can significantly improve financial well-being for migrants and their families (Atkinson and Messy, 2015). The International Labor Organization (ILO, 2009, 2011a, 2011b, 2016, 2019) has published handbooks on financial management in several countries to enhance migrant workers’ financial management skills.

However, the effects of financial education remain unclear. Financial education programs customized for immigrant families have a positive influence on their financial well-being. Gibson and colleagues found that financial education promoted financial knowledge and information-seeking behavior among migrants from Pacific Islands, East Asia and Sri Lanka in New Zealand and Australia (Gibson et al., 2012). The World Bank and the Indonesian government’s financial education program revealed positive changes in savings and loans when the program was provided to both immigrants and their stay-behind families in Indonesia (Doi et al., 2014). Seshan and Yang (2014) found that after a financial workshop for Indian migrant workers in Qatar, they shared financial decision-making with their spouses, and the savings increased significantly in the group with a low level of savings. Still, repeated financial education programs are required to sustain financial literacy (Barcellos et al., 2016). In their experimental study of immigrants in the United States of America (USA), Barcellos et al. (2016) found that financial knowledge acquired from one-time intervention faded away after six months. One-time seminars, especially provided by private banks were considered ineffective among financial educators and migrant worker support providers in Korea (Jang et al., 2019). These seminars tended to focus on advertising banks’ saving products and transfer fees, which did not cover wide areas of financial information necessary for migrant workers.

According to a study on OFWs in Korea (Jang et al., 2020), most of the participants had some experience of financial education either in the Philippines or Korea. It is interesting to note that more participants received financial education after migrating to Korea. Also, participants' satisfaction with the financial education received in Korea was higher than the financial education they received in the Philippines, which may be due to differences in education availability or increased interest in finance. OFWs in the study were especially interested in teaching programs about investments, saving methods, budgeting and business start-ups after their return.

To address some of the gaps on financial education-related programs for migrants, this study explored two research questions about the financial capacity of OFWs in Korea: (1) What are the characteristics of OFWs’ financial capabilities, and (2) what are the variables related to an OFWs’ financial behavior?

Methodology

Research design

This study is based on survey data collected through collaboration between the Migration Research and Training Centre and the Philippine Overseas Labor Office (POLO) in Korea. In 2019, the two institutions conducted surveys to explore the needs and current status of OFWs’ financial behavior and attitude, with a view developing effective financial education programs for them. The research proposal was reviewed and approved by a board composed of internal and external researchers. The survey questionnaire included items about (a) financial behavior, (b) financial literacy, (c) financial attitudes and self-efficacy, (d) experiences of financial education programs in the Philippines and Korea, and (e) demographic characteristics. The questionnaire was developed by researchers at the Migration Research & Training Centre. The staff at POLO Korea explored whether the questionnaire would be appropriate and understood by OFWs. The self-administered survey was written in English and the staff at POLO Korea provided explanations in Tagalog to participants where necessary. Responses from 116 survey participants were analyzed. The respondents were recruited from two half-day financial education seminars on financial attitudes, orientation to the Philippines’ National Reintegration Program, and investment and entrepreneurial options. POLO Korea organized the seminars, and participation in the survey was voluntary. The convenience sampling used by the study and the small sample size offer only a glimpse of the financial capabilities of OFWs in Korea and cannot be generalized to the larger population of OFWs. Still, the research project attempted to provide a better understanding of the current status of the financial well-being of migrant workers in Korea.

Variables and measures

Financial behavior

This variable was measured by items asking the participants how often they engaged in 10 financial activities, as used in previous studies (e.g., Danes et al., 2013; Xiao et al., 2007). These 10 financial activities included (a) tracking monthly expenses, (b) having spending plans, (c) spending within budget, (d) looking for the best prices for purchase, (e) paying monthly bills on time, (f) paying monthly credit balances in full, (g) saving regularly, (h) setting aside money for emergencies, (i) contributing to investments or retirement accounts other than the national pension, and (j) discussing money matters with family. Since more than 40 percent of the participants reported that the credit card activity item was not applicable to them, it was excluded from our study. Cronbach’s alpha coefficient was 0.66, which is acceptable (Ursachi et al., 2015). Responses ranged from 1 (never) to 5 (always). The financial behavior score was calculated as the sum of the nine activities, with total scores ranging from 9 to 45.

Financial literacy

Items and questions to assess financial literacy.

Note: The items and questions were adapted from the 2014 World Bank Survey on enhancing financial capability and inclusion in the Philippines (World Bank, 2015).

Financial attitudes

These were measured by summing two items about the participants’ agreement with the following statements (Kempson et al., 2013): (a) “I am very disciplined when it comes to managing money” and (b) “I always get information or advice when I make an important financial decision.” Pearson’s correlation coefficient for the two items was 0.64. The answer to each question was a five-point scale ranging from 1 (strongly agree) to 5 (strongly disagree).

Financial self-efficacy

Participants were asked about their financial self-efficacy in the Philippines and Korea. Participants’ agreement with the following statements was measured (Danes et al., 1999): (a) “I feel confident about making financial decisions in the Philippines” and (b) “I feel confident about making financial decisions in Korea.” Pearson’s correlation coefficient for the two items was 0.82. Responses ranged from 1 (strongly disagree) to 5 (strongly agree).

Financial education

This was a binary variable that measured whether participants had received financial education in Korea and the Philippines.

Demographic characteristics

Information on participants’ age, gender, level of education, marital status, whether they had children and years spent in Korea was obtained.

Analysis

The research questions analyzed using descriptive statistics and hierarchical regression analysis. Descriptive statistics were employed to understand the financial capabilities of OFW, such as financial understanding, which indicates objective knowledge necessary for financial behavior and financial management. Hierarchical regression analysis was performed to examine the association between independent variables and financial attitudes and self-efficacy, with a view to understanding OFWs’ psychological readiness to make sound financial decisions.

Results

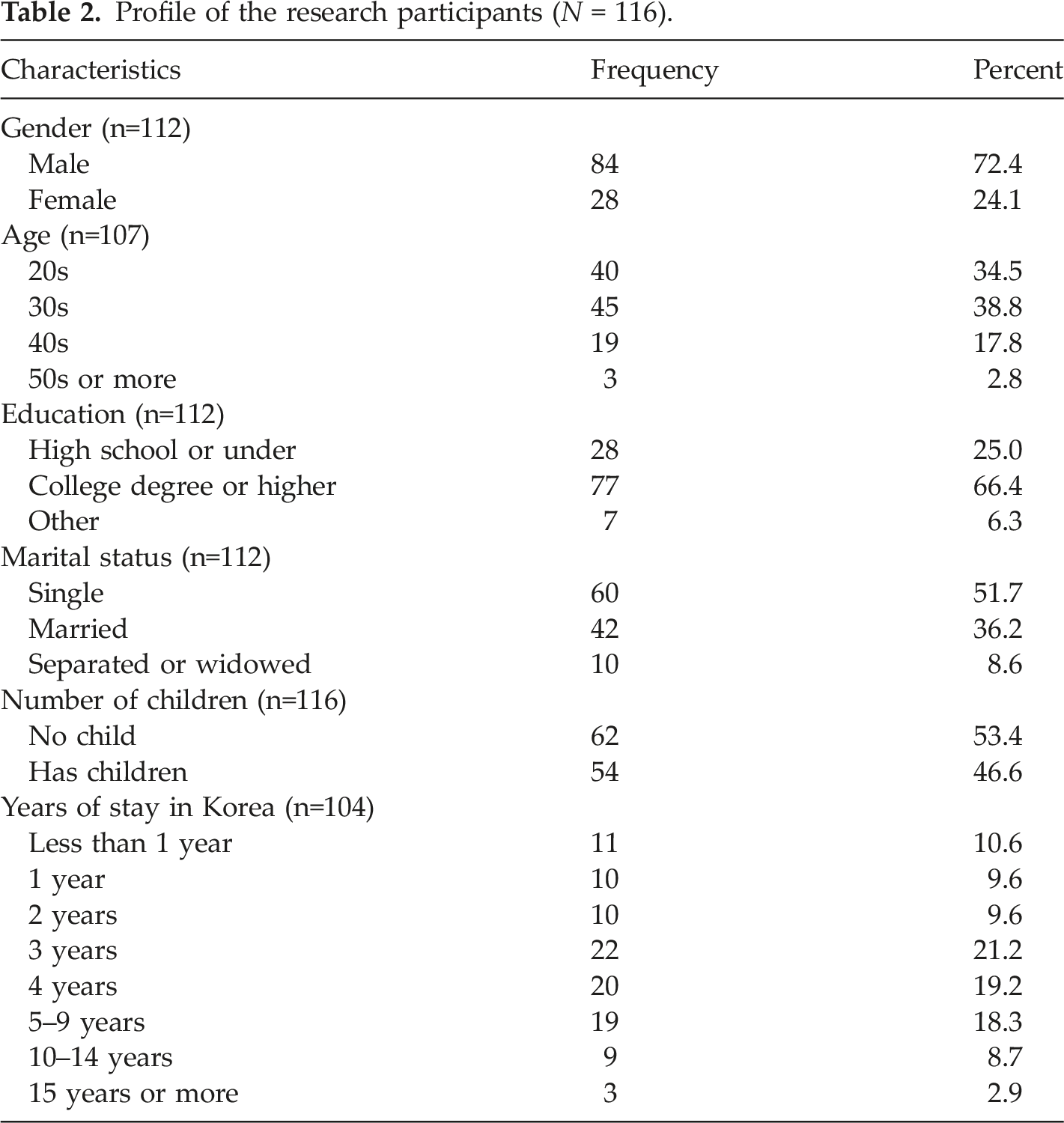

Characteristics of the participants

Profile of the research participants (N = 116).

Financial capability of OFWs

Financial behavior

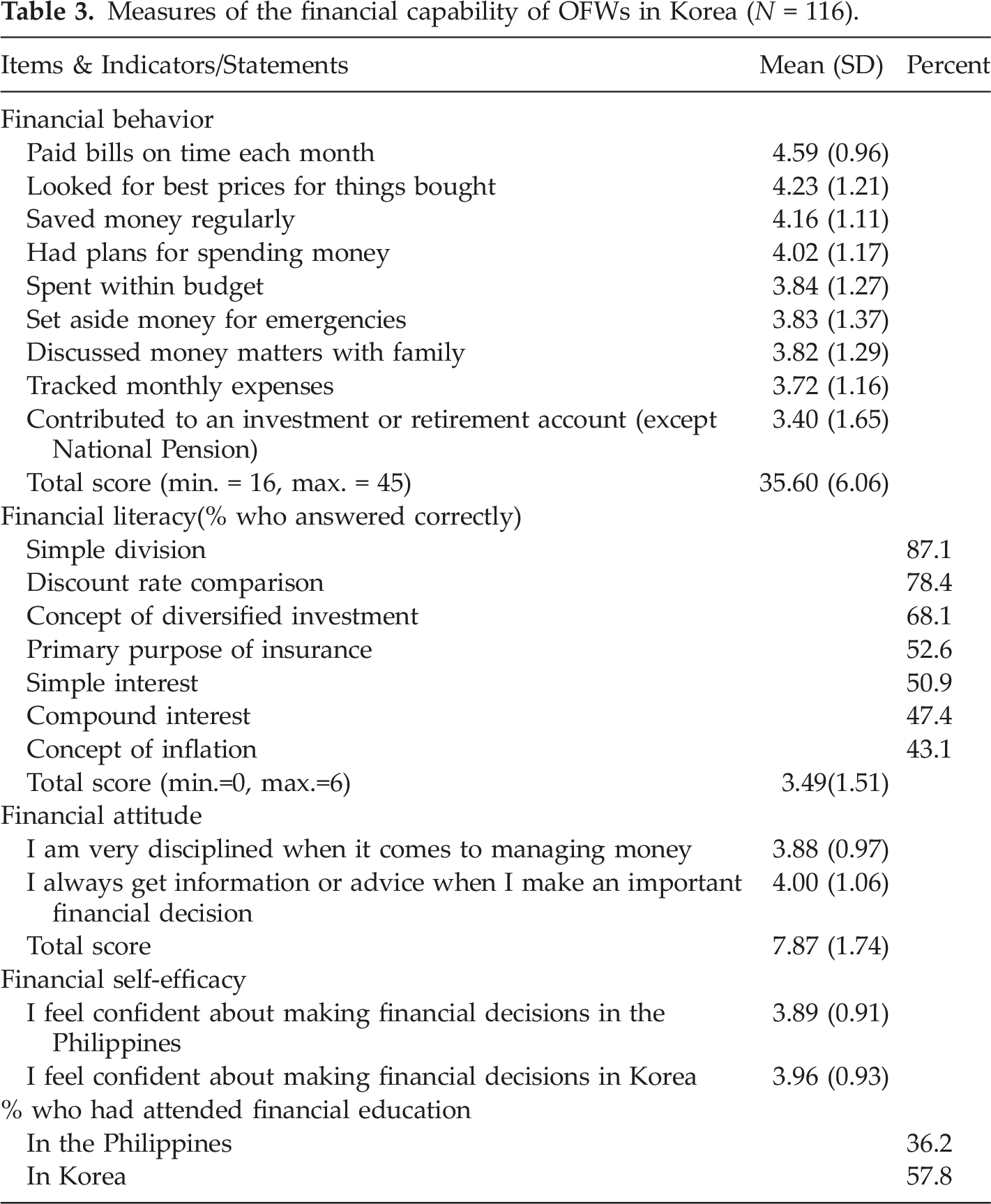

Measures of the financial capability of OFWs in Korea (N = 116).

Financial literacy

Of the seven items measuring financial literacy, the mean score was 3.49 (SD = 1.51), which was about half of the total items (Cronbach’s α = 0.60). By item, most respondents correctly answered the questions on simple division (87.1 percent) and the discount rate comparison (78.4 percent). About 68.1 percent of the participants understood the concept of diversified investment; however, only about half of the participants correctly answered the question on the primary purpose of insurance (52.6 percent). More complex financial concepts, such as the concept of inflation and compound interest, were not well understood by many participants (43.1 percent and 47.4 percent, respectively).

Financial attitude

The mean scores of participants on the two statements on financial attitudes suggest positive attitudes. The statement, “I am very disciplined when it comes to managing money,” had a mean score of 3.88, SD = 0.97 while the statement, “I always get information or advice when I make an important financial decision,” had a mean score of 4.00 and SD = 1.06. Cronbach’s α for both items is 0.64.

Financial self-efficacy

Participants were more confident in making financial decisions in Korea (mean = 3.96, SD = 0.93) than in the Philippines (mean = 3.89, SD = 0.91, Cronbach’s α = 0.82).

Experience of financial education

More participants responded that they had received financial education in Korea (57.8 percent) than in the Philippines (36.2 percent).

Association between variables

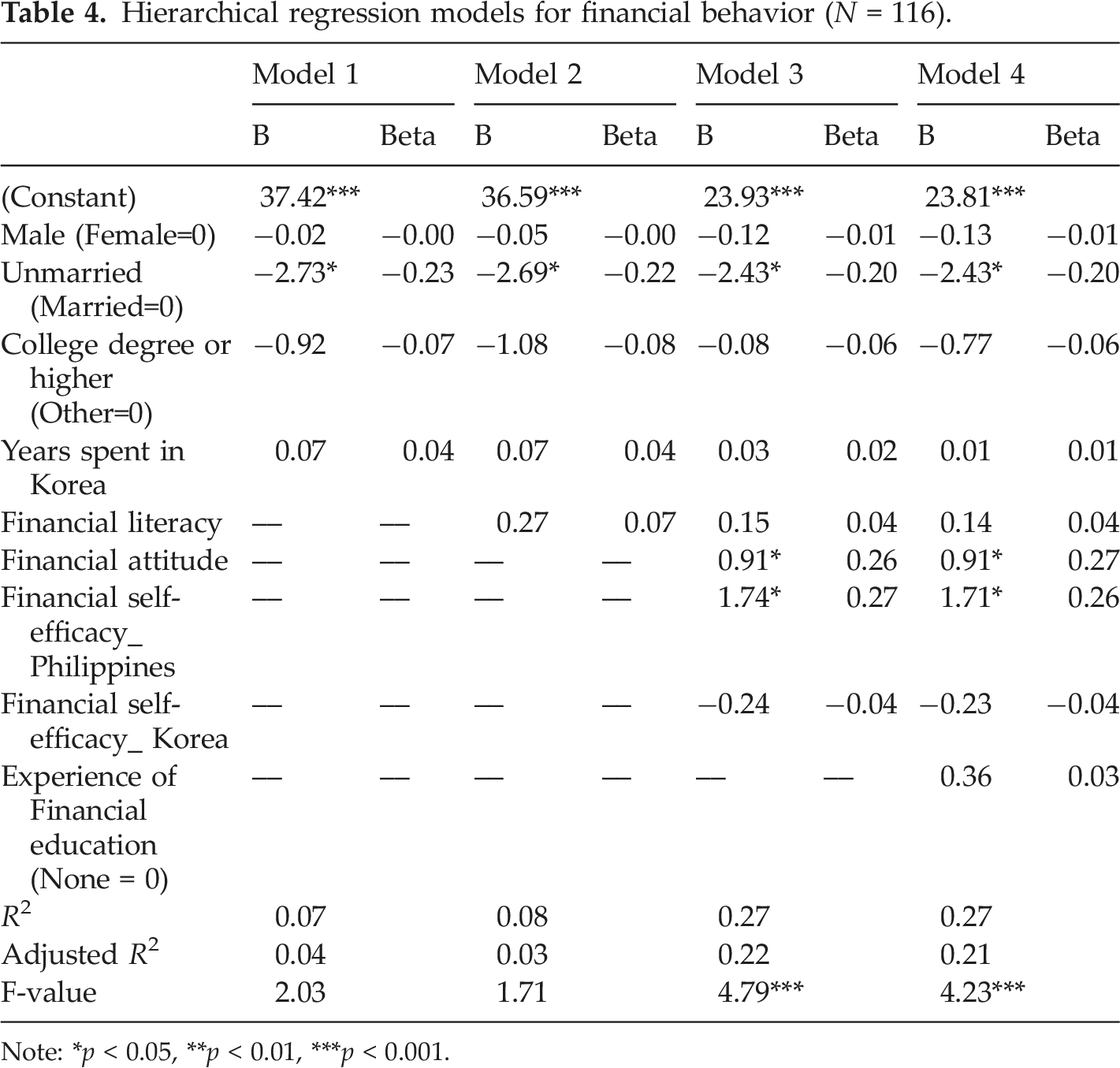

Hierarchical regression models for financial behavior (N = 116).

Note: *p < 0.05, **p < 0.01, ***p < 0.001.

Model 1 included only the demographic characteristics of the participants. Among the demographic characteristics entered in the model, marital status was significantly associated with financial behavior. Unmarried participants were less likely to display sound financial behavior than their married counterparts (B = −2.73, p < 0.05). Other variables, such as gender, education, and years spent in Korea, were not significantly associated with participants’ financial behavior. Model 1 explained 7 percent of the variance in financial behavior.

Model 2 estimated the influence of financial literacy and demographic characteristics. Financial literacy did not have a significant relationship with financial behavior, that is, it did not contribute to predicting financial behavior above the variance explained by the demographic characteristics in Model 1. The influence of marital status on financial behavior remained significant in Model 2.

The financial attitude and self-efficacy variables were entered in Model 3. Financial attitude and financial self-efficacy in the Philippines were significantly related to positive financial behavior (B = 0.91, p < 0.05, B = 1.74, p < 0.05, respectively). However, financial self-efficacy in Korea did not have a significant relationship with financial behavior. The influence of marital status on financial behavior was still significant in Model 3. The model significantly improved the prediction of financial behavior, as Model 3 explained 27 percent of the variance in financial behavior.

The experience of financial education was entered in Model 4, but the model prediction did not improve. Moreover, it decreased the adjusted R2 value. Thus, attending a financial education program was not significantly related to financial behavior.

Discussion and implications

Migrant workers contribute to their families’ financial resources and the economic development of their country of origin. It is necessary to support them in managing their income effectively by promoting positive financial behavior, in addition to providing and improving access to adequate financial services. The Philippine government has encouraged OFWs to achieve their migration goals by providing several financial education programs before and after migration. As a receiving country, Korea has provided programs supporting Filipino migrants’ social integration and preparing them for their return to the country of origin. The results of this study could contribute to the development of efficient financial education programs in both countries.

The results reveal that the OFWs were not enough equipped with complex financial management skills (e.g., understanding the concept of inflation, 5-years compound interest rate, interest rate calculation and comparing investment products). They tended to show sound behavior for simple financial activities, but these may not be sufficient to prepare for their financial future. They demonstrated lack of understanding of concepts such as inflation or compound interest, which could jeopardize their decision-making related to savings or investments. OFWs in Korea may experience difficulties in accessing Korean financial services and thus may not be able to save enough money in Korea to meet their financial goals. For the participants, sending remittances to their remaining families might be the most accessible way to manage their income. Given that most participants expressed interest in the topic on how to invest (Jang et al., 2020), it is necessary to cover the importance of long-term financial management through investment and saving for later life. Jang et al. (2019) found that OFWs were interested in making investments or savings in Korea and Philippines. They had low levels of awareness, however, on how to avail such services in Korea. As OFWs tend to stay in Korea for several years, this information would help increase their financial capability. It could also be incorporated within the current Happy Return Programs 2 provided by POLO Korea and Korea’s Ministry of Employment and Labor.

Participants reported their financial attitudes positively. While their financial self-efficacy in Korea was higher than in the Philippines, financial self-efficacy in the Philippines (not in Korea) was positively associated with their financial behavior. Providing information about the financial environment in Korea may further empower them during their stay in Korea and could enhance positive financial behavior.

Financial literacy did not reveal a statistically significant positive association with financial behavior. Considering the positive influence of financial self-efficacy in the Philippines with financial behavior, the findings suggest that developing financial education programs that foster financial literacy and financial attitudes and self-efficacy is crucial to encourage migrant workers to self-monitor their financial behavior. Having taken financial education was not significantly related to financial behaviors. This could be influenced by the quality of financial education programs, such as their content, duration, or frequency. Previous literature raises concerns about the inefficiency and inadequacy of financial education programs (Atkinson and Messy, 2015; World Bank, 2015). The effects of financial education cannot be guaranteed if the content does not equip migrant workers with necessary financial skills and promote sound financial attitudes. Previous studies show that people with low income might not show improvements in financial behavior solely by attending financial education programs (Collins, 2013; Fernandes et al., 2014; Son and Park, 2018), which could be applicable to this study as well. Doi et al. (2014) argued that providing opportunities for financial education should also target their families in the home country.

Among the demographic characteristics, marital status was related to financial behavior; however, years spent in Korea did not reveal a significant relationship with financial behavior. Unmarried participants showed less positive financial behavior, which could be due to them having fewer family obligations. For married participants, the obligations of financially supporting their families could be a motivation for sound financial behavior. Married participants are likely to send a sizable amount of their income to their family and, consequently, do not have much money left for spending in Korea (Jang et al., 2019). Unmarried participants could spend more money in Korea, which might have influenced their financial behavior.

There are varying tendencies of financial behavior and financial education needs across migrant worker groups. Supporting migrant workers and their families by fostering sound financial behavior would contribute to managing the labor market, achieving financial inclusion of the receiving country, and supporting the economy of the sending country. Therefore, both receiving and sending countries need to cooperate to promote the healthy financial behavior of migrant workers, leading to their successful return to the sending country.

There is an emerging interest in the financial welfare of migrants in Korea. For example, the Financial Supervisory Service 3 in Korea conducted a seminar on introducing financial services in Korea to migrants and helps in protecting them from financial scams. There are a few financial education programs provided by Korean institutions, such as the Financial Supervisory Service Korea, the Korea Consumer Agency, NGOs, and banks (Jang et al., 2019). However, most of the programs are for migrants who are fluent in Korean; therefore, migrant workers who have newly arrived or lack Korean language proficiency may not have access to these programs. As most reliable financial programs are provided by institutions sponsored by the Korean government or the governments of sending countries, it would be ideal for these institutions to collaborate with each other to develop accessible financial education programs in Korea in the migrants’ native languages.

The required content and delivery methods of financial education programs for migrants need to be discussed by related stakeholders. As most migrant workers are likely to stay in Korea for a substantial amount of time, it would be better to construct content applicable to Korea and their home country. Budgeting, household financial management, and managing debts could be included, whether in the Korean context or their home country’s context. Learning how to calculate currency exchange rates, methods of money transfer, and the availability of various financial services in Korea could be topics that they could benefit from knowing while staying in Korea. As many migrant workers are interested in investing and launching businesses, providing education programs that meet these needs could help increase their interest in financial education.

Limitations

There are several limitations to this study. We did not explore variables such as the amount of remittances and the participants’ post-Korea plans due to the small sample size. These limitations provide only a partial picture of migrant workers’ financial behavior. Qualitative studies could help obtain a more in-depth understanding of the difficulties OFWs may experience in Korea and considering migrants’ varying financial goals to develop better financial education programs for them.

Conclusion

The current study explored OFWs’ financial capability (i.e., financial literacy, attitudes, self-confidence, and behavior) and examined how these variables were associated with their financial behavior. Filipino migrants in the current study reported positive financial attitudes and were confident in financial management. However, their financial literacy was not sufficient to manage complex financial matters. It is interesting to note that aspects such as financial attitudes and financial self-efficacy in the Philippines were positively associated with financial behavior, while financial literacy and objective knowledge did not contribute to financial behavior. Similarly, previous exposure to financial education, which is aimed at motivating migrant workers towards sound financial behavior, did not have a significant influence on financial behavior. These findings imply that financial education programs provided to OFWs need to be more comprehensive to connect objective, cognitive financial knowledge to readiness for sound financial behavior. Despite the aforementioned limitations, this study provided an empirical basis to understand OFWs' financial capability through quantitative analyses investigating the associations among financial behavior, literacy, attitudes and self-efficacy, and education.

This study revealed that OFWs’ financial behavior was associated with their financial attitudes and self-efficacy. Future studies need to examine if the financial behavior and related variables vary depending on migrant workers’ countries of origin. It would also be interesting to compare the results of this study with those of Filipino migrants in other countries of destination.

Footnotes

Acknowledgments

This manuscript is an updated and revised version of the Migration Research and Training Centre Working Paper “Factors related to the financial capacity of Filipino workers in South Korea” (Series No.2020-03). The authors thank the APMJ reviewers for their useful comments and recommendations

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.