Abstract

This article reasserts the value of the examination of class relations. It does so via a case study of tax-processing sites within HM Revenue and Customs, focusing on the changes wrought by the alterations to labour and supervisory processes implemented under the banner of ‘lean production’. It concentrates on the transformation of front-line managers, as their tasks moved from those that required tax knowledge and team support to those that narrowed their work towards output monitoring and employee supervision. Following Carchedi, these changes are conceptualised as strengthening the function of capital performed by managers, and weakening their role within the labour process.

Introduction

The 1970s produced a significant debate within sociology on the rise of a new middle class that, unlike the middle class of independent producers and the self-employed, was intimately connected to developments within capitalist labour processes. Within the debate, Poulantzas (1975) and Carchedi (1977) emphasised the specific social relations of those who, while not owning the means of production, carry out functions on behalf of capital. Braverman (1974) was also central to the debate, as his contribution to labour process analysis centred on the increased division of labour and the creation of new roles to superintend the performance of reconfigured labour as workers’ knowledge was progressively captured, codified and desublimated into the growing hierarchies of control. These hierarchies resulted in the increased division of managerial work and the diminution of the hitherto extensive power of front-line managers (FLMs), as managerial hierarchies became staffed increasingly by graduate intakes (Child and Partridge 1982). So powerful was this tendency that in a number of accounts, managerial and supervisory employees were characterised as being proletarianised as they experienced ‘greater insecurity, stress, [and] decline in pay relative to senior management’ (Scarborough and Burrell 1996: 185), and were conceptualised as wage labour and members of the working class (Meiksins 1986; Smith and Thompson 1999).

Today, theories focusing on the centrality of workplace relations in the generation of class relations have all but disappeared (Atkinson 2009), overshadowed firstly by what Crompton (2008) termed the ‘employment aggregate’ approach to class’, associated with Goldthorpe (1980) and Erik Olin Wright (1997), and secondly by more cultural analyses influenced by Bourdieu’s (1986) emphasis on cultural and social, as opposed to economic, capital (Savage 2000; Skeggs 1997; Hebson 2009). Where there is contemporary concern with groups at work that might be still termed ‘new middle class’, excessive weight rests on subjectivity and the ontological insecurity of managers, (see, for instance, Thomas and Linstead 2002; Willmott 1997). Even theorists who continue to acknowledge their debt to Braverman now eschew the connection between class and the labour process as crude and unhelpful (Hassard et al. 2009). The legacies of Carchedi and Poulantzas fare no better, with Smith and Thompson (1999: 219) dismissing them as being concerned with ‘the very sterile functionalist project of manufacturing classes out of the technical division of labor’. Indeed, all theories relating labour process perspectives to class analysis are rejected in toto, as ‘attempts … to reconnect the analysis to class theory … are flawed enterprises’ (1999: 205).

This paper takes issue with these conclusions to return to social class and the workplace, not in terms of a long British tradition of determining class through subjective self-classification (see Nichols 1979 for an effective critique of this approach, and Marks and Baldry 2009 for its continuation), but rather utilising much ignored Carchedian perspectives on the class relations entered into during production. Of course, class relations in capitalist societies are manifested beyond production. Indeed, Marx’s detailed examination of class within the production process was entitled ‘Results of the Immediate Production Process’ (Marx 1976). That class relations were not restricted to this sphere was indicated both by his stress on the ‘immediate’ and through other works, such as Class Struggles in France (2007). Nevertheless, despite this qualification, focus on relations in ‘the hidden abode of production’ (Marx 1976: 279-80), with an attendant concentration on ownership, control, and the production of surplus, was central; and now, as then, these relations are frequently ignored or obscured.

This article examines the changing class relations reflected in, and mediated by, the roles played by front-line managers (hereafter FLMs) in Her Majesty’s Revenue and Customs (HMRC). The object of the research is significant for its size. HMRC employed over 90,000 workers when it was established in 2005 by the merger of Customs and Excise and the Inland Revenue, a figure that had been reduced to 67,000 by 2010. The department is responsible for the administration and collection of taxes, ranging from income to corporation tax and National Insurance contributions, as well as the distribution of Child Trust Funds and the payment of Tax Credits. The progressive implementation of changes in workplace organisation took place from 2005 onwards under the rubric of lean production (or ‘Lean’, as it is became known), which was a purported means by which services could be maintained and improved despite the reduction in headcount. The changes comprised the adoption of classic Taylorist work-study techniques, task fragmentation, ICT-enabled changes in flow, standard operating procedures, and arbitrary hourly targets. Documenting these changes extends our knowledge of lean production to white-collar work, thereby adding to accounts of the intensification of work in the automotive industry (Stewart et al. 2009), as well as to earlier studies highlighting the impact of lean production on the health and safety of workers (Lewchuk and Robertson 1997). Elsewhere, closer parallels are drawn to these works, dealing with the degradation of work, the relationship of Lean to new public management, the impact on workers’ health and safety and industrial relations, and the performance of the trade union (Carter et al. 2011a; 2011b and 2013a; 2012 and 2013b). The primary focus here is on the exercise of authoritarian management and the neglected area of class relations.

The purpose, therefore, is not to engage with the extent to which the model of Lean utilised is a ‘pure’ or coherent one. In their evaluation, hired consultants expressed reservations about the extent of HMRC’s success in becoming Lean, albeit noting that it ‘is moving in the right direction’ (Radnor and Bucci 2007:7), but more pertinently, all implementations inevitably depart from Womack et al.’s original model (Danford 1998), and even subsequent work by Womack and Jones (2003) has a different emphasis. What is important here is the fact that the use of the term ‘Lean’ was synonymous in HMRC with changes sought by a management committed to a new regime that has been promoted as an exemplar for the rest of the Civil Service and beyond (Radnor and Boaden 2008). The term is retained as a shorthand for these changes.

The analysis of workplace changes is foregrounded by a brief examination of the classic writings on class and supervision, and the ways in which developments in the organisation and supervision of white-collar labour have impacted on the balance between the roles of coordination and control traditionally performed by FLMs. The HMRC case study describes contested changes that have increased control, intensified white-collar work and altered the balance of tasks within managers’ work. Finally, the paper assesses the implications of changing roles for managers’ union membership and class relations.

Class, management and supervision

Accounts frequently attribute to Marx a binary class structure under capitalism comprising a bourgeoisie and a proletariat based on ownership of the means of production and the need to sell labour power, respectively (Carter 1985). The resurgence of interest in Marx’s work in the 1970s attempted to dismantle this orthodox view. While the growth of capitalist production eliminated many petty bourgeois, small-scale and independent producers, and thus supported the idea of proletarianisation and a polarised class structure, new studies directed attention to the simultaneous growth of a new middle class configured within large-scale capitalist enterprises. There were sharp disagreements about the exact basis of, and appropriate terminology for, this phenomenon, but there was agreement that the class structure was far from a simple dichotomy. Although the analysis of Poulantzas (1975) gained far more prominence, the work of Carchedi (1977) was arguably more consistent with Marx’s theory (see Wright 1978 for an effective critique of Poulantzas). Carchedi pointed to the consequences for class relations as enterprises grew: ownership became dispersed through joint-stock companies, and owners’ involvement in management and production ceased, replaced progressively by managerial hierarchies.

Management of capitalist enterprises had always possessed dual functions of control and supervision, on the one hand, and coordination and unification of the production process, on the other (Marx 1991: 510). While the former tasks arose specifically because of the antagonistic relations of production, due to the complexity of production, the latter would be necessary under any socialised system, while coordinating and unifying production managers were part of the collective worker. It followed that the supervision and control necessary for capitalism (in Carchedi’s term the ‘global function of capital’) added nothing to the use value of products, and were not part of a labour process. Marx described the costs of these tasks as ‘faux frais de production’ (incidental costs) (Marx 1976: 446). In contrast, coordinating and unifying tasks were part of the labour process paid from variable capital. Much of the discussion on white-collar and state labour has revolved around the significance of the categories productive and unproductive labour; the particular significance of Carchedi’s contribution was his attempt to re-draw the contours of this debate by insisting that the tasks of supervision and control, however necessary under capitalism, were neither productive nor unproductive labour, but were non-labour. With this analysis, Carchedi maintained that it was possible to distinguish a new middle class that did not own the means of production, but carried out, though not necessarily exclusively, those functions associated with the global function of capital.

These differences in perspectives on class were mirrored within the analysis of state employment. Some writers treated the vast majority of state employees as productive workers (Cockburn 1977; Gough 1975). In contrast, Poulantzas (1978) maintained that all state employees outside certain nationalised industries and transport were either bourgeois or petty bourgeois. In the context of the Civil Service in general, and HMRC in particular, all site-level employees would therefore be petty bourgeois. FLMs and the people they supervise alike would be given no noticeably significant distinguishing social functions or separate interests. Observed conflict and antagonism would have no social structural basis. Carchedi’s position allowed for more distinctions consistent with Marx’s analysis. Just as the social relations of individual firms involve unifying and coordinating roles, so does any complex society need roles that ensure social reproduction and the generation, coordination and transmission of socially useful knowledge. Such work is part of a labour process, and as such, those performing it are part of the working class. However, just as the capitalist company is exploitative and requires the management of the supervision of wage labour, the capitalist state is oppressive, with a need for ideologists and a repressive apparatus. Those performing these tasks are not part of the labour process, and not members of the collective worker (Carter 1995).

These perspectives inform the approach here. However, while FLMs are viewed as part of the management hierarchy and can be characterised as new middle class, their actual day-to-day relations and the nature of their social functions are complex, and thus no theoretical schema can substitute for an examination of their actual and varied relations. Contrary to Smith and Thompson, starting from an analysis of the structural bases of class does not necessarily entail perspectives on social classes that display ‘an aversion to empirical work and a tendency to create classes alfresco’ (Smith and Thompson 1999: 219).

Changing relations in white-collar work

Sociological work on supervisors tends to focus on those overseeing manual labour processes. While post-Second World War accounts characterised FLMs as being caught between the competing social forces of capital and labour (Roethlisberger 1945, Wray 1949), later ones charted the long-term decline of their power as managerial hierarchies grew (Nelson 1975). As Rose et al. (1987: 8) show, the claim that ‘supervisors are progressively being denuded of their powers and functions within industry’ was common to studies from very different political perspectives. Post-industrial theorists saw the rise of newly skilled categories of labour, frequently organised in teams, rendering supervisors largely redundant. Theorists from a Marxist perspective, arguing the tendency of capitalism to deskill workers, envisaged a different path: simplified work could be controlled by technical or bureaucratic organisational means (Edwards 1979), thus emptying supervision of authority and discretion. This process, according to Braverman, was accompanied by ‘multiplying ranks of supervisors, foremen and petty managers’ (1974: 407).

Evaluating these positions, Rose et al. (1987) acknowledged that while foremen and inspectors’ powers of sanction on subordinates (affecting promotion prospects, suspension or discipline) had declined, they were still involved in task allocation and decisions about the pace and intensity of work, leading to the conclusion that: ‘independent, direct and authoritative supervision is still a significant element in the apparatus of social control at the point of production’ (1987: 20). Despite the confidence with which this contention was made, it was likely unfounded, not least because it ignored the long-term weakening of supervisors’ functions (Ray 1989: 68), a weakening further displayed in the case study examined here.

There is no a priori reason to suppose that these developments should be paralleled in white-collar areas. Nevertheless, there is a long tradition of recognising that the class position of routine white-collar employees is often little different from that of manual workers (Crompton and Jones 1984; Baldry et al. 2007), and much contemporary work emphases the convergence of deteriorating conditions, even to the extent of claiming that ‘the burden of change has fallen increasingly on a hitherto rather better protected and better rewarded group of people – salaried white-collar middle managers’ (Hassard et al. 2009: 5). Major changes within white-collar work have been driven by increased competition, government cuts and rationalisation, and the adoption of ICT innovations. Unsurprisingly, ICT impacts on the social organisation of production, with Hassard et al. (2009: 5) claiming that it ‘has seemingly eliminated the need for many of the traditional roles of middle managers, such as monitoring front-line employees and conducting horizontal and vertical communication’. Accordingly, thousands of middle-manager jobs have been eliminated, while the roles of those remaining ‘have increased massively in scope and scale’ (2009: 6). Moreover, they are just as subject to control from above as other employees, with control embedded in targets and the requirement to collect and collate statistics that simultaneously monitor and expose managers’ own performance (Nichols and Beynon 1977; Boreham et al. 2008).

The evolution of white-collar work organisation has impacted on the role of supervision. Before the advent of call centres in the utilities sector, for instance, supervisors played ‘a minor role in managing an individual clerk’s workload, acting more as technical experts, often undertaking clerical duties that required authorisation of expenses, or the allocation of allowances to customer accounts’ (Ellis and Taylor 2006: 114). Using Carchedi’s perspectives, supervisors had at this point a significant role within the labour process, but that role has been weakening as the demands for more greater supervision and control of labour escalate. The imposition of quantitative targets and performance management particularly associated with call centres and their integration of ‘advanced telephony with various computer technologies’ (Taylor and Bain: 353) provided the means for linking corporate strategy and workplace productivity, tying supervisors more closely to value extraction and transforming workplace relations, as both managers and workers were constrained by the new demands. Baldry et al.’s (1998) study of the intensification of white-collar work in large private and public-sector offices (1998: 174) stresses, alongside electronic surveillance, the importance of the physical reorganisation of the workplace: ‘the modern office is characterized by cellular or team forms of organization in which supervision or team leaders, or other HRM equivalents, perform the role of continuous visual surveillance’. It is not clear from this account the extent to which managers continued to engage in labour-process activities. Team leaders in the private-sector office studied certainly did retain a role, and the absence of team leaders in the public-sector offices suggests residual retention of line-management roles in advising and supporting workers on labour-process issues. The decline in this latter aspect in HMRC is significant, and is traced below through an examination of the way changes in HMRC transformed managers’ responsibilities, from those concerned with supporting employees and production to new responsibilities emphasising control and supervision, thus providing the focus for an examination of changing class relations.

Methodology

The research is concerned with changes in class relations in contemporary white-collar employment. The Civil Service in general, and HMRC in particular, is an appropriate site for such research, since the department has a large number of highly concentrated white-collar service employees, and was subject to a process of reorganisation that allowed an evaluation of the social effects of changes to the labour process, supervision and control. The research was particularly pertinent since HMRC employees’ experiences of working under the new conditions were intended to be prototypical for significant areas of the Civil Service. The results are based on work carried out in 2008-11 at six large processing sites of HMRC that were subject to the implementation of the ‘Lean’ package. A mix of qualitative and quantitative data was collected. Trade union representatives were interviewed at all sites. Consistent with the approach to class analysis adopted, there were no direct questions on class affiliation, but detailed accounts were solicited on changes in work content and authority relations. The interviews, together with additional ones with administrative grades, revealed a concern with the changing nature of management, and, in response, interviews were extended to supervisory grades (FLMs) at four sites. In total, 36 staff were initially interviewed. The interviews guided the construction of an 11-page survey, focusing on levels of consultation with staff; job discretion; the impact of teamworking; work intensity; quality; job satisfaction; sickness, ill health and absence; managers’ views; and union effectiveness at local and national levels. Standard Likert-scale questions supplemented others derived from white-collar work-studies and concerns raised in exploratory interviews. The questions were formatted so that in order to be consistent, both positive and negative responses to statements had to be selected. Extended comments were also invited. The questionnaire was piloted and amended before distribution in 2008 to approximately 15 per cent of the workforce at each site. In total, 1650 questionnaires were distributed, and 840 (51 per cent) returned. Of the returns, 125 (15 per cent) were from administrative assistants (AAs), 627 (75 per cent) from administrative officers (AOs) and 83 (10 per cent) from FLMs. These returns, and the initial and supplementary interviews with and about line management, form the evidence base for the arguments developed. All interviews and their locations remain anonymous in order to ensure that individuals cannot be identified.

The research methods used here are underpinned by retrospective accounts of the situation in HMRC before the introduction of Lean. There are dangers that staff views are coloured by views of a ‘golden past’. However, the changes were still recent and on-going when the research was undertaken. Moreover, HMRC staff surveys taken year-on-year themselves indicate developing discontent, as staff considered the deteriorating quality of working life. To take just one example amongst many, in response to the question ‘I would recommend the Department as a good place to work’, in 2006, 28 per cent of respondents agreed and 46 per cent disagreed (HMRC 2006). By 2010, the respective figures were 10 per cent and 63 per cent (HMRC 2010). The responses in our research are subjective, but they are rich in the detail of change, as well as of attached emotion. Moreover, as Gabriel (1993) points out, it is the conditions of the present that produce nostalgia, and it is these conditions that are the focus.

The transformation of front-line managers in HMRC

Before successive reforms started by the 1997 Conservative government, proactive line management was not a prominent feature of Civil Service work (Carter and Fairbrother 1999). The establishment of ‘agencies’ (Fairbrother 1994) aimed to break-up a uniform, centralised Civil Service and its accompanying common conditions of service. In the process, bureaucratic relations were fractured, clearer managerial relations and responsibilities promoted, and private-sector management techniques introduced. Within the agencies, ‘new public management’ centralised policy-making while at the same time decentralising accountability for the attainment of targets (Pollitt 1990). The Gershon Report (2004) highlighted economies to be achieved by the rationalisation of staffing, closure and concentration of operating sites, and the simplification of processes. A reduced workforce, concentrated into large processing sites using standardised operations, would, it was hoped, produce efficiency savings and raise service levels. These developments would build upon the growth of contact (call) centres in the Civil Service to make organisations more efficient by separating routine enquiries from processing (Fisher 2004).

The subsequent introduction of Lean from 2005 into HMRC, alongside ICT developments, was part of a long process of reformulating both accountability and the nature of work, moving HMRC closer to a culture of command and control. Changing the social relations with subordinates and thereby the class practices of FLMs was critical in ensuring that they articulated more clearly the perceived interests of the state as employer, as specified by Gershon. The corollary of this movement, the elimination of elements of FLM roles that could be conceived as being part of the labour process, was integral to this re-articulation. The constitutive elements of class relations of FLMs are examined through the loss of roles associated with knowledge of tax issues, reflecting the transition of FLMs from experts contributing within the labour process to gatherers of statistics and monitors of the performance of others; the attempts by some FLMs to maintain discretion and older traditions of work and relations; and the effect of changes on FLMs’ trade union orientation.

From expertise and management to statistics and control

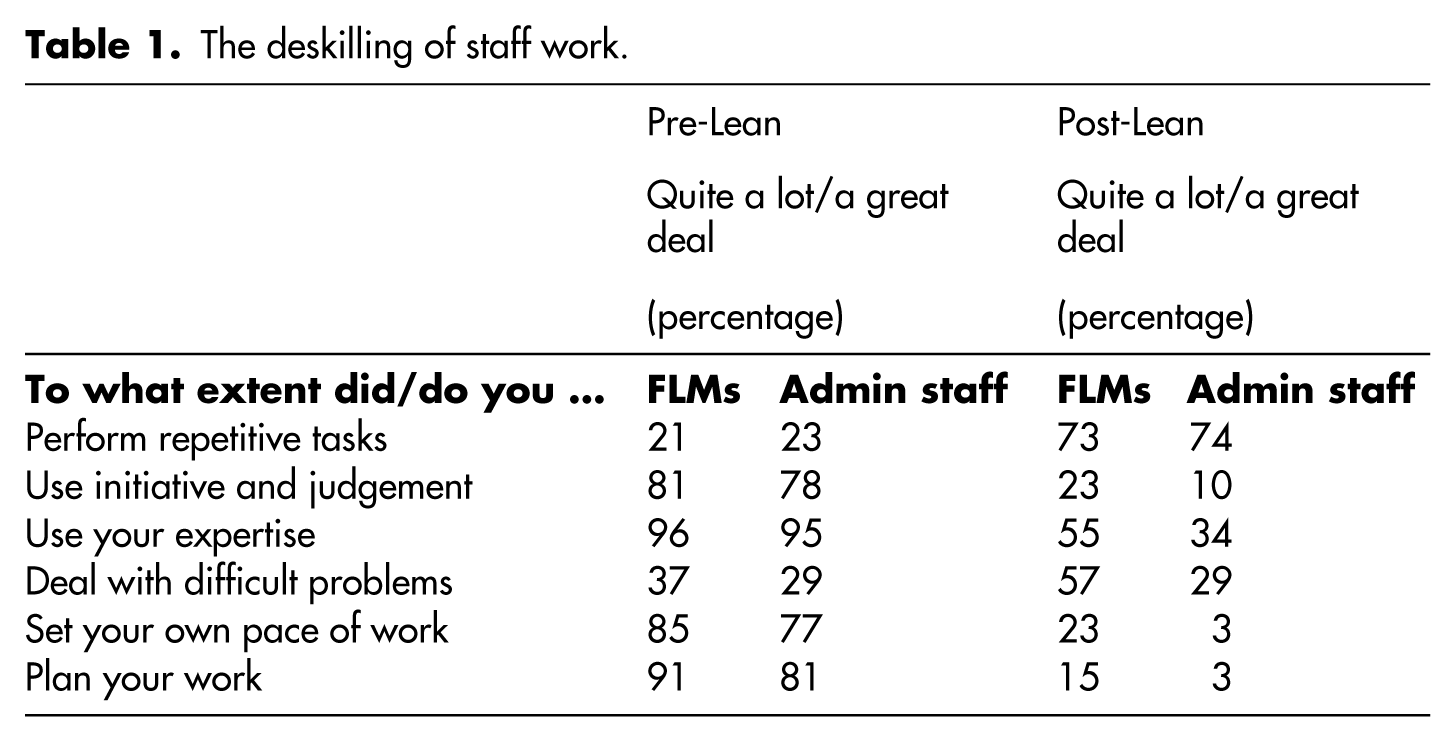

Prior to the introduction of Lean, FLMs’ roles were broader and less antagonistic towards employees. Traditionally, FLMs were longstanding, experienced employees who had expertise in the substantive issues concerning taxation. They were constrained by a management structure and procedures, but still conceived themselves as managers, confident of their abilities, exercising discretion, having a degree of autonomy, and taking pride in their work and performance. FLMs’ opposition to the package of measures associated with Lean showed few displays of nostalgia (Strangleman 1999). Nor did it have to respond to any narrative for change advanced by HMRC. Staff considered that changes were for the worse, and numerous concrete illustrations were forthcoming. Previously, for instance, knowledge of individuals in their sections was important, allowing FLMs to utilise different aptitudes: ‘anybody good at phone calls, I’d give them the difficult calls’ (branch secretary and former FLM, Site 5). Similarly, before Lean, supporting staff was a key aspect, and time was spent ‘coaching, assisting staff, actually dealing with work issues, staff issues, and being what’s classed as an old fashioned manager’ (FLM, Site 1). In contrast, under Lean, managers have substantially less control over their work as measured by perceived power to decide the pace and planning their work, when to take breaks and so on (Table 1). Questionnaire responses demonstrated that 85 per cent of FLMs considered that they had set their own pace of work pre-Lean quite a lot/a great deal, compared with only 23 per cent post-Lean. The contrast was even greater for the ability to plan their work, with figures of 91 per cent and 15 per cent, respectively.

The deskilling of staff work.

The erosion of their autonomy proceeded alongside deskilling as their work became more prescribed and repetitive: pre-Lean, only 21 per cent of FLM respondents performed repetitive tasks quite a lot/a great deal, compared with 73 per cent post-Lean. The use of their expertise had been dramatically reduced, from 96 per cent using expertise quite a lot/a great deal before Lean to 55 per cent after implementation. There was a similar perceived decline in the use of their initiative and judgement. Deskilling and loss of control were therefore combined aspects of the same processes, manifested in the repetitive collection and collation of information and the production of large volumes of statistics that not only monitored the performance of teams, but also constrained their own ability to make judgements. The following sentiment was common: You have to follow the set Lean standards for day-to-day working … as soon as I come in now, I have to fill in three sets of charts on my own board … go through and fill in my manager’s board, come back and by that time I’ve already probably about three hours’ worth of hourly stats to collect … whereas before I had obviously autonomy to use my own initiative. (FLM, Site 1)

Former autonomy included how to deploy staff: ‘You can’t do that under Lean. Everybody’s supposed to do the same. Everybody’s supposed to be the same, and as human beings, we’re not’ (Branch Secretary, Site 5).

The introduction of Lean signalled an attempt by higher management to tighten control of work processes. The system of collecting hourly output statistics, for instance, was designed to pressure FLMs to increase employee productivity, as indicated in this account: I send in what I reckon will be my available staff [for the following week] on a Wednesday … My manager will then send it back to me basically showing what the planned production is for each particular day … [but] in practice it’s unachievable. So each day, I’m basically failing personally to meet my targets … I would say every single [FLM] in the office without fail, every day, does not achieve their targets, and then has to stand at half past eleven every day and justify why you haven’t met it. (FLM, Site 1)

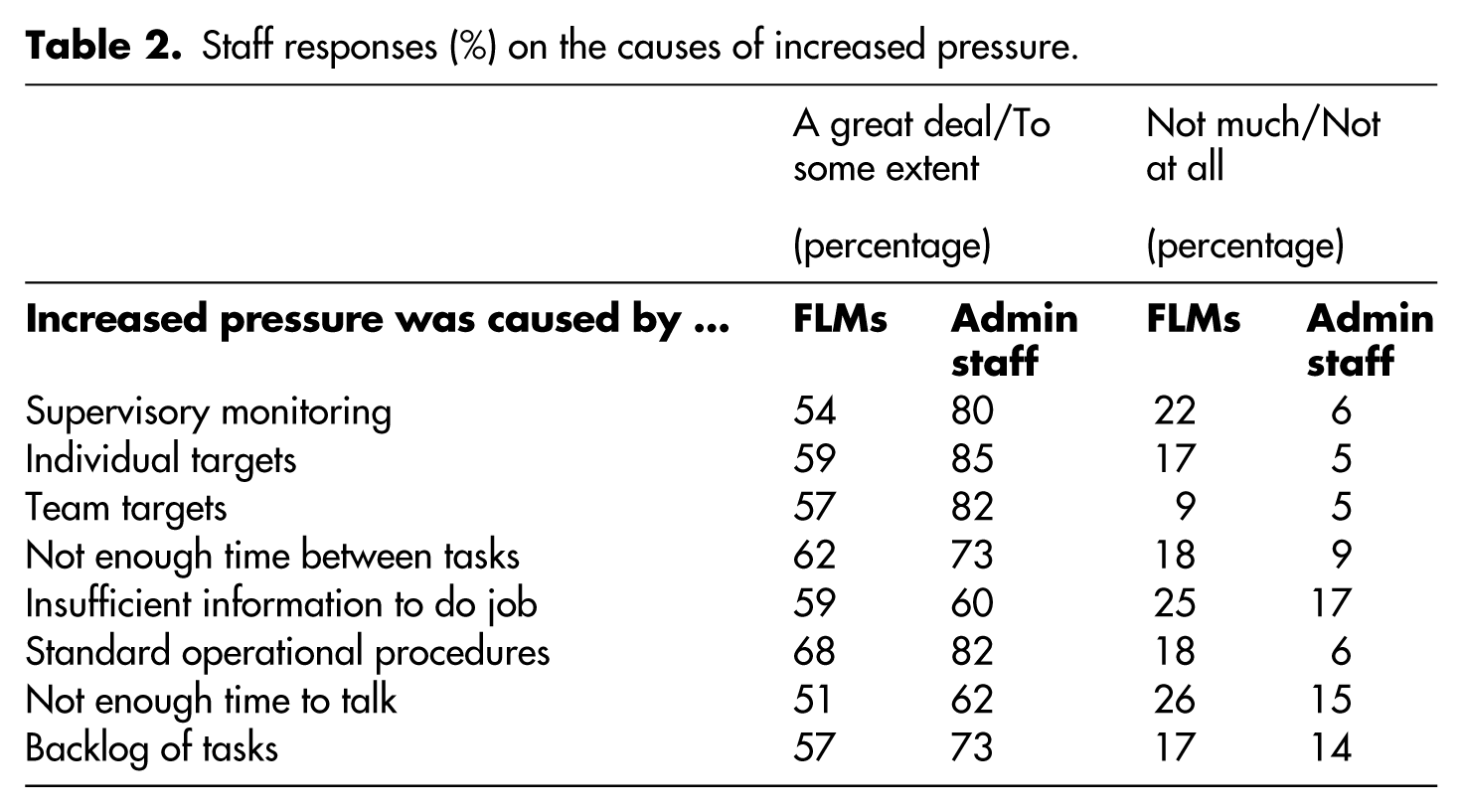

These expectations of FLMs resulted in a rise in the reported levels of pressure: 86 per cent of FLMs reported feeling quite/very pressured after Lean, compared to only 29 per cent before its introduction. The main causes of this increase, as highlighted in Table 2 , were identified as being the imposition of Standard Operating Procedures (68 per cent), and insufficient time between tasks (62 per cent). Other significant causes included individual and team targets.

Staff responses (%) on the causes of increased pressure.

The impact of Lean increased the pressure on managers, an impact replicated and intensified on administrative workers, so that the number feeling quite/very pressured rose from 14 per cent pre-Lean to 95 per cent following implementation. The new roles forced upon FLMs were implicated in this increased pressure, with new interactions between FLMs and their teams perceived almost entirely negatively. Individual targets topped the stated causes of increased pressure, but 80 per cent of administrative staff cited additional pressure being caused a great deal/to some extent by the associated monitoring of FLMs. In Womack et al.’s (1990) The Machine that Changed the World, one of the few comments made about the effects of Lean on workers was that they would find the work challenging and thus interesting. Where rhetoric met practice in HMRC, ‘challenging’ became narrowly interpreted as encouraging FLMs to ‘challenge’ poor performance: The hourly interventions … take place, but only if somebody was under-achieving … [FLMs] would have interaction with their staff, but only when there was a negative, never when there was a positive, or even just to build up a healthy working relationship, other than I’m the boss and you’ll answer to me. (FLM, Site 2)

Notwithstanding that targets were frequently unachievable, FLMs were expected to ensure that they were met, and failure resulted in pressure on them that they in turn were expected to transfer to their team.

Increased friction with employees

Little wonder, then, the workforce saw Lean as encouraging ‘bullying and control over staff’ (AO, Site 5, questionnaire) resulting in much higher rates of disciplinary action instigated by Early Management Action (EMA) against individuals over issues such as performance, working patterns and attendance. One FLM (Site 2) reported that ‘the team next to me has got three on EMA out of a team of nine or ten’. As a result of this significant move towards a more disciplinary regime, those managed by FLMs now view them very differently: [Previously] managers knew you, your capabilities, your quality of work and shortcomings as well. Now they choose figures to enter onto a board and to persecute us with. They are no longer involved with tax work. (AO, Site 6, questionnaire)

Increased friction is not restricted to the single issue of performance. Despite negotiated flexible working arrangements, at site level HMRC were attempting to curtail them as incompatible with Lean working (as advocated by Radnor and Bucci 2007): I had to speak to a guy yesterday because he put on his sheet … that he was going to work till 5 o’clock. He decided to go home at 4. He was pulled into the office the next day and was told he could well be subject to disciplinary proceedings. (FLM, Site 5)

Increasingly, punitive action is also being taken over sickness and absence. Managers’ discretion had been removed not so much by changes to the content of rules but by senior management’s insistence that FLMs responded in a standardised way when absences reached a particular number: It was [the departments’] interpretation that [FLMs] were making excuses for not operating the policy against individuals that they had good working relationships with because they were too friendly … So the drive was then ‘These are the rules; this is what you’re employed to do; this is what we expect you to do and over the next 12 to 18 months your manager will be having your sickness absence records for your staff every month to make sure you’re doing it’. (FLM, Site 2)

The combined changes to the work of FLMs – the routinisation, the collection of statistics and monitoring of performance – has signalled a significant cultural shift in the organisation, envisaging that managers doing their job ‘properly’ should no longer exercise managerial discretion in dealings with employees.

Resisting reforms and maintaining traditions

The new management style required neither substantive knowledge nor confidence to make decisions: Managers’ judgement … is something that doesn’t really exist any more … They want you to be exactly the same as the next person in the next city in the next county as if everybody is managed exactly the same. (FLM, Site 2)

The same standard operating procedures that govern tax handling under Lean have been applied to the supervision of tax labour. This restructuring of the roles of FLMs has taken its toll. They found themselves unable to influence implementation or to address problems within the workforce. Questionnaire responses from FLMs indicated that 72 per cent of manager respondents disagreed/strongly disagreed with the statement that Lean had made their jobs more interesting, and 74 per cent of managers agreed/strongly agreed that it had reduced their ability to manage with discretion. Only 16 per cent agreed/strongly agreed that they could influence the way Lean was implemented, and 53 per cent agreed/strongly agreed that it was now more difficult to deal with workers’ individual problems.

Managers felt relatively powerless and stressed by the expectations placed upon them. Many felt alienated from procedures, and did not identify with aspects of Lean. Fixing on the use of red signals, indicating that production was falling behind targets, one reported, ‘It’s always in red because they don’t do it right, because they work on timings that are too low anyway. So they’re never going to get it in green as long as they live’ (FLM, Site 4).

Experienced FLMs regarded the prescriptive polices around Lean as ‘interference in the role of the FLM’ (FLM, Site 6). These views have reportedly not gone unnoticed by senior management: The department tells us, or the senior management in the department estimate, that 35 per cent of their managers are ‘beyond redemption’. They recognise that 35 per cent of their managers cannot do the job the way they want them to do it. (Branch Committee member, Site 3)

Inability to do the job stemmed not from so much from weaknesses in FLMs’ technical capabilities, but from their attitudes, with some active resistance to aspects of Lean and the new managerial regime: We have [meetings] with my HO [higher officer] every day, and they’re sitting talking about an individual’s production. I’ve stopped it straight away because that’s not supposed to be happening, but again I’m viewed as negative because I’m not taking part in an allegedly constructive discussion. (FLM, Site 1)

Similarly, experienced managers took pride in their knowledge of tax work and were acutely aware of the causes of variations in performance and cycles of work that made nonsense of the demand for consistent achievement of hourly targets. This knowledge allowed them to question demands: If you could justify [failure to meet targets] then that in theory is the end of the matter. Providing your justification seems to be solid, then that would be fine. I would struggle to see how some people could justify it, though, if they don’t understand the work … the only thing that you’ve got is that the computer says that this is what you should be achieving. (FLM, Site 2)

Conflict between their personal assessments and the imperatives of their roles caused FLMs on occasions to adopt seemingly contradictory positions. One FLM was implementing Early Management Action for sickness absence while simultaneously providing union representation for the member: ‘I went through the procedures, but then went to the board’s medical examiner with him as his union rep and argued … that no action should be taken’ (FLM, Site 2).

There was therefore evidence of resistance to the closer integration of FLMs into the function of capital, but this resistance had definite limits. First, and obviously, FLMs themselves were open to disciplinary action for poor performance if they stepped too far out of line: ‘There would have been a proviso in there before about demotion, but I’ve never seen anyone demoted – dismissed or they’ve bucked their ideas up – nobody’s ever been demoted’ (FLM, Site 2). By insisting on FLM action against staff, senior management consciously attempted to break the ties between FLMs and lower grade employees. The organisation redefined the relationship between FLMs and staff to make clear that: You’re not their friend; you’re their manager and that’s what we pay you to do … not finding excuses for people you actually happen to get on with … So it made it a level playing field, although that playing field had been reduced so far down that we were all playing well below sea level. (FLM Site 2)

The second limitation was that resistance did not extend to all FLMs. The growing pressure on FLMs from those above was having an effect. FLMs were fearful that: ‘If I don’t do this, somebody’s going to be coming along to check up on me, so I’d better do it’. And gradually, piece-by-piece, their own personality basically is disappearing because you’ve got to come in and do what it tells you and look at the instructions and follow the instructions, and don’t really think outside that. (FLM, Site 2)

As another FLM indicated that FLMs are being alienated from their teams and drawn into conflict: ‘Some of the managers are caught in the cleft now, because the staff are looking for them to be the buffer and they can’t be the buffer any longer, and that becomes problematic’ (FLM, Site 1).

Fear was not necessary for some to adopt the new ethos, however. At all sites, interviewees remarked on how the cultural change has seen the emergence of a new layer of managers, particularly as ‘a lot of the people, who … didn’t want to experience the Lean existence, took the option of early retirement’ (FLM, Site 2). Staff with different attitudes and backgrounds replaced experienced FLMs: ‘They’ve come from Customs, they’ve come from Tax Credits, they’ve never done the job, they’ve never read a technical memo’ (FLM, Site 6 Do you operate Lean as Lean should be operated? Are you a supporter of problem solving? Are you a supporter of this? Are you a supporter of that? Do you go to lots of meetings that take you away from your desk? (FLM, Site 2)

Nor are these criteria for promotion restricted to lower managerial positions: We had members of staff who were seconded to the Lean team and trained up as consultants, and out of the 19 promotions or 20 promotions that we had to HO [Higher Officer], I’d say at least 15 of them were actually known as really big supporters of Lean. (Branch Committee member, Site 5)

These developments have profoundly damaged the confidence of managers, their social relations and their attitudes towards the union.

FLMs, the labour process and trade unionism

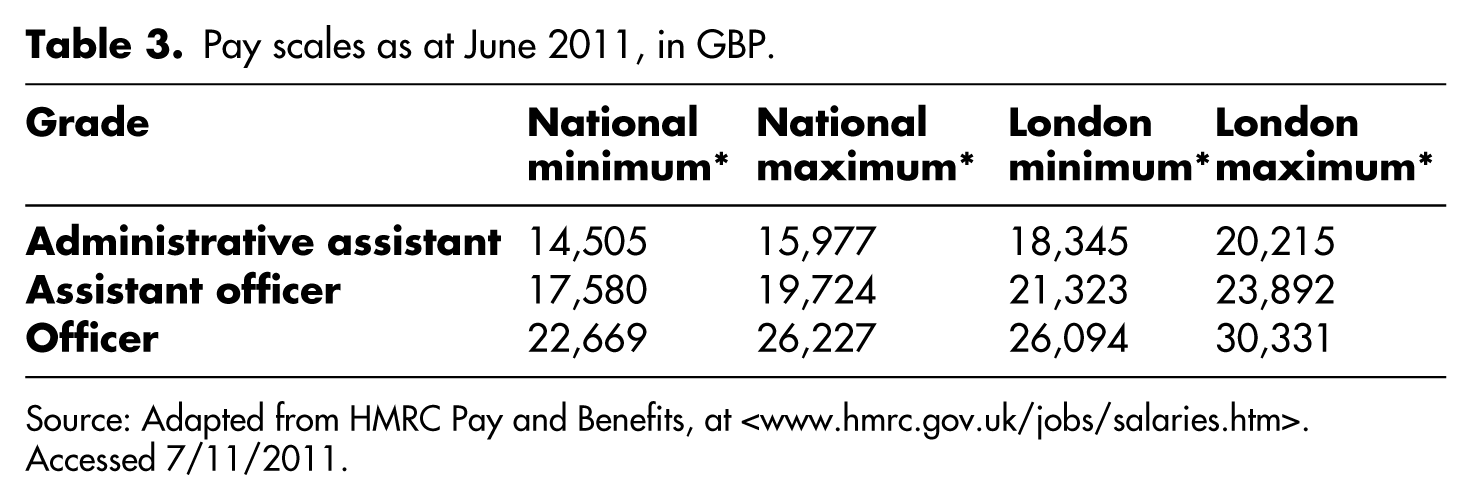

The changed balance within FLMs’ work, and the generational shift in those promoted, has potentially significant consequences for the culture of the workplace and, specifically, the ability of the union, PCS, to maintain membership and unity. Overall density of the union amongst the grades it represents is more than 80 per cent, and includes a high number of FLMs, including some who are trade-union representatives. That FLMs belonged to the union is not surprising. The majority were traditionally drawn from the AO grade that they supervised, their pay continued to be negotiated by the union, and the pay premium, although significant, changed insufficiently to explain on its own a fracturing of FLM interests ( Table 3 ).

Pay scales as at June 2011, in GBP.

Source: Adapted from HMRC Pay and Benefits, at <www.hmrc.gov.uk/jobs/salaries.htm>. Accessed 7/11/2011.

Management initiatives associated with Lean threaten to disrupt this settlement. Union opposition to Lean initially appeared antagonistic to the FLMs responsible for implementing it. FLMs’ resulting ambivalence to the union moderated subsequently, as they turned to it to represent them when experiencing difficulties with other members. One representative talked of FLMs asking: Can you represent me in this meeting? Because this person is saying that I’m not implementing the rules properly and that I’m having a go at them, when really I’m just doing my job … they might believe you because they’re not believing me (laughing). (FLM representative, Site 2)

Not all implementation of Lean was as consciously even-handed, in part because, as the managerial regime hardened, union-orientated FLMs found themselves isolated within management ranks: We had a case … tantamount to bullying for a management grade who doesn’t toe the party line on the Lean front, who actually wants to use their own common-sense and run a team sensibly, being made to feel very bad. They’re really ostracised. (Branch Committee member, Site 5)

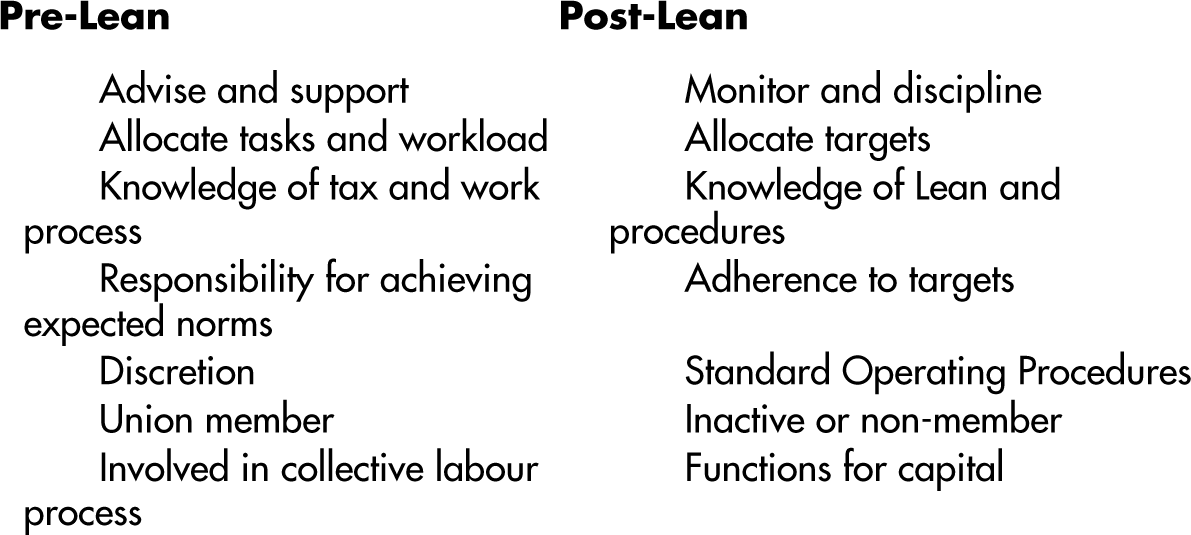

As a result of senior management attitudes, many FLMs were unwilling to enter into conflict with peers and senior managers, and appear much closer to the ideal-typical post-Lean manager, concerned with targets, monitoring and discipline (

Figure 1

), that the changes were designed to create. The effects of this attempted transformation are uneven, but were particularly pronounced in the case of new FLMs. Their lack of experience and the fact that their training was minimal coloured relations with those they supervised. One manager stated: I still feel that you cannot manage a task unless you actually understand the task. It’s no use me saying that this is an achievable target unless I’m willing to sit down and show you that it is, and if I can’t sit down and do that, then I think you lose a bit of credibility with the staff you’re managing. (FLM, Site 2)

Ideal-typical manager, Pre- and Post-lean.

This evaluation is borne out by the perceptions of those supervised: ‘How can they tell me how I’m going wrong in my job when they don’t know how to do the job themselves’ (Focus Group member, Site 5). The lack of substantive knowledge of work being supervised places managers in an invidious position, reducing them to invoking, and mechanically following, procedures even where they are inappropriate. One FLM expressed the resulting attitude as: ‘You’re going to respect me because I’m going to implement these rules. I’ve nothing else to hide behind, so I will hide behind these’ (FLM, Site 2). The failure to defend teams against excessive demands in turn lowered cooperation and exacerbated teams’ disillusionment and hostility. The cycle of distrust increased FLMs’ reliance on the delegated authority from higher management, and as a consequence, in one manager’s judgement, ‘They just do as they’re told’ (FLM, Site 6). At separate sites, those supervised by the new generation of FLMs caricatured many of them as ‘Lean zealots’ and ‘Lean robots’.

The erosion of managers’ independence, substantive knowledge and confidence, and the growing hostility and friction with their teams, have significant implications for the trade-union orientation of the new breed of FLMs. Without the respect of their teams, and increasingly dependent on positional authority, they are unlikely to contradict higher management or be amongst those retaining membership and requesting help from the union: An increasing number of managers … are moving away from PCS as a point of support, and once they lose the support element of the union then there isn’t a great deal left, because they’ll get the [union negotiated] pay rises … you may as well save your money. (FLM, Site 2)

Earlier work on white-collar trade unionism noted the different preoccupations from manual trade unionism of some groups and located the causes as being related to social class at the workplace (Carter 1985). Within the present context at HMRC, it is not difficult to envisage pressure for separate FLM organisation.

Conclusion

The changes associated with Lean have assumed particular prominence within HMRC, and the organisation has been used to champion similar ones throughout the Civil Service and beyond. The significance of the analysis here, therefore, goes beyond one government department. Lean brought with it a marked change in the work of FLMs as the balance of their tasks moved from support and advice towards greater supervision and monitoring. Earlier studies on front-line managers stressed the long-term diminution of their powers as managerial hierarchies were extended. In reaction to this perspective, Rose et al. maintained that while some aspects of their traditional role had been lost, they still held on to task allocation and decisions about pace and intensity of work, unequivocally concluding, ‘First-line supervisors under advanced capitalism are neither rendered progressively less powerful nor less authoritative’ (1987: 20). This conclusion has not been borne out in HMRC, where all these powers have been removed and, although some power over labour has superficially increased, it is less independent and more clearly subject to control from above. Nor has Hassard et al.’s (2009) contention that there have been massive increases in the scope and scale of their managerial roles been substantiated. Under Lean, they have less discretion and utilise fewer skills, with their roles neither having, nor requiring, substantive knowledge of taxation issues.

The widespread introduction of targets under the auspices of Lean has resulted in reconfiguring the roles of supervision, disciplining their practice, weakening their ties with labour, and sharpening conflict. Changes in the labour process represented an attempt to tie FLM roles more tightly to the interests of the state as employer, with a number of consequences for their social relations at work. As FLMs performed less direct tax work and, in Marx’s conceptualisation, progressively less work of coordination and unification, their social and economic roles moved from contributing within the labour process, as part of collective labour, to non-labour. Procedural changes increasingly required them to perform tasks associated with the function of capital, namely supervision and control designed to extract more surplus from those under their immediate control.

These processes validate Carchedi’s perspectives. The fact that there are few authors applying them empirically is more to do with theoretical disagreement than the impossibility of so doing. Nor does conceptualising class through social roles in production leads to an inevitable embrace with a ‘sterile functionalist project’ (Smith and Thompson 1999). The transformation of the work of FLMs was neither even nor automatic, and has been met with varying responses, from opposition to opportunistic identification. Experienced FLMs, with confidence in their knowledge of both substantive issues and the processes and rhythms of tax collection, have not accepted hourly targets as legitimate, and have been reluctant to place unfair pressure on the staff beneath them. Similarly, in the face of mandatory reporting of absences and action taken to curtail them, they have done their best to mitigate the effects of procedures and to retain some exercise of judgement. Other FLMs reluctantly complied with the imposition of Lean, aware that they themselves were now exposed and subject to performance monitoring. A third response, from a group largely comprising younger, inexperienced FLMs, embraced Lean, volunteered for problem-solving events, accepted its mantras, and have been rewarded by rapid promotion.

Some FLM discontent with Lean was evident, but discontent was amplified in the wider workforce suffering from work intensification and greater levels of stress and illness – outcomes closely related to the changed nature of supervision. The concerted attempt to detach FLMs from the rest of the workforce and to transform them into unambiguous agents of higher management through enforcing their monitoring and supervisory roles has generated more antagonistic social relations with their teams. FLMs traditionally came from the groups they subsequently supervised, and brought with them understanding of the work, sympathy with workers and common union membership. Union membership was underpinned by these histories, and the now different routes into management risk making union membership if not untenable, then at least unlikely. The new roles primarily consist of the function of capital, and with FLMs’ role in the labour process weakened and confidence eroded, it is difficult to envisage the bases of effective union action.

These developments give rise to a paradox. In most class schemas, from Weber (1958) through to those influenced by Bourdieu (1986), non-economic capitals, skills, specialist knowledge and discretion are markers for membership of the middle class, and the loss of these features signals a proletarianisation process. In contra-distinction, using Carchedian perspectives, the experiences of FLMs in HMRC highlight both a de-skilling and a significant removal from the labour process, strengthening functions on behalf of capital and thus further incorporation into a new middle class. By so characterising this movement, the analysis connects their roles in the generation of surplus with their changing interests and identities. There are problems and contradictions in these developments: it is far from clear, for example, that any of the supposed productivity benefits claimed are real or realisable (Carter et al. 2013a), and the removal of skill and initiative from FLMs will not help in this regard. Nevertheless, in so far as concerted and effective workplace organisation, and wider social opposition, to government and employer offensives are absent, Britain’s period of austerity and employment loss may well encourage similar experiences, with class relations changing and polarising at the point of production, and processes escaping scrutiny as the sociology of class absents itself from the workplace.

Footnotes

Acknowledgements

We would like to thank PCS representatives and officials for their cooperation with the research, and the union nationally for funding the survey and transcription costs. Conclusions and any errors are solely our responsibility.