Abstract

While performance-related pay (PRP) has been implemented in most OECD countries over the past four decades, its effectiveness is still up for debate. What is under-investigated in the previous literature is under what conditions the public sector can effectively implement an optimal design of a PRP system. This study investigates how the target of PRP, the design of performance pay, and organizational context affect the effectiveness of PRP. The findings indicate that PRP has a positive association with organizational performance but the aspects of performance it affects differ depending on to whom it is implemented and how PRP is designed. This study also finds that the positive effect of PRP for top executives is attenuated if organizational outcomes are not easily observable. This article suggests that public managers should pay careful attention to employee characteristics, pay design, and organizational contexts for the successful implementation of PRP in the public sector.

Introduction

Performance-related pay (PRP), the pay scheme that attempts to link individual effort and outputs to compensation, has long been practiced both in private and public sectors. The underlying assumption behind PRP is that organizational performance will increase as incentives are tightly aligned with individual performance that achieves organizational goals (Heinrich & Marschke, 2010; Moon, 2000). Since the late 1970s, the public sector has embraced this notion with the new public management wave and broadly applied pay-for-performance systems for government employees (Bellé, 2015; Perry et al., 2009; Spano & Monfardini, 2018). While it has already been four decades since PRP first received attention in many OECD countries, its popularity has not declined; rather, it is receiving renewed interest in many countries (Bellé, 2015; Jones & Hartney, 2017).

Despite broad implementation in the public sector across the globe, the literature that synthesized the studies on PRP are inconclusive about PRP’s effects on organizational performance (Hasnain et al., 2012; Perry et al., 2009; Weibel et al., 2009). It is, however, not a surprising conclusion considering the multifaceted dimensions of PRP. The public sector can employ PRP in a variety of ways with respect to pay design (e.g., incentive size; whether to link incentives to individual, team, departmental, or entire organizational performance), the target of PRP (e.g., senior civil servants only, or all employees; employees with high motivation or with low motivation), and performance measurement (e.g., who measures performance; whether performance is measured with quantitative or qualitative criteria; how performance is linked to compensation). Additionally, PRP outcomes may vary depending on the organizational context in which PRP is implemented. These complex facets of PRP imply that it is important to disentangle the relationship between various dimensions of PRP and organizational outcomes by considering specific conditions under which an incentive system is effective.

The complex relationship between PRP and organizational performance has already been emphasized in previous literature (Heinrich, 2007; Perry et al., 2006, 2009; Weibel et al., 2009). For example, Perry et al. (2009) called for scholarly attention to find “effective contingent pay designs for public contexts,” by noting that “a variety of antecedent employee and organizational characteristics and environmental conditions, together with pay system design, affect critical intermediate variables . . . [which], in turn, influence affective and performance outcomes” (p. 41). This study is a response to this earlier call, given the research focusing on moderating factors in the public sector is still limited (Bregn, 2013; Weibel et al., 2009). Specifically, by utilizing the data of 30 public enterprises in South Korea over the 2012 to 2018 period, this study examines how the target of PRP, pay system design, and organizational contexts moderate the relationship between PRP and organizational performance.

The findings of this study add evidence to the view that it is important to design an incentive system with careful attention to the target of the program (e.g., top executives versus mid- and low-level employees), pay design (e.g., organization-based incentives versus individual- or team-based incentives), and organizational context (based on the observability of organizational outcomes). First, this study finds that PRP generally has a positive association with organizational performance—but its effect depends on whom PRP targets. When implemented for chief executives, PRP has a positive association with financial performance; when implemented for mid- and low-level employees, it has a positive association with managerial performance. Second, this study shows that pay design also matters in terms of having impacts on differing aspects of performance. When incentives are tied to individual- or team-based performance pay, PRP is likely to have a positive association with financial performance; when incentives are linked to organizational performance, PRP has a positive association with advancing public values.

Importantly, this study cautions against generalizing the impact of PRP by showing that the same incentive system can produce different outcomes depending on organizational contexts. By applying Wilson’s (1989) typology, which classifies public organizations based on the observability of organizational outcomes, this study finds that the positive effect of PRP for top executives is attenuated in organizations where it is difficult to quantitatively measure organizational outcomes or attribute the desired end results to organizational outcomes. Supporting earlier arguments that PRP can yield different outcomes depending on contextual factors (Chenhall, 2003; Perry et al., 2006, 2009; Weibel et al., 2009), this study shows that one size does not fit all when implementing a PRP system. Public managers should consider organizational context and various intermediate factors of PRP before introducing a contingent pay system in the public sector.

Literature Review

Principal-agent theory, expectancy theory, and reinforcement theory are prevailing theories that support the implementation of PRP (Hasnain et al., 2012). Principal-agent theory deals with designing a contract to address two agency problems—adverse selection and moral hazard—that result from the information asymmetry between principal (the employer) and agent (the employee) (Alvarez & Hall, 2006; Holmstrom & Milgrom, 1991). Adverse selection occurs because the agent has more private information than the principal before signing the contract—PRP can serve as a tool to filter out poor personnel and attract capable employees who expect to benefit from a performance pay system (Delfgaauw & Dur, 2008; Hasnain et al., 2012; Heinrich, 2007). Moral hazard happens because the level of effort the agent exerts is not readily observable to the principal. In that case, the principal can design a contract to incentivize the agent to exert effort for his own benefit by tying pay to the agent’s performance (Hasnain et al., 2012; Heinrich, 2007; Miller, 2005).

Expectancy theory (Lawler, 1971, 1981; Porter & Lawler, 1968; Vroom, 1964) focuses on the relationship between effort, performance, and outcomes. According to expectancy theory, individuals make behavioral choices based on their expectations of the extent to which their behaviors will lead to desired outcomes (Kellough & Lu, 1993). Because the motivation of individuals to exert effort is greatest when there is a tight relationship between effort, performance, and outcomes (Hasnain et al., 2012; Kellough & Lu, 1993), expectancy theory implies that it is important to convince employees that their performance has a tight linkage with outcomes, and positive outcomes are highly probable if they make the effort to perform well (Kellough & Lu, 1993).

The premise of reinforcement theory is that individual behaviors are “a function of contingent consequences” (Luthans & Stajkovic, 1999), and target outcomes are the result of reinforced behaviors (Perry et al., 2006; Skinner, 1969). Thus, to produce desirable organizational outcomes, managers in the workplace should identify the correct reinforcers that increase functional performance behaviors (Luthans & Stajkovic, 1999). In the case of PRP, reinforcement theory suggests that it is important to find the right reinforcer (e.g., pay) that intensifies employee behaviors linked to desirable organizational outcomes. The implication of reinforcement theory for PRP design is that individual behaviors must be observable and measurable so that the behaviors can be modified with a reinforcer.

On the other hand, motivation theories emphasize “the hidden costs of rewards” (Lepper & Greene, 1978), by focusing on individuals’ intrinsic and extrinsic motivations. Motivation-crowding research stresses that external incentives such as monetary or other financial rewards can “crowd out” intrinsic motivation (Frey, 1997; Frey & Jegen, 2001; Frey & Osterloh, 2005). When people perceive that outside intervention reduces their self-determination, or their intrinsic motivation is not appreciated or acknowledged by others, they substitute intrinsic motivation with extrinsic control (Frey, 1997). This motivation-crowding out argument is reinforced by other theories, such as self-determination theory (Deci, 1971; Deci et al., 1999; Deci & Ryan, 2004), which stresses intrinsic motivation generated from self-initiated activities (Weibel et al., 2009), or public service motivation research (Perry & Hondeghem, 2008; Perry & Porter, 1982; Perry & Wise, 1990), which emphasizes public service motives of public employees.

Scholars have produced voluminous research on the effects of PRP on performance since the late 1980s (Perry et al., 2009). Several scholars have synthesized this large body of PRP research to analyze the effects of PRP and assess the current status of PRP research. Jenkins et al. (1998) conducted the first meta-analysis on the impact of financial incentives on performance. By moderating the research by study setting (i.e., laboratory, experimental simulation, and field settings), task type, and theoretical framework, they concluded that financial incentives are likely to meaningfully increase performance quantity, but negligibly increase performance quality. Condly et al. (2003) expanded the number of moderators in their meta-analysis and reported that monetary incentives have a greater positive impact on performance than non-monetary incentives. Also, they found that team-based incentive programs have a more positive impact on performance than individual-based incentive programs. In their meta-analysis of studies on the impact of PRP on performance, Weibel et al. (2009) reported that PRP has a positive association with performance in the case of uninteresting tasks, but PRP reduces performance in the case of interesting tasks—which suggests that PRP can have a crowding-out effect for highly motivated individuals.

Hasnain et al. (2012) conducted a meta-analysis on 110 empirical studies of PRP in the public sector by classifying studies by the observability of outputs and outcomes in organizations where PRP is implemented. While they found that the majority of high-quality studies report positive effects of PRP, these positive effects were mostly concentrated in jobs where outcomes are observable, such as teaching, health care, and revenue collection. Importantly, they found that the effects of PRP are unclear in traditional public service jobs where outcomes are not easily observable. Their findings reinforce the argument drawn from the earlier synthesis of PRP research (Perry et al., 2006, 2009) that it is crucial to consider the characteristics of organizations where PRP is implemented. Other comprehensive studies that synthesized the research on PRP also emphasize the importance of employee and job characteristics, pay design, and organizational context, all of which could affect the efficacy of PRP (Perry et al., 2006, 2009). Finally, a recent study that synthesized public service motivation research (Ritz et al., 2016) reports that a PRP system is counterproductive and should be replaced by traditional or alternative pay systems. In sum, the earlier studies that investigated the effects of PRP emphasize the importance of accounting for various dimensions of PRP for the analysis. The next section builds hypotheses based on this consideration regarding PRP studies.

Hypotheses

Top management is particularly important for PRP application because they impact the choice of strategy, goal-setting, and management decisions, all of which can affect organizational performance (Gerhart et al., 2009). Because executives’ behavior is commonly unobservable and costly to measure, their compensation is generally tied to organizational performance to motivate them to act in the interest of their principals (Gerhart et al., 2009; Murphy, 1999). Despite the significance and the wide application of executive PRP systems, most extant research in the private sector only partially answers the question of its net effect on organizational performance (Elsayed & Elbardan, 2018; Gerhart et al., 2009). Executives’ PRP may indirectly benefit firm performance through its impact on managerial actions such as the choice of firm strategy, development and investment decisions, and the degree of diversification (Elsayed & Elbardan, 2018; Gerhart et al., 2009; Murphy, 1999), while the opposing view concludes that there is surprisingly little evidence that executive PRP is effective for firm performance (Murphy, 1999), and executive PRP systems fail to reduce slack and may create perverse incentives (Bebchuk & Fried, 2006).

The main sentiment in the public sector is that PRP is effective for top management (Perry et al., 2009; Risher & Fay, 2007), which is supported by the view that individuals require a sufficient level of discretion and control over tasks to respond to an incentive system. If individuals perceive that they lack enough discretion or control to influence outcomes due to external environment or procedural rules or regulations, they have little expectations of reward and are less likely to respond to an incentive system (Heinrich & Marschke, 2010; Pearce et al., 1985). This argument suggests differences on the degree to which PRP affects executives compared to employees: top management with enough discretion and influence to make important decisions for organizations may thus be more reactive to PRP than low-level employees, as they may feel that they can change the status quo of an organization with their influence.

On the other hand, researchers who emphasize individual motivation as a primary determinant of the success of PRP argue that PRP can be effective for low-level employees and detrimental to upper management. They assume that people who undertake uninteresting tasks are primarily extrinsically motivated, while those whose tasks are interesting are intrinsically motivated (Weibel et al., 2009). Because executives are more likely to undertake more challenging and interesting tasks than lower-ranked employees, PRP may have a harmful impact on executives by crowding out their intrinsic motivation (Spector, 1986; Weibel et al., 2009).

Based on these two competing arguments on the moderating effect of the target of PRP on performance, this study examines the following hypothesis:

Hypothesis 1: Performance-related pay for top executives has a greater positive association with organizational performance than performance-related pay for mid- and low-level employees.

Performance-pay design can vary by linking pay to the performance of an individual, a team, a department, or even an entire organization. While existing studies report that team-based incentives are generally more effective than individual-based incentives, studies in the public sector that focus on the group-based incentives are scarce (Perry et al., 2006). Group-based incentives may be more effective in improving organizational performance than individual-based incentives because group-based incentive systems produce group motivation, which is greater than the sum of individual motivations (Condly et al., 2003). Tying pay to group performance may also reduce costs related to evaluation and conflict among employees that results from destructive competition (Hasnain et al., 2012) and promote greater team cohesion, coordination, trust, and support (Gomez-Mejia & Franco-Santos, 2015). The positive effect of team-based pay is supported by a recent meta-analysis on the relationship between collective PRP and team outcomes conducted in the private sector (Nyberg et al., 2018).

However, group-based incentives may result in negative outcomes due to free-riding or “social-loafing” (Bandura, 1997), when individuals tend to exert less effort in teams than when they are assessed individually (Condly et al., 2003; Hasnain et al., 2012). The tendency to free-ride on collective effort intensifies as a group gets bigger, and it becomes more difficult to identify and measure individual effort within the group performance (Dixit, 2002; Hasnain et al., 2012). Also, group performance may be affected by a host of other factors beyond individuals’ effort and control (Gerhart et al., 2009). Therefore, pay tied to the entire organization’s performance may produce less positive effects than when performance-pay is linked to individual or team effort. From this argument, this study proposes the following hypothesis:

Hypothesis 2: Organization-based performance-related pay has a smaller positive association with organizational performance than individual- or team-based performance-related pay.

Organizations generally have multiple goals (Ethiraj & Levinthal, 2009), and goals in the public sector are particularly ambiguous, imprecise, and often subject to asymmetric measurement (Burgess & Ratto, 2003; Frey et al., 2013; Holmstrom & Milgrom, 1991; Marsden & Richardson, 1994). Also, complex services that generally involve multidimensional tasks (Bregn, 2013; Hasnain et al., 2012; Weibel et al., 2009) make the public sector susceptible to distorting behaviors by incentivizing individuals to focus only on tasks that are measurable and observable, while it might be crucial to do unobservable tasks (Bregn, 2013; Heinrich & Marschke, 2010; Weibel et al., 2009).

Therefore, the efficacy of a performance-based incentive system largely depends on the precise measurement of performance and the ability to link incentives to the attributions of performance (Dixit, 2002; Ethiraj & Levinthal, 2009; Heinrich, 2007; Holmstrom & Milgrom, 1991; Ouchi, 1977). Previous literature also reports that individuals who are not intrinsically motivated tend to have a strong incentive to respond to performance indicators that are quantifiable and easy to measure (Frey et al., 2013). Also, the pursuit of subunit goals rather than global goals is more likely to produce better performance, which can be explained by less noise and uncertainty involved with subunit goals (Cohen, 1984; Ethiraj & Levinthal, 2009). In a similar vein, incentives tied to well-specified organizational goals may increase performance, as it is more likely to make performance commensurate with effort (Perry et al., 2006). When goals are unclear and outcomes cannot be easily distinguished from external forces, performance decreases as individual motivation dampens (Heinrich, 2007). This is supported by the findings of Hasnain et al. (2012), which classified public sector jobs based on the observability of outcomes defined by Wilson (1989) and reported that positive effects of PRP are limited to public sector jobs where outcomes are observable. Therefore, this study investigates the following hypothesis:

Hypothesis 3: The level of outcome observability moderates the effect of performance-related pay on performance.

Performance-Related Pay in Korean Public Enterprises

Public Enterprise

To investigate the hypotheses, this study focuses on PRP systems of public enterprises in South Korea. 1 A public enterprise 2 is a type of public entity that includes features of both a government organization and a private business. A public enterprise embodies the characteristics of a private firm by generating more than half of its revenue through business activities, but unlike a private firm, a public enterprise emphasizes public values in providing goods and services, and the government exerts a great deal of influence on its business management and pay system. While these distinctive characteristics make it reasonable to classify a public enterprise as a public sector organization, it should be noted that the effects of PRP in this analysis may be overestimated compared to that of a pure government organization, as PRP tends to be more effective in the private sector than the public sector (Hasnain et al., 2012; Perry et al., 2006, 2009).

Performance-Related Pay in South Korea

The Korean government initiated a performance incentive system in the late 1990s, and PRP is implemented in conjunction with a performance management system (Kim, 2014). In 2010, the central government released a PRP guideline expanding the performance pay system for public entities. The guideline aimed to simplify an extant complex pay system and emphasized performance-pay, particularly for top managerial positions. The assessment criteria by which performance pay is allocated differ between top executives and mid- and low-level employees in public enterprises. Performance pay for top executives is based on organizational performance, whereas performance pay for mid- and low-level employees is based on two performance evaluation criteria: organizational performance, and individual or team performance. Organizational performance is evaluated by the central government and individual or team performance is assessed internally.

Methods and Data

This analysis uses data on Korean public enterprises for the 2012 to 2018 period. Because Korean government changes in PRP categories for employees became effective in 2012, this study does not include data before 2012 to avoid a bias resulting from this mechanical shift of PRP categories.

Dependent Variables

This study examines how PRP affects the performance of public enterprises in South Korea. Because a public enterprise emphasizes both public service provision and financial performance, it is important to look beyond finances when measuring its performance (OECD, 2015; Papenfuß & Keppeler, 2020). Therefore, this study focuses on the three aspects of performance: financial performance, management performance, and business performance. As an indicator of financial performance, this study uses sales revenue per employee and the ratio of sales revenue to labor costs. These measures indicate the degree to which a public enterprise generates revenues and its labor productivity.

Management performance is related to the achievement of various management factors that assess how well a public enterprise fulfills its social responsibility, satisfies customers, manages its business transparency, pursues business innovations, complies with government policies, achieves managerial and financial efficiency, and manages labor relations. These indicators for management performance are important measures that assess the degree to which a public enterprise attains its public values. This study obtained management scores from the evaluation report 3 published by the Ministry of Economy and Finance. The annual evaluation of public enterprises is conducted by a group of outside experts, who are selected by the central government to represent a mix of fields, 4 regions, and gender. To ensure the objectivity of the evaluation, evaluators are subject to strong ethics guidelines, and each score must be cross-confirmed by multiple evaluators. 5

Business performance is measured by business scores reported in the government’s annual evaluation report. The business-related scores measure the degree to which each public enterprise attains specified business goals. 6 Admittedly, because management and business performance are not readily observable by nature, the scores obtained from the government report might not accurately capture the performance of public enterprises. Nevertheless, these scores can serve as good proxies for performance given the comprehensive and rigorous nature of performance evaluation initiated by the central government.

Explanatory Variables

The main variable of interest is PRP implemented in Korean public enterprises. Specifically, this study aims to investigate the moderating effects of the target, pay design, and the context of PRP on organizational performance. To evaluate how PRP works differently depending on the target (i.e., executives vs. mid- and low-level employees), this study employs the share of performance pay for top executives in their total wages and the share of performance pay for mid- and low-level employees in their total wages as explanatory variables. To measure the moderating effect of pay design, this study uses the share of performance pay in total wages for mid- and low-level employees tied to: (1) organizational performance, and (2) individual or team performance.

To investigate the effect of a key contextual factor in PRP—the observability of outcomes—this study borrows the typology of public organizations from Wilson (1989). Wilson (1989) provides an analytic framework that classifies public organizations based on the observability of outputs (activities) and outcomes. Wilson (1989) describes that outputs are work done by operators on a day-to-day basis, such as “tickets written, accidents investigated, and arrests made by police officers,” whereas outcomes are “the results of organization work, which shows how the world changes because of the outputs” (p. 158). Depending on the observability of outputs and outcomes, public organizations can be classified into four types: production organizations, in which both outputs and outcomes are easily observable; procedural organizations, in which only outputs are observable; craft organizations, in which only outcomes are observable; and coping organizations, in which neither outputs nor outcomes are observable.

To apply Wilson’s (1989) typology on Korean public enterprises, this study relied on the observability of outcomes based on specified goals of each organization. The government’s annual performance evaluation report publishes the specific goals of each public enterprise. Based on the observability of outcomes driven by these goals, this study coded the organizations as “craft” or “coping.” Specifically, public enterprises were coded as “craft” if outcomes are observable and if desired performance endpoints can be attributed to the performance of a public enterprise. If the majority of outcomes related to specified goals belongs to these criteria, the organization was coded as “craft,” whereas it was coded as “coping” if the majority of specified goals does not meet the criteria. For example, the Korea Railroad Corporation has five specified business goals: increasing the number of train passengers, ensuring the punctuality of train times, increasing the efficiency of rail freight transport, ensuring the safety of trains, and developing new business. Because the majority of specified outcomes are observable, it was coded as a craft organization. On the other hand, the Korea Tourism Organization, which has four specified goals—attracting foreign tourists, facilitating MICE tourism, 7 attracting foreign medical tourists, and revitalizing domestic tourism—was coded as a coping organization because it is difficult to solely attribute organizational outcomes to the performance of an organization. External factors—such as the economy, or the increased international popularity of K-pop—may have played a dominant role in producing the Korea Tourism Organization’s organizational outcomes. Table 1 presents a description of the full coding procedure for the two aforementioned examples. The full list of public enterprises classification is presented in Appendix 1. No public enterprises were classified as “production” or “procedural” because none strictly met the criteria of these two organization types. 8

Examples of a Coding Procedure.

Control Variables

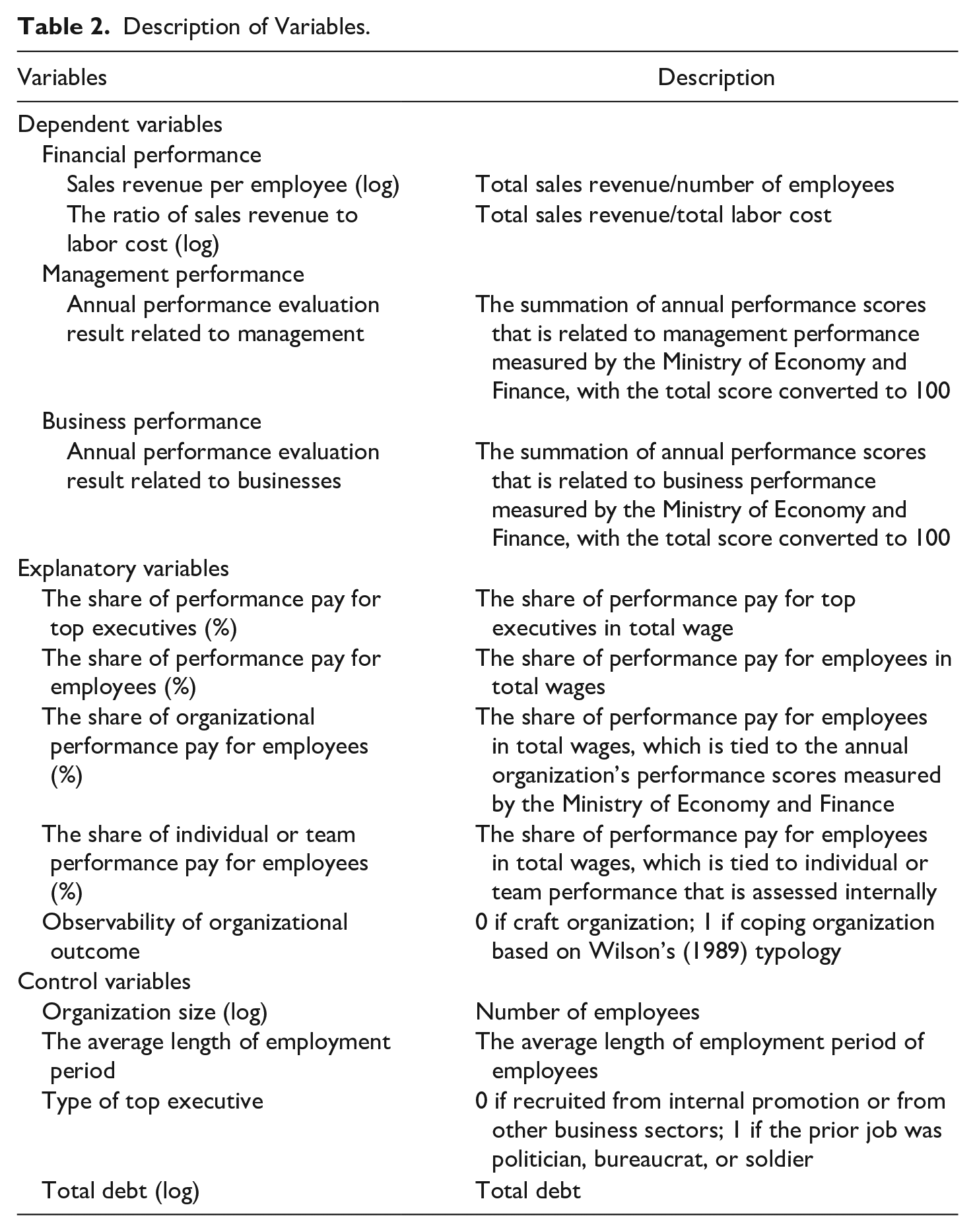

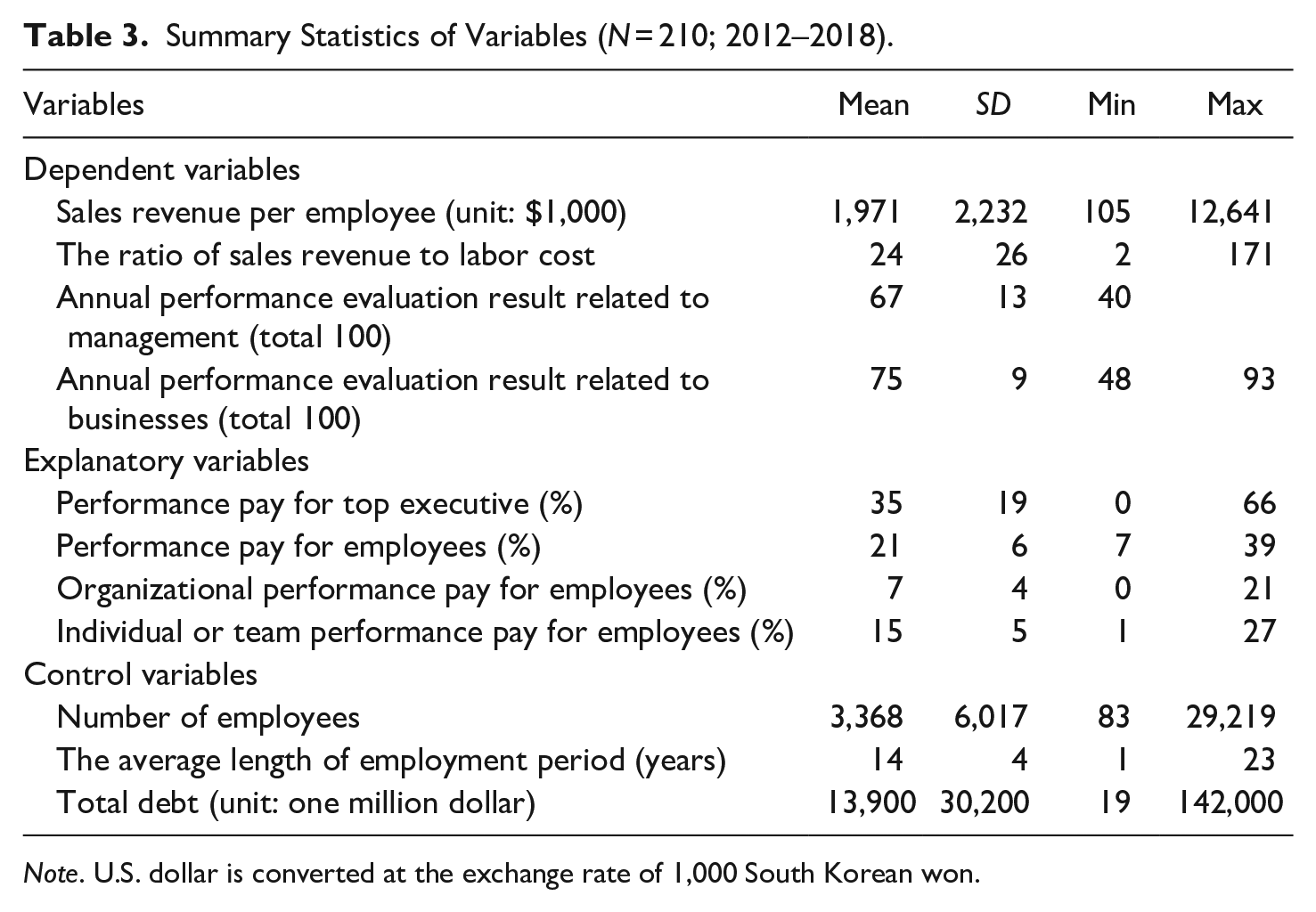

Control variables include the size of organization (i.e., number of employees), the average length of employment period, the previous job of the top executive, and total debt. A public enterprise may become more bureaucratic and less innovative as it ages and gets bigger, thereby diminishing performance (Ha & Jung, 2014). This study also controls for the previous job of the top executive. Because the top executive in public enterprises is appointed by the Korean government, the media has often criticized that unqualified top executives assume leadership positions due to political reasons. Top executives who were previously politicians, bureaucrats, or soldiers are coded as 0, whereas top executive who were either promoted internally or from the private sector are coded as 1. This study assumes that top executives with no previous business experience are less competent than top executives with extensive experience in the field. Finally, as large debt can reduce organizational performance (Hasnain et al., 2012), this study controlled for total debt level of public enterprises. 9 Table 2 presents the variables used in the study and Table 3 shows the summary statistics.

Description of Variables.

Summary Statistics of Variables (N = 210; 2012–2018).

Note. U.S. dollar is converted at the exchange rate of 1,000 South Korean won.

Empirical Model

The empirical model below tests hypotheses 1 and 2:

where

The following model tests the effects of performance pay design on organizational performance (hypothesis 3):

where

Finally, the following empirical model investigates the impact of the observability of outcomes on organizational performance:

To measure the moderating effect of the observability of organizational outcomes, performance pay for top executives and employees is respectively interacted with

One possible concern about this research method is an endogeneity issue. Because PRP is affected by organizational performance, PRP may not affect organizational performance but organizational performance may influence the allocation of PRP. Another possible concern is that there may be other unobserved factors that affect organizational performance such as ownership, the share of funding (Bozeman & Bretschneider, 1994; Heinrich & Fournier, 2004; Papenfuß & Keppeler, 2020), goal ambiguity, the alignment of goals with prosocial values, 10 and individual composition (Papenfuß & Keppeler, 2020). While it may not perfectly address this possible endogeneity, the fact that all PRP variables included in the model are based on the previous year’s performance assessment provides the implicit lagged effect in the PRP mechanism, thereby addressing the possibility that PRP and performance are jointly determined. For example, this year’s performance pay is determined by last year’s performance, and thus performance cannot concurrently be determined with the pay. Besides the inclusion of control variables, year and firm fixed effects control for time-invariant as well as firm-invariant characteristics, thereby reducing an endogeneity concern to some extent. Nevertheless, this analysis attempts to identify associations—not casual relationships—between PRP and organizational performance.

Data Sources

This article investigates how PRP implemented in public enterprises in South Korea is associated with organizational performance. The majority of PRP variables and control variables were obtained from the publicly available government data source called “All Public Information In-One (ALIO).” Management and business data were collected from the annual performance evaluation report published by the Ministry of Economy and Finance. In addition, the previous jobs of top executives in public enterprises were collected from publicly available information. The unit of this analysis is a public enterprise.

Empirical Results

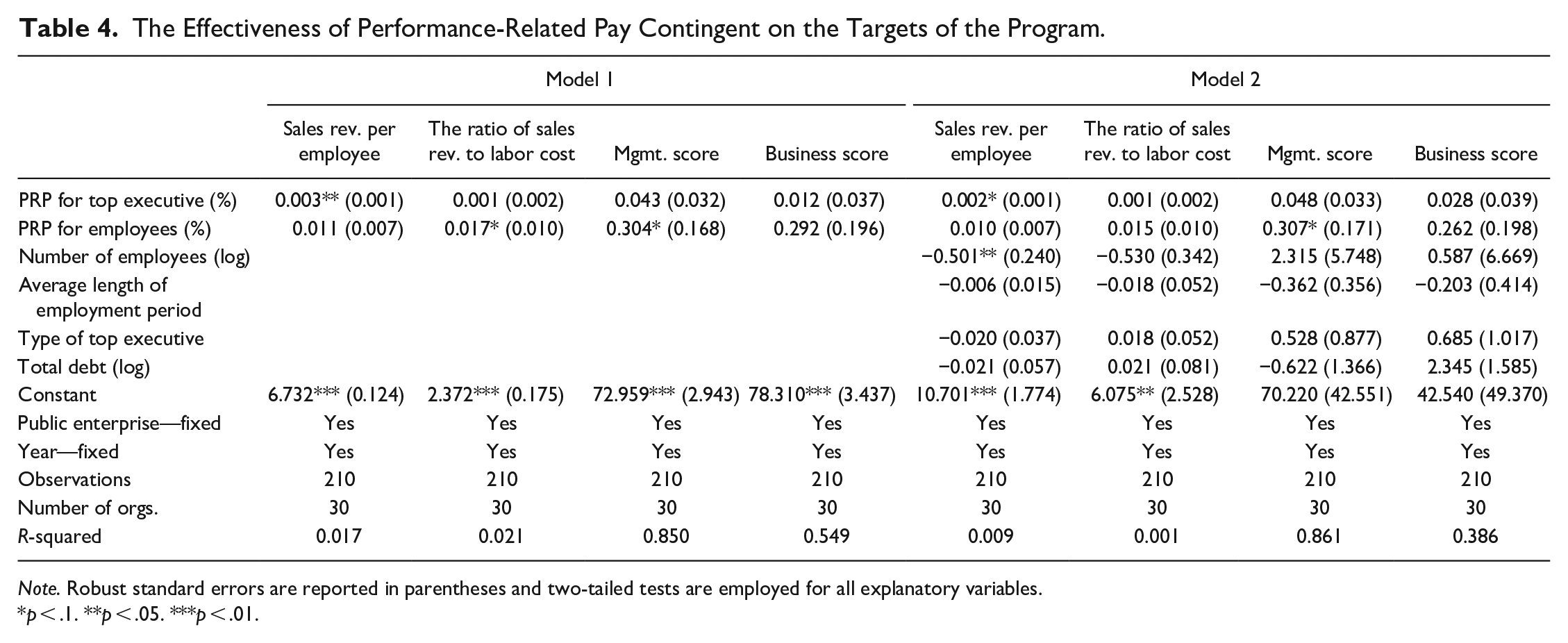

Table 4 presents whether PRP influences the performance of public enterprises measured by financial, management, and business performance, when implemented to chief executives and employees, respectively. The results that exclude control variables (model 1) show that PRP has a positive association with sales revenue per employee when implemented to top executives, while it has positive associations with labor productivity and management score when implemented to employees. When control variables are included (model 2), the statistical significance of employee PRP disappears for the ratio of sales revenue to labor cost and remains significant only for management score. Holding other variables constant, increasing a top executive’s share of performance pay by ten percent (e.g., from 30 percent to 33 percent of total wages) is associated with a two percent increase in sales revenue per employee. On the other hand, a ten percent increase in employees’ share of performance pay is associated with a three-point increases in management score, which is about one-ninth of the difference between mean and minimum management scores. This finding contradicts the argument that PRP is not effective for high-level employees who are assumed to have high intrinsic motivation due to their interesting and challenging tasks (Spector, 1986; Weibel et al., 2009). Rather, the results indicate that PRP may be associated with differing aspects of performance, depending on to whom it is implemented. Chief executives—who have greater autonomy and control in terms of their decision-making—are more likely than lower-level employees to be motivated to focus on financial performance, which is more readily observable than other aspects of performance such as the emphasis on publicness or social responsibility.

The Effectiveness of Performance-Related Pay Contingent on the Targets of the Program.

Note. Robust standard errors are reported in parentheses and two-tailed tests are employed for all explanatory variables.

p < .1. **p < .05. ***p < .01.

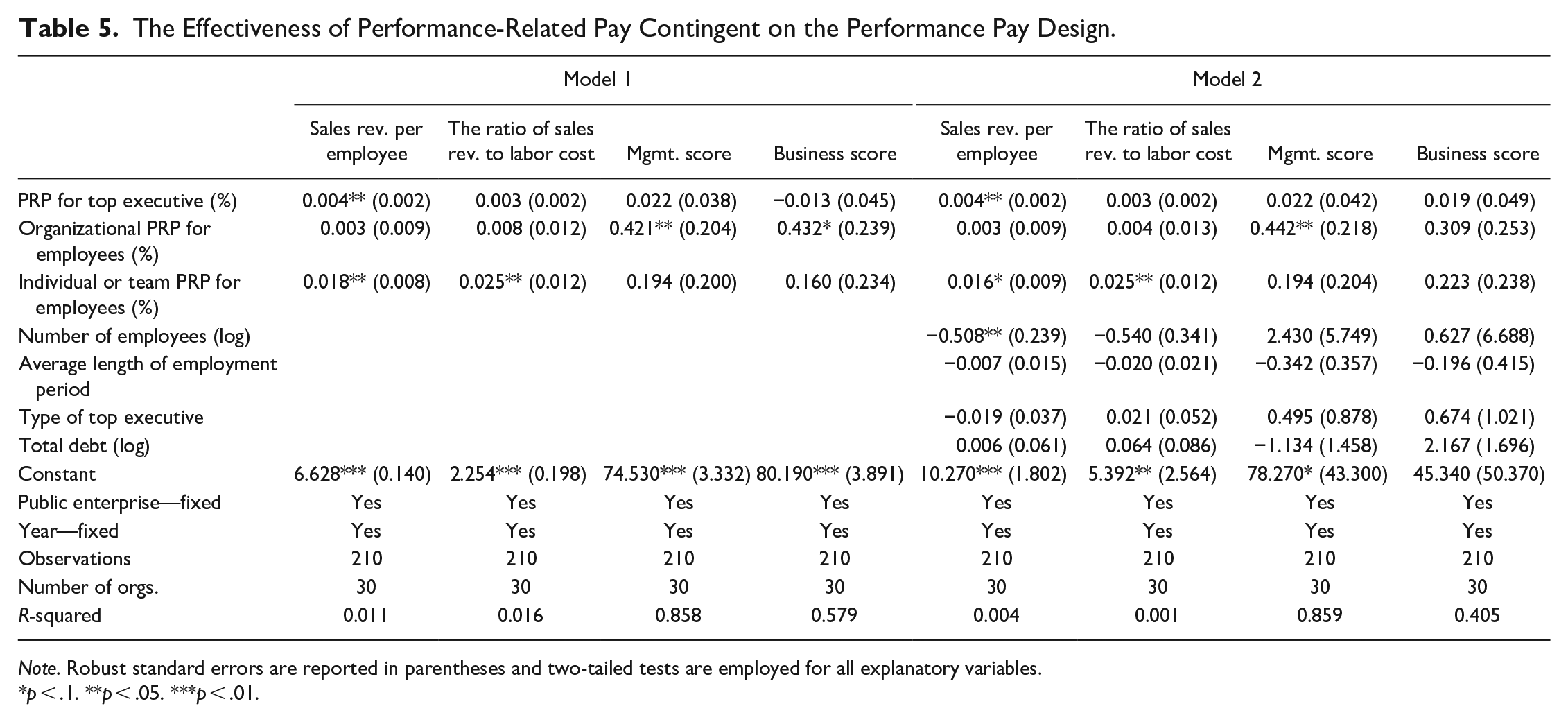

Table 5 illustrates how different PRP pay designs are associated with organizational performance. This study exploits the fact that employees in Korean public enterprises receive two types of performance pay—organization-based PRP and individual- or team-based PRP—to test the relationship between pay designs and performance. The results that omit control variables (model 1) show some interesting points that positive effects of PRP for employees are broken down by differing aspects of performance depending on pay designs. PRP for employees that is tied to individual or team performance has positive associations with measures for financial performance while PRP that is tied to organizational performance has positive associations with management and business scores. When control variables are included (model 2), however, organization-based PRP is statistically significant only for management score and it is no longer significant for business performance. All else being equal, a ten percent increase in the current share of individual- or team-based PRP is associated with a 16 percent increase in sales revenue per employee and a 25 percent increase in the ratio of sales revenue to labor cost. On the other hand, a ten percent increase in the current share of organization-based PRP is associated with a four-point increase in management performance score, which is about one-seventh of the difference between mean and minimum management scores. The positive association of PRP for top executives with performance remains consistent with the results in Table 4, with increased statistical significance. The results indicate that individuals may tend to focus more on recognizable outcomes when their efforts are linked to more narrowly defined targets over which they can exercise greater control. As shown by the earlier results associated with the target of PRP, the results in Table 5 also imply that governments should pay attention to the design of PRP, by which differing aspects of organizational performance are affected.

The Effectiveness of Performance-Related Pay Contingent on the Performance Pay Design.

Note. Robust standard errors are reported in parentheses and two-tailed tests are employed for all explanatory variables.

p < .1. **p < .05. ***p < .01.

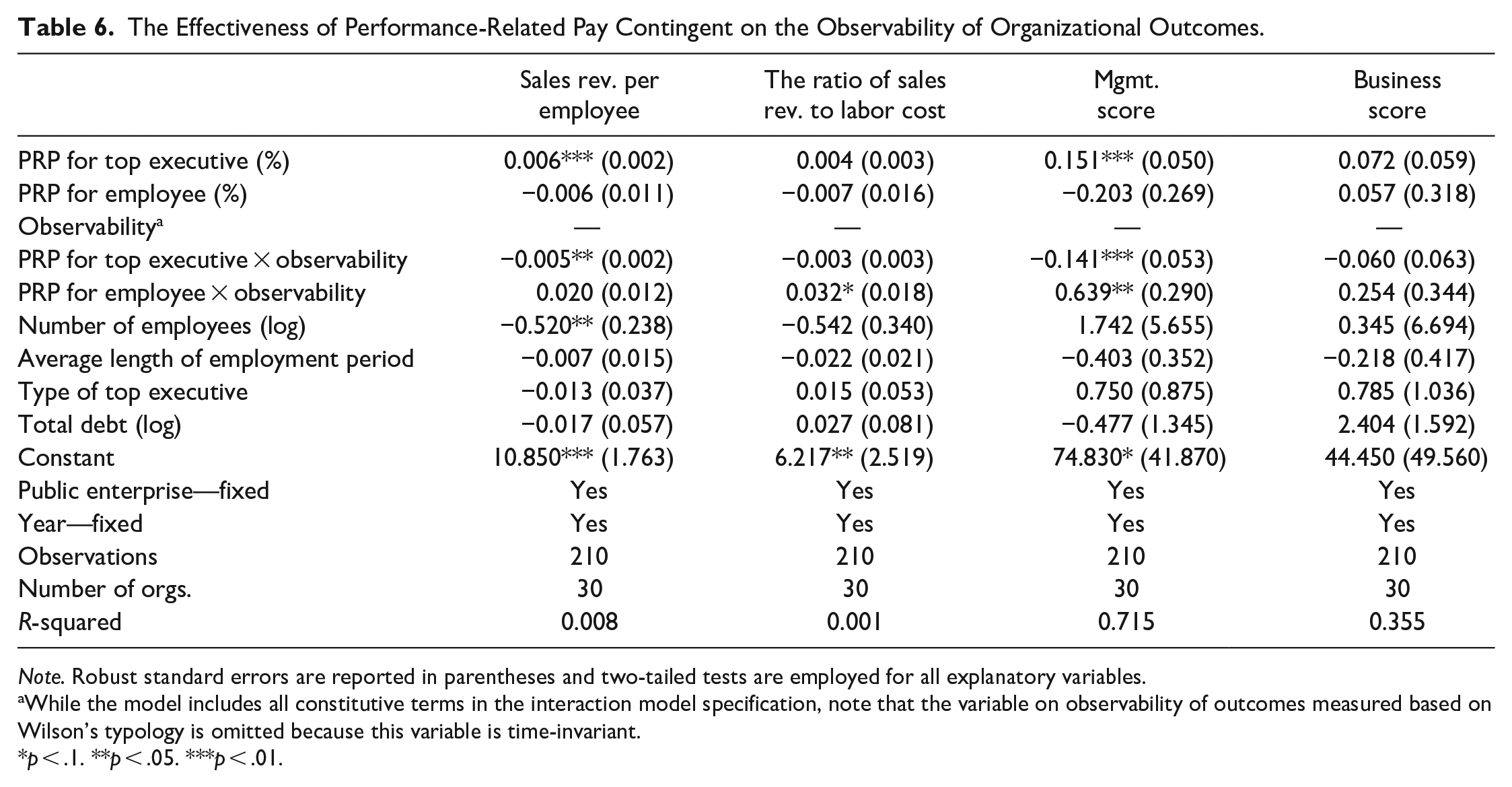

Table 6 shows how the observability of organizational outcomes is associated with the effectiveness of PRP. This study proposed that the effectiveness of PRP is lower for coping organizations where it is difficult to measure outcomes or attribute the desired end results to the activities of organizations than for craft organizations where it is relatively easy to measure outcomes. The result in Table 6 confirms the hypothesis when confining results to PRP implemented to top executives. When a public enterprise is a coping organization, the results show that the positive effect of executive PRP is significantly reduced, by offsetting the positive impact of executive PRP close to zero. This finding supports an earlier argument that organizational context moderates the effectiveness of PRP (Perry et al., 2006, 2009). While performance pay for top managerial positions generally produces positive outcomes, the effectiveness may be attenuated in certain contexts. Top executives in coping organizations may perceive that their vision, strategy, and performance have little effect on organizational performance, thereby decreasing the effectiveness of PRP. PRP for employees, however, has a positive association with financial performance and management performance in coping organizations but a negative association in craft organizations.

The Effectiveness of Performance-Related Pay Contingent on the Observability of Organizational Outcomes.

Note. Robust standard errors are reported in parentheses and two-tailed tests are employed for all explanatory variables.

While the model includes all constitutive terms in the interaction model specification, note that the variable on observability of outcomes measured based on Wilson’s typology is omitted because this variable is time-invariant.

p < .1. **p < .05. ***p < .01.

While this finding is puzzling at first, the fact that the application of Wilson’s (1989) typology is based on the observability of organizational outcomes, not individual outcomes, may have produced this confounding result. The fact that organizational outcomes are unobservable does not necessarily mean that individual performance is not observable or measurable. In the context of PRP in Korean public enterprises, Wilson’s (1989) typology might be more relevant to PRP for top executives than PRP for employees, because top executives’ performance pay is directly linked to organizational performance whereas employees’ performance pay is determined by both organizational performance and team or individual performance. Nevertheless, the analysis in other research settings that use contextual factors as moderators merits further investigation for the generalization of results.

Among control variables, this study finds that the size of organization measured as the number of employees (log) has a negative association with sales revenue per employee across all models. Large organizations, on average, may be more bureaucratic and less innovative, thereby negatively affecting organizational performance (Ha & Jung, 2014).

Discussion and Conclusion

Despite the inconclusive effects of PRP reported in the previous literature, PRP has been consistently implemented in public sectors across most OECD countries over the past four decades (Bellé, 2015; Spano & Monfardini, 2018). Based on the synthesis of ample research on PRP, scholars concluded that these inconclusive effects are attributable to the complexity of PRP and called for research that considers the various moderating factors of PRP (Perry et al., 2006, 2009). Responding to this earlier call for research that takes various characteristics of PRP and the contexts of organizations into account, this study investigates how PRP is associated with performance depending on the target of the program (top executives versus mid- and low-level employees), pay design (organization-based incentives versus individual- or team-based incentives), and organizational context (based on the observability of organizational outcomes). For empirical analysis, this study utilizes data on 30 Korean public enterprises between 2012 and 2018.

The findings suggest that performance pay generally has a positive association with organizational performance but the aspects of performance it affects may differ depending on to whom PRP is implemented. The results show that individuals who have a great deal of discretion and control over organizations may be incentivized to focus on readily recognizable indicators, such as financial performance, when their incentives are linked to performance. Chief executives may perceive that performance related to the emphasis on public values—which is often perceived as vague and unobservable—is more difficult to attain by exerting their own discretion than other distinctive indicators such as sales revenue. This finding not only counters the argument that performance pay is counterproductive for high-level employees who are assumed to have high intrinsic motivation, it also implies that it is worth investigating the nuanced role of PRP in relation to employee characteristics and performance type.

Public organizations can choose to design performance pay in various ways. Incentives can be linked to the performance of an individual, a team, a department, or even an entire organization. Despite evidence that pay design matters for the effectiveness of PRP, we lack research exploring the effects of pay design on performance (Perry et al., 2006). The dual PRP systems for employees in Korean public enterprises—in which some portions of incentives are linked to the organizational performance and other portions are linked to individual or team performance—enables us to test the effects of pay design. This study’s findings provide some evidence that the way governments design PRP can impact organizational performance. The results show that individual- or team-based performance pay tends to have a positive association with financial performance, whereas organization-based performance pay has a positive association with management performance that emphasizes the achievement of public values. The findings indicate that individuals are more likely to be motivated to focus on measurable performance, such as financial performance, when incentives are tied to tasks they can easily influence.

Finally, the results show that the effectiveness of performance pay can differ depending on organizational context. Specifically, by borrowing the organization typology of Wilson (1989), this study finds that the positive impact of PRP for top executives is reduced in organizations where outcomes are not easily observable or difficult to attribute to organizational activities. In the context where incentives are tightly linked to organizational performance organizations but performance is not easily observable, the effectiveness of PRP rarely persists. This finding provides an important implication with respect to the conditions under which PRP works.

One notable point that runs through all findings in the tests of the hypotheses is that PRP is more likely to motivate individuals to focus on observable and measurable performance when they have greater responsibility, discretion, and control over their tasks and outcomes. This argument is supported by the findings that the higher an individual’s rank in an organization and the more tightly tasks and measured outcomes are linked, the more likely the individual is to focus on observable and measured performance. Also, the finding that PRP is particularly effective for top executives when organizational performance is observable adds to the evidence that contextual factors play an important role in the effectiveness of PRP. In conclusion, this research indicates the importance of PRP studies that account for subtle and nuanced moderating factors, deviating from a dichotomous approach that examines the effectiveness of PRP by itself.

This study, however, has some limitations to be noted. First, as discussed earlier, readers should note that public enterprises have characteristics of both public and private sectors. While Korean public enterprises are subject to strict regulations and rules of the Korean government and must emphasize public values, these organizations obtain more than half of their revenue from business activities. Based on the previous evidence that PRP is likely to be most effective in the private sector (Hasnain et al., 2012; Perry et al., 2006, 2009), it is worth noting the possibility that the positive effects of PRP in this study’s data may be overestimated. The public sector has more constraints regarding budgets and stewardship (Perry et al., 2009), and tasks in the public sector are more complex and difficult to measure (Bregn, 2013; Hasnain et al., 2012). Second, the data was collected from South Korea, which emphasizes collective values more than in western cultures (Kim et al., 1990), which suggests that the positive effects of PRP in this study might be attenuated to some extent due to a culture in which employees tend to push back against performance pay. Third, it should be noted that there might be a problem of limited statistical power for identifying statistically significant relationships in the analyses, due to the relatively small sample of organizations employed in this study. Finally, while the application of the typology of Wilson (1989) provides some insights into understanding the impact of organizational contexts on performance, disagreement may exist in the classification of organizations, especially for those that are near the subtle border between coping and craft organizations.

Nevertheless, this article elucidates why PRP is effective in certain contexts while it fails in other contexts. The findings of this study emphasize that it is important to consider the target, pay design, and the context of an organization for the successful implementation of PRP. By building on Wilson’s (1989) classification that this article utilized, future research with more sophisticated criteria that classify organizations based on the observability of outcomes would lead to more generalizable findings.

Footnotes

Appendix

High-Level Evaluation Categories of the Annual Performance Evaluation Report (Example: Korea Railroad Corporation).

| Year | 2012 | 2013 | 2014 | 2015 | ||||

|---|---|---|---|---|---|---|---|---|

| Performance | Evaluation category | Score | Evaluation category | Score | Evaluation category | Score | Evaluation category | Score |

| Management performance | Leadership | 5 | Leadership | 5 | Business strategy and social contribution | 11 | Business strategy and social contribution | 14 |

| Accountable business management | 3 | Accountable business management | 3 | Business efficiency | 8 | Business efficiency | 8 | |

| Public evaluation | 5 | Public evaluation | 5 | Human resource management | 2 | Human resource management | 2 | |

| Social contribution | 7 | Social contribution | 7 | Financial management | 17 | Financial management | 14 | |

| Business efficiency | 6 | Business efficiency | 6 | Pay and employees’ welfare management | 12 | Pay and employees’ welfare management | 12 | |

| Human resource management | 4 | Human resource management | 2 | |||||

| Financial management | 12 | Financial management | 12 | |||||

| Pay and performance management | 8 | Pay and performance management | 7 | |||||

| Labor management | 5 | Labor management | 3 | |||||

| Sub total | 55 | 50 | 50 | 50 | ||||

| Business performance | Transportation business | 17 | Transportation business | 17 | Business performance management | 13 | Business performance management | 13 |

| Safety management | 14 | Rail freight business | 8 | Transportation business | 16 | Transportation business | 16 | |

| Facilities inspection and repair | 10 | Unprofitable business management | 3 | Rail freight business | 5 | Rail freight business | 5 | |

| Non-transportation business | 4 | Safety management | 16 | Safety management | 11 | Safety management | 11 | |

| New business development | 6 | New business development | 5 | New business development | 5 | |||

| Sub total | 45 | 50 | 50 | 50 | ||||

| Total | 100 | 100 | 100 | 100 | ||||

| Year | 2016 | 2017 | 2018 | |||

|---|---|---|---|---|---|---|

| Performance | Evaluation category | Score | Evaluation category | Score | Evaluation category | Score |

| Management performance | Business strategy and social contribution | 14 | Business strategy and social contribution | 18 | Business strategy and leadership | 6 |

| Business efficiency | 8 | Business efficiency | 5 | Social contribution | 22 | |

| Human resource management | 2 | Human resource management | 4 | Business efficiency | 5 | |

| Financial management | 14 | Financial management | 10 | Human resource and Financial management | 9 | |

| Pay and employees’ welfare management | 12 | Pay and employees’ welfare management | 13 | Pay and employees’ welfare management | 8 | |

| Public participation | 5 | |||||

| Sub total | 50 | 50 | 55 | |||

| Business performance | Transportation business | 21 | Transportation business | 21 | Transportation business | 11 |

| Rail freight business | 6 | Rail freight business | 6 | Rail freight business | 3 | |

| Safety management | 17 | Safety management | 17 | Safety management | 10 | |

| New business development | 6 | New business development | 6 | New business development | 3 | |

| Business performance | 12 | |||||

| Performance management | 6 | |||||

| Sub total | 50 | 50 | 45 | |||

| Total | 100 | 100 | 100 | |||

Note. The performance categories indicate the high-level evaluation categories, each of which includes sub-categories.

Acknowledgements

I am grateful to the editors and three anonymous reviewers who all provided constructive and excellent comments on a previous draft. I also thank Nicolai Petrovksy, J.S. Butler, and Daniel Torres for their valuable comments to improve my article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.