Abstract

We establish a link between supply chain finance (SCF) and capital structure adjustment by core firms through a data set of listed firms on the Shanghai and Shenzhen Stock Exchanges. We find that SCF can significantly speed up capital structure adjustment, especially for the under-leveraged firms. Enhanced financial strengths and competitive advantages underlie this impact. Comprehensive examinations also suggest that SCF may speed up cash turnovers, lower financing costs, and improve firm values. In addition, the impact is more substantial on firms of smaller sizes, located in better-developed regions, those without bank–firm connections, and those with higher environmental dynamism. However, the impact seems similar on private firms and state-owned enterprises (SOEs), or across industries of various degrees of competition. Our findings bear such policy implications that SCF can accelerate capital structure adjustment and contribute to the quality economic growth in emerging markets.

1. Introduction

Capital structure, as the ratio between liabilities and assets, has an optimal value, or target capital structure, which allows a firm to enhance its value, growth and subsequent operation (Loof, 2004). The trade-off theory suggests that when the tax offset from liabilities is equal to the cost of financial distress, the firm achieves its target capital structure. A vast number of studies suggest the existence of target capital structures of firms and develop models to evaluate them (Flannery and Hankins, 2013).

Academic studies, from the perspectives of agency theory (Jensen and Meckling, 1976), underinvestment (Myers, 1977), overinvestment (Rocca, 2011), and free cash flows (Bessler et al., 2011), suggest that leverage ratios deviating from those in target capital structures would be harmful. On one hand, leverage ratios higher than those in target capital structures may motivate firm executives to maximise equity values rather than firm values, lead to excessive risky investments, and incur higher agency or bankruptcy costs. On the other hand, leverage ratios lower than those in target capital structures may promote defensive management, sacrifice tax shields, cause cash flow issues, reduce growth opportunities, and lead to overconfident executives.

Dynamic internal and external factors often require firms to achieve target capital structures (Fischer et al., 1989). The actual leverage ratios of firms are often either higher or lower than their target levels. When firms, in a particular year, achieve target capital structures, the changing internal and external factors would impose further adjustment needs. Internal factors normally include firm size, stock price, profitability, firm age and corporate governance (Chang et al., 2014; Dang et al., 2014). External factors include interest rates, financial systems, legal regimes and macro economies (Faulkender et al., 2012). Actual capital structures of firms and their target capital structures often show deviation, proximity and deviation again in the long-term (Flannery and Rangan, 2006). With many unexpected events in place, such as the Covid-19 pandemic, the world has recently become more turbulent and unpredictable, imposing more needs for firms to timely adjust their capital structure.

However, capital structure adjustments incur both fixed and variable costs. Firms often adjust their capital structure through raising debts, share repurchase, dividend payouts, lowering debts and issuing shares (Leary and Roberts, 2005). These means lead to fixed costs, such as accounting, evaluation and legal fees, and variable costs, which are related to firm performance, prospective growth and financial market development. Underperforming firms or those of low growth may find it difficult to access funding from creditors or investors, and subsequently refrain from capital structure adjustments. Therefore, firm quality and capital structure adjustment costs, especially the variable costs, are key elements in allowing capital structure adjustments.

Supply chain finance (SCF) can be regarded as an effective means of short-term financing and a practice of financial dimension of sustainable supply chain management (SSCM). Based on the trade relationship with upstream and downstream firms, core firms may take advantage of their credit rating, expected cash flows and bank loans, and provide receivables as well as prepaid, and inventory financing to the supply chain. In other words, SCF involves core firms at the centre of the ecosystem, their upstream suppliers, downstream distributers, retailers and financial institutions. Core firms organise, manage and coordinate the supply chains through data, control and key positions in various sectors. Since the recent Global Financial Crisis (GFC), a fast-growing number of firms have committed to SCF to enhance management efficiency over cash flows in alignment with product and information flows. The organic integration of bank loans and core firm credits may significantly optimise benefits for both banks and firms in supply chains (Gornall and Strebulaev, 2018). With better controls of capital, logistics and information flows, the core firms subsequently support ecosystems of suppliers, manufacturers, distributors and customers.

The evolving literature has defined SCF as a meaningful innovation from the finance and supply chain perspectives. As a financial innovation, SCF may establish links between banks and firms for short-term financing purposes (Dyckman, 2010). Core firms may take advantage of their position and provide capital to other firms in supply chains, especially the small and medium-sized enterprises (SMEs), which often have significant financing constraints due to their size and ownership type (Li et al., 2020c). This financial innovation helps lower transaction costs, improve risk management, enhance capital efficiency and escalate the performance of supply chains (Zhang et al., 2019). Furthermore, SCF may innovatively optimise the ecosystem of supply chains (Gomm, 2010). SCF may provide enhanced framework design and risk management for certain industries (Hofmann and Belin, 2011). The optimal solutions of financial needs of suppliers, manufacturers, distributors and customers – as well as integrated materials, information and capital flows – may enhance the performance and competitiveness of supply chains in the marketplace (Lanier et al., 2010).

Since SCF plays increasing roles in facilitating economic growth, the Chinese government has issued a series of supportive policies. For example, the People’s Bank of China (PBC, 2016) requires in its No. 42 Document of 2016 that the financial sector works closely with firms in supply chains. Similarly, the State Council (2017) issued a Guidance in 2017 to encourage innovations in supply chains. The China Banking and Insurance Regulatory Commission (CBIRC, 2019) formally required the banks to promote SCF in support of growth of the real economy. The recent Covid-19 pandemic has also escalated the role of SCF in the economic world. The PBC (2020) mandates in its Document No. 226 of 2020 that financial institutions dedicate more efforts to SCF to stabilise supply chains and production. Given China’s inefficient banking system and poor financial infrastructure (Allen et al., 2005; Xu and Lin, 2007), where the bond and stock markets are supplementary to its loan market (Wu and Xu, 2020), SCF has become an emerging new ingredient in the largest bank-based economy.

In the meantime, it may have been difficult for Chinese firms to adjust to target capital structures. Chinese firms, especially the large number of SMEs and those of private ownership, often find themselves significantly constrained in accessing financial resources crucial for survival and development, and must incur higher funding costs than the market would entail (Jiang et al., 2014). Their capital structure adjustment speeds 1 may also be slow, after weighing up the adjustment costs and related benefits (Li et al., 2020b; Lockhart, 2014).

Given that SCF has emerged as a new means of flexible financing to effectively alleviate financial constraints (Ali et al., 2019; Song et al., 2020), an interesting question arises: Does SCF lower adjustment costs and accelerate capital structure adjustments? SCF may effectively improve bank–firm collaborations, efficiently distribute financial resources among firms in supply chains and significantly improve competitiveness. It seems necessary to examine the relationship between SCF and firm costs in adjusting their capital structure. Firms may demonstrate asymmetric adjustment speeds in their upward and downward leverage movements in developed markets (Byoun, 2008; Yin and Ritter, 2020). Given China’s institutional context, it may also be necessary to examine the asymmetry of adjustments in the capital structure of Chinese firms. To the best of our knowledge, such literature is scarce.

We find – through a proprietary data set of listed firms on the Shanghai and Shenzhen Stock Exchanges – that SCF may speed up capital structure adjustments by core firms, especially the under-levered ones. Improved financial strengths and enhanced competitive advantages are underlying this impact. Comprehensive examinations also suggest that SCF may speed up cash turnovers, lower financing costs and improve firm values. Furthermore, the SCF impact may be more substantial on smaller-sized firms, those located in better-developed regions, those without bank–firm connections and those in higher environmental dynamism. However, the SCF impact is indifferent between private firms and state-owned enterprises (SOEs) or across various industries.

This study can be meaningful in the following aspects. First, it enriches the evolving literature on SCF. SCF is a combination of finance and supply chain to innovatively solve supply chain-based financing issues. As a form of complex systems engineering, SCF has attracted in-depth contributions by researchers from both finance and management disciplines to address financial services in efficiently integrated and managed supply chains, and to achieve lower transaction costs, optimal resource allocation and sustainable development. Current SCF studies focus, respectively, on finance (Camerinelli, 2009; Dyckman, 2010; Wuttke et al., 2013a) and supply chain (Cho et al., 2019; Hofmann, 2015; Wuttke et al., 2013b). The finance strain, from the perspective of financial institutions, analyses the contribution of SCF as a short-term financing solution (Dyckman, 2010) aimed at lowering the credit risk of bank loans (Zhao et al., 2015), improving cash flow transparency or financial effectiveness of SCF participants (Lamoureux and Evans, 2011), and enhancing flexibility of payments for the buyers (Wuttke et al., 2013a). The supply chain strain, from the perspective of supply chain management, analyses member collaboration and the integration of logistics, information and cash flows, aimed at optimising inventories and the supply chain’s operational efficiency (Blackman et al., 2013; Wuttke et al., 2013b). Although some studies acknowledge the financial value and supply chain value of SCF, they mainly demonstrate the economic consequences of SCF from the view of banks as fund suppliers and SMEs as fund consumers. There is a lack of empirical evidence on financial and economic consequences of the core firms in SCF. We examine its impact on firm capital structure adjustment from the perspectives of cash holding and competitive advantage, with comprehensive consideration to both finance and supply chain attributes. Such exploration may push the boundaries of both strains of SCF literature. Our study may, therefore, provide meaningful evidence on SCF impact, and extend the literature boundary on both finance and supply chain strains with firm-level financial evidence.

Second, this study contributes to the evolving literature on capital structure. Existing studies, through theoretical discussion or empirical evidence, find that firms have target capital structures, which are decided by debt and bankruptcy costs. As a variable, their capital structures are often affected by both internal and external factors. As a result, firms constantly adjust their capital structures towards their target ones (Fischer et al., 1989; Flannery and Hankins, 2013). In addition, both firm internal factors, such as size, investment level, governance and financial flexibility (Devos et al., 2017) and external ones, including macroeconomy and legal environment (Cook and Tang, 2010; Oztekin and Flannery, 2012), may affect the pace of capital structure adjustment. However, there has been a lack of examination of these adjustments made either as passive or initiative responses to a particular factor. As a significant financial innovation in recent years, SCF has offered firms strategic choices in capital structure adjustments. The core firms in supply chains may initiatively commit to SCF with a better focus on long-term targets. Little evidence is provided by current literature on this recent financial innovation and the capital structures of firms. Our study may shed light on the emerging new link between SCF and firm capital structure.

Third, this study may also contribute to the discussions on sustainable management of supply chains. The broad definition of sustainability includes environmental, financial or economic, and social dimensions (Golicic and Smith, 2013; Hartmann and Moeller, 2014). Current sustainability studies on supply chains have explored the development of green products, provision of employee-friendly environments and education facilities, and corporate social responsibilities (Esfahbodi et al., 2016; Zhu et al., 2005). Some others explore the factors affecting supply chain sustainability and the governance of supply chains (Gimenez and Sierra, 2013; Tachizawa and Wong, 2014), such as management support or commitment, employee participation, client stress, coordination of suppliers and social entity stakeholders. At least to a certain extent, sustainability discussions related to supply chains have ignored the financial factors, which are important premises to assure sustainable operations of supply chains. This study on SCF may extend SSCM discussions in the financial dimension. In recent decades, Chinese firms play increasingly important roles in the global supply chain. SCF can be a meaningful way of enhancing the financial strength of firms, optimising cash flows, enhancing competitive advantages, providing resources to achieve better green innovations, work environments, environmental protection and corporate social responsibilities. Therefore, this study may provide a new point of view to the sustainable supply chain discussions. Given that the Covid-19 pandemic aggravates the risk of supply chain interruption and even bankruptcy, it can be valuable to encompass supply chain stability considerations, where SCF enhances firm capacity to cope with sudden incidents, to sustainably manage supply chains under uncertainties, and to maintain and rebuild global SSCMs.

The rest of the article is structured as follows: The section ‘Literature review and hypotheses’ reviews the literature and develops our hypotheses. The section ‘Data and research methodology’ describes our data and research methodology. The section ‘Results analysis’ analyses the results. The section ‘Underlying mechanisms’ explores underlying mechanisms. The section ‘Extended examinations’ extends our examinations to economic consequences, and the section ‘Conclusion’ concludes the article.

2. Literature review and hypotheses

2.1. SCF and capital structure

The resource-based theory suggests that firms take advantage of their resources to compete with others (Barney, 1991). Since capital structure adjustment is an important means for firms to join the market competition (Bolton and Scharfstein, 1990; Brander and Lewis, 1986), they may lose their competitiveness when they cannot access sufficient resources, including internal and external financial resources. Theoretically, capital structure adjustment can be achieved through changing the ratio between equity and debts, including debt increase, share repurchase or dividend payout, paying off the debt, and issuing new shares (Leary and Roberts, 2005). Given the development of China’s financial markets, most listed firms rely on bank loans in their financing behaviour, while corporate bonds and share repurchase are rare (Fu et al., 2015). As a result, most firms in China adjust their capital structure through debt increase, debt decrease, issuing of shares and dividend payouts. Given the SCF context, firms may access more financial resources and subsequently have better capacity to adjust their capital structure.

Firms may need to actively and initiatively adjust their capital structure 2 to manage the financial risk of supply chains and that of deviation from their target structures. The impact of SCF on their capital structures may be examined from the perspectives of improved financial strengths, competitive advantages and risk management needs.

SCF may improve the financial strength of core firms for capital structure adjustments. Information asymmetry and credit risks can be meaningfully reduced through enhanced collaboration between firms in the supply chain and related banks. Therefore, SCF may effectively mitigate their financial constraints (Rahman, 2020). On one hand, core firms can take better advantage of commercial papers to pay upstream suppliers, which can access cash through factoring, reverse factoring or discounted drafts (Lekkakos and Serrano, 2016). On the other hand, core firms can take advantage of flexible payments by their customers either in cash or commercial papers which can be endorsed and used in lieu of cash to pay the suppliers. As a possible result, SCF can effectively provide an alternative to external financing through bringing forward accounts receivables and delaying accounts payables (Hofmann and Kotzab, 2010). The improved cash turnover efficiency would significantly improve their cash holdings (Pan et al., 2020). Cash constraints often push capital structure adjustment costs higher and slow down the adjustment speed (Byoun, 2008). On the contrary, improved cash holdings can, besides the coverage of fixed costs, reduce reliance of firms on external funding sources (Acharya et al., 2007). Firms with more cash holdings can be better motivated to adjust capital structures and develop resilience to various shocks from the market. Faster adjustment in capital structures may also facilitate access to external funding at lower costs and make timely, profitable investments. As a result, improved financial strength through SCF can reduce capital structure adjustment costs and speed up the adjustment.

In addition, SCF can improve the competitive advantages of core firms for capital structure adjustments. SCF allows the simultaneous management of their working capital and that of other firms, corresponding to the product and information flows in the supply chains (Wuttke et al., 2013b; Zhao et al., 2015). This means that the core firms not only consider their own capital needs but also that of the upstream and downstream firms, aiming at optimisation of the overall capital flows of supply chains (Li et al., 2020a). SCF further strengthens the links between the core firms and their suppliers or customers. In the meantime, SCF allows the embedded services of banks and other third-party institutions. As a result, managing cash flows in the supply chain allows the core firms to strategically establish a financial alliance with related firms or financial institutions. Through consolidations in procurement procedures, production, warehousing, distribution and other supply chain elements, they can respond quickly to market demands and develop competitive advantages of the supply chains.

The reduced transaction costs and lowered information asymmetry within supply chains may further confine opportunistic behaviour and moral hazards, improve efficiencies of core firms and develop new competitive advantages (Owen-Smith and Powell, 2004). SCF may strengthen their ties with other firms in supply chains and those with major creditors, especially the banks (Uzzi, 1997). In other words, SCF develops collaborative ties between the core firms and their creditors, essential for both lowered capital structure adjustment costs and faster speeds.

Furthermore, SCF can increase the needs of core firms in their capital structure adjustment for better risk management. Core firms often provide guarantees for business activities by other firms, either upstream or downstream in the supply chains, exposing themselves to additional operational and credit risks. In cases of defaults, the core firms may have to fulfil the guarantees at the cost of their own liquidity or even solvency. Given the noticeably inefficient elements of market infrastructure in the Chinese market, where information asymmetry can be outstanding and banks control most financial resources but demonstrate reluctance to lend to private firms (He et al., 2019; Wu and Xu, 2020), core firms in SCF may have to face escalated risk management needs in a highly dynamic market and in increasingly complex circumstances (Trkman and McCormack, 2009). In other words, SCF can also impose the need for core firms to adjust their capital structures efficiently.

Based on the above theoretical discussion, we develop our first hypothesis as follows:

2.2. SCF and asymmetric speed in capital structure adjustments

Firms may demonstrate risk-averse tendencies when facing benefits but risk-taking tendencies when facing losses (Tversky, 1979). Given that the same level of wealth change may bring asymmetric impact to firm executives, that is, the negative losses often have a stronger impact than positive gains, and firms may demonstrate asymmetric speed in capital structure adjustments. In other words, despite the same level of deviation from their target capital structure, to avoid losses or bankruptcy, over-leveraged firms tend to show faster but more downward capital structure adjustment than their under-leveraged counterparts in the upward leverage adjustments (Byoun, 2008; Faulkender et al., 2012).

Similarly, SCF may be related to asymmetric speed in a core firm’s capital structure adjustments. With growing risk exposures, SCF may impose stronger needs for over-leveraged core firms to commit to downward capital structure adjustment than doing the opposite. In comparison, with more cash holdings and fewer liquidity risks, SCF may impose fewer needs for under-leveraged core firms to adjust their capital structures upwards towards higher leverages. In other words, SCF might further confirm the asymmetric speed in a core firm’s capital structure adjustments, that is, more rapid downward adjustments than upward ones. Improved competitive advantages may lead the core firms to adopt more conservative capital structures with sufficient risk buffers.

However, SCF may also allow the core firms additional choices in their capital structure. Increased cash holdings, improved competitive advantages, closer ties with other firms in supply chains, and enhanced collaboration with creditors may, in effect, improve the risk buffers for them without lowering their leverage, and induce firm executives to further take advantage of their market positions. In other words, with improved risk management skills and more resources, they may opt to use capital structures as tough strategic tools for predatory pricing or to push competitors out of the market (Bolton and Scharfstein, 1990; Brander and Lewis, 1986), that is, more rapid upward adjustments than downward ones. In such situations, the core firms in supply chains may tend to purposely adjust their leverage upwards. SCF may, therefore, alternatively distort the asymmetric speed in their capital structure adjustments.

Based on the above theoretical discussion, we develop our second hypothesis as follows:

3. Data and research methodology

3.1. Data

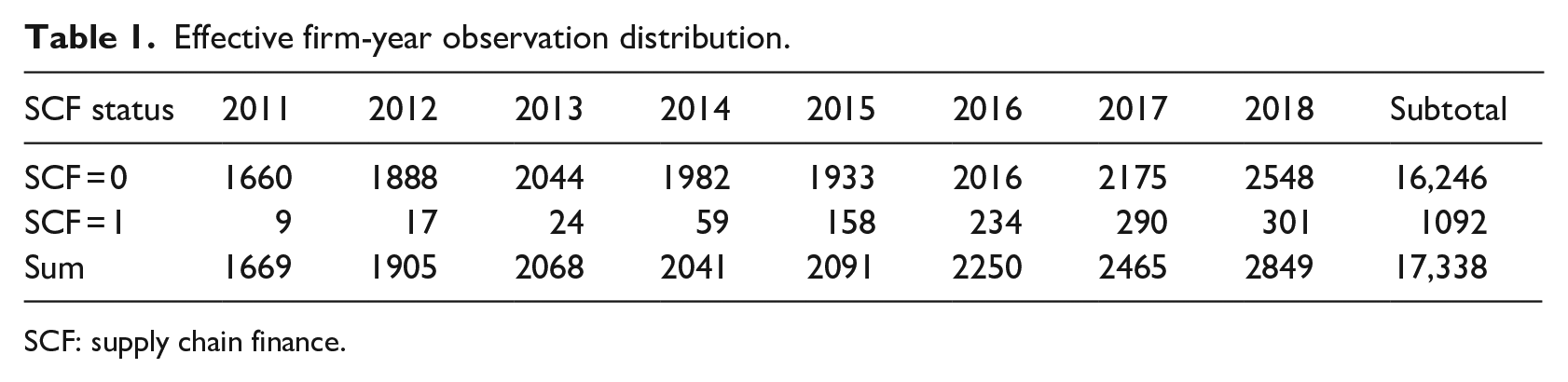

We adopt all listed A-share firms on the Shanghai and Shenzhen Stock Exchanges between 2011 and 2018 as our initial samples. We first exclude all financial firms. We exclude firms in information transmission, software and information technology services, transportation, warehousing and postal service sectors, most of which are service providers to supply chains and cannot be classified as core firms in SCF. We further exclude firms of less than 2 years of observations, those categorised as Special Treatment (ST) or Particular Treatment (PT), those with debt ratios of less than 0 or greater than 1, and those with missing data. In addition, we manually collect SCF information from the financial reports of firms, public announcements and Baidu searches. 3 We have in total 17,338 effective firm-year observations, including 1092 with SCF and 16,246 without. Table 1 reports the firm-year distribution of our effective observations.

Effective firm-year observation distribution.

SCF: supply chain finance.

We derive the financial data of firms from the CSMAR and Wind databases. For the regional development measurement, we adopt the Marketisation Index of China’s Provinces NERI Report 2018 (Wang et al., 2019). We also winsorise the statistics data at a 1% level to exclude extreme values.

3.2. Variables

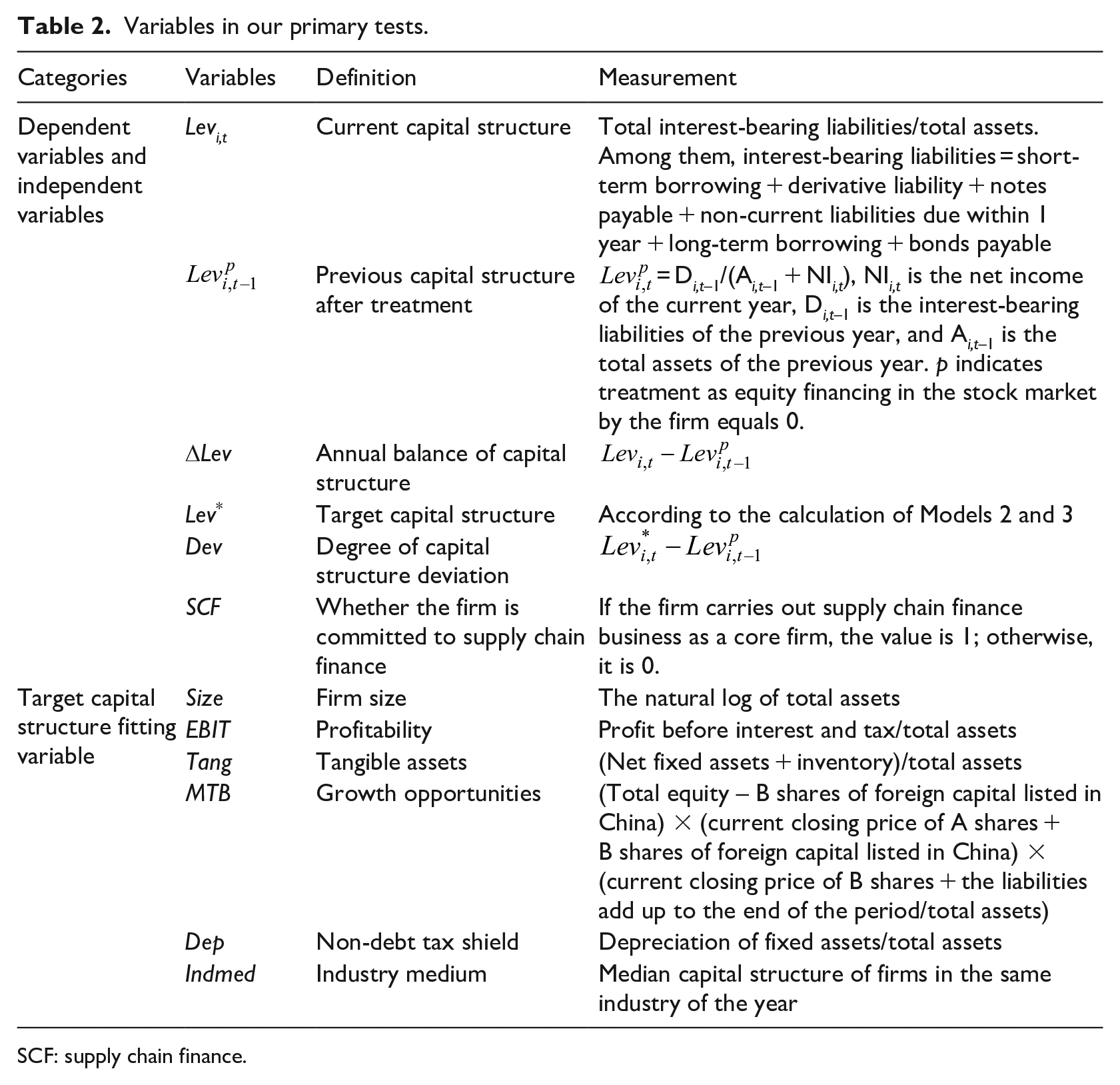

We adopt a list of variables for our primary tests. Capital structure (Lev) is measured as the total interest-bearing liabilities/total assets. Debt-to-market and book debt ratios are commonly used to measure firm capital structure. The optimal capital structure would be the trade-off between tax-efficient debts and related costs (Franco and Merton, 1963). As a result, changes in the market value of debt would not directly affect benefits from the tax shield. However, in cases of bankruptcies and liquidations, creditors often claim their titles in terms of book values rather than market values. In addition, market values may be highly volatile and make it difficult for quantitative analysis or specific management targets (Jalivand and Harris, 1984). As a result, the value of a firm is often closer to its book value. We adopt the book debt ratio for capital structure measurements.

Target capital structure fitting variables include firm size (Size), profitability (EBIT), the ratio of tangible assets (Tang), growth opportunities (MTB), the non-debt tax shield (Dep), and the medium of capital structures in the industry (Indmed). These six fitting variables are suitable for target capital structure measurements (Faulkender et al., 2012).

SCF is a dummy variable, indicating whether a firm is committed to SCF, in other words, whether the core firm clearly disclosed that it provides SCF services to its upstream and downstream firms through cooperation with banks or financial firms established by the firm; if yes, it equals 1, otherwise 0. This may be the only direct measurement of SCF in the literature (Pan et al., 2020). Table 2 provides a list of variables with their detailed definitions.

Variables in our primary tests.

SCF: supply chain finance.

3.3. Method

Following Flannery and Rangan (2006), Lemmon et al. (2008) and Faulkender et al. (2012), we adopt the following equation (1) to estimate target capital structure.

In equation (1), Levi,t refers to the firm’s interest-bearing debt ratio of the year.

Considering that the firm may not change its liabilities or equity during the year while dividend payouts still lead to changes in its capital structure (Faulkender et al., 2012), we develop equation (2).

where

In equation (3), β is the regression coefficient. X refers to the target capital structure fitting variable. Since we may assume that current firm capital structures may be perfect, then the observed capital structures can be the target ones. However, given the dynamics in firm capital structure, there are certain deviations between the assumed target capital structures and the specific structures that firms have (Faulkender et al., 2012; Lemmon et al., 2008). Equation (3) can help us estimate their target capital structure.

Combining equations (2) and (3), we get equation (4).

β can be obtained from equation (4) and put back into equation (3) to achieve

Adding the interaction between the specified variable and the degree of deviation, the variable’s influence on the speed of capital adjustment can be tested, and a comprehensive multi-factor capital adjustment model can be constructed (Flannery and Hankins, 2013; Flannery and Rangan, 2006; Im et al., 2020). Where Devi,t, the degree of deviation from target capital structure, as in Table 2, is measured as the difference between the target capital structure of the year and the actual capital structure in the previous year. ΔLevi,t is the difference between the actual capital structure of the year and that of the previous year. If the actual capital structure equals the target capital structure, then Devi,t = ΔLevi,t, suggesting that the core firm has no deviation from its target capital structure and SCF may not affect the firm’s capital structure. However, when Devi,t ≠ ΔLevi,t, the interaction between SCF and Devi,t could test the impact of SCF on the speed of Devi,t moving towards ΔLevi,t, that is, capital structure adjustment speed. Therefore, we introduce an interaction term to examine the impact of SCF on the capital structure adjustment speed.

Based on equation (2), the benchmark model for dynamic capital structure adjustment can be derived as the following equation (5).

Since we need to examine the influence of SCF on capital structure’s dynamic adjustment speed r, we can assume r as a linear function of the constant and the influence factor, indicated by equation (6).

where λ0 + λ1SCF indicates the capital structure adjustment speed after SCF adjustment.

Combining equations (5) and (6), we can get equation (7).

In equation (7), λ1 can reflect the impact of SCF on capital structure adjustment. Since SCF only has values of 1 or 0, a significant and positive value of λ1 would suggest SCF accelerates the capital structure adjustment speed and vice versa. λ1/λ0 can be used to indicate the impact of SCF on capital structure adjustment speed.

3.4. Fitting target capital structure and FE measurement

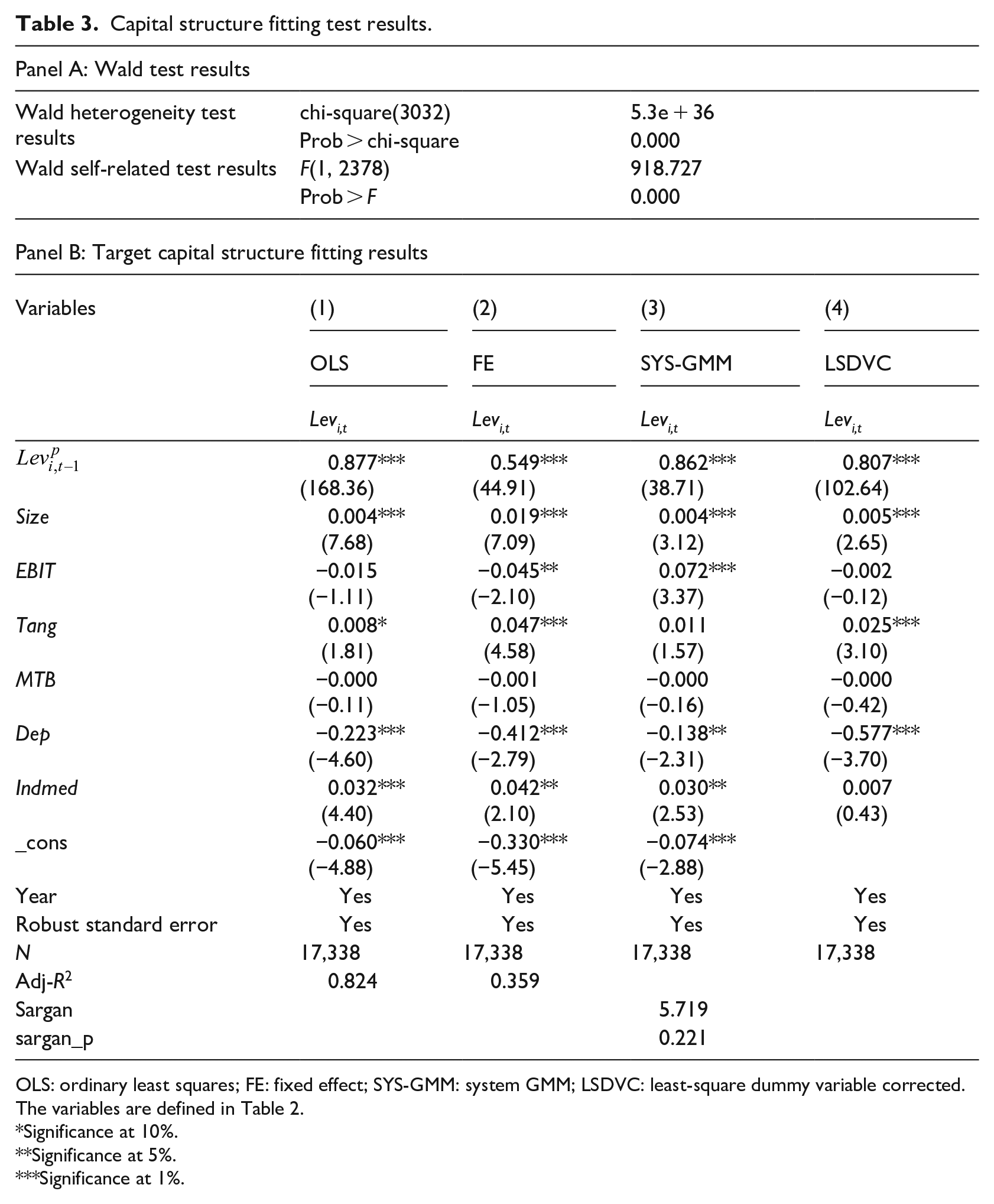

We regress the capital structure fitting variables with equation (4) and obtain the fitted values of the target capital structure. To assure the validity of our regression, we do a Wald test with equation (4). Table 3, Panel A reports Wald test results, indicating autocorrelation and heteroscedasticity problems in our samples.

Capital structure fitting test results.

OLS: ordinary least squares; FE: fixed effect; SYS-GMM: system GMM; LSDVC: least-square dummy variable corrected. The variables are defined in Table 2.

Significance at 10%.

Significance at 5%.

Significance at 1%.

To solve this problem, we use LSDVC to fit the capital structure, bootstrapped standard errors, and clustering robustness to correct the standard errors. Table 3 Panel B reports equation (4) regression results in comparison with ordinary least squares (OLS), fixed effects (FEs), and system GMM (SYS-GMM) results. Given that the actual capital structure adjustment speed falls between the OLS and the FE estimation results, respective minimum and maximum values (Flannery and Rangan, 2006), the actual adjustment speed in our context shall be between 12.3% and 45.1%, that is, the estimated coefficient of Lev shall be in the range of 0.549 to 0.877. SYS-GMM and LSDVC results are both in this range. Therefore, we adopt LSDVC to measure target capital structures and use SYS-GMM to measure the target capital structures in the robustness test.

We also do a Hausman test on panel regression models. With chi-square and p values of 573.93 and 0.0000, respectively, it is appropriate for us to apply an FE in our measurements.

4. Results analysis

4.1. Statistics summary

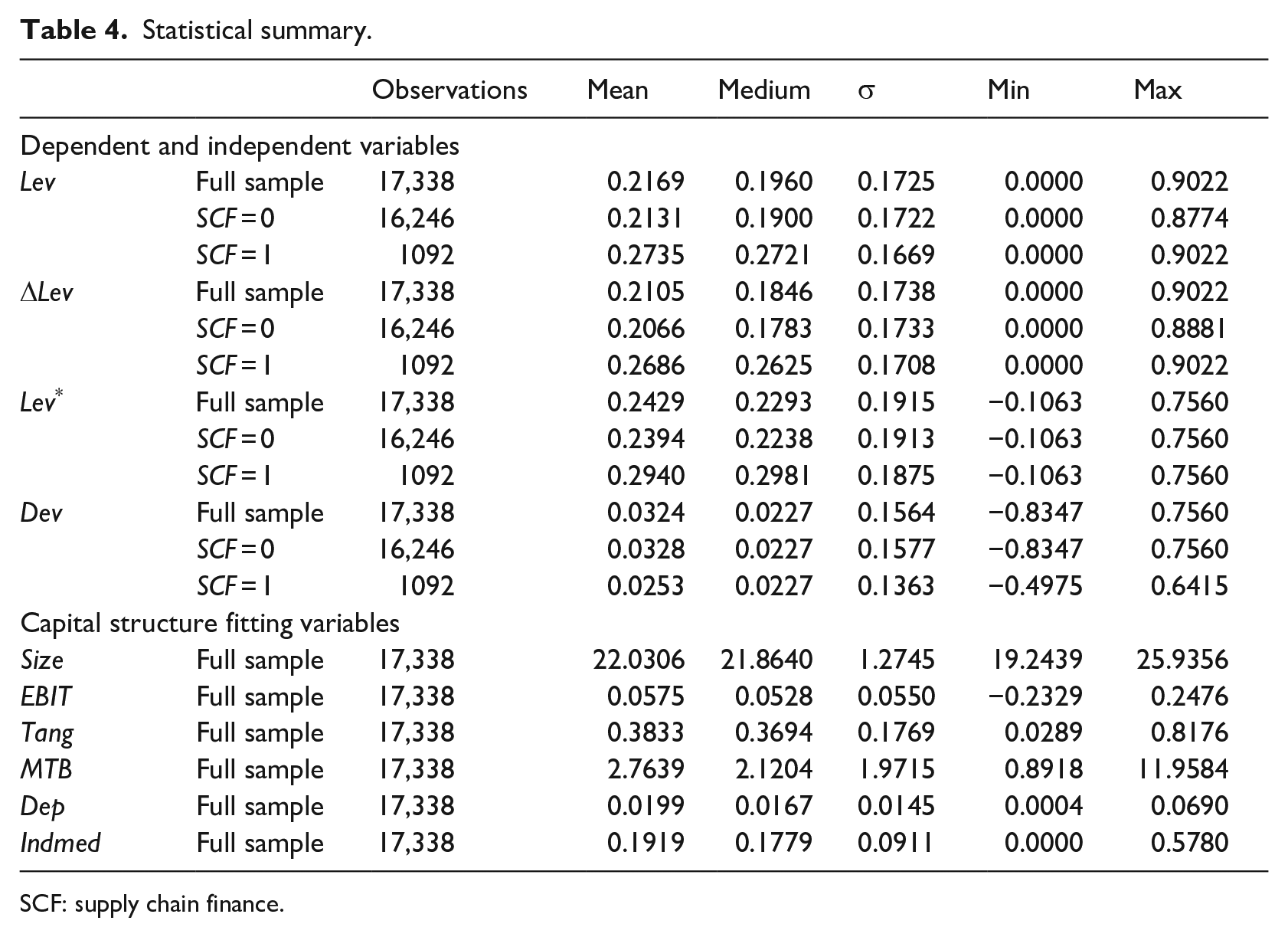

Table 4 reports the statistics summary of the variables for our primary tests. Lev has respective mean and medium values of 21.69% and 19.60%, with noticeable differences across the entire sample of firms, suggesting heterogeneity characteristics of capital structure. Lev* and Dev suggest noticeable differences between their actual and target capital structures. Both ΔLev and Dev are positive, suggesting that firms adjust their capital structures towards the target levels. However, the adjustment speeds need to accelerate.

Statistical summary.

SCF: supply chain finance.

Comparing the SCF and non-SCF groups, we can see that Lev, ΔLev, and Lev* are much higher among firms committed to SCF than their counterparts without, suggesting higher leverages in the SCF group. In the meantime, Dev in the SCF group is much smaller than that in the non-SCF group, suggesting closer to target capital structure levels by firms committed to SCF. In other words, SCF can accelerate adjustment speed towards their target capital structures, supportive of our H1.

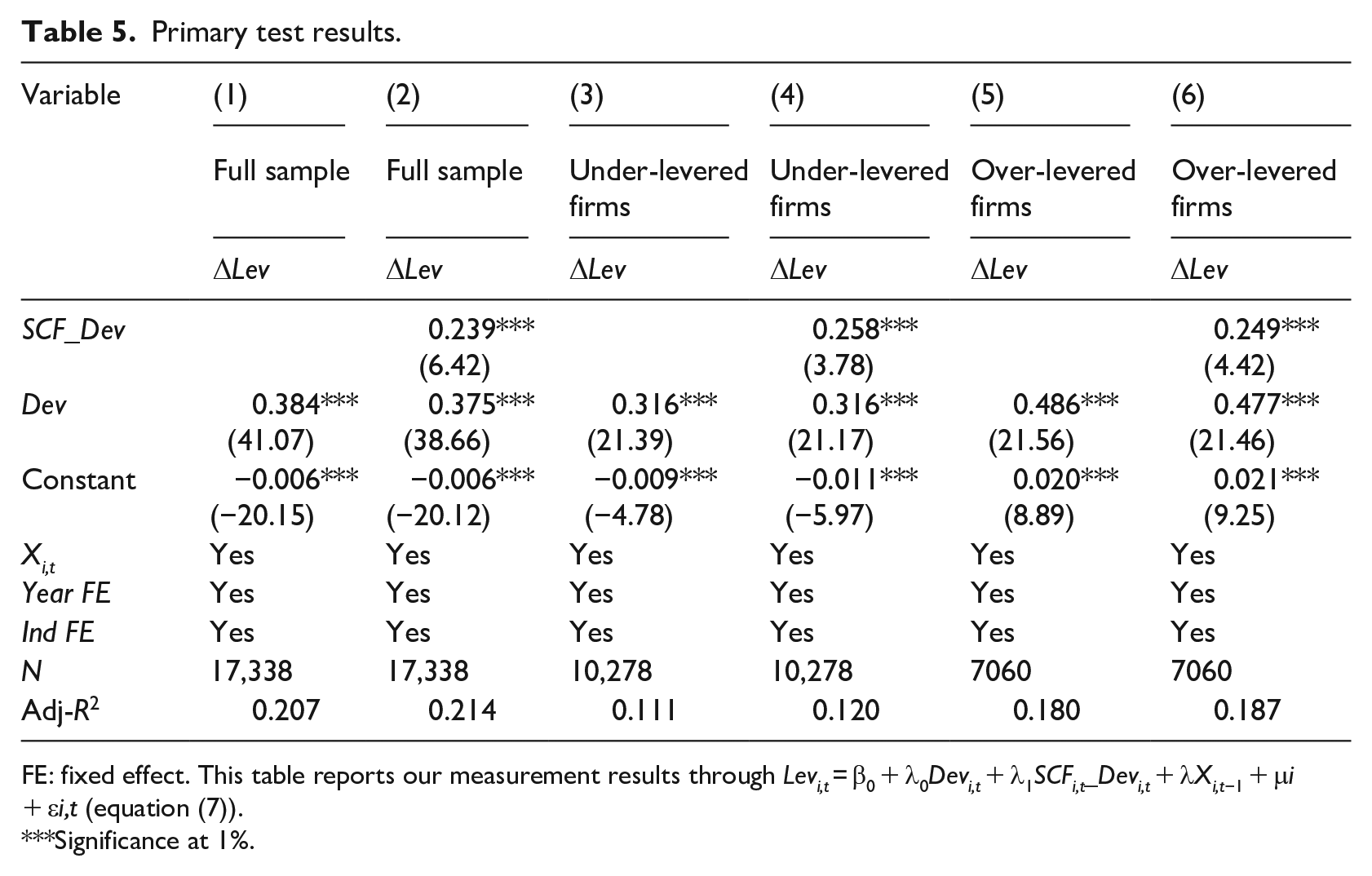

4.2. Primary test results

Table 5 reports our primary test results through equation (7). Column (1) indicates that Dev has a value of 0.384, that is, average capital structure adjustment speed at 38.40% for each year in our sample period. Column (2) indicates that SCF_Dev is significant and positive, suggesting that, compared to those without, firms committed to SCF demonstrate 63.70% (0.239/0.375) faster speed in capital structure adjustments. In other words, SCF accelerates capital structure adjustment speeds, supportive of our H1.

Primary test results.

FE: fixed effect. This table reports our measurement results through Levi,t = β0 + λ0Devi,t + λ1SCFi,t_Devi,t + λXi,t−1 + μ i + ε i,t (equation (7)).

Significance at 1%.

Columns (3) – (6) report our test results on H2a and H2b. When the actual capital structures are lower than their targets, firms adjust their capital structures upwards, and vice versa. Columns (3) and (5) report that firms adjust their capital structures upwards and downwards, respectively, at speeds of 31.60% and 48.60%. Confirmed by a Fischer test and p of 0.000, a significant difference exists between the regression coefficients of the two groups. These results suggest that the downward adjustment speeds are faster than the upward ones, that is, asymmetry exists in the adjustment speeds of capital structure, in conformity with the findings of previous studies (Byoun, 2008; Faulkender et al., 2012). Columns (4) and (6) report the SCF impact on adjustment speeds, suggesting that SCF can significantly and positively promote both upward and downward adjustments in the capital structure.

Interestingly, SCF accelerates upward adjustment speed by 81.60% (0.258/0.316), much more significant than its promotion of the downward adjustment speed by 52.20% (0.249/0.477). In addition to further supporting H1, these results also support H2b, that SCF improves a firm’s upward adjustments in capital structures to maximise its profits and expel competitors. In other words, SCF can provide firms with choices of faster upward adjustments in their capital structure.

4.3. Robustness

We adopt three different ways to verify our primary findings for robustness purposes.

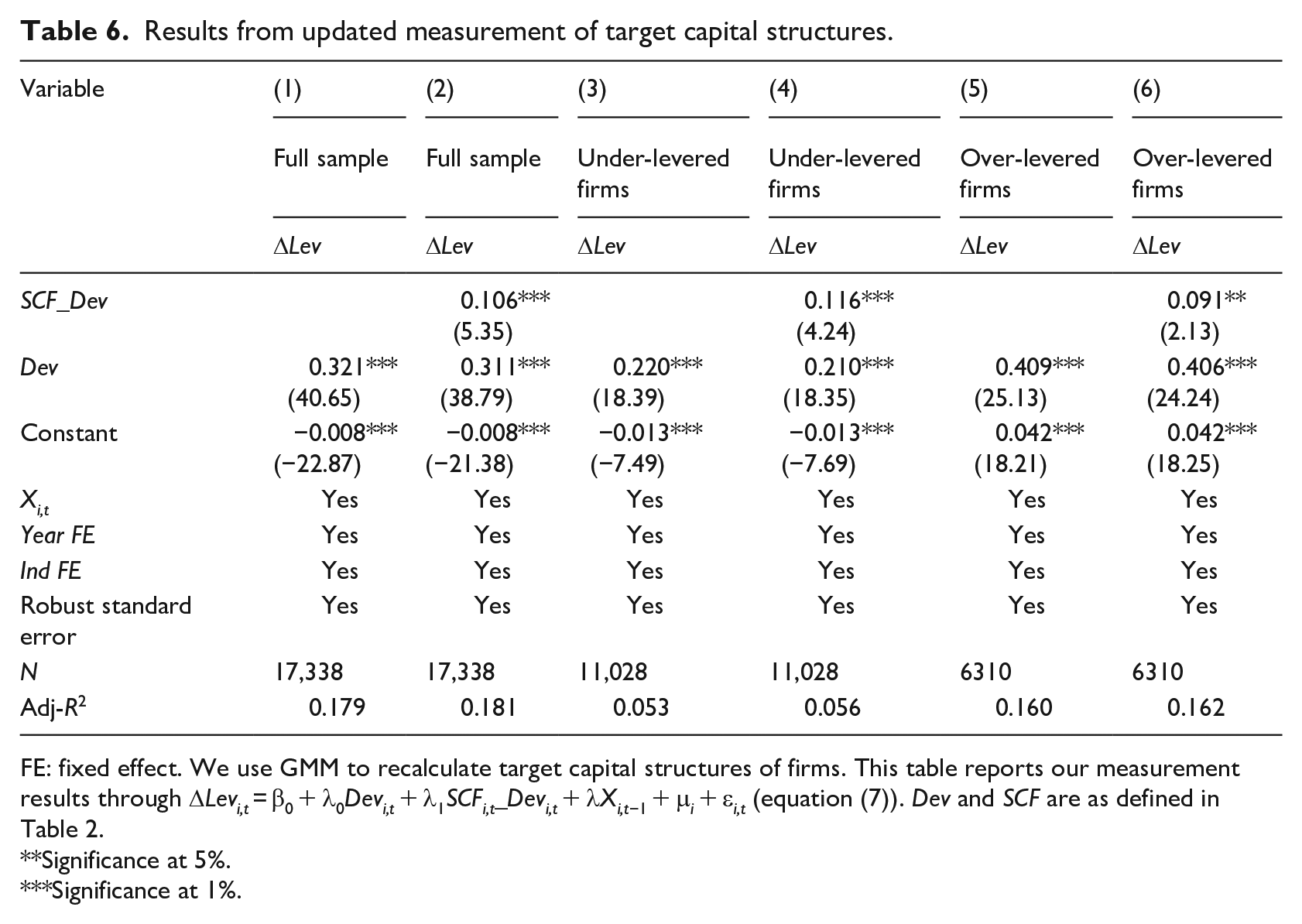

First, we use an alternative measurement of target capital structure. Following Blundell and Bond (1998), we recalculate target capital structures through SYS-GMM and repeat our tests with equation (7). The p of AR(2) in the fitting result is 0.946, and there is no second-order serial correlation. Sargan and Hansen tests, respectively, report p of 0.221 and 0.340, suggesting the robustness of these models. Table 6 reports our test results, which conform to our primary findings.

Results from updated measurement of target capital structures.

FE: fixed effect. We use GMM to recalculate target capital structures of firms. This table reports our measurement results through ΔLevi,t = β0 + λ0Devi,t + λ1SCFi,t_Devi,t + λXi,t−1 + μ i + ε i,t (equation (7)). Dev and SCF are as defined in Table 2.

Significance at 5%.

Significance at 1%.

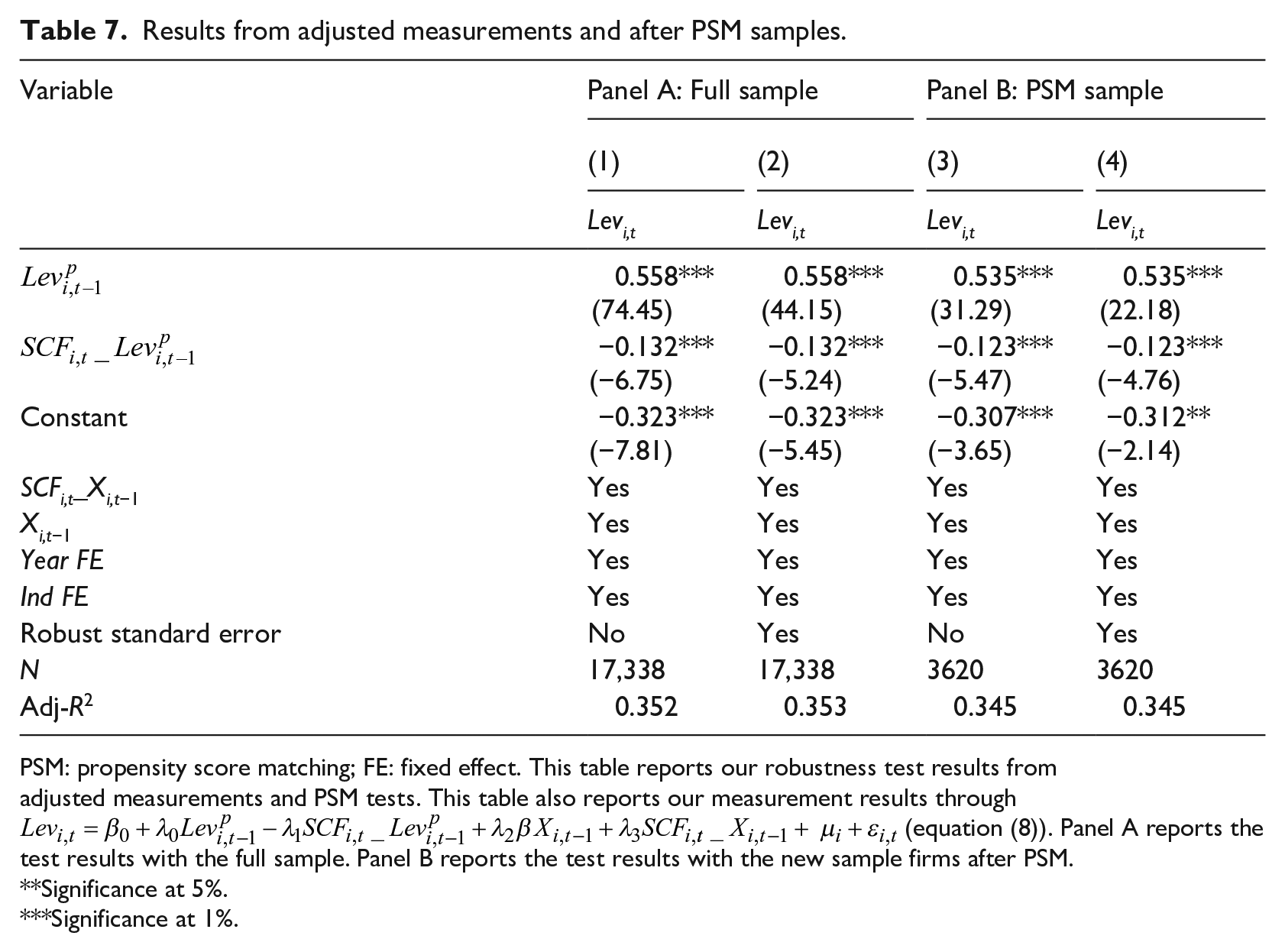

Second, we update our method in the capture of dynamic adjustments of capital structure. Considering that equation (7) may cause large deviations of adjustment speed for fewer accuracies in the measurement of target capital structure, and possible failure to capture the interactions between SCF and capital structure determinants, we directly combine equations (6) and (4) to get equation (8) for FE tests.

In equation (8), since λ1 has a minus sign in front, if this coefficient has a negative value, SCF positively contributes to capital structure adjustment speed, and vice versa.

Table 7 Panel A reports measurement results with equation (8). With or without robust standard error control, the results are consistent with our primary test results on H1.

Results from adjusted measurements and after PSM samples.

PSM: propensity score matching; FE: fixed effect. This table reports our robustness test results from adjusted measurements and PSM tests. This table also reports our measurement results through

Significance at 5%.

Significance at 1%.

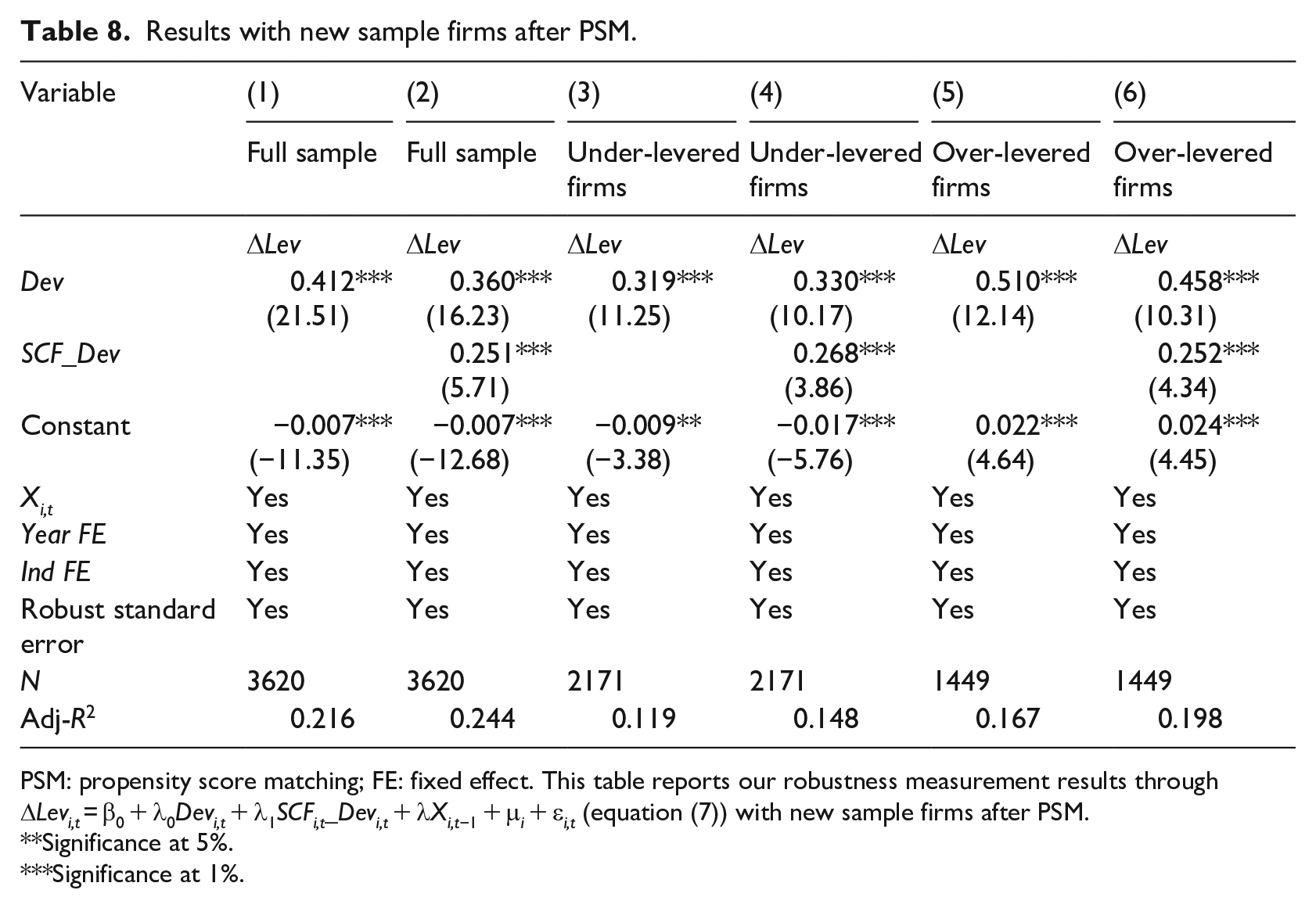

Third, we apply propensity score matching (PSM) for robustness tests. To mitigate the possible endogeneity issue and estimation error from Fama-French Model (FFM), we treat SCF as a dependent variable, and Size, EBIT, Tang, MTB, and Dep as matching variables, with controls over industry and year. We apply a 1:1 matching ratio as in logit regressions to get the closest firms without SCF for the control group. Then, we re-examine SCF impact with the new samples after PSM.

Table 7 Panel B reports the measurement results through equation (8). Table 8 reports our measurement results through equation (7) with the new samples. Both H1 and H2b are further supported. Our findings are still robust through these new tests.

Results with new sample firms after PSM.

PSM: propensity score matching; FE: fixed effect. This table reports our robustness measurement results through ΔLevi,t = β0 + λ0Devi,t + λ1SCFi,t_Devi,t + λXi,t−1 + μ i + ε i,t (equation (7)) with new sample firms after PSM.

Significance at 5%.

Significance at 1%.

5. Underlying mechanisms

As discussed in subsections ‘SCF and capital structure’ and ‘SCF and asymmetric speed in capital structure adjustments’, we further examine financial strengths and competitive advantages as mechanisms underlying our primary findings. Given the data constraints, we cannot examine the risk management needs of firms in this study.

We choose cash holdings (Cash) and competitive advantages (Com) as variables for mediating effect tests, where Cash = (monetary capital + transactional financial assets)/(total assets – cash and cash equivalents), and Com equals the difference in the growth rate of operation income between the firm and the industry average (Fresard, 2010). Extending equation (8), we develop the following equations (9) to (11) to examine the mediating effects of Cash. 5 When ω0 is significantly positive, the λ1 of equations (10) and (11) are both significantly negative, and the absolute value of λ1 in equation (11) is less than λ1 in equation (8), then cash holdings are underlying SCF impact on adjustment speeds.

Similarly, we develop equations (12), (13), and (14) to examine the mediating effects of Com.

In equations (9) to (14), we introduce Cash-related variables, including firm size (Size), growth opportunities (MTB), profitability (EBIT), capital investment (Capex), cash flow from operations (CF), working capital (Nwc), and growth in significant business income (Grow), as well as Com-related variables, including Size, capital intensity (CI), the duality of the chairman and CEO (Dual), the ratio of independent directors on the board (Indr), average board member age (Age), and equity concentration (Share).

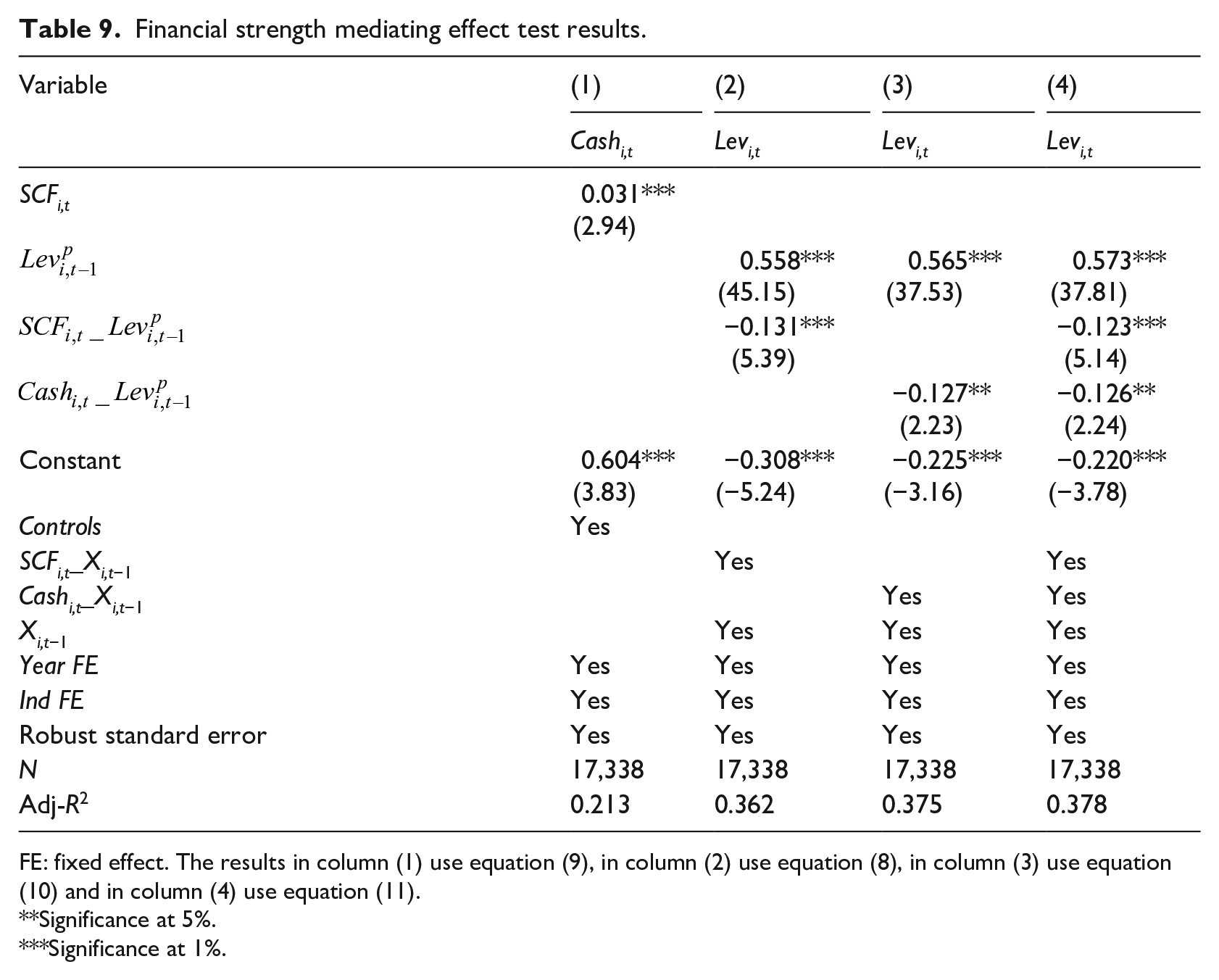

Table 9 reports our financial strength mediating effect test results. Column (1) indicates that SCF and Cash are significantly and positively related, suggesting that SCF positively contributes to the financial strengths of firms. SCF_Levp in Column (2) suggests that SCF accelerates adjustment speeds. Cash_Levp in Column (3) suggests that cash holdings and adjustment speeds of capital structures are significantly and positively related. Column (4) indicates that both SCF_Levp and Cash_Levp are negatively and significantly related to Levi,t. In addition,|–0.123| is smaller than|–0.132| as indicated in Table 7. As a result, our causal mediation analysis suggests that SCF accelerates adjustment speed of capital structures through improved cash holdings. In other words, improved financial strengths are underlying SCF impact on adjustment speeds.

Financial strength mediating effect test results.

FE: fixed effect. The results in column (1) use equation (9), in column (2) use equation (8), in column (3) use equation (10) and in column (4) use equation (11).

Significance at 5%.

Significance at 1%.

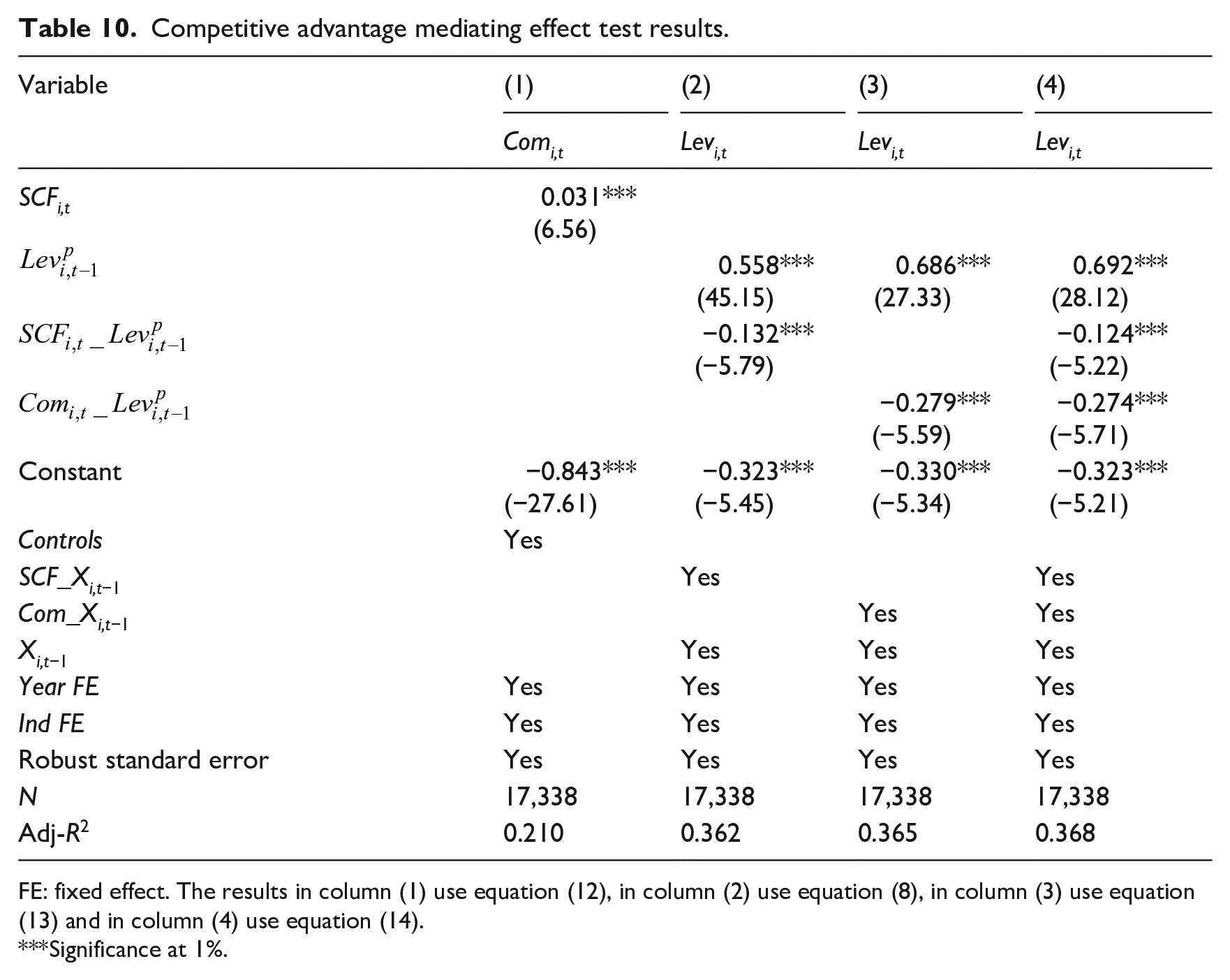

Table 10 reports our competitive advantage mediating effect test results. Like our results in Table 9, these results suggest that SCF accelerates adjustments of capital structures through improved competitive advantages. In short, both improved financial strengths and competitive advantages could be mechanisms underlying our primary findings.

Competitive advantage mediating effect test results.

FE: fixed effect. The results in column (1) use equation (12), in column (2) use equation (8), in column (3) use equation (13) and in column (4) use equation (14).

Significance at 1%.

6. Extended examinations

6.1. SCF, debt costs and alternative mechanism indicators

Since adjustment costs may also be decisive towards a firm’s adjustment of capital structures (Faulkender et al., 2012), we need to explore the relationship between SCF and adjustment costs. External financing happens through either debt or equity markets. Most firms rely on debt, especially bank loans, in their capital structure adjustment (Frank and Goyal, 2004; Hackbarth et al., 2006).

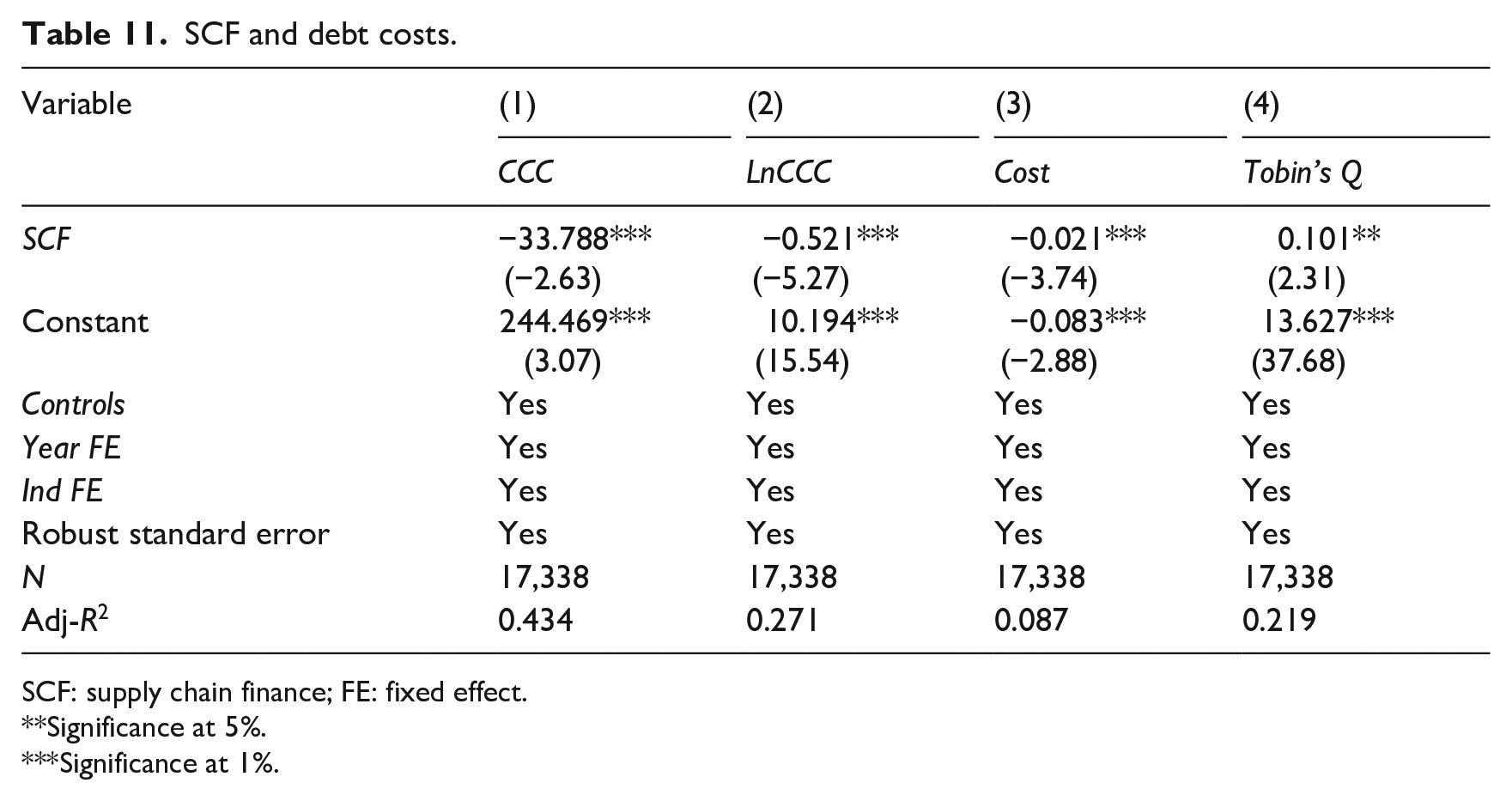

Given that SCF bears the features of being paid earlier and making payment later, SCF improves the capital management efficiency and cash holdings of core firms. We may relate their financial strengths to changes in their working capital efficiency. In the meantime, SCF may strengthen business ties in the supply chains, improve information and logistics flows and enhance competitive advantages. We may relate competitive advantages of firms to their value creation capabilities. As a result, we may define debt financing cost (Cost) as the ‘interest expense divided by the average of short-term and long-term total debt’, CCC as the working capital efficiency indicator (Farris and Hutchison, 2002) measured as ‘accounts receivable turnover + inventory turnover-accounts payable turnover’ and Tobin’s Q as a value creation capability indicator.

Table 11 reports our examination results on SCF, debt costs and alternative mechanism indicators. SCF is significantly but negatively related to Cost, suggesting that SCF may effectively reduce financing costs of firms, which are significant towards capital structure adjustment speeds. SCF is also significantly but negatively related to CCC, suggesting that SCF may effectively shorten cash turnover periods, in conformity with Hofmann and Kotzab (2010). Given China’s inefficient financial and legal systems (Allen et al., 2005), the link between SCF and CCC may be particularly important for core firms. Furthermore, SCF is significantly and positively related to Tobin’s Q, suggesting that SCF may improve firm values.

SCF and debt costs.

SCF: supply chain finance; FE: fixed effect.

Significance at 5%.

Significance at 1%.

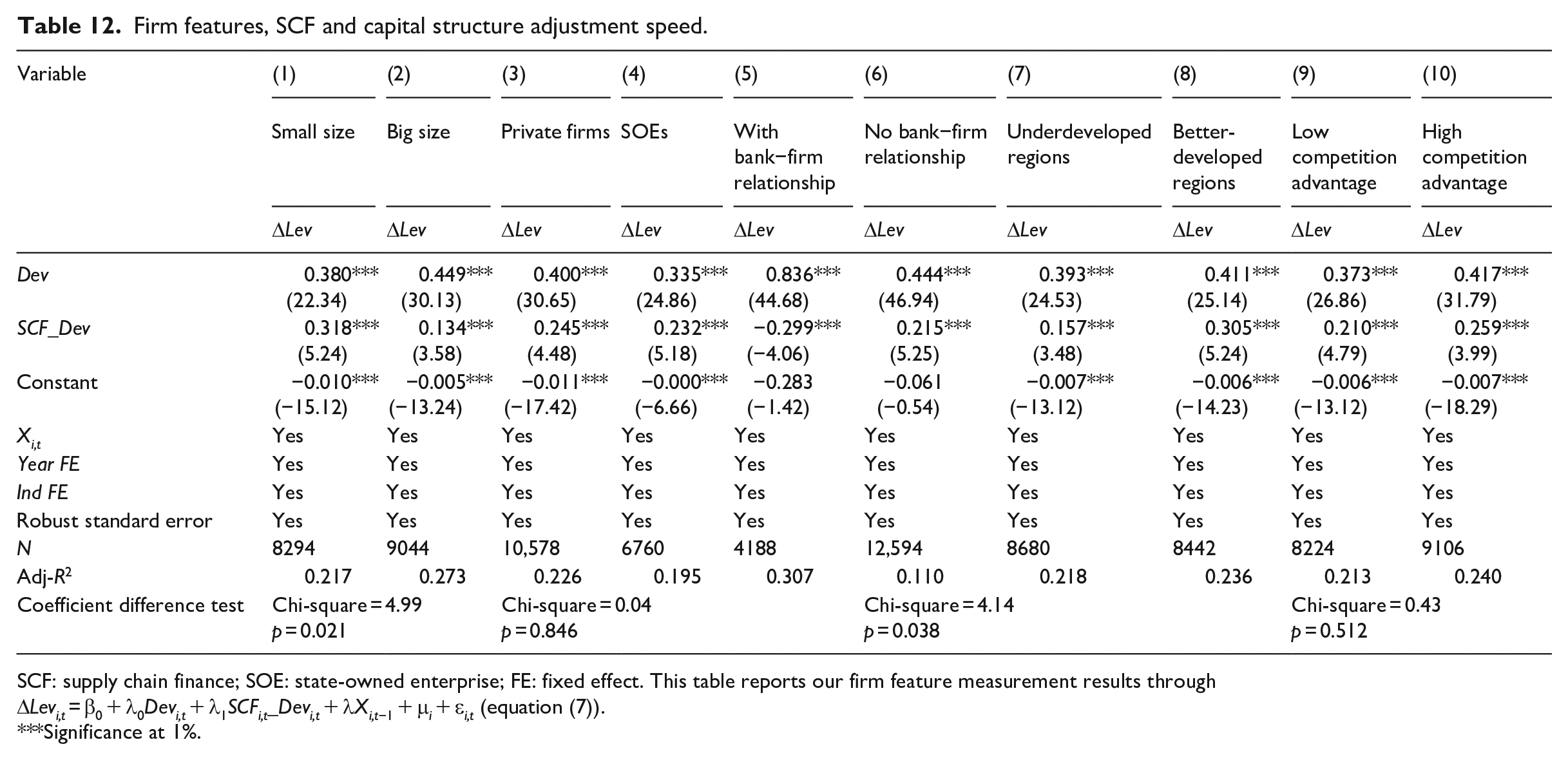

6.2. Firm features, SCF and capital structure adjustments

We further examine firm features, SCF and capital structure adjustments. Firm features include firm size (Byoun, 2008), ownership type (Li et al., 2009), bank–firm relationship (Pan and Tian, 2020), firm location (Wang et al., 2019) and industry-level competition (Peress, 2010). Larger firms may make faster adjustments. State ownership may alleviate the debt constraint of firms and reduce motivation for SOEs to adjust capital structures (Xu et al., 2015). In comparison, private firms are often disadvantaged in access to financial resources. Bank–firm relationship (BC) measured by a dummy on whether a bank or a firm hold each other’s shares or a firm executive has a banking background, may also affect access to bank loans. A firm’s location in a developed or an under-developed region may also affect its access to capital and funding costs. The degree of competition in the industry (HHI) measured as the firm’s concentration in its industry may be another feature affecting its capital adjustments.

Table 12 reports our examination results. Columns (1) and (2) indicate that SCF is significantly and positively related to capital structure adjustment speeds among both smaller and larger firms. In comparison, SCF impact is much stronger among smaller firms at 83.68% (0.318/0.380) than among larger firms at 29.84% (0.134/0.449). Since smaller-sized firms are subject to more financing constraints, SCF may have effectively alleviated these constraints and contributed to higher speeds of capital structure adjustments. Columns (3) and (4) indicate that SCF impact on adjustment speeds seems indifferent between SOEs and private firms, without bias towards ownership types. Columns (5) and (6) suggest that SCF impact is different towards firms with or without bank–firm relationships. SCF may be an effective substitute for a bank–firm relationship for firms without bank connections. Columns (7) and (8) indicate that SCF impact is more robust in better-developed regions, suggesting that the development of financial markets may strengthen SCF impact on capital structure adjustments. Columns (9) and (10) indicate that SCF impact is similar among firms across industries with various degrees of competition, suggesting that the level of competition would not affect SCF impact on a firm’s capital structure adjustment speed.

Firm features, SCF and capital structure adjustment speed.

SCF: supply chain finance; SOE: state-owned enterprise; FE: fixed effect. This table reports our firm feature measurement results through ΔLevi,t = β0 + λ0Devi,t + λ1SCFi,t_Devi,t + λXi,t−1 + μ i + ε i,t (equation (7)).

Significance at 1%.

6.3. Environmental dynamism, SCF and capital structure adjustments

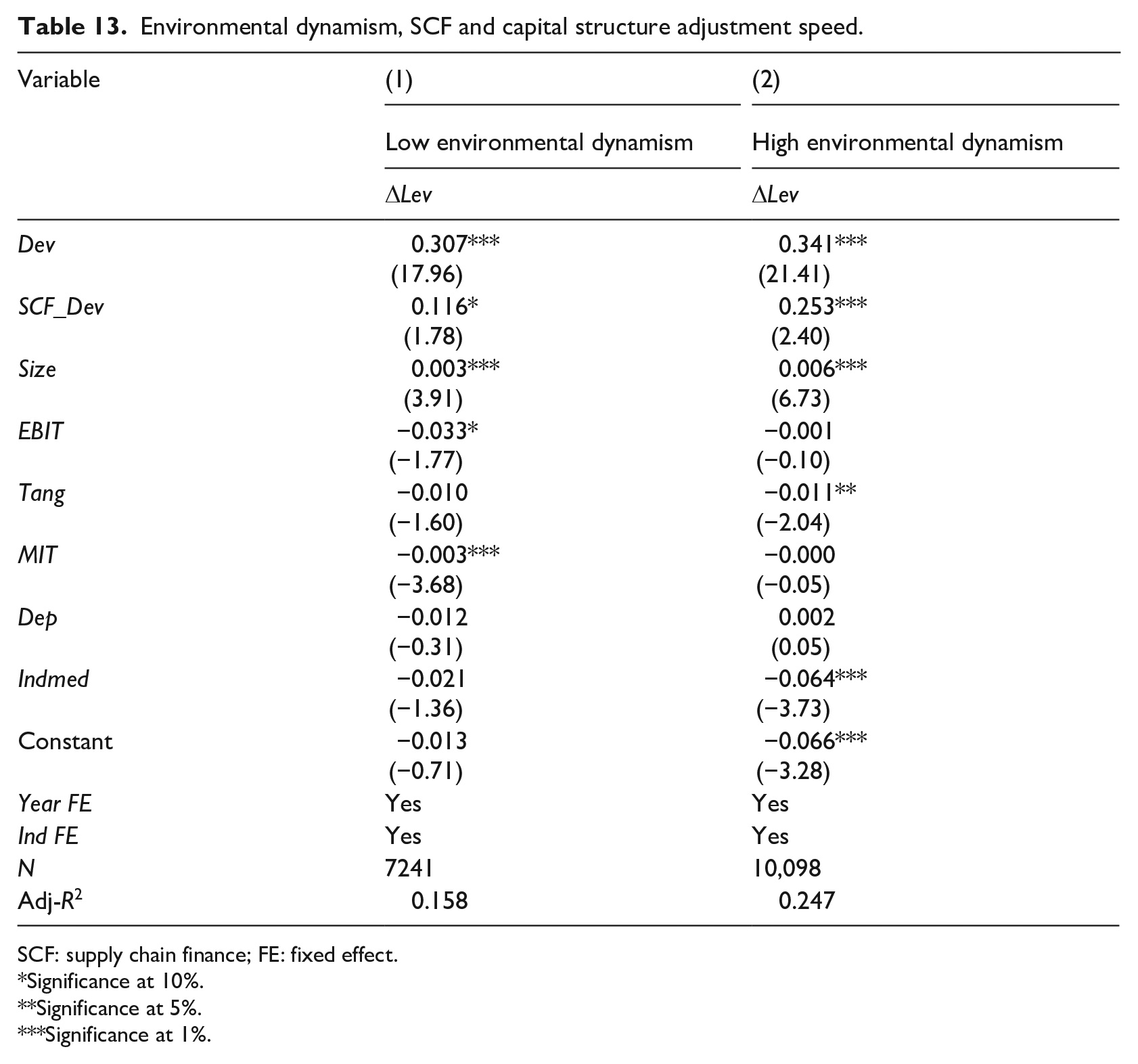

We also examine the impact of environmental dynamism. Increasing dynamism of the external environment may lead to greater uncertainty or unpredictability of firm performance (Boyd, 1995; Dess and Beard, 1984). We adopt the standard deviation of a firm’s sales income over the past 5 years as a proxy for environmental dynamism (Cheng and Kesner, 1997; Ghosh and Olsen, 2009). 6 We divide sample firms into high and low dynamism groups and repeat our primary test. Table 13 reports our test results, which suggest that SCF may better accelerate capital structure adjustments among firms with higher environmental dynamism and help firms to cope with greater uncertainty in the market.

Environmental dynamism, SCF and capital structure adjustment speed.

SCF: supply chain finance; FE: fixed effect.

Significance at 10%.

Significance at 5%.

Significance at 1%.

7. Conclusion

We present evidence that SCF can significantly contribute to faster capital structure adjustments. Such an impact is more substantial among under-leveraged firms. Improved financial strengths and enhanced competitive advantages are underlying SCF impact. Further examinations suggest that SCF leads to faster cash turnovers, lower financing costs and higher firm values. In other words, SCF may comprehensively improve capital structure adjustment from various aspects. Our extended measurements suggest that SCF has a stronger impact on capital structure adjustment by smaller firms, those without a bank–firm relationship, those located in better-developed regions and those in higher environmental dynamism. SCF impact is also indifferent towards ownership types or levels of competition across various industries.

In other words, SCF may effectively alleviate the financing constraints of smaller firms, substitute the bank–firm relationship in a firm’s access to bank loans, stimulate firm development with more financial resources, overcome the traditional bias towards private ownership, and facilitate capital structure adjustments across industries regardless of the level of competition in the market. Given noticeable environmental dynamism arising from the Covid-19 pandemic, trade wars, Brexit and so on, SCF may help firms to better cope with increased uncertainty or unpredictability of the market. The positive economic consequences may also suggest that SCF has become a meaningful new ingredient in China’s financial infrastructure, which may also be vital for high quality and sustainable economic growth in the post-GFC era.

Our study may bear such practical implications that core firms take advantage of SCF to optimise their capital structure and enhance firm value and their competitiveness. Government policies may encourage SCF to benefit more upstream and downstream SMEs in supply chains and effectively alleviate their financial constraints. Furthermore, core firms may adopt finance technology (Fintech), such as big data, block chain and artificial intelligence, to develop more integrated, symbiotic and digitalised SCF platforms to achieve continuously and sustainably better products and services. In the meantime, better risk management, such as real-time warnings, would also serve sustainable supply chains and benefit the real economy.

For the emerging markets, financial reforms and infrastructure investment would allow more financial products and services and enrich the flexibility of SCF in the long-term. Given the growing demand for banking services and products from SCF, banks may consider its heterogeneity as well as supply chains in their financial innovations, which may also be vital future research topics for informing sustainable economic growth.

Footnotes

Final transcript accepted 18 March 2022 by Xiaoping Zhao (AE, Special Issue).

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study is funded by the National Social Science Fund Major Project (19AGL010), National Social Science Fund Youth Project (18CJY027) and Shandong Provincial Natural Science Foundation, China (ZR2019MG004, ZR2020MG030).