Abstract

This study investigates the trading behaviour of foreign institutional investors (FIIs) and domestic institutional investors (DIIs) in the Indian stock market and also the relation between stock returns and equity flows by FIIs and DIIs. The study uses a wider definition of DIIs that includes not only mutual funds (MFs) but also banks, domestic financial institutions and insurance companies. The results show that the trading pattern followed by FIIs and DIIs is opposite of each other. While FIIs act as positive feedback traders, DIIs act as contrarian investors and negative feedback traders. High lagged stock returns result in increased FII investment. The DIIs, on the other hand, appear to book profits when the market moves up and buy when it moves down. Contrary to findings of earlier studies that MF investment has no effect on future stock returns, the study finds that DII investment has a significant positive relation with future stock returns. The study also finds weak evidence of a negative relation between FII investment and future stock returns.

Keywords

Introduction

Flow of funds into the stock markets from different investor groups has important implications for investors and policy makers as movements in stock markets are often attributed to such flows. The investor groups that have been the subject of study include foreign institutional investors (FIIs) and domestic institutional investors (DIIs), such as mutual funds (MFs), households, insurance companies, pension funds, closed-end funds, investment trusts, etc.

Several studies have examined the dynamic relationship between returns and institutional investment in developed and emerging markets. Most of these studies attempt to establish a cause and effect relationship between FII and DII inflows and outflows on one hand and stock returns on the other. Some studies examine the trading behaviour (herding, positive/negative feedback trading) of FIIs and DIIs. Another set of studies examine the effect of FII investments on volatility of stock returns in the domestic markets. Still others look at factors affecting FII inflows and firm-specific characteristics preferred by FIIs.

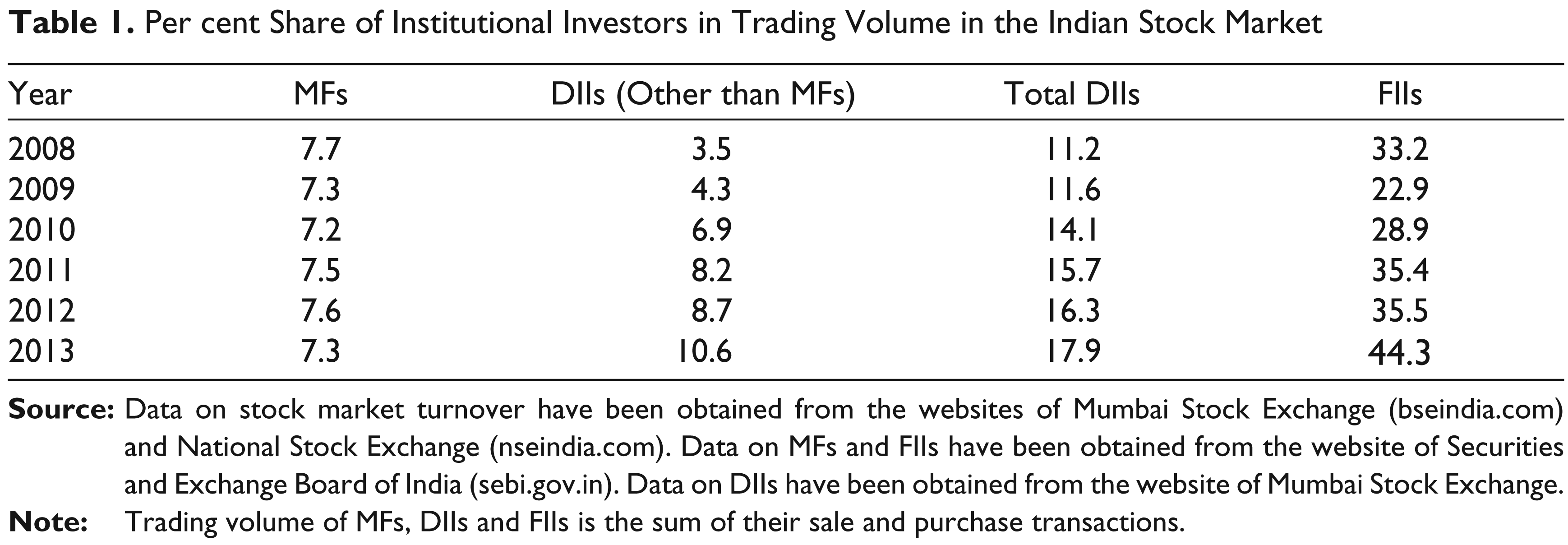

Per cent Share of Institutional Investors in Trading Volume in the Indian Stock Market

In the Indian stock market, FIIs and DIIs account for a major share of the trading volume. As depicted in Table 1, while the share of DIIs in the stock market turnover has increased from 11 per cent in 2008 to 18 per cent in 2013, the share of FIIs has increased from 33 per cent to 44 per cent during the same period. Taken together, institutional investors (FIIs and DIIs) accounted for about 62 per cent of the total trading volume in 2013. Since both FIIs and DIIs are significant players in the stock market, their trading actions have an impact on the stock market movements. Small investors are generally guided by the actions of the institutional investors in taking investment decisions. The problem these small investors face is whether they should track the investment behaviour of FIIs or DIIs. It is, therefore, important to understand the distinct investment behaviour of FIIs and DIIs. Studies that have examined the flows and trading behaviour of FIIs and DIIs in India define the DIIs narrowly to include only domestic mutual funds while there are many other DIIs, such as banking companies, insurance companies and development financial institutions.

As shown in Table 1, the share of DIIs other than MFs is more than that of MFs in recent years. In the year 2013, while MFs accounted for 7.3 per cent of the stock market turnover, other DIIs accounted for 10.6 per cent. The article examines the trading behaviour of FIIs and DIIs, the latter defined broadly as described above and also the relation between stock returns and investment flows of FIIs and DIIs.

The results show that the trading patterns followed by FIIs and DIIs are opposite to each other. While FIIs act as positive feedback traders, DIIs act as contrarian investors and negative feedback traders. High lagged stock returns result in increased FII investment. The DIIs, on the other hand, appear to book profits when the market moves up and buy when it moves down. Lagged DII and FII flows contain information to predict the future stock returns.

The rest of the article is organized as follows. Second section reviews the related literature. Third section describes the data used in the study. The methodology used for the study is presented in the fourth section. Empirical results are discussed in the fifth section and sixth section presents the conclusions.

Related Literature

The studies on the subject document different trading behaviours of institutional investors and the relation between equity flows and stock returns. Bose (2012) explores the dynamic interaction between investment flows of MFs and FIIs, and finds a strong negative relationship between the net investments by these two classes of institutional investors. Domestic MFs are found to determine their investment flows on the basis of their own previous investments, FII investments as well as market returns. The study also finds weak evidence of net investments by FIIs having a causal influence on stock market returns but fails to identify any causal relation between domestic MFs’ net investments and domestic stock returns.

Ray (2009) attempts to identify whether a causal relationship exists between the net investment made by FIIs and the equity return in the Indian stock market. The author finds evidence that suggests that the equity returns Granger cause FII investments, but not the reverse. Kumar, Tavishi and Khatua (2012) find strong evidence of positive feedback trading of FIIs and a bidirectional relation between FII flows and equity market returns in India. Studies by both Chakrabarti (2001) and Mukherjee, Bose and Coondoo (2002) show that the FII net inflows into India are mainly driven by Indian stock market returns. They also find that stock market return is, however, not significantly influenced by variation in these flows. Sehgal and Tripathi (2009) find a causal relationship between return on the Bombay Stock Exchange (BSE) Sensex and FII inflows (gross purchases) and no such relationship between return on the BSE Sensex and FII outflows (gross sales). In the case of MFs, they find that return on the BSE Sensex causes both MF inflows and MF outflows. They also find a two-way causality between FII outflows and MF outflows. Thenmozhi and Kumar (2009) analyze the causal relationship between MF flows and market returns. They find that MF outflows (sales) are significantly affected by returns in the stock market, but returns are not significantly influenced by variation in these flows. Thiripalraju and Acharya (2011) find that MF investment is negatively related to lagged index return. They also show that over a period of time, bidirectional causality between returns and MF investment has been replaced by unidirectional causality and domestic MFs no longer influence domestic stock returns. Both FIIs and MFs follow feedback trading and there is a strong negative correlation between FII and MF flows. As FIIs follow positive feedback trading, it suggests that MFs follow contrarian strategies.

Batra (2003) finds that there is a strong evidence of FIIs chasing trends and adopting positive feedback trading strategies at the aggregate level on a daily basis. However, there is no evidence of positive feedback trading on a monthly basis. They also find that foreign investors have a tendency to herd together in their trading activity in India. The trading behaviour and biases of the FIIs do not appear to have a destabilizing impact on the equity market.

In summary, the literature in the Indian context first provides evidence that there is a negative correlation between FII and DII investment (Bose, 2012; Thiripalraju & Acharya, 2011). Secondly, FIIs pursue positive feedback trading (Batra, 2003; Kumar et al., 2012; Thiripalraju & Acharya, 2011). Thirdly, while some studies find a bidirectional causality between FII flows and equity returns (Bose, 2012; Kumar et al., 2012), others (Chakrabarti, 2001; Mukherjee et al., 2002; Ray, 2009) find that there is only unidirectional causality that flows from equity returns to FII flows. Finally, domestic MFs do not have any influence on stock returns (Bose, 2012; Thenmozhi & Kumar, 2009; Thiripalraju & Acharya, 2011). Besides the effect on institutional investment on market returns, some studies (Tripathi & Seth, 2014) have linked the stock market performance to macroeconomic factors.

Similar evidence has also been found by studies in markets outside India. Grinblatt and Keloharju (2000) find that the foreigners investing in Finland tend to be momentum investors while domestic investors, particularly households tend to be contrarians. Boyer and Zheng (2009) examine the joint behaviour of aggregate stock market returns and net cash flows (net purchases of equity) to the stock market from the different investor groups (MFs, foreign investors, pension funds, etc.) in the United States over a 53-year time period. They find little evidence on investor flows following past stock market returns and weak evidence on the ability of investor flows to forecast the future stock market returns. In their study on the US institutions, Cai and Zheng (2004) find that stock returns Granger cause institutional trading (especially purchases) on a quarterly basis and that stock returns are negatively related to lagged institutional trading. Oh and Parwada (2007) study the relation between fund flows and stock market activity in Korea and find a positive relationship between stock market returns and MF flows measured as stock purchases and sales. However, in terms of net trading flows, they find that MF investors are negative feedback traders. Samarakoon (2009) investigates the relation between equity flows by different investor classes and returns in Sri Lanka and finds that purchases and sales of domestic and foreign investors, both institutional and individual, are positively related with past returns, except during crisis periods, when they are negatively related. Domestic institutional and foreign individual purchases lead to higher future returns whereas domestic individual purchases lead to lower future returns. Foreign institutional purchases do not impact future returns. Sales by domestic investors have no impact on future returns while sales by foreign investors lead to higher future returns.

As pointed out earlier, the extant literature in the Indian context considers DIIs as consisting of MFs only. This article includes MFs, banks, insurance companies and domestic financial institutions in the definition of DIIs.

Data

The study uses daily data on equity flows by FIIs and DIIs and the daily closing values of the BSE Sensitive Index (BSE Sensex). The data set covers the period from 16 April 2007 (the first date from which DII investment data is available) to 31 December 2013. The data on equity flows has been obtained from the website of Securities and Exchange Board of India (SEBI) and data on the BSE Sensex has been obtained from the website of the Mumbai Stock Exchange. However, investment transaction data, though separately available for MFs, is not separately available for insurance companies, banks and domestic financial institutions. Therefore, the article deals with the consolidated data on DIIs.

All equity flows are measured in domestic currency, Indian rupee (₹). Stock returns are continuously compounded daily returns measured in domestic currency.

Methodology

The relation between stock returns and investment flows (equity flows) of FIIs and DIIs and the investment behaviour of these institutions is examined using correlation analysis, Granger causality and vector autoregression (VAR) analysis.

Correlation analysis is used to understand the contemporaneous relation between different variables. Granger causality tests are used to determine the direction of causation between returns and institutional investment. To better understand the causality between returns and investment, a bivariate VAR model is used. The VAR model helps determine whether past returns can be used to predict the future flows and vice versa. In the VAR model, equity flows and stock returns are endogenous variables. The VAR system enables prediction of future equity flows using past stock returns while controlling for information about future equity flows contained in past equity flows. Similarly, the system enables prediction of future stock returns using past equity flows while controlling for the information contained in past stock returns. These controls result from the specification of lagged values of the dependent variables as regressors. The VAR model used is specified by Equations (1) and (2) below:

A lag of seven periods is used in the system based on the Akaike information criterion (AIC), Bayesian information criterion (BIC) and Hannan–Quinn criterion (HQC). The system is estimated separately for the FII and DII equity flows. The variables used for equity flows are FII net (FIIN) investment and DII net (DIIN) investment. Net investment is the difference between gross purchases and gross sales made by the institutions. The variable used for stock returns is BSER.

Equation (1) in the VAR system provides evidence as to whether the past stock returns affect flows. The coefficients on Returnt–j, where j = 1–7, would indicate whether the equity flows are correlated with past stock returns. The lagged equity flows, Equity Flowt–j, where j = 1–7, control for information about future equity flows contained in past equity flows.

Equation (2) in the VAR system provides evidence as to whether the flows affect future stock returns. The lagged returns up to seven lags are also included as regressors in Equation (2) to control for the information contained in lagged returns up to seven lags. Also, to control for the price–pressure effect of concurrent flows on returns, equity flow at time t is also included as a regressor in Equation (2). The F-test of the joint significance of the slope coefficients of the lagged variables is used to assess whether the past returns affect future equity flows or past equity flows affect the future returns. The model is estimated using ordinary least squares (OLS) with robust standard errors that are heteroskedasticity and autocorrelation consistent (HAC).

Before testing the relationship between FII/DII flows and stock returns, we test the stationarity of all the variables using the augmented Dickey Fuller test and the Phillips–Perron test. All selected variables have been found to be stationary.

Empirical Results

Results of correlation analysis are presented in Table 2.

Results of Correlation Analysis

The correlation analysis shows that there is a significant contemporaneous negative correlation (–0.48) between net investment of FIIs and DIIs. This indicates that their investment strategies differ. The opposite investment behaviour of DIIs and FIIs is also somewhat evident from the fact that over the sample period, it is only 31 per cent of the time, the DIIs and FIIs have been on the same side (buy or sell) of the trade, that is, they both have been either net buyers or net sellers on the same date. The evidence is consistent with the earlier findings of Bose (2012) and Thiripalraju and Acharya (2011).

Further, while the contemporaneous correlation between FII net investment and stock returns is positive, it is negative between DII net investment and stock returns. This is consistent with the hypothesis that FII behave as momentum investors and DIIs behave as contrarian investors.

There is a high positive correlation (0.44) between current and one-day lagged investment of FIIs. The positive contemporaneous correlation between FII net investment and stock returns coupled with positive correlation between current and lagged investment is consistent with the positive feedback trading behaviour of FIIs. There is also a high positive correlation (0.63) between current and one-day lagged investment of DIIs. The negative contemporaneous correlation between DII net investment and stock returns coupled with positive correlation between current and lagged investment is consistent with the negative feedback trading behaviour of DIIs. Here again, the evidence supports the findings of Kumar et al. (2012), Thiripalraju and Acharya (2011) and Batra (2003).

The results of the Granger causality test are presented in Table 3.

Results of Granger Causality Test

In line with the previous research, the Granger causality test results in Table 3 show that there is a unidirectional causality that flows from stock returns to DII and FII investment.

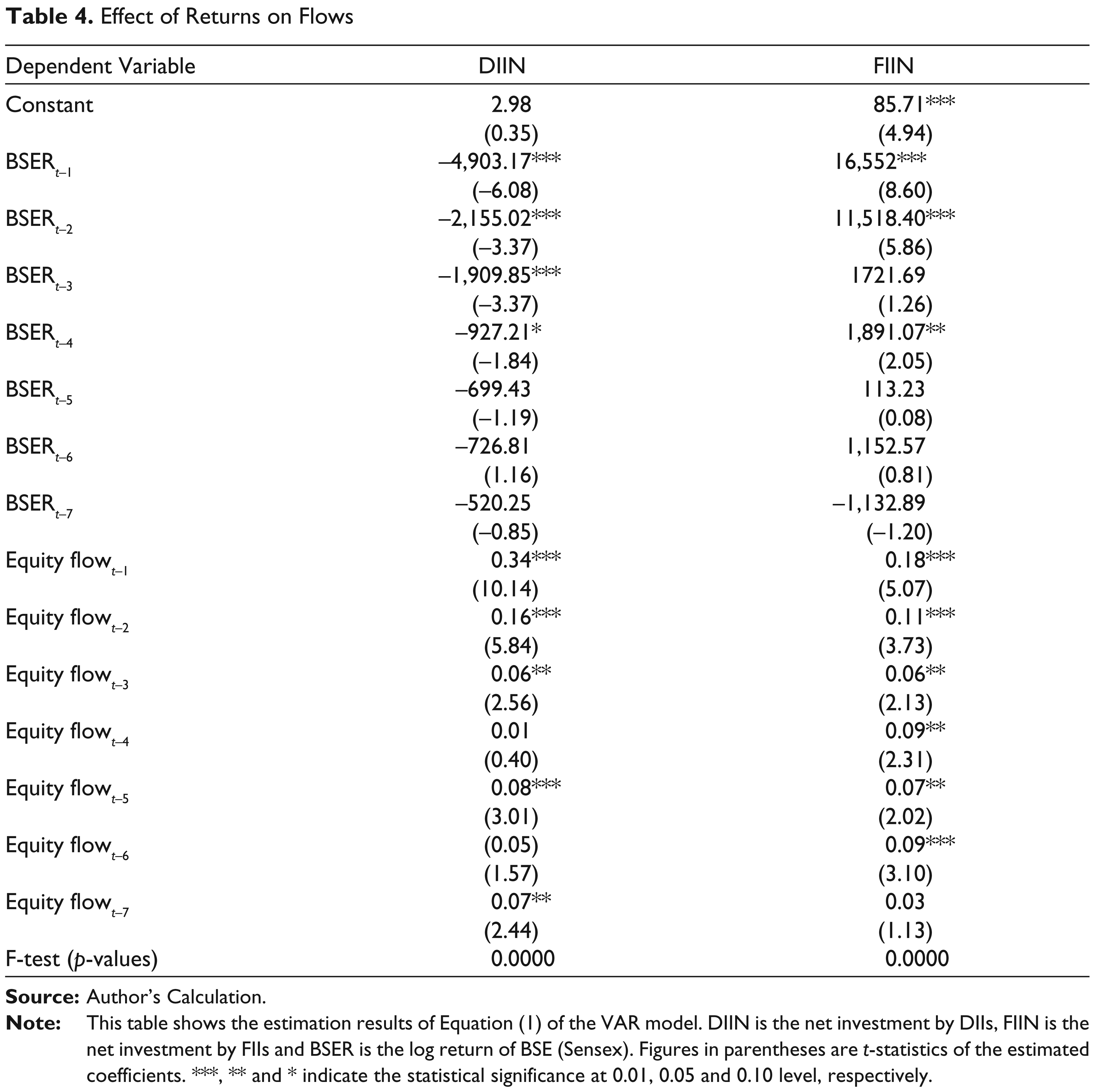

Results of fitting the VAR model are presented in Tables 4 and 5. Table 4 presents the coefficient estimates in regressions of equity flows of investor types on past stock returns. The purpose of this model is to assess the ability of past stock returns to predict the future equity flows after controlling for the effects of past flows.

Effect of Returns on Flows

Past returns at the first four lags are significantly negatively related to net investment of DIIs. In the case of FIIs, there is a significant positive relation between past returns and net investment at lag 1, lag 2 and lag 4. Thus, DIIs appear to follow a contrarian investment strategy while FIIs appear to follow a momentum trading strategy. The p-values of the F-test of joint significance of lagged returns in predicting the future flows show that lagged returns are strongly significant in predicting the net investment of the two investor types, after controlling the impact of past flows. However, the investment behaviour of DIIs and FIIs is exactly opposite.

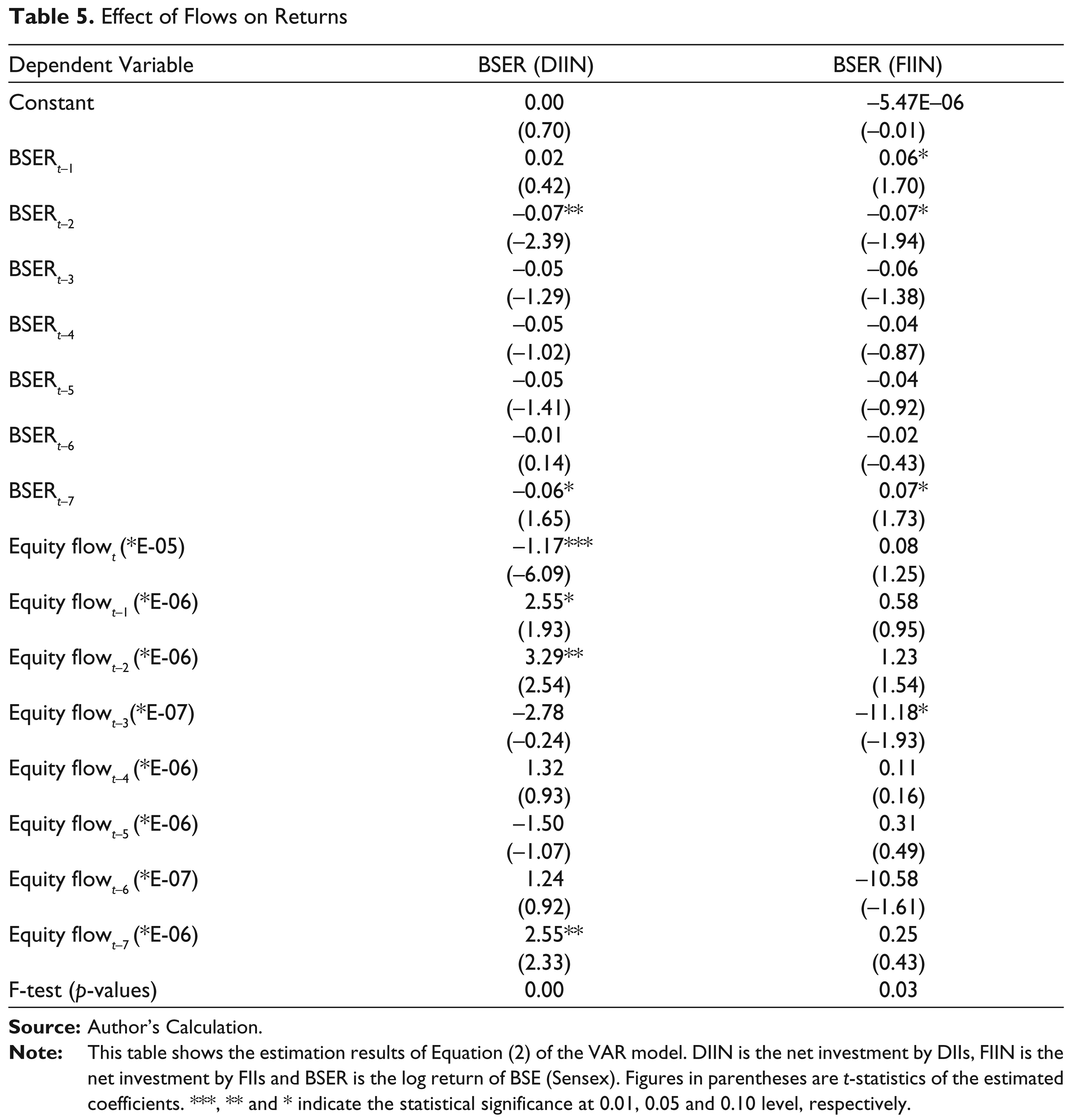

Table 5 presents the coefficient estimates in regressions of stock returns on past equity flows of investor types. The purpose of this model is to assess the ability of past equity flows to predict the future stock returns after controlling for the effects of past stock returns and potential price–pressure impact of concurrent equity flows.

Effect of Flows on Returns

Flows of DIIs have a statistically significant positive effect on stock returns at lag 1, lag 2 and lag 7. Flows of FIIs have a statistically significant negative effect on stock returns at lag 3. The evidence indicates that investment flows of DIIs have more information content compared to the investment flows of FIIs in predicting future stock returns. In the case of DIIs, the p-value of the F-test indicates joint significance of coefficients of lagged flows at a level of 0.01. The level of significance is 0.05 in the case of FIIs.

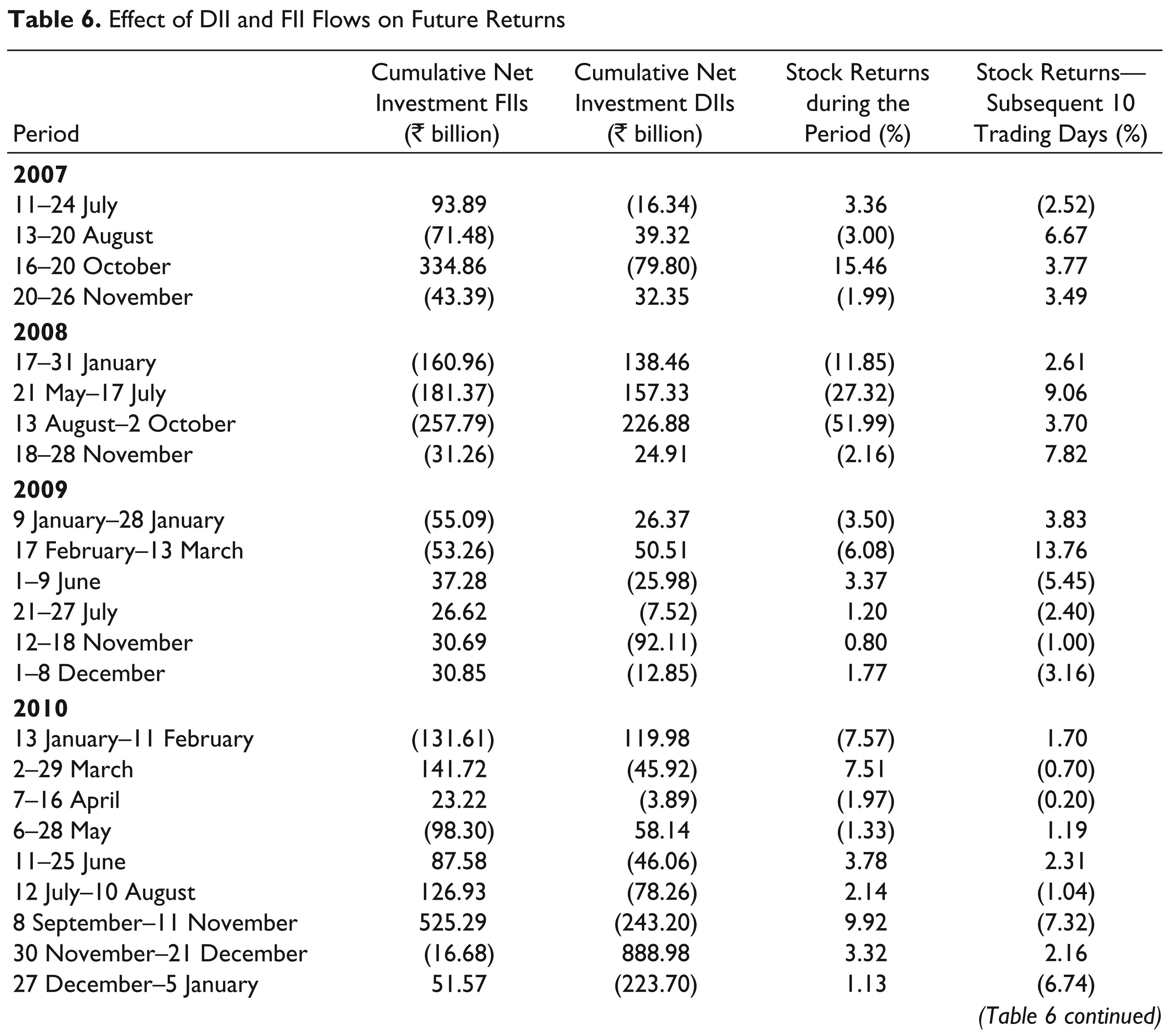

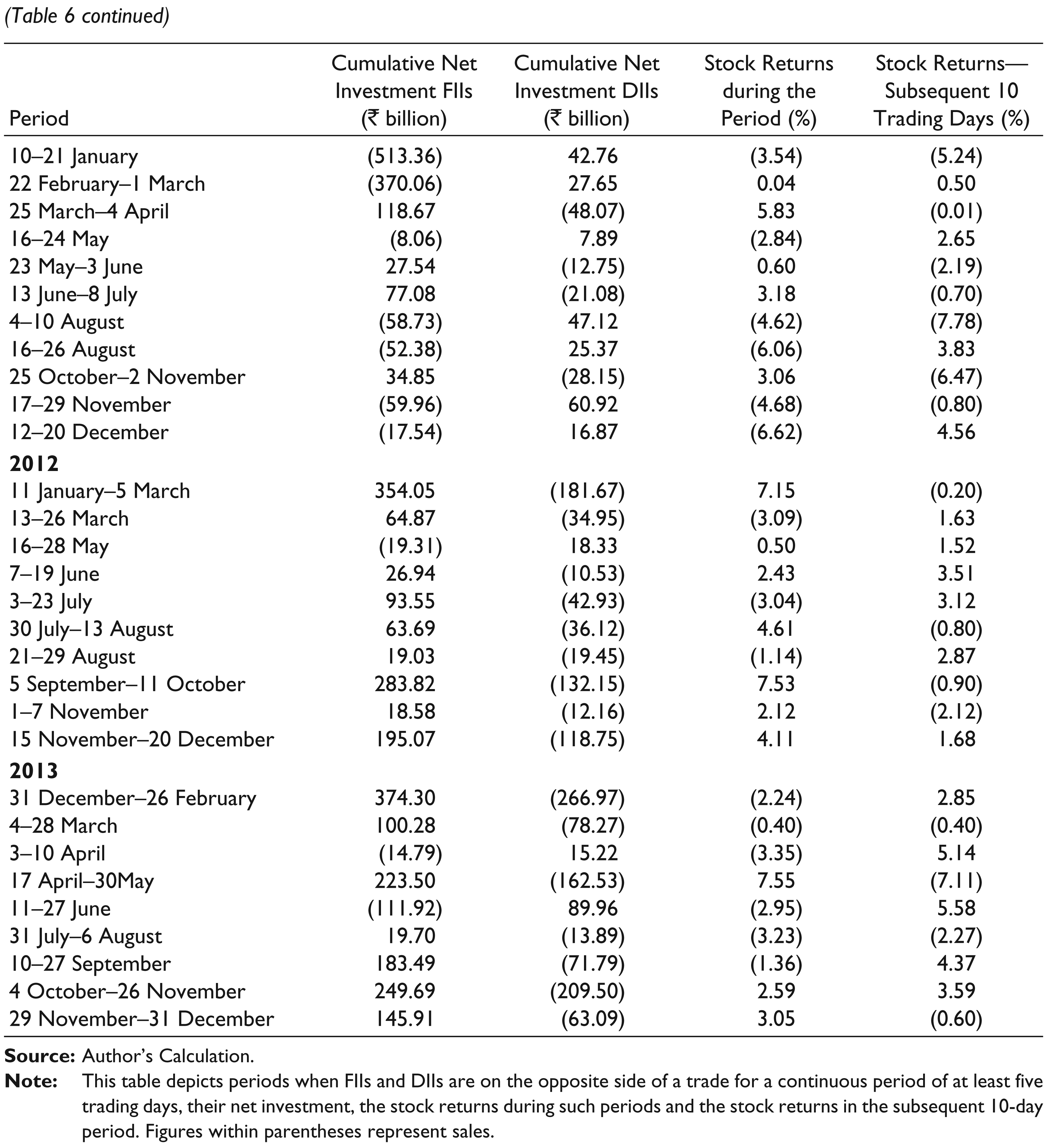

Empirical evidence shown so far suggests that investment behaviour of DIIs and FIIs is just opposite to each other. DIIs sell when FIIs buy and DIIs buy when FIIs sell. While FIIs behave as momentum traders, DIIs follow a contrarian trading strategy. FII and DII investments also contain information to predict the future stock returns. There is a strong evidence that DII flows are positively related to future stock returns. In the case of FIIs, there is a weak evidence that FII flows are negatively related to future stock returns. We get further evidence on whether FII and DII net investment contains information for predicting the future stock returns by identifying periods in the sample period when FIIs and DIIs are on the opposite side of a trade for a continuous period of at least five trading days, and examining the relation between such trading action and future stock returns.

As shown in Table 6, there are 53 periods when FIIs have been buying (selling) and DIIs have been selling (buying) for a continuous period of at least five trading days. In 21 of the 53 periods, the FIIs have been net sellers and DIIs have been net buyers. In 18 of those 21 periods, the cumulative stock returns in the subsequent 10 trading days (2 weeks) are positive. In the other 32 of the 53 periods, the FIIs have been net buyers and DIIs have been net sellers. In 21 of those 32 periods, the cumulative stock returns in the subsequent 10 trading days (2 weeks) are negative. Overall, in 39 of these 53 periods (74 per cent of the cases), stock returns over the subsequent 10 trading days have the correct sign, which means that the sign of future returns matches that of the DII flows in the preceding period and is the reverse of the sign of FII flows in the preceding period.

Effect of DII and FII Flows on Future Returns

While Bose (2012), Thenmozhi and Kumar (2009) and Thiripalraju and Acharya (2011) do not find any relation between MF investments and future stock returns, the present study finds strong evidence of such relation between DII investment and future stock returns.

Conclusions

This study investigates the trading behaviour of FIIs and DIIs in the Indian stock market and also the relation between stock returns and equity flows by FIIs and DIIs. The study uses a wider definition of DIIs that includes not only MFs but also banks, domestic financial institutions and insurance companies. The study uses correlation analysis, Granger causality test and the VAR model for the purpose. The study finds that the trading behaviour of FIIs and DIIs is opposite to each other. While FIIs act as momentum traders, the trading behaviour of DIIs is contrarian. While FIIs behave as positive feedback traders, DIIs act as negative feedback traders. The findings are consistent with similar findings by earlier studies based on Indian data that considered only MFs as comprising the DIIs. However, contrary to the findings of earlier studies that MF investment has no effect on future stock returns, the study finds that DII investment has a significant positive relation with future stock returns. The study also finds a weak evidence of a negative relation between FII investment and future stock returns. Therefore, small investors can take cues from the trading actions of both FIIs and DIIs in taking investment decisions.

Footnotes

Acknowledgements

The author is grateful to anonymous referees of the journal for providing useful comments and suggestions to improve the quality of the article. However, the usual disclaimers apply.