Abstract

It is generally assumed that family firms emphasize socioemotional wealth, which exacerbates wealth expropriation from noncontrolling shareholders. We examine this issue in the context of nonfamily shareholders, specifically institutional investors, and find that institutional investors avoid investments in family firms. Furthermore, integrating institutional theory with a socioemotional wealth approach, we find that financial regulation can mitigate external investors’ concerns. These two results are important theoretically because they provide insight into the effect of agency problems specific to family firms and are important for management practice because they can provide guidance for family firms interested in new sources of capital.

Introduction

Family ventures generally start with capital from the family, but as they grow they may need external sources of capital to expand. Currently, institutional investors provide the majority of external equity capital for public companies (Bennett, Sias, & Starks, 2003). Therefore, a family firm looking to expand may need to look for external capital from institutional investors. However, some of the issues specific to family firms may make institutional investors wary of investing in family firms. In addition, the relation between institutional investors and family firms may also be affected by the regulatory regime within which the interaction takes places. In this article, we address two questions which prior literature has not fully explored (Hutton, 2007). First, we investigate whether family firms will have lower levels of institutional ownership. Second, we examine the effect of the regulatory regime on the level of institutional ownership of family firms.

Family-owned firms are generally considered less susceptible to the traditional agency problem (Jensen & Meckling, 1976) in which the owner and manager have conflicting interests and information (Type 1 agency problem; Bhaumik & Gregoriou, 2010; Villalonga & Amit, 2006). Indeed, it has been suggested that family firms represent one of the most effective solutions to the agency problem in organizational governance (e.g., Daily & Dollinger, 1992; Kang, 2000). Recent research, however, has suggested that family firms suffer from another type of agency conflict. Large inside (i.e., family) shareholders may use their controlling position in the firm to extract private benefits at the expense of the minority (i.e., nonfamily) shareholders (e.g., Bertrand, Mehta, & Mullainathan, 2002; Gao & Kling, 2008). This problem is known as the Type 2 agency problem (Bhaumik & Gregoriou, 2010; Villalonga & Amit, 2006).

Although the extraction of private financial benefits by the controlling shareholder is a potential problem for any firm with a large shareholder, a more pressing problem for family firms is the extraction of private nonfinancial benefits. The objectives of the “family” in family firms may be fulfilled with the controlling families maximizing their private benefits at the expense of other shareholders (Bhaumik & Gregoriou, 2010). Such self-interest of family owners tends more toward the buildup of socioemotional wealth (SEW; Gómez-Mejía, Haynes, Núñez-Nickel, Jacobson, & Moyano-Fuentes, 2007; Berrone, Cruz, Gómez-Mejía, & Larraza Kintana, 2010; Cennamo, Berrone, Cruz, & Gómez-Mejía, 2012; Miller, Le Bretton-Miller, & Lester, 2013; Zellweger, Kellermanns, Chrisman, & Chua, 2012), which is not necessarily financial. SEW from a family firm’s perspective are those attributes that meet the controlling family’s affective needs such as identity, the ability to exercise power, and continuation of the family dynasty (Gómez-Mejía et al., 2007; Zellweger et al., 2012). Therefore, their goals may diverge from those of anonymous investors seeking high financial returns (Berrone, Cruz, & Gómez-Mejía, 2012; Kellermanns, Eddleston, & Zellweger, 2012; La Porta, Lopez-de-Silanes, & Shleifer, 1999; Miller & Le Breton-Miller, 2006). Although family owners and anonymous investors may be expected to share common economic interests, there is little reason to suppose that they have common nonfinancial preferences (Schulze, Lubatkin, Dino, & Buchholtz, 2001). Since SEW cannot be expressed in purely financial terms, standard contracting solutions for agency problems are likely to be less effective for family firms.

In this article, we examine the impact that the pursuit of SEW by family firms has on the decisions of sophisticated nonfamily shareholders, specifically institutional investors such as mutual funds and investment managers. First, we ask whether this Type 2 agency problem which results from family pursuit of SEW leads more sophisticated investors to avoid investments in family firms. Second, drawing on institutional theory we ask whether financial regulation can mitigate sophisticated investors’ concerns about this Type 2 agency problem. These two questions are important because they provide insight into the impact of agency problems specific to family-owned firms. These questions are also important for management practice because the answers can provide guidelines for family-run firms interested in attracting new sources of capital.

Investors are not homogenous. Institutional investors such as mutual funds, brokerages, insurance companies, pension funds, investment banks, and endowment funds are more sophisticated than individual (retail) investors because they use professional analysts with financial accounting expertise to advise them on investment decisions (Utama & Cready, 1997). Also, as full-time investors, institutions have greater time and attention necessary to process complex financial information than retail investors (Hirshleifer & Teoh, 2003). Compared with retail (naïve) investors, this sophistication would presumably lead such investors to be more cognizant of Type 2 agency problems arising from SEW pursuit in family firms. Although there is significant research on family firms as well as on institutional investors, there has been little research on the nexus of these two. In fact, in her discussion of Ali, Chen, and Radhakrishnan (2007), Hutton (2007) suggests that “given differences in corporate governance and disclosure practices of family versus non-family firms documented in both Ali et al. (2007) and Wang (2006), it would be interesting to know whether institutions invest more or less heavily in family firms” (p. 289). This question is important because institutional investors provide the bulk of external capital and are the price-setting marginal investors for most firms (Bennett et al., 2003). In this article, we address the above issue directly.

Second, although recent research has begun to examine the implications of Type 2 agency problems and nonfinancial motivations of family members, there is a paucity of research on the influence of changes in regulation on these problems. Accordingly, we draw on insights from institutional theory, which identifies the state or government as an actor that can and will exert significant influence on firms through legislation, to explore this issue. The Sarbanes–Oxley Act of 2002 (hereafter SOX) is the legislation with the greatest impact on organizational governance in the past decade. It forced several changes in firm governance which may have mitigated some of the families’ ability to maximize their own private benefits at the expense of minority shareholders. First, the audit committee must be composed of independent directors and at least one accounting expert (DeFond & Francis, 2005). Second, much of the Act requires either additional disclosure or more certification of the disclosures made by the firm, with higher personal penalties for false information (Engel, Hayes, & Wang, 2007; Lobo & Zhou, 2006). Jointly, one would expect the effect of SOX to be a shift in power from insiders to outsiders and, thus, limit the ability of the family to maximize their own private benefits. Consequently, we use the passage of SOX to investigate the effect of regulatory regime changes on the relation between institutional investors and family firms.

The rest of the article is organized as follows. The following section contains the literature review and hypotheses development, which is followed by a section containing the methodology. The subsequent section provides the data description and empirical analysis. The penultimate section contains a sensitivity analysis of our results. The final section discusses our findings and presents the conclusions.

Literature Review and Hypothesis Development

Agency Theory

Type I Agency Costs

The theory that underlies much of the research in organizational control is agency theory (see, reviews by Baiman, 1982, 1990; Lambert, 2001). In the most basic case, the principal, who provides capital and owns the enterprise, offers a wage to an agent (the manager) to manage the enterprise on behalf of the principal. The theory assumes that the agent’s utility (or satisfaction) increases with the amount of compensation and decreases with the effort that he or she has to put in. Therefore, a rational agent accepts the offer as long as the wage adequately compensates him or her for the effort. Generally, the principal is neither involved in nor aware of the day-to-day operations of the enterprise. Hence, there is potential for the agent to shirk or extract personal financial benefits from the firm at the expense of the principal (Kaplan & Atkinson, 1998; Stevens & Thevaranjan, 2010). Either of the two situations amounts to rent seeking by the agent at the expense of the owner and is referred to as the Type 1 agency problem (Bhaumik & Gregoriou, 2010; Villalonga & Amit, 2006). The Type 1 agency problem is mitigated as the manager owns a higher percentage of the firm (Jensen & Meckling, 1976). The intuition here is straightforward: The higher the percentage of a firm owned by a manager the more aligned are the incentives between the manager and the shareholders. Hence, a family-owned and operated firm appears to be an ideal solution to the Type 1 agency problem.

Type II Agency Costs

However, there is another facet to the agency problem which occurs when an insider who owns a significant fraction but not the entire firm has the opportunity to expropriate wealth from other shareholders (known as Type 2 agency problems; Bhaumik & Gregoriou, 2010). An insider with significant voting rights/control can use the firms’ resources for personal benefit thus forcing the other shareholders to subsidize the activities of that insider. Unlike traditional agency problems which can be mitigated via contracting, Type 2 agency problems exist between the various owners and explicit contracting is not generally available. Rather, minority shareholders rely on having common motivations (similar utility functions) as more powerful inside shareholders (Schulze et al., 2001). Consequently, as utility functions diverge, minority shareholders face a greater risk that firm decisions will be made against their interests.

Limitations of Agency Theory

Even though it has proven useful in some settings, the principal–agent model has been criticized for the diminished realism of adhering strictly to narrow financial self-interest. Agency theory, expressed in the principal–agent model, relies on the assumption that all preferences can be expressed in economic terms (Schulze et al., 2001). When the reasonable assumption of utility maximization is simplified in models as financial wealth maximization, the applicability of the principal–agent model diminishes because individuals have preferences for both noneconomically and economically motivated behaviors, and people are naturally driven to maximize the utility they gain from each (Arrow, 1963; Becker, 1974; Buchanan, 1975; Thaler & Shefrin, 1981). Noneconomic factors that provide equal if not greater utility to an individual include ethics (Stevens & Thevaranjan, 2010), fairness (Arrow, 1985), and altruism (Schulze et al., 2001). Furthermore, a number of related noneconomic motivations specifically related to family firms have been gathered under the concept of SEW (Gómez-Mejía et al., 2007, etc.). In this article, we investigate the reaction of external providers of capital to the noneconomic motivations of family firm insiders; hence, we draw on the SEW approach to understand what induces such motivations.

Family Firms and the Theory of Socioemotional Wealth

Family firms are those firms in which the founding family maintains a significant ownership interest and/or operational control (Anderson & Reeb, 2003). Family firms are not merely a different empirical setting but rather are significantly different from nonfamily firms (Berrone et al., 2012). Family motivations are not the same as those of purely economically motivated actors typically employed by agency theory. Consequently, agency theory as it has been developed does not apply well to family firms.

To deal with this difference, Gómez-Mejía et al. (2007) developed a general model of SEW that extends beyond agency theory and offers a way to understand choices made by family firms that appear at odds with the predictions of agency theory. The SEW approach is a broadly conceptualized approach which captures a different behavioral reference frame (loss aversion) and a different type of utility function which focuses on nonfinancial motivations. These nonfinancial motivations are known collectively as SEW which is defined from a family firm’s perspective as those attributes that meet the controlling family’s affective needs such as identity, the ability to exercise power, and continuation of the family dynasty (Gómez-Mejía et al., 2007; Miller et al., 2013; Zellweger et al., 2012). In essence, SEW is the sum of nonpecuniary benefits that a family would obtain through control of the firm.

The important aspect of the SEW approach for our investigation is that family shareholders do not share the same goals as other investors. Thus, strategic choices that will benefit the family’s SEW endowment might come at the expense of other stakeholders (e.g., institutional investors) who do not share in these SEW utilities (Berrone et al., 2012). Family members’ concern about the loss of socioemotional endowment frequently takes priority over risk aversion to financial losses even when agency theory predicts that family members would avoid strategic choices that carry a significant risk of financial loss (Berrone et al., 2012).

Founding family members as large shareholders have the ability to expropriate wealth from nonfamily shareholders by collecting private benefits (Fama & Jensen, 1983; Morck, Shleifer, & Vishny, 1988; Shleifer & Vishny, 1997) and appear to be motivated by SEW. Family members with enough votes can abuse their power by extracting resources from the firm or by favoring family members in hiring decisions (Faccio, Lang, & Young, 2001; Dyer, 2006; Morck & Yeung, 2003; Schulze et al., 2001). Furthermore, family firms may be less concerned about communication with minority shareholders leading to higher information asymmetry. Chen, Chen, and Cheng (2008) find that family firms provide fewer earnings forecasts, conference calls, and fewer issuances of public debt and equity compared with nonfamily firms. Mosebach and Thomas (2008) find lower dividends per share in family firms than in nonfamily firms. Chen, Chen, Cheng, and Hutton (2008) show that when the founder serves as the CEO of his or her family firm, accounting becomes less conservative, likely due to other family members’ inability or unwillingness to monitor the founder CEO. More directly pertaining to our study, Anderson and Reeb (2004) demonstrate that family-controlled firms tend to resist the presence of independent directors on the board.

Consistent with the SEW approach, recent research on family ownership has noted that families have preferences for nonfinancial objectives (Anderson & Reeb, 2003; Sharma, Chrisman, & Chua, 1997). Family owners appear to be interested in SEW at the expense of financial wealth (Berrone et al., 2010). Thus, even when all actors in the firm behave in their own self-interest, the family owners’ nonfinancial interest will likely diverge from other owners seeking high returns (La Porta et al., 1999; Miller & Le Breton-Miller, 2006). They engage in altruistic activities (Schulze, Lubatkin, & Dino, 2003a), entrench relatives (Gómez-Mejía, Makri, & Larraza, 2010; Gómez-Mejía, Núñez-Nickel, & Gutierrez, 2001) and strive for family control even at the expense of higher returns (Gómez-Mejía et al., 2007, Jones, Makri, & Gómez-Mejía, 2008; Schulze, Lubatkin, & Dino, 2003b). Family ownership provides relatives with secure employment as well as perquisites that they would not otherwise receive (Gersick, Davis, Hampton, & Lansberg, 1997; Ward, 1987). Family owners refuse to replace themselves when a growing firm requires external expertise (Wasserman, 2003) or pass on the firm to an underqualified next generation because of nepotism (Perez-Gonzalez, 2006). Overall, the research discussed above indicates that family owners pursue SEW at the expense of financial wealth and consequently their interests are going to diverge from other shareholders seeking financial wealth.

Institutional Investors

Institutional investors are entities with large amounts to invest, such as mutual funds, brokerages, insurance companies, pension funds, investment banks, and endowment funds. These types of investors have become a “dominant force in financial markets” with more than 50% of equity ownership and have now become the marginal investor that determines the final stock price for most firms (Bennett et al., 2003).

Institutions are generally more sophisticated than individual (retail) investors (Utama & Cready, 1997) because they employ analysts with financial accounting expertise to advise their fund managers on investment decisions. Also, as full-time investors, institutions have greater time and attention needed to process complex financial information compared with retail investors (Hirshleifer & Teoh, 2003).

Prior research shows that institutional investors try to exert influence on the firms they invest in and attempt to sway the actions of such firms and their managers. Almazan, Hartzell, and Starks (2005) contend that monitoring by institutional investors is an important governance mechanism for corporate management. For example, in the early 80s Fiat of Italy, a family-owned firm, was forced by Mediobanca, a private bank that held a strategic stake in the firm, to accept an outside CEO to stave off bankruptcy (McHugh, 2004). The firing of Richard Grasso, the CEO of New York Stock Exchange, happened largely because of the outrage of institutional investors over perceived excesses in his compensation package (Kelly, Craig, and Dugan 2003). Similarly, institutional investors mobilized and voted down the senior executive compensation package for GlaxoSmithKline in 2003 (Hebb, 2006). Bushee (1998) shows that the presence of institutional investors inhibits managers from carrying out earnings manipulation through cutting R&D expenses. Hartzell and Starks (2003) show that institutional investors exercise a monitoring role on executive compensation. They find that the pay-to-performance sensitivity increases when institutional holdings increase, and the level of compensation declines as the level of institutional holdings increase. In addition to empirical evidence, three committee reports from the United Kingdom, the Cadbury (1992) Report, the Greenbury (1995) Report and the Hampel (1998) Report place special obligations on institutional investors to use their clout in their investee companies to implement good corporate governance standards.

Hypothesis Development

As discussed above, in family firms, there is an emphasis on building and maintaining SEW at the expense of maximizing financial performance. A key aspect of the pursuit of SEW by family firms is that SEW is tied up in the control of the firms. Zellweger et al. (2012) maintain that “. . . the family’s control of the firm through ownership is critical to creating and preserving socioemotional wealth because such control is what allows the family to pursue its interests through the firm” (p. 851). Stockmans, Lybaert, and Voordeckers (2010) state that family owners would be willing to forego economic performance in order to preserve the family’s SEW. Blanco-Mazagatos, De Queveda-Puente, and Castrillo (2007) concur and show that family firms will increase their debt capital even though raising equity from outside shareholders may be more efficient, to preserve family control.

Family firms’ pursuit of SEW at the expense of profit will put them at odds with institutional investors who prefer to invest in firms which maximize financial returns and where they can exercise a certain amount of influence over the firm, resulting in potential conflicts with the family owners of a family firm. Berrone et al. (2012, p. 260) make the same point by arguing that “the family will make strategic choices to avoid these potential SEW losses” even if it is at the expense of other principals (and name institutional investors as an example of other principals). Therefore, even though family firms may outperform non–family-owned firms (Anderson & Reeb, 2003; Lee, 2006), institutional investors will avoid family firms because (a) as sophisticated investors, institutions will be aware of the SEW-driven Type 2 agency problems unique to family firms and (b) institutions will not be able to exercise the same level of active governance over family firms. Hence we state our first hypothesis as follows:

Hypothesis 1: Family firms will have a lower level of institutional ownership.

Institutional Theory and Sarbanes–Oxley Act: Conceptual Framework and Hypothesis Development

The SEW approach focuses on describing the motivations and resulting behavior of families in family firms. It suggests (and we have hypothesized above) that others (nonfamily owners) are affected by the family pursuit of SEW. Although SEW-consistent behaviors have been demonstrated and evaluated in many regulatory regimes, the relation between the regime and the family’s ability to act on the desire for SEW has not be examined. To help understand this relation and formulate an empirical prediction, we draw on institutional theory.

Institutions are “the rules of the game in a society, or, more formally, are the humanly devised constraints that shape human interaction,” and include both formal constraints (such as rules and regulations) and informal constraints (such as conventions, customs, traditions, and codes of behavior; North, 1990, p. 3). Thus, institutions are the framework within which human interaction takes place and they define as well as limit the set of individuals’ choices.

Individuals operate within one or more institutions and seek legitimacy within each (Eisenhardt, 1988). Each institution brings its own set of rules and, thus, its own institutional logic or decision-making criteria. These logics may be either complimentary or contradictory with other institutions of which an individual is a member. Thornton (2004), in a more general categorization of the Friedland and Alford (1991) typology, suggests six sectors: the market, the corporation, the professions, the state, the family, and religion as the dominant institutions in society.

Although institutions are “the rules of the game,” they are not permanent. Each of the institutions as well as each individual’s membership in a particular institution is subject to change over time. Organizations, such as firms, form to take advantage of the opportunities presented by the institutions. Thus, there is a symbiotic relationship between organizations and institutions. As these organizations evolve, this leads to institutional change which in turn may lead to more organizational evolution. This change tends to be incremental as a result of the imbeddedness of constraints in institutions and the dependency of the organization on the institutional framework which creates a “lock-in.” However, more abrupt changes can occur. These are usually the result of formal rules changes due to legislative or judicial decisions (North, 1990).

The key insight from institutional theory that is applicable to our situation is the effect of external regulatory shocks. Organizational change can be affected by institutional change, and such change can be quite rapid and visible when forced by regulatory change. Thus, institutional theory suggests that regulation affects the relation between institutional investors and family firms and that a change in regulation could affect that relation.

SOX is a regulatory change that forced significant changes in the corporate governance environments enabling us to analyze the impact of regulation of the family’s pursuit of SEW. SOX was passed in 2002 to restore public confidence in the financial markets that had been roiled due to the corporate scandals of the early 2000s. To improve the quality and quantity of information provided to the public, SOX imposes severe penalties (both civil and criminal) for misrepresentation of information and fraud (Chang, Fernando, and Liao, 2009). Furthermore, management and CEOs have to evaluate the effectiveness of internal controls and report the findings to the public. The CEO and CFO have to certify that the financial reports comply with the relevant rules and regulations (Engel et al., 2007). Audit committees of public companies are required to be fully independent and financially literate (DeFond & Francis, 2005). Many studies have examined the impact of SOX on various aspects of firm performance. For instance, Lobo and Zhou (2006) show that SOX has resulted in lower discretionary accruals and increased conservatism in the post-SOX period. Coincident with SOX, NYSE and NASDAQ changed their listing requirements. Both required a majority of independent directors on the board and tightened the definition of independence.

From a family firm’s perspective, SOX has three main provisions that served to shift the balance of power in the boardroom from insiders to noncontrolling shareholders. First, by requiring the audit committee to comprise independent directors, SOX has the effect of necessitating the recruitment of independent directors to the board. At the same time, the NYSE and NASDAQ imposed even more stringent requirements by mandating a majority of independent directors on the board. The presence of independent directors on the board will inhibit the insiders from extracting private benefits (or focusing on SEW enhancements at the expense of financial wealth) more effectively than compliant family members. Second, SOX (Section 404) mandated improvements to internal controls, requiring the external auditors to attest to their adequacy. Effective internal control systems are an important means of safeguarding the assets of the organization, thus preventing their expropriation by insiders at the expense of the (in the case of family firms) noncontrolling shareholders. Third, by requiring more stringent financial reporting quality and disclosure, SOX will inhibit insiders from expropriating wealth by manipulating accounting information. Therefore, in total, SOX serves to change the power imbalance between the insider shareholders (family owners) and outsider shareholders.

For example, commenting on the Parmalat bankruptcy of 2003, Francesco Giavazzi, an economist at Bocconi University in Milan quoted by McHugh (2004) says, “In my view, what happened at Parmalat would not have happened if there were even one or two outside directors. There was no one sitting at the table who was truly independent of the family.” According to the prior statement, the Parmalat bankruptcy which occurred as a result of “. . . an unaccountable strong block holder (which was the controlling family, the ‘Tanzis’) is willing and able to wield its power at the expense of unprotected minority shareholders” (Melis, 2006, p. 58), would not have happened if the firm was compliant with the SOX mandates for independent directors. On a more positive note, Melis (2006, p. 58) also mentions Telecom Italia which is listed on the NYSE and hence “is subject to US securities laws and in particular Sarbanes-Oxley . . . may be considered an example of Italian best practice, thanks to the company’s effort to strengthen minority shareholders’ protection in order to be more competitive in capital markets.”

According to our first hypothesis, institutional investors would avoid family firms because of their concern about the family’s pursuit of SEW at their expense, which is caused by the power imbalance between the family and the minority shareholders. As the above discussion of institutional theory suggests, regulation affects this balance of power and regulatory change is one way that this balance of power can change quickly. Thus, a reasonable extension of the first hypothesis is that in the event the power imbalance is alleviated by regulatory change, institutional investors would become less averse to family firms. The stipulations of SOX and the two cases discussed above clearly demonstrate the ability of SOX to improve minority shareholder protection. Our second hypothesis investigates whether institutional investors have indeed increased their stake in family firms after SOX. Therefore, our second hypothesis serves to provide additional confirmation of our first hypothesis as well as enable us to study the effects of a change in regulation on institutional investors’ reaction to curbs placed on SEW pursuit by family firms. The second hypothesis is stated as follows:

Hypothesis 2: Institutional investor ownership of family firms increased after SOX.

Research Methodology

Variables

Institutional Ownership

Our dependent variable is institutional ownership. Consistent with prior research, this variable is measured as shares held by institutions divided by total shares outstanding with data drawn from the Thompson 13f database.

Family Firms

We use the S&P 500 list of 2002 and the Business Week 2002 identification of family firms in the S&P 500 list of that year in our analysis. Anderson and Reeb (2003) classify a firm as a family firm if the founder and/or his or her descendants hold positions in the top management or on the board or are among the companies’ largest shareholders. Business Week uses this definition to classify 177 of the S&P 500 firms in 2002 as family firms and the remainder as nonfamily firms. This classification has been used by several prior studies such as Ali et al. (2007) to identify family firms. Although the Business Week classification of family firms was done in 2002, as in Ali et al. (2007) we expect “stickiness” in the firm classification and assume that the classification will be valid for the sample period, 1998-2006.

Control Variables

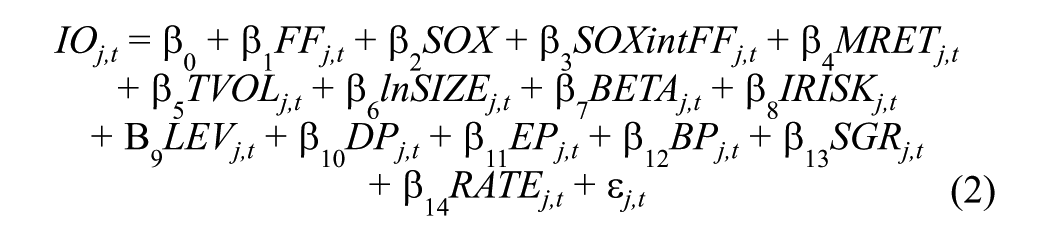

We include control variables to capture previously documented determinants of institutional ownership. Following prior research, we include three measures of risk. We include beta (BETA), calculated from a market model using daily stock returns over the prior annual period to capture systematic risk. Idiosyncratic risk (IRISK) is measured as the standard deviation of market model residuals over the prior annual period. We also include a measure of leverage (LEV), measured as debt-to-assets (Bushee & Noe, 2000). Higher levels of systematic risk and leverage are associated with higher levels of institutional ownership (Badrinath, Gay, & Kale, 1989; Skinner, 1989). Higher levels of idiosyncratic risk are associated with lower levels of institutional ownership (Bushee, 2001).

We include annual market-adjusted returns (MRET) proxy for firm performance which has been shown to be positively associated with changes in institutional ownership (Bushee & Noe, 2000; Lang & Lundholm, 1993; Sias, 1996). The level of trading volume in the stock (TVOL), measured as the average monthly volume over the year divided by average shares outstanding, controls for institutional investor preferences for more liquid stocks (Bushee & Noe, 2000). Firm size, measured as the log of market value of equity (lnSIZE), captures differences in institutional ownership between small and large firms (Bushee & Noe, 2000; Sias, 1996).

We also include a number of variables to capture changes in fundamental growth and income ratios on which institutions might base their trading decisions (Bushee, 2001; Bushee & Noe, 2000). These include dividend yield (DP), the earnings-price ratio (EP), the book-price ratio (BP), and sales growth (SGR). Finally, we control for the S&P stock rating (RATE), which is a measure of the prudence of the investment for the institution, because some institutions avoid stocks with lower ratings due to fiduciary concerns (Badrinath et al., 1989; Bushee & Noe, 2000; Del Guercio, 1996).

Models

Hypothesis 1 examines the relation between institutional ownership and family firms.

Following prior literature, we develop and estimate the following model to test this hypothesis:

where for firm j in period t,

IOj,t = institutional ownership measured as shares held by institutions divided by total shares outstanding

FFj,t = indicator variable equal to 1 if the firm was classified as a family firm by Business Week magazine in 2002 (Weber, Lavelle, Lowry, Zellner, & Barrett, 2003)

MRETj,t = annual market adjusted returns for year t

TVOLj,t = average monthly volume over year t divided by average shares outstanding

lnSIZEj,t = log of market value of equity

BETAj,t = beta computed from a market model using daily stock returns over an annual period for year t

IRISKj,t = the standard deviation of market model residuals over an annual period

LEVj,t = debt-to-assets ratio

DPj,t = dividend yield

EPj,t = earnings-price ratio

BPj,t = book-price ratio

SGRj,t = sales growth

RATEj,t = S&P stock rating

We estimate Model (1) using a fixed effects regression to control for firm level and year fixed effects. Our variable of interest is FFj,t, which is an indicator variable which takes the value of 1 if the firm is a family firm or 0 otherwise. In accordance with our first hypothesis, we expect FFj,t to be negative and significant.

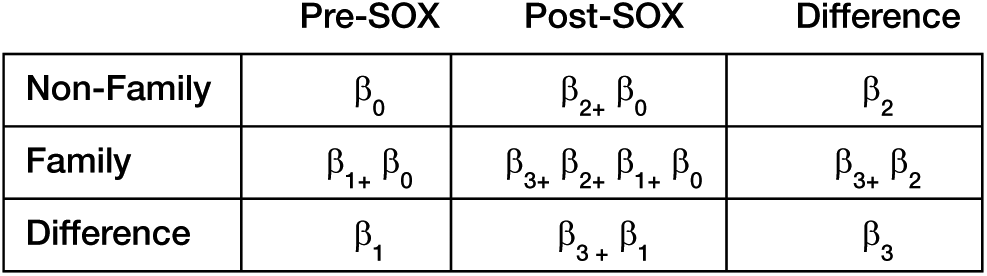

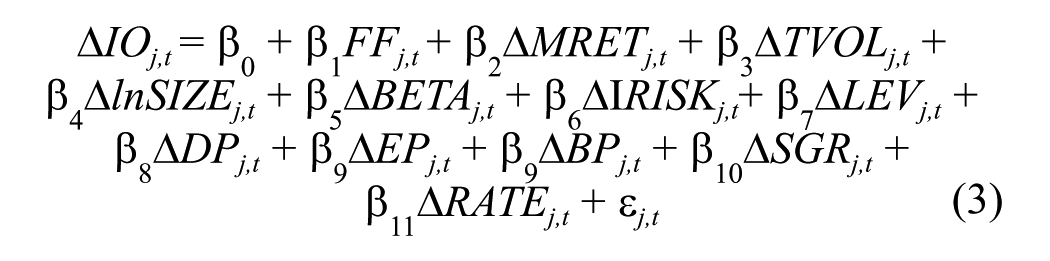

Hypothesis 2 examines the difference in institutional ownership levels between family and nonfamily firms after the provisions of SOX became effective. Since we intend to examine the marginal impact of SOX on family firms relative to nonfamily firms, we use a differences-in-differences design. The differences-in-differences design is a powerful research design since it captures only the change in the group of interest relative to any change in the comparison group. Thus, it controls for any contemporaneous changes other than the effect of interest. We begin to test this hypothesis by first estimating the following model:

where SOX is an indicator variable equal to 1 if the year is after SOX implementation in 2002 (in this sample, years 2003-2006) and 0 otherwise. We focus our attention on the coefficient on the interaction of SOX and FF variables (SOXintFFj,t) which as can be seen in the lower right-hand box of Figure 1 is the difference in the differences (Wooldridge, 2002; Zhang, 2005). In accordance with the second hypothesis, we expect the coefficient on SOXintFFj,t, to be positive and significant. The rest of the variables have the same meanings as defined above.

Difference in differences model.

Data and Empirical Analysis

Data

Our sample period for our primary tests is from 1998 until 2006. We obtain institutional ownership data from the Thompson 13f database and data for control variables from Compustat and CRSP. As discussed below, we follow prior research and use the S&P 500 list of 2002 and the Business Week 2002 identification of family firms in the S&P 500 list of that year in our analysis. Prior research (Lee, 2006; Perez-Gonzalez, 2006, and others) exclude regulated industries (utilities and financial firms) from their analyses since the regulations under which such firms operate exposes them to a different set of pressures and incentives that are not discussed in this research. Hence, following such research, we exclude regulated industries from our sample. This yields a sample of 295 individual firms of which 119 are designated family firms and a total sample size of 2,655 firm-year observations.

Descriptive Statistics

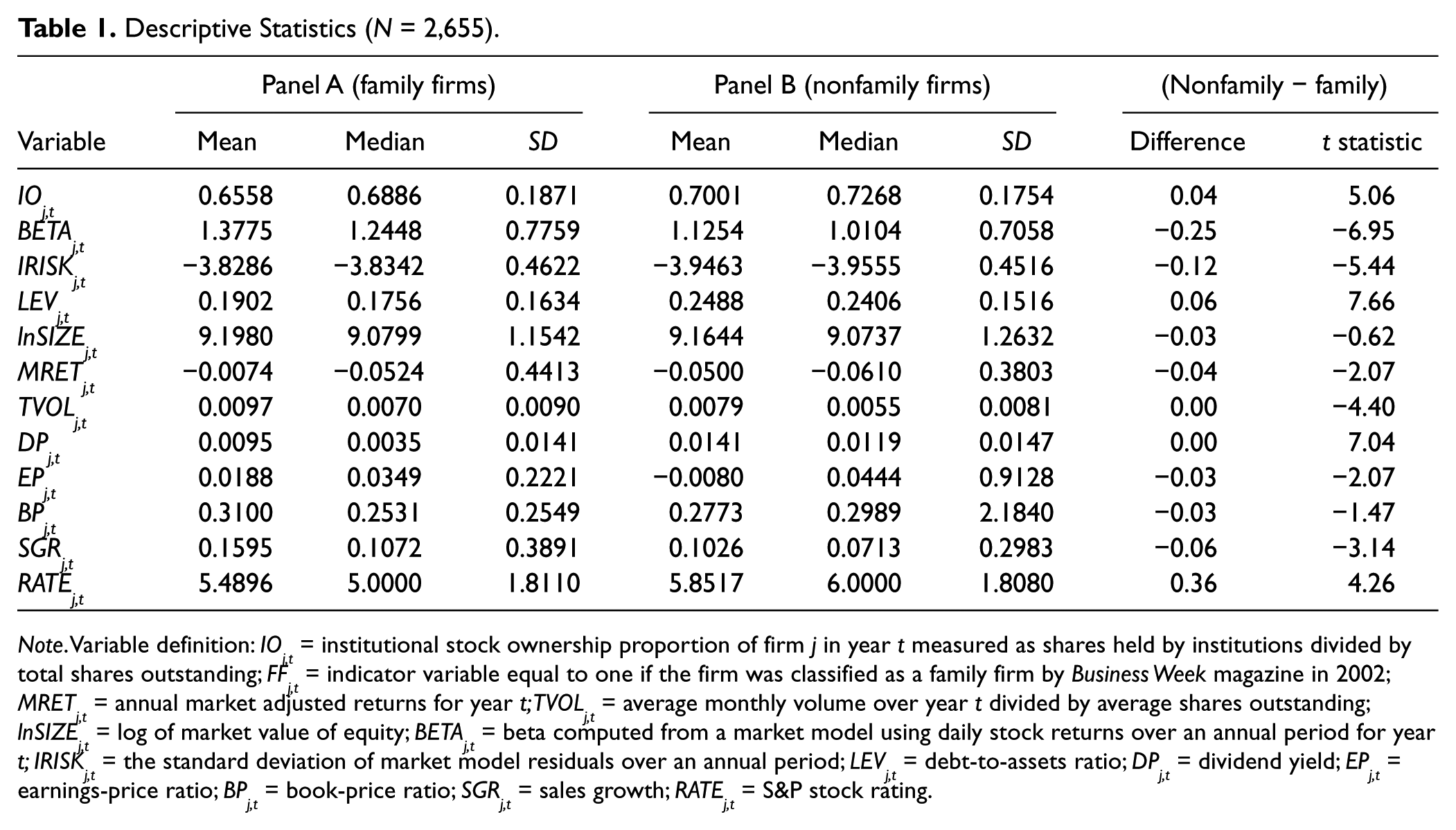

Table 1 presents summary descriptive statistics of the variables used in this study for the entire sample.

Descriptive Statistics (N = 2,655).

Note. Variable definition: IOj,t = institutional stock ownership proportion of firm j in year t measured as shares held by institutions divided by total shares outstanding; FFj,t = indicator variable equal to one if the firm was classified as a family firm by Business Week magazine in 2002; MRETj,t = annual market adjusted returns for year t; TVOLj,t = average monthly volume over year t divided by average shares outstanding; lnSIZEj,t = log of market value of equity; BETAj,t = beta computed from a market model using daily stock returns over an annual period for year t; IRISKj,t = the standard deviation of market model residuals over an annual period; LEVj,t = debt-to-assets ratio; DPj,t = dividend yield; EPj,t = earnings-price ratio; BPj,t = book-price ratio; SGRj,t = sales growth; RATEj,t = S&P stock rating.

Panel A shows the univariate statistics for family firms whereas Panel B shows the same for nonfamily firms. Institutional ownership in family firms is significantly lower than in nonfamily firms (66% vs. 70%). This provides an initial confirmation that institutions have different preferences for family versus nonfamily firms.

Other variables which affect the proportion of institutional ownership also show systematic differences between family firms and nonfamily firms. Beta and idiosyncratic risk are significantly higher for family firms indicating higher systematic and idiosyncratic risk. Family firms also have a lower S&P rating on average. However, family firms have less leverage.

Family firms are approximately the same size as their nonfamily counterparts. They have greater trading volume making them more liquid and, therefore ceteris paribus, more desirable investments for large institutions. Annual market-adjusted returns and sales growth are significantly larger for family firms indicating that they appear to have been performing better during our sample period. Finally, family firms demonstrate differences in fundamental growth and income ratios with higher earnings to price ratios and lower dividend yield.

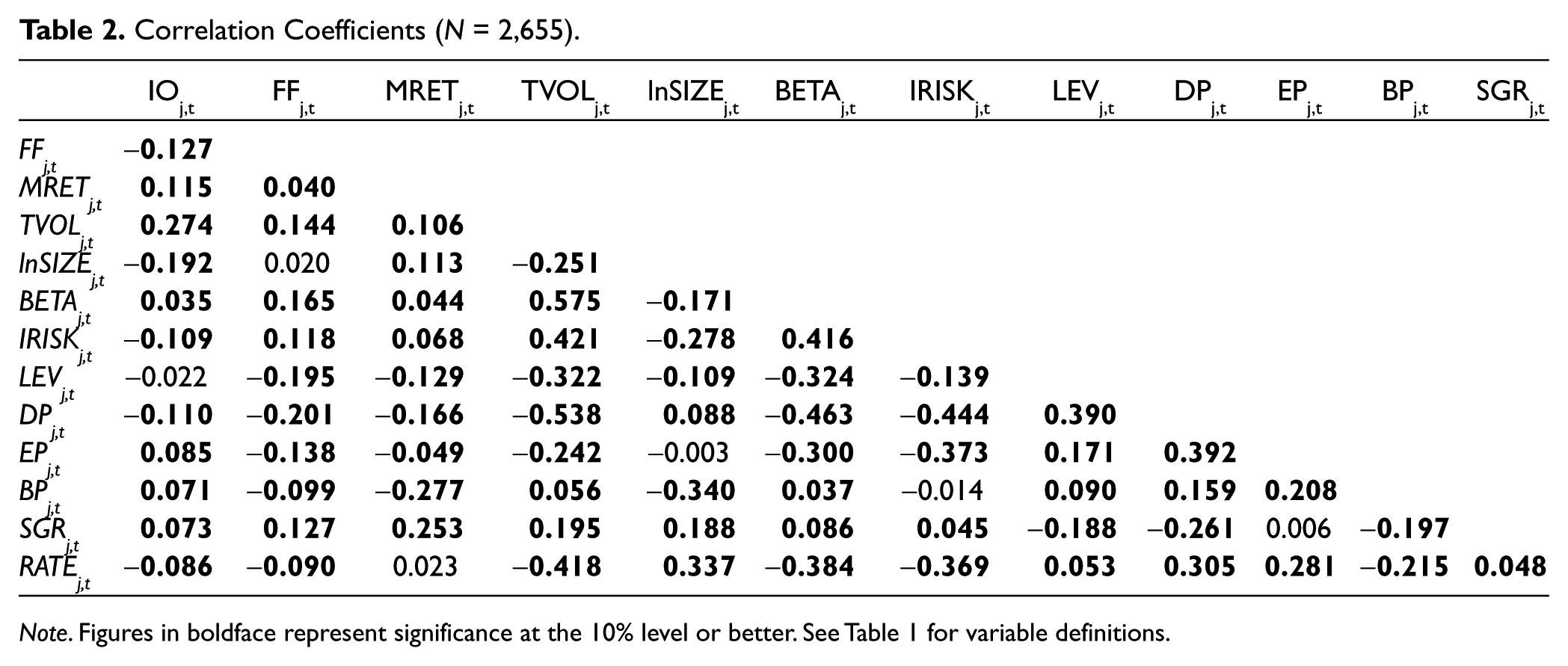

Table 2 presents the correlation tables.

Correlation Coefficients (N = 2,655).

Note. Figures in boldface represent significance at the 10% level or better. See Table 1 for variable definitions.

The table shows simple correlations between institutional ownership, the family firms variable, and relevant control variables. The results demonstrate that on a univariate basis, institutional ownership is negatively correlated with the family firms’ variable suggesting that institutional ownership decreases when the firm in question is a family firm while confirming the results of Table 1. Institutional ownership is positively and significantly correlated with annual market-adjusted returns, trading volume, beta, the earnings to price ratio, the book-price ratio, and sales growth, while being negatively and significantly correlated with firm size, idiosyncratic risk, dividend yield, and the S&P stock rating. Our variable of interest family firms is positively and significantly correlated with annual market-adjusted returns, trading volume, beta, idiosyncratic risk, and sales growth, while being negatively and significantly correlated with leverage, the S&P stock rating, the earnings-price ratio, the book-price ratio, and dividend yield. Given the significant differences that exist in the control variables which could explain (or mask) the difference in institutional investment in family firms, we perform multivariate analyses.

Multivariate Analysis

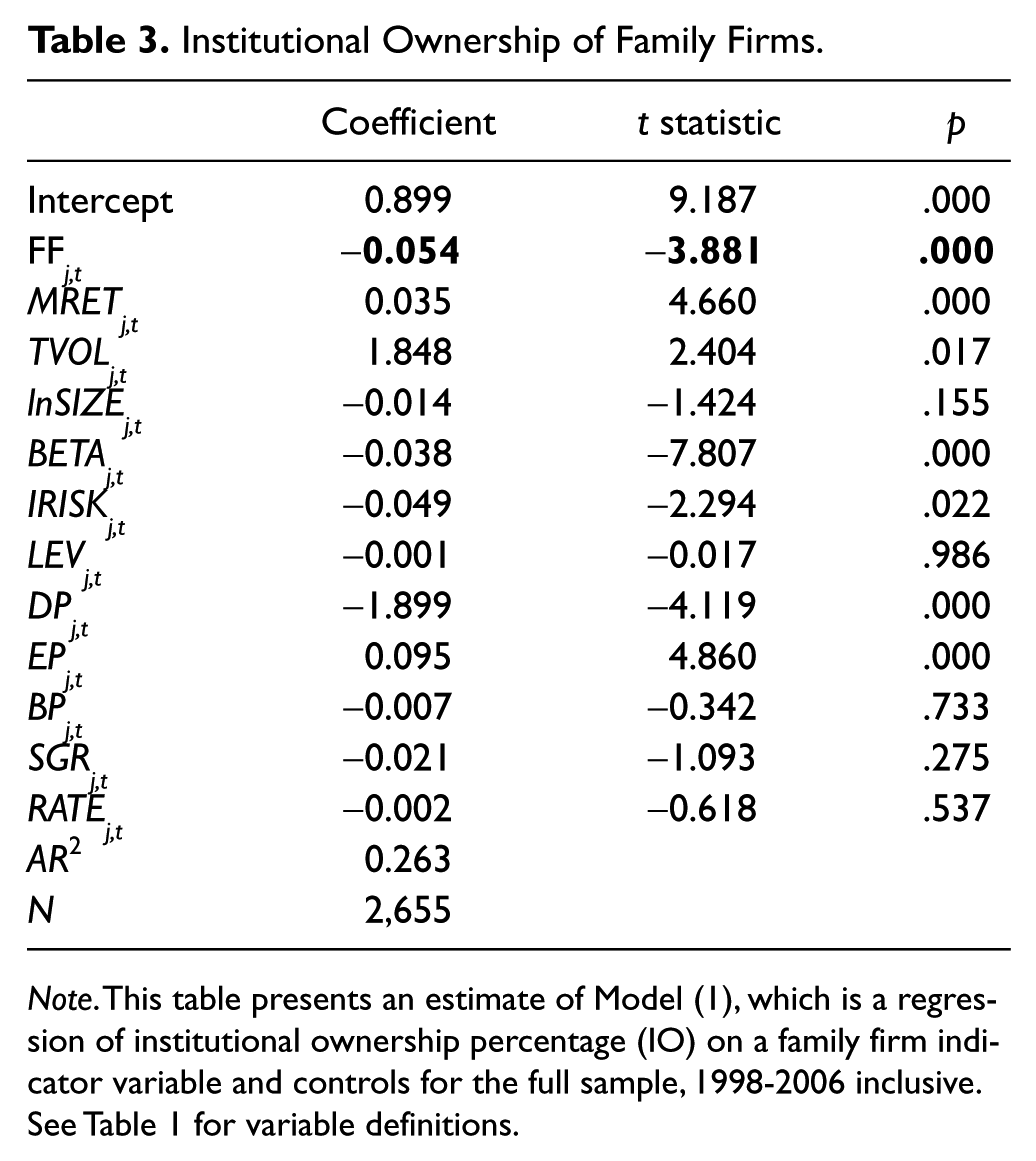

Table 3 presents the estimate of Model (1) using a sample of S&P 500 firms (excluding financials and utilities) for the entire sample period spanning 1998-2006. The regression results show that the variable of interest, FFj,t is negative and significant (coefficient = −0.054; t-stat = −3.88). The coefficient indicates that, after controlling for other factors that explain it, institutional ownership, is 5% lower for family firms. This shows that if a firm is a family firm, ceteris paribus, the level of institutional ownership is significantly less than in a nonfamily firm.

Institutional Ownership of Family Firms.

Note. This table presents an estimate of Model (1), which is a regression of institutional ownership percentage (IO) on a family firm indicator variable and controls for the full sample, 1998-2006 inclusive. See Table 1 for variable definitions.

The coefficients on the control variables are generally consistent with prior research. The adjusted R2 of 26.31% implies that our model explains around 26% of the variation of institutional ownership in this sample. This is consistent with the explanatory power of prior models of institutional ownership (Bushee, 1998).

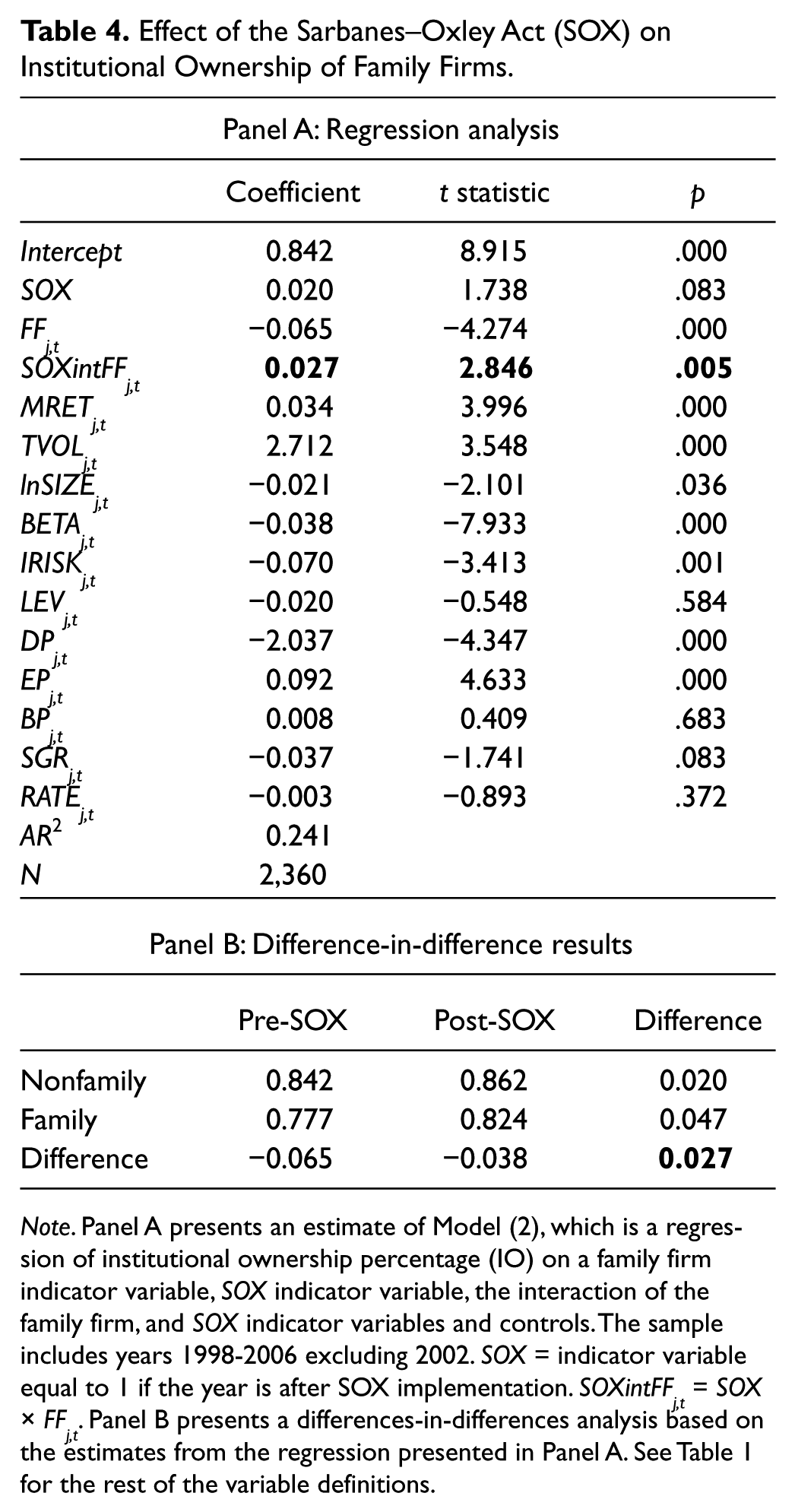

Panel A of Table 4 presents the results of Model (2), which tests our second hypothesis.

Effect of the Sarbanes–Oxley Act (SOX) on Institutional Ownership of Family Firms.

Note. Panel A presents an estimate of Model (2), which is a regression of institutional ownership percentage (IO) on a family firm indicator variable, SOX indicator variable, the interaction of the family firm, and SOX indicator variables and controls. The sample includes years 1998-2006 excluding 2002. SOX = indicator variable equal to 1 if the year is after SOX implementation. SOXintFFj,t = SOX × FFj,t. Panel B presents a differences-in-differences analysis based on the estimates from the regression presented in Panel A. See Table 1 for the rest of the variable definitions.

The second hypothesis evaluates the impact of SOX on institutional ownership in family firms. We estimate Model (2) on a sample of firms that spans 1998-2006 excluding 2002 (since this is the year that most of the SOX requirements became effective). This provides a period of 4 years prior to and 4 years after SOX to examine the effect of SOX on institutional ownership of family firms. The results show that, consistent with our second hypothesis, the variable of interest, SOXintFFj,t is positive and significant, suggesting that institutional investors increase their ownership in family firms after SOX. The coefficients on the control variables are generally consistent with prior research. The adjusted R2 of 24.1% implies that our model explains around 24% of the variation of institutional ownership in this sample consistent with prior research. To facilitate understanding of the differences-in-differences design the results are summarized in Panel B of Table 4 in the same format as Figure 1.

As Panel B of Table 4 makes clear, institutional ownership increased for all firms in our sample after SOX. In the pre-SOX period institutional ownership is 6.5% less for family firms on average, but post-SOX the difference is only about 3.8%. Post-SOX, institutional ownership in nonfamily firms increased by 2% whereas institutional ownership in family firms increased by 4.7%. Thus, institutional ownership in family firms increased by 2.7% more than it did in comparable nonfamily firms. This difference is statistically significant at the 1% level.

In all our regression analyses, we use the firm-level clustering method recommended by Petersen (2009) to correct for autocorrelation and heteroscedasticity and year-fixed effects since we have a panel data set. Variance inflation factors indicate that multicolinearity is not a problem in either regression.

Sensitivity Analysis

The dependent variable in our primary regression analysis is defined as shares held by institutions divided by total shares outstanding consistent with prior research (Bushee, 1998). However, our research is concerned with family firms which by definition frequently have large insider ownership. This may cause a purely mechanistic difference in institutional ownership across family versus nonfamily firms as investors are simply unable to acquire a higher percentage of ownership as a result of family ownership. We use two different approaches to demonstrate that our results are not driven by a mechanistic negative correlation between institutional ownership and family ownership.

First, we approach the problem by redefining our dependent variable to exclude the effect of ownership by family members. The dependent variable in our reported models is the number of shares owned by institutions divided by all outstanding shares which would include shares owned by institutions, retail investors, and family members. Using blockholder data based on the work of Dlugosz, Fahlenbrach, Gompers, and Metrick (2006), we identify and exclude from our calculations blocks of shares owned by family members. The resulting dependent variable is number of shares owned by institutions divided by shares owned by institutions and retail investors. Thus, it captures exclusively the relative distribution of available shares between institutions and atomistic, retail investors. We replicate all our analyses using this adjusted dependent variable and find results that are quantitatively and qualitatively similar to our reported results.

Second, we use the presence of institutional investors at different thresholds as a dependent variable. The idea is that the granularity offered by the thresholds, although not immune to the possibility of a mechanistic negative correlation between institutional ownership and family ownership, is less likely to be affected by it. We use thresholds at different levels of granularity from deciles to quartiles. We use probit models to replicate all our analyses using these adjusted dependent variables and find results which are quantitatively and qualitatively similar to our reported results. Consequently, our results do not appear to be driven by a simple mechanistic negative correlation between institutional ownership and family ownership.

In our SOX analysis, we use a difference-in-difference analysis based on a pooled regression. We verify that result in two distinct ways.

First, we examine each of the subsamples independently. We perform independent regressions of Model (1) for the period 1998-2001 and 2003-2006. Although this does not allow for a statistical test across models, it allows us to verify that results are as we expect within each period if a change has indeed taken place in response to SOX. The coefficient on our family firms indicator is −0.065 in the pre-SOX period and −0.038 in the post-SOX period as expected.

Second, as another sensitivity check, we perform a changes analysis using the following model:

where Δ denotes the change in each variable from the pre-SOX period to the post-SOX period. For each variable, we calculate the post-SOX average and the pre-SOX average. This changes analysis allows each firm to act as its own control for all firm-specific factors. We find the coefficient on FFj,t (β1) to be approximately 0.02 and significant at the 10% level, which demonstrates a significant change consistent with our pooled regression providing additional confidence in our results. The magnitude of the change is also comparable with the results shown in Table 4.

Discussion and Conclusions

Discussion of Results and Contribution to Theory

A distinguishing feature of our research is its focus on outside stakeholders. Theory development and empirical investigation of SEW has focused, so far, on internal stakeholders (family members, managers of family firms, etc.) and the consequent effects on firm behavior and performance. Prior research has suggested that external stakeholders might suffer as a result of the family firm’s strategic choices and demonstrated negative outcomes for external stakeholders in some settings (Berrone et al., 2012; Gordon & Nicholson, 2008; L. A. Kidwell & Kidwell, 2010; R. E. Kidwell, 2008). To add to prior work, we theorize that not all external stakeholders treat such potential losses passively. Rather, we expect that sophisticated external investors will act proactively and strategically in response to potential deviation from financial profit maximization in family firms which are likely to emphasize SEW. Specifically, we argue that sophisticated investors are more likely to identify these problems in family firms and avoid investments in such firms. Consequently, we predict that institutional investors, who are more sophisticated than retail investors, will ceteris paribus, be averse to investing in family firms.

Consistent with our first hypothesis, we demonstrate that institutional investors’ stake in family firms is, on average, 5% less than in nonfamily firms. These results hold after controlling for other known determinants of institutional investment. There is evidence of superior financial performance of family firms and family firms are less likely to suffer from Type 1 agency problems, both of which should lead to greater institutional investment in family firms. Thus, the most likely explanation of our results is that Type 2 agency problems are more prevalent and difficult to resolve in family firms. Furthermore, based on our results, it appears that sophisticated investors such as institutional investors are better able to recognize such problems in family firms than retail investors.

Much of the current research has noted the positive benefits of family firms pursuing SEW (Berrone et al., 2010; Cennamo et al., 2012). On the other hand, some studies (i.e., Kellermanns, Eddleston, & Zellweger, 2012) have suggested that pursuit of SEW by family firms is not universally positive and may, in fact, prove harmful to nonfamily stakeholders. Our first finding may be interpreted as being consistent with this view. Namely, pursuit of SEW by family firms leads to Type 2 agency problems between the family and outside investors seeking high returns which cannot be easily resolved with financial contracts. In addition, if the family firm needs to access the capital markets, these Type 2 agency problems may prove harmful to the family firm itself since they make family firms less attractive to institutional investors which are an increasingly important source of capital.

Furthermore, SEW consistent behaviors have been demonstrated and evaluated in many regulatory regimes. Yet the relation between the regime and the family’s ability to act on the desire for SEW and the resulting decisions made by external stakeholders has not been fully considered or examined. We draw on institutional theory and posit that in regulatory regimes which provide more protections for external stakeholders, external stakeholders will be less concerned about family firms deviating from the profit motive. We use the passage of SOX to explore this issue empirically.

The corporate governance environment improved significantly after SOX and such improvement served to substantially reduce the power imbalance between inside and outside shareholders. We argue that, in this case, government regulation in the form of SOX eases some of the tension between the external stakeholders and family within a family firm. Consequently, we predict that ceteris paribus, institutional investors will be relatively less averse to investing in family firms after SOX.

Consistent with our second hypothesis, we demonstrate that the aversion to family firms by institutional investors declined significantly subsequent to SOX. First, these results confirm our original contention of Type 2 agency problems within family firms. Second, these results provide novel evidence of the ability of regulation to mitigate the Type 2 agency problems that develop due to the pursuit of SEW by family owners. This advances our understanding of family firms because this study provides specific evidence of the impact of a regulation on the conflicting motivations of outside investors and the family in family firms.

We, thus, identify two distinct theoretical contributions in this article. The SEW approach has so far helped to explain family firm behavior that deviates from the predictions of purely financial motivated agency theory. The approach has focused on explaining the behavior of the firm or internal actors within the firm. In this article, we extend the insights from SEW to predict the actions of external entities who may be affected by SEW pursuit in family firms. We show that sophisticated investors are proactive in their avoidance of family firms because of the emphasis on noneconomic interests in such firms, thereby demonstrating the applicability of the SEW approach to external actors. Second, drawing on institutional theory we hypothesize and demonstrate in one setting that the formal regulatory regime has an effect on the extent to which external stakeholders are likely to be affected by a family’s affective motivations. This expands the focus of the SEW approach and suggests that future research more fully consider both the formal and informal rules under which the family operates. Both sets of rules influence the ability of the family to act on the SEW-based motivation and the consequent behavior of the family firm. Thus, properly incorporating this institutional view with SEW approach should lead to more accurate predictions.

Our article forms an interesting complement to a recent study, Miller et al. (2013), which evaluates institutional pressure to conform to industry norms on family firms. They rely on institutional theory to argue that family firms compensate for their unconventional governance structures by strictly conforming to industry norms in the strategies. Implicit in their arguments is that external actors (i.e., market participants) tend to look negatively on the unconventional governance structure of family firms, hence the need for strategic conformance. This is confirmed by our results for the test of the first hypothesis which shows that institutional investors tend to avoid family firms. Miller et al. (2013) find that such conformity has a positive effect on family firms’ financial performance when measured using accounting variables such as return on assets. However, conformity has no impact on the market’s perception of family firms suggesting that investors do not see any value addition through such conformity. By comparison, our study shows how institutional pressure on family firms and the consequent changes actually bring about tangible changes in the actions of some (and quite important) market participants, namely, institutional investors. Although both studies evaluate markets’ perception of changes brought about by institutional pressures, there are two significant differences. Our study evaluates the market participants’ response to involuntary changes in the governance and control structure of the firm whereas the Miller et al. study looks at voluntary strategic conformity. Whether the observed difference in results is due to the nature of change in the two studies (governance and control structure vs. strategic conformity) or the nature of the choice (involuntary vs. voluntary) is a subject for future research.

Practical Implications

Our results also have practical implications for family owners, institutional investors, and regulators. As previously mentioned, institutional investors have become a “dominant force in financial markets” accounting for more than 50% of total U.S. equity ownership and are now the price-setting marginal investors for many firms (Bennett et al., 2003). Furthermore, family-owned businesses compose the majority of firms in the world and more than one third of the S&P 500. Consequently, institutional investors’ preferences for investing in family firms have implications for the ability of individual family firms to raise capital and for the proper societal distribution of capital. By showing that institutions own a smaller percentage of family firms, ceteris paribus, we show that the unique features of family firms’ ownership structure lead institutions to avoid investments in them. Also, by showing that SOX decreased the difference between family and nonfamily firms, we provide regulators with information about the effectiveness of SOX in mitigating the Type 2 agency problems that develop due to the pursuit of SEW by family owners.

Encouraging institutional investments may not be the best strategic alternative for family firms especially where the protection of the family’s SEW is an important goal. Institutions’ pursuit of profit can lead to significant value loss for the family. For example, two institutional owners initiated a 2006 proxy fight over the Topps Company, which led to significant control and financial losses for the founding family (de la Merced, 2006).

However, some family firms will want to expand, at which point they will outgrow the internal sources of financing available to family firms, and will need to seek external capital. In today’s business environment, institutional investors are a significant source of external equity capital. Hence, our findings also provide guidance to family firm owners about how the concerns of nonfamily shareholders may be mitigated. Since the SOX-mandated corporate governance improvements reduced the aversion of institutional investors to family firms, additional reforms of corporate governance in the form of more independent boards and board subcommittees and more transparent controls to prevent wealth expropriation could further mitigate institutional investor aversion. Moreover these suggestions would be of even greater importance to smaller (and nonpublic) family firms that wish to approach sophisticated capital sources for investments. Since SOX reforms were mainly targeted toward public firms, proactively implementing the reforms suggested above may increase the probability of private family firms raising capital from sophisticated investors.

Limitations

Although our study does provide new evidence and extends theory on the effect of Type 2 agency problems due to SEW considerations within family firms and the ability of regulation to mitigate these problems, it has certain limitations that yield future research opportunities. A main insight of our study is the reaction of external stakeholders of family firms to longitudinal changes imposed on the socioemotional fabric of such firms by regulatory change. One potential limitation of our study is that our measure of regulatory change is a time variable (pre- and post-SOX). There were several other changes that occurred during the same period such as the dot.com crash and the corporate scandals because of improper financial reporting, that may also be responsible for the observed results. Although these other happenings potentially pale in magnitude compared with the effects of SOX (President G. W. Bush called SOX “the most far-reaching reform of American business practices since the time of Franklin Delano Roosevelt”; Bumiller, 2002) a possible solution to settle this question is to replicate this study internationally in different regulatory settings. By doing so, it would be possible to evaluate the external stakeholder response to different regulatory regimes when time is invariant. This would provide additional insights into external stakeholder reactions on the interaction of the three institutional logics: markets, family, and government.

A second limitation of our study is that it focuses on large, public U.S. corporations for which empirical archival data are publicly available. An extension would be to evaluate the affinity of institutional investors for smaller and/or unlisted family firms, which would necessitate hand-collected data. A study conducted using a carefully designed survey (as recommended by Berrone et al., 2012) will be able to collect more detailed data that can provide additional insights on these issues. Finally, we use empirical data to analyze external parties’ (in this case, the institutional investors) realized aversion to family firms. However, a survey of institutional investors may yield a more detailed picture of their actual awareness of Type 2 agency problems and SEW considerations in family firms and the extent to which such considerations affect their investment decisions. Therefore, although this study is a first step in investigating the reactions of external parties to the unique motivations of family firm managers, the insights can be confirmed and expanded by additional research along the suggested paths.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.