Abstract

The pattern of international capital flows has changed dramatically in the process of globalization. In this study, we argue that human capital (HC) facilitates a region’s reversal from being a net recipient of external resources to being an active contributor in the global market. Using a panel vector autoregressive regression method, we examine the relationships among regional HC, foreign direct investment (FDI), and outward FDI during 2004–2015 in China. Our results show that HC plays a key role in both attracting FDI and generating outward FDI. The findings contribute to research on the dynamic capacity building of regions participating in the global economy, especially strengthening HC for local economies participating in the global economy as either investment recipients or contributors.

Introduction

The global economy is dynamically shifting and has arrived at a turning point. It is characterized by the emergence of multi-dimensional flows of capital, and changes in economic perceptions toward a more balanced view of human capital (HC) and physical capital. This study uses the case of China to explore how HC facilitates the reversal of a region’s position from being a net recipient of external resources to being an active contributor in the global market. Revealing this shift is of interest for understanding the complexity and trends of globalization.

The global economic landscape has been changing, particularly since 2008, which was a critical point for the globalization process (Milesi-Ferretti and Tille 2011). 1 Prior to this, the world economy was dominated by capital flows from developed to developing economies. After 2008, emerging economies rose and capital flows from developing to developed economies increased. This was especially true for some of the BRICS countries. 2 This provided opportunities for firms from emerging markets to merge these international companies at lower prices. Companies from BRICS countries have quickly become multinationals through acquisitions and greenfield investments, competing or cooperating with multinational corporations (MNCs) from developed economies. 3 This phenomenon can be viewed as a reversal in the role of developing economies and has challenged existing academic theories and practices in the global economy.

The case of mainland China (China hereafter) is worth investigating with respect to this issue. First, foreign direct investment (FDI) is not only a critical generator of economic growth but also introduces knowledge and technology to new destinations. Regions are expected to share greater benefit from FDI when they are integrated into global production networks (Dennis Wei, Liefner, and Miao 2011). Therefore, the transition from receiving FDI to transmitting outward foreign direct investment (OFDI) indicates the rise of an economy with strong and abundant capital that is expanding into new markets, seeking new resources and land, exploring new opportunities and risks, and making higher profits than what it would obtain in the home country. According to the United Nations (2017), China was the top OFDI provider in Asia in 2016. This reversal from FDI to OFDI cannot occur if regional development depends exclusively on the external environment or if the region does not outperform the global market.

Second, HC is closely linked to absorptive and transmissive capacities of international capital flows and the current explanations for the Chinese growth miracle are far from satisfactory. Most research on OFDI in China attributes this to the growth of the Chinese economy (Brink 2015; Hanemann 2014), and there has been less concern with a region’s transmissive capacity. China has implemented compulsory education for several decades since the reform and opening up, enabling most of its citizens to achieve a higher education level than previously (Huang 2015). Under this circumstance, we expect HC to play a critical role in supporting China to absorb FDI and thereby reverse the FDI trend to an OFDI trend.

The rest of the paper is structured as follows. Second section presents a review of the theory underlying the relationships among HC, FDI, and OFDI. Third section describes the growth and changes in the HC, FDI, and OFDI of China. Fourth section introduces the methods and data to measure the interrelationship of these three factors. Fifth section summarizes and discusses the results, focusing on the shifting role of HC. Sixth section concludes with policy implications and pathways for future research.

Understanding Globalization through HC, FDI, and OFDI

The interrelationship of HC, FDI, and OFDI can be understood by the absorptive and transmissive capacities of a region in the global economy. Absorptive capacity can be understood as the capacity to recognize, assimilate, and apply the value of external resources to local economic development (Todorova and Durisin 2007). Often rooted in endogenous growth factors (Giuliani 2005), this type of research emphasizes knowledge absorption, technology innovation (Fabrizio 2009), and the promotion of HC accumulation as major drivers of competitiveness (Cohen and Levinthal 1989; Spithoven, Clarysse, and Knockaert 2011). Furthermore, by examining the building process of the absorptive capacity of the actors in the network, the growth and success of emerging economies has been articulated for the case of China (Xu, Wan, and Sun 2014; C.-H. Yang and Lin 2012) and India (Jayaraman, Choong, and Ng 2017), showing that absorptive capacity acts as the key determinant of regional success (Doranova, Costa, and Duysters 2011).

At the junction of knowledge and capital investment, HC acts as the key for improving internal capabilities. Previous literature has shown that the absorptive capacity level relies on education level, working experience, and training experience (Spithoven, Clarysse, and Knockaert 2011). These facts suggest that knowledge underlies intertemporal and international shifts in production functions in the global economy, although it may intentionally promote production and wealth distribution and redistribution only. Similarly, absorptive capacity can be used to comprehend how internal capabilities may be employed to harness FDI, for example innovation is closely associated with foreign workers and their network (Solheim and Fitjar 2018).

Likewise, the transmissive capacity of HC matters when a region expands globally, and involves questioning the ability of underdeveloped countries to upgrade their capacity to cope with investment conditions globally. The scope and geographical limitation of globalization depends on people’s skills and knowledge to recognize the value of the investment destination, on the ability to adapt to the local context, such as the efforts to adapt technology to local contexts, and on the technical capabilities of domestic firms (Saliola and Zanfei 2009). HC acts as a catalyst in transforming the role of a country in the global economy by attracting external investment and knowledge to foster the ability to generate them locally. Education-based HC improvement helps a firm or region to enlarge its technological boundaries and successfully absorb new technologies (Faems and Subramanian 2013; Brekke 2021). The cooperation between universities and companies (Tsai 2009) improves the labor pool and upgrades the technology and industrial value chains that support the local economies with which they are integrated (Barra and Zotti 2017). It is easier and common for MNCs to select a region with similar first languages. Other factors include historical and cultural ties; for example, Japanese MNCs heavily invest in South Asia (Edgington and Hayter 2012). Collectively, HC enhances a region’s ability to deal with inflows and outflows of capital in the global economy.

However, few studies directly explore linkages between capital flows and HC accumulation. Most research takes developed economies as the source of FDI, and two courses of capital flows—vertical and horizontal—are identified, determined by the technology gap in the origin and destination regions, thereby making HC an influential factor. In terms of switching from FDI to OFDI, the investment development path (IDP) theory explains the transition of a region from the FDI destination to the source, based on changes in localization advantages (Dunning 1981). The theory considers five stages in OFDI development—initial (near zero), emerging, increasing, overpassing inward FDI, and neutralized by inward FDI. Some transitional economies may leapfrog ahead by skipping some stages (Svetličič and Rojec 2003). However, others argue that developing countries are unable to develop localization advantages to execute international activities (Erdilek 2003; Kuada and Sørensen 2000).

For these reasons, it is important to investigate how a country or region may reverse its position from being a net receiver of external resources to being an active contributor in the globalized economy. We postulate that HC plays a critical intermediate role.

Hypothesis 1 could formalize conducting effects for a region participating in the global economy through the exchange of capital, people, information, knowledge, and technology, among which HC plays a critical role. Allowing for dramatic changes that have occurred in capital flows, business cooperation, and industrial development after the 2008 financial crisis, we further hypothesize that mutual effects among FDI, HC, and OFDI were shaped after the 2008 financial crisis. In addition, HC is more likely concentrated in economically prosperous regions, while these regions have higher FDI and OFDI (Luo, He, and Guo 2016). Manuelli and Seshadri (2014) and Karahasan and Lopez-Bazo (2013) show that HC’s quality varies systematically with the level of development, and IPD theory suggests that there are five stages of relationships between FDI and OFDI. Therefore, we examine whether the interrelationship of HC, FDI, and OFDI differs across regions with different development levels.

FDI, HC, and OFDI of China during Globalization

Since the beginning of the economic reform and economic opening of the 1980s, China has evolved from a low-income to a middle-income economy. China received a massive inflow of global investment, from about USD 430 million in 1982 to more than USD 170 billion in 2016, with every 1 percent increase in foreign investment contributing 0.07 percent of Chinese economic growth (Agrawal and Khan 2011). These investments have also brought new information, knowledge, and technology (Freeman and Huang 2015).

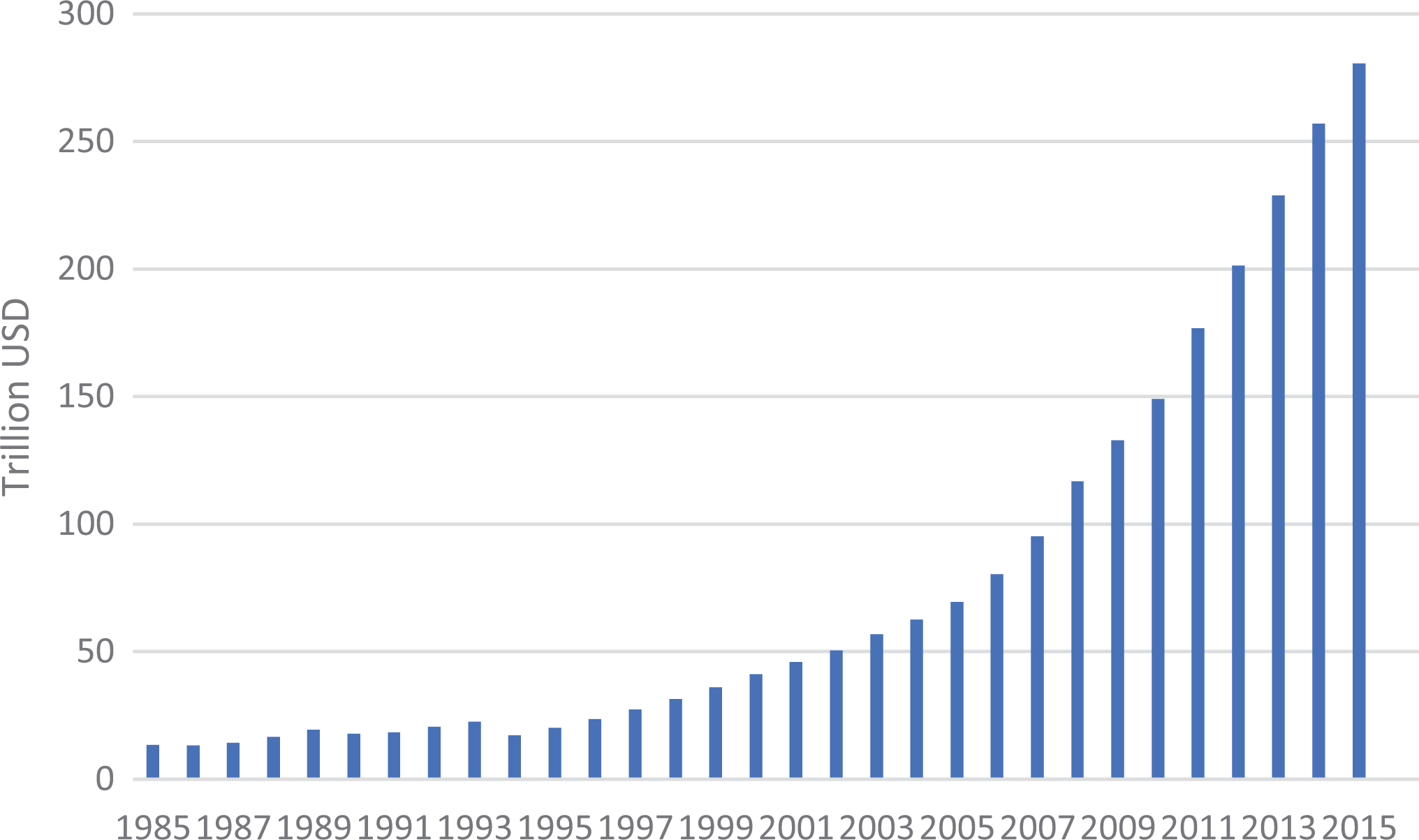

Alongside China’s economic achievements, its HC has grown dramatically from approximately USD 13.4 trillion in 1985 to over USD 280 trillion in 2015 (Figure 1). The improvement in the quality of the workforce in the process of HC accumulation has been attracting FDI, thereby consistently driving economic growth. Owing to the large number of skilled laborers and public infrastructure investments, China has received more FDI than other developing countries with similar per capita income levels (Noorbakhsh, Paloni, and Youssef 2001; Zhang and Markusen 1999). Teixeira and Heyuan (2012) find micro-level evidence that the quality of HC attracts FDI to China indirectly through firms’ R&D. Importantly, the growth of the Chinese economy has spurred Chinese capital investments in other countries. This globalization feature highlights China’s increasingly important role in the global economy.

Stock of human capital in China.

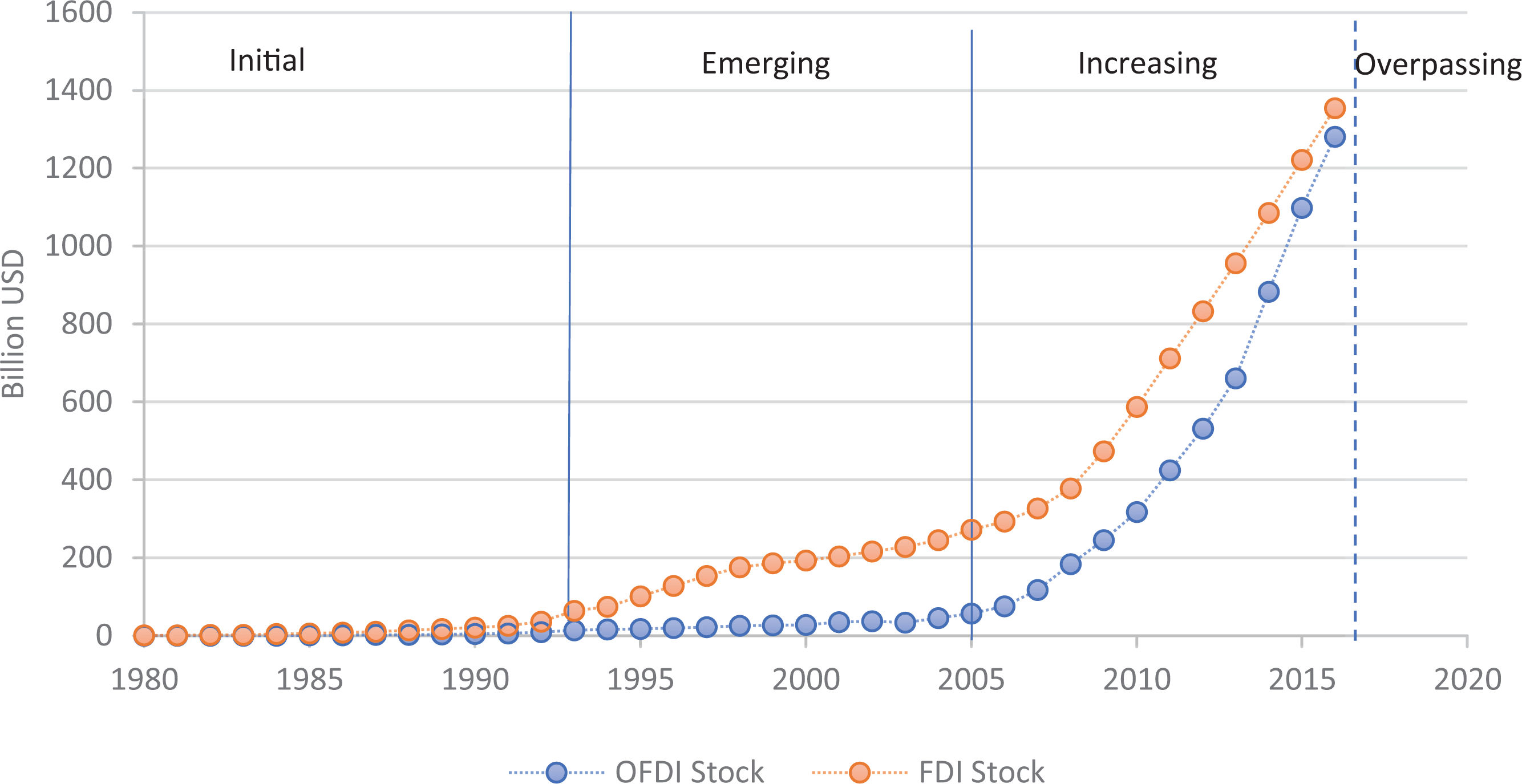

Figure 2 shows changes in FDI and OFDI in China during 1982–2016. To some extent, these changes demonstrate the initial stage (near zero) and the overtaking of FDI by OFDI, reflecting the transformation of China’s role in the globalization process from “borrower” to “lender” of FDI.

China’s FDI and OFDI during 1982–2016.

Substantial differences in HC are found in China, resulting from the country’s economic, developmental, and demographic characteristics (Figure 3). The highest values of HC are found in Guangdong (USD 25.71 billion), Shandong (USD 21.05 billion), and Jiangsu (USD 19.76 billion), which are densely populated regions with high levels of educational and technological development. Beijing and Shanghai share a high level of HC per capita, but their total population is not as high as the aforementioned provinces, and therefore, their HC stock is smaller. HC is high in Chongqing because of its population size. The growth rate of HC varies significantly from five times in Tianjin to double in Tibet during 2004–2015.

Figure 3 also reveals a substantial variation in FDI and OFDI. Overall, the central and western regions take up less than 20 percent of the FDI in China in 2015. OFDI stock in the eastern region was USD 286.54 billion accounting for 83.2 percent of the regional OFDI, while the western and central regions have a share of only 16.8 percent. In other words, the top ten provinces with the highest OFDI stock accounted for 80.3 percent of the local OFDI. Such variation indicates that Chinese regions have a different level and accumulation pace of HC, FDI, and OFDI as they participate in the globalization process.

Regional distribution of HC, FDI, and OFDI in 2015.

Despite the large regional differences within China in terms of OFDI, research at the provincial level has received limited attention. Exceptions include Chen (2014) and You (2017), who measure Chinese regional OFDI and argue that regional features may significantly affect OFDI, given the large size of the country. This perspective provides a lens to understand the different means (receiver and supplier) by which Chinese regions participate in the globalization process. Although the Chinese economy is the world’s second largest, this fact cannot fully explain the expansion in overseas investment. There is no consensus on what has facilitated China’s transformation. Prior research mostly uses regression analysis to test unidirectional relationships and is unable to capture the interactions among HC, FDI, and OFDI. In this study, we argue that HC plays a shifting role and thereby aims to fill the gap in the literature on this relationship.

Methods and Data

Methods

As HC, FDI, and OFDI are interdependent, one solution to identify their interrelationship is the panel data vector autoregressive (VAR) method. Panel VAR has been widely used to test a variety of interdependent economic issues (Canova and Ciccarelli 2013). Within the realm of FDI-related literature, Hou et al. (2020) use this method to examine endogeneity from both source and destination countries and model heterogeneous global and local shocks to FDI. Zeng et al. (2020) study the relationship among energy consumption, FDI, and economic development in Zhejiang, China from 1993 to 2017 and find that FDI contributes to economic growth indirectly through energy consumption; therefore, the study proposes that Zhejiang should pay attention to the efficiency of energy when using FDI to develop its economy. Manu et al. (2020) employ a panel VAR and granger causality test to reveal that a nexus exists in FDI and economic growth in African countries. Many other applications include analysis of FDI and social welfare (Ehouma Jacques et al. 2020) and FDI and environmental quality (Abdouli and Hammami 2017). By contrast, there are few studies about FDI flows and HC, although HC is crucial for absorbing inward capital flows and facilitating outward capital flows, and these three factors are endogenous and interdependent. We apply the VAR and Granger causality test to check the robustness of the association between FDI and OFDI inflows with HC.

Specifically, we explore the sources of covariance among the residuals in each of the three equations and compute the impulse-response and variance decomposition by using the technique of Choleski decomposition (Enders 2008; Hamilton 1994; Love and Zicchino 2006). We select an ordering of the variables that posits the degree of within-year endogeneity of each of the three variables of interest. For perspective, the variables that appear earlier in systems are more exogenous than those that appear later (Love and Zicchino 2006). In the 1980s, China was in a weak economic state, with shortages of both investment and HC, and FDI has subsequently played a key role in stimulating the accumulation of HC in China. In recent years, the ordering of “FDI–HC–OFDI” is taken for formulating the VAR model.

One drawback of employing panel VAR is that the number of degrees of freedom decreases drastically with each additional variable introduced into the dynamic system. Based on this consideration, we limit our system to three variables. 4 To address the problem of the standard fixed-effect estimator (Nickell 1981), we follow the Helmert procedure (Arellano and Bover 1995). Taking lagged values as instruments, we identify the panel VAR model using the least squares dummy variable estimator as follows:

where

In the baseline analysis, we focus on the results from IRFs and forecast error variance decompositions (FEVDs). After generating the reduced-form results and the moving average representation of the model, the IRFs and FEVDs are derived by Monte Carlo simulations with 1,000 repetitions. IRFs are used to simulate how a variable reacts to one standard deviation of shock in the disturbance term in period t, holding all other shocks at 0. FEVDs can further show the explanatory ability of one variable relative to the others.

We choose a one-lag specification throughout the analysis of this study 6 for the following reasons. First, considering the time length limitations in our sample, and as Attinasi and Metelli (2017) mention, there are not as many degrees of freedom as in the finance literature wherein high-frequency observations are available. Second, keeping the lag structure consistent facilitates direct comparability between results obtained in this study. 7 Finally, the credibility of information criteria has been doubted in the econometrics literature (for details, see Han, Phillips, and Sul 2017).

At different stages, the dynamic system “FDI–HC–OFDI” can display different characteristics. To explore the differences between the pre- and post-2008 periods, we conduct the panel VAR analysis separately on both the frames.

Furthermore, to rule out the possibility that the regional GDP level may influence the dynamic system “FDI–HC–OFDI,” we divide our provincial sample into two groups according to their average RGDP during the period 2004–2015 using USD 154,813 as a cut-off value. 8

Data

There is extensive debate on the measurement of HC because of its conceptual multidimensionality and data limitations. The most common proxy of HC is average years of schooling, which assumes that more education makes it easier to master new technologies (Easterlin 1981; Florida 2002; Fraumeni 2015; Mincer 1989). Education has been preferred by macroeconomic researchers as an HC measurement for growth inequality since 1980s (Barro 2001). For example, Jones (2014) confirms that variation in average education attainment can explain different income levels across countries. However, Fraumeni (2015) notes that younger individuals have a significantly higher educational attainment but lower income level than older people. Hence, lifetime income measures, including expected future working experience and all individuals’ income in a country, are recommended.

Furthermore, HC is a more comprehensive concept than education. Among early attempts to construct an HC account, Kendrick (1976) considers an investment approach. In this approach, HC is regarded as a combination of accumulative investment expenditures and depreciated existing stocks. The investment factors he considers include human capital-related expenditures, such as child raising, education, training, medical, health, safety, and transportation. Ederer (2006) adopts an HC endowment measure for European countries. This measure considers not only investment of formal education but also family background and working experience. Nevertheless, it is not tractable in the Chinese context because of data limitations.

In addition to investment, income is perceived as another important dimension, as it relates to consumption and investment (Z. Yang and Pan 2020a, 2020b). Some research constructs an index value rather than a monetary value (Le, Gibson, and Oxley 2003; Mulligan and Sala-i-Martin 2000). One advantage of this index is that it takes into account the heterogeneous quality and relevance of schooling. However, in such a setup, the Cobb–Douglas-style assumption could lead to a decrease in HC if the growth of GDP were slower than that of physical capital.

Considering data availability and quality, the data for the quantitative analysis are from the project “China’s Human Capital: Measurement and Index Construction” 9 (H. Li et al. 2013, 2014). The calculation of HC is based on the Jorgenson–Fraumeni (J–F) lifetime income approach. The lifetime expected incomes are as follows:

where Ly, s, a, e represents the population by year, gender, age, and education level, and mi is the expected future income of the population in each stage.

From the above formula, we know that an important component of the income approach is the estimation of future potential earnings for all individuals in the population. This can be expressed in the expansion equation of the following Mincer function:

where ln(inc) denotes the logarithm of income. Avwage represents the nominal value of per capita net income within the province. Avgdp is the nominal GDP per capita. Ratio means the primary industry employment ratio of the total working population. Sch is the years of education. Exp and Exp2 represent the work experience in years and the squared term, respectively. u is the error term. For coefficients, β2 represents the marginal returns to education; β3 and β4, the parameters of Sch·Avgdp and Sch·Ratio, respectively, capture the job market situation of the educated population; and β5 and β6 together explain the return-to-work experience. They derive these coefficients by regressing micro-level data from the Urban Household Survey, China Health and Nutrition Survey, Chinese Household Income Project, China Household Finance Survey, and Chinese Family Panel Studies.

Compared to traditional measurements, such as years of schooling, this dataset is suitable for the analysis in this study for several reasons. First, by combining conventional factors, the extended J–F framework measures HC comprehensively. The J–F lifetime income approach highlights the importance of long-term investments, such as education and health, in HC accumulation. Moreover, this method emphasizes informal channels of HC accumulation, such as work experience. Second, unlike other approaches, the income approach makes the data measured in currency comparable to economic factors and facilitates understanding of the volume of HC from an economic perspective. Third, this method is in line with the Organisation for Economic Co-operation and Development (OECD) standard. Recently, research in OECD countries has focused on calculating the country’s total HC stock and developing J–F national HC accounts. Since it also applies the J–F framework, this HC index by the China Center for Human Capital and Labor Market Research may also be regarded as an adjusted Chinese HC account. Thus, it enables international comparisons in the case of globalization. The HC data used here are nominal HC stock. 10 To facilitate data comparability, we transform the HC data from renminbi to USD by the annual average exchange rate. All data are measured in million USD.

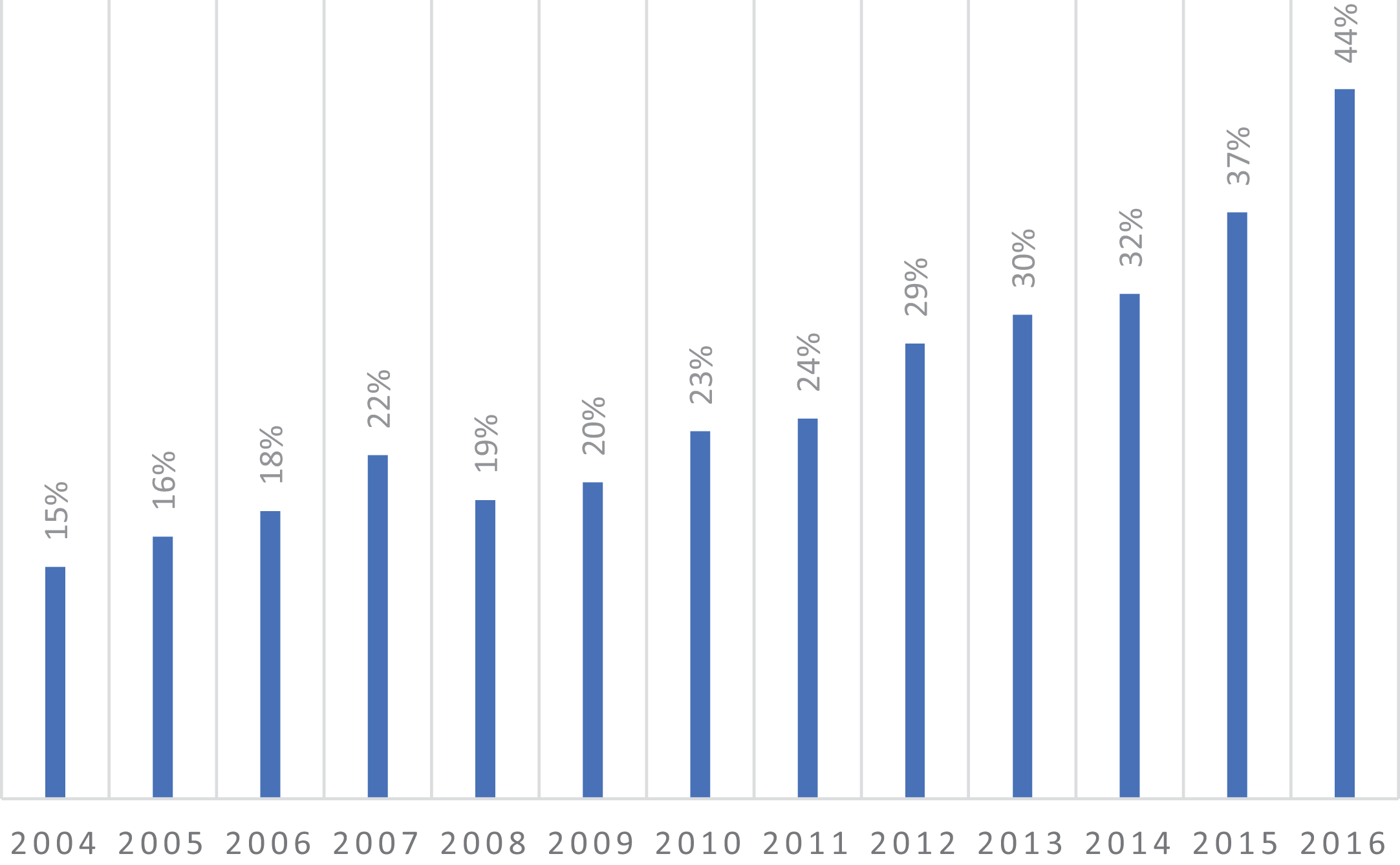

Chinese regional data on FDI, OFDI stock, and RGDP are collected mainly from the Report on Foreign Investment in China, the Statistical Bulletin of China’s Outward Foreign Direct Investment, and the China Statistical Yearbook (Figure 4). 11 Since the Ministry of Commerce provides provincial or regional OFDI data beginning from only 2004, the analysis is performed on thirty-one provinces in China for the period 2004–2015. 12

Proportion of regional OFDIs in China during 2004–2016.

Shifting Role of HC in Facilitating Globalization in China

Baseline Analysis

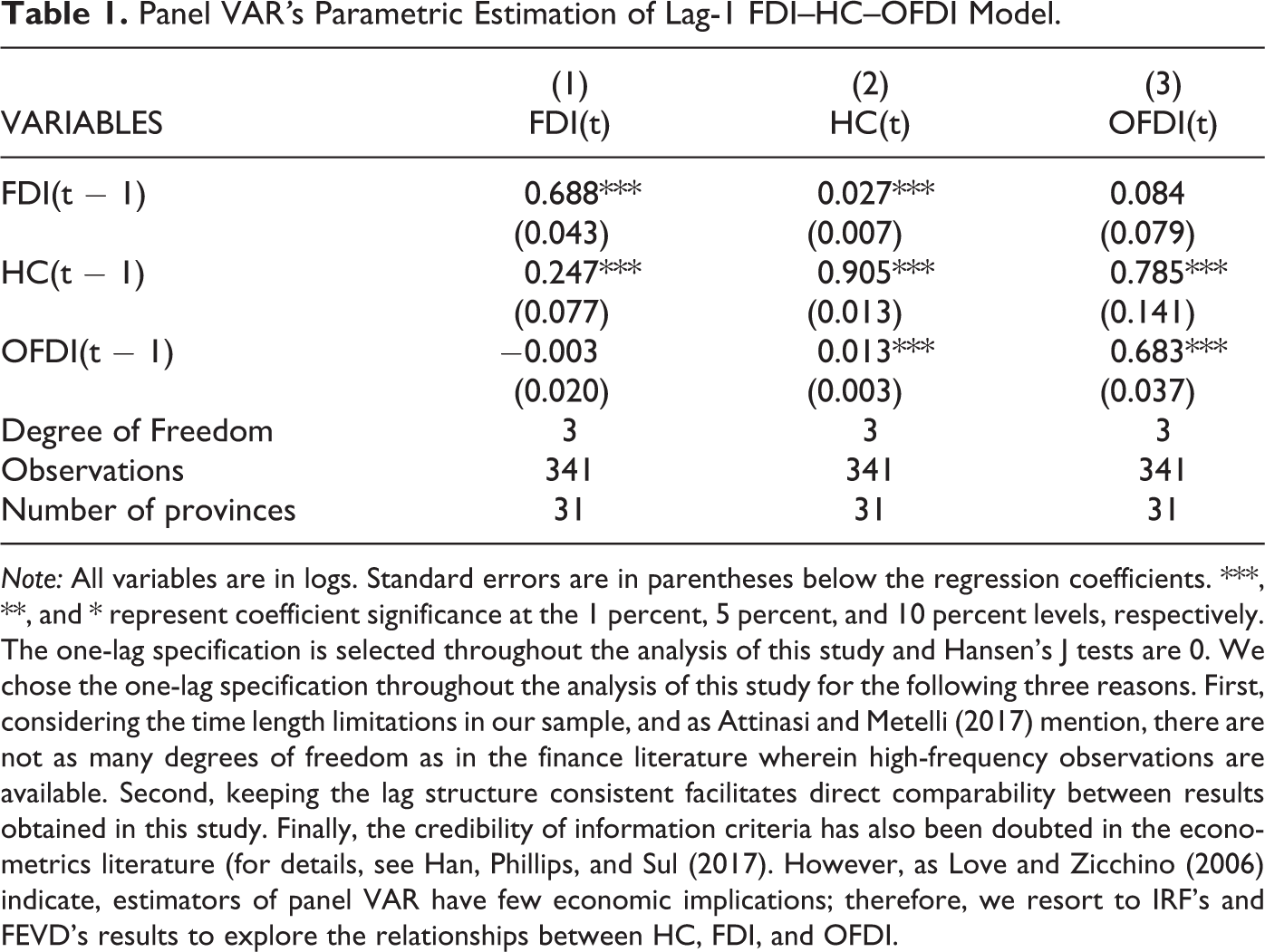

The results of the panel VAR model are presented in Table 1. The one-lag HC associated with both FDI and OFDI is statistically significant. FDI and OFDI with one lagged term contribute to HC accumulation. However, as Love and Zicchino (2006) indicate, estimators of panel VAR have few economic implications; therefore, we resort to the results of IRFs and FEVDs to explore the relationships among HC, FDI, and OFDI.

Panel VAR’s Parametric Estimation of Lag-1 FDI–HC–OFDI Model.

Note: All variables are in logs. Standard errors are in parentheses below the regression coefficients. ***, **, and * represent coefficient significance at the 1 percent, 5 percent, and 10 percent levels, respectively. The one-lag specification is selected throughout the analysis of this study and Hansen’s J tests are 0. We chose the one-lag specification throughout the analysis of this study for the following three reasons. First, considering the time length limitations in our sample, and as Attinasi and Metelli (2017) mention, there are not as many degrees of freedom as in the finance literature wherein high-frequency observations are available. Second, keeping the lag structure consistent facilitates direct comparability between results obtained in this study. Finally, the credibility of information criteria has also been doubted in the econometrics literature (for details, see Han, Phillips, and Sul (2017). However, as Love and Zicchino (2006) indicate, estimators of panel VAR have few economic implications; therefore, we resort to IRF’s and FEVD’s results to explore the relationships between HC, FDI, and OFDI.

Figure 5 shows that the sources of HC accumulation (second column) are from HC, FDI, and OFDI, with the response of HC to FDI and OFDI at 0.016 and 0.010, respectively, based on a one standard deviation shock in the sixth year. These findings support the argument that FDI benefits knowledge spillovers. In addition, the results indicate that such effects reach their peak about six years after the inflow of FDI. This impact is evident in local wealth creation, enhanced educational and training capacity, and improved HC in China.

Impulse-response function from the baseline model.

HC plays a key role in attracting FDI and outputting OFDI. FDI reacts positively to the HC shock, peaking at 0.017 in the sixth year. This is consistent with the literature emphasizing the importance of HC on FDI inflows (Easterlin 1981; Lucas 1990; Noorbakhsh, Paloni, and Youssef 2001; Salike 2016). The time lag of six years at the peak may indicate a matching process of foreign investment and local labor forces in China, such as the search for cheap labor, especially at the early stages of the opening of the Chinese economy, or the search for skilled labor in the high-tech industry, which involves the process of embedding in local social networks (Yeung, Liu, and Dicken 2006). By comparison, OFDI’s response to a one standard deviation HC shock reaches 0.057 in the seventh year, which is much higher than that for FDI, indicating that HC plays a more critical role in outputting OFDI than in FDI. The fact that many Chinese firms have not performed well outside of China, as evidenced by a drop in stock prices or failure in acquisition, shows that knowing the market, which includes cultural awareness (Li, Liu, and Qian 2019), laws, and social networks, may be more important than merely holding capital.

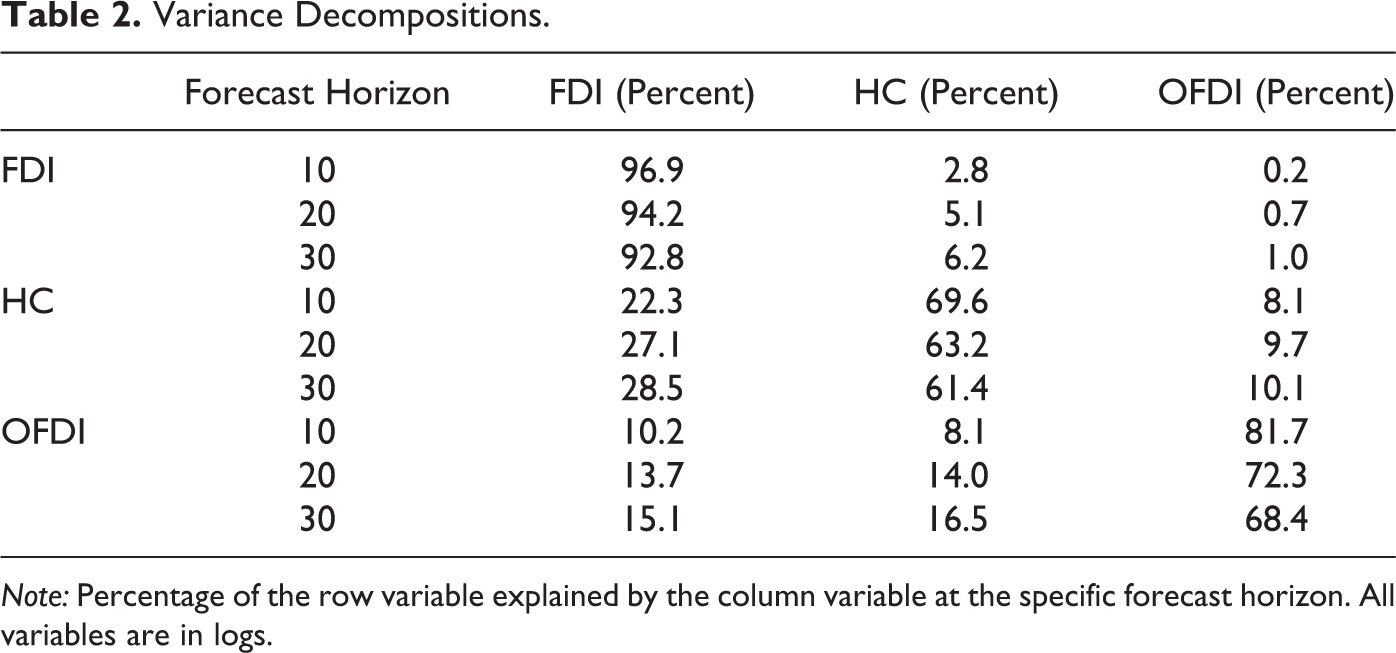

Variance decomposition can be used to further understand relative weights on the sources of impacts (Table 2). The role of HC in affecting the variance of FDI increased from 2.8 percent to 6.2 percent and accounted for OFDI’s variation from 8.1 percent to 16.5 percent, respectively, from tenth to thirtieth years. In addition, the HC pattern is quite stable in the ten to thirty-year period, with approximately 22.3 percent to 28.5 percent of the change by FDI, 8.1 percent to 10.1 percent by OFDI, and 69.6 percent to 61.4 percent by HC itself, confirming that globalization has not only boosted regional economic performance but also helped China to accumulate HC through international exchange of labor.

Variance Decompositions.

Note: Percentage of the row variable explained by the column variable at the specific forecast horizon. All variables are in logs.

Pre- and Post-Financial Crisis

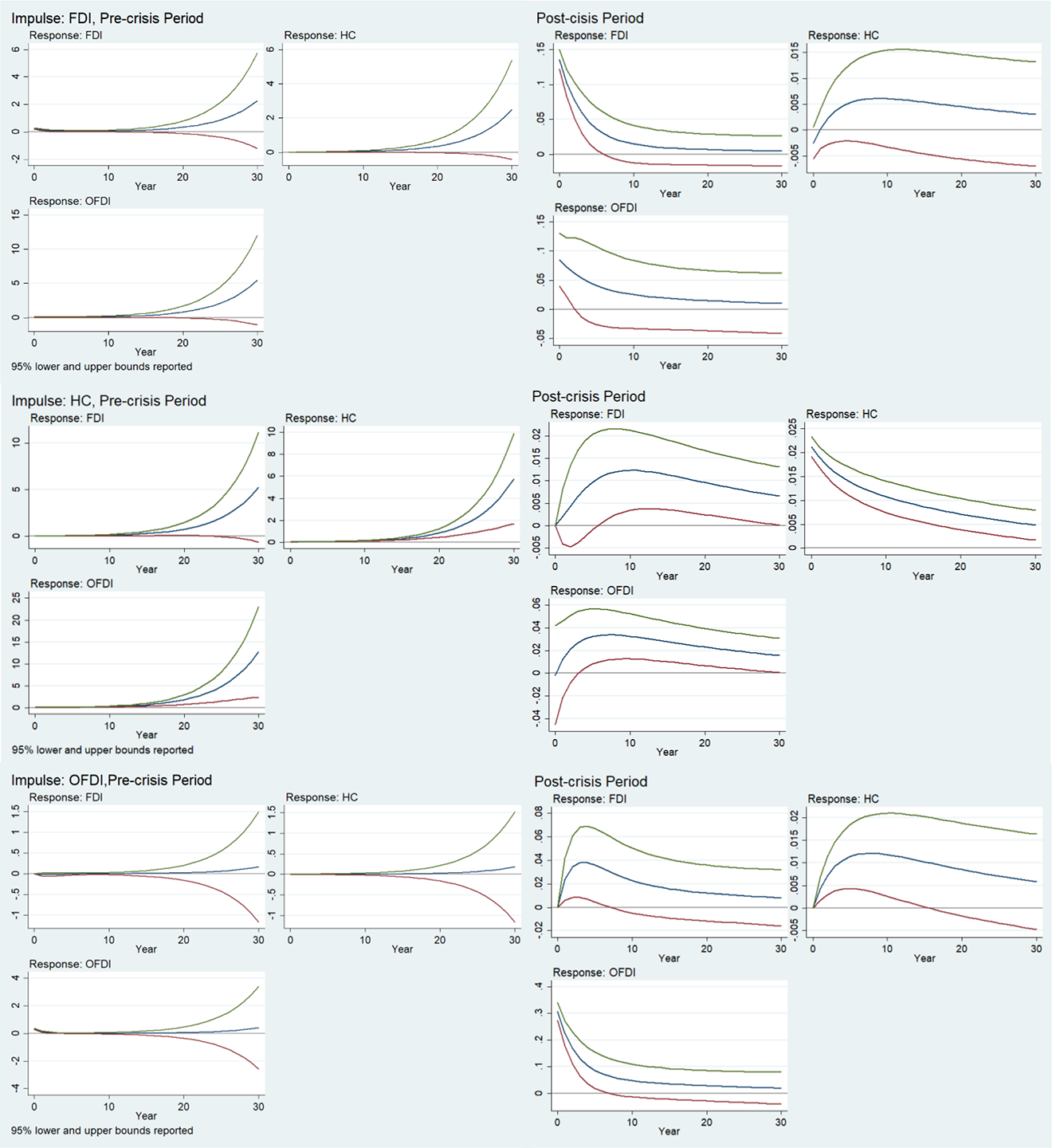

IR helps to capture the dynamic relationships among the three variables. However, these relationships may vary given different financial endowment levels. To assess the effects of an exogenous shock to HC, FDI, and OFDI, in this subsection, we separately compare IR patterns in different periods. As shown in Figure 6, there are dramatic structural changes in the interrelationship of HC, FDI, and OFDI before and after 2008 based on the significantly different IRF patterns.

Impulse-response functions between 2004–2008 and 2008–2015.

The dynamic response of each key variable to exogenous shocks grew before 2008. Specifically, for all IRs in the pre-crisis period, the magnitudes of all coefficients are positive; this is consistent with circular casual interrelationship among HC, FDI, and OFDI. Therefore, the IR patterns before 2008 confirm that Chinese regional economies benefited from participating in the global economy, and a positive circle was formed and enhanced among HC, FDI, and OFDI.

This situation, however, changed after 2008, with different trends and rising patterns in the IRF among those three vectors. In particular, the response of HC to an FDI shock reached a peak of 0.006 for the six-year lag, and reached 0.012 to an OFDI shock at the seven-year lag, implying that HC accumulation in China still needs to actively interact with the global market, even though it has already benefitted significantly from globalization. HC accumulation mainly has resulted from higher competition for investments, including the OFDI reform by the Chinese government, the comparative advantage of Chinese economic endowment, and trade conflicts in the global market.

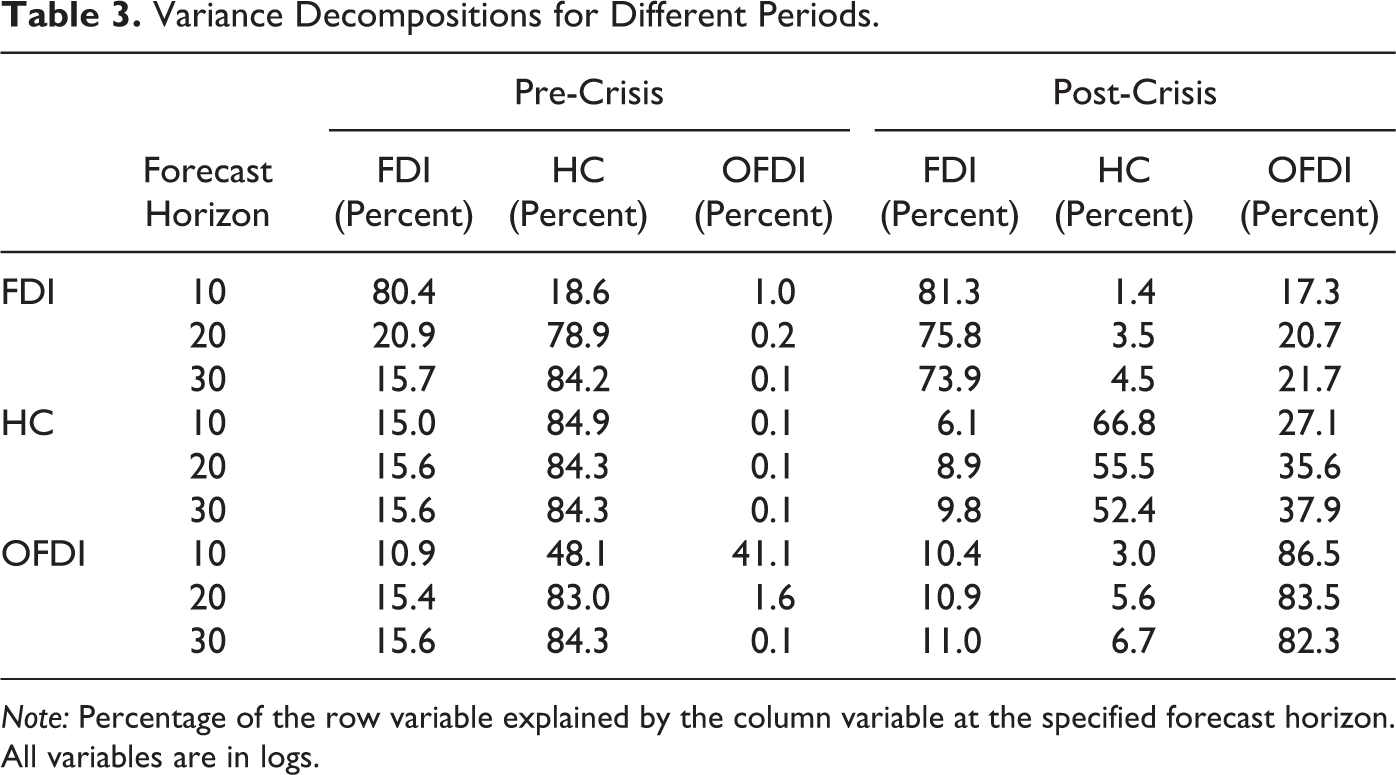

Next, we compare variance decomposition results for different time periods. Taking ten years as an example, HC contributed 18.6 percent and 48.1 percent to the variances of FDI and OFDI during the pre-crisis period to dramatically fall to 1.4 percent and 3.0 percent, respectively, after the crisis (Table 3). This indicates that even though HC strongly contributed to the Chinese economy before 2008, HC cannot satisfy the new demand for FDI and OFDI. The underlying reason is that the whole economy is transitioning from high- speed to high-quality development. After 2008, a salient trend is that OFDI had a stronger impact on HC, FDI, and OFDI (Table 3), reflecting an increase in China’s active involvement in the global economy. In particular, the main sources of HC variation changed from 84.3 percent (HC) and 15.6 percent (FDI) before 2008 to 55.5 percent (HC) and 35.6 percent (OFDI) after 2008. This means that OFDI not only has created job opportunities for Chinese but also has provided more chances for Chinese to update their knowledge from the host countries. For example, more than 50 percent of 2.837 million staff members employed by overseas Chinese enterprises were from China at the end of 2015, which is similar to the scale of a large city in China. When these staff return to China, they are able to contribute to China’s future HC accumulation.

Variance Decompositions for Different Periods.

Note: Percentage of the row variable explained by the column variable at the specified forecast horizon. All variables are in logs.

Overall, a comparison of the results from IR and variance decomposition imply that the role of the Chinese economy in the global economy shifted after the global financial crisis. Furthermore, the results show that the Chinese economy underwent a structural transformation during the globalization process, with HC accumulation driven by a more active going-out strategy.

The Role of HC at Different Development Levels

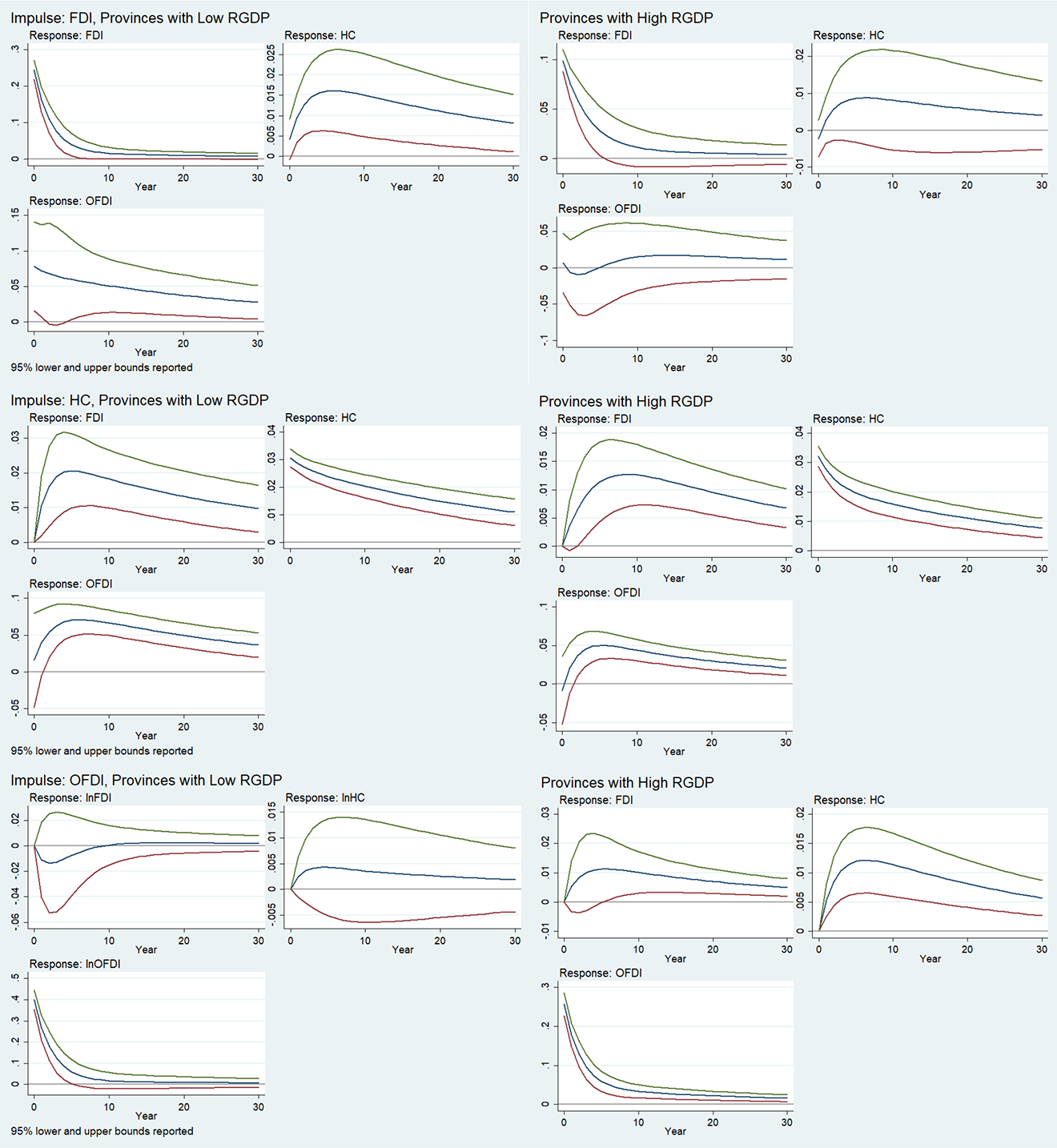

Figure 7 reports the results of IRFs at different development levels. As for the FDI impulse, the response of FDI itself was higher in low-development regions than in higher-development regions at the beginning of the period, reflecting stronger path dependence or follow-up effects for regions with lower development levels. For example, in the low-RGDP group, Chongqing’s FDI grew fastest (988 percent) in China during the period of 2004–2015 through industrial transfer. In another example, FDI in the Guizhou Province increased from USD 2.234 billion in 2004 to more than USD 18 billion.

Impulse-response functions between the low- and high-GDP groups.

The HC response to the FDI impulse was stronger in regions with low development levels. As in the second stage of IDP, there was a learning-by-doing and know-how transmission process for local HC. For example, FDI in Chongqing promoted the quality of skilled workers. According to the 2010 National Census and 1 percent National Population Sample Survey in 2015, the share of workers with education level higher than a high school qualification grew from 10.38 percent to over 14.24 percent in Chongqing, while, in Guangdong, the change was from 10.73 percent to 13.92 percent.

Figure 7 suggests that OFDI reacts positively to FDI in regions with lower development levels, but the same relationship was not replicated in regions with higher levels of development. Furthermore, there is a clear contrast in the IRF of FDI to OFDI between regions with low and high development levels. Such reactions rarely occur in the former group but reach a 0.1 standard deviation of the OFDI shock for the latter group. Therefore, OFDI can be induced by FDI in provinces with low GDP, while OFDI helps to attract FDI in the higher-development regions. This can be explained theoretically by the recursive process of local wealth creation with FDI and OFDI in provinces with different development levels. As regional GDP grows, outward investment becomes a business strategy aimed at extending the region’s market. Hence, OFDI may introduce some inward FDI through the process of international commercial collaboration. Owing to these two processes, such regions as Guangdong and Zhejiang with high FDI have become sources of OFDI. In particular, Guangdong, ranking third in FDI absorption, has the largest stock of about 25 percent of the top ten local OFDI sources among provinces in China in 2015.

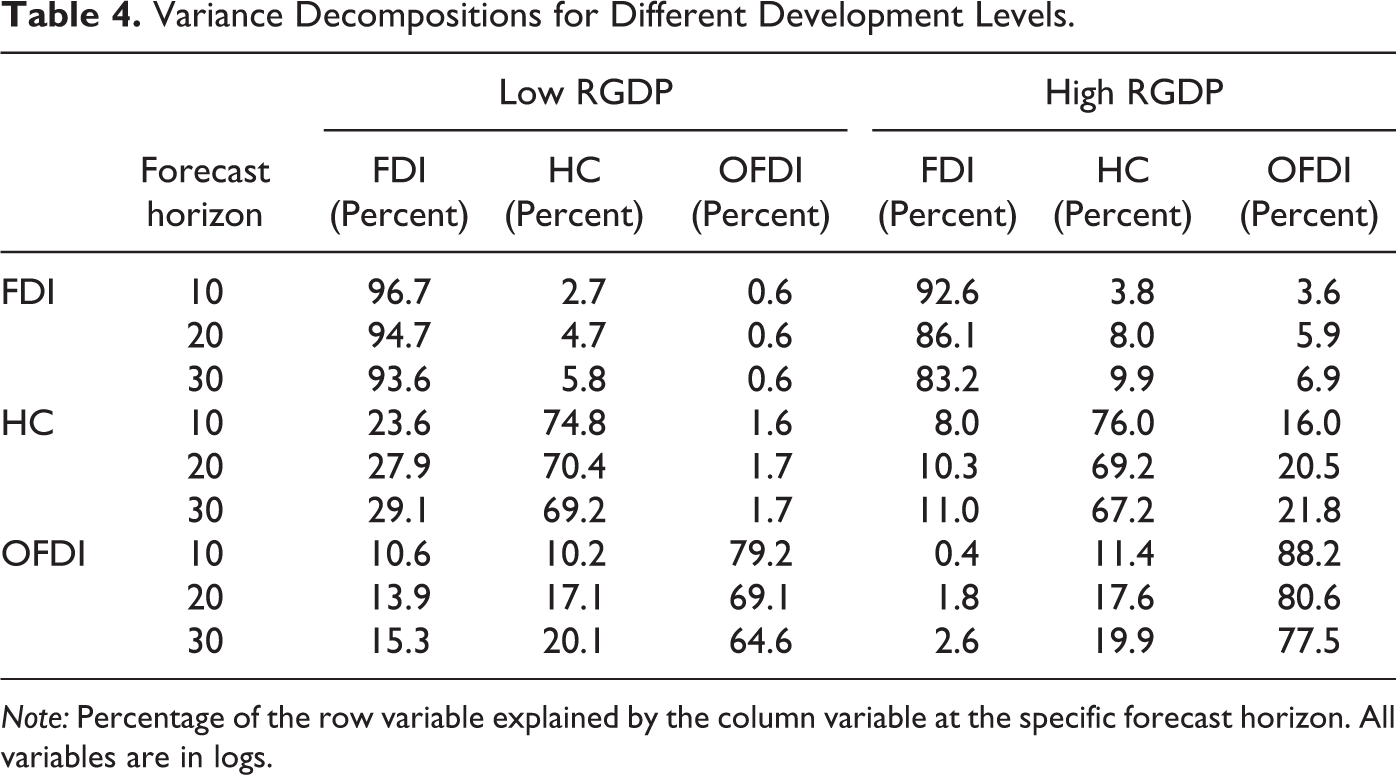

Table 4 shows that the level of HC can count for a slightly higher share of change in FDI and OFDI when the development level is high. The same impact is detected for OFDI on the other variables and itself. Moreover, unlike the low-RGDP group in which HC accumulated 1.6–1.7 percent from OFDI, the explanatory ability of OFDI on HC was around 20 percent. This suggests that HC accumulation is more dependent on FDI in low-RGDP regions that need investments to promote workers’ skills, such as the quid pro quo policy in the early period of opening up in China (Holmes, McGrattan, and Prescott 2015). 13 However, consistent with what we find from FEVDs for the post-crisis period, HC relies more on OFDI in high-RGDP regions that need a larger international market. This is because FDI cannot meet the needs of updating knowledge.

Variance Decompositions for Different Development Levels.

Note: Percentage of the row variable explained by the column variable at the specific forecast horizon. All variables are in logs.

Robustness Checks

5.4.1 Baseline results with RGDP

In light of new growth theory, economic development measured by GDP should be a control variable in panel VAR regressions. This would aid understanding of whether GDP growth is the result of economic development, or HC itself. Therefore, we also report results with the additional control of RGDP. As shown in Appendix Figures B1 and B2, we observe similar patterns as the baseline results for both IRF and FEVD.

5.4.2 Alternative measurements for HC

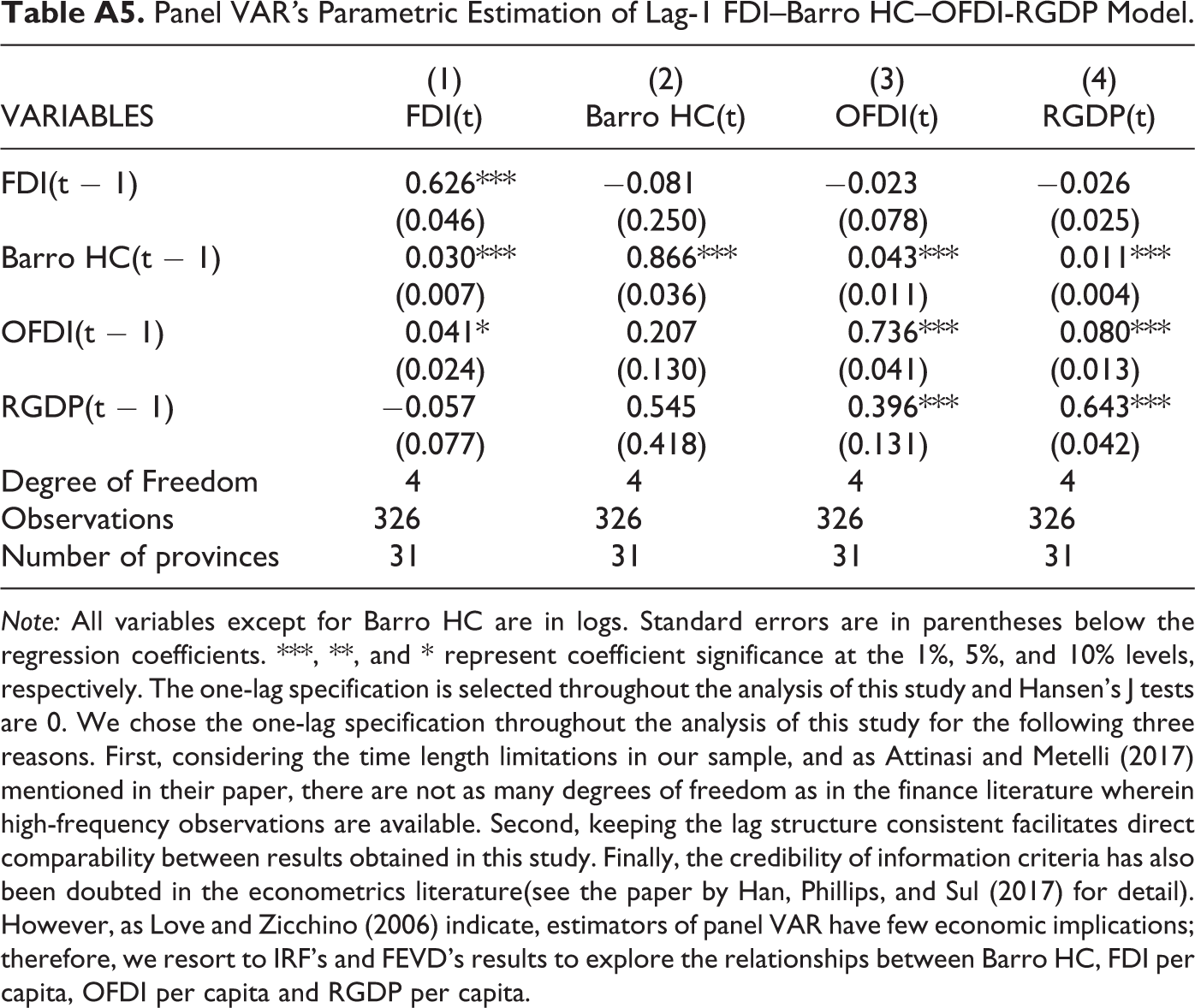

Here, we also consider other HC measures that do not discriminate on whether smaller cities can be used for the robustness tests, including the share of college degree holders and Barro-style HC (Barro 2001). When using these relative measures for HC, we use per capita measures for FDI, OFDI, and RGDP. The results of the panel VAR are reported in Appendix Tables A4 and A5. As implied in Appendix Figures B3 and B4, IRF and FEVD are robust if we use the share of college degree holders as a proxy for HC. Furthermore, Appendix Figures B5 and B6 use Barro HC as a proxy for HC and imply consistent results.

Conclusion

The global economy has been changing continuously amid uncertainty and ongoing new events. The reversal of a region or a country from being a borrower to a lender of investment funds is a vivid example of such changes. This study used the Chinese economy to investigate this process and the underlying role of HC. Using panel VAR models, this study explored the dynamic relationships among FDI, HC, and OFDI. First, our baseline analysis of IRFs implies that FDI benefits knowledge spillovers and HC plays a key role in both FDI and OFDI accumulation. Second, variance decomposition indicates that HC plays an increasingly key role in absorbing inward FDI and promoting outward investment. Third, the dynamic interrelation of HC, FDI, and OFDI varies across different time periods and different development levels. It is noteworthy that FDI contributes more to HC before 2008 while OFDI dominates FDI in the process of HC accumulation after 2008. This finding suggests there has been a structural change in the Chinese economy in the process of globalization. We also find that the roles of OFDI and HC are larger in more developed regions than in less developed ones.

This study contributes to the literature by uncovering a new phenomenon of reversal in the process of globalization and the importance of HC in leveraging regions participating in the global economy. In the global economy, HC dramatically enhances the absorptive capacity of regions. HC helps to deal with external capital, knowledge, and technology, and, in return, contributes to an increase in transmissive capacity. HC accumulation becomes possible when accelerated technological progress, amplified societal wealth, and high family incomes induce increased investment for the formation of HC at school and in employment through an intergenerational financing process. Since knowledge and skills are key strategic resources to gain competitive advantage, HC can help a region to expand its external investment.

The study also has policy implications for other emerging economies. In particular, the rise of emerging economies, such as China, has led to a reversal, wherein the economy has been transformed from a receiver of external resources to a supplier of global resources, such as FDI. Our results emphasize that the local economy needs to be more active and positively cooperative with other countries. Facing the reality that the global economy (external resources) does not benefit everyone equally, absorptive capacity contributes to the examination of a region’s growth along with global influences, by inquiring about the region’s ability to employ internal capabilities to harness external capital assets (i.e., FDI).

Given the importance of investigating the dynamic relationships among HC, FDI, and OFDI, further research is needed to clarify and explore reversals by examining the linkages, roles, networks with dynamic capabilities, and variations in the global economy. The analysis could be improved if detailed data were available allowing the investigation of greenfield and brownfield investments.

Footnotes

Appendix A

Panel VAR’s Parametric Estimation of Lag-1 FDI–Barro HC–OFDI-RGDP Model.

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| VARIABLES | FDI(t) | Barro HC(t) | OFDI(t) | RGDP(t) |

| FDI(t − 1) | 0.626*** | −0.081 | −0.023 | −0.026 |

| (0.046) | (0.250) | (0.078) | (0.025) | |

| Barro HC(t − 1) | 0.030*** | 0.866*** | 0.043*** | 0.011*** |

| (0.007) | (0.036) | (0.011) | (0.004) | |

| OFDI(t − 1) | 0.041* | 0.207 | 0.736*** | 0.080*** |

| (0.024) | (0.130) | (0.041) | (0.013) | |

| RGDP(t − 1) | −0.057 | 0.545 | 0.396*** | 0.643*** |

| (0.077) | (0.418) | (0.131) | (0.042) | |

| Degree of Freedom | 4 | 4 | 4 | 4 |

| Observations | 326 | 326 | 326 | 326 |

| Number of provinces | 31 | 31 | 31 | 31 |

Note: All variables except for Barro HC are in logs. Standard errors are in parentheses below the regression coefficients. ***, **, and * represent coefficient significance at the 1%, 5%, and 10% levels, respectively. The one-lag specification is selected throughout the analysis of this study and Hansen’s J tests are 0. We chose the one-lag specification throughout the analysis of this study for the following three reasons. First, considering the time length limitations in our sample, and as Attinasi and Metelli (2017) mentioned in their paper, there are not as many degrees of freedom as in the finance literature wherein high-frequency observations are available. Second, keeping the lag structure consistent facilitates direct comparability between results obtained in this study. Finally, the credibility of information criteria has also been doubted in the econometrics literature(see the paper by Han, Phillips, and Sul (2017) for detail). However, as Love and Zicchino (2006) indicate, estimators of panel VAR have few economic implications; therefore, we resort to IRF’s and FEVD’s results to explore the relationships between Barro HC, FDI per capita, OFDI per capita and RGDP per capita.

Appendix B

Acknowledgment

We would also thank Prof. Mick Dunford for his insightful comments and encouragement.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research is sponsored by a grant of Supported by the Strategic Priority Research Program of the Chinese Academy of Sciences (Grant No. XDA23100402), the Natural Sciences Foundation of China (No. 41530751), the support from Early Career Talent Program of Chinese Academy of Sciences “Youth Innovation Promotion Association CAS” (Y201815), and Kezhen Talent Program of IGSNRR, CAS (2016RC101).