Abstract

This research contributes to institutional theory by examining the influence of informal institutions on formal institutions and the effects of formal institutions on inward foreign direct investment. In particular, the authors integrate prior research from multiple disciplines to identify and to examine the roles of a country’s formal regulatory, political, and economic institutions. The results suggest that the country’s informal institutions, in the form of the cultural dimensions of collectivism and future orientation, shape the country’s formal institutions. In turn, each of the three formal institutions affects the country’s level of inward foreign direct investment differently. To facilitate future research, the authors also provide a set of measures for formal institutions in 50 countries.

Keywords

Reflecting continued globalization and internationalization efforts by firms (Beinhocker, Davis, & Mendonca, 2009; United Nations Conference on Trade and Development, 2004), scholarly attention to institutions continues to surge. Recent work on institutions emphasizes their critical influence on firms’ strategies and performance (Peng, Sun, Pinkham, & Chen, 2009; Peng, Wang, & Jiang, 2008). In light of their importance, our study addresses three limitations in the broader management literature on institutions. First, work to date provides an incomplete picture of relationships between a country’s informal institutions, which reflect the collective meanings and understandings shared by its inhabitants, and the codified rules and standards that constitute its formal institutions. Second, “we have limited and fairly inconsistent knowledge of which institutions and what kinds of institution [sic] (i.e., causal factors) attract or do not attract the long-term investments of MNEs [multinational enterprises]” (Pajunen, 2008: 653). A third limitation underlies the previous two: A strikingly small number of studies examine an array of informal and formal institutions across a large number of countries over time.

This study is one of the first to theoretically explain and empirically examine how a country’s informal institutions shape its many formal institutions. Using data on 50 countries over nine years, we accomplish this objective by developing a new set of measures for three types of important formal institutions, each of which serves a different role in society. In addition, we examine the influence of the three types of formal institutions on the attractiveness of the country’s markets for investments by MNEs, as evidenced by inward foreign direct investment (FDI). By examining multiple and diverse institutions, we are able to provide insights into the types and characteristics of institutions that attract or discourage MNE investments into a country.

Our theoretical framework integrates management research on institutional theory with insights from two adjacent disciplines: organizational institutionalism (from sociology) and institutional economics (from economics). Organizational institutionalism focuses on the processes through which a society’s collective actions and values shape the development and maintenance of the society’s institutions (e.g., Powell, 1991; Tolbert & Zucker, 1996). Complementing this approach, research in institutional economics emphasizes the implications of institutions for important outcomes such as investment behavior, the functioning of markets, and wealth generation (e.g., Levine & Renelt, 1992; Whitley, 1992). At the intersection of these fields, research in management subdisciplines (e.g., international management and strategic management) explores how institutions affect managers’ decisions (Hoskisson, Hitt, Wan, & Yiu, 1999; Rumelt, Schendel, & Teece, 1991).

Conceptual (Redding, 2005; Reed, 1996) and qualitative (Collin, 1998; Greif, 1994) research suggests that a country’s informal institutions, which are reflected in its culture, influence the evolution of its formal institutions. However, empirical investigations of this relationship have generally examined a small number of countries (i.e., two to four; Witt & Redding, 2009) or have focused on a single attribute of formal institutions (e.g., Salter & Niswander, 1995). In turn, there are questions about the extent to which such research is generalizable both to different institutions and to a broader spectrum of countries. Likewise, identifying a possible source of inconsistent research findings linking institutions and FDI, Redding (2005) and Jackson and Deeg (2008) argued that a vast majority of studies examine the linkage between formal institutions and FDI using a small number of indicators or even just one. However, institutional environments are multidimensional, complex, and polycentric, and the various institutions are interdependent (e.g., North, 1990; Ostrom, 2005; Scott, 1995). Thus, we can understand the true effects of such environments only by simultaneously examining multiple institutions.

Accordingly, our study makes three contributions to the management literature. First, we synthesize theory and research from adjacent disciplines to identify three types of formal institutions, describe the roles they play in society, and develop measures of them. Second, we link the countries’ informal institutions, as reflected in the culture, to these three types of formal institutions. Third, we establish the consequences of each formal institution for the country’s receipt of FDI. In short, the measures and theory we provide may improve scholars’ understanding of the roles that different institutions serve, the forces that shape them individually, and their distinct implications. Furthermore, this work should serve as a foundation for future research into firm strategies and their implications for performance.

Conceptual Development

Informal Institutions and Formal Institutions

Informal institutions are enduring systems of shared meanings and collective understandings that, while not codified into documented rules and standards, reflect a socially constructed reality that shapes cohesion and coordination among individuals in a society (Scott, 2005). Representing shared values and noncodified standards, culture is an important reflection of a country’s informal institutions (North, 1990; Peng et al., 2008). A country’s culture constitutes “created and learned standards for perception, cognition, judgment, or behavior shared by members of a certain group” (Fu et al., 2004: 288). Embedded in a nation’s heritage (Greif, 1994), culture is durable, long-lasting, and relatively stable, with incremental changes occurring slowly (Brett, Tinsley, Janssens, Barsness, & Lytle, 1997; McGrath, MacMillan, Yang, & Tsai, 1992; Reed, 1996). Culture embodies societal members’ norms and values by defining, for example, what actions are considered ethical, acceptable, and desirable (Reed, 1996) and by facilitating a shared understanding of such expectations (Tsui, Nifadkar, & Ou, 2007). Although the culture is tacitly understood by societal members, this knowledge is largely acquired through socialization processes (Greif, 1994).

Formal institutions represent structures of codified and explicit rules and standards that shape interaction among societal members (North, 1990). They promote order and stability by providing authoritative behavioral guidelines and enabling the formation of expectations regarding behavior (Scott, 1995). Although informal institutions change incrementally as culture is transmitted from one generation to the next (Rohner, 1984), formal institutions are more malleable in that they are a product of human agency (DiMaggio, 1988). Formal institutions begin as solutions to problems in society. These solutions diffuse until they crystallize into established rules and standards that influence subsequent behaviors (Tolbert & Zucker, 1996). As individuals in society conform to these rules and standards and they become taken for granted and routinized, they are reproduced in subsequent time periods (Powell, 1991), and the society recognizes and accepts them as formal institutions (Witt & Redding, 2009). Thus, as DiMaggio (1988) argued, formal institutions reflect the motivation and collective actions of societal members seeking to solve problems that obstruct the ability to achieve goals deemed to be important. Understanding formal institutions, therefore, requires understanding the logic and rationale underlying the solutions societal members develop (Scott, 2005), and this logic and rationale are embodied in the society’s informal institutions (North, 1990).

Although formal institutions are relatively stable once established, they are based on the shared cognitive understandings and acceptance of individuals in the society, both of which evolve and produce change (Zucker, 1987). Thus, scholars have suggested that a driving force in their development and maintenance is the society’s culture (Jackson & Deeg, 2008; Redding, 2005; Reed, 1996). Specifically, culture reflects and further influences the beliefs (Schooler, 1996), values (Hofstede, 1980), norms and priorities (Sirmon & Lane, 2004), and assumptions (Huang & Harris, 1973) that are broadly shared by individuals in a society and that “underpin [its] formal institutions” (Redding, 2005: 123). In this sense, culture “represents the tool kit” from which individuals select and institute solutions to the problems the society confronts (DiMaggio & Powell, 1991: 28). To form and persist, however, the formal institutions must be perceived by a critical mass of people in society to be efficacious solutions to its problems (Tolbert & Zucker, 1996). When the formal institutions no longer provide acceptable solutions, individuals seek new solutions that fit the evolving social context of the society (Powell, 1991).

Cultural influences provide a foundation that shapes how a country’s people view the world (Chui, Lloyd, & Kwok, 2002), determines how they make sense of events occurring in that world (Witt & Redding, 2009), and helps them interpret the explanations offered by others (Zilber, 2006). In turn, culture serves as a base for the development of formal institutions by influencing what problems are identified, their perceived importance (Schwartz, 1999), the generation of potential solutions for them (Reed, 1996), the evaluation of such solutions (Zilber, 2006), and the behaviors enacted to implement the solutions (Prasad & Elmes, 2005). Behaviors consistent with the culture are likely to be evaluated efficaciously (Fu et al., 2004). Therefore, culture is expressed through the resulting formal institutions (Redding, 2005). Through this process, formal institutions reflect, embody, and reinforce the country’s culture across the population (Inglehart & Baker, 2000). By serving as a basis of formal institutions, culture thus leads to stable and systematic differences across countries (Greif, 1994; Hofstede, 1980). In this way, “[h]istory matters. It matters not just because we can learn from the past, but because the present and the future are connected to the past by the continuity of a society’s institutions” (North, 1990: vii).

Market exchanges are the cornerstone of economic activity and are inherently social in that actors who have competing interests must transact with one another (Granovetter, 1985). Because formal institutions define what is acceptable and discipline nonconforming behavior, they allow individuals to form expectations about the actions and commitments of exchange partners, enable equilibrium practices to emerge (Greif, 1994), and support the conduct of exchanges (Redding, 2005). Thus, the presence of legitimate and recognized institutions to define and oversee business behavior is critical for long-term wealth creation (Kostova & Zaheer, 1999). In this respect, institutions not only impose constraints but also provide opportunities (Boddewyn, 1988; Oliver, 1997).

Institutions Critical to Managers

Countries’ institutional environments are complex and are composed of several formal institutions. Three types of formal institutions most likely to be important to managers include regulatory, political, and economic institutions. As a whole, these three types of formal institutions constitute and define an established order within which businesses operate. Reflecting the notion that “institutions are commonly state-linked” (Zucker, 1987: 446), each institution is enacted primarily by the activities of governments, based on their sovereign authority to devise legal and control systems that establish rules, monitor adherence to these rules, and discipline nonconformity (Covaleski & Dirsmith, 1988). The different types of formal institutions are identifiable by the societal functions to which certain laws and governmental oversight apply.

First, an important responsibility of government is to regulate the activities of domestic and foreign organizations operating within a country. Regulatory institutions establish rules intended to reduce uncertainty about the activities of organizations by standardizing practices and demanding conformance. Although the scope and content of regulations vary, they codify society’s expectations and preferences regarding the power and autonomy of organizations (North, 1991; Scott, 1995). For example, such regulatory institutions enact and enforce laws to protect property rights and restrict the activities of foreign organizations (Bekaert, Harvey, & Lundblad, 2005; Spicer, McDermott, & Kogut, 2000).

Second, governments establish rules and standards that define the nature of the political process (Hillman & Keim, 1995), including how power is distributed within government (Henisz, 2000), which individuals are allowed to participate in it, and how such rights are exercised (Persson, 2002). The resulting political institutions constitute the rules and standards through which governments and citizens establish new formal institutions and alter existing ones, a critical function that affects the stability of the institutional environment and the predictability of changes in that environment (DiMaggio & Powell, 1991). Political institutions embody a collection of arrangements. Broadly, they range from autocratic institutions that concentrate power in the hands of a few individuals and discourage the involvement of other citizens, on one hand, to democratic institutions that distribute power among multiple individuals and encourage active participation by all citizens, on the other (de Mesquita & Siverson, 1995; Fearon, 1994; Ross, 2001).

Third, some formal institutions embody the rules and standards that shape the availability and value of the society’s financial resources, which in turn support capital investments. These economic institutions are evident in a country’s monetary and fiscal policies (e.g., Fischer, 1993; Lucas, 2003). In turn, such “financial factors are an integral part of [a country’s] growth process” (Levine & Zervos, 1998: 554).

Two cultural dimensions especially likely to influence regulatory, political, and economic institutions are collectivism and future orientation. Collectivism reflects the extent to which a country’s inhabitants value membership in integrated, cohesive social units and place priority on the interests of these units. In contrast, individualistic societies tend to value and give priority to the independent and autonomous person. Government policies result from multiple and often conflicting interests among different groups of citizens, politicians, and organizations (Persson, 2002). The resulting regulatory and political institutions depend on how the society prioritizes the rights of individuals, their participation in government, the distribution of resources, and other civic concerns (Oates, 1999). Collectivism shapes how institutions promote or suppress the interests of specific organizations or individuals relative to the interests of society as a whole (Gelfand, Bhawuk, Nishii, & Bechtold, 2004; Triandis, 1995). Thus, the degree of a society’s emphasis on collective interests versus individual interests likely influences the characteristics of regulatory and political institutions.

Future orientation reflects the extent to which long-term outcomes are emphasized over short-term ones such that planning and investing are directed toward long-term gratification and results (Ashkanasy, Gupta, Mayfield, & Trevor-Roberts, 2004; Brodbeck, Frese, & Javidan, 2002). Capital accumulates as individuals and organizations forgo current spending by, for example, electing to save. This tendency is partially dependent on social norms prevalent in a society (Cole, Mailath, & Postlewaite, 1992), including those related to delayed versus immediate gratification (Hofstede & Bond, 1988). In turn, the accumulated capital provides a means to invest in long-term growth opportunities (e.g., Feldstein, 1983). Therefore, future orientation may influence both the demand for and the supply of capital, thereby shaping the characteristics of the economic institutions that manage that capital.

Hypotheses

Collectivism and Regulatory Institutions

As “the preeminent collective actor” in many societies (Zucker, 1987: 455), organizations play a pivotal role in outcomes such as wealth generation and dispersion, leisure, social status, and the use of resources. Partly because of this influence, regulatory institutions exist to define and enforce guidelines to control the activities of organizations conducting business in a country (Busenitz, Gomez, & Spencer, 2000). Government officials communicate their priorities and objectives through both actions and inactions by, for example, enacting rules to oversee some activities while not interfering with others (Hillman & Keim, 1995). In this way, government officials also use regulatory institutions to exert control over some of the country’s resources (Guthrie, 2006).

Collectivism can facilitate the development of regulatory institutions that tightly control the activities of organizations operating within a country. Collectivist societies often value adherence to social norms and attempt to standardize behavior to ensure adherence to such norms (Greif, 1994; Newburry & Yakova, 2006). A considerable amount of research suggests that individuals in collectivist societies often govern business activities by invoking formal rules and emphasizing authority (e.g., Earley & Gibson, 1998; P. B. Smith, Peterson, & Wang, 1996). For example, Salter and Niswander (1995) found that collectivism encourages the development of well-defined and strict financial reporting rules for organizations.

Concern for the well-being of others is also important to collectivists (Morris, Avila, & Allen, 1993), and goodwill and cooperation among societal members is thus expected (Huff & Kelley, 2003). Despite the desire for social harmony, in-groups and out-groups are often salient in collectivist societies (Triandis, 1995). People sometimes take actions against the interests of out-groups, especially when such behavior benefits the in-group (Chen, Peng, & Saparito, 2002). A by-product of this social dynamic can be popular support for strong regulatory institutions that tightly control the behavior of all organizations, thereby promoting trust and cohesion among the disparate entities (e.g., Knack & Keefer, 1997). Such regulatory institutions help provide order, stability, and reliability in social interactions while disciplining nonconformity (Greif, 1994; P. B. Smith, Dugan, Peterson, & Leung, 1998). Tinsley (1998, 2001), for example, found evidence that collectivists prefer to rely on regulations for resolution of conflicting interests in economic exchange.

Conversely, given their focus on pursuing self-interest, individualists largely eschew the involvement of authority figures in their affairs (P. B. Smith et al., 1996). They value independence and personal accomplishment over group interests (Newburry & Yakova, 2006), favor autonomy over dependence on the collective (Spence, 1985), and prefer variety to standardization (Mueller & Thomas, 2001). Thus, individualists may be reluctant to accept and support strict regulatory institutions, as they discourage the unilateral pursuit of self-interests. Therefore, we expect that societies with collectivist cultures will promote stronger regulatory institutions than will those with individualistic cultures. These arguments lead to the following hypothesis.

Hypothesis 1: Collectivism is positively related to the control that regulatory institutions exercise over organizations’ activities.

Collectivism and Political Institutions

“[R]ooted heavily in national culture” (Hillman & Hitt, 1999: 830), political institutions help shape future institutional changes (Powell, 1991). Specifically, they provide a framework that affects the development and alteration of other institutions by influencing societal members’ perceptions of the changes that are possible, the extent to which these changes are needed, and how they are to be enacted (DiMaggio, 1988). Political institutions also distribute power within a society (DiMaggio & Powell, 1991; Henisz, 2000) while inevitably representing the interests of powerful individuals (Scott, 1995; Zinn, 2003). Electoral laws, legislative rules, and the content of legislation define the power not only of politicians but also of individual citizens (Persson, 2002; A. Smith, 1937). For example, by establishing the laws that define political rights and civil liberties, political institutions delineate how and to what extent citizens can actively participate in institution building (Matten & Crane, 2005).

In individualistic societies, the person is considered the primary and most important social unit (Hui, 1988). Rather than valuing submission to the state, individualists tend to favor “autonomy, independence, and freedom” (Shane, 1993: 59). Thus, relative to collectivist societies, individualist societies often place greater emphasis on opportunities for individuals to participate in the political process. Indeed, Gelfand, Triandis, and Chan (1996) found that individualistic values are largely at odds with autocratic political institutions that subjugate individual interests and demand high levels of acquiescence and submission to the state.

Conversely, the need for heavy involvement by individual citizens in political processes is partly inconsistent with the communal nature of collectivist societies. Relative to individualistic societies, collectivist societies emphasize community over individual interests (Chen et al., 2002). In addition, collectivists are more likely to view others’ motives and intentions as benevolent (Huff & Kelley, 2003), to acquiesce to authority figures (Morris & Leung, 2000), and to accept monitoring and sanctioning to ensure conformance to group norms (Yamagishi, Cook, & Watabe, 1998). Likewise, “individual initiative is not highly valued and deviance in opinion or behavior is typically punished” in many aspects of collectivist societies (Mueller & Thomas, 2001: 59). These conditions, together with the partially fragmented nature of most collectivist societies (Greif, 1994), often reduce the strength of organized opposition to established political leaders, thereby providing them discretion to solidify and concentrate power (Persson, 2002). Thus, democratic political institutions may be less common in collectivist societies and more common in societies with a strong individualistic culture. This reasoning leads to the following hypothesis.

Hypothesis 2: Collectivism is negatively related to democratic political institutions.

Future Orientation and Economic Institutions

Future-oriented societies prioritize long-term outcomes such as economic growth and development. Individuals and organizations in these societies value opportunities to make the capital investments necessary to facilitate such outcomes (Brodbeck et al., 2002). These investments are costly and forward-looking by nature (e.g., Guthrie, 2006), and a ready supply of capital is often necessary to fund them (T. Beck, Demirguc-Kunt, & Peria, 2007). A country’s economic institutions shape the incentives and abilities of financial intermediaries (e.g., banks) to make the capital available, thereby influencing the capital investments of individuals and organizations (Levine, Loayza, & Beck, 2000). Specifically, governments can influence capital investments through monetary mechanisms, fiscal mechanisms, or both. Monetary mechanisms involve alterations of the money supply through, for example, the policies of central banks and the control of interest rates (Bernanke & Reinhart, 2004). Fiscal mechanisms include annual surpluses and deficits in government budgets (Fischer, 1993). Using these tools, governments can influence the supply of and the demand for capital.

Economic institutions can encourage capital investments by increasing the capital available to individuals and organizations. In particular, they must maintain an adequate money supply to ensure the availability of the capital necessary to fund investments. When the money supply is high, interest rates naturally decline (Gali, 1992). In turn, declining interest rates reduce the cost of accessing capital (i.e., the interest rate) and increase the opportunity costs of keeping capital in cash form, thereby encouraging investment (Romer, 1992). The propensity of individuals in a society to value and respond to such investment incentives partially depends on the extent to which the societal values emphasize long-term outcomes (e.g., Cole et al., 1992; Hofstede & Bond, 1988).

Beyond these monetary considerations, the future orientation of a society may also be evident in the country’s fiscal policies. When capital availability declines (e.g., due to an economic downturn), future-oriented societies are likely to value short-term government deficits. Deficits enable governments to offset capital shortages by infusing more money into the private sector than they remove through taxation. Reduced taxation also enables individuals and organizations to retain and possibly reinvest more of their investment returns, thereby increasing capital availability further (e.g., Boskin, 1978). Governments often must borrow to cover the budget shortfall. When they borrow domestically (i.e., from local individuals and organizations), they use some of the capital allocated to the private sector (Feldstein, 1983; Fischer, 1993). However, through subsequent payouts to domestic entities, governments facilitate a steady supply of liquidity in the market (e.g., Holmstrom & Tirole, 1998). In addition, governments sometimes finance deficits with foreign borrowing (Edwards, 1984). Future-oriented societies are likely to value economic institutions that promote such fiscal policies because they facilitate capital investments by ensuring that individuals and organizations have access to the financial resources needed to fund such investments. These arguments suggest the following hypothesis.

Hypothesis 3: Future orientation is positively related to economic institutions promoting capital investments by domestic entities.

Having examined the influence of informal institutions on formal institutions, we now turn to a discussion of how the formal institutions influence countries’ inward FDI, which reflects the attractiveness of the country’s institutional environments to the managers of MNEs (Pajunen, 2008).

Regulatory Institutions and Inward FDI

MNE managers have discretion in allocating their organizations’ resources. FDI decisions reflect their evaluation of opportunities available in a country’s markets and the support and limitations posed by the country’s institutional environment (Pajunen, 2008). Often, MNE managers value economic growth in a country because it enhances the likelihood that MNEs will earn acceptable returns on invested capital. Governments can enact policies that facilitate economic growth, such as providing and promoting public goods and creating laws to protect private property. Thus, some government actions can promote a positive environment for foreign investments. However, many regulations create an environment that discourages foreign investments. In particular, government policies often lead to inefficient use of financial resources (e.g., to satisfy special interests) and can distort private incentives through taxes and targeted regulations that create inefficiencies (Browning, 1976; Levine & Renelt, 1992). Taxes on certain value-adding activities, for example, can lead businesses and individuals to engage in fewer such activities and/or to move them to locations where taxation is more favorable (e.g., Ballard, Shoven, & Whalley, 1985; Oates, 1999; Trostel, 1993). Furthermore, regulatory institutions sometimes impose undue costs, are ineffective, or are counterproductive. When they produce such outcomes, they are unlikely to improve a country’s economy (Collin, 1998; Hill, 1995). Thus, the impacts of regulatory institutions vary depending on the laws and policies enacted and enforced and on the way firms respond (Hennart, 1989; Williamson, 1991).

Prior research suggests that managers seek to invest in countries with institutional environments that allow MNEs to leverage their firm-specific advantages and access local resources (e.g., human capital; Dunning, 1998; Loree & Guisinger, 1995). Government intervention in the affairs of organizations introduces direct compliance costs as well as indirect costs associated with distorted incentives (Guthrie, 2006; Tirole, 2003). For example, government interventions such as wage and price controls limit MNEs’ flexibility and increase their exposure to unfavorable market conditions. Likewise, many governments restrict foreign ownership levels, thereby disallowing the use of wholly owned subsidiaries by foreign firms and limiting the willingness of MNE managers to locate certain activities in the country (Hennart, 1989). Such regulations can reduce domestic firms’ exposure to foreign markets and innovations and restrict the product and service options available to consumers. In turn, the diminished involvement in international commerce can limit economic growth (Levine & Renelt, 1992; Moran, 2000). As a result, MNE managers typically value institutional environments that promote free and open markets (Globerman & Shapiro, 2003).

Because governments can maintain power without foreign managers’ support, regulatory institutions largely favor local firm interests over foreign firm interests (Boddewyn, 1988). When regulatory institutions are designed to provide governments with greater discretionary control, MNEs are subjected to enhanced moral hazard by these institutions, especially after MNE investments have been made (Teece, 1986a). Thus, managers try to avoid large resource commitments when regulatory institutions are overly strong and unfriendly (Delios & Beamish, 1999).

Regulations also impose costs on local organizations. The costs invoked by tight regulations alter incentives and reduce employer flexibility (Saint-Paul, 2002), perhaps stifling the development and availability of human capital and reducing the country’s attractiveness to MNEs. In addition, tight regulations impose costs on entrepreneurs, thus reducing their incentives and ability to innovate (Begley, Tan, & Schoch, 2005; Zapalska & Edwards, 2001) and depriving the local market of important knowledge resources sought by many foreign investors (Almeida, 1996; Feinberg & Gupta, 2004). Conversely, regulatory institutions promoting a more friendly business environment are likely to attract FDI (Globerman & Shapiro, 2003). These arguments underlie the following hypothesis.

Hypothesis 4: Regulatory institutions exercising greater control over organizations’ activities are negatively related to inward FDI.

Political Institutions and Inward FDI

MNE managers often seek to encourage government officials to enact policies in the interests of the MNE (Vernon, 1971). Political institutions provide an avenue through which MNE managers can influence officials’ decisions and receive fair or even preferential treatment (Boddewyn, 1988; Hillman & Hitt, 1999). As a result, MNE managers often work to establish desirable relationships with local government officials (Luo, 2001).

Perhaps because government officials operating in democratic systems rely on popular support, which is more common when the economy is strong, relations between businesses and governments in these systems are often more friendly than in autocratic systems (Hillman & Keim, 1995). In addition, democratic political systems are generally more transparent, in part because of the large number of influential and informed stakeholders. Foreign firm managers often value such transparency because it reduces uncertainty, enables them to identify and conform to government demands and priorities, and improves their ability to engage government officials (e.g., Orr & Scott, 2008). Moreover, a likely by-product of institutions promoting the interests of individual citizens and encouraging their participation in government is more active participation in the labor market, thereby increasing the number and skills of available workers (Edelman, 1990; Sutton, Dobbin, Meyer, & Scott, 1994).

Conversely, concentration of authority in a few individuals enables government officials to be more self-serving and to manipulate institutions for personal gain, particularly when there are minimal checks and balances. Such conditions may create inefficiencies (Persson, 2002), erect barriers to entrepreneurship and innovation (Bowen & De Clercq, 2008), and reflect elevated government consumption of a country’s resources (Ross, 2001). In turn, the managers of MNEs are likely to limit investments in countries with autocratic political institutions.

Autocratic political institutions also facilitate instability and unpredictability in the institutional environment because policy is subject to the whims of a small number of individuals (Henisz, 2000) and often produces institutional voids (Puffer, McCarthy, & Boisot, 2010). In addition, whereas democratic political institutions provide opportunities to influence government officials through interest groups, elections, and lobbying (Hillman, Keim, & Schuler, 2004), revolution may be the primary option available to enact changes when political institutions are autocratic. MNE managers expect to experience uncertainty when investing abroad (Zaheer, 1995), but instability in the institutional environment exacerbates this uncertainty (Henisz & Delios, 2001). In particular, instability complicates managers’ efforts to leverage MNEs’ assets (Teece, 1986a), hampers learning (Newman, 2000), and limits the reliability and consistency of economic forecasts (Andersen, Bollerslev, Diebold, & Vega, 2003). Therefore, whereas stability in political institutions can contribute to economic growth (Temple, 1999) and may attract foreign investments (Busse & Hefeker, 2007), the potential instability associated with nondemocratic political regimes may contribute to lower foreign investment (Chan & Makino, 2007; Delios & Henisz, 2003). In turn, we suggest the following hypothesis.

Hypothesis 5: Democratic political institutions are positively related to inward FDI.

Economic Institutions and Inward FDI

Although local individuals and domestic organizations often finance investments primarily using local sources, foreign MNEs also have access to capital from their home markets. In fact, they often rely on financial intermediaries in their home markets to fund entry into foreign countries (Klein, Peek, & Rosengren, 2002). Nonetheless, the monetary and fiscal policies that promote capital availability for domestic investors inevitably influence foreign MNEs even when such policies are not primarily directed at these firms (Tirole, 2003).

Monetary policies that persistently protect domestic investors’ access to capital may generate other consequences that are unattractive to MNE managers. Maintaining high money supplies and maintaining low interest rates create conditions that devalue a country’s currency (Burdekin & Weidenmier, 2001; Romer & Romer, 2000). Although “depreciation of the domestic currency increases the relative wealth of foreign firms, enabling them to outbid domestic firms in acquiring corporate assets” (Klein et al., 2002: 664; Froot & Stein, 1991), such inflation may also increase the requirements for satisfactory returns and reduce the value of repatriated profits. Often, MNEs must mitigate such concerns through hedging and pricing adjustments, both of which increase the complexity and uncertainty associated with FDI (e.g., Bartram, Brown, & Minton, 2010; Lessard & Zaheer, 1996; Sundaram & Black, 1992). Therefore, the potential for currency devaluation often discourages MNEs from entering foreign markets (Woodward & Rolfe, 1993).

In addition, fiscal policies that promote capital investments by ensuring capital availability for domestic entities may have consequences that reduce the country’s attractiveness to foreign MNEs. In particular, governments using fiscal policies to provide capital for domestic entities may lack the funds to provide financial incentives to entice FDI from MNEs. For example, the frequent use of budget deficits raises the costs of borrowing and limits the government’s subsequent flexibility (e.g., English, 1996; Oates, 1999). Likewise, using deficits generally increases governments’ default risk and illiquidity, especially if they rely heavily on foreign borrowing (Edwards, 1984). Foreign borrowing also reduces governments’ incentives to invest in the private sector because some of the benefits are appropriated by the foreign investors providing the capital (Sachs, 1989). Indeed, using deficits and foreign borrowing to promote capital availability for domestic entities sometimes provides incentives for governments to behave opportunistically toward MNEs by, for example, altering policies that attracted MNEs after they have made investments (e.g., Teece, 1986b; Tirole, 2003). Moreover, the use of certain types of domestic bonds to promote capital investments can commit governments to issue payouts when they are no longer needed, perhaps producing too much liquidity in subsequent time periods (Holmstrom & Tirole, 1998). Thus, economic institutions that prioritize capital investment by domestic entities may in turn reduce the country’s receipt of FDI, thereby leading to the following hypothesis.

Hypothesis 6: Economic institutions promoting capital investments by domestic entities are negatively related to inward FDI.

Method

Sample

To examine the influences on and implications of institutional environments, we collected and analyzed data on 50 countries. These 50 countries (listed in Table 1) were chosen because they are geographically and economically heterogeneous. Of these countries, 21 were located in Europe, 15 in Asia, 9 in North, South, or Central America, 3 in Africa, and 2 on the continent of Australia, providing an institutionally and culturally diverse sample. In addition to developed economy countries, our sample also includes a number of large emerging economy countries, such as Brazil, Russia, India, and China (collectively known as the BRIC countries; O’Neill, 2001), and some smaller developing economy countries, including Nigeria, Slovenia, and Romania. In total, we have 450 country-year observations (i.e., nine years of data). Because of the limited number of observations, deletion of cases due to missing values for primary variables would dramatically reduce the useable cases for the factor and regression analyses, leading to low power and biased parameter estimates (Allison, 2001). Therefore, we used maximum likelihood estimates to iteratively impute missing values for the data because this technique is more accurate than mean substitution or case deletion methods (Schafer & Graham, 2002). All measures exist at the country level.

Sampled Countries

Measures

Inward FDI

Inward FDI (measured as FDI inflows) was collected from the World Bank’s World Development Indicators (WDI; World Bank, 2004). Inward FDI represents capital investments in a country from organizations located in other countries. This investment takes the form of manufacturing facilities, research and development centers, joint ventures, and so on. Such entities may be owned partially or entirely by the investing organization. We measured our institutional variables at time t, and we utilized inward FDI at time t+1.

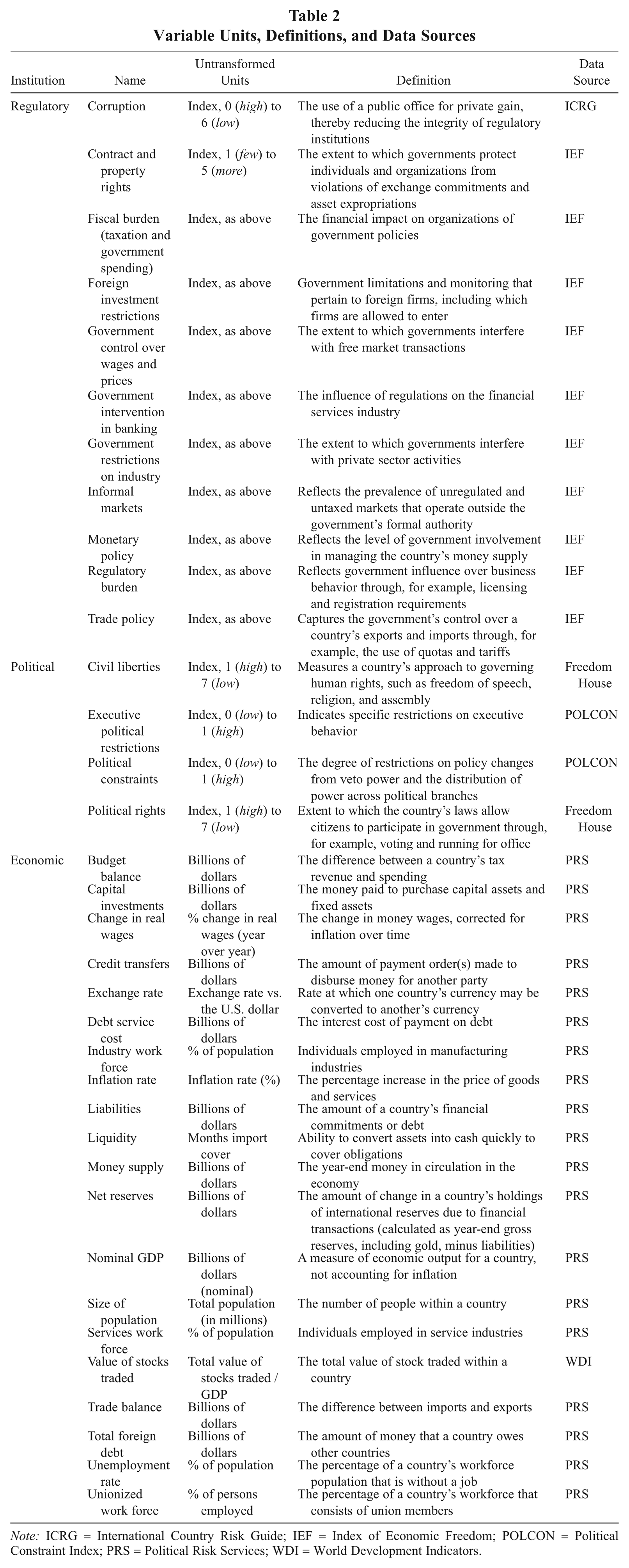

Formal institutions

Formal institutions served as both dependent variables (Hypotheses 1–3) and independent variables (Hypotheses 4–6). We utilized a number of data sets as sources for the data on formal institutions: Euromonitor International, Index of Economic Freedom (IEF; Gwartney, Lawson, & Block, 1996), Freedom House’s annual survey of political rights and civil liberties, the Political Constraint Index (POLCON) data set (Henisz, 2000), International Country Risk Guide (ICRG), Political Risk Services (PRS), and the World Bank’s WDI. 1 Using these sources, we constructed an extensive data set of institutional measures. We performed a principal components analysis, an appropriate data reduction technique, to reduce this large number of measures to a set of representative indicators (Conway & Huffcutt, 2003; Pedhazur & Schmelkin, 1991). Table 2 contains the large set of variables (organized by the formal institution on which we expected them to load), their units of measurement, definitions, and data sources. Below, we describe the 20 variables that loaded on the regulatory, political, and economic institutions factors.

Variable Units, Definitions, and Data Sources

Note: ICRG = International Country Risk Guide; IEF = Index of Economic Freedom; POLCON = Political Constraint Index; PRS = Political Risk Services; WDI = World Development Indicators.

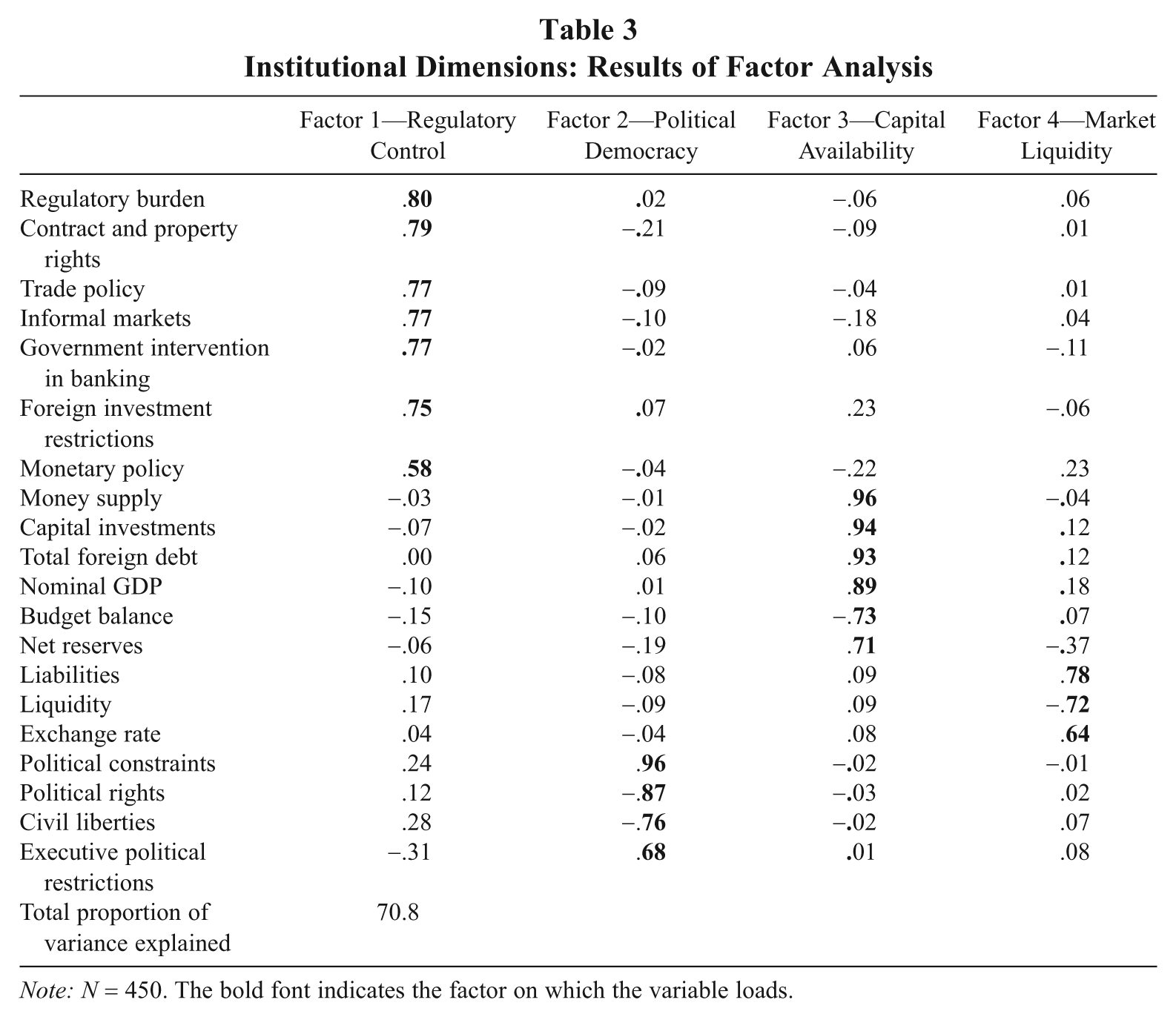

In the principal components analysis, the factors were extracted using the following three criteria: (a) Kaiser’s (1956) criterion rule specifying the use of factors with unrotated eigenvalues greater than one, (b) the scree test (Cattell, 1966), and (c) conceptual interpretation of the factors (Tabachnick & Fidell, 2001). Scholars have utilized several rotation methods, broadly categorized as orthogonal and oblique (Fabrigar, Wegener, MacCallum, & Strahan, 1999). Although orthogonal rotations (e.g., varimax) do not allow factors to be correlated, oblique rotations (e.g., oblimin) permit correlated factors. Thus, oblique rotation is appropriate when there are theoretical reasons to expect that the optimal factor structures are correlated (Fabrigar et al., 1999). A country’s institutions generally share common variance and are interdependent (Jackson & Deeg, 2008; Whitley, 1992). 2 Therefore, oblique rotation was used.

Using the Kaiser criterion, five factors were selected. However, this rule sometimes leads to overextraction (Fabrigar et al., 1999; Floyd & Widaman, 1995). Therefore, we also used the scree test to identify the last substantial reduction in the magnitude of eigenvalues. Evaluation of the scree plot indicated that the reduction occurred between four and five factors, thereby providing support for a four-factor solution. Items were excluded when they had high cross-loadings (greater than ± 0.4) on more than one factor. After items were deleted, the initial solution was recalculated to ensure the appropriate number of factors.

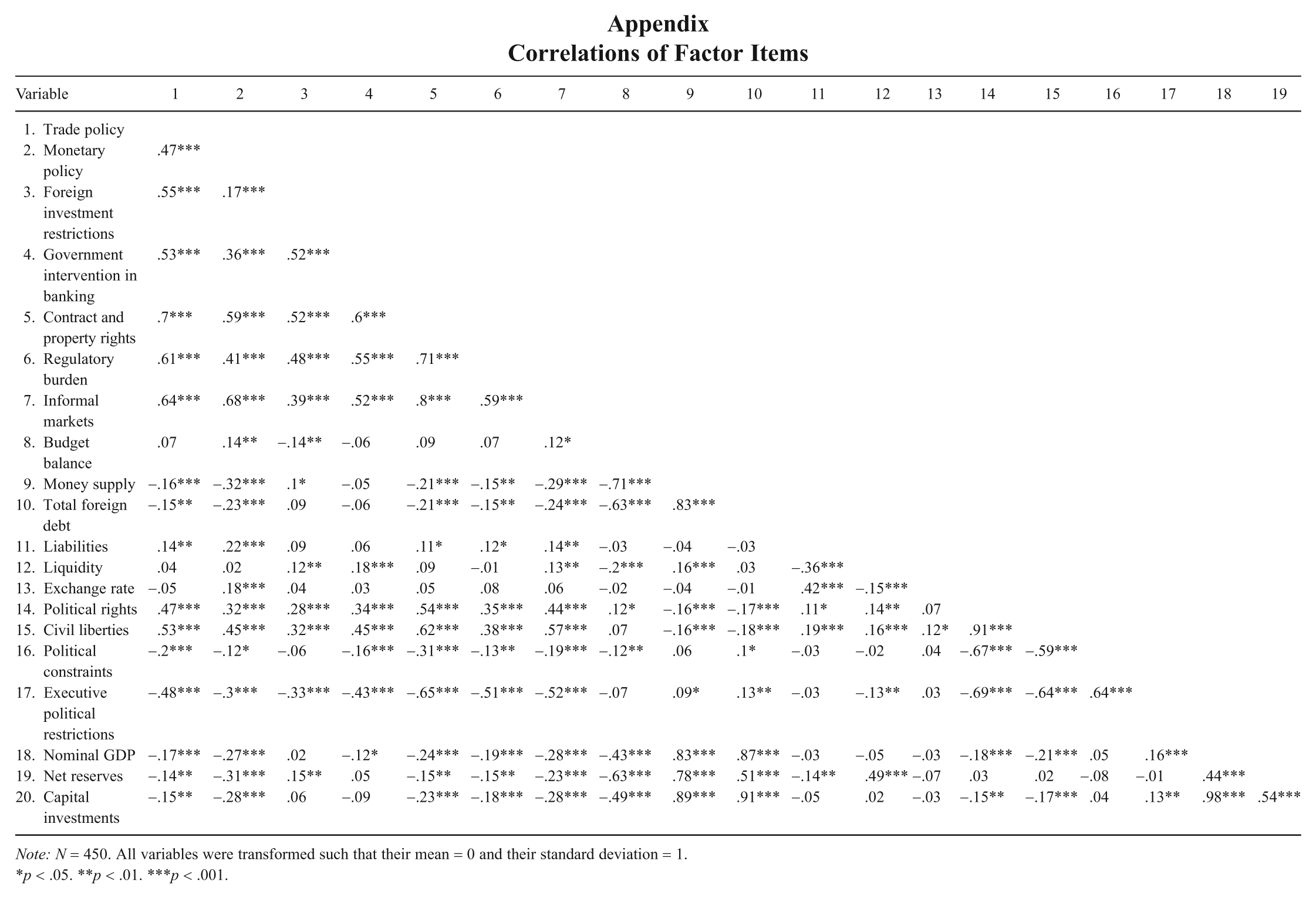

Table 3 shows the results of the final four-factor solution. Overall, 20 variables exhibited a simple structure, wherein they have high loadings on only one factor (Tabachnick & Fidell, 2001). The bivariate correlations of the variables loading on the factors are presented in the appendix. To assess the stability of our institutional factors over time, we conducted the factor analysis a second time after dividing the data into two time periods (1995–1999 and 2000–2003). The results showed that the factors were stable in the composition and magnitude of factor scores. These four factors explain about 70.8% of the total variation in the items. Correlations among these factors are shown in Table 4. Thus, empirically, this factor solution is a sound representation of the individual variables, and the factors relate well to the institutions predicted by the theory.

Institutional Dimensions: Results of Factor Analysis

Note: N = 450. The bold font indicates the factor on which the variable loads.

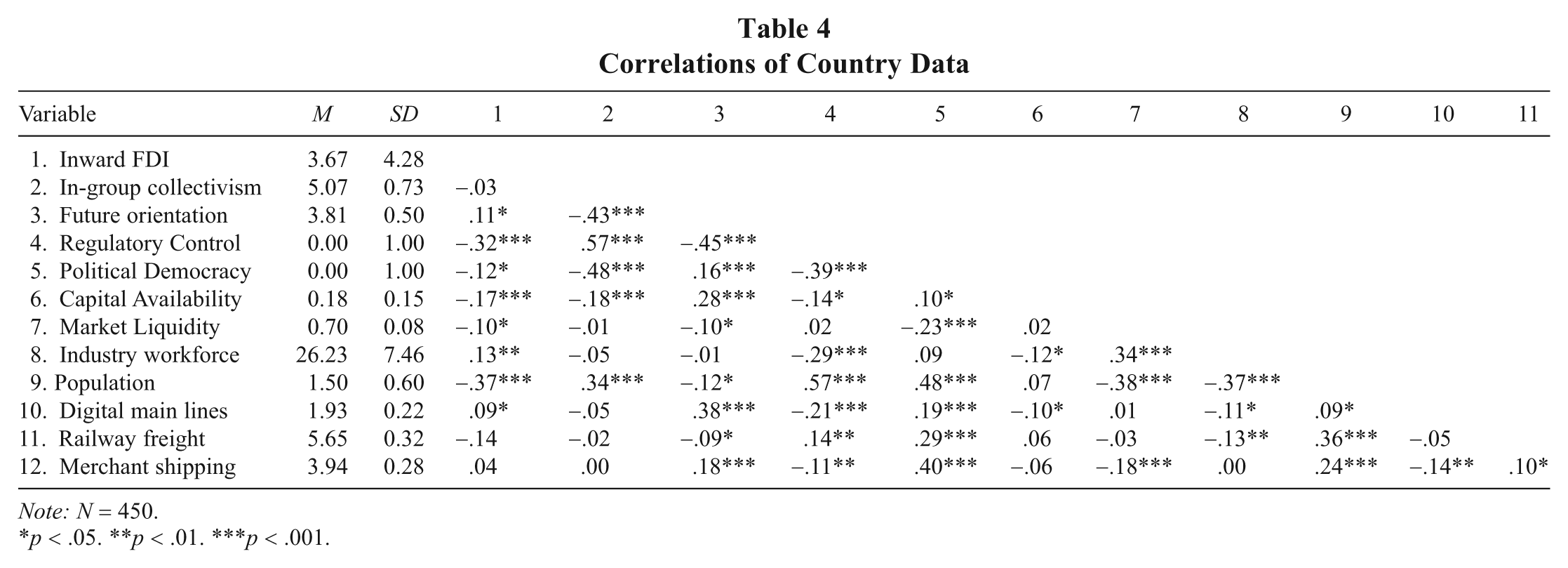

Correlations of Country Data

Note: N = 450.

p < .05. **p < .01. ***p < .001.

Regulatory institutions

Regulatory institutions establish and enforce laws and policies that govern business activities. Seven items loaded on the first factor, which represents regulatory institutions. This factor reflects several ways governments exercise control over organizations. Consistent with expectations, regulatory burden, trade policy, contract and property rights, foreign investments restrictions, government intervention in banking, monetary policy, and informal markets all have positive loadings, indicative of greater involvement by government in the affairs of organizations. We refer to this factor as Regulatory Control and use it in the tests of Hypotheses 1 and 4.

Political institutions

The second factor, political institutions, reflects the means through which government officials and other individuals enact changes in institutions. As expected, both political constraints and executive political restrictions load positively on this factor, and both civil liberties and political rights load negatively (both of the latter two variables are reverse scored). The resulting combination of variables and their loadings on this factor suggest that political institutions concentrating more authority in a few government branches and officials are also associated with fewer civil liberties and political rights. Thus, high scores on this variable indicate more democratic political systems and low scores indicate more autocratic systems. We name this factor Political Democracy, and we use it in tests of Hypotheses 2 and 5.

Economic institutions

Economic institutions influence the capital investment decisions of individuals and organizations by affecting both their access to capital and its value. Although we anticipated a single economic institutions construct, Factors 3 and 4 both reflect the country’s management of its capital resources. Capital investments, money supply, net reserves, and total foreign debt, all of which reflect the availability of capital in an economy, load positively on the third factor. In addition, nominal GDP loads positively, suggesting that there is often more capital available in larger economies, and budget balance loads negatively. The negative loading implies that budget deficits provide short-term infusions of capital into the economy. Thus, this factor reflects the availability of capital for domestic entities. We refer to this factor as Capital Availability.

On the fourth factor, liabilities and exchange rate load positively and liquidity loads negatively. High liabilities reflect the debt of domestic entities held by foreign financial institutions. In turn, these liabilities reduce the liquidity of domestic entities. Through increasing debt and declining liquidity, the value of the country’s currency is diminished (as evidenced by a rising exchange rate). For example, declining currency values might reflect the negative outlook foreign entities likely have about countries with high liabilities and low liquidity (e.g., Buiter, 1987; Frankel & Rose, 1996; Grilli & Roubini, 1992). Thus, prior research suggests that these variables are linked in the manner presented here. We name this factor Market Liquidity. We use both of these economic institutions factors to test Hypotheses 3 and 6.

The factors exhibited good discriminant validity. 3 We utilized the factor scores to test our hypotheses. Skewed factors were log transformed before we tested the hypotheses.

Informal institutions: Culture

We used culture to represent informal institutions. Given limitations identified in the Hofstede measures (Ailon, 2008; Fang, 2010; McSweeney, 2002), we used data from the Global Leadership and Organizational Behavior Effectiveness project (GLOBE; House, Hanges, Javidan, Dorfman, & Gupta, 2004) to measure cultural practices in each country. 4 Specifically, we used in-group collectivism and future orientation, the theoretical variables of interest. In-group collectivism reflects the extent to which the behavior of societal members corresponds to the interests and goals of the social units (e.g., families and organizations) to which such individuals belong. Future orientation reflects the degree to which the behavior of individuals in a society represents the pursuit of long-term outcomes.

House and Javidan (2004) noted that GLOBE measured the culture of certain societies rather than that of countries per se. Although most of the countries in our sample match the societies included in GLOBE, there are slight differences in five cases. First, GLOBE includes a full range of measures only for English-speaking portions of Canada. Second, GLOBE includes separate measures for the former East Germany and the former West Germany. We estimated the populations of the former East Germany and the former West Germany by using data from Eurostat that specified the populations of 16 major metropolitan areas. To generate a single measure for Germany, we constructed a weighted average by multiplying the population estimates by the GLOBE scores for the respective regions and then summing the products. Third, the GLOBE scores for South Africa include measures derived from a “black sample” and a “white sample.” We weighted the GLOBE scores by the populations of these subgroups, using data provided by the Economist Intelligence Unit, and summed the products to generate a weighted average to serve as a single score for South Africa. Fourth, GLOBE includes separate measures for French-speaking and German-speaking portions of Switzerland. As with South Africa, we weighted the GLOBE scores by the populations of these subgroups, using information from the Economic Intelligence Unit, and constructed a weighted average for Switzerland. Fifth, although our data set includes the United Kingdom, GLOBE measured the culture of England only. Thus, we used the scores for England to represent the United Kingdom.

Controls

We controlled for two key variables in the models with formal institutions as the dependent variables. First, we controlled for the effects of a country’s population. The population of a country often influences its regulatory, political, and economic institutions due to the additional restrictions on firms, centralization of government, and capital investments needed as its population increases (e.g., Coale & Hoover, 1958; Heath & Binswanger, 1996). In addition, we controlled for industry workforce (as a percentage of total employed) as a proxy for the impact of economic development on formal institutions. Both variables are from PRS.

In the regressions using inward FDI as the dependent variable, we attempted to isolate the effects of the formal institutions from the effects of the culture variables. Using the GLOBE data, we included in-group collectivism and future orientation in these regressions. We also included four additional controls. Firms often invest in foreign markets to gain access to new sources of skilled labor (Dunning, 1998). Thus, we again used the industry workforce variable. In addition, a country’s physical infrastructure supports economic exchange and may attract FDI (Loree & Guisinger, 1995). Therefore, we used three infrastructure variables as controls. Transportation infrastructure is an important enabler of business activities because it is necessary for the movement of goods and services within a country’s economy (Davis, Desai, & Francis, 2000). We controlled for railway freight (in millions of net ton-kilometers logged) and merchant shipping (in thousands of gross tons shipped logged) to account for a country’s transportation infrastructure. In addition, because it enables the flow of information and knowledge, telecommunications infrastructure is an important contributor to economic growth (Roller & Waverman, 2001). Thus, we included the variable digital main lines (as a percentage of telephone main lines) as a control. The information for all three infrastructure variables was obtained from Euromonitor.

Results

Our data set includes observations for each of the sampled countries annually for nine years, and all variables are at the country level. Due to the panel nature of these data, intertemporal correlation among the error terms may create contemporaneous correlation, which violates an important assumption of ordinary least squares regression (N. Beck & Katz, 1995). We adopted Certo and Semadeni’s (2006) recommendation to model the data using either random-effects or fixed-effects regression. Because cultural variables are largely slow to change, the culture data are not available in panel form. Thus, the cultural variables are the only time-invariant variables in the analyses. Plumper and Troeger (2007) offered a solution for analyzing panel data that include a time-invariant independent variable. They suggested that in these circumstances random-effects models perform better than pooled ordinary least squares regression or fixed-effects models do. As a result, we used random-effects modeling.

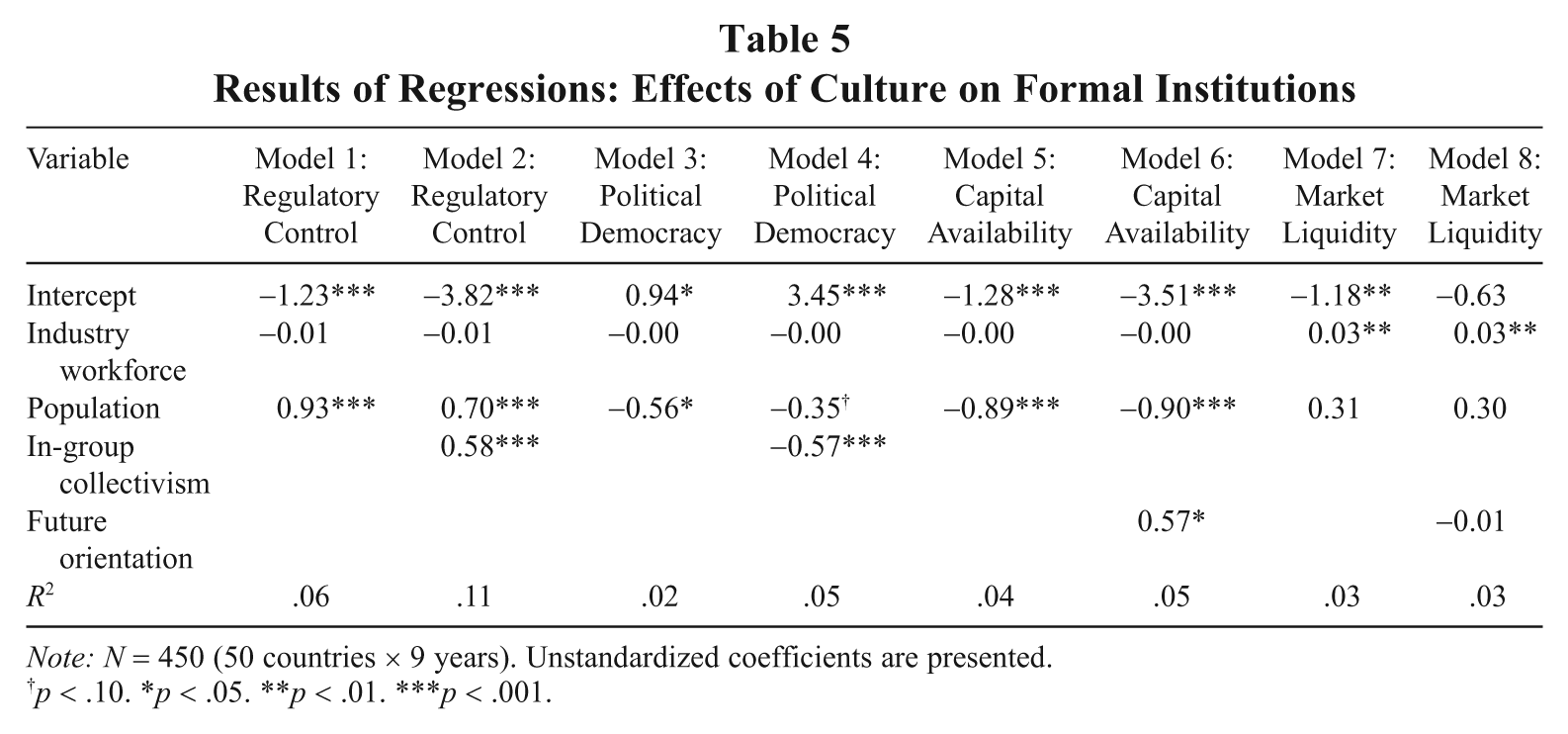

Models 1–8 of Table 5 provide the random-effects regression results for the relationships between the cultural variables and the institutional variables, reflecting the tests of Hypotheses 1–3. We first entered control variables in the odd-numbered models. Hypothesis 1 posited that collectivism is positively related to the control regulatory institutions exercise over the activities of organizations. Model 2 of Table 5 shows that in-group collectivism has a positive and statistically significant relationship with the level of Regulatory Control (b = 0.58, p < .001), providing support for Hypothesis 1. Hypothesis 2 predicted that collectivism is negatively related to democratic political institutions. Model 4 shows that in-group collectivism has a negative and statistically significant relationship with Political Democracy (b = −0.57, p < .001). Therefore, Hypothesis 2 receives support. Hypothesis 3 posited that future orientation is positively related to economic institutions promoting domestic entities’ capital investments. Model 6 shows that the relationship between future orientation and Capital Availability is positive and statistically significant (b = 0.57, p < .05). However, the relationship between future orientation and Market Liquidity is not statistically significant (b = −0.01, ns). Thus, Hypothesis 3 receives partial support.

Results of Regressions: Effects of Culture on Formal Institutions

Note: N = 450 (50 countries × 9 years). Unstandardized coefficients are presented.

p < .10. *p < .05. **p < .01. ***p < .001.

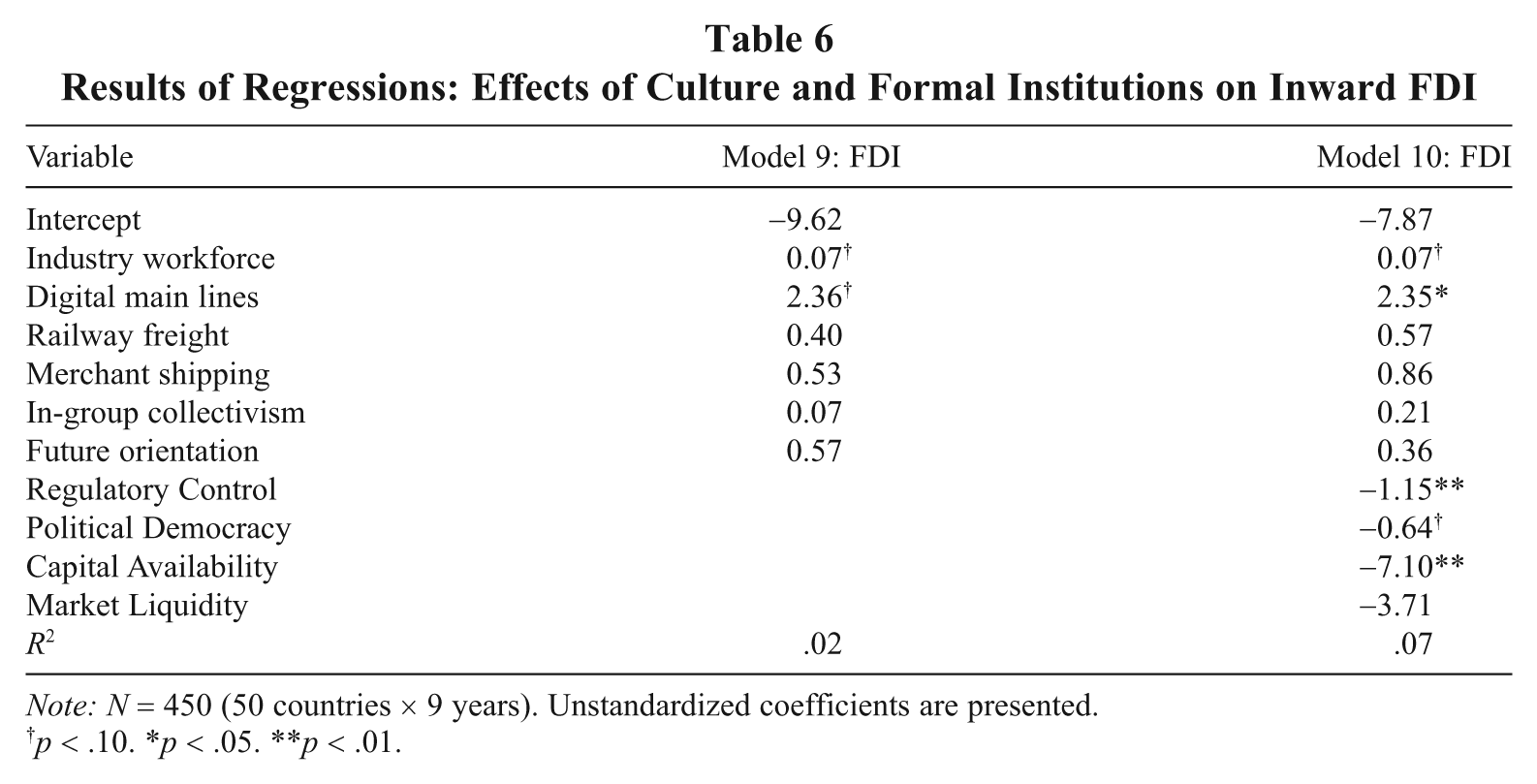

Hypotheses 4–6 explore the relationships between the formal institutional variables and inward FDI. In Model 9 of Table 6, we entered control variables. Hypothesis 4 suggests that inward FDI is lower in countries with formal institutions exercising greater control over the activities of organizations. Model 10 shows that the coefficient for Regulatory Control is negative and statistically significant (b = −1.15, p < .01), thus providing support for Hypothesis 4. Hypothesis 5 states that inward FDI is higher in countries with democratic political institutions. However, the coefficient for Political Democracy is negative and marginally statistically significant (b = −0.64, p < .10). Thus, this result is counter to the prediction in Hypothesis 5. Hypothesis 6 posits that inward FDI is lower in countries with economic institutions promoting capital investments by domestic entities. Model 10 of Table 6 shows that the coefficient for Capital Availability is negative and statistically significant (b = −7.10, p < .01). The coefficient for Market Liquidity is not statistically significant (b = −3.71, ns). Therefore, Hypothesis 6 receives partial support.

Results of Regressions: Effects of Culture and Formal Institutions on Inward FDI

Note: N = 450 (50 countries × 9 years). Unstandardized coefficients are presented.

p < .10. *p < .05. **p < .01.

Discussion

To address several shortcomings in extant management research on institutional theory, our purpose was to examine multiple institutions in a large number of countries over several years. This study makes three primary contributions to the literature. In this section, we discuss each contribution and its implications for future research in the field. We then discuss the limitations of our study and additional future research opportunities.

Conceptualizing and Measuring Three Country-Level Formal Institutions

Our first contribution involves offering a framework and set of tools to facilitate further empirical and theoretical research on formal institutions. Specifically, in integrating research on institutional theory across disciplines, we identified three types of country-level formal institutions, described the functions they serve, and developed measures for them in a large number of countries. The first, regulatory institutions, reflects government policies and laws that constrain and limit the activities of organizations. Second, political institutions define how power is distributed in government, who is allowed to participate in it, and how that participation occurs. In turn, these institutions shape the processes through which governments and individuals create or change formal institutions. Finally, economic institutions oversee countries’ financial resources. Although we expected a single indicator for economic institutions, our factor analysis revealed one measure reflecting capital availability and another reflecting market liquidity.

Understanding why and how the institutional environment influences managers’ strategic decisions has often been a challenge for researchers, in part because there has been little consensus about the relevant formal institutions in the institutional environment and how to measure them. Using primary sources in a limited number of countries, empirical research often anchors the measurement of institutions in specific issues such as quality management (e.g., Kostova & Roth, 2002) and entrepreneurship (e.g., Busenitz et al., 2000) or examines institutional environments using qualitative methods (e.g., Witt & Redding, 2009). Thus, measurement of key constructs of such important metaconcepts as the institutional environment has been criticized for lack of consensus among researchers, low reliability, and lack of construct and content validity (Boyd, Gove, & Hitt, 2005; Boyd & Reuning-Elliot, 1998). For example, scholars have measured regulatory institutions using proxies such as the World Competitiveness Report indicators of state influence (e.g., Yiu & Makino, 2002) and industry-specific metrics (e.g., Russo, 2001), invoking different theoretical explanations to justify the different proxies.

The theoretically based constructs we have established, measured using rich empirical data in 50 countries, may enable scholars to revisit older questions as well as pursue new ones. Consistent with our approach, Ostrom (2005) suggested that there are multiple and distinct independent institutions within countries (i.e., institutional environments are polycentric) and that there is diversity in the attributes of such institutions across countries. In concert with the arguments of North (1990) and Scott (1995), management scholars emphasize the consequences of variation in institutional environments for managers’ decisions and organizational outcomes (e.g., Delmas & Toffel, 2008; Delios & Beamish, 1999). Armed with these constructs and measures, scholars can examine the consequences of multidimensional, interconnected, and polycentric institutional environments as well as explanations for the diversity of such environments.

In particular, scholars could build on our research by examining the combined influence of multiple institutions on managers’ selections of geographic regions, host countries, entry modes (e.g., greenfield ventures), acquisition targets, or strategic alliance partners. These institutional measures will also enable scholars to generate more comprehensive indicators of institutional distance, which has been shown by prior research to have an important influence on firms’ international strategies and their consequences (Kostova, 1999; Kostova & Roth, 2002). We also encourage future research that explores the integrated effects of formal institutions. Because of the government’s involvement in implanting regulatory and economic institutions, for example, political institutions may influence the attributes of regulatory and economic institutions or may moderate relationships between the latter two types of institutions and firm strategies. Moreover, our measures will enable scholars to pursue novel theoretical foci such as those proposed by Kostova, Roth, and Dacin (2008). In short, our conceptualization and measures of formal institutions should facilitate additional research that will advance understanding of international strategy. Indeed, the utility of the constructs and measures is supported by the findings that informal institutions influence formal institutions and that different formal institutions have distinct effects on inward FDI.

The Link between Informal Institutions and Formal Institutions

We provide one explanation for the diversity of formal institutions across countries. In particular, we have linked the informal institutions of countries to their formal institutions. Drawing on theory identifying culture as an important aspect of informal institutions (e.g., North, 1990; Peng et al., 2008), we have argued that culture provides a foundation on which a country’s formal institutions develop. Societal members devise formal institutions to remedy problems the society confronts. The norms and values embodied in its culture are influential in shaping individuals’ evaluation of these problems, prioritizing their importance, shaping the development of solutions for them, and facilitating the implementation of such solutions. Over time, the society’s norms and values reinforce the formal institutions and enable them to be accepted, supported, and maintained in the society. Stated differently, our research suggests that major dimensions of a country’s culture influence the continued development and evolution of the country’s formal institutions. In this sense, our study provides evidence that formal institutions reflect the society’s collective actions and behaviors (DiMaggio, 1988; Powell, 1991; Tolbert & Zucker, 1996).

Our research showed relationships between two dimensions of a country’s culture and the country’s formal institutions. In particular, our study suggests that collectivism increases the level of control regulatory institutions exert, while reducing the democratic nature of political institutions. Collectivism fosters concern for the interests of society over those of individuals. Thus, regulatory control to ensure that organizations act in ways beneficial to society is valued. Moreover, democratic political institutions give voice to individuals and special interests. Therefore, to promote broader community interests, countries with cultures high in collectivism may favor weaker democratic processes to limit the power of smaller subsets of the population and to ensure that the distribution of power favors the state.

This study also found partial support for the proposed positive relationship between future orientation and the presence of economic institutions promoting capital investments by domestic entities. Future-oriented cultures emphasize long-term outcomes and the importance of making the necessary investments to facilitate such outcomes. In turn, countries with strong future orientations are likely to build economic institutions that craft monetary and fiscal policies to encourage long-term investments. The first economic institution measure reflects rather unambiguous indicators of the availability of financial capital in the economy. Therefore, the positive relationship with future orientation was expected. However, we did not find a relationship between future orientation and institutions shaping market liquidity. Two of the components of this measure, liabilities and liquidity, largely represent accumulated values on organizations’ balance sheets. Thus, these measures may reflect accounting conventions rather than the immediate demand for and supply of capital. The third component, exchange rate, depends heavily on the actions of entities outside the given country. As such, beyond local market conditions, it may be at least partially dependent on conditions in foreign markets.

We encourage future research that examines the sources of informal and formal institutions. Indeed, we lack the data to show definitively that informal institutions are the source of formal institutions, and more in-depth historical examinations are required to address this issue. For example, Greif (1994) examined how the culture of two societies in the 11th and 12th centuries contributed to the development of different formal institutions for governing economic exchanges and enforcing property rights. He argued that formal institutions develop along path-dependent trajectories that are shaped by the culture of the society. Over time, the resulting institutional changes reinforce the culture. In other words, cultural norms and values may underlie the development of formal institutions. In turn, the formal institutions reinforce these norms and values. Likewise, Beisel (1990, 1993) explained how cultural norms and values facilitated the establishment of laws and enforcement mechanisms prohibiting certain behaviors in 19th-century American cities. She argued that individuals often manipulate formal institutions to create and preserve a social order that is both consistent with and favorable to the individuals’ norms and values. Her conclusions suggest that culture may give rise to certain formal institutions, which in turn protect and solidify the culture.

More complete understanding of culture and formal institutions may also require research spanning levels of analysis, an important consideration in management research (Hitt, Beamish, Jackson, & Mathieu, 2007). Indeed, culture and formal institutions influence behavior differently at individual, organizational, and country levels of analysis (Chreim, Williams, & Hinings, 2007; Kirkman, Lowe, & Gibson, 2006).

The Implications of Formal Institutions for FDI

This study has also contributed to future research by documenting the influence of regulatory, political, and economic institutions on a country’s attractiveness for strategic investments by MNEs, as revealed through inward FDI, controlling for the influence of culture. These results provide a form of criterion-related validity for our measures of formal institutions.

Building on arguments that institutions shape the behavior of organizations (DiMaggio & Powell, 1983; Meyer & Rowan, 1977), we found evidence that formal institutions have unique effects on inward FDI beyond the influence of culture. For example, our findings suggest regulatory institutions that tightly control the behavior of organizations discourage inward FDI, implying that managers seek to minimize government involvement in MNE affairs. In this respect, our results are in line with research showing that regulatory institutions exercising control over specific MNE activities (e.g., labor relations) reduce FDI inflows (Pajunen, 2008).

In addition, we found that political institutions influence inward FDI. We expected MNE managers to find institutions that concentrate power in a single branch of government to be unattractive because such concentration can result in rapid, unexpected, and major shifts in government policy and can discourage human capital development and innovation. In light of “[t]he popular assumption . . . that political stability of a country is conducive to FDI inflows” (Pajunen, 2008: 654; also see Chan & Makino, 2007, and Loree & Guisinger, 1995), our results showing a negative relationship between more democratic political institutions and inward FDI were unexpected. However, Li and Resnick (2003) also found that increasingly democratic political institutions reduce a country’s attractiveness for inward FDI.

There are several possible explanations for the result we found. First, relative to democratic institutions, autocratic institutions provide less protection for individuals, perhaps enabling firms to leverage their investments with fewer constraints. Second, the transparency and accountability of democratic political institutions limit the discretion of government officials to provide special treatment for certain MNEs. A third explanation is that, although prior theory suggests that greater checks and balances produce more stable and predictable policies, the electoral process may promote instability and unpredictability because government officials respond to the changing demands of voters. Moreover, policies frequently change due to the turnover of elected officials. To the extent democracy produces instability and lower predictability, our results are consistent with the view that MNE managers often prefer to minimize uncertainty. Fourth, although we argued that autocratic institutions might promote inefficiencies, others have noted that limiting the individuals involved in the political process can eliminate inefficiencies stemming from inconsistent and potentially conflicting interests (e.g., Inman & Rubinfeld, 1997; Oates, 1999). Fifth, a curvilinear relationship may exist between political democracy and inward FDI. Because of this possibility, we conducted a post hoc analysis to investigate the second-order effect. However, the coefficient was not statistically significant. Given the different arguments regarding the effects of democratic political institutions, we encourage further research in this area.

Finally, the results linking economic institutions to inward FDI were mixed. First, we provide evidence that economic institutions promoting capital availability for domestic entities discourage inward FDI. One explanation is that MNEs can access capital from their home markets but are negatively influenced by monetary and fiscal policies that weaken government finances and increase the possibility of inflation. Second, the market liquidity measure was unrelated to inward FDI. Perhaps these institutions have neutral effects on the size of MNE investments but influence the decisions MNE managers make once investments are in place. For example, when making their initial decisions to invest in a country, MNE managers may neglect institutions that shape the liabilities and liquidity constraints of local firms. However, once MNEs have invested, these institutions may influence subsequent decisions such as supplier selection, the terms of exchange with partners, and so on. Alternately, perhaps MNE managers are more attuned to the changes in these institutions than to their conditions at a point in time. For instance, because the exchange rate ensures that holdings of one currency are equal in value to holdings of another, MNE managers may be ambivalent about the current exchange rate. Instead, they may focus their attention on changes in the exchange rate, which can affect the value of repatriated profits, returns on invested capital, and so on. Another explanation is that MNEs may be able to address the constraints that market illiquidity imposes by utilizing home-market economic institutions. More generally, the mixed effects of the economic institutions may reflect the flexibility MNEs often have in mitigating the pressures that economic institutions produce, relative to the legal pressures that regulatory and political institutions impose (Kostova et al., 2008). Therefore, we also encourage additional research on the influence of economic institutions on MNE strategies.

Although formal institutions influence managers’ strategic decisions to enter markets and the amounts MNEs invest in those markets, importantly, the informal institutions did not appear to affect the amount of inward FDI. One explanation is that informal institutions play a smaller role in the major decisions made by MNE managers than do formal institutions. Alternately, perhaps a country’s culture is a less important consideration for MNE managers than is the cultural distance between that country’s culture and the culture of the MNE’s home country, as prior research suggests (Hennart & Larimo, 1998). Nonetheless, culture appears to provide an important basis for the development of countries’ formal institutions, which in turn affect MNE managers’ decisions. Due to degrees of freedom restrictions, we could not investigate whether formal institutions mediate the relationship between culture and FDI. However, examining possible mediation would be a promising area for future research.

Additional Limitations and Future Research Suggestions

Our research also has other limitations. Unfortunately, the data for some desirable variables (e.g., level of educational achievement) were unavailable for many countries. To include such data would have substantially reduced the number of countries in the study. Therefore, we made a trade-off in order to have a larger sample of countries.

In addition, there were few relationships with the market liquidity institution, implying a need for greater theoretical examination of this variable. For example, other informal institutions may give rise to it, and it may have implications for other firm strategies and actions (e.g., capital structure and partnering decisions). Degrees of freedom and length constraints also disallowed the examination of the influence of more cultural attributes on the other formal institutions variables.

In conclusion, our study has conceptualized and produced measures for countries’ regulatory, political, and economic institutions. We found that informal institutions, as reflected in culture, influence these formal institutions. This study also identified the effects of different formal institutions on inward FDI, which captures a country’s attractiveness to MNE managers. The theoretical model and empirical tests of it provide a strong catalyst for future management research drawing on institutional theory to explain firm strategies and their outcomes.

Footnotes

Appendix

Correlations of Factor Items

| Variable | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 | 19 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Trade policy | |||||||||||||||||||

| 2. Monetary policy | .47*** | ||||||||||||||||||

| 3. Foreign investment restrictions | .55*** | .17*** | |||||||||||||||||

| 4. Government intervention in banking | .53*** | .36*** | .52*** | ||||||||||||||||

| 5. Contract and property rights | .7*** | .59*** | .52*** | .6*** | |||||||||||||||

| 6. Regulatory burden | .61*** | .41*** | .48*** | .55*** | .71*** | ||||||||||||||

| 7. Informal markets | .64*** | .68*** | .39*** | .52*** | .8*** | .59*** | |||||||||||||

| 8. Budget balance | .07 | .14** | −.14** | −.06 | .09 | .07 | .12* | ||||||||||||

| 9. Money supply | −.16*** | −.32*** | .1* | −.05 | −.21*** | −.15** | −.29*** | −.71*** | |||||||||||

| 10. Total foreign debt | −.15** | −.23*** | .09 | −.06 | −.21*** | −.15** | −.24*** | −.63*** | .83*** | ||||||||||

| 11. Liabilities | .14** | .22*** | .09 | .06 | .11* | .12* | .14** | −.03 | −.04 | −.03 | |||||||||

| 12. Liquidity | .04 | .02 | .12** | .18*** | .09 | −.01 | .13** | −.2*** | .16*** | .03 | −.36*** | ||||||||

| 13. Exchange rate | −.05 | .18*** | .04 | .03 | .05 | .08 | .06 | −.02 | −.04 | −.01 | .42*** | −.15*** | |||||||

| 14. Political rights | .47*** | .32*** | .28*** | .34*** | .54*** | .35*** | .44*** | .12* | −.16*** | −.17*** | .11* | .14** | .07 | ||||||

| 15. Civil liberties | .53*** | .45*** | .32*** | .45*** | .62*** | .38*** | .57*** | .07 | −.16*** | −.18*** | .19*** | .16*** | .12* | .91*** | |||||

| 16. Political constraints | −.2*** | −.12* | −.06 | −.16*** | −.31*** | −.13** | −.19*** | −.12** | .06 | .1* | −.03 | −.02 | .04 | −.67*** | −.59*** | ||||

| 17. Executive political restrictions | −.48*** | −.3*** | −.33*** | −.43*** | −.65*** | −.51*** | −.52*** | −.07 | .09* | .13** | −.03 | −.13** | .03 | −.69*** | −.64*** | .64*** | |||

| 18. Nominal GDP | −.17*** | −.27*** | .02 | −.12* | −.24*** | −.19*** | −.28*** | −.43*** | .83*** | .87*** | −.03 | −.05 | −.03 | −.18*** | −.21*** | .05 | .16*** | ||

| 19. Net reserves | −.14** | −.31*** | .15** | .05 | −.15** | −.15** | −.23*** | −.63*** | .78*** | .51*** | −.14** | .49*** | −.07 | .03 | .02 | −.08 | −.01 | .44*** | |

| 20. Capital investments | −.15** | −.28*** | .06 | −.09 | −.23*** | −.18*** | −.28*** | −.49*** | .89*** | .91*** | −.05 | .02 | −.03 | −.15** | −.17*** | .04 | .13** | .98*** | .54*** |

Note: N = 450. All variables were transformed such that their mean = 0 and their standard deviation = 1.

p < .05. **p < .01. ***p < .001.

Acknowledgements

This article was accepted under the editorship of Talya N. Bauer. We benefited from comments by Jean-Luc Arregle, Don Bergh, Jean Boddewyn, Lance Brouthers, and Doug Schuler on earlier versions of this article. We also benefited from participants’ comments in research colloquia presented at the University of Connecticut, University of Illinois, University of Miami, and Rice University. The participation of M. Paz Salmador was graciously supported by the Fulbright Program.