Abstract

As a considerable area of conflict in the US broadcast market, the issue of retransmission payments has gained momentum in Europe as well. By conducting case studies of two European regions, Flanders and Denmark, this article focuses on the political economy of retransmission payments in the broadcaster-to-distributor market. It is suggested that the competitive position of an actor in a bargaining game crucially depends on contextual factors, including market concentration, vertical integration and product differentiation.

In European markets, broadcasters used to depend on fairly simple revenue streams for many years. Until the 1980s, public service broadcasting derived income from licence fees, possibly complemented by advertising revenues. When audiovisual markets were liberalised, a dual order emerged in which public service broadcasters’ funding model remained unchanged and private, free-to-air television companies built a lucrative business selling advertising (Michalis, 2007). With television advertising markets gradually shrinking and support for public service broadcasting declining, the golden years of broadcasters’ profitability may have come to an end. Since new players have entered the business at all stages along the value chain, the pie has to be divided amongst an ever-increasing number of actors. Consequently, the changing economic environment has compelled broadcasters to look at alternative and more stable sources of income (Jung and Chan-Olmsted, 2005).

The striving for diversification of revenues became most obvious in the United States. Broadcast networks started arguing that cable operators earned money with their content without adequate compensation. Consequently, they began to aggressively pursue retransmission payments from cable operators. Fights between broadcast networks and cable operators have ended in mediatised blackouts, with broadcasters pulling off their signals during negotiations as bargaining leverage and campaigning to raise public awareness. Blackouts between programmers and distributors, once rare, are now becoming commonplace in the US market, with high-profile examples of ‘cable battles’ between Fox and Time Warner Cable, and NFL Network and Comcast dominating the debates about a fair revenue sharing model between both parties. While addressing the News Corporation’s 2009 annual meeting, Rupert Murdoch stressed that ‘asking cable companies and other distribution partners to pay a small portion of the profits they make by reselling broadcast channels, the most-watched channels on their systems will help to ensure the health of the over-the-air industry in America.’ Paradoxically perhaps, Murdoch’s BskyB platform has consistently argued against the payment of retransmission fees in the United Kingdom, as insisted on by the then BBC Director-General Mark Thompson. 1

By conducting in-depth case studies of two European markets, 2 this article focuses on the political economy of retransmission fees in the broadcaster-to-distributor market. These payments are highly controversial in the United States and Canada, but the issue is on the rise in European television markets as well. Being an area of considerable industry conflict, negotiations of retransmission payments may well illustrate the intensifying competition for scarce resources and reflect the on-going battle for power and control in the market. However, as will be shown in the case studies, market-specific bargaining parameters largely influence which party gains control over these monetary streams and, hence, the audiovisual value network. In addition, policymakers – even though some would argue their powers are limited – also affect the power balance between broadcasters and the distributors of their signal. Starting from a political economy perspective, the next section deals with the circulation of power within broadcast markets. After a note on the research design, the markets in Flanders (the northern region of Belgium) and Denmark are discussed and compared, using a mix of qualitative and quantitative data. In the final section, conclusions are provided and future perspectives are set.

Power and control in broadcasting

Power balance in media industries

Much of the literature on power balance in media industries is rooted in the political economy of communication. This critical approach aims at unravelling social and, in particular, power relations within media ecosystems and analysing structural processes of control over the production, distribution and consumption of information goods. The political economy of communication examines the institutional aspects of media and telecommunications systems, with particular attention to the economic attributes of cultural commodities, and the historical relationships between industry, state and consumers (Mosco, 2009). Through studying the concentration of ownership and control in media industries, political economists deal with corporate power and look at structural inequalities within capitalist market systems. Following this perspective, firms may exert market power on competitors when achieving monopolistic control over industry bottlenecks, such as premium sports rights or distribution networks. Bottlenecks refer to scarce but essential resources upon which the economic performance of an industry strongly depends. Hence, ownership of industry bottlenecks allows companies to play a ‘gatekeeper’ role in the market. As Poel and Hawkins (2001) contend, any analysis of access issues in bottleneck environments should take into account the commercial relation of the access providers with both service providers and end-users. The control of access to scarce resources, however, may be jeopardised in an era of plenty, which urges firms to seek new ways of constraining abundance in order to preserve market power (Mansell, 1999). With the rapid adoption of digital media technologies that substantially reduce distribution bottlenecks, Flew (2011: 86–87) questions ‘whether the economic power conferred by control over distribution channels and networks is diminishing over time or is being reconfigured around alternative sources of economic rents, such as highly restrictive copyright and intellectual property regimes’.

With regard to the power balances in broadcasting markets, and more specifically between broadcasters and distributors, traditional political economists consider power relations as static and determined, contending that distributors have gained economic power to the detriment of creativity and content creation. A seminal contribution to the field was made by Garnham (1987: 31), arguing that ‘it is cultural distribution, not cultural production, that is the key locus of power and profit’. The author contends that because the business of cultural goods is as much about ‘creating audiences’ as it is about ‘producing cultural artefacts’, distribution is characterised by the highest level of capital intensity, ownership concentration and multi-nationalisation. Distributors act as gatekeepers, controlling access and bundling programming to commoditised audiences. Controlling the distribution bottleneck is like having a ‘liquor licence’ that awards distributors a privileged position along the value chain. In contrast to the high number of producers, economic power resides with those few firms that have oligopolistic control over the delivery of cultural productions – referring to the hourglass structure of media industries (many producers, few distributors). This concentration of ownership may result in power asymmetry with relations of power skewed towards distributors, and broadcasters highly depending on delivery networks controlled by multichannel operators (Hesmondhalgh, 2007).

According to another viewpoint, however, technological forces, and more abundance in transmission technologies in particular may loosen and eventually eliminate this distribution bottleneck. Hence, economic power is considered a fluid concept that, depending on the configuration of business activities, circulates within the industry. As spectrum scarcity comes to an end, new distributors may come into the market and erode the power of established gatekeepers. Todreas (1999: 34) points out that profits move upstream, stating that ‘conduit[s] will resemble a commodity while content will have the opportunity to create branded, high-value-added products’. Whereas the cable era was characterised by little competition with incumbents protected by technology and politics, the proliferation of new distribution ‘pipes’ in the digital era will transfer power to producers of content, who will benefit from distributors’ rivalry for delivering the best content. Control of intellectual property thus becomes a lucrative asset for the content business, possibly evolving as the new competitive bottleneck. Must-have broadcasters gain leverage over distributors in negotiations and may derive better financial terms as the distribution bottleneck erodes. Following the thesis that the broadcasting industry is evolving from a distribution economy to an attention economy (Davenport and Beck, 2001), powerful brands that successfully capture and aggregate consumer attention may benefit from scarcity. Hence, economic power in broadcasting may shift from a distributor’s ability to ‘reach’ mass audiences to a broadcaster’s ability to ‘attract and maintain’ mass audiences (Christophers, 2008).

Broadcaster-to-distributor market

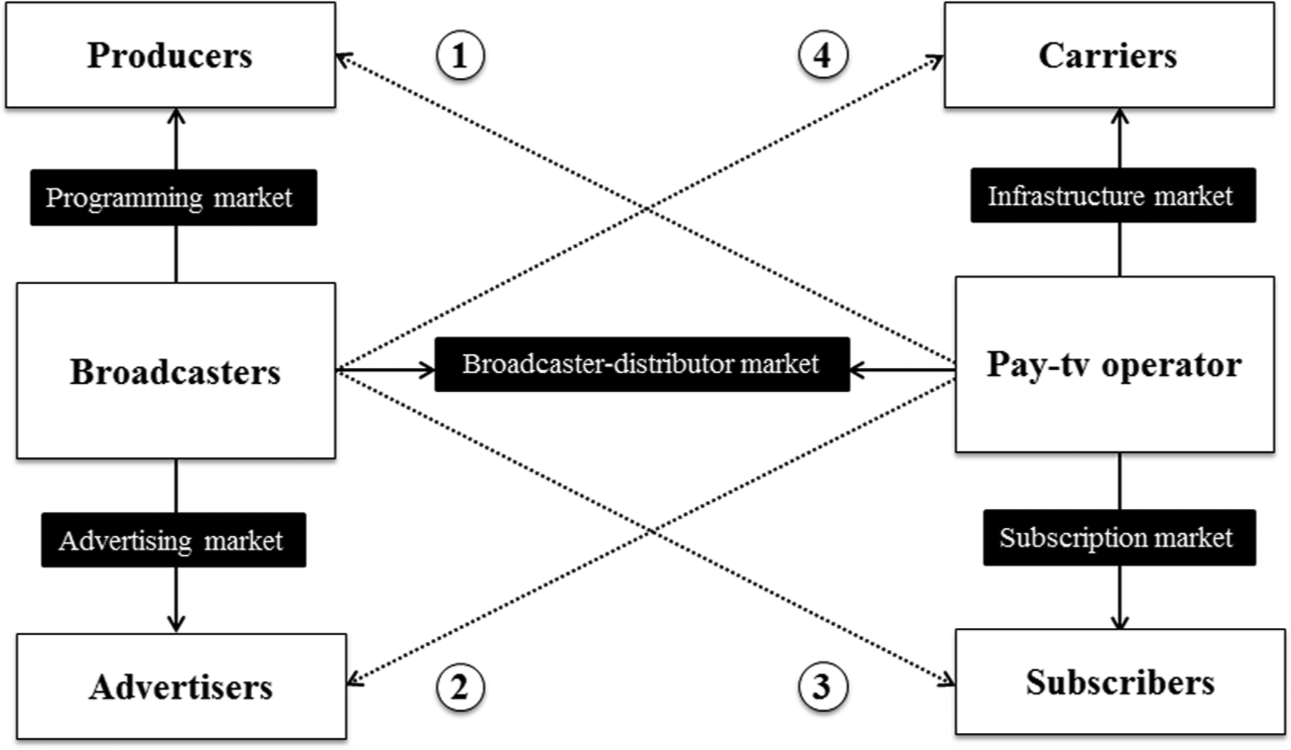

Instead of this bipolar discussion of which player exerts power over the other reducing the debate to a ‘patron–client’ relationship, with companies either in distribution or programming dominating the market, the allocation of power within broadcast markets is probably much more complicated. Rather than sticking to hollow aphorisms such as ‘content is King, but distribution is King Kong’, we assume that the allocation of power is not a linear process but highly depends on the institutional context of broadcasting, including the set of complex relationships between different parties in the business ecosystem. Hence, economic power, and more in particular bargaining power, in broadcast markets is context-specific, highly determined by the allocation of scarce resources within the industry and the individual nature of the broadcaster–distributor relationship and path dependency in media policies. As the strategic context of broadcasting is continuously in motion, the balance of power in the industry is in flux, as these relationships lack mutual trust (Donders and Evens, 2011). The increasing sources of uncertainty in the broadcaster-to-distributor market, in which both parties negotiate the economic terms of distribution similar to those of manufacturers and retailers, however, have provoked conflicts between broadcasters and multichannel operators, who are grasping the opportunities for intervening in each other’s markets, creating sources of market power and hence influencing the distribution of revenues in the system. Figure 1 shows that pay-TV operators are looking to partner with content producers (1) and advertisers (2), whereas broadcasters are directly connecting with viewers (3) and network carriers (4). These conflicts, resulting from but also provoking strategic by-passing behaviour, eventually end up in a battle for power and control in broadcast markets and are illustrated by tough negotiations for carriage payments. In the United States, broadcast networks ABC, NBC and Fox have launched the Hulu platform, which allows consumers to watch their favourite shows directly over the Internet across multiple screens. Hulu forms a counterweight to YouTube and the ‘TV Everywhere’ services deployed by distributors such as AT&T and Comcast. Similarly, Google-owned YouTube has announced partnerships with over 20,000 content providers to provide an online alternative to television broadcasting. In response, US broadcast networks have collectively blocked access to Google TV and have demanded fair payment if their shows are retransmitted by Google.

Double-sided broadcaster-to-distributor market.

First and foremost, the broadcaster-to-distributor market is characterised by a mutual dependence between broadcasters and distributors. Such horizontal relationship is based upon the complementariness of their interests: broadcasters need distribution to reach an audience and sell advertising, while distributors need broadcast programming to attract subscribers (Bergman and Stennek, 2007). During negotiations, broadcasters and distributors negotiate about the level of payments and agree upon the economic conditions for carriage. Distributors are aware of their control over the suppliers’ access to consumers, which may give them a strategic advantage in carriage negotiations. In buyer–seller relationships, however, it is not always in the retailer’s best interest to reduce a supplier’s margin, especially not – like in multichannel markets – where the value proposition of a platform strongly depends on the supplier’s input quality. For the entire broadcasting industry, squeezing the margins of less powerful broadcasters may prove counterproductive in the long run, diminishing consumer choice and quality, and restricting financial capacity to invest in innovative content and services. By receiving monthly US$7 per subscriber, cable channel HBO is able to continue its investments in expensive high-quality series and deliver a value-added component for US cable providers – whereas the average fee for cable channels is less than US$1 per subscriber. Hence, the industry’s long-term viability may crucially depend on a fair distribution of investments and profits between all stakeholders in the media ecosystem (Donders and Pauwels, 2012).

Since each party controls crucial platform functionalities, one could speak of a market with bilateral bargaining power, which closely relates to a second distinctive feature of this double-sided broadcaster-to-distributor market (see Figure 1). Current frictions and tough bargaining games between broadcasters and distributors directly relate to the arising nested, double-platform structure of the broadcasting industry. Since broadcasters and distributors both operate as a multi-sided platform, leveraging common components and shared user relationships, they are moving into another’s market, resulting in a multi-platform bundle, a phenomenon called platform envelopment (Eisenmann et al., 2011). HBO has sought direct access to viewers by providing online programming via its paid ‘HBO GO’ app, whereas cable operator Comcast has swallowed broadcaster NBC to secure access to popular programming. Such strategies for expanding market power eventually lead to corporate clashes and anti-competitive behaviour. Coordinating demand between multiple markets enables each platform to employ strategies to internalise market externalities and reduce the ‘taxes’ imposed by other’s platforms. Especially when they are vertically integrated with programming suppliers, distributors with market power may have incentives to set higher retail prices and discourage the promotion of unaffiliated channels. By exerting pricing power, distributors can reduce the exposure of broadcast channels and negatively influence advertising revenues of rivalling channels (Kind et al., 2010). In addition to this pricing power, distributors eventually decide upon channel carriage, tier and position in the electronic programming guide. By allocating a channel in a high price-tier, or by positioning it as a high-number channel, distributors can negatively influence a channel’s rating and performance, and, hence, exert bargaining power during negotiations (Chen and Waterman, 2007). After eight years of negotiation, Time Warner Cable and NFL Network finally reached an agreement in September 2012. NFL Network will be put on a basic digital tier rather than a high-priced sports tier package, and will thus benefit from higher viewership and retransmission payments.

Without acknowledging the impact of individual negotiation skills and brinkmanship, economic power is largely determined by a wide array of bargaining parameters, including the regulatory environment, market structure and technology change. In this article, the focus is on the level of competition in the market. Drawing upon industrial organisation theory, a firm’s competitive position may depend on the degree of concentration in the market, extent of entry barriers and product differentiation (Peitz and Belleflamme, 2010). Firstly, the broadcaster-to-distributor market takes the form of an hourglass structure, a market characterised by a small number of large buyers and a large number of sellers. Horizontal integration tendencies with distributors result in considerable buyer power, enabling them to negotiate advantageous deals with broadcasters (Chipty and Snyder, 1999; Tiffen, 2007). Crawford and Yurukoglu (2012) claim that large distributors such as Comcast have about 17% lower programming costs than small-sized distributors. Given the vertical integration strategies between broadcasters, pay-TV operators and carriers, ownership of programming and/or network infrastructure may lead to market foreclosure. Not only competing distributors could be disadvantaged, distributors may also leverage affiliated channels to discriminate independent broadcasters (Chipty, 2001; Lee and Kim, 2011; Waterman and Choi, 2011). Time Warner Cable’s ownership of sports rights partly explains the long-lasting battle between the cable provider and the competing NFL sports network. Secondly, economic power is reinforced by high entry barriers in distribution, which are relatively low in production and programming. Technological progress has lowered entry costs and multiplied the overall number of distribution platforms and broadcasters in the market. Apart from a few telecommunications operators that leveraged their existing network infrastructure to successfully enter the multichannel video business, the multitude of new players in broadcasting is involved in content production and programming. As switching costs are likely to be higher between distributors than broadcasters (viewers tend to switch more easily between channels than between platforms), this may add bargaining power to distributors (Menezes and Quadros, 2009). Finally, market players tend to reduce substitution effects by differentiation strategies. As differentiating between transmission technologies proves difficult, distributors need to differentiate in the services they provide. Hence, they enter into agreements with popular programmers and invest in the exclusive acquisition of must-have productions. Consequently, must-have broadcasters, usually those with the highest viewership or those providing hit programming, as well as niche channels that bring in specific and valuable target profiles, obviously have more bargaining power than undifferentiated, generic channels. Sports channel ESPN charges US$5.15 per subscriber, whereas Fox Sports receives US$2.10 per month. Since ESPN manages to acquire top premium sports rights, Fox Sports is unable to command the premium pricing that ESPN enjoys. However, the more distributors invest in their own original programming, the less bargaining power broadcasters have (Chan-Olmsted, 2005).

Research design

In the remaining part of the article, a comparative analysis of the broadcaster-to-distributor market in Flanders and Denmark is presented, with specific emphasis on the market structure and the practice of retransmission payments. Both representing small broadcast markets, Flanders and Denmark, share a lot of structural commonalities, which justify a comparative analysis. The two markets are characterised by small population sizes (6.28 million inhabitants in Flanders versus 5.56 million in Denmark) and are among the most prosperous regions in Europe, with a gross domestic product per capita of €28,779 and €30,806 in Flanders and Denmark, respectively (compared to an EU 27 average of €25,051). 3 Flanders and Denmark may, as open economies, highly depend on neighbouring countries for economic wealth and export, but neither has a same-language giant neighbour whom they can rely upon for the influx of cultural goods and broadcast services. Regarding broadcasting, both countries have a long tradition of the public service broadcast institution being the leading media company in the market, complemented by a limited number of nationwide private channels. From a distributor’s perspective, cable penetration is high (98.2% and 71.6% in Flanders and Denmark, respectively) with rather moderate but increasing competition from other distribution technologies. In addition, digital television services are successful and widely diffused (76% and 73%, respectively). 4 Finally, both markets are subject to European regulation, and are among the few EU member states that have no specific cross-media law.

Previous research has identified market size as a significant factor in assessing economic conditions, constraints and challenges broadcasting systems face in smaller markets, referring to the limited availability of resources, economies of scale problems, concentrated markets, lower investments in domestic programming and restricted consumer choice (see Lowe et al., 2011; Trappel, 2011). Despite the similarities they share, Flanders and Denmark were selected as case studies because large differences can be found with regard to the relationships between broadcasters and distributors. Hence, the focus of the comparative analysis is on relating differences in bargaining position to the variance in market structure and the level of competition among the selected markets. Although these differences may be influenced by divergent political views regarding the role of the state in economic life, 5 the qualitative analysis mainly focuses on the economic context of the broadcaster-to-distributor markets in Flanders and Denmark.

Given the multi-faceted character of the broadcaster-to-distributor market, a multi-disciplinary and multi-method approach of the research issue was deemed necessary. Regarding the multi-disciplinary nature of the study, a political economy analysis of this converging market requires a review of literature on economics, political science and media studies, but also benefits from readings in information technology and copyright law. In light of this, a multi-method approach relying on a triangulation of methods is preferred to an exclusive reliance on literature review, policy analysis or interviews. In addition to a literature study and document analysis (legislation, case law, corporate financial reports and press statements), 17 field interviews were conducted with representatives from media companies 6 and regulators, or academics specialised in the field. The data were collected in the context of a research project funded by SBS Broadcasting, then operating in both markets. In addition to the data collection process, findings were validated through a workshop with four national experts in political economy, media economics and telecommunications policy, whereas three international experts were asked to review and comment upon the case studies during the project.

Case Studies

Denmark: channel proliferation and fragmented distribution

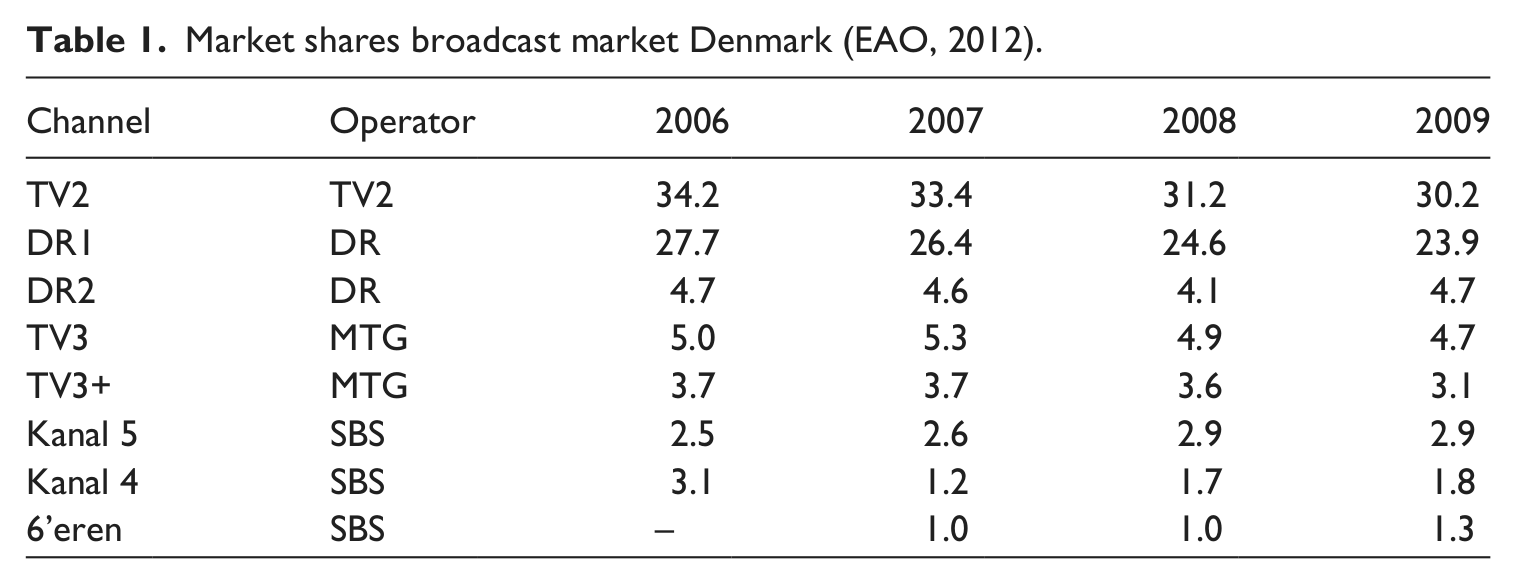

The Danish broadcast market is probably one of the few remaining in Europe in which public service broadcast channels, operated by DR and TV2, occupy over half of the daily audience share. Next to these generalist channels, public service operators also host some 10 thematic channels that cater for specific niches. Market leader TV2 dominates the market with 30.2%, followed by DR1 with 23.9% – public service broadcasting accounting for 68.8% of the viewing market (including niche channels). Because of this dominance of public service broadcasting, private channels have a rather moderate viewing share in Denmark. TV3 was the first private channel that launched a Danish channel, operating from London to circumvent severe advertising regulations. The channel is owned by the Swedish Modern Times Group (MTG), which also operates TV3+ and TV2 Sport (together with TV2), and has a large footprint in Nordic and Baltic television markets. Operated by the international SBS Broadcasting group and owned by ProSiebenSat.1 Media, the other main channels, Kanal 4 (women’s channel), Kanal 5 (movies and series) and 6’eren (men’s channel), are the only private channels that managed to slightly increase their market share in recent years (see Table 1). Similar to TV3, SBS’s channels are UK-licensed to circumvent Danish advertising rules. Television advertising accounts for 18.4% of total advertisement expenditure (€366 million), which has decreased in recent years. The plenitude of channels and the fragmentation of the audiovisual landscape have produced a saturated market and fierce competition for advertising sources, driving most of the channels towards (basic) pay-TV status.

Market shares broadcast market Denmark (EAO, 2012).

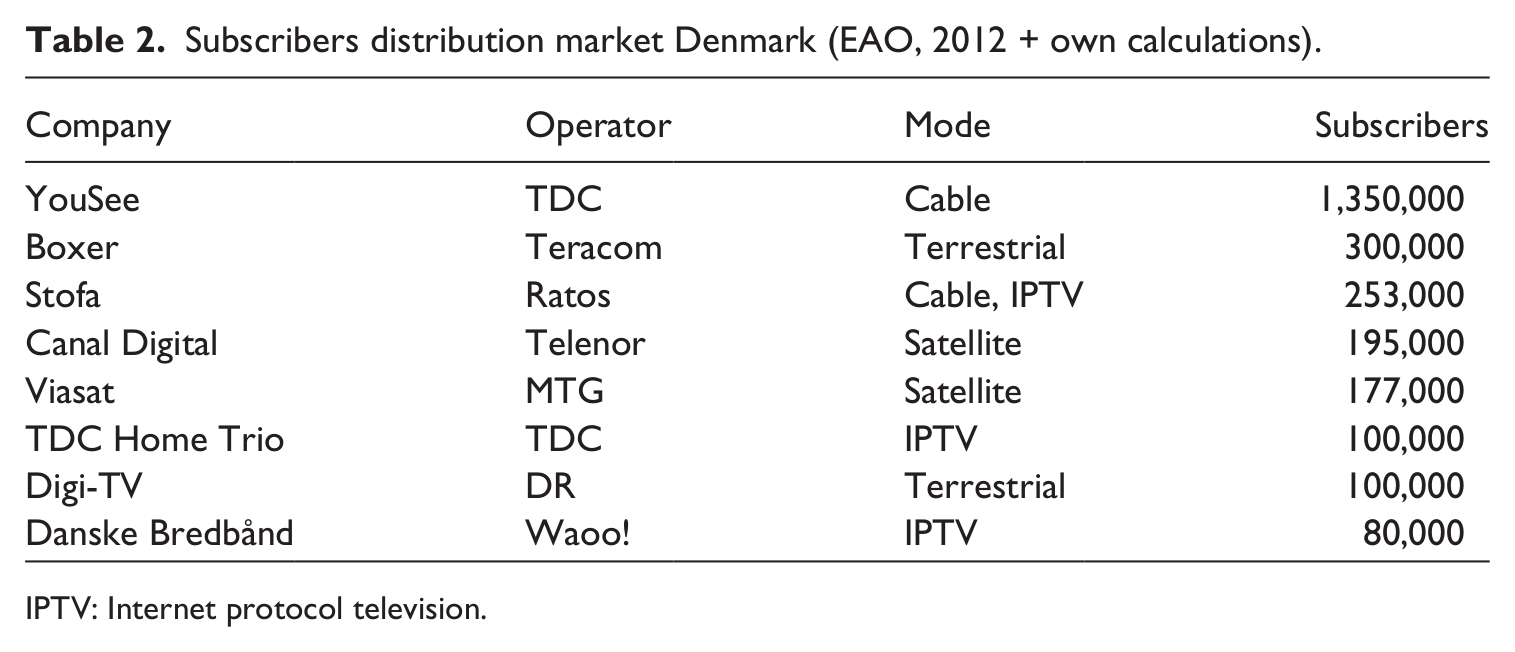

The multichannel market in Denmark is dominated by cable operators, with a footprint of approximately 1.8 million out of a 2.5 million total television household population. Cable is the main television distribution platform, with about 1.6 million households connected to cable television services. The cable market, which accounts for 64% of all television connections, is controlled by YouSee, a 100% subsidiary of the former telecommunication monopolist TDC, serving 1.35 million customers. Main competitor Stofa serves about 253,000 households. In addition to these two major cable suppliers, Denmark hosts a large number (>1500) of smaller independent, decentralised operators, so-called satellite master antenna television associations (SMATV), non-profit organisations that manage large building and housing associations serving about 550,000 households. These associations negotiate with distributors that wholesale packages to community networks. In exchange for multi-year agreements with mainly cable and satellite operators, antenna associations receive discounts due to network ownership and scale. In urban regions TDC faces increased competition from Waoo!, grouping local utility companies providing telecommunication services over fibre-optic networks, and has, as a response, started its own Internet protocol television (IPTV) service after swallowing some local providers.

In less densely populated areas there is tight competition between satellite and terrestrial service providers. The Danish market hosts two satellite operators, with a combined subscriber base of approximately 380,000. Canal Digital, part of Norway’s Telenor Group, serves some 195,000 customers with its direct-to-home platform. More interestingly, pan-Nordic satellite operator Viasat serves approximately 177,000 subscribers and is owned by MTG. Hence, the company can leverage its affiliated TV3 programming in the distribution market. Except for cable operators, competing platforms have no access to TV3. In return, Canal Digital has secured the exclusive carriage of the SBS channels on satellite platforms. As terrestrial analogue signals were switched off by November 2009, a public service multiplex is operated by Digi-TV transmitting, free of charge, national and regional public service channels. In addition, a commercial gatekeeper Boxer TV provides some 30 pay-tv channels. Since TV2 lost its must-carry status in January 2012 and is no longer carried as a free-to-air channel, Boxer sales tripled to about 300,000 customers (Table 2).

Subscribers distribution market Denmark (EAO, 2012 + own calculations).

IPTV: Internet protocol television.

Regarding the payment of retransmission fees, this model quickly gained ground in Denmark. Payments became common practice in the late 1990s when Viasat entered the television distribution market, which had long been dominated by TDC Cable TV (later rebranded YouSee). Viasat was keen to differentiate from other multichannel operators and spent large amounts of money to carrying exclusive programming. With digitisation, a window of opportunity was opened for several niche channels to target interesting viewer profiles. With low levels of advertising, however, it became hard to finance this growth in programming, with most of the channels digital-only and originally with limited reach. Supported by distributors, TV2 News was established as the first 24/7 news channel in the Nordic area. In March 2012, Kanal Sport, focussing on smaller sports, was established, and initially secured distribution from YouSee. Such carriage agreements, including financial compensation, allow new channels to pre-finance operations and reach the critical mass necessary for building a sustainable business model. Generally, channels are remunerated via minimum guarantees and per-subscriber fees – varying between €0.2 and €2 – depending on the bargaining position of the channel. The example of TV2 shows that retransmission payments function as a substantial revenue source for television companies. In its annual report 2011, the company reports that between 2006 and 2011, retransmission income grew from €34 million to €92 million, rising from 12.9% to 29.8% of total revenues. Negotiating its move to pay television, TV2 will receive a monthly €1.35 retransmission fee per household, adding some extra €40 million in turnover. However, TV3 channels take the highest share of these retransmission payments, which were valued at €315 million in 2009. The TV3 network takes some 30% (€96.11 million), whereas SBS channels account for 14% (€44.64 million) of the total distribution market, which is expected to grow further in the coming years.

Flanders: content triumvirate and cable monopoly

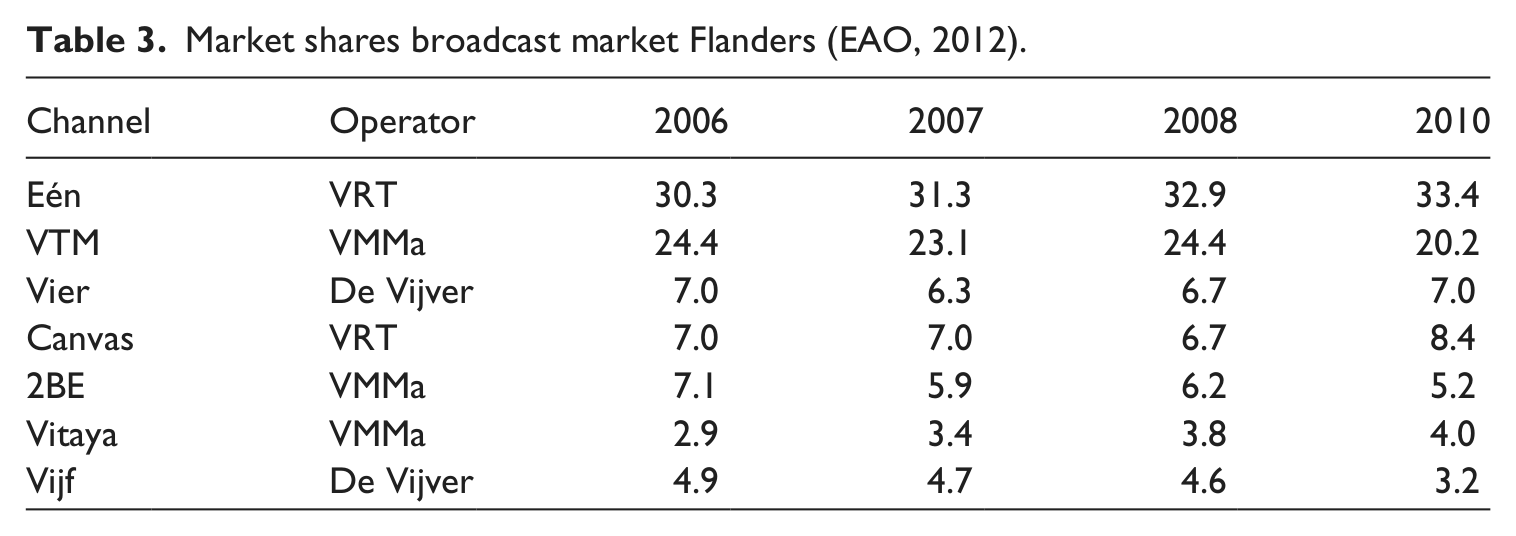

In the Flemish broadcast market, competition between the public broadcaster VRT and its private counterparts is fierce. VRT has dominated the market for many years since it regained viewer leadership from VTM in 2001. In addition to the generalist channel Eén, VRT also operates the information channel Canvas, Ketnet (children programming) and Sporza (sports). VRT is totally licence-funded and carries no television advertising. In addition to VTM, the leading private television company VMMa also operates 2BE (series and reality), Anne (music), Vitaya (health), Jim (music) and vtmKzoom (kids). In 2011, other popular channels in the market, Vier (series and reality) and Vijf (women), were purchased by production company Woestijnvis and cross-media groups Corelio and Sanoma. As a result of enduring consolidation, these three main operators account for more than 80% of the total viewer market – with fierce competition for advertising income (Table 3). Television advertising accounts for 38.1% of all gross investments, equivalent to €941 million.

Market shares broadcast market Flanders (EAO, 2012).

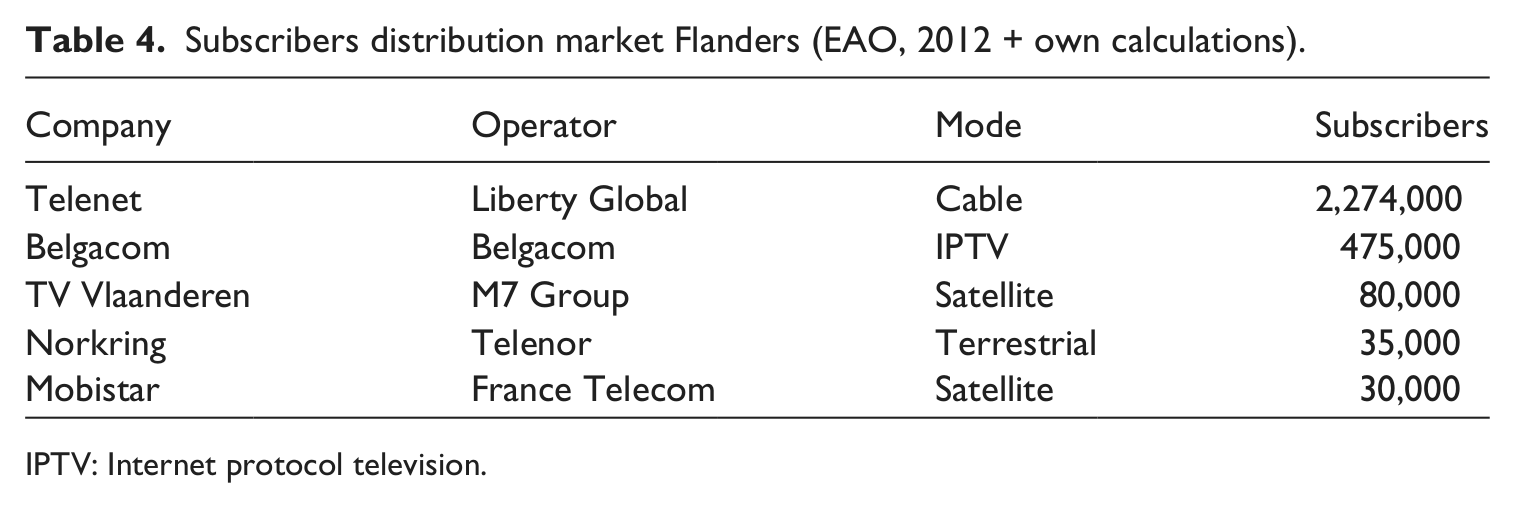

Thanks to a penetration of over 98% and its compatibility with antenna reception, cable technology became the dominant distribution technology in Flanders. Historically, this market was monopolised by Telenet but its former monopoly has been ended with the introduction of digital television. Today, the television distribution market is characterised by a duopoly, with Telenet being a dominant player (holding a market share of over 80%) and state-controlled telephony provider Belgacom acting as a challenger (Table 4). In addition, Telenet entered into an agreement with multiplex operator Norkring to launch a nationwide digital terrestrial offer – possibly in an attempt to foreclose the market. Apart from cable subscriptions, Telenet has launched a number of thematic channels with local producers, such as Studio 100 (kids) and Njam! (cooking). It also owns pay-TV network Canal+ (rebranded Prime) and acquired large packages of premium rights, including those of sports competitions and US series. In 2012, Telenet announced that it would invest €30 million in local and independent content production (in exchange for the video-on-demand and pay-TV rights), and also acquired the first rights to broadcast the popular HBO series (e.g., Game of Thrones and Boardwalk Empire).

Subscribers distribution market Flanders (EAO, 2012 + own calculations).

IPTV: Internet protocol television.

Telenet faces competition from Belgacom, which successfully launched an IPTV offer over its copper network. It quickly gained market share after acquiring exclusive sports rights in 2005 (e.g., Champions League football), now serving some 475,000 households in the northern part of the country. Digital television is also delivered by two satellite providers, TV Vlaanderen and Mobistar, but these initiatives have not been an overwhelming success in the cable-dominant region, and failed to challenge Telenet’s dominant position. For Mobistar, the second largest mobile operator, the provision of television is an important cornerstone in its strategy to provide multi-play services, including telephony and Internet. At the end of 2010, the media and telecommunications regulators decided that Telenet and Belgacom would need to open their network so that alternative operators could compete in the television distribution market.

With regard to retransmission payments, negotiations between broadcasters and distributors have provoked several conflicts in recent years. After all, carriage payments do not exceed more than 4% of total turnover for Flemish broadcasters. Renegotiating contracts after previous carriage agreements had expired proved difficult, especially since the two main distributors have built up a substantial subscriber base. At the end of 2011, for example, Telenet announced that it would reduce the retransmission payments to regional broadcasters from €1.59 to €0.18 per subscriber – based on market shares. After wide-scale protest by these channels and intervention by the Flemish media minister, the case was settled and a three-year-long transition period during which retransmission fees would gradually be decreased was announced. Simultaneous with distributors’ attempts to reduce carriage payments, domestic broadcasters contest the level of retransmission fees (normally in the form of single, lump-sum payments) by arguing that for distributors the provision of digital television acts as a growth engine for their multi-play strategies. Broadcasters argue that they invest the bulk in content production and that distributors capture most of the economic value broadcasters generate. Hence, broadcasters want a larger share of this growing pie and also tap into the revenues generated by bundled service packages. The exploitation of comfort services, which make it easy for viewers to record programmes and watch them later, form a second issue of major dispute. Digital video recorders not only affect potential revenues derived from video on demand, which distributors share with broadcasters, but also threaten the advertising-based business private television companies rely upon – allowing consumers to bypass advertising. In 2010, VRT, VTM and VT4, in an open letter to the press, explicitly complained about the threat of fast-forwarding advertising. They now claim a fair share of the fees distributors charge consumers for the use of these comfort services – compensating them for declining advertising income. Following these disputes, Telenet has still not secured carriage of VMMa channels for its mobile TV everywhere service Yelo – illustrating the soured relationship between the two parties. Instead, VRT, VMMa and Vier have unfolded plans for an on-demand web TV service to by-pass distributors and exploit their content online via the Rumble platform.

Comparative analysis

In the theoretical section of the article, it has been argued that market structure, and more specifically the level of competition in the market, is an important determinant of bargaining power. Considering the degree of market concentration, channel ownership and product differentiation, the case studies suggest that relationships between broadcasters and distributors in Denmark are more trust-based than in Flanders, and that both parties pronouncedly acknowledge their mutual dependence or, at least, that Danish broadcasters gain more leverage over multichannel operators. Comprising a comparative analysis, this section tries to link the relative economic power of broadcasters vis-à-vis distributors to the different bargaining parameters. In so doing, the context-specific nature of individual broadcaster–distributor relationships, emphasising crucial contextual factors –market concentration, vertical integration and product differentiation – that influence the competitive position of an actor in a bargaining game is highlighted.

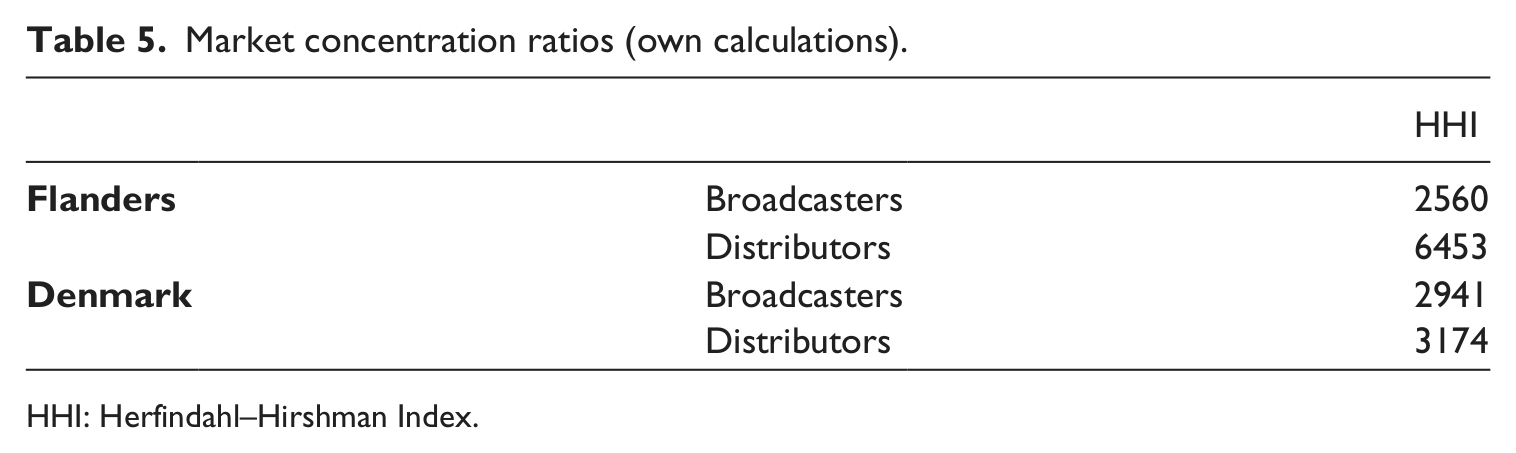

Firstly, broadcasting markets in Flanders and Denmark are relatively highly concentrated, with public service broadcasters taking the lead. In Denmark, this public service dominance is even stronger than in Flanders, but this does not prevent private broadcasters from gaining leverage as well. As the Danish distribution market is much more fragmented than the Flemish one with several substitutes in rural areas, private broadcasters can play satellite and terrestrial companies against each other, and bargain the most favourable carriage conditions. Despite a market share of over 54% and a strong presence in densely populated areas, YouSee has less market power than one should think. The company mainly relies on its contracts with housing associations, which generally own the access network and have the freedom to choose between several interested suppliers. In Flanders, however, Telenet acts as a powerful gatekeeper due to its quasi-monopoly. Since broadcasters rely extremely upon cable carriage, this is creating a power asymmetry in the broadcaster-to-distributor market. Now that Belgacom has been settled as a powerful runner-up, broadcasters could face difficulties in bargaining lucrative contracts for IPTV as well. Using the widely applied Herfindahl–Hirshman Index (HHI) as a measure of competition and market power, 7 Table 5 suggests that broadcaster-to-distributor markets in Denmark are indeed more equally balanced than in Flanders, where these relationships seem more skewed in favour of distributors. Since all markets have a HHI score higher than 1800, this means that broadcast and distribution markets both in Flanders and in Denmark are highly concentrated. However, HHI scores for broadcast and distribution markets in Denmark are more or less equal, whereas HHI scores for Flanders differ largely. A HHI score of 6453, more than three times the allowed threshold of 1800, indicates excessive market power in the distribution market in Flanders.

Market concentration ratios (own calculations).

HHI: Herfindahl–Hirshman Index.

Secondly, vertical integration tendencies are most obviously found in distribution companies in Flanders compared to Denmark. In addition to the combined role as a pay-TV and network operator, distributors in Flanders have unfolded several activities in commissioning and producing content. Not only have Telenet and Belgacom launched various thematic channels to enhance the attractiveness of their programming supply, but also the companies were involved in an aggressive bidding war for acquiring the exclusive rights of the national and European football leagues. By providing top premium programming, normally catering for niche audiences, they are directly entering the arena of niche television already developed by small broadcasters. Although hard to prove, several of these smaller broadcasters complain about anti-competitive conduct and a refusal to deal. In contrast to the established broadcasters, niche channels are often deprived of retransmission payments. Such tensions hardly exist in the Danish market, where – except for the vertical link between Viasat and TV3 – no distributor is involved in programming. YouSee, for example, has explicitly stated that it has no intention of competing with established channels or taking part in sports rights auctions. However, the ownership of TV3 enables Viasat to exert market power, and has provoked conflicts with other satellite and terrestrial operators. By carrying TV3 exclusively, Viasat tries to foreclose distribution in rural areas and lure consumers to their platform. There have been concerns that Viasat would withdraw its TV3 bouquet within community associations that signed a contract with Canal Digital. Instead, both distributors reached an agreement to distribute TV3 within housing associations. Private broadcasters, mainly those operated by SBS, have financially benefitted from this rivalry and were able to bargain lucrative terms for carriage by Canal Digital and Boxer.

Finally, the lack of vertical integration enables Danish broadcasters to gain market power. Indeed, the more distributors rely on external programming for offering compelling packages, the more bargaining power broadcasters derive. Since distributors in the Danish market do not bid for premium sport rights, broadcasters have developed a portfolio of attractive programming allowing them to enter into beneficiary contracts with platform operators. In addition, public and private broadcasters are strongly differentiated and cover various viewer segments in the market that can attract specific target audiences to distributors’ programming tiers. Hence, Danish distributors have followed the same strategy US cable operators deployed when these started financing cable networks in the 1970s to enrich their programming supply. Since advertisement expenditures are insufficient to finance the broadcast ecosystem, distributors have started to financially support broadcasters to guarantee high-quality programming. This is less the case in Flanders, where operators are directly involved in programming through premium rights ownership and mainly the smaller channels suffer from achieving favourable carriage conditions. By deploying content activities, one could even argue that Telenet and Belgacom want to create audience fragmentation and weaken broadcasters’ bargaining position.

Conclusion

Based on two detailed case studies, this article included a political economy analysis of retransmission payments in European broadcast markets. As these markets are characterised by fundamental institutional reform, so are the relationships between broadcasters and distributors that form an important subset of the institutional framework in which these parties operate. Both in and outside Europe, tough negotiations for retransmission payments illustrate the on-going battle for power and control in the business ecosystem. Instead of assuming a patron–client relationship with either broadcasters or distributors in the driver’s seat, it was assumed in this article that the allocation of bargaining power within the industry is largely determined by the ownership of scarce resources and influenced by structural features of the market wherein broadcasters and distributors navigate. Contending that each party controls crucial platform functionalities, we have argued that the broadcaster-to-distributor market is characterised by bilateral bargaining power, eventually leading to platform envelopment strategies.

Building further on industrial organisation theory, the circulation of economic power within broadcast markets was linked to the market structure and the level of competition in broadcasting. The case studies suggest that relationships between broadcasters and distributors in Denmark are more trust-based and cooperative than those in Flanders, and that Danish television companies have acquired more leverage over distributors compared to their Flemish counterparts. Indeed, the high level of market concentration, illustrated both by horizontal and vertical integration tendencies in the Flemish distribution market, suggest that pay-TV operators are able to exert bargaining power over broadcasters. An analysis of the Danish market, in contrast, suggests a more balanced distribution of power between both parties, as is also reflected in the level of retransmission payments, which was smoothly accepted as an industry practice in Scandinavian broadcast markets. Whereas these payments account for about 4% of the total industry turnover in Flanders, income from retransmission represents up to one third of the total revenues of Danish broadcasters.

Since the focus of the article was predominantly on the structure of broadcast markets, little emphasis has been put on regulatory interventions and their consequences. Despite the substantial stakes at play, public policymakers in Europe have undertaken few specific attempts in regulating broadcaster-to-distributor markets and preserving a fair balance between broadcasters and distributors. In certain countries, national regulators have imposed ownership rules, but such regulations have not prevented large media companies, either broadcasters or distributors, from developing into powerhouses that settle carriage negotiations in their favour. Apart from preserving fair competition in the market by eliminating artificial entry barriers and fighting the excessive concentration of economic power leveraged by particular players, it seems that policymakers are rather limited in their options for dealing with carriage disputes between two or more contracting parties. In extreme cases, regulators could regulate the level of the fees or impose mandatory binding arbitration when parties are not negotiating ‘in good faith’ to avoid blackouts and ensure consumer choice. In Flanders, several Members of Parliament have submitted a proposal to change Flemish media legislation to ensure more fair negotiations between broadcasters and distributors, stressing the former’s exclusive rights over their content and the latter’s obligation to add functionalities to this content and charge for it only after approval of the right holders. The change of decree has not been approved yet as several issues regarding free flow of services (as ensured by European law) will have to be resolved first.

The article has practical implications for both industry stakeholders and policymakers. For policymakers, analysing economic structures of broadcast markets may identify important issues for cultural policies, such as the effects of corporate concentration on media diversity and pluralism in society. The results indicate that regulatory intervention aimed at creating a level playing field between broadcasters and distributors could have far-reaching implications for the financial health of the broadcast market, which suffers from shrinking advertising expenditures and increasing competition from online video platforms. Lowering entry barriers in network access (e.g., open access rules) or imposing limits in market concentration (e.g., through cross-ownership regulation) could increase competition in the distribution market and improve relationships with broadcasters. Ultimately, regulators can impose a separation between content production and distribution activities when ownership restrictions fail to eliminate anti-competitive conduct and abolish dominant positions. For broadcasters, the results suggest that providers of attractive and differentiated programming may develop bargaining power and enter into more advantageous carriage agreements with distributors. Since operators are continuously seeking for the best content to differentiate from competing platforms, the supply of domestic programming could add to the competitive position of broadcasters, and hence pay off the substantial investments in providing high-quality programming through more valuable retransmission deals. Platform operators, from their perspective, could increase investments in original content to spur the value of their offerings. Ownership of top premium content is also seen as a means to leverage bargaining power vis-à-vis content providers.

As a concluding note, the importance of retransmission payments and carriage disputes as a research issue will only increase in the future. Against the backdrop of rapid technological changes, most notably the deployment of broadband television, the global battle for power and control in television markets has just started and will only intensify in the coming years. Since the scope of the article is limited to two case studies, future research could focus on including more countries – taking into account the methodological challenges related to case-oriented comparative analysis – to produce more generalisations concerning the impact of the bargaining parameters discussed in the article. In addition, the number of bargaining parameters could be expanded, constructing a complex of interrelated factors that contribute to the competitive position of a negotiating company. Other sources of bargaining power could be considered, eventually building a statistical model to assess the impact of related parameters on carriage negotiations in a quantitative way. Combined with qualitative case studies, such a multi-method research design would allow the complete unravelling of the complex relationships between content producers and distributors in broadcasting markets, and the identification of sources for policy intervention.

Footnotes

Funding

This research received no specific grant from any funding agency in the public, commercial or not-for-profit sectors.