Abstract

Research on entrepreneurial marketing is now fairly common, and macromarketing is an established field. However, studies that incorporate variables of interest to both entrepreneurial marketing and macromarketing scholars are scarce. In the spirit of the special issue, this study crosses disciplinary boundaries in order to investigate how a macro-level policy variable (i.e., excise taxes) affects a key marketing variable (i.e., product quality) in a sample of small firms (i.e., microbreweries). The results of the study support Barzel’s “flight to quality” hypothesis. We conclude that high excise taxes invite quality-based competition. Furthermore, entrepreneurial microbreweries appear to recognize the flight to quality, and they capitalize on the opportunity to bring relatively high quality products to market. Implications for entrepreneurial marketing researchers, macromarketing researchers, and public policy are discussed.

Introduction

Entrepreneurs face many obstacles when creating and running small businesses. In the United States (U. S.) brewing industry, major obstacles often take the form of regulation. Microbrewery owners face a challenging regulatory environment consisting of various federal and state laws that govern when, where, and how beer is produced, distributed, and sold. State governments have the ability to regulate alcohol commerce through the imposition of sales restrictions and excise taxes, and the latter are popular policy instruments. State-level excise taxes in the brewing industry are levied against breweries on a production basis (Tremblay and Tremblay 2005).

The received view among policy makers is that per-unit production taxes (i.e., excise taxes) are effective instruments for curbing the demand of potentially harmful products and offsetting the social costs of hazardous consumption (Grossman et al. 1993). Health experts have likened excise taxes on beer products to “user fees” (Cook and Moore 1994). The rationale is that heavy drinkers claim a disproportionate share of government expenditures on criminal justice services and medical care, and they also generate a disproportionate amount of private insurance costs. Proponents of excise taxes argue that the additional tax raises the price of the dangerous product to a level that accounts for the costs of negative externalities associated with its consumption (Cnossen 2005; Cook and Moore 1994). Unfortunately for policy makers, using excise taxes to reduce or recoup the social costs of alcohol consumption may have unintended side effects on entrepreneurship.

Tax policy can have a noticeable impact on the entrepreneurial environment (Gnyawali and Fogel 1994). Low business taxes and tax shelters increase the likelihood of entrepreneurial activity and new venture creation (Dana 1987). Previous studies on entrepreneurship and public policy demonstrate that entrepreneurs consider tax policies when making business decisions about financing (MacKie-Mason 1990), choice of location (Buss 2001), and marketing strategy (Hunt 2000). Initial research on the subject of public policy and entrepreneurship in the U. S. brewing industry suggests that high excise taxes may negatively affect small, independent brewers, as states with high excise taxes have fewer microbreweries per capita than states with low excise taxes (Friske and Zachary 2017; Gohmann 2016; Gohmann, Hobbs, and McCrickard 2013; Malone and Lusk 2017). However, these studies only tell one side of the tax policy-entrepreneurship story.

Despite the seemingly negative relationship between excise taxes and entrepreneurship, the latest research on microbreweries indicates that they are performing very well relative to the larger production breweries (e.g., Molson Coors Brewing Co., Anheuser-Busch InBev). In fact, the number of independent microbreweries operating in each state has increased over the last ten years (Watson 2018), and states with high excise taxes actually have higher rates of new venture creation than states with low excise taxes (Friske and Zachary 2019). In other words, growth rates of new microbreweries are not hindered by high excise taxes. As entrepreneurial brewers find creative ways to overcome high taxes and sales restrictions (Gloukhovtsev, Schouten, and Mattila 2018), microbreweries continue to make impressive gains in market share (Watson 2018)

What accounts for the growth in microbreweries, especially in states with high excise taxes? We hypothesize microbreweries have taken advantage of a shift in product quality expectations induced by high excise taxes. The “flight to quality” hypothesis (Barzel 1976) originates from the third law of demand (Alchian and Allen 1964). It describes a behavioral pricing phenomenon in which consumer preferences shift toward high quality products as a result of a production tax. The excise tax is passed down to beer consumers, raising the price of the lower cost, lower quality products relatively more than the higher cost, higher quality substitutes. In response, consumers gravitate toward high quality products because they realize that the value of higher priced, higher quality products has increased relative to lower priced, lower quality products. In other words, consumers will receive more quality per dollar spent when purchasing higher priced, higher quality products. Therefore, the demand of high quality products relative to low quality products increases (Barzel 1976; Nesbit 2007). Microbreweries are in an advantageous position to capture the unmet demand for high quality beers because they are more nimble than large-scale corporate brewers and because their production processes rely on specialty, high quality ingredients combined with artisanal brewing techniques (Oliver 2012).

In the spirit of the special issue, this study crosses disciplinary boundaries in order to investigate how a macro-level policy variable (i.e., excise taxes) affects a key marketing variable (i.e., product quality) in a sample of small firms (i.e., microbreweries). Because microbreweries (Level 1) are nested within states (Level 2), we use a hierarchical linear model (HLM) to test the relationship between excise taxes and product quality, and we also include a relevant selection of controls at each level based on relevant studies by Gohmann (2016) and Friske and Zachary (2019). The results of the HLM analysis indicate that excise taxes have a positive, statistically significant effect on product quality. We reanalyze the data with a Level 1 random effects model as a robustness check, and we reach the same conclusion. In short, our results imply that entrepreneurs facing high excise taxes are incentivized to focus on product quality.

The rest of the study is organized as follows. First, we provide more detail about Barzel’s “alternative approach to taxation” (1976) and subsequent studies that empirically test the flight to quality hypothesis. Second, we discuss the limitations of existing research on the flight to quality before grounding Barzel’s model in Resource-Advantage (R-A) Theory, which provides the overarching theoretical framework for this study. Then we describe the methodological components of the study, including the sampling and data collection procedures, measures, and analysis. The results section follows. We conclude with a discussion section that addresses the study’s implications for macromarketing scholarship, entrepreneurial marketing research, and public policy.

The Flight to Quality Hypothesis

The Alchian and Allen (1964) theorem in economics, which is sometimes referred to as the third law of demand, is an interesting application of the principle of economizing behavior (Razzolini, Shughart, and Tollison 2003). The theorem states that a fixed charge (e.g., transportation costs) reduces the price of a higher quality good relative to a lower quality good and, as a result, triggers a shift in consumer preferences toward the higher quality product (Alchian and Allen 1964). The first law of demand still applies in that fewer goods of both types will be consumed (Razzolini, Shughart, and Tollison 2003). However, the theorem suggests that some firms will recognize the shift in consumer preferences and develop higher quality products over the long run to satisfy consumer demand (Bohanon and Van Cott 1984).

Barzel (1976) provides an initial test of the Alchian and Allen theorem, although he examines how excise taxes (not transportation costs) influence demand. Barzel shows that an excise tax on units of production leads to a lower opportunity cost of purchasing the higher quality option of two substitute goods, which results in a consumer flight to quality (Barzel 1976). Barzel’s original research context is the cigarette market, and follow-up tests of the flight to quality hypothesis in the cigarette market have produced mixed results. For example, Johnson (1978) and Sobel and Garrett (1997) find that that consumers are more likely to purchase premium brand cigarettes as opposed to generics when state governments raise excise taxes on tobacco products. In contrast, Sumner and Ward (1981) find no evidence of the flight to quality in the cigarette market, and Espinosa and Evans (2013) conclude that increased excise taxes may lead to substitutions from carton to pack sales but do not lead to substitutions between brands. Tests of the flight to quality hypothesis in other markets, such as the markets for gasoline (Lawson and Raymer 2006; Nesbit 2007) and wine (James and Alston 2002; Ljunge 2011), have also produced mixed results.

Limitations of Existing Research

From a macromarketing or entrepreneurial marketing scholar’s perspective, the inconsistent results among existing flight to quality studies are compounded by four additional problems. First, none of the studies are grounded in marketing theory. The lack of an underlying theoretical foundation to guide hypothesis development and model specification may partially explain the mixed and sometimes contradictory results that appear in the literature (Hunt 2011), and it may also explain why some studies lead to “dead ends” (Murray, Evers, and Janda 1995). Second, previous studies lack a valid measure of product quality. For instance, Barzel (1976), Johnson (1978), Sumner and Ward (1981), and Sobel and Garrett (1997) operationalize high quality and low quality substitutes as premium-brand versus generic cigarettes. Likewise, Nesbit relies on premium and regular-grade gasoline to distinguish high quality goods from low quality substitutes. These dichotomies provide extremely coarse measures of product quality, and they are not based on consumer perceptions of quality. Third, extant empirical research does not examine how excise taxes affect production. The logical outcome of the flight to quality hypothesis is that marketing organizations will recognize shifting consumer preferences and develop higher quality products over the long run to satisfy demand (Barzel 1976; Bohanon and Van Cott 1984). However, researchers have yet to examine the marketing strategy implications of the flight to quality. Fourth, prior work does not account for the nested data structure of samples used in flight to quality research. There are multiple firm-level factors that affect product quality, but excise taxes are a state-level phenomenon. Ignoring the analytical problems presented by cross-level data prevents researchers from separating individual firm and tax policy effects on the outcome of interest, and it may also lead to dramatic overestimation or underestimation of observed relationships among variables (Raudenbush and Bryk 2002).

The current study seeks to contribute to the macromarketing and entrepreneurial marketing literatures by building on previous studies that examine the relationship between public policy decisions and entrepreneurial activities (e.g., Hollander 1984; McArthur, Weaver, and Dant 2016; Paswan and Tran 2012). Not only does this study test the flight to quality hypothesis in the context of entrepreneurship, but it also addresses the aforementioned theoretical and methodological limitations of prior research. By grounding the flight to quality hypothesis in R-A Theory, we provide a formal mechanism to understand the relationship between excise taxes and entrepreneurial activities like new product development. R-A theory is well established in the macromarketing literature (Hunt 2000), and it has recently received attention in the entrepreneurial marketing domain (Friske and Zachary 2017, 2019) because it realistically assumes that societal factors, such as public policy and political institutions, can improve or impede conditions for entrepreneurs (Hunt 1999). This study also provides multiple methodological improvements on past studies. Unlike prior studies that rely on proxies or coarse, subjective measures of product quality, our objective measure of quality is based on consumer ratings collected from a consumer review website. Moreover, we properly account for the shared variance in hierarchically structured flight to quality datasets by employing HLM to test the relationship between excise taxes (a state-level variable) and product quality (a brewery-level variable). This type of analysis contributes to an emerging stream of macromarketing research that uses secondary data in a multilevel context (e.g., Stump, Gong, and Li 2008), although it is underused in entrepreneurial marketing research.

Resource-Advantage Theory

R-A Theory is a dynamic, evolutionary, process theory of competition that has been introduced to a variety of business disciplines but has gained the most traction in marketing (Hunt 2011). The theory describes competition as a “disequilibrium provoking process” that consists of “the constant struggle among firms for comparative advantages in resources that will yield marketplace positions of competitive advantage and…superior financial performance” (Hunt 2011, p. 11). A firm’s marketplace position reflects its efficiency and its effectiveness in creating value for a target market. Firms that occupy disadvantaged positions will constantly attempt to surpass advantaged firms by obtaining new resources, creating resources, or leveraging existing resources in a more efficient or effective manner.

According to R-A Theory, “entrepreneurship is the means by which firms discover, create, or assemble resource assortments that allow them to produce valued market offerings” (Morris, Schindehutte, and LaForge 2002, p. 9). Following the Schumpeterian tradition, R-A theory proposes that the entrepreneur’s ability to develop innovative market offerings contributes to the dynamic, disequilibrating nature of free market economies (Dixon 2000; Hunt and Morgan 1996). R-A theory also maintains that the entrepreneur’s ability to recognize opportunities is a vital resource (Hunt and Morgan 1996). In short, R-A Theory views entrepreneurship as a critical component of competition because entrepreneurs are catalysts of economic activity (Hunt and Morgan 1996). Once an entrepreneur recognizes a market opportunity, the entrepreneur can generate “economic dynamism” by producing the “proactive innovations” that disrupt existing markets (Hunt and Morgan 1996, p. 109).

One critical—but often overlooked—facet of R-A Theory is that it acknowledges the external environment’s effects on competitive processes. Societal resources, societal institutions, the characteristics of competitors, the characteristics of suppliers, consumers, and public policy influence competition. With respect to public policy, Hunt (2011) argues that governments have the ability to enhance or impede entrepreneurship through regulation and taxation. Although R-A Theory scholars favor an economic freedom approach to public policy, R-A Theory assumes that policies have differential effects on firms within an industry (Hunt 1997, 1999, 2011; Hunt and Arnett 2006). In other words, a policy that improves one firm’s marketplace position may hurt a competing firm’s marketplace position. Furthermore, R-A Theory’s concept of proactive innovation through entrepreneurship implies that entrepreneurially-oriented firms “do not consider the external environment as a given, or as a set of circumstances to which the firm can only react or adjust” (Morris, Schindehutte, and LaForge 2002, p. 6). Rather, entrepreneurs may view a policy as “an opportunity horizon where the marketer attempts to redefine external conditions in ways that reduce uncertainty and lessen the firm’s dependency and vulnerability” (Morris, Schindehutte, and LaForge 2002, p. 6-7).

We hypothesize that entrepreneurial firms can spot opportunities in states with high excise taxes and will react by bringing high quality products to market (Hunt 1999, 2011). In the entrepreneurial marketing literature, opportunities are defined as “unnoticed market positions that are sources of sustainable profit potential” (Morris, Schindehutte, and LaForge 2002, p. 6). Through environmental scanning, entrepreneurial microbreweries should be able to identify a shift in consumer preferences toward high quality products. Moreover, it is relatively easy for microbreweries to begin production of high quality beers because their small scale makes them nimbler than incumbent production breweries, which rely on high-volume production processes and carry significant fixed costs. If entrepreneurial organizations in the brewing industry recognize and pursue opportunities induced by high excise taxes, then excise tax rates should be positively associated with measures of product quality in a sample of microbreweries.

Method

Research Context

In this study, we test the flight to quality hypothesis in the U. S. brewing industry. The U. S. brewing industry has recently become a popular context for policy research because it is one of the most heavily regulated industries in the country and because regulations vary dramatically from state-to-state (Gohmann 2016; Malone and Lusk 2017). State governments have the authority to regulate many aspects of alcohol commerce, including the right to place restrictions on beer sales and levy excise taxes on beer production (Oliver 2012). Excise tax rates exhibit significant variance among states. For instance, Wyoming has the lowest excise tax rate in the nation at $0.59 per 31 gallon barrel of beer, and Alaska has the highest rate at $33.17 per barrel (Watson 2018).

Despite the challenging regulatory environment, entrepreneurs have established microbreweries in all 50 states. Since 1979, the number of licensed microbreweries operating in the U.S. has grown from two firms to over 6,000 firms. Recent growth in the beer industry is tied to the success of new microbreweries. Few macrobreweries (e.g., Heineken, InBev) have entered the market since the 1980s (Oliver 2012). Figure 1 provides a graphical illustration of the industry’s growth relative to the U. S. population.

Historical U. S. population and brewery count.

Data Collection and Sampling Procedures

The final dataset contains several state-level variables and brewery-level variables. We collected the data from multiple sources. Consumer perceptions of product quality for the year 2013 function as the dependent variable in the study (n = 1,764 ratings of mean product quality). This perceptual data was hand-collected from RateBeer (2014), a review website for beer products. Initial data collection took place over several weeks beginning in late 2013 and ending in early 2014. State-level excise taxes represent the independent variable in the study. Excise tax rates are measured in U. S. dollars ($USD) per 31 gallon barrel for the year 2013. Data regarding state excise tax rates is collected from the Brewers Almanac (2013), which is published by the Beer Institute, a national trade association that represents brewers, importers, and industry suppliers (n = 50 states).

In addition to the above variables, we include several theoretically relevant control variables in the model to mitigate problems related to omitted variable bias (Spector and Brannick 2011). At the state-level, we include controls for sales taxes and small brewery tax credits and exemptions. Sales tax rates are measured as a mean statewide percentage. We measured tax credits and exemptions using a dummy variable coded “1” if a small brewery tax credit or exemption is present, and a score of “0” if the state does not grant small brewery tax credits or exemptions. Furthermore, we created dummy variables to control for keg registration laws and Sunday sales restrictions. Information about sales taxes, tax credits/exemptions, and sales restrictions is collated from government websites and the Brewers Almanac (2013). We also control for the financial ability of consumers in a given state to purchase beer by including disposal income per capita. Income information is available through the Bureau of Economic Analysis website (U. S. Bureau of Economic Analysis 2017). Following previous work on the subject of entrepreneurship in the U. S. brewing industry (Gohmann 2016), we include a measure of economic freedom for each state, which is obtained from the Fraser Institute’s Economic Freedom of North America index. This measure reflects the extent to which public policy is generally supportive of the ability of individuals and businesses to engage in economic activity (Stansel, Torra, and McMahon 2017). Additionally, we include control variables that reflect the demand for beer and the competition among breweries. Beer consumption is measured in gallons per capita, and competition is measured as the number of licensed breweries operating in each state in the year 2013. Both of these variables are provided by the Brewers Almanac (2013).

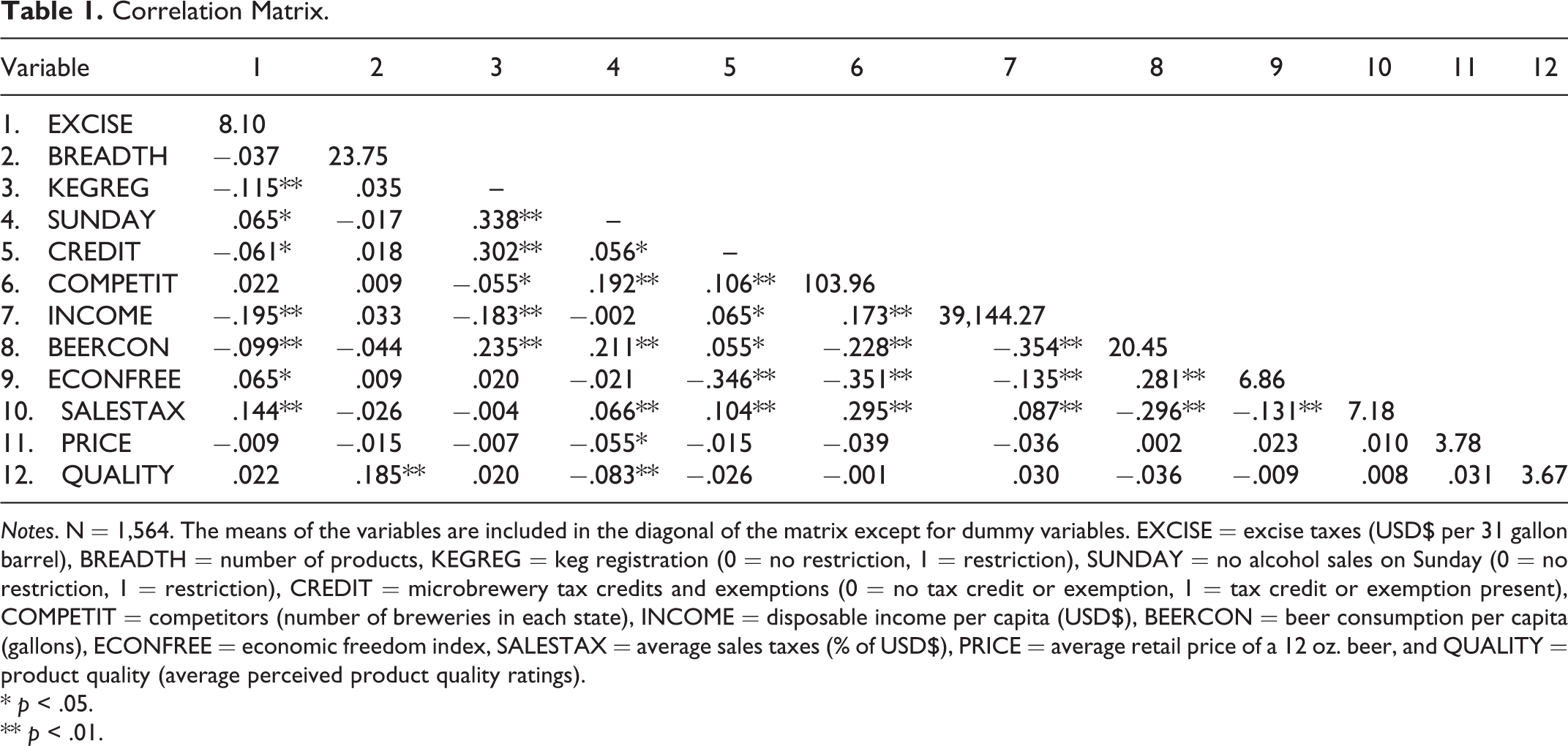

At the brewery-level, we control for the average price of the brewer’s products and product line breadth. The pricing data reflects the average retail price in $USD of a 12 oz. beer on the Craftshack (2018) and Craft Beer Kings (2018) websites. Product line breadth is a simple count of a brewery’s products listed on the RateBeer website in 2013. After the removal of outliers and mean imputation of missing values, the final dataset consists of 1,564 observations for each brewery variable and 42 observations for each state variable. Table 1 displays descriptive statistics and correlations among all the variables in the study.

Correlation Matrix.

Notes. N = 1,564. The means of the variables are included in the diagonal of the matrix except for dummy variables. EXCISE = excise taxes (USD$ per 31 gallon barrel), BREADTH = number of products, KEGREG = keg registration (0 = no restriction, 1 = restriction), SUNDAY = no alcohol sales on Sunday (0 = no restriction, 1 = restriction), CREDIT = microbrewery tax credits and exemptions (0 = no tax credit or exemption, 1 = tax credit or exemption present), COMPETIT = competitors (number of breweries in each state), INCOME = disposable income per capita (USD$), BEERCON = beer consumption per capita (gallons), ECONFREE = economic freedom index, SALESTAX = average sales taxes (% of USD$), PRICE = average retail price of a 12 oz. beer, and QUALITY = product quality (average perceived product quality ratings).

* p < .05.

** p < .01.

HLM Analysis

Because there are several breweries within each state, the dataset has a multilevel structure. Breweries are nested, or grouped, within states. The multilevel structure of the dataset implies that there is some degree of dependence among the brewery-level observations from each state. In other words, average product quality may be affected by state-level factors in addition to brewery-level factors. To test for the presence of non-independence in the data, we analyzed a null model in HLM7 with product quality as the dependent variable (Raudenbush and Bryk 2002). The Intraclass Correlation Coefficient (ICC) indicates that 4% of the variance in product quality is due to state-level factors (ICC = .04, χ2 (42, N = 1,564) = 95.698, p < .001).

In our multilevel model, Level 1 represents the brewery-level and Level 2 represents the state-level. The dependent variable (product quality) is on Level 1, as are the control variables for retail price and product line breadth. The independent variable (excise taxes) is on Level 2, along with the controls for small brewery tax credits and exemptions, sales taxes, etc. For the analysis, we group-mean centered the Level 1 control variables to account for the influence of state-level factors on the estimation of their parameters, and we grand-mean centered the Level 2 predictor (i.e., excise taxes) and the Level 2 control variables in accordance with Raudenbush and Bryk (2002).

After addressing the multilevel structure of the dataset, we have another statistical issue to resolve: whether to use a fixed-effects or random-effects model. We perform a Hausman test to determine whether a fixed-effects or random-effects model should be used. The null hypothesis of the Hausman test states that the difference between models is not systematic, meaning that the coefficients in the random-effects model and the fixed-model are consistent, but the random-effects model should be used because it is more efficient. The alternative hypothesis states that the difference in models is systematic, meaning that the fixed-effects model should be used because the coefficients in the random-effects model are not consistent (Hausman 1978). The results of the Hausman test indicate that a random-effects model is more appropriate for the analysis (χ2 = .89, p > .05).

Exogeneity Test

Another assumption of the model is that the independent variable, excise taxes, is exogenous. To test the exogeneity of the independent variable, we followed a procedure advocated by Wooldridge (2010). First, we removed the dependent variable, product quality, and regressed the excise taxes variable on all exogenous variables in the model. Then, we predicted the residuals from the regression. Finally, we reran our model with product quality as the dependent variable, with one exogenous variable removed, and with the predicted residuals from the previous regression included in the model. According to Wooldridge (2010), if the z statistic for the predicted residuals is significant, then there is evidence of endogeneity. However, we fail to reject the null hypothesis of exogeneity, indicating that the excise taxes variable is exogenous in our model (β = .072, p > .05).

Results

If entrepreneurial microbreweries recognize opportunities in the consumer flight to quality, then high excise taxes should provide incentives to develop high quality products to meet consumer demand. Therefore, we hypothesize that excise tax rates are positively associated with product quality. We test our conceptual model as a hierarchical linear model with random effects in HLM7 using robust standard errors. The results of the analysis (see Table 2) reveal evidence of a positive relationship between excise taxes and product quality, in support of the flight to quality hypothesis (γ = .002*, p < .05).

HLM Results.

Notes. L2, N = 42. L1, N = 1,564. L2 (state-level) variables: EXCISE = excise taxes (USD$ per 31 gallon barrel), KEGREG = keg registration (0 = no restriction, 1 = restriction), SUNDAY = no alcohol sales on Sunday (0 = no restriction, 1 = restriction), CREDIT = microbrewery tax credits and exemptions (0 = no tax credit or exemption, 1 = tax credit or exemption present), COMPETIT = competitors (number of breweries in each state), INCOME = disposable income per capita (USD$), BEERCON = beer consumption per capita (gallons), ECONFREE = economic freedom index, and SALESTAX = average sales taxes (% of USD$). L1 (brewery-level) variables: product quality (dependent variable), PRODBREADTH = number of products, and PRICE = average retail price of a 12 oz. beer.

*p < .05.

**p < .01.

Although the multi-level model is theoretically justified given our research context (Luke 2005), some HLM researchers suggest that multilevel analysis of grouped data may be unnecessary when ICC values are smaller than .05 (Bliese 2000). Therefore, to validate the results of the HLM analysis, we reanalyzed the data using a random-effects Level 1 regression model with robust standard errors. Whereas HLM analysis allows researchers to separate within-group effects from between-group effects, a Level 1 regression model simply blends them together into a single coefficient (Huta 2014). We conducted the Level 1 regression analysis in Stata 14 and chose a random-effects model over a fixed-effects model because of the results of the aforementioned Hausman test. Again, we find that excise taxes are positively related to product quality (see Table 3), in support of the flight to quality hypothesis (β = .002*, p < .05).

Robustness Check Results.

Notes. 42 clusters. N = 1,564. EXCISE = excise taxes (USD$ per 31 gallon barrel), KEGREG = keg registration (0 = no restriction, 1 = restriction), SUNDAY = no alcohol sales on Sunday (0 = no restriction, 1 = restriction), CREDIT = microbrewery tax credits and exemptions (0 = no tax credit or exemption, 1 = tax credit or exemption present), COMPETIT = competitors (number of breweries in each state), INCOME = disposable income per capita (USD$), BEERCON = beer consumption per capita (gallons), ECONFREE = economic freedom index, SALESTAX = average sales taxes (% of USD$), Product Quality (dependent variable), PRODBREADTH = number of products, and PRICE = average retail price of a 12 oz. beer.

*p < .05.

**p < .01.

Discussion

The purpose of this study is to examine how excise taxes affect product quality in a sample of small firms. The results of the analysis indicate that excise taxes are positively correlated with product quality. We conclude that high excise taxes encourage quality-based competition, and entrepreneurial organizations pursue the opportunity to bring relatively high quality products to market. This study provides several methodological improvements on past studies. More importantly, the results of the study have theoretical implications for macromarketing and entrepreneurial marketing scholarship, as well as practical implications for public policy.

Implications for Macromarketing Scholarship

This study contributes to an emerging literature at the intersection of macromarketing and entrepreneurship (Davies and Torrents 2017; Hamby, Pierce, and Brinberg 2017; Paswan and Tran 2012; Sridharan et al. 2014; Viswanathan et al. 2014). The results of the analysis indicate high excise taxes are positively correlated with product quality in a sample of SMEs. We conclude that the presence of high excise taxes invites quality-based competition, and it appears that entrepreneurial organizations in the brewing industry respond to high excise taxes by developing marketing strategies that feature high quality products. In sum, the results of our study reinforce Paswan and Tran’s conclusion that “entrepreneurship is a socioeconomic phenomenon and is intricately and dynamically linked with other institutions and phenomena in the marketplace” (2012, p. 26). The flight to quality is truly a macromarketing phenomenon in that a state’s excise tax policy has the ability to influence a small firm’s marketing strategy.

A second macromarketing implication is that consumers may be the ultimate beneficiaries of high excise taxes on beer production. Although excise taxes raise the price of products, they also lead to higher quality market offerings in the long run. Entrepreneurial microbreweries respond to high excise taxes by developing new, innovative, high quality products. If the growth rate of new ventures in the brewing industry remains steady (Friske and Zachary 2019), consumers will have increased access to a wide assortment of high quality beers in the future.

Implications for Entrepreneurial Marketing Scholarship

This study also contributes to an emerging literature on entrepreneurial marketing (Kraus et al. 2012). Excise taxes typically have a negative connotation in entrepreneurship and marketing scholarship. However, high excise taxes might actually facilitate entrepreneurship in the U. S. brewing industry. High excise taxes invite quality-based competition, which is attractive to small, relatively new ventures such as microbreweries. Microbreweries are in a better position than large-scale macrobreweries (e.g., A.B. InBev) to pursue opportunities related to quality-based competition because they are low-volume producers with small fixed costs. Accordingly, microbreweries can quickly adapt their marketing strategies to exploit opportunities that arise from market imperfections (Katila, Chen, and Piezunka 2012). The results of this study imply that microbreweries in states with high excise taxes can successfully differentiate their products from larger incumbent competitors by focusing on quality.

Entrepreneurial marketing researchers may also be interested in the coefficients of the PRODBREADTH (γ10) and COMPETIT (γ05) control variables. Both are statistically significant and positive in the model. The former indicates a positive relationship between product line breadth and product quality, probably as a result of “upward stretching” (Kirmani, Sood, and Bridges 1999). Upward stretching (or stretching up) occurs when firms add higher quality, more expensive products to their portfolios. Upward stretching is a logical line extension strategy in response to the flight to quality, and it tends to work well for small firms that are trying to establish a reputation for prestige (Kirmani, Sood, and Bridges 1999). The sign of the COMPETIT (γ05) coefficient at Level 2 indicates that competition has a positive effect on product quality. Entrepreneurs often focus on product quality as a base for differentiation (Davies and Torrents 2017) because it creates customer loyalty and lowers sensitivity to price (Phillips, Chang, and Buzzell 1983). In states where competition is particularly fierce, the struggle among small firms to bring increasingly high quality products to market results in a wide selection of innovative offerings (Hunt 2011). In the U. S. brewing industry, it is important to remember that microbreweries not only compete against production breweries, but they also face competition from other microbreweries (Watson 2018).

Implications for Public Policy

The results of the study indicate that policy makers can influence product quality through excise taxes and create market opportunities for SMEs with high quality production capabilities. In markets characterized by large-scale incumbents that produce low quality, low priced products, excise taxes could enable SMEs with high quality production capabilities to enter the market without having to compete directly against incumbents. This is an advantage for small firms because large incumbents may have more resources and higher levels of customer awareness. Moreover, microbreweries are nimbler than macrobreweries, and thus they are better suited to exploiting opportunities that might arise from changes in tax policy (Katila, Chen, and Piezunka 2012).

Policy makers view excise taxes as an instrument for reducing and recouping social costs. In the brewing industry, politicians use excise taxes to defray public health costs associated with the consumption of alcohol. Laissez faire economists often discourage excise taxes as a policy lever because of their negative effects on small businesses (Gohmann 2016; Gohmann, Hobbs, and McCrickard 2013; Sobel 2008). However, our results suggest that higher excise taxes may ultimately benefit entrepreneurially-oriented firms. Furthermore, if politicians remain concerned about unintended side effects on small businesses, then excise tax credits or exemptions may be issued. Recent research on the subject of tax credits and exemptions indicates that such policies “do not disrupt the entrepreneurial forces that generate new jobs and marketplace innovations” (Friske and Zachary 2019).

Limitations and Future Research Directions

Although we find evidence in support of the flight to quality hypothesis, further research is needed to overcome the limitations of the current study. For example, in the current study, we tested the relationship between excise taxes and product quality. However, a key tenet of the flight to quality is that consumer demand increases for higher quality products, and firms respond to the shift in consumer preferences by creating higher quality products. We do not directly test the increase in demand for higher quality products, although the increase is inferred because of the increase in the supply of higher quality products. Future research should empirically test the changes in consumer preferences to confirm this key tenet of the flight to quality hypothesis. Another limitation of the current study is the cross-sectional dataset. Because the dataset is cross-sectional, we are not able to determine how marketing strategies change over time in response to increases or decreases in excise tax rates. Finally, the study is limited to one industry, and the majority of firms in the sample are privately owned, making the collection of data on firm-level resources very difficult. Future research should investigate the effects of excise taxes in other industries to increase the generalizability of our findings, and future research should include more controls for firm-level resources that could influence product quality.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.