Abstract

Background

SMEs failure is common within the first 5 years. For efficient resource management and improve corporate performance, SMEs need management accounting systems. Structure, strategy, and staff qualifications affect MAS adoption in organizations.

Objective

: This study aims to examine the effect of contingent factors in the adoption of MAS, as well as the effect of MAS on performance, and also the role of MAS as a mediator between performance and contingent factors in SMEs in Jordan.

Methods

PLS-SEM was used to evaluate a questionnaire of accounting department heads and finance managers from Jordanian SMEs (N = 415).

Results

Decentralization, accounting staff qualification, differentiation strategy, and low-cost strategy directly increase MAS adoption. This study shows that MAS improve performance significantly. This study also shows that MAS mediate the relationship between decentralization, accounting staff qualification, differentiation strategy, and low-cost strategy and SME performance in Jordan.

Conclusions

The study found that contingent factors can help us understand how managers can use MAS information to improve performance. The results only somewhat expand the corpus of research on MAS’s usefulness, but they help us understand the aspects that may affect MAS design and performance in firms.

Introduction

Jordan, an upper-middle-income country, heavily depends on small and medium-sized enterprises (SMEs) as a key driver of its economy. In 2021, SMEs represented 95% of Jordan’s business market, highlighting their pivotal role in the country’s economic structure. 1 SMEs account for approximately 95% of all officially registered firms, contribute more than 50% to the Gross Domestic Product (GDP), and provide employment for around 60% of the Jordanian labor force. 2 These figures underscore the critical importance of SMEs to Jordan’s economy and their essential role in any economic growth strategy. In contrast to Europe, where SMEs are defined as companies with fewer than 250 employees and a total turnover not exceeding EUR 50 million, Jordan classifies SMEs as firms with fewer than 100 employees and a total turnover not exceeding JOD 3 million (with 1 JD equivalent to USD 1.41). 3 According to the Trade and Supply Act No. 10 of 2005, the Ministry of Industry defines small enterprises as those engaged primarily in industrial activities, with a capital below JOD 30,000 and fewer than 10 employees registered with the Social Security Administration. Within Jordan, microbusinesses comprise 89% of all enterprises, while small businesses account for 9%, and medium and large enterprises make up the remaining 2%. 4

Small and medium enterprises (SMEs) play a critical role in the economic development of countries. SMEs in Jordan exert substantial influence across multiple domains, including employment generation, wealth accumulation, income distribution, the acquisition of technological capabilities, and the equitable allocation of resources among a heterogeneous array of efficient and dynamic enterprises. According to the result of Diegtiar et al., 5 the significance of SMEs mostly stems from their unique qualities. Consequently, the advancement of SMEs is commonly perceived as a feasible approach to achieve sustainable economic growth and development within a particular economy. The expansion of SMEs facilitated by the application of management accounting practices is expected to play a significant role in fostering the advancement and expansion of the Jordanian economy. This is primarily due to the anticipated outcomes of increased job opportunities, enhanced entrepreneurial and managerial capabilities, mitigation of rural-urban migration, technological advancements, the emergence of ancillary industries, and improved income distribution equity.

Nevertheless, as stated by Shqair et al., 6 a significant proportion of SMEs experience failure within the initial 5 years of establishment. Additionally, a lesser number of these enterprises cease to exist between the sixth and tenth year, resulting in only a modest 5–10% of emerging SMEs successfully enduring, prospering, and reaching a state of maturity. This suggests that the survival rate of SMEs in Jordan is below 5% over the initial 5 years of operation. This observation also implies that SMEs in Jordan have faced challenges in their ability to make significant contributions to the country’s development. According to Alliyah et al., SMEs also necessitate sufficient and advanced management accounting procedures and systems in order to effectively handle limited resources and improve the firm’s worth. While SMEs may encounter limitations in implementing comprehensive management accounting processes due to their smaller scale and restricted resources, they encounter comparable complexities and uncertainties as bigger organizations, making them more susceptible to failures. According to Pedroso et al., there is a notable deficiency in the utilization of accounting information systems among SMEs in developing countries. This deficiency has been identified as a potential contributing factor to the failures experienced by SMEs. The lack of comprehensive record-keeping and accounting information poses challenges for financial institutions in assessing the possible risks and returns associated with lending to SMEs, hence leading to their reluctance to provide loans.

Management accounting has been proposed as a significant management methodology that contributes value by consistently examining the efficient utilization of resources by individuals and organizations in generating value for consumers, shareholders, and other stakeholders. 7 Management accounting systems (MAS) are integral information systems utilized by managers to access relevant data for the purpose of making informed decisions that contribute to optimal performance outcomes. These systems conventionally employ a range of methodologies, such as product standard costing, absorption costing, and budgeting, in order to furnish managers with prompt and precise information. This information aids in cost control, productivity measurement, and enhancement, thereby facilitating the attainment of business objectives. 8 SMEs necessitate appropriate and advanced management accounting approaches and systems to effectively handle limited resources and improve customer satisfaction and value for both owners and managers. According to the American Association of Accountants (AAA) in 1972, there exists a correlation between management accounting systems and the planning and control functions performed by managers. According to AAA, planning involves the identification and creation of objectives, as well as the optimization of resource utilization and measurement. On the other hand, supervision entails the assessment of operational activities through the provision of motivation and assistance in evaluating performance and effectiveness in attaining organizational goals.

According to Nugrahani et al., the integration of MAS within organizations provides users with access to financial and non-financial data, facilitating the processes of planning, regulation, and decision-making, thereby enhancing the overall performance of the company. Nevertheless, due to the contingent nature of management accounting, no system is universally applicable and can be implemented by all organizations in all circumstances. A misalignment between contingent factors and management accounting systems is possible. 9

The design of the MAS characteristics is influenced to a certain degree by both internal and external contingent factors. 10 According to Shabbir et al., 10 firms consist of two primary environments: internal and external. These conditions, similar to those seen in other firms, have a crucial influence on the efficiency of corporate operations. The organizational qualities have a direct impact on the properties of MAS. The MAS functions as a subordinate component within the broader framework of Management Control Systems (MCS). 11 The implementation of MAS in firms is shaped by contingent factors such as organizational structure, company strategy, and staff qualifications. 12 The selection of control strategies within an organization is greatly affected by its organizational structure, which establishes the hierarchy of authority and responsibility as individuals’ progress through it. 13 The effectiveness of the MAS in companies relies on the caliber of information required at various management levels. According to Chenhall et al., the organizational structure has an impact on how information is communicated between different divisions within a company. Organizations often use a comprehensive decentralization approach to enhance performance by distributing decision-making authority. According to Celik et al., employees at larger companies possess specialized knowledge about the manufacturing process, whereas in smaller firms, decision-making power is typically concentrated in a central authority. The characteristics of MAS should align with the organizational structure.

The presence of unskilled personnel is a contributing element that hinders the effectiveness of MAS features in companies.14,15 The MAS qualities require a staff member who comprehends the business environment and possesses expertise in the field. 3 emphasizes that staff qualification is a crucial factor to consider while establishing attributes for MAS in organizations. According to kingazi et al., 15 MAS supplies decision-relevant information that is utilized by management in their daily operational activities. Moreover, the dissemination of information enhances the synchronization across various departments operating within organizations. 16 Hence, the expertise of the staff is a crucial factor to consider while developing the qualities of MAS in companies.

An organization’s corporate strategy outlines its long-term course to fulfill its goal and accomplish its objectives. To optimize resource allocation, enterprises require accurate information to select the most optimal alternative. 1 The companies encounter both domestic and international rivalry inside the market. To get an advantage over their competitors, they must develop a suitable strategy.1,11 Kesumawati et al. state that the company’s methods effectively facilitate resource management, resulting in the creation of value for both customers and shareholders. In addition, Glushakova et al. 2 contended that MAS offers valuable information that can aid companies in overcoming market rivalry. According to Porter et al., when it comes to corporate strategy, corporations can get a competitive advantage by having a favorable market position.

Ghasemi et al. suggest that firms can achieve competitive advantages in the market by implementing either cost leadership or product differentiation strategies. 17 Competitive advantages can be expanded by asserting that a company can adopt a cost leadership strategy by prioritizing the achievement of lower costs compared to competitors by enhancing productivity and efficiency. Alternatively, companies that differentiate their products aim to create distinct and unique offerings 4 analyzed the factors that impact the configuration of a MIS. They contended that there exists a correlation between the approach utilized and the information pertaining to MAS attributes in companies. Hence, it is imperative to examine the correlation between the qualities of MAS and the specific business strategies employed by organizations to outperform their competitors in the market.

Prior research in this area has revealed little interest in the use of MAS, particularly from significant sectors and businesses in underdeveloped nations.18–21 Contingent factors are frequently utilized to best describe the implementation of MAS12,13,22–25 According to Refs. 11, 15 and, 26 there is a need for additional study to gain more clarity and insights into the relationship between contingent factors and MAS usage, as previous studies have yielded inconclusive results.

Moreover, research has indicated that MAS effectively supports management in formulating strategic decisions, resulting in enhanced overall performance within organizations.27,28 Although MAS are highly relevant for enhancing performance, there is a scarcity of research on this topic, particularly in developing nations and in SMEs.29–32

The present research study used a contingent model derived from existing literature to assess the impact of several contingent factors on MAS and performance. The aim is to evaluate the effectiveness of implementing these systems in SMEs in Jordan. The scope of our investigation encompasses the subsequent research questions

33

: 1. What are the contingent factors affecting the adoption of MAS by SMEs in Jordan? 2. What is the effect of MAS on the performance of SMEs in Jordan? 3. Does MAS adoption play a mediation role in the relationship between the contingent factors and the performance of SMEs in Jordan?

Literature review and hypotheses

Management accounting systems (MAS)

Management accounting refers to the strategic use of extensive knowledge and methodologies by firms and managers to make informed decisions, particularly regarding financial information, which gives them a competitive advantage. 7 According to Nugrahani et al., management accounting is the systematic provision of managers with both financial and non-financial information. Management accounting is the systematic study of providing appropriate financial and non-financial information to facilitate decision-making, planning, control, and performance evaluation in a potentially successful company. 11 Management accounting plays a crucial role in facilitating decision-making at all levels of an organization. 14 Moreover, management accounting plays a crucial role in facilitating efficient corporate administration by furnishing managers with relevant information to make informed decisions about the organization’s success. 17 Moreover, Hutahayan 30 clarifies that management accounting focuses on providing information to individuals within the firm to enhance their decision-making abilities and optimize the efficiency and effectiveness of current operations. Furthermore, the primary objective of management accounting is to enhance the performance and profitability of the business and support managers by offering pertinent financial and non-financial information to facilitate decision-making. 19 From the several definitions, it can be inferred that management accounting focuses on furnishing information to managers, namely to those who are integral to an organization and responsible for directing and overseeing its activities.

Over time, the concept of Management accounting systems (MAS) has evolved, shifting from its original focus on furnishing timely, accurate, and valuable data for decision-making to encompassing a broader spectrum of information derived from both internal and external environments.

34

In accordance with Chenhall et al.,

35

comprehensive information on management accounting includes both internal and external non-financial information after the fact, as well as internal and external non-financial information before the fact. According to Alliyah et al., the key features of quality management accounting information include broad scope, timeliness, aggregation, and integration. • Broad scope: Future-oriented (probabilistic) information refers to information that encompasses a wide range of future events and involves estimation. External factors such as economic environments, population expansion, technological advancements, consumer preferences, labor relations, consumer organizations, financial information including market size and growth share, and financial factors such as production rates, scrap levels, and machine efficiency.

12

• Timeliness: Timely, current, and tailored information that meets the requirements of internal users, such as accurate reporting frequency, rapid reporting speed, automated receipt, and instant reporting.

19

• Aggregation: Complete yet succinct information is provided, such as in sectional reports, temporary reports, and effects of events on functions. Portions of summary reports, summary reports, hypothetical claims, and models for making decisions: Policies for DCF inventory credit, distinct fixed and variable costs (combined based on time periods and functional domains), and models for analysis or decision-making (such as inventory models, DCF, and marginal analysis).

19

• Integration: The information that is supplied demonstrates how different parts of information are integrated; for instance, specific activity targets and how they relate to one another inside sub-units, as well as reporting on intra-sub-unit interactions.

12

When implementing a MAS within an organization, it is crucial to consider the characteristics of the information that will be produced. Customizing MAS according to the individual requirements of each organization is crucial, as it plays a pivotal role in facilitating decision-making in enterprises. The design and implementation of accounting systems differ depending on the circumstances, influenced by both internal and external influences.9,20,26 The literature has thoroughly investigated the variables that influence the level of sophistication of MAS under various circumstances.

Contingency theory

Previous research investigating the influence of MAS attributes on SMEs performance predominantly employed contingency theory. The relationship among environmental factors, organizational characteristics, MAS, and performance has been extensively explored in the literature, as demonstrated by studies such as refer Refs. 18 and 36 Factors like staff qualifications, organizational structure, and overarching company strategy inherently shape MAS design. Notably, specific innovation strategies play a pivotal role in determining performance outcomes in competitive environments. An organization’s inclination towards actively pursuing novel concepts and engaging in the creative phase of product development manifests in its innovative behavior. 37 Fit serves as the cornerstone principle of contingency theory, delineated into four primary types: selection fit, interaction fit, system fit, and mediating fit. 38 The nexus between contextual variables, components of MAS, and organizational outcomes often aligns with the intermediate fit model. 39 Scholars such as Hariyati Gunarathne, Monehin,40–42 and Shenkar 43 have all utilized this ergonomic model in their prior research. Previous investigations on mediation regarding the MAS variable offer insightful perspectives on the influence of mediating variables on the correlation between contingent factors and financial success. 27 The significance of examining the correlation between the application of management accounting information and performance was underscored by Ref.,38 encompassing both direct and indirect impacts influenced by variables signifying the comprehensive influence of MAS implementation on performance. To scrutinize the mediating function of MAS in the relationship between contingent factors and performance, a median model was developed for this study.

The relationship between contingent factors and MAS

An essential factor that significantly affects MAS is the organizational structure. 21 . Amara 23 defines the organizational structure as the methodical delineation of different responsibilities for team leaders or group assignments, with the aim of ensuring the execution of the organization’s activities. In comparison to mechanistic structure, organic structure is characterized by more decentralization, less vertical differentiation, fewer hierarchical layers, non-formalization, and horizontal ways of communication. 44 The structure has been extensively examined by several writers based on several aspects, including decentralization/centralization and formalization in the fields of machine learning, for example, Refs. 22 and 41. A majority of these research has characterized and quantified the structure as decentralization.

Decentralization pertains to the extent of delegated authority of department heads at lower levels, including implementations associated with management accounting systems, which are acknowledged as a crucial component of an organization’s monitoring package. 11 Decentralization commonly manifests as departmentalization, which entails the need to monitor and synchronize the activities of all departments/divisions within the organization. This enhances the responsiveness and complexity of MAS as the top management exercises control over the departments. 15 Decentralization grants business unit managers increased autonomy in coordinating and overseeing activities, along with enhanced access to information that is not available to the central authority. 25 This results in a heightened requirement for management accounting (MA) systems to support managers in their tasks such as planning, supervisory, and decision-making in decentralized organizations. 45

Decentralized managers require comprehensive and evolving information, including non-financial, external, and forward-looking data, to effectively make a range of marketing, pricing, and inventory control choices. 46 MAS provide the same extensive knowledge attributes as contemporary methodologies that might be beneficial for managers in decision-making within a decentralized organizational structure.

Shahzadi et al. observed that the organizational structure has an impact on the level of control that a manager can exert in order to motivate the labor force. As a result, the organizational structure that the firm chooses will determine how well the MAS design performs in making strategic decisions. This choice might impact the efficiency of the workflow, the flow of information, and the control system.9,13,34,36 In the current study, the concept of decentralization will be defined according to Ref. 47, as referenced in 34. Decentralization refers to the differentiation of an organization based on the level of decision-making independence granted to sub-unit managers, and it is achieved through several means.

Previous literature reviews have revealed conflicting findings about the correlation between decentralization and the implementation of advanced MAS designs.12,36,48 have presented empirical evidence demonstrating a positive correlation between decentralization and the use of advanced MAS.

49

proposed that a decentralized structure requires a more advanced MAS to ensure that all levels of the organization have access to reliable information for effective planning, controlling, and decision-making.

15

made the intriguing observation that the aggregation and integration of information are crucial for managers in decentralized structures. However, managers in both centralized and decentralized structures require information that is comprehensive in scope and timely. This implies that companies may choose to maintain a centralized structure if their primary objective is to acquire a broader range of information and receive it on time. Nevertheless, Amaa et al.

23

discovered that only managers operating within a decentralized corporate framework characterized by elevated degrees of uncertainty would necessitate a substantial range of knowledge. The disparities in the aforementioned findings may be attributed to variations in the business landscapes and economic conditions in which the organizations operate. Consequently, it is possible for a hypothesis that:

The qualifications of accounting personnel have been identified as an internal component that influences the design of MAS. 46 The qualification level of accounting staff refers to the experience level of knowledge and skills that accountants have obtained to perform specific tasks inside their organizations. 45 Competent accounting personnel has a significant impact on firms since their level of knowledge and understanding of accounting principles directly influences the growth, success, and long-term viability of the business. 50 Companies also hire professionally qualified accounting staff to implement MAS to assist managers in decision-making and internal reporting. Furthermore, lack of personnel could be a crucial element in the implementation of modern MAS. 46

According to Ref. 15, the credentials and expertise of accounting personnel significantly influence an organization’s progress and achievements. The proficiency of accounting personnel is paramount due to its significant impact on resource allocation and utilization, performance assessment, organizational policy development, and decision-making. 3 The extent to which an organization possesses accounting knowledge is a determining factor in the adoption of a MAS. Both Kingazi and Adu-Gyami15,21 corroborate this notion. Their research reveals a significant positive correlation between the qualifications of an organization’s accounting personnel and its adoption of MAS. According to Ref. 12, the significance of accounting personnel’s expertise surpasses their qualifications in the context of MAS implementation within an organization. 51 posited that the importance of MAS fluctuates in response to modifications in the operational milieu. Therefore, experience devoid of appropriate qualifications would quickly lose its relevance.

Kingazi et al. contend that the qualifications of accounting personnel wield significant influence over the divergence in MAS utilization between large enterprises and SMEs. They underscore the capacity of prominent organizations to engage proficient accounting personnel and to segment the accounting function into discrete domains encompassing management, cost, and financial accounting. Conversely, smaller entities typically engage accounting specialists, either through direct employment or contractual arrangements, primarily for financial reporting and tax compliance purposes.

12

Notably, leading organizations enlist highly adept accounting professionals tasked not only with financial statement preparation but also with furnishing managerial decision-making support and facilitating the establishment and sustenance of competitive advantages.3,45 A study by Nugrahani et al.

46

delineated the influence of management accounting personnel credentials on MAS adoption rates, indicating a propensity for heightened adoption among organizations employing certified accountants, particularly in the domain of contemporary MAS.

21

Consequently, the proficiency exhibited by accounting professionals’ manifests directly in the implementation of MAS within organizational contexts. Henceforth, it is incumbent upon organizations to prioritize the enhancement of accounting personnel capabilities or the recruitment of seasoned management accountants to attain superior performance outcomes.

12

As a corollary, the ensuing hypothesis is postulated.

Organizations require strategy modifications to adjust to an environment where incremental strategic changes or significant adaptation will result in a beneficial transformation of the organization’s structure. 52 Achieving optimal efficiency and uniformity in a company requires a comprehensive overhaul of all its components, such as culture, strategy, people, system, structure, and more. 32

Latifah et al. identified three strategies: defender, prospector, and analyzer. Defenders, cost leaders in a stable, cramped production environment, rely more on manufacturing, finance, and engineering than research, marketing, and development for organizational success. Prospectors (relatively differentiators) compete through business expansion and product innovation. They actively seek ways to extend and improve products, causing market instability and changes from competitors. Industry leadership matters more than profit efficiency. Thus, they prioritize development and market research. Lastly, analyzers keep the greatest defender and prospector qualities.52,53

Lestari et al. classified tasks as build, hold, and harvest. Build strategy aims to expand market share and competitiveness, although short-term profitability may decrease. Sector-leading corporations may use this method. Harvesting strategies focus on short-term cash flow and profitability rather than market share. Two previous tasks are combined in hold. Companies use this method to maintain market share and ROI. 52

Companies may acquire a competitive edge by focusing on cost leadership or differentiation. 52 Cost leaders work to provide their organization cheaper items. Obtaining advantageous raw material prices and applying sophisticated production technologies to lower product costs may give a competitive edge. 17 Differentiators produce unique products to attract customers. High product quality, availability, after-sales and delivery services, and flexibility. 54 That does not mean the cost leader should ignore pricing, product, and other differentiators, but they may arise in the lower focus stage. While quality, productivity, and other cost leadership goals are important, organizations executing a product differentiation strategy should prioritize differentiation goals. Porter’s approaches matter for this study for three reasons. First, MA benefits organizations that prioritize cheap prices and product differentiation. 52 Second, Porter’s techniques are simpler and better for Jordan’s competitive market.52,53 Porter’s techniques are built on earlier observations and have the right reach, making them academically sound.53,54

According to the literature, the main objective of management accounting is to generate value for the organization by providing information that assists management in creating and maintaining competitive advantages. 11 Management accounting is an integral part of the creation of a corporate strategy. Hence, corporate strategy and management accounting are intricately connected 2 . Pham et al. 55 concurred that both the business strategy and the MAS influence the business strategy. According to 11, organizations must integrate MAS into their overall company strategy to achieve the desired performance. According to Azudin et al., among other contingent factors, the strategic objectives of the institution have an impact on the adoption of MAS in an organization. According to 23, the competitive strategy is a determining factor in the choice of MAS for an organization. In addition, Glushakova et al. 2 affirmed that there is a positive correlation between corporate strategy and non-pecuniary performance measurements, thereby reinforcing this perspective. The strategic orientation of the company has an impact on the MAS that the entity will employ. 54 In contrast, Uyar et al. 56 contended that management accounting information has a significant impact on both the formulation and execution of corporate strategy, thus establishing a mutual dependence between the two.

Companies that opt for a strategic approach are typically classified into three categories: differentiation, cost leadership, and focus strategies.

17

Those adhering to cost leadership strategies commonly rely on traditional costing techniques, although conducting a competitive analysis might offer more advantages. Conversely, organizations embracing a differentiation strategy prioritize their investments in marketing and differentiating expenses. It is often observed that organizations employing a differentiation strategy tend to exhibit a higher level of MAS adoption compared to those following a cost leadership approach. Furthermore, it is anticipated that firms pursuing a cost leadership strategy will implement MAS focusing on cost information at a higher organizational level compared to those adopting a differentiation strategy.

11

The adoption of a focused approach, which integrates cost leadership and differentiation strategies, has been noted to influence MAS adoption in certain developing economies.

55

Building upon this discussion, this study incorporates business strategy as a contextual determinant of MAS adoption extent. The third hypothesis is formulated as follows:

The relationship between MAS and performance

The nexus between the utilization of management accounting systems (MAS) and organizational performance is well-established within the broader framework of management accounting and control systems and organizational effectiveness. The literature defines a management accounting and control system as a comprehensive framework providing valuable information to aid managers in making proficient decisions to achieve organizational objectives10,18,46. Kesumawati and Godil11,12 demonstrated that leveraging a substantial volume of MAS information assists managers in mitigating job complexity and ambiguity, thereby facilitating effective decision-making. Extensive utilization of MAS information compels managers to explore alternative courses of action, leading to a notable improvement in task understanding and enhanced performance.13,44

In a study by Puspitawati et al., 30 the relationship between management accounting information and organizational performance was investigated. Research by Alliyah et al. 18 revealed a direct correlation between management accounting information and production performance, indicating a positive association. Furthermore, empirical evidence elucidated that the facilitator of organizational learning played a moderating role in the linkage between knowledge availability and performance enhancement. Other scholars also delved into the relationship between various management accounting strategies. For example, Damayanti et al. 57 scrutinized the association between MAS and performance, revealing that MAS exerts a detrimental impact on performance in environments characterized by low perceived environmental uncertainty. Moreover, Shabbir et al. 10 emphasized that heightened competitive pressures have prompted a greater emphasis on differentiation strategies, leading to organizational structural adjustments, adoption of state-of-the-art production technologies, and incorporation of advanced management accounting practices. These advancements have escalated reliance on non-financial accounting information, thereby positively influencing organizational performance.

Damayanti et al. 57 identified a positive correlation between diverse information utilization and stock returns. However, the author did not find any significant association between information usage and indicators such as ROA or sales growth. In their respective studies, Adu-Gyamfi and Bransah21,58 investigated the relationship between marketing rivalry intensity and the impact of benchmarking and monitoring information provided by the MAS on business unit performance. Their research unveiled that managers’ utilization of such information influences the nexus between market competitiveness level and business unit success. This discovery underscores that firms leveraging MAS information were adept at effectively addressing market competition challenges, thereby enhancing overall performance.

In their study, Shabbir et al.

10

discovered a detrimental correlation between several strategic control measures, such as market research, benchmarking, strategic audits, and performance. Alliyah et al.

18

found that MAS had an impact on the connection between strategic decisions and performance. The study demonstrated that the extensive range of MAS information had a positive impact on performance. Nugrahani et al.

46

examined the impact of a customer-centric approach and non-financial performance measuring tools on performance. The study demonstrated a direct correlation between the implementation of a customer-focused approach and the utilization of non-financial performance measures. However, it found no connection between non-financial performance systems and overall performance. Alliyah et al.

18

examined the correlation between MAS and organizational performance, revealing a favorable association, particularly when there is a high level of perceived environmental uncertainty (PEU). The connection exhibited a negative correlation when the level of PEU was low. A study by Nguyen et al.

13

examined the correlation between MAS and organizational performance, validating a favorable connection, particularly in situations with a high level of PEU. Furthermore, Shabbir et al.

10

validated the correlation between MAS and sub-unit performance. Thus, the present study posits the following hypothesis:

The role of MAS on the relationship between contingent factors and performance

According to 23, organizations have the ability to utilize a collection of MAS to create valuable information for decision-making about resources. This, in turn, leads to dynamic management practices and the achievement of a competitive edge. The theoretical frameworks proposed by 14 and 21 consist of interconnected contingent elements that posit the utilization of MAS as a means for businesses to achieve their intended organizational objectives and outcomes. According to 55, in order to achieve better judgments that result in higher performance, firms should implement suitable MAS to provide managers with the essential information required for making rational decisions. The significance of MAS in moderating the link between contingent variables and performance has been extensively studied, particularly in developing nations. 59

According to 15,21,24,36,48,55,60,61, contingent factors are connected to MAS and these systems are connected to performance. Therefore, it can be postulated that MAS acts as a mediator in the relationship between contingent factors and performance.

Research methodology

The present study employs a quantitative approach to investigate the mediating role of MAS in the relationship between performance in SMEs in Jordan and various contingent factors. The variables are thoroughly discussed, and the data are rigorously scrutinized and analyzed to test hypotheses and present the research findings, accompanied by corresponding recommendations.

Utilizing a descriptive-analytical methodology, this field study examines the impact of MAS on the correlation between performance and contingent factors in Jordanian SMEs. The questionnaire and study design were formulated through a comprehensive review of recent studies (published within the last 5 years) that investigated similar research topics. The aforementioned investigations include studies by Alliyah, Pedroso, Godil, and Msomi et al.12,18,25,28,29,31,50,62 This study examines a questionnaire designed to assess the mediating role of MAS in the relationship between contingent factors and performance. Additionally, a questionnaire was developed to determine the correlation between the factors comprising each component of contingent factors, MAS and performance.

Nevertheless, the survey has been translated into Arabic to accommodate the non-English-speaking country where it will be conducted. The terminology has been translated with precision to facilitate the comparison of survey findings with similar surveys (including aspects such as contingent factors, MAS, and performance) and to guarantee the validity and reliability of the translated questionnaire. Eight accounting experts who are knowledgeable in the field pretested the questionnaire. This technique facilitates the provision of optimal input regarding the layout and substance of the questionnaire.

In line with ethical research standards, participant involvement in this study was entirely voluntary, with informed consent obtained from all respondents prior to data collection. Confidentiality and anonymity were strictly maintained, and personal information was handled with care to protect the participants’ privacy. The research adhered to the ethical guidelines set forth by the institution’s ethics committee, ensuring compliance with the standards for research involving human subjects.

The selection of Structural Equation Modeling (SEM) for this study is predicated upon its inherent capacity to concurrently scrutinize the intricate interplay among multiple independent and dependent variables. Within the realm of SEM, two primary methodologies emerge: covariance-based structural equation modeling (CB-SEM) and variance-based structural equation modeling (VB-SEM). The decision between these methodological frameworks is contingent upon considerations such as the distributional properties of the data and the overarching objectives of the investigation. CB-SEM is particularly apt for endeavors focused on validating singular theoretical constructs or conducting comparative analyses among multiple theoretical frameworks. In contrast, variance-based structural equation modeling, also recognized as Partial Least Squares-based Structural Equation Modeling (PLS-SEM), is conducive to exploratory research endeavors with predictive objectives. It is noteworthy that CB-SEM permits the incorporation of one or more indicators per latent construct, subject to a minimum threshold of three indicators. VB-SEM serves a dual function: firstly, to quantify the extent to which variations in dependent constructs can be elucidated, and secondly, to evaluate data fidelity by appraising the efficacy of the measurement model. 63 Given the empirical nature of the present study and its alignment with the aforementioned methodological criteria, Partial Least Squares Structural Equation Modelling (PLS-SEM) was deemed the most appropriate analytical modality.

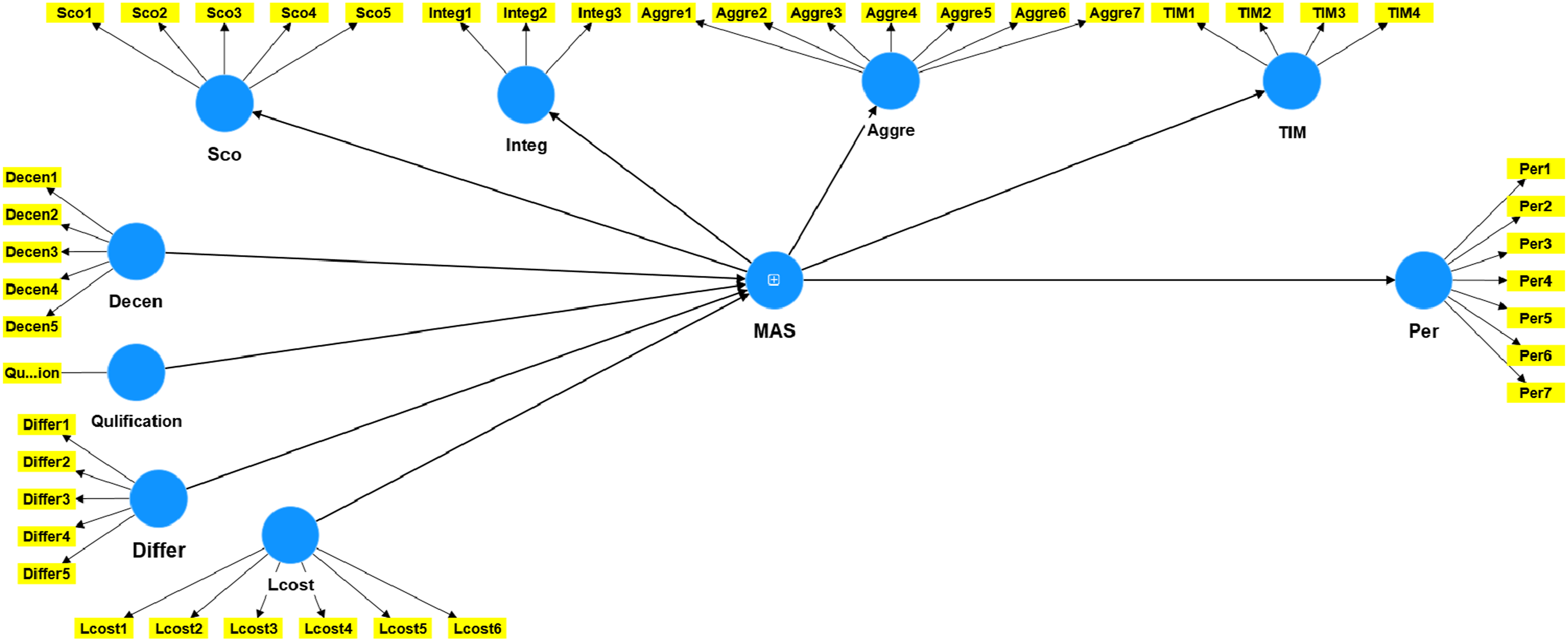

Research model

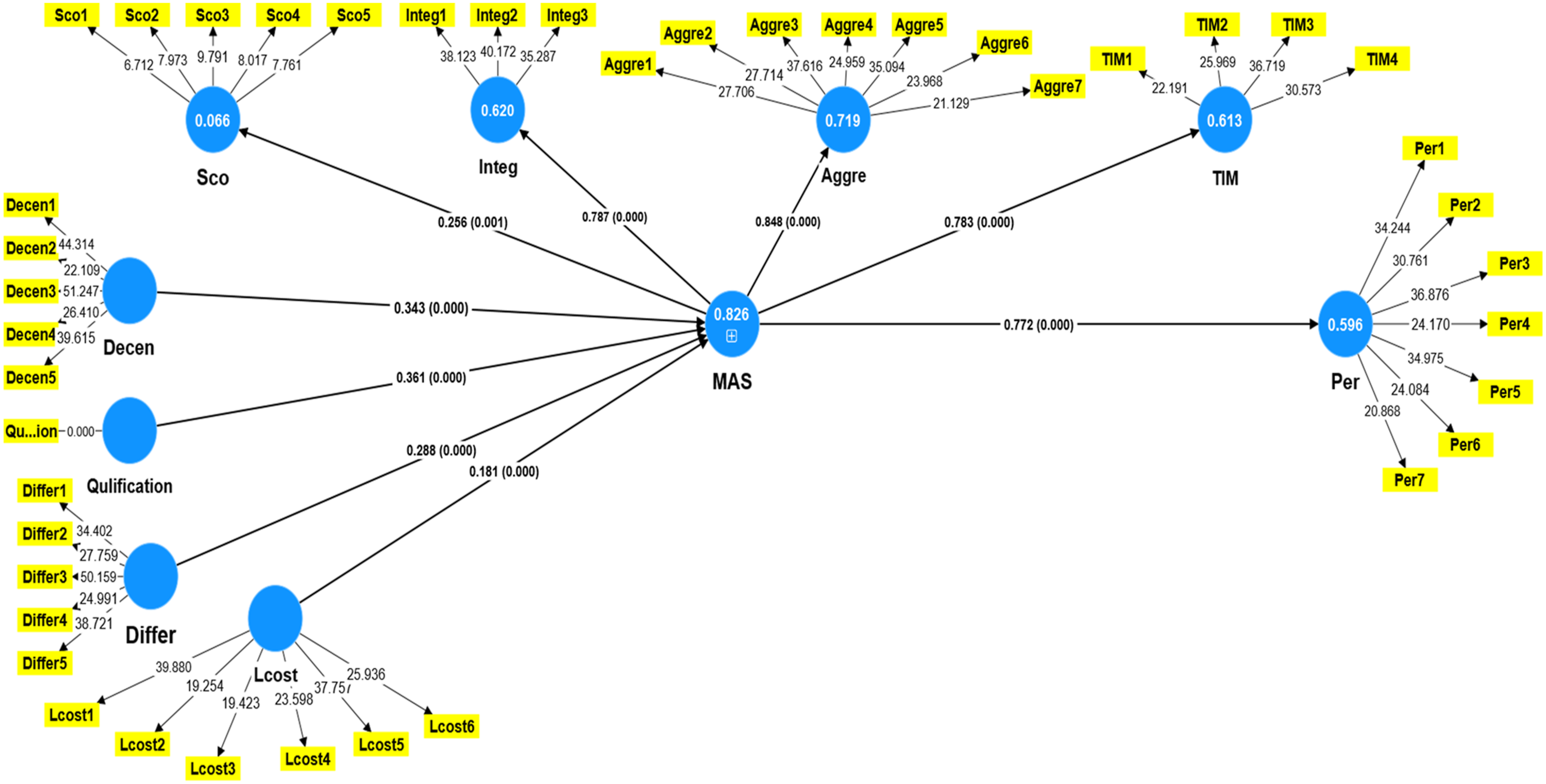

The study accomplished its primary objective and specific goals by constructing a research framework that incorporated relevant prior studies, such as those conducted by Pedroso and Nurhidayah29,31 Figure 1 demonstrates the connections between these variables. Research model.

The respondent’s perception of the “qualification level of accounting staff” is characterized as narrow in scope, lacking complexity, and direct. Therefore, it is deemed suitable to adopt a measurement approach employing a construct comprising a single item. Diamantopoulos et al. 64 posits that when an attribute is perceived as concrete, it can be effectively measured using only one item. Supporting this assertion, research by Diamantopoulos et al. 64 demonstrates that a single-item predictor exhibits comparable predictive validity to that of a multi-item scale. Partial Least Squares Structural Equation Modelling (PLS-SEM) offers an advantageous framework for handling single-item constructs without encountering identification concerns or necessitating additional criteria or constraints. As noted by Hair et al., 63 in the context of a single-item construct, the direction of interactions between the construct and the indicator holds no significance, as the construct and item essentially represent the same underlying concept.

Population and sample

According to 65, a target population refers to a collection of comparable elements or objects possessing the necessary information for the researcher, facilitating inferences. The Jordanian Chamber of Industry (2018) survey reported that there were approximately 1230 manufacturing enterprises formally registered with the Jordanian Chamber of Industry in Jordan. Among these, 98% were categorized as small and medium-sized enterprises (SMEs). The companies included in the study sample were selected using the probability sampling technique, ensuring that all respondents had an equal opportunity of being chosen, as described by Sekaran et al. 66

The study sample comprised 464 heads of accounting departments and financial managers from Jordanian SMEs, who were selected randomly. A total of 464 questionnaires were distributed, out of which 415 were collected, accounting for 89.4% of the total distribution. All collected surveys were included in the subsequent statistical analysis. Therefore, the final sample consisted of 415 employed respondents from these SMEs.

The high response rate of the survey instils confidence in both the study and its findings. A low response rate would compromise the statistical robustness of the collected data, particularly when dealing with large cohorts, thereby diminishing the reliability of the results. This observation aligns with the findings of Sammut et al., 67 suggesting that higher response rates improve the validity and statistical integrity of the sample. Moreover, research by Lee et al. 68 indicates a positive correlation between increased response rates and the perceived credibility of results among key stakeholders.

Data analysis

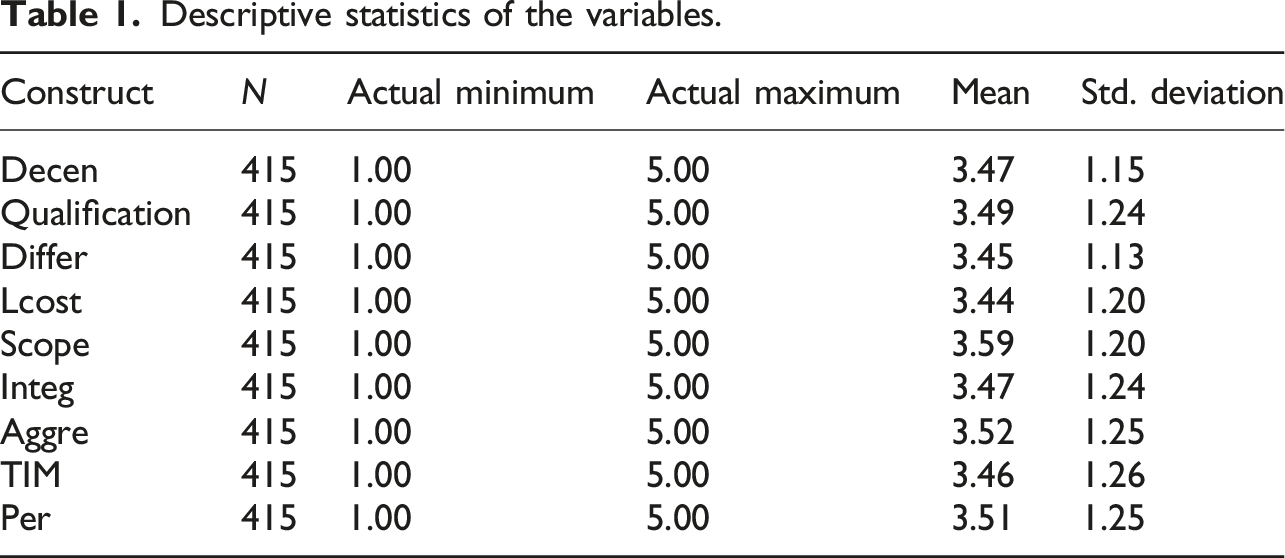

Descriptive analysis

The mean score for the dimensions of the components assessed using five Likert scales varied between 3.44 and 3.59. The findings indicated that the mean values for decentralization and qualification level of the accounting staff were 3.47 and 3.49, respectively. Standard deviations of 1.15 and 1.24 were present with these values, respectively. These findings indicate that the organizations surveyed have a moderate inclination to react to the decentralization and skill level of their accounting personnel. Addressing these variables mitigates the extent of influence that poses a risk to the achievement of an organizational objective. The elevated magnitude of the standard deviation indicates that the views in response to these changes vary among the organizations being analyzed. This elucidates that SMEs lack equivalent resources and competencies. The findings indicate that the product differentiation strategy and low-cost strategy had a mean value of 3.45 and 3.44 with a standard deviation of 1.13 and 1.20, respectively. Thus, the majority of enterprises that responded saw the implementation of both a product differentiation strategy and a low-cost strategy as being of moderate importance.

Descriptive statistics of the variables.

Research instrument

The current research incorporated items derived from the existing literature to develop a questionnaire using a five-point Likert scale (ranging from strongly agree to strongly disagree) based on the variables utilized in the study. A set of 19 items were employed to assess the four aspects of MAS: 7 items for measuring aggregation according to reference 57, 3 items for measuring integration according to references 15 and 57 5 items for measuring the broad scope according to references 15 and 57, and 4 items for measuring timeliness according to reference 57. In addition, an assessment of decentralization was conducted using 5 items from reference 23. The qualification level of accounting staff was evaluated using one item from reference 45. Differentiation strategy was assessed using 5 items from reference 57, low-cost strategy was assessed using 6 items from reference 57, and performance was evaluated using 6 items.20,38

In order to assess the content validity of the survey instrument, a limited number of potential respondents or experts in the field of study are consulted to obtain their views on the exact wording and phrasing of the questionnaire. 66 Thorough knowledge of content validity is crucial. 69 Content validity refers to the extent to which a collection of items, when considered together, constitutes a sufficient operational definition of a concept. 69 Business researchers typically establish the content validity of tools by computing a content validity index (CVI) using the ratings of experts on the relevance of items to construct accurate measurements. Yusoff et al. 69 proposed that a legitimate scale should necessarily be evaluated by a panel of at least three experts, however more than 10 experts were deemed superfluous.

The suggested study involved the selection of six specialists divided into two groups. One group was composed of three seasoned professionals from Jordanian firms, while the second group included three professors from the Department of Business Administration from Jordanian universities. In order to prevent a neutral and ambivalent midway, the items were assessed for relevance, clarity, and simplicity using a four-point Likert scale (“not relevant” = 1, “needs some revision” = 2, “relevant but needs minor revision” = 3, and “very relevant” = 4) 69 . Yusoff et al. 69 advised selections one and two as irrelevant, three and four as relevant, and I-CVI should be 1.00 for 3–5 experts and 0.78 for 6–10 experts, 69 a scale-level content validity index (S-CVI) of 0.80 or above is appropriate. For a scale to have strong content validity, Yusoff et al. 69 propose items with I-CVIs of 0.78 or higher and S-CVI/Ave of 0.90 or higher. In this investigation, all constructs had higher S-CVI/Ave values of 0.92-1.00 and I-CVIs of 0.83-1.00.

Measurement model evaluation

The precision and reliability of the data were ensured through the utilization of Partial Least Squares Structural Equation Modeling (PLS-SEM) to assess the quality of the measurements. Prior to conducting the experiment, this study evaluated the model’s ability to differentiate between groups, establish a common understanding of those groupings, maintain internal consistency, and produce dependable indicator results. • •

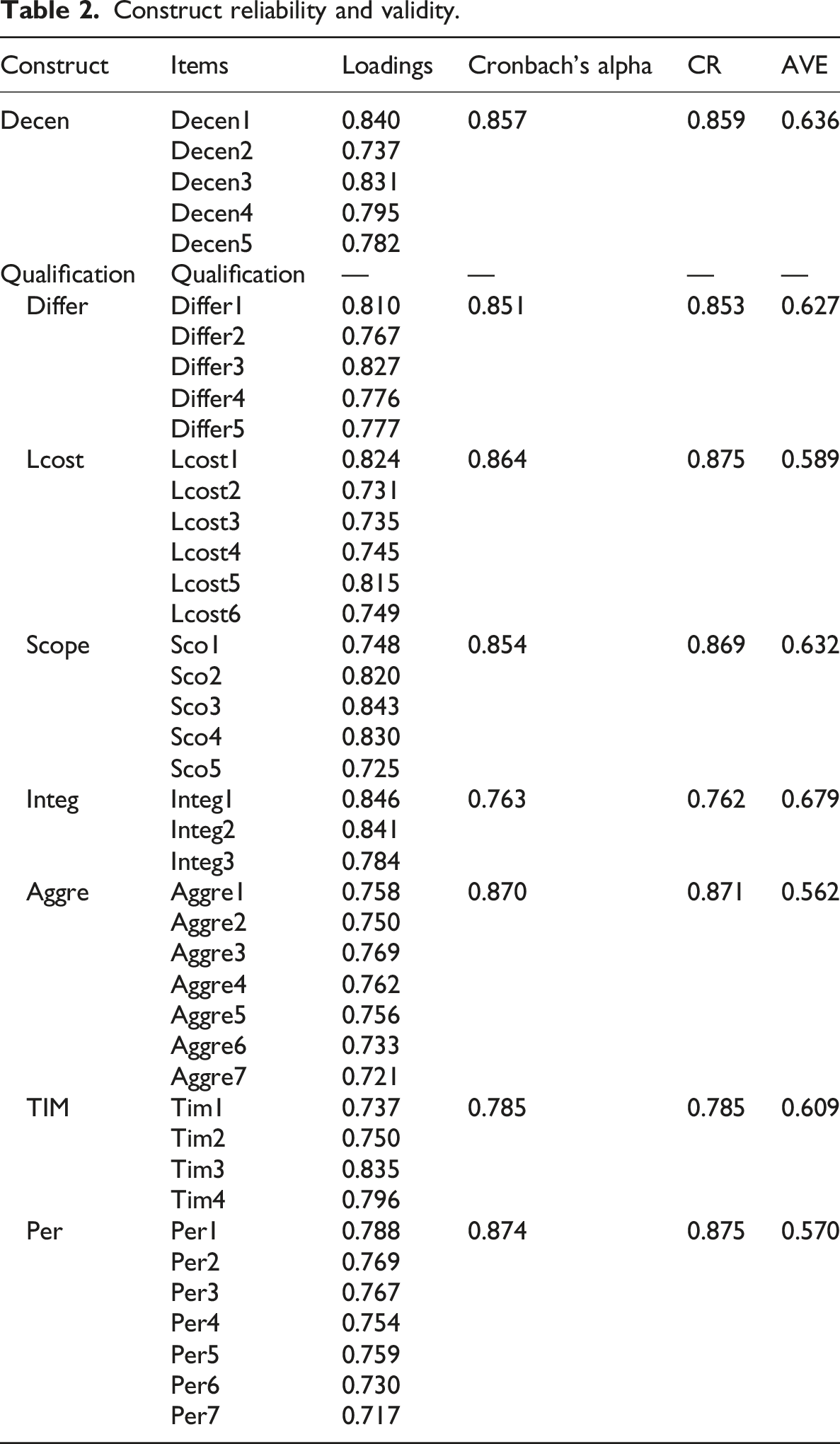

Construct reliability and validity.

The reliability of the indicator was assessed by using the outside loadings of each measure, and it is required that the product loading factor be more than 0.70.

63

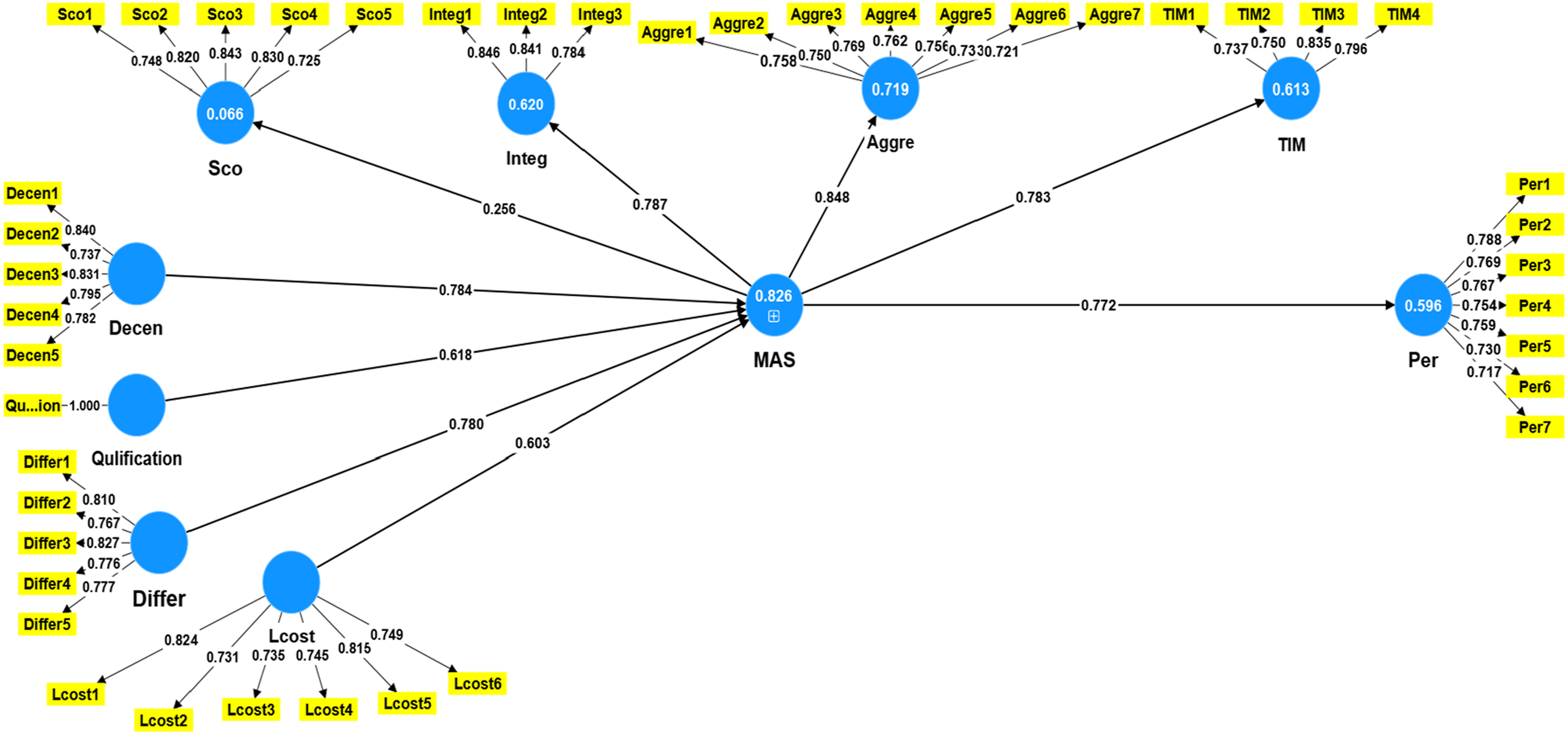

Every item has a value of more than 0.70; hence, none of the items will be removed. The factor loadings have been presented in Table 1 to provide a clearer representation. Additionally, Figure 2 provides further information. Measurement model.

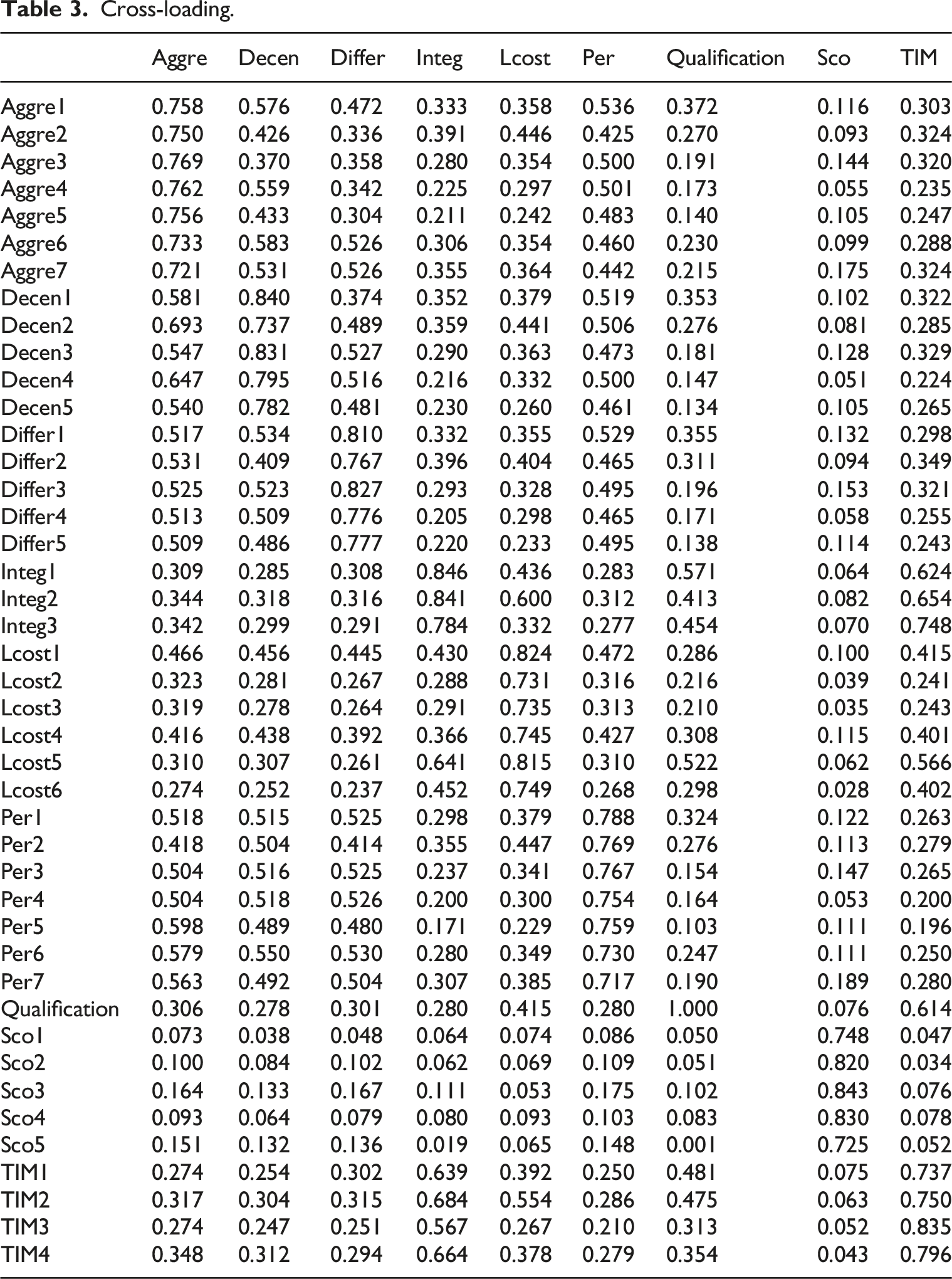

Cross-loading.

Findings of Fornell-Larcker criterion.

Structural model evaluation

The PLS route modeling study involved testing the structural model after the measurement model (inner model). Hair et al. 70 propose examining the model’s (R2) values, the magnitude of effect (f2), and the predictive relevance. The technique of bootstrapping was employed to assess the statistical significance of the model’s anticipated associations.

R-square (R2)

The evaluation of the structural model in PLS-SEM requires the use of the R2 criterion, as stated by Hair et al. 63 The R-squared statistic is a measure that may be utilized to assess the proportion of the overall variation in the dependent variable that can be ascribed to each predictor. 63 The R2 values of 0.75, 0.50, and 0.25 are considered large, moderate, and weak, respectively, according to 63. According to Figure 1, the research model explains 59.6% of performance and 82.6% of the overall variation in MAS. The study yielded satisfactory R-square values for the endogenous latent variables.

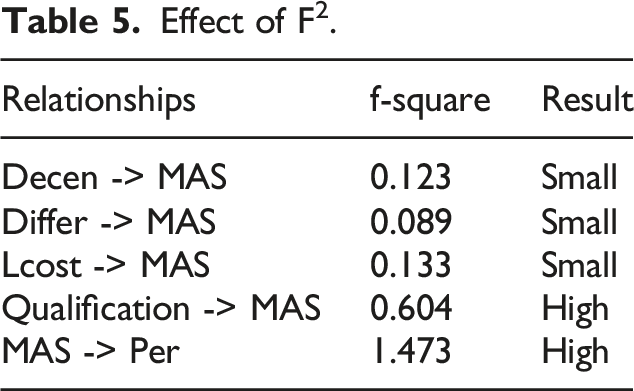

Effect size (F2)

Effect of F2.

According to Table 5, the impact of decentralization in MAS had an effect size of 0.123, while the effect size of the qualification level of accounting staff in MAS was 0.604. The product differentiation strategy in MAS had an effect size of 0.089, whereas the low-cost strategy in MAS had an effect size of 0.133. Furthermore, the size of the effect of MAS on performance was 1.473.

Construct cross-validated redundancy

Q2 test.

The Q2 test results for all endogenous latent components are shown in Table 6 of the current study in the column labeled 1-SSE/SSO. For MAS (Q2 = 0.242) and performance (Q2 = 0.335), the values were above zero, showing the predictive usefulness of the model. 73

Direct effects testing

Direct relationships.

Note: **p < 0.01.

The result.

The mediating relationships testing

Researchers first assessed the direct effect of exogenous and endogenous elements before looking for mediator linkages, or indirect influence. Many statistical techniques are available to draw conclusions and compute confidence intervals (CIs) in the evaluation of the mediation impact, such as bootstrapping69,74,75 coefficients process, and causal step. The causal step technique proposed by Baron and Kenny does not provide or quantify inferential testing. 32 The Sobel test reduces indirect influence, necessitates non-standard route parameters, and lacks statistical strength since the indirect effect is not normally distributed. 70 It also performs poorly with small sample sizes. The standard error formula and the assumption of normally distributed indirect effect sampling constitute the foundation of the coefficient’s method conclusion; however, there is not a clear-cut standard by which to choose. 70

The results of the mediating.

Note: **p<0.01.

The findings from Table 8, derived through bootstrapping, highlight the significant role of management accounting systems (MAS) in shaping various organizational dynamics. Firstly, MAS demonstrates a significant influence on the relationship between decentralization and performance (β = 0.265, 95% CI = 0.154–0.376). Additionally, MAS exhibits a noteworthy impact on the connection between the qualification level of accounting personnel and organizational performance (β = 0.279, 95% CI = 0.232–0.322). Moreover, the results underscore MAS’s role in modulating the relationship between differentiation strategy and performance (β = 0.222, 95% CI = 0.128–0.328), as well as the link between low-cost strategy and performance (β = 0.140, 95% CI = 0.094–0.187). Thus, the findings lend support to hypotheses H6, H7, H8, and H9.

Discussion and conclusion

Theoretical implications

This study aimed to determine the mediating role of MAS in the correlation between contingent variables and the performance of SMEs in Jordan. In general, the participants in the study held the perception that their respective firms would adopt MAS, leading to improved performance. Regarding the first study objective, the results suggest that contingent factors, including decentralization, the qualification level of accounting staff, differentiation strategy, and low-cost strategy, have significant positive influences on the adoption of MAS by SMEs in Jordan.

The implications of the study suggest that businesses that adopt a decentralized approach, characterized by well-defined entities and authority for each department, are more inclined to achieve success in establishing MAS. 34 By granting departments full decision-making authority, they can take a more proactive approach to planning, regulating operations, and handling information that is not accessible within the company. 49 This enables them to make successful management decisions. Nevertheless, in a nation undergoing a shift from a centralized economy to a market economy, such as Jordan presently, the centralized organizational structure remains prevalent in firms. 20 Additionally, many corporate managers received their training and grew up in a centralized economy, which exposed them to a stereotypical and overly administrative culture. Consequently, the majority of subordinate leaders across all sectors of the organization are unable to make autonomous choices without the endorsement of top-level executives. This somewhat restricts the company’s ability to respond to shifts in the business landscape, thereby impacting the competitiveness of firms. The restrictions mentioned are considered obstacles that have a substantial impact on the implementation of MAS in Jordanian SMEs. Hence, to facilitate the implementation of MAS, corporate managers must modify their management approach by explicitly delegating greater responsibility and power to individual departments, thereby enabling them to make proactive and effective management choices. 48

Furthermore, the study underscores the significant influence of accounting personnel expertise on the successful adoption of MAS within SMEs in Jordan, thereby confirming the second hypothesis. These findings underscore a discernible correlation between the proficiency levels of accounting personnel within SMEs and the utilization of MAS. These results are in alignment with Nugrahani et al., 46 who similarly observed that heightened expertise among accounting staff in MAS enhances the likelihood of SMEs embracing an integrated strategy encompassing scope, integration, aggregation, and timeliness. This observed trend may be attributed to the fact that accounting staff, vested with authority over SME processes, exhibit a heightened sensitivity towards the utilization of MAS, which serve as a primary source of financial information. 12 By proposing that appropriate accounting and control procedures are contingent upon factors influencing the firm, this study adds to the existing body of evidence supporting contingency theory.

Additionally, it was shown that low-cost and distinctiveness initiatives played a significant role in enhancing MAS acceptance among Jordanian SMEs. The findings imply that businesses stand to benefit more from the use of MAS if they place a higher priority on differentiation and cost-effective strategies. MAS assists them in making decisions and monitors their progress in relation to their strategy in light of the unstable external environment. 54 There is a claim that Jordanian SMEs have enough low-cost and unique strategies in place to enable the use of MAS. According to 55, the companies are commended and honored for their superior product quality, distinctive features, updated production processes, enhanced organizational architecture, and higher capacity utilization. Based on Kingazi et al., 15 the businesses’ use of MAS to accomplish their intended goals is a noteworthy illustration of their understanding of business strategy.

In accordance with the fifth hypothesis, the findings suggest a positive impact of MAS on the performance of SMEs in Jordan. This result aligns with the conclusions drawn by Alliyah et al. 18 in their research. Moreover, alongside its comprehensive coverage, the timely dissemination of information stands out as a crucial factor in mitigating the risks of financial loss or damage.10,18,46 Integrating the management accounting information system across all operational facets of a company can significantly enhance managerial decision-making. The utilization of data aggregation within the management accounting system streamlines the process of managers assessing the potential ramifications of forthcoming decisions. As a result, the wealth of information that MAS provides can be extremely useful in the decision-making process.13,44

Hypothesis 5 suggests that MAS has a significant influence on the performance of SMEs. In addition to its extensive scope, the prompt dissemination of information must be a paramount consideration to mitigate the risk of financial loss or the occurrence of damage. The integration of the management accounting information system into all operational aspects of a corporation can facilitate managerial decision-making. The utilization of aggregation inside the management accounting system facilitates the process of management in evaluating the potential consequences of forthcoming decisions. Consequently, the extensive array of information offered by MAS will prove highly advantageous in the process of decision-making. 18

Furthermore, it can be demonstrated that MAS play a mediating role in the relationship between differentiation strategy and organizational success. These findings align with previous investigations by Pham and Wahyuni,55,61 who similarly identified the mediating function of MAS in the connection between differentiation and performance. Additionally, MAS serves as a mediator in the association between a low-cost strategy and performance, as supported by Sreekumar et al. 60 research.

In light of Damayanti and Bransah,21,57,58 it’s evident that companies are increasingly recognizing the significance of strategic management, leading them to leverage MAS to achieve their objectives. By facilitating decision-making and progress evaluation, MAS enables managers to assess the effectiveness of their chosen strategies, whether aimed at cost leadership or product differentiation. Consequently, this analytical approach contributes to enhanced firm performance.

The objective of this research is to examine the potential mediating role of MAS in the relationship between the achievement of qualifications for accounting personnel and their performance. It may be inferred that the qualifications of financial personnel can enhance the performance of SMEs by promoting the overall utilization of MAS.3,45 This conclusion is significant as it highlights the substantial impact that workers have on organizational outcomes through their decision-making processes, which are influenced by their individual traits. MAS have the potential to enhance organizational profitability through the provision of information support in strategic decision-making and operational control.12,21 Consequently, employees at SMEs must focus on their daily job responsibilities and undergo training to ensure they remain informed about employment requirements.

The results indicate that MAS serve as a mediator in the connection between decentralization and performance. This finding aligns with Anh et al. 24 research, which demonstrated that MAS plays a mediating role in the decentralization-performance relationship. Furthermore, Pavlatos et al. 48 observed that strategic cost management affects the link between decentralization and performance, elucidating why organizations reliant on horizontal communication within management opt for MAS adoption. Managers perceive the information provided by these accounting systems as indispensable.

Practical implications

The study’s findings have an impact on financial professionals, practitioners, and policymakers in Jordanian SMEs. The roadmap’s explanation of Jordanian SMEs’ most key MAS adoption and organizational success factors provides valuable insights. This supports the Jordanian government’s investment goals and boosts MAS adoption and organizational performance. The severe situation in Jordan has caused economic changes in the Jordanian corporate market, lowering investment rates. Some management and accounting procedures must be changed to compete in the market. Consumer expectations and preferences have changed, requiring MAS and strategic interventions related to internal and external variables to recognize and address them. The results of the research suggest ways SMEs might boost performance and gain a competitive edge. Effective MAS use and awareness of factors can achieve this. Industrial firms should focus on MAS in addition to other factors to ensure long-term success and greater performance. Factors and MAS should be coupled to improve SMEs’ performance.

Managers should focus on Jordanian SMEs and government activities that may affect MAS use. Due to these factors, organizations may need to prioritize particular MAS. SMEs in Jordan should adjust their performance metrics by adding or removing measures to adapt to their business climate. They may also need to modify weights for different measurements.

Limitations and future research

The current study is subject to some constraints and offers recommendations for future research. A primary constraint of this study is its inherent nature as a cross-sectional study. To guide future research, we suggest investigating the longitudinal impact of the influence of MAS on performance. Furthermore, the participants of this study comprised individuals who held positions as heads of accounting departments and financial managers. Therefore, we propose that future recommendations include a heterogeneous sample and longitudinal examination to identify how and to what extent MAS impact performance. Furthermore, our study concentrated on a single country and examined the influence of situational variables on MAS and operational effectiveness. This restricted the applicability of our study, both to the provided sample and to other nations. Hence, we propose that forthcoming research should prioritize the examination of interactions among pertinent factors by employing bigger sample sizes across a greater number of nations. Furthermore, we were unable to present substantiating evidence for the correlation between all contingent variables and MAS. We recommend that future study compare the effects of all contingent variables on MAS. In conclusion, the study’s narrow emphasis on a single country restricted the analysis of contingent variables, MAS, and performance in various institutional settings. Thus, we propose that future studies examine the research variables in various institutional settings.

Statements and declarations

Footnotes

Acknowledgments

We wish to acknowledge support from Arab Open University-Jordan.

Author contributions

Conception: Anas Ghazalat and Alaa Mansour.

Methodology: Anas Ghazalat and Alaa Mansour.

Data collection: Shadi Alkhasawneh and Mohammad Alhmood.

Interpretation or analysis of data: Anas Ghazalat, Shadi Alkhasawneh, and Mohammad Alhmood.

Preparation of the manuscript: All authors.

Revision for important intellectual content: Anas Ghazalat and Alaa Mansour.

Supervision: All authors.

Conflicting interest

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.