Abstract

The role of the Board’s Compensation Committee is to approve the design of the pay programs for the top executive officers and to approve specific payments based on the plans and the company’s performance. Typically, the specific responsibilities of the compensation committee is specified within the company bylaws. This includes composition of the committee, statement of pay philosophy, implementation of plans approved by the board, identification of specific performance objectives, assessment of competitive pay practices, approval of employment contracts, role of external consultants, preparation of a Compensation Discussion and Analysis Report consistent with Securities and Exchange Commission requirements and filing a copy of the committee minutes to the board of directors and responding to their questions. Committee members have responsibility to put shareholder’s interest above their own (duty of loyalty), understanding the issues and alternatives (duty of care) and exercising prudent judgment (avoiding conflict of interest) and acting in good faith. These actions are required to meet the business judgment rule and avoid being held liable to their actions.

Keywords

Role of the Compensation Committee

The establishment of a committee of the board of directors responsible for the pay of corporate officers and employee directors has become commonplace. In addition to approving the design and mix of compensation programs, it is also responsible for approving payments. Thus, it is accountable not simply for the form in which the corporate officers are paid but also for the level of payment. To ensure comparable treatment, the committee would also review for information purposes pay increases of other nonofficer executives within the company who are at a comparable pay level.

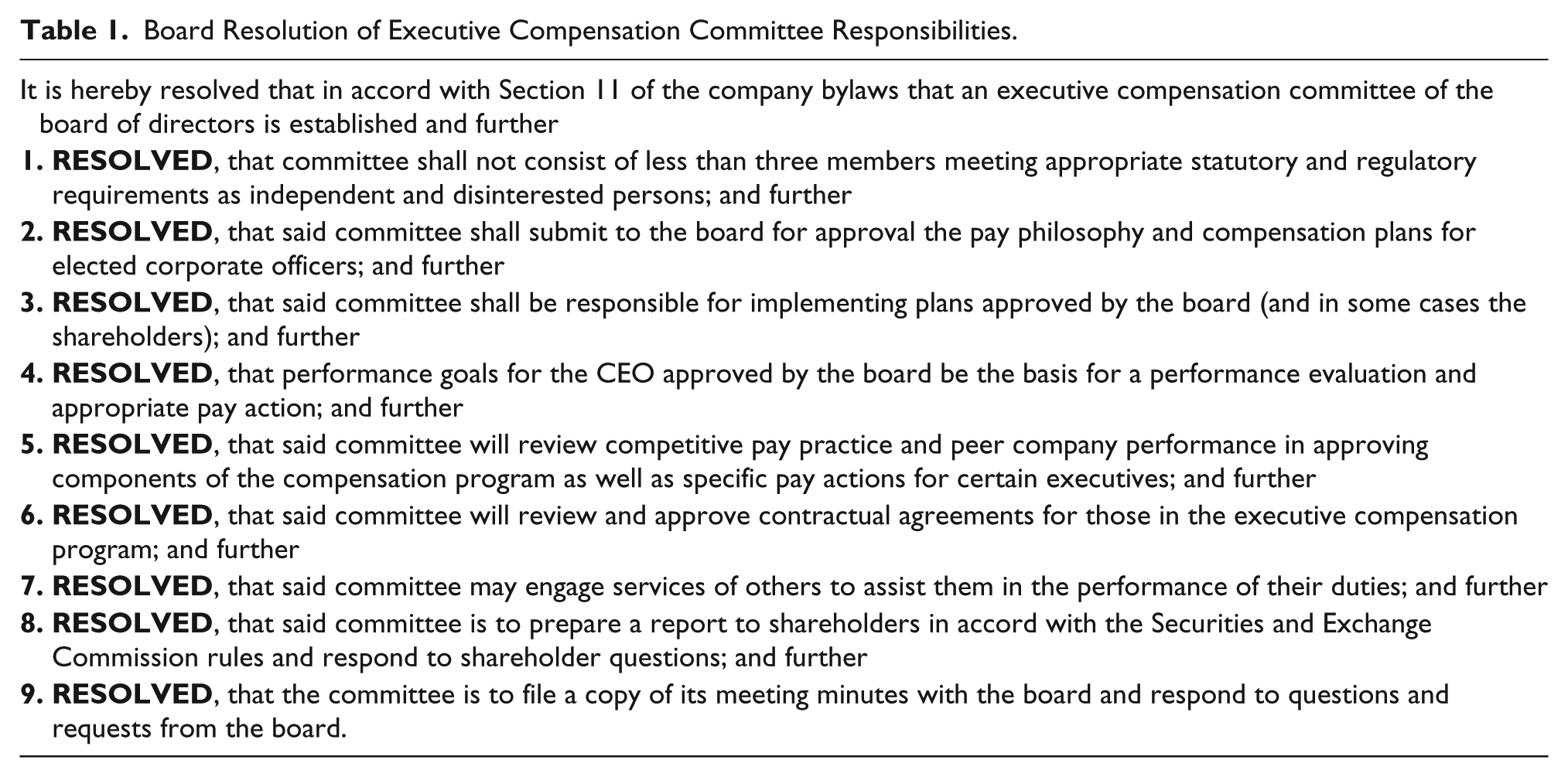

The board-approved resolutions (Table 1) are the basis for defining and describing the compensation committee role, beginning with the size and composition of the committee. They constitute the committee charter.

Board Resolution of Executive Compensation Committee Responsibilities.

Committee Membership

A rather common definition is the one shown in Table 1: The committee “shall not consist of less than three members meeting appropriate statutory and regulatory requirements as independent and disinterested persons.” Typically, all committee members are members of the board.

Composition of the Committee

Depending on the makeup of the particular board, the compensation committee made up solely of outside directors could consist of former government officials, bankers, lawyers, academicians or executives of other firms. Some people are critical of companies whose board membership consists of retired members of management and those considered to be suppliers of contractual services (e.g., bankers, outside counsel and management consultants). The retired executive may have fraternal ties to existing management, having hired and trained them. The presence of suppliers on the board may give a false signal to others that this company is “tied up” with a supplier. Such individuals cannot be considered true outside directors, that is, individuals independent of management.

Furthermore, Section 162(m) of the IRC imposes even stricter requirements. It stipulates the conditions under which pay in excess of $1 million for any of the proxy-named executives may be tax deductible for the company. In addition to excluding from the committee anyone receiving fees from the company for any professional services and current employees of the company, it also excludes former officers of the company, as well as any former employee receiving compensation for prior services (except for statutory benefit plans).

Because many of the performance measures used in the executive incentive pay plans are financial in nature, it could be argued that the compensation committee have at least one person who is a member of the audit committee. If this is not practical because of the meeting dates of the two committees, perhaps it is appropriate to periodically have a combined meeting of the two committees.

Knowledge of executive compensation programs is obviously extremely helpful in serving on a compensation committee. However, from the viewpoint of knowledge, the best candidate is an executive compensation consultant or similar individual in the employ of another company.

Another excellent candidate for the compensation committee is the professional director (i.e., someone whose only employment is serving on a number of boards), usually a retired executive. This may become a very attractive second career for those who wish to take early retirement within their own firms, especially if shrinking inside-board sizes preclude being elected while working.

Because experience is important, it may be unwise to rotate members of the committee too early. Perhaps rotation of one person every several years would allow the committee to retain the needed expertise.

Committee Chair

The chair may either be elected by members of the committee or by the board, based on a recommendation from the governance committee (which also recommends who serves on the committee).

The responsibility of the chair is to prepare the agenda for each meeting (ensuring members have meeting materials in sufficient time to review prior to the meeting), preside at each meeting and ensure committee actions are reported in meeting minutes and are later implemented. Before preparing a monthly meeting agenda, the chair should establish a key event timetable for the year.

Committee Secretary

Rather than appoint one of the committee members as secretary, it might be appropriate to select the head of human resources (since it is expected that that person will be in attendance at virtually every meeting anyway). An alternative would be to appoint someone from the general counsel’s staff, such as the attorney responsible for Securities and Exchange Commission (SEC) matters.

In addition to ensuring the meeting minutes are prepared and distributed in a timely manner, the secretary should see to other requests by the chair and committee members. This ranges from ensuring a meeting place with appropriate support materials, beverages and food to compiling and distributing agenda materials in accordance with the chair’s request. By ensuring these are distributed in advance, committee members have an opportunity to call in and ask questions prior to the meeting, thereby reserving meeting time for discussion rather than fact finding.

Pay Philosophy and Compensation Plans

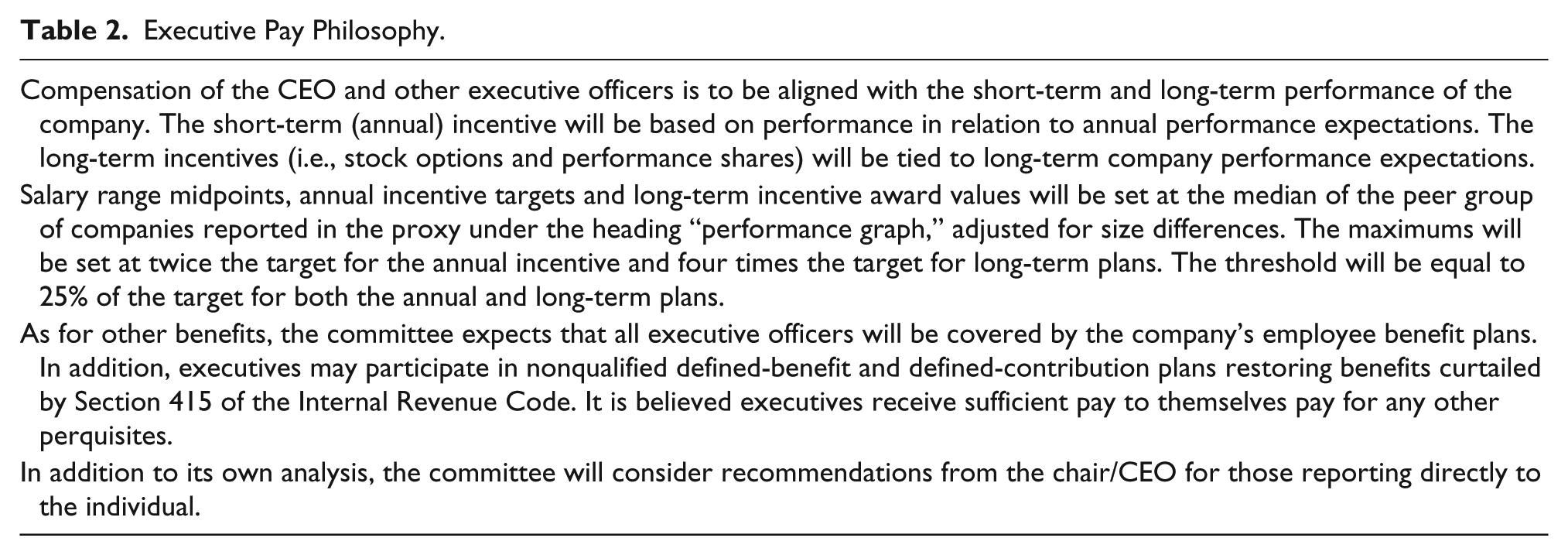

The second resolution in Table 1 states “that said committee shall submit to the board for approval the pay philosophy and compensation plans for elected corporate officers.” The committee needs to articulate the basis on which it will pay the executive officers of the company. An example is shown in Table 2.

Executive Pay Philosophy.

Pay for executives in general and the CEO in particular is often viewed in absolute dollars and not in relation to performance. However, a CEO paid a fraction of the pay of a counterpart may be overpaid in relation to performance. Conversely, a CEO paid several times that of a counterpart may be underpaid in relation to performance.

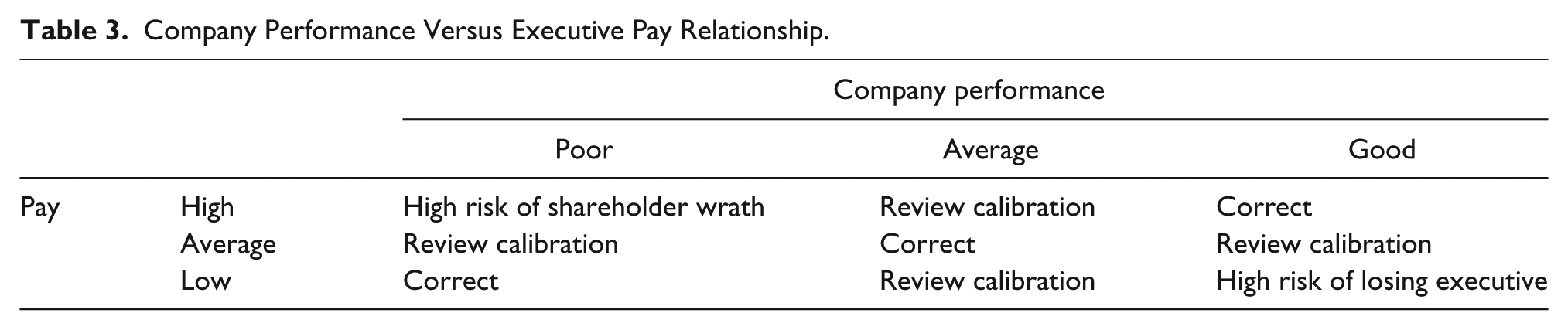

The relationship of pay to company performance is shown in Table 3. In this nine-cell matrix, there are three situations where pay and company performance are correctly aligned, four situations where the calibration needs to be reviewed and two that are definitely out of balance. High pay combined with low company performance will draw criticism from shareholders (and perhaps employees); low pay in relation to good performance suggests the company is at risk of losing the executive unless there are mitigating circumstances (e.g., the executive is a major shareholder and does not need additional pay).

Company Performance Versus Executive Pay Relationship.

Furthermore, it is important to view executive pay (especially for the CEO) in relation to others in their own peer group. Performance should not only simply be company financials but also total shareholder return, which is stock price plus reinvested dividends.

The committee’s task is not an easy one; it must balance financial expectations of management with degree of difficulty in goal attainment and cost to shareholders. In many instances, simply quantifying corporate strategy and goals in a manner that will allow structuring a short- or long-term incentive plan is a challenge in itself. Add to this the need to relate to pay levels of officers of other companies after adjusting for profit performance, and it is easy to see that the responsibility is more easily defined than accomplished.

A logical requirement is an annual report reflecting pay levels for a specified list of companies. This could be prepared either by an internal staff or by an outside consultant. Using this data, the committee could ascertain what level of adjustment is appropriate for the affected group. This in turn might be reviewed with an outside consultant for reasonableness.

Compensation Plans

Because of their fiduciary role in relation to the shareholder, it is logical to expect members of the compensation committee to be performance oriented in direction but cautious in specific plan design. A plan that is similar to those of other companies (especially in the same industry) is more likely to be acceptable than an innovative creation. However, the plan may not be right for this company.

In large part, this conservative approach is attributable to a lack of knowledge by which to adequately judge the efficacy of a new approach. It is much easier to rely on the judgments of other boards: “If they have it and apparently it is not causing problems, then it is probably right for us, too.” This is not to imply that compensation committees are unique in this respect. It is not uncommon for some executives to be more risk taking in their rhetoric than in their actions. The committee needs to be sure that the proposed plan is appropriate.

Probably the greater obstacle facing the committee is simply getting up to speed with the forms of compensation and their relationship to specific accounting, tax and company situations. Unfortunately, too few committee members are well schooled in executive pay programs before joining the committee; some can’t tell the difference between a stock option and a stock award. The task is difficult enough given the myriad pay-delivery forms, and it is unduly complicated by media messages promising 101 ways to reward executives effectively. Too often, these are shallow gimmicks rather than creative new techniques, and the committee members must see through these messages.

Thus, it is critical for the compensation committee to have sufficient knowledge of company objectives and compensation design to be able to judge the efficacy of a specific proposal. It is just as important to ask whether this is the optimum solution as to ask whether the proposed course of action itself needs some modification. In other words, before being certain that the specific plan has no inconsistencies or inaccuracies, be certain that a more desirable plan has not been overlooked or incorrectly discarded! This can only be accomplished by reviewing all the forms of executive pay design and deciding why each is inappropriate for this company. It is insufficient to test the efficacy of a proposal simply on the basis of whether or not it appears to reflect good staff work. In a number of situations, these committees are initiating their own studies and proposals instead of passively awaiting a proposal from management. Many suffer from a plethora of reports and recommendations to digest and from little staff support to ensure efficacious analysis.

On one hand, the pay package must be attractive and competitive. On the other, the committee must ensure that the compensation package is not considered by shareholders to be a waste of corporate assets. If the latter is the case, a lawsuit may very well follow. Just because several companies in desperate need of a particular CEO have offered multimillion-dollar bonuses is no rationale for increasing the pay of several vulnerable people by several hundred thousand dollars.

To meet its responsibilities, the committee should ensure that its pay-delivery system for top managers is consistent with expected short- and long-term results. This is the optimum. The minimum is to ascertain that pay is not inconsistent with company goals. Between these two is the “no man’s land” into which the majority of pay systems fall. Many a compensation committee has heard the plea to change the plan because “it isn’t paying anything.” This may be the best indication that it is a good plan. It may not be paying because performance is not adequate. However, few resist the temptation to change the goals or the plan in order to make an adequate payout. In these situations, performance becomes a secondary consideration.

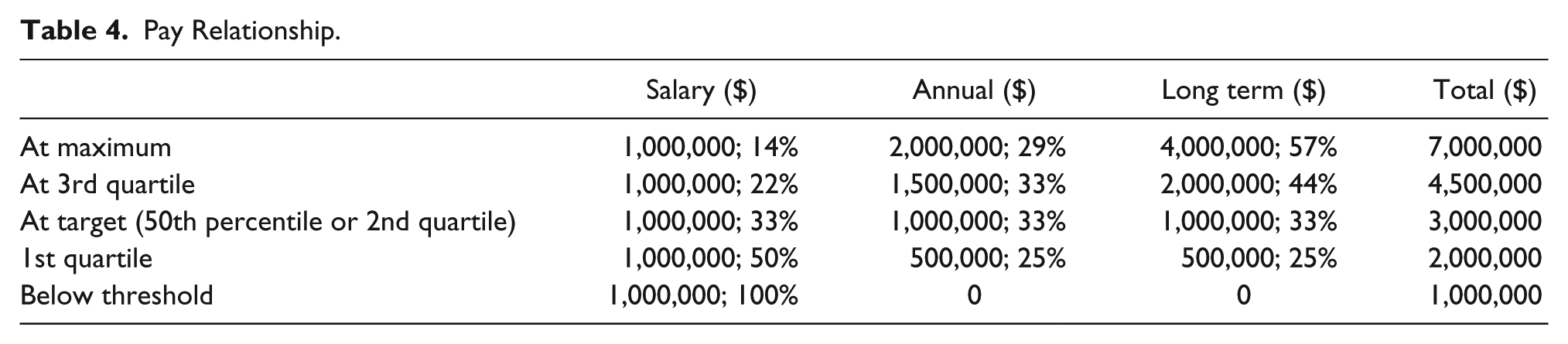

In designing annual and long-term incentive plans, one needs to determine not only the payout at target but also the prescribed minimum and maximum. It is also necessary to determine the relationship of each to salary and the percentage all three constitute of total compensation. Table 4 shows an example in which the three are expected to contribute equally at target, but at maximum, annual and long term are two and four times salary, respectively, placing significantly more emphasis on long term. Where they both double salary, the percentages would be salary 20%, annual incentive 40% and long-term incentive 40%. Note what happens below threshold.

Pay Relationship.

The advantages and disadvantages of each specific plan must be reviewed in terms of anticipated performance and level of payment over the prescribed time period. Only by simulating results and examining payment will it be possible for the compensation committee to judge the efficacy of the proposals. It would also be logical to have the consultant attend every annual shareholder meeting, not just when a plan change is proposed—both to provide expert answers to shareholder questions and to get first-hand impressions of shareholder pay concerns.

With the selected plan or combination of plans in hand and the defined level of pay for officers under specific conditions of company performance decided, it is necessary for the plans to be formally drafted by counsel and submitted to the full board for approval. In almost every case, the plan would also be submitted to shareholders after board approval, although awards instead could be made contingent on shareholder acceptance. A company may choose one form over another simply because of the low profile it may get in the proxy statement. For many years, stock options were much less visible than stock awards in isolating individual gains. Now, present-value calculations and exercise gains receive significant attention.

The compensation committee would also determine how much should be paid from the sum of previous carryforwards and current-year performance. It would also typically authorize the amount to be carried forward to the next year. This could simply be the total available less this year’s awards; however, apart from a reserve to cover warranted bonuses in consecutive lean years, it would be reduced.

Implementing the Plan

In Table 1, a resolution stated “that said committee shall be responsible for implementing plans approved by the board (and in some cases the shareholders).”

Administration of the actual pay program will focus on all five components of the officers’ pay package, including their relative mix. It is therefore assumed the committee will be responsible not only for approving any recommendations on salary increases but also the units of participation under both the short- and long-term incentive plans. This committee would also determine modifications to basic employee benefit plans (e.g., allowing an unfunded plan to restore benefits curtailed by the maximums of the Employee Retirement Income Security Act) and eligibility for specific perquisites.

The committee must determine the following for each of the compensation elements: the required action, the basis on which a decision is to be made and the responsibility for proposing and approving various actions. These might be handled by a company with two compensation committees: an executive compensation committee for elected corporate officers consisting solely of nonemployee directors and an employee compensation committee consisting of the CEO, COO and vice president of human resources for all others.

CEO Performance

The fourth resolution in Table 1 stated that “performance goals for the CEO approved by the board be the basis for a performance evaluation and appropriate pay action.” Evaluating CEO performance is a two-step process. First, identify the performance expectations; second, tie them to annual and long-term incentive plans payouts. (Expectations such as succession plans, access to management and positive board relationships might also be added.)

With the first step, the board of directors is responsible for assigning specific goals for the CEO and, working with the compensation committee, for measuring the degree of successful attainment, leading to pay actions.

The expected performance of the CEO will begin with, and be defined by, the business plan. What is the company’s vision? What is its mission? What are the objectives and goals that will enable fulfillment of the vision? What are the threats and opportunities facing the organization? What are the major strategies the company needs to undertake to address the resulting issues?

Directors will evaluate the plan, helping the CEO consider strategies from different perspectives. Once the board approves a plan, it will expect periodic progress reports from the CEO.

The second step is to evaluate performance in terms of the expectations laid out in the business plan. Pay actions will be based on these assessments. CEOs must know objectives to be evaluated, and the board must ensure consistency of evaluations with approved plans. The board should also articulate how it expects these objectives to be accomplished. Accomplishments should embody honest and ethical behavior. Furthermore, the CEO must convince those in the company (and on the board) of his or her full commitment to achieving the vision.

Competitive Data

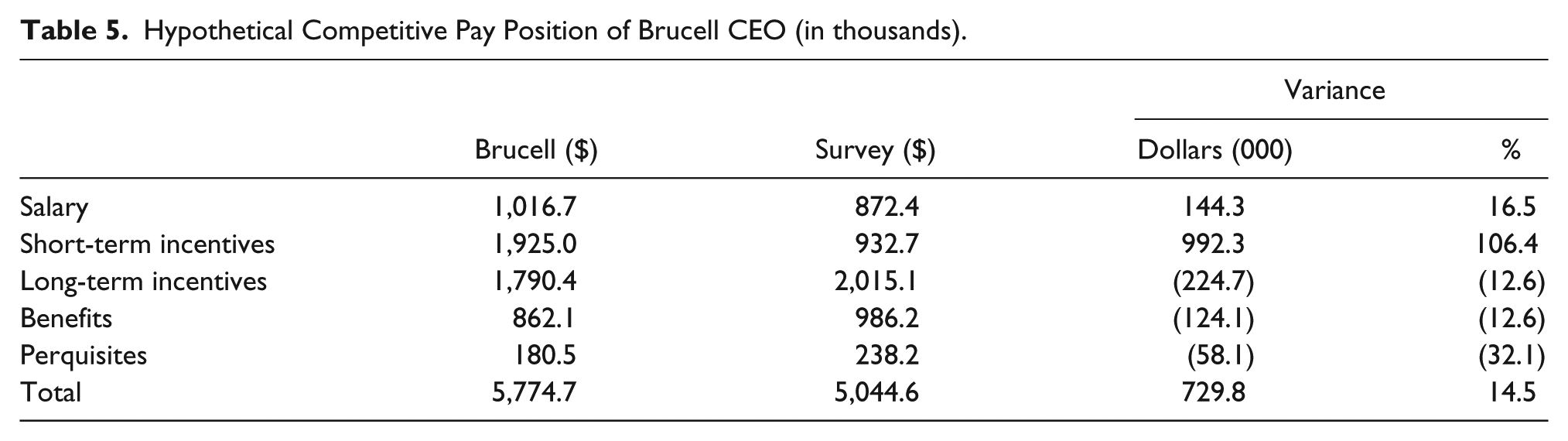

In Table 1, the board stated that “said committee will review competitive pay practice and peer company performance in approving components of the compensation program as well as specific pay actions for certain executives.” Therefore, it would be appropriate for the compensation committee to request an analysis of competitive position of pay for at least the CEO and four other executives named in the proxy. Table 5 shows how this summary might look for the chair/CEO.

Hypothetical Competitive Pay Position of Brucell CEO (in thousands).

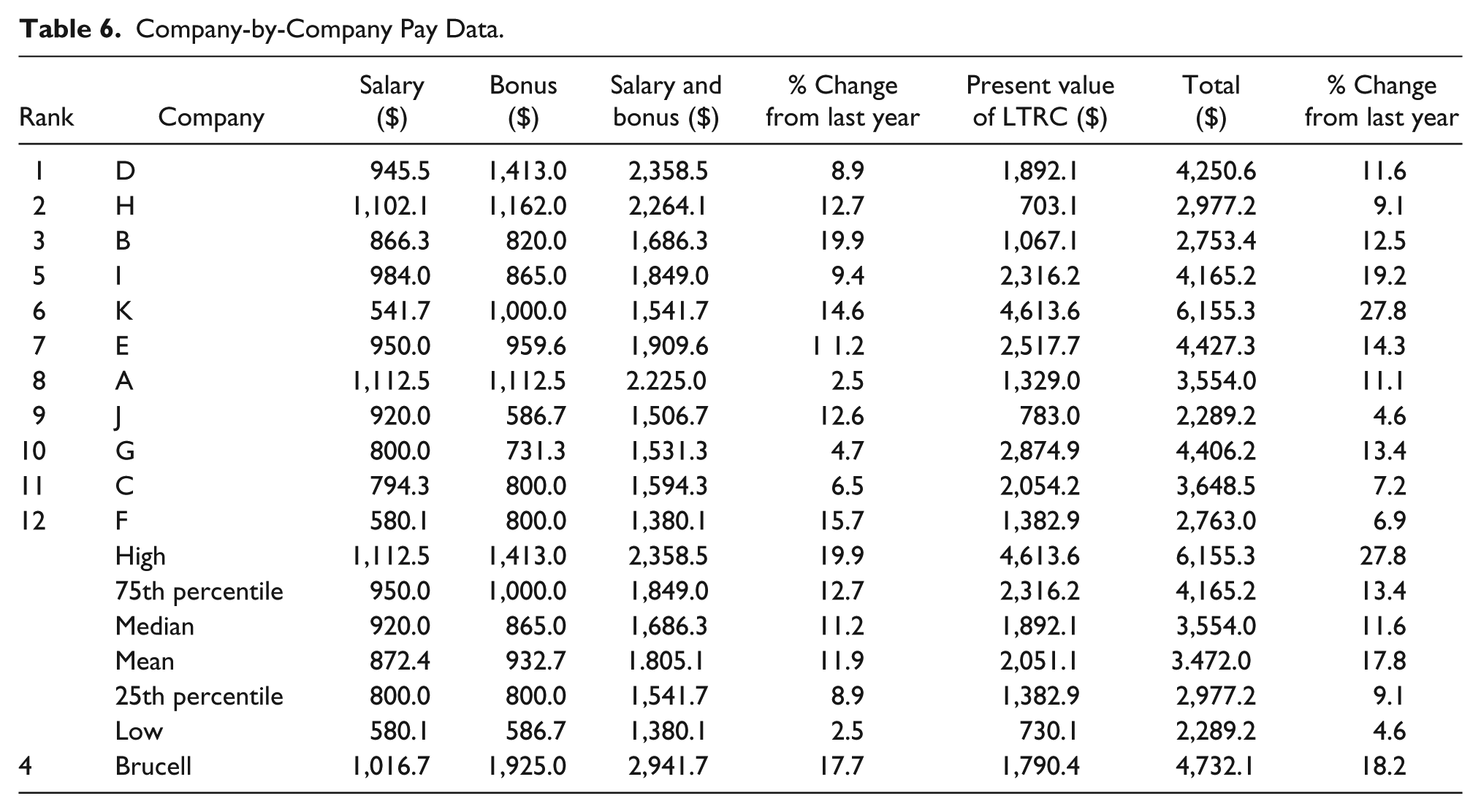

Although each of these two analyses suggests Brucell’s CEO is overpaid, such a conclusion should be withheld until Brucell’s financial and shareholder return performance has been compared with the survey group. This information is shown in Table 6.

Company-by-Company Pay Data.

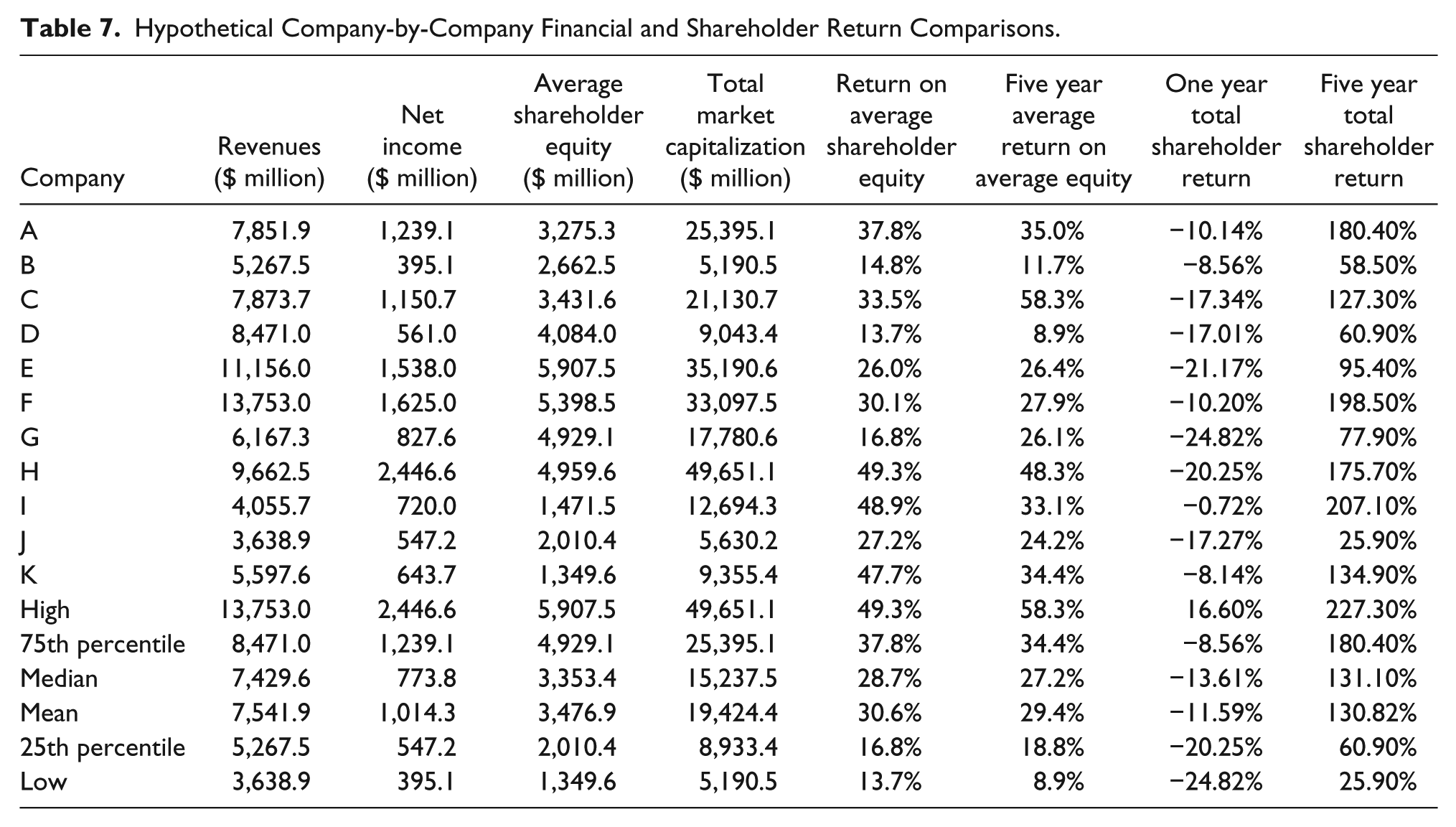

Table 7 shows a company-by-company breakdown of the same chair/CEO data for salary and incentives, ranked by salary plus annual incentives. Comparisons of Tables 6 and 7 can be done in a myriad number of ways, ranging from simple averages to complex multiple correlations. The methodology should be no more complicated than justified by the data or of interest to the committee.

Hypothetical Company-by-Company Financial and Shareholder Return Comparisons.

Typically, the committee makes performance decisions on the CEO and other executives named in the proxy (and perhaps other selected executives). This would occur after reviewing the actions for individuals in the next lower organizational level, perhaps decided by a separate committee, for informational purposes. When determining the form in which to distribute the award, the executive’s stated preference should be considered. However, it is also important to examine company needs. If the company is in a cash bind, it should lean toward distribution in the form of company stock; if there is a concern about equity dilution, then distribution should be in cash. If both are true, a combination award (perhaps with deferred payment) should be made to lessen the impact on dilution and cash flow.

After making the awards, the committee is responsible for monitoring plan performance and acting on salary recommendations for officers. Some committees want not only to be responsible for the pay of corporate officers but also to be fully appraised of succession plans. Thus, the committee has a basis for judging the depth of management talent or lack thereof. It is also helpful in understanding differences in recommended pay increases (one person may be on the inside track and the other an outside shot, at best). Some request that management succession plans be in writing and reviewed at least annually.

Review of Job Grades

The compensation committee should assign job grades for the CEO and other corporate officers. In assigning grades, proposals with supporting documentation are brought forth by management for committee action. Decisions would be based on a combination of external parity and internal equity.

As part of this decision process, the committee must determine not simply the total annual compensation structure but also what portion will be salary and what portion short-term incentive. What relationship will each of the three have to the marketplace and at what percentile ranking?

Approving Payouts

Management would submit for approval a schedule of payouts, including calculations of performance factors in accordance with the plan. The audit committee should be asked to attest to the accuracy, enabling the committee to accept the validity of the information. The committee would then discuss and approve the payouts. Payment would be reported to the board. Depending on board policy, the report may simply be accepted or the matter should be reviewed and discussed. In any event, action must be in accordance with Section 162(m) of the IRC if the company wishes to get a tax deduction for payments in excess of $1 million for the proxy-named executives. This means the board cannot overturn the committee’s actions, although it should be informed of the committee’s decisions.

Contractual Agreements

In Table 1, the board stated that “said committee will review and approve contractual agreements for those in the executive compensation program.”

There are two types of executive contracts: employment and termination. The two may be combined, the first describes the services to be provided by the executive and the compensation for the defined period of service. The second describes the payments to be received on termination and the responsibilities of the executive (e.g., noncompete and nonsolicitation agreements). Termination conditions include the following: for cause (e.g., willful misconduct, conviction for a crime and/or breaching the terms of the employment contract), change of control (namely, an acquisition or merger), poor performance (but not for cause) and retirement.

Employment contracts typically include the following: title, reporting relationship, duties, terms of contract, salary, employee benefits, perquisites, short-term incentive plan, long-term incentive plan and termination pay. Termination payments depend on the type of termination of service. Termination for cause typically provides no payments. A change of control contract provides payments that typically are several years of pay. Termination for poor performance is a function of position and years of service.

Since the company wants to get something if the individual quits, noncompete, nonsolicitation and, if possible, nondisclosure language is included. It should be remembered that the contract is more for the protection of the individual than the company.

It has been said that employment contracts, especially the severance portion, are similar to prenuptial agreements (and about as pleasant to address). Nonetheless, the time to examine the document is before (not after) signing.

It is important for the committee to review carefully the terms, conditions and payouts of the employment agreement and the various types of terminations before they are approved. Severance pay is viewed as pay-for-failure and is subject to close scrutiny by the stakeholders. When the amount is viewed as egregious, the compensation committee and board of directors are opened to criticism for not being more diligent in their responsibilities. Inasmuch as these are legal documents, they should be reviewed by corporate counsel, as well as the committee’s compensation consultant.

It is also important that the contract be clear on claw backs. If the company restates its financial statements, executive pay should be recalculated on the basis of the revised numbers and excess payments returned to the company. The Sarbanes-Oxley Act requires this for CEOs and CFOs if there was inappropriate action. Good corporate governance would apply the rule to all restatements.

The committee should, wherever possible, ensure the company reserves the right to modify or terminate a plan. The committee may also want to ensure that a contract will continue unless either party exercises the right to cancel the contract, typically within 90 days of an anniversary date.

Consultants

Consistent with the seventh resolution in Table 1, “said committee may engage services of others to assist them in the performance of their duties,” committees look to outside (external) consultants to assist them. This is not a slap at the competency of the inside executive pay planners but a reference to fiduciary trust. It seems a little less than an arm’s-length transaction to have the inside executive pay planner (who is in the reporting chain to the CEO) advise the compensation committee on the appropriate form and level of pay of the CEO. It would be unlikely that many CEOs would advance a negative report. One possibility is to have the pay planner report directly to the committee, although the career possibilities of such an individual would be questionable. Even if that were done, it is important for the compensation committee to have access to an experienced executive compensation consultant with no ties to the organization or its management. Reasons include the following:

Belief that with a wave of the person’s wand, the laborious design process will be circumvented by the materialization of a simple, easy-to-understand and easy-to-operate plan that will be perceived as equitable by all parties concerned. Committees with this approach probably still believe in the tooth fairy.

Limited time frame and/or lack of executive compensation plan design expertise within the company could necessitate going to a consultant who can provide the know-how and sufficient resources to accomplish the job quickly.

Employing a consultant prepared to support the position of the committee gives validity to the program challenged by a shareholder.

Engaging an individual and/or firm well recognized for preeminence in the area of executive compensation design is an overt signal to the outside world that this committee is “doing right”—excellence by inference. With “so-and-so” as the consultant, one must conclude the company has an effective pay-delivery system.

This raises the question: Who should engage the consultant? Should it be management, the committee or both?

Historically, the consultant has been engaged by management to support the validity of its request. Needless to say, this puts enormous pressure on the consultant to agree with management.

The practice is to have the compensation committee take charge of the process, requiring the consultant to work with management but report to the committee (who will pay the fees and if necessary replace the consultant). Suggestions that management also have a consultant are not practical. This simply sets up a dueling match between the two consultants. The committee must remember its fiduciary responsibility.

Which Consultant?

Rather than immediately sign up a consultant, it would seem appropriate to do a little market research. Some consulting firms have broad-gauge management views: “We can tackle anything.” Others are more specialized in nature, ranging from total compensation planning to only executive pay design. Each has its advantages and disadvantages. A top-notch pay planner from a more specialized firm will be more likely to custom-tailor a plan. However, the individual may not have sufficient broad-gauge management background to have accurately assessed corporate needs.

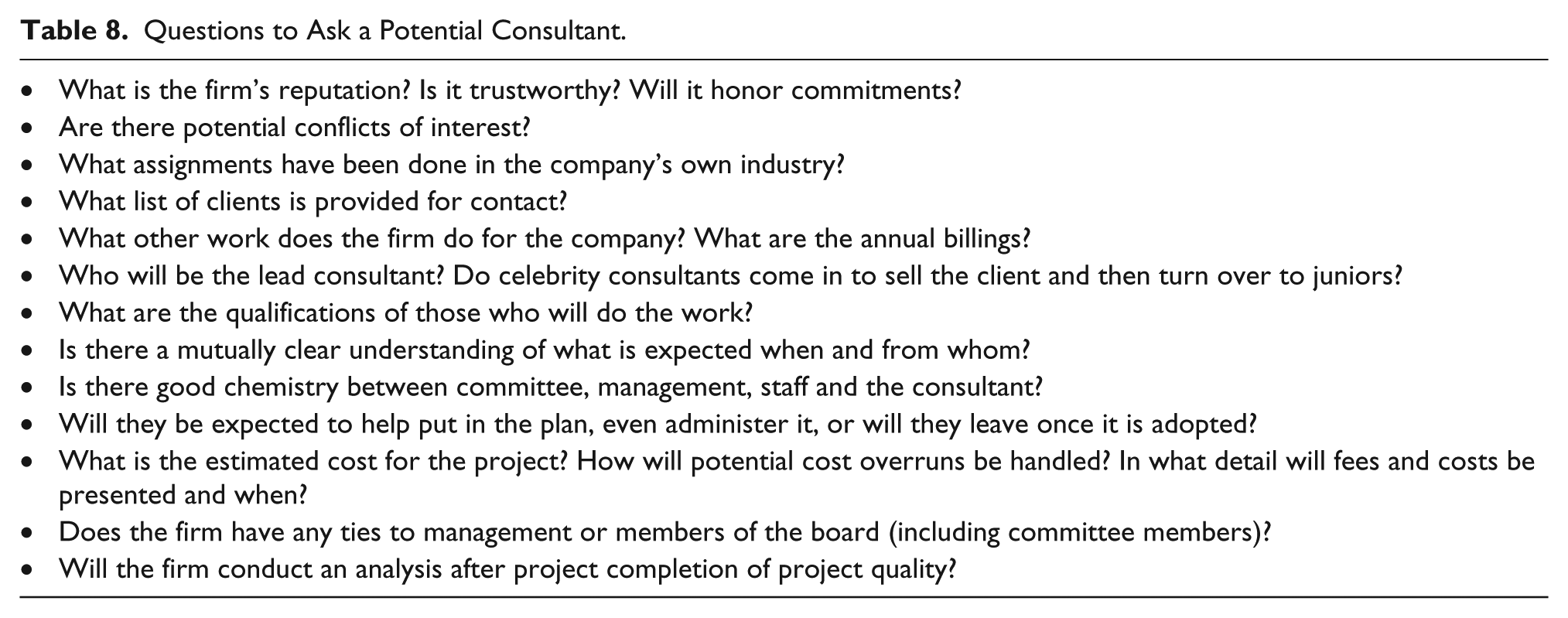

Few committees seem to approach the problem objectively. Rather than identify one firm, several should be identified and asked for a request for proposal. Each candidate should be provided sufficient data to allow an accurate assessment—what, when and how much. Does the firm have the necessary expertise? Ask for references. A partial list of questions to ask is shown in Table 8.

Questions to Ask a Potential Consultant.

Each proposal should be analyzed to determine if the problem has been accurately defined as well as whether the approach suggested is feasible. A cost–benefit analysis of the proposal should be prepared, including items such as consultant charges, company time, disruption and program cost.

In looking at consultants, one should also attempt to identify the loud proponents of a specific form of plan. If Ms. X is recognized as a performance-share advocate, the company should be more interested in how she will justify that type of plan within the company than be surprised that she recommends such a program. She has a solution in search of a problem. Unfortunately, unless the problem meets the definition, the misapplied solution subsequently becomes part of the problem.

Consultant Alternatives

It would be logical to engage an executive compensation specialist as a consultant to the compensation committee. The chosen specialist should be neither an employee nor engaged in consulting assignments with the company, thus avoiding potential conflict-of-interest situations. The individual could be employed to review the quality of recommendations and/or to develop specific recommendations based on committee objectives.

An extension of this would be to appoint the consultant as a permanent member of the committee, with the written agreement that the person will not work for management. As indicated earlier, an executive compensation expert in the employ of another company outside the industry might also be a candidate for membership in the compensation committee. Even combining these two sources, there are many more opportunities than there are knowledgeable individuals.

On the other hand, some companies look to the auditing firm to comment on the appropriateness of the design of a pay package and its level of payment. This is a logical extension of what they may later have to comment on anyway; the reasonableness issue is one that will have to be addressed with the Internal Revenue Service if not with shareholders. The auditing firm has an advantage over another consulting firm in that it already knows the company rather well. However, since audit fees approved by management far exceed consultant fees, the latter recommendation may lack objectivity.

Even if management consultants are employed, it is critical that a large company have an internal executive compensation expert. The individual should be sufficiently versed in all forms of executive pay to provide another dimension to material advanced by the external consultant. As indicated earlier, having this person report directly to the committee rather than to management would certainly improve the face validity of the individual’s recommendations.

Shareholder Matters

A Table 1 resolution stated “that said committee is to prepare a report to shareholders in accord with the Securities and Exchange Commission rules.” This is consistent with a 1992 SEC requirement that a report from the compensation committee must be included in the shareholder proxy. This was to be considered a “furnished,” not a “filed,” document. Among the requirements was to note whether the compensation of the named executive officers was in compliance with Section 162(m) of the Internal Revenue Code. The report was also to indicate the pay philosophy in general and how the CEO pay was determined in particular. The SEC warned committees not to use boilerplate language but rather to personalize and customize the report of the company in question. The members of the compensation committee were to be named at the end of the report. In 2006, the SEC reaffirmed the requirement for such a report, again stating it is considered a “furnished” rather than a “filed” document.

It also introduced the Compensation Discussion and Analysis report (CD&A), similar to the Management Discussion and Analysis found in the company’s 10-K. The CD&A is a filed report and is to be certified by the principal executive officer and the principal financial officer.

The CD&A is to provide investors with a view of the company’s executive compensation program and the reasons behind the numbers in the various compensation tables found in the proxy. It is expected to answer the following questions in plain English:

What are the objectives of the company’s compensation programs and what is it designed to reward?

What is each element of compensation?

Why does the company choose to pay each element?

How does the company determine the amount (and where applicable the formula) for each element?

How does each element and the company’s decisions regarding that elements fit into the company’s overall compensation objectives and affect decisions regarding the other elements?

Have shareholder say-on-pay votes been included in the program, and if not, why not?

What actions if any were taken after the close of the last fiscal year that would affect the above?

A material adverse effect on the company because of accepted risk is also to be included in the proxy report.

This is too important a document to be left to the lawyers and the consultants; the committee must be actively involved to take ownership. One is cautioned to develop such a report carefully. It should be specific to the company and be more detailed than shown in Table 6. It is important that the reader look to the SEC documents for accurate, complete and detailed descriptions and requirements. Submitting the compensation committee report to shareholders for a nonbinding vote would demonstrate that the committee believes it has acted properly but is interested in shareholder reactions.

Other SEC required pay-related material to be included in the proxy includes a summary compensation table, grants of plan-based awards, outstanding equity awards at fiscal year-end, stock option exercises and stock option awards vested, pension benefits, nonqualified deferred compensation and potential payments upon termination or changein-control. Each of these would be reviewed by the committee and the board before including in the proxy.

Shareholder Questions

The Table 1 resolutions include responsibility for the committee to “respond to shareholder questions.” Although questions from shareholders could come at any time during the year (especially after something has been reported in the press), they are most likely to occur at the company shareholder meeting.

Many companies attempt to identify likely questions prior to the meeting and then research the appropriate response. Regardless of how much time is spent on this process, invariably there will be unexpected questions. Nonetheless, the process is still worthwhile because it stimulates thinking.

A starting point is the proxy statement.

Have there been any significant changes in the compensation and incentive tables from the previous year?

Is there anything in the compensation committee report that is likely to raise questions? Is there any descriptive changes regarding pay elsewhere in the proxy?

Examples that could be drawn from this review might include the following:

Is the CEO on the compensation committee of any member of the company’s compensation committee?

What were the performance objectives for the CEO, along with their weighting and rating?

What was the increase in the CEO’s total pay for the last year versus the increase in shareholder value?

What perquisites did the top five receive and what was the cost for each?

Are the companies used for pay comparisons the same as in the proxy stock chart? If not, why not?

Some of this material could also be covered in preparation for the annual shareholder meeting.

Committee Meeting and Board Requests

In our Table 1 example, the board stated that “the committee is to file a copy of its meeting minutes with the board and respond to questions and requests from the board.”

Committee Meetings

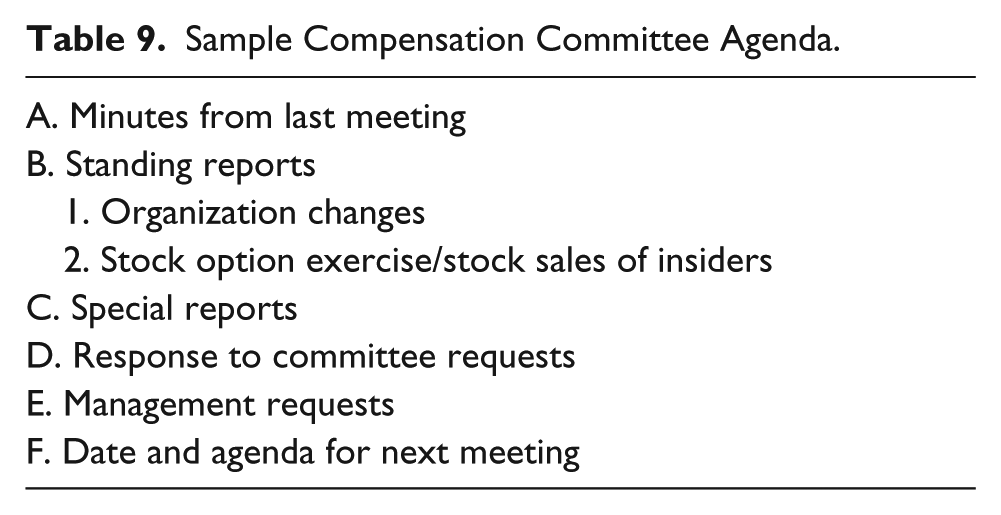

While meetings could be scheduled for any time during the year, it is common practice to schedule meetings to immediately precede board meetings. This not only minimizes scheduling problems but also ensures timely reporting to the board of committee actions. For many, the meeting would be scheduled for the morning the board is to meet. However, committee members arriving the night before might use the opportunity to informally discuss the meeting agenda over dinner. Table 9 shows a sample agenda.

Sample Compensation Committee Agenda.

Meeting Agenda

Before preparing a monthly meeting agenda (Table 9), the chair should establish a key event timetable similar to the one in Table 2 for the year. In this example, salary actions are effected on a common date (April 1) rather than distributed throughout the year; short-term and long-term incentive rewards are also reviewed in March. However, benefit and perquisite actions are effected the first of the year. As the year progresses, this timetable is adjusted to reflect the addition of other committee or management requests.

When meeting to take action on compensation programs, it is important for the compensation committee to ascertain not only the annual cost to the company for that program but also the flow-through costs (e.g., an increase in salary will have an impact on the person’s pension). It is critical that potential actions be reflected in the tables that will be reported in the proxy for the year. The purpose of looking to these tables, and especially prior-year data, is to take action that will be appropriate, thus avoiding embarrassing shareholder questions. It would also be appropriate to prepare a summary compensation table as the one required in the proxy with the same format but reporting W-2 data for the year reported. Because actual pay data, rather than estimated FAS 123R values, is sometimes reported in the business press, the compensation committee and the board of directors need to know this information in order to be able to explain the differences.

Because many of the proxy-required compensation tables are expected to have footnotes explaining the items in the columns, it would make sense that the compensation committee have spreadsheets prepared detailing the items. For example, a spreadsheet for perquisites might have columns for the following: personal use of aircraft, personal use of automobile, personal use of company apartment, executive medical costs and any other personal-use items. Not only does it make it easier to prepare the summary compensation table and the footnotes, but if done early enough, it also provides the committee the opportunity to decide whether or not it wishes to provide these items at company expense. Similar spreadsheets are appropriate for payments due to the named executive at the time of leaving by type of termination (e.g., change of control performance termination, pension and other types of departures). The use of spreadsheets (also known as tally sheets) is considered a “best practice” by shareholder proxy service organizations and the Delaware Supreme Court.

Meeting Sessions

Committee members should be able to rely on information presented. Namely, the information should be complete and not misleading or biased. Therefore, it is important that the credentials of the presenter be reviewed and any relationships with the management revealed. Sufficient time must be permitted to thoroughly review the material. It may be appropriate to schedule two meetings—one for discussion and the next for voting.

In discharging its responsibilities, the compensation committee should always require that materials be received in sufficient time for committee members to review prior to the meeting. This should include the ability to call in their questions. Time at the meeting is best used for discussion rather than information gathering. The committee should refuse to consider proposals received without adequate lead time (except in rare emergency situations). The committee should indicate format requirements for management to minimize confusion and delays. The committee should also hold management responsible not only for raising issues but also for offering possible solutions (with costs and rationale). However, the committee should not be expected to research and resolve all issues raised by management.

At the meeting, directors should discuss issues fully and should, where appropriate, introduce and consider advice from specialists in reaching a decision. Decisions should be the result of the careful examination of sufficient information rather than the result of limited time.

The chair may wish to begin and end each meeting in executive session with only members of the committee present. This allows them to express any comments or concerns. When not in executive session, in addition to the committee secretary, it is common to extend an invitation to the board chairman and CEO.

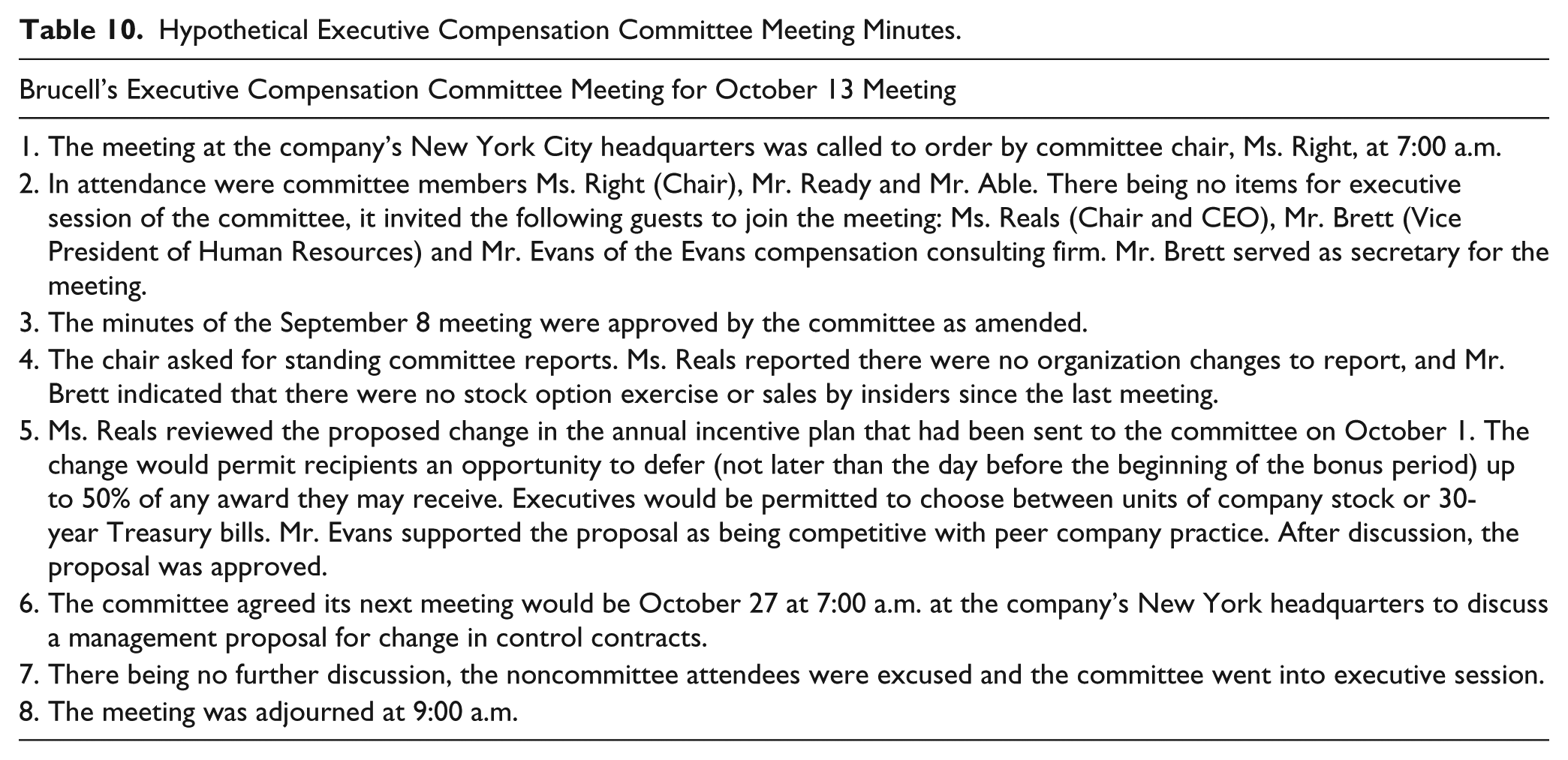

Meeting Minutes

The secretary of the committee will be asked to take minutes of the meeting and file a copy with the board of directors. Minutes should accurately reflect discussions and agreements consistent with good corporate governance. An example is shown in Table 10.

Hypothetical Executive Compensation Committee Meeting Minutes.

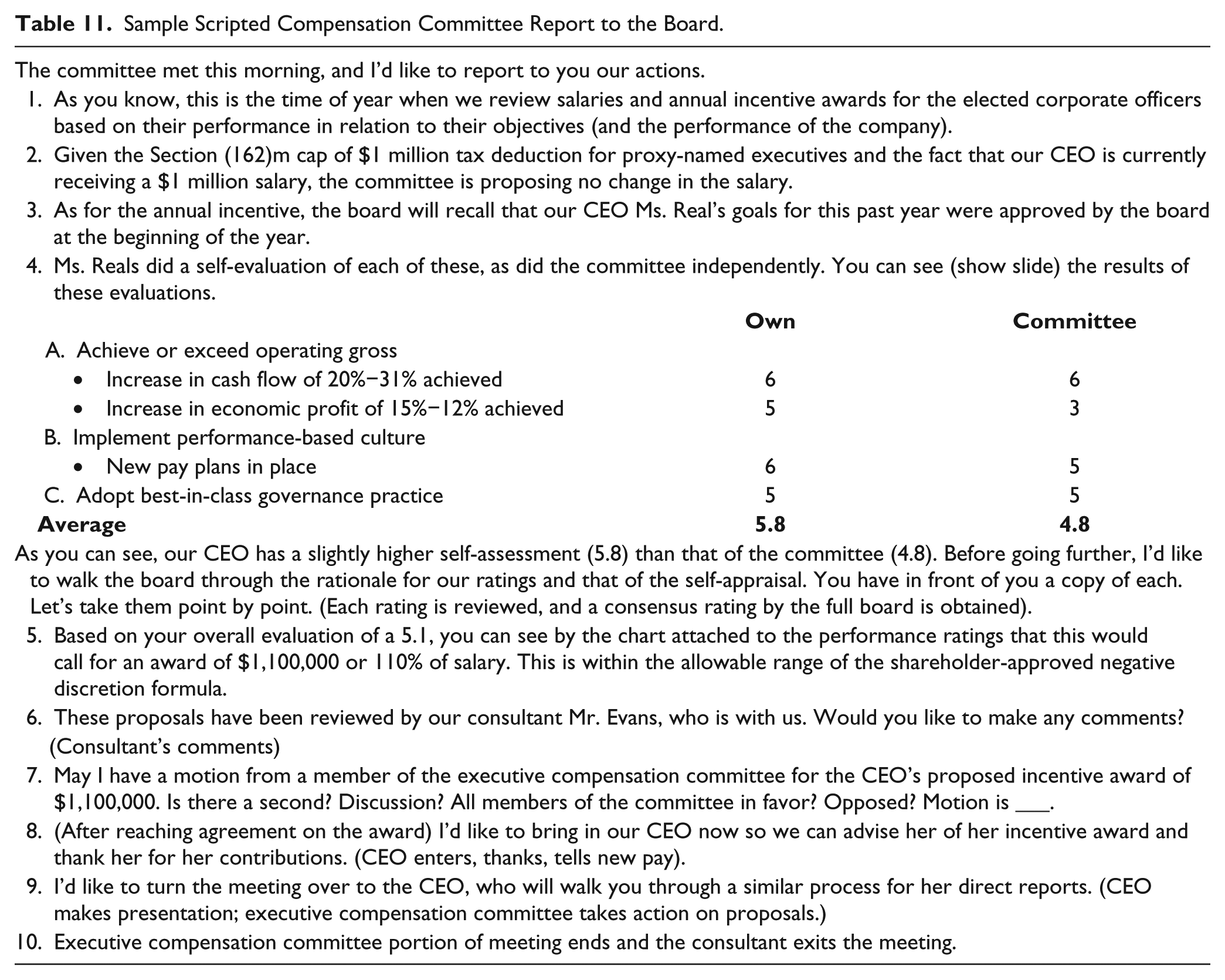

Report to the Board

The committee secretary may be asked to script a presentation by the committee chair to the board of directors reporting on the committee meeting. This request is most likely to come from a new chair and/or one not well versed in executive compensation. Table 11 shows an example.

Sample Scripted Compensation Committee Report to the Board.

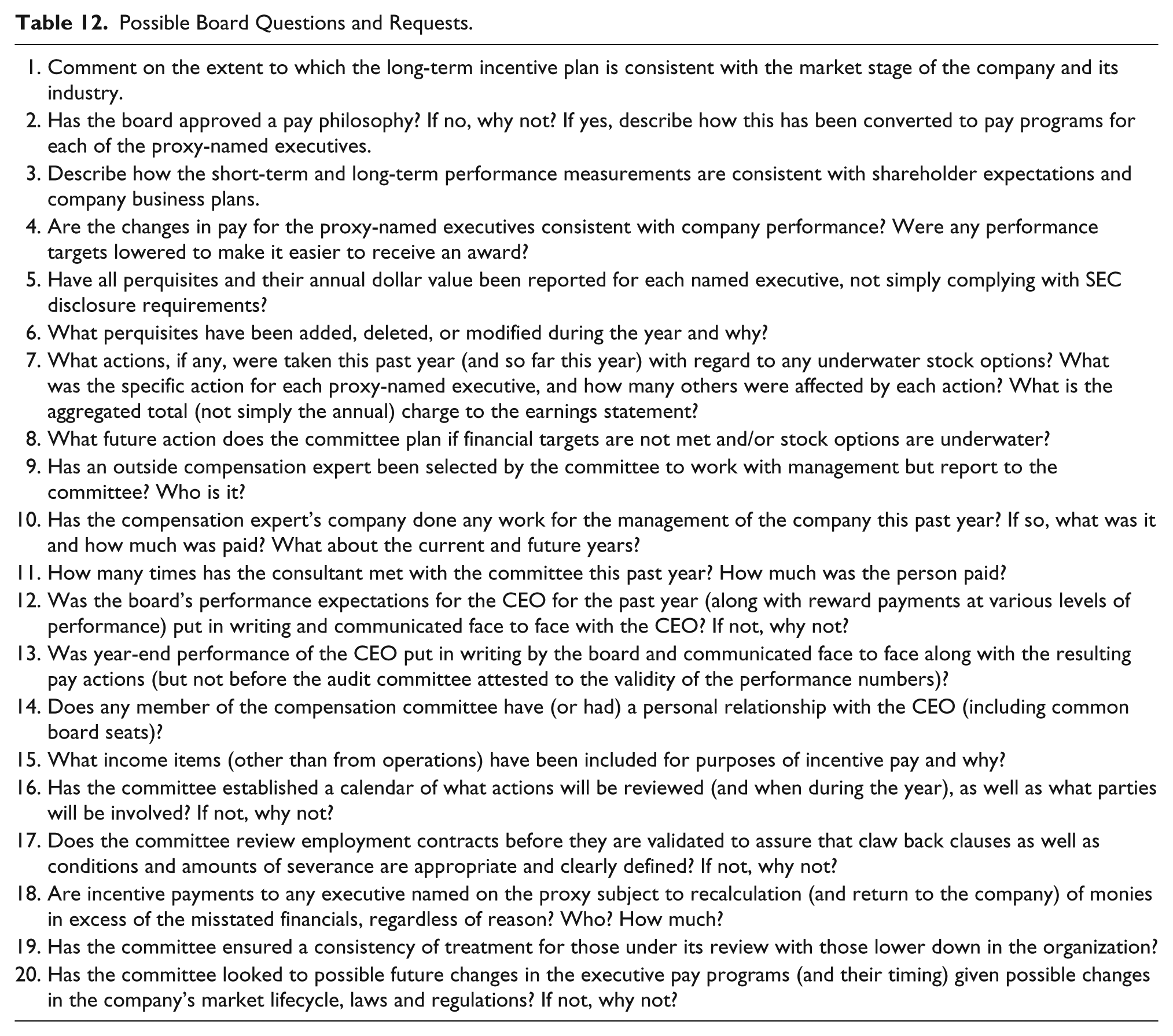

Board Questions and Requests

Typically, the questions and requests would be as a follow-up to the earlier-mentioned committee responsibilities. Table 11 provides examples of the type of questions and requests that the board might pose. The committee can minimize the follow-ups by anticipating what might be asked and including the information in the data provided. The list in Table 12, although representative, is far from complete.

Possible Board Questions and Requests.

Summary

The compensation committee of the board of directors is a very important committee, and in recent years because of shareholder concerns about executive pay and SEC requirements on disclosure, it has become even more important and time consuming.

For those reasons, it is very important that persons added to the committee be knowledge of executive compensation. Lacking sufficient knowledge, the board should set up orientation programs using internal and external assistance. The committee responsibility is too important to lack sufficient knowledge.

Committee members are to be reminded of their responsibility for duty of loyalty (putting shareholder interests above own or other interests), duty of care (understanding the issues and the alternatives), exercising prudent judgment (avoiding conflict of interest) and acting in good faith. These are important factors to meet the business judgment rule ensuring they cannot be held liable for poor decisions or mistakes.

Informed committee members acting in compliance with the business judgment rule should result in actions in accord with shareholder expectations and SEC requirements.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.