Abstract

This article interrogates recent policy pronouncements around the promotion of emerging financial technologies (fintech) as means of enabling financial inclusion. It is argued that situating this emergent ‘turn to technology’ in the context of a longer-running pattern of failed efforts to promote the development of financial markets for the poor in the Global South offers us a useful lens on the dynamics of neoliberalism. The article develops this analysis by drawing together interlinked discussions of ‘neoliberal reason’, highlighting the central role played by the diffusion of market institutions in neoliberal projects with Marxian discussions highlighting the crucial underlying role of labour in enabling the operation of markets. In this context the appeal to ever-more fine-grained information with which to allocate credit underlying the turn to technology can both be read as yet another attempt to ‘re-engineer’ the market, and also seen as a doomed project. Empirically, this argument is fleshed out through an engagement with key framework documents around financial inclusion and technology from the World Bank and G20.

Introduction

One of the flagship outcomes of the World Bank and IMF’s Joint Annual Meetings for 2018 was the ‘Bali Fintech Agenda’ (BFA). The BFA was launched with considerable fanfare by a panel featuring Bank of England Governor Mark Carney, IMF President Christine Lagarde, World Bank President Jim Yong Kim, South African Reserve Bank Governor Lesetja Kganyago, Indonesian Finance Minister Sri Mulyani and Indonesian President Joko Widodo. The BFA follows a number of similar pronouncements. Notably, the Alliance for Financial Inclusion (AFI), a network of central banks and finance ministries, announced the ‘Sochi Accord on Fintech for Financial Inclusion’ the previous month (AFI, 2018), and the G20 published a set of ‘High-Level Principles for Digital Financial Inclusion’ (HLPs) in 2016 (GPFI, 2016). These documents reflect an emerging consensus around fintech as a means of supporting ‘financial inclusion’ – the extension of access to a range of financial services to the poor, primarily in the Global South.

This article interrogates this recent ‘turn to technology’. This is an important task because the turn to technology offers us a lens on key trends in neoliberal development governance. Financial inclusion, as several authors have argued, is a paradigmatically neoliberal approach to poverty (Price, 2019; Soederberg, 2014). Indeed, financial inclusion has increasingly been substituted in policy discussions for ‘microcredit’, about which critics argued the same (e.g. Bateman, 2010; Rankin, 2001). The assumption that enabling greater access to formal savings, credit and insurance will lead to reductions in poverty epitomizes neoliberal logics seeking to extend markets and market-like devices into ever-wider areas of social life. Yet, financial inclusion also has to be viewed as a failure, even on its own terms, as the results of efforts to expand ‘access’ to financial services have often been much slower and more uneven than advocates expected.

In this article, I argue that the turn to technology represents an effort to grapple with the limits of (financial) markets and the difficulties in constructing them. These limits are ultimately rooted in a fundamental contradiction: the reason why the poor are held to need greater access to credit, savings and insurance (namely, low and unpredictable incomes) is precisely the same reason why they are ‘bad’ credit risks, and why savings or insurance products are often ill-suited. These fundamental and persistent limits to the project of financial inclusion, though, are mystified in the turn to technology by a focus on the technical intricacies of constructing markets. Ultimately, the turn to technology thus needs to be understood as a fraught response to repeated failures in development governance.

The article makes this case in four steps. The next section examines the specific contents of the BFA, G20 HLPs, and Sochi Accord. Then, the article develops an understanding of neoliberalism, drawing on interlinked discussions of a ‘neoliberal reason’, highlighting the central role played by the diffusion of market institutions and speculative logics in neoliberal projects (e.g. Konings, 2016; Mirowski, 2009; Peck, 2010) and critical discussions of ‘markets’ (e.g. Cahill, 2019; Christophers, 2014), complemented by engagements with Marx highlighting the crucial underlying role of labour in enabling the operation of markets. The next section applies this framework in situating the turn to technology in the wider trajectory of policies for ‘financial inclusion’. The final section reconsiders the limits of fintech in light of this discussion.

In presenting this argument, the paper makes three contributions. First, while it has been common to critique ‘financial inclusion’ as a ‘neoliberal’ project, reflections on what its troubled trajectory can tell us about neoliberalism have been much rarer. This is an important gap to address because the trajectory of financial inclusion and fintech offers a lens on the fragile nature of the ‘market’ itself as a social form and the troubled processes of failure and adaptation underlying neoliberalization (see Best, 2016; Brenner et al., 2010).

Second, much of the critical literature on microcredit and financial inclusion in general (e.g. Aitken, 2013; Gruffydd-Jones, 2012; Mader, 2018), and on emergent fintech applications in particular (e.g. Aitken, 2017; Gabor and Brooks, 2017), has tended to treat financial inclusion as an extension of processes of financialization, particularly following the literature on the financialization of daily life (Martin, 2002). The latter refers to a process in which everyday uses of financial techniques and subjectivities have become increasingly ‘inescapable’, in Hall’s (2012: 407) evocative terms. Contributions treating fintech in this light (e.g. Aitken, 2017; Gabor and Brooks, 2017) have usefully highlighted important pathologies of emergent applications, particularly tendencies towards panoptic surveillance of everyday life and the concurrent production of new modes of discipline and stratification. But treating fintech as an extension of financialization often makes it much harder to give sufficient attention either to the political dynamics underlying the turn to technology, or the somewhat truncated character of its actual roll-out. In developing an analysis of the turn to technology emphasizing the uneven development of neoliberal logics of marketization, this article thus makes a contribution to emerging literatures on the analytic and empirical limits to financialization (e.g. Christophers, 2015; Montgomerie and Tepe-Belfrage, 2017).

Finally, and relatedly, in highlighting ways in which the turn to technology has sought to respond to underlying limits of market-making, this article calls attention to the centrality of labour and livelihoods in explaining the uneven progress of neoliberalization. In this sense, this trajectory should probably serve as a caution against eliding processes of neoliberalization and financialization. Neoliberalism and financialization are often seen as conjoined processes (e.g. Duménil and Levy, 2004; Fine, 2013; Fine and Saad-Filho, 2017). The turn to technology suggests that this relationship is more troubled in practice than is often assumed. Indeed, the evidence in this article suggests that broader effects of neoliberal reforms on labour markets across the Global South may even have made the extension of certain kinds of financial accumulation harder. As a number of authors have noted, precarious, irregular and informal forms of work are decidedly on the rise, particularly across the Global South, processes that have often been exacerbated by neoliberal reforms (see Harris and Scully, 2015; Selwyn, 2014). The series of failures and adaptations mapped out in this article would seem to suggest that this increased precarity has hindered the development of at least some kinds of financial accumulation. It’s on this point that engagements with Marx around markets and fetishism, the ways in which financial markets obscure yet remain reliant on particular configurations of productive activity, are particularly useful.

Fintech for financial inclusion: an emerging (neoliberal) consensus

Taken together, the BFA, Sochi Accord and HLPs point to an emerging consensus around a set of potential benefits of fintech and of emergent risks and areas for regulatory intervention. Four key points are worth underlining.

First, the BFA, HLPs and Sochi Accord are non-binding statements of principles. The background paper to the BFA, for instance, is explicit that ‘The Agenda does not represent the work program of the IMF or the World Bank, nor does it aim to provide specific guidance or policy advice at this stage’ (World Bank and the International Monetary Fund, 2018: 10). They are, in this sense, reflective of a wider use of ‘soft law’ and informal ‘best practices’ in setting regulatory standards for the promotion of financial inclusion (on which, see Soederberg, 2013). They are also, as a result, somewhat ambiguous documents that leave considerable scope for interpretation in translation into national and regional policy.

Second, maybe more importantly, the BFA, HLPs and the Sochi Accord are reflective of a growing regulatory emphasis on fintech as both a source of new risks and a key means of securing wider participation in financial markets by the ‘unbanked’. The sense throughout these guidelines is of fintech as a Janus-faced beast that might on one hand enable ever-wider access to ever-more-efficient financial markets, yet create new risks and regulatory challenges in so doing. The core appeal of fintech is very much pitched in terms of its ostensible capacity to extend access to financial services – for instance, a press release to accompany the announcement of the BFA quotes then-World Bank President Kim: ‘Countries are demanding deeper access to financial markets, and the World Bank Group will focus on delivering fintech solutions that enhance financial services, mitigate risks, and achieve stable, inclusive economic growth’ (World Bank, 2018). The first point of the BFA identifies the key (potential) benefits of expanded use of fintech primarily in terms of ‘inclusion’, access and ‘deepening’ of financial activity: ‘increasing access to financial services and financial inclusion; deepening financial markets; and improving cross-border payments and remittance transfer systems’ (World Bank and the International Monetary Fund, 2018: 7).

Yet, all three identify emergent challenges for financial stability and integrity. The BFA suggests that fintech enables financial activity to blur national boundaries, and that ‘These developments could lead to increased multipolarity and interconnectedness of the global financial system, potentially affecting the balance of risks for global financial stability’ (World Bank and the International Monetary Fund, 2018: 9). In the HLPs, in particular, a key emphasis is placed on limiting the potential for criminal activity, fraud and other threats to ‘financial integrity’, noting that monitoring of risks is necessary to ‘build cyber resilience into financial markets and safeguard the financial system from illicit activities’ (GPFI, 2016: 9). This is echoed in the Sochi Accord, which notes that ‘leveraging fintech for financial inclusion creates new regulatory challenges and poses cybersecurity, data privacy, money laundering and consumer protection-related risks’ (AFI, 2018: 2). The underlying argument is centred on the need for regulators to balance emergent risks against the need to minimize regulatory barriers to entry for new firms. A key technique for doing so, discussed further below, has been to carve out time-bound or product-specific regulatory exceptions for experiments with new activities targeting the poor. So-called ‘regulatory sandboxes’ for fintech applications, discussed further below, are a key example (see Jenik and Lauer, 2017).

Third, another important area of emphasis is the importance of the physical infrastructures of financial markets. Point II of the BFA and principle 4 of the HLPs both focus specifically on improving the quality of ICT infrastructure. This could be read in the first instance as recognition by policy makers of the materiality of markets – of the breadth of physical and informational substrates needed to enable financial transactions. But underlying both documents is a particular theory of how to deepen and strengthen those infrastructures; namely, if left the regulatory space to do so, markets will develop infrastructures on their own. It is up to regulators primarily to ensure reliable systems of personal identification and to prevent anti-competitive behaviour by requiring inter-operability.

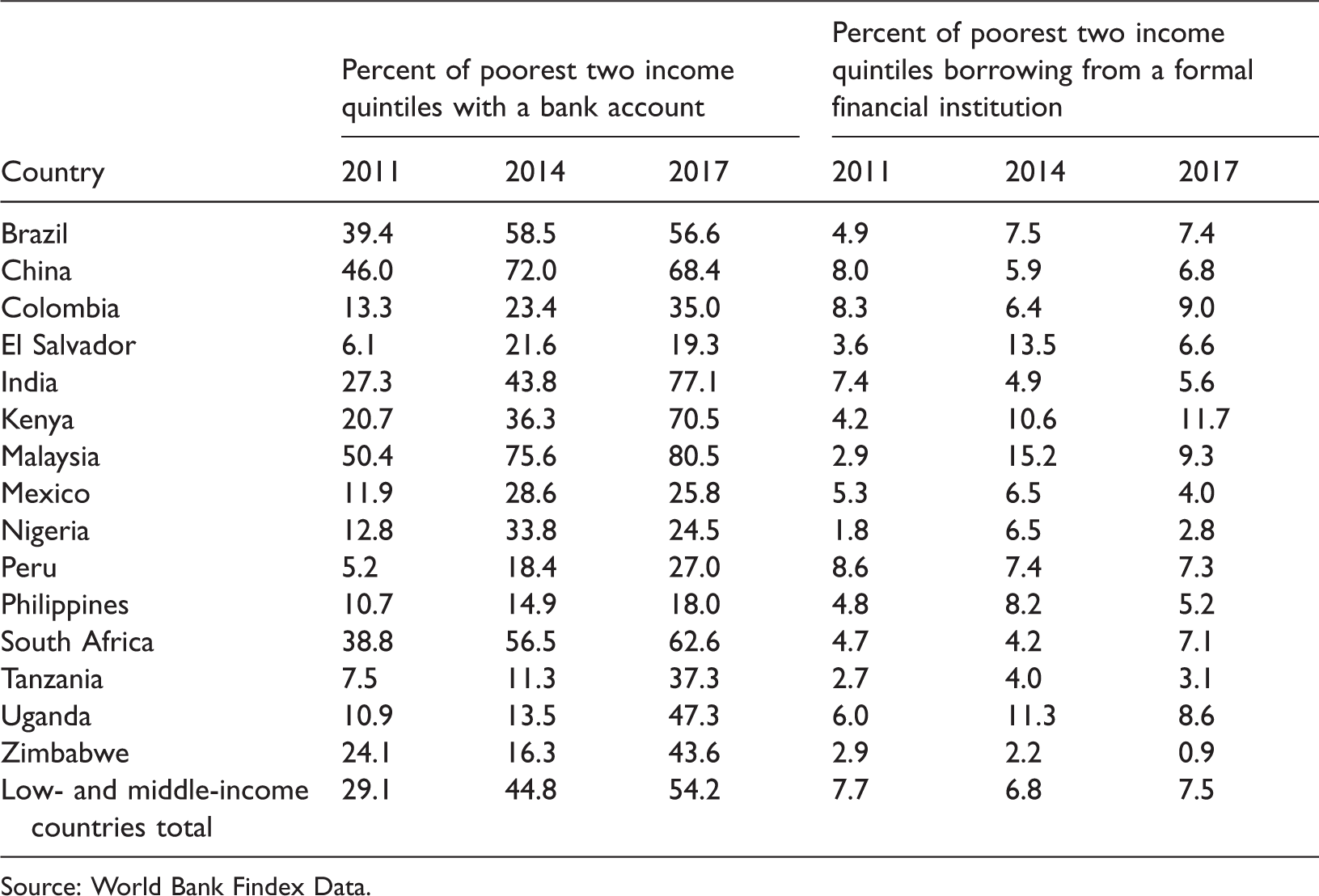

Finally, the timing of these new initiatives centring on fintech for financial inclusion should not escape attention. They come on the heels of a decade of uneven results in terms of extending financial services to the ‘unbanked’. The World Bank’s series of ‘Findex’ surveys of global financial inclusion are the most comprehensive measures of ‘financial inclusion’. The headline figure is a reduction in the estimated number of ‘unbanked’ people (measured specifically by whether or not they have a bank account) from 2.5 billion in 2011, to 2 billion in 2014, and 1.7 billion in 2017 (see Demirgüç-Kunt and Klapper, 2012; Demirgü-Kunt et al., 2015, 2018). However, this overstates the degree of progress. Significantly, the reduction in the number of ‘unbanked’ is largely offset by a notable growth of dormant bank accounts. In the 2011 survey, the World Bank estimated there were 150 million dormant accounts globally, roughly 10% of the global total (Demirgüç-Kunt and Klapper, 2011: 21), by 2014, these numbered 460 million, and 15% of the global total (Demirgüç-Kunt et al., 2015: 18), and 20% of accounts by 2017 (Demirgüç-Kunt et al., 2018: 64). Borrowing from formal financial institutions, moreover, continues to be heavily outweighed by borrowing from family and friends or informal lenders in most developing regions. As Table 1 shows, the growth of ‘access’ to formal credit has been slow, uneven and even prone to reversals in particular cases. Indeed, in the aggregate, the estimated proportion of people borrowing from formal financial institutions in the two lowest income quintiles in lower- and middle-income countries fell between 2011 and 2014, and had yet to return to 2011 levels in the latest survey in 2017.

Indicators of financial inclusion in selected countries.

Source: World Bank Findex Data.

In brief, the BFA, Sochi Accord, and G20 HLPs reflect an emerging policy consensus that fintech is a potential means of overcoming increasingly evident obstacles to fostering greater ‘inclusion’ and access to global financial markets. The underlying role in terms of governance is understood in terms of ensuring market ‘integrity’, the reliability of contracts and increasingly the robustness, resilience and accessibility of basic material telecommunications and data infrastructures. This is a vision of governance in which regulators are meant to play a considerable role in constituting markets, but primarily by ensuring competition and carving out spaces in which private investments can be made in infrastructures.

In what follows, I argue that we can usefully both put this agenda in the context of the longer-running failures of financial inclusion, and also make sense of its limits if we think about it in terms of its fundamentally neoliberal logics. Seen in this light, we can see the turn to technology less as a deepening of wider processes of ‘financialization’ (per Aitken, 2017; Gabor and Brooks, 2017) and more as a contingent development bound up with longer-running regulatory processes of failure, adaptation and experimentation. The promotion of fintech is, at once, a recognition of the expanded range of activities needed to promote the development of markets, and a doubling down on a particular set of regulatory techniques and practices that have a longer history. Before turning to a discussion of this history, though, it is first useful to unpack the concept of ‘neoliberalism’ more clearly.

Neoliberalism, markets, risk

Neoliberalism, it almost goes without saying, is often a slippery concept (Ferguson, 2010; Venugopal, 2015). It refers variously, or sometimes at once, to an intellectual agenda rooted in neoclassical economics, a political programme devoted to economic deregulation and marketization, and a ‘class-project’ – an assault on global working classes on behalf of (financial) capital (see Fine and Saad-Filho, 2017; Harvey, 2007; Selwyn, 2014). To label something ‘neoliberal’ is typically a form of critique in and of itself. In critical discussions of microcredit and financial inclusion, the concept of ‘neoliberalism’ has unquestionably often been used in this vein (e.g. Bateman, 2010). Given the centrality of ‘financial inclusion’ to contemporary neoliberal development agendas, however, its travails arguably represent an important opportunity to reflect more broadly on the dynamics of neoliberalism.

The troubled progress of financial inclusion would seem in the first instance to speak to a number of contributions that have highlighted the uneven and truncated character of processes of neoliberalization more broadly (see Brenner et al., 2010; Peck, 2010, 2013a), and the continual dynamics of failure and adjustment that have often underlain such processes (see Best, 2016; Peck, 2010). This approach requires viewing neoliberalism as a set of logics, or a mode of reason, unfolding (unevenly) through particular regulatory projects (see Konings, 2016; Peck, 2010). As Mirowski (2009) and others have noted, a crucial organizing logic of neoliberal politics understood in this sense is an epistemic faith in the ‘market’, as an aggregate of individual speculative bets, as the most efficient means of processing information and allocating resources. In so far as there is a core ‘neoliberal’ belief, then, it is that ‘prices in an efficient market “contain all relevant information” and therefore cannot be predicted by mere mortals’ (Mirowski, 2009: 435). This has implications for neoliberalism as a political project – crucially that ‘the market’, ‘(suitably re-engineered and promoted) can always provide solutions to the problems seemingly caused by the market in the first place’ (Mirowski, 2009: 439).

We can usefully read the promotion of financial inclusion in general and of fintech in particular in this light. They represent part and parcel of a broader shift in neoliberal development governance towards increasingly more dispersed interventions aimed at making more and better information available in order to enable those ‘markets’ to work properly. The turn to technology could equally be read as a growing recognition of the materiality of markets and the need for concrete infrastructures to facilitate flows of information. The key point is: the promotion of fintech fits this wider logic of efforts at creating ‘suitably re-engineered’ (Mirowski, 2009: 436) markets in response to earlier failures.

Here it is relevant to point out that a number of linked literatures have effectively pointed out that ‘markets’, as such, are neither neutral nor natural phenomena. A growing literature in economic sociology and geography, following Michel Callon (1998) and Donald MacKenzie (2006), has emphasized the ‘performative’ character of markets. This has entailed treating markets as ‘the contingent outcomes of the manner in which they are performed and reiterated’, to use Boeckler and Berndt’s (2013: 425) terms. A good deal of emphasis has been placed here on the particular devices – standards, metrics, formulae, and socio-technical objects – through which market values are produced and rendered stable. Muniesa et al., for instance, note that ‘Markets contain devices that aim at rendering things more “economic” or, more precisely, at enacting particular versions of what it is to be economic’ (2007: 4). On one level, the promotion of fintech is very much about tinkering with such devices in hopes of more effectively capturing a particular ‘version of what it is to be economic’. 1

Yet, the troublesome nature of the promotion of financial inclusion also points towards some more fundamental limits that neoliberal projects of ‘re-engineering’ run up against. In particular, it calls attention to the contradictory configurations of labour and livelihoods needed for the construction of markets (cf. Peck, 2013b). Increasingly, a key reason why the poor are held to need efficient financial markets is precisely to enable more effective management of fluctuating incomes. The G20 Principles for Innovative Financial Inclusion (discussed in the next section) for instance, note that ‘A crucial problem for poor people is that their incomes are not only low, but also irregular and unreliable … an annual average income of US$2 a day may in actuality range from a high of US$5 to low days when no income is earned’ (AFI, 2010: 4). Access to financial services, then, is needed so that the poor can ‘manage this low, irregular and unreliable income to ensure regular cash flow and to accumulate sufficient amounts to cover lump sum payments’ (AFI, 2010: 4). Yet, as argued further below, it is for precisely this reason that creating new financial markets for the poor has proven consistently difficult.

Here, a number of recent Marxian contributions to studies of ‘the market’ are useful in so far as they highlight the necessary interplay of productive activity and ‘fetishized’ market relations (e.g. Cahill, 2019; Christophers, 2014). This point has perhaps not been explored sufficiently in Marxian writing on financialization, which (notwithstanding notable debates among authors) has often made much of the distinction between ‘interest-bearing’ financial capital and productive capital, emphasizing the growing dominance of the former over the latter and the increasing disconnection of financial profits from production (e.g. Fine, 2013; Fine and Saad-Filho, 2017; Lapavitsas, 2013). Workers’ incomes, in so far as they are considered in this process, are often understood as being subject to new forms of ‘financial expropriation’, in which consumption is increasingly mediated through the financial system (Lapavitsas, 2013).

For present purposes, given the failure to construct functional markets at the core of this article, a slightly different reading of Marx is perhaps more helpful. The notion of commodity fetishism orienting Marxian discussion of markets is, at its core, about the fraught transformation of labour. Through its embodiment in circulating commodities, for Marx, ‘concrete labour becomes the form of the manifestation of its opposite, abstract human labour’ (Marx, 1990: 150). Notably, Marx later observes that this dynamic of abstraction reaches its logical conclusion in circulations of money in financial markets. Here, ‘all that we see is the giving out and the repayment’ and ‘everything that happens in between’ – namely concrete productive activities that enable the repayment of debts and interest – is ‘obliterated’ (1991: 471). Importantly, though, this ‘obliteration’ is only ever partially achieved. As Harvey notes, financial capital remains dependent on a ‘process of realization within the continual flow of production and consumption’ (2006: 95). In so far as financial profits appear to be ‘decoupled’ from productive activities, or purely speculative, then they represent ‘the capital mystification in its most flagrant form’ (Marx, 1991: 516, emphasis added).

The corollary here is that financial markets, and particularly the kinds of consumer financial markets of interest in the promotion of financial inclusion, cannot be conjured easily. The (accordingly) troublesome and failure-prone character of neoliberal interventions has not often been given sufficient attention. There have been a number of important contributions that have sought to locate the sources of financial crises in the overextension of credit and inability of financial capital to realize returns in the ‘real’ economy – per Harvey’s oft-cited aphorism, ‘no matter how far afield a privately contracted bill of exchange may circulate, it must always return to its place of origin for redemption’ (2006: 246). Froud et al. (2010), for instance, point to the inability of pre-crisis financial innovations in the USA to overcome the ‘tyranny of earned income’. Soederberg (2014) somewhat similarly highlights the ways in which ‘debtfare’ policies seeking to govern poverty and social reproduction through the extension of new forms of credit have created systemic contradictions in the USA and Mexico. But the other implication of the problem of ‘everything that goes on in between’ highlighted by Marx has received considerably less attention; namely, constructing financial markets in the first place is liable to be difficult in the absence of underlying configurations of labour social reproduction that enable regular payments of, for example, interest, premia and savings. The point here is that Marx’s reflections on markets and fetishism offer a useful way of thinking through the fundamental limits against which neoliberal projects aiming to conjure and re-engineer financial markets are likely to continually run up. It is both difficult for the poor to participate in markets, and unprofitable to construct new markets for them, for precisely the reason the poor are often held to need the construction of new markets – namely, low and unpredictable incomes.

Indeed, these conditions appear to have become more common globally in the context of increasingly widespread austerity, the renewed commodification of housing and basic services and stripping back of employment protections. It is beyond the scope of this article to argue this point at length, but there is something approaching consensus that precarious and irregular livelihoods are on the rise in most places in the context of wider neoliberal reforms (e.g. Phillips, 2016; Selwyn, 2014, 2019). Authors have identified important countervailing tendencies, including the widening of some kinds of social protection (e.g. Ferguson, 2015; Harris and Scully, 2015), and argued that precarity cannot be solely attributed to neoliberalism as it is more deeply rooted in capitalist and colonial modes of exploitation (e.g. Bernards, 2018; Harris and Scully, 2015). But the general association between neoliberal reforms and increasingly precarious incomes, particularly of the poorest, seems to hold fairly widely. If we pay attention to ‘everything that goes on in between’, in short, we might suggest that financial inclusion has often run up against limits imposed by the effects of prior neoliberal reforms on labour and livelihoods across the Global South.

To pull these threads together, we can suggest that efforts to construct new markets for financial services in particular are dependent on configurations of labour and livelihoods enabling borrowers to repay credit, or pay insurance premia, out of wages or other earnings. Highlighting the encounter between continual efforts to re-engineer markets and the configurations of productive and reproductive activities on which they rest offers us a crucial means of understanding the troubled progress of neoliberal reforms in general, and of slotting the turn to technology into the fraught history of neoliberal engagements in poverty finance more narrowly. In this context the appeal of ever-more fine-grained information with which to properly allocate credit can be read both as yet another attempt to ‘re-engineer’ the market (Mirowski, 2009), but also as a doomed project. In the next section, I start to flesh out this argument by tracing the longer trajectory of failure and adaptation in neoliberal developmentalism underlying the recent turn to fintech.

Situating the turn to technology

As noted above, the turn to technology can be read as an emergent response to accumulating failures in promoting financial inclusion. We better understand the political dynamics at play by recognizing (1) that the project of financial inclusion itself needs to be read in the context of a longer cycle of failures and adaptations; and (2) that initial articulations of the financial inclusion agenda laid much of the groundwork for the consensus currently embodied in the Sochi Accord, G20 HLPs and BFA.

From microcredit to financial inclusion

The emergence of microcredit as a development fad, notably, has its origins in responses to the failures of structural adjustment in the 1990s and 2000s. Microfinance, in so far as it was seen as a means of ‘empowering’ the poor in developing countries, particularly marginalized women (see Rankin, 2001), by giving them access to credit that in theory would allow them to participate in entrepreneurial activities, exemplified a wider movement towards more dispersed forms of development practice aimed at producing markets more directly (see Cammack, 2004).

In practice, though, the fact that microcredit remained heavily dependent on public subsidies led the World Bank in particular to seek to shift microfinance operations onto more explicitly commercial bases. Particularly notable here are efforts, often driven by the World Bank from the early 2000s, to promote the ‘sustainability’ of microcredit by forging linkages to global capital markets. This often took the form of mechanisms to facilitate the flow of information to investors, particularly through the establishment of microcredit rating techniques, ‘Microcredit Investment Vehicles’ and the securitization of microloans (see Aitken, 2013; Henrikksen, 2013; Soederberg, 2014).

Commercial microcredit failed. While broader problems with microcredit are well-rehearsed elsewhere (see Bateman, 2010; Bateman et al., 2018; Maclean, 2013; Rankin, 2001; Taylor, 2012), it is worth noting two things. First, commercial microfinance institutions rarely lent money to the poorest. Even microfinance advocates often had to concede that ‘most institutions serving the poorest borrowers attract profit rates too small to attract profit-maximizing investors’ (Cull et al., 2009: 13), pointing to a ‘profit–outreach tradeoff’. Second, where microloans were made, studies accumulated revising claims about positive impacts downwards to enabling ‘consumption smoothing’ rather than entrepreneurial investments that would raise incomes (see Bateman, 2010; Taylor, 2012). These questionable positive impacts were compounded by crises prompting concerns about overindebtedness – most notably the October 2010 suicides of highly indebted farmers in Andhra Pradesh, India (see Taylor, 2011, 2012).

Microfinance initiatives have persisted – and have even been transported into new territories in the Global North (Gerard and Johnston, 2019). However, microfinance has increasingly been subsumed into a wider agenda of ‘financial inclusion’ since 2010. An important step here was the announcement of the ‘G20 Principles for Innovative Financial Inclusion’ in 2010 (AFI, 2010) and the subsequent Maya Declaration on Financial Inclusion in 2011. This turn to ‘financial inclusion’ does represent a shift from the ‘microcredit’ agenda in some ways (see Mader, 2018). In the first instance, ‘financial inclusion’ shifts objectives away from poverty reduction per se and towards the extension of formal saving and lending to the poor in and of itself (see Taylor, 2012). This move implies a different understanding of the role of finance in enabling development. ‘Financial sector deepening’ is held to be necessary for the effective allocation of resources to enable ‘inclusive growth’ and for the management of risks on an individual level (Mader, 2018). Relatedly, ‘financial inclusion’ implies access to a wider range of financial tools beyond microcredit, especially including savings, payment systems and insurance (AFI, 2010: 1).

There is thus a shift here in terms of the way that financial markets are perceived to enable poverty reduction – it is much less a question of allocating resources to entrepreneurs, and much more a means of developing markets for the provision of risk management. Importantly, linked to this shift has been a growing recognition of a wider range of material and informational infrastructures needed to facilitate the development of these markets.

Technology and financial inclusion in and after the G20 Principles

The G20 Principles and Maya Declaration lay much of the groundwork for subsequent discussions of technology for financial inclusion. Two points are important. First, the G20 Principles place a heavy emphasis on ‘transaction costs’ as a limit on access to finance. On its first page, the AFI report outlining the G20 Principles notes that ‘As a general rule, transaction costs do not vary in direct proportion to a transaction’s size. Thus serving the poor with small value services is simply not viable using conventional retail banking or insurance approaches’ (AFI, 2010: 1). New technologies, especially mobile transactions, and ‘innovation’ more broadly, are increasingly identified as key means of reducing these costs. A recent report from McKinsey and Company, for instance, argues that: ‘Every step towards the full digitalization of financial services helps reduce costs, making it profitable for providers to serve a much larger range of customers’ (McKinsey & Co., 2016: 31).

New forms of mobile payment systems are perhaps the paradigmatic example here (see Maurer, 2012). Most prominently, M-Pesa – a mobile payment system operated by South African telecoms provider Vodacom, first established in Kenya – has grown dramatically, expanding into conventional banking services, following its establishment in 2007. M-Pesa is frequently explicitly cited as an example of good practice, in the AFI report and elsewhere (e.g. Suri and Jack, 2016). For instance, the McKinsey report cited above makes note of the reach of mobile money in Kenya – where nearly 70% of adults had a mobile money account at the time – as supporting evidence for the claim that ‘a growing majority of people in emerging economies now own a mobile phone, which can give them ready access to financial services’, and dramatically lower costs for financial institutions to serve ‘poorer and more remote consumers’ (McKinsey & Co., 2016: 31). The key claim here is that mobile technologies can enable the rapid and inexpensive extension of financial systems to populations that would normally be excluded from participation in mainstream financial markets by physical barriers resulting in overly high transaction costs, particularly because cellular networks are comparatively easy to set up in remote areas. A recent G20 report on financial inclusion notes explicitly: ‘Digital technologies have reached developing countries much faster than previous technological innovations; this is illustrated by the fact that households in developing countries are more likely to own a mobile phone than to have access to electricity or improved sanitation’ (GPFI, 2017: 9). As Maurer very aptly notes, this set of claims also includes ‘de facto, an argument for the privatisation of infrastructure development, as well as “regulatory flexibility”, and often, a retreat of the regulatory state’ (2012: 593).

It is here that the second key point about the understanding of technology in the G20 Principles and Maya Declaration becomes clear. The key mechanism by which ‘innovation’ is meant to take place is by allowing the ‘regulatory space’ for private sector experiments with new technologies and new modes of service delivery that might lower costs. This is explicit on the first page of the G20 Principles report: Financial sector policy and regulation is critical to the use of technology to promote financial inclusion. Increasing numbers of countries with large excluded populations are pioneering policy and regulatory innovations that open space for financial inclusion and similar new approaches to the delivery of formal financial services. (AFI, 2010: 1, emphasis added)

Making fintech

This final section returns to the specific trajectories of the ‘turn to technology’, and explores its limits. In the period since the AFI report, the transaction costs narrative from the 2010 G20 Principles, and exemplified by mobile money, is increasingly coupled with a diagnosis of slow progress in promoting financial inclusion as a product of the absence of adequate data with which to assess credit and insurance risks. In the words of one group of consultants, where lenders in the Global North can rely on paystubs, property registers and detailed credit histories, ‘such data are often lacking in the Global South’, leaving lenders and insurers ‘unable to properly understand their consumers and assess their risk, either forcing them to charge high interest rates to protect against unforeseen risk or discouraging them from serving new markets’ (Insight2Impact, 2016: 4).

To some extent this is reflective of longstanding concerns, particularly for the World Bank. The World Bank organized a taskforce to propose a set of basic principles on credit reporting in 2011. The report made mention of the implications of improved credit information for lending: ‘Improved information flows also provide the basis for fact-based and quick credit assessments, thus facilitating access to credit and other financial products to a larger number of borrowers with a good credit history’ (World Bank, 2011: 1). But this was decidedly a secondary concern here to issues of market ‘integrity’. The World Bank’s Doing Business reports have also regularly pointed to a positive correlation between credit bureau coverage and private credit as a share of GDP (2016: 59). But increasingly these concerns are raised in terms of their implications for financial inclusion. Importantly, digital technologies, both new forms of data and techniques for processing them, are increasingly seen as solutions that might help avoid the long, laborious and costly work of building up credit information infrastructures. A report commissioned by the Inter-American Development Bank (IADB) notes that ‘alternative analytics … help develop more robust client risk profiles at a fraction of what it would cost to compile such information manually’ (Hoder et al., 2016: 18). The key point here is that fintech applications respond to discrete challenges of market construction that have been repeatedly identified in two decades’ worth of interventions.

The World Bank and G20, together with a number of central banks and financial regulators in both Global North and South, have also increasingly promoted and coordinated targeted regulatory frameworks for fintech applications aimed at promoting ‘access’ to finance for the ‘unbanked’. Recently, CGAP (Consultative Group to Assist the Poor) in particular has promoted ‘regulatory sandboxes’ – time-limited, product-specific licences for particular companies to conduct ‘experiments’ with ‘innovative’ practices and technologies (see Jenik and Lauer, 2017). The concept was first implemented by the Consumer Financial Protection Bureau in the USA in 2012, and has been announced or implemented increasingly in low- or middle-income countries including Malaysia, India, Mauritius, Brazil, Mexico, Jordan, Kenya, Sierra Leone, China and Thailand. In early 2018, the UK’s Financial Conduct Authority proposed the development of a ‘global sandbox’. This was subsequently taken up by CGAP and a range of financial regulators through the proposed formation of a ‘Global Financial Innovation Network’ (GFIN) in August 2018 to facilitate coordination between financial regulators (GFIN, 2018). GFIN launched a pilot programme for cross-border experiments in early 2019 (FCA, 2019). This can usefully be read as an extension of earlier techniques for promoting ‘enabling regulatory environments’.

Another increasingly important form of support has been providing financial and in-kind support to particular fintech firms. The Entrepreneurial Finance Lab (EFL), for instance, a key fintech firm developing ‘psychometric’ credit scoring practices, was developed out of a 2006 research initiative at the Harvard Kennedy School. It was incorporated as a private company in 2010, and subsequently attracted funding from a number of different bilateral and multilateral development agencies. In 2013, the project was funded by the G20’s ‘SME Finance Challenge’, an initiative launched alongside the G20’s Principles for Innovative Financial Inclusion and managed by the World Bank’s International Finance Corporation, that included funding from the governments of Canada, the USA, the UK, Korea and the Netherlands (SME Finance Forum, 2014). A number of subsequent pilot studies were sponsored by the IADB and World Bank, and carried out in Latin America. The IADB facilitated and published studies co-authored by EFL staff testing models developed in the project discussed above with SME (small and medium enterprise) borrowers in Argentina (Klinger et al., 2013b) and Peru (Klinger et al., 2013c). A similar pilot project was carried out by World Bank staff in Peru in 2012 (Arráiz et al., 2015a, 2015b). EFL subsequently merged with Big Data credit scorer Lenndo in late 2017.

When set in the context of the uneven progress of the ‘financial inclusion’ agenda, growing attention to technology appears to reflect a further revision of neoliberal understandings of market-building. Where the promotion of commercial microfinance, and the early promotion of financial inclusion, tended to emphasize the construction of institutional vehicles to facilitate access to global capital markets and standardized forms of information, the ‘turn to technology’ represents a shift towards engagements with the minute, material elements of the devices needed to mobilize information and set prices.

What can fintech do?

It might be useful here to highlight the kinds of technologies that have emerged in this context. ‘Alternative’ forms of credit data are perhaps especially salient; two major developments are notable.

First are applications of ‘Big Data’ and machine-learning algorithms in credit scoring for the ‘unbanked’. Big Data applications have proliferated, if unevenly, in recent years in global finance more generally (see Campbell-Verduyn et al., 2017). In contrast to what might be called ‘small’ data – produced directly through controlled sampling techniques, limiting scope, time frame, size and variety – Big Data are produced continually, in high volume, varied and often as a by-product of the normal operation of information technologies rather than through direct investigative processes (see Kitchin and Lauriault, 2015). The analysis of such mass volumes of data is made possible by the application of computerized algorithms which are distinguished from the static ‘models’ used in traditional statistical analyses by their dynamic and recursive character (Beer, 2017). Big Data, particularly in the context of growing mobile phone and internet use in developing countries, are seen as a vital source of alternative credit scoring for ‘unbanked’ consumers: The increased use of digital technologies by [micro, small and medium enterprises (MSMEs)] and their customers is generating a wealth of new data that can be used to understand the MSME market, assess creditworthiness, and manage risk more effectively. A growing number of financial technology companies, known as ‘fintechs’, are developing innovative tools to do precisely this. As a result, traditional financial institutions are faced with both a unique challenge and an enormous opportunity. (Hoder et al., 2016: 7)

Second, there have also been efforts to develop alternative forms of ‘small’ data for evaluating credit in the absence of formal credit histories and employment or property records. Most prominent, perhaps, are so-called ‘psychometric’ credit scores (see Aitken, 2017; Bernards, 2019). Psychometric tests aim to quantify cognitive attributes for the purpose of screening individuals’ suitability for certain tasks. They originated in efforts to develop ‘scientific’ techniques for hiring (see Schmidt and Hunter, 1998). One of the highest profile such systems has been developed by EFL. EFL has developed a test drawing on measures of intelligence and ‘integrity’ which is administered to potential borrowers lacking detailed credit histories (see Klinger et al., 2013a). The test is normally administered by computer in a bank branch, but the company has developed online and mobile versions in some settings as well. In the case of either ‘big’ or ‘small’ forms of data, though, the basic point is that adopting alternative forms of credit data – often as a means of assessing the psychological character of borrowers rather than their more opaque economic circumstances – is framed as a way of diminishing collateral requirements and interest rates that might otherwise disqualify MSMEs from formal borrowing.

The possibility of expanding loan portfolios to irregular workers without increasing default risk is the core promise made by advocates of new forms of credit scoring. As the above IADB report puts it, this ‘presents a significant opportunity to expand MSME portfolios at a lower cost than was previously possible, while maintaining acceptable levels of risk’ (Hoder et al., 2016: 18). EFL echoes these arguments. While noting that psychometric credit scores are unable to match the predictive power of detailed credit histories, ‘In an information scarce setting, a tool that can signal a 50% increase in default risk is a useful signal and can identify a profitable subset of an overall population that is too risky to lend to and otherwise indistinguishable’ (Klinger et al., 2013a: 43). Experiments with fintech are increasingly explicitly articulated, in short, around the livelihood activities of the ‘unbanked’.

There is already something of a contradiction at work here with respect to inclusion. There is a logic of segmentation, stratification and exclusion – of sorting out those able to profitably participate in credit markets from those ‘too risky’ to do so – at play in the development of alternative forms of credit data (Aitken, 2017: 291). Some hints about the limits of the turn to technology in terms of promoting inclusion are made more evident by considering the wider trajectory above. New forms of stratification seem unlikely to overcome the underlying ‘profit–outreach tradeoff’ (Cull et al., 2009). Indeed, as Mader (2018) rightly argues, financial capital has continued to ‘cherry pick’ its engagements with the agenda of financial inclusion, primarily through high-interest loans to the urban, ‘less poor’. Fintech applications ultimately promise, at best, more fine-grained forms of cherry-picking. They do not help to solve the more fundamental underlying problem, which is simply that irregular and precarious incomes are exceedingly difficult to convert into predictable ‘asset streams’ (Leyshon and Thrift, 2007) amenable to financial speculation. This trajectory is usefully understood in terms of the ongoing confrontation between neoliberal logics of perpetually re-engineered marketization, particularly the emphasis on markets as processors of information, and ‘all that goes on in between’ (Marx, 1991) in terms of productive activity and livelihoods in order to enable commodified, fetishized market activities. The turn to technology represents a continuation of particular regulatory logics implicit in previous interventions to promote microfinance and financial inclusion, without addressing the underlying challenges that have hampered these projects.

Conclusion

In this article I have shown how the turn to technology in financial inclusion slots into a longer trajectory of failures and mutations of neoliberal development governance. It clearly encapsulates a trend towards experimentation and provisional governance in response to repeated failures. The turn to technology also fails to move beyond the more fundamental challenges stemming from the problematic construction of ‘markets’ underlying neoliberal reasoning. There is a particular (neo)liberal logic underlying these developments. The BFA, Sochi Accord, and G20 HLPs can be read in the first instance as reflections of an emergent consensus around how ‘suitably re-engineered and promoted’ (Mirowski, 2009) markets for financial services for the poor might be brought about through appropriately nurtured technological innovation. In concluding here, I argue that it remains questionable whether building such infrastructures, in and of itself, is enough to enable the constitution of new forms of financial markets. The turn to technology, I argue here, is better understood as a fraught and failure-prone effort to re-engineer financial markets that might effectively serve borrowers with irregular and unpredictable incomes.

We usefully understand what is at stake in this turn to technology if we understand it in terms of neoliberal governance. The turn to technology, in short, represents an effort to make an end-run around a long-running and critical paradox in the ‘financial inclusion’ agenda by ‘re-engineering’ (per Mirowski, 2009) financial markets – this time with interventions aimed at infrastructural components of financial practice, tinkering with the devices through which market relations are enacted (see Muniesa et al., 2007). But this is an effort that seems destined to continue to founder on the problem of ‘everything that goes on in between’ (per Marx 1991). This is perhaps especially significant because it suggests dynamics of failure and adaptation that readings of fintech and financial inclusion in terms of ‘financialization’ are likely to miss.

This matters because it underlines just how far ‘fintech’ is a political phenomenon, in the sense of being bound up with the promotion of particular political projects by national and global regulators. It represents (yet another) contingent and fraught effort to tinker at the margins of neoliberal development models. Analyses that start from the premise that fintech is part and parcel of wider processes of ‘financialization’, whatever their other important contributions, are likely to miss this important aspect of the underlying politics of ‘innovation’. The turn to technology is perhaps not so much a sign of the ‘inescapability’ of finance (per Hall, 2012) as it is of continued efforts to grapple with the recurrent failures of neoliberal efforts to build and re-engineer financial markets.

Footnotes

Acknowledgements

Thanks to the anonymous reviewers at this journal for their comments, which have greatly improved the finished article.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.