Abstract

This research note investigates the failure probability of British Initial Public Offerings (IPOs) on the Alternative Investment Market (AIM) in terms of spatial proximity to London and operating within the financial services sector. The results suggest that financial services firms in proximity to London experience a higher failure rate on AIM. It is suggested that part of the higher failure rate observed on AIM, compared to the failure rate of small IPOs elsewhere, can be explained by the London dominance of AIM, which favours those financial sector businesses that manage to achieve an IPO.

Introduction

It is now recognised that the majority of small firms have neither the desire nor scope to grow, and as such are able to source their funding needs from cash flow, overdrafts and small-scale debt financing (Davies, 2011; Fraser, 2005). However, for the minority of firms that seek growth, there is a widely-held view (from Macmillan Committee, 1931, to Klagge and Martin, 2005) that whatever the structure of the (debt and equity) capital markets, neither financial institutions nor markets have provided adequate amounts and/or types of capital to support such growth. One response to this problem of generating access to equity funding was the establishment of the Alternative Investment Market (AIM) in 1995. However, current evidence illustrates that AIM is dominated by London-based Initial Public Offerings (IPOs) (Amini et al., 2010), suggesting that access to market-based equity finance is easier for London-based firms. In addition to this London effect, AIM is characterised by a substantial concentration of financial firms, most of which are located in or around London. Given the relatively lower costs of start-up in financial firms, and the understanding or acceptance of these types of businesses by London-based investors, many of these IPOs are very young businesses 1 which are neither as successful nor as profitable 2 as their regional counterparts.

Prior research on AIM IPO failure (Espenlaub et al., 2012; Gerakos et al., 2011; Kashefi-Pour and Lasfer, 2011) has failed to take into account the London dominance of AIM and its concentration of financial firms in explaining the failure probability of British firms listed on AIM. However, evidence suggests that London dominates the UK economy in various forms (for example, see Department for Business, Enterprise and Regulatory Reform, 2008) and hence, we expect that the failure profile of AIM listed firms is affected also by the London dominance of AIM and its concentration of financial firms. Therefore, this research note offers a critical contribution to the small IPO failure literature in the UK through investigating the relevance of spatial proximity to London and being in the financial services in explaining the failure rate on AIM. Consistent with several studies addressing IPO failure (Audretsch and Lehmann, 2005; Carpentier and Suret, 2011; Demers and Joos, 2007; Hensler et al., 1997; Jain and Kini, 2000; Jain and Martin, 2005; Weber and Willenborg, 2003), we consider failure as the following:

all companies whose stocks were delisted by the London Stock Exchange (LSE) due to non-compliance with AIM rules;

all cancellations made at the request of the companies;

failed companies due to dissolution or being in administration; and

any company that is used as a shell for a reverse takeover.

In other words, this covers all delistings from AIM other than graduation to the Main Market, which are considered successful according to Carpentier and Suret (2011). The rationale behind this definition is that in the context of IPOs, where public shareholders are involved, investors are left with shares of questionable value when the firm is no longer on the market. However, given the literature on the difference between business failure and closure (see for example, Bates, 2005; Headd, 2003; Shepherd and Wiklund, 2006) we replicate the analysis without those firms cancelled at the request of the company and find that the results remain virtually unchanged. 3 Using a sample comprising the population of all the British companies listed on AIM from its launch in June 1995 until the end of 2004 (which are then tracked until the end of 2009), we establish the actual failure rate of British IPOs on AIM. We then analyse whether proximity to London, being in the financial sector or the interaction of these two effects contribute toward the high failure rate observed on AIM.

The remainder of this research note is organised as follows. The next section reviews previous studies on IPO failure. Then, method, data and research questions are presented, followed by the empirical results. The final section presents the conclusions.

Related literature

Empirical studies investigating IPO firms’ ability to survive are relatively limited and mainly concern large IPOs in the USA. Contemporary evidence on this suggests a number of factors influencing IPO ability to survive in the aftermarket, such as size, age, initial returns, industrial sector, insider ownership, profitability, liquidity, state of the market, venture capitalist participation and the prestige of underwriters (Bhabra and Pettway, 2003; Carpentier and Suret, 2011; Demers and Joos, 2007; Espenlaub et al., 2012; Hensler et al., 1997; Howton, 2006; Jain and Kini, 1999, 2000; Jain and Martin, 2005; Jain et al., 2008; Platt, 1995; Schultz, 1993; van der Goot et al., 2009; Weber and Willenborg, 2003).

Although there are fewer studies investigating the failure of small IPOs (see Bradley et al., 2006; Brau and Osteryoung, 2001; Seguin and Smoller, 1997; Weber and Willenborg, 2003 for US evidence), a considerable number do focus on non-US IPOs. More specifically, Audretsch and Lehmann (2005) investigate the effect of ownership on young and high-tech IPO firms using a dataset of German IPOs listed on the Neuer Markt from 1997 to 2002. They find that chief executive officer ownership does not affect firm survival after controlling for human capital knowledge and intellectual property of the firm. Carpentier and Suret (2011) analyse the survival and success of Canadian penny stock IPOs from 1986 to 2003, reporting that the failure rate of their sample is lower than the failure rate of large US IPOs. It was also found that survival probability is lower for issuers with no revenue or negative earnings; moreover, they document that firm characteristics at the IPO are significantly associated with IPO ability to survive. More recently, a few studies have focused on the UK AIM market. Gerakos et al. (2011) compare AIM IPOs listed between 1995 and 2008 with IPOs listed on other regulated exchanges, and suggest that failure probability is higher for firms listed on AIM compared to firms on NASDAQ, the LSE Main Market and Over-the-Counter Bulletin Board (OTCBB). Kashefi-Pour and Lasfer (2011) study the impact of debt financing on the voluntary delisting decision of non-financial AIM IPOs, using data from 1995 to 2009 suggesting that delisting probability is higher for IPOs with higher leverage and lower growth opportunities. Finally, Espenlaub et al. (2012) investigate IPO survival on AIM by focusing on the impact of the reputation of IPO advisers (known as the ‘Nominated Adviser’ – ‘Nomad’). They examine all IPOs (domestic and foreign) listed on AIM from 1995 till 2004 and find that IPOs backed by reputable Nomads survive longer.

Given the longstanding view in the UK that regional location plays a significant role in the entrepreneurial activity of small firms (see for example, Anayadike-Danes and Hart, 2006), and that AIM seemingly has a London effect which interacts with its financial sector effect, this research note extends the literature on small IPO failure in the UK through considering the relevance of being close to London and in the financial services sector in explaining the failure probability of British AIM IPOs.

Method

Sample

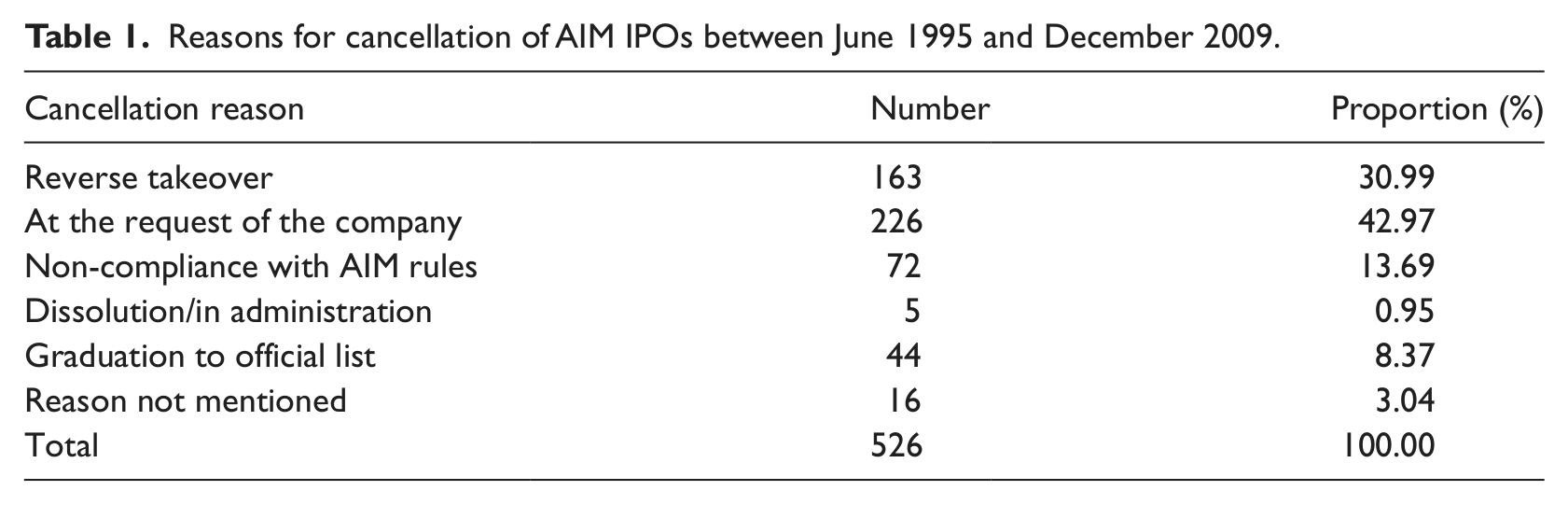

The initial sample of this study is the population of British companies that went public on AIM from June 1995 to the end of 2004. The start date of 1995 is when the market was established, and the end date of 2004 was chosen to allow a sufficient period (five years) to track potential failures until the end of 2009. The initial sample consists of 732 British companies which have their main base of operation in the UK. However, after excluding 11 companies with missing data, the final sample is reduced to 721 IPOs. We hand-checked the status of the sample IPOs at 31 December 2009 to identify whether the firms were still listed; for each of the delisted stocks, we identify the date and reason of the cancellation and the various reasons given are shown in Table 1.

Reasons for cancellation of AIM IPOs between June 1995 and December 2009.

Table 1 suggests that the most likely reason for the cancellation of an AIM IPO is at the request of the company. Table 1 also shows that 44 of the cancellations (8.3%) are due to graduation to the official list of the LSE. These firms are the most successful firms that have taken advantage of the AIM environment in order to grow and achieve a listing on the Main Market, and therefore are not considered to be failures. 4

Characteristics of the sample

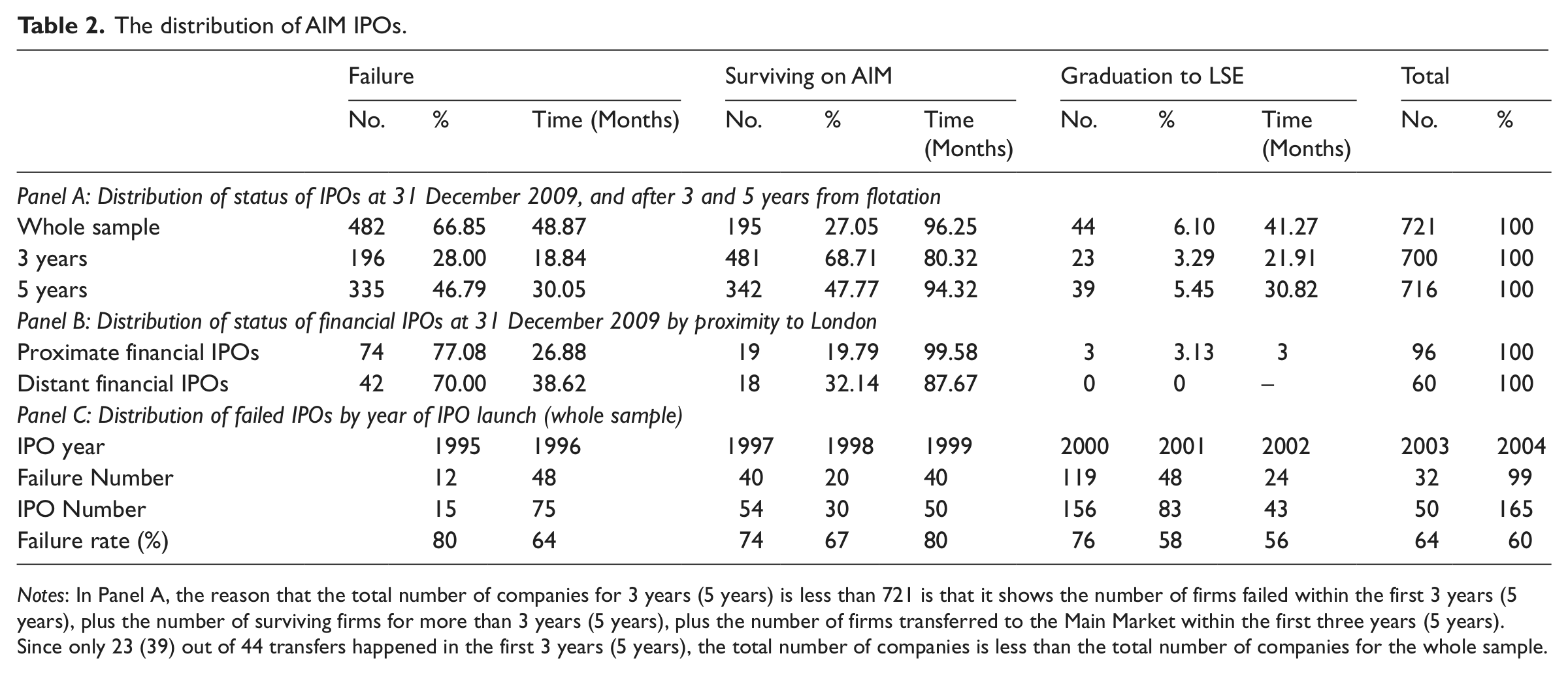

Table 2, Panel A, presents the distribution of the status of the IPOs at 31 December 2009, and after three and five years from flotation. Overall, 66.8 percent of the sample experienced failure, a proportion of 27 percent of IPOs remained listed on AIM, and 6.1 percent of the IPO firms graduated to the Main Market. The presented results suggest that the failure rate of small British IPOs is substantially higher than the failure rate reported for small IPOs in the USA(40.5%) by Fama and French (2004), and for small IPOs in Canada (48.5%) by Carpentier and Suret (2011). Moreover, the three-year failure rate of the sample (28%) is slightly lower than the corresponding failure rate of 31.5 percent documented for small US IPOs (Bradley et al., 2006). However, with respect to the five-year failure rate, we observe that almost half of the firms going public on the AIM market experienced failure within five years. This failure rate is considerably higher than that reported for small firms in the USA: that is, the 37.4 percent failure rate after five years reported by Seguin and Smoller (1997), and the 25.3 percent failure rate after four years reported by Weber and Willenborg (2003). This rate is also much higher than the five-year failure rate for small IPOs in Canada, equal to 11.6 percent, reported by Carpentier and Suret (2011).

The distribution of AIM IPOs.

Notes: In Panel A, the reason that the total number of companies for 3 years (5 years) is less than 721 is that it shows the number of firms failed within the first 3 years (5 years), plus the number of surviving firms for more than 3 years (5 years), plus the number of firms transferred to the Main Market within the first three years (5 years). Since only 23 (39) out of 44 transfers happened in the first 3 years (5 years), the total number of companies is less than the total number of companies for the whole sample.

Panel B of Table 2 shows the distribution of the status of the financial IPOs at 31 December 2009 by proximity to London. It shows that the failure rate of the financial IPOs located in or around London (77.1%) is higher than the failure rate of the distant financial IPOs (70%). Panel B also suggests that proximate financial IPOs have a lower average time to failure. Moreover, a higher proportion of the distant financial IPOs remained listed on AIM (32.1% versus 19.7%) at the end of the study period. Overall, the results in Panel B suggest that financial services firms proximate to London are of a lower quality compared to those financial firms distant from London.

Panel C of Table 2 shows the distribution of the failed IPOs by year of IPO launch. It shows that the highest failure rate by year is for firms going public in 1995 and 1999. More specifically, 80 percent of IPOs taking place in 1995 and 1999 failed by the end of the study period. Panel C also suggests that the lowest failure rate by year is for IPOs in 2002, with 56 percent experiencing failure by the end of the study period.

Research questions

Given the London dominance of the UK economy and based on the current evidence that IPO activity on AIM has a London effect (Amini et al., 2010), we expect that spatial proximity to London plays a role in explaining the failure probability of AIM listed firms. More specifically, we expect lower-quality firms to go public in or near London, which then experience a higher failure probability. This can be explained by supply and demand arguments: the former suggests that access to equity finance is easier for firms located closer to London because there are more potential investors in the London area which prefer to trade in firm stocks with a close geographical proximity (Coval and Moskowitz, 1999; Grinblatt and Keloharju, 2001). Moreover, there are lower tangible and intangible costs (transaction costs, liquidity costs and information asymmetry costs) faced by London proximate firms choosing the IPO route (Wójcik, 2009). Hence, given potential investor preference for firms in proximity to London and the lower costs they encounter, supply of equity finance is provided more easily for these firms. Consequently, we expect that London proximate firms on AIM are of a lower quality compared to more distant IPOs. This is because easier access to equity finance encourages more flotations in the London area, whereas distant firms experience more difficulty in raising equity capital due to a shortage of the supply of equity finance; only the higher quality ones, which are more confident in attracting potential investors or managing higher costs, choose a London listing.

By contrast, demand arguments suggest that of the firms that are distant from London, only the stronger ones with consistent growth rates will choose a London listing. For example, due to the lack of a demonstration effect, only those firms with a better awareness of entrepreneurs of other sources of finance choose to go public. Both of the above arguments suggest a relatively higher quality for distant firms compared to London-based firms. Given the above, we suggest that whatever the reason (supply or demand), lower-quality firms based in or around London chose to pursue IPOs, and hence hypothesise that firms closer to London experience a higher failure rate on AIM.

Furthermore, AIM is characterised by a significant concentration of financial firms (financial is the most dominant sector on AIM, accounting for 21.6 percent of the sample IPOs), with the majority of them being located in or around London (of the 156 financial IPOs in the sample 96 [62%] are within 50km of the LSE). In addition, financial firms account for a major part of AIM failures (of the 482 failures observed in the current sample, 116 [24.1%] are financial firms). Given the above, and the fact that AIM has a London effect (London accounts for 39.5 percent of AIM IPOs and 42.9 percent of its failures), which interacts with its financial sector effect, we also hypothesise that financial services firms closer to London experience a higher failure rate. More specifically, this research note is focused to answer the following research questions:

RQ1: Do IPO firms closer to London experience a higher failure rate after flotation? RQ2: Do financial services firms closer to London experience a higher failure rate after flotation?

Procedure

In order to answer the above research questions we investigated the failure of British AIM IPOs by estimating survival using the Cox Proportional Hazards (CPH) model. The CPH model has been used in existing research to model the failure probability of IPOs (for example, see Carpentier and Suret, 2011; Jain and Kini; 2000; Jain and Martin, 2005; van der Goot et al., 2009). The major advantage of the CPH model is that there is no assumption about the distribution of the baseline hazard function; hence, the model is semi-parametric and there is no need to make any assumption about the underlying distribution of the data (Carpentier and Suret, 2011). The dependent variable in the CPH model is the hazard rate that influences the occurrence and timing of failure (LeClere, 2000) and represents the conditional probability of failure, given that the firm has survived until the end of the study period. More specifically, the CPH model is expressed as follows:

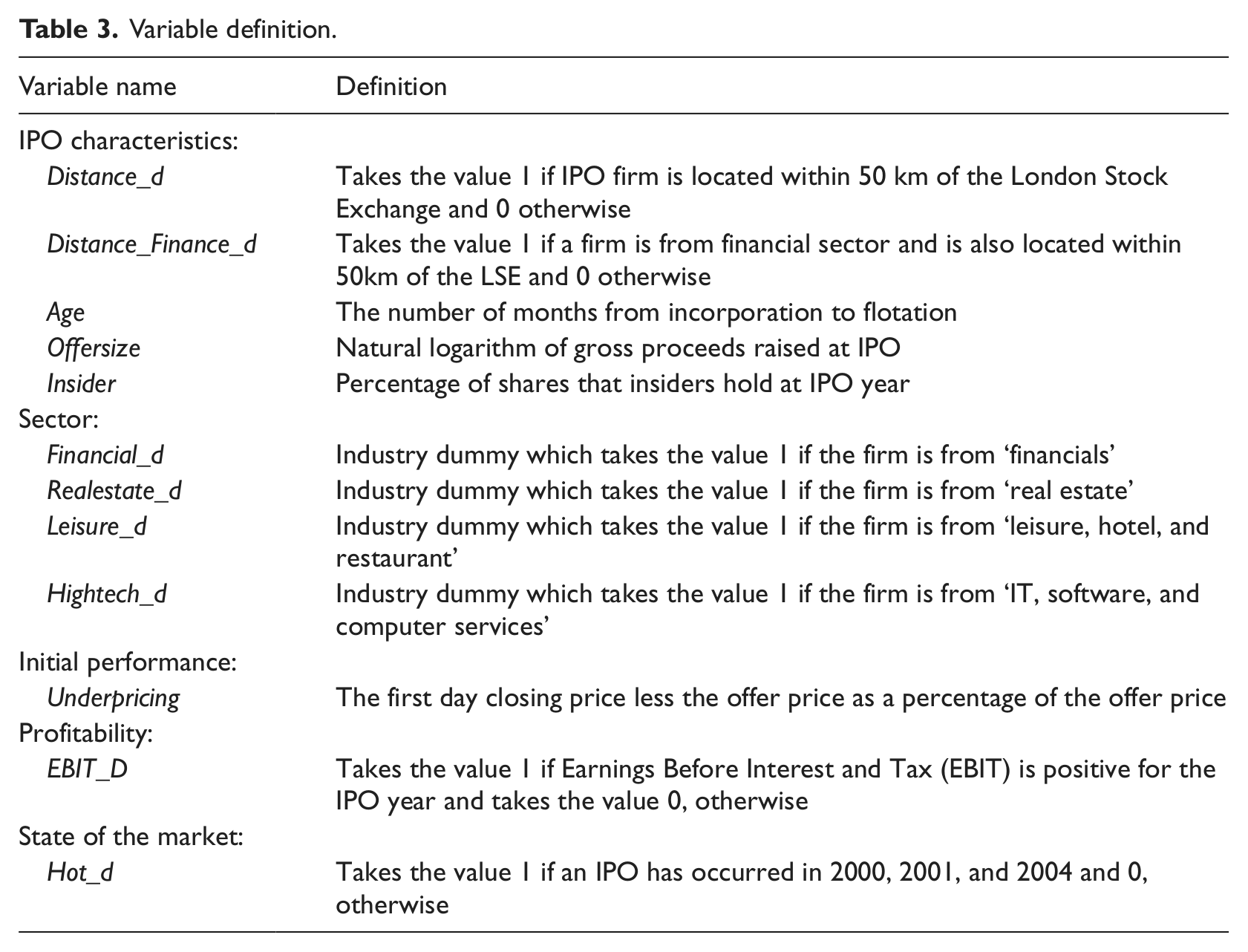

where h(t | X) is the conditional failure rate for an IPO firm with characteristics X (the probability of failure during a very small time interval, assuming that the firm has survived to the beginning of the interval (Jain and Kini 2000), h0(t) is the baseline hazard, t is the duration until the date of occurrence of failure, X is the vector of independent variables (covariates), and β is the vector of unknown regression parameters. The independent variables (covariates) are defined in Table 3.

Variable definition.

Results

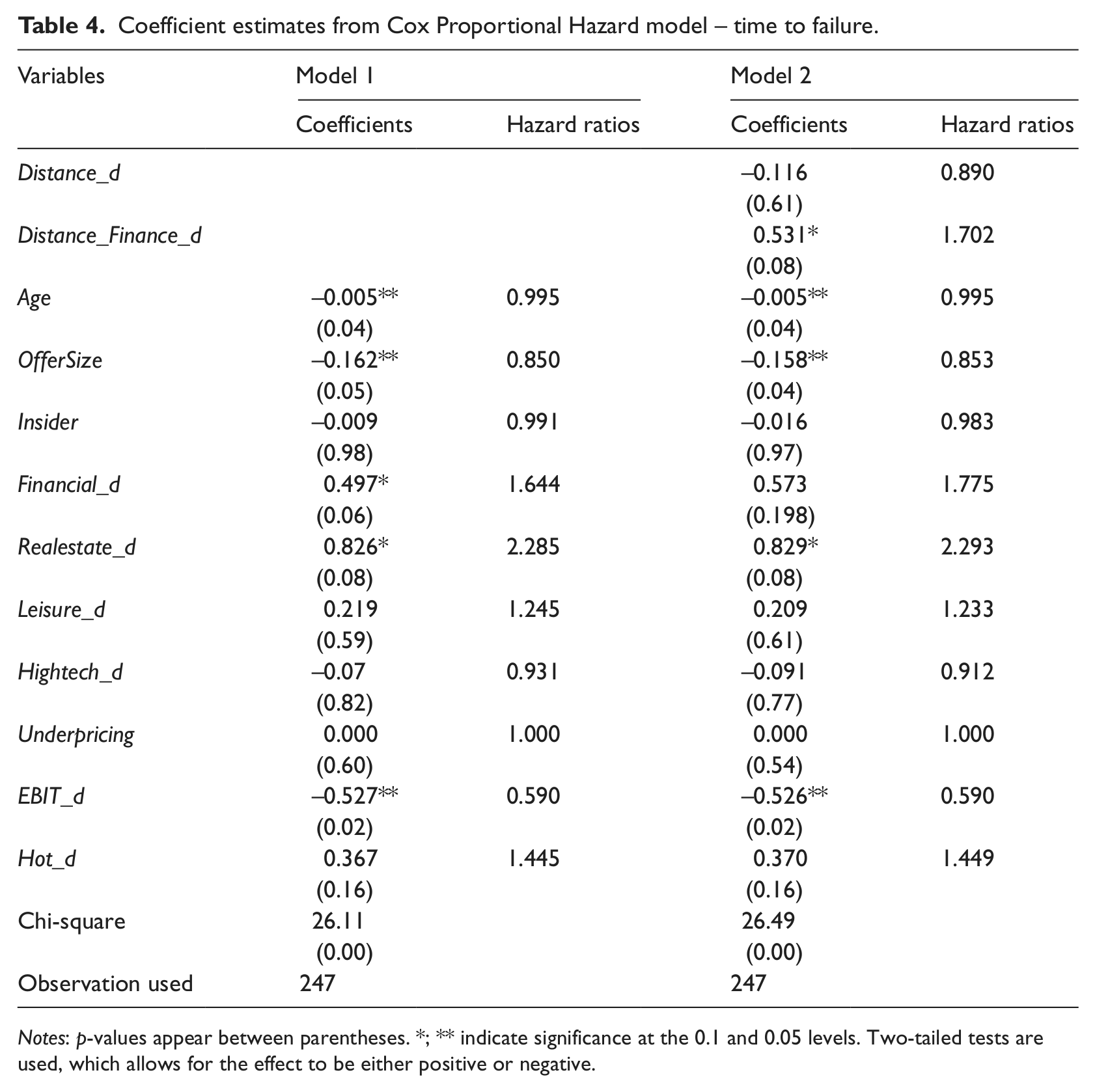

The results of the estimated CPH model are presented in Table 4. The table includes two models. Model 1 includes the conventional variables used in predicting the failure probability of IPOs. 5 Model 2 incorporates two new variables to examine whether proximity to London and being in the financial sector have any additional explanatory power in estimating the failure probability of small British IPOs on AIM. More specifically, in order to answer the research questions developed earlier, Model 2 incorporates two new variables, Distance_d, a dummy with a value of 1 for firms within 50km of the LSE, and Distance_Finance, a dummy with a value of 1 for financial firms within 50km of the LSE. Table 4 also reports hazard ratios (defined as the exponential of the regression coefficient) that measure the effect of a one unit increase in a covariate on the hazard rate. 6 The Chi-squares statistic shows that both models are highly significant.

Coefficient estimates from Cox Proportional Hazard model – time to failure.

Notes: p-values appear between parentheses. *; ** indicate significance at the 0.1 and 0.05 levels. Two-tailed tests are used, which allows for the effect to be either positive or negative.

Model 1 suggests that firms’ characteristics at IPO significantly affect their failure rate, with age, offer size and a positive Earnings Before Interest and Tax (EBIT) at IPO decreasing, and being in the financial and real estate sectors increasing, the probability of failure. The negative relationship between age or size and failure probability is consistent with the current evidence on IPO ability to survive (such as Espenlaub et al., 2012; Hensler et al., 1997; Jain et al., 2008). Moreover, the lower failure probability documented for firms with positive earnings at the time of IPO is in line with Carpentier and Suret’s (2011) findings on Canadian small IPOs, which suggest that failure probability is higher for IPOs with no revenue or negative earnings.

Regarding the relationship between spatial proximity to the LSE and failure probability, the results in Model 2 show that failure probability is higher for financial services firms located within 50km of the LSE. The hazard rate for Distance_Finance_d (1.702) suggests that the failure risk of financial IPOs within 50km of the LSE is 170.2 percent of the failure risk of other IPOs. The positive effect of Distance_Finance_d on failure probability is in line with the arguments developed earlier, supporting our second hypothesis that given the interaction of the London effect and the financial sector effect of the AIM, financial services firms closer to London experience a higher failure rate. However, Distance_d itself is not significant, suggesting that mere proximity to the LSE does not directly influence the failure probability of small British IPOs. Hence, it is the interaction of being close to London and being in the financial sector that increases the failure probability on AIM.

Comparing the results presented in Model 1 and Model 2, it is seen that after including the two new explanatory variables, Distance-d and Distance-Finance-d, in our estimation Financial_d is no longer significant. This suggests that the positive relationship between failure probability and being in the financial sector is significant only for financial firms proximate to London. Overall, the results of the CPH model reported in Table 4 provide a positive answer to RQ2, suggesting that financial services firms closer to London experience a higher failure probability.

Conclusion

Since the late 1980s there have been several attempts by policymakers in the UK to narrow the small firm equity gap, with the establishment of AIM in 1995 being seen as a partial solution to this problem. However, recent evidence suggests that AIM is dominated by London-based IPOs (Amini et al., 2010) and hence, it seems that access to market-based equity finance is provided more easily to these firms. Another distinguishing feature of AIM being a significant presence of financial firms, most of which are located in or around London. Given the fact that AIM has a London effect which interacts with its financial sector effect, there is a suspicion that these two effects also should be present in explaining the failure rate of the British firms listed on AIM. However, current evidence on IPO survival on AIM (Espenlaub et al., 2012) has failed to take into account these effects.

Therefore, this study contributes to the small firm finance and the IPO failure literatures through analysing the relevance of spatial proximity to London and being in the financial services in explaining the failure of small British firms listed on AIM. Using a sample comprising the population of all the British companies that were listed on AIM from the time that it was first launched in June 1995 until the end of 2004 (tracked until the end of 2009), we have documented that the failure rate of the British IPOs on AIM is equal to 66.8 percent as of 31 December 2009. We then investigated the effect of proximity to London, as well as the interaction of proximity and being in the financial sector, in order to model the failure probability of British IPOs on AIM. The presented results suggest that failure probability increases for the financial firms located within 50km of the LSE. As stated previously, according to our supply and demand arguments, this can be driven by quality issues, namely that lower quality firms go public in or near London which then experience a higher failure probability. However, there could be other factors associated with the differential failure rates in London versus non-London-based financial services firms: for example, business risk issues might play a part. More specifically, London-based financial service firms could have a considerably different business profile to their regional non-London based counterparts. It is conceivable that financial services firms in London may engage in riskier financial products, and consequently be more internationally focused. This would suggest a greater range of business risk factors and therefore, an inherently higher risk of failure. In contrast, financial services firms distant from London may be more strongly associated with more conventional areas, such as financial planning and insurance, and be domestically or even regionally focused (within the UK). Regional firms wishing to diversify product lines and/or internationalise may need to be closer to research analysts and global clients or partners and so, may relocate to London prior to AIM IPO. An additional factor which can play a role in explaining the higher failure probability of London-based financial services firms might be a difference in the quality of Nomads associated with proximate and distant financial IPOs. According to Espenlaub et al. (2012), IPOs backed by reputable Nomads survive longer. Therefore, higher failure rate of proximate financial firms also might be partly affected by a difference in the quality of Nomads.

Overall, the results provide implications regarding the observed higher failure rate of small British IPOs on AIM, compared to the failure rate of small IPOs elsewhere (Canada and the USA, in particular). As stated earlier, AIM is characterised by a significant concentration of financial firms, of which many (72%) are within 50km of the LSE. Given the result that failure probability increases for financial firms proximate to London, part of the higher failure rate of British IPOs on AIM can be explained by the London dominance of AIM, which favours the rise of financial sector businesses that manage to achieve an IPO. The least we can learn from the above is that investors should be more cautious with London-based IPOs active in the financial sector.

Footnotes

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.