Abstract

India’s retailing sector is expected to remain in a transition spiral for the foreseeable future. Because of India’s unique context—in terms of history, regulation, institutions, demographics, geography, and traditions—available theories of retail evolution have limited applicability to the retail situation in India. Drawing from the literature, as well as from empirical research and practical experiences of over a decade, this article presents a conceptual frame for understanding the retail sector of India and the likely future trajectory of this sector.

Keywords

In developing Asian countries like India, China, Indonesia, and the Philippines—and even in advanced nations like Japan, France, and South Korea—both the shopper and the retail systems are in transition. In India, even in the most advanced urban settings, there are no “true modern shoppers.” Nor are there “true modern outlets” since even the Western-style superstores generally have to incorporate some traditional elements. Both the consumer side and the retail side in India are in a transition spiral and will remain so for the foreseeable future.

On the retailer or the supply-side, the bulk of the grocery and branded consumables retailing in India is via the Small Traditional Store (called Kirana store in India; STS). Even the small segment of urban shoppers in, say, central Mumbai—who have easy access to modern self-service retail outlets—split their custom, with the dominant share of the monthly shopping usually happening at the STS outlets. While the presence of modern self-service retailers is growing, the share of modern stores in 2009 had reached only 6.5 percent in India (NielsenWire 2010), compared to 65 percent in China. The pace of change in India, however, has been very fast. By mid-2011, the share of modern retail had already climbed to 10 percent according to estimates by major brand marketers (Singh and Sharma 2011).

The bedrock of retail in India consists of STS, and this is easily evident in the retailing of food and fast-moving consumer goods (FMCG)—the typical branded items available in a Western supermarket. Since the average Indian spends on limited product categories (only eight in 1991), food and beverage accounts for 74 percent of the total retail market (CII-ATK 2006). These STS are conveniently located in neighborhoods or clustered in traditional markets where dry and wet goods stores facilitate the practice of daily food shopping, even by the most affluent segments of Indian consumers.

The sheer numerical size of the STS retail in India puts India in a league by itself. The sector is so large that even the available estimates vary, depending on the source and year of data. Table 1 presents a compilation of key overall statistics on the total size of India’s retail sector. Even though the overall number of retail outlets is declining as modern retail segment continues to grow at a fast clip, retail density in India remains at a very high level. Among large economies, India’s “retail density” (measured as stores per 1,000 people) stands alone with a double-digit density of 11. Based on a variety of sources including NielsenWire (2010) and Lu (2010), comparable figures are China (0.4), United States (3), and Japan (7). Note that Japan has maintained a retailer-to-population ratio closer to that of India than either United States or China.

Key Statistics on Total Size of India’s Retail Sector

This article develops conceptual frames to describe, comprehend, and—to some extent—project into the future the dialectics of modern and traditional retail systems in India. The term retail system is used in this article to encompass the economic aspects of structure, conduct, and performance of retail organizations, as well as sociocultural and behavioral elements from retail studies in the fields of sociology, anthropology, and marketing.

The primary goal of this article is to assess, build, and refine a theoretical frame for the traditional–modern retail dynamics of India. This is done, however, not from a purely conceptual angle. The research taps into an empirical knowledge base of multiple years of field studies and observational experience of India’s retail sector. The narrative to follow is structured thus: Research frame: Elaborates on India’s exceptionalism, which influences our analysis of its retail system—both its current state and its future trajectory. Baseline view of India’s retail system: Presents a concise baseline view of India’s retail system in 2010 drawing upon empirical knowledge from a variety of sources. Preliminary conceptual framework: Relying on general economic and social theories about retailing, particularly those in marketing and related applied fields, this section presents a conceptual framework for the evolution of India’s retail sector. Themes arising from rapid transition: This section draws strongly from the empirical knowledge base to develop seven significant themes that characterize the state and evolutionary trajectory of India’s retail sector. Refining the conceptual frame: Integrating theoretical sources and contemporaneous practical insights, a refined and hopefully stronger theoretical frame is developed. Concluding observations: In addition to summarizing and drawing of conclusions, this section identifies research priorities for understanding India’s retail evolution.

Research Frame

It is well accepted that major transformations in retailing structures occur in periods of rapid economic development (Reardon and Berdegué 2002). The wheel of retailing and accordion theories (Brown 1987; Hollander 1960, 1966; Izraeli 1973) have been used to explain retail evolution in the advanced economies, particularly the United States. After reviewing such theories, Markin and Duncan (1981) concluded that an ecological-adaptive model is a better representation (than wheel or accordion representations) of how retailing institutions adapt and transform. From the perspective of developing countries, some authors have argued that the wheel and accordion theories of retail evolution, anchored in the US settings, have limited relevance in developing and emerging economies (Kaynak 1979).

The main reason for the limited relevance of Western retail theories to countries like India is that Western theories, in various ways, focus on competitive dynamics among modern retail formats (intertype competition), while in India the unfolding process is of modern retail formats making inroads into a massive and established base of traditional and unorganized retailing. Conceptualizing about retail evolution in India, therefore, requires examination of the impact of the modern sector on the traditional retail sector rather than focus on competition across different formats within the modern sector.

India is an exception in many respects. Until recently, food purchases dominated retail consumer behavior in India. With growing affluence, however, discretionary spending has expanded the number of categories, which increasingly include products—and particularly new brands—that had not been available in the Indian market in the past. This has created a very different competitive landscape in India compared to the advanced economy of the United States as well as the emerging but state-guided emerging economy of China.

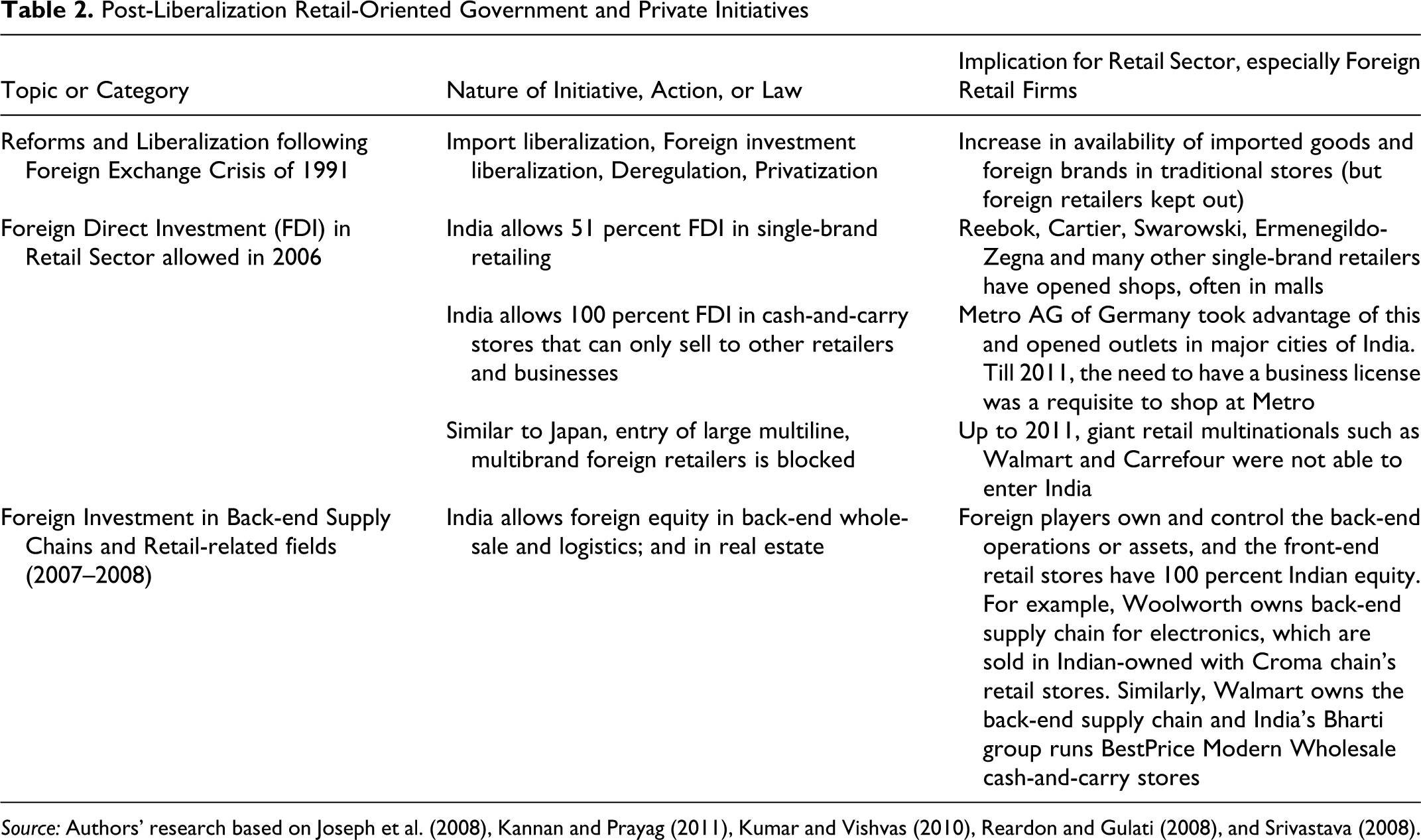

There are many reasons for India’s “retail exceptionalism.” First, public policy regarding retailing has attempted to protect both small and large Indian retailers from foreign competition. This is very different from other countries, such as in Saudi Arabia, where the state has played a big role in retail development (Shechter 2011). Aware of the rapid retail changes in China and other countries—especially the specter of the so-called Walmart effect (Basker 2007; Franklin 2001; Goetz and Swaminathan 2006; Paruchiri, Baum, and Porter 2009)—the Indian government and the Indian private sector took proactive steps to shape the retail evolution. Table 2 summarizes these governmental and private initiatives, and their main implications. The main effects of these state and private actions have been the relative protection of small traditional retailers as well as relative freedom for Indian firms—in the modern sector—to establish modern chain stores before the entry of giant multinational retail chains such as Walmart, Carrefour, and Tesco into India.

Post-Liberalization Retail-Oriented Government and Private Initiatives

Source: Authors' research based on Joseph et al. (2008), Kannan and Prayag (2011), Kumar and Vishvas (2010), Reardon and Gulati (2008), and Srivastava (2008).

Second, in India, a greater polarization of retail structures—with diversity in urban, particularly metro (India’s term for the largest cities) areas, but not in rural areas—has emerged. While some attempts have been made to introduce modern format stores in rural areas, and a few successful modern format stores exist in Tier II cities (e.g., Margin Free shops in south India; Sengupta 2008), most of the modern retail outlets can be found in urban, specifically metro areas. This has occurred not due to public policy, but as a consequence of modern retailers' attempts to cater to limited but fast-rising segments of affluent and upwardly mobile consumers (Singh and Sharma 2011).

In selected markets, modern retail outlets—both chain and independent stores—in food and nonfood categories can be found in neighborhood locations as well as in agglomerations such as shopping malls. The nature of competition is varied—intertype, intercategory as well as intratype. Specifically, intratype competition within the modern retail segment (one mall vs. another mall, one hypermarket vs. another) has increased due to this geographical concentration as has intertype competition (supermarket vs. STS). Within the traditional sector, intratype competition has existed for a long time, resulting in historically unique practices that allow coexistence rather than competitiveness among STS (see, e.g., Varman and Costa 2009). The retail practices of modern large retailers, however, differ substantially from the practices of STS and influence the responses of STS outlets to competitive threats from modern stores.

Like the United States and China, India is a large country with ample opportunities for regional variations. However, the regional differences in India (and China) have fostered a distinct retail evolution than that which occurred in the United States. While the US pattern has been uneven—with family-owned retail outlets concentrated in city centers and large, modern retail formats in the suburbs (Dawson 2001)—this difference has been consistent in all regions of the United States. Japan, which is smaller geographically, has experienced greater regional variation in retail structure than in the United States (Takeuchi and Bucklin 1977). In China, regional differences are evident as urban–rural and coastal–hinterland distinctions (Polsa and Xiucheng 2011; Sternquist and Chen 2006). Regional differences increase the challenges of modern retailing (Halepete, Iyer, and Park 2008), and one response by modern retailers has been to concentrate their efforts in major cities, thereby further accentuating regional disparities in Indian retailing. North India, for instance, accounts for 33 percent of the total Indian modern retail market, whereas Eastern India accounts for only 9 percent (CII-ATK 2006). In contemporary India, the competitive threat from modern retail outlets is therefore concentrated in metropolitan cities (Singh and Sharma 2011), but more specifically in limited regions. This has created greater intratype competition between modern retail outlets within a region while influencing traditional retail outlets to develop counter strategies in other regions. Competition is both local (immediate) and national (anticipatory).

Finally, the development of brands in India is at a very different stage than comparable changes in retail evolution in United States or Europe. In the United States, packaged and branded goods and modern retail firms grew in parallel during the early part of the twentieth century. By the early 1930s, for instance, A&P had already established 10,000 of its “economy stores” (Groceteria 2011), and these self-service stores grew rapidly and expanded in size and product assortment as the number of branded product categories exploded after World War II. These retail outlets, easily reached by the rising numbers of automobile-owning consumers, became convenient channels of distribution for the consumer product companies.

While India’s and China’s growing and affluent populations have attracted the attention of global and domestic brands—product brands as well as retail firm brands—Indian public policy has been less favorable to foreign brands. By allowing foreign brands and foreign retailers to enter the market, China encouraged competition. Public policy in India, however, has allowed only single brand retailers to enter the market. As a result, local and domestic supermarkets have increased in India (PwC 2011) while they have declined in China (Polsa and Xiucheng 2011).

Furthermore, in India, single-brand foreign retailers (e.g., Swarovski, Nike) in luxury and specialty categories are concentrated in modern agglomerations such as shopping malls while foreign branded products—in food, health and beauty aids, and appliances—are marketed through Indian-owned retail outlets, STS as well as increasingly Indian-owned modern retail chains. For instance, Chroma, an Indian-owned retail chain (similar to Best Buy in the United States) specializes in electronics and offers foreign brands from all over the world. Foreign multibrand electronic retailers such as Best Buy from the United States or Dixons Retail from the United Kingdom are not allowed entry into the Indian market. At the same time, Indian retailers have been able to respond to the growing affluence by developing and marketing their own retail brands in new product categories such as jewelry (e.g., Tanishq) and apparel (e.g., Pantaloons), and locating the outlets in varied retail environments—malls as well as street fronts.

In addition, private brands have grown at a much earlier stage of India’s retail evolution. Protected by public policy, and attracted by the large size of the price-conscious and value-conscious market segments, Indian retailers have introduced private labels in many product categories. Big Bazaar, for instance, has its own private brands in food as well as cleaning products, and some of these private brands are priced at the same level as national brands. Given that private brands earn higher retail margins, loyalty to the retailer is developed at a much earlier stage in the retail evolution, even though modern outlets account for a very small share of total retailing in India.

Finally, many Indian retailing firms have been created by large, Indian conglomerates without any prior experience in retailing. This has not been the case with the development of retailing in the United States (Kacker 1988). Clarence Saunders, for instance, started the self-service concept with the Piggly Wiggly store in Memphis, Tennessee, in 1916. He started his life as a grocer and had extensive experience in the grocery business at the retail and wholesale levels. After the Piggly Wiggly success, Saunders went on to found another retail chain (Time 1929). On the west coast, self-service was started in 1912 and extended to a wide variety of retail formats in food and nonfood categories (Kacker 1988). In China, foreign firms, particularly from Asia, are pioneering the retail format in luxury and specialty product categories (Goldman 2001), while state-owned and cooperative firms in food retailing are banding together to compete with foreign competitors (Sternquist and Chen 2006). In India, on the other hand, we have retail giants emerging from business houses such as Tata, Aditya Birla, Reliance, and Bharti Telecom. These firms have financial assets, as well as symbolic advantages in terms of their well-known brand names (Sengupta 2008), but not the skill-based or transaction-based strengths developed from prior experience in retailing (see Alexander and Myers 2000).

With this unique retail setting that differs not only from the advanced American and European retail settings but also to some extent from other emerging economies such as China (Goldman 2001; Sternquist and Chen 2006), Brazil (Bianchi and Arnold 2004; Lenartowicz and Balasubramanian 2009), and Chile (Bianchi and Arnold 2004), India poses some unique challenges in terms of conceptualizing retail evolution. In the next section, we present a concise baseline view of India’s retail system drawing on varied empirical sources and then offer a preliminary conceptual framework for the evolution of India’s retail sector.

Retailer Operations in India: A Baseline View

Compared to the past, there has been increased generation of data and case studies on the rapidly growing retail sector (see, e.g. CII-ATK 2006; Joseph et al. 2008; PwC 2011). In this section, our main focus is on the 1990–2010 period. We draw upon our own primary data from field research studies and experiential learning of retailing in India, case studies done by faculty and students at a leading business school in India, and a comprehensive accumulation of secondary data on India’s retail sector.

The traditional wholesale and retail trading community in India tends to be caste-specific. This was the case even in 2010. Scheduled castes, scheduled tribes, and other historically disadvantaged groups own 53 percent of India’s retail establishments. These social groups, however, own a lower (46) percent of retail establishments in urban areas and a higher (58) percent in rural areas (see Government of India 2005). Over 93 percent of retail establishments finance their business from internal sources. A survey of unorganized (i.e., STS) retailers reports that only 12 percent have access to institutional credit (see Joseph et al. 2008). Since credit is essential for retail operations, the STS rely on nonfinancial institutions such as moneylenders. Indeed, prior to the growth of the financial sector in India, even into the 1990s, to raise working capital some of the larger STS shop owners often acted as “informal banks” accepting “deposits” from their customers who had savings and offering these depositors interest rates much more attractive than banks. The caste and family relationships within retail establishments and between wholesale and retail establishments create a network of ties that affect business decisions regarding procurement and credit policies. In fact, such ethnosocial ties are an enduring characteristic of retailing throughout the developing world (Lenartowicz and Balasubramanian 2009; Speece 1990).

Since the average retail establishment employs very few paid employees, the hours worked are long. In 2005, more than 79 percent of retail establishments were operated by owners and family members that allowed them to develop long-term relationships with their customers. The personalized relationships are supplemented by retailers' willingness to provide credit and other services that are not provided by modern stores. These relationships also characterize micro enterprises as noted in a qualitative study of subsistence consumer-merchants (SCMs) in southern India (Viswanathan, Rosa, and Ruth 2010).

The typical STS retailer in India (see Figure 1

) is likely to: Serve neighborhood residents as its primary customers. Be small and provide limited visibility of products, with little emphasis on planograms. Display only widely advertising packaged goods on a few visible display counters and shelves, with other items stored in the “back room” or nearby small storage spaces. Use its own logic for organizing and displaying the products, a logic that is not easy to understand except perhaps by regular customers who visit the store frequently. Employ family members or paid assistants/helpers to fetch products. Sell at the printed Maximum Retail Price (MRP) and not manage margins strategically. Look for fast rotation of stocks. Extend credit to regular customers and even offer home delivery to such customers.

Traditional STS outlets.

Within urban areas, town size makes a big difference in retailer type and behaviors. The key difference is in retailer (STS) density: urban shoppers have greater choice of retailers and competition is greater. In large cities (population > 0.5 million), shop density is high and there is horizontal rivalry. In smaller cities (population < 0.5 million)—which incidentally are the growth points of India’s economy at this writing—the shops are fewer, draw their customers from a larger area, and wield more influence over their customers.

Modern retail institutions, such as supermarkets, department stores, hypermarkets (supercenters), specialty stores, and malls, are appearing as new layers on top of the massive existing bedrock of STS retailing in India and thus place demands on consumers to learn new “patronage behaviors” (Dholakia and Sinha 2004). Often, modern institutions choose new cities and suburbs (often in spaces that were erstwhile farm areas), places that have no history of preexisting STS outlets and, indeed, no preexisting populations. In such new cities and suburbs, modern institutions can build their brands and customer loyalty in ways not encumbered by legacy STS outlets. When modern stores open in existing urban areas, such as central business districts or old and well-established suburbs, they encounter entrenched STS competition and competitive dynamics become more complicated (see Figure 2 ).

Modern retail.

Preliminary Conceptual Framework

Theoretical sources relevant to retailing are available from multiple base disciplines such as economics, sociology, anthropology, and geography; as well as from applied disciplines such as marketing, fashion merchandising, and service design. For the purposes of this article, with its macromarketing orientation, the relevant sources of theory are those that have examined retail institutions from a marketing systems perspective (see, e.g., Brown 1987; Hollander 1966; Izraeli 1973; Kaynak 2009; Markin and Duncan 1981).

In their analysis of retail competition in a US market area, Miller, Reardon, and McCorkle (1999) distinguish three types of competition—intercategory, intertype, and intratype. In India, the intratype (one STS outlet vs. another, one hypermarket vs. another) is common; intertype (STS outlets vs. large broad line specialist such as Big Bazaar) is growing; and intercategory (small traditional vs. general merchandise supercenter) has not emerged yet. Using two theoretical perspectives—symbiosis (mutually beneficial) and Darwinism (survival of the fittest)—Miller, Reardon, and McCorkle (1999) had examined sporting goods retailing in the Denver Standard Metropolitan Statistical Area (SMSA) and found support for symbiosis, albeit asymmetrical; while Darwinism characterized intratype competitive outlets.

In India, intratype competitive retailing (STS vs. STS) appears to coexist peacefully for decades, survive, even flourish, perhaps because of caste/family ties (Speece 1990) and lack of capital resources to expand, but also because of embedded institutional practices in traditional bazaars that foster selective cooperation even while competing (Varman and Costa 2009). Darwinian processes are not much evident in STS versus STS competition (Varman and Costa 2009), although this may change rapidly in the near future, especially in the cities where some well-endowed STS outlets may start “breaking from the pack” by modernizing in limited ways. Sengupta (2008) argues that increases in brands and brand variants (Stock Keeping Units [SKUs]) result in retailers exploring ways to improve productive usage of available store space and self-service format is often the first path to modernized retailing.

On the other hand, intratype competition among modern outlets is likely to be fiercer, particularly because these outlets are geographically concentrated. For the limited number of affluent consumers, with the mobility and resources to patronize the large format stores, convenient location in terms of proximity is less important than product assortment and other service-related variables. Once a private automobile is used to navigate the city traffic, a high-income consumer in Gurgaon (an affluent new city just outside of Delhi) is as likely to patronize the more distant DLF City Centre Mall as the competing and more proximate MGF Mega City Mall. By 2010, the Gurgaon exurb of Delhi had sixteen malls, with eight more under construction. In such a setting, a Darwinian process is likely to unfold over the next few years. At the same time, positive symbiotic effects, such as STS outlets clustering around malls or hypermarkets to take advantage of the retail traffic, are likely to be limited in the Indian context. Traditional STS have deep roots in their established locations and their constrained managerial, technological, and financial resources limit their ability to change operating procedures or relocate closer to modern outlets and agglomerations.

Based on key theoretical concepts about retail evolution, one should expect the retail evolution in India to exhibit many of these characteristics: With rising incomes and fast-paced growth of the economy, all types of retail competition—intratype, intertype, and intercategory—will intensify. In terms of intertype competition, the traditional retail sector will lose ground to the modern retail sector, and quite rapidly. The process will be similar to the changes that happened in the retail history of Western countries (Goldman, Ramaswami, and Krider 2002; Humphrey 2007; Wilson and Oulton 1983). Intratype competition within traditional as well as modern retailing, in various categories, will be Darwinian with only the fittest and the best enterprises surviving and prospering. The embedded cultural practices that often promoted cooperative “live and let live” behaviors in the traditional retail sector will become increasingly hard to sustain as competition intensifies. Intercategory competition will start in small ways and then build up fast as “category killer” types of stores appear and become popular. When very successful and very large retail stores become entrenched, “symbiotic” clustering of small stores around these giant stores will emerge in ways that are mutually sustaining and supportive. Adaptation—its speed and its political and cultural appropriateness—will become a key strategic factor in determining which types of retailers survive and succeed.

With this brief backdrop of what can be expected from extant theory, the next section turns again to the empirical reality of the unfolding retail processes in India and explores the themes emerging from the rapid transition of India’s retail sector.

Exploration of Cotemporaneous Themes

The actuality of retail transformation in India is complex. It has been shaped, and will continue to be shaped, by India’s demography, urbanization patterns, business history, regulatory frameworks, cultural traditions, and consumer behaviors. The retail structure in India exhibits more diversity, especially in terms of store size, than any other major economy in the world and this state of affairs is likely to continue for foreseeable decades.

This section presents empirically and experientially developed insights about the structure of retailing, relationships of retailers and wholesale suppliers, relationships of retailers with their shoppers, and the behaviors of Indian shoppers. In each of these areas—structures, relationships, and behaviors—strong forces of change are in evidence, but also persistent are traditional patterns that are unchanging or capable of only slow, glacial transformation. While these themes are not in any theoretically informed order, the consumer-/shopper-oriented themes pertaining to STS are presented first, and themes pertaining to modern large stores and modern-STS competition are presented next.

Shopping Patterns Favor STS

Multiple factors in India cause shoppers to patronize their neighborhood STS. Earning daily wages and with no fixed monthly incomes, most shopping trips are to acquire daily necessities and meals for the day. Convenience of store location plays an important role and the frequency of store visit is as high as eleven times in a month. For brand marketers, lower priced value packs and single-use sachets generate substantial sales, particularly in the STS outlets. Since STS outlets often extend credit to regular shoppers, the shopper loyalty to the STS is cemented further.

In a 2009 study using structured questionnaires as well as qualitative methods in two large (Mumbai, Kolkata) and two midsized (Aligarh, Vizag) cities in India, location convenience was the most important reason for patronizing the store and 20 percent of the shoppers interviewed reported visiting the store at least once daily. As one Kolkata shopper commented: At this old age [referring to own age] it is not possible to remember everything all the time…and as a result I end up going to the market [i.e., the traditional retail street] a number of times in one single day. (Observational fieldnotes, Kolkata, 2009)

For nonfood categories, similar shopping practices favor the small, unorganized retail stores. Traditional Indian clothing habits have been supported by tailors and dressmakers, rather than through the purchase of manufactured, ready-to-wear apparel. Similar patterns exist in purchase of jewelry. While both the apparel and the jewelry categories are significant in the modern outlet sector, small, owner-operated stores with customer relationships that sometimes exist across generations, continue to survive and prosper.

Familiarity Breeds Comfort: STS Advantage

For stores selling groceries and daily use items, convenient, neighborhood location is a key to retail patronage. Location alone, however, is not the only advantage. The relationship with the customer is an important driver: The owner of MH Department store [in Vizag, India] knows at least 200 of his regular shoppers by name. Credit is often extended based on personal relationships. (Observational fieldnotes, Vizag, 2009)

…one can come dressed in only a towel [i.e., bare bodied with just a loin cloth] to shop at my store… A shopper has to dress up to go to a modern store…(Retailer interview, Kolkata, 2009)

The majority of these STS retail outlets have regular customers who typically know what they will get from that store, where exactly the product is located inside the store (even though there is usually no self-service access), and how much it costs. When a customer arrives and asks for a product, the storekeeper hands over an item, thus indicating an implicit and consensual understanding about the specific variant (the SKU) that is transacted. Only rarely would the storekeeper ask the customer questions to determine which variant the customer intends to buy.

STS owners are able to capitalize on personal relationships and social networks within the community to maintain loyal customers and expand their potential sales despite the increasing presence of large, modern retail competitors in bigger cities. In specialized retail categories, STS outlets may offer very high levels of customization and flexible credit terms. Tailors and jewelers, for example, customize products and offer informal methods of extended payment options difficult to match by large modern retailers.

While the shoppers at these STS outlets frequent their local small stores regularly and often, these shoppers are not averse to buying from modern outlets, particularly if new products and brands are available. Shoppers occasionally buy packaged goods or ready-to-wear blouses and shirts from the modern, big stores. Very few shoppers, however, go to modern big stores regularly.

Identification-Based Trust as a Source of STS Advantage

In the context of shopping at STS, the relationships between shopkeepers and shoppers appear to be of the identification-based trust type. That is, they know each other. The four-city study of STS outlets conducted in 2009, and referred to earlier, found that: STS shopkeepers have close and long relationships with their shoppers, with the average duration of continuous store patronage being nine years. STS shop owners know more than 100 of their regular shoppers by name. Credit is often extended based on personal relationships. The reverse also happens in that stores will hold money paid in advance in escrow. Stores often charge less than MRP (printed on packages by law in India) to their preferred regular shoppers. Stores accept phone orders and provide home deliveries to regular shoppers. Children are often offered treats (candy) and sometimes the store would babysit kids while parents run some quick errands.

In this type of relationship, both parties come to closely identify with each other’s wants and needs, display empathy, and engage in personal and family-related conversations. Some of the relationships have been established over many years, as the following comments indicate:

Meanwhile the shopkeeper as well as his assistant kept on suggesting other items, not included in the list, to enable me to recollect any item that I might have missed out like tomato sauce [ketchup], coffee, pickle, orange squash and the newly arrived 5-in-1 grain biscuits of Britannia…all of which I asked to be included in the list. (Shopper interview, Mumbai, 2009) The shopkeeper is well acquainted with my husband. My husband visits this shop often… As the shopkeeper is an old man who, besides exchanging pleasantries with my husband, almost always offers him a chair to sit upon and take rest. When he saw me approaching he stepped forward to offer me a chair and inquired about my husband’s health…(Shopper interview, Kolkata, 2009)

When the shopper-store relationships are strong, the product information from the shopkeepers is perceived as highly credible. The shopkeeper is seen as looking out for the customer’s interest. In such cases, in out-of-stock situations, shoppers usually accept the alternative brand suggested by trusted shopkeepers. In some cases, the shopkeepers cement the credibility further by offering a personal guarantee or additional services: I inquire the shopkeeper about the validity and reliability of the advertised new product. A little conversation with the shopkeeper gives me knowledge about the particular brand. Being a regular shopper is an advantage over others in that the shopkeeper sometimes supports me with advice about buying the new product or not…. (Shopper interview, Aligarh, 2009) I made the payment and was about to leave when he [shopkeeper] asked whether I wanted potatoes or onion[s]. I said I didn’t, but added that I was going to buy two kilograms of green peas from the vegetable seller [a different, nearby shop]… which also his [the original shopkeeper’s] assistant would have to carry home for me. He [the original shopkeeper] agreed…. (Shopper interview, Kolkata, 2009)

While the identification-based trust relationships typically take years to build, with fast-paced economic growth and the resulting geographical mobility of the professional class, the more sophisticated STS owners have developed rapid ways to size up the trustworthiness of even new customers. The following illustrates such rapid build-up of STS-shopper trust: When we moved to this new cluster of high-rise apartments in Mumbai, I had to find out what the convenient stores were in this new and relatively unfamiliar area of Mumbai. I went to the nearby chemist [pharmacy] store. The owner noticed me and came over: “Sir, why are you here? Just tell us what you need and we will deliver it to your apartment.” The owner noted down my address and phone number, and gave me a card with a customer number. He said: “When you need anything, Sir, just call the store, mention your customer number, and tell us what you need…we will have it delivered, usually within half an hour or less…” I tried their home delivery system a few times and it worked as promised…But I was not convinced how the store would react if I placed a really small order. One night I called and said I needed two aspirins—not two strips, just two tablets. Sure enough, in the next 15 minutes, the doorbell rang and the pharmacy delivery guy was there with my two tablets…. (Interview of high-level executive, sixty-two years old, Mumbai, 2011)

Flexibility and Rapid Response of STS to Consumer Demand

Because the average STS outlet is small and has limited space, the retailer replenishes his stocks frequently, even daily. Limited working capital impels the retailer to seek rapid stock turnover. Manufacturers of FMCG—the so-called FMCG brands—as well as wholesalers are prepared to sell to STS outlets in smaller quantities and to extend credit. If stockouts occur, the STS retailers do not want to lose customers and the STS shop owners are usually able to convince the shoppers to accept alternatives. If new products become available and customers become aware of these new products before the retailer, the retailer is able to respond rapidly to these demands. The retailer would often promise that a desired (but unavailable) new item would be in the store the very next day. In some cases, for preferred regular customers, the STS retailer would even send an errand boy to borrow and fetch the item desired by the customer from a nearby (competing) STS outlet—another instance of the inter-STS cooperative behavior observed by Varman and Costa (2009). The identification-based trust seems to work mutually between STS and shoppers; and also between STS and their suppliers (wholesalers and FMCG brand sales representatives): We found that the wholesalers [whose outlets often look no different than STS] were highly responsive to the demands of retailers who bought from them. One wholesaler had a simple rule of thumb: ‘If 5 retailers ask me for an item that I do not carry, I will buy the item and have it available the next day.’ (Observational field notes, Mumbai, 2011)

For the past one year the shopkeeper himself rings up [regular customers] to inform about any new offers on products available at the store. So he [the shopper] feels that for him this store is the best in this locality…” (Observational fieldnotes, Vizag, 2009)

Slow but Inexorable Modernization of STS Outlets

Since almost no self-service access to merchandise takes place in STS shopping contexts, an overwhelming majority of shoppers specify the product category or brand, with nearly two-thirds of shoppers specifying brand-plus-SKU. Here is a relevant comment from a Mumbai shopper: …However I specified the brands for each product…Maggie Tomato Sauce (500 grams), Nescafe Coffee (100 grams), Mother’s Recipe Pickle (350 grams), Kissan Orange Squash (750 ml). (Shopper interview, Mumbai, 2009)

After I had finished dictating the list [to the shop assistant] I ran my eyes over all the shelves in the shop to see if I had missed out anything and to check out any new [product] arrivals… (Shopper interview, Mumbai, 2009) Although I try to carry a list of things most of the time, the goods displayed on the shelves also serve to remind me of things to buy sometimes…(Shopper interview, Kolkata, 2009)

I am purchasing my monthly supplies from the same shop for the last 13 years after experimenting with all leading shops of the area…and I came to the conclusion that at this shop you get not only the variety but also the quality…and also you are well attended [to]…and there is lots of space in the shop so you can stand easily…(Shopper interview, Aligarh, 2009) Good Luck Stores used to be like any other Kirana store in this Mumbai neighborhood. In the most recent visit [by the research team], after a gap of several months, we noticed dramatic changes. The store had installed glass shop windows and an automated door, cleaned up and organized the interior, and installed air conditioning. Organized shelves and a couple of aisles had replaced the cluttered storage inside. Outside the store, there was parked a motorized three-wheeler, used for fast home delivery of merchandise to neighboring homes. (Observational fieldnotes, Mumbai, 2011)

Modernizing STS outlets.

The dynamics of the interactions between the STS shopkeepers and their suppliers—be they multiline and independent wholesale suppliers or authorized and exclusive distributors of major FMCG brand marketers—have become crucial in determining how far, how fast, and how effectively the STS outlets in India modernize. Under some conditions, the supplier is able to emerge as an influential adviser to STS shop owners.

STS outlets in India, especially those with a modicum of capital and educated forward-thinking owners, find it relatively easy to keep their customers, but controlling operating costs and maintaining profitability levels have become major challenges. In terms of intertype competition, the leading STS outlets have won the battles for the hearts and minds of shoppers through flexible, adaptive, and personalized services. Winning a share of the pocket books of shoppers, however, is the next challenge STS outlets face—especially as cost-efficient mega-retailers such as Walmart, Tesco, and Metro from the West and India’s own Future Group (Big Bazaar, Food Bazaar) and Spencer’s increase their footprints.

Paradoxes Arising from the Growth of Modern Retailing

The growth of modern retail has brought with it a rapid expansion in shopping center square-footage. While the extraordinary growth of shopping centers has provided more space for brands and modern retailers to grow their business, much of the growth has been concentrated in the biggest metropolitan areas. Until 2010, almost half the shopping center space had been developed in India’s biggest cities like Mumbai and Delhi. Indeed, concerns have been raised that such overbuilding of modern shopping spaces could potentially lead to the failure of a significant number of these malls.

Growth of modern retailing in India is riddled with paradoxes: In the biggest cities, despite the proliferation of malls, real estate rental costs have remained high for retailers, adversely affecting their competitiveness. Some single-brand retailers have signed on as high-rent tenants with the aim of maintaining a foothold in key visible markets, even though they fully expect these shops may not make money in the foreseeable future. The intensive development of malls, without adequate zoning and planning of support infrastructure, such as water, sewage, power, roads, public transit, and parking, is stressing not just the city but also the malls themselves. The overall result is often a “reversal of convenience” where the convenience of one-stop shopping under one roof is undermined by the inconvenience of spending an inordinate amount of time in traffic jams and hunting for parking spaces. While very large cities may potentially overbuild modern retail spaces, smaller cities and exurban and rural spaces still have very limited or often no availability of modern retail formats.

The emergent retail structure thus is lop-sided: sophisticated and modern in a few of the largest, most affluent urban enclaves; mostly STS-based (with occasional sprinkling of malls and supermarkets) in the less-affluent parts of large cities and in smaller cities; and nearly totally STS-based in small towns and rural areas. Even when large format stores dominate, the problems of traffic and parking often force large stores to emulate STS services such as home delivery or push cart vending (such as Reliance Thanda door-to-door push carts by the Reliance Fresh supermarket chain).

While modern retailing faces all such challenges, it is nonetheless expanding at a dramatic pace. Share of modern retailing has climbed from 5 to 10 percent in the first decade of the twenty-first century and could double again well before the second decade ends (Singh and Sharma 2011; McKinsey 2008; PwC 2011). Entertainment choices—food courts and cinema, for instance—are changing the nature of outlet choices (Srivastava 2008) and visits to malls are increasingly being incorporated as a regular household activity involving multiple family members.

In terms of the overall competitive framework, intertype competition is despite difficulties ultimately favoring modern retail formats in India. Such stores are gradually winning a bigger share of the retail pie. In some categories, especially the nonfood and non-FMCG categories, the ascent of modern formats will be quite rapid, especially in the cities. Within category competition among large retailers is also intensifying and not all modern retailers will be able to compete with equal ease. To the extent that foreign multibrand retailers (Walmart, Carrefour, Tesco) are kept at bay, the best-of-class Indian large format retailers have a chance to out-compete those peers that fall behind in terms of assortment or services.

Modern Innovation to Counter Traditional Resilience

In many traditional contexts, the insertion of modern retail formats creates various patterns of resistance and reaction. In China, Walmart super stores attempted to sell nicely filleted, shrink-wrapped fish displayed neatly on ice, but the Chinese consumers refused such prepackaged fish (McGee 2007): Chinese shoppers don't want to buy dead fish, even if impeccably displayed on beds of ice. They prefer to select their fish and seafood while it's still alive. That's why Wal-Mart's extensive fish section contains more fish tanks than display counters -- and small nets to bag your selection. Young shoppers are eager to help. “We come here every day; he likes to help select the fish,” says one mother of her toddler son.

Faced with the rapid and flexible adaptability of the leading STS outlets, other malls and modern retail stores in India have started trying innovations to entice customers, encourage repeat visits, and build store loyalty (see Figure 4

). Kannan and Prayag (2011) report several examples of such innovative tactics: Bangalore’s Total Mall offered free pick-up and drop-off services to customers, obviating the need to drive (or take public transport) to the mall and to hunt for parking spaces. The bookstore chain Crosswords (similar to Barnes & Noble) started accepting phone orders and making home delivery of ordered items. Max Retail, a fashion clothing chain from Dubai-based Landmark Group, hired students from the National Institute of Fashion Technology to act as consultants to shoppers on matters of colors and wardrobe choices. Madura Fashion and Lifestyle offered the “All India One Stock” service—wherein if a customer could not find a garment in a particular size in a store, the chain would source it from another store in the country, and deliver it to the customer’s home for free. Ishania Mall in Pune introduced a loyalty card program for shoppers at that mall.

Mixing the old with the new in modern outlets.

Refining the Conceptual Framework

There are many reasons why the on-the-ground retail transformation in India is laced with multiple complexities. Chief among these reasons are the following: The sheer size of the retail sector, composed until 1990 of primarily STS outlets, dwarfing the retail sectors of every other country in numerical terms. The particularistic “lags” of India in terms of urbanization, modernization, Westernization, and incomes (levels as well as distribution). India not only does not look like the advanced West, it does not look much like the advanced East (e.g., Japan, South Korea) either. The political economic makeup of the country—with layers of feudalism, colonialism, socialism, and capitalism—make governance (and infrastructure development) extremely challenging. The latest example of this was a late 2011 decision by Indian government to open the country’s retail sector fully to major multinationals like Walmart and Tesco, by allowing majority foreign ownership of retail firms; but then a quick reversal of this policy and the suspension of this decision following street protests by small retailers and their allied political interests (Agarwal 2011).

The challenge of interpreting retailing transformations in India lies in the historical lag conflating with the real-time, media-linked process of contemporary globalization. At one level (e.g., urbanization) India is like the United States of the 1890s and, at another level (e.g., innovative retail atmospherics), India coexists on the same temporal plane as the United States of 2010. This is especially the case in terms of the rapidity with which retail trends and consumption styles circulate globally. Indeed, in the contemporary context, the United States is as likely to borrow retail or consumption trends from India (e.g., some multiplex cinemas in India’s malls offer gourmet sit-down meals to movie watchers), as India is likely to emulate trends from the United States.

What, then, are the theoretical insights, extensions, and refinements that can be gained from the on-the-ground experience of retailing in India? The following points provide an adaptive reprise of the theoretical statements presented earlier: Intensification of competition: As expected, there is intensification of all types of competition—intratype, intertype, and intercategory—but not at a pace that makes it impossible to adapt. Intertype competition: As in the advanced as well as other developing countries, the traditional retail sector in India is losing ground to the modern retail sector, but at a pace far slower than that in comparably sized countries. This provides a window of opportunity for many traditional retailers to adapt and thereby decelerate the erosion of the traditional sector. Adaptation: For the traditional stores, the cultural appropriateness of adaptation has become a key. In many cases, traditional stores are able to design a service mix that is unbeatable by even large and well-capitalized modern stores. Such traditional stores—which should of course no longer be seen as “archaically traditional” but rather be perceived as “progressively traditional” —will be survivors of India’s retail transformation process, and possibly spawn some new models for global retailing. Darwinism: Neither the traditional nor the modern retail sectors had experienced “adapt-or-die” levels of Darwinism in the 1990–2010 period, but this will change in selective geographies and categories in the foreseeable future. In both traditional and modern retail sectors, in some parts of India and in some retail categories, intense forms of Darwinism can be expected. Given India’s diversity, these trends are unlikely to be massive and national. Culturally embedded cooperation: As competition intensifies, such behaviors would be under pressure, but they will not disintegrate. Japan provides an affluent exemplar. It is a nation where public policy and private actions have maintained many patterns of culturally embedded cooperation. Intercategory competition: Such competition would start in small ways but would not build up to a major crescendo. In the West, particularly the United States, “category killer” mega-stores reached a zenith, but may have retreated to some extent. Since the US experience is available as a case study, countries like India are unlikely to commit to “category killer” type mega-retailing in the same massive way that the United States did. Symbiotic clustering: The experience of retail transformation in India up to this juncture provides no clues as to whether a clustering of small and symbiotically related stores around successful mega-stores would happen or not. Most of India’s retailing is in situ—geographically and historically anchored. There is hardly any experience of small stores making conscious location decisions with reference to large mega-stores.

Concluding Observations

To conclude this article, it is useful to revert to the three guiding issues posed at the start: (a) the reasons for the persistence of STS in India, (b) the barriers to quick dominance by modern stores in categories like grocery retailing, and (c) the factors that may shape the retail landscape of India in the foreseeable future.

With respect to the persistence of STS, some of the factors that supported such retailing are changing—particularly in big cities and in newly created affluent suburbs. In established cities, towns, and villages, the factors supporting the persistence of STS remain mostly unchanged. Furthermore, leading-edge STS outlets are exhibiting adaptive patterns that are able to woo and retain customers through personalized services. The STS sector would shrink, but it would not disappear, or turn into a very minor part of the retail landscape.

The dominance of modern retailing would happen but only in selective geodemographic settings: affluent enclaves, newly created suburbs, new and planned cities. Such settings do not have entrenched legacies of STS, and modern stores would be able to create new patterns of customer loyalty. In other settings, we can expect a long drawn out tussle between modern and STS formats.

Among the factors that would shape the future retail landscape of India, physical infrastructure and adaptive strategies of retailers are likely to be the most important. It is unlikely that, in the foreseeable future, India would develop a physical infrastructure comparable to advanced parts of Europe or of Asia. Neither the automobile-based retail culture of the United States nor the train-based retail culture of Japan and some European cities provides models for India. The infrastructure development pattern of India will be a patchwork. The adaptive strategies of retailers, modern as well as STS, will play increasingly important roles in shaping India’s retail landscape. Multiple examples of such adaptive approaches—delivery services, tailoring and customization services, and more—are already emerging. Retail manager and researchers need to watch these with care and deep interest.

Like other emerging and fast-growing markets, India is experiencing major transformations in its retailing sector. India, however, is also home to the largest number of STS in the world. Even as modern retailing makes rapid inroads in India, most STS outlets are resilient in terms of their service mix and remain competitive. Shoppers, even in large metro cities, are still loyal to neighborhood STS outlets. Based on the research themes outlined, a mixed retail system comprising of large modern stores and STS outlets can be expected to continue in India for the foreseeable future.

Footnotes

Acknowledgment

The authors are grateful to editors Alladi Venkatesh and Terrence Witkowski and for their many valuable comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.