Abstract

This paper analyses the Sustainable Development Goals of the United Nations in the 2030 ‘Transforming the World’ Agenda, from 2015, as a contribution to business ethics and ethical economy. The Sustainable Development Goals combine political aims with visions of economic development and social justice and are therefore important for business ethics and corporate social responsibility. Thus, the Sustainable Development Goals constitute a driver for ethical economic development and social change. However, there is a need for critical analysis of the possibilities of Sustainable Development Goals of functioning as a vision and a strategic tool for management and governance. The aim of the paper is to investigate these possibilities of the Sustainable Development Goals of contributing to business ethics and ethical economy with mobilization of business, public institutions and organizations, and non-governmental organizations. After presenting the Sustainable Development Goals, the paper critically discusses their scope and potential for corporate social responsibility, business ethics and corporate sustainability. This involves the problem of how the Sustainable Development Goals can contribute to a transformation towards another economy. As a contribution to business ethics, the paper elaborates on partnerships for Sustainable Development Goals, sustainable performance management systems and the Sustainable Development Goal Compass with the aim of interpreting Sustainable Development Goals as a basis for progressive business ethics models.

Keywords

Introduction

The Sustainable Development Goals (SDGs) of the United Nations in the 2030 ‘Transforming the World’ Agenda (United Nations, 2018a), from 2015, can be interpreted as a contribution to localization of the global economy. The SDGs combine political aims with visions of economic development and social justice (Hildebrandt, 2016; Sachs, 2012, 2015). In this sense, the SDGs constitute a driver for local economic development and social change in private business, NGOs and public organizations and institutions. However, there is a need for critical analysis of the possibilities of SDGs of functioning as a vision and a strategic tool for interdisciplinary economic development and for management of business and public organizations and institutions for economic development and urban regeneration. The aim of the SDGs is to be an instrument for economic development and regeneration, contributing to economic empowerment and social and political change. In this article, the goal is to investigate these possibilities of the SDGs of contributing to social innovation of the economy with mobilization of business, public organizations and institutions, and NGOs.

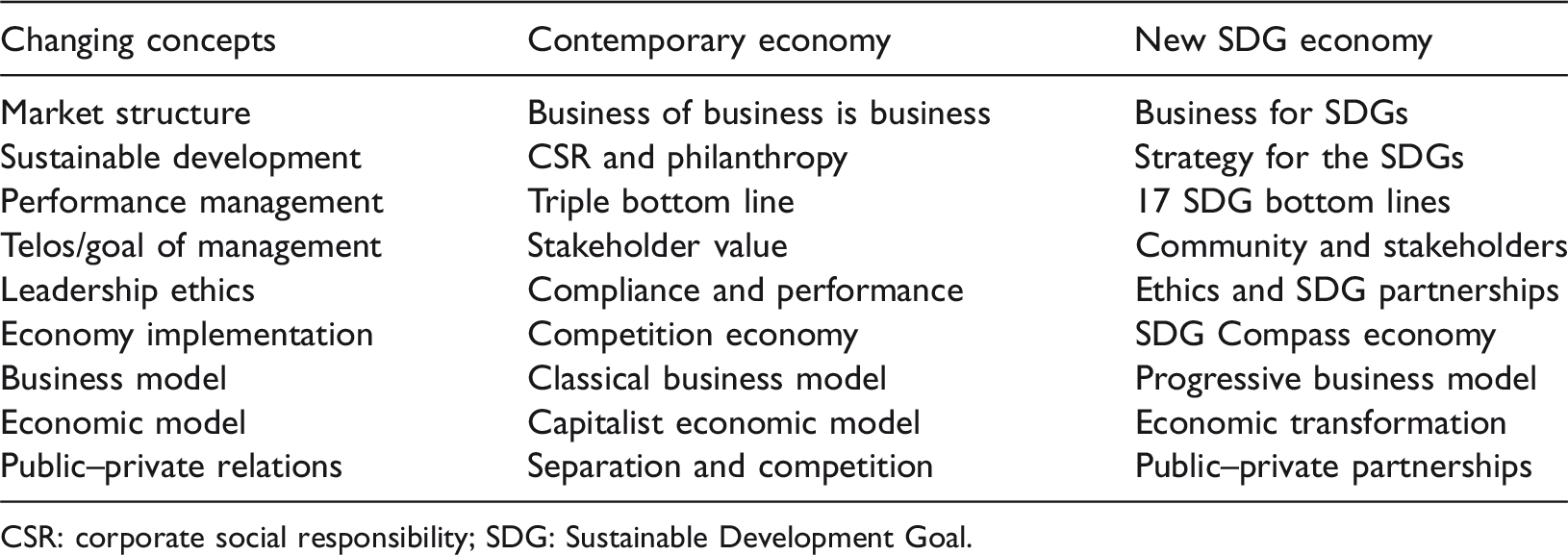

Thus, the SDGs serve as a framework for a new development of business ethics, corporate social responsibility (CSR) and corporate citizenship (Van Zanten and Van Tulder, 2018). We move from the triple bottom line of people, planet and profit to the 17 bottom lines of the SDGs and business organization, public organization or institution need to have visions and values related to all these goals and their corresponding targets (Rendtorff, 2018). The SDGs imply a new conception of the business corporation contributing to political and environmental goals of the development of the international community, which applies locally to develop an ethical economy. With this development, the SDGs constitute a major framework for a new global economy, making the global local and changing the relation between global capitalism and local economy. Accordingly, we can see the SDGs as a framework for developing new progressive business models with regard to large, small and medium-sized enterprises in the local and global community (Rendtorff, 2018; Székely and Knirsch, 2005).

We can illustrate this transformation from CSR and business ethics to SDGs and progressive business models in private business, NGOs and public organizations and institutions with Table 1.

Transformation from CSR and business ethics to SDGs and progressive business models.

CSR: corporate social responsibility; SDG: Sustainable Development Goal.

Accordingly, the paper presents this transformation of business strategy both in private business and in public organizations and institutions for the SDGs in order to discuss what kind of progressive business models for a transformation of the relation between global and local economy this implies (Hildebrandt, 2016; O’Higgins and Zsolnai, 2017; Rendtorff, 2015, 2018). Here, it is important to present the SDGs in relation to concepts and visions of global and local business ethics, CSR and corporate citizenship (Dyllick and Hockerts, 2002; Marrewijk, 2003; Montiel, 2008).

Thus, the paper consists of the following main sections. Introduction; From the Millennium Goals to the SDGs; Need for transformative leadership towards sustainability; From sustainable development to corporate sustainability; SDGs and the transformation towards another economy; Partnerships for the SDGs; SDGs and performance management systems; The SDG Compass: A tool for SDG management; A case example: Carlsberg Group; Conclusion: SDGs and progressive business models.

From the Millennium Goals to the SDGs

The SDGs of the Transforming the World 2030 Agenda for Sustainable Development by the United Nations (2018a) follows up on the Millennium Development Goals of the UN from 2000, which were considered important goals for the world community to be achieved by the states. The SDGs are much more detailed and they were adopted by the 193 member states of the UN, which continues the consensus of the Millennium Goals, but engages society as such more broadly, including governments, businesses, NGOs and civil society. There are 17 SDGs and they are specified with 169 sub-targets which together focus on people, planet and prosperity (United Nations, 2018a). The private sector, businesses and public organizations and institutions are essential for realizing the SDG Agenda for transforming the world by 2030. The United Nations (2018b) integrates the SDGs with its other activities directed towards businesses – including business for human rights, the UN Global Compact, the World Business Council for Sustainable Development and the world business initiative for sustainable reporting – in its efforts to motivate businesses to contribute to sustainable development. With this, we can say that the SDGs have become the major focus of developing a locally embedded and sustainable economy to deal with global and universal movements of capitalism and growth.

The comprehensive and holistic dimension of the SDGs can be demonstrated by the fact that they contain nine more goals than the Millennium Goals, with 17 goals and 169 targets. The 17 goals concern the following topics: 1. No Poverty; 2. Zero Hunger; 3. Good Health and Well-Being; 4. Quality Education; 5. Gender Equality; 6. Clean Water and Sanitation; 7. Affordable and Clean Energy; 8. Decent Work and Economic Growth; 9. Industry, Innovation and Infrastructure; 10. Reduced Inequalities; 11. Sustainable Cities and Communities; 12. Responsible Consumption and Production; 13. Climate Action; 14. Life Below Water; 15. Life on Land; 16. Peace, Justice and Strong Institutions; 17. Partnerships for the Goals (United Nations, 2018a). With this, we see that the SDGs are very comprehensive and aim at social change in local economies. Moreover, the SDGs cover more than earlier goals for sustainability in general in the sense that they add prosperity, peace and partnerships to people, planet and profit, which is particularly relevant for businesses. Indeed, the concept of economic growth is very relevant for the SDGs that combine concern for the environment with the idea of prosperity and economic growth.

Need for transformative leadership towards sustainability

An important challenge for businesses, NGOs and public organizations and institutions now is to translate and realize the SDGs. They must realize SDGs in their vision and mission, business strategy, value chain, stakeholder management and in relation to their environment in order to create a strong transformation towards sustainability (Becker, 2006; D’Alisa et al., 2014; Daly, 1994, 1999; Ingebrigtsen and Jakobsen, 2006; Nielsen, 2013, 2015; Rendtorff, 2009, 2018; Sagoff, 1988). We can consider this as the major challenge of developing a new relation between global business goals and local economies of sustainability, and businesses face this challenge as an integration of business activities in the community. We can call this a search for new progressive business models and new strategies and practices for sustainable development. For businesses, the ultimate question is how they relate to the SDGs and what they can do to overcome eventual gaps between the reality of business and visions of the SDGs (Kremer and Biesheuvel, 2017). A further question is what companies and public organizations and institutions can do to overcome the gaps and what barriers they face in order to comply and align with the SDG gaps (Kremer and Biesheuvel, 2017: 3–4). Here, companies need to work actively with the SDGs and embed them in their daily, local business practice.

A new progressive business model for the SDGs involves this question of what a company can do to align and comply with the SDGs (O’Higgins and Zsolnai, 2017). A progressive business model can be defined as a concept of business that combines economic earnings and profits with genuine social and environmental sustainability. A progressive business model needs to go beyond distinctions between profit and non-profit, shareholders and stakeholders, market and non-market, social economy and market economy, open and closed organization, politics and economics and thereby embed its business activities in the social fabric of society. This can be combined with social innovation and social entrepreneurship, contributing to new visions and ideas of embedding sustainability in business life (O’Higgins and Zsolnai, 2017). The problem is what the company can do to overcome the traditional concept of business as directed towards individual benefit, by contributing to create value for business and society at the same time. This progressive model would involve suggestions for strategies and performance instruments to be in accordance with the SDGs and be more sustainable.

The focus on new progressive business models for the SDGs involves reflecting on the possibility of new models for measuring sustainability performance of global reporting in relation to the SDGs. In many cases, the problem is not least the conceptual discussion of the theoretical dimensions of progressive business models (O’Higgins and Zsolnai, 2017). Rather, the challenge is to embed and realize progressive business models in the sustainability practice of the corporation. This also contributes to the understanding of how businesses and private contributions can contribute to the realization of the SDGs (Verboven and Vanherck, 2016). The new SDG Agenda is directed towards partnerships between the public and the private sectors, and businesses play a pivotal role in these partnerships for realizing the SDGs.

There have been many criticisms of the concept of sustainable development. Critical voices see the concept of SDGs as ‘sustainability-washing’ (Buhmann, 2018), where the Western world wants to defend their conception of the world without taking into account the point of view of developing countries (Kremer and Biesheuvel, 2017: 8). A basic criticism is that the defence of sustainability is an argument for a ‘green capitalism’, a concept of green growth that implies a neo-liberal conception of the economy that has nothing to do with sustainability.

Indeed, the SDGs raise a lot of questions as continuation of the Millennium Goals. How do the SDGs relate to the Millennium Goals and how can they be conceived as a further development of the Millennium Goals? Many questions emerge in relation to the shape and framework of the SDGs. How can we prioritize among the goals? Are the goals too ambitious and unrealistic? How is it really possible to eradicate poverty or combat climate change? Can the SDGs create human action or awareness, even when they appear very abstract and unrealistic? And can the SDGs really be universalized to be valid for all societies? And translated into the conceptualization of transformative leadership, we can ask: How does it change performance management? What is the telos/goal of management and leadership focusing on SDGs? How do we implement the new ethics of leadership in SDG management? How can the SDGs in private business and in public organizations and institutions improve public–private interaction for new partnerships? These are important questions if we want to embed the SDGs as progressive business models for local business practices in different societies everywhere in the world. To focus on these issues can help to develop real and authentic transformative leadership, where the SDGs represent the central vision for developing a new integration of local and global economy.

From sustainable development to corporate sustainability

The contemporary framework of corporate sustainability began with the Brundtland Commission Report from 1987 of which the SDGs are a later development (World Commission on Environment and Development, 1987). Already with the Brundtland Commission, the UN saw sustainable development as essential for survival of the planet. This was the new foundation of a progressive business model, where the ultimate goal of the business corporation is to serve society. Moreover, it gives a better focus for management of NGOs and of public organizations and institutions. The aim of sustainable development and concern for future generations was the survival of humanity on planet Earth. In 1997, the British consultancy theorist and practical sustainability manager John Elkington wrote the book Cannibals with Forks, in which he defined the triple bottom line focusing on people, planet and profit as an essential development of the UN sustainability framework (Elkington, 1997). Elkington (1997) saw as the aim of the sustainable corporation not only to perform on economic earnings, but also to focus on the social bottom line (including human rights) as well as the environmental bottom line (including concern for climate change). This idea of the triple bottom line represented an important effort to localize universal concepts of sustainability and the ideas of people, planet and profit in relation to the concept of sustainable development in the UN vision of the Millennium Goals and the SDGs.

In addition to Elkington’s theory of corporate sustainability based on the UN framework, Edward Freeman’s (1984) theory of stakeholder management represents a conceptual revolution of a progressive business model that contributes to conceptualizing the business model of corporate sustainability (see also Bonnafous-Boucher and Rendtorff, 2016). Stakeholder management represents a transformation of the way we think about value creation and it enables embedded value creation through cross-sector partnerships among business, public institutions and organizations, NGOs and civil society. The stakeholder management approach to value creation implies a combination between non-profit and profit-oriented purposes for the benefit of sustainable development of society. Indeed, the progressive business model of stakeholder management moves beyond conceiving business ethics as a theoretical narrative in contrast to the real life of profit and practical value creation.

With stakeholder management, companies have a social purpose of contributing to sustainable development and value creation of economic, social and ethical value. With this, Freeman (1984) emphasizes that for stakeholder management, value creation is relational (see also Bonnafous-Boucher and Rendtorff, 2016; Rendtorff, 2018). It is not about a cold exchange, but is based on mutuality and partnerships. Thus, Freeman distinguishes between transactions and relationships. Relationships are based on human values, caring and love, and this is the new dimension of socially embedded business and economics. As a relational activity, value creation for sustainability is based on stable relations through time.

Accordingly, stakeholder management emphasizes the social embeddedness of value creation for sustainability in the local community economy (Bonnafous-Boucher and Rendtorff, 2016; Freeman, 1984; Rendtorff, 2018). Value creations are embedded in social institutions and we create value in the context of community. It is here that stakeholder theory emphasizes trust and trust relations as essential for partnerships for sustainability. The economy has to take into account human complexity and value creation for sustainability among stakeholders built on authentic human relations, in which human beings respect, trust and care for each other. If the SDGs are to be integrated into the capitalist system of cooperation, it is important to be aware of the social dimension of relational values in business in a community of stakeholders.

SDGs and the transformation towards another economy

With the global challenge of protecting people, the planet and profits, in the framework of stakeholder management, the SDGs are meant to function as a catalyst for visions of new progressive and sustainable business models (Hildebrandt, 2016; O’Higgins and Zsolnai, 2017; Rendtorff, 2015, 2018). In this sense, the SDGs become a central part of theory development of CSR and corporate sustainability (Dyllick and Hockerts, 2002; Marrewijk, 2003; Montiel, 2008). Despite ambitions and hopes associated with the SDGs, researchers continue to warn against SDG-washing (Buhmann, 2018) and the risk of the SDGs becoming just superficial jargon for covering up malpractice (Van Zanten and Van Tulder, 2018) or leading to a narrow instrumental approach to the SDG indicators at the expense of reflective ethical reasoning.

Furthermore, critical approaches to dominant paradigms of economy, for example ecological economics (Costanza, 1991; Costanza et al., 1997, 2001; Daly, 1999) and solidarity economy (Dacheux and Goujon, 2011; Laville, 2010, 2015) point to the need for a fundamentally different understanding of economic activity in order to realize a transition towards sustainability (Becker, 2006; D’Alisa et al., 2014; Daly, 1994, 1999; Ingebrigtsen and Jakobsen, 2006; Nielsen, 2013, 2015; Rendtorff, 2014, 2017; Sagoff, 1988). Thus, we need a broader political economic contextualization of corporate responsibility and leadership in order to understand the conduct of businesses within a broader societal, political and economic frame. This is the basis for developing progressive business models for embedding SDGs in local economies.

In this context, embedding SDGs in business transitions towards sustainability in the philosophy of management and ethical leadership, CSR, corporate responsibility and sustainable economics is a theoretical and practical challenge for research and the practice of sustainable transition.

Research in ethical leadership in philosophy of management has been focusing on different traditions of leadership models of business ethics, including the ethical manager, organizational ethics, values-driven management and governance ethics in organizations (Brown and Treviño, 2006; Rendtorff, 2009, 2018; Scherer AG et al., 2014; Treviño, 1986; Treviño et al., 2000, 2003; Treviño LK and Brown ME 2005). The great challenge in research on ethical leadership now is to use this theory approach to develop an embedded concept of transformational SDG leadership in the transition towards sustainable development.

Research in CSR and sustainability has been focused on the triple bottom line (Elkington, 1997; Kashmanian et al., 2011; Norman and MacDonald, 2004) and on clarifying concepts of responsible business, e.g. political CSR (Rendtorff, 2018; Scherer and Palazzo, 2011), creating shared value (Porter and Kramer, 2003, 2006, 2011). Now this research must focus on the ‘gap frame’ of translating SDGs into embedded, institutional and collective responsibility in value-creating business cases (Hammoudeh, 2018, Hess, 2017; Hildebrandt, 2016; Muff et al., 2017; Nielsen, 2015; Rendtorff, 2018).

Investigations in ecological economics, as well as in sharing and circular economics, have been focusing on the transition towards sustainability (Nielsen, 2013). This is applied at the micro, meso and macro levels of society. But a deeper understanding of embedding sustainability in business management and economics is still under development (Baumgartner and Rauter, 2017). Moreover, the use of these economic theories to understand and analyse SDGs is still not accomplished. Focused research is therefore needed to understand SDGs and sustainable economics.

The aim of these economic theories of transition to sustainability is to develop theories and concepts of ethical leadership and CSR that specifically encompass concerns about sustainability (Rendtorff, 2009, 2013, 2014; Scherer and Palazzo, 2008, 2011). This is relevant both for private business and for public organizations and institutions. This involves, first of all, a study and categorization of the philosophies and paradigms of sustainability in philosophy of management, CSR and sustainable economics, such as positivistic, constructivist, deep ecological and Anthropocene perspectives. On the basis of this categorization, the implications for integration of sustainability concerns in ethical leadership, responsibility and political economics will be discussed. Thus, we can see how progressive business models in business organizations are necessary to deal with the potential challenges that arise in relation to contributing to sustainable development (Muff et al., 2017).

Partnerships for the SDGs

Such a formulation of SDGs in the framework of ecological economics, philosophy of management, stakeholder management, CSR and paradigms of ethical business can also be considered as the framework for theorizing about SDG partnerships. We have already seen how the SDGs enable a new progressive business model of relational stakeholder management in both private business and public organizations and institutions. This is indeed the foundation of partnerships for the SDGs (Bonnafous-Boucher and Rendtorff, 2016; Freeman, 1984).

The member countries of the United Nations (2018a) commit to realizing the SDGs with a focus on the responsibility of governments. However, it is important to emphasize that the concept of partnerships implies that governments go into global partnerships for the SDGs and also that they enter into partnership with businesses, NGOs and civil society. The concept of partnerships is accordingly essential for the SDGs and different kinds of partnerships are important for the achievement of the SDGs. Here, goal number 17, Partnerships for the SDGs, is very important as a goal that is different from the other goals since it refers to the multi-stakeholder process of meeting the goals and to the institutions, organizations and people involved that need to work together in order to realize the SDGs.

In contrast to the Millennium Goals that focused mostly on the states as responsible actors, it is important to emphasize that the SDGs relate more broadly to the involvement of businesses in working towards the goals and targets (United Nations, 2018a). The idea of the SDGs is that businesses are as responsible for sustainability as governments and other actors are. The business model should be based on sustainability; this means that businesses should follow the principles of sustainable development of the Brundtland Commission and John Elkington’s (1997) triple bottom line, while also integrating the visions of ecological economics, philosophy of management and ethical business in new visions of embedding SDGs in business practice (World Commission on Environment and Development, 1987).

With the SDGs, the international community proposes a multi-stakeholder approach to solve global and local problems. Therefore, the SDGs are on the agenda for governments, businesses and civil society. In this context, it is important to emphasize that the SDGs as such are also a result of multiple partnerships and interactions. NGOs, governments, business and civil society worked together to formulate the SDGs as ambitious as they are, and the UN’s diplomatic and political project of SDGs has been based on a collective process to form the SDGs as ambitious world goals.

Because of this interaction, the SDGs continue the process from the Rio Summit on sustainability in 1992 through the Millennium Goals to the formulation of the present world goals. It is important to be aware that this process has led to the fusion of environmental and climate goals in the present concept of the SDGs (United Nations, 2018a). This can indeed be considered as a result of the global and local partnership process that is behind the SDGs. The environmental and climate world goals are not treated as separate from the economic challenges that the world is facing. The partnership process behind the goals has been an integrated and open consultation process that resulted in such combined social and environmental goals for the world community.

Accordingly, the concept of partnerships is in itself behind the new vision of the SDGs. The process of formulating the goals has been complex and it is important to keep in mind the great complexity of the SDGs with the 17 goals and 169 targets. At the same time, it is important to remember that all countries of the UN adopted the 2030 SDG Agenda. Indeed, this answers the question of whether the goals are universal. They must be, since all countries have committed to the goals, which means that the SDGs cannot be reduced to a perspective for the developing world not including the rich countries. All countries and all sectors of society must be responsible. We cannot just export problems and issues from one sector to the other.

Thus, it can be argued that the ultimate aim of CSR and corporate citizenship is sustainable development realized with the SDGs through relational stakeholder management partnerships. In Europe, the EU Commission has conceptualized CSR as a voluntary effort closely linked to sustainability, but there has not been much specific advice about how to develop progressive business models for sustainability. However, with the SDGs together with other initiatives such as business for human rights, the Global Compact, Global Reporting Initiative and World Business Council for Sustainable Development, such a framework for a sustainable corporation emerges.

Indeed, the literature for CSR and stakeholder management makes a close link between sustainability and good corporate performance. Sustainability is considered as a good business case and business model that can be profitable for the company.

Applying stakeholder theory with its vision of relational partnerships among private business, NGOs and public organizations and institutions, it is possible to argue for a business model for sustainability (Bonnafous-Boucher and Rendtorff, 2016; Freeman, 1984; Rendtorff, 2018). Customers are increasingly focusing on ecological and more sustainable products. Employees want to have a meaningful job and be proud of their corporation in order to worker harder. Shareholders and investors consider sustainability as important for the future of the company, which can be considered prudent risk management. Governments and local community as well as NGO stakeholders also expect corporations to be responsible for sustainability and sustainable development and, by complying and aligning with this, a corporation can increase its social and political legitimacy in a specific society. This contributes to an increase in brand value and trustworthiness of the company in society, which is an argument for the business case of corporate sustainability.

SDGs and performance management systems

Thus, in theory there are many good arguments for integrating the SDGs in business management systems, both for private business and for public organizations and institutions. In fact, with John Elkington’s (1997) triple bottom line, a proposal for sustainability management in practice was already developed. The triple-bottom-line concept was applied to many companies, but it was also criticized for being unrealizable, because it was not very clear what it meant to work for many bottom lines at different times. Therefore, the arguments against Elkington were that better and practical sustainability performance management systems and models were needed.

In this context, the Global Reporting Initiative was an effort to develop an objective system of management and performance to improve sustainability. Other authors have also tried to develop practical models for measurement of sustainability in organizations. They have distinguished among different levels of implementation of strategies, from pre-compliance to compliance and beyond compliance to value- and passion-based approaches to compliance with sustainability.

Moreover, sustainability performance measurement is an approach that contributes to the realization of sustainability in the management of the firm (Kremer and Biesheuvel, 2017: 15). This field of research and practice comes from finance and accounting and the focus has been on developing instruments to measure the performance of the organization. The idea of the ‘performance management revolution’, with greater focus on the measurements of performance, was to consider performance as something broader than pure economic and financial performance. In a sense, this focus on performance develops Elkington’s focus on people, planet and profit to the idea of a broader measurement of the performance of business organizations.

In this context, the idea of the balanced scorecard, as developed by Kaplan and Northhouse, constitutes an important part of this effort to develop practical models of measurement of business performance as something broader than pure financial performance (Kremer and Biesheuvel, 2017). Accordingly, there is a vast literature on this basis, with efforts to develop systems of performance management. The literature focuses on measurement and on development of management systems that increase the performance of the company while, at the same time, being able to take into account a broader concept of performance than the traditional economic performance model.

A sustainability performance management system is a system to measure the performance of a company and evaluate the efficiency of this performance. With regard to a particular company, this system comprises all the indicators and measures that evaluate the performance of the company towards achieving the goal of sustainability. Together with the SDGs, it is a part of the Agenda for Sustainable Development to set up specific targets and measures to evaluate performance towards achieving the SDGs. Therefore, it is necessary to develop a system of measurement for the SDGs (Kremer and Biesheuvel, 2017: 23).

The SDG Compass: A tool for SDG management

The SDG Compass can also be considered as a management tool to embed and localize the SDGs for specific business purposes (United Nations, 2019). The SDG Compass was developed by the Global Reporting Initiative, as a tool for SDG reporting and an instrument to encourage organizations to work with the SDGs. This is an instrument for companies to integrate the SDGs in their activities. An important dimension of the SDG Compass is the measurement of sustainability performance, which companies use to develop a strategy for SDGs. This tool should contribute to create a new concept of the business strategy of the corporation, enabling the integration and embedding of the organization in the local economy.

Indeed, the SDG Compass also indicates the necessity of an SDG-performance management system in order to evaluate and measure the progress of specific companies towards realizing the SDGs (United Nations, 2019). Nevertheless, the development of a performance measurement system only comes after the realization of a strategy for the SDGs. Therefore, performance management systems presuppose strategy systems for the SDGs. Here, we can go into detail with a discussion of the SDG Compass.

So what is the SDG Compass? It is defined as a tool that gives the company tools and knowledge to integrate the SDGs as an element of its core strategy (United Nations, 2019). This tool has been created by the Global Compact, the World Business Council and the Global Reporting Initiative.

In contrast to the Millennium Goals, the SDG Compass explicitly emphasizes the role of businesses and corporations in contributing to sustainable development (United Nations, 2019). The SDG Compass states that businesses should identify innovative business opportunities based on the SDGs. The Compass focuses on the increased business value of sustainability, and the world goals can increase businesses’ motivation to use resources economically.

The SDGs increase business relations to stakeholders, and businesses are integrated into political and legal decision-making by following the SDGs (United Nations, 2019). By working on the SDGs, businesses can find better motivation from stakeholders. SDGs include businesses’ contribution to a better society, better markets, better financial institutions and institutions based on good governance and non-corruption. The SDGs create a common vision and goal for the future and integrate businesses in society in partnerships for common solutions.

A case example: Carlsberg Group

What does it mean in practice to work with the SDG Compass and to move from CSR to SDGs? We need case studies in order to illustrate the challenges, barriers and business possibilities of the SDGs. Here, the international Danish brewer Carlsberg Group represents an example of a corporation working strategically with the SDG Compass, trying to move from CSR to SDGs by placing the SDGs in the centre of its strategy. Carlsberg present climate change as a challenge that they want to deal with in their business strategy. This involves contributing to the transition towards a low-carbon economy (Carlsberg Group, 2019). Carlsberg has the high ambition of reaching a zero-carbon footprint by aligning with the Paris agreement goals. The challenge is whether this goal is too ambitious and whether Carlsberg can do this by 2030, and the business has formulated partial targets of a 30 and 50% switch to renewable electricity energy sources.

Similarly, the company is aiming at zero water waste (Carlsberg Group, 2019). Since a brewery is dependent on clean water, it is important to reduce water waste. The company has therefore formulated a target of reducing water waste to a minimum with 25% of present water use by 2022 and 50% by 2030. The company proposes partnerships to achieve this goal in cooperation and partnership with local public organizations and institutions and with NGOs.

Moreover, the company will work for zero irresponsible drinking, promoting a drinking culture where there is no irresponsible consumption (Carlsberg Group, 2019). It is in that context that the company promotes availability of alcohol-free beer and recommends consumers to be responsible when they drink.

Carlsberg also considers zero work accidents as a target, following the 2030 SDG Agenda. The company will work for a safe working environment and it wants to change its working culture so there are no accidents in the business. The targets following the SDG Compass are a strong reduction of accidents by 2022 and further reductions to zero by 2030 (Carlsberg Group, 2019).

If we look at the Carlsberg sustainability strategy, we can see that the SDGs are considered essential as the future transformative potential of the corporation. The SDGs constitute an important possibility for moving beyond a traditional strategy of ‘the business of business is business’ towards a strategy where business is business for the SDGs. In this new strategy, CSR is not only philanthropy, but integrated in the strategy for the SDGs, and this strategy combines business and SDGs. In performance management, Carlsberg faces the difficult move of going from the triple bottom line to the 17 SDG bottom lines. This is difficult and Carlsberg has selected the issues of CO2 emissions, water waste, no irresponsible drinking and zero work accidents as some of the bottom lines, but the corporation has to work more to face all 17 SDG bottom lines.

Nevertheless, the focus on the telos of management moving from stakeholder value to community value is clear in the leadership ethics of Carlsberg moving from compliance and performance towards an ethics of SDG partnerships. With this SDG Compass economy, Carlsberg also moves from a classical business model towards a much more progressive business model. There is an economic transformation towards a community economy where Carlsberg acts as a responsible corporate citizen in public–private partnerships. The challenge of Carlsberg is to prove that this ambitious strategy is more than SDG-washing. Zero carbon emission, zero water waste, zero irresponsible drinking and zero work accidents are all very promising targets, but also extremely hard to achieve. Moreover, these targets are only some of the many targets that the company could focus on in order to comply with the SDGs.

Conclusion: SDGs and progressive business models

In conclusion, we can summarize the argument of this paper as follows. We began by presenting the SDGs in the 2030 ‘Transforming our World’ Agenda of the United Nations as a vision for progressive business models for integrating local and global economy. The paper has demonstrated how there is a continuous development of the concept of sustainable development from the Brundtland Report in 1987, through the Rio Declaration in 1992 and the Millennium Goals in 2000 to the SDGs in 2015. This has contributed to creating the basis for a sustainable stakeholder economy, enabling a transformation of capitalist economics towards a more ecologically oriented solidarity economics. Even though the paper also touched upon some difficulties and barriers to realizing a sustainable economics, it also showed the possibilities and potentialities of the SDGs as the basis for corporate sustainability management and new progressive business models, whether for private business, NGOs, or public organizations and institutions. With this proposal of the SDGs as a contribution to a transformation of business and economics, we moved on to discuss three challenges of implementation: partnerships for the SDGs, measurement of SDG performance and the SDG Compass as the basis of a strategic tool for SDG implementation. Thus, the success of this transformative economic Agenda depends heavily on the use of these management tools and instruments to embed SDGs in local community economic practice.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.