Abstract

Gender diversity in corporate boards and the functioning of compensation committees are two issues that have caught the attention of legislators and regulators in many countries. Using data from 5,630 observations from public companies in the United States, we find that firm and board characteristics are associated with the presence of females on the compensation committee. However, female presence on the compensation committee is not significantly associated with CEO pay (as a proportion of shareholder wealth increase). We then discuss issues related to research on gender diversity in corporate boards, and offer some suggestions for future research on diversity in corporate boards.

Introduction

In this article, we examine the gender diversity of compensation committees, and whether such diversity is associated with the relative magnitude of CEO compensation. We then derive an agenda for future research about diversity in corporate boards, with a particular focus on compensation and audit committees. We are motivated by recent efforts of legislators in many countries seeking to increase the proportion of women in corporate boards, through persuasion and/or legislative quotas.

The non-profit group Catalyst, which seeks to promote women in business and leadership, notes that less than 20% of board seats in the S&P 500 companies are held by women (Catalyst, 2015); the proportion is even lower among smaller firms, and the lack of female representation in corporate boardrooms is a global phenomenon (Deloitte, 2013). This has led to legislative gender quotas on corporate boards in some countries. Norway led the way in 2003 with a requirement that at least 40% of the directors of public companies must be female. Subsequently, a diverse array of countries such as France, Spain, Italy, Malaysia, India, and the UAE have implemented gender quotas for boards of public companies (Deloitte, 2013; “The Spread of Gender,” 2014). Similar legislation has been proposed elsewhere, including Brazil, Canada, Germany, Israel, and the Philippines, while governments in Australia, Sweden, and the United Kingdom have encouraged companies to voluntarily increase female representation on corporate boards or risk having quotas imposed at a later date (Ernst & Young, 2014; “The Spread of Gender,” 2014). In the United States, the Securities and Exchange Commission (SEC; 2009) has issued a rule requiring companies to disclose the role of diversity in considering candidates for director nominations.

Evidence related to any relationship between board diversity and performance has both public policy and governance consequences. If there is consistent evidence that there is a positive association between board diversity and firm performance, then there is a business case for diversity. In the absence of such evidence, arguments for diversity must be made on other grounds. And, if diversity leads to lower performance then the costs of diversity must be considered in any discussion about making boards more diverse.

In theory, gender diversity on boards can have positive implications for firms. Diversity in the boardroom can lead to consideration of alternative viewpoints (Zahra & Pearce, 1989); board diversity also increases the external legitimacy, and can make the firm more attractive to talented employees (Hambrick, Werder, & Zajac, 2008). Conversely, diversity can also increase conflict, worsen communication, and reduce trust (“The Downside of Diversity,” 2014). Empirical evidence about the performance effects of gender diversity on boards is mixed. Adams, de Haan, Terjesen, and vanEes (2015, p.78) note that the mixed findings related to diversity and firm performance can be attributed to “differences across studies in measures of performance, methodologies, time horizons, omitted variable biases and other contextual issues.”

In evaluations of board performance, it may be more appropriate to focus on the composition of the sub-committees of the board because most board decisions are made within smaller groups or committees (Kesner, 1988). In the context of accounting, two board committees are particularly relevant: audit and compensation committees. The former is an integral part of the financial reporting process, while the latter often uses accounting numbers in setting targets related to executive compensation contracts (and, thus, influences managerial judgments related to accounting). Both of these committees have a crucial role in the corporate governance process.

Some studies have examined the association between gender diversity and the functioning of audit committees. 1 Srinidhi, Gul, and Tsui (2011), using data from 2001 to 2007 and after controlling for self-selection, find that firms with female directors on the audit committee exhibit higher earnings quality (as measured by lower discretionary accruals and lower propensity to manage earnings and beat benchmarks by a small amount). Similarly, Thiruvadi and Huang (2011) show, using data from 320 S&P SmallCap 600 firms, that the presence of a female director on the audit committee is associated with lower discretionary accruals. In contrast, Sun, Liu, and Lan (2011) find, using a sample of 525 observations over the period 2003 to 2005, that there is no association between the proportion of female directors on audit committees and performance-matched discretionary accruals. In terms of audit committee processes, Thiruvadi (2012) shows that audit committees with at least one female director are likely to meet more often than all-male audit committees while Ittonen, Miettinen, and Vähämaa (2010) find that firms with female audit committee chairs have lower fees.

However, empirical research about diversity in compensation committees is sparse. Two prior studies find that female directors are less likely to be appointed to the compensation committee (Adams & Ferreira, 2009; Bilimoria & Piderit, 1994). We extend this line of research by examining (i) the factors associated with a gender-diverse compensation committee and (ii) the association between the presence of female directors on the compensation committee and (a) executive pay, and (b) subsequent restatement of financial statements.

Compensation Committees and Gender Diversity

The performance of compensation committees of public companies has come under increased scrutiny from the public and regulators in recent years. Some common criticisms of compensation committees are that top executives are overpaid and that such compensation often has little association with performance (Landy, 2008; Morgenson, 2013). 2 A significant part of the blame for the global financial crisis is attributed by some to the outsized compensation and skewed incentive structures of corporate executives (Bebchuk, 2012; Ritholtz, 2009). Such concerns have also been reflected in recent actions by legislators and regulators. Sections 951 to 954 of Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 includes multiple provisions related to executive compensation of public companies, including the independence of compensation committees and their use of compensation consultants, as well as more detailed disclosures about pay-for-performance and the ratio of CEO pay relative to other employees. Subsequently, the SEC (2012) promulgated new rules related to the stock exchange listing standards for compensation committees.

Much of the blame for outsized executive compensation is attributed to docile and ineffective compensation committees. In theory, a strong and independent nominations committee should select effective and independent directors, a subset of whom would become members of the compensation committee; this should ensure that the executives are adequately, but not excessively, compensated. In practice, however, the CEO is dominant in many public companies and has a strong influence on who is selected for the board and also who is appointed on the compensation committee (Bear, Rahman, & Post, 2010). Compensation committees use compensation consultants to set the pay of the executive; however, a former Chancellor of the Exchequer noted in testimony to the U.K. Parliament that “remuneration consultants . . . are a profession that makes prostitution seem thoroughly respectable” (Lawson, 2013).

Westphal and Zajac (1995) find that CEOs are likely to select directors who are demographically similar to them, which in turn can lead to a board that is more likely to support the CEO (including, executive compensation related matters). In contrast, greater diversity on the board can lead to more effective monitoring (Bear et al., 2010).

Prior studies show that gender diversity on the board is associated with higher levels of monitoring by the directors. Nielsen and Huse (2010) find that higher proportions of female directors are positively related to board strategic control. Adams and Ferreira (2009) show that gender-diverse boards are associated with better attendance records, and that CEO turnover is more sensitive to stock performance in such firms. 3 Thus, based on prior empirical evidence that gender-diverse boards are associated with greater monitoring, we conjecture that female directors will tend to emphasize more on pay-for-performance; hence, gender diversity on the compensation committee makes it less likely that there will be excessive executive pay. 4 This leads to our hypothesis (in the alternative form):

Method and Data

Our primary data source is The Corporate Library’s directorship database for the years 2006 to 2008. We obtain our financial and stock price data from the Compustat and CRSP databases. To minimize the influence of outliers, we winsorize all continuous variables at the first and 99th percentiles.

We use the following model to examine the determinants of factors associated with the presence of a female on the compensation committee:

The dependent variable, FEM, is measured in two different ways. First, we use a dichotomous variable, FEMD, which takes the value of 1 if there is at least one female on the compensation committee and 0 otherwise; we use a logistic regression model for this analysis. Second, we use a continuous measure, FEMP, which is the proportion of females on the compensation committee; we use an ordinary least squares (OLS) regression for this analysis. In our analyses, we control for clustering by firms.

Our independent variables are based on results from prior studies. As larger firms are more likely to have a diverse board (Carter, D’Souza, Simpkins, & Simpson, 2003; Hillman, Shropshire, & Cannella, 2007), we expect the coefficient on LMV (log of market value) to be positive. Carter et al. (2003) find that the proportion of women and minorities on boards increases as the number of outsiders on the board increases; extending this logic, we expect a positive coefficient for PROUT (proportion of outside directors on the compensation committee). Higher the number of directors on the board, the greater the likelihood that there will be females on the board; this in turn increases the likelihood of female representation on the compensation committee. Similarly, the greater the number of directors on the compensation committee, the higher is the likelihood of a female director being present on the committee. Hence, we include BDNUM and CCNUM in our model.

Coffey and Fryxell (1991) argue that the influence of institutional investors may make it more likely that companies will adopt diversity practices; hence, we expect a positive coefficient on INSTOWN. Pressure from governance activists is more likely when a firm has not been performing well in the recent past. Such arguments suggest that female directors on the compensation committee would be less likely in firms with better long-term performance (LTPERF). We include an indicator variable for NYSE listing because there are significant differences between NYSE- and non-NYSE-listed firms along many governance dimensions (Wintoki, 2007). Finally, we expect that women are more likely to be appointed to the board and committees of the board in firms that are incorporated in more liberal states. We measure this using the proportion of votes for Barack Obama minus the proportion of votes for John McCain during the U.S. presidential election of 2008 (OM).

Next, we use the following model to examine the relation between gender-diverse compensation committees and executive compensation:

The dependent variable, PAYPER, is the ratio of annual change in market value of the company over the total compensation of the CEO. This ratio measures the “bang for the buck” for shareholders from a given dollar of CEO compensation; higher values are “better” from the perspective of shareholders (who are represented by the compensation committee). As in most corporate governance research, we control for firm size. We also control for compensation committee composition (PROUT) and board size (BDNUM), as these two factors can drive the extent to which the compensation committee and the board are proactive and look out for shareholder interests. We control for institutional ownership (INSTOWN) as institutions are more likely to exert pressure on the board. As in the earlier regression for compensation committee membership, we include controls for the stock exchange (NYSE) and the political climate of the state of location of the company (OM). AGE and TENURE measure the average age and tenure of the compensation committee directors. We also include Book-to-Market ratio and return volatility as additional controls, apart from industry dummies based on the Fama-French classification. FEMCC is our variable of interest, and we use two different measures for this variable: FEMD and FEMP, which are defined as before.

Results

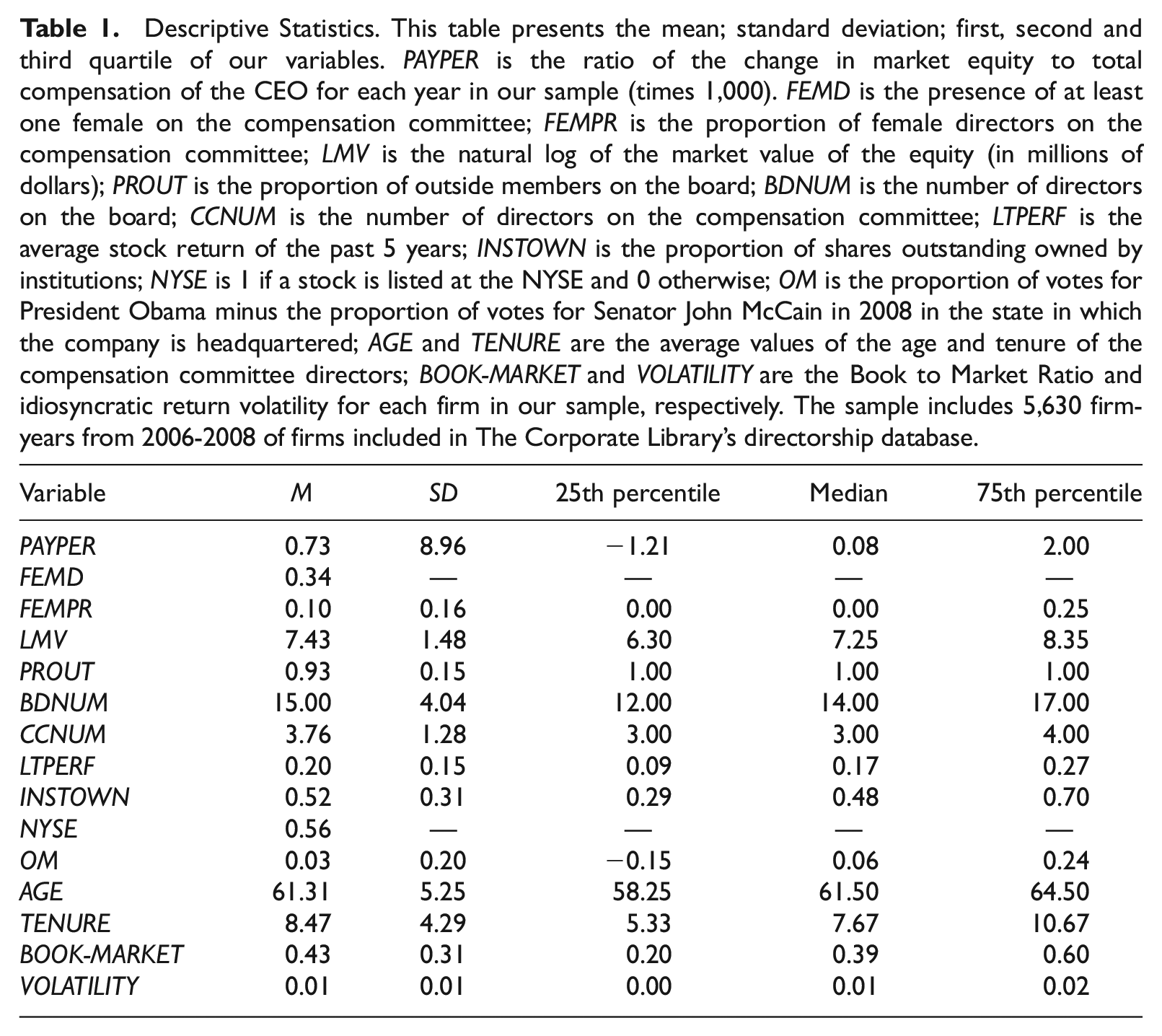

Table 1 provides descriptive evidence about the sample. Overall, 34% of the observations have at least one female director on the compensation committee. In terms of individual directors, just over 10% of the compensation committee directors are female. The average number of directors on the full board and compensation committee are 15 and 3.76, respectively. Outside directors account, on average, for 93% of compensation committees. The average age of compensation committee directors is 61.31, and the average tenure of such directors is 8.47 years. 5

Descriptive Statistics. This table presents the mean; standard deviation; first, second and third quartile of our variables. PAYPER is the ratio of the change in market equity to total compensation of the CEO for each year in our sample (times 1,000). FEMD is the presence of at least one female on the compensation committee; FEMPR is the proportion of female directors on the compensation committee; LMV is the natural log of the market value of the equity (in millions of dollars); PROUT is the proportion of outside members on the board; BDNUM is the number of directors on the board; CCNUM is the number of directors on the compensation committee; LTPERF is the average stock return of the past 5 years; INSTOWN is the proportion of shares outstanding owned by institutions; NYSE is 1 if a stock is listed at the NYSE and 0 otherwise; OM is the proportion of votes for President Obama minus the proportion of votes for Senator John McCain in 2008 in the state in which the company is headquartered; AGE and TENURE are the average values of the age and tenure of the compensation committee directors; BOOK-MARKET and VOLATILITY are the Book to Market Ratio and idiosyncratic return volatility for each firm in our sample, respectively. The sample includes 5,630 firm-years from 2006-2008 of firms included in The Corporate Library’s directorship database.

In untabulated results, we find that women account for about 11% of the total number of directors and the overall number of compensation committee directors for the firms in our sample. 6 Thus, the dearth of female directors, documented in many prior studies, continues to be the case in our sample. However, the data also indicate that given a board membership, a female is at least as likely to be on the compensation committees as her male counterparts. In addition, we also find that, compared with their male colleagues, female directors on compensation committees in our sample are younger (60.1 vs. 61.6 years old), have shorter tenure as directors (8.0 vs. 8.5 years), and are more likely to be outsiders (94.6% vs. 93.4%). These findings reinforce results from prior research that female directors are different from their male counterparts in many other demographic characteristics.

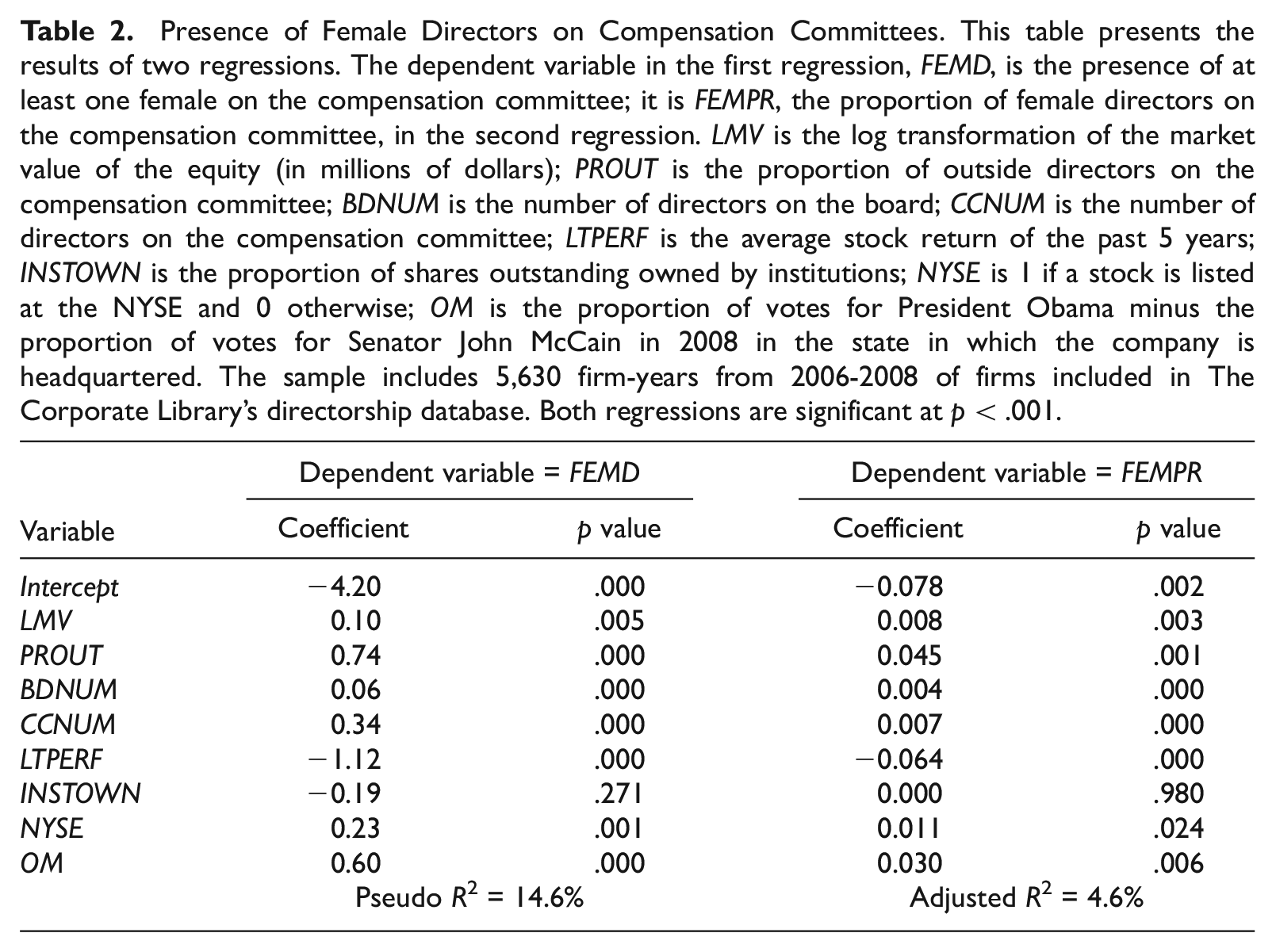

Table 2 presents the results from the regressions to examine factors associated with the presence of female directors on the compensation committee. The first (logistic) regression has FEMD as the dependent variable, while the second (OLS) regression has FEMP as the dependent variable. All of our control variables, except institutional ownership, are significant at conventional levels in both regressions. The results indicate that females are more likely to be present on the compensation committee of firms when the firm (a) is larger, (b) has a higher proportion of outsiders on the board, (c) has more directors on the board, (d) has more members on the compensation committee, (e) has worse long-term performance, (f) is listed in the NYSE, and (h) is incorporated in a state that is politically more liberal.

Presence of Female Directors on Compensation Committees. This table presents the results of two regressions. The dependent variable in the first regression, FEMD, is the presence of at least one female on the compensation committee; it is FEMPR, the proportion of female directors on the compensation committee, in the second regression. LMV is the log transformation of the market value of the equity (in millions of dollars); PROUT is the proportion of outside directors on the compensation committee; BDNUM is the number of directors on the board; CCNUM is the number of directors on the compensation committee; LTPERF is the average stock return of the past 5 years; INSTOWN is the proportion of shares outstanding owned by institutions; NYSE is 1 if a stock is listed at the NYSE and 0 otherwise; OM is the proportion of votes for President Obama minus the proportion of votes for Senator John McCain in 2008 in the state in which the company is headquartered. The sample includes 5,630 firm-years from 2006-2008 of firms included in The Corporate Library’s directorship database. Both regressions are significant at p < .001.

In Table 3, we present the results related to our hypothesis. Both of the regressions in Table 3 are statistically significant. Considering the governance-related variables, we find that (a) the coefficient of BDNUM is negative and significant, indicating that larger boards are less likely to be “efficient” in terms of protecting shareholder interests; and (b) the coefficient of TENURE is negative and significant, indicating that compensation committees that have long director tenure are more likely to be associated with higher executive compensation. 7 However, the gender variable is not significant in either regression.

Female Directors on Compensation Committees and Executive Compensation. This table presents the results of two multivariate OLS regressions. The dependent variable, PAYPER, in each regression is the ratio of the change in market equity to total compensation of the CEO (times 1,000) for each year in our sample. LMV is the log transformation of the market value of the equity (in millions of dollars); PROUT is the proportion of outside directors on the compensation committee; BDNUM is the number of directors on the board; CCNUM is the number of directors on the compensation committee; LTPERF is the average stock return of the past 5 years; INSTOWN is the proportion of shares outstanding owned by institutions; NYSE is 1 if a stock is listed at the NYSE and 0 otherwise; OM is the proportion of votes for President Obama minus the proportion of votes for Senator John McCain in 2008 in the state in which the company is headquartered; AGE and TENURE are the average values of the age and tenure of the compensation committee; Book-Market is the ratio of book to market equity; Volatility is the idiosyncratic daily return volatility averaged over each month; Industry-Dummies are dummy variables for the Fama-French 48 industry classification. The sample includes 5,630 firm-years from 2006-2008 of firms included in The Corporate Library’s directorship database. Both regressions are significant at p < .01.

Further Tests

As an additional test, we use the CEO efficiency ranking from Forbes magazine in 2009 and use the reverse of this ranking (i.e., higher values represent a better compensation committee) as the dependent variable. When we combine the Forbes data with our dataset, we are able to obtain all relevant data for 172 firms. In this analysis, we use the average values (over the 3 years) of the independent variables in regression model (Equation 2) above. Once again, we find that the gender variables are not significant in the model.

While the audit committee is primarily responsible for the quality of financial reporting, the actions of the compensation committee can have an indirect effect on financial reporting quality. If a compensation committee is effective, then the magnitude of the possible executive compensation would not be excessive and executives should be less likely to manipulate financial statements (to achieve compensation related goals) which then have to be restated. 8 Hence, we examine subsequent restatements of financial statements. We find that the subsequent restatement rates are 12.4% and 12.9% for the observations with and without a female director on the compensation committee; the difference is not statistically significant.

Overall, the results indicate that gender diversity on the compensation committee is not associated with CEO pay or subsequent restatements. Any null result is, of course, subject to questions about the power of the test. However, we note that our sample size is quite large, and we obtain similar inferences with multiple dependent variables as well as two different measures of the independent variable of interest. Finally, our inferences remain unchanged when we use a two-stage regression approach to control for endogeneity.

Discussion

Many studies have highlighted the fact that women are underrepresented on corporate boards. This has led to politicians intervening, indirectly through persuasion or directly through legislative quotas, to increase female representation on corporate boards. Norway was the first country, in 2003, to mandate quotas for female directors. Subsequently, many countries spanning the development and cultural spectrum have acted to implement gender quotas for corporate boards. In the United States, since 2009, the SEC has required companies to disclose the role of diversity in considering candidates for director nominations. In addition, activist investors and board monitoring and rating agencies (such as Institutional Shareholder Services and Thirty Percent Coalition) have sought to put pressure on public companies to include more women and other minorities in boards of directors.

SEC Commissioner Aguilar (2010), in a speech justifying the SEC’s 2009 rule related to board diversity, cited a study by CalPERS that diverse boards perform better than boards without diversity in terms of shareholder value. However, there are also many studies that show there is no (or negative) association between board diversity and subsequent performance (Gupta, Lam, Sami, & Zhou, 2015; Post & Byron, 2015). The use of research for social changes only increases the necessity for careful consideration of data and method related issues, in addition to detailed discussion of alternative explanations and limitations.

Prior research suggests that female directors are quite different from their male counterparts in the boardroom, along many dimensions. For example, studies show that compared with male directors, female directors are more likely to be (a) outsiders (Adams & Ferreira, 2009) and (b) more educated (Hillman, Cannella, & Harris, 2002). While research on corporate governance in general is subject to endogeneity problems (Hermalin & Weisbach, 1998), this may be particularly relevant for diversity: To the extent there are both corporate and personal characteristics that are associated with board/committee diversity, it is difficult to separate out the consequences of board/committee diversity from other causes. For example, de Cabo, Gimeno, and Nieto (2012) find that female directors are less likely at riskier banks. Similarly, Adams and Ferreira (2009) find that female directors are more likely to be outsiders than their male counterparts. Hence, care must be taken to disentangle the effects of gender from other underlying differences. The study by Srinidhi et al. (2011) is an example of carefully considering self-selection issues and using multiple measures to address the effects of diversity on audit committees; however, such careful approach to design, analysis, and inference remains the exception.

As more countries seek the legislative route for gender diversity, a natural temptation is to view such legislative quotas as exogenous shocks where endogeneity-related concerns become less of an issue (Ferreira, 2015). However, here again caution is warranted. For example, some studies have examined the introduction of such quotas on Norwegian firms’ performance (Ahern & Dittmar, 2012; Matsa & Miller, 2013). Nevertheless, a problem with such studies is that, unlike in the case of SOX, most legal developments take time; an initial version of the Norwegian quota law was enacted in 2003, but penalties were introduced only in 2005 and with an additional 2-year grace period to comply. Thus, a clean test becomes difficult given the many other confounding events during lengthy transition periods.

Norwegian data also show that forced diversity can be counterproductive. In Norway, the gender quota rule was applicable only for public limited companies. Perhaps not surprisingly, the number of publicly listed Norwegian companies decreased from 564 in 2003 to only 179, 5 years later (Dizik, 2015). Can we ignore the costs of going-private? How do we measure costs associated with going-private? Another problem relates to “golden skirts”—the phenomenon of a few highly sought after women sitting on multiple board seats, but busy-boarding does not enhance the quality of monitoring. In other words, legislative and regulatory action must consider both the benefits and costs associated with laws or regulations. As the “The Downside of Diversity” (2014) notes, “diversity can bring risks as well as benefits and perils as well as perks”; this is especially true for diversity that is driven by legislative and/or regulatory actions. This in turn requires well-designed empirical studies that address both sides of the equation.

There are many studies (primarily in management) that seek to examine the association between diversity and firm performance. However, given that there are too many other variables that can affect firm performance, perhaps it is more useful to focus on the effects of diversity on the corporate governance process, rather than seeking to detect causality between board diversity and firm performance. In this context, it is useful to remember that many substantive board actions happen not at the level of the full board but at sub-committees of the board. This means that there are some unique research opportunities for accounting researchers—by focusing on the audit and compensation committees. Furthermore, while some recent studies have examined the effects of audit committee diversity on a variety of measures that proxy for financial reporting quality as well as the interaction between the committee and auditors, research related to the compensation committee is sparse. More generally, a quick search indicates that there are numerous papers that have appeared in premier accounting journals with the phrase “audit committee” in the title of the article, but there is none with the phrase “compensation committee” in the title.

Research related to compensation committees is particularly useful because the composition and performance of corporate compensation committees has come under increased scrutiny in recent years, fueled in part by complaints about outsized executive pay. Such concerns have led to actions by both legislators and regulators; both SOX and the Dodd-Frank Act include sections related to executive compensation and the composition of compensation committees of public companies, while the SEC (2012) has promulgated new rules related to the standards for compensation committees.

In this study, we find that women continue to be significantly underrepresented on corporate boards. However, contrary to findings reported in earlier studies, we find that female directors are at least as likely as their male counterparts to serve as members of compensation committees. This suggests that the bias against female presence on the compensation committee, documented in prior studies examining earlier periods, may have given way to gender neutrality. We find that gender diversity on the compensation committee is associated with company characteristics, including size, exchange listing, ownership, and long-term performance. However, our findings also suggest that female presence on the compensation committee is not significant in influencing CEO compensation, nor is such presence associated with subsequent restatements of financial statements. Overall, it does not appear that the presence of females on the compensation committee leads to significant differences in the compensation of executives.

Our findings also suggest potential areas for future research. We find that there are very few instances where there is more than one female on the compensation committee. This has implications for the working of the committee, as representatives of underrepresented groups (such as women and minorities) may be more willing to open up and project their views when there is more than one of them in a group (Torchia, Calabro, & Huse, 2011).

We conclude by noting two other diversity-related areas that are worthy of attention from researchers. First, it would be interesting to examine the reaction of executives and boards in countries that have legislated gender quotas for corporate boards, as also the variations in such reactions across countries. As noted earlier, many public companies in Norway reacted to the legislation by becoming private. A different type of reaction occurred in India after the legal requirement, enacted in 2013, that all exchange listed companies must have at least one female director. Galani (2015) notes, “[s]ome Indian companies have broken the spirit of the rule by making token appointments. Reliance Industries, the country’s largest conglomerate by market value, has installed the wife of Chairman Mukesh Ambani as a director” while “[t]he stepmother of tycoon Vijay Mallya now sits on the board of a company in which he has a large stake.”

Second, there are many aspects to diversity and gender is only one factor. Research related to other aspects of board and committee diversity, including race and nationality, is sparse or non-existent. This in turn raises many interesting questions, which are opportunities for future research, about the effects of diversity on the performance of corporate boards. For example, are the effects of different forms of diversity different, and if so, how? Is one form of diversity more beneficial (or, costly) than the other? How do different forms of diversity interact in the functioning of boards and committees? How do different forms of diversity, and the pressure to have such diverse representation in boards, vary across countries and cultures? Empirical evidence about such issues would be quite useful for both academics and policy makers.

Footnotes

Acknowledgements

The authors thank an anonymous reviewer for many useful comments on an earlier version of the article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.