Abstract

Using a stakeholder engagement perspective, we investigate the collective influence of institutional investors on a comprehensive set of climate change disclosures for a global sample of large companies. The proposition tested in this paper is that the influence of these powerful stakeholders is positively associated with climate change disclosure via corporate communications channels. We find the extent and quality of climate change disclosures to be associated with three indicators of corporate responsiveness to institutional investor expectations about the disclosure of this information. These are completion and publication of the Carbon Disclosure Project (CDP) questionnaire on CDP’s website, indications in corporate communications that CDP activities have influenced climate change disclosures, and the extent and quality of climate change information provided in CDP questionnaire responses.

1. Introduction

This research investigates the influence of institutional investors on corporate disclosure of information about climate change. Climate change disclosures include those about: regulatory, physical and other risks and opportunities of climate change; greenhouse gas (GHG) emissions intensity and energy use; participation in emissions trading schemes; corporate governance and strategy in relation to climate change; and performance against GHG emissions reduction targets. While various regulatory requirements to disclose information about GHG emissions and risks related to climate change are emerging in some jurisdictions, 1 change related disclosure in annual and/or sustainability reports or on company websites remains largely voluntary.

Using a stakeholder engagement perspective, we investigate the collective influence of institutional investors using a comprehensive set of climate change disclosures for a global sample of large companies. Institutional investors represent a powerful and legitimate stakeholder group for companies in which they hold substantial shareholdings. They are also a group that has expressed a desire for high quality information about corporations’ exposure to risks associated with climate change (Lash and Wellington, 2007; Smith et al., 2008; Stanny and Ely, 2008). Indeed, Smith et al. (2008) conclude that the response of institutional investors to voluntary, market-based disclosure initiatives indicates that investor demands for climate disclosure has driven private action faster than either regulators or politicians have addressed the underlying issues. Further, the PRI Association and UNEP Finance Initiative (2010: 2) state:

Large institutional investors are in effect ‘universal owners’, as they often have highly-diversified and long-term portfolios that are representative of global capital markets. Their portfolios are inevitably exposed to growing and widespread costs from environmental damage caused by companies. They can positively influence the way business is conducted in order to reduce externalities and minimise their overall exposure to these costs. Long-term economic wellbeing and the interests of beneficiaries are at stake. Institutional investors can, and should, act collectively to reduce financial risk from environmental impacts.

Collective action by institutional investors in relation to climate change disclosure has been spearheaded by the Carbon Disclosure Project (CDP). This independent, not-for-profit organization represents 534 institutional investors with over US$64 trillion in assets under management. It collects climate change data from approximately 3000 companies around the world by asking them to complete it its questionnaire. This questionnaire was sent to 4500 companies globally in 2010. The CDP can be seen as a ‘secondary stakeholder’ that has facilitated collaborative engagement by institutional investors to increase corporate accountability in relation to climate change (Arenas et al., 2009). CDP is a recent initiative that is global, represents a large coalition, and addresses the climate change concerns of institutional investors. It seeks greater transparency from companies and uses corporate engagement as its preferred form of interaction (Hebb, 2008). 2

In this paper we argue that the influence of institutional investors has increased expectations on companies to disclose climate change information, not only by responding to the CDP questionnaire but also via primary corporate communications channels such as annual and sustainability reports and company websites. We investigate to what extent and in what ways institutional investors influence climate change disclosure by large companies.

We commence our analysis by describing the nature, extent and quality of climate change disclosures by non-financial companies included in the Global 500 index. We use a comprehensive measure of disclosure that captures the extent and quality of climate change information, and are able to breakdown this measure into its component parts to glean insights about the nature of corporate climate change disclosures. While there have been several recent research articles investigating climate change disclosures made via responses to the CDP questionnaire (Kolk et al., 2008; Luo et al., 2010; Peters and Romi, 2009; Stanny, 2010; Stanny and Ely, 2008), climate risk disclosures by US companies in 10-K reports (CERES, 2009; Doran and Quinn, 2009), and the quantity of disclosure for a broader set of climate change disclosures in annual and sustainability reports (Freedman and Jaggi, 2005; Prado-Lorenzo et al., 2009), ours is the first known study to examine the extent, quality and nature of a comprehensive set of climate change disclosures for a sample of large global companies. This comprehensive, global approach allows us to (1) overview international reporting practices related to a broad set of corporate climate change disclosures, (2) identify which aspects of these disclosures are falling short of investor expectations and regulatory intervention is therefore most likely to be needed, and (3) explore sectoral and country differences in these disclosures.

Next, we test hypotheses about the relationship between institutional investor influence and corporate climate change disclosure. We capture this stakeholder influence using three measures of corporate responsiveness to institutional investor expectations about the disclosure of climate change information. The first indicator of institutional investor influence occurs when a company chooses to complete the CDP questionnaire and consents to its response being published on the CDP website. Next, we examine annual and sustainability reports and company websites for indications that institutional investor expectations have influenced corporate climate change disclosures. There are a variety of ways in which companies can indicate the influence of CDP activities on their disclosures ranging from making a statement in their annual or sustainability report that they have participated in CDP activities through to providing their full CDP questionnaire response on their company website. The third indicator relates to the extent and quality of climate change information that a company includes in its CDP questionnaire response. While some companies report extensive information about several aspects of climate change impacts, others are less forthcoming in their responses (Kolk et al., 2008; Stanny, 2010). The results support all three hypotheses, thus confirming the important role of institutional investor engagement in relation to climate change disclosure.

Our examination of the relationship between institutional investor influence and corporate climate change disclosure extends the literature on the determinants of climate change disclosure. Previous research has investigated a range of factors potentially associated with climate change disclosures including company size, leverage, profitability, shareholder resolutions, regulatory threats, economic consequences, and several factors related to specific sectors and countries (Freedman and Jaggi, 2005; Luo et al., 2010; Peters and Romi, 2009; Prado-Lorenzo et al., 2009; Reid and Toffel, 2009; Stanny and Ely, 2008). However, the influence of institutional investor engagement activities has not been previously examined. Our finding of a highly significant relationship between institutional investor influence and climate change disclosure supports the tenets of stakeholder theory and demonstrates the potential for this powerful and legitimate stakeholder group to influence corporate disclosures. We control for several other factors found to be associated with these disclosures in prior research, thereby demonstrating the importance of institutional investor influence over and above these other factors. A final contribution of this research relates to the growing body of literature on stakeholder engagement. Our study extends this area of research by investigating and finding support for the role of collaborative shareholder engagement in relation to climate change disclosures. Our research provides robust empirical evidence in support of claims in the literature that institutional investor demand can drive corporate action.

The remainder of our paper is organized as follows. The next section reviews the prior literature and develops the hypotheses for the study. Section 3 outlines the data and our method. Section 4 presents the results of the analysis and Section 5 concludes.

2. Literature review and hypotheses development

2.1 Prior literature

Corporate disclosure of climate change information is a growing area of research interest. Recent studies have investigated (a) the disclosure of climate change risks and opportunities, (b) a broader set of climate change disclosures in annual and sustainability reports, and (c) disclosures made in responses to the CDP questionnaire.

Disclosure of climate change risks and opportunities is the topic of two recent studies. Doran and Quinn (2009) analyse the climate change related risk disclosure trends in Standards and Poor’s 500 (S&P’s 500) from 2000 to 2008. They show that despite management knowledge about the risk created by climate change and its physical and financial impacts, about 76.3% do not report these risks in their annual filings. Similarly, CERES (2009) find that the majority of their sample of 100 global companies do not disclose any GHG or climate change risk information in 2008, and the quality of information reported was at best ‘fair’. These two studies do not investigate other types of climate change disclosures such as those related to GHG emissions and their management.

Freedman and Jaggi (2005) and Prado-Lorenzo et al. (2009) investigate several factors related to a broader group of annual and sustainability report disclosures of GHG emissions and the effect of climate change on corporations. The focus of Freedman and Jaggi’s (2005) research is the impact that ratification of the Kyoto protocol has on climate change disclosures. They find that companies from countries that ratified the Protocol have higher disclosure indexes compared to companies in other countries. Their self-constructed disclosure index captures five categories of disclosure expected to capture the Protocol-related disclosures and is developed based on both equal and differential weighting schemes. Prado-Lorenzo et al. (2009) examine a variety of factors associated with climate change disclosures of Fortune 500 companies. They find positive associations with company size and market capitalization and a negative association with profitability. These researchers construct an unweighted index of 19 items to capture the quantity of climate change information disclosed. However, the quality and nature of the disclosures is not considered as part of their index.

Several authors have investigated the determinants of corporate responses to the CDP questionnaire and the extent and type of information included in these responses. Kolk et al. (2008) examine the rate of response to the CDP questionnaire and the type of information disclosed. They conclude that CDP has achieved considerable success in terms of response rates; however, there is little evidence of successful value commensuration. Stanny and Ely (2008) and Stanny (2010) investigate the determinants of disclosures made by US firms in their responses to CDP. Stanny and Ely find that the propensity to respond to the CDP questionnaire is related to company size, previous disclosures and foreign sales. Stanny (2010) documents that while there is a high rate of response to the CDP survey, there is a low rate of disclosure of detailed information about carbon emissions and the strategies to deal with climate change. She interprets this disclosure behaviour as support for legitimacy theory.

In the global context, Peters and Romi (2009) investigate country differences in responses to CDP across 28 countries. They find that the level of disclosure in CDP responses is related to the environmental regulatory stringency of the government, the environmental responsiveness of the private sector and the market structure of each country. Reid and Toffel (2009) explore corporate responses to shareholder activism and find that companies that have been targeted, and companies in industries in which other companies have been targeted, by shareholder actions on environmental issues are more likely to publicly disclose information to the CDP. They also find that companies that operate under carbon emission trading laws or in countries with proposals to issue new emissions constraint laws have higher emissions disclosure levels than their counterparts from other countries.

A recent study by Luo et al. (2010) also considers responses to CDP in the global context. They investigate the impact of economic, regulatory, social and financial market factors on voluntarily disclose of GHG emissions information to the CDP by Global 500 companies. They find that these disclosures are related to company size, belonging to a carbon intensive sector, being in a country that has an ETS and/or a common law country. On the other hand, they find that GHG emissions disclosures to CDP are not related to leverage or capital raisings. This final result is interpreted as evidence that emissions disclosures are not driven by market factors. These authors conclude that the major driving force for climate change disclosure comes from the general public and government, rather than other major stakeholders such as shareholders and debtholders. This interpretation contrasts with several previous studies that conclude that climate change is starting to play a decisive role in investment decisions processes (Lash and Wellington, 2007; Schultz and Williamson, 2005; Smith et al., 2008).

While the decision to respond to the CDP questionnaire and consent to the response being made publically available represents a form of corporate disclosure, this is quite different to the voluntary disclosure decision to include this type of information in corporate communications such as the annual or sustainability report. In this study we focus on climate change disclosures made in corporate communications, and how this is influenced by the activities of CDP in collaboration with institutional investors.

2.2 Theory and hypotheses

Our hypotheses about the relationship between institutional investor influence and corporate climate change disclosures are underpinned by stakeholder theory and the process of collaborative shareholder engagement. Stakeholder theory typically views the world from the perspective of the management of the organization who are concerned strategically with the continued success of the company (Roberts, 1992; Ullmann, 1985). From this perspective, a company′s continued existence needs the support of its stakeholders and their approval must be sought and the activities of the corporation adjusted to meet their expectations. While legitimacy theory considers the overall society and its role in organizational legitimacy, stakeholder theory explains the role of particular stakeholders in shaping management strategies.

The more powerful the stakeholder, the more prepared the company must be to adapt to meet the stakeholder’s expectations. That is, firms take actions in order to fulfil the expectations of particular stakeholders who have the power to impact on their performance (Deegan, 2009). Mitchell et al. (1997) propose three overarching attributes that contribute to stakeholder salience: power, legitimacy and urgency. The more important the stakeholder to the organization, the more the consideration given to managing and dealing with this stakeholder (Gray et al., 1996). Corporate disclosure is seen as part of the dialogue between the company and its stakeholders (Roberts, 1992). Companies have incentives to disclose particular information to salient stakeholders in order to demonstrate to them that they are complying with their expectations.

From the perspective of institutional investors, active ownership through corporate engagement activities represents a compelling force in representing owners’ interests in companies (Hebb, 2008). Institutional investors holding large equity positions are vulnerable to the performance of the market as a whole, i.e. they are ‘universal owners’ and thus have an incentive to reduce risks. Indeed, ‘corporate engagement is a legitimate use of the owners’ rights in a company to provide oversight and protect shareholders’ (Hebb, 2008: 7). Activist owners seek greater accountability to shareholders, transparency and a higher standard of corporate behaviour (Hebb, 2006). Rather than asking companies to sacrifice long-term profitability, shareholder engagement seeks higher corporate standards in order to reduce risk over time, thus adding to shareholder value (Clarke and Hebb, 2004). Gifford (2009) studies the factors that drive effective shareholder engagement and finds that power and legitimacy are critical to stakeholder salience. Institutional investor legitimacy derives from being a credible and respected mainstream institution, with a legitimate claim on the company such as a large shareholding. Shareholder engagement is a new and developing tool that has the ability to significantly influence and raise standards of corporate disclosure (Clarke and Hebb, 2008; Hebb, 2006).

The stakeholder engagement perspective is particularly relevant when considering corporate social responsibility (CSR) and disclosures about it since it concerns a broader group of stakeholders and set of issues than tend to be considered by alternative perspectives such as agency theory. CSR is a broad concept that includes both social and environmental issues, including climate change. Cormier et al. (2004) argue that managers’ perceptions about stakeholders’ interests are a key determinant of environmental and social disclosure practices. They attribute this to ‘an intrinsic commitment’ from managers toward stakeholders. In addition, van der Laan et al. (2005) affirm the stakeholders’ role in determining the extent and quality of social disclosure. There are several stakeholder groups that are potentially interested in corporate accountability related to climate change. However, we focus on institutional investors since they represent a particularly powerful and legitimate stakeholder group in this setting. While CSR suggests that companies respect all their stakeholders, the shareholder engagement perspective concerns itself solely with the long-term interests of shareholders (Gifford, 2009; Hebb, 2008).

Institutional investor coalitions have a unique opportunity to influence and engage corporate management. Indeed most institutional investor coalitions use some form of corporate engagement to achieve their goals (Clark and Hebb, 2004; Hebb, 2008). Collective action by institutional investors in relation to climate change disclosure has been spearheaded by the CDP. The CDP can be seen as a ‘secondary stakeholder’ that has facilitated collective action by institutional investors to increase corporate accountability in relation to climate change. The research confirms that secondary stakeholders, such as non-government organizations (NGOs), are key players in the arena of CSR (Arenas et al., 2009). These authors find that NGOs are usually recognized by other stakeholders as one of the main actors who are often at the forefront in the introduction and development of CSR. Some NGOs are perceived by companies as being important stakeholders, while other stakeholders recognize that pressure from some NGOs has led to an improvement in corporate behaviour. CDP is arguably an NGO that holds this status among large companies and other stakeholders, particularly institutional investors. The collective action of institutional investors in concert with the CDP represents a powerful coalition of stakeholders that we expect to have an influence on corporate climate change disclosure.

We capture this stakeholder influence using three measures of corporate responsiveness to institutional investor expectations about the disclosure of climate change information. The first indicator of institutional investor influence occurs when a company chooses to complete the CDP questionnaire and consents to its response being published on the CDP website. Completing the questionnaire is voluntary and demonstrates a willingness to share climate change information with institutional investors that are part of the CDP coalition. It is a direct response to the explicit expectations of a powerful and legitimate shareholder collaboration. Further, consenting to having its CDP response published on the CDP website shows a responsiveness to the expectations of a wider group of stakeholders since this consent essentially puts the information into the public arena. The influence of institutional investors on the extent and quality of corporate climate change disclosure is therefore expected to be greater for companies that complete the CDP questionnaire and consent to their response being published on the CDP website. This expectation is formally stated in Hypothesis 1:

H1: Companies that complete the CDP questionnaire and consent to having their response published on the CDP website have higher climate change disclosure scores than companies that choose not to participate in CDP activities.

Second, we examine annual and sustainability reports and company websites for indications that institutional investor expectations have influenced their climate change disclosures. There are a variety of ways in which companies can indicate the influence of CDP activities on their disclosures ranging from making a statement in their annual or sustainability report that they have participated in CDP activities through to providing their full CDP questionnaire response on their company website. Including such disclosures in their corporate communications is viewed as prima facie evidence that CDP activities have influenced climate change disclosure. By indicating their response to CDP, companies convey a message to investors, and simultaneously to other stakeholders, that they are complying with and fulfilling investors’ expectations. The expectation of detailed and transparent climate change related information has been communicated by investors (through the CDP information request), and this also conveys an expectation that this issue will be given more attention and be addressed by management. One aspect of doing this is enhancing disclosure practices in an effort to improve the relationship between management and external stakeholders (Roberts, 1992; van der Laan Smith et al., 2005).

Statements about participation in CDP activities are likely to be complementary to disclosures about particular climate change impacts and risks, whereas the inclusion of the full CDP questionnaire response is likely to be a substitute for providing more detailed information in the annual or sustainability report. On the other hand, including a link to the CDP website publication of a company’s full CDP response may serve as either a complement or substitute for other disclosures. For the majority of companies we expect that this relationship will be complementary since the provision of a link to the CDP questionnaire response provides the reader with additional information that may be considered too detailed or extensive to include in the annual or sustainability report. Overall, we propose a complementary relationship between explicit indications of the influence of CDP and the extent and quality of corporate climate change disclosure, stated formally in the following hypothesis:

H2: For companies that complete the CDP questionnaire, those that indicate the influence of CDP activities in their corporate communications have higher climate change disclosure scores than those that do not mention CDP.

The final indicator relates to the extent and quality of climate change information that a company includes in its CDP questionnaire response. While some companies provide extensive information about several aspects of climate change impacts, others are less obliging in their responses to CDP (Kolk et al., 2008; Stanny, 2010). The incorporation of detailed and useful information in a company’s response to CDP is an indication that it takes the expectations of this powerful and legitimate shareholder coalition seriously, and is therefore prepared to adjust its behaviour accordingly. We expect that those companies that are most responsive to institutional investors as indicated by a willingness to provide a comprehensive CDP questionnaire response will also be the most forthcoming in their voluntary disclosure practices. This hypothesis can be formally stated as follows:

H3: For companies that complete the CDP questionnaire, there is a positive relationship between climate change disclosure scores based on their CDP response and those based on disclosures made via corporate communication channels.

3. Data and method

3.1 Sample selection and data collection

The sample for this research is taken from the largest 500 companies in the FTSE Global Equity Index Series (G500) as of June 2009. This index comprises the largest 500 companies globally, ranked by sales. While it is clear that this sample is biased toward very large companies, it is justified in the context of this research since large companies are likely to have substantial shareholdings by institutional investors. Indeed, these ‘universal owners’ tend to have highly diversified and long-term portfolios that are representative of global capital markets, thus making the G500 an eminently suitable group of companies for this research. In addition, disclosure practices (especially environmental disclosures) of large companies are richer than small and medium sized companies (Deegan and Gordon, 1996; Patten, 1991).

One hundred and ten companies from the financial sector were excluded from the G500 for this research since companies in this sector are intrinsically different to those in other sectors and have different reporting requirements. A further 34 companies were excluded because they were acquired, they completed the CDP questionnaire in a language other than English or they were not included in the 2008 CDP Global 500 sample. Hence, the final sample for the research comprises 356 large global non-financial companies.

Data related to corporate climate change disclosures were hand collected from annual and sustainability reports and company websites, with these company reports being accessed either via Bureau van Dijk’s OSIRIS database or directly from company websites. The annual and sustainability reports accessed for each company were the most recent reports available as at June 2009. For the majority of our sample these were the reports dated at the end of either June or December 2008. Data related to CDP questionnaire responses and disclosure scores were obtained from the 2008 CDP Global 500 Report and the CDP website. Companies are asked to respond to the questionnaire at the beginning of each year, with a submission closing date of 31 May. Hence companies responding to the 2008 CDP questionnaire do so before finalizing their annual and sustainability reports for that year. Data for control variables were acquired from the OSIRIS database.

3.2 Calculation of climate change disclosure scores

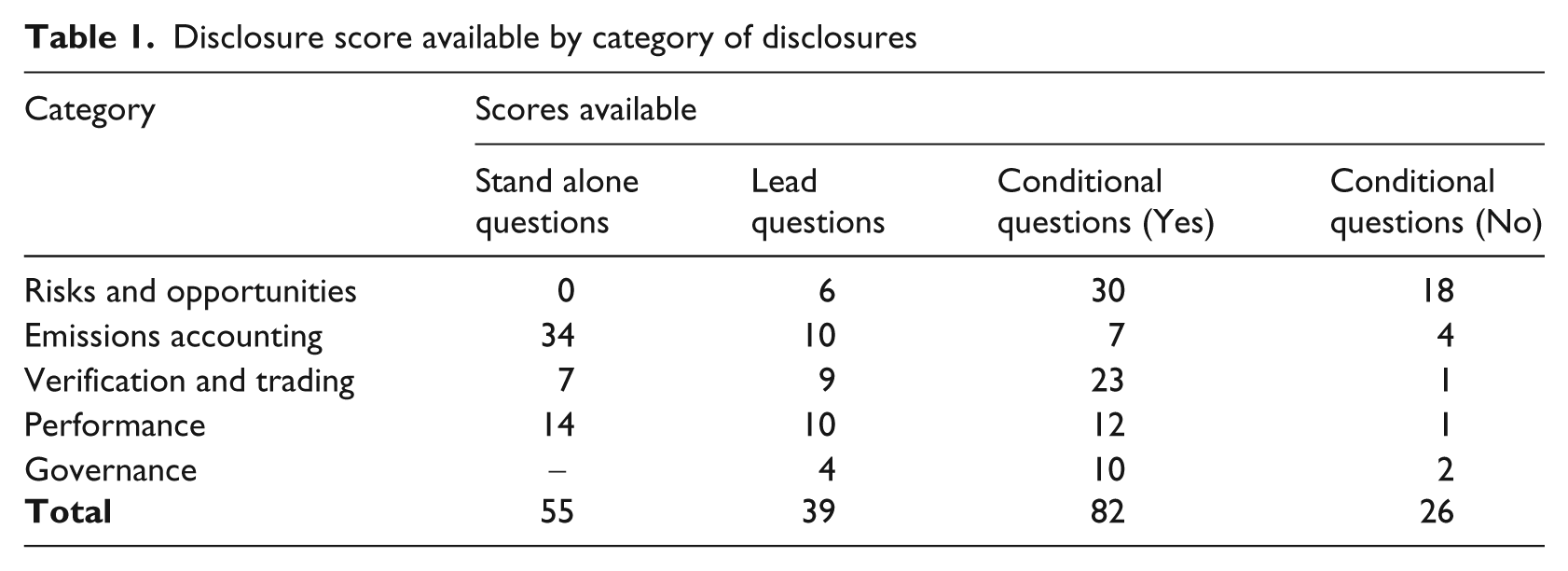

We calculate a climate change disclosure score based on the annual and sustainability reports as well as disclosures made via websites for each company in the sample. Content analysis is used to analyse the sample companies’ annual and sustainability reports. A scoring (or indexing) approach is employed since this method incorporates an analysis and interpretation of the meaning of the disclosures (Beck et al., 2010; Cormier et al., 2005). In addition, this type of approach overcomes some of the limitations that are inherent in volumetric approaches such as ‘green washing’ problems (Al-Tuwaijri et al., 2004). Sub-scores are assigned for the following five categories of disclosure: risk and opportunities, GHG emissions accounting, verification and trading, emissions management performance and climate change governance.

This research uses the Carbon Disclosure Leaders Index (CDLI) 2009 methodology to calculate disclosure scores. This is the scoring methodology used by CDP to identify companies for inclusion in the CDLI. We use the 2009 CDLI methodology rather than the 2008 methodology since it incorporates some improvements that make it a superior methodology for scoring climate change disclosures. The decision to use the CDLI methodology has been made for several reasons. First, there is congruency between the objectives and outcomes of this score and the objective of this research. In particular, the CDLI methodology captures the issues that investors have indicated are most important since it is based on responses to the CDP questionnaire, which has been developed based on extensive consultation with institutional investors. Second, choosing an existing methodology increases the research’s external validity. Third, the CDLI methodology has been developed by experts and advisors from CDP and PricewaterhouseCoopers (PwC). Finally, and most importantly, the CDLI methodology focuses on specific information relevant to GHG emissions and climate change rather than simply counting the amount of information (words, lines or pages). For example, the methodology identifies and captures important aspects of climate change such as its financial implications, how its various impacts are being dealt with and the level of transparency around these issues. That is, this methodology considers the content and quality of disclosures in addition to the quantity.

The CDLI methodology uses a mixture of binary and weighted values to calculate a disclosure score that captures the extent and quality of information (Wiseman, 1982), and considers the importance and materiality of specific information to particular users. For the binary values, companies are given one point for answering particular questions regardless of the answer provided. For the weighted values, companies are scored based on various scales, and the scores assigned to each scale are different. These scales consider information quality in terms of: (a) the information details and relevance to the company, (b) examples or case studies provided, and (c) quantitative or financial information. The materiality or importance of particular information is considered by assigning a weighted number of points to different types of information (for example, total scope 1 GHG emissions data receives three points). Varying points are assigned depending on the disclosure type. For example, for disclosures about risk and opportunities, up to five points are assigned based on whether information provided is general, qualitative or quantitative, the relevance of information to the company and whether information about the financial implications of risks and opportunities is provided. Thus the total disclosure score captures the informativeness of a company’s disclosures (in terms of both the quality and quantity of the disclosure).

Table 1 illustrates the scores and how they are distributed between categories. The circumstances of each company are considered in the design of this methodology. Possible total scores range from 120 to 176 points depending on how each company answers the lead questions. That is, depending on whether a company answers yes or no to each lead question, different points are assigned to its answers to the following questions. For example, if a company has not taken action to independently verify and assure its information and has thus answered no to this question, it will not be scored zero because it did not answer the following questions such as the scope of verifications, the verification’s standards that it adopted and the assurance level that has been given to this company. In such cases, the company has to answer whether it has plans to have its carbon emissions information verified in future. The more lead questions that a company answers ‘yes’ to, the more conditional questions that the company will be required to answer, thus making the total possible score higher than for a company that answers ‘no’ to many of the lead questions.

Disclosure score available by category of disclosures

The disclosure score for each sample company was calculated by one of the paper’s authors and a random sub-sample of these was checked by the other author. No discrepancies were found. Each company’s actual score is divided by its possible score to derive a total disclosure score out of 100 for each sample company.

3.3 Independent variables

The hypotheses of this study predict relationships between the dependent variable, climate change disclosures made via corporate communication channels, and whether companies complete the CDP questionnaire and consent to their response being published on the CDP website (H1), explicit indications of the influence of CDP (H2) and CDP disclosure scores (H3). For H2 and H3, the relevant sub-sample for analysis is those companies that complete the CDP questionnaire, while the full sample is used to test H1.

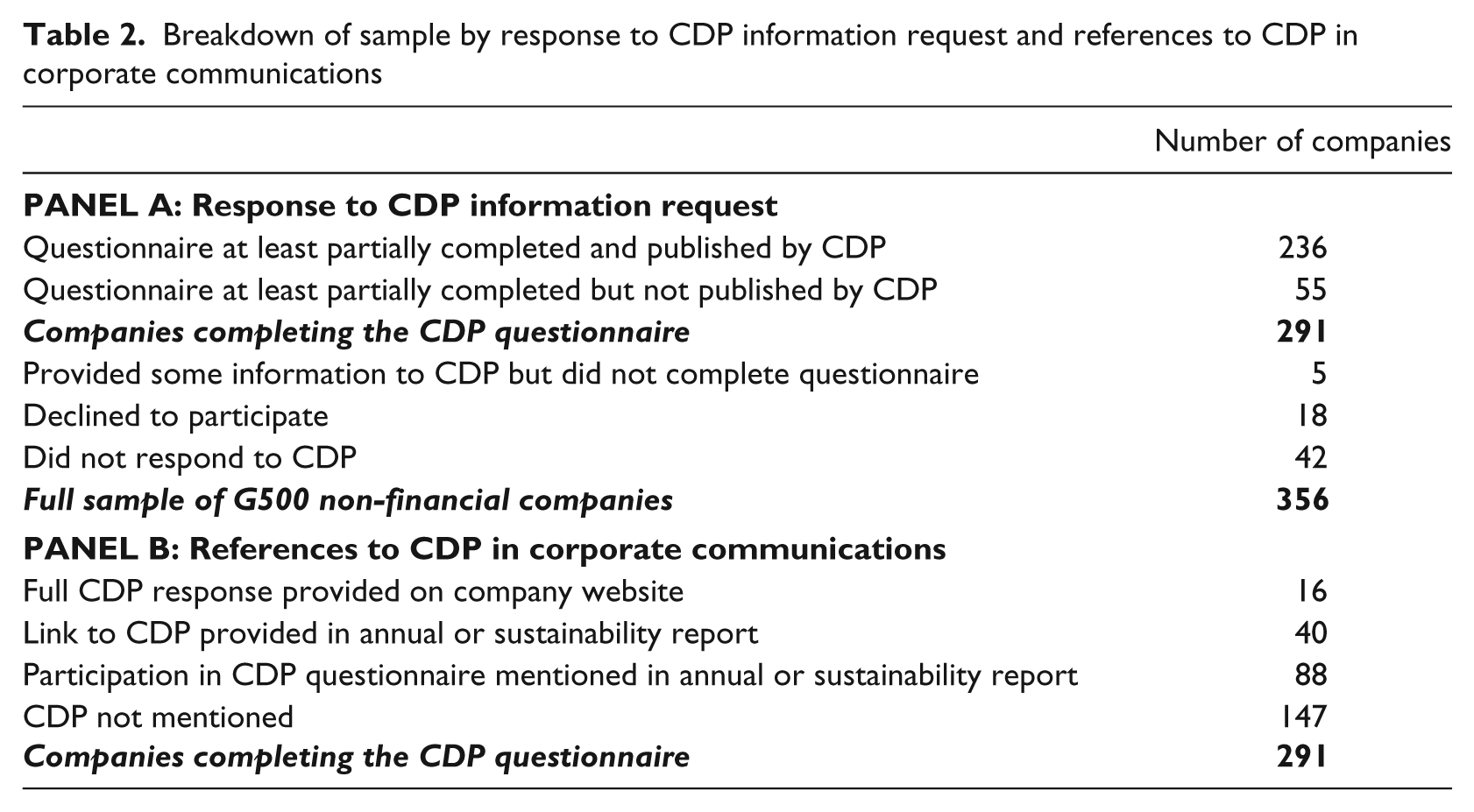

Table 2 shows the breakdown of the sample by (a) response to the CDP information request and (b) references to CDP in corporate communications. Out of the 356 companies considered for this research, 236 completed or partially completed the CDP questionnaire and consented to having their response published on the CDP website. A further 55 companies completed or partially completed the questionnaire but did not consent to having it published, thus giving a total of 291 companies at least partially completing the CDP questionnaire. Of the remaining companies, five provided some information such as their sustainability report to CDP but did not use the questionnaire. Eighteen companies declined to participate and 42 did not respond to CDP’s information request. These numbers attest to the potential influence of institutional investors in relation to climate change disclosure.

Breakdown of sample by response to CDP information request and references to CDP in corporate communications

Of the 291 companies that completed the CDP questionnaire, 16 provided their full CDP response on their company website and 40 provided a link to CDP in their annual or sustainability report. A further 88 companies mentioned their participation in CDP in their annual or sustainability report, while the remaining 147 companies made no reference to CDP in their corporate communications. Overall, 144 or 49.5% of the companies completing the CDP questionnaire made some sort of reference to CDP, thus providing an explicit indication that CDP activities influenced their climate change disclosure choices.

Of the 16 companies that provided their full CDP response on their company website, 11 did not make any other climate change disclosures elsewhere in their corporate communications. This suggests that, in the majority of cases, providing the full CDP response acts as a substitute for presenting climate change information in the annual or sustainability report. On the other hand, all of the 40 companies providing a link to CDP in their annual or sustainability report and all but one of the 88 companies mentioning their participation in CDP in their annual or sustainability report made at least some other climate change disclosures.

CDP disclosure scores are available from CDP for 245 of the sample companies. CDP and PwC staff members calculate CDP disclosure scores for all G500 companies completing the CDP questionnaire using their CDLI methodology. 3 However, only 68 companies are included in the index (CDLI 2008). These comprise the 34 G500 companies with the highest CDP disclosure scores from each of the carbon-intensive and non-carbon-intensive sectors.

3.4 Empirical model

The model used to test the hypotheses is:

where CCDISC is the climate change disclosure score and XCDP indicates the relevant independent variable used to test each of our hypotheses as follows:

H1 – completed and published CDP questionnaire

H2 – link to CDP website or CDP participation mentioned

H3 – CDP disclosure score.

Each of these independent variables is expected to be positively related to CCDISC.

The literature review presented in Section 2 shows that several variables have been recognized in prior research as potential drivers for disclosure practices. These variables are therefore included as control variables in this study. Several studies have posited a positive relationship between disclosure level and profitability on the basis that firms with superior income have a greater motivation to disclose their performance (Clarkson et al., 2008; Prado-Lorenzo et al., 2009). In addition, it is claimed that profitable firms tend to provide detailed disclosures in order to avoid public pressure and political and transaction costs (Inchausti, 1997; Ng and Koh, 1994). Return on total assets (ROA) is used as a proxy for firm profitability, and is calculated by dividing the profit or loss before taxes by total assets.

Numerous previous studies have controlled for firm size. Two dominant reasons explain this relationship. First, large firms are more capable of disseminating detailed information based on their resources. Second, these firms are susceptible to greater scrutiny from the public (Liu and Anbumozhi, 2009; Stanny and Ely, 2008). In relation to environmental disclosure, most of the prior literature finds that environmental disclosure is positively associated with firm size (Clarkson et al., 2008; Cormier et al., 2005; Freedman and Jaggi, 2005; Liu and Anbumozhi, 2009; Richardson and Welker, 2001; Stanny and Ely, 2008). More recently, Prado-Lorenzo et al. (2009) find that firm’s size is positively related to the disclosure of GHG emissions information. Firm’s size (SIZE) is estimated as the log of total revenues. Several prior studies have controlled for leverage on the basis that highly levered firms have an incentive to avoid agency costs which may be imposed by creditors (Clarkson et al., 2008), or to keep particular stakeholders (investors creditors) informed in order to avoid debt-covenant breaches (Freedman and Jaggi, 2005). Leverage (LEV) is measured as the sum of non-current liabilities and loans scaled by stockholders’ equity.

In addition, country and industry dummy variables are used to control for variations in regulatory requirements and other incentives to disclose that could be expected to vary across countries and sectors. Prior research has found that there are country and industry differences in societal or political pressures related to climate change (Freedman and Jaggi, 2005; Luo et al., 2010; Peters and Romi, 2009; Prado-Lorenze et al., 2009; Reid and Toffel, 2009). There may also be industry differences related to the extent of emissions data estimation uncertainty or proprietary costs around carbon reduction strategies and technologies for particular sectors.

4. Results

4.1 Descriptive statistics for climate change disclosure scores

The mean and median climate change disclosure scores for our full sample of 356 companies are 21.53% and 20.00% respectively, with a maximum of 94%. A score of zero was assigned to 45 companies that did not make any climate change disclosures in their corporate communications. The climate change disclosure scores for the 16 companies providing their full CDP response on their company websites are equal to their CDP disclosure scores and are substantially higher than the disclosure scores of other companies in the sample. To avoid potential biases in the results, these 16 companies are removed from the remaining analysis, thus leaving 340 companies in our sample for hypotheses testing, 275 of which completed the CDP questionnaire and 230 of which have a CDP score available. Once these 16 companies are removed, the mean and median climate change disclosure scores for our sample of 340 companies reduce to 19.09% and 19.00% respectively, with a maximum of 51%. These descriptive statistics are shown in Table 3.

Climate change disclosure scores for sample of 340 companies

When the five categories of disclosure are considered, ‘emissions accounting’ is the category with the highest mean and median scores, and ‘risks and opportunities’ is the category with the lowest scores. However, the maximum score possible varies between categories and, when this is taken into consideration, ‘governance’ is the area of climate change disclosure with the highest score relative to what is possible. ‘Risks and opportunities’ remains as the worst area of climate change disclosure. Indeed, 129 of the sample firms do not disclose anything about their climate change risks and opportunities. This compares with 54 that do not report emissions data, 85 that do not provide information about verification and trading, 79 that fail to report on their performance and 51 that do not provide detailed climate change governance information.

Total climate change disclosure scores stratified by country and industry are presented in Table 4. Panel A shows that UK companies are the clear leaders in climate change disclosure with mean and median disclosure scores both equalling 31%. The minimum UK score of 19% indicates that all UK companies in the sample made at least some climate change disclosures. Companies from other European Union (EU) countries rank second with mean and median disclosure scores of 26.39 and 26% respectively. The highest disclosure score of 51% is achieved by German company, Deutsch Post, while the second ranked company, Sony Co, is from Japan.

Climate change disclosure scores by country and industry for sample of 340 companies

Note: the maximum possible disclosure score is 100.

The industry classifications shown in Panel B of Table 4 are based on sector affiliation as defined by the Global Industry Standard Classification (GISC). 4 Sample companies are assigned to sectors based on their principle activities as determined by company revenues. Materials and utilities are the two industry sectors with the highest climate change disclosure scores, while industrials, energy, telecommunications and healthcare are the worst disclosing sectors.

4.2 Descriptive statistics for independent and control variables

Table 5 presents descriptive statistics for CDP disclosure scores and the control variables. Panel A of Table 5 shows that while our sample firms are all large in that they belong to the G500 and as indicated by mean and median revenues, there is substantial variation in total revenues with the minimum value being just US$1,340,000. Total revenues are logged for hypotheses testing (SIZE). ROA ranges from −31.05% to 40.66% with a mean of 8.63%, while the mean debt level is 1.21 times equity (LEV). The extreme minimum and maximum values shown for this variable are due to very low or negative equity values for seven sample firms. These extreme outlier values were trimmed to a value of 5, which reduced the extent of skewness for this variable. Slightly reduced sample sizes for return on assets (ROA) and leverage (LEV) are due to missing data for these variables.

Descriptive statistics for control variables and CDP disclosure scores for sample of 340 companies

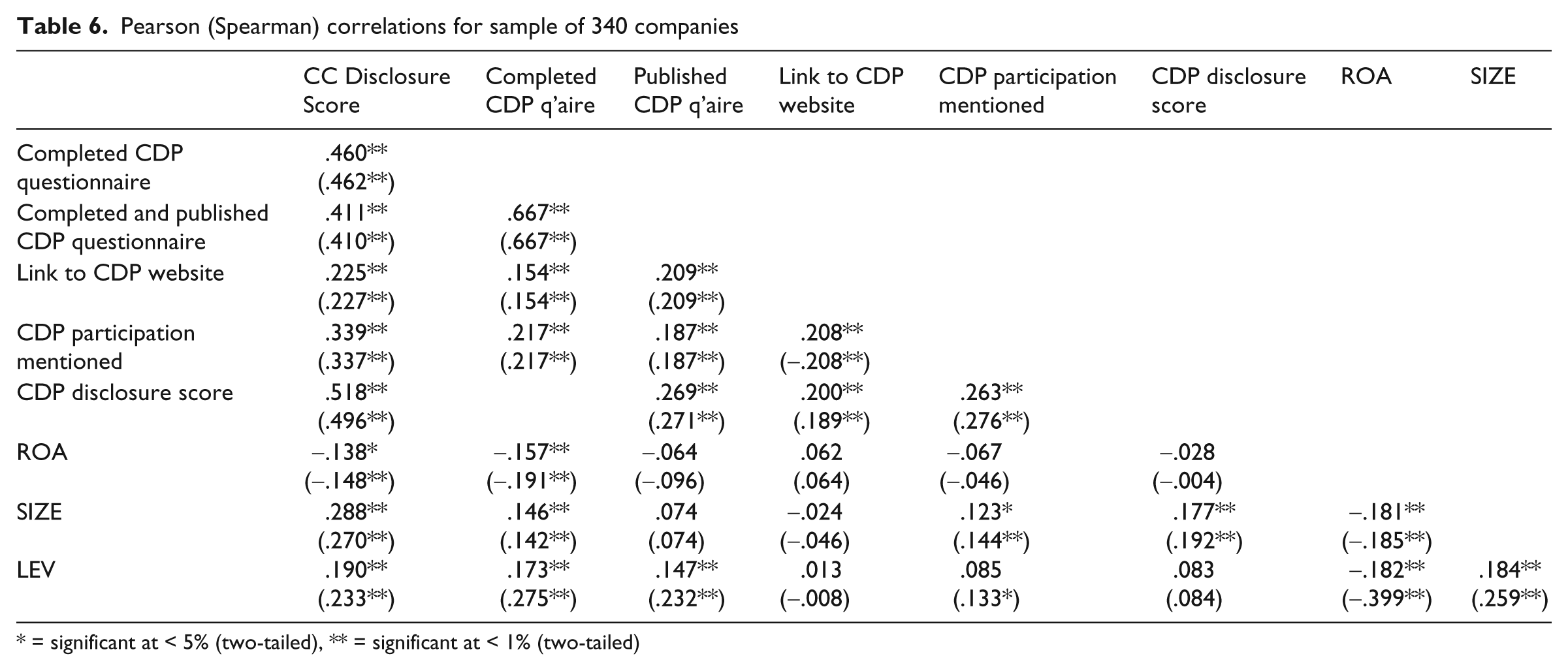

Panel B of Table 5 shows that mean and median CDP disclosure scores are strikingly higher than mean and median climate change disclosure scores based on corporate communication channels, indicating that companies tend to disclose only a relatively small portion of the information that they provide to CDP in their annual and sustainability reports. A paired-samples t-test of the difference in these scores is highly significant with a t-statistic of 32.57. However, while these scores are significantly different, they are also positively correlated. The Pearson correlation coefficient between these two variables of 0.518 (see Table 6) is also highly significant and provides prima facie evidence that companies that report most to CDP also disclose more via their corporate communications.

Pearson (Spearman) correlations for sample of 340 companies

= significant at < 5% (two-tailed), ** = significant at < 1% (two-tailed)

A comparison of the climate change disclosure scores shown in Tables 3 and 5 shows that, when just the sample of 230 companies for which a CDP score is available are considered, these scores are higher than when the full sample is considered. This difference appears to indicate that companies completing the CDP questionnaire are more forthcoming in their other corporate communications than those that choose not to complete the CDP questionnaire. This relationship will be formally tested using multivariate analysis in the next section.

Table 6 shows that our dependent variable is significantly correlated with all of our independent and control variables, thus providing initial support for our hypotheses and choice of control variables. Further, none of the correlations between the independent and control variables are high enough to indicate the potential for multicollinearity in our multivariate hypotheses tests.

4.3 Influence of institutional investors on climate change disclosure

Results of hypotheses testing are shown in Table 7. All of our models are significant with adjusted R2 between 0.389 and 0.489. Results for H1 show that climate change disclosure scores are significantly positively correlated with completing the CDP questionnaire and consenting to having it published on the CDP website. The coefficients shown in the first two columns of Table 7 indicate that the act of completing the CDP questionnaire increases a company’s climate change disclosure score by an average of 11.4 points compared with companies that do not complete the questionnaire, while companies that choose to both complete the CDP questionnaire and consent to its publication on the CDP website have a disclosure score that is 9.4 points higher on average.

Regression results: dependent variable is climate change disclosure score

significant at p < 0.01, * significant at p < 0.05 two-tailed. ROA = profit or loss before taxes divided by total assets. SIZE = natural log of total revenues. LEV = the sum of noncurrent liabilities and loans scaled by stockholders’ equity.

H2 is also strongly supported with the inclusion of both a link to the CDP website and explicit statements about participation in CDP activities being positively associated with increased climate change disclosure. As expected, both of these activities are complementary to the extent of detailed climate change disclosures made in annual and sustainability reports. When CDP disclosure scores are considered (H3), we find that these scores are significantly positively associated with climate change disclosure scores. Thus, all of the hypotheses are supported.

All of our models indicate a significant positive correlation between SIZE and disclosure scores, while no association is found for profitability (ROA). Leverage is significant only when firms that do not complete the CDP questionnaire are included in the sample. These results appear to indicate that non-CDP responding companies with higher leverage tend to make more climate change disclosures than those with lower leverage. In addition to the variables shown in Table 7, a series of country and industry dummy variables were included in each regression to control for variations in regulatory requirements and other incentives to disclose that could be expected to vary across countries and sectors. Consistent with the results shown in Table 4, firms from the UK and other EU countries tend to have significantly higher disclosure scores than those from other countries. When industry is considered, firms in the materials sector tend to have significantly higher disclosure scores while those in the consumer staples and telecom sectors have significantly lower disclosure scores.

To control for potential impacts of using slightly different scoring systems for our two disclosure measures (2009 CDLI for disclosure scores based on annual and sustainability reports and 2008 CDLI for CDP disclosure scores) we rerun the test of H3 using 2009 CDP scores which are based on the 2009 CDLI methodology. The results for this regression are similar to those shown in Table 6, with a coefficient on the CDP disclosure score variable of 0.352 and a t-statistic of 10.102

In addition to running the regressions using total climate change disclosure score as the dependent variable, we rerun each of these tests using the five sub-categories of disclosure. Each of our three hypotheses is supported for each of these five sub-categories of disclosures indicating that the activities of institutional investors influence all types of climate change disclosures. In addition to our hypothesized variables, there is some variation in the relationships between each category of disclosure and the control variables. Disclosures about risks and opportunities are weakly associated with industry differences. However, they are not related to firm size, profitability or leverage, and do not vary significantly between countries. GHG emissions disclosures are more prevalent for large firms from the UK and other EU countries and are less likely to be reported by some industry sectors. Verification and trading disclosures are less likely to be disclosed by US companies. Disclosures about performance in the area of emissions management are positively associated with firm size, as are climate change governance disclosures.

5. Conclusion

The results of this research provide support for the contention that the influence of institutional investors is positively associated with climate change disclosure by large companies. In support of the tenets of stakeholder theory and collective shareholder engagement, we provide evidence of the ability of a powerful stakeholder coalition of institutional investors to influence corporate reporting. We find the extent and quality of climate change disclosures to be associated with three indicators of corporate responsiveness to institutional investor expectations about the disclosure of this information. These are completion and publication of the CDP questionnaire on the CDP’s website, indications in corporate communications that CDP activities have influenced climate change disclosures, and the extent and quality of climate change information provided in CDP questionnaire responses.

It is possible that another correlated factor is driving both a company’s response to CDP and its climate change disclosures made through corporate communications channels: the extent of climate change risks faced by each company and how these risks are managed, i.e. its climate change value or performance. Given the difficulty in measuring this construct, especially for companies that choose not to disclose the information needed to assess it, we leave the examination of this possibility to future research.

Our research also provides some evidence that a powerful coalition of stakeholders is able to gain benefits for other stakeholders that may lack the ability to do so. The public disclosure and reporting of climate change information is potentially beneficial to a broader group of stakeholders than institutional investors. Further, while not directly tested in this research, there are also likely to be benefits associated with improved emissions management associated with the increased disclosures documented in this paper. Such emissions reductions benefit a broad group of stakeholder and societal interests.

Finally, there is a potential limitation in our study that needs to be acknowledged. The sample companies are very large which means that, on average, they are more likely to make CSR (including climate change) disclosures and to have institutional investors. Also, the companies that complete the CDP questionnaire dominate the sample. To some extent, this means that we are testing the responsiveness of already responsive companies to institutional investor pressures.

Footnotes

Acknowledgements

This research has benefited from the comments of Tim Cadman.

Funding

We are grateful for the financial support of the Accounting and Finance Association of Australia and New Zealand (AFAANZ).