Abstract

The processes of structural change and modernization in the food distribution industry have been submitted to different economic and institutional frameworks in European countries. Three essential factors have affected structural change in Spain: 1) the role of technical and organizational innovations, 2) institutional factors such as regulation and market structures, and 3) foreign direct investments. This article discusses with the framework of the “latecomers.” In these countries, the factor of innovation has been produced in terms of appropriation, whether this is technological or organizational, usually influenced by foreign models or through direct foreign investment. The impact of these innovations has been highly conditioned by inflexible institutional surroundings. Considering the Spanish food trade in the last sixty years is a good way understanding processes of structural change in Mediterranean Europe. This research helps one understand the role taken by countries, which introduced factors of innovation and growth in less favourable surroundings than those of developed Europe.

Keywords

Introduction

The literature on retailing history has grown considerably since the late 1990s (see review by Alexander 2011). Some factors, such as the interest aroused by advances in the history of consumption in the UK, generated new issues for European retailing historians (Benson 1994; Benson and Ugolini 2003; Fraser 1981; Gardner and Sheppard 1989). Works with complementary visions of retailing maintained a basically historical perspective (Alexander and Akehurst 1998; Alexander et al. 2009; Bowlby 2000; Coles 1999). Scholars have mainly focused on the more developed countries and those that adapted faster to the North American model (e.g. Lescent-Giles 2002; Schröter 2008; Sandgren 2009), but had paid less attention to other countries. Consequently, the history of Spanish retailing offers significant insights. Spanish distribution lagged significantly behind (and was in a peripheral position to) European retailing in the middle of the 20th century. Nevertheless, in the 1980s and 1990s Spanish grocery retailing accelerated its convergence with Europe and became incorporated into globalization through intense structural change (Casares Ripol 2004; Cruz Roche 2012; Mollá et al. 2002). Spanish retail evolution was idiosyncratic in the European context and its structural change refers to specific stages that were a consequence of the Spanish backwardness after World War II.

As Markin and Duncan (1981) explain, the most efficient way to understand change in marketing institutions is to view it as a set of analytically separable processes. We can apply this conceptual approach to retailing formats. Formats are a key factor in retailing, and the introduction and diffusion of self-service in Europe was one of the most important changes in the distribution sector in the 20th century (Du Gay 2004). As a consequence of Americanization, self-service was introduced in European retailing in the interwar period, but the real expansion began in the post-war years (Alexander and Akehurst 1998; Shaw, Curth, and Alexander 2004). In the Spanish case, the development of retail formats lagged until the 1970s. Self-service was slowly introduced in the 1960s and became common in supermarkets, hypermarkets, malls, and hard-discount stores by the 1980s. By the end of the century, Spanish retailing was becoming increasingly concentrated.

The aim of this article is to find and analyze the historical factors that have brought about this evolution. We consider three essential factors that have affected structural change: 1) the role of technical and organizational innovations, 2) institutional factors such as regulation and market structures, and 3) foreign direct investment (FDI) due to the limits of domestic capital for producing innovation and change. The weight of these factors has varied depending on the historical circumstances of the countries in consideration and their level of development (Reardon and Berdegué 2002). Our conceptual approach includes a social and cultural scenario in which change occurs. The holistic component, intrinsic to the historical and institutional foundations of the analysis, considers the role different characteristics play in the structural change, such as managerial agency, which is an empirically valid perspective, particularly when joined with complementary perspectives (see Eisenhardt 1989).

A Research Frame: Innovations

The role of innovation has been addressed in numerous disciplines, such as marketing, retail management, retail geography, and business history. In the Spanish case, the backwardness of the retail industry did not favor endogenous changes, and the role of exogenous influences was more significant. This perspective allows us to focus on key organizational and technological changes around the introduction of self-service and supermarket retailing formats in Spain. We deploy a wider definition of innovation that refers to the processes of diffusion and innovator-imitator transference (Dosi 1982) and that blends the various types of innovation in the evolutionary theory of economic change (Nelson and Winter 1982). Moreover, Alexander, Shaw and Curth (2005) note the need to keep in mind the role of knowledge management and learning processes within companies when considering the processes of innovation in retailing.

With this focus, it is useful to search for a conceptual model that lets us study the new diffusion and assimilation mechanisms. After the Civil War, 1936–1939, small shopkeepers populated the Spanish retail industry. In this setting, a self-service store was an innovation that could be considered both a new “presence” and a new “customer experience,” using the terms of Sawhney, Wolcott, and Arroniz (2006). Nevertheless, it would be premature at this stage to apply a conceptual framework, the “innovation radar” designed to manage complicated business models. However, this framework will be useful once Spanish distribution entered the era of second globalization. Some of the diffusion processes of these innovations, such as self-service (see Figure 1) at the end of the 1950s and in the 1960s, resembled the “self-service community of practice” (Wenger 1998; Wenger and Sneyder 2000), although the institutional strength of these groups in Spain was far lower than in the European environment.

Self-service in a Spanish town in the early 1960s. Source: authors

Some conceptual approaches will also be used to analyze the Spanish case, especially beginning in 1986 when Spain joined the European Economic Community (EEC). The diffusion processes of innovation and Americanization and the dissemination processes produced in terms of “appropriation” are better adapted to the Spanish case long term. From the viewpoint of the diffusion of innovation, both the concept of technological adoption (Rogers 2003) and the process of Americanization (Kipping and Bjarnar 1998; Zeitlin 2000) led to this relevant focus. The concept of appropriation emphasizes the role played by the recipient of an innovation as an active subject with adaptive and processing capacities (Alberts 2010; Eglash et al. 2004; Nolan 1994). Similarly, a number of knowledge conduit typologies, such as those suggested by Kacker (1988) and Gertler (2001), also offer a wide field for considering the transfer of innovation and the potential to promote learning between companies (also see Alexander, Shaw, and Curth 2005).

Institutions and FDI

An institutional approach emphasizes the relationships between organizations and the environment (Markin and Duncan 1981). The institutional environment constitutes a key factor of this theory that spans political and sociological aspects such as laws, rules, cultural beliefs and customs. Consequently, company decisions, their marketing actions, and consumer behavior can be considered in this context (Handelman and Arnold 1999). In institutional terms, the field of retailing consists of a wide range of components. The legal framework, whether local, regional or national, is of particular importance, as is the role of public institutions and certain private institutions, such as industry associations, trade unions and consumer associations, to name but a few. Of particular interest in this research are regulatory surroundings and the structure of the domestic market. Until Spain liberalized in the 1980s, its regulatory system was very interventionist with important, and strongly resented, consequences for market structures. The latter were very undeveloped because of economic and social backwardness after the Spanish Civil War (measured in terms of income per capita), the small sizes of the distribution companies, and the local scope of their markets (weak domestic investments).

From the 1970s FDI put new energy and a new dimension into Spanish distribution. Recent debates have summarized the role of international retailing at the global level (Alexander 2013; Godley and Hang 2012). From an institutional point of view, Huang and Sternquist (2007) discuss a framework that explains the foreign market entry choices of international retailers. They underline the importance of external and internal institutional environments in retailers’ decisions. On the whole, retail historians should not only consider relationships between the issuers and recipients of investments, that is, the basic conditions of the chosen market. They should also consider such important elements as domestic market regulation (Morris 1999; Shaw et al. 2000) and the movement of capital in both the issuing and receiving countries (Cho 1985; Klopstock 1973), what some scholars have called “receptivity” (Tschoegl 1987). This term, which has been used mainly for bank investments, refers to an economic recipient’s level of openness (Walter and Gray 1983). In general, countries with few comparative advantages in international markets, which often coincide with their belated industrialization, will tend to enact laws that protect their markets. This factor should be taken into account when considering less-developed countries and is useful for analyzing Spanish retailing in the long run.

This last approach leads us to consider the latecomer status of Spanish companies and the country itself as another determining factor under an institutional point of view. The arrival of FDI in the 1970s and subsequent globalization allowed latecomer companies in the retail industry to develop new strategies for utilizing new opportunities and emerging networks (Mathews 2006). At the end of the 20th century, the Spanish economy and Spanish food distribution reached a position of convergence in the heart of the European Union. This led to a context of structural change in which innovations and institutions (in the sense defined herein) held a central role. To summarize, conceptual frameworks that emphasize a historical and interdisciplinary point of view (i.e. consider a marketing approach), allow us to deepen our knowledge of the retail development (Alexander and Akehurst 1998; Buckley 2009; Hollander et al. 2005).

The period studied spans three stages. The first, from 1950 to 1971, starts with a much delayed distribution model in which the European formats of self-service and the supermarket slowly began to come forward. This trend was introduced in Spain at the end of the 1950s through native initiatives that were strongly supported by currents of external dissemination. An intermediate stage, characterized by the rise of the FDI through French hypermarkets, occurred in the 1970s. The third phase came with burgeoning globalization, which had a great impact on the world economy in the 1980s and 1990s. In this stage, Spanish food retailing experienced the strong influence of global currents of FDI in retailing, which had considerable impact on the domestic market.

In this study, we used primary sources from Spanish national and foreign archives related to foreign investment, as well as corporate documentation from supermarket chains, voluntary chains, and multinational superstores. Similarly, press and business publications, annual Spanish distribution directories, and personal interviews, especially with people who were involved in management processes and modernization, were used as a documentary basis for this work.

In the next section, we will study the conditions for the late adoption of new distribution formats in Spain. Then, we will address the strong structural change and the salutary lesson that led to the arrival of direct French investment at the start of the 1970s. The fourth section will directly discuss the establishment of foreign investment and the consequences of entry into the EEC, which directly globalized the Spanish retail market. Finally, we will draft some conclusions.

Early Years: The European Gap (1950–1971)

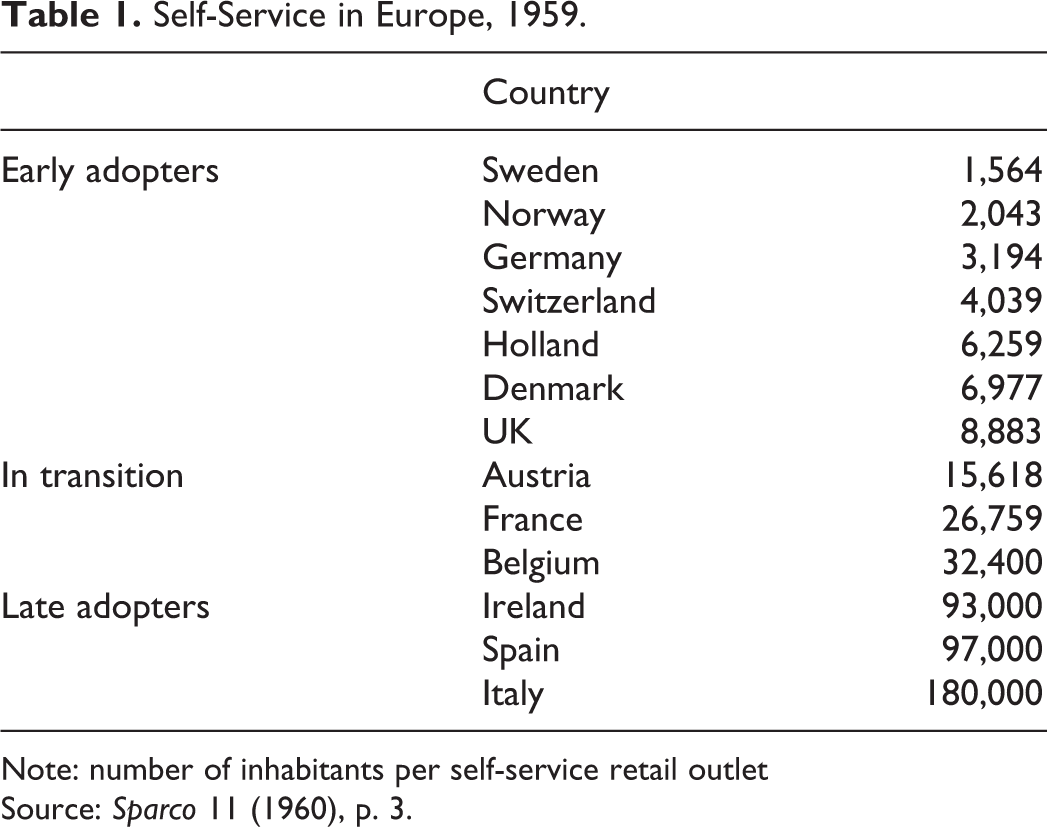

Macroeconomic evidence shows that Spain lagged behind developed Europe. Between 1945 and 1951, the private consumption of food, drink, and tobacco in Spain grew as a proportion of GDP until it reached nearly 50 percent. The ratio fell 14 percentage points over the next five years, indicating what would be the historical trend: between 1960 and 1995, this percentage reduced to a third, progressively converging to the European average (IRESCO 1978; Prados de la Escosura 2003; Uriel, Moltó, and Cucarella 2000). Spain also trailed in terms of retail formats. In 1959, Spain had only 15 supermarkets and, along with Italy and Ireland, found itself amongst the countries of Europe late to adopt self–service retailing (see Table 1).

Self-Service in Europe, 1959.

Note: number of inhabitants per self-service retail outlet

Source: Sparco 11 (1960), p. 3.

Persistence

The reasons for this delay are the slow modernization of retailing during the interwar period (Maixé-Altés 2009a), the weak income per capita in the Spanish economy, and the economic and social disruption after the Civil War. The international isolation of General Franco’s regime and his disastrous policy of economic self-reliance not only led the country to total poverty in the post-war period but also completely distorted the market rules (Barciela and López Ortiz 2003; Guirao 1998).

The years between 1940 and the mid-1950s were a lost period for Spanish retail distribution. Government regulations aimed to check rationing systems by creating the General Commissariat of Supply and Shipping (henceforth CAT in its Spanish abbreviation, Act 10 March 1939). In this context, corruption grew, as did the black market (in Spanish, estraperlo 1 ), within a framework of product shortages of offers and prices set by the government. On one hand, food manufacturers and retailers were not adopting modern methods of distribution. For example, they presented and sold most foods loose without packaging. On the other, the culture of consumers and retailing practices responded to archaic guidelines that had become obsolete in developed Europe (Interview with Álvaro Ortiz de Zárate, Madrid, February 25, 2010). In these years, the conditions for modern marketing in Spain were simply not present. With a shortage of modernized business formats and a lack of teaching institutions, the economic backwardness just generally did not favor the creation of structural change in the retail sector (Garcia Ruiz 2007; Puig 2003). This situation distanced Spain from the framework in which the European retail sector was developing (Shaw and Alexander 2008; Shaw, Curth, and Alexander 2004).

After the early Franco years, the first signs of economic reform appeared with the signature of the Pact of Madrid between the Spanish and U.S. governments in September 1953. This accord led to the arrival of American military aid, but also created an institutional framework favoring the recovery of business expectations (Calvo 2001; Viñas 1981). The Spanish Productivity Council (Comisión Nacional de Productividad Industrial, henceforth CNPI) was the instrument that developed these initiatives. CNPI began its activity in the first months of 1953 owing to extraordinary credit approved by the Cortes, Franco’s legislative body (ACCM 1953, 1954). It followed the model established by European countries that were members of the European Productivity Agency (Alexander, Phillips, and Shaw 2008).

The implementation of the Stabilization Plan in 1959 was a step forward in opening up the Spanish economy. The increase in the income per capita between 1960 and 1975 explains some of the transformation. This development is associated with a model of growth during the 1960s known as “desarrollismo” (a “fast but disorderly growth” in the words of Garcia Ruiz 2007). However, the gross added value of commerce grew at a lower rate than did GDP during these years (INE 1960-1975; IRESCO 1978). As a result, retailing changed slowly while the institutional environment incorporated new restrictions.

The government request insisted that Spain become a mixed economy in which the public sector played a fundamental role. However, public initiatives were guided by criteria more interventionist than dynamic and, in many cases, private initiative lacked the necessary push. The Dirección General de Comercio Interior [General Department of Internal Commerce], created in 1957, overlapped its functions and skills with those of the CAT. The result was a new general department that had minimum advocacy in rationalizing commerce (ACCM 1957-1959; CNPI 1959a). Something similar occurred with the Law of Repression of Restrictive Practices of Competition of 1963, which created the Defense Court of Competition. Although inspired by articles 85 and 86 of the Treaty of Rome (the treaty that established the European Economic Community), its influence was marginal within such an interventionist regulatory framework. The development of the legislation related to market rules and competent autonomous bodies in price control merely contributed to increasing this regulatory web. In conclusion, the institutional tangle hindered the actions of economic agents.

Progressive Forces

In the 1950s and 1960s three currents influenced the obsolete Spanish economic framework and brought change to the Spanish food trade: CNPI initiatives in the retail field (perhaps a more effective area for government intervention), the influence of European retailing (this could be considered an early adopter stimulus), and, finally, entrepreneurial actions by some Latin American businessmen (Cubans and Mexicans) who emigrated to Spain in the post-war period. Other conduits of knowledge about self-service and supermarket innovations, such as the trade press and dealings between retailers and equipment suppliers, were minimal in this period (see Alexander et al. 2005).

After the productivity programs in the manufacturing industry were implemented, at the heart of the commission, an idea arose to create a specific program to promote modern commercial distribution techniques, especially in the field of grocery retailing (ACCM, Annual Report of the CNPI, 1957-1960; CNPI 1959a, b). Priority was given to professional training seminars on self-service and retail practices as direct knowledge transfers (applied in running a business). Program implementation began in 1956 with the participation of three institutions: the CNPI, the Madrid Chamber of Commerce, and the Ministry of Commerce. Pro-Franco union organizations, professionals, and manufacturers and equipment distributors, such as National Cash Register (NCR), also collaborated (ACCM 1953-1956).

The CNPI sent various teams to the United States and Europe on study trips (1956–1958) with the participation of 57 specialists and businessmen (see Figure 2). Technical exchange programs with Europe, which implemented two campaigns, complemented this line of action. One program was directed at food consultants (study trips to Denmark, German Federal Republic and France) and another related to the European teaching programs on food (study trips to Sweden, Norway and Denmark). The programs were managed by the national productivity centers of Sweden, Norway, Denmark, France, and Germany and included visits to productivity centers, food trade schools, industry associations, and retail and wholesale firms (CNPI 1959a).

Participants of the study trip to U.S. in 1957. Source: Madrid Chamber of Commerce

Meanwhile, the Madrid Chamber of Commerce, through its productivity office and as s collaborator with the CNPI, organized training programs for retailers and wholesalers in a number of Spanish cities. Marketing campaigns and the contracting foreign specialists to train local executives were also launched. This office was directed by Álvaro Ortiz de Zárate and the American technician, August W. Swentor, both of whom became true promoters of modern marketing and retailing practices in Spain during those years 2 . Simultaneously, an office was created that directed advice to businesses over the entire national territory, and finally, in April 1958, there was an exhibition on self-service in Spain (including a pilot supermarket in Madrid) (ACCM, Report, 1957-1960; CNPI 1959a; Swentor 1959).

Finally, the Ministry of Commerce, through the CAT, installed a network of public supermarkets throughout Spain “with the aim to stimulate private initiative and incite the transformation into traditional traders” (ACCM 1957-1960). By 1970, these were present in 15 cities, with a total of 20 establishments and a sales area average of 295 square meters (ACCM, Report, 1957-1960; MC 1971).

The influence of European retailing comprised a second diffusion current. The pioneer of this trend was SPAR, the Dutch voluntary grocery wholesaler, which arrived in 1959. This was the first entrance of a European group and Spanish businessmen’s first contact with European style food distribution. The arrival of SPAR must not be interpreted as FDI, but rather as a transfer of knowledge. In fact, with the exception of some attempts by the French in the 1960s, foreign capital was not interested in the Spanish market until the 1970s.

The process SPAR followed in Spain is a paradigm of the situation in countries that were very far behind in the food trade. This movement was very well received by a group of Spanish businessmen from the wholesale and retail sectors. SPAR Española SA was born, integrated by Spanish partners who in 1960 already had 31 wholesale centers that served 2,227 retail outlets and 70 percent of Spanish territory (SPC 1960, see Figure 3). As the 1960s advanced, the leadership in creating new self-service retail outlets was in the hands of the voluntary chains such as SPAR, Végé (1960), IFA and IGA (1967), VIVO (1968), CENTRA (1971), and VIVO-Una (1974), which, because of their characteristics as franchises, spanned the entire territory.

Adriaan van Well, the visionary Dutch wholesaler when SPAR was introduced in Spain, Madrid May 1, 1960. Source: SPARCO, 3 (1960).

The reasons these businessmen were excited by this franchise was that they considered it a tool within reach of many small and medium-sized businesses that might have been short of capital but that were very aware of the need to modernize Spanish food distribution and its potential business opportunities. During this early stage, these businessmen were the most effective tool in transferring knowledge throughout the business sector (direct knowledge transfers), especially because of the capacity for technical and professional training offered by their collaborative structures to their associates. A Ministry of Trade and Tourism report was very expressive in this sense:

Since their introduction in 1959, voluntary chains have significantly contributed to the transformation of many traditional businesses through spreading new technology, new ways of selling (this was one of the basic engines of the transformation of small shopkeepers into self-service outlets), better means of management and commercial organisation and training of personnel employed in that sector, etc. (IRESCO 1978, p. 117)

In the year 1970, voluntary chains comprised over two hundred central wholesale depots, a warehousing area that exceeded 600,000 square meters and approximately 62,000 associated retailers (IRESCO 1977, p. 48). However, despite the expansion of these franchises, the spread of self- service was very slow. There were 8,678 self-service outlets, supermarkets and hypermarkets in Spain in 1975 (of which 6,178 had sales areas between 40 and 120 m2, 1,636 between 120 and 400 m2, 314 between 400 and 2,500 m2, and 10 more than 2,500 m2). Many supermarket multiples began to appear in the 1960s, but they still maintained a very local character until the beginning of the 1980s and had little impact on larger markets (i.e., Caprabo, Barcelona; Sabeco, Saragossa; Cruz Mayor, the Canary Islands; Eroski, the Basque Country; Vegonsa, Galicia; and Luis Piña, Andalusia) (IRESCO 1984, p. 40; Maixé-Altés 2009b).

A third, albeit minor current of diffusion followed the entrance into Spain of some Cuban businessmen and Mexican family firms. These arrivals knew the North American model very well (Moreno Lázaro 2012). Among the Cuban expatriates, Cesar Rodríguez, José Fernández and Ramón Areces stand out, being key men in the development of two important department store chains: Galerías Preciados and El Corte Inglés (Cuartas 2005; Toboso 2001, 2007). Also from Cuba, José M. Mayorga, his cousin Valeriano López, and both their wives, the Waddington sisters, founded SIMAGO, the popular department store chain, in 1960 (Castro 2010). Mexican businessmen of Spanish origin who settled in Spain in the 1960s include Jaime Jorba (Bimbo) and Plácido Arango (Aurreá Supermarkets) (Moreno 2010; Moreno Lázaro 2012).

Despite these three currents, however, the overall diffusion of new practices in Spanish food retailing in the 1950s and 1960s was modest, especially in relation to what was happening in more developed Europe.

New Formats

CAT authorized on average 282 self-service establishments a year in the first half of the 1960s and 797 in the second half of the decade. In the first half of the 1970s, the annual average grew to 1,011 establishments a year (MC 1971, 1974). This slow pace reflects the rare incidence of the new retail formats, with the only exceptions being SIMAGO and the department store chains (Castro 2010; Gómez Mendoza 1984). The case of SIMAGO deserves special attention for two reasons: it was the first chain of popular stores with a national reach to introduce supermarkets into its establishments and, moreover, it soon became the bridgehead of French capital investments in Spanish distribution (Castro 2010, 2011). In 1963, three years after its creation, it had four establishments, some 3,500 square meters of sales area (branches in Madrid, Santander, Oviedo and Gijón) and obvious management problems (LSA 1973). José M. Mayorga, president of the chain, chose to seek advice from a European leader of popular stores, the PRISUNIC chain (Caracalla 1989). The response was very positive, and collaboration was implemented through a subsidiary of PRISUNIC, the consultancy firm Paul Planus. Jean Pierre Dollberg, consultant and advisor with the PRISUNIC subsidiary, after a few months of study and faced with the company’s delicate financial situation, proposed a shock plan to get the accounts into shape and rationalize SIMAGO’s client and supplier relations (LSA 1973), interview with Pierre Dollberg, see Figure 4). In June 1963, both parties reached an agreement, French capital entered the company, and French managers took over strategic control of SIMAGO (FBU-SAR1963). As a whole, the decisions made by SIMAGO’s owners were a consequence of the high managerial transaction costs in the Spanish market.

Jean Pierre Dollberg, CEO of SIMAGO in the mid-1960s. Source: LSA, 1036 (1986)

The new managers had to rely on all of their experience in the sector to ensure that the project was successful. In the words of Dollberg himself, “Knowing the future is terribly useful, we have saved much time” (LSA 1973). In fact, his team reached the conclusion that the Spanish market was some ten or fifteen years behind the French one. They once again confronted an environment previously experienced by PRISUNIC in France, although now intensified by the particular idiosyncrasies of Spanish retailing.

The new management team followed a strategy of diversifying and applying marketing techniques that were little known in Spain. A new market culture was gradually introduced when the knowledge management and learning processes within the company eventually reached the Spanish retailing industry. The new group was made up of eight firms that spanned a wide range of activities (SIMAGO, Grandes Almacenes Populares or GAPSA, PRISUMA, SICOMI, Restaurantes Técnicos, OGAMIS, and HOGARAMA). Its establishments had an average sales area of 1,000 square meters and were divided in equal parts between grocery and the rest, with some 1,500 references that maximized the brands themselves, SIMAGO and TAURO (FBU-SAR 1974). Using “everyone under the same roof” techniques that had already been experienced in France, the group introduced a soft discount, strengthening its support for fresh products. The strategic turn was a success: SIMAGO went from 3,500 square meters in sales area in 1963 to nearly 150,000 ten years later (LSA 1986).

Modern Marketing

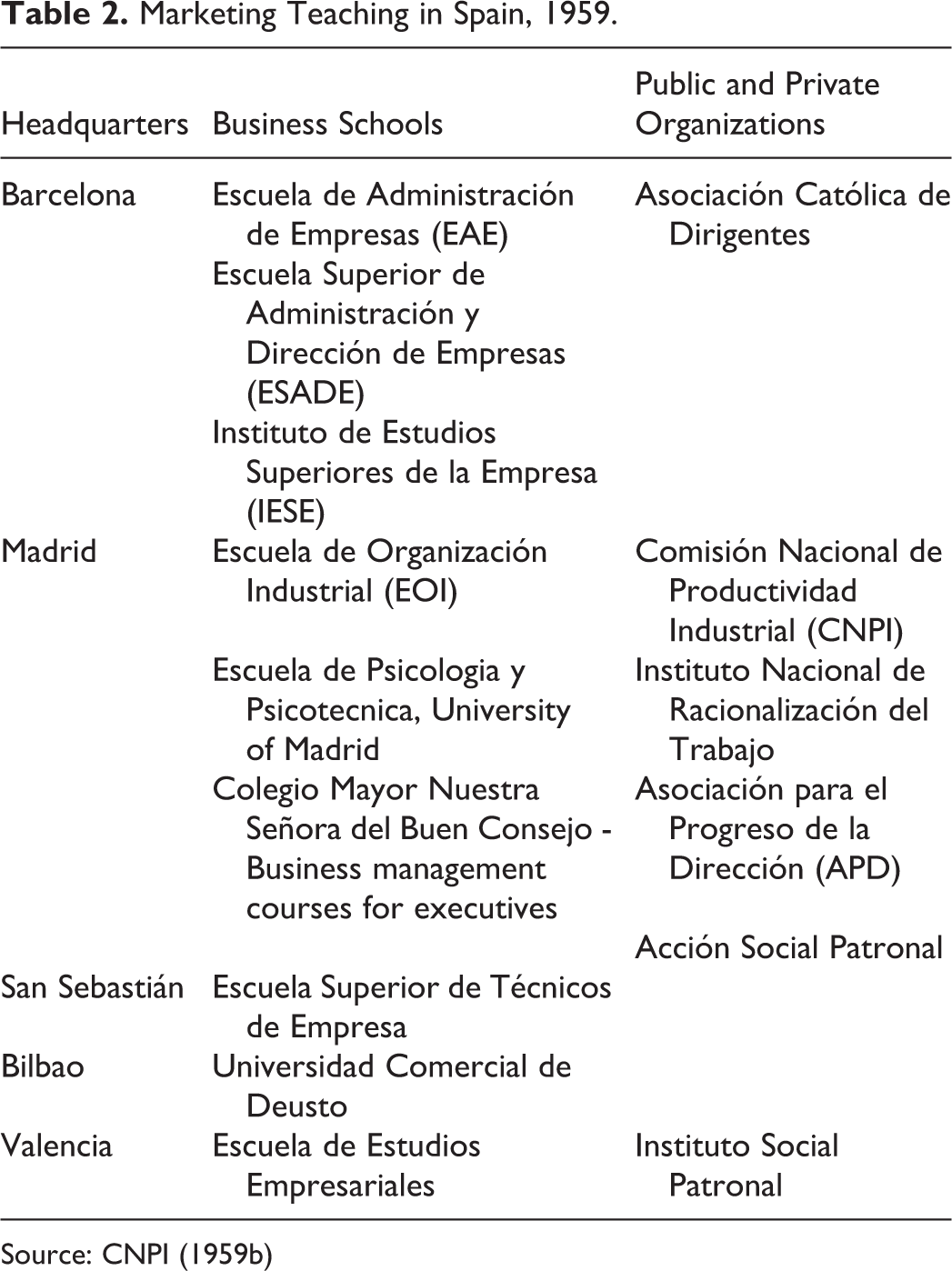

One piece of evidence of the gap between Spanish and European retailing was the difficulty in introducing modern marketing techniques. As Garcia Ruiz (2007) showed, the spread of marketing ideas in Spain encountered cultural resistance, and a lack of know-how slowed down the process. The role played by the CNPI and later by marketing clubs that extended throughout the entire country constituted a first step toward modern marketing practices in Spain. It is worth mentioning the progressive ideas that teaching marketing had introduced in the various public, business, and social institutions. Initially, it carried little weight in the university environment, as shown in Table 2. At the end of the 1950s, centers were located in Barcelona, Madrid, the Basque country, and Valencia, coinciding with the most developed areas and with the country’s greatest business traditions. University studies of advanced marketing developed as the 1970s progressed, in both public universities and private centers (see Puig 2003).

Marketing Teaching in Spain, 1959.

Source: CNPI (1959b)

The data available through the 1950s suggest that for the first time in Spain, a group of business leaders emerged who were integral to an informal retail community of practice (Wenger and Sneyder 2000). Some of the members of this group were linked to the CNPI’s initiatives and the study trips to Europe, where they had their first contacts with representatives from SPAR Europe. They included future multiple retailers and major businessmen, such as the Elosua family firm, the Pascual brothers, Ventura González, Fernández de Cossio, and Sainz, to name but a few. Others belonged to groups that had promoted the first steps toward modern marketing management in Spain at the start of the 1970s by collaborating with the CNPI and the Chambers of Commerce of the main Spanish cities, i.e.: Asociación para el Progreso de la Dirección (APD) [Association for the Progress of Management], marketing clubs and advanced marketing teaching] (ACCM 1953-1960; SPC1960-1965). Similarly, the American Chamber of Commerce in Spain collaborated with the managers of the U.S. National Sales Executives. They also organized an Annual Distribution Conference, while the American Marketing Association promoted the Annual Marketing Conference (Garcia Ruiz 2007; Puig and Alvaro 2004).

In conclusion, the 1960s witnessed the first steps in economic development and the gradual emergence of factors that promoted the modernization of commercial practices. However, this combination was not sufficient to cause structural change in the outdated Spanish grocery retailing sector. Businesses would have to wait for the arrival of the FDI in 1972 for such a change to occur.

FDI: A Catalyst for Spanish Food Retailing in the 1970s

In the early 1970s, while Spanish income per capita was converging with those of more developed countries, the economy suffered from a crisis. Neither economic policy nor business responded flexibly to the new economic parameters following the rise in oil and raw material prices, as well as changes in world demand, which came about in the years 1973 and 1974. The reasons were twofold. On the one hand, the economy was protective and characterized by state intervention, and thus was not able to respond to market forces. On the other hand, the economic crisis coincided with the end of one political regime and the transition towards another very distinct one.

The Lack of Legislation

A regulatory desert confronted the arrival in Spain of the first French hypermarkets in the 1970s. In fact, no specific regulations gave them legal security (IRESCO 1978). There were two issues in this situation. First, the legal vacuum converted Spain into a very receptive market despite the lack of legal security, because the Spanish market had been converted into a “blank slate” where foreign capital could enter without restrictions. Second, the ground was already prepared for the arrival of French firms. French retailing had a scouting party in SIMAGO, which had introduced modern distribution 10 years earlier (see Figure 5), a “human tide” of 10 million potential customers, and the most liberal legal framework of Europe (PV 1981). In this context, Huang and Sternquist’s (2007) analytical framework explains the French entry choices, taking into consideration both Spanish and French institutional environments (Burt 1991).

A SIMAGO store in Madrid in the early 1960s, the predecessor of later hypermarkets. Source: authors

During the second half of the 1970s, within a context of intense institutional change caused by the arrival of democracy, the first small steps were taken towards planning the domestic market. Decree 300/1978 designed a new framework for managing commerce and the domestic market, accompanied by autonomous bodies such as the Instituto de Reforma de las Estructuras Comerciales (IRESCO) [Institute for the Reform of the Commercial Structures] and the National Institute of Consumption. This reform, without doubt, had good intentions, but it did not adapt to the rapid changes that were occurring in the sector: the arrival of the FDI, the territorial opening of multiple retailers, and department store expansion and diversification. The circumstances derived from the economic crisis conditioned the regulatory processes at the end of the 1970s and for most of the 1980s. As an example, we only need to state that the Spanish domestic market at the start of the 1980s was subject to the application of tariff quotas, both products and factors of production (Barceló Vila 1981).

The institutional conditions of the Spanish market gave advantages to new stores since, unlike in most European countries, there were no restrictions on opening new establishments. French investors knew they had to hurry before the legislation became more restrictive. In the words of Dennis Defforey, cofounder of the French group Carrefour: “…stupidity is contagious” (LSA 1978). Defforey was referring to the consequences of 1973 French commercial legislation for his shops. The presence of French capital in SIMAGO since 1963 had established the basis for French investors to be able to consider new projects at the start of the 1970s, such as bringing the concept of the French hypermarket to Spain. SIMAGO looked for French partners for this adventure, PRISUNIC and Euromarché, which brought their know-how to the store. Later, one of the greats of French and European distribution, Carrefour, incorporated itself into the Spanish market via a series of strategic alliances (Castro 2010).

The Firsts French Hypermarkets

On July 19, 1973, SIMAGO and EUROMARCHÉ opened the first hypermarket in Spain in the locality of Prat de Llobregat (Castro 2010), very near Barcelona, next to the Mediterranean motorway and the access road for French tourism on the Spanish coast (DA 1974). Confirming forecasts, half of the clients were tourists in the first four months after the hypermarket’s opening. In October 1973 the first Carrefour in the country opened its doors, half a kilometer from the first hypermarket and also very near the motorway. The regulatory framework was, in this case, of great importance. It is, therefore no coincidence that the first Spanish supermarkets were located near the motorway.

The entry of the hypermarket promoted by SIMAGO into the Spanish market precipitated Carrefour’s strategic decision, although the company was also interested in an emerging market such as Spain’s (LSA 1975). Carrefour imported its staff: the entirety of the new center’s middle and top executives was French (LSA 1974). Thus, there apparently was no great dissemination of managerial innovation among Spanish managers, at least in this specific case and in this first stage of French FDI in Spain. This situation was very remote from that suggested by Kacker (1988) and Getler (2001) noted above.

After the first months, activity in both stores declined and sales did not meet expectations as a consequence of accumulated strategic errors (Lhermie 2003, p. 35; DA 1976). Obviously, the economic crisis, accompanied by considerable inflation peaks did not help. However, as Marcel Fournier revealed (LSA 1975), market studies and clientele analyses were overly optimistic about the working classes as a customer base for Carrefour.

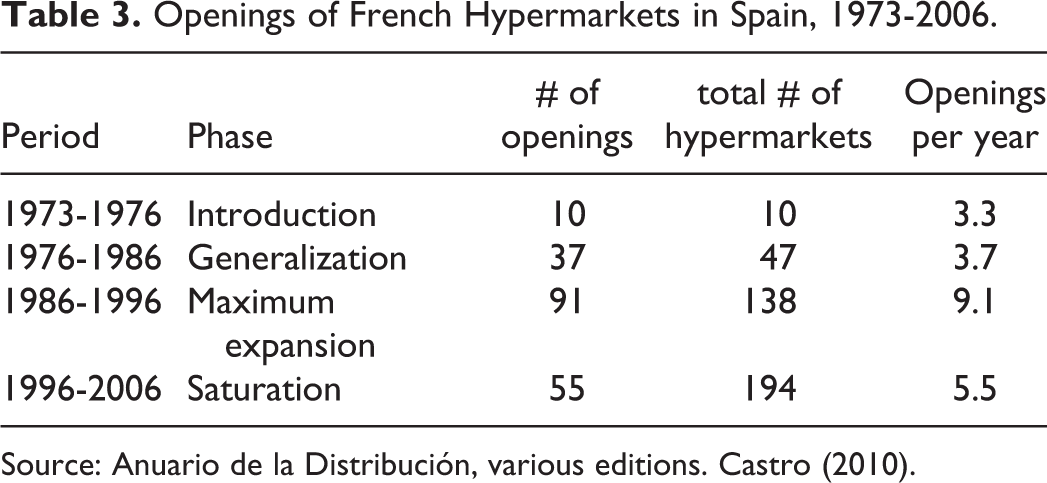

In Spain in the 1970s, the real clientele belonged to the upper middle class, a segment with access to motorcars, but these consumers were not willing to make purchases in warehouses (Sordet and Wantz 2005). Spain’s market was not as simple to enter as French operators had supposed. Effectively, there was no competition in the hypermarket sector, but there was also no culture of large retail spaces. Moreover, in food distribution, competitors began to grow with new concepts such as proximity stores. All in all, the capacity of Spanish clientele to adapt to the new trend, including in Catalonia, had been overestimated. There, presumably, the area’s higher income levels should have promoted greater penetration. Despite this, the agents were convinced of the projects’ future potential (LSA 1978). In fact, between 1973 and 1976, seventeen hypermarket projects were launched, mainly located on the coast and supported by the Mediterranean motorways, of which only ten were completed (see Table 3, AFCCM 1973-1976).

Openings of French Hypermarkets in Spain, 1973- 2006.

Source: Anuario de la Distribución, various editions. Castro (2010).

In these years, Carrefour consolidated the objectives that, as a group, they had established previously in France: decentralization and self-financing. Decentralization involved each hypermarket, from the departments to the providers. This philosophy extended to the suppliers’ who had to deliver the goods to centers and wait to be paid. The idiosyncrasies of paying providers in Spain, such as 120-day payment terms, favored the short-term financing of the hypermarkets. Less than 15 percent of the cost of the 11 new hypermarkets opened by Carrefour was financed by bank credit (PC 1983). Finally, to Hispanicize the brand, the holding company’s management created a new brand, PRICA (an acronym of Precio y Calidad [Price and Quality]), again taking the name of a supermarket chain from the sixties (LSA 1980a; FBU-ARPS 1964-1967). Carrefour’s managers apparently learned from their “strategic experiments” in their first stages in the country, to use the terminology of Sawhney, Wolcott, and Arroniz (2006).

In 1976, another great name in French distribution arrived: Promodès. This French holding company carried out a detailed study of the market based on prudence and knowledge of the errors committed previously by its competitors. Thus, the first Continente hypermarket of the group in Alfafar (Valencia) was born. Its offerings were directed to clientele with high incomes. The results were stable and less seasonal than those of its Carrefour predecessors (LSA 1990). Its expansion policy was based on serving the urban nuclei on the Mediterranean coast and on access to the provincial capitals of the inner peninsula (Sordet and Wantz 2005), and they also committed to a multi-formed culture from the nearest supermarket to the hypermarket (LSA 1987)).

Promodès’ policy in France had been the soft discount (Shopi, Banco or huitàhuit). However, Paul-Louis Halley, the president of Promodès, wanted to apply in Spain the German hard discount model, based on offering a single brand and prices that were up to 30 per cent below average. In 1979, the first DIA supermarket opened in Madrid, the result being a hybrid between the soft and hard discount, that is, a smaller discount and a not overly extensive assortment of well-known brands (Sordet 1997). These circumstances suggest the role of the recipients of innovations that incorporate adaptive and processing capacities (appropriation) (Alberts 2010). A suitable franchising policy favored the expansion of that model since Promodès understood that conducting business in Spain required more diversification. Hence, the Promotora de Centros Comerciales Centros Shopping came about in 1978, creating the first Spanish malls. Its impact was fundamental for the construction of the country’s first official commercial center, Baricentro, which opened its doors in Barberá del Vallés (some 15 kilometers North of Barcelona), in April 1980 (LSA 1980b).

Another factor worth mentioning is the role of the major multi-national food producers in the sector’s growth in Spain. Unilever, for example, supported the expansion of supermarkets and hypermarkets throughout the 1970s and the 1980s (Jones 2005, pp. 140, 301). These firms wanted to take advantage of the growth of large stores as a means to access the emerging middle classes, having learned from the early disappointments of French hypermarkets. This trend was boosted by Spain’s entry into the EEC on January 1, 1986.

This first advance in international investment in Spanish retail was characterized by some peculiarities:

Regulation in the domestic market was minimal. This favored entry, but the lack of clear rules made access difficult. These circumstances were, in certain ways, different from other European cases (Morris 1999; Shaw et al. 2000). Regulatory conditions in France affected the movement of capital to Spain. The 1973 Loi Royer (Royer Act) promulgated December 17 helped to halt the expansion of hypermarkets in order to protect traditional commerce. This was one of the reasons for the international expansion of major French distributors (PV 1981; LSA 1973). Retail know-how and the modernization of managerial activity had been lagging when the French arrived. Only with the advent of Promodès and the consolidation of PRYCA (Carrefour) was the basis of the French retail model transferred to Spanish counterparts. This was connected to the French retailers’ market entry strategy (direct investment) and to the managerial decisions that paved the way in the early years. In turn, this could be related to how the French retailers managed asymmetric information and to agency theory, which played a role in Spanish firms’ evolution in the 1980s and 1990s (Doherty 1999).

Consequently, this first stage of the FDI in Spain had substantial importance for the regulatory conditions on both sides of the investments (Cho 1985). These diverging conditions (regulatory excess in France and by default in this first stage in Spain) had fed the receptivity of the Spanish market just as Tschoegl (1987) noted. That is, they favored opening up Spanish markets to French capital, the influence of which was the main factor in modernizing retailing in this period. A final aspect to consider is the prematurity this movement, which was ahead of what was usually called second globalization. Proximity, prior knowledge of the market, and regulatory pressure at home meant that the French led other international investment in Spanish retailing.

Global Models

The expectations created around Spain’s membership in the European Market explain much of what happened in the beginning of the 1980s and 1990s. The improvement in business expectations accelerated economic growth in the first years after Spain’s EEC membership. During the period from 1986 to 1988, the gross formation of capital increased to an annual average rate of 14.1 percent in real terms, double the average growth of investment in the OECD countries during this period. The gross formation of capital that in 1985 was approximately 19 percent of the GDP grew to approximately 26 percent of GDP in 1989. This demand growth increased GDP, in real terms, by 4.8 percent annually. Furthermore, Spain's production increased in just four years by nearly 20 percent in real terms, moving closer to the average for the European Community. Spanish income per capita, which in 1985 was 71.8 percent of the average income per capita of the EC, increased rapidly to 75.9 per cent in 1989. After this fast growth, Spain’s economy joined in the settled-down global economy of the 1990s.

New Competitors

The arrival of French hypermarkets meant a strong and salutary lesson for Spanish distribution that accelerated its modernization and its convergence with Europe. Between 1980 and 1981, Spanish capital entered, as did a new French competitor, in the hypermarket sector. In October 1980, the first Hipercor was inaugurated in Seville, promoted by El Corte Inglés, the Spanish department store chain that was founded after the Civil War. Similarly, the Basque cooperative group Eroski (created in 1969) began to diversify its activity as a multiple retailer, opening its first hypermarket in 1981 in Vitoria (Cuesta Valiño 2005). Both companies embraced the teachings of the French pioneers. Innovator-imitator transfer explains this diffusion process in evolutionary terms. Furthermore, the 1980s were also a period when contractual groups, such as Euromadi and IFA, began to grow and could use members’ local knowledge of trading conditions (Dobson, Waterson, and Davis, 2003). Finally, in February of that same year, Gérard Mulliez’s group created the first Spanish Auchan in the industrial area of Utebo in Zaragoza, jumping on the bandwagon as General Motors was settling in the region (LSA 1981). The new branches Hispanicized their banner under the name of Alcampo, developing a policy as a family business that was different from other competitors: diversifying and Hispanicizing the supply, another means of “appropriation” (Gobin 2006; DA 1992).

The outlook of Spanish retail near the time of Spain’s entry into the EEC was quickly changing. As stated in a report by the French embassy in Madrid, although the Spanish market presented difficulties for French distribution companies, Spain’s imminent entry into the EEC would change the rules of the game (FEM 1985). First, the number of competitors increased, and multiple Spanish retailers began regional and extra-regional expansion. The economic growth of the 1980s and 1990s was accompanied by increased urban populations, which, along with other variables, favored the spread of modern large distribution. The powerful development of mass consumption that was generated in Spain’s economy was not directed exclusively at hypermarkets. The greatest market share belonged to supermarkets. Between 1980 and 1995, they virtually doubled their sales every five years (Maixé-Altés 2009b). In the whole of Europe, only Italy had a comparable trend (see Table 4).

Number of Establishments in Europe, 1971-2001.

Sources: General report on domestic commerce in Spain, Ministry of Commerce and Tourism, IRESCO, August1978 (Statistical annexe nº 35). Eurostat (1993). Euromonitor (2002)

* Federal Republic of Germany before 1990.

The arrival of the European Economic Area ushered in a new stage of growth that demanded new capital to finance expansion. In the case of PRYCA and Promodès, their financing came from entering the equity market, which was an extraordinary innovation for Spanish retailers. Alcampo, being influenced by its corporate culture, did not resort to equity financing. The Auchan group took advantage of the opening of new shopping centers—the third generation of commercial centers—to become one of the main instigators of retail “category killers” in Spain (Leroy Merlin, Decathlon), (LSA 1992). These new formats, accompanied by new plans for urbanism, were part of extensive diversification processes.

In 1994, a new exogenous factor attributed to FDI changed corporate methods: the arrival of the German hard discount model. Between 1994 and 1995, the German groups Tengelmann (Plus Supermarket), Lidl, and Rewe (Penny Market) arrived in Spain, all with a powerful growth strategy that impacted the structural collapse of the Spanish market, which, from the first appearance of modern formats, had not cultivated the hard discount ( País 2005, pp. 37-39). Lidl, the most active group installed over 200 establishments in less than two years. Tengelman followed with over 80 in the same period. From here on, growth expanded rapidly (Cuesta Valiño 2005).

Although the market penetration of the new format was not as revolutionary as its competitors had anticipated, it certainly piqued the interest of traditional business and trade groups (Interview with Javier Campo, Director General of DIA from 1985 to 2007, Madrid, March 25, 2010). For the very first time, the Spanish market began to show signs of saturation. On one hand, the retail market incorporated increasingly global competitors, but on the other, the regulatory frame became more restrictive.

The growing pressure on traditional commerce (especially in Catalonia), among other factors, led to the passing of new regulations that implicitly favored supermarkets by limiting stores to 2,500 square meters. A national act (Act 7/1996, 15 January) regulated retail trade similar to the French Royer Act of 1973 and thus reduced the attractiveness of the Spanish market. Alongside this act, Organic Act 2/1996 came into force, largely maintaining the tradition prior to 1996, which had left the regulation of retail trade in the hands of regional governments. The result was rather heterogeneous legislation at the national market level compared with the retail sector. Consequently, the new regulations, which for the first time had set guidelines for the retail trade, meant that growth strategies in the Spanish market turned towards mergers and acquisitions.

What Is Spain’s Place in the Global Retailing Scenario?

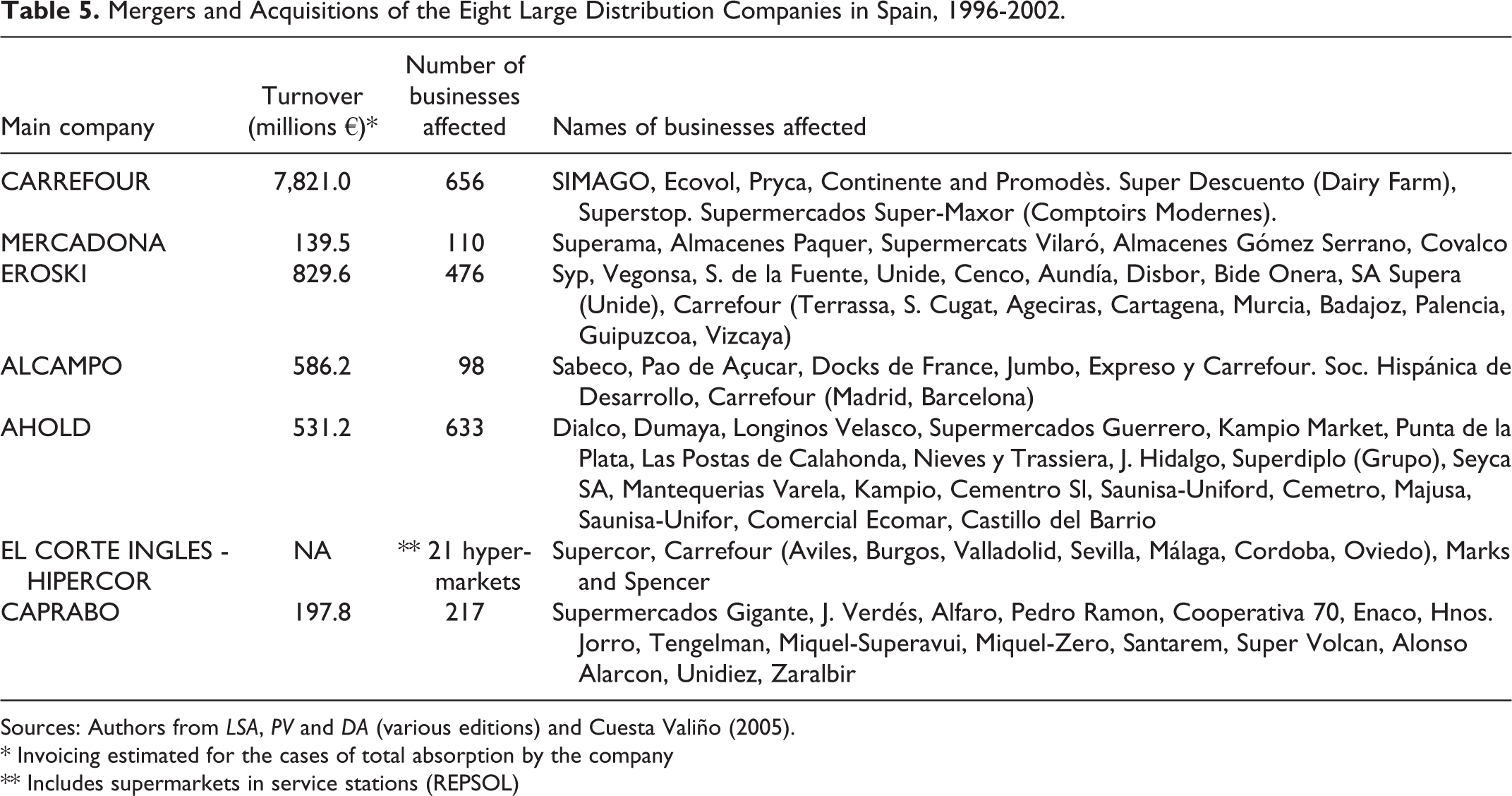

Table 5 shows the increasing concentration in the distribution sector. As was happening in other sectors of the Spanish economy, commercial distribution companies responded to market changes by growing. This increase was characterized by greater recourse to external means of growth (Cruz Roche 2012). In 1992, the top thousand companies invoiced almost 24 billion euros. Five years later, just the top 25 companies in the sector had this volume of turnover. However, concentration had still not yet reached the levels of 2005, a year when 66.1 percent of sales was controlled by eleven distribution groups and five companies controlled half of the market. In contrast, in the years when the number of large Spanish companies was declining, French distribution continued to have huge weight, not only in Spain but also elsewhere in Europe. Nor was the access of new multinationals (such as Leader Price and Royal Ahold) into the Spanish market by any means negligible. However, the processes of concentration were more advanced in the rest of Europe. Without a doubt, one of the most significant changes with repercussions for Spain was the Carrefour-Promodès merger in 1999. Corporate movements in Great Britain, Germany, Switzerland and the Netherlands resulted in lost positioning in the ranking of some Spanish companies.

Mergers and Acquisitions of the Eight Large Distribution Companies in Spain, 1996-2002.

Sources: Authors from LSA, PV and DA (various editions) and Cuesta Valiño (2005).

* Invoicing estimated for the cases of total absorption by the company

** Includes supermarkets in service stations (REPSOL)

Widening and extending markets and the evolution of food consumption had profound implications on the structure of distribution chains at the end of the 20th century. Increasing business concentration, internationalization, and horizontal and vertical competition contributed to this evolution (Colla 2001, pp. 7, 47). The integration of wholesale functions within retail companies caused the disappearance of most traditional food wholesalers. The development of horizontal competition occurred as a result of a business policy that had more impact on service differentiation than on final prices. Finally, vertical competition continued to grow in the intermediary markets in which large distributers had high negotiating power with manufacturers and suppliers (Méndez and Ouviña, 2002).

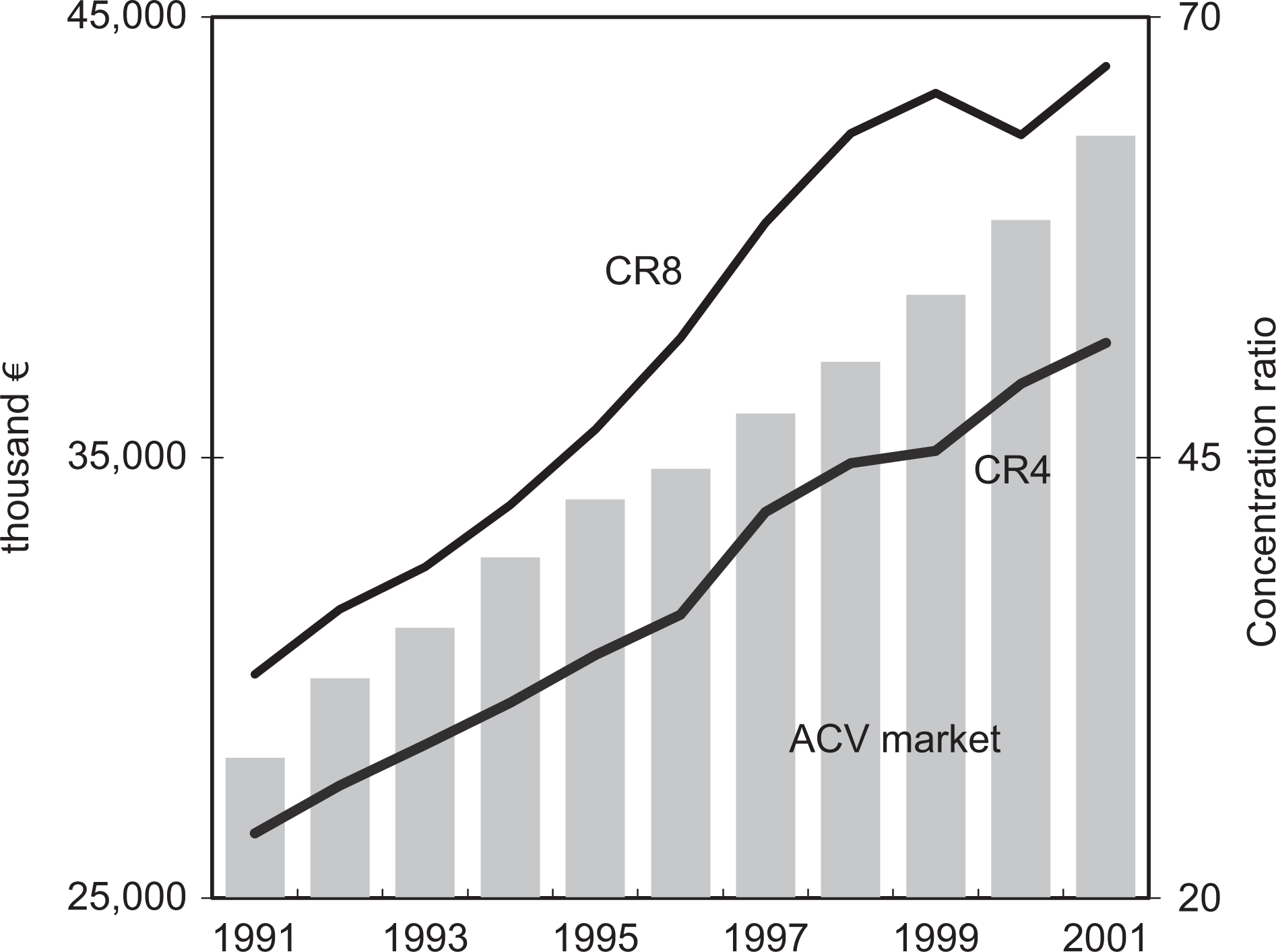

All in all, growing concentration stood out most in this final period of Spanish food distribution before the recession of 2008. If we analyze the concentration of packaged product distribution using Nielsen’s all commodities value (ACV, fresh food products are excluded in this analysis), we obtain interesting results (see Figure 6; Cruz Roche, Rebollo Arévalo, and Yagüe Guillén 2003). These data highlight the notable rise in concentration, duplicating the concentration ratio for the fourth and eighth largest distribution companies. Spain was close to the European average, but continued to show strong disparity. In 2001, for instance, the concentration in Spain’s ACV market was 45.6 percent (three large distribution companies), which placed it ahead of Italy and Greece and behind Portugal, Ireland, Germany and the United Kingdom with a quota between 55 and 50 percent. Sweden led with 95 percent concentration (Nielsen directory).

Evolution of business concentration in the ACV market of high consumer products in Spain, 1991-2001. Notes: ACV, all commodity value. CR4 and CR8 are concentration ratios, the fourth and eighth largest companies in the sector respectively. Source: Nielsen.

Companies’ policies differed from one another. However, the backdrop was the depletion of a model based on the hypermarket. The most notorious case is that of Mercadona, the Valencian supermarket chain (the Roig family’s firm) that began to expand at the end of the 1980s. Favored by the 1996 legislation, it expanded throughout the whole of Spain until it became first in the supermarket sector, ahead of the large French chains and Eroski. This company settled on a hybrid system: it developed an internal growth policy based on opening new establishments (it invested in large supermarkets and disinvested in hypermarkets) and also implemented a discount strategy with its own brands, a positive image, market knowledge, and extreme control over its suppliers (Audicana Arcas 2002; Ton and Harrow 2012). Mercadona provides a characteristic example of the adoption of retail practices and the recipient’s transforming capacities. However, other companies, such as the Dutch Ahold, pursued very aggressive foreign take-overs, buying chains of establishments with large market share. In turn, the cooperative group Eroski’s growth strategy combined internal and external growth via a policy of alliances with regional supermarket chains. Mercadona’s progression impacted Carrefour and Alcampo. Both groups imitated some of the domestic competition’s strategies by diversifying and deepening their relationships with suppliers.

Including wholesale functions also strengthened he concentration of retail distribution. Large companies followed two different strategies on this matter. Multinationals such as Carrefour and Auchan, whose base was the hypermarket, integrated wholesaler functions, creating specialized companies that guaranteed supply at European levels (e.g., fresh fruit and vegetable products). Other companies (especially leaders in the supermarket sector) created purchasing groups. Thus, purchases of companies associated with the center were unified, and other flows of communication (transport, warehousing, payment) were managed.

It is worthwhile to point out the supranational character of European purchasing centers (Copernic, ALIDIS, Carrefour, Metro, Tesco, Schwartz Group, Auchan, IRTS and Ahold). The two leading centers, Coopernic and ALIDIS, with over 100 and 80 million euros invoiced, respectively in 2007, were alliances that were conceived in the middle of the first decade of the 21st century (Nielsen and Alimarket). Coopernic (Colruyt, Belgium; CONAD, Italy; Coop, Switzerland; E. Leclerc, France and REWE Group, Germany), with its headquarters in Brussels, is a group of groups. Created in 2006, it joined five large independent European food distributors, four of which were cooperative companies that represented small retail organizations. In turn, ALIDIS, the alliance formed by the Spanish cooperative Eroski, the French group Les Mousquetaires, and Edeka (Germany), acted as a European purchasing center. These new centers were constituted vertically and enjoyed autonomy from alliance members in their procurement decisions.

Therefore, Spanish distribution did not escape the two phenomena that most affected Western economies: concentration and globalization. However, Spanish companies have only made relatively small advances and still have a long way to go in terms of both concentration and access to external markets. Even with their active participation in global retailing, Spanish companies do not seem to opt for internationalization. Only Corte Inglés sketched out an entrance process in Portugal and Eroski in France, where the latter in 2006 already had 4 hypermarkets, 18 supermarkets, and 17 petrol stations. That very year it invested 14 million euros in a new hypermarket, although in this case, the group’s entry into the French market resulted from its intervention in a troubled French cooperative. In turn, the Galician chains of Gadis and Froiz took advantage of their proximity to the northern region of Portugal to begin their penetration in this market. Mercadona and Coviran also showed a similar interest. Nevertheless, the internationalization of Spanish food distribution companies was not as pronounced as that in apparel, for which firms such as Inditex (Zara), Cortefiel, and Mango managed to situate themselves in the main European cities. The paradigmatic case is Inditex, which has expanded over five continents.

Conclusions

Studying the Spanish market over its fifty-year history has provided a framework for understanding the factors that have contributed to the structural change in food trade markets in peripheral Europe. The starting point is that the Spanish economy offered significant opportunities. From a peripheral position in the 1960s and 1970s, Spanish grocery retailing accelerated its convergence with Europe and incorporated itself into second globalization through intense structural change. Two main factors for analytical purposes have been considered: on the one hand, the role of innovations and on the other, institutional factors such as regulation, market structures and FDI. A holistic component, inherent to the historical and institutional approach, and a marketing approach also informs our analysis. This conceptual point of view falls within a social and cultural framework in which change occurs.

The diffusion of new retail practices did not occur widely in early Spanish grocery retailing. The spread of marketing ideas encountered cultural resistance and business leaders who could be considered part of an informal modern community of practice would truly constitute a diffuse network. Nevertheless, starting in the 1970s, FDI provided a salutary lesson for the domestic market and its retail practices.

Herein, we chose to focus on innovation in retail formats. The role of innovations was significant, but in the least developed countries, the spread of innovation and technological and knowledge transfers relates to the concept of “appropriation,” an approach that emphasizes the recipient’s adaptive capacities. The Spanish case, comparable to the situation in other peripheral Mediterranean countries, is an example of how the host country “borrowed” outside influences and made them its own, creating hybrids, such as Mercadona, that were more suitable to its own market. The cases of supermarket chains such as DIA or Mercadona are paradigmatic.

The introduction of these modernization factors into lagging peripheral markets sustained itself on three pillars: the economic situation, the institutional framework, and foreign influence. The most obvious factor is the actual evolution of the Spanish economy. The moments of greater expansion were accompanied by growth in income per capita. These conditions favored the expansion of the country’s commercial fabric in volume and diversity. In fact, until the “desarrollismo” (policy of economic development) of the 1960s, self-service did not exist in Spanish cities. Similarly, it was the country’s entry into the EEC that favored the development of French hypermarkets on Spanish ground.

The institutional framework and foreign influence played a role that either amplified or reduced the effects of economic growth on Spanish distribution. The state created favorable institutions in the first case and accentuated its interventionist policies in the second. These are the factors that permitted varying the receptivity of Spanish grocery retailing (that is, the level of its opening as a recipient economy). For example, diverging regulatory conditions in France and Spain had directed French capital toward the Spanish market in the 1970s, while new regulatory conditions in the mid-1990s reduced the attractiveness of the Spanish market.

The subjects that have been presented suggest that the institutional framework was more of a hindrance than a stimulus in modernizing the sector. Foreign influence and the modernization it engendered was the third protagonist in this history. Very soon, foreign agents, who were not always investors (before the 1970s, they had operated as instruments of knowledge transfer rather than direct investors), ended up being attracted by a market of over thirty million consumers similar in cultural terms. Beginning in the 1960s, companies such as SPAR and SIMAGO initially and Carrefour and Continente later positioned themselves for the Spanish market. The market was less docile than was estimated by foreign agents, owing to the presence of both archaic commercial structures and native competition. The arrival of FDI and globalization allowed latecomer companies and the retail industry to develop new strategies towards emerging networks. On the one hand, innovator-imitator transfer explains the new dissemination process in evolutionary terms. On the other, some Spanish contractual groups began to grow using members’ local knowledge of trading conditions, and foreign firms “Hispanicized” their offerings. Once local competition developed, the market widened and competition grew. The case of Mercadona, which owed its growth to the legislation in the mid-1990s, is probably the most significant.

This article shows that foreign companies were the first vehicles in modernizing Spanish commercial structures. Moreover, they favored the later insertion of these structures within a global market (in logistical rather than commercial terms). Spanish companies learned from these foreign influences and even surpassed them, although Spanish food retailing had still not considered internationalization a viable strategy. Eventually, it appearrf that peripheral Europe was more sensitive to FDI than was developed Europe.

The history presented here can help us learn about the endogenous and exogenous processes that contributed to modernizing food distribution in Mediterranean Europe. Comparative analysis of other countries, such as Italy whose food distribution also took a while to modernize itself, or Portugal and Greece, whose modernization processes lagged even further behind, can provide even more perspective.

Footnotes

Notes

Acknowledgments

Both authors would like to acknowledge comments from Fredrik Sandgren and the rest of participants at the Session “Structural Change in the Distributive Trades in the Long Run: The Impact of Innovation and Institutions” at the 17th European Business History Association Congress in Uppsala, Sweden. They also thank editor Terrence Witkowski for the comments received and in the refereeing process that have improved the article. The usual caveats apply.

Declaration of Conflicting Interests

The authors declare no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The first author acknowledges the financial support from two MEC grants (Ministry of Economy and Competitiveness), Award number HAR2010-18544, sub programme HIST and HAR 2013-40760-R. The second author also acknowledges MEC support (ECO2012-35266) and CEMU 2012-034.