Abstract

Much of the literature on environmental sustainability in global value chains (GVCs) focuses on how ‘lead firms’ (usually global buyers or retailers) can improve the environmental conditions of production among their various layers of suppliers. This approach focuses on the vertical governance dynamics of environmental upgrading along with GVCs. In our contribution, we emphasize the role of horizontal governance as a driver that underpins environmental upgrading processes. These horizontal elements include institutional support, pressure from civil society groups and political dynamics at the local level – which have been relatively overlooked in this literature so far. We examine environmental upgrading in Italian wine value chains, focusing on the fast-growing but environmentally-contested Prosecco and Valpolicella districts. Our analysis suggests that firms within the same industry may follow different processes of environmental upgrading – through certification, going ‘back to tradition’, technological innovation and/or as an articulation of local politics – also depending on their size. We conclude that horizontal governance is playing a more important role than previously thought in shaping environmental upgrading and provide some suggestions for future research in this realm.

Introduction

Green growth, corporate social responsibility and environmental stewardship have become part of the everyday lexicon of business. Mounting pressures are spurring firms to reduce their environmental impacts, sustainability is increasingly at the core of policymakers’ concerns (especially at the EU level), consumers are becoming more selective, and even financial investors are starting to center their strategies on the social and environmental performance of companies. Many firms have at least rhetorically embraced the sustainable development goal agenda and regularly publish environmental reports to document their commitments and those of their suppliers. Demands for better environmental practices are cascading along with value chains.

In order to improve the environmental impacts of global value chain (GVC) operations, suppliers are under pressure to modify production practices and undertake environmental upgrading. But what are the forces that shape these processes? Much of the literature on environmental upgrading in GVCs has been concerned with addressing the role of ‘lead firms’ (often global buyers or retailers) in pushing various layers of suppliers to improve their environmental practices (De Marchi et al., 2019; Goger, 2013; Lund-Thomsen and Lindgreen, 2014; Poulsen et al., 2018). Accordingly, much attention has been devoted to understanding how lead firms have been able, more or less effectively, to vertically implement their sustainability strategies among their first- and second-tier suppliers (Amengual and Distelhorst, 2019; Jia et al., 2019; Wohlgezogen et al., 2021). Although the key role of local actors and politics has already been highlighted in relation to how they may shape economic and social upgrading trajectories in GVCs (see, e.g., Lund-Thomsen and Nadvi, 2010; Marslev et al., 2022; Pipkin, 2011; Selwyn, 2007), this has not been documented for environmental upgrading yet (for a partial exception, see Krauss and Krishnan, 2022).

In adapting the framework of governance that Gereffi and Lee (2016) developed in relation to social upgrading, we suggest that vertical, top-down governance is just one among several governance dynamics that can support the adoption of better environmental standards and practices along GVCs. Specifically, we highlight the role of horizontal governance – involving pressure from civil society groups, institutional support and political dynamics at the local level – in shaping environmental upgrading. We show that, even within the same value chain and in the same localized territory, very different processes of environmental upgrading co-exists – and that this plurality matters for reflecting on policy and strategic options (Salas-Zapata and Ortiz-Muñoz, 2019; Xiao et al., 2019; Zimmermann et al., 2021).

To do so, we examine environmental upgrading in Italian wine value chains, usually considered as ‘buyer-driven’ (Ponte, 2019). We focus on two Italian districts 1 (Prosecco and Valpolicella) that both operate in Veneto region (although Prosecco is also produced in Friuli-Venezia Giulia), thus controlling at least partially for regional political factors. Both are very successful districts in terms of growth in production and exports, and both have experienced recent critical attention in relation to what this growth means for the health of local communities and their environment.

In this article, we approach environmental upgrading as a set of processes, rather than as an outcome (on the distinction between the two, see Krishnan et al., 2022) and assess the relative importance of vertical and horizontal governance dynamics in shaping it. We do so by inductively identifying four main trajectories of environmental upgrading – through certification, by going ‘back to tradition’, through technological innovation and/or as an articulation of local politics. 2 Our findings are based on qualitative analysis of three sets of materials (in view of triangulating evidence): (1) primary data collected from October 2020 to March 2023 through semi-structured interviews, based on a common guide, with a total of 68 industry operators – including private, corporate and cooperative wine producers and marketers, regulatory institutions, consortia for the protection of geographic origin, sustainability certification agencies, suppliers of inputs, research institutions and labour unions (see Appendix Table 1) 3 ; (2) participant observation, visual inspection of exposition stands, informal conversations and attendance of seminars at the main Italian wine fair and expo (see Appendix Table 2) 4 ; and (3) secondary sources, including websites and corporate documents, reports developed by local or national industry associations, and detailed materials posted on the websites of the main wine sustainability initiatives and certifications active in Italy.

Environmental upgrading in GVCs

In analyses of GVCs, the general term upgrading has been used to highlight paths for actors to ‘move up the value chain’ for economic gain, with much of the focus in the early literature on ‘vertical’ relations among actors and on how knowledge and information flows within value chains between lead firms and their suppliers (Gereffi, 1999). Efforts seeking to assess which paths and aspects of upgrading originate from combinations of socio-spatial dynamics and ‘learning from global buyers’ have also been undertaken (Alcacer and Oxley, 2014; Giuliani et al., 2005; Pietrobelli and Rabellotti, 2011), together with studies that illustrate the active role of suppliers in some of these dynamics (Giuliani et al., 2018; Sako and Zylberberg, 2017).

GVC scholars initially highlighted the importance of a ‘high road’ trajectory to upgrading (from process to product to functional upgrading) eventually leading to performing functions in a value chain that have more skill and knowledge content (Gereffi, 1999). Others argued that a specific trajectory should not be an end in itself, and that attention should also be paid to what conditions can improve the position of disadvantaged actors along with GVCs (e.g., smallholder producers, developing country processors and women entrepreneurs) (Glückler and Panitz, 2016; Neilson et al., 2018b; Ponte and Ewert, 2009; Tokatli, 2013). These approaches also included the examination of ‘value capture trajectories’ (how actors can capture higher shares of value added; Neilson et al., 2018a; Yeung and Coe, 2015) and the complex overlaps of upgrading and downgrading that are emerging (Bernhardt and Pollak, 2016; Blažek, 2016).

Recently, the research agenda on upgrading in GVCs has also been moving away from the exclusive examination of economic features and towards the consideration of social (Barrientos et al., 2011; Rossi, 2015) and environmental aspects (De Marchi et al., 2013; Havice and Campling, 2017). In this context, environmental upgrading has often been conceived as a process (e.g., changes undertaken to improve or minimize the environmental impact of GVC operations, including production, processing, distribution, consumption and disposal or recycling; De Marchi et al., 2019), rather than outcome (e.g., the biophysical manifestations, impacts on market access, and reputation; Krishnan et al., 2022).

A key question for the GVC literature (starting from Gereffi, 1994 onwards) has been to understand the conditions under which upgrading can accrue, focusing in particular on the features of its governance structure. Initially, studies focused on unipolar value chains – where lead firms in one functional position of the chain (usually global buyers) play a dominant role in shaping what other actors along with the chain do and under what conditions. Others have explored the dynamics of governance in GVCs characterized as bipolar, where two sets of actors in different functional positions both drive the chain, albeit in different ways (Fold, 2002). Finally, others showed that multipolarity can involve other actors outside the value chain, such as international NGOs, trade unions, governments and multi-stakeholder initiatives (Nadvi and Raj-Reichert, 2015). Ponte and Sturgeon (2014) further suggested examining governance across a unipolar to multipolar continuum, and called for analyses identifying the main drivers of these GVCs, and the different degrees and mechanisms of driving.

In their seminal contribution to social upgrading, Gereffi and Lee (2016) proposed the analysis of two types of governance: vertical (which we further disaggregate into top-down and bottom-up) and horizontal. Vertical governance has been by far the most studied. In our approach, vertical top-down governance includes the strategies implemented by global lead firms to ensure their suppliers are enacting the standards they require (see e.g., Alexander, 2020). Such standards are often developed or enforced in the context of multi-stakeholder initiatives, thanks to collaboration with NGOs, trade unions and industry associations (de Bakker et al., 2019). The nascent literature on environmental upgrading suggests that it is more likely to happen in GVCs characterized by unipolar governance and where lead firms are consumer-facing companies with higher reputational risks (Ponte, 2019; Poulsen et al., 2016). It also suggests that changes in supplier practices are not necessarily reflected in better environmental outcomes – a process-outcome divide (Goger, 2013; Khan et al., 2019; Khattak et al., 2015).

We also highlight a different form of vertical governance, which has bottom-up features and is undertaken by suppliers. It is driven mainly by internal, strategic factors, rather than by global buyers’ specific requests – as suppliers seek efficiency, differentiation or legitimation (see, e.g., Poulsen et al., 2016, 2018). Some of the literature shows how lower-tier and/or less powerful actors may actually be the engines of environmental upgrading, and in some cases even in opposition to the requests placed by lead firms (Alford and Phillips, 2018; Selwyn, 2007). Often, such bottom-up initiatives take place within industrial districts, where firms specialized in the same industries and sharing the same environmental issues are concentrated, and where local collective action is undertaken (De Marchi and Di Maria, 2019).

In Gereffi and Lee's typology (2016), horizontal governance is defined in opposition to vertical top-down governance operating along the chain and is used to refer to locality-based coordination mechanisms driven by private actors (e.g., industry associations), civil society groups (e.g., labour unions or NGOs) or local or regional governmental bodies (Bair and Palpacuer 2015). Case studies in the developing world (see, e.g., Lund-Thomsen and Nadvi, 2010) suggest that local collective institutions can play an important role in spurring local firms to improve labour conditions, especially in highly visible GVCs where suppliers also face important pressures from buyers. However, not much is known about the role of horizontal governance, especially at the local level, in shaping environmental upgrading processes (Alexander, 2020; Havice and Campling, 2017), a research gap we start addressing in our contribution.

Background: Prosecco and Valpolicella

Prosecco

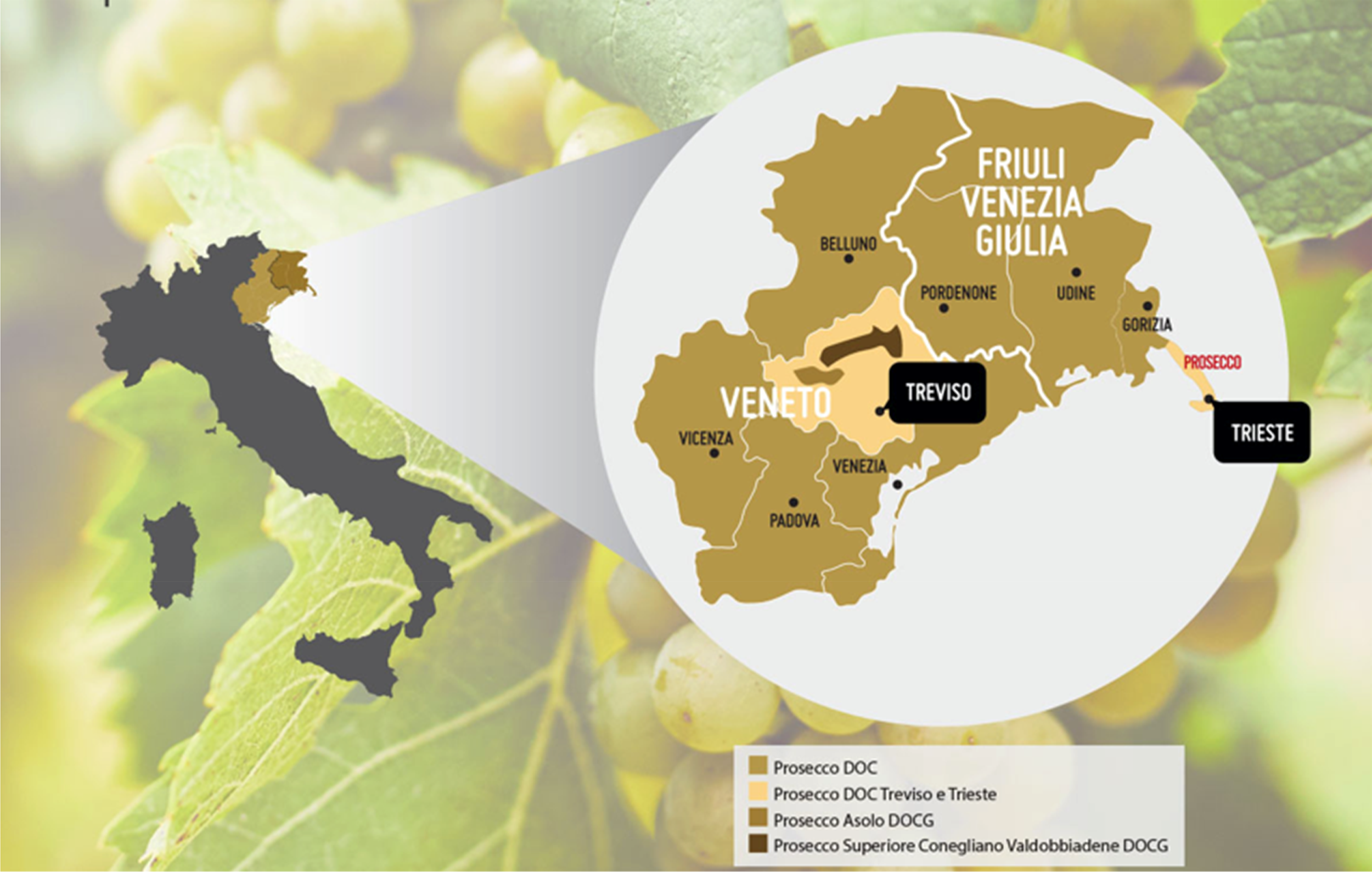

Prosecco sparkling wine is produced in north-east Italy from grapes of the glera vine. The classic area of production is located on steep hills around Valdobbiadene and on gentler slopes and flatland close to Conegliano (see Map 1). The first consortium charged with protecting the Prosecco geographic denomination was established in 1962 (Prosecco DOC, Denominazione d’Origine Controllata). But as the 2008 EU wine reform (Itçaina et al., 2016; Pomarici and Sardone, 2020) deepened the regulation of indications of geographic origin, the DOC area was under threat of losing its exclusive claim because the denomination Prosecco was related to a grape variety, not a territorial place. This meant that Prosecco, under new EU legislation, potentially could be produced anywhere where such grape had been planted. In reaction to this threat, the consortium managed to construct a historical heritage story to apply for a reform of the geographic indication system for Prosecco. The reform process expanded the overall Prosecco DOC from a relatively small area within the province of Treviso to other four provinces in Veneto and the whole of Friuli-Venezia Giulia region (see Map 1). In parallel to this, the original Conegliano and Valdobbiadene area was upgraded to DOCG (Denominazione d’Origine Controllata e Garantita), which denotes higher quality – along with the establishment of the new DOCG of Asolo Prosecco and the sub-denominations Prosecco DOC Treviso and Trieste (see details in Ponte, 2021).

Prosecco area of production.

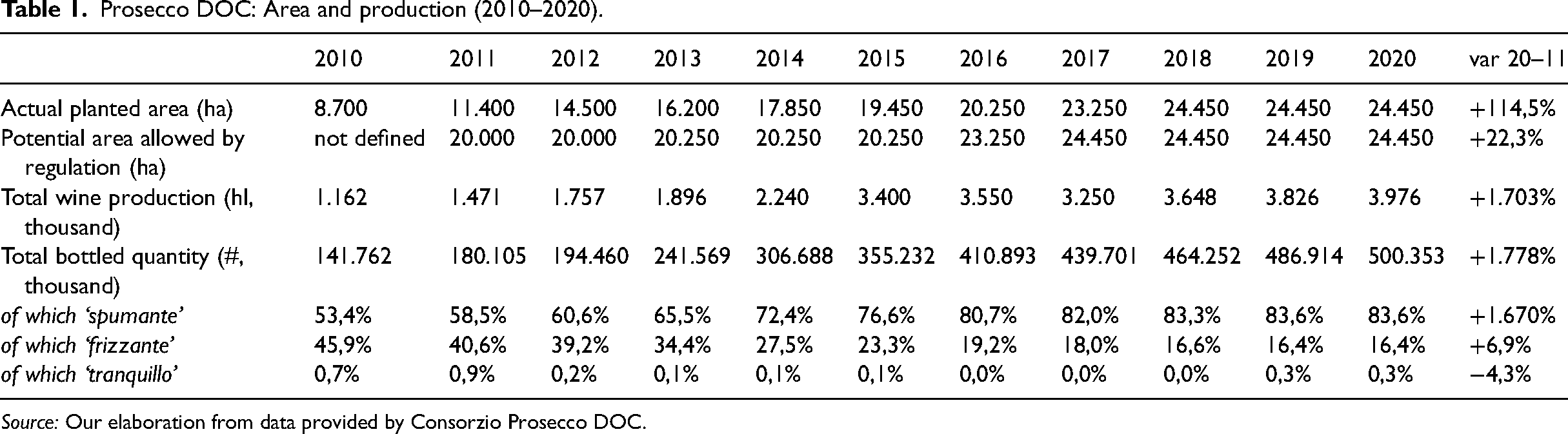

Following these reforms, and in conjunction with a quick uptake in demand, the total planted area of the Prosecco DOC has grown from 8,700 hectares in 2010 to almost three times as much, 24,450 hectares in 2019. Production volumes followed suit, from 141 million bottles in 2010 to 464 million in 2019 (see Table 1). Similar trends took place in the DOCG area. Although the rest of the Italian wine industry has also innovated and adapted in the past two-three decades (Cusmano et al., 2010), the performance of Prosecco has been particularly impressive. Prosecco accounts for about one-third of global exports of sparkling wine in terms of volume, while its main competitors (Cava and Champagne) together account for one-third. 5 It should be noted that Champagne attracts much higher unit prices than Cava or Prosecco. Data on the total value of sparkling wine exports (a proxy for these three origins) indicate that France accounted for €3 bn in 2018 (52% of global exports by value, down from 70% in 2003), with Italy (€1.5 bn, or 25%) and Spain (€0.5 bn, or 7%) following suit. 6

Prosecco DOC: Area and production (2010–2020).

Source: Our elaboration from data provided by Consorzio Prosecco DOC.

Valpolicella

Valpolicella wine production is also organized around a consortium of producers (Consorzio per la Tutela dei Vini Valpolicella, CTV) located within a set of municipalities within the province of Verona in Veneto region (see Map 2). Differently from Prosecco, the more specific denominations of Valpolicella, within the broad geographic denomination, are based on different types of wine, rather than referring to separate geographic areas: Valpolicella DOC; Valpolicella Ripasso DOC; Amarone della Valpolicella DOCG; and Recioto della Valpolicella DOCG. The original Valpolicella consortium was founded in 1925, while the DOC area was established in 1968. From 2010, like all DOC/DOCG consortia in Italy, it has been allowed to play the functions of wine promotion and valorization. In the same year, it set up the DOCG denomination for its top-quality wines (the iconic Amarone and its sweet version Recioto). Like Prosecco, Amarone became known beyond the local and regional markets relatively recently. It was bottled with that name for the first time in 1952, and until 1990 it was only mentioned as a dry variant of Recioto (V1).

Valpolicella areas of production.

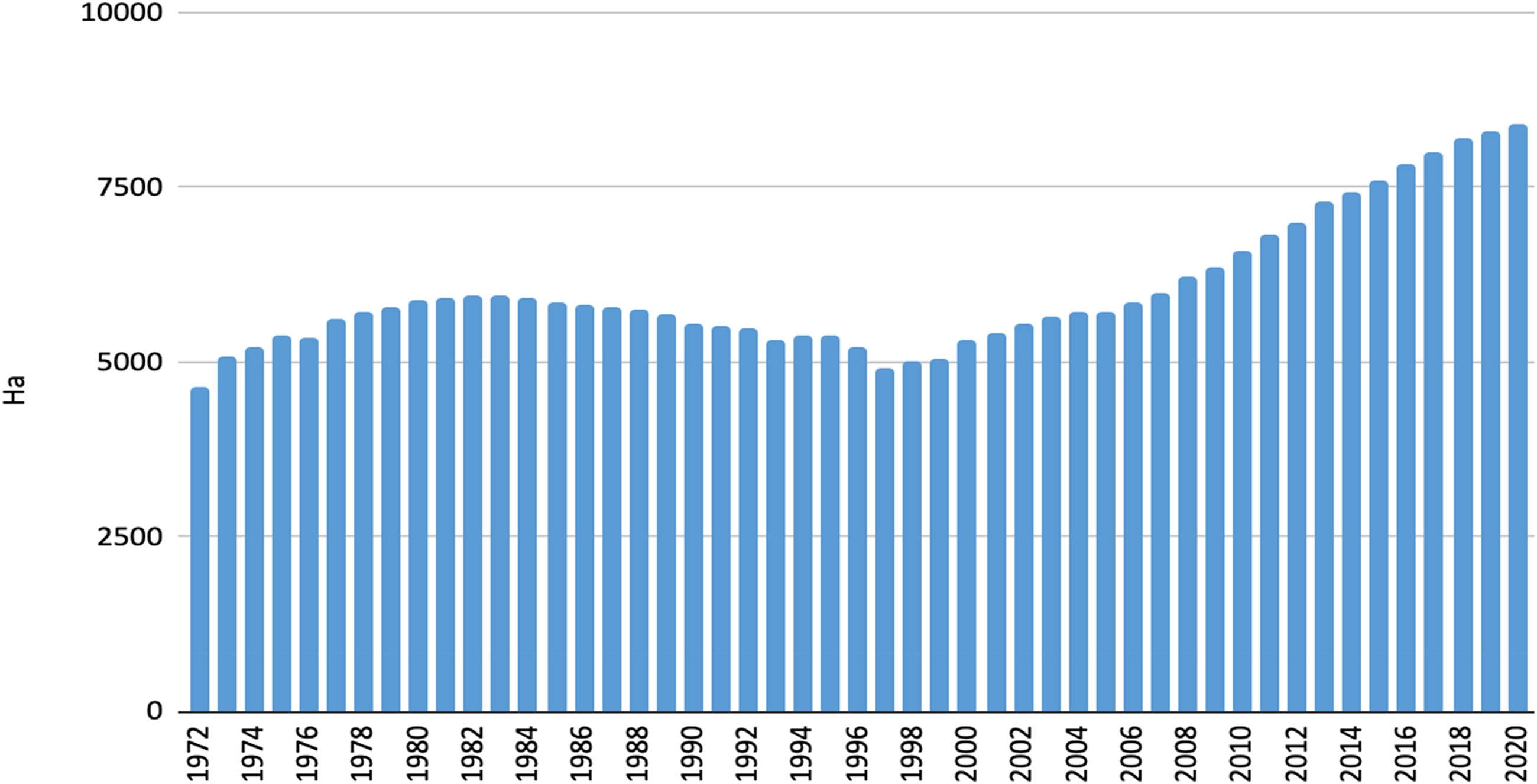

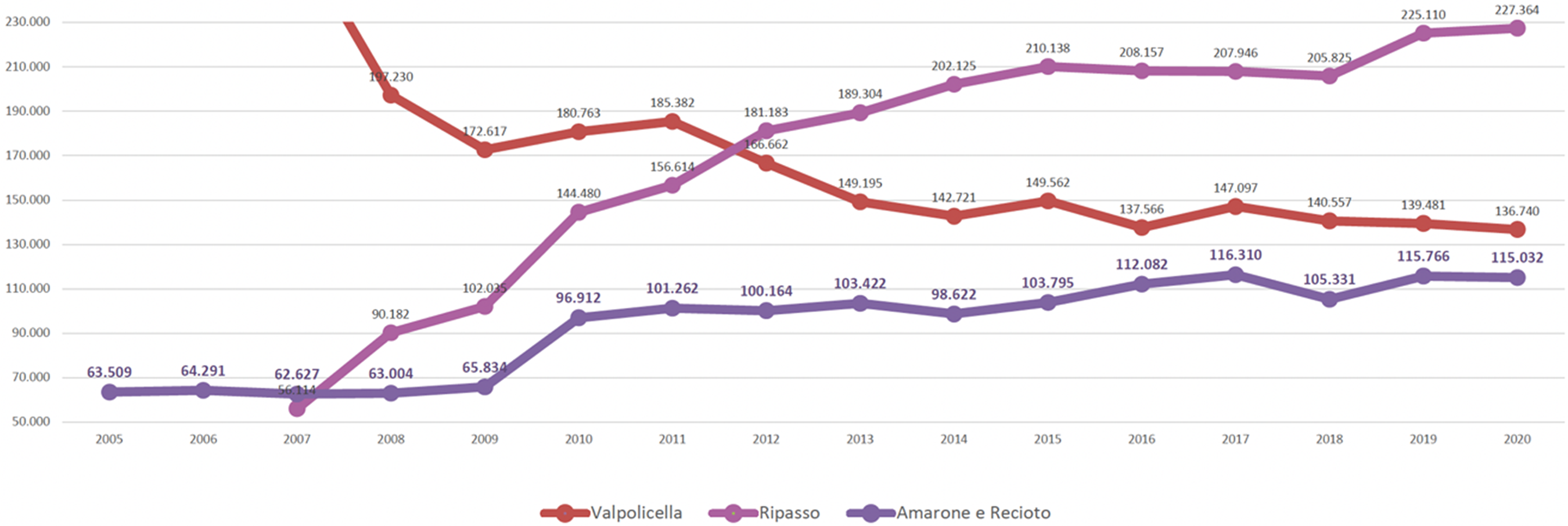

Like in the case of Prosecco, the area under production in Valpolicella has seen major growth since the turn of the century – from 5,229 ha in 2000 to 8,398 ha in 2020 – and reversing a declining trend observed in the 1980s and 1990s (see Figure 1). Production has also followed a similar trend, but with lower proportional growth in the 2010s and 2020s, indicating lower yields and higher quality. This is reflected in the trends of wine production by type (see Figure 2). Total Valpolicella sales amounted to about €600 million in 2020, 70% of which are to 87 export markets. 7

Viticultured area (ha; top) of Valpolicella grapes (1972–2020).

Production by type of Valpolicella wine (2005–2020; 0.75 litre bottle- equivalent).

Environmental upgrading processes in Prosecco and Valpolicella

As the area planted with Prosecco or Valpolicella wines has increased, so have the pressures of winemaking activities on local social and ecological systems (Ponte, 2021). Yet, our analysis in this section shows that local producers follow very different processes of environmental upgrading 8 : (1) through sustainability certification; (2) by going ‘back to tradition’; (3) through technological innovation; and (4) as an articulation of local politics. In the second step of our analysis, we will also identify the forms of governance (top-down vertical, bottom-up vertical and horizontal) that shape these four sets of processes of environmental upgrading.

Environmental upgrading as achieving sustainability certification

All the broad sustainability certifications that are emerging in the Italian wine value chain are the result of national initiatives, and in one case local. SQNPI (Sistema Qualità Nazionale Produzione Integrata) certification was developed by the Italian Ministry of Agricultural, Food and Forest Policy starting in 2016. It organizes various regulations that are scattered around different regions and harmonizes them in view of providing a set of guidelines for integrated production in agriculture (including for wine grapes). The SQNPI standard includes a set of ‘good agricultural practices’ and integrated management and is certified by accredited third-party auditors (Interviews P3, IG1). SQNPI certifies the grape must and the bottled wine, which can carry the bee logo (see Figure 3, left). In parallel to SQNPI, the Italian Ministry of Ecological Transition has developed a sustainability certification specifically targeted at wine production – called VIVA Sustainability and Culture. It includes technical specifications for calculating sustainability performance in vineyards and wine production in relation to four aspects: air, water, territory and vineyard (IG16). However, this certification has not fully taken off – as of early 2023, only 154 firms (including 14 cooperatives) had been certified, of which 23 in Veneto region.

Logos of the main sustainability certifications used in the Italian wine value chain.

A third sustainability certification system that is taking hold in the wine industry is Equalitas, which seeks to cover all three main dimensions of economic, social and environmental sustainability. The Equalitas standard includes integrated production management, good communication with stakeholders and communities, good practices within firms and with their suppliers and measures against labour exploitation on farms. Equalitas offers three possible foci of certification: the farm, the wine and the whole geographic denomination (once 60% of all area under production is certified) (IG3, IG11). A fourth is the World Biodiversity Association's (BWA) ‘Biodiversity friend’ certification. Despite ‘world’ featuring in its name, this is a local initiative developed by a group of ecologists in Verona that helps assess the impact of production processes on the biodiversity of production areas (in wine but also other agri-food products) (IG10).

The Prosecco DOCG consortium aims to facilitate the SQNPI certification of 50% of farmers by the end of 2022 and 100% by 2029.

9

Equalitas certification is the focus of sustainability efforts by the consortium of the larger Prosecco DOC area, but in Valpolicella only three firms have obtained it so far. In Valpolicella, the consortium instead developed its own certification system for the sustainable production of wine grapes (RRR – Reduce, Retrench, Respect), which is based mainly on integrated crop management practices. RRR was developed by the Valpolicella consortium in response to the perceived limitations of SQNPI: ‘We developed RRR because we perceived the national level protocol as insufficient for us – these standards were too rigid and did not reflect local realities. For example, they did not include the safeguarding of local populations and the impacts agro-chemical application on those who live in the area … The idea was to eventually expand it to other DOC areas and merge it with SQNPI, but this did not happen. SQNPI has high technical value, but it has not been sold well to the wine industry. But RRR is now used only in Valpolicella. It is difficult to have it recognized by the monopoly buyers in Scandinavia’ (V9).

One of the main incentives for RRR certification is provided in the regulations for the production of Amarone. Only a certain percentage of total grape production is allowed to be vinified for the highly priced Amarone, the rest goes for the production of other, cheaper, Valpolicella wines. But if grape producers meet the RRR standard, they are allowed an extra 5% of grapes to be used for Amarone production (V8). As of 2021, 1,210 ha had been RRR certified in Valpolicella (or 15% of the total area), but at the 2022 Vinitaly expo a representative of the consortium announced that they were moving away from RRR certification protocols and instead focus on SQNPI certification (which is now awarded automatically to holders of RRR) (VWF22_3).

These sustainability certification systems are fairly recent and cover a broad set of aspects and indicators. These were predated by two other certification systems – for biodynamic wine production and for the organic production of grapes for wine. Biodynamic wines remain a very small proportion of production in both Prosecco and Valpolicella and producers have a somewhat cult status. Although there is a certification system for biodynamic wines, many producers do not seek it and instead communicate their overall philosophy of production directly to their buyers and consumers. Organic production of grapes for wine has been only tepidly pushed by the consortia in both Prosecco and Valpolicella and has had a relatively limited uptake – only 3.3% of the planted area in Prosecco DOCG and 10% in Valpolicella, even including areas under conversion.

10

This is much lower than the national average of 18% (VWF22_22). Several producers in the hilly areas of Prosecco argue that it is very difficult to make organic Prosecco, and nearly impossible to make it biodynamic due to high rainfall (P1). In Valpolicella, several of the large wine producers we interviewed argued that they need to have organic wine to be able to win tenders with the Scandinavian monopoly buyers. This has been a major driver of current organic conversion efforts (V10), which however are still relatively limited. One producer claimed that: ‘It is technically feasible to make organic wine in Valpolicella, although it needs more manual labour and more hours of machine operation, because one needs to go more often to the vineyard. In the first years of conversion, we observed a lowering of yields (−15%) which affected the balance sheet of the farms – also because farmers had to buy more machinery for mechanical weeding, etcetera. This is also why organic wine should cost more … Yet, it is difficult to sell organic wine as supermarket chains demand the same price as for non-organic wine, and the pressure to cut corners is definitively there to meet these demands’ (V4).

Other producers confirmed that ‘the consumer understands the value of organic, but the supermarket buyer wants it at the same price. It is absurd! … We even sell some of our organic wine without the label. It is better than selling it at the same price as conventional wine’ (V12). Another stated that ‘sometimes it does not make sense from a financial point of view, but we do it anyway to make buyers happy’ (V8).

In sum, the main sustainability certification systems that are emerging in the wine value chains of Prosecco and Valpolicella are mainly the result of national and local initiatives by various ministries and industry consortia. Organic and biodynamic certifications, which have been developed internationally, are still relatively small. As we will show later, these have not been strongly requested by wine buyers in Italy or abroad, with the important exception of monopoly buyers in Scandinavia and Canada. This observation is confirmed by the low proportion of stands that signalled sustainability messaging to wine buyers at the 2022 Vinitaly wine fair (18% of all Prosecco and Valpolicella stands in the Veneto pavilions; these do not include those located in the dedicated organic pavilion). When there is any signalling, however, reference to one or another certification is the preferred method (in 80% of instances), with organic certification accounting for about half of these. Overall, we observe all three kinds of governance at play in relation to sustainability certifications – some vertical top-down elements (especially from Scandinavian and Canadian monopolies), some vertical bottom-up (large firms proactively adopting sustainability certifications even in the absence of demand), but also horizontal – with strong national institutional support in the development of sustainability standards coupled with local consortia playing key roles in driving adoption among their members.

Environmental upgrading as going ‘back to tradition’

Small wine producers show less orientation towards sustainability certification in their process of environmental upgrading in comparison to large ones.

11

Rather, they tend to link environmental stewardship to traditional methods of training vines and harvesting. Two small Valpolicella producers, for example, indicated the following: ‘Our vineyards are planted with the Veronese pergola system, which allows you to make fewer treatments and thus you help the environment and actually save in costs. The pergola protects the grape bunches during the hot hours of the day, which is important because Corvina is a delicate grape … The Guyot system has become popular because it allows you to harvest mechanically once you have harvested selected grapes for Amarone production [by regulation, Amarone can only be harvested by hand]. With the pergola system, all harvesting is manual’ (V1).

‘Guyot allows a more intensive form of planting … This leads to more compacted soils, rows that are closer to each other and thus more interventions which means more tractor passages, each time placing more weight on the soil and compacting it further. Compact terrains lack enough oxygen and have lower water retention properties, they also have less capacity to allow ionic exchange. As a result, the vine has higher needs from a point of view of nutrition and water. Forcing the vines this way means that they are more prone to be affected by disease, they live shorter lives and lose the typicality of flavour that comes from a long-term match with their natural terrains’ (V3).

Other small producers reinforced these arguments. One told us that they want to ‘eliminate the use of plastic string to tie the vines – there are now threads that are biodegradable in six months. You can also use willow branches. In a newly established vineyard, we are using bamboo and wooden poles instead of iron and plastic poles. We are also making an effort to restore and maintain drywalls, which are very good natural environments for useful insects. It is quite beautiful to set up a vineyard like this’ (V5).

In Prosecco areas, similar arguments are made – with distinctions made between the hand harvesting of ‘heroic agriculture’ in the hilly areas in the Valdobbiadene DOCG area vis-à-vis the mechanized harvesting that takes place on the plains. However, these distinctions are discussed in relation to the use of manual labour and related challenges, rather than in connection to environmental upgrading (see details in Ponte, 2021).

Another aspect of the discussion of environmental upgrading as going back to tradition is explicitly or implicitly related to the preservation of biodiversity. As one of our interviewees told us, there are three relevant aspects of biodiversity in viticulture. The first is about viticulture as monocropping: ‘Old-style viticulture was not a monoculture system. There were rows of grape vines but they were 20 metres from each other because they needed to pass through with the oxen plough. In between vines, you planted maize, vegetables, whatever’ (V3). The second aspect is the natural biodiversity of the ecosystem within which the vineyard is integrated: ‘This is preserved not only by avoiding herbicides, but also leaving the grass to grow high and not cutting the grass when it is still full of wildflowers. It is important to maintain an equilibrium between species where there is no predominance of one kind over the others’ (V3). A third element of biodiversity in viticulture has to do with the diversity of grape varieties: ‘Grape vines have the great property that they self-select … They are good at making genetic variants. It is very important therefore to avoid homogenization. This is why it is essential to rediscover the genetic diversity of vines in the fields, to preserve the variants that have developed in time … Everyone thinks of biodiversity in terms of the ecosystem, but they forget the biodiversity of vines’ (V3).

As the quotes included in this section make it clear, for small producers the most recurrent environmental upgrading processes are related to tradition, the maintenance of biodiversity and the stewardship of land. These producers are rarely found at wine fairs, although they may feature in dedicated small producer pavilions (which we did not visit at Vinitaly in 2022). These are strong indicators of bottom-up vertical dynamics in the sense that they are generated by producers and communicated (usually orally) to their buyers and direct consumers.

Environmental upgrading as technological innovation

Spurred by incentives at the national and regional levels, in both Prosecco and Valpolicella one of the main set of processes implemented by large players to improve their environmental footprint is related to technological innovation. These processes include solutions linked to the language of ‘Industry 4.0’ technologies adapted to viticulture, or ‘Viticulture 4.0’, such as resistant varieties, precision spraying machines, mechanical defoliage and precision viticulture. Several producers have started to plant new vineyards with resistant varieties, which need only few agro-chemical applications (IG12, IG15). However, they also complain that the consortia regulations do not allow them to use these varieties for DOC wine production (V5, V12).

Several large producers and the consortia of both districts also reported an increase in the use of lower emissions vehicles, LED-based illumination systems, solar panels, geo-thermal energy, cold accumulation systems, ecological materials for packaging, the use of pomace for distillation and pruning biomass for compost, energy and biochar production processes. The use of renewable energy and better packaging materials is also increasing in both districts. Representatives of one of the large cooperatives active in the Prosecco DOC area told us that traditional sprayers are disappearing, and that many farmers now use the more efficient ones that better target the vine (P13). A large operator also argued that these technologies are ‘helpful to achieve better traceability, which is becoming increasingly important to manage the supply of grapes and the blending of special batches’ (P18).

In Valpolicella, large operators reported a similar set of approaches: ‘We protect the environment with specific agronomic techniques, such as mechanic weed control and the use of pheromones … we also have a circular economy approach beyond the vineyards. For example, we use thermoregulators for winemaking … One of the main current challenges is related to packaging, especially light glass, recycling and the use of alternative materials – such as paper instead aluminium capsules … The monopoly buyers in Scandinavia are pushing hard on materials and packaging. This trend is there and we cannot ignore it, although demands are very different in other export markets. We follow a logic of continuous improvement’ (V2).

‘A lot of the drive for re-evaluating packaging solutions is coming from the monopolies in Northern Europe and Canada: they want lower CO2 emissions and lighter bottles. For example, in Quebec, we had to lighten the bottle of Ripasso from 650 g to 450 g or pay a penalty of 25c per bottle. We actually saved money both on the bottle and on transport!’ (V11)

These sets of observations suggest that there are important bottom-up vertical dynamics at play (combined with some top-down in relation to packaging) in the way large operators adopt environmental upgrading processes. These are facilitated by multiple knowledge networks (Sedita et al., 2021). But the mechanisms at play here are quite different from those highlighted in the previous section in relation to going ‘back to tradition’ – they hark to ideas of technological innovation and circular economy. At the same time, there are also important horizontal governance factors at play, given that various layers of government provide important incentives for the purchase of Viticulture 4.0 technology.

Environmental upgrading as an articulation of local politics

What we refer to as articulation of local politics in the following discussion has two main aspects. The first is related to the major health and environmental problems that the spraying of agro-chemicals for viticulture is causing in local communities. The second is discussed under the rubric of viticulture expansion and changes in land use.

The first aspect became quite controversial when, in November 2016, the public broadcaster RAI 3 released a documentary on Prosecco, highlighting the negative health impacts of agro-chemical spraying in the core Prosecco DOGC area, where vineyards are literally planted everywhere, including next to residential areas and schools. 12 The documentary also refers to protests by local committees against what they see as the indiscriminate application of agro-chemicals. A follow-up documentary released in 2017 includes footage with the director of the DOC consortium – where he indicates that the new rules promoted at the local level have banned the use of glyphosate, thus going beyond EU and Italian regulatory standards. 13 This is indeed a sign of environmental upgrading, but one that is based on reaction to pressure from local committees, not from international buyers of Prosecco (Basso and Vettoretto, 2020; Ponte, 2021; Visentin and Vallerani, 2018), aimed at maintaining their ‘social license to operate’ (e.g., Moffat et al., 2016).

Valpolicella has avoided such negative publicity, and indeed a representative of one of the main cooperatives argued that ‘sustainability is important to keep good relations with local populations’ (V8). Another interviewee stated that they have had ‘similar problems as in Valdobbiadene, with local populations complaining about the spraying of agro-chemicals, but without the media attention so far. Local committees protested with their municipal administrations first. The municipalities wanted to contain the possible reputational damage and worked to promulgate local regulations to limit the use of agro-chemicals, but not all municipalities have done so’ (V9).

The second aspect of local politics relates to current attempts seeking to slow or stop area expansion. As seen earlier in this article, the viticulture area expanded dramatically in the 2010s in both Prosecco and Valpolicella – followed by moratoria on new plantings. Other scholars have already highlighted the problematic nature of that they call ‘viticulture sprawl’ in the Prosecco DOCG area – with vineyard expansion replacing traditional cropland, grassland and woodland (Basso, 2019; Basso and Vettoretto, 2020). Something similar is also occurring in Valpolicella. 14

In sum, environmental upgrading processes (for both large and small producers) have taken place in close articulation with local politics – in response to accusations of environmental and health hazards arising from viticulture expansion and intensification. Local protest committees and media exposure (in Prosecco) and fear of the same (in Valpolicella) are partially reshaping local regulations and practices on the use of agro-chemicals and allocation of planting lefts – clear signs of horizontal governance at play.

The governance of environmental upgrading

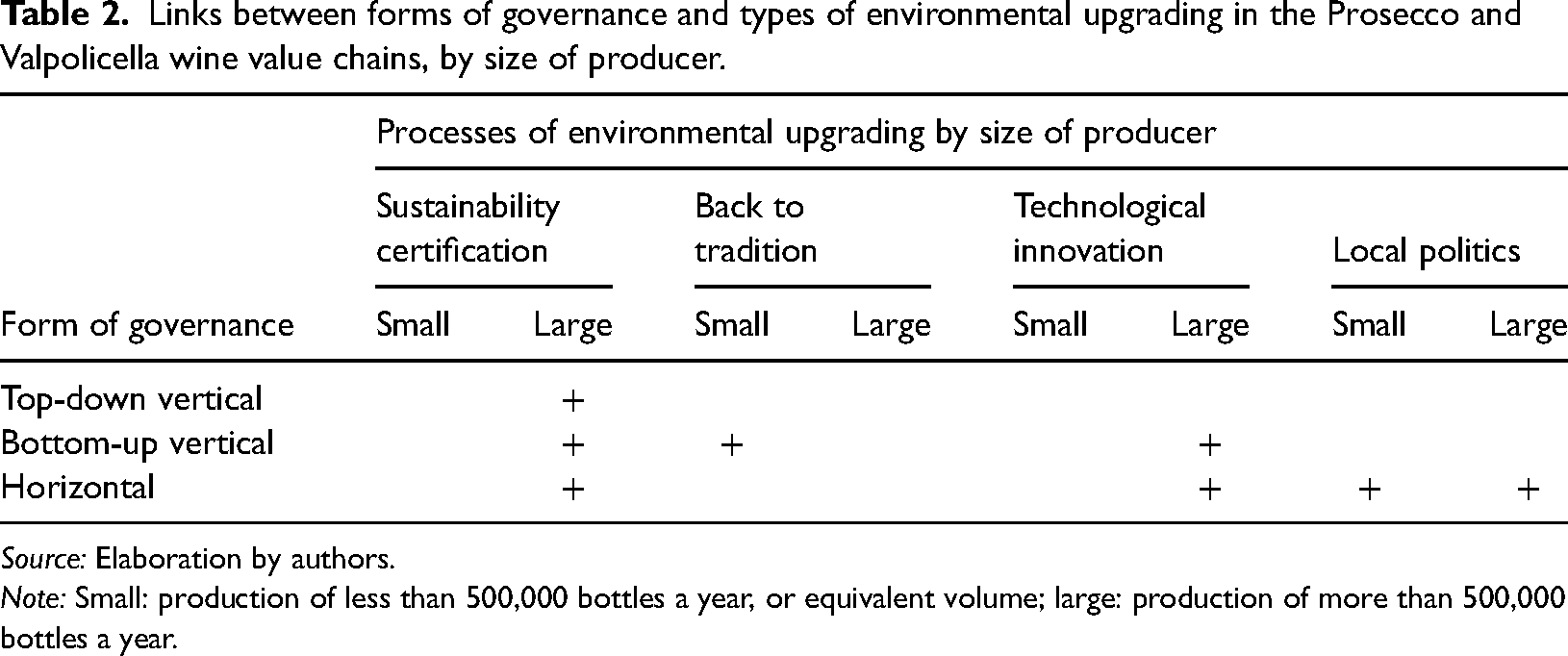

In this section, first we further leverage the material presented above to illustrate how top-down vertical, bottom-up vertical and horizontal governance shape each set of upgrading processes we identified – differentiating by the size of wine producer (see summary in Table 2). Second, we highlight three possible factors that can make horizontal and bottom-up vertical governance more likely to influence environmental upgrading – in addition to, or in substitution for, top-down vertical governance.

Links between forms of governance and types of environmental upgrading in the Prosecco and Valpolicella wine value chains, by size of producer.

Source: Elaboration by authors.

Note: Small: production of less than 500,000 bottles a year, or equivalent volume; large: production of more than 500,000 bottles a year.

In both Prosecco and Valpolicella, top-down vertical governance mechanisms are present, but they do not seem to be dominant in explaining environmental upgrading trajectories, being limited to requirements related to sustainability certification. Indeed, broad sustainability certifications and demands linked to carbon footprint (packaging, recycling of materials, etc) are neither requested in the domestic market nor in most export markets – with the important exception of state monopolies in selected Scandinavian countries and Canadian states. Although these are retailers, their strategies are driven by public policy objectives, including those related to sustainability – so, they are not the classic private ‘global buyers’ that the GVC literature usually refers to. Sustainability certifications do not seem to play a major role in the hotel, restaurant and catering channel or in the direct/internet sales channel.

Hence, differently from many other agro-food sectors (see, e.g., Giuliani et al., 2017; Kleemann et al., 2014; Krauss and Krishnan, 2022), we do not observe an all-encompassing buyer-driven dynamic of environmental upgrading. Although demand for wine made from organic grapes is increasing, producers in Prosecco and Valpolicella are not rushing into organic conversion, also because of the impact on margins that this would entail if a premium is not paid. Sustainability certifications and carbon footprint reductions are still ‘nice to have’ rather than ‘must have’, and even these mostly apply to large wine producers. On the contrary, small producers tend to specialize in niche markets (including those for organic and biodynamic wines), but not necessarily through certification per se – as they may opt to specialize in the production of ‘natural wines’, which are currently quite popular in many top-end wine markets.

When it comes to bottom-up vertical governance, there are significant differences among wine producers of different size in how they approach environmental upgrading. On the one hand, many of the large producers, spurred by their consortia, are pro-actively seeking sustainability certifications. They are also involved in technological innovation – partly guided by incentives for ‘Viticulture 4.0’ investment (which are also a feature of horizontal governance). On the other hand, small producers tend to prefer to go back to tradition in their stewardship of nature, biodiversity and land – demonstrating some degree of autonomy and vision in shaping their processes of environmental upgrading.

As indicated in many quotes in the previous section, horizontal governance is actually playing an important role in shaping environmental upgrading processes. This is happening through proactive approaches characterized by cooperation between (both large and small) producers, producer consortia and local/regional political networks. There are horizontal governance elements in relation to both sustainability certification – given the major role various ministries and consortia have played in developing them – and in relation to technological innovation, which is being promoted by various layers of government through targeted incentives. But these processes can also have reactive features, particularly in Prosecco where protests by local committees and media exposure have led to the revision of local regulations (both at the municipal and consortia levels) and to a strong institutional pushback against accusations that viticulture expansion is creating serious environmental problems. In Valpolicella, this has happened more indirectly, as part of a strategic intent to avoid the kind of media exposure Prosecco had experienced. 15 Reactive horizonal governance may be playing a more important role in our case studies than in other wine value chains, in Italy and elsewhere. This is because of the dramatic increase in viticulture areas, meaning that vineyards are being planted literally next to houses and public buildings – a growth that was driven by the market success of Prosecco and Valpolicella wines especially in the past decade. This success has also led to growing tensions between wine industry operators who benefit from this growth and those who are suffering from negative externalities. This has exacerbated the conflict between inhabitants and wine industry operators with the latter trying to adjust their practices as a result of local protests and pressure (Basso and Vettoretto, 2020; Ponte, 2021; Visentin and Vallerani, 2018).

We argue that the salience of these observations is not confined to the wine value chain in these two districts, but has broader implications for other wine districts and value chains. In view of providing some directions for further research, we suggest three factors that may make horizontal governance (and to some extent bottom-up vertical governance) more likely to shape one or another of the four trajectories of environmental upgrading we identified.

The first factor is issue visibility – local communities and political systems can be activated by the direct and visible environmental impacts of value chain operations, thus opening the possibility of environmental upgrading as an articulation of local political struggle. From this point of view, local actors in other wine districts or other value chains can also work on strengthening such visibility, especially where part of the value of the product is accrued from locally specific features.

A second factor is proximity – environmental upgrading as a return to tradition can best function through direct interaction between (smaller) producers and direct consumers. Physical proximity and interaction open the possibility of closely involving customers in supporting the environmental upgrading efforts of smaller firms. Food and wine tourism is growing worldwide, indicating that consumers are increasingly interested in visiting production sites and in experiencing production processes first-hand. This allows them to engage directly with local firms and gain a deeper appreciation of production within different social, cultural, landscape and environmental contexts.

A third factor is the presence of public incentives that can drive (larger) industry players to take technological innovation and/or sustainability certification trajectories towards environmental upgrading (in addition to, or in substitution of, top-down vertical governance pressures). At the same time, such incentives can also coalesce all firms to improve their performance to meet public goals (i.e., local health conditions and economic development).

Conclusion

In buyer-driven GVCs, such as the one for wine, vertical governance dynamics are said to be key in shaping environmental upgrading trajectories – either in terms of top-down (see, e.g., Alexander, 2020; Ponte, 2019) or bottom-up governance (especially when suppliers are based in the Global North; see, e.g., De Marchi and Di Maria, 2019). What we observed in the Italian wine value chains of Prosecco and Valpolicella is that top-down and bottom-up vertical governance elements are not dominant in shaping environmental upgrading. Our in-depth case analysis suggests that horizontal governance plays a more important role than it has been argued so far in the literature – driven by protest committees based in local communities and amplified by media exposure, together with various layers of public support, incentives and regulation. Furthermore, our analysis highlights a multitude of environmental upgrading processes can take place place at the same time. These are all aiming at reducing the environmental impacts of production, but operate through very different sets of actions.

Our study focused on two exemplar cases. However, we are not arguing that Prosecco and Valpolicella are representative of a broader set of experiences in other wine value chains or indeed other agro-food industries. We are not claiming that the four categories of environmental upgrading processes we identified are a complete categorization either, nor that all four are relevant to other wine industries or value chains. Rather, we argue that within the same industry, very diverse environmental upgrading processes can take place, and that these should be identified and understood in relation to GVC governance dynamics. Typologies of environmental upgrading can be thus identified inductively in every industry, but starting from a common analytical understanding based on three observations: that such processes may be characterized by leveraging different types of competences and technological bases; that the motivations for their introduction can be diverse; and that they may be different for producers of different size or market specialization – thus that analyzing the full spectrum of actors is fundamental. Finally, we argue that to explain how horizontal and vertical governance dynamics shape environmental upgrading processes we need to further understand the roles of issue visibility, proximity and public incentives.

Ultimately, we encourage researchers to add more nuance to the relations between governance and environmental upgrading in value chains. In ‘buyer-driven’ and unipolar value chains, there has been a tendency to overlook the role played by local and regional actors, such as territorial institutions, consortia organized around geographic indications, local government through municipal regulation, national government through incentives and subsidies, activist networks or single-issue pressure groups. Against this background, our analysis suggests the importance of disentangling vertical (top-down and bottom-up) and horizontal governance structures, as each is driving different forms of environmental upgrading – in view of suggesting appropriate policies, strategies and activist approaches that could facilitate better environmental upgrading processes and ultimately outcomes.

Footnotes

Author’s Note

Stefano Ponte is also affiliated with University of Johannesburg and Valentina De Marchi is also affiliated with Universitat Ramon Llull, ESADE.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors thank Gianluca Perillo for invaluable research assistance. Stefano Ponte would also like to acknowledge financial support from SSHRC (Canada), grant number 895-2018-1002: The Hidden Costs of Global Supply Chains.