Abstract

Alternative credit scores have become an increasingly important tool for lenders to assess risk and authorize investment in consumer debt. Using alternative data and processing techniques that leverage machine learning (ML) and Artificial Intelligence (AI), these models are designed to bypass existing barriers to risk-based pricing, which is the idea that financial institutions offer different interest rates to consumers based on their likelihood of default. Through an algorithmic audit of one lender's (Upstart) credit scoring model, I find that alternative data, particularly whether an applicant has a bachelor's degree, strongly impacted loan outcomes. This raises important equity concerns about overhauling lending criteria via opaque models that restructure the logic of risk assessment. In following the logic of risk assessment generated by Upstart's model, I also audit three fintech-bank partnerships and examine the balance sheets of banks providing capital via Upstart's platform. This is done to demonstrate rising capital allocation to these types of loans at banks engaged in fintech-bank partnerships, in one case rising from 0.14% to 15.6% of the banks’ balance sheet over three years. My analysis shows that alternative credit scoring systems function as a key piece of calculative infrastructure, which allows some institutions to bypass barriers to risk-based pricing, and becomes an infrastructural site for tech startups to partner with financial institutions seeking out new sources of revenue.

Introduction

With U.S. household debt climbing above $16 trillion in the first quarter of 2022, the share of consumer debts accounted for automobile, credit card, and personal loans have grown dramatically over the past decade. Where the percentage of non-housing debt fluctuated between rates of 25% and 33% of total consumer debt prior to the 2008 financial crisis, non-mortgage debts approached 40% of all consumer debt in the years leading up to the COVID-19 pandemic (Household Debt and Credit Report, 2022). A growing industry of consumer lenders is partially responsible for this shift, as companies leverage platform technology and proprietary risk assessment algorithms to disburse debt in new ways. Following this story, this study is rooted in the acceleration of consumer debt as an engine of economic growth, particularly personal loans, and investigates the calculative tools used to deploy this debt in new ways.

Personal loans are flexible, mostly unsecured (Wolfson, 2022) financial products that can be used for expenditures ranging from household expenses to debt consolidation. Prior to the COVID-19 pandemic, personal loans were the fastest growing U.S. financial product at a yearly growth rate of over 12 percent (Lemdo Stolba, 2021), and while growth slowed to 6 percent in 2021 due to U.S. federal pandemic assistance programs, growth in personal loans is expected to return to previous highs (VanSomeren, 2022). Constructing a market for personal loans has required lenders address the unique risks of unsecured consumer debt (UCD). UCD is debt not backed by an existing asset, meaning these types of loans often involve higher interest rates for consumers and greater risk for institutions. Consumer lenders have responded by creating ‘alternative’ risk assessment models that use non-standard financial data and processing techniques as a way of circumventing the increased risk associated with UCD. These systems have been successful in legitimating personal loans as an object of investment as evidenced by a spate of securitization deals (Avant, 2021; KBRA, 2022) and growing fintech-bank partnerships in the sector (Williams, 2022).

The prevalence of fintech-bank partnerships remains an open question that has drawn increasing attention from a trio of U.S. regulators. In July of 2021, the Office of the Comptroller of the Currency (OCC), Federal Reserve, and Federal Deposits and Insurance Corporation (FDIC) issued shared guidance for risk mitigation when banks partner with fintech firms (Board of Governors of the Federal Reserve System, Federal Deposit Insurance Corporation and Office of the Comptroller of the Currency, 2021). This guidance encourages additional risk mitigation when banks use fintech products to augment core operations such as lending and deposits. Echoing these concerns at a conference in New York, the head of the OCC, Michael Hsu, warned bankers that novel “Banking-as-a-Service” arrangements may be creating systemic risks for the financial system (Williams, 2022). Of particular interest for this paper is Hsu's suggestion that smaller community and regional banks may be most at risk as they struggle to compete with larger banks developing in-house technology.

This paper responds to the call from U.S. regulators for additional research on fintech-bank partnerships (OCC, 2022) by auditing the infrastructure of one company's (Upstart) alternative credit scoring model. Upstart is a consumer lending firm headquartered in San Mateo, CA that specializes in alternative credit risk assessment. Upstart has become one of the largest fintech lenders through its online lending platform and uses machine learning credit models to issue products ranging from automobile to personal loans. In auditing Upstart's model, I ask two research questions: 1. How do alternative credit scoring models impact loan outcomes? and 2. How do alternative credit scoring models change bank lending priorities? In answering the first question, I find that alternative financial data, particularly whether an applicant has a bachelor's degree, strongly impacted loan outcomes in the audit. This raises important equity concerns about overhauling lending criteria with new statistical methods that restructure the logic of risk assessment. Second, I find that each bank identified to be hosting loans on Upstart's platform had an outsized portion of its balance sheet allocated to personal loans. Further, several of these banks saw a sharp rise in capital allocation, in one case rising from 0.14% to 15.6% of the banks’ balance sheet over three years. Building from Marron's (2007) argument that paradigmatic shifts in lending are facilitated by changes in the calculative tools used to construct risk, this study documents both the tools—alternative credit scoring models—as well as the shift in lending patterns emerging out of their adoption in consumer finance.

Following the introduction, this paper proceeds in three parts. First, I develop a theoretical framework for understanding alternative credit scores as calculative infrastructure. Second, I conduct an algorithmic audit of Upstart's model (Audit I) and document the impacts of alternative credit scores on consumers. Third, I audit the partnership arrangements of Upstart (Audit II) to identify three fintech-bank partnerships and document the impacts of these partnerships on bank balance sheets. I conclude by summarizing the findings of the audit and discussing the significance of novel risk assessment algorithms and the financial partnerships emerging from these models.

Geographies of calculative infrastructure

Over the past five years, economic geographers have developed a research agenda (Lai and Samers, 2021; Wójcik, 2021a, 2021b) to understand financial technologies and their impact on economic processes– ranging from studies of cryptocurrencies in startup financing (Zook and Grote, 2020) to refugee governance in fintech banking and lending (Bhagat and Roderick, 2020). Especially relevant to this paper is the insight from Hendrikse et al. (2020) that strategic couplings between individual firms, technologies, and state regulation plays an outsized role in the adoption of fintech products and services.

While this agenda has been instrumental to understanding the structural changes brought about by fintech (Wójcik, 2021a, 2021b), comparatively little has been written about the role of financial technologies in constructing markets (Berndt and Boeckler, 2011) for consumer debt. Zook and Spangler (2022) offer a useful conceptualization of debt as an instrument–that is to say debt as a financial product–and debt as a condition, meaning indebtedness as a lived process. Efforts by financial capital to flatten the distinctions between debt as an instrument and debt as a condition often fail as the “mortgaged lives” (García-Lamarca and Kaika's, 2016) of consumers become constitutive of the “financialization of everyday life” (Burton et al., 2004; Lai, 2018; Langley, 2010; Martin, 2002).

Building from this starting point, my framework focuses on alternative credit scoring models as they restructure debt as an instrument, while also attending to the ways debt is made to matter (Barad, 2007; Amoore, 2013) through its enrollment in debt as a condition– particularly the ways that borrowers have leveraged personal loans in debt consolidation and struggles to reclaim financial citizenship (McCanless, 2021). First, I explore the history of risk-based pricing and its continuities with novels forms of credit scoring. Second, I conceptualize alternative credit scores as a piece of calculative infrastructure deployed by institutions generate new sources of revenue. Consequently, this paper draws from work seeking to understand how the financial system interfaces with risk assessment technologies ranging from real estate (Fields, 2018), to climate finance (Taylor, 2020)–that is to say, sites where technology is deployed in the hopes of profiting from risk.

Alternative credit scores, alternative visions of risk

The purpose of twentieth century U.S. fair lending laws was to standardize the collection and use of credit data, while simultaneously generating economic demand through expanded markets for consumer debt (Kear, 2014: 100). Legal frameworks like the Fair Credit Reporting Act (FCRA) ensured the privacy and accurate collection of consumer credit information, while laws such as the Equal Credit Opportunity Act (ECOA) and the Fair Housing Act (FHA) mandated that credit information not include a series of protected categories such as race or gender (Evans and Miller, 2019). These frameworks do not mandate that credit must be non-discriminatory; in fact, discrimination amongst applicants is the purpose of credit rating systems (Marron, 2007), but rather that U.S. lenders cannot discriminate on the basis of a protected category of information.

An unintended consequence of this framework is the incentivization of firms to create statistical methods that price risk for those on the margins of credit access (Marron, 2007). Risk-based pricing is the idea that financial institutions “offer different consumers different interest rates or other loan terms, based on the estimated risk that the consumers will fail to pay back their loans” (CFPB, 2016). Underwriting models that use risk-based pricing have long been used in car, home, and auto insurance – but were notably applied to financial services in the 1990's as statistical models seeking to maximize economic demand created markets for ‘subprime’ loans (Marron, 2007: 122).

The fallout from subprime lending led to a preference amongst most financial institutions for models that prioritize linear connections between standard data and financial risk (Thomas et al., 2005), creating an opening for other less regulated actors, such as financial technology firms, to experiment with new data and processing techniques. For example, industry researchers at FinRegLab have shown that cash flow data from an applicant's bank account is able to broaden the availability of credit and better predict loan performance for financial institutions (Courchane & Baines, 2019). Other approaches train models to process data associated with educational attainment, employment history or type of income, and even intentionally designed psychometric tests (Dash et al., 2021; Renton, 2017).

To be clear, the impetus behind alternative credit scoring is not new (Marron, 2007; Kear, 2014). However, alternative credit scores depart from prior forms of credit scoring in two key ways. First, new types of credit data are being used to “bank the unbanked” (Aitken, 2017) and rework the performance of financial subjectivities (Kear, 2017). Second, the complex statistics associated with AI and ML are not merely passive technical objects but rather “engines” (MacKenzie, 2008) that produce correlations which materialize connection across vast “neighborhoods” of data (Chun, 2021). These connections, within the context of alternative credit scoring, should be understood as producing a construction of risk that governs credit access.

Financial technology as infrastructure

July 2021 saw the US Federal Reserve issue a call for comments on regulation to fintech-bank partnerships. Specifically, the call requests further information on fintech applications that streamline bank operations relating to back-office paperwork, artificial intelligence in asset management, alternative credit scoring and risk assessment models, blockchain and custody of digital assets, amongst others (Federal Reserve, 2021). These technologies, designed to simplify the complex assemblage of human, technological, and financial processes within banks, exemplify what Bernards and Campbell-Verduyn (2019) understand as financial infrastructure. Following Bowker and Star (1996), Bernards and Campbell-Verduyn (2019) develop a theoretical framework that leverages science and technology studies (STS) to understand how financial tools, devices, and techniques drive financial systems. Conceptualizing financial infrastructure in this way highlights the “combination of human and non-human elements” which “enable key functions in global finance” (p. 5) such as microfinance loans for consumers from the Global South (Gabor and Brooks, 2017; Langevin, 2019; Bernards, 2019) or the resolution of counterparty risk in derivative markets (Genito, 2019).

As a subcategory of financial infrastructure, calculative infrastructures “designate the relatively stabilized chain of accounting calculations and associated narratives, the ensemble of calculative technologies, and rationales that have come to appear necessary” (Kurunmäki and Miller, 2013: 1101) in the governance of quantified life (Mennicken and Miller, 2012). In that vein, calculative infrastructure has been used to understand the economization of failure (Kurunmäki and Miller, 2013; Kurunmäki et al., 2019), particularly in relation to corporate and healthcare systems (Juven, 2019; Reilley and Scheytt, 2019) as the ability to forecast risk and index failure has become a defining feature of business operations. Thus, calculative infrastructure is defined as the tools, techniques, and infrastructures built to manage and economize risk.

Taking note of this work and recognizing the applicability to credit risk assessment–I deploy the term to understand how alternative credit scores function as calculative infrastructure in stabilizing risk-based pricing on consumer loans (Marron, 2007). While this differs from prior uses in that it does not focus on corporate or institutional failure, it extends an observation in Kurunmäki and Miller (2013) that calculative infrastructures are becoming increasingly diffuse within everyday life. In conceptualizing alternative credit scores as infrastructural, I track this diffusion of calculative infrastructure within consumer finance by focusing on the fintech-bank partnerships that materialize the logic of risk assessment produced by novel credit scoring techniques.

Audit I: alternative credit scores as calculative infrastructure

Alternative credit scores as calculative infrastructure reformulates risk assessment in ways that authorize investment in consumer debt. The following section designs and implements an algorithmic audit of one alternative credit scoring model from the firm Upstart, and unpacks the vision of risk rendered by its model in order to situate its outcomes for consumers. This section proceeds by describing the methodology used to conduct the audit before describing its results. Models like Upstart's are increasingly common in consumer finance, introducing opaque machine learning techniques that draw non-linear connections between variables and lending outcomes. As a result, the focus on Upstart's model should be understood as a test case for the diffusion of calculative infrastructure in the “financialization of everyday life” (Lai, 2018). The finding documented in this section that educational attainment shapes credit access under Upstart's model raises important questions about how calculative infrastructure might encroach on protected characteristics such as an applicant's race or gender (see also SBPC, 2020).

Designing an algorithmic audit

An algorithmic audit (Benjamin, 2019; Brown et al., 2021; Bucher, 2018; Burrell, 2016) uses experimental methods to analyze a piece of digital infrastructure such as a ranking algorithm on a website. Other applications of algorithmic audits include social media feeds (Bucher, 2018) facial recognition software (Banerjee et al., 2022; Keyes and Austin, 2022), or employment advertising programs (Imana et al., 2021). In situations where access to a given technology is limited, algorithmic audits offer a way to investigate algorithmic governance

This paper models its audit design on a study conducted by the Student Borrower Protection Center (SBPC). The SBPC is a leading advocate group working to expand consumer protections for student loans and combat the student debt crisis in the U.S. The SBPC audit used one researcher to submit a series of dummy profiles through Upstart's ‘check your rate’ option. Those profiles manipulated user volunteered information pertaining to an applicant's educational institution, documenting differences in loan outcomes associated with where a borrower received a bachelor's degree. This audit found that a dummy profile showing a degree from majority Black Howard University was far more likely to receive an inflated rate when compared to a hypothetical borrower from majority white New York University or majority Latinx New Mexico State University (SPBC, 2020).

I expand on the approach developed by the SBPC by using 12 close contacts to run profiles through Upstart's ‘check your rate’ option which was accessed on the homepage of Upstart's website. The backgrounds of volunteers were between the ages of 23 and 31, all had bachelor's degrees, and wide ranges of underlying credit histories. The role of participant backgrounds in this audit is fraught given that firms use third-party data and risk analytics providers to locate borrowers across data infrastructures. This inability to account for all flows of information circuited into Upstart's model introduces a series of limitations and biases to this study. Most importantly, this limits my ability to draw conclusions across profiles (i.e., John-1 vs. Patricia-1), as real credit histories influenced these markedly different outcomes. This does not, however, limit my ability to draw connections between profiles (i.e., John-1 vs. John-3). As shown in the results section, broadening the pool of dummy profiles from 1 (in the SBPC audit) to 12 (in this audit) captures a broader segment of user volunteered information and its integration into alternative credit scoring models.

Where the SBPC audit tested for the impact of educational institutions on loan outcomes, I designed profiles to test for three categories of user volunteered information. Those categories were their location within several Memphis, Tennessee, neighborhoods, whether the applicant had a bachelors or certificate degree, and whether the applicant was a barber/hairstylist or an insurance salesperson. I chose to locate the dummy profiles in the city of Memphis because of my familiarity with the city's neighborhoods and the stark levels of racial and economic segregation in the selected ZIP codes. I tested for differences associated with a bachelor's degree in business from the University of Memphis compared to a certificate 2 degree in barbering/hairstyling from Empire Beauty School in East Memphis. I also tested for differences in employment between an insurance sales agent (salaried) and a barber/hairstylist (non-salaried). The specifics for the second and third categories of information were chosen due to the socially saturated nature of these data and their potential to serve as proxies (Chun, 2021; Phan and Wark, 2021) for protected classes of information pertaining to race or gender under U.S. fair lending laws.

Alongside the user volunteered data for location, education, employment, the platform required a second category of user information pertaining to an applicant's financial status. These consisted of income, savings, and loan amount, which I used as control variables to better understand the manipulated variables of location, education, and employment data. I found profiles reflecting middle- and upper-class financial situations to be less likely to trigger the platform's fraud detection system which was necessary to gather sufficient data for analysis. Another avenue for an algorithmic audit of credit risk systems might test for whether dummy profiles showing a more distressed financial situation trigger platform security measures more often than those evidencing a stable financial situation. See Table 1 for a full list of manipulated and control variables used in the algorithmic audit:

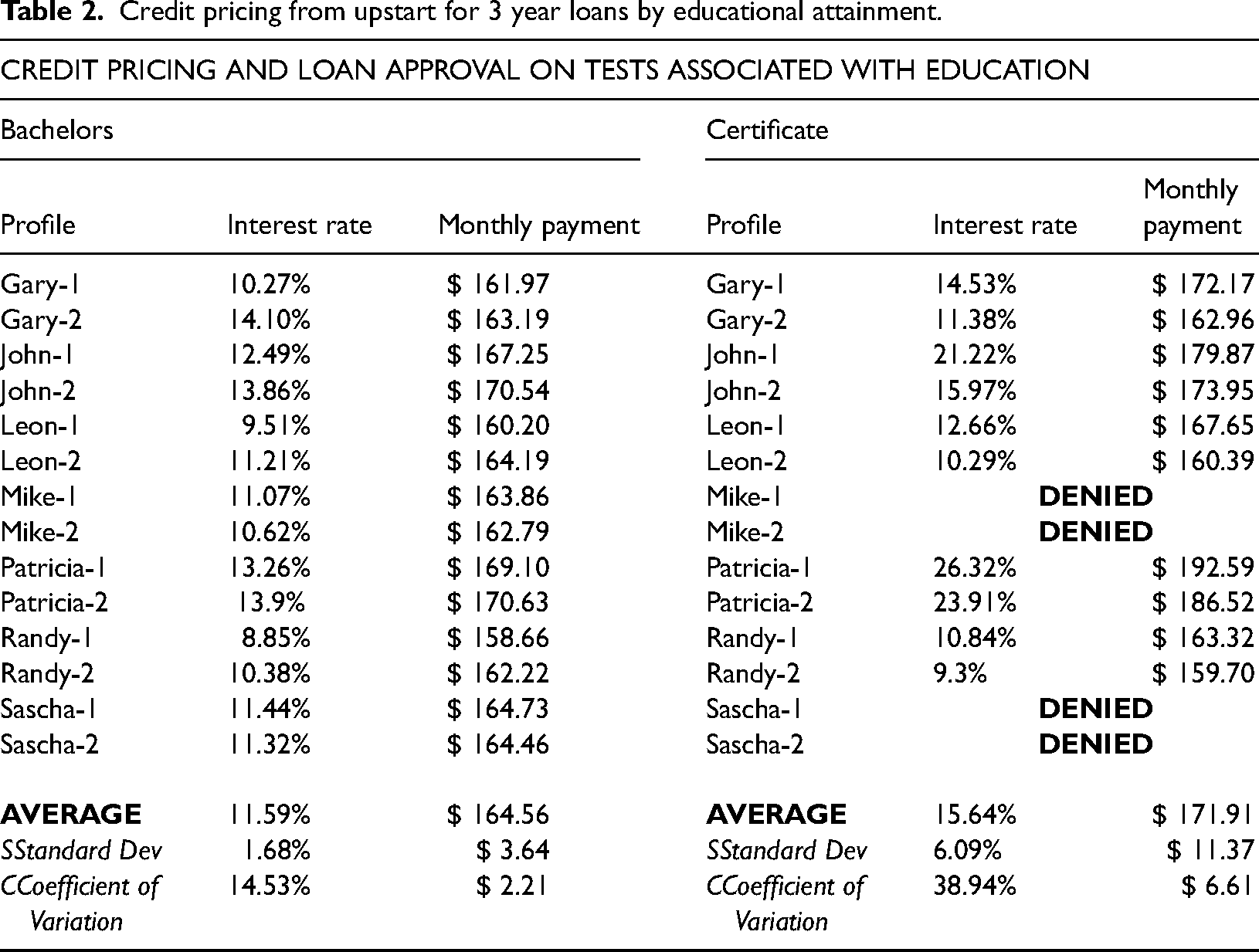

List of manipulated and control variables used in algorithmic audit.

The results from the audit are grouped into two categories for analysis: 1. results associated with loan approvals and credit pricing and 2. documentation of bank sponsors providing capital to be hosted on Upstart's platform. The first result is summarized in Table 2 and used to analyze the impact of alternative data on Upstart's alternative credit scoring model. Descriptive statistics such as the standard deviation and the coefficient of variation are used to understand the variance in Upstart's model. The second result, comprised of the three banks offering loans to the dummy profiles, is analyzed in the following section of this paper (Audit II)

Credit pricing from upstart for 3 year loans by educational attainment.

Impacts of alternative credit scores on credit approvals and pricing

Table 2 shows dummy profiles that received at least one approval based on varied input of educational attainment. The results in Table 2 represent one third of all profiles in the audit as a parallel set of profiles were used to test for impacts on outcomes relating to location, which showed no impact, and employment, which was inconclusive. The results summarized in Table 2 show the interest rate and pricing on loans testing for education.

This audit finds that user volunteered data has a strong impact on Upstart's lending process. Profiles showing a certificate degree were over 4% more expensive than those reflecting a bachelor's degree. Additionally, certain profiles saw dramatic fluctuations in pricing when moving between a bachelors and certificate degree. This is evidenced by the much higher coefficient of variation for certificate profiles, 14.53 for bachelor's degrees and 38.94 for certificates. For example, Gary's and Randy's series of profiles showed minimal differences in pricing when moving between a bachelors and certificate degree. However, Patricia and John experienced a dramatic rise in rates—doubling from 13% to 26% on a 3 year loan in the case of Patricia-1.

These differences between profiles (e.g., Patricia-1 Bachelors vs. Patricia-1 Certificate) provide evidence that user volunteered data is impacting Upstart's pricing model. One interpretation of these results is that dummy profiles ran by volunteers with robust credit histories were rendered calculable with standard credit data, explaining why these profiles received stable rates when educational status was changed. For the second cohort of profiles which saw dramatic rate fluctuations—those seemingly on the margins of credit access in Upstart's model—the provision of user volunteered data rendered the risk on their applications calculable, albeit with a cost that was nearly 2× more expensive on certain profiles.

Supporting this conclusion is the data on approvals and denials. Mike and Sascha were approved for loans at relatively low rates with a bachelor's degree, but were denied when their profiles were changed to reflect a certificate degree. Unlike Patricia and John, these profiles did not experience dramatic rate fluctuations, but rather an outright foreclosure of credit access. This suggests that Upstart's model deploys the predicative capacity of education as a filter through which applicants on the margins of credit access are sorted. Profiles with the ‘right’ credentials are rendered calculable and open to high-cost investment, while others are interpreted as too risky without the credential of a bachelor's degree.

The immediate implication of these findings is that firms use alternative credit scoring models to expand the pool of borrowers that can access credit, but on highly uneven terms. The profiles in this audit evidence that process, with some – Gary, Leon, and Randy – receiving a standard rate when moving between a bachelors and certificate degree, and others–Patricia, John, Sascha, and Mike–experiencing dramatic differences in loan outcomes. Further research is needed to identify the characteristics of those targeted by new risk assessment models and the underlying, ‘real’ factors informing these different algorithmic interpretations of risk.

Education as a racial formation as a data formation

The primary finding of this audit is that alternative credit scores affect lending outcomes and provide the “calculative agency” (Çalışkan and Callon, 2010; Fields, 2018) to invest in personal loans. Given limited access to the model, this study can only theorize why education enables Upstart's model to operate in this way. Nevertheless, theorizing the significance of education is important given education's role as a political-economic credential that governs lives and livelihoods in the U.S. (Rosenman et al., 2022).

One way of theorizing education's significance to these findings is that educational attainment functions as a proxy in Upstart's model. Similar models have raised concern amongst consumer advocates that a variable like education may proxy for legally protected categories such as race or gender (SPBC, 2020) Given the social significance of education, it is not hard to envision how a proxy derived from education could enable what Simone Browne (2010; 2015) calls “digital epidermalization” in which the bio-spatial dimensions of race become “rendered as digitalized code” (2015: 109) and integrated into systems such as biometric property technologies (McElroy, 2019, 2020). Within the context of credit risk assessment, digitally epidermalized proxies may facilitate a process of “predatory inclusion” (Chaudry, 2018; Puar, 2012; Taylor, 2019) by which borrowers racialized as Black are included within finance, but on terms that become wealth depreciating (Charron-Chénier and Seamster, 2021), while borrowers racialized as white leverage differential access to further asset accumulation (Adkins et al., 2020; McCanless, 2021).

A second way of understanding these results is by unpacking the classifications and categorizations generated from education. This approach suggests that educational attainment is not simply a socially saturated data point, but rather an algorithmic classification produced by machine learning techniques and the application of inductive reasoning to large datasets. Phan and Wark's (2021) theory of “racial formations as data formations” show how large-scale, data-processing systems produce digital structures with the capacity to “produce race by other means” via the racial imperative “to classify, to differentiate and, crucially, to determine context” (4). In contrast with proxies which seek to locate racial identification on the other side of the model, racial formations as data formations produce categorizations of risk that impose racializing logic without an auditable connection to what Simone Browne calls the “visual economy of race”

While theoretical, these formulations might not be too far afield, as a recent report from Relman Colfax, the law firm tasked with monitoring Upstart's model, found that Upstart was approving Black borrowers less frequently than white counterparts (Relman Cofax, 2022). While the firm is careful to note this does not constitute a fair lending violation given that fair lending laws do not actually require equitable lending, this does suggest that alternative credit scoring models fail to get around existing inequities in lending, while potentially reworking similar patterns of racialized inequity in new ways. In conclusion, it is important to clarify that the ability of machine learning models to generate discriminatory classifications is not significant on its own—machine learning algorithms can generate any number of connections between seemingly disparate datapoints—rather these classifications assume significance as they are integrated into financial infrastructure. As the next section will show, the predictive power of Upstart's model has drawn partners from the financial sector, seeking new ways to allocate capital in novel fintech-bank partnerships.

Audit II: accessing calculative infrastructure via fintech-bank partnerships

Fintech-bank partnerships have come under increased regulatory scrutiny in 2021 (Federal Reserve et al., 2021) as regulators increasingly argue that novel fintech applications may create unseen risks to the financial system (Williams, 2022). While few details have been provided on exactly which types of fintech-bank partnerships pose the most risk, lending and risk assessment were identified as an area of concern in a call for research published by the OCC in June 2022 (OCC, 2022). In taking up this call for further research on fintech-bank partnerships, I extend the idea of an algorithmic audit to the second category of results – namely the three institutions found to be offering loans in the audit—and investigate the impact of calculative infrastructure on each bank's balance sheet. These three banks: First Federal Bank of Kansas City, Cross River Bank, and Customers Bank reflect the specific partnership arrangements of Upstart, rather than the industry as a whole, but provide some of the first data on fintech-bank partnerships and their impact on capital allocation across multiple banks. Ultimately, I argue that the capacity of calculative infrastructure to price risk has resulted in partnerships between fintech firms and bank partners that draw from the unique circumstances of each bank in altering capital allocation in consumer lending.

Connecting audit insight with financial infrastructure

Much like technology companies that use platforms to strategically mask their operations, financial institutions represent their own kind of ‘black-box’. Insight into the institutions that define financial capitalism, such as investment banks, pension funds, or private equity firms, is notoriously difficult. In many cases, capital allocation is a closely guarded component of competitive advantage. One notable exception is FDIC insured banks. U.S. regulators require that banks insured by the FDIC report detailed accounts of their operations which are made publicly available through the Federal Financial Institutions Examination Council (FFIEC).

As a result, this section leverages the strategic visibility of FDIC insured banks to audit the financial infrastructure of Upstart's alternative credit scoring model. To do this, I analyze the balance sheet of each bank found to be hosting loans on Upstart's platform. I do this by analyzing call reports between the years of 2017–2021. Call reports are quarterly financial documents that provide a detailed snapshot of an insured bank's lending and deposit activity. These documents provide rich material for “critical financial analysis” (Kass, 2020) and unpack the “technocratic nature” (p. 4) of bank capital allocations, connecting this process to real-world phenomena such as the use of alternative credit scores in consumer finance,

Across all banks identified in the audit, there was considerable growth in installment lending. Installment lending is chosen because it represents the accounting category under which the personal loans issued by Upstart would be tabulated on these banks’ balance sheets. Notably, installment lending encompasses more than personal loans, as other non-standard credit products such as private student loans are accounted under this line item. However, given the public advertisements for personal loans at these three banks, as well as a lack of identifiable private student loan offerings, installment lending functions as an acceptable ‘proxy’ by which I track the movement of personal loans from Upstart's lending algorithm onto the balance sheets of these three banks.

An analysis of installment lending at these banks develops two key findings: 1. that alternative credit scoring models can increase the percentage of bank capital allocated to certain financial products and 2. the character of that growth is dependent upon the local and institutional context of each bank. The three case studies in this section illustrate how fintech-bank partnerships may change lending patterns at banks, as well as the ways that banking is dependent on local and institutional context, such as declining community bank shares in mortgage markets or the acquisition of tech startups by commercial banks.

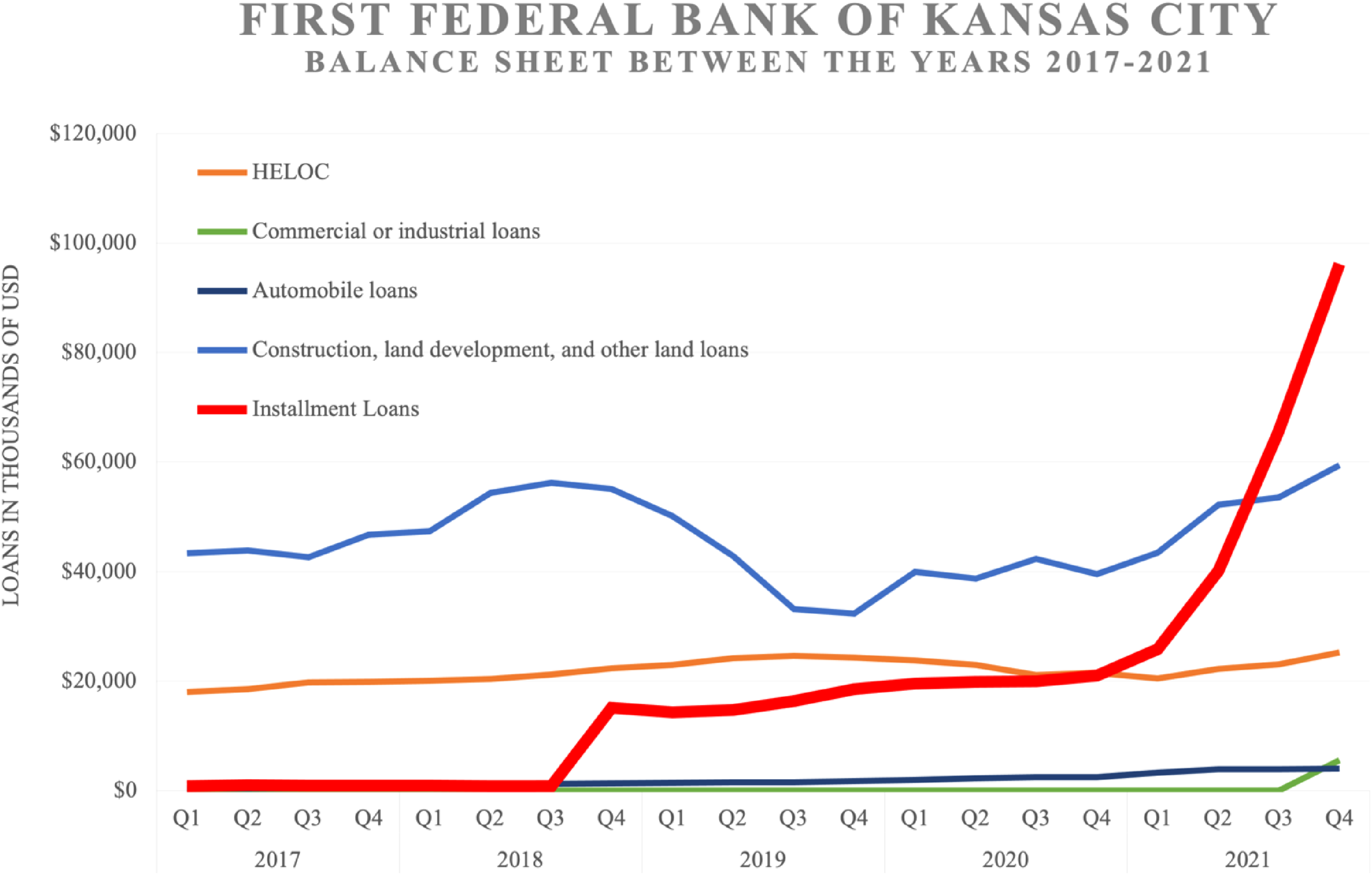

First federal bank of Kansas city

The first bank identified in this audit is First Federal Bank of Kansas City, which is a community bank headquartered in Kansas City, MO with a total lending balance sheet of $616 million in the fourth quarter of 2021. First Federal fits the profile of a community bank, with a majority of its capital tied to mortgage lending ($425.4 million) and residential construction loans ($59.4 million). Historically, community banks have been central to U.S. mortgage markets (Freund, 2010) but have faced a series of pressures following 2008 financial reform. This shift has seen declining rates of community bank openings and a reduced share of originations in the mortgage market (Lux and Greene, 2022) with non-bank lenders such as RocketLoans, QuickenLoans, or LoanDepot leveraging online offerings to become the U.S.’ largest mortgage lenders.

Declining shares in the mortgage market have pushed community banks to seek out alternative sources of revenue. We can see this political economic story play out on the balance sheet of First Federal as the bank structures a majority of its operations around residential real estate, but is increasingly prioritizing alternative investments. Figure 1 shows that over 65.7 million, or 15.6 of its total balace sheet is tied up in installment lending as of 2021. This is especially notable given that installment lending comprised only 0.14% of the bank's balance sheet before Q3 2018 before two large spikes in 2018 and 2021. Given the constrained regional market at First Federal, this dramatic shift in lending priorities is likely the result of accessing online markets through partnership with Upstart.

The presence of First Federal Bank of KC in this audit and the associated spikes in installment lending in 2018 and 2021 shows how fintech-bank partnerships can change capital allocation at banks. The reason for this partnership is likely the specialization in data and analytics at fintech firms. For a bank such as First Federal, underwriting unsecured consumer loans would be costly and time intensive. By paying to access calculative infrastructure, community banks such as First Federal are able to originate new pathways for local capital to invest in UCD. Notably, this case illustrates how political economic shifts in the mortgage market position community banks like First Federal as potential partners for fintech firms developing calculative infrastructure designed to assist smaller banks in accessing markets for personal loans.

Cross river bank

The second bank identified in the audit is Cross River Bank, which is headquartered in Fort Lee, NJ, and had a balance sheet of $8.06 billion in the fourth quarter of 2021. Unlike First Federal, Cross River is a state-chartered bank designed to capitalize the fintech sector (Tan, 2022). U.S. state charters are banking licenses issued by state regulators and have been one way that fintech firms—particularly those seeking to integrate cryptocurrencies and blockchain—have attempted to gain expedited access to the financial system (Botella, 2021). The success of Cross River Bank in capitalizing the fintech sector, both in terms of partnering with firms like Upstart to issue personal loans, as well as in providing direct investments to fintech startups, suggests a need for close monitoring of state charters and their capacity to facilitate fintech-bank partnerships.

Of Cross River's $8.06 billion lending balance sheet, $1.67 billion (20.7%) was allocated to installment loans in 4Q 2021. While comprising the largest percentage of the banks audited in this study, 20.7% is a notable departure from pre-pandemic allocations as installment lending constituted 55.5% of Cross River's balance sheet in the 1Q 2020. Driving the shift in commercial and industrial lending seen in Figure 2 was Cross River's partnership with a fintech firm called Ocrulus, which Cross River leveraged to become one of the largest payroll protection program (PPP) lenders in the country (Cross River Bank, n.d.) and provides additional evidence that fintech-bank partnerships are enabling banks to quickly disburse capital through digital channels and access new sources of revenue.

Analysis of First Federal Bank of Kansas City's balance sheet between 2017 and 2021. Source: Author's analysis of Federal Deposits and Insurance Corporation Call Report Data.

Analysis of Cross River Bank's balance sheet between 2017 and 2021. Source: Author's analysis of Federal Deposits and Insurance Corporation Call Report Data.

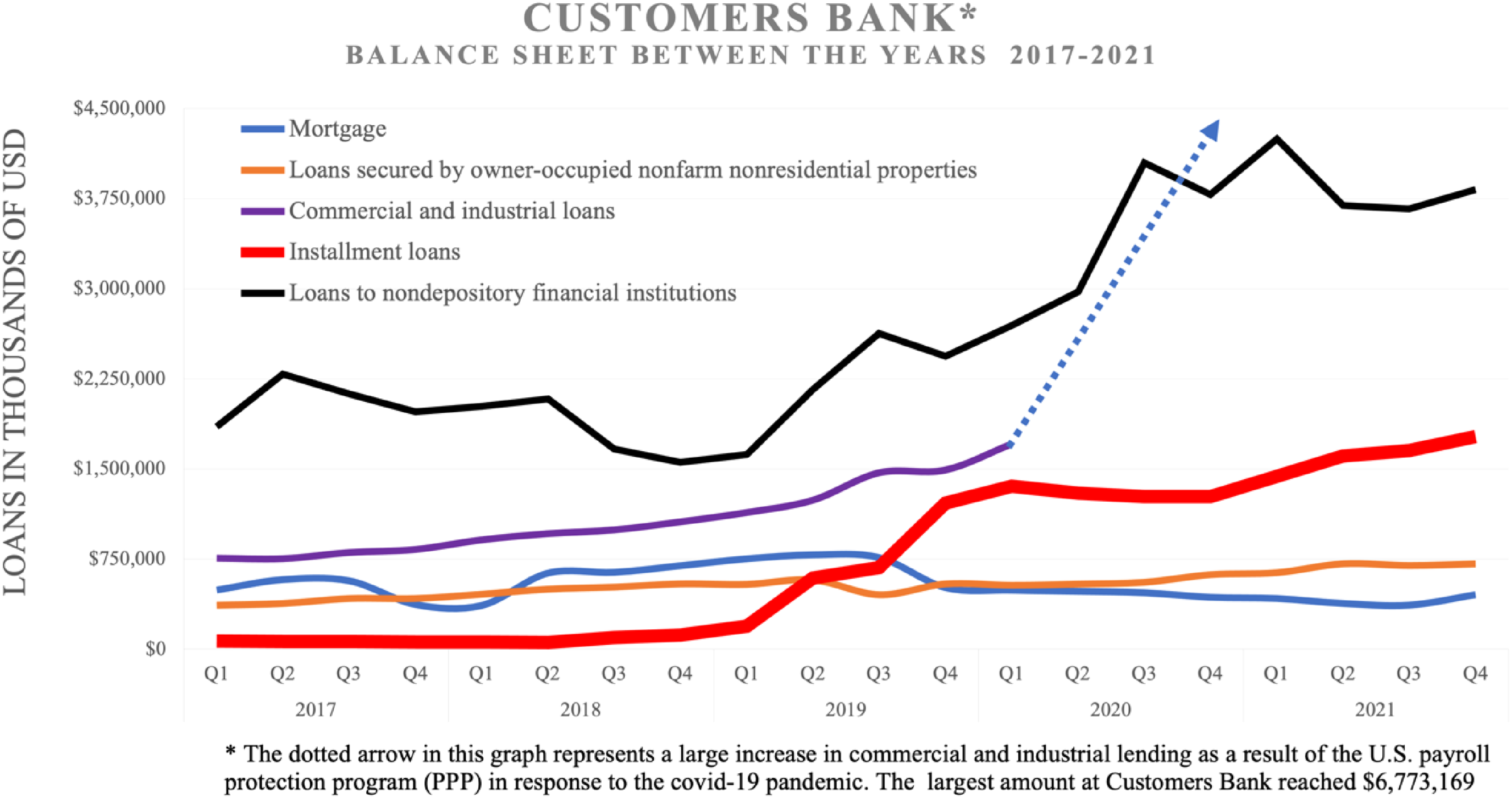

Analysis of customer bank's balance sheet between 2017 and 2021. Source: Author's analysis of Federal Deposits and Insurance Corporation Call Report Data.

Cross River Bank's appearance in this audit provides insight into state banking charters and the ways these introduce new investments in the financial system, an area identified by U.S. regulators as a topic of concern (Williams, 2022). Given the conclusion of U.S. pandemic assistance programs such as PPP, Cross River's balance sheet is likely to return to pre-2020 allocations. The sustained investment in installment lending from banks such as Cross River has been central to the development of the fintech-consumer lending sector, as firms like Upstart rely on sustained investment from Cross River to raise capital.

Customers bank

Customers Bank is the final institution identified in this audit. Customers Bank is headquartered in Phoenixville, PA with a regional footprint in the U.S. mid-Atlantic and midwest. The bank had a total balance sheet of $16.9 billion in the fourth quarter of 2021 and invests heavily in installment lending as well as loans to non-depository financial institutions. Likely because of its size and status as a relatively large, commercial lender, Customers Bank has taken a different approach to investing in installment loans.

That approach involved the purchase of a subsidiary fintech firm – BankMobile – to increase digital deposits and facilitate partnerships with firms like Upstart (Blumenthal, 2016). BankMobile, as a subsidiary of Customers’ Bank, has been successful in routing business onto Customer Bank's balance sheet. Of their $14.57 billion balance sheet, Figure 3 shows that $1.77 billion (or 12.1%) is attributed to installment lending, which is notable given the size of the bank and consistent growth between 2018 and 2021. It is also worth noting their allocation of $3.82 billion (26.2%) towards “loans to non-depository financial institutions” (26.2%, which are often loans to non-bank mortgage lenders (Campbell, 2022).

Customers Bank illustrates how the acquisition strategy of regional banks may inform the development of fintech-bank partnerships. As banks continue to navigate a post-2008 regulatory environment in which non-bank lenders have become major players, banks may look to acquire technology firms in order to facilitate new sources of revenue through partnerships with intermediaries like Upstart. While this is a singular case, the model illustrated by Customers Bank shows how a regional bank can leverage the acquisition of a technology firm to expand digital operations and facilitate partnerships with firms like Upstart to generate new revenue lines.

The role of fintech-bank partnerships in opening new spaces of investment

Partnerships between banks and fintech firms may be altering conceptions of risk and investment at U.S. banks (Campbell, 2022). This audit provides a snapshot of three banks partnering with one fintech firm, Upstart, in assessing risk and issuing consumer loans. These cases are not meant to be representative of the banking sector as a whole, but rather examines each banks balance sheet in order to understand the institutional context behind fintech-bank partnerships.

The banks identified in the audit ranged from a small community bank with branches in one U.S. city, to a commercial lender operating across several states in the U.S. midwest. Each bank leveraged the calculative infrastructure from Upstart's model to prioritize investment in ways that correspond with the unique cases of each bank, from declining shares in the mortgage market as was the case with First Federal, to funding personal loans as part of a broader effort to prop up the fintech sector in Cross River. These differences suggest that fintech-bank partnerships are responsive to local and institutional context and encourages further research that investigates how novel partnership arrangements are forming out of unique banking environments and regulatory pressures in the banking sector.

Ultimately, this audit provides a partial answer to the question: how do alternative credit scoring models change bank lending priorities? Across the three banks identified in the audit, access to calculative infrastructure – in this case, alternative credit scores – enabled new or sustained investment in consumer loans. The impact on bank balance sheets was particularly evident in the case of First Federal where the percentage of installment loans jumped from 0.14% to 15.6% over three years. This ability of calculative infrastructure to price risk on consumer debt is one way that fintech-bank partnerships may be opening new spaces of investment; however, further research is needed on the broader scope of fintech-bank partnerships and their impact on capital allocation, such as bank funding of NDFIs (Campbell, 2022).

Conclusion

This paper examines how alternative credit scoring systems construct risk and create financial partnerships. I have taken up this task in three parts. First, I developed a theoretical framework for understanding alternative credit scores and the infrastructural partnerships they facilitate. Second, I conducted an algorithmic audit of Upstart's model and documented the impacts loan outcomes. Third, I audited the financial infrastructure underlying Upstart's model and identify three fintech-bank partnerships, documenting the impacts on each banks' balance sheet. Ultimately, I argue that the vision of risk projected by alternative credit scoring models represents one form of calculative infrastructure as banks partner with fintech firms in seeking out new sources of revenue.

One key finding of this paper is that alternative credit scores impact loan outcomes. Specifically, I find that alternative data showing applicants with a bachelor's degree received rates that were 4% less expensive than those showing a certificate's degree. I suggest that the significance of education to Upstart's model raises important equity concerns associated with overhauling lending criteria with opaque machine learning models that defy straightforward explanation. In particular, the integration of education is notable given its potential to proxy for protected characteristics such as race or gender. I argue that this pushes us to understand education, and its interpolation in credit risk measures, not only in terms of its calculative significance to earning potential, household indebtedness, or social networks, but rather as a system of classification that may “produce race by other means” (Phan and Wark, 2021: 4) when central to visions of credit risk.

A second finding of the audit is that banks identified to be hosting loans on Upstart's platform held outsized amounts of personal loan debt on their balance sheets. Each of these banks saw sudden rises in capital allocation, one case rising from 0.14% to 15.6% over three years, likely as a result of partnering with Upstart. I argue that the shifts in lending patterns documented by this audit reflects the local and institutional context of each bank. These ranged from a small community bank with branches in one U.S. city, to a large commercial lender operating across several states, each leveraging the calculative infrastructure of Upstart's model to open new sources of revenue. The different pressures and conditions these banks were responding to suggest that the regulatory urgency (Federal Reserve et al., 2021) to understand fintech-bank partnerships should engage with local and institutional conditions across a variety of bank types, particularly the smaller regional and community banks identified by the head of the OCC as facing pressures to compete from technological advancements and consolidation amongst large banks (Williams, 2022).

The findings of this paper provide a better understanding of risk-based pricing in alternative credit scoring models, namely those using alternative data and processing techniques derived from AI and ML. The broader impact of institutional adoption of these technologies on patterns of lending and risk assessment remain unclear (Federal Reserve et al., 2021); however, what is clear is that alternative credit scores opened new pathways of investment for banks identified in this audit. By allowing institutions to access what was previously a niche market with trouble appropriately pricing risk, alternative credit scores established a degree of calculative agency (Çalışkan and Callon, 2010; Fields, 2018) over consumer debt. In short, the stabilization of risk assessment enabled by Upstart's model was able to alter pathways of investment at these banks.

These findings signal three areas for additional research. First, research is needed to identify characteristics of those targeted by alternative risk-assessment models and their impact on consumer well-being. Second, algorithmic audits are relatively untested as a ethod for assessing financial algorithms, and as a result, should be further evaluated given their adoption by non-academic researchers and consumer advocates such as the Student Borrower Protection Center in the U.S., (SPBC, 2020) or the OpenSCHUFA campaign in Germany (Palmetshofer, 2018). Other applications might take up rent optimization algorithms and their role in pricing housing markets (Vogell, 2022), or the role of investment advising technologies in determining real estate acquisitions (Son, 2022). A final area for additional research pertains to fintech-bank partnerships and the arrangements engendered by novel conceptions of risk (i.e., which institutions, how profitable are these ventures, what issues are these banks responding to, etc.). Taken together, these suggest a need to better understand financial technology, the particularities of how these technologies are integrated into financial systems, and the ways new technology circumvents consumer protections.

Footnotes

Acknowledgements

Many thanks to Matthew Zook for his advice and input on this paper, to Jacob Saindon and Alex Sutphin for their help in thinking through the data, as well as everyone in the publications workshop at the University of Kentucky. I also want to thank the three anonymous reviewers as well as the twelve participants who made this study possible.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article