Abstract

The following study looks at both qualitative and quantitative data collected from surveys of transit agency managers during and after the Great Recession to see if managers report changes in service provision arrangements in response to fiscal pressure. We investigate whether contracting out services is used as a method of cutback management. We find that the majority of agencies are unable to respond to current economic situation by changing service arrangements because of various and sometimes costly constraints such as state law, the level of competition in the bidding process, and length of contracts.

Introduction

The 2007–2009 recession, deemed “the Great Recession,” 1 was the longest and deepest recession in the U.S. history since the World War II (Bureau of Labor Statistics [BLS] 2012; Labonte 2010). It caused massive budget deficits at all levels of government, but state and local governments in particular were hit hard because of the limitations on their ability to borrow for operating costs. Public bus service, operated by cities, counties, and special purpose governments, was no exception. Transit agencies, unlike other local governments, depend more heavily on sales taxes, federal and state allocations, and user fees than the traditional property tax. Since these revenue sources are more vulnerable to an economic downturn than the property tax, the expectation would be that public transit would be hit even harder by the Great Recession.

Contracting out has long been viewed as a cutback mechanism (Winston and Shirley 1998). Competition between private companies should lead to cost savings (Savas 2005; Brown, Potoski, and Slyke 2006), economies of scale (Wassenaar, Groot, and Gradus 2013), and improve the quality of services for government. Since contracting out is very common in the transit industry, it is logical that the industry would be tempted to shift more services to contractors as a way to respond the fiscal stress caused by the Great Recession.

This study first examines the theoretical and empirical research on the “make or buy decision” and the potential impact of using contracting out as a cutback management measure. Then it focuses on answering the following question: do transit agency managers report an increase in the amount of services contracted out as a response to the Great Recession? This question is then answered by analyzing national survey data from 2009 (during the great recession) and in 2011 and 2013 (after the recession). Both qualitative and quantitative data collected from the three surveys are then summarized and framed in the broader discussion of contracting out and cutback management.

Exploring the Make or Buy Decision

Contracting out has long been proposed as a cutback mechanism during recessions, generally, for local governments (Moore 1987; Lopez-de-Silanes, Schleifer, and Vishny 1997; Kodrzycki 1994); and specifically in the transit industry where contracting out to reduce costs is quite common (Cox and Mundle 1997; Gomez-Ibanez and Meyer 1993; Winston and Shirley 1998). Privatization and contracting out are based on a widely shared assumption that if something is produced by private companies then governments may save money by purchasing it as opposed to making it in-house. Contracting out can improve production efficiency because it can often create competition among potential vendors (Savas 2005; Brown, Potoski, and Slyke 2006). Governments can save money by capitalizing on private market’s economies of scale (Wassenaar, Groot, and Gradus 2013). Therefore, contracting out is often an appealing solution to solve budgetary problems. For example, Wassenaar, Groot, and Gradus (2013) find that the most relevant motivational factor for contracting out services in Dutch municipalities is efficiency (Wassenaar, Groot, and Gradus 2013).

However, there is also a growing literature which does not find automatic cost savings from contracting out because of high transaction costs (Zullo 2008; Leland and Smirnova 2009; Brown and Potoski 2003). Zullo’s (2009) study on the relationship between fiscal stress and intermunicipal contracting demonstrates that the association between fiscal stress and contracting out is weak and that budget deficits did not increase contracting out. Smirnova and Leland (2013) identify the level of competition in the provision of services as one of the key elements to contracting out savings for public transit. Since transit agencies usually have just one contract, and there is lack of competition both in the provision of services and in the bidding process (Smirnova and Leland 2013; Transportation Research Board 2001), this may account for the lack of savings related to contracting out. The level of competition can be enhanced through frequent rebidding, however, the contracts in the transit industry tend to be long (some over thirty-five years; Smirnova and Leland 2013). This may be due to transit managers building trust with their contractors as a strategy to deal with incomplete information on contracts (Brown, Potoski, and Slyke 2007). Such long-term relational contracts may allow parties to face uncertainties of changing fiscal conditions, but they limit competition. And even though efficiency can be the primary motive for contracting out decisions, managers do not often base these decisions on clear cost comparisons (Wassenaar, Groot, and Gradus 2013). Moreover, the discussion of service provision would be triggered by complaints or “structural underperformance” (p. 430) rather than ongoing program evaluations (Wassenaar, Groot, and Gradus 2013). In other words, public entities exhibit certain inertia with regard to service provision decisions. 2

The switch between in-house and contracting out involves both conversion and transaction costs. The conversion costs involve one time expenditures such as setting up a monitoring unit for contracting out (Smirnova and Leland forthcoming), while transaction costs involve the additional costs of drafting bids and contracts, and monitoring contractors’ performance. In the transit industry, Smirnova and Leland (2014) emphasize monitoring as the key activity for the success of contracting out; but this activity involves tangible costs of performance management. Transaction costs also depend on the asset specificity or the extent to which transit agency resources (e.g., large busses) can be redeployed for other purposes. Higher asset specificity leads to larger and less efficient contracts (Smirnova and Leland 2013) and reduces managers’ motivations for contracting out services (Wassenaar, Groot, and Gradus 2013). At the same time, the transaction costs involved in contracting out were not selected as a relevant aspect of managerial decision making (Wassenaar, Groot, and Gradus 2013).

Brown, Potoski, and Van Slyke (2008) find that conversion costs structure the future choices of service delivery (Brown, Potoski, and Van Slyke 2008). That is, local governments that contracted out in the past are more likely to consider changes in the future. They note that conversion costs lead to certain inertia. The first choice of service delivery becomes the determining factor for the future decisions (Brown, Potoski, and Van Slyke 2008).

Other important considerations that the managers face when altering their current contracting relationships include the length of the existing contract (if they are already contracting out) and the politics surrounding the decision to alter arrangements. First, a contract’s length underscores the complexity of the contracting process, which often means an existing contract cannot be altered on a whim without substantial cost increases. The risks associated in changing providers or service provision may preclude any changes in production arrangements as well. Due to time constraints and inherent uncertainty, managers may strive for the most familiar decisions, and stick with the status quo, despite calls for a policy change that they believe may potentially cut costs.

The literature on campaign contributions also suggests that political support from current contractors may perpetuate keeping elected officials in office that support particular agreements and highlights why there is little change in contracting out services overtime (Baron 1989; Morton and Cameron 1992; Fuchs, Adler, and Mitchell 2000). Lopez-de-Silanes, Schleifer, and Vishny (1997) in their search for the political determinants of the decision to contract out suggest that politicians derive benefits from in-house provision (support of unions or pubic employees) over contracting to a private firm and therefore have an incentive to keep current arrangements even under pressure from votes to reduce taxes unless they become too expensive. The uncertainty about the outcomes emphasizes stability, that is, the crisis is simply temporary, but providing services to the public is a long-term commitment. After all, what worked very well in the past may be the best policy for the future. Therefore, this article presents an exploratory qualitative and quantitative study of the “make or buy” decision in the transit industry. The purpose is to find out exactly how agencies responded with changes to their service delivery arrangements to the fiscal pressures during the Great Recession.

Based on these theoretical frameworks, the expectation is that the transit industry would adjust their service delivery arrangements in response to the fiscal stress brought about by the Great Recession. However, based on empirical studies, the alternative expectation would be that agency managers would not use contracting out as a strategy during the recession due to fiscal stress. For these managers, the costs of changing arrangements would overshadow the costs of keeping the same service provisions under tight budgetary constraints. It may be easier to reduce service levels as opposed to changing the actual delivery arrangements to meet budgetary requirements. Thus, the current economic period represents a quasi-experimental design that allows for empirical observation of how transit agency managers report the impact of fiscal stress on service delivery arrangements. The following section discusses the data and methods in more detail.

Survey Design and Methods

The transit managers were surveyed in 2009, 2011, and 2013. The survey was distributed to all transit agency managers who were listed in the National Transit Database (NTD) in 2009 (606), 2011 (612), and 2013 (680). The NTD is the largest source of industry statistics, and the agencies reporting to the NTD provide over 90 percent of all transit services in the United States (American Public Transit Association [APTA] 2011). The surveys were conducted in July and August 2009 (during the Great Recession) and after the Great Recession in August and September 2011 and 2013. Self-administered surveys provide an anonymous and cost-effective way to examine transit agency managers’ perceptions about contracting arrangements. Both open- and closed-ended questions were used to understand both how and why the Great Recession may impact a particular agency’s service delivery arrangements. One hundred and thirty-seven agencies responded in 2009, with a response rate of approximately 22.6 percent. In 2011, the response rate was 30.7 percent and 36.6 percent in 2013. A series of questions were included in the survey to identify the respondent’s agency characteristics including agency type, services provided, vehicles operated in maximum service, 3 service area, service population, and region. This study focuses specifically on fixed route bus operations as the most widespread mode of transportation in the United States. The surveys conducted during 2011 and 2013 have additional questions on manager’s perceptions of the effects of the recession on contracting behavior.

Transit agency managers were specifically asked to indicate their level of involvement in contracting out within the next five years. This study found that service provision plans were influenced by the length of the existing contract that typically last at least three years. That is, the agency may be constrained by previous contracts and is unable to change their provision right at that particular moment in time. Therefore, fiscal pressure can only provide an impetus for future changes. There are three major nominal categories that were asked in the survey: no change in the level of contracting, plans to decrease contracting, and plans to increase contracting. Plans to decrease the level of contracting represent both a decrease in the number of functions/operations contracted out and conversions from the contracting out to in-house operations. Plans to increase the level of services contracted out may represent either a plan to increase the number of contracts or a conversion from in-house operations to contracting out.

In 2011, the survey also contained specific questions on whether the recent recession impacted service provision arrangements of transit agencies. This included the following question: “Which of the following statements best describes how the current recession has influenced your service provision arrangements?” Managers could select one of the three statements on whether they saw no impact on current arrangements, an increase in contracting out or a decrease in contracting out. An open-ended question then asked for further details on why the agency would consider altering their existing arrangements. The following section discusses our survey results in detail.

Survey Results

Both the qualitative and quantitative survey results describe how agencies changed their contracting behavior in response to the fiscal pressure of the Great Recession and the reasons why the agency opted to keep their current arrangements or change their existing arrangements. Table 1 shows how managers responded to the following survey question; “How do you foresee your agencies future involvement in contracting out in the next five years?” 4 for 2009, 2011, and 2013.

Contracting Involvement in the Next Five Years.

aPlease note that in 2009, this question was not directly asked about the Great Recession. In 2011 and 2013, we specifically asked transit managers to select “Which of the following statements best describes how the current recession has influenced your service provision arrangements?” Managers could select no impact, a decrease contracting out or an increase in contracting out.

Table 1 illustrates that both during and after the recession, at least 74 percent of transit managers did not expect their arrangements to change in the next five years. This is in line with the previous literature’s (Brown, Potoski, and Slyke 2008) findings of inertia in service delivery arrangements. One-tenth to one-fifth of agencies reported that they plan to increase the amount of services contracted out in the next five years. Less than one-tenth of transit managers indicate that they plan to decrease the amount of services they contract out in the next five years. These agencies all had smaller vehicle fleets and simpler service structures.

In 2011 and 2013, managers were asked a specific question if the recession influenced service provision: “Which of the following statements best describes how the current recession has influenced your service provision arrangements?” The choices they were given included no impact, a decrease in contracting out, or an increase in contracting out. 5 Transit agency managers gave very similar responses to both questions asked in 2011 and 2013. Agencies with elected officials on their boards or a combination of elected and appointed officials on their boards were more likely to consider decreases in contracting out when compared to other agencies. About 20 percent of agency managers who responded that the recession had no impact noted that they did still plan to change their service provisions within the next five years for other reasons. Therefore, in order to better understand their responses, they were categorized into three different categories: no change, an increase in contracting out, and a decrease in contracting out. Table 2 summarizes the qualitative survey responses that explain why the agencies experienced or did not experience the recessionary pressures.

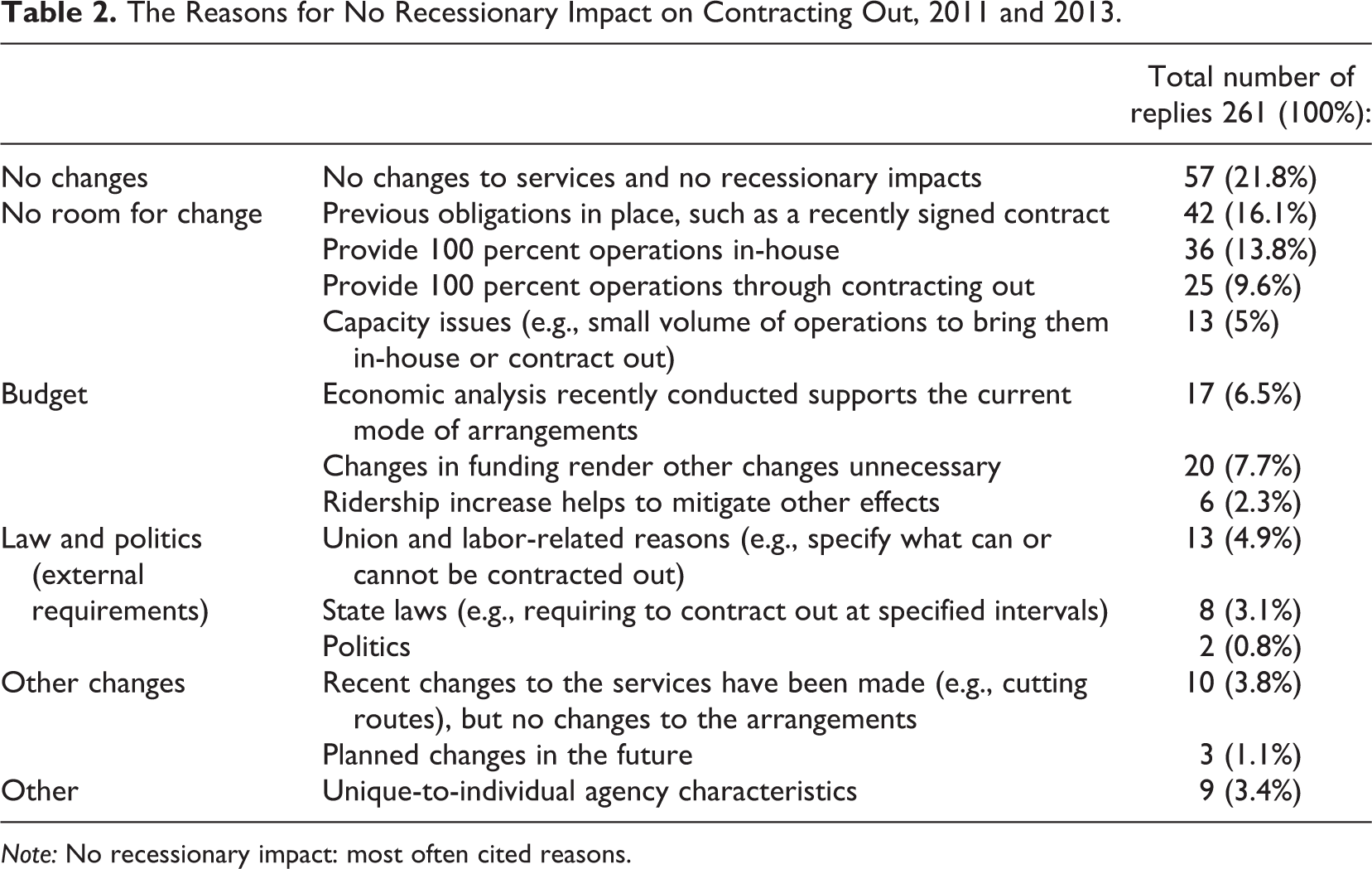

The Reasons for No Recessionary Impact on Contracting Out, 2011 and 2013.

Note: No recessionary impact: most often cited reasons.

No Recessionary Impact

Table 2 indicates several common factors that were cited by managers when they have selected that the current recession has no impact on whether they provide services in-house or contract out. The responses are grouped into the following major categories: no changes, no room for change, budget, law and politics, other changes, and other factors.

One-fifth of all respondents indicated that they did not experience recessionary pressure and did not plan to make any service changes (no changes category). In fact, some stated that their area was not hurt by the recession when compared to other cities. Some managers also reported an increase in ridership during this time period. At the same time, four-fifth of managers indicated that there were other reasons why recession did not influence their consideration of service arrangements.

Several respondents mentioned that two items, the recession and service arrangements, were not necessarily connected and that they do not contract out in response to fiscal pressure, rather they simply cut the level of services. As one manager indicated, “The recession reduced our overall tax revenue, but did not change our strategy regarding in-house and contracting services.”

According to the managers, one of the factors that impeded any change in service delivery arrangements was inflexibility of their existing contracts. This is evidenced in the comments from many respondents that stated there was no room for changing their current arrangements. In order for fiscal pressure to cause agencies to consider alternative modes of service provision, the agencies should need to have the flexibility to enact a change. There appears to be a number of factors that prevent agencies from switching arrangements to cut costs. Indeed, the next most frequently cited reason for the absence of recessionary pressure was actually a recently signed contract that was in effect when the recession began (16.1 percent). Previous long-term obligations can preclude any potential short-term changes. Many managers responded that the length of their current contract was actually longer than the recession. As one manager stated, “We have kept the same contract provider for 10 years, so the current recession has not had an impact on this decision.” Factors that fall under the category of capacity issues can be further subdivided into those where conversion costs are high or that agency size is an impediment to change. Agencies that provide all of their services in-house (13.8 percent) or through contracting out (9.6 percent) have higher conversion costs to consider when switching arrangements than those that engage in partial contracting. And some managers who reported that their agencies contract out for all of their services mentioned that they no longer had the capacity to bring the services back in-house even if they believed it would save money. One manager stated, “We have always contracted out our services, and don’t anticipate having the capacity (and political support) in the near future to make any changes.” Others said that their board had a policy to always contract out services for liability reasons or that the risk needs to be managed through contracting out so switching to in-house provisions was never an option. Agency capacity issues were also referenced in about 5 percent of the cases. The agency may be too small to attract any interested contractors or does not have the internal capacity to provide services in-house.

Budgetary factors were also frequently mentioned by the transit managers. For example, agencies may have conducted an economic analysis prior to the recession (6.5 percent) and this may have given them the rationale to either keep the same arrangements, or switch to in-house provisions, or contract out. The budget itself, especially changes to funding, and recent economic analyses were highlighted as important reasons for not responding to the fiscal pressure of the recession. If an agency has just conducted a cost–benefit analysis for outsourcing its operations or brining the operations in-house and found no potential cost savings, then the bottom line arguments become the reasons for keeping the same service arrangements. Alternatively, if the findings of economic analysis indicate potential cost savings from changes (contracting out more or bringing more operations in-house), then these cost-savings arguments becomes the impetus for the change.

Law and politics were also cited as reasons to keep current service delivery arrangements as is. Among the different legal provisions that may preclude agencies from making any changes to existing service provision arrangements, the most frequently cited were state law (3.1 percent) and union and labor-related considerations (4.9 percent). In a few cases, politics (0.8 percent) were also mentioned as reasons to stick with their current arrangements. Labor concerns and union provisions played an important role in contracting out because they may prohibit the use of contract labor or prescribe specific contracts an agency may sign. In some cases, state law prohibits municipalities from hiring union workers. So the only way to hire union labor is to contract out. Some managers also cited political barriers to changing their arrangements. One stated that “the revenue loss wasn’t severe enough to even consider and it would have been very difficult in our political environment and with our unionized work force” and “the recession led us to look into it but the powers that be decided no.”

Finally, it is interesting to note that several agencies mentioned that they cut services in response to budget difficulties, but they did not change their contracting arrangements in order to save money. Essentially managers responded in the survey that they implemented other types of changes in response to the recession. Many adjusted their level of service provision in order to adapt to fiscal constraints or they simply used a cheaper contractor but still kept the same level of services. About 3.8 percent of respondents indicated that instead of making changes in their current service provision arrangements, it was simply easier to reduce the amount of services they provided (e.g., cut the number of hours they operated or the number of routes they provided). Another 1.1 percent indicated that even though the recession had no bearing on their decision, they still plan to revisit their current arrangements.

Increasing Contracting Out

Table 3 summarizes the comments made by managers who did consider contracting out more of their services due to the recession. Budget reasons such as cost-effectiveness (59.1 percent) and decreases in funding (20.5 percent) were cited the most often. The issue of labor was also raised. The transit managers at the time of recession are under increased pressure to reduce all costs through any means possible. A few managers that increased contracting out as a response to the recession said that “obtaining quality services at a lower cost in a recessionary environment becomes more politically acceptable” and that the economy and reduced internal budgets did force them to look at alternatives to help offset operating budget shortfalls. Another said that a reduction in state subsidies caused them to look for additional revenues through contracting out. Reverting recent changes have also been highlighted as a response to the recession (other changes).

The Reasons for Increasing Contracting Out, 2011 and 2013.

Note: Most often cited reasons for increasing contracting out during the recession.

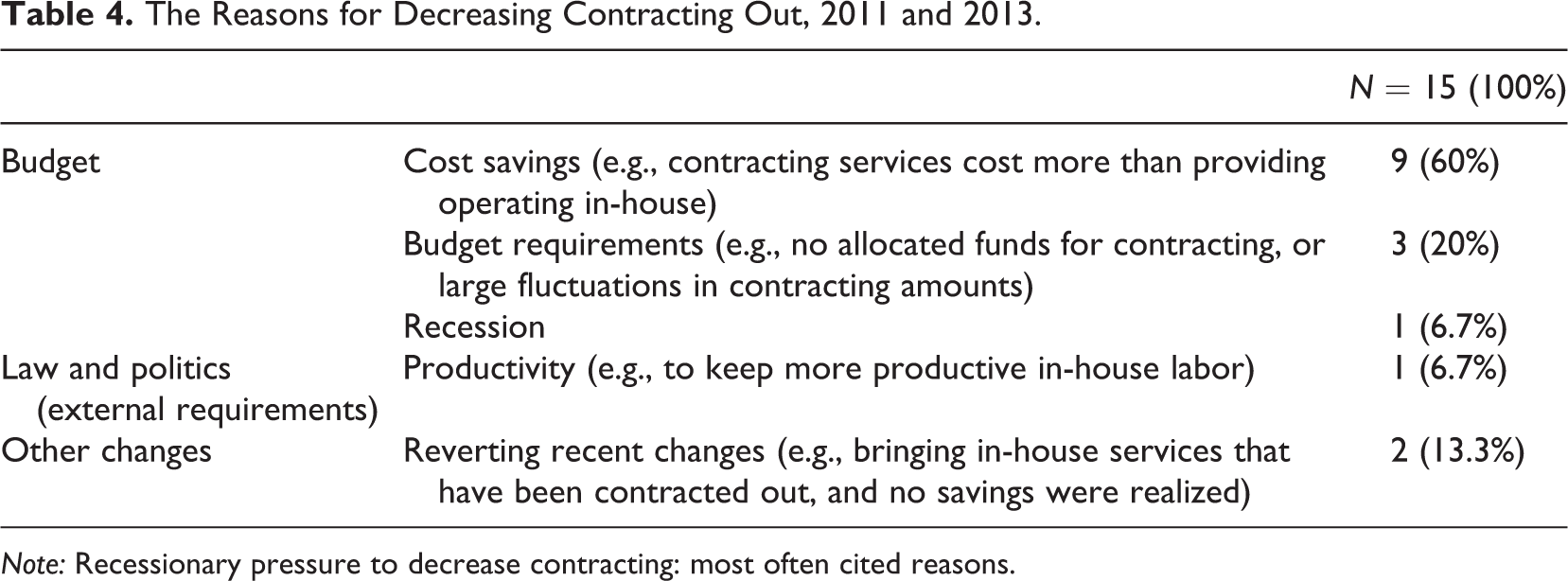

Decreasing Contracting Out

Table 4 summarizes the reasons given by managers for considering bringing services back in-house. As one of the managers stated, “the contractors get cut first” (budget). Another manager said they canceled a contract because they could not afford it. A manager from an agency that decreased the amount of services they contracted out said that “when we resumed direct operations, our costs decreased considerably.” Yet, another manager identified that keeping a productive in-house staff was their primary goal during the recession (labor and politics factors in Table 4). In other situations, the recent contract may have been brought in-house precluding any further changes (other changes).

The Reasons for Decreasing Contracting Out, 2011 and 2013.

Note: Recessionary pressure to decrease contracting: most often cited reasons.

Overall, our findings paint a nuanced picture of the decision to contract out. Even though the majority of respondents indicated that the current recession did not have effect on whether they increased or decreased the amount of services they contracted out during the recession. They did mention that there were other alterations besides contracting out that they did have to explore because of fiscal pressure during the recession. For example, they may have had to increase ridership in order to generate more user fees to mitigate negative fiscal effects. In some cases, the service delivery mode (in-house or contracting out, or both) did not change, but the operations themselves were adjusted to cut costs. Politics also plays an important role, as managers in two particular cases cited that their boards demanded change that was not based on an efficiency or effectiveness during the recession.

Conclusion

Our survey results support the literature that finds inertia in service provision decisions (Brown, Potoski, and Slyke 2008). More importantly, this study highlights the important reasons for this inertia such as previous obligations, state and local regulations, political and community stakeholders’ involvement, as well as local ridership and/or funding trends that help to combat the effects of the recession. The qualitative responses from the survey indicate that the make or buy decision involves more factors than just cost savings. And even though the cost-savings play an important role in the decision to make or buy services, there are other factors, such as legal constraints and labor considerations, which shape their decisions.

Transit agency managers in this study cite several important obstacles to altering their service provisions. There are several political and legal barriers to switching arrangements in order to save money during a recession. Public officials need to consider that federal and state laws may not allow for outsourcing or providing for direct services. For those that keep services in-house, they are also concerned with the risks associated with outsourcing. For those that already contract all of their transit services, there is a concern that they no longer have the capacity to bring services in-house if needed, and their existing contracts may not allow them to move operations in-house without incurring severe financial penalties. Labor unions representing current employees also play a role on both sides of the issue, but overall tend to encourage agencies to keep their arrangements the same and not to change them. In states like Texas where contracting out is the only way to use unionized labor, unions favor current contracting arrangements. In states where contracting out is mandated for some services, labor unions fight to keep services in-house.

The timing of contracts and the length of the recession are also important components shaping transit agency contracting decisions. The findings of three waves of transit surveys, 2009, 2011, and 2013, indicate that the decision-making time horizon is much longer than the recessionary period. Since a change in service provision is costly because of transaction and conversion costs, agencies that currently contract out for service are under greater pressure to adjust their contracting patterns during a fiscal crisis. The qualitative survey responses indicate how various agencies adjust their individual situation to various budgetary constraints.

Agencies that contract out all or part of their services did experience more pressure from the Great Recession to increase the amount of services they contract out than agencies that kept all of their services in-house. This finding emphasizes that the original decision to contract out (or keep services in-house) frames future decisions (Brown, Potoski, and Slyke 2008). For this reason, the initial decision of whether to make or buy transit services should take into account future transaction costs and the unlikelihood that these decisions will frequently be revisited. Thus, the changes that affect long-term economic standing should not be taken due to short-term fluctuations in the economy, and the majority of the survey respondents agree with this conclusion by their actions. Even during the Great Recession, most service provision arrangements could not be altered regardless of whether or not they saved money in the short run.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.