Abstract

This study examines whether individual auditors with experience as independent directors provide better audit performance than those without independent directorship experience. Using the Chinese setting where audit partners’ names are publicly disclosed, we find that audit partners with independent director experience provide higher audit quality for clients that operate in the same industries as the companies where they concurrently hold or have previously held directorships. However, directorship experience at companies in different industries has an insignificant effect on audit quality. These findings suggest that independent director service enables audit partners to gain industry-specific knowledge. This leads to knowledge spillovers on the audits of clients in the same industries. This study contributes to the literature by identifying an alternative channel through which auditors gain industry-specific knowledge which enhances their performance.

Keywords

Introduction

In recent years, a growing literature explores how financial statement quality is affected by individual auditor characteristics. Auditors may acquire expertise through practice and experience (Bonner & Walker, 1994; Chen et al., 2017; Chi et al., 2017), industry specialization (Bratten et al., 2020; Chi & Chin, 2011; Chin & Chi, 2009), or by relying on information transfer through individual auditors’ social networks (Bianchi, 2018; He et al., 2016; Lim et al., 2018; Pittman et al., 2018). This study considers whether serving as an independent director in another firm improves the auditor’s performance. We also examine whether directorship experience within the same industry leads to more pronounced effects as compared with directorships in a different industry.

We examine this issue in the Chinese setting where audit partners’ names are publicly disclosed. 1 The China Securities Regulatory Commission (CSRC) has required each listed company to have at least one financial expert serving as an independent director since 2001 (China Securities Regulatory Commission, 2001). Financial experts are defined as parties with “experience as a public accountant, auditor, principal financial officer, controller, or principal accounting officer” (Securities and Exchange Commission, 2003). Therefore, many Chinese listed firms invite auditors to sit on their boards.

Independent directors need to acquire industry-specific information to serve as effective monitors and advisors (Linck et al., 2008). Auditors who have served as independent directors acquire expertise that allows them to make better professional judgments. In other words, directorship experience is likely to create a knowledge spillover effect and enhance auditors’ performance.

Using a sample of Chinese listed companies from 2001 through 2018, we find that financial reports audited by partners with directorship experience (hereafter “independent director audit partners” or IDAPs) within the same industry as the client exhibit lower discretionary accruals, but this finding does not extend to clients in different industries. These findings suggest a spillover of industry knowledge. The findings are robust with regard to the choice of other proxies related to the information value of financial statements. Additional analyses indicate that the positive effect of directorship experience on audit quality is attenuated by audit partners’ client-specific or industry-specific experience, suggesting that directorship experience may play a more important role for partners who are less familiar with a client or an industry. Moreover, investors perceive higher audit quality for firms audited by IDAPs, regardless of the industries where IDAPs hold directorship. Finally, supporting the idea that industry-specific directorship experience matters, we find that IDAPs with directorship experience in the same industry are more likely than other partners to induce client recognition of goodwill impairment.

This study is motivated by the increased public and academic attention paid to auditor characteristics at the partner level (DeFond & Zhang, 2014). Despite extensive prior research on auditor independence (Blouin et al., 2007; Chen et al., 2010; Chi et al., 2012; Guan et al., 2016), the effect of individual auditor characteristics is understudied. Our study adds to the literature by documenting an alternative channel through which individual auditors can accumulate industry-specific knowledge and hence provide better financial reports. Moreover, our findings suggest that industry knowledge gained from directorship experience can be useful for understanding fair value estimates—an audit area where the Public Company Accounting Oversight Board (PCAOB) frequently discovers audit deficiencies (Ahn et al., 2020).

Prior studies investigate whether financial experts improve financial reporting quality of the companies where they serve as independent directors (Abbott et al., 2004; Farber, 2005). To the best of our knowledge, this study is the first to address the positive externalities or contagious effects arising from serving as an independent director. That is, directorship experience can be beneficial to other firms where the financial expert provides professional services.

The remainder of this article is organized as follows. The next section describes institutional background related to independent directors in China. The third section reviews relevant literature and develops the hypotheses. The fourth section discusses the research design, followed by the sample selection and univariate analysis in the fifth section. The sixth section reports the empirical results, and the last section concludes.

Institutional Background

Although the Chinese stock exchanges have developed rapidly since their establishment in the early 1990s, the CSRC did not require listed companies to have independent directors until 2001. Since 2001, the CSRC’s guidelines require that at least one third of board members be independent, and at least one independent director must have financial expertise in a listed company. Each independent director must not hold more than five directorships or hold a directorship in a company for more than six consecutive years. Since 2001, an increasing number of auditors have been appointed as independent directors, providing that the companies where they hold directorships are not economically related to their audit clients.

The Chinese Independent Auditing Standards mandate the disclosure of audit partner names, and each audit report must be signed by two audit partners (Ministry of Finance, 1995). In addition, Chinese listed companies disclose the profiles of executives and board members in their annual reports. Therefore, China provides an ideal setting for us to identify audit partners who have experience as independent directors.

Literature Review and Hypothesis Development

Importance of Industry Knowledge for Auditors

The quality of an audit involves many different components, and it may be impossible to combine them into a single measure (Sarath, 2016). One of the components of audit quality emphasized by the IAASB is “industry knowledge, including an understanding of relevant regulations and accounting issues”; so audit firms should provide sufficient training to “audit partners and staff on audit, accounting, and, where appropriate, specialized industry issues” (International Auditing and Assurance Standards Board [IAASB], 2014). As monitors or advisers, independent directors need to acquire firm-specific information (Linck et al., 2008). In the context of IDAPs, the knowledge and information gained from directorships can enhance auditors’ competencies in auditing their clients, especially when their audit clients operate in the same industry and use similar accounting practices as the company where they hold a directorship. As of the trend toward the use of fair values and other estimates, audits of fair value measurements and estimates have become a major challenge for auditors (Baugh & Mauldin, 2018; Glover et al., 2017). Making appropriate judgments is difficult in the case when recognition, measurement and disclosure decisions involve assumptions, probabilities, and forward-looking expectations (IAASB, 2014). As independent directors can gain information about industry-specific factors including government policies that affect future developments at a company or in an industry, this forward-looking information about the economic prospects of an industry is valuable when IDAPs assess clients’ fair value estimates or predict their ability to continue as going concerns. Moreover, IDAPs typically serve as audit committee members. By monitoring the financial reporting process, IDAPs gain information on industry-specific accounting or auditing issues. This helps them to identify key audit risks in peer firms and to detect material misstatements more effectively. In summary, we expect directorship experience to improve auditors’ professional judgments, which in turn improves audit quality.

Based on these arguments, we hypothesize that:

Research Design

Measurement of Audit Quality

There is no unique definition of audit quality, given heterogeneous preferences across different market participants, and audit quality measures cannot be treated independently from financial reporting quality (Carcello et al., 1992; Demski, 1973; Sarath, 2016). Therefore, discretionary accruals, a component of accounting quality, are a reasonable proxy to measure audit quality. We use two versions of discretionary accruals as proxies for the components of audit quality that might be influenced by IDAPs. First, we calculate discretionary accruals using the following model (Kothari et al., 2005):

where the subscripts j and t represent company j in year t. TACC is total accruals calculated as income minus cash flows from operations. ΔREV and ΔREC are the change in revenue and the change in account receivables from year t−1 to year t, respectively; PPE is gross property, plant, and equipment. These variables are scaled by beginning total assets. ROA is returns on assets. We estimate Equation (1) for each industry-year with at least 20 observations and use the residuals as discretionary accruals (DA1).

Second, we use performance-matched discretionary accruals (DA2) proposed by Kothari et al. (2005) to measure audit quality. We first estimate the modified Jones model in Equation (2) for each industry-year.

DA2 is defined as the difference in residuals between each observation and the matched observation with the closest ROA in the same industry-year. Higher discretionary accruals indicate lower audit quality.

Audit Quality Models

We use the following model to test whether IDAPs provide higher audit quality (using discretionary accruals as an empirical proxy for audit quality) than other auditors (H1).

The model used for testing H2 is specified as follows:

In Equation (3), IDAP is coded 1 if a company is audited by an IDAP, 0 otherwise. If the empirical results support H1, the coefficient on IDAP will be negative. In Equation (4), IDAP_SAME is coded 1 if a company is audited by an IDAP who has directorship experience in the same industry, 0 otherwise. IDAP_DIF is equal to 1, if a client has an audit partner with directorship experience in a different industry, and 0 otherwise. H2 predicts that β1 will be smaller than β2. Using the CSRC industry classification scheme, we classify industries using two-digit industry codes for the manufacturing sector and one-digit industry codes for other sectors (Gul et al., 2013).

We include firm characteristics following Gul et al. (2013) and Chi et al. (2017). We use LNTA (logged total assets) to proxy for client size. ROA (return on assets) and LOSS (an indicator for negative operating income) capture profitability. LEV is financial leverage (the ratio of total liabilities to total assets). Prior studies provide mixed results on the effects of ROA, LOSS, and LEV on discretionary accruals. OCF (operating cash flows) is expected to be negatively associated with discretionary accruals. SALEGROW (sales growth) and MTB (market-to-book ratio) capture the positive effect of growth opportunities on incentives for earnings managements. We control for AGE (listing age) because older Chinese listed companies may have exhausted the capital raised in IPOs and may be financially distressed (DeFond et al., 2000).

In terms of auditor characteristics, TopN (an indicator for a Big 4 global audit firm or Top 10 domestic audit firm) is expected to be associated with higher audit quality. PCI is partner-level client importance (Chen et al., 2010). FEMALE is coded 1 if a client is audited by a female partner. EDU is the average educational level of the audit partners. CLIEXP is the average client-specific experience of the partners. EXP (INDEXP) is the average auditing experience (industry-specific auditing experience) of the partners, where a partner’s auditing experience (industry-specific auditing experience) is defined as the cumulative number of years since the partner audited any listed company (any listed company in a given industry). PARTNER is coded 1 if a client is audited by an equity partner. We also control for partner-level industry specialists (INDSPEC). Year and industry dummies are included, and standard errors are clustered by client.

Sample Selection and Univariate Analysis

Sample Selection

The sample period is from 2001 through 2018 because the CSRC has required listed companies to have financial experts as independent directors since 2001. The primary data source is the China Stock Market and Accounting Research (CSMAR) Database. We review each independent director’s profile and identify those who are IDAPs during the sample period. We collect data on auditors’ demographic information from the inquiry system of the Chinese Institute of Certified Public Accountants (CICPA). 2

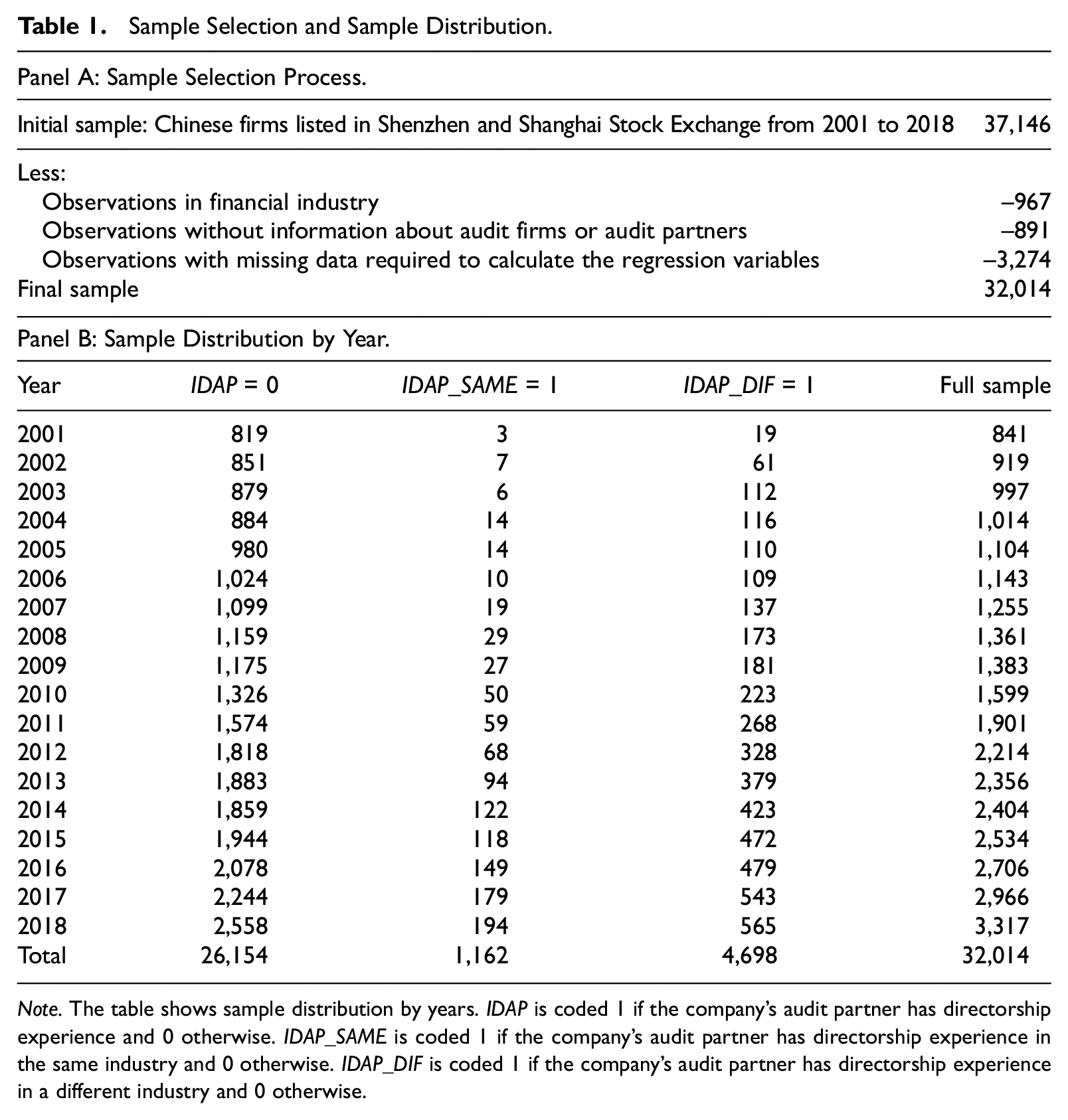

We start with a sample of 37,146 firm-year observations. After removing financial institutions and firm-years without auditor-related information or with missing values of the regression variables, the final sample contains 32,014 observations. The detailed sample screening process is provided in Panel A of Table 1.

Sample Selection and Sample Distribution.

Note. The table shows sample distribution by years. IDAP is coded 1 if the company’s audit partner has directorship experience and 0 otherwise. IDAP_SAME is coded 1 if the company’s audit partner has directorship experience in the same industry and 0 otherwise. IDAP_DIF is coded 1 if the company’s audit partner has directorship experience in a different industry and 0 otherwise.

Note. The table shows sample distribution by industries. IDAP_SAME is coded 1 if the company’s audit partner has directorship experience in the same industry and 0 otherwise.

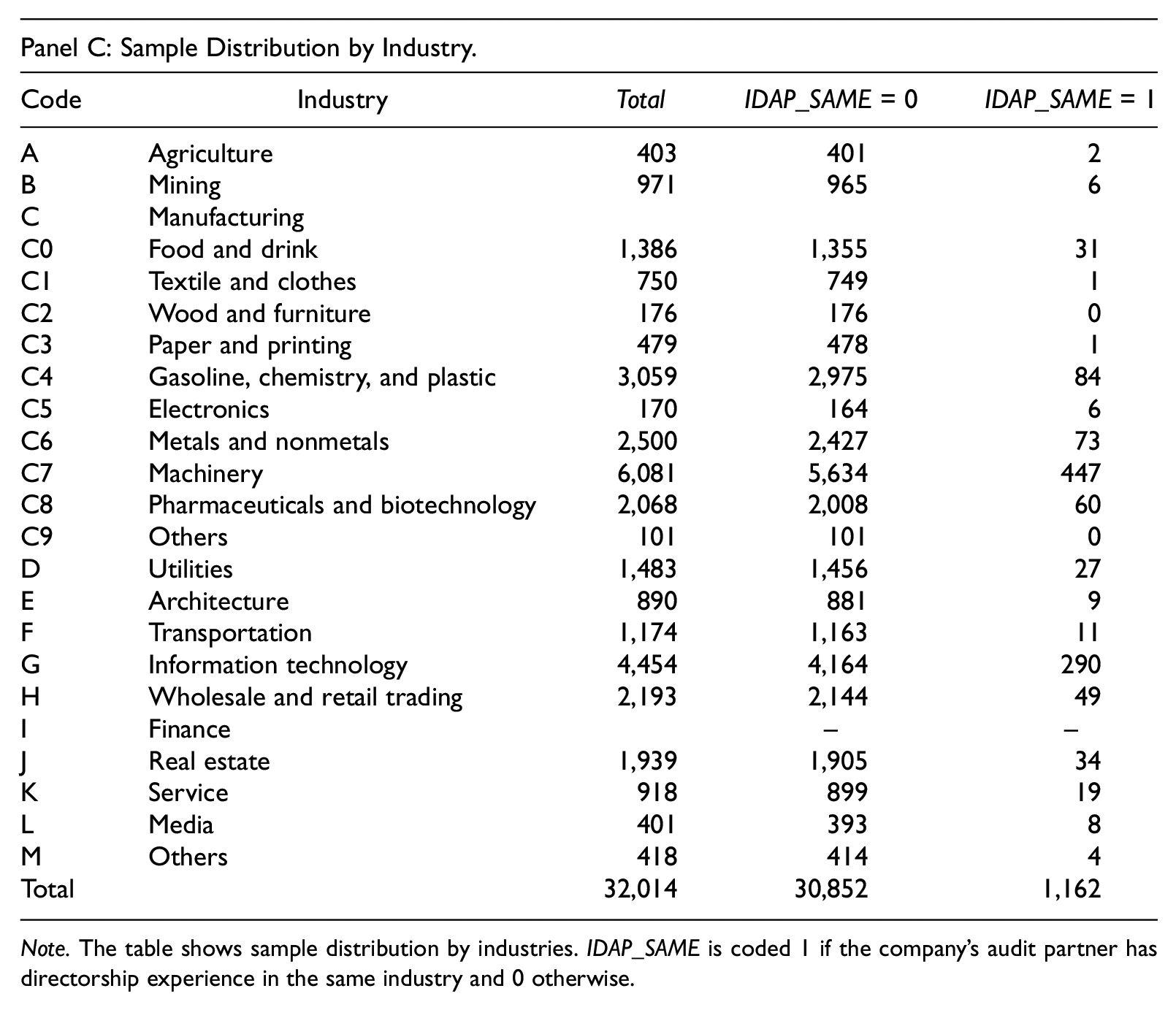

Panel B presents the sample distribution by year. The number of firms audited by IDAPs with directorship experience in the same industries (IDAP_SAME = 1) increases from 3 in 2001 to 194 in 2018. The number of firms audited by IDAPs with directorship experience in different industries (IDAP_DIF = 1) also increases over time. As Panel C shows, the sample is not distributed evenly across industries. There are 447 firms-years where IDAP_SAME is coded 1 in the machinery industry, whereas no firm-years have IDAP_SAME equal to 1 in the wood and furniture sector.

Descriptive Statistics

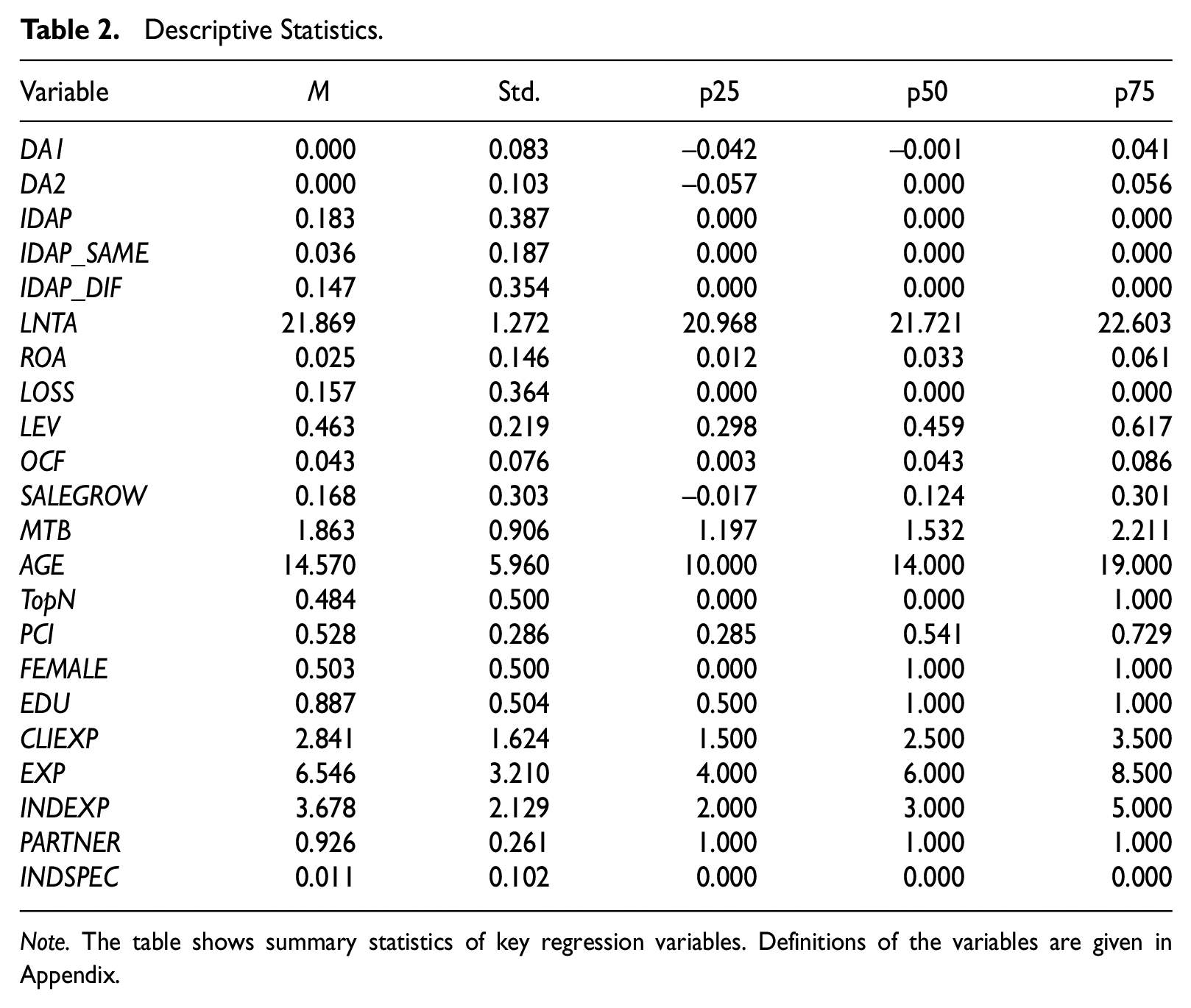

We report descriptive statistics for the regression variables in Table 2. The mean values of DA1 and DA2 are close to 0 with standard deviation of 0.083 and 0.103, respectively. Among the sample firms, 18.3% are audited by IDAPs. IDAP_SAME and IDAP_DIF are 0.036 and 0.147 on average, indicating that 3.6% and 14.7% of the firms are audited by IDAPs having directorship experience in the same and different industries, respectively. The descriptive statistics for the financial variables are in line with prior China-based studies (e.g., Chen et al., 2010; Huang et al., 2015). LNTA is 21.869 on average, indicating that the average total assets are 3.14 billion RMB. The mean value of ROA is 0.025, so net income accounts for 2.5% of total assets on average. Approximately 15.7% of the firms report an operating loss.

In terms of auditor-related variables, 48.4% are audited by Big 4 or Top 10 audit firms. On average, a partner audits a client for 2.841 years (CLIEXP) and a partner’s industry-specific experience (INDEXP) is 3.679 years.

Descriptive Statistics.

Note. The table shows summary statistics of key regression variables. Definitions of the variables are given in Appendix.

Empirical Results

Regression Results for Hypothesis Testing

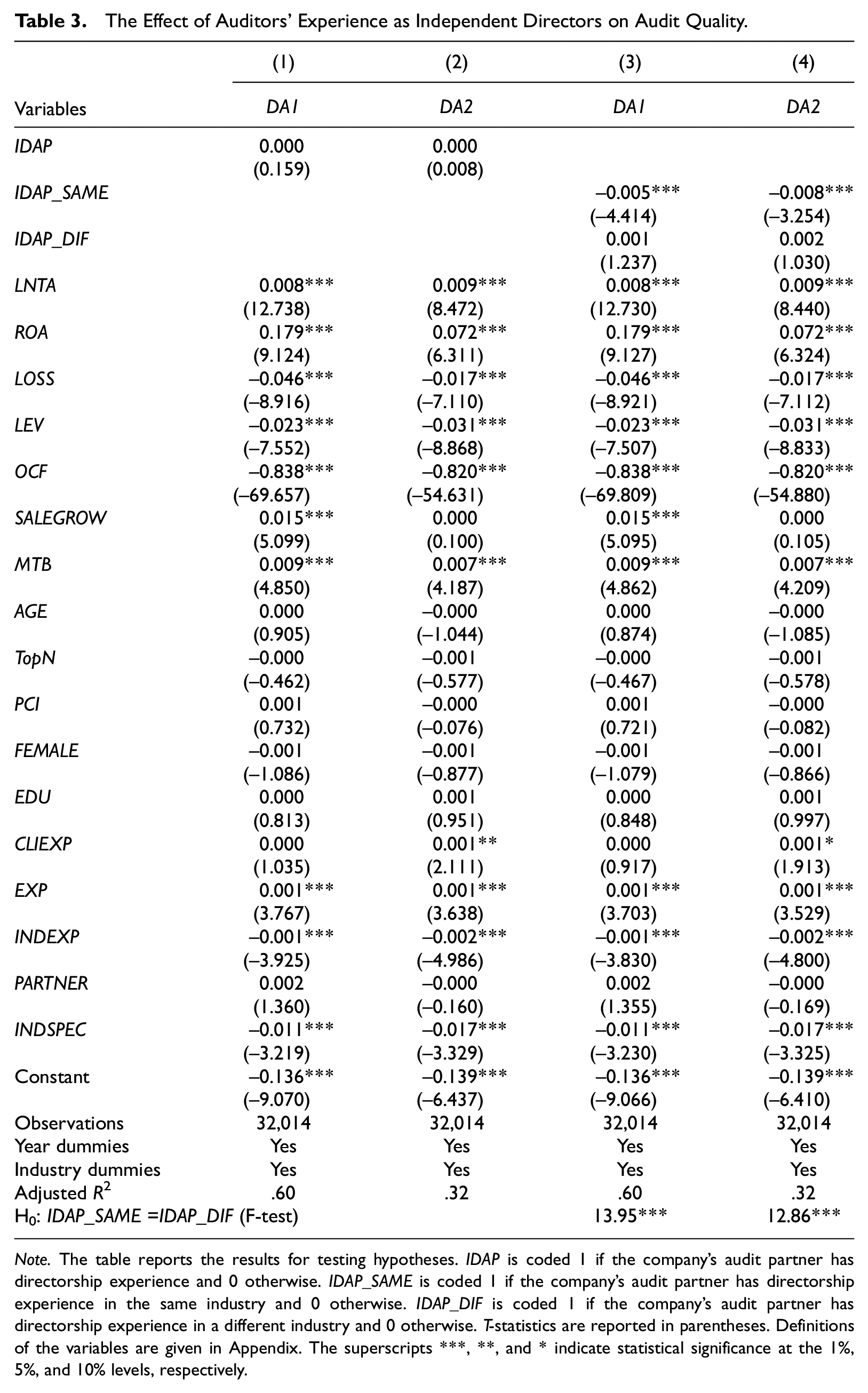

We present the regression results from testing the hypotheses in Table 3. In columns (1) and (2), the coefficients on IDAP are insignificant, which does not support H1. In columns (3) and (4), we report the results from testing H2. The coefficients on IDAP_SAME are negative and significant at the 1% level, whereas the coefficients on IDAP_DIF are insignificant. These results suggest that IDAPs provide higher audit quality to clients in the same industries as companies where they sit on the board. The F-test indicates a significant difference in the coefficients between IDAP_SAME and IDAP_DIF. This supports H2 and suggests that knowledge spillovers are stronger if IDAPs have directorship experience in the same industry rather than in a different industry. As IDAP_SAME accounts for a small proportion of the firms audited by IDAPs (19.8%), the insignificant relation between IDAP and audit quality is driven mainly by the IDAPs with directorship experience in different industries.

The Effect of Auditors’ Experience as Independent Directors on Audit Quality.

Note. The table reports the results for testing hypotheses. IDAP is coded 1 if the company’s audit partner has directorship experience and 0 otherwise. IDAP_SAME is coded 1 if the company’s audit partner has directorship experience in the same industry and 0 otherwise. IDAP_DIF is coded 1 if the company’s audit partner has directorship experience in a different industry and 0 otherwise. T-statistics are reported in parentheses. Definitions of the variables are given in Appendix. The superscripts ***, **, and * indicate statistical significance at the 1%, 5%, and 10% levels, respectively.

Regarding the control variables, LNTA and ROA are positively related to discretionary accruals, whereas LOSS and LEV are negatively related to discretionary accruals. Clients with lower operating cash flows (OCF) and more growth opportunities (MTB and SALEGROW) use more earnings management. Finally, auditors with more industry experience (INDEXP) and greater industry specialization (INDSPEC) provide higher audit quality.

Additional Tests

The Moderating Effect of Auditors’ Client-Specific or Industry-Specific Experience

Auditors can accumulate knowledge as their audit tenure or industry auditing experience becomes longer (e.g., Chen et al., 2008; Chi et al., 2017). Accordingly, we predict that the effect of directorship experience will be weaker when IDAPs have longer industry or client-specific experience.

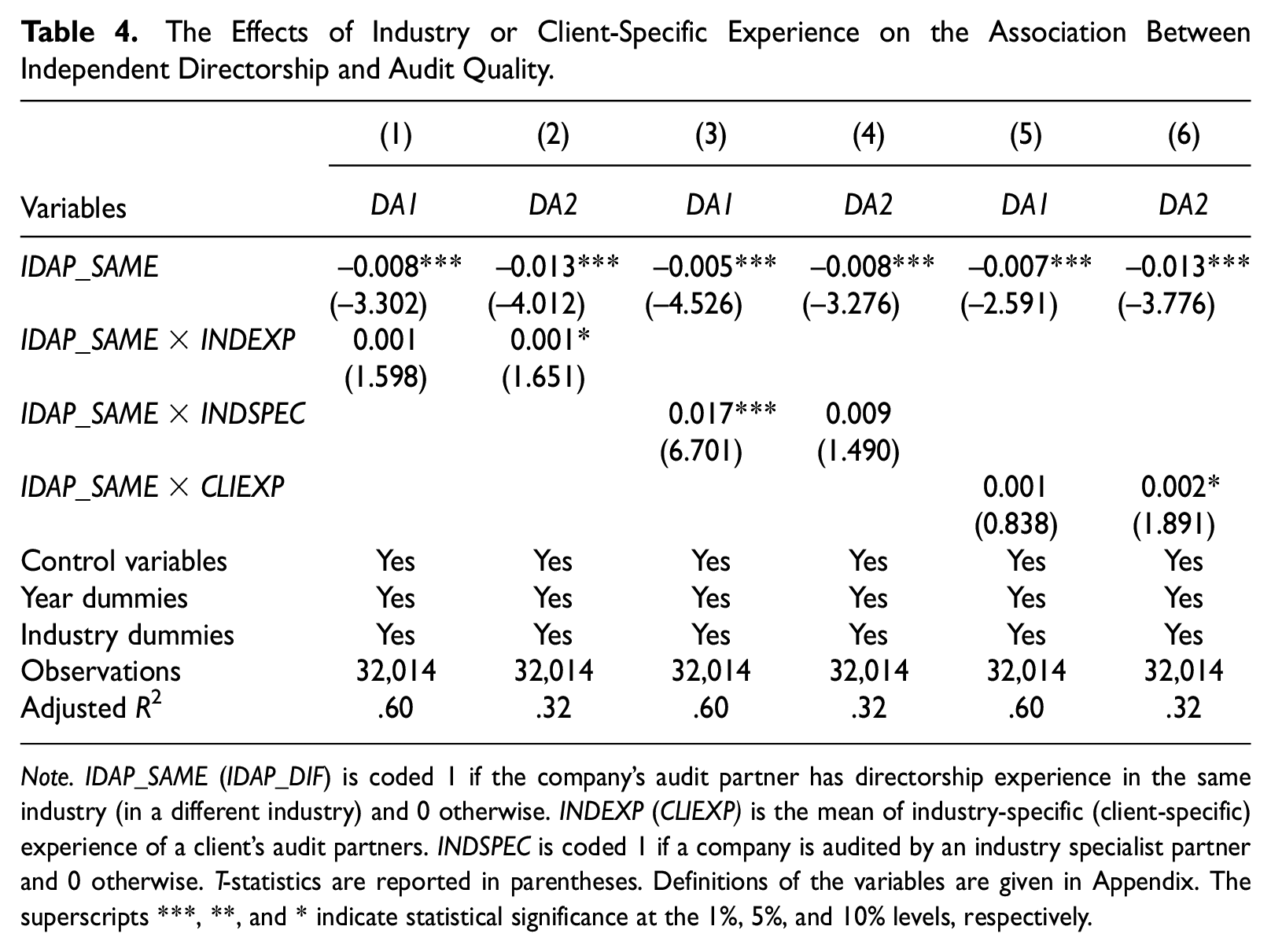

To examine the moderating effect of partner-level industry experience (industry specialization), we add the interaction term IDAP_SAME*INDEXP (or IDAP_SAME* INDSPEC) into Equation (4). Columns (1)–(4) of Table 4 reveal that IDAP_SAME*INDEXP and IDAP_SAME*INDSPEC are positively related to DA2 and DA1, respectively, and the coefficients on IDAP_SAME remain negative. In columns (5) and (6), we include the interaction term IDAP_SAME*CLIEXP. The coefficients on the interaction term are positive in both models but significant only for DA2. Overall, these results provide evidence that the effect of directorship experience is attenuated by audit partners’ industry or client-specific experience.

The Effects of Industry or Client-Specific Experience on the Association Between Independent Directorship and Audit Quality.

Note. IDAP_SAME (IDAP_DIF) is coded 1 if the company’s audit partner has directorship experience in the same industry (in a different industry) and 0 otherwise. INDEXP (CLIEXP) is the mean of industry-specific (client-specific) experience of a client’s audit partners. INDSPEC is coded 1 if a company is audited by an industry specialist partner and 0 otherwise. T-statistics are reported in parentheses. Definitions of the variables are given in Appendix. The superscripts ***, **, and * indicate statistical significance at the 1%, 5%, and 10% levels, respectively.

IDAPs on Audit Committees

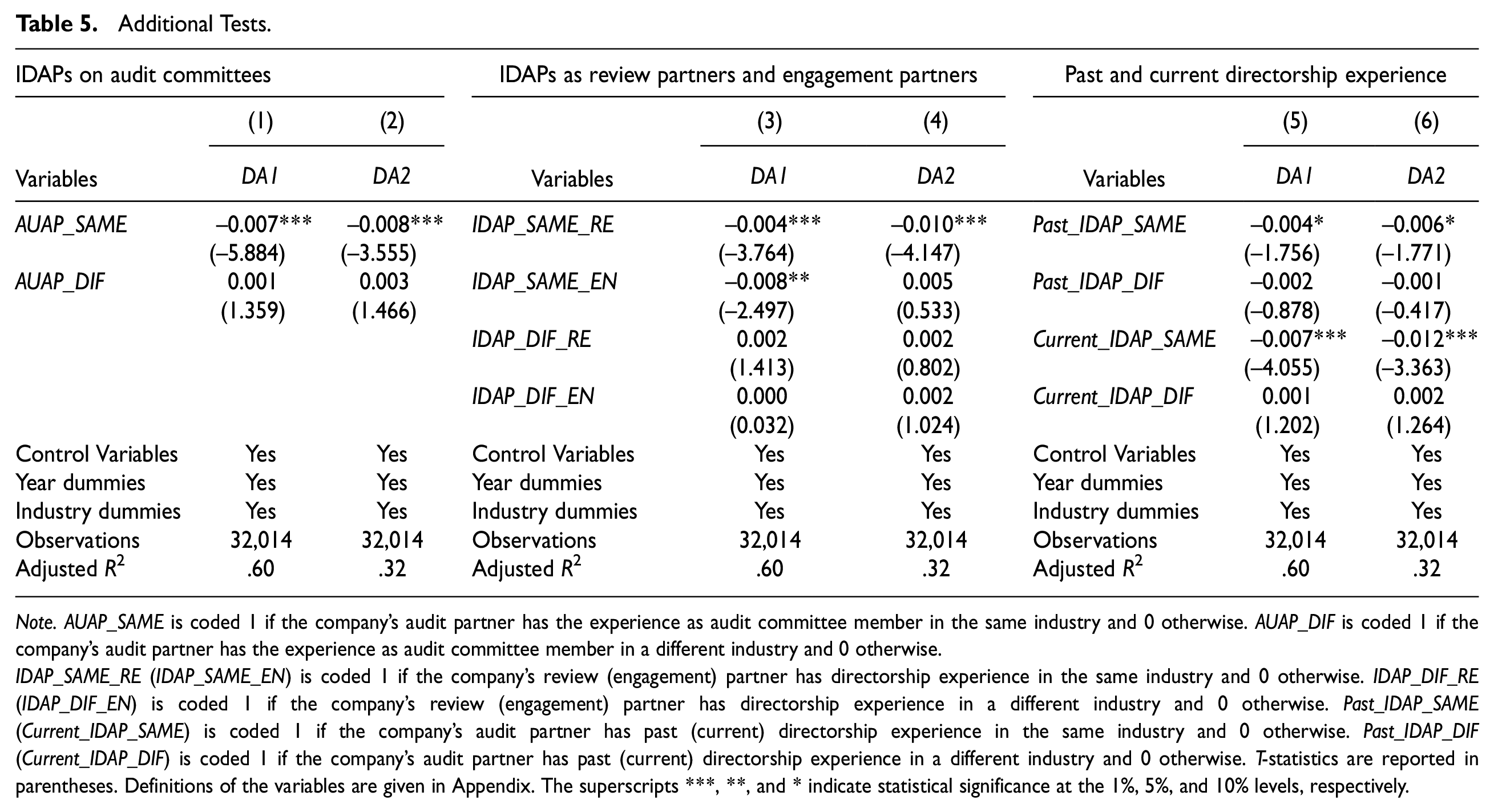

The main responsibility of an audit committee is to oversee the financial reporting process; thus, experience as an audit committee member may have a more direct effect on IDAPs’ audit quality. In the sample, approximately 87% of individual IDAPs are audit committee members. We set AUAP_SAME (AUAP_DIF) to equal 1 for clients audited by IDAPs with the experience as audit committee members in the same (different) industry and retest H2. The regression results in columns (1) and (2) of Table 5 indicate that our main findings are unchanged.

Additional Tests.

Note. AUAP_SAME is coded 1 if the company’s audit partner has the experience as audit committee member in the same industry and 0 otherwise. AUAP_DIF is coded 1 if the company’s audit partner has the experience as audit committee member in a different industry and 0 otherwise.

IDAP_SAME_RE (IDAP_SAME_EN) is coded 1 if the company’s review (engagement) partner has directorship experience in the same industry and 0 otherwise. IDAP_DIF_RE (IDAP_DIF_EN) is coded 1 if the company’s review (engagement) partner has directorship experience in a different industry and 0 otherwise. Past_IDAP_SAME (Current_IDAP_SAME) is coded 1 if the company’s audit partner has past (current) directorship experience in the same industry and 0 otherwise. Past_IDAP_DIF (Current_IDAP_DIF) is coded 1 if the company’s audit partner has past (current) directorship experience in a different industry and 0 otherwise. T-statistics are reported in parentheses. Definitions of the variables are given in Appendix. The superscripts ***, **, and * indicate statistical significance at the 1%, 5%, and 10% levels, respectively.

Directorship Experience of Engagement Partners and Review Partners

As explained previously, in China, an audit report is typically signed by two partners. The signature of the review partner is located above that of the engagement partner (Lennox et al., 2014), enabling us to separately test for an effect of directorship experience for review versus engagement partners. The untabulated statistics reveal that 1,013 of 1,162 firm-years with IDAP_SAME = 1 have review partners with directorship experience in the same industry (IDAP_SAME_RE = 1). The regression results in columns (3) and (4) of Table 5 indicate that engagement and review partners with directorship experience in the same industry deliver higher audit quality in the DA1 model, but only review partners with same industry experience deliver higher audit quality in the DA2 model. 3 Audit quality is unaffected when either the review or engagement partner has directorship experience in different industries (IDAP_DIF_EN = 1 or IDAP_DIF_RE = 1).

Past and Current Experience as Independent Directors

In our main analyses, we test for an effect of IDAPs’ directorship experience on audit quality without identifying whether directorship experience is current or in the past. To test whether there is any difference between current and past directorship experience, we re-estimate Equation (4) distinguishing between the types of experience.

Columns (5) and (6) of Table 5 show that past and current directorship experience in the same industry (Past_IDAP_SAME and Current_IDAP_SAME) are negatively related to earnings management, but neither past nor current directorship experience in different industries (Past_IDAP_DIF or Current_IDAP_DIF) has an effect on audit quality. F-tests (untabulated) show no significant difference between Past_IDAP_SAME and Current_IDAP_SAME.

Alternative Measures of Audit Quality

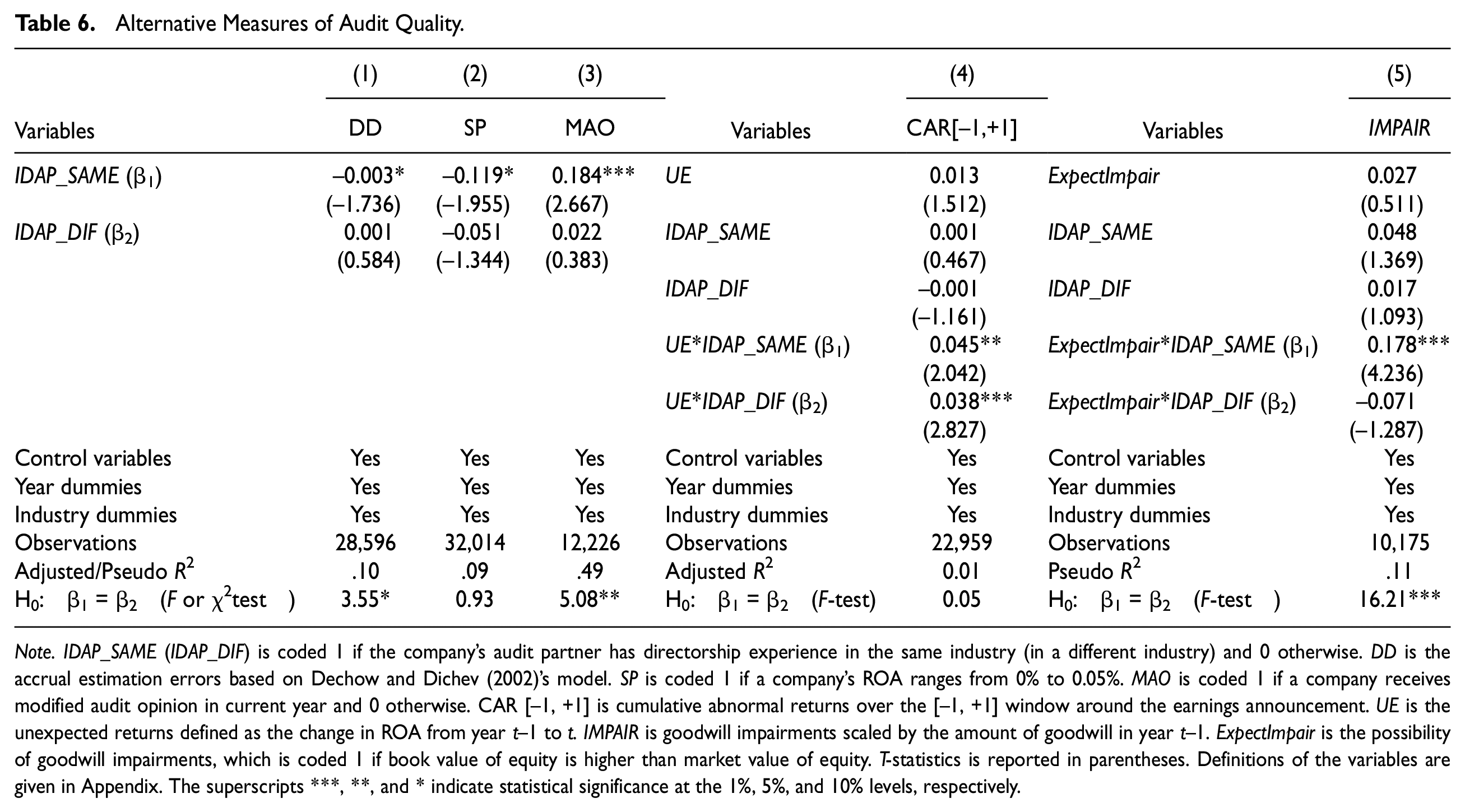

As mentioned earlier, there is no unique definition of audit quality, and discretionary accruals are one of the empirical proxies for audit quality. To check the robustness of our results, we use various alternative measures to capture different facets of audit (accounting) quality. The first is accrual estimation errors based on Dechow and Dichev (2002)’s model (DD model). We regress the change in working capitals on operating cash flows in year t−1, year t, and year t+1 for each industry-year with at least 20 observations, and we use the residuals as accrual estimation errors (DD). 4 The second measure is the likelihood of reporting small profits (SPs) with ROA between 0% and 0.5%. We also use modified audit opinions (MAO) as another proxy. MAOs are issued to the firms that are financially distressed or violate generally accepted accounting principles (GAAP), so we estimate a probit model for MAO using the subsample of firms that are financially distressed or subsequently restate their current financial statements. 5 As shown in columns (1)–(3) of Table 6, IDAP_SAME is negatively related to DD and SP, but is positively related to MAO. The coefficients on IDAP_DIF are insignificant in the three models. F-tests (χ2-tests) show that the coefficients on the two variables are significantly different in the DD (MAO) models. These results are consistent with our main findings.

Alternative Measures of Audit Quality.

Note. IDAP_SAME (IDAP_DIF) is coded 1 if the company’s audit partner has directorship experience in the same industry (in a different industry) and 0 otherwise. DD is the accrual estimation errors based on Dechow and Dichev (2002)’s model. SP is coded 1 if a company’s ROA ranges from 0% to 0.05%. MAO is coded 1 if a company receives modified audit opinion in current year and 0 otherwise. CAR [−1, +1] is cumulative abnormal returns over the [−1, +1] window around the earnings announcement. UE is the unexpected returns defined as the change in ROA from year t−1 to t. IMPAIR is goodwill impairments scaled by the amount of goodwill in year t−1. ExpectImpair is the possibility of goodwill impairments, which is coded 1 if book value of equity is higher than market value of equity. T-statistics is reported in parentheses. Definitions of the variables are given in Appendix. The superscripts ***, **, and * indicate statistical significance at the 1%, 5%, and 10% levels, respectively.

We also test investor perceptions of audit quality using the earnings response coefficient (ERC) as follows:

where CAR [−1, +1] is cumulative abnormal returns over the [−1, 1] window around the earnings announcement, and UE denotes unexpected earnings. Following He et al. (2016), we include control variables LNTA, LOSS, LEV, MTB, DRISK (volatility of daily returns during the year) and auditor characteristics from Equations (3) and (4). Column (4) of Table 6 shows that UE*IDAP_SAME and UE*IDAP_DIF have positive coefficients in the ERC model. The results suggest that investors perceive that IDAPs provide higher audit quality than do other auditors, regardless of the industries where they gain directorship experience.

In our hypothesis development, we argue that IDAPs may have access to forward-looking information, which is useful for fair value estimates. To provide empirical evidence on the argument, we test whether IDAPs are better at evaluating goodwill impairments. We estimate a Tobit model as follows:

IMPAIR represents goodwill impairments in year t scaled by the amount of goodwill in year t−1. ExpectImpair is coded 1 if the book value of equity exceeds the market value of equity (Beatty & Weber, 2006). Clients with ExpectImpair taking the value of 1 have a higher probability of goodwill impairments. If IDAPs can detect and restrict clients’ opportunistic avoidance of goodwill impairments, then we will observe a positive coefficient on ExpectImpair*IDAP_SAME. 6

In column (5) of Table 6, we find that IDAPs with directorship experience in the same industry are more likely than those with directorship experience in a different industry to induce the recognition of goodwill impairments for clients who have higher risk of goodwill impairment.

Propensity Score Matching

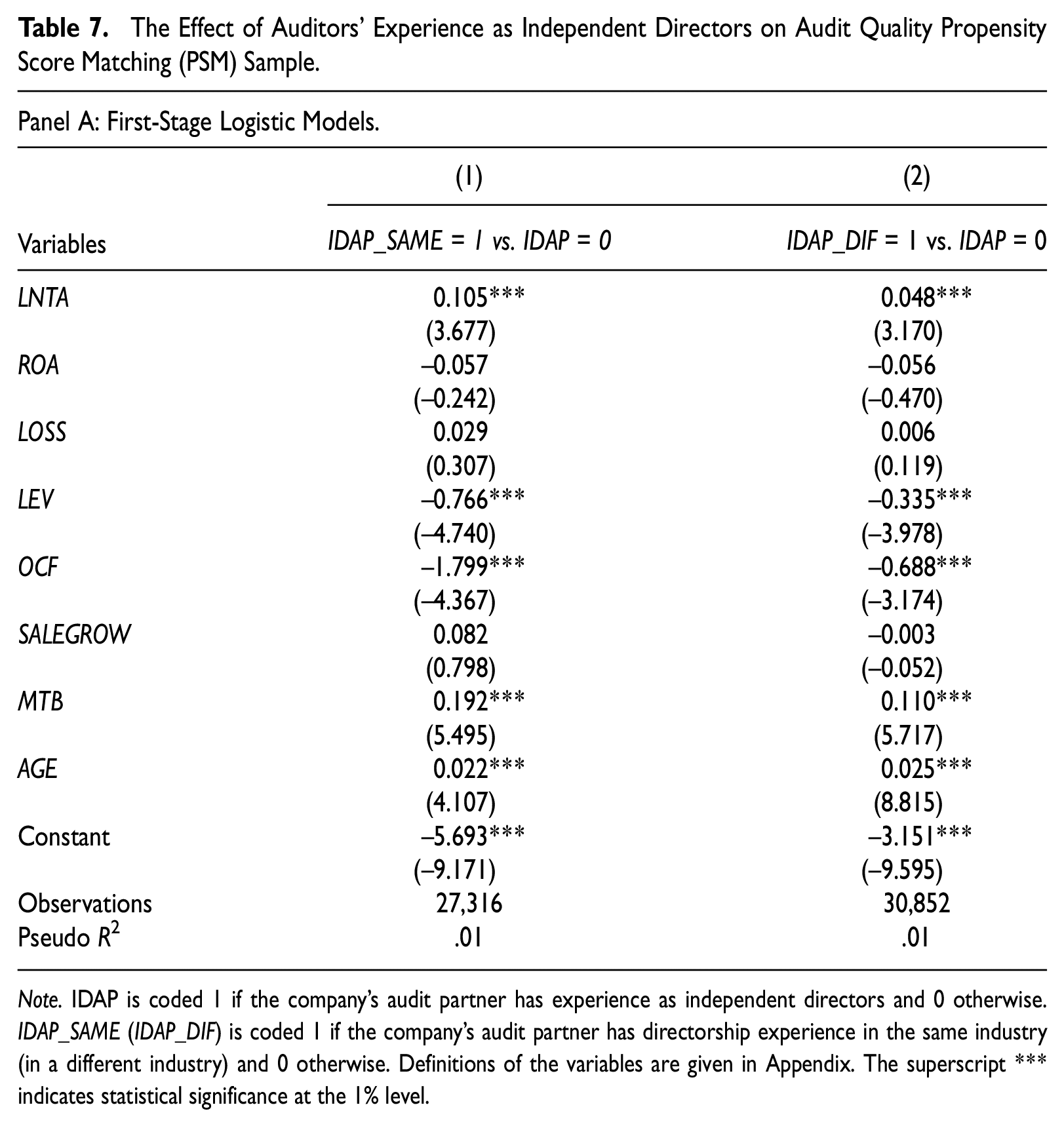

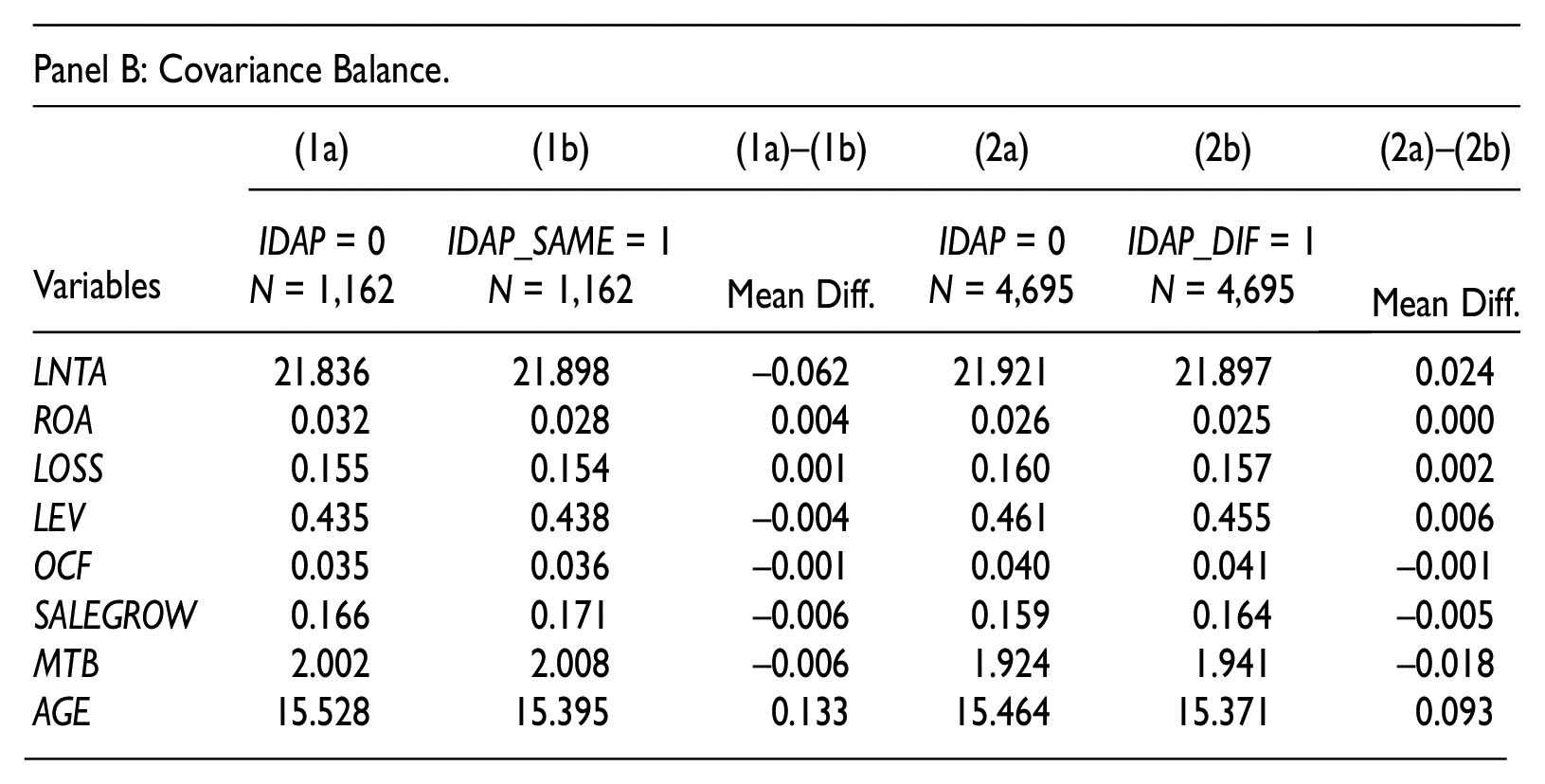

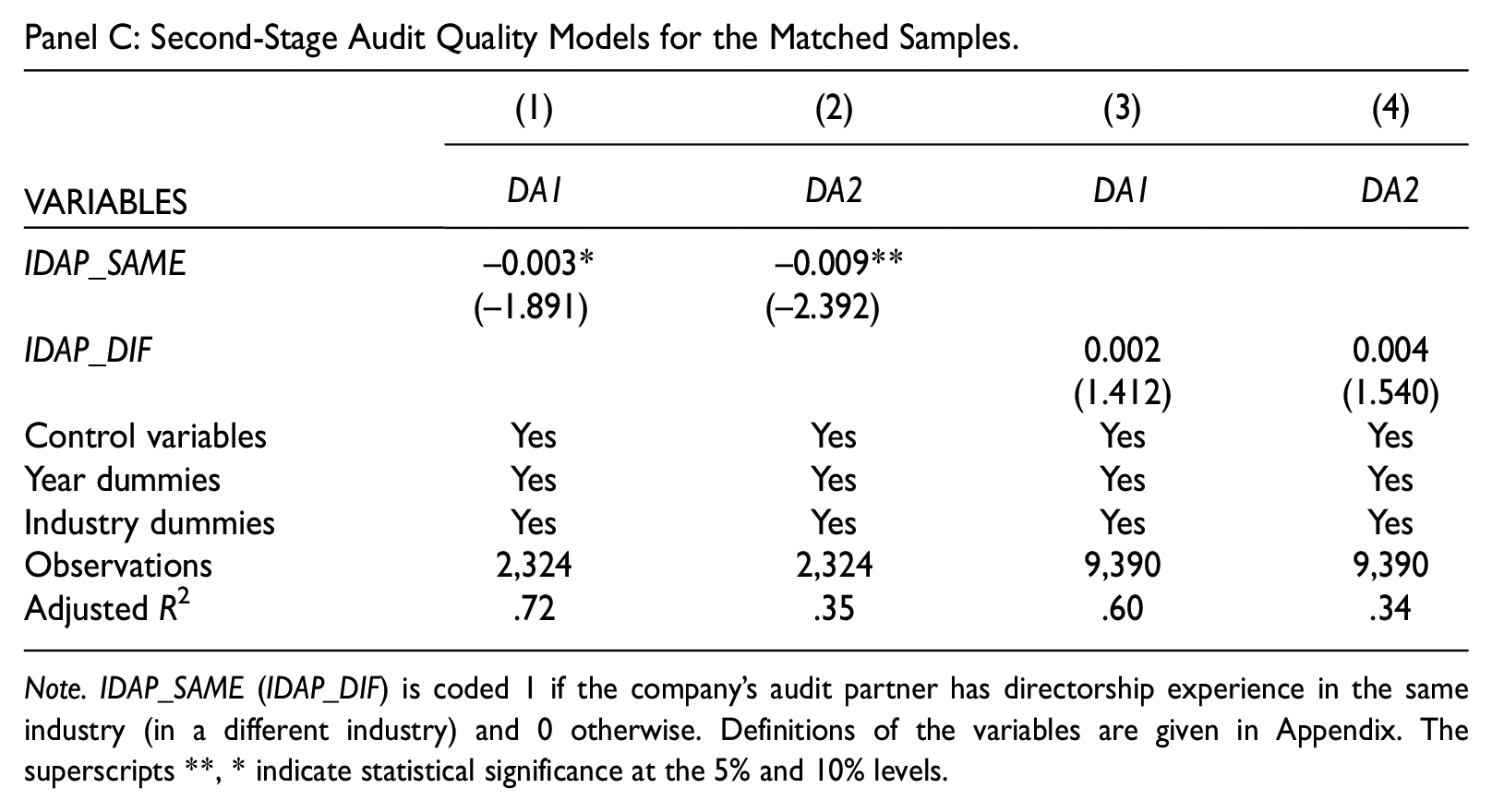

The high audit quality of IDAPs may be attributed to differences in characteristics between clients audited by IDAPs and non-IDAPs. We use Propensity Score Matching (PSM) approach in an attempt to mitigate this concern, but we acknowledge that matching on observables cannot control for differences in unobservables so this test is not conclusive. Moreover, the results may still be subject to other limitations such as selection bias or omitted variables issues (Shipman et al., 2017). We partition the clients into three subsamples, namely, the firm-years where IDAP equals 0, the firm-years where IDAP_SAME equals 1, and the firm-years where IDAP_DIF equals 1. Panel A of Table 7 reports the results from the first-stage logistic regression models. Compared with the clients of non-IDAPs, firms audited by IDAPs with directorship experience either in the same or different industries are larger and have less financial leverage, lower operating cash flows, higher market-to-book ratios, and are older. Based on the results from the first-stage models, we match each firm-year where IDAP_SAME is coded 1 with a firm-year where IDAP is equal to 0, without replacement, at a caliper distance of 0.05. We then replicate the above procedures to match the firm-years where IDAP_DIF is coded 1 with those audited by non-IDAPs. Panel B shows insignificant difference in the mean of the financial variables for the matched subsamples after PSM, that is, PSM mitigates observable difference in client characteristics. We re-estimate the audit quality models using the matched samples, and the results shown in Panel C indicate that our main findings are robust.

The Effect of Auditors’ Experience as Independent Directors on Audit Quality Propensity Score Matching (PSM) Sample.

Note. IDAP is coded 1 if the company’s audit partner has experience as independent directors and 0 otherwise. IDAP_SAME (IDAP_DIF) is coded 1 if the company’s audit partner has directorship experience in the same industry (in a different industry) and 0 otherwise. Definitions of the variables are given in Appendix. The superscript *** indicates statistical significance at the 1% level.

Note. IDAP_SAME (IDAP_DIF) is coded 1 if the company’s audit partner has directorship experience in the same industry (in a different industry) and 0 otherwise. Definitions of the variables are given in Appendix. The superscripts **, * indicate statistical significance at the 5% and 10% levels.

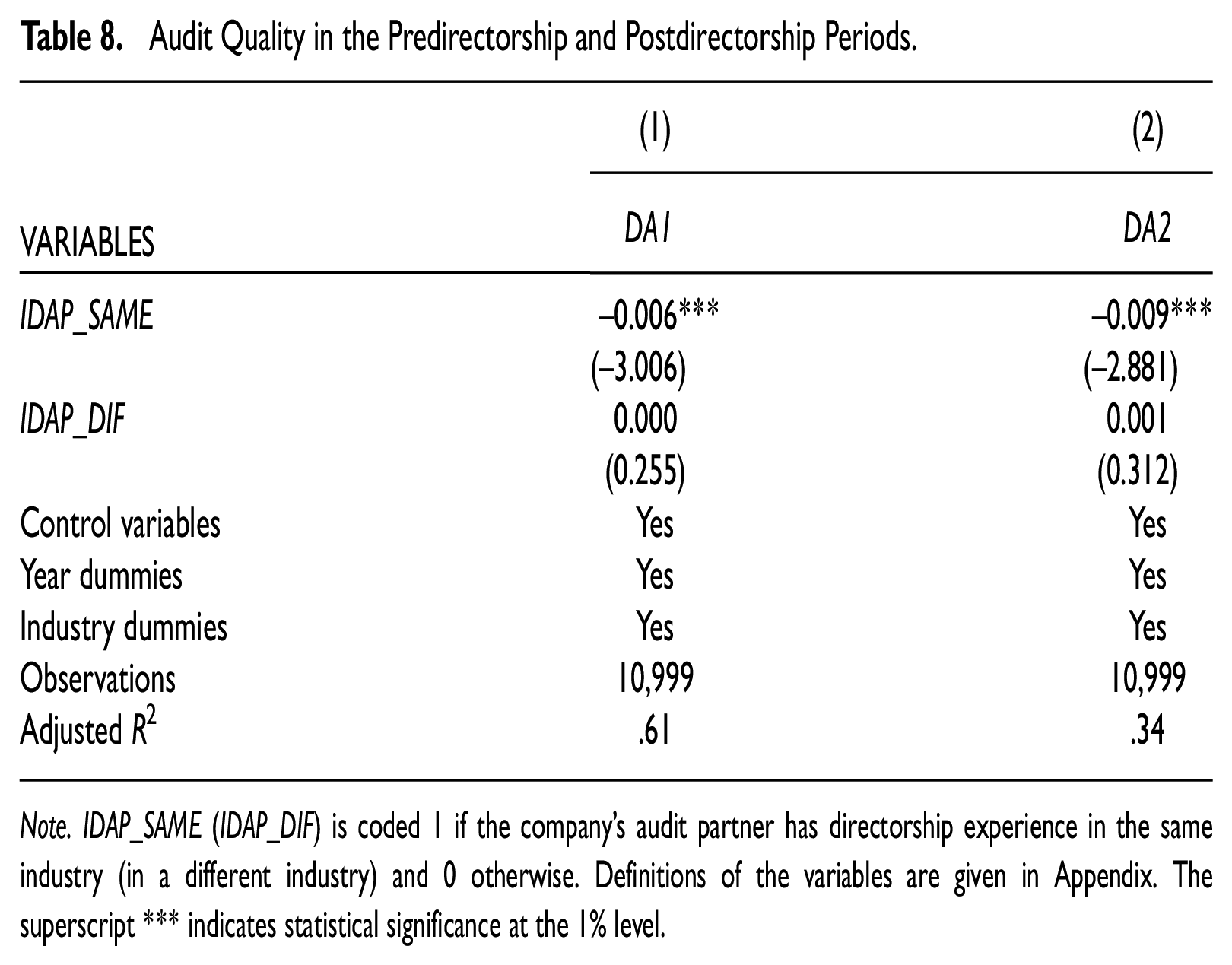

Audit Quality in the Predirectorship and Postdirectorship Periods

An alternative explanation for our main findings is that audit partners who deliver higher audit quality are more likely to be invited as directors. In an attempt to rule out this possibility, we compare the audit quality of IDAPs in the predirectorship and postdirectorship periods. Specifically, we test the audit quality models using a panel of clients audited by at least one IDAP during the sample period. Thus, we exclude firm-year observations that were never audited by an IDAP during the sample period. As the key variables IDAP_SAME and IDAP_DIF capture the firm-years audited by IDAPs after they gain directorships, the benchmark group (where both IDAP_SAME and IDAP_DIF are equal to 0) is the client-years audited by IDAPs in the predirectorship period. As shown in Table 8, IDAP_SAME continues to have a negative coefficient, suggesting that audit quality improves after IDAPs gain directorship experience in the same industry, whereas the coefficient on IDAP_DIF remains insignificant.

Audit Quality in the Predirectorship and Postdirectorship Periods.

Note. IDAP_SAME (IDAP_DIF) is coded 1 if the company’s audit partner has directorship experience in the same industry (in a different industry) and 0 otherwise. Definitions of the variables are given in Appendix. The superscript *** indicates statistical significance at the 1% level.

Subsample Analysis: Accounting Firms With IDAPs

Finally, to address whether the results are subject to self-selection bias of audit firms, we limit the sample to clients audited by audit firms where there is at least one IDAP. Untabulated results reveal that the main findings are robust to this subsample analysis.

Conclusions

This study examines whether audit partners who have experience as independent directors (IDAPs) provide higher quality financial statements than those without directorship experience. The results show that IDAPs provide superior quality only when their directorship experience is in the same industry as their clients. Additional analyses provide evidence that auditors’ client- and industry-specific experience attenuate the positive effect of directorship experience on audit quality, implying that directorship experience is more important for new auditors or for auditors with less industry experience. The results are robust to a host of sensitivity tests using alternative measures of audit quality.

Our study contributes to the literature on auditors’ knowledge acquisition and competence. We identify an alternative way through which auditors can acquire industry-specific knowledge to enhance their professional judgments and hence performance. Moreover, our study provides evidence on positive externalities or contagious effects of appointing financial experts as independent directors. That is, directorship experience can be beneficial to other firms where financial experts provide professional services. The findings should be useful for accounting firms in making partner assignments and for clients in selecting audit partners.

Footnotes

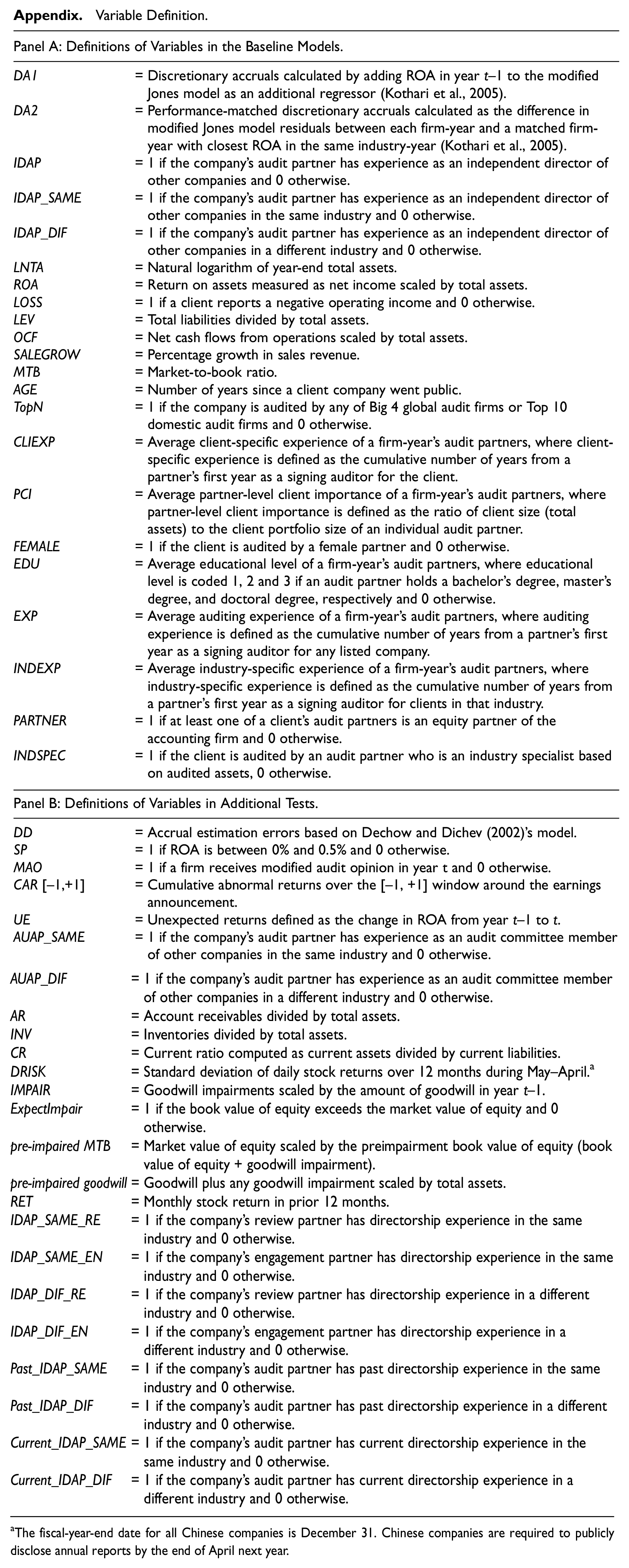

Appendix

Variable Definition.

| Panel A: Definitions of Variables in the Baseline Models. | |

|---|---|

| DA1 | = Discretionary accruals calculated by adding ROA in year t−1 to the modified Jones model as an additional regressor (Kothari et al., 2005). |

| DA2 | = Performance-matched discretionary accruals calculated as the difference in modified Jones model residuals between each firm-year and a matched firm-year with closest ROA in the same industry-year (Kothari et al., 2005). |

| IDAP | = 1 if the company’s audit partner has experience as an independent director of other companies and 0 otherwise. |

| IDAP_SAME | = 1 if the company’s audit partner has experience as an independent director of other companies in the same industry and 0 otherwise. |

| IDAP_DIF | = 1 if the company’s audit partner has experience as an independent director of other companies in a different industry and 0 otherwise. |

| LNTA | = Natural logarithm of year-end total assets. |

| ROA | = Return on assets measured as net income scaled by total assets. |

| LOSS | = 1 if a client reports a negative operating income and 0 otherwise. |

| LEV | = Total liabilities divided by total assets. |

| OCF | = Net cash flows from operations scaled by total assets. |

| SALEGROW | = Percentage growth in sales revenue. |

| MTB | = Market-to-book ratio. |

| AGE | = Number of years since a client company went public. |

| TopN | = 1 if the company is audited by any of Big 4 global audit firms or Top 10 domestic audit firms and 0 otherwise. |

| CLIEXP | = Average client-specific experience of a firm-year’s audit partners, where client-specific experience is defined as the cumulative number of years from a partner’s first year as a signing auditor for the client. |

| PCI | = Average partner-level client importance of a firm-year’s audit partners, where partner-level client importance is defined as the ratio of client size (total assets) to the client portfolio size of an individual audit partner. |

| FEMALE | = 1 if the client is audited by a female partner and 0 otherwise. |

| EDU | = Average educational level of a firm-year’s audit partners, where educational level is coded 1, 2 and 3 if an audit partner holds a bachelor’s degree, master’s degree, and doctoral degree, respectively and 0 otherwise. |

| EXP | = Average auditing experience of a firm-year’s audit partners, where auditing experience is defined as the cumulative number of years from a partner’s first year as a signing auditor for any listed company. |

| INDEXP | = Average industry-specific experience of a firm-year’s audit partners, where industry-specific experience is defined as the cumulative number of years from a partner’s first year as a signing auditor for clients in that industry. |

| PARTNER | = 1 if at least one of a client’s audit partners is an equity partner of the accounting firm and 0 otherwise. |

| INDSPEC | = 1 if the client is audited by an audit partner who is an industry specialist based on audited assets, 0 otherwise. |

| Panel B: Definitions of Variables in Additional Tests. | |

|---|---|

| DD | = Accrual estimation errors based on Dechow and Dichev (2002)’s model. |

| SP | = 1 if ROA is between 0% and 0.5% and 0 otherwise. |

| MAO | = 1 if a firm receives modified audit opinion in year t and 0 otherwise. |

| CAR [−1,+1] | = Cumulative abnormal returns over the [−1, +1] window around the earnings announcement. |

| UE | = Unexpected returns defined as the change in ROA from year t−1 to t. |

| AUAP_SAME | = 1 if the company’s audit partner has experience as an audit committee member of other companies in the same industry and 0 otherwise. |

| AUAP_DIF | = 1 if the company’s audit partner has experience as an audit committee member of other companies in a different industry and 0 otherwise. |

| AR | = Account receivables divided by total assets. |

| INV | = Inventories divided by total assets. |

| CR | = Current ratio computed as current assets divided by current liabilities. |

| DRISK | = Standard deviation of daily stock returns over 12 months during May–April. a |

| IMPAIR | = Goodwill impairments scaled by the amount of goodwill in year t−1. |

| ExpectImpair | = 1 if the book value of equity exceeds the market value of equity and 0 otherwise. |

| pre-impaired MTB | = Market value of equity scaled by the preimpairment book value of equity (book value of equity + goodwill impairment). |

| pre-impaired goodwill | = Goodwill plus any goodwill impairment scaled by total assets. |

| RET | = Monthly stock return in prior 12 months. |

| IDAP_SAME_RE | = 1 if the company’s review partner has directorship experience in the same industry and 0 otherwise. |

| IDAP_SAME_EN | = 1 if the company’s engagement partner has directorship experience in the same industry and 0 otherwise. |

| IDAP_DIF_RE | = 1 if the company’s review partner has directorship experience in a different industry and 0 otherwise. |

| IDAP_DIF_EN | = 1 if the company’s engagement partner has directorship experience in a different industry and 0 otherwise. |

| Past_IDAP_SAME | = 1 if the company’s audit partner has past directorship experience in the same industry and 0 otherwise. |

| Past_IDAP_DIF | = 1 if the company’s audit partner has past directorship experience in a different industry and 0 otherwise. |

| Current_IDAP_SAME | = 1 if the company’s audit partner has current directorship experience in the same industry and 0 otherwise. |

| Current_IDAP_DIF | = 1 if the company’s audit partner has current directorship experience in a different industry and 0 otherwise. |

The fiscal-year-end date for all Chinese companies is December 31. Chinese companies are required to publicly disclose annual reports by the end of April next year.

Acknowledgements

The authors appreciate the helpful comments and suggestions from Prof. Bharat Sarath, Prof. Linda Myers, two anonymous referees, Mr. Roy Lo and participants of the workshops at University of Macau, Hang Seng University of Hong Kong, Harbin Institute of Technology, Shenzhen and 2019 Conference in Accounting, Finance, Economics and Law held by Hong Kong Polytechnic University.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Jingjing Li acknowledges financial support from the National Natural Science Foundation of China (grant nos. 71702196 and 71772181) and Shenzhen Key Research Base of Humanities and Social Sciences (grant no. KP191001).