Abstract

Local governments in Georgia are empowered to levy a 1 percent local option sales tax (LOST), approved by referendum at the county level and is distributed to the county and qualified municipal governments (The terms city and municipality are used interchangeably throughout this article, per OCGA 36.30.1.). Distribution shares are not based on a strict formula but rather are renegotiated at certain trigger points, including the decennial census. Using a multiple regression model, this research analyzes contextual and management factors, finding the strongest predictors of increased LOST revenue share by cities to be designation as county seat, fewer fellow municipalities, and higher reliance on LOST in the city’s total revenue stream.

Introduction

The State of Georgia authorizes local jurisdictions up to 3 percent collection of local option sales taxes (LOSTs). These taxes are assessed at the county level and each percentage point is directed to a different purpose. 2 The three most common are the Educational Local Option Sales Tax (ELOST), which provides support for local school systems and not the city/county government at hand; 3 the Special Purpose Local Option Sales Tax (SPLOST), which is approved at the county level by referendum for a designated list of capital projects; and the LOST, which is general purpose revenue with the stated purpose of a property tax rollback for property owners within the jurisdiction. This ELOST–SPLOST–LOST combination is in place in 147 of the state’s 159 counties. 4

Though levied at the county level, qualified city governments within the respective county are entitled to a portion of that LOST revenue. While they are guaranteed a proverbial seat at the table, there is no strict formula for determining the proportion of LOST revenue received by each actor. Rather, city and county governments are obligated to negotiate that distribution at particular trigger points, including obligatory renegotiation every ten years (postcensus). The renegotiation process is structured by state code (Official Code of Georgia, Annotated [OCGA] 48-8), which provides eight bases for distribution shares. The objective of this research is to identify factors predicting shares (collectively amounting to 1.00 or 100 percent within each applicable county) of the LOST revenue to cities in their respective counties.

Previous research on LOSTs has focused heavily on the fiscal theory of the LOST as a tax instrument and focused strictly on public budget and finance literature. This research contributes to the understanding of interjurisdictional and management factors related to the proportional share of LOST revenue received by municipal governments.

Literature Review

The factors at play in LOST distribution, and the literature and theories associated with those factors, are plentiful. Previous research in interjurisdictional relations and outcomes from the municipal perspective is best understood as being either contextual or self-determined in nature. The contextual variables are those in which the city government has little, if any, influence or ability to change. The self-determination variables are those in which the city has the ultimate control.

Contextual Factors

Contextual factors create an environment in which the government functions and address concerns about equity and necessary intergovernmental relations. The overarching concept in LOST distribution is “something for everyone.” While this ensures all jurisdictions access to this revenue stream and seems to have had a positive influence in adoption of LOST in Georgia, the concept does not preclude a county from having a perceived “unjust” allocation of sales and use taxes (Hosseini 2009). Because distribution is a zero-sum game (one government’s take of LOST has direct implications on another’s), there is inherent pressure to take advantage of all plausible claims with little regard to the implications on others.

Beyond Georgia, this was seen in the Bradley-Burns Act (BBA) in California which set out to establish an “integrated uniform system” for sales tax. BBA provides that counties in the state can impose a sales tax of up to 1.25 percent. Cities, in turn, can levy up to 1 percent. The caveat in California’s local sales and use tax provisions is that because cities are geopolitical subsets of the county, the entirety of the city’s municipal sales and use tax is counted against the maximum 1.25 percent at the county level (without required consultation or consent of the county). This could leave the county government with as little as .25 percent sales and use tax within certain parts of their jurisdiction through by virtue of the actions of others.

Literature on intergovernmental relations is often characterized in terms of vertical (local–state–federal) and horizontal (city–city, county–county, state–state) relationships (O’Toole 2007). Throughout this literature, there is little definition of the county–city relationship—some have suggested that the municipality is fundamentally subordinate to the county, while others contend the opposite. Cities are geopolitical subsets of counties and the dynamic of that relationship often differs on a case-by-case basis. This is seen in the BBA example in California juxtaposed with Georgia, where both city and county provide comparable menus of services/facilities and share from a fixed pool of LOST resources, and Oklahoma, where county and municipal governments are empowered to make independent tax rate decisions without implications on the other (Hosseini 2009; Burge and Rogers 2010). There is little consistency in the perception and treatment of the city–county relationship and previous research provides little clarity on any potential political predominance of one over the other.

Further complicating the interpretation of the city–county relationship is the legal treatment of municipal and county governments, which varies from state to state. While Georgia’s counties have obligatory constitutional duties, cities do not. Similarly, while county governments are exhaustive of the entirety of the state, cities are not—roughly 9.3 percent of the state’s land area and 45.9 percent of the state’s population are in an incorporated area. Even with these differences, both city and county governments in Georgia yield home rule. The result is potential for divergence and conflict among entities with comparable interests, authorities, and responsibilities.

Management Factors

Local governments are empowered to make these management decisions, are responsible for implementation, and bear ultimate responsibility for the outcomes. Of particular interest in this research are decisions surrounding revenue management and form of governance.

The ability of local governments to levy sales and use taxes on their own accord has grown over the past half century. At present, forty-five states impose a general sales tax (Alaska, Delaware, Montana, New Hampshire, and Oregon do not). Thirteen states do not permit sales and use taxes to be assessed at the local level. Delaware and New Hampshire are the only two that have neither a statewide or local option sales tax. Consequently, the tax rate in both states is 0%. (Bjur et al., 2008, Drenkard, 2012). Sales tax as an empowerment mechanism for local governments has four widely accepted goals: (1) a means to fund additional services; (2) a contribution to revenue stability through diversification, flexibility, and responsiveness; (3) property tax relief; and (4) an ability to capture revenue from nonresidents, also known as exporting the tax base (Jung 2002).

Previous research has found success in Georgia: $.48 of every $1.00 of LOST revenue in Georgia goes toward increased spending, supporting the concept of additional services; $.28 for every $1.00 of LOST revenue provides property tax relief; and revenue streams have become increasingly diversified (Jung 2002; Pajari 1984). Beyond Georgia, these objectives have been achieved in Illinois, Oregon, and Utah (Krmecec 1991; Lucier 1970; McKeown 2000).

Revenue management includes other concepts. Relevant to this research are the city’s involvement in the SPLOST process and decisions regarding revenue diversification, such as a property tax. It is impossible to divorce politics from taxation and issues of distribution. Political pressures from communities are unique and a jurisdiction’s response to those pressures can be vital. These revenue management decisions and the political responses by leadership within the city are internal actions for which accountability is an expectation.

A second management concept with direct implication on distribution is politics and leadership structure, specifically the municipal form of government. Georgia’s municipalities function under a council manager, mayor council, or commission form of government. The mayor council can be subdivided into strong mayor or weak mayor forms of government, but both ultimately lack the vested authority in a professional, appointed city manager or administrator. The manager is distinct from the mayor (whether weak or strong) in that the manager assumes leadership for many of the administrative tasks, brings experience and expertise to local government leadership, and contributes a level of professionalism that many believe does not exist under the leadership of a mayor. Beyond the professionalism, the manager’s role as community builder and facilitator/engager has grown and there are implications beyond administrative responsibilities (Wikstrom 1979; Nalbandian 1999). No matter what the perception of the manager, mayor, council, or the relationships that exist between the three, the decision regarding form of government is one that rests with the city and for which only they can be held responsible for the outcomes.

Research Question and Hypotheses

The importance of the LOST as a revenue source and the level of reliance on sales taxes in city budgets prompt the question, what are the factors predicting the share of LOST revenue Georgia’s cities are receiving? Cities are inherently complex, resulting in a number of plausible indicators that have been framed in the review of previous research and literature and that yield a series of hypotheses, both contextual and self-determined:

Hypothesis 1.1: In situations where there are a higher number of jurisdictions competing for LOST distribution, individual cities will receive a lower share of LOST revenue.

While the intergovernmental relationships that emerge as a result of LOST renegotiation are based on similar interests and are interactions that occur with regularity, there are political interests that emerge in an arena marked by stiff competition and limited resources (Agranoff and McGuire 1998). Consequently, more actors in the negotiation results in increased complexity of competitive relationships to the point where cities stand to lose ground.

Hypothesis 1.2: Cities assuming the role of county seat (home of the county courthouse, responsible for all state administrative functions) will receive a greater share of LOST revenue.

The city that serves as the county seat has long been shown to have a different dynamic in the county than their counterparts (Moxley and Proctor 1995; Schellenberg 1970). Previous research has indicated that there is a substantive relationship between status as the county seat and the leverage held by the given city (Rogers 2004). This would, in practice, apply to financial negotiations with the county. Typically home to increased consumer spending—restaurants, service-based establishments, stores—the county seat often has a higher level of retail spending than their counterparts, and thus increased leverage in negotiations (Price 1968). Further, Rogers (2004) finds those cities serving as county seat have a property tax base substantially different from other cities. Empirical research has found that county seats have greater ability to export the tax base and have sales tax revenues 3.32 percent higher. Because of this difference, the obligatory tie that exists by virtue of being county seat, and the generally higher level of interest paid to county seats by the public, it is reasonable to believe that this status may have value in predicting the city’s leverage in the negotiation process and ultimately on the LOST share received.

Hypothesis 2.1: If a city’s budget has a higher reliance on sales/use tax in total revenue, it will receive a greater proportion of LOST distribution.

At the county level, previous research has found that at the county level, LOST represents anywhere between 7 and 35 percent of total revenue and did not “exacerbate revenue disparity” (Jung 2002; Zhao and Hou 2008). On a practical level, a stated purpose of the LOST is property tax rollback which would introduce a higher level of revenue diversity to a city budget. With higher reliance on this source of revenue, there is inherent pressure placed on the city’s actors for higher distribution. The distribution has direct impact on revenue reliance, and with the disproportionate distribution found at the county level, similar impacts are expected for cities.

Hypothesis 2.2: Cities that do not assess a property tax will have a greater proportion of LOST distribution.

The sales and use tax and property tax are inextricably connected (Jung 2002). Stemming from Hypothesis 2.1, if a city is not receiving revenue by levying a property tax, necessary funds will have to be recouped from another source and the need for funds will put increased pressure on those negotiating on behalf of the city government.

Hypothesis 2.3: If a city receives SPLOST revenue for capital projects from county collections, they will receive a greater proportion of LOST distribution.

Cities receiving LOST revenue do not necessarily receive SPLOST revenue, and even in those cities receiving SPLOST, the share of revenue directed toward city projects has been less than 10 percent (Jung 2002). There are, however, instances of cities that qualify for these funds and engage in negotiations with their respective county for the “project list” that accompanies a SPLOST referendum. Because these cities have previous negotiation experience, the city has already demonstrated leverage in receiving support for capital project via SPLOST revenue, there will be a tendency toward the same leverage in garnering larger LOST distribution share.

Hypothesis 2.4: If a city has a council-manager form of government, it will receive a greater proportion of LOST distribution.

For many decades, the city manager has been acknowledged as both an administrator and a driving force in municipal policy (Almy 1975; Wikstrom 1979; Nalbandian 1999). While intended to bring professionalism into and politics out of city management, the two are inextricably connected. The nature of council manager cities has changed in recent decades, increasing their responsiveness to the political demands of their constituents (Frederickson, Johnson, and Wood 2004), but with professional management in place, cities continue to have a well-trained and full-time advocate for their interests and extract the greatest benefit for their jurisdiction.

Data and Methods

Data used in this research were generated by the Georgia Department of Revenue, Georgia Municipal Association, United State Census Bureau, and Carl Vinson Institute of Government at the University of Georgia. The unit of analysis in this study is the municipality and observations were dropped for municipalities located in counties in which there was no LOST distribution at the 2010 observation point: (1) seven in which LOST is diverted directly to the school district, (2) five which do not assess LOST, (3) one with no incorporated municipalities, and (4) one consolidated city–county government with no “orphan” cities that yield implications. This totals fourteen counties and sixty-nine associated municipalities.

In some instances, cities straddle county lines and can have geopolitical presence in as many as four counties. Those cities are entitled to LOST distribution within each county, but engage in each negotiation process separately. Consequently, each individual city–county combination is treated as a separate observation with appropriate variables being applied only to that pairing (proportion of county population, LOST revenue share, etc.).

In measuring the predicting factors of LOST revenue share among cities, this analysis will utilize a multiple-regression model. 5 Because the cumulative proportion of LOST distribution within each county is 1.00 and each county is a self-contained “zero-sum game” as acknowledged earlier, data are clustered by county and controls are included for both jurisdictional population and total revenue.

Research Findings

Among the 454 observations, the range of LOST distribution share is .0001–.8040 (.01 percent to 80.40 percent of LOST revenue), with an average of .1134 (SE = .1419). The most prominent predictor of distribution share is the proportion of the county’s population residing within the city. This is outlined as one of the eight bases for negotiation by state code and is used by some counties as the singular basis for determining distribution. Statewide, however, 49.50 percent of cities are receiving a LOST share greater than their share of the county’s population, 10.80 percent are receiving a share equal to their proportion of the population, and the remaining 39.70 percent receive a LOST share less than their share of the population, indicative of significant variation.

The first two hypotheses address situations in which interjurisdictional context is vital and two significant findings derive from these variables. The number of jurisdictions within the county and the designation as county seat are two variables that are beyond the scope of city leadership. The role of additional municipalities is important, as more actors competing for the same limited funds results in increased and more complex competition. Empirically, a higher number of municipalities within a given county has a negative coefficient, indicative of lower distribution shares for the individual cities within the county. Second is the county’s designation as county seat. The designation is relatively static (the last time a county seat was changed was 1937 in Bryan County with a shift from the now defunct city of Clyde to the city of Pembroke) and there is a statistically significant coefficient indicating a higher share of LOST distribution for those 145 cities than for their counterparts (Georgia Humanities Council 2011).

The second series of hypotheses focus on self-determined, management variables. Revenue management is a significant concern. Local government leaders must identify and maintain healthy, stable, and diverse revenue streams to ensure that the jurisdiction’s service delivery and debt service needs are met on an annual basis. Increased reliance on LOST revenues in the city’s overall revenue stream does generate a significant positive coefficient, indicative of higher distribution shares. As identified earlier, there are significant ties between LOST and property taxation in both state law and in revenue management practices, but the significant findings generated by higher reliance on LOST revenue are not seen in the decision to assess a property tax, which has no statistically significant relationship with LOST distribution share.

The third management-based hypothesis is whether or not the city receives revenue from SPLOST. By virtue of receiving funds (to any extent) from this special purpose tax, the city has engaged in negotiations with county leadership that is ultimately responsible for developing a list of capital projects for approval at referendum. Engaging in that project list development process and consequently receiving SPLOST funds is demonstrated to be significant, having a positive relationship with the LOST revenue share.

The final hypothesis focuses on the form of government employed by a city. When applied to the entire sample of cities, having a council manager rather than a mayor council or commission form of government has no significant impact on LOST distribution.

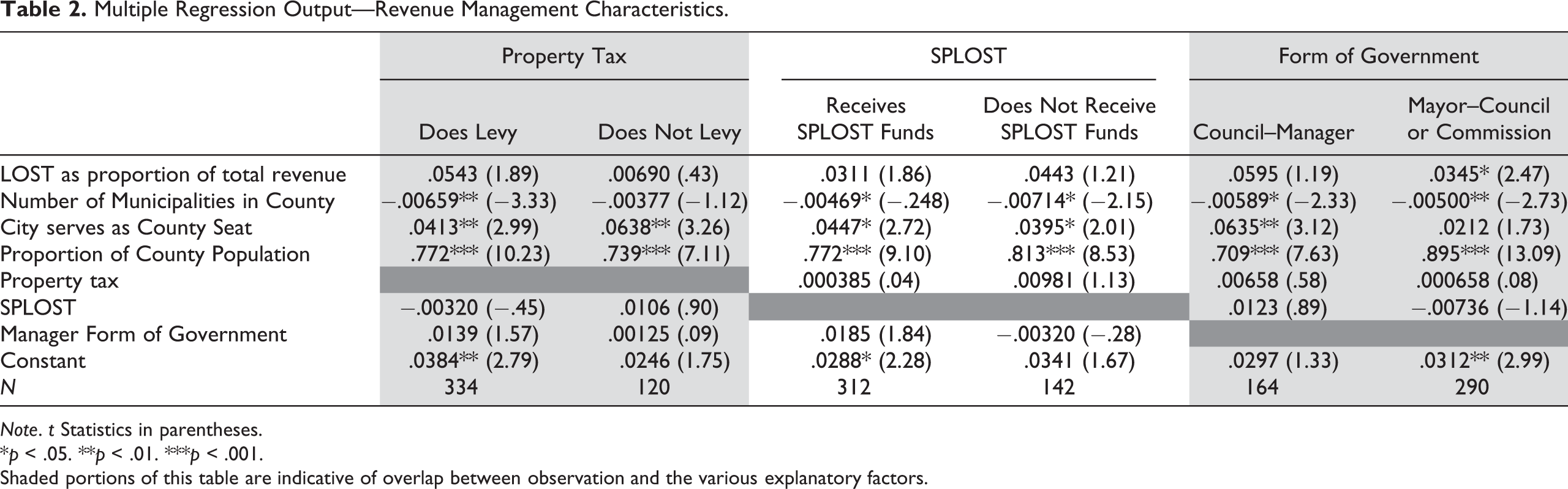

Beyond these broad findings, there are questions that can be addressed to subsets of the population of cities. Factors from the second set of hypotheses (Hypothesis 2.2 to 2.4) are self-determined in nature and it is reasonable to more deeply explore the potential implications of municipal decisions about these three management practices. The initial model (including all variables seen in Table 1) was reconstructed to focus on the options available to city governments as it relates to property tax assessment, SPLOST, and form of government, all seen in Table 2. For each of these, the dependent variable remained the LOST distribution share, but the variable of interest was dropped and regressions were run for cities based on their management practice.

Multiple Regression Output (Clustered by County).

Note. t Statistics in parentheses.

*p < .05. **p < .01. ***p < .001.

Multiple Regression Output—Revenue Management Characteristics.

Note. t Statistics in parentheses.

*p < .05. **p < .01. ***p < .001. Shaded portions of this table are indicative of overlap between observation and the various explanatory factors.

First, this analysis considers a city’s decision to assess a property tax. Within this data set, 26.4 percent (122 of 454) of the observed cities receiving revenue from the LOST do not levy a property tax, thereby limiting sources of tax revenue. The Georgia Municipal Association advises its members that in the case of these cities that do not levy a property tax (millage rate of 0) there is still an entitlement to LOST funds (LOST: Definitions, Legal Requirements, and FAQ 2011). Recalling that property tax rollback is an inherent part of the LOST legislation, the decision not to assess a property tax puts cities in a peculiar position. It is possible that a city uses LOST revenue to generate a property tax rollback equal to their total would-be property tax, resulting in no property tax. A second possibility is that a city decides not to assess a property tax and constructs a budget accounting for LOST receipts with the intent of not assessing a property tax. Regardless of the motive for their decision, the findings for these cities opting not to levy the property tax differ from those that do levy the tax. Among those cities opting not to assess a property tax, the number of municipalities located within the county (a consistently negative coefficient) is no longer significant and the proportion of the county’s population residing within the city is significant, though with a coefficient lower than those cities assessing a property tax. Regardless of decision to levy a property tax, SPLOST receipt, form of government, and LOST as proportion of revenue all lack significance.

The next subset considers SPLOST receipts. The SPLOST is similar to the LOST, in that it is assessed at a 1 percent rate at the county level, but is distinguished from the LOST in that it is subject to referendum every five years,6 is limited to capital expenditures, and appears on the ballot as a predetermined list of projects developed by local leadership based on projected revenue. Cities are not guaranteed access to SPLOST revenue in the same way that they are to LOST revenue, but many (68.7 percent) do receive SPLOST funds. From a quantifiable perspective, these SPLOST revenues serve to enhance the diversity of a city’s overall revenue and could consequently influence a city’s financial decision making. From a management perspective, it serves as an opportunity to engage in revenue sharing negotiations in a different context, to enhance professional skills, and to develop expertise in the necessary negotiation skills. The opportunity to negotiate and the experienced gleaned from that opportunity are valuable, as it was seen in the earlier regression that the city’s receipt of SPLOST revenue alone (as a 0, 1 measure) has a significant relationship with the LOST distribution share (Table 1). When separated and juxtaposed, the variables shown to be significant to cities receiving SPLOST funds are the same as those for cities not receiving SPLOST funds. The number of municipalities within the county, as was the case in the broader model, produces a negative coefficient for both; designation as county seat and proportion of the county’s population within the city were both positive; and the form of government, assessment of property tax, and reliance on LOST in total revenue streams had no significant relationship.

The final subset is city form of government. Among cities receiving LOST revenue, 36.1 percent have a council manager form of government. Among the three supplementary models (SPLOST, form of government, and property tax assessment), the differences seen in council manager versus other forms of government are the most substantial. Higher reliance on LOST revenues in the city’s total revenue streams produces statistically significant positive results for mayor council and commission forms of government, but not for their council manager counterparts. As was the case with the initial, all-inclusive model, a higher number of municipalities within the county has a negative impact on the distribution received by an individual municipality. This is consistent, regardless of form of government, though the negative coefficient is not as large for mayor council/commission forms of government, indicative of a somewhat mitigated effect of additional municipalities in those forms of government. Also, duplicative of the broader findings was the significance of the proportion of the county population living within the city. Both council manager and other forms of government were positive and significant, though the nonmanager cities generated a higher positive coefficient. The distinction between forms of government within the cities does not generate any significant results concerning receipt of SPLOST or assessment of property taxes.

Conclusion

In practice, these findings indicate certain characteristics that may prove advantageous for a city, given its population within the context of the broader county. Georgia law regarding LOST provides leverage to cities that they may not have otherwise.

Issues of overlapping jurisdiction are difficult to empirically address. One of the earliest and most prominent limitations of the theory in Intergovernmental Relations (IGR) and public choice literature was offered by Ostrom, Tiebout, and Warren. It is acknowledged that there is never a single government at play and that decisions by residents are never strictly based on the revenue/expenditure structure of a single jurisdiction. In the case of LOST distribution, a city resident has a vested interest both in the city and in the county where they reside. Any contention of a single-jurisdiction interest has “limited validity” and the resulting governance and negotiation processes are both a “crazy-quilt pattern” and an “organized chaos” (Ostrom, Tiebout, and Warren 1961).

What becomes increasingly evident as a result of this research is that the jurisdictional concerns that are beyond the scope of officials’ decision-making power and those management practices that are at the discretion of local officials have some relationship with one another.

Just as the cities that are the subject of this article are varied and diverse, so are the states and their laws surrounding local sales taxes. While Georgia provides leverage demonstrated in this model, studies applied to different structures in different states (thirty-five with sales and use tax options available to local governments) would be advantageous future research for a more thorough understanding of the differing roles of local governments in the context of American federalism.

City leaders must acknowledge and embrace their external and internal climates (contextual and managerial characteristics), using them to their advantage, and turn on critical eye on themselves, identifying and overcoming their unique challenges when sitting at the table with their counterparts from other local jurisdictions. As has been demonstrated throughout this article, cities are dynamic organizations. Throughout previous research, local service delivery has been described as having “substantial and ubiquitous interjurisdictional variation” that is reflective of differing bureaucratic and political structures (Saiger 2009). The menu of public goods and services is not static. To the contrary, those available goods and services and the values of the public that demand them are continually evolving and it becomes the responsibility of the government and local leadership to “adapt to” these changing values (Alchian 1950). Cities are obligated to adapt to their environment, effectively and efficiently meet the service needs of their residents, and maintain healthy and stable revenue streams.

Every representative approaches LOST negotiations armed with awareness of their own jurisdiction’s circumstances and needs, individual and varying objectives, and an internal climate unique from their counterparts in other jurisdictions. Therefore, to take full advantage of their access to those funds, cities should develop an understanding of the “competition” (other jurisdictions) and reflect on their own leadership decisions and structures that are vying for the same funds, always considering the dynamic between the two. Further, as local governments continue renegotiation at the designated trigger points, empirical research will have the opportunity to consider changes in behavior and predicting factors over time that might offer insight to the political, managerial, and interjurisdictional nature of LOSTs in Georgia.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.