Abstract

Questions regarding the economic consequences of US grand strategy have gained new salience. This article provides an empirical test of the relationship between US military expenditures and public debt and clarifies the real constraints the US faces issuing debt. Neither results from the statistical analysis nor the economic theory of sovereign debt support the retrenchment position regarding the impact of military spending on public debt (1973–2015). Tax cuts are the most significant determinant of debt not military spending, social benefits or interest payments. Evaluating new hypotheses about alternative mechanisms through which military spending may damage the economy remains a priority.

US grand strategy has always been a flashpoint, but the debate between those who advocate a continuation of America’s postwar policy of deep engagement and those who recommend strategic disengagement is undergoing a profound transformation. 1 Once relegated to corners of academe, a few think tanks, and fringe political candidates, the question of whether the United States should “come home” has assumed a new political salience. China’s rise, an assertive Russia, other fast rising powers, US relative economic decline and the much deeper relative economic decline of most US allies have all placed new pressure on the United States’ deeply engaged global posture. The 2016 US presidential campaign, meanwhile, featured candidates on both left and right backing away from long-standing premises of deep engagement, from free trade to reflexive support for allies, to defense spending. That followed a startling break from a tradition of stalwart Republican support for Pentagon spending when Republican lawmakers agreed to deep defense cuts associated with sequestration in 2013. These positions track significant shifts among an American public increasingly disinclined toward global leadership and worried about the costs of foreign policy commitments (PEW, 2013).

Over the last quarter century, the US has consistently accounted for over a third of global spending on defense, and in 2015, the real total US public debt stood at 103% of GDP and the US public debt held by the public amounted to 74% of GDP. 2 Does the relatively high level of defense spending demanded by the United States’ deeply engaged grand strategy drive debt and decline? Advocates of pulling back emphatically say yes (Drezner, 2013; Gholz et al., 1997; Layne, 1997, 2002; MacDonald and Parent, 2011; Pape, 2009; Posen, 2007; Posen and Ross, 1996; Walt, 2005; Walt, 2011). Randall Schweller (2014: 8), for example, warns that “it won’t be long before the American people—encumbered by federal debt that will reach 70 percent of GDP in 2012 and a debt-to-revenue ratio approaching 262 percent—demand significant retrenchment from their government’s far-flung global commitments.” Republican presidential candidate Donald Trump agreed, stressing that “We’re a debtor nation. … [and] one of the reasons we’re a debtor nation [is that] we spend so much on the military, but the military isn’t for us. The military is to be policeman for other countries” (Makela, 2016).

Deep engagement’s academic defenders acknowledge that the grand strategy demands comparatively high levels of defense spending but question its contribution to US economic woes and argue that the net effect is economically positive. For them, the forward leaning posture that relatively high levels of spending enable produces stability and economic benefits, while pulling back would compromise both (Brooks et al., 2013; Gottlieb, 2012; Kagan, 2012; Sestanovich, 2014). If the US were less militarily powerful and engaged, key regions would become destabilized and conflict-prone and the world economic order, of which the US is a primary beneficiary, would unravel, leading to foregone economic opportunities in an insecure world. Underlying these arguments is skepticism concerning the claim put forth by proponents of retrenchment about the economic downsides of funding a globe-girdling military presence.

Thus far, neither side has subjected its core claims about the implications of defense spending for US economic prospects to empirical scrutiny. This article brings statistical evidence to bear on the argument that sustaining the current grand strategy is suboptimal because military spending contributes to debt-induced decline. In examining this argument, we stress that escalating debt is not the only possible economic consequence of military spending. Nor are the economic effects of military spending the only economic cost that retrenchment proponents highlight. However, it is an important proposition that is woven through both academic and more popular arguments for the need to pull back.

We find scant support for retrenchment supporters’ arguments about military spending causing decline via the debt channel. We proceed in four sections. First, given the complexity of the debate, we further specify the place of competing claims about the economic implications of defense spending in the larger research program on US grand strategy. Second, we examine the debate in the context of economic theory, unpacking the logic underlying the retrenchment proponents’ argument and showing why we would not expect the strongest versions to apply to a country occupying the United States’ position in the global economy. Third, we test retrenchment supporters’ argument by examining the relationship between military expenditures and public debt—a key driver of decline in many of their analyses. We offer robust evidence that US military spending does not explain America’s economic decline via the sovereign debt channel. Fourth, we propose a research agenda to advance current knowledge. We conclude by summarizing the main findings and teasing out implications for the retrenchment debate.

Military spending, public debt and economic decline

We focus on the economic implications of US military posture because they play a central but understated (and understudied) role in contending analyses of US grand strategy. As Meernik (2008: 46) notes, the “rich literature on imperial overstretch, hegemonic decline and foreign policy change is a vast, largely untapped source of empirically testable propositions that deserve and need to be analyzed.” In particular, questions regarding the economic consequences of US grand strategy have emerged as crucial. Even realist scholars who define grand strategy in purely security terms (e.g. Posen, 2014: 1: “grand strategy is a nation’s theory about how to produce security for itself”) accept that the economy is the ultimate source of a state’s power (Posen, 2014: chap. 1). They agree, moreover, that preserving its power position is a core aim of the United States’ grand strategy. It follows that if a given grand strategy entails economic burdens that undermine long-term economic prospects, it can be said to be counterproductive.

Surveying the large literature on retrenchment, two basic arguments concerning military expenditure emerge. First is a simple opportunity cost claim: resources devoted to the military cannot be used for other purposes. This claim conflates two logics, one normative and the other economic. That is, the opportunity cost can be reckoned in purely welfare terms, where retrenchment proponents commonly assume some normative preference on the part of the US public for non-military spending, whether that spending is better for the economy or not. Often, however, retrenchment proponents appear to assume that resources freed from the Pentagon would be used in ways that enhance growth or productivity in the long term, such as infrastructure or education. The second main claim is that military spending increases public spending and debt, which harms the economy. The US has a high ratio of public debt to GDP, and no other country spends more on defense. Military spending therefore logically contributes to America’s economic decline.

This second claim is ubiquitous in arguments for pulling back, and we single it out for empirical scrutiny. Despite scholarly disagreement over which strategy should replace deep engagement, retrenchment supporters hold a common assumption: the postwar policy of projecting US military power beyond the horizon has led to military overstretch and is a source of economic distress. As Cindy Williams (forthcoming, 2016: 2) warns:

Debt held by the public in 2014 was larger as a share of the economy than at any time in US history, with the exception of seven years during and after World War II … Absent further policy changes … debt will mount within a few decades to levels never before experienced by this country. The consequences for the American economy and for the nation’s place in the world could be severe.

In keeping with these arguments, 65% of the US public say they favor scaling back military commitments to reduce the debt (PEW, 2013). By pulling back and pursuing a less ambitious grand strategy than that practiced during the postwar era, proponents of retrenchment argue that the US can reverse its economic misfortune. As Williams (forthcoming, 2016: 5) puts it “A strategy of restraint seems ideally suited to the nation’s fiscal picture.”

Retrenchment proponents see American military spending as contributing to the growth of public debt 3 and the country’s relative economic decline, and they argue that as it approaches its credit limit, the US should cut military spending and act preemptively to forestall steeper decline and even bankruptcy. Some retrenchment supporters also fear that negative feedback between military overstretch and economic decline will eventually put America’s coercive hegemony at risk because economic might is the wellspring of military might (Calleo, 1982; Chace, 1981; Kennedy, 1987a, 1987b; MacDonald and Parent, 2011). In short, retrenchment proponents agree that reducing military spending is an economic necessity, although they disagree about the extent to which the US should reduce its spending and overseas presence as well as the desirability of sustaining military primacy.

This argument is noteworthy not only because of its centrality to the retrenchment argument, but also because academic defenders of deep engagement have as yet no direct response. Scholars and policymakers who oppose retrenchment maintain that American military dominance has produced significant economic benefits and warn that reductions in military spending will reduce these benefits (Brooks, et al., 2013; Brooks and Wohlforth, 2016; Gottlieb, 2012; Kagan, 2012; Sestanovich, 2014). Three main arguments point to such benefits. First, according to a research program closely connected with the work of Robert Gilpin and Stephen Krasner, military power underwrites an open economic order. In a series of books, Gilpin and Krasner explain the logic and evidence for hegemonic orders that rest in part on an outsized global military role (Gilpin, 1975; Gilpin, 1981, 1987, 2001; Krasner, 1978). A dominant military power that equates its own interest with expanding economic globalization benefits from providing a stable political context that makes economic exchange more secure and predictable (Brooks, et al., 2013; Brooks and Wohlforth, 2016; Norrlof, 2008, 2010).

Second, military primacy generates other direct benefits, such as official support for the hegemon’s currency; sustained capital inflows during times of distress; protection of residents’ foreign investments; and economic contributions to the hegemon’s military activities, including economic transfers through basing fees (Beckley, 2011; Helleiner, 2008; James, 2009; McNamara, 2008, Norrlof, 2008, 2010; Posen, 2008).

Third, the preeminent military power leverages security to extract economic favors from allies in exchange for protection. As a background condition, security allows the hegemonic power to win concessions in economic and trade negotiations (Ikenberry, 2011; Mastanduno, 2009; Norrlof, 2010). Economic agreements flow from the barrel of a gun.

These arguments are attracting a growing response (Drezner, 2013; Kirshner, 2007) but they do not directly address the links connecting deep engagement, high military expenditures, debt and decline—a concern that has preoccupied critics of US grand strategy for four decades. After all, throughout history, the largest most competitive economies have generally been the greatest military powers of their time. Theories of hegemonic decline predict that either war or economic weakening will erode the dominant power’s military leadership (Gilpin, 1981, 1987; Kennedy, 1987a,b; Modelski, 1987; Rasler and Thompson, 1994). Scholars who advocate retrenchment specify the mechanism causally linking military expenditures with economic decline: military spending has contributed to increased public debt, and escalating debt has, in turn, been responsible for America’s relative economic deterioration. Lacking, thus far, is a rigorous evaluation of the evidence for these claims.

Is the argument right? Analyses of the effect of US military expenditures on US public debt have received relatively little attention. A small stream of literature investigates the relationship between military spending and public debt. Scholars have found evidence that military expenditures can explain public debt, though mostly for small, especially developing, countries (Kollias et al., 2004; Looney and Frederiksen, 1986; Narayan and Narayan, 2008; Nikolaidou, 2011). A recent exception uses panel data to investigate whether a positive correlation exists for NATO countries (Alexander, 2013). The study shows that defense spending as a share of GDP determines the public debt share of GDP, but the research does not disaggregate the results for the United States (Alexander, 2013). Greater consideration has been given to determining the association between military spending and external debt, which consists of a portion of the public debt and comprises both government and private debt (Anfofum et al., 2014; Dunne et al., 2004; Feridun, 2005; Looney, 1989, 1998; Smyth and Narayan, 2009; Wolde-Rufael, 2009).

We answer this question in two stages, starting with the most relevant economic theory and then turning to empirical analysis.

Theory: The bankruptcy myth

The key propositions here are that US military spending drives its public debt, and that high levels of US public debt threaten its economy. As shown in Figure 1, America’s public debt relative to GDP has experienced a long-term upward drift. Given this trend line, scholars worry that the significant amount of debt issued to finance America’s grand strategy has increased the overall amount of debt and exposed the US government to the risk of bankruptcy (Gholz and Press, 2001; Layne, 2010; MacDonald and Parent, 2011). Drawing lessons from great power fiscal pressures in the past, MacDonald and Parent (2011: 19) make an analogy between the government’s budget constraints and the spending constraints of households and firms: “The underlying logic of this behavior is solvency. States, like firms, tend to go bankrupt when they budget blithely and live beyond their means.”

US public debt relative to GDP 1973–2015.

Even critics of MacDonald and Parent’s logic of retrenchment agree with these insolvency claims. “[P]ower transition[s] do not generate insolvency more rapidly or with greater severity than other periods in a state’s decline” (Haynes et al., 2012: 190). While questioning whether power transition causes insolvency, this statement accepts that insolvency is at issue. Responding to this criticism, MacDonald and Parent confirm their concern with insolvency:

In contrast, a great power that falls in the ranks from number three to number four is more likely to lack capabilities, be closer to bankruptcy…[because to live] beyond one’s means is possible temporarily, but prolonged insolvency invites a terrible reckoning. (Haynes, et al., 2012: 202)

The strongest version of the case for the economically debilitating nature of deep engagement’s military expenditures is thus that continued high military spending risks insolvency. The problem with this argument is that it is not supported by standard economic theory. First, governments do not go bankrupt in a strict sense. Although firms and households can run out of money and become insolvent,

[t]he simple definition of insolvency—negative net wealth—is hardly applicable to sovereign borrowers […] because, in almost all instances, the outstanding debt of a state is less than the assets owned by the government or by its nationals and that the government might seize by resorting to its coercive powers. (De Bonis et al., 1999: 70)

Moreover, whereas governments have the option of seizing domestic assets to honor debt, sovereign assets cannot be easily liquidated through the judicial system or by force, further differentiating sovereigns from non-sovereigns (Panizza et al., 2009: 652–655).

Second, states can choose to avoid a strict interpretation of insolvency, according to which “the total stock of outstanding debt (domestic plus external debt) cannot exceed the present discounted value of current and future net incomes—i.e., the difference between tax revenues and government expenditures” (De Bonis, et al., 1999: 70). Based on this criterion, countries that fail to undertake policy reforms to generate higher income will become insolvent (De Bonis, et al., 1999: 70–71).

Third, bankruptcy can be interpreted still more loosely as a hard borrowing constraint, with mounting debt triggering a sovereign debt crisis. However, some governments, notably the American government, do not face bankruptcy even in this sense. Countries operating under a flexible exchange rate regime and capable of borrowing in their own currency cannot be forced into insolvency. Both of these conditions apply to the US. The dollar floats freely, and despite significant recent challenges, no other currency plays a comparable international role (Cohen and Benney, 2013; Norrlof, 2014).

The exchange rate regime matters because countries can reduce the size of their debt relative to their economy in three essential ways: by stimulating growth, running government surpluses or inflating the debt away. The effectiveness of creating inflation by printing money hinges on a freely floating exchange rate. Countries with fixed exchange rates cannot turn to the printing press to repay debt without the risk of depleting foreign exchange reserves because foreign investors will withdraw their investments in anticipation of inflation and pending devaluation. By contrast, countries with freely floating currencies that have not committed to converting their currency into any other country’s currency, an artificial currency, such as Special Drawing Rights, or gold or any other metal do not have to worry about depleting foreign exchange reserves in the face of a speculative attack. Rather, investors fear inflation, upward pressure on interest rates and downward pressure on the currency (Wray, 1998).

Another division exists between countries borrowing in their own currency and countries borrowing in foreign currency. The American, British and Japanese governments primarily borrow in their own currencies. In fact, most advanced countries borrow in their own currency to some extent, depending on external demand for bonds denominated in their currency. The US government has first-rate borrowing opportunities because it provides the principal reserve currency, generating high external demand for US Treasury bonds, allowing the US to borrow at low rates.

Combined, a freely floating exchange rate and the capacity to borrow in one’s own currency create the possibility of inflating debt away. Borrowing in the domestic currency protects the government from an increase in the (domestic currency) value of debt as a result of inflationary pressures and associated depreciation. However, even governments capable of inflating their debt away pay a price. Normally, interest rates rise to compensate investors for holding bonds that are expected to lose value because of inflation and depreciation. By taxing domestic investors (with inflation) and foreign investors (with depreciation), this adjustment process allows a country to avoid involuntary default and improve its competitiveness vis-à-vis the rest of the world. However, the government obviously cannot issue an infinite amount of debt. Inflationary pressure constrains borrowing, and a collapse in the demand for bonds causes interest rates to rise, given the inverse relation between bond prices and yields.

One cannot assume that this adjustment will play out in an orderly fashion, even for the US. A scenario could well materialize with reduced savings and investment owing to rampant inflation. In a worst-case scenario, consumers will begin to hoard goods in anticipation of higher future prices causing foreign investment to decline, especially when expectations of further depreciation persist. A falling dollar will hurt some domestic actors because depreciation increases the value of debt denominated in foreign currency; unlike the American government, not all private individuals, firms, corporations and financial institutions can borrow in dollars. Depreciation also increases the price of imports, including the price of both intermediate inputs for business and final goods for consumers. Excessive public debt can thus have adverse effects on the overall health of the economy.

Although high levels of public debt pose potential problems for any country, the US literally faces no looming insolvency. If intended figuratively, the evocation of a debt ceiling does not provide any indication of how to test the economic implications of borrowing. The retrenchment debate should include a discussion of the consequences of public debt in different contexts and for different actors because borrowing places varying constraints on governments and non-governmental actors, governments operating under different exchange rate regimes, governments issuing debt in domestic as opposed to foreign currency and governments supplying the principal international currency.

Well established economic theory tells us that the insolvency argument for US grand strategic retrenchment is unfounded, but also that high levels of public debt can have economic downsides for the United States. Scholars who do not assume that failure to rein in spending will result in fiscal insolvency stress these downsides, arguing that rising US indebtedness contributes to economic decline (Pape, 2009; Walt, 2011). We have identified a number of questions that have yet to be addressed before scholars can conclude that these apply to the United States, given its unique international position and expected levels of debt. But a prior question begs answering: how significant is military spending as a driver of US public debt?

Empirical analysis: Military spending and US public debt

Our analysis considers precisely the period during which academic interest in the links between hegemonic grand strategies, military spending and economic decline took root and flourished: from the post-Vietnam 1970s, through the “Reagan buildup” of the 1980s to the dramatic escalation of US ambitions and defense spending in the 2000s. The time frame for our analysis covers the period when the US dollar has been freely floating, 1973q2–2015q1. Although Nixon uncoupled the dollar from gold in August 1971, countries continued to peg to the dollar until the signing of the Smithsonian agreement. We thus present the first empirical study of the influence of US military spending on its public debt.

We offer a statistical test of the argument that US military spending contributes to economic decline by increasing the public debt. Because all government spending has the potential to increase the public debt, the real test is whether growth in military spending significantly determines growth in public debt, which involves examining the following hypothesis:

Data and methods

Drawing on an original dataset (1973–2015), we calculate quarterly percent changes in the growth of US public debt (the dependent variable), military expenditures (the main explanatory variable) and four control variables—GDP, social benefits, interest payments on the debt, as well as income tax. In constructing our dataset, we collected statistics from Global Financial Data (GFD, 2016) and the Bureau of Economic Analysis (BEA, 2016) including defense data from the US National Product Accounts. We use US defense statistics reported by the BEA since they are preferable to the data reported by SIPRI and NATO (Brauer, 2007).

Our dependent variable is total (i.e. gross) US government debt. We use gross debt to avoid criticism that we are not accounting for the entire stock of debt. Some economists prefer to use an alternative measure of government debt, the debt held by the public, which excludes the portion of debt held by the government (intra-governmental holdings). Intra-governmental holdings are non-marketable securities held in government funds and consist of debt that one branch of the government owes to another branch. “Government funds (e.g., Social Security and Medicare trust funds) are typically required to invest excess annual receipts in federal debt securities issued by the Treasury Department, thus creating liabilities of the Treasury and assets of the trust funds” (Office of Management and Budget [OMB], 2014: iv). 4 In this study, we report our findings for our main variable of interest measured as gross government debt but have verified that our results are robust to the specification of debt measured as debt held by the public.

Our main explanatory variable is military spending and consists of defense outlays by the Defense Department. Because of data limitations, we do not include separately-budgeted outlays for overseas contingency operations (OCO). The non-defense variables often singled out as having the most effect on public debt are: social security, Medicare/Medicaid, state, local and federal income taxes. Our variable “social benefits” includes all welfare transfers to households; in particular, social security, Medicare, Medicaid, unemployment insurance, and the various items under the category “other” spending. However, we exclude veterans’ benefits since these could be considered part of the costs of defense required to finance the current grand strategy. 5 In addition, we also include interest payments on the debt, which represent the cost of past spending. We also explicitly control for the “Bush tax cuts” by controlling for changes in income tax. Indeed, we control for changes in income tax more broadly defined since we not only include federal taxes but also state and local tax. In addition, GDP growth could affect growth in public debt if periods of slow growth prompt the government to pursue a more Keynesian policy, placing upward pressure on the debt. Since changes in spending do not immediately affect the debt, we lag all spending variables one quarter. Lastly, we note that all our data are “real,” seasonally adjusted, in constant 2010 US dollars.

We use Ramsey’s (1969) error specification error test (RESET) to ensure that the functional form of our model is correctly stated. While we should not expect endogeneity in the form of reverse causality given that public debt does not cause military spending, we nonetheless consider the possibility of omitted variable bias using the linktest. The test assumes that if the model is properly specified the addition of independent variables should not be significant, except by chance (cf. Tukey, 1949). Therefore, on both theoretical grounds and according to the test, the model does not suffer from specification error owing to omitted variables.

Before proceeding with time series analysis, we ensure that the data are stationary. The augmented Dickey–Fuller test (1979) indicates that the variables have a unit root. Stationarity is achieved through first differencing, giving us quarterly differences in growth. Both the Breusch–Pagan/Cook–Weisberg test (1979, 1983) and the White test (1980) reveal heteroskedasticity. To check for serial correlation, we use Durbin’s (1950) alternative to the Durbin–Watson test as well as the Breusch–Godfrey test (Breusch, 1978; Godfrey, 1978) for higher order serial correlation. We find some degree of serial correlation according to both tests. 6 To overcome both heteroskedasticity and serial correlation, we perform a Newey–West (1987) regression as well as a Prais–Winsten (1954) feasible generalized least squares regression (FGLS). Although Newey–West and Prais–Winsten errors protect against serial correlation, we explicitly address serial correlation by including a lagged dependent variable (LDV) in models 2, 4, and 6. Inclusion of a lagged dependent variable has substantive meaning since past levels of debt influence the size of the debt. We also report findings from a baseline ordinary-least-squares (OLS) regression with robust (Hubert–White sandwich) standard errors that corrects for the presence of heteroscedasticity.

Findings

This article scrutinizes the argument that growth in military spending is responsible for growth in US public debt. As illustrated in Figure 2, the paces of change in the two variables have moved in opposite directions at least as frequently as they have moved together.

US public debt and military expenditures, 1973–2015.

If changes in US military spending do not correlate with changes in US public debt, the mechanism specified by retrenchment supporters has no empirical support. While there may be other causal pathways whereby military spending contributes to economic decline, evidence against the hypothesis that growth in military expenditures drives US debt constitutes evidence against the case for retrenchment based on debt-fueled decline.

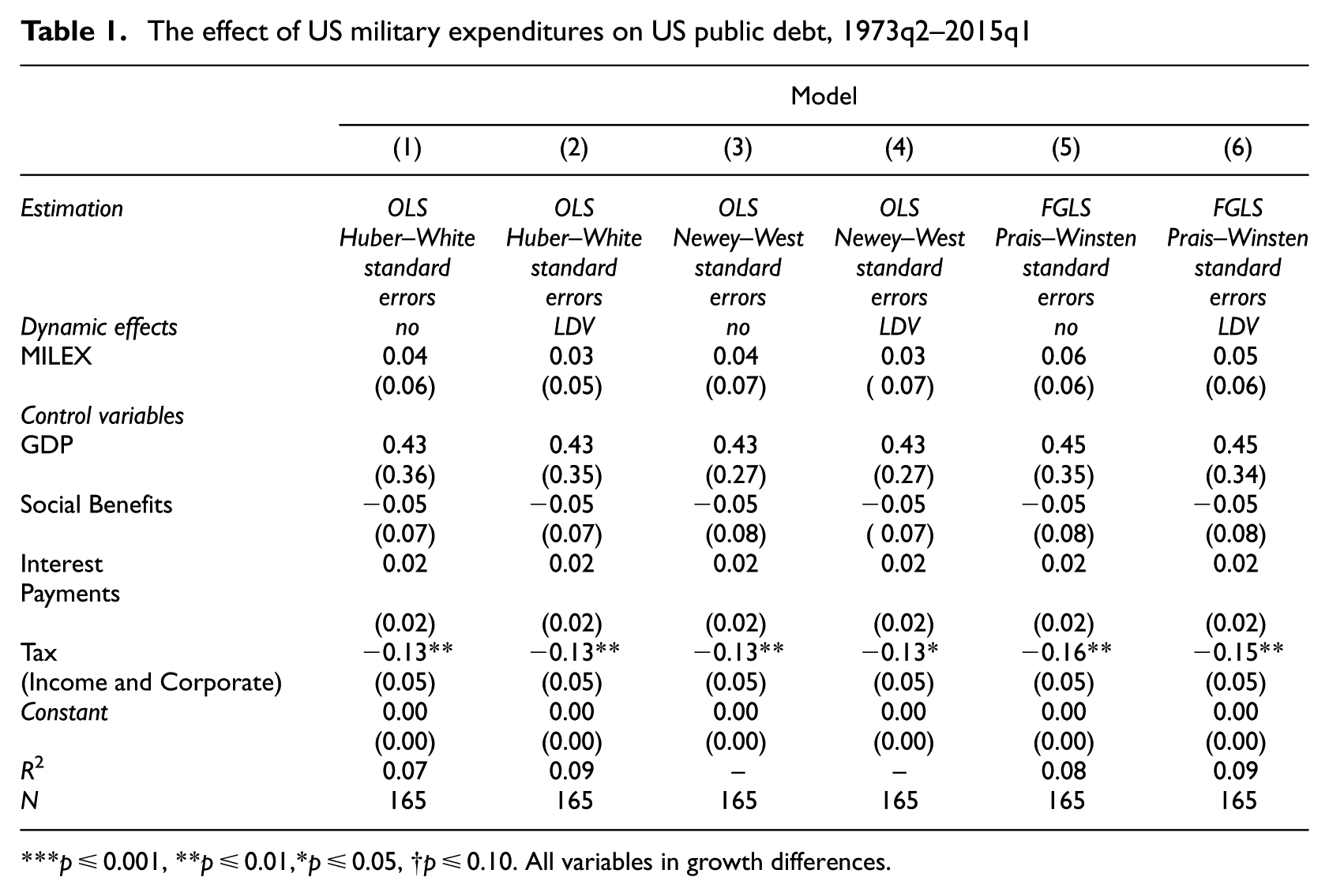

The results in Table 1 demonstrate that we must reject H1. We find no significant association between quarter-to-quarter increases in the growth of military expenditures and public debt. Growth in US military spending does not correlate with growth in US debt. The most significant explanatory variable for growth in America’s public debt is income tax. This variable is substantively important and significant across all six estimation techniques. Given rising levels of debt, and the negative association between income tax and the public debt, we infer that tax cuts have been a main contributor to the expansion of public debt in the US. Consequently, raising taxes should lower the debt. It is noteworthy that even social benefits, which includes spending items such as health care and other forms of welfare spending that are usually singled out as responsible for increasing the debt, are not statistically significant drivers of the debt. We also note that R 2 is rather low across the models (higher in the smaller samples). Given our inclusion of principal contributors to the debt, as well as our diagnostic test indicating that the functional form of our models is not mis-specified, we interpret this as suggesting that public debt is difficult to predict.

The effect of US military expenditures on US public debt, 1973q2–2015q1

p≤0.001, **p≤0.01,*p≤0.05, †p≤0.10. All variables in growth differences.

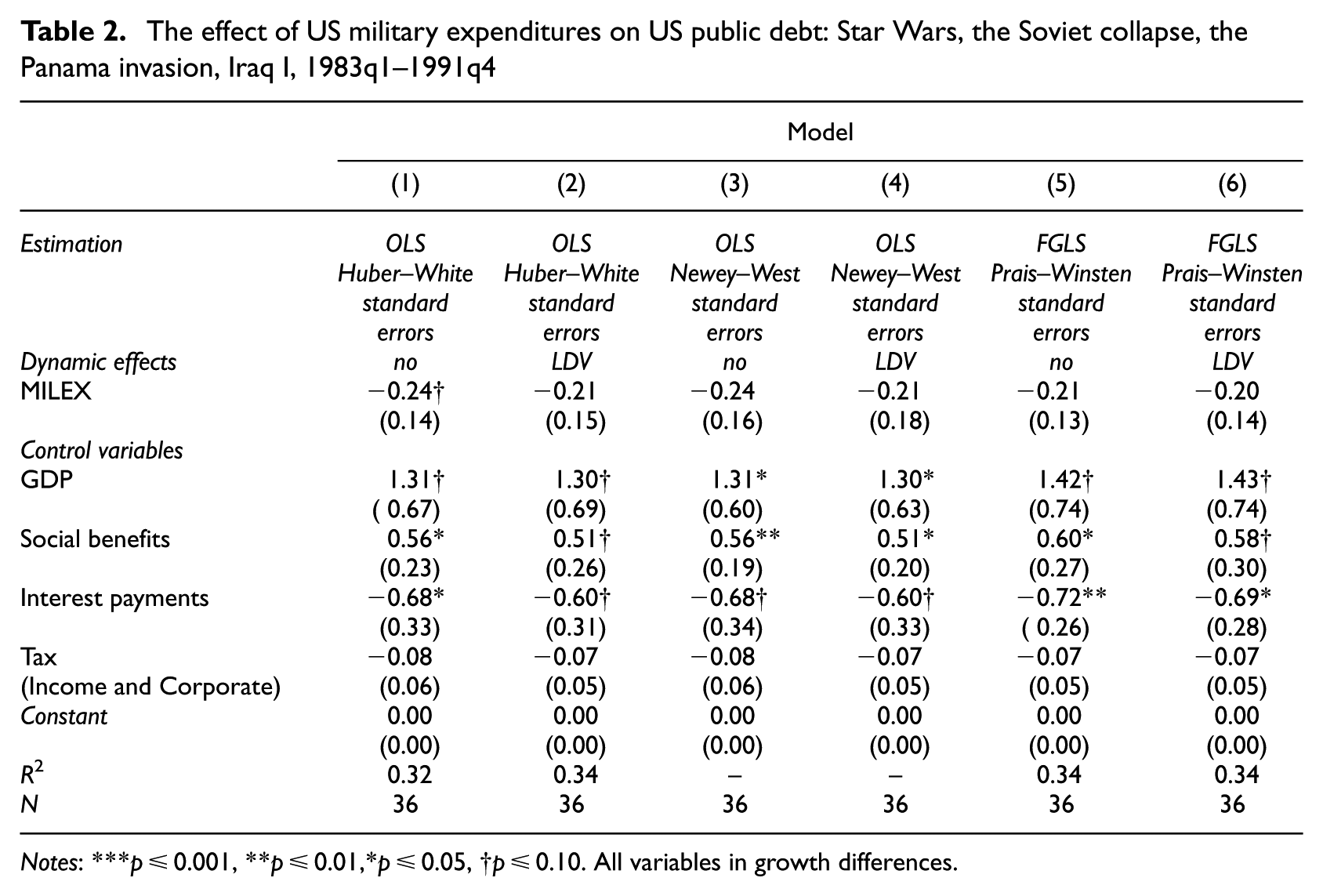

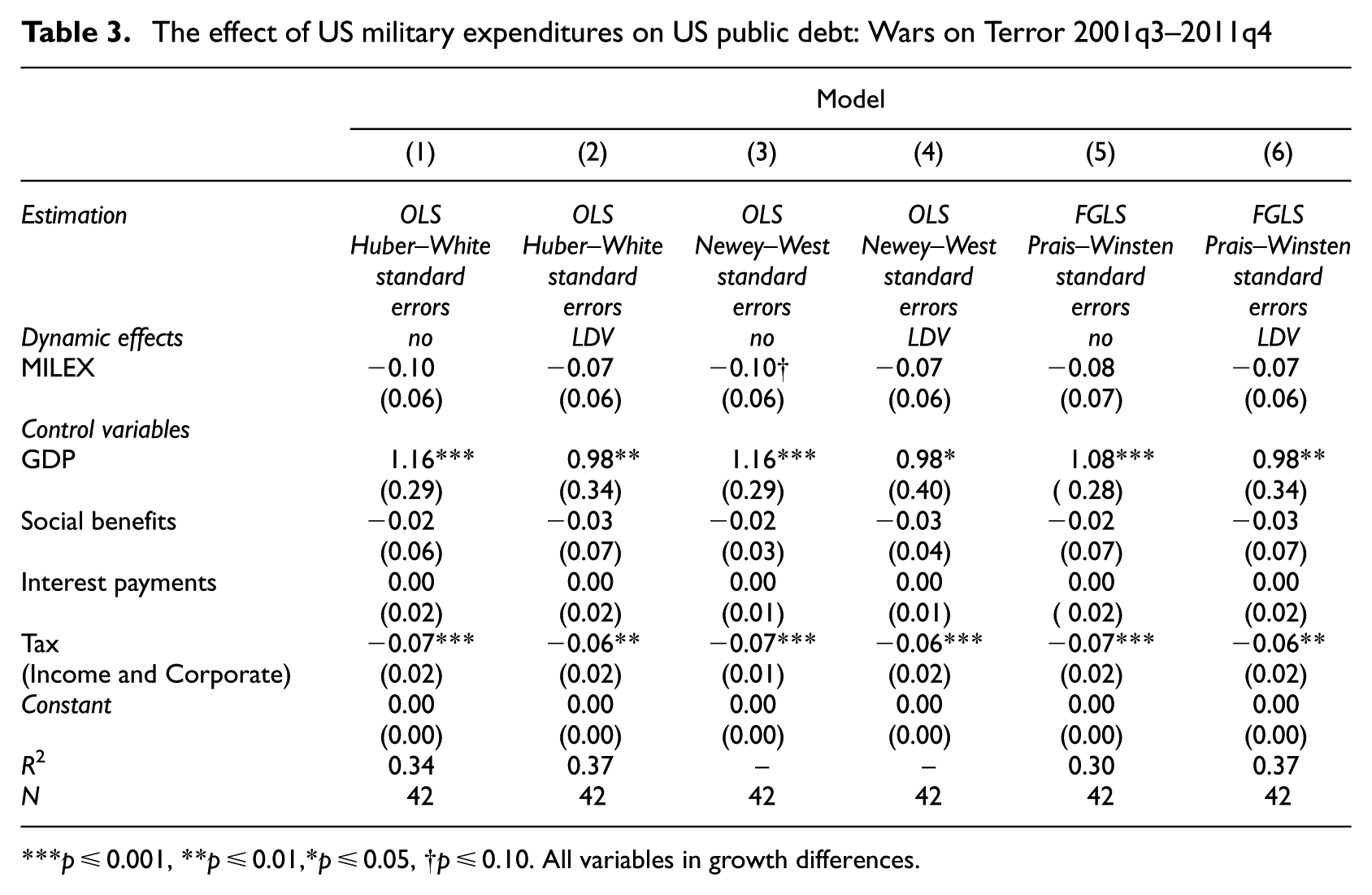

Retrenchment proponents might object that long-term associations are less important than key periods in which the grand strategy leads to major buildups, such as the 1980s and the post-9/11 decade. These were two periods that featured major increases in military spending, international activism, large deficits and widespread concern over debt and decline. Table 2 runs the same regression between the first quarter of 1983—when Ronald Reagan intensified the arms race with the Soviet Union—and the dissolution of the Soviet Union in the fourth quarter of 1991. This period also coincides with the Panama Invasion 1989–1990 and the 1991 Gulf War led by George HW Bush. Yet, during this time military spending does not have a statistically significant impact on the debt. 7 During this time, some of our models suggest that growth in interest payments on the debt, social benefits and GDP significantly impact growth in the debt. The positive association between a growing economy and rising debt may seem counterintuitive. We should expect economic slowdown to put more pressure on the government to spend as tax revenues shrink with rising unemployment while demands for federal benefits increase. But governments are not necessarily responsive to these pressures. Some governments spend procyclically, continuing to spend as GDP increases and/or do not try to cushion economic downturns, in which case falling GDP would have coincided with lower government spending. If spending was not curtailed during times of expansion, demands to reduce deficits and debt may result in austerity policies as the economy contracts. Table 3 reports regression results between the third quarter of 2001 and the fourth quarter of 2011, corresponding to the Wars on Terror launched against Afghanistan and Iraq in response to the attacks against the United States on September 11, 2001. During this period, as “non war”, that is, base defense spending rocketed up 40%, from $390 to $540 billion in constant (2010) terms, we still see no evidence of military spending augmenting the debt. Caution is however warranted in interpreting these results owing to the omission of OCO funding, which financed a substantial part of the wars on Afghanistan and Iraq and which is not included in base defense spending. Changes in taxes and GDP are significant determinants of the public debt with tax cuts and economic growth increasing the debt. While the results in Tables 2 and 3 are suggestive, we warn against drawing strong inferences based upon them in light of the few observations in the regression.

The effect of US military expenditures on US public debt: Star Wars, the Soviet collapse, the Panama invasion, Iraq I, 1983q1–1991q4

Notes: ***p≤0.001, **p≤0.01,*p≤0.05, †p≤0.10. All variables in growth differences.

The effect of US military expenditures on US public debt: Wars on Terror 2001q3–2011q4

p≤0.001, **p≤0.01,*p≤0.05, †p≤0.10. All variables in growth differences.

The core implication of these results—that defense spending in the post-Second World War era is frequently dwarfed by other drivers of public debt even during periods of defense buildups and activist foreign policy—is consistent with analyses conducted by the non-partisan Congressional Budget Office (CBO). After declining steadily in the post-war period (including in the Vietnam War years) federal debt held by the public climbed sharply in the Reagan presidency, from 24.5% of GDP in the last pre-Reagan year to 39% in the first post-Reagan year (CBO, 2010). The causes of the budget deficits that fueled that growth have been the subject of partisan debate ever since, but, consistent with our results, other contributors (notably much higher interest payments owing to the Federal Reserve’s anti-inflationary monetary policy) outweighed military spending in CBO’s retrospective analysis (CBO, 1988). The same goes for the post 9/11 decade. In explaining how its 2001 forecast of a $5.6 trillion surplus by 2011 ended up as a $6.1 trillion deficit, CBO (2012) estimated that economic changes alone contributed far more than all increased military spending, including on all OCO in Afghanistan, Iraq and elsewhere. 8 Our findings also support the CBO’s assessment that lower than expected tax revenues including tax cuts significantly contributed to increasing the debt.

Overall, the findings reported above suggest that the growth in military spending is not responsible for the growth in America’s sovereign debt. Our findings cast doubt on the central claim made by retrenchment proponents. While more restrictive criteria for these propositions may establish them as conditionally true, the available evidence does not support their current formulation.

Robustness checks

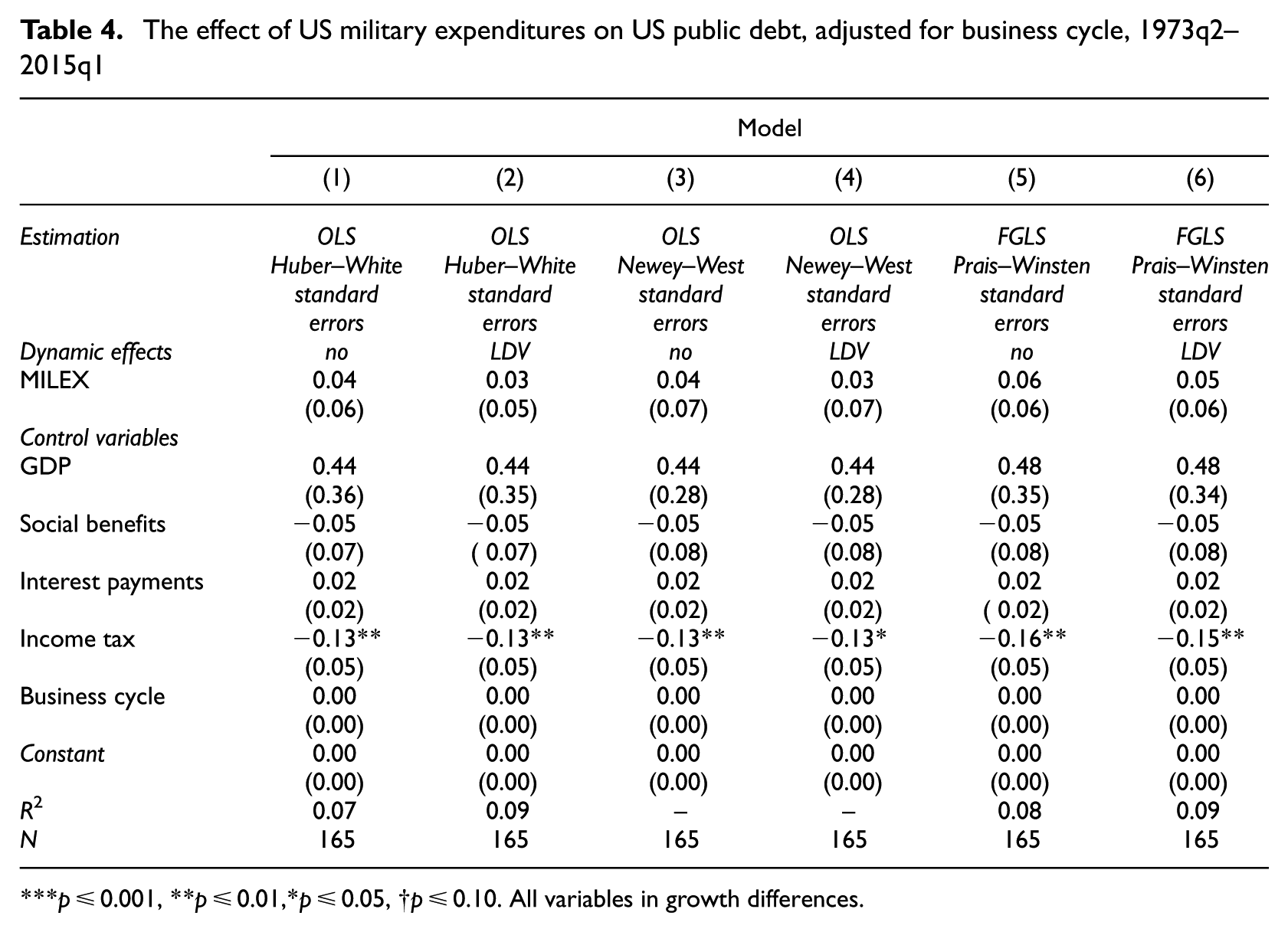

To ensure that all of the regressions are robust to the inclusion of additional variables that might affect the debt, as well as temporal aggregation of the unit of analysis, we report regression results for the business cycle and also examine year on year growth in spending and debt. Based on data from the National Bureau of Economic Research (NBER), we examine the impact of the contraction (expansion) of the business cycle from peak to trough (trough to peak). 9 We include this variable because one might expect a contraction of the business cycle to increase the debt and an expansion of the business cycle to reduce the debt.

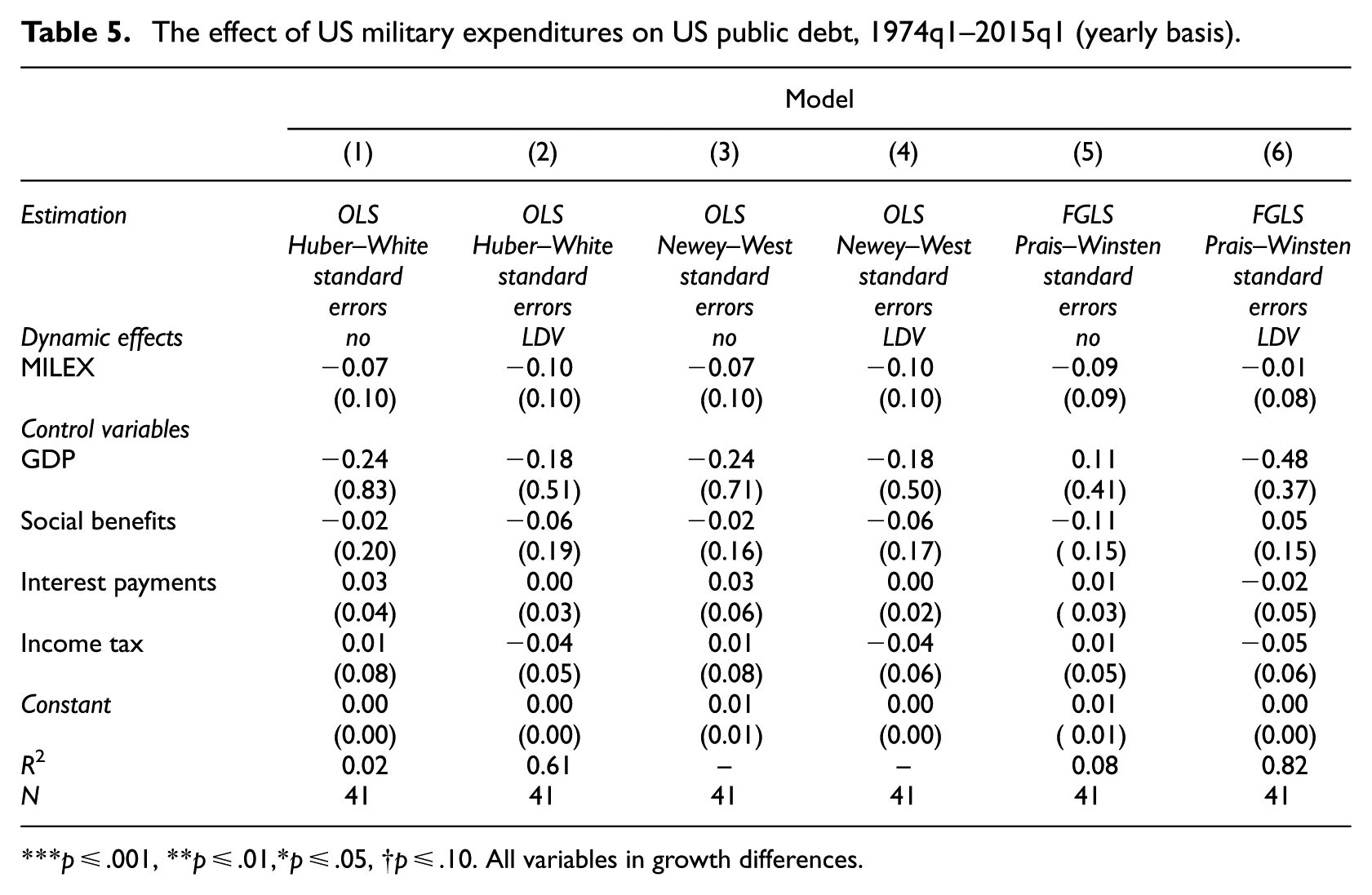

As shown in Table 4, inclusion of the business cycle does not alter the significance, or substantive effect, of our main explanatory variable (growth in military expenditures) on the dependent variable (growth in public debt) nor does it significantly impact the control variables. We also verify that any reduced form of the model does not change our results. The model is extremely robust, practically invariant to our controls. Table 5 performs the regression using yearly (instead of quarterly) growth differences in spending. More precisely, we estimate our models using year-on-year regression to examine if differences in the rate of spending between the current and the previous year determine differences in the growth of the debt in the current year. We find that these yearly changes in military spending do not predict the debt. Past levels of debt account for nearly all the predictive power in the models (compare R 2 with and without LDV); the LDV is highly significant across all models.

The effect of US military expenditures on US public debt, adjusted for business cycle, 1973q2–2015q1

p≤0.001, **p≤0.01,*p≤0.05, †p≤0.10. All variables in growth differences.

The effect of US military expenditures on US public debt, 1974q1–2015q1 (yearly basis).

p≤.001, **p≤.01,*p≤.05, †p≤.10. All variables in growth differences.

Advancing the debate

Our findings contradict key claims concerning the economic consequences of funding America’s grand strategy. While military spending, like all forms of government spending, has the potential to contribute to the public debt, some retrenchment supporters assert a stronger claim. They argue that military spending should be reduced to save the country from dire economic consequences, which might even lead to bankruptcy. While spending less on the military may—as part of a larger fiscal policy initiative—help reduce the overall level of debt, retrenchment advocates have not clarified why reducing military spending, as opposed to other budgetary items, should be a priority when the rate of growth in military spending does not predict growth in US public debt.

Retrenchment opponents correctly highlight that military spending has played a marginal role in increasing the public debt (Brooks, et al., 2013). The statistical results reported in Table 2 provides robust empirical proof of their claim, and generalizes and extends their argument to the entire era of a freely floating dollar. Military spending has not been a principal driver of the public debt since 1973. Based on the available evidence, the absence of a statistically significant correlation between US military spending and the public debt contradicts the claim that forestalling further growth in the debt requires downsizing the military. The evidence also contradicts the broader claim that reducing military spending offers the best way to prevent debt-fueled decline.

This result does not eliminate all motivations for curtailing military expenditures, which may still be sensible if Americans value alternative targets for expenditure reduction—social security, health care, unemployment benefits, education, R&D, infrastructure or other government programs—more than they value military spending. In addition, US citizens may prefer curtailing defense expenditures to accepting higher taxes. As we show, however, tax reductions have a strong, positive effect on the growth in debt. Therefore, substantial cuts in military spending would be required to counteract tax reductions. While some retrenchment supporters correctly focus on these tradeoffs (Walt, 2011: 12; Williams, forthcoming, 2016), it is unclear how low they see military spending going. Historically, the key cause of rising US public debt has been war, the Civil War, the First World War and the Second World War. But after the Second World War no war has been of that magnitude (and the United States adopted a flexible exchange rate in the 1970s). Retrenchment supporters do not dispute US involvement in the World Wars. Nor do they generally dispute US containment of the Soviet Union, although they believe it came at the price of rising deficits and debt. However, even during the most intense period of the arms race in the latter Cold War, Reagan’s buildup in the 1980s, military spending does not appear to have been the main cause of increasing debt. If some levels of military spending are justified despite their impact on the debt, while other levels do not significantly impact the debt, the case for retrenchment based on the debt impact of military spending is weak.

Ultimately, political preferences shape societal choices over government spending, thus moving the argument away from the realm of economics. As noted by Francis Bator (1989) when retrenchment was debated in the 1980s:

political does not mean arbitrary. There are real choices to be made here: choices not about deficits, or debt, or taxes, but about the best use of our labor and material resources. Opinions will differ about the best choices; that is what makes the problem political rather than merely technical. (Bator, 1989: 121)

We derive three recommendations for future research on the economic consequences of America’s grand strategy.

First, strengthening the economic basis of the arguments will facilitate both quantitative and qualitative tests of the main variables in the analysis. Revised propositions about the economic consequences of public debt need, at a minimum, to avoid the misleading language of insolvency and bankruptcy to account for variations in the constraints confronted by different countries and to recognize the weaker constraints faced by great powers such as the US. It is long past time to retire the “household budget” analogy when discussing the economic cost of the grand strategy of a superpower with the key global reserve currency in the age of flexible exchange rates.

Second, greater attention should be given to demarcating boundary conditions for the proposed arguments. By revising propositions to include the impact of additional variables and developing more precise claims about the nature of different sets of relationships, new associations might be revealed. Future research should clarify the circumstances under which military spending contributes to economic decline. What causal pathways, not mediated by debt, connect military spending and decline?

Third, the conversation should migrate to a new level of inquiry with greater emphasis on validating key claims. Perhaps most important, both sides in the debate should be clearer about the nature of the different arguments regarding the economic costs of US grand strategy that are in play. The deep engagement→military spending→debt→decline argument is especially strong because it posits that the strategy is ultimately self-defeating, failing to achieve a core objective of sustaining US material preeminence over the long run. It is arguably for precisely this reason that the claim has been popular with critics of US foreign policy since the decline debates of the 1980s. Too often, however, this strong argument is mixed up with a less direct (if still important) claim about the welfare effects of shifting resources from military to other ends. How military expenditures at the average levels the US has sustained affect long-term macroeconomic performance remains an open question for economists. And whether shifting resources away from military to other purposes and what purposes those might be (health care, unemployment benefits, social security, funding for infrastructure or education, tax cuts, etc.) is a political question that can only be answered by voters.

Conclusion

The resources allocated to upholding America’s grand strategy have come under fire in the context of its economic decline relative to rising rivals. While retrenchment advocates oppose the continued funding of external US ambitions on multiple grounds, the debate has recently sharpened around the economic repercussions of sustaining deep engagement. Scholarly and public interest in this issue came to the fore as hard caps on government spending, so-called sequestration, were imposed on a protesting Pentagon. Subsequent developments in American politics—notably the 2016 Republican primary—revealed that a substantial portion of the US electorate responds to expressions of concern that US economic prosperity is being sapped by military security subsidies to allies.

To address this issue, we leverage a unique dataset of quarterly US military spending and public debt as well as other government spending items between 1973 and 2015 to investigate a key claim made by retrenchment proponents. Our dataset encompasses the period between the second quarter of 1973 and the first quarter of 2015. This period spans the entire period of a freely floating dollar. Retrenchment advocates claim that military spending has fueled the growth of public debt, which will have adverse consequences for US growth and might, some worry, drive the US to the verge of bankruptcy. They raise critical questions about the contribution of military spending to sovereign debt as well as the larger ramifications of continuing to fund military primacy and alliance commitments in a challenging economic environment. However, they have not backed their claims with systematic empirical inquiry nor grounded their arguments in the economics of sovereign debt.

This article redresses this gap in the literature in two ways. First, we clarify the actual economic constraints faced by the United States in issuing sovereign debt. Though the potential consequences of excessive debt can be severe, including punishing interest rates as well as sharp and disorderly depreciation, the idea of US insolvency cannot be reconciled with standard economic theory. Second, we subject the claim regarding military spending driving growth in US debt to an empirical test. Our findings cast doubt on the central claim made by retrenchment proponents. According to the statistical analysis, there is no support for the argument that military spending brings on economic decline via the sovereign debt channel.

The bottom line is that an oft-expressed economic argument against the United States’ globally engaged grand strategy—that the military expenditures it entails is responsible for escalating debt—lacks grounding in empirical evidence and economic theory. Needless to say, the intuition about the necessity for the United States to retrench to counter economic decline could still be valid. A new research program should establish the particular circumstances, if any, that require retrenchment on economic grounds. We make three recommendations in this regard. First, to advance the debate, future research should elaborate theoretical propositions that are consistent with economic theory. Second, the scope conditions for the theorized relationship between observed variables should be specified. When does military spending cause economic decline via other mechanisms than via debt? Third, the extent and depth of our knowledge regarding these revised propositions should be broadened through systematic empirical research.

The results in this article unambiguously reveal the lack of evidence for one position currently adopted by retrenchment proponents; however, they do not unequivocally support existing levels of spending. Alternative propositions about the relationship between military spending and economic decline may support military retrenchment. Even so, the level of spending dedicated to defense may ultimately not be an economic but a political question. Even if military spending does not substantially contribute to the public debt, lower spending may nonetheless be desirable if the American public places a higher value on alternative spending. This normative component should figure in the debate moving forward. Scaling back military expenditures could be justified if America’s grand strategy can be funded using fewer resources or if such a strategy no longer serves the American people or the rest of the world.

Supplemental Material

Hegsust_cmps_supp_data – Supplemental material for Is US grand strategy self-defeating? Deep engagement, military spending and sovereign debt

Supplemental material, Hegsust_cmps_supp_data for Is US grand strategy self-defeating? Deep engagement, military spending and sovereign debt by Carla Norrlof and William C. Wohlforth in Conflict Management and Peace Science

Footnotes

Acknowledgements

We thank Mattias Vermeiren, Daniel McDowell, Andrew Baker, Jonathan Kirshner, Hubert Zimmermann, Stephen G Brooks, Jeffrey W Taliaferro, Jonathan Markowitz, Michelle Getchell, Eugene Gholz, Benjamin Miller, Michelle Murray, Wu Riqiang and Benjamin Valentino as well as three anonymous reviewers and the editor for helpful comments. We also thank Grace Skogstad and Gail Copland for financial support as well as Chris Cochrane for constructive feedback on an early draft.

Authors’ note

Preliminary versions of this article were presented at Ghent University, 20 March 2013, Dartmouth College, 17 October 2014, and at the annual meeting of the International Studies Association in Atlanta, Georgia, 16–19 March 2016.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.

Supplementary Material

The dataset and any other supporting materials employed for the analysis can be accessed via a supplementary data file hosted on SAGE’s CMPS website.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.