Abstract

Can the design of governmental institutions promote timely governance? This article investigates this question by examining the relationship between the design of fiscal institutions and budgetary delays across the fifty states. These budgetary offices are created by lawmakers to advance sound fiscal policy and sustainable public finance. This article argues that the unbiased information provided by nonpartisan budget offices minimize the likelihood of budgetary delay as well as lessen how long budgetary stalemate persists when a delay occurs. The findings suggest that nonpartisan fiscal institutions do not prevent budgetary delay but substantially reduce the duration of budgetary gridlock.

Introduction

From fiscal years 1961 to 2019, the state of New York has missed its budget deadline nearly two-thirds of the time (thirty-eight of fifty-nine budgets). Indeed, between 1985 and 2004, New York’s legislature delivered its state budget late, forcing the state government to rely on interim budgets. Such delays are not costless (e.g., Pulsipher 2004), and lawmakers and observers criticize the process (e.g., DeWitt 2019; Williams 2019; McMahon 2020) since timely budgets are viewed as a measure of good governance (Putnam 1993). New York is not the only state to struggle with its budget: Five states on average have been late in passing their budget each year since 1961, with at least one state late every year.

Budgeting can lead to contentious negotiations since they determine the levels of spending and revenues and thus a state’s priorities (Rosenthal 1990). Consequently, compromise frequently falters when executive and legislative actors end up in in budgetary standoffs (National Conference of State Legislatures 1995; Kousser and Phillips 2009, 2012). In recent years, partisan budgetary deadlocks have resulted in late budgets becoming commonplace (Farmer 2017), with proposed causes including divided government (Andersen, Lassen, and Nielsen 2012; Cummins 2012; Kirkland and Phillips 2018), partisan polarization (Birkhead 2016), institutional conditions (Klarner, Phillips, and Muckler 2012; Fowler and Rudnik 2015), and the economy (Andersen, Lassen, and Nielsen 2012).

Still, state legislatures themselves vary in their fiscal capacity, including their access to unbiased fiscal information. Thirty-nine states have nonpartisan budgetary institutions that are designed to provide unbiased fiscal information to state lawmakers. In contrast, ten states in addition to New York maintain partisan fiscal institutions, embedding them in existing state legislative committees. This article exploits this variation by examining if a state legislature is more likely to pass a state budget on time when nonpartisan budgetary institutions provide them with unbiased information. Using a dataset of all state legislative budgetary bodies spanning a half-century, the analysis investigates whether and how these fiscal bodies affect budget passage and whether the presence of a nonpartisan body helps to resolve budget impasses more quickly. Ultimately there is little evidence that the presence of a nonpartisan fiscal office makes budget impasses less likely. However, when controlling for the degree of partisan polarization of a legislature (Shor and McCarty 2011), the involvement of a nonpartisan fiscal institutions appears to end budgetary delays more than thrice as quickly as compared to states with partisan fiscal institutions.

Budgetary Delay and Nonpartisan Fiscal Institutions

Students of budgetary delay have focused primarily on the effects of partisan control of government and the ideological composition of legislatures. Broadly speaking, divided government depresses legislative productivity (Bowling and Ferguson 2001; Hicks 2015). With respect to the budgetary process, divided government is meaningful because the governor in nearly every state has wide-ranging powers over the budget. For example, forty-three states endow the governor with line-item veto powers to nullify specific provisions of the budget bill (Holtz-Eakin 1988; Krupnikov and Shipan 2012). In contrast, one-party states leads to less political gridlock over the budget (Farmer 2019). Consequently, divided government arguably promotes budgetary disputes within state legislatures and increases the likelihood that a budget will be late (Clarke 1998; Andersen, Lassen, and Nielsen 2012; Cummins 2012; Lu and Chen 2016; Kirkland and Phillips 2018).

Rising partisan polarization in state governments also corresponds to increased acrimonious debate throughout the budgetary process (Shor and McCarty 2011; Birkhead 2016). Polarized parties and intercameral differences stagnate the legislative process, resulting in fewer bills passed each year (Binder 2003; Rogers 2005; Hicks 2015). Additionally, large ideological gaps between the executive and legislative branches increases the probability that the governor’s budget will be contested by the legislature (Clarke 1998).

Beyond political indicators, economic conditions and state laws affect the likelihood of budgetary delay. Favorable economic circumstances reduce the probability of budget impasses. Budgetary surpluses grant lawmakers latitude in reaching consensus over the budget, as indecisive lawmakers can be bought out through side payments (Evans 2004). Similarly, falling unemployment rates decreases the likelihood of budgetary delay (Andersen, Lassen, and Nielsen 2012). In contrast, state laws can dramatically amplify the costs of budgetary gridlock for lawmakers. The political price of budgetary delay for lawmakers is higher during an election year and when state laws mandate a government shutdown in the lack of an enacted budget (Andersen, Lassen, and Nielsen 2012; Klarner, Phillips, and Muckler 2012; Fowler and Rudnik 2015). For example, Minnesota’s twenty-day shutdown in 2011 furloughed nineteen-thousand public employees and suspended public services, escalating pressure on lawmakers to pass a budget (MacKellar 2017).

Negative ramifications almost always follow budgetary delay. States commonly incur additional costs from extended or special sessions and late fees from vendors under state contract, in addition to legal action from dismissed state employees (Pulsipher 2004; Niquette 2009). Consider Illinois’ 736-day-long budget crisis from 2015 to 2017. Budget stalemate between Republican Governor Bruce Rauner and Democratic House Speaker Mike Madigan regarding implementation of Rauner’s “Turnaround Agenda” led to the state’s credit rating being downgraded several times, with Illinois having been on the verge of becoming America’s first state with a “junk” credit rating (Egan 2017). Core components of the “Turnaround Agenda” like the elimination of collective bargaining rights and cuts to workers’ compensation rates stalled Illinois from passing a complete state budget for fiscal years 2016 and 2017, leading state agencies to either cut services or borrow funds for their operations. Ultimately, the Office of the Illinois Comptroller reported that the impasse affected “billions of dollars in stalled programs, and cost over a billion dollars in late payment interest penalties, higher debt service costs, and lost investment…[and] hindered recovery post-Great Recession” (Mendoza 2018, 11).

Lost in the partisan struggle between Governor Rauner and the Illinois legislature was the role of budgetary information. As mandated by Illinois’ Legislative Commission Reorganization Act of 1984, its Commission on Government Forecasting and Accountability (CGFA) provides the legislature with reports regarding revenue projections and operations, in addition to advice on long-term planning and budgeting (Illinois Commission on Government Forecasting and Accountability n.d.). While the CFGA’s duties are similar to other budgetary institutions across the United States, the office is overseen by twelve sitting legislators appointed by the four legislative leaders (Speaker of the House, House Minority Leader, Senate Majority Leader, and Senate Minority Leader) each appointing three members. Despite being an intendedly bipartisan office, these legislators often pursue their own partisan policy priorities. For example, when Republican State Senator Jil Tracy announced her appointment to the CGFA, she indicated “the need for more business-friendly reforms” (Tracy 2017). Concerning budget bills, legislators’ personal interests undoubtedly conflict with one another in the CFGA, reducing the effectiveness of the budgetary institution. These partisan fiscal institutions potentially stymie the budgetary process, as leaders struggle to identify the information that promotes fiscal responsibility.

In contrast, the reports from nonpartisan fiscal organizations are designed help to facilitate agreements and bargaining. These institutions are apolitical legislative government agencies with a mandate to critically assess and provide unbiased advice on fiscal policy and performance. Their functions include fiscal and budgetary analysis, revenue estimating, budget recommendations, and the publication of materials for both legislators and the public at-large. Beyond reports, staff members may be meaningful actors in the budget process. For example, the director of Iowa’s nonpartisan Legislative Services Agency meets three times per year with governor representatives to project state revenues as a precursor to budget negotiations (Richardson 2020).

If budgets are considered as contracts among lawmakers (Wildavsky 1964), nonpartisan fiscal bodies reduce transaction costs for legislators by providing crucial information for state budgetary decisions (Coase 1937). Moreover, a long-established literature emphasizes the significance of information for legislatures. Access to information is a vital political tool, amplifying power and influence within the chamber (e.g., Gilligan and Krehbiel 1987; Krehbiel 1991; Jones and Baumgartner 2005; Baumgartner and Jones 2015; Zelizer 2018). Given that legislators regularly lack the policy expertise to make informed decisions (e.g., Simon 1957, 1982; Kingdon 1989; Jones and Baumgartner 2005), nonpartisan fiscal institutions serve as vital reference points for legislators when crafting budgets. Thus, the unbiased reports from nonpartisan budgetary bodies promote sound policy and sustainable public finances by reducing the negotiation costs that may delay budget passage (Goodman and Clynch 2004). This leads to the first hypothesis:

As previously stated, partisan rancor amplifies the likelihood of budgetary delay (Clarke 1998; Andersen, Lassen, and Nielsen 2012). This is partially attributable to the minority party denying the majority party policy victories to bolster their own election hopes (Aldrich 2011). While majority lawmakers may seek to reach compromise and limit the reputational and electoral costs of delay (Calmfors 2011; Von Trapp, Lienert, and Wehner 2016), minority legislators possess a collective political incentive to obstruct majority goals (Lee 2009, 2016). Legislative behavior that accentuates majority party failings benefits minority legislators, especially given recent rises of negative partisanship and affective polarization within the electorate (Iyengar et al. 2019).

On average, compromise is a negative outcome for the minority party because cooperating with the majority undercuts their future electability (Gilmour 1995). Although public opinion polls suggest declines in approval ratings (and therefore reelection prospects) for lawmakers during budgetary gridlock (Kousser and Phillips 2009), competitive dynamics may make it beneficial for minority parties to prolong budget impasses. In states that have partisan fiscal offices, minority legislators can continue to cite the partisan information that serves their purposes, complicating the majority’s ability to pass a budget.

Partisan information sources likely muddles the budget process, extending budgetary delays. For example, the majority and minority party of each chamber in New York’s legislature have their own budget staff. These personnel provide information exclusively to their respective membership, tailoring budget data to advance their own priorities and shape policy over budgetary spending. Ultimately, New York lawmakers like Senator Liz Kreuger (D-28) characterize the budget process as “making it up as you go along” (Krueger 2019). The credible information provided by nonpartisan fiscal institutions likely streamlines debate over the budget when the budget is delayed. This logic underlies New York State’s recent attempts to limit its budgetary chaos, with its State Senate Committee on Ethics and Internal Governance voting in March 2019 to advance a bill to create a nonpartisan legislative fiscal office.

Overall, the credible information provided by nonpartisan fiscal offices likely streamlines debate over the budget when the budget is delayed. Facts from a singular nonpartisan entity limit the effectiveness of obstructing with partisan information. This ought to be an unconditional effect, occurring even when a state has multiple budgetary institutions operating at the same time (e.g., California’s nonpartisan Legislative Analyst’s Office (LAO) and its partisan budget staff housed in each chamber’s committees (e.g., California’s Senate Budget and Fiscal Review Committee)). This is because nonpartisan fiscal bodies are entrusted to constrain lawmakers and provide the necessary information to efficiently allocate resources to advance economic stability (Beetsma et al. 2019). Moreover, the nonpartisan information distributed by these offices provide reelection-minded legislators with an outlet to support budget passage to limit the negative consequences associated with budgetary gridlock. This leads to the second hypothesis:

Data and Methods

Variation in the presence of nonpartisan budgetary bodies is required to explore the effects of the design and impact of budgetary institutions on budgetary passage. Data on state legislative budgetary bodies across all fifty states comes from Emrich (2020), who categorizes nonpartisan fiscal offices based on if they had “nonpartisan,” “independent,” or “objective” fiscal information in their description. As a robustness check, this coding was cross-referenced with the National Conference of State Legislatures’ (2019) categorization. Supplemental Figure 1 provides a visualization of nonpartisan fiscal institutions across the United States, and Supplemental Figure 2 shows a chronological panel view of each state and the date of implementation of its nonpartisan fiscal office. Every state has a fiscal body throughout the entire time series. Supplemental Table 1 lists each state’s (or state legislative chamber’s) legislative budgetary institution and its year of enactment.

The analyses use two outcomes variables capturing the existence of and duration of a budgetary delay. The dependent variables are collected using the method of Klarner, Phillips, and Muckler (2012) and Birkhead (2016), who harmonize budget due dates from the Book of the States collection with state legislative journals. A budget is noted as late if it was passed after the first day of the new fiscal year (July 2 for most states). Cumulatively, the data cover 1961 to 2016, with a total of 2,124 state-years across forty-nine states. State-years may be missing for a variety of reasons. First, Nebraska is excluded from the analysis given its unicameral legislature. Second, several states operate with a biennial budgeting system and thus appear every other year in the data set. Third, legislative journals were unable to be recovered for some years. For example, budget data for Alaska extends from 2007 to 2016. Likewise, data for Illinois only exists between 1992 and 2016 due to Illinois’ adoption of dozens of smaller budget bills prior to 1992, making it effectively impossible to determine an adoption date (Klarner, Phillips, and Muckler 2012).

Of the 2,124 state-years, there were 321 budget impasses, totaling about 15.1 percent of the sample. Supplemental Figure 3.A plots the percentage of late budgets by year. Fiscal delay fluctuates from two to twenty-four percent of budgets in a given year, although there are no obvious patterns in the data. Despite no clear year-to-year relationships, there are state-specific trends. Twenty states did not have a budget delay over the past fifty-six fiscal years, while seven states were late on their budgets over fifty percent of the time. Supplemental Table 2 provides the frequency, average length, and maximum length of budgetary delay by state.

Given the binary nature of budgetary delay, hypothesis 1 is tested with a logistic regression model with two-way random effects (Smithson and Merkle 2013). The dependent variable is a dichotomous indicator equal to 1 if a state budget was passed after the start of the fiscal year or biennium, and 0 if the budget was passed on time. Year random effects are included to account for year-to-year differences in budgetary delays common across all states and state random effects are used to capture unit-invariant characteristics.

The second outcome variable, the length of a budgetary delay, accounts for how late a budget is. Following Box-Steffensmeier and Jones (2004), hypothesis 2 is analyzed using an event history model with the Cox proportional hazards method. In terms of survival analysis, the “survival” is the period from the time the budget was late to the time it was finally passed and the “death” is the final passage of the budget (i.e., the end of the delay). The longest delay in the dataset is Illinois in fiscal year 2016 where no budget was passed (i.e., a delay of 365 days). The shortest delay was a single day, which occurred nineteen times. The dependent variable is a ratio variable equal to the number of days after the start of the fiscal year or biennium before a budget was passed. The primary independent variable for both models is the presence of a nonpartisan budgetary institution in a state in a given year. This is a dummy variable equal to 1 if the state has a nonpartisan fiscal body, and 0 if the state only has a partisan fiscal institution. Every state has a fiscal body throughout the entire time series (see Supplemental Figure 2). Across the whole time series, states with nonpartisan fiscal institutions had late budgets roughly 16.7 percent of the time, whereas states with partisan fiscal bodies were late roughly 14.1 percent of the time.

Supplemental Figures 3.B and 3.C present the percentages of late budgets over time partitioned by the form of the state’s budgetary office. Supplemental Figure 3.B illustrates delay when a state has a nonpartisan fiscal institution; Supplemental Figure 3.C shows delay with partisan fiscal bodies. Overall, there is relatively little difference in the levels of budgetary delays from 1960 to 2000. However, impasses became marginally more likely after 2000 in states with partisan budgetary offices. Delays peaked in 2009 during the fallout of the Great Recession when over half of the partisan fiscal states passed their budgets late.

The same covariates are used to test both hypotheses. First, political variables that influence budgetary delay are used by including a dummy variable to account for divided government, a dummy for if a state has a shutdown provision, and a dummy for if the fiscal year is also an election year. Ideological characteristics of a state are captured by taking the difference between the median ideology score of the majority party in each legislative chamber. Next, institutional factors are included by creating an interval variable when a state’s legislative session starts relative to the start of the fiscal year, an interval variable for a state’s start month of the fiscal year, a dummy variable for if a state requires a legislative supermajority to adopt a budget, a dummy for if a state operates on a biennial budgeting system, a dummy variable for if a governor has line item-veto powers, and an interval variable controlling for the professionalization of the legislature. Finally, fiscal conditions are controlled for by incorporating the lagged total surplus for a state and the budget’s size. Supplemental Text 1 provides a detailed description of the covariates used.

Predicting the Likelihood and Duration of Late Budgets

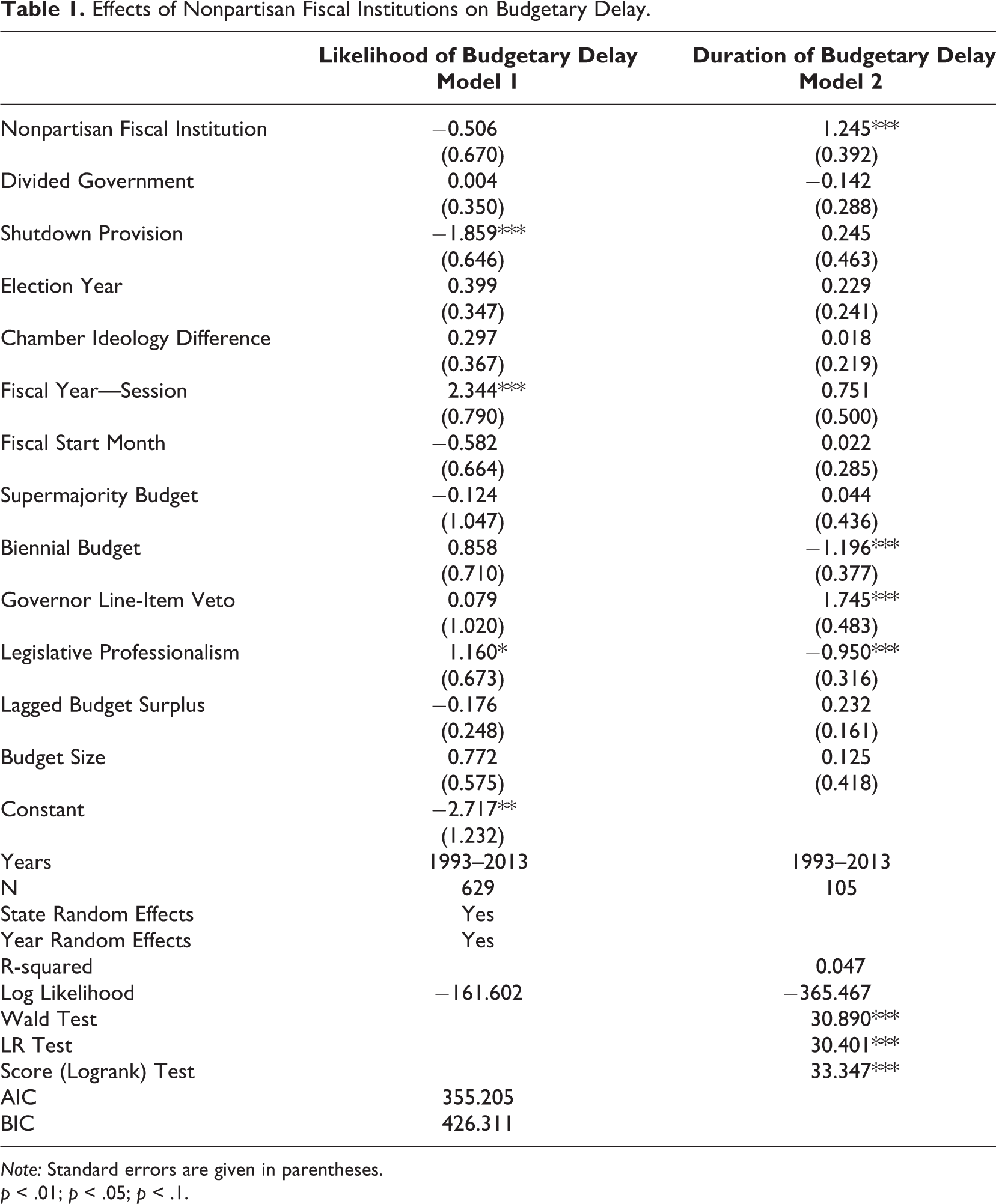

The results of the logistic random effects and Cox proportional hazard models are provided in Table 1. For ease of interpretation, all continuous independent variables are standardized (i.e., have a mean equal to 0 and standard deviation equal to 1) to facilitate direct comparisons in effect sizes across all variables (Gelman 2008). Model 1 shows the relationship between the presence of a nonpartisan fiscal office and budgetary gridlock. Overall, there is little evidence that nonpartisan fiscal institutions reduce the likelihood of budgetary delay, thus offering no support for hypothesis 1. As a robustness check, Supplemental Table 3 estimates the same model using two-way fixed effects for state and year and clustered standard errors. Results are unchanged regardless of model specification.

Effects of Nonpartisan Fiscal Institutions on Budgetary Delay.

Note: Standard errors are given in parentheses.

p < .01; p < .05; p < .1.

A single control variable is significant in reducing the likelihood of budgetary delay. Consistent with previous research (e.g., Klarner, Phillips, and Muckler 2012), the presence of a government shutdown provision greatly reduces the probability of budget impasses. The high political costs associated when a shutdown is triggered likely compels lawmakers to enact a budget and avoid public animus. In contrast, the probability of stalemate grows as session length increases. Longer sessions correspond to smaller private costs of budgetary delay for lawmakers, as legislators in these states are not required to remain in the state capital for indefinite budget negotiations.

Although the findings from model 1 indicate that nonpartisan fiscal institutions do not influence the likelihood of budgetary delay, these offices may affect how long a budget impasse lasts. Many states had budget delays extending over months, whereas others resolved their budgets a few days after the deadline. For example, the average delay for New York was over forty days, and between 1994 and 2004 the state averaged a delay of eighty days.

Model 2 presents the results of the Cox proportional hazard models based on the 105 budgetary delays that occurred between 1993 and 2013. The results are provided as hazard ratios, where if the hazard ratio is less than 1, larger values of the independent variable are associated with longer budgetary delays. In contrast, when the hazard ratio exceeds 1, it means larger values are related with shorter budgetary delays. Model 2 demonstrates that nonpartisan fiscal institutions an influential moderator of budgetary gridlock in recent years, greatly reducing the duration of fiscal delay. The only other variable that significantly reduces the length of budgetary delay is if a governor possesses line-item veto powers. Line-item vetos are likely vital for negotiating budget agreements once the negative effects of a budget delay have occurred as the governor can unilaterally veto outlier requests that would otherwise condemn compromise.

Two variables prolong budgetary gridlock: the presence of a biennial budgeting system and higher levels of legislative professionalism. Crafting two-year budgets are problematic for lawmakers since economic forecasts two years into the future are somewhat unreliable (Snell 2011). Likewise, professionalized legislatures greatly extend budgetary delays, as empowered legislatures often pursue their own policy interests (Rosenthal 1990). This has led to budgetary standoffs between political branches given the executive’s historical control over budget procedures, with entrenched executive and legislative branches each waiting for who will “blink” first (Kousser and Phillips 2009, 2012).

Given the log link function associated with the Cox proportional hazards model, Supplemental Figure 4 illustrates the exponentiated effect of nonpartisan fiscal bodies on budgetary delay derived from model 2’s estimates based on 1,000 simulations. The most transparent ribbon shows the 95 percent probability interval, whereas the less transparent ribbon illustrates the central 50 percent interval. The middle line shows the interval’s median, and demonstrates that delays are on average 3.47 times shorter when a state has a nonpartisan fiscal institution relative to a partisan fiscal body. Succinctly, lawmakers appear to utilize unbiased information when pressure is magnified during budget impasses.

Discussion and Conclusions

These findings indicate that nonpartisan budgetary information has differing effects on the state budgetary process. While nonpartisan fiscal institutions do not depress the likelihood of budget impasses, they are meaningful in limiting budgetary delay. Lawmakers’ electoral priorities and partisan conflict likely overwhelms information during initial budget deliberations. However, once the negative consequences of late budgets are realized, unbiased information in legislatures provides a resource for lawmakers to reconcile political negotiations on critical policy issues. These results align prior research that suggests that increased state legislative capacity moderates lawmaker behavior (Barber, Bolton, and Thrower 2019).

Despite the potential for electoral sanctions after a budget is late, lawmakers seem unconcerned with delayed budgets during an election year (Cummins 2012). Despite a long literature in legislative politics arguing that distributive benefits directly affect lawmakers’ electoral outcomes (e.g., Mayhew 1974; Fenno 1978; Arnold 1990; Finocchiaro and Jenkins 2016), fear of electoral reprisal may be reduced since state legislators are reelected at exceedingly high rates and therefore lawmakers may not feel pressure to reach a budgetary compromise (Rogers 2015). This finding has important implications for electoral accountability because a cornerstone of democracy is the mass public’s evaluation of elected officials’ performance (Healy and Malhotra 2013).

Finally, these results show that institutional differences function as an important explanatory factor for understanding policy change. Like prior work exploring the determinants of budgetary delay (e.g., Klarner, Phillips, and Muckler 2012; Birkhead 2016), government shutdowns in the absence of a budget and the timing of the legislative session relative to the start of the fiscal year are the most influential predictors of budgetary gridlock. Similarly, the presence of a nonpartisan fiscal office is a prominent factor in ending budget impasses. These findings suggest that statutory regulations that constrain lawmakers in state legislatures are more meaningful than political or economic factors, contrary to contemporary analyses lamenting the negative gridlocking effects of partisan polarization (National Conference of State Legislatures 2018).

Supplemental Material

Supplemental Material, sj-docx-1-slg-10.1177_0160323X21990731 - The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay

Supplemental Material, sj-docx-1-slg-10.1177_0160323X21990731 for The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay by Colin Emrich in State and Local Government Review

Supplemental Material

Supplemental Material, sj-docx-2-slg-10.1177_0160323X21990731 - The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay

Supplemental Material, sj-docx-2-slg-10.1177_0160323X21990731 for The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay by Colin Emrich in State and Local Government Review

Supplemental Material

Supplemental Material, sj-docx-3-slg-10.1177_0160323X21990731 - The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay

Supplemental Material, sj-docx-3-slg-10.1177_0160323X21990731 for The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay by Colin Emrich in State and Local Government Review

Supplemental Material

Supplemental Material, sj-docx-4-slg-10.1177_0160323X21990731 - The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay

Supplemental Material, sj-docx-4-slg-10.1177_0160323X21990731 for The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay by Colin Emrich in State and Local Government Review

Supplemental Material

Supplemental Material, sj-docx-5-slg-10.1177_0160323X21990731 - The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay

Supplemental Material, sj-docx-5-slg-10.1177_0160323X21990731 for The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay by Colin Emrich in State and Local Government Review

Supplemental Material

Supplemental Material, sj-docx-6-slg-10.1177_0160323X21990731 - The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay

Supplemental Material, sj-docx-6-slg-10.1177_0160323X21990731 for The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay by Colin Emrich in State and Local Government Review

Supplemental Material

Supplemental Material, sj-docx-7-slg-10.1177_0160323X21990731 - The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay

Supplemental Material, sj-docx-7-slg-10.1177_0160323X21990731 for The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay by Colin Emrich in State and Local Government Review

Supplemental Material

Supplemental Material, sj-docx-8-slg-10.1177_0160323X21990731 - The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay

Supplemental Material, sj-docx-8-slg-10.1177_0160323X21990731 for The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay by Colin Emrich in State and Local Government Review

Supplemental Material

Supplemental Material, sj-docx-9-slg-10.1177_0160323X21990731 - The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay

Supplemental Material, sj-docx-9-slg-10.1177_0160323X21990731 for The Impact of Nonpartisan Fiscal Institutions on Budgetary Delay by Colin Emrich in State and Local Government Review

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.