Abstract

Diffusion models explore the reasons policies transfer across governments. In this study, we focus on U.S. state level efforts in affordable housing. Drawing predominately from policy diffusion literature, our research examines the determinants of the creation of state Housing Trust Funds (HTFs). We utilize event history analysis with logit regressions and survival modeling to examine how problem severity, neighbor adoption, economic standing, elected leadership, housing investment, and demographics predict state HTF adoption. Results indicate that both problem severity and elected leadership predict the adoption of HTFs. This work improves our understanding of state policy diffusion and efforts in housing affordability.

Introduction

The determinants of when governments adopt policy have been an enduring area of study for public policy scholars. As one theory of the policy process, diffusion models explore the conditions under which policies transfer across governments. Throughout decades of work, scholars have applied the diffusion mechanism in numerous policy and national contexts. Recent contributions have included policy areas such as energy policy (Nicholson-Crotty and Carley 2018), tobacco policy (Pacheco 2017), medical marijuana laws (Johns 2015; Hannah and Mallinson 2018), and same-sex marriage (Fay 2018). Theories of policy diffusion also have been applied to different national contexts, including China, Germany, Latin American countries, and the United States (Meseguer 2004; Shipan and Volden 2014; Abel 2019; Heggelund et al. 2019). We continue in this line of policy diffusion research in the context of U.S. states with application to housing affordability.

An enduring theme of policy diffusion research is that states can innovate and learn from one another to solve problems. The housing policy arena has experienced a deepening problem – housing affordability. The standard definition used to define affordable housing is households that pay no more than 30% of their income toward housing costs (Stone 2006). The literature on housing affordability has grown over the last several decades as the severity of the problem has intensified, while the federal government has passed on more responsibility for state and local governments to meet housing needs. Housing is a basic necessity that not only provides physical safety but is a primary requirement for an individual's overall well-being (Bratt, Stone, and Hartman 2006). Extant research has shown the impact of housing and neighborhoods on economic, social, physical, and mental health outcomes (e.g., Burgard, Seefeldt, and Zelner 2012; Steiner, Makarios, and Travis 2015; Chetty, Hendren, and Katz 2016). The private housing market is unable to provide housing for the lowest-income households and factors such as housing discrimination and income inequality contribute to the lack of access to decent affordable housing (Bratt, Stone, and Hartman 2006). Government intervention is required to address these issues that are at the root of the affordable housing crisis.

Housing affordability represents a policy area with a unique combination of characteristics for state innovation. For one, housing policy innovation has a set of obstacles as a redistributive policy area benefiting people of lower political power. Theories on the “race to the bottom” and social construction of target populations outline the barriers to successful policy creation and implementation. Additionally, this policy area has experienced worsening problems, punctuated with a major negative event—the 2007–2008 financial crisis and housing collapse—that disproportionately affected the poor and racial and ethnic minorities. Coupled with increasing severity, federal burden shedding (Weaver 2020) has pushed states to fill the gap of declining support; a trend seen in many other redistributive policy areas (Franko and Witko 2017).

In this study, we utilize the policy diffusion framework to examine the factors that lead to the creation of state housing trust funds (HTFs). State governments, through enabling legislation, create HTFs to generate money dedicated to affordable housing initiatives without having to go through an appropriation process. We use panel data on 50 states from 1980 to 2016, collected from state Housing Trust Fund and Housing Finance Agency websites, Census data, and American Community Survey (ACS). This study builds on the foundational work of Scally (2012) in the housing literature by updating the last 12 years of HTF adoption—which covers the end of the housing bubble, the collapse of the housing market and subsequent recession, and the last decade of recovery and economic growth. We analyze HTF adoption through event history analysis (EHA) utilizing logit and survival analyses to identify factors that influence the likelihood of policy adoption. Results indicate that both problem severity and elected leadership predict the adoption of HTFs.

This study can inform not only housing policy researchers, but the broader political science and policy process scholars on how housing policy dynamics give insights to theories of policy adoption. For the housing field, this study contributes to the knowledge on when states are primed to adopt beneficial policy solutions that expand the affordable housing stock. The housing policy arena is not emphasized to the same extent in theories of policy adoption compared to the extensive and growing research in the fields of education, welfare, criminal justice, environmental, and health policy to name a few. This work advances the policy process literature on diffusion by expanding to a new policy area – housing affordability. Theoretically, this study adds to the diffusion literature by examining not only another redistributive policy area but one that has gone through a national crisis and faced a devolution of responsibility from federal to state governments 1 . This study pushes diffusion theory forward by showing how in a strained policy area (like housing), problem severity and elected leadership matter for policy adoption. Our findings contribute to the understanding of housing policy diffusions.

Literature: Policy Diffusion and Housing Policy

Policy Diffusion

Research in policy innovation and diffusion has been rapidly growing since Walker (1969). At the most basic definition, policy innovation occurs when governments adopt new policies while policy diffusion is the transfer of policies, programs, and ideas from one government to another (Shipan and Volden 2008; Graham, Shipan, and Volden 2013; Shipan and Volden 2014). Studies of policy diffusion have been applied to a wide range of policy fields, including state lotteries (Berry and Berry 1990; Cruz-Aceves and Mallinson 2019), education (McLendon, Hearn, and Deaton 2006; Birdsall 2019), abortion regulation (Medoff and Dennis 2011), tax and expenditure limits (Miller and Richard 2010; Seljan and Weller 2011), and criminal justice (Hoyman and Weinberg 2006). Recent work includes policy areas such as energy policy (Nicholson-Crotty and Carley 2018), health policies (Pacheco 2017), marijuana legalization (Johns 2015; Hannah and Mallinson 2018), public budgeting (Krenjova and Raudla 2017), policy networks (Yi, Berry, and Chen 2018), same-sex marriage (Fay 2018), and antismoking restrictions (Shipan and Volden 2014). There is also emerging research looking at the diffusion mechanism outside of the U.S. context to expand the external validity of the theory across countries (Beer and Cruz-Aceves 2018; Heggelund et al. 2019). In addition to the vast field of policies studied over the decades, the literature has expanded to studying numerous policy areas at once, to create more generalizable findings on diffusion dynamics (Boehmke and Skinner 2012). The literature has been critiqued for a pro-innovation bias (Karch et al. 2016), missing the other ways policies can transfer across governments even without legislation. Smith (2020) for example, shows how policy diffusion occurs through the budgetary process and bureaucracy, developing common standards in the context of early childhood education.

The policy innovation and diffusion literature stipulate that a combination of internal features (Berry 1994; Berry and Berry 2014) and diffusion mechanisms lead to policy adoption. The theory of policy diffusion suggests that governmental policy decisions are affected by not only neighboring governments (a definition that has expanded beyond a simple geographical understanding of neighbor) for horizontal diffusion (Berry and Berry 1990; Graham, Shipan, and Volden 2013), but also governments at other levels in vertical diffusion (Allen et al. 2004; Karch and Rosenthal 2016). Diffusion literature theorizes that federalism allows for innovation, learning, and trial-and-error across jurisdictions. Decentralization will lead to innovation by the state governments through the greater number of jurisdictions, variation in ideological ranges, and smallness of government and scale to enact policies (Adams 2020).

Policy Theory and Housing Affordability

Lowi (1964)'s categorization of policies by the distributive, regulative, constituent, and redistributive has been useful to decipher how mechanisms of diffusion vary by policy area. Additionally, Hollander and Patapan (2017) outline the ways that federalism can enable but also at times stifle policy innovation and diffusion in morality policies. The context of housing policy highlights policy adoption in a redistributive policy area, leading to its own unique obstacles to innovation and diffusion of policies (Shipan and Volden 2012). Scholars have theorized that national governments are best able to address redistributive policy (Oates 1968; Peterson 1995). Viewing federalism as a way for states to be competitors, states can adopt the policy as reactive, strategic, anticipatory, or preemptive to other states’ actions (Berry and Berry 1990; Baybeck, Berry, and Siegel 2011). Applying the competition logic to redistributive policies at the state level has led to differing viewpoints among scholars on the “race to the bottom” in policy adoption (Figlio, Koplin, and Reid 1999; Allard and Danziger 2000; Berry, Fording, and Hanson 2003). The concern is that competition would lead to less optimal outcomes for society as states negotiate to serve the less fortunate while simultaneously not becoming “welfare magnets” (Peterson and Rom 2010). The federal government, however, has made efforts at separating itself from many redistributive type policies. There are also many examples of state and local governments successfully implementing redistributive policies (Swanstrom 1988; Martin 2001). In housing, for example, the federal government has applied such policy dynamics as coercion and burden shedding (Weaver 2020). To generalize, the federal government has decreased budget authority for public housing and reduced its commitments to expand the supply of federal subsidized housing over time, leaving states and local governments with the burden to address the growing affordability crisis. Decentralizing housing affordability support has spurred states to innovate on their own to address their populations’ needs (Adams 2020).

Drawing from the social construction framework (Schneider, Ingram, and Deleon 2014), scholars have shown how political power and positive/negative social construction of target groups can dictate the public policy process. It can be much easier to generate support from legislators and/or the population for policy beneficiaries that have political power and are positively constructed as deserving of government support. Redistributive policies typically benefit those people who have low political power and vary in society's judgement of their “deservingness” for help. This social construction orientation coupled with a competition mentality can make policy innovation and diffusion in redistributive policies a challenge.

The housing policy area holds these characteristics. Many of the issues around housing affordability illustrate the politics of the poor and minority communities. The incidence of housing affordability issues has historically fell disproportionately on racial and ethnic minorities. Finding legislative ways to support housing initiatives relied on Congressional coalitions centered on addressing poverty plus innovative funding mechanisms. However, contemporary research in this area shows how many households across socioeconomic status, racial groups, and ethnicities face housing affordability issues today, especially in high-cost cities. This has expanded the target groups in need. Of the housing support that is offered, research has shown that federal government support favors owners over renters and it targets higher-income households (Krueckeberg 1999; Fischer and Sard 2017; McCabe 2018). This illustrates how efforts at redistribution are not always completely effective at reaching the most vulnerable groups. Furthermore, federal funding for some housing programs, such as Low-Income Housing Tax Credits, are distributed to states based on population and not need (Keightley 2017).

The literature devoted to understanding the role states play in the area of affordable housing production is sparse although their involvement and importance in this arena are increasing. Before 1980, states had minimal involvement in housing policy and finance (Goetz 1995). In the past couple of decades, states have had to innovate to address the affordable housing crisis. From 1990 through 2016, the national median rent and the median home price have risen faster than inflation (20% and 41%, respectively) (Joint Center for Housing Studies 2018). The number of low-cost rentals has fallen since 2012 making up only 25% of the national rental stock in 2017 (Joint Center for Housing Studies 2020). Rapidly increasing housing expenses and stagnant incomes have widened affordability gaps. There are only 36 affordable units available for every 100 extremely low-income renters, which leaves 71% of extremely low-income renters severely cost-burdened (National Low Income Housing Coalition 2020). Due to the loss of privately and publicly federally funded affordable rental units, diminishing federal support, rising housing costs, and the increasing number of rent-burdened households, the need to fill the gap between demand and supply for affordable housing remains (Larsen 2004).

Extant research has started to assess the role states play and how they are innovating to expand affordable housing during federal devolution of local housing expenditures (Basolo and Scally 2008; Scally 2009). State housing finance agencies have stepped in to develop financing mechanisms that address local housing needs (Scally 2009). As an example, state housing finance agencies issue mortgage revenue and multifamily housing bonds to help finance homeownership opportunities and rental housing for moderate- and lower-income households. Another mechanism that gained popularity in the 1990s is the establishment of state HTFs with a dedicated source of funding (Brooks 1995). Below the case of HTFs is explained. We then offer a theoretical section on determinants of state HTF adoption.

Policy Context: The Need for Affordable Housing

History of State HTFs

Unemployment and foreclosures as a result of the Great Depression prompted federal support for a range of public benefits which included the creation of the Federal Housing Administration to insure privately issued mortgages and a role for the federal government in the production of housing (Landis and McClure 2010). Until the 1970s, the federal government was focused on the production of housing and directly involved in developing and managing a stock of public housing for the poor. However, by the 1980s, there was diminishing federal support for supply-side production programs and demand-side housing subsidies, such as vouchers, became more prominent (Kleit and Page 2008). This shift led to a reduction in budget authority for housing that started during the later years of the Carter Administration in the late 1970s and was expanded under the Reagan Administration in the 1980s (Connerly 1993; Goetz 1995). These reductions occurred while affordability issues and homelessness were on the rise (Connerly 1993). The federal government shifted some responsibility to states in the form of block grants through the Community Development Block Grant (CDBG) and HOME Investment Partnerships programs. States also authorize their own priorities through Qualified Allocation Plans to distribute tax credits for the federal Low-Income Housing Tax Credit Program (Basolo 1999; Goetz 1995). However, prior to the 1980s, there were few state governments that were involved in housing policy (Goetz 1995).

Decades of weakening federal budget authority for housing and the growing affordable housing crisis have left states and local governments with the responsibility to generate additional funds for the production of affordable housing (Connerly 1990; Ammann 1999; Basolo 1999; Orlebeke 2000). The development community, local housing providers, social service agencies, low-income communities, and advocacy coalitions responded to the growing demand for affordable housing by seeking additional financing mechanisms to produce housing (Brooks 1992). Prior to the 1980s, only three states, California, Connecticut, and Massachusetts had funded housing programs and were prominent in the provision of affordable housing (Goetz 1993). After the 1980s, many states established housing programs, and housing and community development expenditures have continued to increase in the last several decades (Schwartz 2014). States primarily support affordable housing activities through the administration of federal programs such as block grants and Low-Income Housing Tax Credits and their own programs such as tax-exempt bond financing and inclusionary zoning (Mueller and Schwartz 2008). Furthermore, HTFs are used by states to raise capital for affordable housing development (Ammann 1999). HTFs provide a dedicated source of funding for affordable housing and allow local flexibility that attracts private sector partners (Brooks 1995; Larsen 2007).

The origin of HTFs can be traced to 1968 when Delaware was the first state to create one (Larsen 2007). Momentum emerged in the 1980s when California and Maryland initiated HTFs (Connerly 1990; Center for Community Change 2016). This was during a time when many new state housing programs were established (Goetz 1995). Figure 1 highlights state HTF adoptions over time. The map reveals that coastal states in both the East and West, and several Midwest states, were among the first to adopt HTFs. Many of these states like California and New York have urban areas that were the first to experience housing supply shortages, rising housing costs, severe rent burdens, and homelessness. HTFs gained popularity across the rest of the U.S. by the 1990s with 29 states initiating HTFs as federal support for low-income housing continued to diminish (Brooks 2007). By the mid-2000s, 40 states had HTFs (Larsen 2009) and by 2016 nearly all states had at least one housing trust fund (Center for Community Change 2016). Although HTFs can now be found across America, they were originally concentrated in the West and Northeast (Connerly 1993). By 2015, states reported leveraging on average $7 for every $1 that is dedicated to housing trust fund activities and generated more than $790 million, with four states – Connecticut, Florida, New Jersey, New York and Washington D.C. generating more than $50 million annually (Center for Community Change 2016).

Housing Trust Fund State Adoption by Year.

State HTFs Adoption and Administration

Elected governments create HTFs and the money generated is used pursuant to the enabling legislation without having to go through an appropriation process (Center for Community Change 2016). Establishing a housing trust fund often requires public outreach and education, political negotiations, and support from interest groups and the local community (Brooks 1992). At the time of creation, how the funds are distributed and what entity is responsible for such dispersal is incorporated into the legislation, which is permanent; equivalent legislative action is needed to eradicate a housing trust fund (Brooks 1992). The funds are typically managed by the authorizing legislative body or state housing finance agencies (Brooks 1995). A board or advisory committee comprised of governmental staff, industry experts, elected officials, developers, housing providers, social service agencies, community stakeholders, and low-income residents often oversee the operations and are charged with creating the guidelines for identifying need, distributing the funds, and program reporting mechanisms (Brooks 1995).

Many HTFs have a dedicated source of funding when created although a few have been established without one. The first HTFs generated revenue through real estate transfer taxes and linkage fees (charged to developers on new commercial or industrial construction to balance the additional housing needed for employment growth) (Brooks 1995; Ammann 1999). The range of options available to fund HTFs has expanded to almost forty distinctive sources (Brooks 1995). The most common revenue sources include real estate transfer taxes, followed by appropriations from the state general fund, document recording fees, revenues from state housing finance agencies, and interest from real estate escrow accounts. Other sources include bond proceeds, contractor's excise tax, foreclosure filings, interest on title escrow accounts, state income tax, tobacco tax, unclaimed property fund, and utility charges (Center for Community Change 2016).

According to the Housing Trust Fund Project, in 2020 state HTFs generated over $1.6 billion in revenue for housing initiatives. However, the enabling legislation and dedicated source of funding can have a substantial impact on how much revenue a state is able to generate resulting in a wide range of collections state by state. For example, the state housing trust fund in Florida has generated $334,670,000 in 2020 from documentary stamps tax collections (The Regional Economic Consulting Group 2021) compared to Alabama, Idaho, Montana, and Rhode Island that have created HTFs but do not have any revenue sources committed to their funds (Housing Trust Fund Project 2021).

HTFs are typically distributed through a competitive process as grants or loans for both new construction and rehabilitation. Multiple sources of funding such as Community Development Block Grants or HOME are often used in conjunction with HTFs as the amounts awarded from trust funds are not enough to support the entire project (Brooks 1995). The projects primarily provide housing for low-income households, which are households that earn below 80% of the area median income. Some funds are specifically used to serve very low-income (50% of the area median income) or extremely low-income households (30% of the area median income). However, one criticism of HTFs is that they lack deep subsidies and often do not serve extremely low-income households (Connerly 1993; Larsen 2004). Most housing programs administered by state governments only provide shallow subsidies that often serve higher-income households (Mueller and Schwartz 2008). Affordable developments are often required to remain affordable for a specified timeframe (Brooks 1992). Some HTFs provide support for specific populations such as the homeless or individuals reentering society (Connerly 1990; Center for Community Change 2016). Nonconstruction related activities such as foreclosure prevention, down payment assistance, home education and counseling, or rental subsides are also supported by some state HTFs (Brooks 1995; Center for Community Change 2016).

To the authors’ knowledge, there has only been one study conducted that has examined factors that influence state adoption of HTFs. Scally (2012) examined the factors that influence U.S. state housing policy innovation, specifically HTFs over a 20-year period using a state policy innovation framework. The framework included indicators of internal organizational characteristics of agencies administering trust funds, environmental determinants (social, economic, and political), and policy diffusion. Scally (2012) found that states with a higher proportion of Black citizens, previous housing expenditures, higher rates of single-family construction, more politically leaning liberal citizens, and severe affordability issues were more likely to adopt housing trust fund policy innovation.

Data and Methods

We have relied on the literatures in policy innovation and diffusion, housing affordability, federalism, and policy types to develop a model of state HTF adoption. Our model consists of six components: problem severity, neighbor adoption, economic standing, elected leadership, housing investment, and demographics. Below, each component is discussed regarding variables and theory.

Problem Severity

Policy adoption is advanced by the extent of the problem (Walker 1969; Gray 1973). The description above illustrates how the housing affordability crisis has been exacerbated in states. Drawing from the diffusion literature, we expect the severity of the housing crisis to increase the likelihood of HTF adoption—more severe housing concerns likely pressure policymakers to adopt initiatives that support housing production. However, redistributive policy and social construction theory tells us that it is harder to generate new policy given the housing policy context and target group. In this light, we may expect problem severity to have little to no impact on the rate of HTF adoption. Our empirical models will give some clarity to this puzzle. Given our context though, we anticipate that problem severity should increase the likelihood of adoption of HTFs.

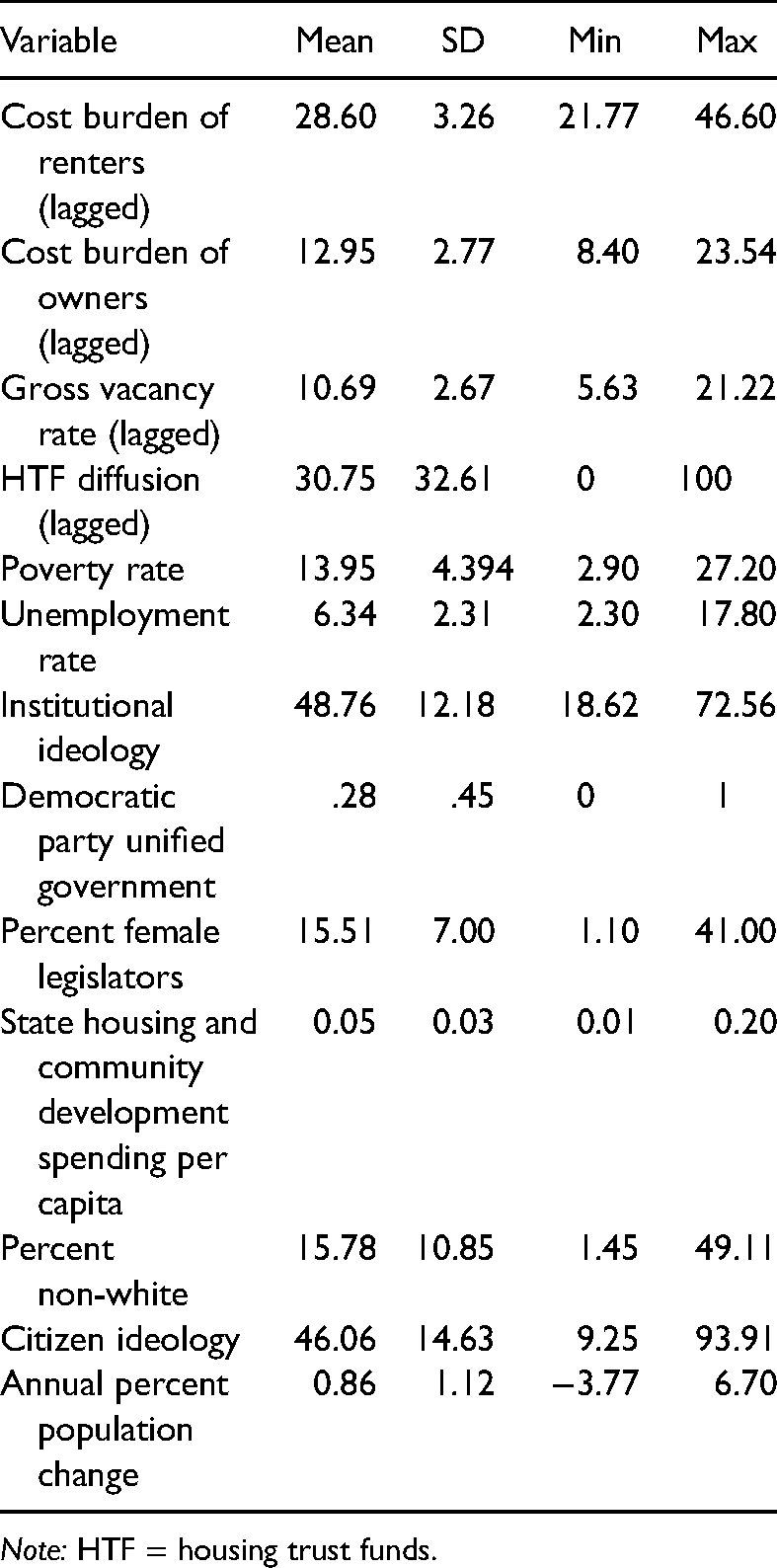

In our empirical models, severity of the housing crisis is measured by three variables: the cost burden of renters, the cost burden of homeowners, and gross vacancy rate. These variables were collected from two sources: Decennial Census and the American Community Survey. The Decennial Survey provided data from 1980, 1990, 2000, and 2010. The ACS was available annually from 2011 to 2016. To fill in the missing data, the mean value was used for the first and last year in the missing range. For example, years 1981–1989 consisted of the mean of 1980 and 1990 in each state. Years 1991–1999 was the mean of 1990 and 2000, and so on.

The two cost burden variables determine how many renters and homeowners are paying 35% or more of their income toward housing costs. There has been a long-standing percent of income standard that was originally 25-percent, and now 30-percent, to measure housing affordability (Herbert, Hermann, and McCue 2018). Households paying more than the 35-percent standard are considered cost-burdened since this leaves them with little to spend on other necessities such as food, clothing, and medical expenses. As expected, the percent share of cost burden renters is higher than homeowners. On average, cost burden owners account for 13% of all households, with the lowest proportion at 8.4% and the highest share at 23.5%. Cost burden renters account for 28.8%, on average for all households, with a range from 3.4% to 46.6%.

Vacancy rates can be used as another indicator of the severity of the affordable housing crisis. Vacancy rates are often used to assess demand in housing markets. Low vacancy rates can be an indicator of a strong housing market with a shortage of housing supply that increases housing costs (Joint Center for Housing Studies 2019). Vacancy rates range from 6.2% to 21.2%, with an average gross vacancy rate of 11%.

Neighbor Adoption

An essential variable in the diffusion literature is the number of neighbor states that have adopted the policy of interest. In our analyses, we use the lagged percent of geographic neighbors (Mintrom 1997; Mallinson 2019) to adopt a HTF to measure policy diffusion. This measure, geographic neighbors, makes the most sense given our context as opposed to other measures of neighbors (like political ideology). Neighboring states often face similar housing market dynamics and housing stock challenges. For example, Walter et al. (2020) documents the different types of housing stock challenges housing organizations face in high-cost western states with rental subsidies compared to aging housing stocks in the northeastern portion of the country. Also, given the race-to-the-bottom theory, the geographical neighbor is an important benchmark in incentivizing/deterring groups of people.

The general expectation from diffusion studies is that neighbor adoption will make it more likely for a state to adopt. Literature identifies three major mechanisms of how neighboring states affect policy adoption: officials noting the positive policy outcomes of neighboring states’ policy, catching up with the economic advantages of neighboring states, and support from constituents (Berry, Fording, and Hanson 2003; Volden 2006; Pacheco 2012). Drawing from theory in redistributive policies though, states may be less likely to innovate. The three major mechanisms noted above may not hold for redistributive policies—positive policy outcomes could deem them as “welfare magnets,” there are other policy areas more suited to lead to economic advantages, and constituent support may not be from those most politically powerful. Thus, theory gives us reasons to expect that the percent of geographic neighbors to adopt a HTF may have little to no impact on states to adopt a HTF. With our housing context in mind, we anticipate that neighbor adoption will most likely not impact HTF adoption.

Economic Standing

The overall economic climate in a state should also influence housing policy development. The economic well-being of the state is measured by the poverty rate and unemployment rate in our models. The state poverty rate range is from 2.9% to 27.2% with an average poverty rate of 13.95%. The average state unemployment rate is 6.34% with a range of 2.3% to 17.8%. The poverty rate is available annually from the Census Bureau and the unemployment rate is available from the Bureau of Labor Statistics.

The economic standing variables also give divergent predictions on HTF adoption. Given the relationship between socioeconomic status and housing, we expect that an increased poverty rate and unemployment rate should raise the likelihood of HTF adoption, as informed by diffusion theory. On the other side, poor economic standing could cause policymakers to act, but in the interests of those with higher social standing and power-like businesses and economic development—and not towards helping low-income households. This could lead to little-to-no impact of economic standing on HTF adoption. Given the importance of housing to those in poverty, we believe the economic standing should influence HTF adoption—the worse the economy, the more likely the adoption.

Elected Leadership

Elected leadership can also influence the likelihood of policy adoption. We explore this connection in two ways: the partizanship of the state legislature and the proportion of female state representatives. To assess the effect of partizanship, we use two measures. The first measure is for government ideology from Berry et al. (1998). In this measure, a higher score means a more liberal ideology. In our sample it ranges from 18.6 to 72.6, with a mean at 48.8. The second measure accounts for institutional control—it is a dummy variable for Democratic party unified government. To the best of our knowledge, the academic literature has not addressed how partizanship guides housing policy efforts. Given this lack of theory, however, we are unsure whether elected official partizanship predicts HTF adoption. In general, we may expect the Democratic party and liberal ideology to be associated with supporting those groups in poverty, thus a greater presence of Democrats (and liberals) in government can increase the probability of policy adoption.

We also included the percentage of female state legislators as a control variable in the models. This data was made available by Center for American Women in Politics at Rutgers and Stateminder from Georgetown University. In our sample, the percentage ranges from 1.1 to 41, with the mean of 15.51. Female state legislators and male state legislators have different policy focuses (Osborn and Mendez 2010; MacDonald and O’Brien 2011). Female members of congress, across party ideologies, represent women beyond their district lines (Carroll 2002). Female representatives, including city managers and legislators, tend to focus more on feminine policies such as social welfare, health, and civil rights (Holman 2014; Funk and Philips 2019; Atkinson 2020). Housing policies, as one of the feminized policy areas, is a top priority topic for female state legislators (Atkinson 2020). We predict that those states with a higher percentage of female state legislators are more likely to adopt a Housing Trust Fund.

Housing Investment

More direct to the policy area, we examine how state monetary investment in housing influences HTF adoption. It is measured by the amount of state funds dedicated to housing and community development per capita. The variable captures federal funds that are administrated at the state level such as the CDBG and the HOME Investment Partnerships Program and housing and community development expenditures from state programs, including loan guarantee programs, tax-exempt bond financing, and trust funds, that are used for activities such as but not limited to: planning, construction, and operation of affordable housing projects; rent subsidies, homeownership and renovation programs; urban renewal and slum clearance; and programs that encourage housing production in the private sector. This variable was collected from the Census Bureau State and Local Finance Data and was available annually. The total state housing and community development spending per capital ranges from 0.01 to 0.2 with the mean of 0.05. Our expectation is that more state monetary investment in housing and community development activities should lead to increased probability of adoption of a HTF. The more money invested signals that state budget officers and policymakers are interested in the policy area. More money should mean more awareness and interest in developing and/or being an innovator on that policy front.

Demographics

Lastly, we account for several state demographic characteristics. Housing policy has historically disadvantaged racial and ethnic minorities (Massey and Denton 1993; Rothstein 2017). To account for this, we include the percent of non-white residents in a state. The average proportion of the population that are racial and ethnic minorities in each state is 15.8% with the smallest proportion at 14.5% and largest at 49.1%. We expect that greater percentages of racial and ethnic minorities will increase the probability of HTF adoption, as historically, these are the groups that need the housing support. However, we do recognize that minority population presence may not lead to adoption, as supported by social construction theories.

Similar to our discussion of government ideology, citizen ideology is another guiding factor in elected official decision-making. We use the Berry et al. (1998) measure for citizen ideology (similar to the measure for government ideology). This measure averages 46.1, with a low of 9.3 and high of 93.9. It is a larger range than the institutional ideology. Like before, we do not have academic literature on housing and partizanship. We can deduce though, that lower income people are more likely to need housing assistance (that a HTF can provide) and lower income people are more likely to identify with the Democratic party and more liberal ideology (McCarty, Poole, and Rosenthal 2003). Concurrently, the Democratic Party with a more liberal ideology, is more active with improving the life of the poor through assistance methods (than the more conservative ideologies and Republican Party) (Ladd and Hadley 1975; Stonecash 2018). This can give some support to the expectation that a more liberal citizenry ideology can make HTF adoption more likely to occur.

Sudden growth in state populations can lead to housing shortages. We control for the annual percent change in total population. On average, population increases by 1% annually at the state level while the largest decline seen was 3.8% and the largest increase experienced was 7%. Greater population numbers enhance the demand for housing and contributes to housing affordability issues. If demand outpaces supply, it can increase the need to develop a HTF. Thus, we expect population growth to increase the probability of the adoption of a HTF.

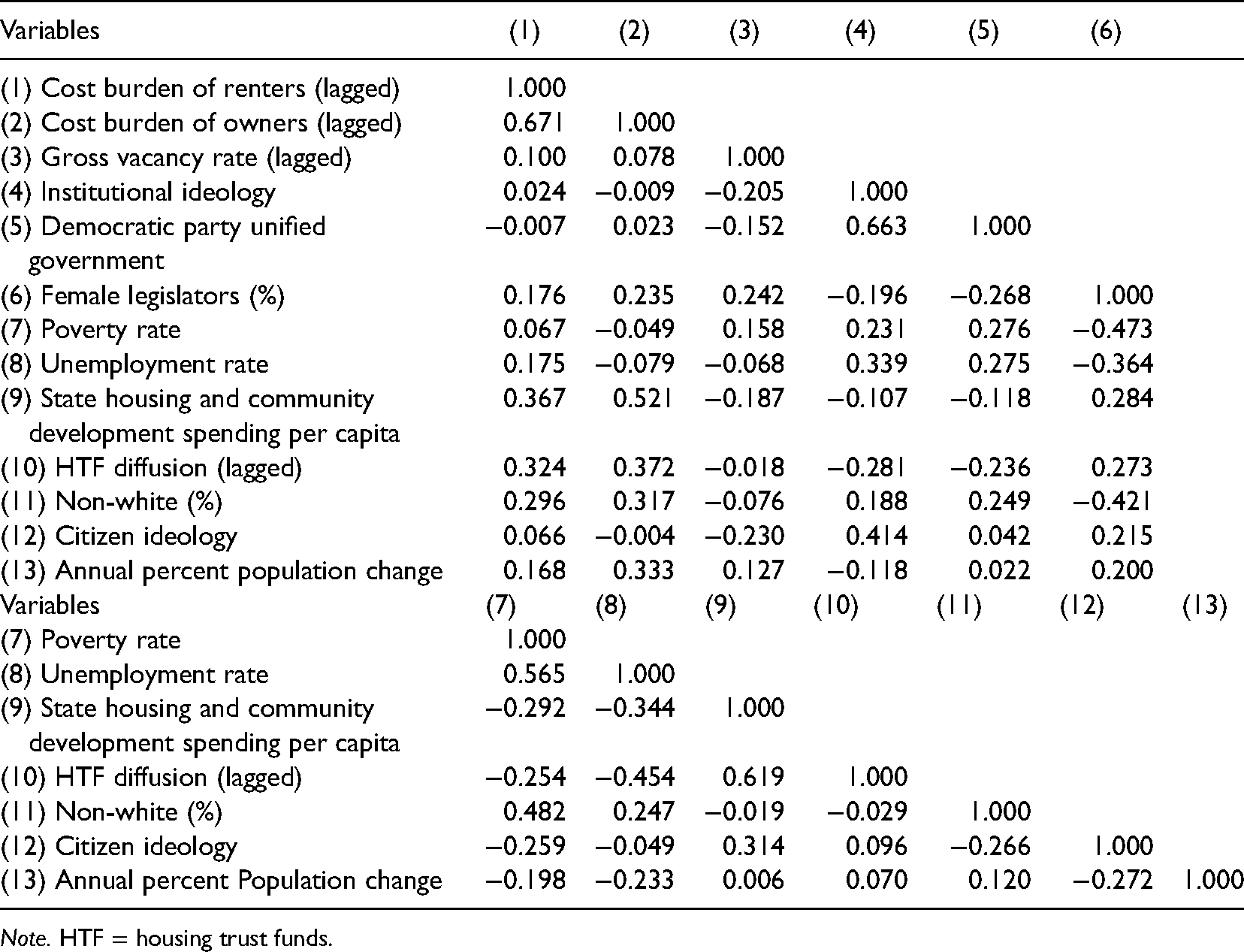

Methods

The dataset consists of 46 U.S. states from 1980 to 2016. The unit of analysis is state-year. Table 1 has the variable descriptive statistics and Table 2 has the correlation coefficients of all variables. We use EHA for two types of empirical tests. EHA is the foundational way to study policy diffusion. The EHA methods allow for studying rare events that occur over a longer time period, within a panel data format. We conduct three logistic regressions and a cox proportional hazard survival model to test the conditions that make policy adoption more likely. These are common methods of analysis within the policy diffusion literature (Berry and Berry 1990; Box-Steffensmeier and Jones 2004; Fay 2018; Hannah and Mallinson 2018). In our context, we are testing how a host of variables contribute to the likelihood of HTF adoption across US states.

Descriptive Statistics N = 757.

Note: HTF = housing trust funds.

Correlation Table.

Note. HTF = housing trust funds.

Our dependent variable for both models is HTF adoption 2 . In each state, the variable is 0 until the year the state adopts a HTF. On the year the HTF is adopted, the variable is coded as 1 and then subsequent observations for that state are dropped from analyses. Additionally, a count variable (starting in 1980) of years until HTF adoption in each state is used for the survival models. If a HTF is never created, as is the case with three of the states in our study, then the count continues until the end of the study period. Information on the year of HTF adoption was based on the work of Scally (2012) and updated with the Center for Community Change Housing Trust Fund Survey Report (2016) and each state's HTF or Housing Finance Agency or similar state government housing agency website.

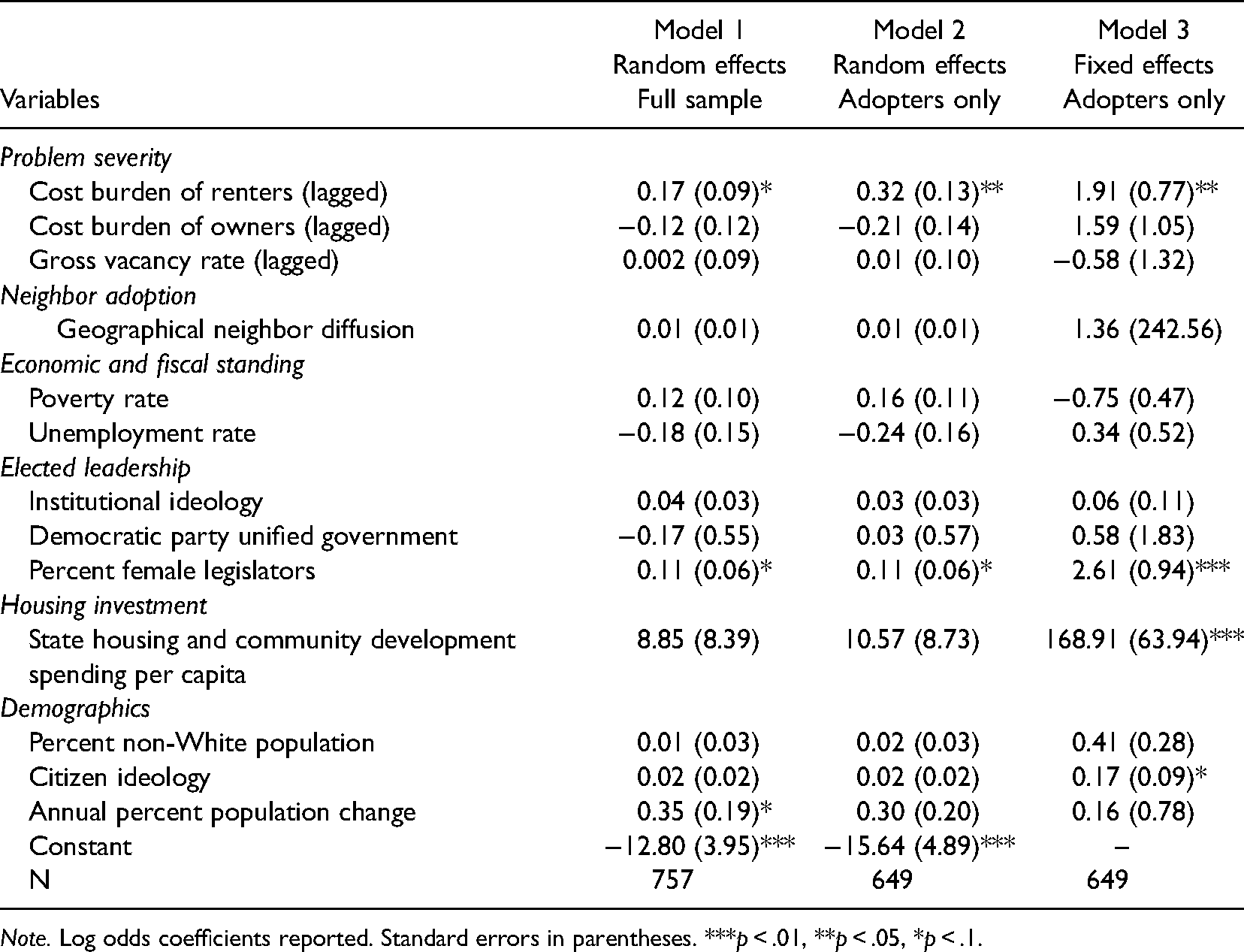

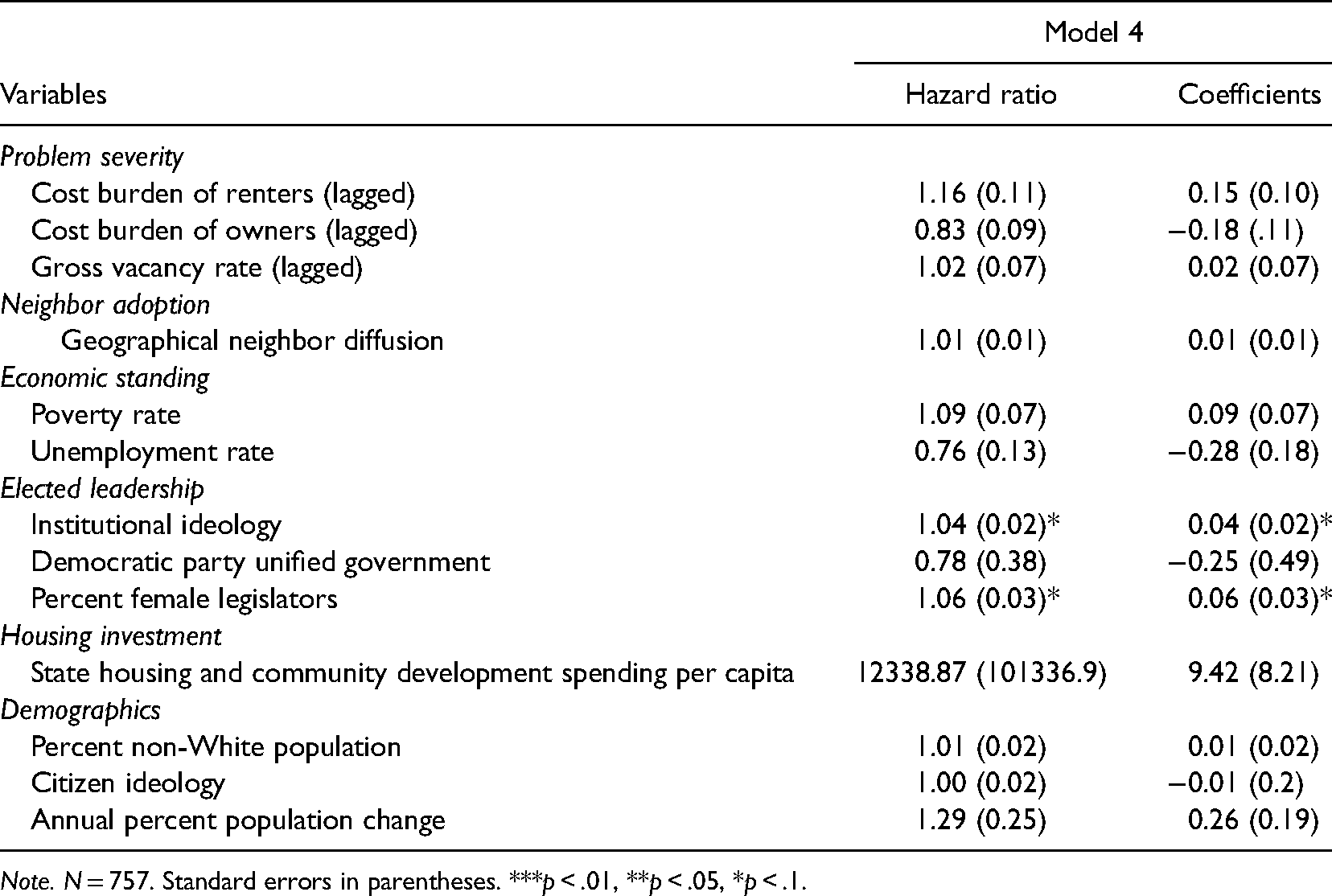

Four states were dropped from all analyses. Alaska and Hawaii were dropped from analyses since they do not have geographical neighbors, an essential element for our study of policy diffusion in the redistributive policy context. Delaware was also dropped from analyses since it was the first state to adopt a HTF (and did so more than ten years before any other state). Nebraska was dropped from the analyses because of its atypical legislative structure. Of the 46 states in the empirical model, 43 have adopted a HTF. The first logit model we report contains the full sample with random effects. The second model is the random effects logistic model for the 43 states who have adopted a HTF. The final logit model (3), has fixed effects to account for the unexplained variance of each state. The fixed-effects model, however, drops the three nonadopters (Wyoming, Utah, and Mississippi) since they have a constant dependent variable, meaning the conditional fixed-effects logit is estimated. Model 2 and Model 3 contain the same sample of states that adopted a HTF (43). Lastly, as Model 4, the cox proportional hazard model uses all 46 states in the analysis. The cox proportional hazard model assesses the hazard rate of an event occurring in a risk period. In our case, the event is the creation of a HTF. This collection of empirical tests will give us a full view of the variables that contribute (or not) to the creation of state HTFs.

Results

Table 3 shows the results of the logistic regressions and Table 4 shows the results of the cox proportional hazard survival model. While none of the models give the exact same results, they do illustrate some themes for each of the concepts expected to influence the rate of HTF adoption in a state 3 .

Logistic Regression Models.

Note. Log odds coefficients reported. Standard errors in parentheses. ***p < .01, **p < .05, *p < .1.

Cox Proportional Hazard Survival Models.

Note. N = 757. Standard errors in parentheses. ***p < .01, **p < .05, *p < .1.

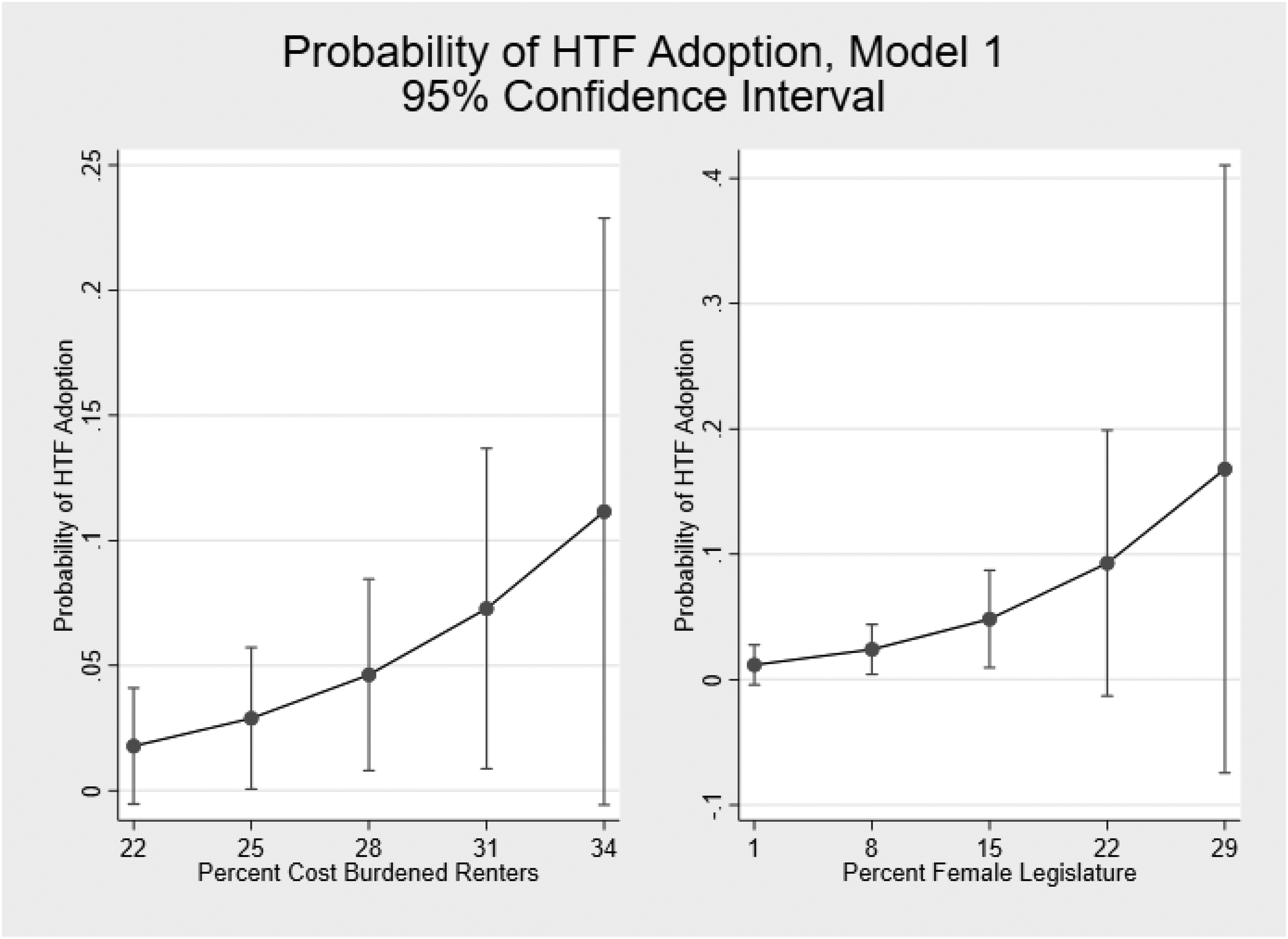

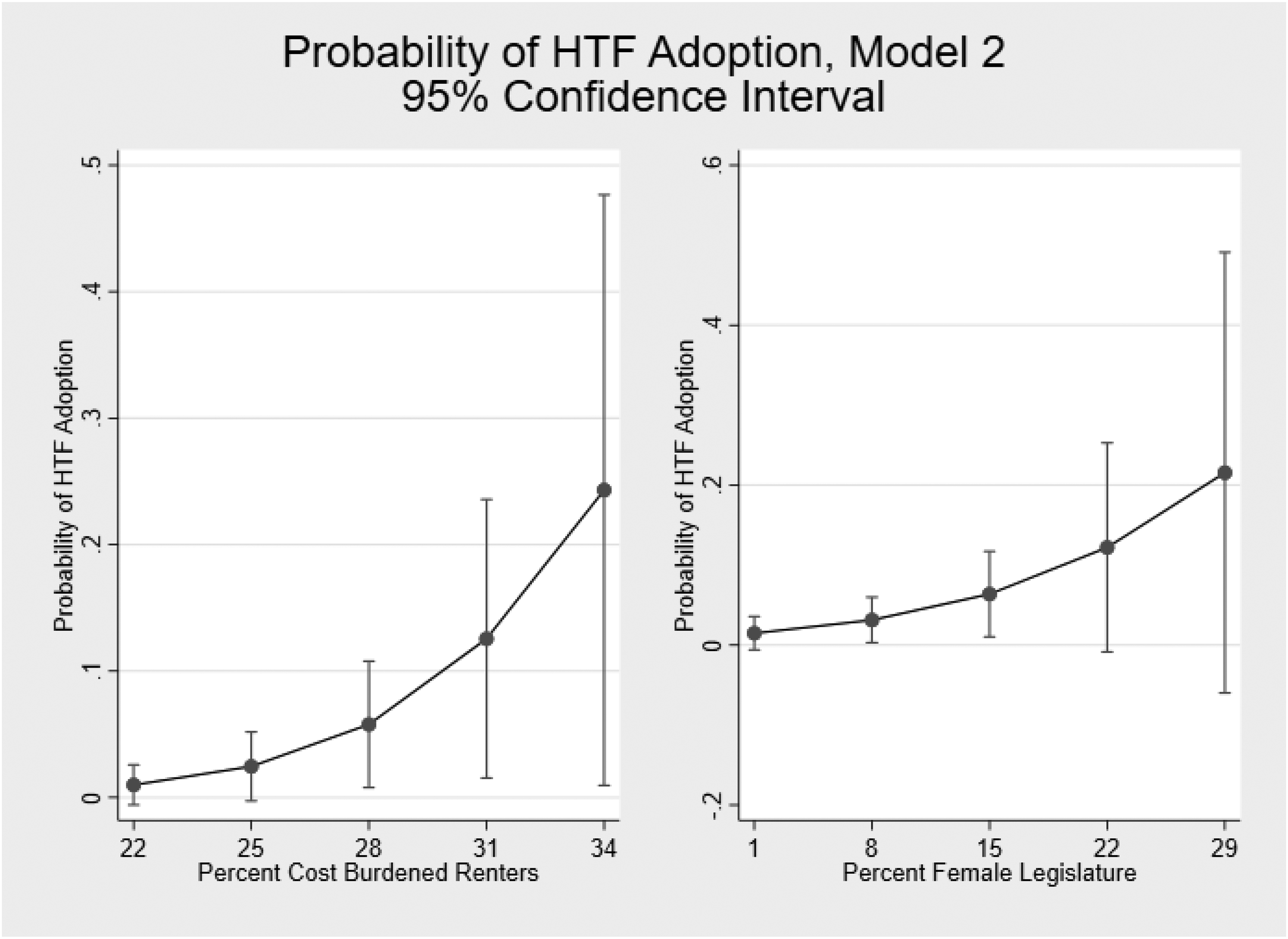

The problem severity variables give some support to the diffusion model. The cost-burdened renter variable is positive and statistically significant in the logit models. This means that as a larger share of renters pays more of their income towards rent, states become more likely to introduce HTFs as a way to fund housing construction and programs. The predicted probability graphs (with variables set to their means) can be seen in Figure 2 for Model 1 and Figure 3 for Model 2. In each graph, we center the variable of interest at about the mean and show the predictions above (below) two standard deviations. In Model 1, at the mean level of cost-burdened renters, the probability of adopting a HTF can reach up to 8%. In Model 2, the mean leads to a top-level of 11% probability of adoption. The probability of HTF adoption increases with greater numbers of cost-burdened renters. Cost burden renter households are often the most vulnerable to housing insecurity and are at the greatest risk of becoming homeless. For this population, state housing trust fund revenues have supported permanent homeless housing, transitional housing, and emergency and permanent rental assistance programs (Center for Community Change 2016). The cost burden to homeowners and the gross vacancy rates are not statistically significant in any of the models. Problem severity represented by cost-burdened renters is in line with diffusion theory that shows problem severity can be a reason to adopt the new policy, even for a redistributive policy area.

Model 1 Predicted Probabilities of Statistically Significant Variables.

Model 2 Predicted Probabilities of Statistically Significant Variables.

In contrast to much of the policy diffusion literature, adoption of a HTF is not influenced by the previous policy adoption by geographical neighbor states. Perhaps other types of “neighbors” are influencing state adoption, such as the sustained organizational influence (Collingwood, El-Khatib, and Gonzalez O'Brien 2019). These findings, though, give some support to the literature on redistributive policies—states do not always deem it in their best interests to be as generous as their neighbors.

The economic variables did not have strong results. The poverty rate and unemployment rate are not statistically significant. This did not support the expectation that economic standing will influence HTF adoption. It supports our other prediction that the allocation of resources may be directed to jobs and/or economic development rather than housing for low-income groups. In states that are struggling economically, housing may not be seen as an essential part of economic recovery efforts.

The effect of elected leadership shows some significant results. Institutional ideology is a statistically significant predictor for HTF adoption in the survival analysis. The variable as a hazard ratio is above one, and positive as a coefficient. It means that HTF adoption becomes 4% more likely with a one-point increase in institutional ideology (a more liberal leaning government). The variable noting a full Democratic government, however, is not statistically significant in any of the models. Of statistical significance across all of the models is the presence of female legislators; a greater number of female legislators is a positive indicator of adopting a HTF. The predicted probabilities in Figures 2 and 3 show a top-level percent probability of adopting a HTF at 9% and 11%, respectively, at the mean level of percent female legislature. This probability increases with more female legislator representation. In the cox model, it shows that a state has 6% increase in likelihood to adopt a HTF with every 1% increase in female legislators. This is in line with the literature on policy areas female legislators promote. Taken together, this does provide some support on a type of “poverty coalition” building as observed in the academic literature and in practice. Our findings suggest that more liberal governments and female legislators support policy development in our redistributive policy context of housing affordability.

For state housing monetary investment, there is one model with a statistically significant finding. The logistic fixed effects model (Model 3 in Table 3) shows a strong, positive relationship between the amount of money spent on state housing and community development per capita and the adoption of a HTF. While we expected housing investment to be a stronger predicter across all models, we can identify a couple of reasons why this relationship may not hold. For one, states may view more money for housing as a substitution for other efforts (like a HTF). Putting more money into existing programs may slow policy creation to new endeavors. Also, we do not know the exact use of those state funds across all states over time except for the broad title of “housing and community development.” The efforts of those funds may not be fully devoted to housing affordability per se, thus would not be a full signal to prior efforts on housing insecurity.

Lastly, the citizen demographics in a state have little influence on the HTF adoption. The only statistically significant result for citizen ideology is in Model 3. It is in line with the institutional ideology results showing that more liberal ideology increases the likelihood of state adoption. The presence of non-white 4 citizens does not have statistically significant effects in our models. Given the historical discrimination of non-white citizens in housing, it is surprising that their presence in a state does not lead to HTF creation. This finding is in line with other work (Flink and Molina 2017) that shows it is not just citizen demand that changes policy, but the need of the target population. The presence of a non-white population does not perfectly predict housing needs. The annual total population change is statistically significant in only the full sample random-effects model. For population growth, it does not always strain housing supply, so perhaps that is why population does not predict HTF adoption.

Discussion and Conclusion

What influences the creation of HTFs for state governments? We revisit this question and confirm and expand on previous findings. We use six categories of variables to predict the adoption of a state level policy: problem severity, neighbor adoption, economic standing, elected leadership, housing investment, and population demographics. Overall, our results give some support that the proportion of cost burden renters, monetary investment in housing and community development, liberal leaning governments, female legislators, and liberal leaning citizens all make state HTF adoption more likely to occur.

Our work has similarities to earlier work on the adoption of state HTFs by Scally (2012). For example, she also finds that state housing expenditures and more liberal citizen ideology increase HTF adoption. It is also not surprising, as Scally (2012) suggests, that the severity of the affordability crisis and the proportion of cost-burdened households is linked to state HTF adoption. On the other hand, Scally (2012) finds that a higher proportion of Black citizens increase adoptions, while we do not find any racial impacts with the additional 12 years of HTF adoption data added to the analysis. Even though the severity of the affordable housing crisis disproportionately impacts racial and ethnic minorities, in more recent years housing affordability has become a mainstream concern for many households, especially those living in high-cost cities. Where political pressure to innovative in the housing arena may have been driven by communities and organizations that historically have been most impacted by residential segregation in the past, political pressure is increasing in all segments of the population to address rising housing costs.

With the influence and uncertainties of the pandemic, hurricanes, fires, and other events, housing policy is an area of increasing importance. Adopting new policies and programs in the housing area is not a simple process. Our study shows that state and local government officials must be aware of many different factors that influence housing policy development. Our contributions extend beyond the housing literature by bringing a newer policy area for consideration to political science and policy process scholars. Basing our work in diffusion theory, we draw from literatures on policy type, social construction, and federalism to develop an understanding of policy development in housing affordability. For the diffusion literature, we add to the body of work on how policy creation works (or does not work) in a redistributive policy area that demanded state innovation due to increasing problem severity and declining federal support (Shipan and Volden 2012; Franko and Witko 2017).

Future work can examine a number of questions on housing affordability generally, and the creation of HTFs more specifically. In housing affordability, research can ask what role female legislators play in the adoption of housing policy and programs at the state level. With a renewed energy for female voices and representation in government, state legislatures’ policy agenda could be reshaped. Research has shown that female legislators tend to focus on social welfare policy areas (Osborn and Mendez 2010; MacDonald and O’Brien 2011; Atkinson 2020) generally, while ours has shown women's potential to prioritize housing. Female legislators may participate and contribute more in the process of forming legislation and programs on housing policies. This is a new line of inquiry that merges the political science and housing fields that have been understudied but may have substantial implications for housing policy innovation. Furthermore, policy diffusion models can be applied to other state housing policies and programs such as the requirements and scoring criteria that are adopted in state Qualified Allocation Plans for the distribution of Low-Income Housing Tax Credits. Moreover, the diffusion models can be explored in other national context and study how housing policies diffuse. Factors such as economic development and culture might also have effects on housing policy adoptions.

In direct relationship to this study, there are avenues for future research. For example, of the states that created a HTF, what leads to the fund being administered by the state Housing Finance Agency or another agency? This type of study falls in line with newer work on administrative agency or process diffusion. Another question is what influences the decision to create a dedicated revenue source and the amount of revenue that the fund generates? Funding is a new aspect to assess in diffusion studies. State and local governments must think strategically about financing mechanisms to fund new policy work and how much revenue these mechanisms will create. The creation of a HTF is a larger financial endeavor that needs consideration for fiscal sustainability. Creating a stable revenue source is essential for trust fund success. There are also potential avenues of research to examine the role of vertical diffusion in HTFs—many local governments have created their own trust funds independent of state efforts. Does municipal HTF creation prompt the county or state to create a HTF or adopt/expand dedicated revenue sources? Do states who create HTFs see a rise in local HTF initiations? Does this impact the types of programs and thus the households that these programs serve? This research can highlight how multiple government actors work in single policy spaces with similar goals.

Future work should evaluate the success of the HTFs. We’ve examined what leads to their creation in a state. However, are the HTFs successful in their work? How does organizational performance vary in this field? HTFs vary in the activities they do to support housing. Do some HTFs do only a small amount of activities well? Do they expand the scope of their work over time? What do HTFs see as the obstacles to their success? There is much work to be done to understand the work of states in the housing policy area.

Footnotes

Acknowledgments

The authors would like to thank Michael Anderson, Jonathan Newburgh, Ken Meier, Nathan Favero, and the participants on the APPAM 2020 Housing Programs Panel for their guidance on this project.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.