Abstract

A “new” neoclassical international political economy (NNIPE) emerged from the 2008 financial crisis showing how macroprudential regulation and capital controls (MPR-CC) can eliminate the systemic risk behind endogenous financial cycles. An implication of this is that decentralized capitalism is inherently financially unstable, which appears to make inroads with heterodox traditions. However, this paper demonstrates that NNIPE represents a superficial, rhetorical appearance of theoretical improvement, as represented in its “style,” while the “substance” of its underlying assumptions and mechanisms remain mired in neoclassicism. Moreover, it grew out of ideologically-motivated ideational change at the International Monetary Fund.

Keywords

1. Introduction

The 2008 financial crisis provided economics with many important insights. Among them, it was found that the economies that used macroprudential regulation and capital controls (MPR-CC) recovered faster than those that did not. Moreover, the crisis evolved from investment banks using off-balance sheet vehicles to leverage capital, unequivocally displaying capitalism’s ability to endogenously generate systemic risk. This questioned the core of neoclassical political economy’s “conventional wisdom” (Galbraith 1958), and created Grabel’s productive incoherence era, described as:

the proliferation of responses to the crisis by national governments, groups of countries, multilateral institutions, and the economics profession that to date have not congealed into a consistent, singular approach… [that]… is intended to signal the absence of a unified, consistent, universally applicable (new) view. 1 (Grabel 2015: 1)

Since the neoclassical school’s focus on microeconomic self-regulation could not explain these issues, it had to change to stay relevant. It substituted microeconomic atomistic risk for macroeconomic systemic risk and led to a need to explain how the latter (a) is endogenously created and (b) can, if at all, be addressed.

This is where the “new” neoclassical international political economy (NNIPE) became indispensable, as represented by Gourinchas and Jeanne (2013), Jeanne (2012, 2013a, 2013b, 2016), Jeanne and Korinek (2010 and 2013, 2014), Korinek (2011, 2013), and Jeanne, Zettelmeyer and Ostry (2008). 2 Consistent with New Keynesianism, the framework states asymmetrically distributed financial information prevents borrowers and lenders from fully internalizing the social welfare effects of their decisions, thereby endogenously generating systemic risk. If an outside shock occurs, the price-signaling mechanism becomes inoperative from financial instability, and social welfare is reduced. However, NNIPE shows MPR-CC can eliminate this by raising borrowing/lending costs relative to marginal returns, removing the wedge between aggregate private and social welfare.

These properties make NNIPE notable for two reasons. First, it echoes the 2008 financial crisis insight that agents’ decision-making endogenously produces systemic risk. Second, it implies decentralized capitalism is inherently unstable—mirroring heterodox traditions and raising questions about potential syntheses. 3

This paper demonstrates that such similarities with heterodoxy are superficial because while NNIPE may have “style” by echoing 2008 financial crisis insights and mirroring heterodox traditions, it lacks methodological and theoretical “substance.” To be clear, the paper’s contention is that NNIPE represents a superficial, rhetorical appearance of theoretical improvement, as represented in its style, while the substance of its underlying assumptions and mechanisms remain mired in neoclassicism. Thus, NNIPE leveraged productive incoherence to minimally alter political economy’s conventional wisdom while maintaining the discipline’s overall ideational power distribution. Further, the International Monetary Fund (IMF) promoted NNIPE because of its own desire to rehabilitate its image within post-2008 ideational dialog.

This paper is organized as follows. Part 2 examines NNIPE in greater detail. The author shows how NNIPE argues asymmetrically-distributed financial information endogenously produces systemic risk and reduces social welfare, which MPR-CC corrects. It then discusses how this welfare maximization exercise was subsequently extended to a variety of topics. Part 3 begins the critique of NNIPE. It first demonstrates that NNIPE suffers from the same methodological shortcomings as Friedman’s positivism and that the assumptions underlying its analysis do not exist in any capitalist system. Second, it uses Minsky’s theory to highlight how financial relations endogenously evolve in capitalism and therefore systemic risk can never be eliminated, directly contradicting NNIPE. Part 4 reveals how the IMF provided early promotional outlets for NNIPE and makes an argument for why the institution offered its support. Part 5 summarizes the arguments made throughout the paper.

2. The Core Mechanisms of the “New” Neoclassical International Political Economy

NNIPE accepts all New Keynesian microfoundations except that now incomplete financial markets asymmetrically distribute all pertinent financial information, preventing borrowers and lenders from fully internalizing their portfolios’ social welfare effects. This skews asset prices from their intrinsic values, distorts prices, and generates systemic risk, which persists until an exogenous shock causes financial instability and a welfare loss equal to the wedge between aggregate private and social welfare. Anton Korinek, one of NNIPE’s core developers, states:

Individual market participants do not internalize their contribution to aggregate financial instability when they make their financing decisions. As a result, they impose externalities in the form of greater financial instability on each other, and the private financing decisions of individuals are distorted towards excessive risk-taking. (Korinek 2011: 1)

Another NNIPE founder, Olivier Jeanne, adds:

Frictions in the credit market lead to an amplification mechanism in which growth in credit and asset prices feed on each other, positively in the boom and negatively in the bust. Individual agents tend to overborrow in the boom because they do not take into account the impact of their borrowing on aggregate systemic risk. (Jeanne 2012: 203–4)

Note how NNIPE uses the New Keynesian “otherwise, for only-if ” assumption to posit that intertemporal-optimizing actors would “otherwise” produce Pareto efficiency “for only-if ” financial information was equally diffused. For example, Korinek maintains, “financial amplification effects occur only when financial markets are imperfect,” implying asymmetric distribution of information is the main issue; “otherwise” the efficient markets hypothesis would hold “for only-if ” there was not a wedge between private and social welfare (Korinek 2011: 5).

NNIPE’s policy response centers on MPR-CC eliminating this problem by raising borrowing/lending costs relative to the transaction’s return. In turn, this transforms MPR-CC from market distorting tools into Pigouvian-type welfare solutions, now making them acceptable to neoclassicism despite being a market impediment.

After this initial formulation, NNIPE authors applied it to a variety of other topics, such as macroprudential considerations (Jeanne 2013a; Jeanne and Korinek 2013, 2014); capital flow issues (Gourinchas and Jeanne 2013; Jeanne 2012; Korinek 2011, 2013); reserve accumulation strategies (Jeanne 2016); credit boom and bust containment (Jeanne and Korinek 2010); international crisis lending and IMF conditionality (Jeanne, Zettelmeyer, and Ostry 2008); and the real exchange rate (Jeanne 2013b). For example, Jeanne shows if the “private marginal gain from reserves… does not coincide with the social marginal gain from reserves… there is a true pecuniary externality coming from the fact that private agents do not internalize the impact of international reserves… which determines [emerging market agents’] access to credit ex ante” (Jeanne 2016: 571). However, since MPR-CC can eliminate this, while the issue considered flexibly changes, NNIPE’s analytical framework and solution remain constant.

This process of MPR-CC fully eliminating endogenously created systemic risk is crucial for why NNIPE rehabilitated post-2008 neoclassical international political economy. Indeed, recall the crisis displayed an endogenous origin, and varying national responses confirmed the efficacy of MPR-CC. NNIPE accounts for both these facts, while preserving prior neoclassical assumptions, mechanisms, and conventional wisdom. It is this feature as to why the author contends NNIPE represents a superficial theoretical improvement, giving it rhetorical style, despite its underlying substance being neoclassicism’s flawed assumptions and mechanisms.

3. A Methodological and Theoretical Critique of NNIPE

NNIPE’s focus is on how asymmetric distribution of financial information prevents market actors from internalizing the social welfare effects of their decisions, leading to systemic risk that MPR-CC eliminates. This has methodological and theoretical flaws.

3.1 NNIPE and Friedman’s Positivism

Milton Friedman argued in 1953:

The only relevant test of the validity of a hypothesis is comparison of its predictions with experience [because,] the relevant question to ask about the “assumptions” of a theory is not whether they are descriptively “realistic”… but whether… the theory works, which means it yields sufficiently accurate predictions. (Friedman 1953: 8–9, 15 italics in original)

NNIPE’s discussion of how MPR-CC eliminates endogenously created systemic risk resembled empirical facts, giving it style. For Friedman and NNIPE authors, this positivism and “conformity of experience to the [policy] implications” would then validate the rest of the framework, regardless of the assumptions’ realism (Friedman 1953: 15).

However, the realism of assumptions matters because that is what gives a framework its substance. For example, if one starts with fictitious assumptions and irrefutable logic subsequently occurs, the deductive conclusions cannot reflect reality outside of a spurious correlation (Crotty 2013). Moreover, Lee pointed out that empirical reality is structured by socially and historically conditioned environments, and explanations of those environments depend on sets of assumptions underlying the explanations themselves. Therefore, “the difference between… true and false theories is how well their explanations correspond to the historically contingent economic events being explained,” meaning the assumptions need realistic properties (Lee 2003: 174).

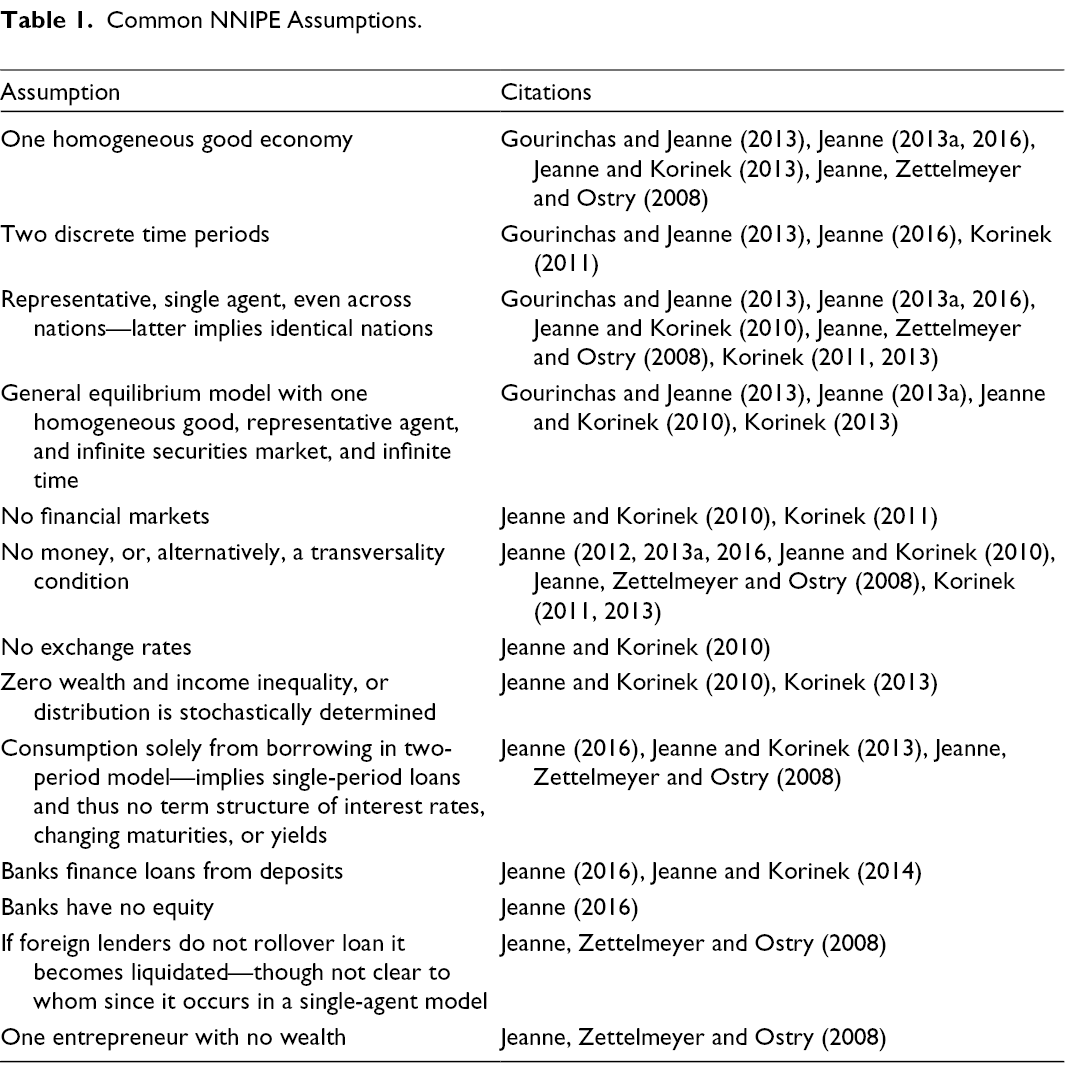

Table 1 is a list of assumptions commonly appearing in NNIPE literature, with the left-hand column naming the assumption and the right-hand column giving the citation in which it appears. These assumptions are prominently featured directly in the main texts, not footnotes. This is important because not a single one plausibly exists anywhere in the capitalist world, yet they are preconditions on which the entire framework is based. For example, NNIPE commonly assumes a single-agent, nonmonetary, homogenous-good, infinite-time economy, which precludes any financial transaction from taking place—yet this is a model of just that! Thus, while its policies have rhetorical style by echoing post-2008 reality, this is only a superficial connection since NNIPE’s foundations lack substance.

Common NNIPE Assumptions.

3.2 NNIPE’s Internalization of Systemic Risk and Hyman Minsky

In Minsky’s financial fragility hypothesis, the biggest question a lender asks a prospective borrower is how the loan will be repaid since this is the lender’s overriding concern. After examining income statements and credit histories, the lender will build a margin of safety into the deal if s/he decides to lend, the funds will exchange hands, and the borrower starts an amortization schedule. During an expansion, the parties develop certain hypotheses.

As the boom’s rising aggregate income allows the borrower to meet or exceed amortization commitments, s/he recognizes the return could increase with a second and/or larger loan. Moreover, this individual is increasingly capable of meeting larger commitments due to the boom, and justifiably becomes more bullish since past and current payments met or exceeded contracted commitments. If the borrower takes out another and/or larger loan, his or her leverage increases.

At the same time, the lender sees the borrower met or exceeded amortization commitments, which improves the latter’s credit score. This justifies the lender granting the second/larger loan, and with less of a safety margin. Further, as the borrower’s amortization and credit history make the lender more bullish on the future, s/he increases the exposure ratio.

As this borrowing/lending dynamic becomes widespread, rising aggregate income provides debtors with (a) the funds necessary to meet amortization payments, and (b) credit scores justifying new and/or secondary loans. Over time, this evolving relationship endogenously produces lower margins of safety, higher leverage and exposure ratios, an aggregate payments chain growing exceedingly complex, and actors whose actions are justified because they followed the credit risk models. In such an environment, it only takes a small disruption to set off financial instability, debt deflation, and insolvency. Minsky did not need asymmetric information to reach this result; he just highlighted how rising aggregate income causes borrowers and lenders to rationally become increasingly bullish as creditworthiness, leverage, and exposure ratios climb and margins of safety decrease.

Minsky’s model directly contradicts NNIPE. NNIPE argues systemic risk comes from borrowers and lenders being unable to internalize the social welfare effects of their decision-making, which MPR-CC eliminates. However, if credit scores, repayment histories, and prospective income streams point toward a loan being made, borrowers/lenders will close the deal regardless of whether actors can internalize it. It makes no difference to the loan officer and/or borrower if s/he can internalize these effects; if the incentive is to make a loan, that is what will be done. Thus, arguing systemic risk occurs because borrowers/lenders cannot internalize welfare is erroneous—even if they “otherwise” could, the loan will still advance if the pro forma indicates it should happen, and there would be systemic risk.

One may object that MPR-CC can at least force agents to internalize welfare effects and eliminate systemic risk, even if they are unwilling to. This would be a reformulation of NNIPE’s position. NNIPE argues MPR-CC have value because actors are unable to internalize welfare effects, which is different from being capable of but choosing not to. In the former, MPR-CC eliminates risk; in the latter, more appropriate sets of policies might tackle the issue, such as changing incentive structures.

However, there is another, more important Minskyian critique of NNIPE. A fundamental property of Minsky’s analysis is that it is evolutionary, meaning no single set of MPR-CC can eliminate systemic risk. For him, systemic risk is an inherent part of capitalism because it is endogenously produced by agents rationally lowering margins of safety and raising leverage and exposure ratios as they respond to profit opportunities—captured by the “stability is destabilizing” quote. Hence, a second theoretical flaw in NNIPE involves its assertion that MPR-CC can eliminate systemic risk because Minsky’s point is that systemic risk is endogenously created and evolves, meaning such tools only alter agents’ exposure to it by redistributing risk across varying segments of financial systems, which may be warranted, but implies systemic risk cannot be eliminated, contradicting NNIPE.

4. The Intellectual Origin and Early Support for NNIPE

J. Fagg Foster argued, “all institutional modifications must be capable of being incorporated into the remainder of the institutional structure,” which “discloses the limits of adjustment… in terms of degree” (Foster 1981: 933–4). An implication of the “minimal dislocation” principle is if a given modification can uphold as much of a previous institutional structure as possible while accounting for “changes [that] occur in the given data” with “answers [that]… change accordingly,” it will experience rapid popularity since it serves vested interests’ needs by being easily integratable with conventional wisdom (Foster 1981: 934).

The author previously noted one of the biggest takeaways of the 2008 financial crisis was that it endogenously evolved to produce systemic risk and that MPR-CC tempered it. Thus, if neoclassicals wanted to maintain conventional wisdom and retain the preexisting ideational power structure, they needed to account for this while “minimally dislocating” “the remainder of the institutional structure.” This is where NNIPE proved its worth, since it employs a neoclassical framework with a single altered assumption. This appealed to the IMF, whose own reputation was in need of a makeover.

By the mid-2000s, the IMF’s influence was at an all-time low owing to its past capital account and financial governance failures (Grabel 2015). When the 2008 financial crisis struck, it recast its image on MPR-CC through “IMF Staff Position Note No. 4” in 2010 (Ostry et al. 2010), and again in 2012 and 2013, respectively, with “The Liberalization and Management of Capital Inflows: An Institutional View” and “Guidance Note for the Liberalization and Management of Capital Flows”—the latter two requiring Executive Board approval. The Fund notes throughout these documents that international capital flows can cause instability, a premature opening of the capital account is the most likely culprit, and inflow/outflow measures may lead to stabilization. Table 2 reproduces conditions from the 2012 paper for when MPR-CC are permissible.

The IMF’s Institutional View for When Capital Controls Are Acceptable.

* Source: IMF (2012).

Similarly, figure 1 features the types of environments in which MPR-CC should be used, which comes from the 2013 “Guidance Note.”

The IMF’s environment for using MPR-CC. Source: IMF (2013).

If the practical applicability conditions in table 2 or environment of figure 1 are critically analyzed, it is apparent the IMF’s scope for MPR-CC is extremely narrow, essentially an “if-you-unfortunately-must” perspective. Table 2 confines MPR-CC to a status of “last resort,” while the environment of figure 1 features a triple imbalance crisis. Given these extreme restrictions, why would the IMF even endorse MPR-CC? The author’s answer to this query is that the IMF recognized these tools’ efficacy because this enabled it to newly rehabilitate its image and claim ideational evolution while largely maintaining conventional wisdom—just as with NNIPE. Consequently, the Fund lent critical early support to NNIPE because at the time the latter’s “otherwise, for only-if ” assumption was a natural complement to its own “if-you-unfortunately-must” perspective, 4 with the organizational benefit being that doing so would restore its status as the leading influence in international political economy.

The Fund was unquestionably NNIPE’s most important source of support. Its current Deputy Director of Research, Jonathan D. Ostry, coauthored one of the earliest NNIPE papers (Jeanne, Zettelmeyer, and Ostry 2008). In acknowledgments, NNIPE authors commonly thank the IMF for financial support (Korinek 2013), productive comments (Jeanne 2016; Korinek 2011), workshop and conference interaction (Jeanne and Korinek 2010; Jeanne, Zettelmeyer, and Ostry 2008; Korinek 2013), or Visiting Scholar appointments (Korinek 2011). Further, individuals not directly at, but closely associated with, the IMF are frequently extended gratitude (Jeanne 2012, 2013a). Finally, Korinek (2011), arguably the most important NNIPE paper in terms of content and readership, started as an IMF Working Paper and was later published in the IMF Economic Review. Thus, when NNIPE was a burgeoning school of thought, the IMF stepped in and afforded its authors camaraderie, finance, research and publication platforms, and academic support. It is the author’s contention that the Fund did so then because both approaches shared a vested interest in slightly shifting conventional wisdom to reflect contemporary stylized facts while not going so far as abandoning the previous ideational power distribution. This created a symbiotic relationship and would imply NNIPE grew out of ideologically motivated ideational change at the IMF.

5. Conclusions on NNIPE

This paper illustrates that NNIPE’s core property is a superficial, rhetorical appearance of theoretical improvement, lending it style in that it mimics insights from the 2008 financial crisis, yet its substance lacks realistic assumptions and theoretical mechanisms. After presenting the core of NNIPE in part 2, part 3 highlighted how NNIPE superimposed pertinent policies onto a neoclassical framework to claim it could eliminate endogenously created systemic risk, which garnered significant ideational prestige at the time. However, in doing so, it nonetheless retained unrealistic assumptions and missed that (a) even if agents could internalize welfare effects, they would not do so if a deal should be made, and (b) financial relationships endogenously evolve over time, meaning these tools redistribute risk, not eliminate it. Nonetheless, NNIPE enjoyed early support from the IMF, which the author argues was done because it enabled the Fund to rehabilitate its image and reassert itself as the dominant intellectual influence in international political economy.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Author Biography