Abstract

The Sarbanes–Oxley Act of 2002 (SOX) permits the provision of tax services by auditors and restricts other major non-audit services previously provided by auditors for their audit clients. This article examines the relation between auditor-provided tax fees and audit fees after SOX. The results, using a tax fee model and an audit fee model with a larger set of non-overlapping independent variables in both models, show a positive relationship between tax and audit fees, after controlling for factors that could drive both fees. An additional test shows that firms that employ (do not employ) their incumbent auditors also for tax service are likely to pay higher (lower) audit fees than in the case when they only (also) employ their auditors for audit service. The results of other tests are also consistent with the suggestion that auditors cross-sell their non-audit services to their audit clients.

Introduction

The Sarbanes–Oxley Act of 2002 (SOX) allows the provision of tax service by incumbent auditors provided that prior approval is obtained from audit committee. At the same time, SOX prohibits many of the non-audit services previously provided by auditors. 1 In 2003, the Securities and Exchange Commission (SEC) issued revised fee disclosure rules, which, among other things, required disclosure of tax fees for the fiscal year ending December 15, 2003 (SEC, 2003). This article investigates whether auditor-provided tax fees and audit fees are jointly determined after SOX. 2 This investigation is important in three ways, which distinguish itself from prior studies.

First, prior studies (e.g., Antle, Gordon, Narayanamoorthy, & Zhou, 2006; L. Chan, Chen, Janakiraman, & Radhakrishnan, 2012; Donohoe & Knechel, 2009; Krishnan & Yu, 2011; Whisenant, Sankaraguruswamy, & Raghunandan, 2003) that examine the relation between audit fees and non-audit fees do not focus on a single non-audit fee, 3 or use a tax fee model. 4 In addition, these studies use a non-audit fee model that shares a very large set of independent variables that also appear in the audit fee model. Therefore, by construction, these variables drive both audit and non-audit fees. This article avoids this situation by focusing on one non-audit service, that is, tax service provided by incumbent auditors. Disaggregating tax service from other non-audit services could be desirable because different types of non-audit services could be determined by different factors and tax service could be more closely related to audit work than other non-audit services (see Francis, 2004; Robinson, 2008). By focusing on tax service, we are able to examine the factors that affect tax service and assess whether tax and audit service fees are determined jointly on an a priori basis. Hence, using a tax fee model would provide more unambiguous inferences of the test results.

Second, this article focuses on auditor-provided tax fees in the post-SOX period whereas prior studies focus on the pre-SOX period. For example, Omer, Bedard, and Falsetta (2006) examine the relation between auditor-provided tax fees and unexpected audit fees before SOX, and Bedard, Falsetta, Krishnamoorthy, and Omer (2010) investigate the voluntary disclosure of tax fees before SOX. Before SOX, information concerning the regulation of tax service, as a type of non-audit services, was changing rapidly and in an uncertain way due to various proposals to limit non-audit services. After SOX, tax service is allowed, thereby giving certainty to the regulatory environment. 5 Before SOX, the disclosure of auditor-provided tax fees was not required but many firms chose to voluntarily disclose them, thereby leading to a self-selection bias. SOX eliminated this self-selection bias by requiring disclosure of auditor-provided tax fees. This disclosure requirement reduces noise in the sample and, accordingly, makes the post-SOX period worthy of analysis.

Furthermore, before SOX, the focus of regulation of the provision of non-audit services of incumbent auditors was not on tax service. Hence, auditor-provided tax service fees were not singled out for disclosure by the disclosure rule of the SEC in 2000 and auditor-provided tax service is allowed by SOX. This regulatory allowance implicitly suggests that tax service would be beneficial to the performance of audit. As the SEC puts it, “the review of the registrant’s tax returns and reserves require substantial knowledge about the audit client” (Sage & Sage, 2005, p. 31). However, with the passage of time, the SEC noted the possibility of independence impairment from the provision of auditor-provided tax services and approved the rules of the Public Company Accounting Oversight Board to further limit the provision of such service (SEC, 2006). This limitation would inhibit the possible knowledge spillover effect of auditor-provided tax service on audit service, or vice versa, thereby resulting in a changed relationship between audit fees and auditor-provided tax fees. Hence, this new or renewed change in regulatory focus makes it necessary to look at again the relationship between audit fees and auditor-provided tax fees in the post-SOX period.

Last and perhaps more important, this article envisages the role of cross-selling of services could play in the relationship between auditor-provided tax fees and audit fees. Although it has long been suggested that Certified Public Accounting (CPA) firms engage in cross-selling of non-audit services to their audit clients (see Levitt, 1996), the accounting literature to date does not provide empirical evidence on the suggestion and does not examine the likely effect of cross-selling of services on the relationship between audit fees and auditor-provided non-audit fees. Drawing on the marketing literature on the bundling of services (see “Cross-selling of services” section), this article suggests that audit fees and auditor-provided tax fees, the non-audit fees that this article examines, may be positively related when cross-selling of non-audit services to audit clients creates more demand for non-audit services 6 without increased scale of economies. Therefore, a positive relationship between audit fees and tax fees or other non-audit fees could exist, with practical justifications.

Before formally testing the association of audit fees with auditor-provided tax fees, this article examines some implications of the cross-selling of services. It reports that clients that do not purchase tax service from auditors are more likely to change auditors. In addition, it finds out that the percentage of clients that purchase both audit and tax services from auditors increases monotonically from the year of auditor change to 3 or more years after the change. These results are consistent with the suggestion that cross-selling tax service to audit clients by auditors makes the clients more difficult to switch auditors for services. The results also support the suggestion that audit firms use audit service to gain incumbency and then sell tax service, or another non-audit service, subsequently to audit clients. An additional test shows that firms that employ their incumbent auditors also for tax service pay higher audit fees than in the case when they only employ their auditors for audit service, and firms that do not use auditors’ tax service pay lower audit fees than in the case had they had used tax service of auditors. Therefore, these results suggest that auditors use cross-selling of tax service to earn higher audit fees. A limitation, however, is that clients that employ tax service from a service provider other than the incumbent auditor cannot be identified because non-auditor-provided tax fees are not publicly observable, and hence, a direct comparison of the fees paid for services with and without cross-selling of services cannot be made.

To formally test the relation of audit fees with auditor-provided tax fees, this article uses two-stage-least-squares (2SLS) regression. The results show that auditor-provided tax fees and audit fees are positively related. Therefore, after controlling for common factors that could drive both audit and tax fees, there exists a positive relationship between audit fees and auditor-provided tax fees. Further tests show that the positive association only holds for clients that pay more than the median amount of auditor-provided tax fees. These results are consistent with the cross-selling of tax service by incumbent auditors to their audit clients, and more cross-selling of tax service is more likely to result in a positive relationship between audit fees and auditor-provided tax fees. Therefore, the results contribute to the literature by providing support for a positive relationship between audit and non-audit fees that could be real in practice but regarded as anomalous or spurious so far in the literature (see “Hypothesis and Regression Models” section). In addition, this article may be the first in the accounting literature, as far as the authors of this article are aware of, that tests arguments of cross-selling of services found in the marketing literature in the context of auditing. Its results also represent probably the first evidence that supports the claim that incumbent auditors cross-sell non-audit services to audit clients (see Levitt, 1996).

This article also contributes to the auditing and tax literature by devising and testing a model of tax consulting fees. The model includes various variables that proxy for the demand of tax services by clients in various aspects of operation. In contrast to prior studies (e.g., Antle et al., 2006) that use a single non-audit fee model for all non-audit services, this article establishes a tax fee model that is more firmly based on theory and specific to the provision of tax service. Whisenant et al. (2003) develop their non-audit fee model (and also audit fee model) by arguing that clients’ operating decisions are affected by agency conflicts among parties to the firms as well as firm complexity, size and risk, and auditors’ characteristics. As proxies for agency conflicts or costs, and firms’ operating characteristics are developed generally without reference to why and how non-audit services are provided by auditors, such proxies could be less relevant to non-audit fees at the end. In addition, as prior studies (e.g., Krishnan & Yu, 2011) examine non-audit fees in the aggregate, the variables included in the non-audit fee model are likely to be applicable across the broad spectrum of all non-audit services. As such, their relevance to a particular non-audit service is likely to be lower than the relevance of the variables in a tax fee model to tax service. Overall, like Simunic (1980) who devises an audit fee model from the demand side, this article develops a tax fee model from the clients’ demand for tax service that may be useful for future studies on auditor-provided tax services.

This article proceeds as follows. The next section develops the hypothesis and discusses the tax fee model and the audit fee model. To support the results reported later on, “Some Tests on the Cross-Selling of Services” section examines some implications of the cross-selling of services. “Results of Joint Determination” section discusses the results of joint determination of auditor-provided tax fees and audit fees, together with additional tests and limitations of the study. The last section concludes the findings.

Hypothesis and Regression Models

Hypothesis Development

When incumbent auditors also provide non-audit services for their clients, the knowledge obtained in conducting audit may be useful in the provision of non-audit services, or vice versa. The literature calls this possibility “knowledge spillover” (see Simunic, 1984). In other words, there is synergy in the joint provision of audit and non-audit services by incumbent auditors. If auditors pass some of the cost savings from knowledge spillover to their clients, then audit fees (or non-audit fees) would be lower than if the two services are provided by two different service providers.

Empirically, audit and non-audit fees should be negatively associated with each other if clients enjoy the benefit of knowledge spillover (see O’Keefe, Simunic, & Stein, 1994). However, prior studies have shown a positive relationship between audit and non-audit fees (e.g., Craswell & Francis, 1999; Davis, Ricchute, & Trompeter, 1993; Ezzamel, Gwilliam, & Holland, 1996; Simunic, 1984). This result is regarded as anomalous because it cannot be explained by knowledge spillover. Abdel-khalik (1990) puts this more succinctly when he writes “ . . . clients should not pay a penalty for acquiring two products from one instead of two suppliers” (p. 296). More puzzling results are reported by Palmrose (1986b) who finds a similar positive relationship between audit fees and non-auditor-provided non-audit fees (i.e., when non-audit services are provided by other, non-auditor, providers).

An intuitively appealing explanation for the positive relationship between audit and non-audit fees is that audit and non-audit services are jointly determined by some common factors. Both audit and non-audit fees increase as these common factors increase. For example, firm complexity may give rise to more audit work as well as more tax compliance work. In other words, the spurious positive relationship between audit and non-audit fees will not be observed once the effects of these common factors are controlled for. Prior studies in this area provide mixed results. First, Whisenant et al. (2003), using a 2SLS regression, report that there is no association between audit fees and auditor-provided non-audit fees after controlling for common factors that are supposed to drive the demand for both audit and non-audit services. Krishnan and Yu (2011) replicate Whisenant et al. using post-SOX data but report a negative relationship between audit and non-audit fees. However, Antle et al. (2006) report that audit fees and non-audit fees are positively related to each other in an expanded system of equations that also includes abnormal accruals as a third jointly determined variable.

The above studies use a very common set of determinants for both audit and non-audit fees. In Whisenant et al. (2003), audit report lag is in the audit fee model but not in the non-audit fee model, and a variable for new financing is in the non-audit fee model but not in the audit fee model. Thus, only audit report lag and new finance distinguish the models of audit and non-audit fees. Although 2SLS regression only requires one independent variable in each model to distinguish the models, the many variables that appear as independent variables in both models would mean that, a priori, both audit and non-audit fees are jointly determined. Empirically, this would also mean that the instruments used in 2SLS regression are weak 7 (see L. Chan et al., 2012). In addition, as non-audit services comprise a diverse set of activities, it is likely that different types of non-audit services could be determined by different sets of factors. Some of these services may share some common determinants with audit service while other types of non-audit services may not. Hence, focusing on a single non-audit service would be germane to the study of the relation between audit fees and non-audit fees paid to auditors.

Another reason that could give rise to the observed positive relationship between audit and non-audit fees is the practice of cross-selling of non-audit services by incumbent auditors to their audit clients (see Levitt, 1996). As the accounting literature does not have much discussion on the subject, this article draws on theoretical and empirical studies in the marketing literature to illustrate how audit service and tax consulting service, the non-audit service that this article focuses on, provided by auditors could be sold in a bundle and the likely effect on audit fees and auditor-provided tax service fees.

Cross-selling of services

Audit service is required by law and tax service is voluntarily purchased by clients. Hence, it is reasonable to expect that, for a CPA firm, the number of clients that purchase audit service is larger than the number of clients that purchase tax service. Alternatively, the first contact made by a CPA firm with a prospective client is via audit service. Thus, audit service is likely to be the first professional service of a CPA firm acquired by clients. Depending on the clients’ decision, tax service may be purchased from the same CPA firm or a different CPA firm. This higher demand level for audit service than for tax service makes it appealing to use audit service as the lead service to sell tax service. In the marketing literature, this form of cross-selling of services is called mixed-leader bundling (see Guiltinan, 1987).

The ability of a CPA firm to sell audit and tax services in a bundle arises from the complementarity of services. This means that services are interdependent in their demand so that clients are potential buyers of a range of services (Guiltinan, 1987). First, complementarity could arise from search economies of clients. Clients will save their time and effort in finding a CPA firm for both audit and tax services than when they find one CPA firm for each service. In the marketing literature, it is found that search economies exist when customers can purchase all the required services from the same supplier (Hoch, Bradlow, & Wansink, 1999). If a CPA firm provides audit service for its clients, then clients also save the time and effort in acquiring information about tax service available from that CPA firm than to seek out similar tax service from other CPA firms. In other words, search economies by clients increase the success of bundling of services.

Complementarity also arises at the firm level for suppliers of services. If either audit or tax service improves the overall image of the CPA firm, or enhances the credibility of the other service, then clients are likely to purchase both services from the same CPA firm than to purchase each service from two separate CPA firms. When the CPA firm is the incumbent auditor, then audit clients know already the professional competence of the CPA firm and have good impression of the firm as a whole. In the marketing literature, it is suggested that customers use reputation to select service providers from whom to purchase new services (Hitt, Bierman, Shimizu, & Kochhar, 2001). It is because service is difficult to evaluate even after purchase (in the case of audit and tax services, they are composed mainly of credence attributes) and service providers exploit this information asymmetry by providing “one-stop shopping” (i.e., selling services in a bundle; see Nayyar, 1993). Consequently, it is reasonable to expect that audit clients are likely to employ also incumbent auditors for tax or other professional services.

Apart from the complementarity of audit and tax services, the strategy of first gaining incumbency as auditors and then cross-selling tax (or other non-audit) services to audit clients also contributes to the success of bundling of services. In the marketing literature, there are studies that report that customers who are satisfied with the service quality and the value of existing services of a provider are more likely to extend the relationship through buying more services from the same service provider (see Bendapudi & Berry, 1997). These customers are also less likely to accept similar services offered by competitors (Sambandam & Lord, 1995). Therefore, if audit clients are satisfied with the performance of audits by the incumbent auditor, then they are also more likely to accept cross-selling of tax or other professional services from the same CPA firm. In other words, first gaining audit incumbency renders clients more difficult to switch to other CPA firms for non-audit services afterward.

To attract prospective clients to purchase the bundle of audit and tax services, CPA firms may discount the price of the lead service in the mixed-leader bundling form of cross-selling. Practically, this means that CPA firms lower the initial fees for audit service and then cross-sell tax service to audit clients. Although initial audit fees are lower, CPA firms would raise subsequent audit fees to cover the initial discount (i.e., there is subsequent price recovery). Therefore, on average, both audit and tax services could be charged at a margin after incumbency is gained, resulting in a positive relationship between audit fees and auditor-provided tax fees.

In addition, the marketing literature (see Nagle & Holden, 2002) suggests that customers are price-insensitive when a product has unique features that differentiate the product from other products or when customers find it difficult to compare competing products. In the case of services like audit and tax services, CPA firms could differentiate their services easily (as compared with products) and make clients difficult to evaluate competing offers. Furthermore, Nagle and Holden (2002) also contend that when customers have made sunk investment in relation to the products or when price is a signal of quality, then customers are less sensitive to the price of products. If similar reasoning applies to audit and tax services, then audit clients who have already established the relationship with the incumbent auditors are more likely to accept the fees charged by the incumbents for services. The incumbents can also use price to signal the quality of services rendered because audit and tax services are difficult to value.

A last reason that customers are price-insensitive is that customers save the time and effort in purchasing a bundle of services from the same provider. If such convenience is highly valued by customers, service providers can even charge near full price for the bundle (Taher & Basha, 2006). If this happens also to audit clients, then CPA firms can sell their services at near normal price in a bundle. All these factors may contribute to the increase in audit fees and auditor-provided tax fees, with a resultant positive relationship between the two service fees.

However, if the audit team and the tax team of the CPA firm work independently of each other, then cross-selling of tax services and economies of scale in either audit or tax work may not be present. Consequently, the relation between audit fees and auditor-provided tax fees may be determined by some common factors, for example, firm size. Overall, the relation between audit fees and auditor-provided tax fees represents the net effect of the various forces and whether audit fees are positively or negatively related to auditor-provided tax fees is an interesting empirical issue. Thus, the following hypothesis is stated in the null form as follows.

The next sub-section discusses tax services provided by incumbent auditors and the tax fee model. The audit fee model is discussed in the last sub-section.

Auditor-Provided Tax Service

Tax consulting service includes tax compliance and planning. Although the preparation of tax returns can involve a lot of time and, therefore, substantial fees, tax compliance services do not add as much value to the client as tax planning services, which help clients save money. Accordingly, tax consultants may derive higher hourly fees from planning services than from tax compliance services and, hence, actively solicit tax planning services. Tax planning services can involve many aspects of the client’s business. The more common services are discussed below.

First, clients with tax loss carryforwards (TLCF) may be able to offset current and future taxable income with the loss carryforwards. Utilization of these tax losses carryforwards may require tax planning. Tax consulting services may become more important when the loss carryforwards are large or when they are about to expire. Moreover, as there is a time limit on carrying forward tax loss, a larger loss may mean a greater real loss on tax savings if the tax loss expires.

Second, clients may distribute cash dividends to shareholders, or repurchase their own stock as a means of distribution. The choice between dividend payment and stock repurchase may require tax consulting services because dividends are taxed to shareholders differently than stock repurchases. Therefore, clients that plan to repurchase their stock may demand more tax consulting service than clients that do not plan to do so.

Third, if clients have foreign operations, they may require tax consulting service for minimizing foreign tax paid. In addition, they may receive foreign tax credit if they repatriate dividends from foreign subsidiaries or if they themselves have foreign-source income. The U.S. tax law requires that foreign income be put in “baskets” together with similar income from other foreign countries. Given these baskets, figuring out how to fully utilize foreign tax credits can be quite complicated in terms of both the amount and timing of repatriation of foreign income. Hence, clients with foreign-source income from subsidiaries or other sources may require tax consulting services to both reduce foreign tax liabilities and utilize foreign tax credits.

Tax consulting services may also be required when top managers, for example, CEO, CFO, CCO, leave the clients. Outgoing managers are paid compensation and clients have an incentive to ensure that the compensation paid is tax deductible by the clients. For example, see Internal Revenue Code (IRC) §§ 280G 4999. § 280G disallows a deduction for a “golden parachute” payment while § 4999 imposes a 20% tax on such a payment. Accordingly, tax planning services may be needed to avoid these penalties while tailoring the departing manager’s compensation package to his or her needs. In addition, § 162(m) disallows a deduction for fixed salary of the CEO and four other highest paid officers in excess of US$1 million. Compensation in excess of US$1 million must be performance-based to be deductible by the corporation. Tax consulting services may be required to ensure that these officers’ compensation packages meet these requirements.

Apart from the above circumstances, there could be other situations that require tax advice. One of these is merger. If the client is involved in merger and acquisition, tax consulting service is also required because clients may have to structure the arrangement so as to minimize the tax consequences or utilize the taxation loss. Another factor is the complexity of clients. A more complex client, for example, one with more business segments, will require more tax compliance work. Last, if the auditor is a Big 4 auditor, then the client may be more readily to employ tax services from the auditor also. Due to the higher quality service provided by a Big 4 auditor, the client may be willing to pay more for tax services offered by a Big 4 auditor.

Related tax literature

In the literature, there are several related studies that we are aware of that may be germane to the determinants of tax fees. 8 One of these is Mills, Erickson, and Maydew (1998) who take the perspective of client’s spending on tax services, either done in-house or by outside experts. Hence, their focus is not on auditor-provided tax services per se. Another is Dunbar and Phillips (2001) who investigate the outsourcing of tax service by companies. A third study is by Lassila, Omer, Shelley, and Smith (2010) who examine firms’ decision to retain incumbent auditors for tax services. A last study is McGuire, Omer, and Wang (2012) who investigate the relation between industry expertise of tax services and tax avoidance. These studies do not bear directly on the determinants of tax fees. Only some of the factors are relevant to our discussion. Similar to our discussion for firm complexity generating higher tax fees, Mills et al. (1998) report that more complex clients spend more on tax services and Lassila et al. find that higher operating complexity of clients is associated with the decision to use incumbent auditors for tax services. Three other factors in these studies are also relevant.

First, Dunbar and Phillips (2001) suggest that larger firms are likely to have their own in-house tax professionals. Therefore, they are less likely to hire outside tax consultants. Mills et al. (1998) also contend that there could be some economies of scale on clients’ spending on tax services. However, when the size of the firm is large, there may simply be higher demand for tax services. Thus, more tax services could be done either in-house or outside. Overall, the relation between tax fees and firm size is an empirical question.

Second, Mills et al. (1998) argue that clients may spend more on tax services when they have more non-current tangible assets that are granted tax allowance. Thus, firms with more property, plant, and equipment are more likely to employ tax services. We extend their argument to suggest that the level of tax fees paid to incumbent auditors would be associated with the proportion of non-current tangible assets in firms’ asset composition.

Third, Dunbar and Phillips (2001) suggest that growing firms are more likely to concentrate on the development of the firms and less likely to have in-house tax professionals to advise on tax matters. Thus, growing firms are more likely to outsource their tax compliance and planning functions. Using similar reasoning, we suggest that firms with higher growth will demand more tax consulting services from their audit firms and hence pay higher tax consulting fees than firms with low growth.

Apart from the above factors, Lassila et al. (2010) suggest that firms’ effective tax rate and opportunity of tax avoidance are likely to be associated with the employment of tax services. However, these two factors proxy for the overall likelihood of using tax services and do not relate to specific instances of employing tax services. They are added as controls in the tax fee model in the next sub-section.

Another related study is Omer et al. (2006) who examine the relation of tax consulting fees with abnormal audit fees before SOX. Some of our determinants of tax consulting fees are similar to theirs, for example, merger, firm complexity, and foreign taxation. Their use of deferred taxation is also relevant as tax advice may be needed to defer income tax liability to the future. Again, like effective tax rate and opportunity of tax avoidance, deferred taxation reflects the overall need to use tax service, and hence it is added as a control in the tax fee model discussed in this article. In addition, we make improvement on some of their variables. For example, we use TLCF in this article instead of operating loss carryforwards, which Omer et al. use. Last, we also do not include a variable for auditor tenure for which Omer et al. do not find significant results.

In the next sub-section, we build a model of tax consulting fees to examine their determinants. We do not suggest that our discussion covers every aspect of tax service and hence our model may have omitted variables. 9 Nonetheless, the purpose of the tax fee model is to have determinants of tax fees that have theoretical or practical justification but not merely empirical relation. A second purpose of the tax fee model is to have more unique variables in the tax fee model but not in the audit fee model so as to reduce the likelihood that tax fees and audit fees are jointly determined, a priori, and the possibility of having weak instruments in 2SLS regression.

Tax fee model

To examine the factors that could determine tax fees paid to incumbent auditors, we run the following tax consulting fee model by ordinary least squares (OLS) regression.

where LTAX = natural logarithm of tax consulting fees (in dollars); LTA = natural logarithm of total assets (in millions); SEGNUM = number of business segments; MERGER = 1 if the firm engages in merger or acquisition activities, or 0 otherwise; GROWTH = geometric mean growth of market value of assets from year t− 2 to year t; FTAX = 1 if the firm has paid foreign tax, or 0 otherwise; MGTOUT = number of top managers who leave the firm; COMP = number of top managers who receive annual pay exceeding US$1 million with incentive components; STKRP = 1 if the firm repurchases its own stock, or 0 otherwise; LTLCF = natural logarithm of one plus tax loss carryforwards (in millions) from previous years; BIG4 = 1 if the firm’s auditor is a Big 4 auditor, or 0 otherwise; DTAX = ratio of deferred taxes to the absolute value of total income taxes; CAPINT = ratio of gross property, plant, and equipment to total assets; ETR = ratio of total income taxes less deferred taxes to the absolute value of pre-tax income; TAVOID = ratio of cash taxes paid to the absolute value of pre-tax income net of special items.

In Model 1, all variables are measured for the current year, unless stated otherwise. The dependent variable is the natural logarithm of tax consulting fees (LTAX). The other variables are determinants of LTAX. As the factors that could affect tax fees are discussed earlier in the article, the discussion here only focuses on the sign of the coefficients. First, we do not have expectations for the sign of a1 as there is no a priori relationship of firm size (LTA) with tax fees. Similarly, we do not have expectations for the sign of a12 and a14. It is because capital intensity (CAPINT) and tax avoidance opportunity (TAVOID) may be positively or negatively related to the level of tax fees, depending on firms’ particular asset structure and tax position. All other coefficients in Model 1 are predicted to be positive as the related variables proxy for the likelihood of using more tax services. In other words, more complex firms (SEGNUM), firms engaged in merger (MERGER), faster growing firms (GROWTH), and firms with foreign operation (FTAX) or tax loss carryforwards (LTLCF) are more likely to use more tax services. Likewise, firms with more managers leaving the firms (MGTOUT) or having annual compensation exceeding US$1 million with incentive component (COMP), firms that repurchase their stocks (STKRP), firms with Big 4 auditors (BIG4), and firms with higher deferred tax position (DTAX) or effective tax rate (ETR) are also more likely using more tax services. Model 1 will also be run with year dummy variables to capture time-specific effects. 10 For the sake of parsimony of space, the results of the year dummy variables are not reported in the article.

The sample consists of observations for the fiscal years 2004 to 2008. Year 2004 is the first full year when firms are required to disclose tax fees paid to incumbent auditors. 11 Tax fee data and details of top management changes are obtained from the Audit Analytics database. Information on management compensation is obtained from proxy statements available from the EDGAR database. Other data are obtained from COMPUSTAT.

Audit Fee Model

Simunic (1980) develops a model of audit fees, which is adopted and expanded by other studies. Earlier work includes Francis (1984), Firth (1985), Palmrose (1986a), and P. Chan, Ezzamel, and Gwilliam (1993). Simunic and Stein (1996) suggest that audit fees are determined by the effort level and expected liability loss of the auditors. Audit effort is affected by firm size, complexity, and audit risk of clients. Liability exposure is related to factors such as reported loss of the clients and leverage. Both audit effort and liability loss increase audit fees. Later studies add other variables to the audit fee model. For example, Craswell, Francis, and Taylor (1995) report that auditor reputation and industry specialization increase audit fees. Carcello, Hermanson, Neal, and Riley (2002) examine the effect of board monitoring on audit fees. They report that audit fees are positively associated with some board characteristics (e.g., board independence and expertise).

Hay, Knechel, and Wong (2006) survey prior studies that use the audit fee model and classify factors that affect audit fees into more than 15 categories. The major ones are firm size, complexity, inherent risk, profitability, leverage, ownership, internal control, auditor quality, audit problems, and non-audit services. Within each category, there are many different measurements of the same variables. In a meta-analysis, Hay et al. report that many variables have consistent results across the empirical studies covered but some others do not (e.g., a reported loss by the client, leverage, internal auditing, corporate governance, auditor specialization, and audit opinion).

It appears that some of the categories or broad factors may determine audit fees but not tax consulting fees. An obvious example is audit problem of clients. In addition, tax consultants are likely to charge the same fee regardless of their clients having high or low inherent risk. Tax consulting fees are also not likely to be affected by the structure of ownership and internal control of clients. Profitability and the level of debt of tax clients also do not affect the level of, and hence the fees charged for, tax consulting services. Hence, intuitively, audit fees and tax consulting fees are not driven by a common set of firm characteristics. In other words, it is likely that audit and tax services are of different nature and require different types of expertise, and they are not jointly determined.

To examine the relation between tax fees and audit fees, the following audit fee model is used. It should be noted that not all available variables are used as it is not practical to do so.

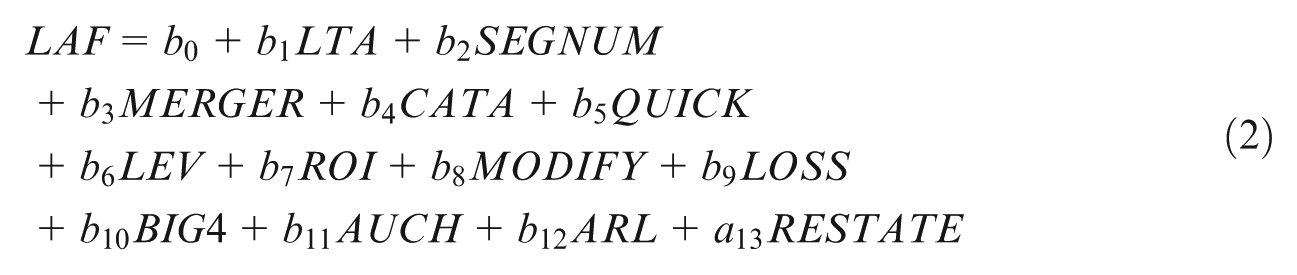

where LAF = natural logarithm of audit fees (in dollars); LTA = as defined in Model 1; SEGNUM = as defined in Model 1; MERGER = as defined in Model 1; CATA = ratio of current assets to total assets; QUICK = ratio of current assets minus inventories, to current liabilities; LEV = ratio of long-term debt to total assets; ROI = COMPUSTAT ROI defined as earnings before extraordinary item divided by the total of long-term debt and book value of preferred stock and common equity, and expressed in percentage; MODIFY = 1 if the firm receives a modified audit opinion, or 0 otherwise; LOSS = 1 if the firm has a reported loss, or 0 otherwise; BIG4 = as defined in Model 1; AUCH = 1 if the firm changes auditor, or 0 otherwise; ARL = number of days between fiscal year end and audit report date; RESTATE = 1 if the firm restates its audited financial statements, or 0 otherwise.

In the audit fee model, all variables are measured for the current year. The dependent variable is the natural logarithm of audit fees (LAF). Other variables are added as controls in the model. As larger firms (LTA) require more audit work (Simunic, 1980), we expect b1 to be positive. Firms with more business segments (SEGNUM) are more complex (Carcello et al., 2002) and we expect b2 to be positive also. Firms that are involved in merger or acquisition activities (MERGER) also require more audit work and hence b3 is expected to be positive. Highly levered firms (LEV), firms with modified audit opinions (MODIFY), and firms with a reported loss (LOSS) increase the audit firms’ litigation risk (see Simunic & Stein, 1996). Hence, we expect b6, b8, and b9 to be positive. More current assets in the firms’ asset composition (CATA) increase audit risk (Turpen, 1990) and b4 is expected to be positive. Firms with less liquid assets (QUICK) are more risky and b5 is expected to be negative. The higher the accounting return (ROI), the more the risk sharing between auditor and client, and hence the lower the audit fees (Craswell & Francis, 1999). Thus, b7 is expected to be negative. As Big 6 (now Big 4) auditors (BIG4) charge higher audit fees because of their higher reputation (see Craswell et al., 1995), we expect b10 to be positive.

Last, auditors are likely to charge lower audit fees for initial engagements (AUCH; Craswell & Francis, 1999) and thus, b11 is expected to be negative. Firms with longer audit report lag (ARL) are likely to pay higher audit fees (Whisenant et al., 2003) and so are firms with restatement of audited financial statements (RESTATE; Stanley & DeZoort, 2007). Thus, b12 and b13 are expected to be positive. As with Model 1, Model 2 will also be run with year dummy variables to capture time-specific effects. For the sake of parsimony of space, the results of the year dummy variables are not reported in the article.

The sample period for Model 2 is 2004 to 2008, the same period for the tax fee Model 1 as we are interested in their possible joint determination. Model 2 will be run together with Model 1 by 2SLS regression, which consists of two steps. In the first step, tax fees (LTAX) and also audit fees (LAF) are expressed in terms of the reduced form of the models, which consists of all the independent variables in Models 1 and 2. Then, the predicted value of tax fees (called PLTAX) and the predicted value of audit fees (called PLAF) are calculated from regression results on the reduced form. In the second step, PLTAX is added to Model 2 and PLAF is added to Model 1 to examine the relation between tax fees and audit fees.

All data for Model 2 are obtained from COMPUSTAT except for audit fees, which are obtained from the Audit Analytics database. As financial firms might have financial and operating characteristics that are not similar to other firms, they are excluded from the sample for Model 2.

Some Tests on the Cross-Selling of Services

Before proceeding to test the relation of auditor-provided tax fees with audit fees, it is desirable to explore some implications from the literature on cross-selling of services. The purpose is to lend credence to the results reported later on in “Results of Joint Determination” section. The first area of investigation is auditor switch. The second area is estimated audit fees of clients if they had made the opposite hiring or not hiring decision for tax services of incumbent auditors.

Auditor Switch

If audit clients are more likely to purchase non-audit services, including tax service, from the same CPA firm who is the incumbent auditor because of search economies or switching costs than from other CPA firms, then clients who purchase both audit and tax services from the same CPA firm are less likely to change auditors. In addition, if a CPA firm first sells audit service to clients and then cross-sell non-audit services, for example, tax service, to audit clients subsequently, then the percentage of audit clients purchasing tax service is likely to be increasing over time since auditor change.

To investigate the above two implications of the cross-selling of services, a sample of auditor change is used. First, the following auditor change model is run by logistic regression to examine whether cross-selling tax services to audit clients makes clients less likely to change auditors.

where AUCH = as defined in Model 2; LTA = as defined in Model 1; LEV = as defined in Model 2; GROWTH = as defined in Model 1; PZS = Z score in year t− 1; PBETA = COMPUSTAT beta in year t− 1; PLOSS = 1 if the firm has a reported loss in year t− 1, or 0 otherwise; PMODIFY = 1 if the firm receives a modified audit opinion in year t− 1, or 0 otherwise; RESTATE = as defined in Model 2; INCFEE = ratio of audit fees in year t minus audit fees in year t− 1, to audit fees in year t− 1; PBIG4 = 1 if the firm’s auditor is a Big 4 auditor in year t− 1, or 0 otherwise; PNOTAX = 1 if the firm reports zero tax fees paid to the incumbent auditor in year t− 1, or 0 otherwise.

Except stated otherwise, the variables are measured for the current year. The dependent variable in Model 3 is AUCH, which is equal to 1 if the firms have new auditors in current year, or 0 otherwise. The variable of interest is PNOTAX, which is equal to 1 if the firms do not pay incumbent auditors for tax services in last year, or 0 otherwise. If it is easier for clients who do not employ their incumbent auditors for tax services to change auditors, then c11 is expected to be positive.

Other variables are added as controls in Model 3. As larger firms (LTA) may have higher switching costs (DeAngelo, 1981), they may be less likely to change auditors and c1 is expected to be negative. 12 Firms with higher leverage (LEV) have higher financial risk (Johnstone & Bedard, 2004). Thus, they are more likely to be dropped by their auditors and c2 is expected to be positive. Firms with higher growth (GROWTH) are more likely to have auditor changes because of higher audit risk (Landsman, Nelson, & Rountree, 2009). Hence, c3 is expected to be positive.

The variables PZS and PBETA control for auditor change due to clients’ litigation risk (Krishnan & Krishnan, 1997). Clients that are likely to go bankrupt (with lower Z score, PZS) are more likely to be involved in litigation (see Stice, 1991). The variable PBETA is a market measure of litigation risk used in prior studies (e.g., Shu, 2000). Hence, c4 is expected to be negative and c5 is expected to be positive. The variable PLOSS and PMODIFY control for clients’ change of auditors because of a reported loss and the receipt of modified audit opinions, respectively (see Chow & Rice, 1982). Both c6 and c7 are expected to be positive.

Clients may also change auditors because of restatement of financial statements (RESTATE; see Mande & Son, 2013) and c8 is expected to be positive. In addition, clients may change auditors because of changes in audit fees (INCFEE) and no expectation is formulated for the sign of c9 as clients may or may not be successful in obtaining lower increase in audit fees after the switch. Last, switching rate among Big 4 clients may be different from switching rate among non-Big 4 clients. The variable PBIG4 captures such possible difference in switching rate and no expectation is formulated for the sign of c10. Model 3 will also be run with year dummy variables to capture time-specific effects and for the sake of parsimony of space, the results of which are not reported in this article.

The sample selection for Model 3 began from COMPUSTAT. The number of available observations for 2004 to 2008 is 12,386. Then, data for auditors’ fees were extracted from the Audit Analytics database. The sample size was reduced to 10,854 because of missing information on auditors’ fees. After deleting observations which were more than four standard deviations from the mean of the continuous variables to control for the effect of possible outliers, the final sample consists of 10,644 firm-year observations. In this sample, 8.7% of the firms change auditors and 20% of the firms did not employ incumbent auditors for tax services in last year. 13

Table 1 reports the results of logistic regression on Model 3. Larger firms (LTA) are less likely to change auditors. However, highly levered firms (LEV) and high growth firms (GROWTH) are more likely to switch auditors. As expected, firms with restatements of financial statements (RESTATE) are more likely to experience auditor changes. Finally, firms with increase in audit fees (INCFEE) and firms audited by Big 4 auditors (PBIG4) are less likely to be associated with change of auditors. More importantly, clients that do not employ their auditors for tax services (PNOTAX) are more likely to change auditors. This last result suggests that cross-selling tax service to audit clients by auditors renders clients more dependent on auditors for services and less likely to switch service providers.

Results of Logistic Regression on Auditor Change (n = 10,644).

Note. The dependent variable is change of auditor, AUCH. The regression includes year dummy variables, the results of which are not reported. NA = not applicable. The variables are defined as follows: AUCH = 1 if the firm changes auditor, or 0 otherwise; LTA = natural logarithm of total assets; LEV = ratio of long-term debt to total assets; GROWTH = geometric mean growth of market value of assets from year t − 2 to year t; PZS = Z score in year t − 1; PBETA = COMPUSTAT beta in year t − 1; PLOSS = 1 if the firm has a reported loss in year t − 1, or 0 otherwise; PMODIFY = 1 if the firm receives a modified audit opinion in year t − 1, or 0 otherwise; RESTATE = 1 if the firm restates its financial statements, or 0 otherwise; INCFEE = ratio of audit fees in year t minus audit fees in year t − 1, to audit fees in year t − 1; PBIG4 = 1 if the firm’s auditor is a Big 4 auditor in year t − 1, or 0 otherwise; PNOTAX = 1 if the firm reports zero tax fees paid to the incumbent auditor in year t − 1, or 0 otherwise.

and *** designate two-tailed statistical significance at the .05 and .01 levels, respectively.

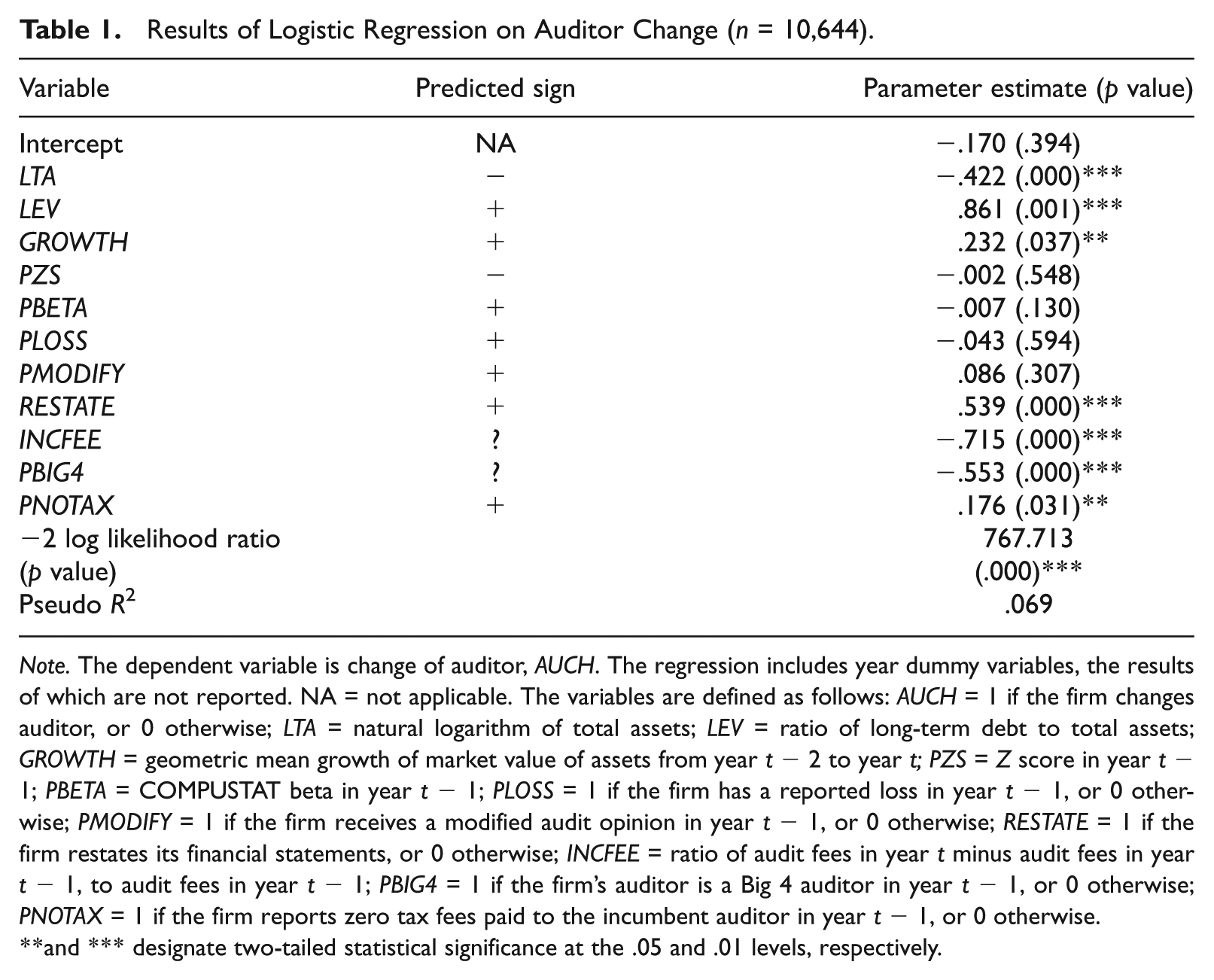

Next, to investigate the suggestion that CPA firms first gain incumbency as auditors and then cross-sell tax service to their clients, the proportion of clients, from the sample for Model 3, that employ their incumbent auditors for tax service is calculated and reported in Table 2. In Panel A, 51% of the clients that switch auditors also employ their auditors for tax service in the year of change. This percentage is significantly lower than the percentage in years after auditor change. Panel B further divides all other years into 1, 2, and 3 or more years after auditor change. The percentage of clients employing both audit and tax services from auditors increases monotonically from 51 in the year of auditor change to 61 in 1 year after, then to 71 in 2 years after, and finally to 79 in 3 or more years after the change. These differences in percentages over time are statistically significant. Therefore, the results suggest that auditors use audit service as the first step to gain incumbency and then sell tax service subsequently. Thus, audit service is the lead service in the mixed-leader bundling form of cross-selling of services.

Clients That Purchase Tax Services From Incumbent Auditors (n = 10,644).

Note. In both panels, the p value of a χ2 test of no association between the number of years after auditor change and the number of clients that purchase tax services from incumbent auditors is reported.

Estimated Audit Fees

In the literature on cross-selling of services, an incentive for service providers to sell services in a bundle is the possibility that the services could be charged at higher prices. In other words, customers who enjoy “one-stop” shopping may be paying more instead of less on services that could be purchased from two or more separate service providers. As the prices paid for services from a separate provider are not observable for customers who purchase services in a bundle, the comparison of prices paid for bundled services and unbundled services can only be made by estimating the prices that could have been paid by customers if they had made the opposite purchasing decision. In the context of audit and tax services, we estimate the audit fees that would have been paid by clients that do not employ their auditors for tax service if they had, instead, used their auditors’ tax service, and vice versa.

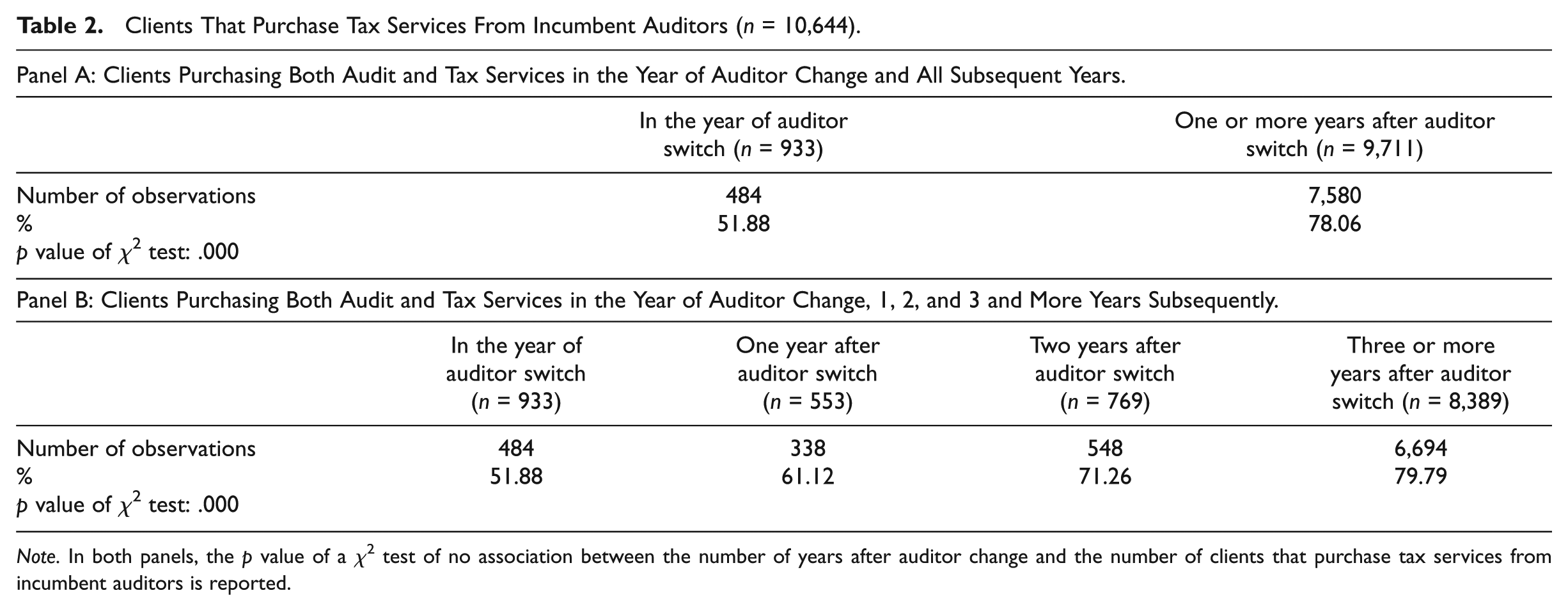

To proceed, audit fees are estimated by Model 2 with control for self-selection. Such a control is necessary as clients have the freedom to engage their auditors for tax service or not and their decision may affect the prices they pay for audit or tax services (see Abdel-khalik, 1990). In line with Lassila et al. (2010), the following choice model for tax service is run by probit regression. The control for self-selection is done by estimating the Inverse Mills ratio (IMR) from the results of the probit regression. 14

where PURE = 1 if the firm reports zero tax fees paid to auditor, or 0 otherwise; LTA = as defined in Model 1; MERGER = as defined in Model 1; FTAXAT = ratio of foreign tax to total assets; FTAX = as defined in Model 1; LTLCF = as defined in Model 1; CAPINT = as defined in Model 1; ETR = as defined in Model 1; TAVOID = as defined in Model 1.

In Model 4, the dependent variable is PURE. It is equal to 1 if the firm does not employ auditor-provided tax service, or 0 otherwise. As PURE is the complement of AUDTX used by Lassila et al. (2010), the predicted sign, if applicable, of the right-hand-side variables in Model 4 is opposite to the sign predicted for the relevant variables by Lassila et al. In addition, we make improvement to the dummy variable for TLCF used by Lassila et al. by measuring TLCF as a continuous variable (LTLCF). We also do not use variables for leverage, auditor tenure, and audit fees for which Lassila et al. do not find significant results. 15

The expectation for the sign of the variables in Model 4 is explained below. First, firms with foreign tax paid (FTAXAT and FTAX) and higher tax loss carryforwards (LTLCF) have higher demand for tax services. Therefore, they are less likely to employ their auditors for audit service only. Thus, d3, d4, and d5 are expected to be negative. Similarly, as larger firms (LTA) and firms engaged in merger activities (MERGER) have higher demand for tax service, they are also less likely to employ their auditors for audit service only. Hence, d1 and d2 are also expected to be negative. In addition, firms with higher effective tax rate (ETR) are likely to employ tax service to reduce tax paid. Thus, d7 is also expected to be negative. Last, no expectation is formulated for the sign of d6 and d8 as the opportunity to use tax service to reduce or avoid tax paid depends on specific situations in which accounting depreciation differs from tax depreciation (CAPINT) and tax avoidance schemes (TAVOID) are challenged by regulators. Model 4 will also be run with year dummy variables to capture time-specific effects. For the sake of parsimony of space, the results of the dummy variables are not reported in this article.

Observations available from COMPUSTAT to run Model 4 were collected. The initial sample consists of 8,737 firm-year observations from 2004 to 2008. Data on auditors’ fees were then extracted from the Audit Analytics database. The sample was reduced to 8,464 observations because of missing information. After deleting observations that were more than four standard deviations from the mean of the continuous variables, the sample consists of 2,288 and 6,019 observations with zero and non-zero tax fees paid to incumbent auditors, respectively. 16

The results of probit regression on Model 4 are reported in Table 3. As expected, larger firms (LTA) have higher demand for professional tax service and are less likely to employ their auditors for audit service only. Similarly, firms with foreign tax paid (FTAXAT and FTAX) are also less likely to use only audit service of auditors. Last, firms with higher amount of tax loss carryforwards (LTLCF) and higher effective rate (ETR) are likely to benefit more from professional tax service, and hence they are less likely to use only audit service of auditors.

Results of Probit Regression on Employment of Tax Service From Incumbent Auditor (n = 8,307).

Note. The dependent variable is no employment of auditor-provided tax service, PURE. The regression includes year dummy variables, the results of which are not reported. NA = not applicable. The variables are defined as follows: PURE = 1 if the firm reports zero tax fees paid to auditor, or 0 otherwise; LTA = natural logarithm of total assets (in millions); MERGER = 1 if the firm engages in merger or acquisition activities, or 0 otherwise; FTAXAT = ratio of foreign tax to total assets; FTAX = 1 if the firm has paid foreign tax, or 0 otherwise; LTLCF = natural logarithm of one plus tax loss carryforwards (in millions) from previous years; CAPINT = ratio of gross property, plant, and equipment to total assets; ETR = ratio of total income taxes less deferred taxes to the absolute value of pre-tax income; TAVOID = ratio of cash taxes paid to the absolute value of pre-tax income net of special items; L. R. = Likelihood Ratio.

and *** designate two-tailed statistical significance at the .05 and .01 levels, respectively.

The variable IMR was estimated from the results of Table 3 and added to the audit fee model. Data available for the audit fee model were collected from COMPUSTAT and the Audit Analytics database for 2004 to 2008. The initial sample consists of 4,638 and 1,557 observations with and without auditor-provided tax service, respectively. After deleting as potential outliers observations at more than four standard deviations from the mean of the continuous variables, the final sample consists of 4,465 and 1,508 observations with and without auditor-provided tax service, respectively. Yearly regressions were run for the two sub-samples separately to generate parameter estimates for calculating the audit fees that would have been paid by clients had they had made the opposite purchasing decision for tax service of auditors.

To proceed, the audit fees that would have been paid by firms that employ their auditors for tax service had they had not used such service of auditors are estimated by multiplying the values of the firms’ characteristics in a year with the estimated coefficients of the parameters obtained from the same year’s regression using firms that report zero tax fees. Then, the estimated audit fees of each firm are subtracted from the actual audit fees of the same firm to arrive at the difference in audit fees (ADDAF). 17

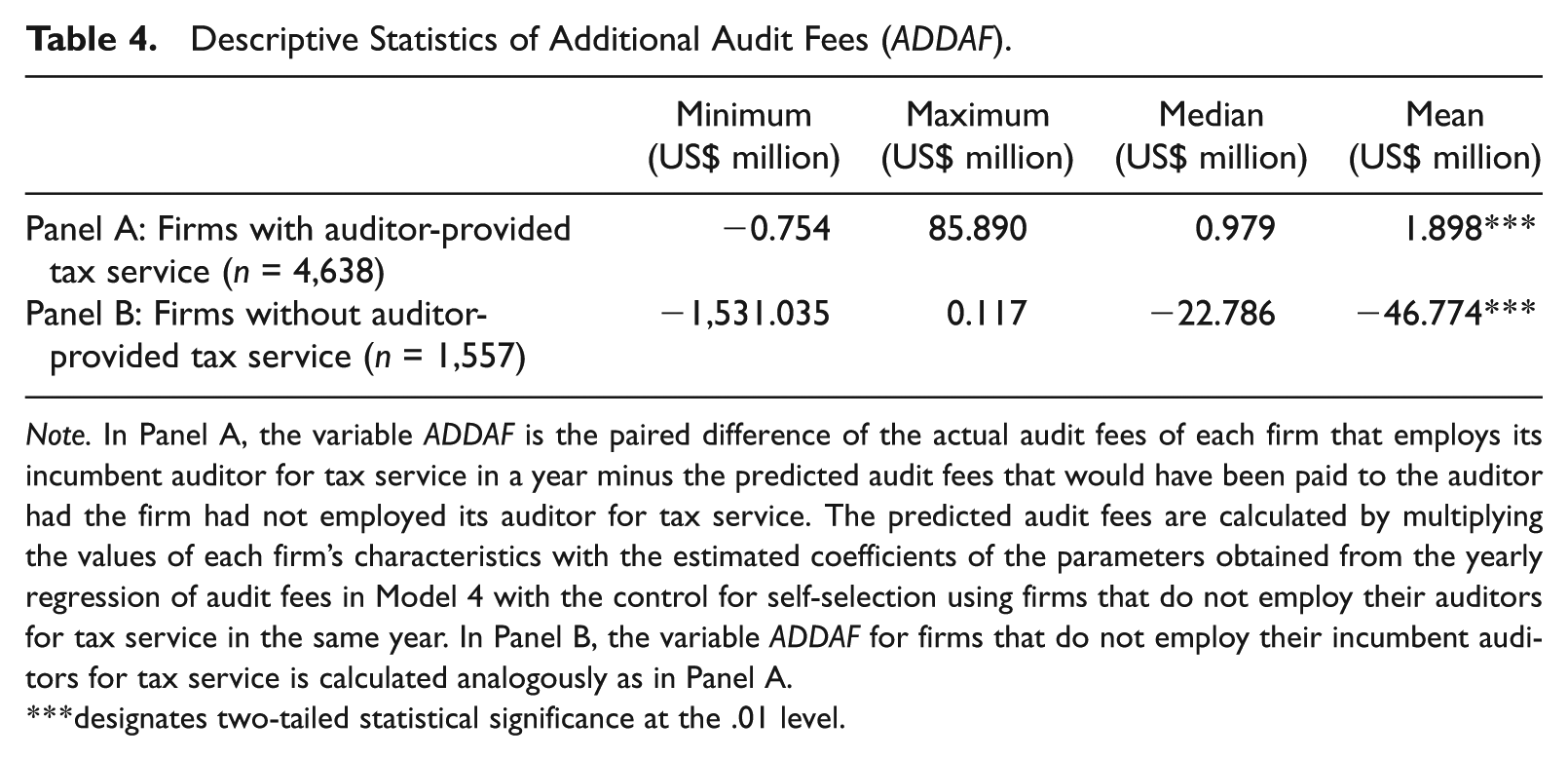

Table 4 reports some descriptive statistics of ADDAF. In Panel A for firms that purchase auditor-provided tax service, ADDAF has a range of −US$0.75 million to US$85.89 million. Therefore, some firms pay lower audit fees than estimated had they had not employed auditor-provided tax service while some firms pay higher audit fees when they employ such service. In addition, the median and the mean are both positive. Hence, there are more sample firms that pay higher audit fees than estimated, and on average, the audit fees are higher when firms employ their auditors for both audit and tax services. Furthermore, the mean of ADDAF is significantly different from zero. This result suggests that it would be more likely than unlikely that firms would pay higher audit fees when they employ their auditors for both audit and tax services.

Descriptive Statistics of Additional Audit Fees (ADDAF).

Note. In Panel A, the variable ADDAF is the paired difference of the actual audit fees of each firm that employs its incumbent auditor for tax service in a year minus the predicted audit fees that would have been paid to the auditor had the firm had not employed its auditor for tax service. The predicted audit fees are calculated by multiplying the values of each firm’s characteristics with the estimated coefficients of the parameters obtained from the yearly regression of audit fees in Model 4 with the control for self-selection using firms that do not employ their auditors for tax service in the same year. In Panel B, the variable ADDAF for firms that do not employ their incumbent auditors for tax service is calculated analogously as in Panel A.

designates two-tailed statistical significance at the .01 level.

Following similar procedures, the variable ADDAF was calculated for firms without auditor-provided tax service. It represents the additional audit fees that would have been paid had they had instead used tax service of incumbent auditors. The results are reported in Panel B. Both the median and the mean are negative. The mean is also statistically different from zero. These results suggest that firms without tax service of auditors are likely to pay higher audit fees had they instead used the tax service than the actual audit fees they currently pay. Once again, the results indicate that it is more likely than unlikely that clients pay more for audit service when they also use their auditors for tax service. They are consistent with the cross-selling of services by auditors to their audit clients, thereby increasing the demand for both services. Hence, audit fees and tax fees are likely to be positively related. The next section investigates the issue formally.

Results of Joint Determination

Sample Selection and Descriptive Statistics

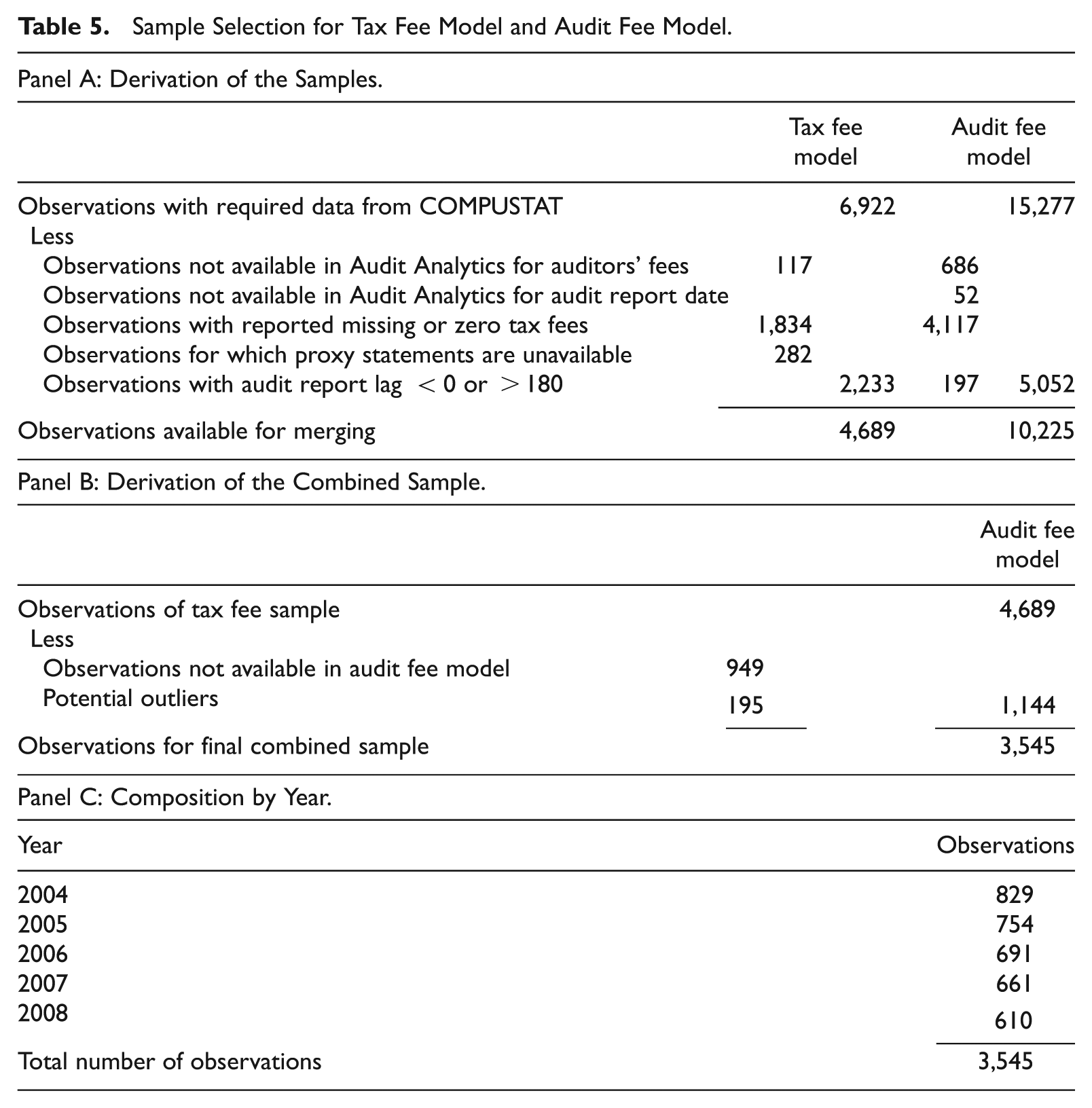

To test directly the relationship between audit fees and auditor-provided tax fees, observations for Models 1 and 2 were collected. Table 5 shows the sample selection. As shown in Panel A, observations with available data for the tax fee model and the audit fee model were collected from COMPUSTAT. 18 Then, the observations were merged with those on the Audit Analytics database. Observations without data on auditors’ fees and audit report date were dropped. Next, the samples were restricted to observations with reported non-zero tax fees. For the tax fee model, proxy statements available from the EDGAR database were searched for information on management compensation and observations without the required proxy statements or information were deleted. For the audit fee model, observations were limited to those with reasonable audit report lag (i.e., non-negative and shorter than 180 days). The final sample for the tax fee model and the audit fee model consists of 4,689 and 10,225 firm-year observations, respectively. 19 In Panel B, the samples were merged. After deleting observations that were greater than four standard deviations from the mean of the continuous variables, the combined sample consists of 3,545 firm-year observations. Panel C gives the yearly composition of the sample and no particularly large clustering of the observations is observed.

Sample Selection for Tax Fee Model and Audit Fee Model.

Table 6 shows the descriptive statistics of the variables of the combined sample. The fee variables, asset size, and TLCF are expressed in monetary terms. The mean value of tax fees (TAX) is US$281,332. The average firm has total assets (AT) of US$2,866 million. On average, the firms have two business segments (SEGNUM). Nineteen percent of the sample firms are involved in merger or acquisition (MERGER). Forty-eight percent of them have repurchased their own stock (STKRP) and 86% of them are audited by Big 4 auditors (BIG4). The average TLCF is US$217 million. Sixty-one percent of the firms have paid foreign tax (FTAX). Management turnover of the firms is low (MGTOUT) and the average firm has two managers with total pay exceeding US$1 million including incentive components (COMP). Gross property, plant, and equipment constitute 50% of total assets (CAPINT). The average effective tax rate (ETR) is 28%.

Selected Descriptive Statistics of the Variables of the Combined Sample (n = 3,545).

Note. SD = standard deviation. NA = not applicable. The variables are defined as follows: TAX = tax consulting fees (in dollars); TA = total assets (in millions); SEGNUM = number of business segments; MERGER = 1 if the firm engages in merger or acquisition activities, or 0 otherwise; GROWTH = geometric mean growth of market value of assets from year t− 2 to year t; FTAX = 1 if the firm has paid foreign tax, or 0 otherwise; MGTOUT = number of top managers who leave the firm; COMP = number of top managers who receive annual pay exceeding US$1 million with incentive components; STKRP = 1 if the firm repurchases its own stock, or 0 otherwise; TLCF = tax loss carryforwards (in millions) from previous years; BIG4 = 1 if the firm’s auditor is a Big 4 auditor, or 0 otherwise; DTAX = ratio of deferred taxes to the absolute value of total income taxes; CAPINT = ratio of gross property, plant, and equipment to total assets; ETR = ratio of total income taxes less deferred taxes to the absolute value of pre-tax income; TAVOID = ratio of cash taxes paid to the absolute value of pre-tax income net of special items; AF = audit fees (in dollars); CATA = ratio of current assets to total assets; QUICK = ratio of current assets minus inventories, to current liabilities; LEV = ratio of long-term debt to total assets; ROI = earnings before extraordinary item divided by the total of long-term debt and book value of preferred stock and common equity, and expressed in percentage; MODIFY = 1 if the firm receives a modified audit opinion, or 0 otherwise; LOSS = 1 if the firm has a reported loss, or 0 otherwise; AUCH = 1 if the firm changes auditor, or 0 otherwise; ARL = number of days between fiscal year end and audit report date; RESTATE = 1 if the firm restates its audited financial statements, or 0 otherwise.

The descriptive statistics of the variables that are specific to the audit fee model is shown in the lower part of Table 6. The sample firms pay higher average audit fees than average tax fees (TAX). They are liquid (CATA and QUICK) and have low leverage (LEV). Twenty-one percent of the firms have a reported loss (LOSS) and, on average, profitability is low (ROI). Fifty-three percent of the firms have audit modifications of all types (MODIFY) and 6% of them have auditor changes (AUCH). The average audit report lag (ARL) is 64 days after the year end and 9% of the firms have restated their audited financial statements (RESTATE).

OLS and 2SLS Results

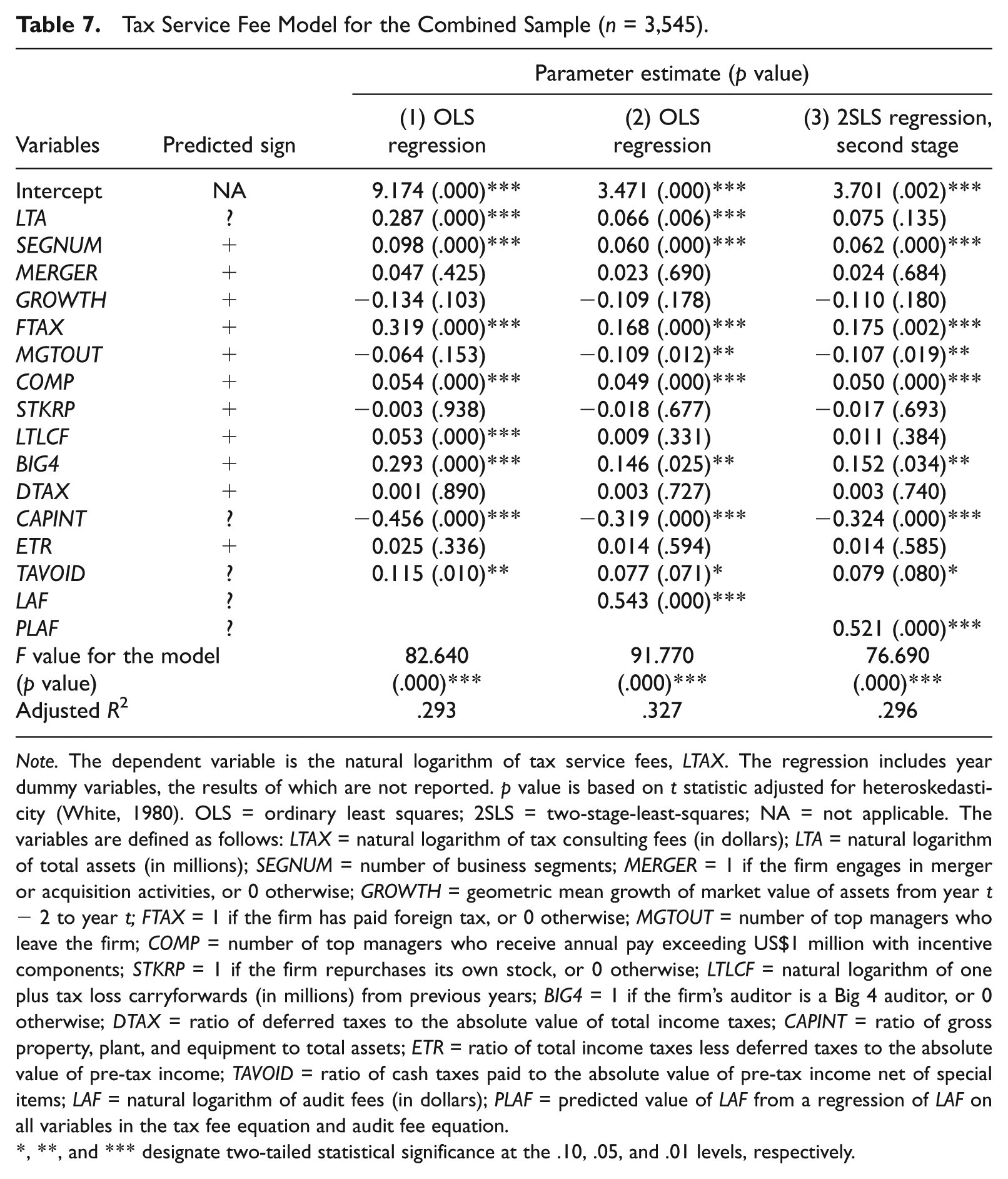

The regression results of the tax fee model are reported in Table 7. Results using OLS regressions are reported in columns (1) and (2) for the sake of comparison. Results of the second stage of 2SLS regression are reported in column (3). In column (1), only the control variables are added. As shown, the variables LTA, SEGNUM, FTAX, COMP, LTLCF, BIG4, and TAVOID are positive as expected (except for LTA and TAVOID where no prediction is made) and significant in the regression. In addition, the variable CAPINT is significantly negative. Hence, larger firms and more complex firms are likely to pay higher tax fees to their incumbent auditors because of higher demand for tax services. In addition, firms with more employees with annual pay exceeding US$1 million including incentive components are likely to pay higher tax fees for structuring the compensation packages. Firms with foreign operation and TLCF also require tax planning services to minimize tax paid, and thus, they pay higher tax fees. Last, Big 4 auditors charge higher tax fees to their audit clients because of their brand name or more quality services than non-Big 4 auditors. Firms with higher likelihood for tax allowance for tangible assets and firms with higher opportunity of tax avoidance are also associated with higher tax fees paid to incumbent auditors.

Tax Service Fee Model for the Combined Sample (n = 3,545).

Note. The dependent variable is the natural logarithm of tax service fees, LTAX. The regression includes year dummy variables, the results of which are not reported. p value is based on t statistic adjusted for heteroskedasticity (White, 1980). OLS = ordinary least squares; 2SLS = two-stage-least-squares; NA = not applicable. The variables are defined as follows: LTAX = natural logarithm of tax consulting fees (in dollars); LTA = natural logarithm of total assets (in millions); SEGNUM = number of business segments; MERGER = 1 if the firm engages in merger or acquisition activities, or 0 otherwise; GROWTH = geometric mean growth of market value of assets from year t− 2 to year t; FTAX = 1 if the firm has paid foreign tax, or 0 otherwise; MGTOUT = number of top managers who leave the firm; COMP = number of top managers who receive annual pay exceeding US$1 million with incentive components; STKRP = 1 if the firm repurchases its own stock, or 0 otherwise; LTLCF = natural logarithm of one plus tax loss carryforwards (in millions) from previous years; BIG4 = 1 if the firm’s auditor is a Big 4 auditor, or 0 otherwise; DTAX = ratio of deferred taxes to the absolute value of total income taxes; CAPINT = ratio of gross property, plant, and equipment to total assets; ETR = ratio of total income taxes less deferred taxes to the absolute value of pre-tax income; TAVOID = ratio of cash taxes paid to the absolute value of pre-tax income net of special items; LAF = natural logarithm of audit fees (in dollars); PLAF = predicted value of LAF from a regression of LAF on all variables in the tax fee equation and audit fee equation.

, **, and *** designate two-tailed statistical significance at the .10, .05, and .01 levels, respectively.

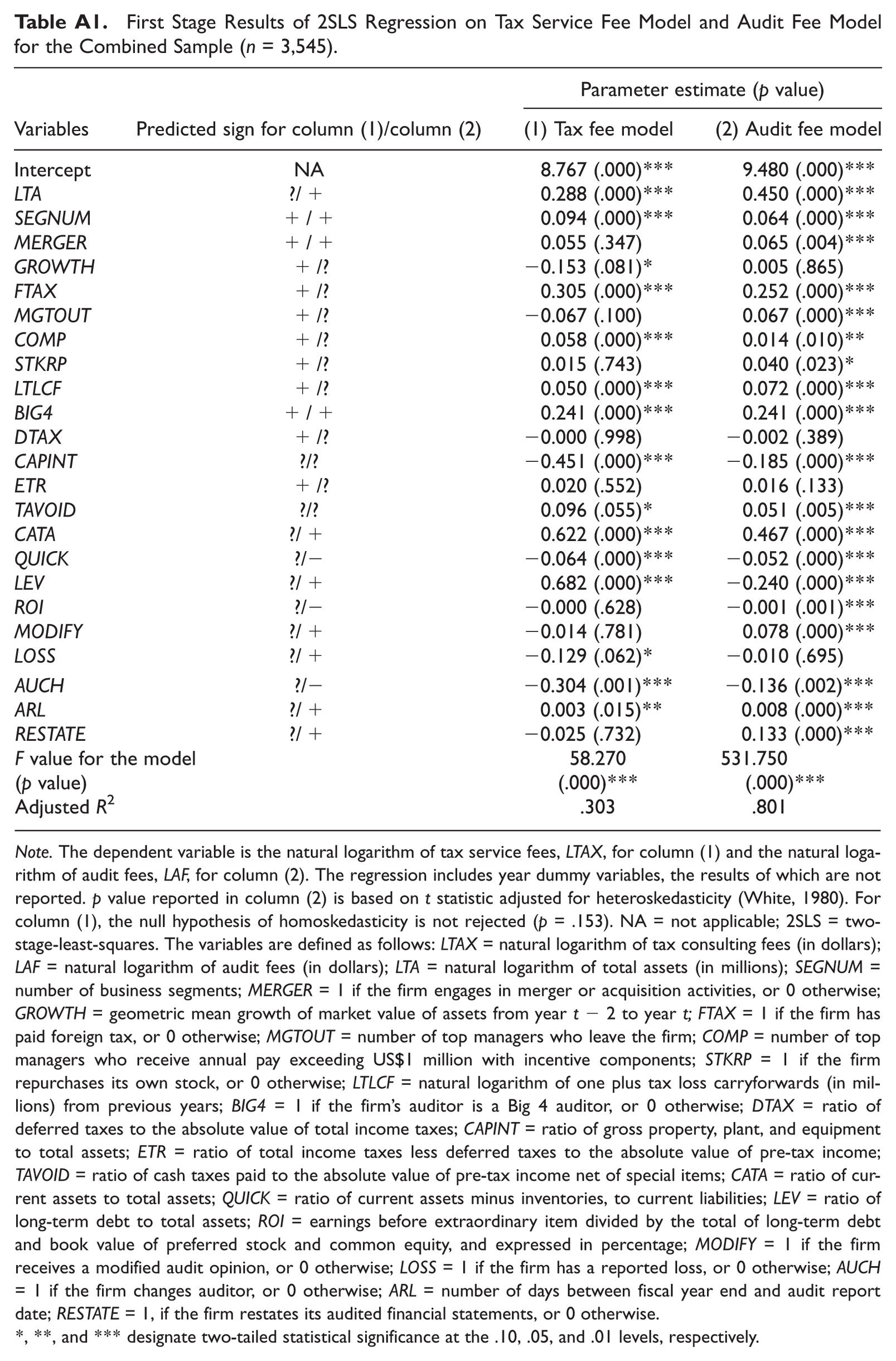

In column (2), LAF is added in the OLS regression. The variable is positive and significant. Therefore, using single equation, the results suggest that audit fees and tax fees are positively related. To control for common factors that could drive both audit fees and tax fees, 2SLS regression is run. The results of the first stage regressions are reported in Table A1 in the appendix and the results of the second stage are reported in column (3) of Table 7. In the first stage, all exogenous variables in Models 1 and 2 are used to predict tax fees and audit fees, so that the predicted value of tax fee and audit fee could be used in the second stage of 2SLS regression. As shown in column (2) of Table A1 for the audit fee model, many of the variables are significant and the variables as a whole are also significant in explaining audit fees, as evidenced by the F value. Then, the predicted value of audit fees (PLAF) is calculated from the results of column (2) of Table A1 and used in the second stage of 2SLS regression. Column (3) of Table 7 reports the results of the second stage regression, in which the predicted value of audit fees (PLAF) obtained from the first stage of 2SLS regression is used. As shown, the variable PLAF is positive and significant. This result suggests that audit fees are positively related to tax consulting fees after controlling for factors that could drive the demand for both audit and tax services.

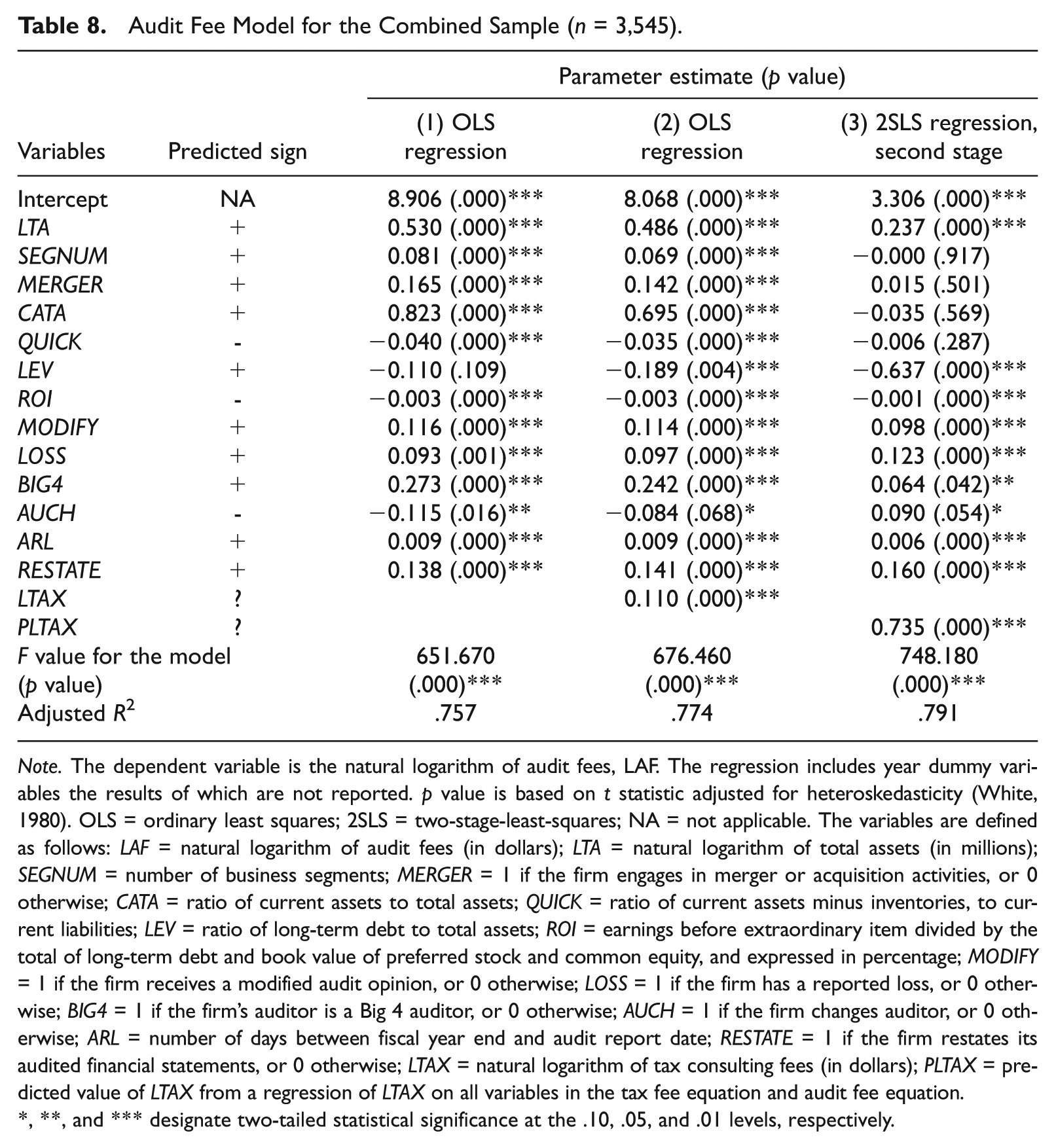

Table 8 reports the results of regressions on the audit fee model. As in Table 7, columns (1) and (2) report the results using OLS regressions for the sake of comparison and column (3) reports the results of the second stage of 2SLS regression. In column (1), all control variables except for LEV are significant and in the expected direction. Hence, consistent with prior studies, audit fees are determined by firm size and complexity, audit risk and the employment of Big 4 auditors. In column (2), the variable for tax consulting fees (LTAX) is added in the regression. Similar to the result of LAF in the tax fee model, LTAX is positive and significant in the audit fee model. Therefore, using single equation, the results suggest that audit fees and tax fees are positively related. Then, 2SLS regression is run to control for the possibility that audit fees and tax fees are jointly determined. The results of the first stage regression are reported in Table A1 in the appendix. As shown in column (1) of Table A1, many of the variables are significant in explaining tax fees. In addition, the regression model is significant, indicating that the variables as a whole can explain tax fees. The predicted value of tax fees (PLTAX) is then calculated from the results of the first stage and used in the second stage. Column (3) of Table 8 reports the results of the second stage of 2SLS regression, which includes PLTAX. As shown, PLTAX is positive and significant. This result suggests that higher tax fees lead to higher audit fees. Overall, the results reported in Tables 7 and 8 suggest that, after controlling for factors that could drive both tax fees and audit fees, there is a positive relationship between audit fees and tax fees, which is consistent with the argument that the demand for tax services gives rise to higher demand for audit services and vice versa.

Audit Fee Model for the Combined Sample (n = 3,545).

Note. The dependent variable is the natural logarithm of audit fees, LAF. The regression includes year dummy variables the results of which are not reported. p value is based on t statistic adjusted for heteroskedasticity (White, 1980). OLS = ordinary least squares; 2SLS = two-stage-least-squares; NA = not applicable. The variables are defined as follows: LAF = natural logarithm of audit fees (in dollars); LTA = natural logarithm of total assets (in millions); SEGNUM = number of business segments; MERGER = 1 if the firm engages in merger or acquisition activities, or 0 otherwise; CATA = ratio of current assets to total assets; QUICK = ratio of current assets minus inventories, to current liabilities; LEV = ratio of long-term debt to total assets; ROI = earnings before extraordinary item divided by the total of long-term debt and book value of preferred stock and common equity, and expressed in percentage; MODIFY = 1 if the firm receives a modified audit opinion, or 0 otherwise; LOSS = 1 if the firm has a reported loss, or 0 otherwise; BIG4 = 1 if the firm’s auditor is a Big 4 auditor, or 0 otherwise; AUCH = 1 if the firm changes auditor, or 0 otherwise; ARL = number of days between fiscal year end and audit report date; RESTATE = 1 if the firm restates its audited financial statements, or 0 otherwise; LTAX = natural logarithm of tax consulting fees (in dollars); PLTAX = predicted value of LTAX from a regression of LTAX on all variables in the tax fee equation and audit fee equation.

, **, and *** designate two-tailed statistical significance at the .10, .05, and .01 levels, respectively.

There are several reasons that could potentially explain the results that audit and tax fees are positively related. First, tax service may be more closely related to audit service than other types of non-audit services. Even before the bloom of the provision of non-audit services by incumbent auditors toward the end of the last century, tax service is traditionally performed by auditors for their audit clients. In addition, auditors may have a stronger competitive position for this type of non-audit services than competitors of other types of non-audit services. Thus, auditors are able to keep some, if not all, of the cost savings from the joint provision of audit and tax services, and clients may not pay lower total fees for both services. Consequently, audit fees and tax fees are positively related to each other instead of negatively related. Second, this article only focuses on tax service as one type of non-audit services. Treating all non-audit services as similar, as in prior studies, may not be appropriate as each non-audit service may be determined uniquely. Thus, focusing on one type of non-audit services may give more unambiguous results in analyses. Last, this article develops a set of possible determinants of tax service fees, most of which do not also appear in the audit fee model. Hence, it avoids using more or less the same set of determinants as audit fees. The more unique set of determinants again would give rise to more reliable results in the analyses.

Scaled independent fee variables for OLS regressions

In the above analyses, the tax and audit fee variables are level variables measured in natural logarithm. It may be possible that, for the OLS regressions, 20 the fee variables, when they are included as independent variables in the other models, may be proxying for firm size. 21 Therefore, for the OLS regressions, the tax fee variable when it is added as an independent variable in the audit fee model and likewise, the audit fee variable in the tax fee model, are scaled by the square root of total assets to linearize the relation between the fee variables and firm size, and to mitigate heterogeneity of the variance due to size (see Kinney, Palmrose, & Scholz, 2004; Simunic, 1980). Using these scaled independent fee variables, the OLS regression results (available from the authors) show that the scaled audit fee variable is positive and significant in the tax fee model, and the scaled tax fee variable is likewise positive and significant in the audit fee model. Furthermore, the variable LTLCF is also significantly positive in the tax fee model. The results of other variables remain substantially the same as in column (2) of Table 7 and of Table 8 where audit fees and tax fees, respectively, are measured in natural logarithm. Hence, the way the fee variables are measured as independent variables does not affect the results previously reported.

Cross-Selling More Tax Services

The above results suggest that cross-selling of tax services by auditors to their audit clients leads to higher audit fees and tax fees. As the positive relationship between audit fees and tax fees is likely to be a result of the cross-selling effort or success of incumbent auditors, it is useful to explore the threshold level of tax service that is required to generate such a positive relationship. To shed some light on the matter, we divide the combined sample at the median of tax consulting fees in the sample. It must be noted, however, that such a sample partitioning is ad hoc as there is no theory in the accounting or marketing literature that can predict the cutoff point. 2SLS regressions were run on the two sub-samples. The results (available from the authors) show that audit fees (LAF) and tax fees (LTAX) are positively related to each other only in the sub-sample above the median of tax fees. Therefore, the results suggest that more cross-selling of tax services leads to both higher audit fees and auditor-provided tax fees.

Limitations

Some limitations of this article should be noted. First, not all variables that can enter into the tax fee model or the audit fee model are used. It is especially germane to the audit fee model, which over the years has expanded considerably since the work of Simunic (1980). Although the variables used in the tax fee model and the audit fee model are representative of the variables that can be used, the possibility that different results may come out if other variables not in the models are used cannot be ruled out. Second, our understanding of the determinants of tax fees and audit fees is limited. For the audit fee model, despite nearly 30 years of development, some variables do not produce consistent results. A notable example is the leverage variable (see Hay et al., 2006). In this article, this variable is insignificant when the tax fee variable is not included in the audit fee model and becomes negative and significant when the tax fee variable is added. Therefore, the results of this article are limited to what we understand to be the determinants of audit and tax fees. Last, the positive relationship between audit fees and tax fees paid to incumbent auditors does not mean that there is no knowledge spillover in the sample firms. As shown in Table 4, some firms that purchase auditor-provided tax services would have paid higher audit fees if they had not had employed tax services of incumbent auditors. Therefore, the results of this article suggest that the effect of knowledge spillover, if it exists, is dominated by the effect of higher demand for either tax or audit services when both are provided by incumbent auditors.

Conclusion