Abstract

As is widely known, public sector pension plans and state and local governments throughout the country are in trouble. Things are about to get worse. The Governmental Accounting Standards Board has adopted new accounting and reporting rules that will make underfunded plans of governments appear to be much more underfunded than under the current rules. The changes involve discount rates, amortization periods, asset valuation and a requirement that local governments that are party to cost-sharing multiple-employer plans report their proportionate share of the plan’s unfunded liability in their financial statements. In a parallel development, Moody’s Investor Services (one of the major credit rating agencies) is about to launch similar changes. The combined effect will be to add significantly to the debt of many local governments and likely force them into Chapter 9 bankruptcy. California is on the cutting edge of this development, with three sizable cities already in Chapter 9. This article will focus on California; however, the developments discussed apply to public pension plans and local governments nationwide.

This article examines the interaction of three important current developments affecting state and local government pension plans in California with ramifications throughout the United States. The first is the extensive underfunding of such plans resulting in part from the Great Recession that began in late 2008. The second is the approval of Statements 67 and 68 by the Governmental Accounting Standards Board (GASB). And the third is a number of Chapter 9 bankruptcy filings by local governments, mainly in California, and the attending litigation.

Governmental pension plans are in trouble throughout the United States. However, it is difficult to address these matters on a national basis because of the differences among the state constitutional and statutory provisions. California will serve as a microcosm of the whole: albeit, a very large and complex microcosm. It has a large number and a rich variety of public pension funds, and also, that is where the action is unfolding.

It is also difficult to generalize about the magnitude of the impact of the matters discussed below. In addition to the numerous differences among the jurisdictions and plans, many state and local governments have made or are making changes via legislation or referenda that will become effective at different times. Suffice it to say that they will change the aggregate underfunding from the hundreds of billions of dollars to the trillions.

This article is limited to public sector defined-benefit (DB) pension plans. It will not address the even larger underfunding problem of other postretirement employee benefits. Nor will it treat defined-contribution plans or hybrid cash balance plans, which, by definition, are always fully funded.

How Public Pension Funding Works

In contrast to the private sector, governmental DB pension plans are usually “contributory.” Employees are typically required to contribute a fixed percentage of their earnings to the pension fund. The governmental employer’s “annual required contribution” (ARC) is variable. It fluctuates from year to year with the funded status of the plan. This is measured by the “funded ratio” (assets/liabilities).

Assets may be either “actuarial value of assets” (AVA) or “market value of assets” (MVA). AVA involves some smoothing (averaging) of asset values over a number of years. This dampens year-to-year fluctuations and aids in government planning and budgeting. MVA measures asset values as of the measurement or valuation date. It is more volatile than AVA. Smoothing masks the true value of the pension plan assets, both up and down. Typically, assets are smoothed over a 3- to 5-year period. The California Public Employees’ Retirement System (CalPERS) adopted 15-year smoothing in 2005 after the experience of the 2001 recession. Given that that now includes the high funding levels of the late 1990s, CalPERS-funded ratios may be especially misleading over the next few years.

Liabilities or “projected benefit obligations” (PBO) are calculated by actuaries based on a number of demographic and economic assumptions. Demographic assumptions include age and seniority of the current participants, turnover rates, average retirement age and age-specific life expectancies of participant and spouse (mortality tables). Economic assumptions include forecasted price inflation, wage and salary increases and promotions and “return on investment” (ROI) of plan assets.

The plan’s PBO is converted to present value by using a discount rate. The discount rate may be thought of as a compound interest rate in reverse. Under current GASB rules, a pension plan may use the expected ROI on assets as its discount rate. That is typically 7.5% to 8.5% with 8% being the most common. The higher the discount rate the, lower the present value of projected liabilities and, hence, the higher the funded ratio and the lower the employer’s contribution. And the lower the discount rate, the higher the employer’s ARC.

The funded ratio and employer ARC are also affected by the amortization period. The current GASB rules allow unfunded liabilities to be amortized over up to 30 years. It was 40 years until 2006.

The combined effect of using a discount rate based on expected ROI, smoothed value of assets and lengthy amortization periods understates the true extent of underfunding of public pension plans. That will change when GASB 67/68 become effective in 2013 and 2014.

Structure of Public Pension Plans

In the public sector, DB pension plans are designated as “single employer,” “agent multiple employer” or “cost-sharing multiple employer.” In a single-employer plan, the employer’s contributions, expenditures and funded status are accounted separately and recognized in their financial reports. In an agent multiple-employer plan, assets are pooled for investment purposes, but everything else is accounted and reported separately. In a cost-sharing plan, the contributions, benefit payments and funded status are pooled. This provides the cost-sharing employers with a sort of insurance against year-to-year rate fluctuations due to variations in experience. That is especially important to small governmental employers. Under current rules, cost-sharing employers do not have to report unfunded liabilities in their financial reports.

In California, as in most other states, there is no clear line between state plans and local government plans. Rather, many state-run plans provide pension services to counties, municipalities and other local agencies within their jurisdiction. There are also many stand-alone pension plans such as the 20 California counties covered by the “1937 Act.” 1 These counties operate pension plans under the provisions of the 1937 Act and may provide pension services for the county and for “districts” within the county. To further complicate matters, San Luis Obispo and San Francisco counties sponsor independent plans that are not covered by the 1937 Act.

California has three large statewide pension plans (plus a number of smaller ones for judges and legislators). In reverse order of size, as measured by membership or asset values, they are the University of California Retirement Plan (UCRP), the California State Teachers’ Retirement System (CalSTRS) and CalPERS.

The UCRP is an example of a single-employer plan (ignoring some loose ends with the Department of Energy). It covers faculty and staff throughout the 10-campus system, its five medical centers and the affiliated Hastings College of Law. 2 It has 116,000 members and $42 billion in assets. For decades, the UCRP was overfunded and operated without either employer or employee contributions. As indicated in Table 1, its funded ratio fell below 100% for the first time in 2009, and the plan has recently reestablished employee and employer contributions.

Funded Ratios, 2001-2011.

Note. UCRP = University of California Retirement Plan; CalSTRS = California State Teachers’ Retirement System; CalPERS = California Public Employees’ Retirement System.

Source. Appendix table in Munnell, A. H., Aubry, J.-P., Medenica, M., & Quinby, L. (2012, May). The funding of state and local pensions: 2011-2015 (Brief No. 24). Boston, MA: Center for Retirement Research at Boston College., May 2012. Retrieved from http://crr.bc.edu/briefs/the-funding-of-state-and-local-pensions-2011-2015/.

Estimated.

CalSTRS is the second-largest public retirement plan in the country. It covers 856,000 certificated teachers, administrators and beneficiaries of public preschool through 14 (community college). It does not cover classified school employees. CalSTRS is a cost-sharing multiple-employer system. 3 It is funded by a statutorily required fixed 8% of earnings employee contribution and an 8.25% employer contribution. In addition, the state contributes about 2.5% of teacher earnings. Table 1 reports that that CalSTRS’ funded ratio has declined from 98% in 2001 to an estimated 73.1% in 2011.

A major legislative overhaul of CalSTRS is likely in 2013, including increased employee and employer contribution rates. In addition to addressing the plan’s underfunding, it will bring CalSTRS into compliance with the state’s pension reform legislation enacted in 2012 (AB 340). It requires an equal split between employee and employer contributions to cover the plan’s “normal costs” (benefit payments and administrative expenses for that play year). 4

CalPERS has 1.6 million members (1.1 million active and inactive and 536,000 retirees and survivors) and $242.5 billion in assets (as of November 2012); it is the largest pension plan in the United States. It may also be the most complex and the most interesting. According to Table 1, CalPERS funded ratio fell from 111.9% in 2001 to an estimated 86.9% in 2011.

CalPERS has three large categories of employers and their employees. One is employees of the State of California (including the faculty and staff of the massive California State University system). The 337,000 state employees account for 30.5% of active and inactive members of the system. The second category consists of 425,000 classified school employees (secretaries, custodians, etc.). It accounts for 38.5% of CalPERS members. The third group is the 342,000 e0mployees (31%) of the 1,573 local public agencies that contract with CalPERS for pension services. 5 For the 1,530 school districts and 1,573 local government agencies (with 2,044 plans), CalPERS is a cost-sharing multiple-employer pension plan.

CalPERS reports funded ratios based on MVA for each employer category. As of June 30, 2011, they were as follows: state, 70.3%: schools, 78.7%; and public agencies, 74.3%. Note that these funded ratios are not comparable with those of Table 1, which are based on AVA.

GASB 67/68

The GASB was established in 1984 to provide accounting and reporting standards for all state and local governments in the United States. It is the equivalent of the better known Financial Accounting Standards Board (FASB) in the private sector. On June 25, 2012, the GASB approved new Statements 67 and 68 to succeed Statements 25 and 27. The new accounting and reporting rules take effect June 15, 2013, for public pension plans and a year later for the governments that sponsor them.

GASB 67/68 statements cover a wide range of accounting and reporting requirements that are beyond the scope of this article. Most important, GASB replaced the existing discount rate used to convert PBO to present value (current dollars). It moved from allowing (but not requiring) a discount rate based on the long-term expected rate of ROI assets to a new “blended” rate. To the extent that pension liabilities are covered by actual assets, plans and employers may continue to use the old discount rate, typically 8%. Beyond that “crossover” point, they must use a much lower rate based on the cost of their other borrowing, derived from an index of high-quality municipal bonds (rated AA or Aa or better). Thus, public pension plans that are well funded or become so may continue to use the higher discount rate. Those that are underfunded, or become so, are going to look worse than before.

GASB 67/68 did two other things that will affect pension funding. One is to require that assets be priced at market value as of the valuation date. That is, it requires nonsmoothed MVA rather than smoothed AVA. This will make asset values fluctuate to a much greater extent. The other is to reduce amortization periods from up to 30 years to a period based on the remaining service lives of the participants, typically 10 to 12 years.

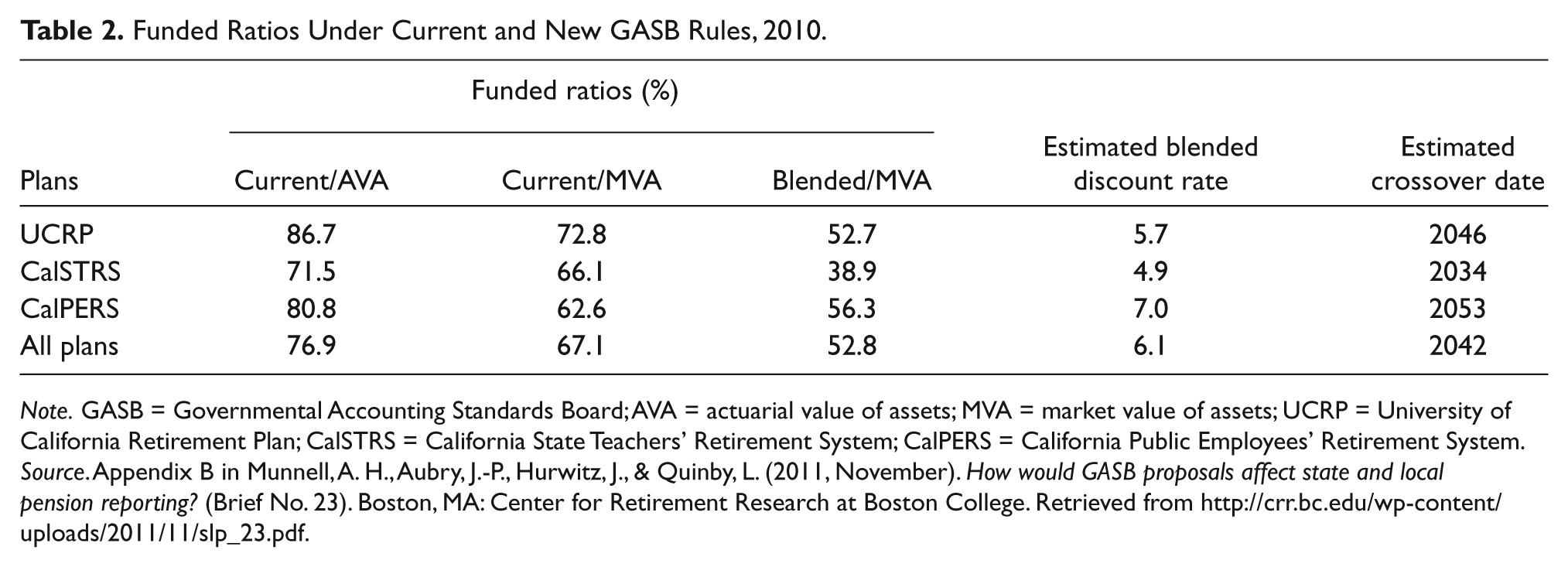

For underfunded public pension plans, the combined impact of the blended discount rate, the market pricing of assets and the curtailed amortization periods will be to make them appear to be in much worse shape than under the old rules. Table 2 displays the estimated impact of GASB 67/68 for all plans and for the three large California plans under different discount rates and asset valuation methods (AVA and MVA). It also shows estimated blended discount rates and estimated crossover dates.

Funded Ratios Under Current and New GASB Rules, 2010.

Note. GASB = Governmental Accounting Standards Board; AVA = actuarial value of assets; MVA = market value of assets; UCRP = University of California Retirement Plan; CalSTRS = California State Teachers’ Retirement System; CalPERS = California Public Employees’ Retirement System.

Source. Appendix B in Munnell, A. H., Aubry, J.-P., Hurwitz, J., & Quinby, L. (2011, November). How would GASB proposals affect state and local pension reporting? (Brief No. 23). Boston, MA: Center for Retirement Research at Boston College. Retrieved from http://crr.bc.edu/wp-content/uploads/2011/11/slp_23.pdf.

The GASB has no enforcement powers, and the new standards are accounting and reporting requirements, not funding requirements. Employers (governments) are urged to develop their own funding policies independent of GASB 67/68.

Another new GASB provision requires governments that are party to a cost-sharing multiple-employer pension plan to recognize in their financial statements their proportionate share (based on contributions) of the plan’s unfunded liability. This may come as a shock to many plan administrators, trustees and elected officials who have always assumed that by making their timely contributions their obligation was satisfied. Now they will discover that in addition to their jurisdiction’s general bonded and other indebtedness, they owe an additional large amount to the pension plan. This will have serious consequences for the credit ratings of numerous municipalities and other local governmental entities.

Moody’s Proposal

In a parallel development, in July 2012, Moody’s Investor Services, one of the three major Wall Street credit rating agencies, proposed changing its methodology for rating the 8,500 state and local governments with 14,000 pension plans that it tracts. In 2011, Moody’s started to add pension underfunding to each jurisdiction’s general indebtedness. Until then, it had accepted the information and data reported by the pension plans and governments. Now Moody’s proposed using a discount rate derived from Citibank’s Pension Discount Curve. For 2010 and 2011, the discount rate would be 5.5% rather than the typical 8% used and reported by the pension plans. In addition to the lower discount rate, Moody’s proposals include using market valuation of assets and reducing amortization periods to 17 years, Moody’s estimate of the remaining services lives of plan participants.

Moody’s estimates that its revised methodology will increase aggregate pension underfunding for the jurisdictions that it rates from $766 billion to $2.2 trillion. Aggregate ARCs will increase from $36.6 billion to $128.8 billion or from 2.6% of revenue to 9.1%. 6

Chapter 9 Bankruptcy

Congress added Chapter 9 to the U.S. Bankruptcy Code in 1937. 7 It applies to municipalities; however, that term includes any governmental unit below the state level. There is no procedural mechanism for a state to declare bankruptcy, although they can default on their “sovereign” debt.

Chapter 9 has been used about 640 times over the past 75 years, mostly for small governmental entities that have been hit with a major expense or revenue loss. A recent example of such a filing occurred in June 2012 after a real estate developer won a $43 million judgment against Mammoth Lakes, California (population 8,200). Because it has been mainly used for small public entities, there is little case law applicable to large cities.

Chapter 9 differs from its private sector counterparts, Chapters 7 and 11, in a number of ways. 8 First, creditors cannot force a government to file for Chapter 9 protection. That is entirely up to the government. Second, the court cannot require the government to raise taxes or sell assets. Third, the court cannot force a government to dissolve or restructure. Fourth, Chapter 9 requires that the filing be authorized by the state government. Some states prohibit them, whereas others allow them under certain conditions or restrictions. California allows them; however, Assembly Bill 507 enacted in 2011 requires the jurisdiction to engage in a mediation process for 60 to 90 days with a “neutral evaluator” chosen by the local government and its creditors. Finally, a Chapter 9 filing must be the last resort. The jurisdiction must be insolvent and have no feasible alternative to bankruptcy. The court may only approve a plan after negotiations between the municipality and its bondholders and creditors.

The Chapter 9 procedures include five major phases. (a) When the local government files a petition under Chapter 9, it is granted an “automatic stay,” which halts litigation and collection activity by its creditors. (b) The court determines the government’s eligibility for Chapter 9 protection. It must have authorization from the state government to file, be insolvent, have no alternatives to filing for bankruptcy and exhibit a willingness to develop a “plan of adjustment” or “bankruptcy recovery plan.” (c) A plan of adjustment is developed that, if approved, allows the local government to change the terms of outstanding bonds and other debt (including that of its employees and retirees). (d) The plan of adjustment is submitted to its creditors for their approval. It does not need the approval of all creditors but must have agreement from at least one class of creditors. (e) The court approves the plan of adjustment, which then replaces the former terms between the local government and its bondholders and other creditors. If the court finds the filing ineligible, the case is dismissed.

A Perfect Storm

The Great Recession that began in the fourth quarter of 2008 and is apparently nearing its end in the private sector is far from over in the public sector. State and local governments have experienced a drastic reduction in revenue from property taxes as a result of the collapse and 3-year decline of real estate values, especially in California. Income and sales tax revenue also declined because of the high unemployment rates and reduced consumer spending just as recession-related expenses such as public assistance, Medicaid (Medical in California) and other entitlement programs increased.

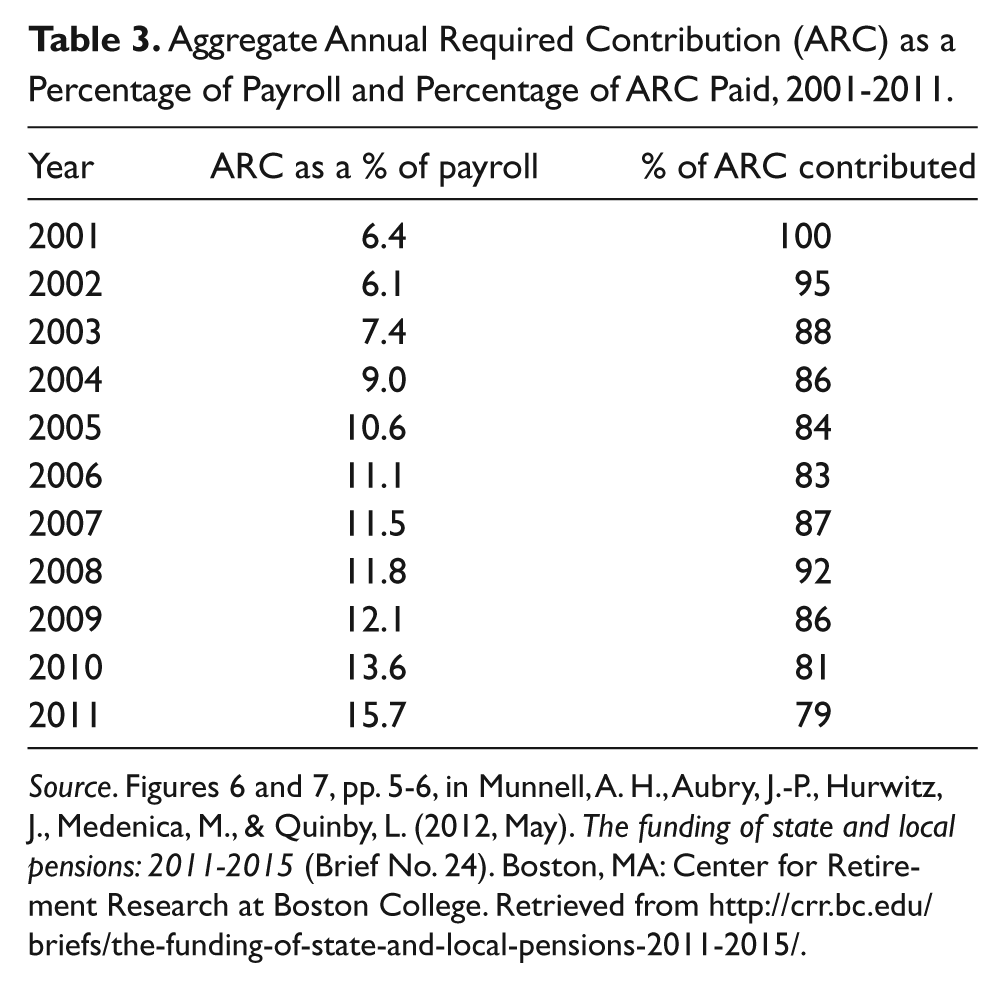

It became increasingly evident that many state and local government pension plans were unsustainable in the long run, in part, because of employer “contribution holidays” and benefit enhancements during the halcyon late 1990s. Matters were made worse by many employers failing to contribute their full ARCs over the years. As indicated in Table 3, as ARCs as a percentage of payroll increased steadily after 2001, the percentage of aggregate ARC actually paid by employers for all plans fell from 100% in 2001 to 79% in 2011. The underfunding problem developed over many years and was accelerated by the Great Recession. Table 4 reports the funded ratio, ARC and percentage of ARC actually paid for the statewide California plans in 2010.

Aggregate Annual Required Contribution (ARC) as a Percentage of Payroll and Percentage of ARC Paid, 2001-2011.

Source. Figures 6 and 7, pp. 5-6, in Munnell, A. H., Aubry, J.-P., Hurwitz, J., Medenica, M., & Quinby, L. (2012, May). The funding of state and local pensions: 2011-2015 (Brief No. 24). Boston, MA: Center for Retirement Research at Boston College. Retrieved from http://crr.bc.edu/briefs/the-funding-of-state-and-local-pensions-2011-2015/.

Funded Ratios, ARC and Percentage of ARC Actually Contributed, California Plans, 2010.

Note. ARC = annual required contribution; UCRP = University of California Retirement Plan; CalSTRS = California State Teachers’ Retirement System; CalPERS = California Public Employees’ Retirement System.

Source. Center for Retirement Research at Boston College. (2011-2012). Public plans database. Retrieved from http://crr.bc.edu/data/public-plans-database/.

Note that CalPERS is at 100% for ARC actually contributed. That is because it has the authority to adjust rates and to require governments to pay in full. CalSTRS, in contrast, had only 63% of ARC paid. Its employer and employee contribution rates are fixed by statute and may only be adjusted by legislation. It appears that the legislature will substantially increase CalSTRS contribution rates in 2013. 9

Recent Chapter 9 Experience in California

For good or for ill, California often leads the nation. It may be about to do so again with three important Chapter 9 filings by relatively large cities: Vallejo, Stockton and San Bernardino. All three contract with CalPERS for pension services.

The City of Vallejo (population 116,000) filed for Chapter 9 protection in May 2008, prior to the state’s adoption of the neutral evaluation process. Its eligibility was confirmed in September 2008 and its plan of adjustment approved in August 2011. The city used the plan of adjustment process to reduce its health care benefits for retirees to $300 per month and to extract concessions from its unions. City officials considered cutting pension costs but decided not to after CalPERS threatened a lengthy and costly legal battle.

The City of Stockton (population 292,000) began its neutral evaluation process in March 2012 and filed for Chapter 9 protection in June 2012. Its eligibility for Chapter 9 protection is being challenged by a major bond insurer, Assured Guaranty, Ltd. Such insurance companies ensure that the sponsor’s contributions to a multiemployer pension plan will be paid. If Stockton fails to make its required contribution to CalPERS, the insurer must make them.

Assured Guaranty contends that Stockton is ineligible for Chapter 9 because it has not negotiated or consulted with all of its creditors, specifically CalPERS. The city assumed it did not have to negotiate with CalPERS because pension benefits are guaranteed by the state constitution and case law. In other words, CalPERS has “primacy” as a creditor.

There are important issues and a lot of money riding on this dispute. It may boil down to whether federal Chapter 9 bankruptcy law trumps state constitutional requirements. It probably does. Both Assured Guaranty and CalPERS have “deep pockets.” If CalPERS and the city of Stockton prevail, the insurer(s) will be out a lot of money and an important precedent will have been set. If not, vested pension benefits for current employees and even retirees may be at risk. Many financially strapped cities and other local governments will see Chapter 9 as an escape from unsustainable pension liabilities.

The city of San Bernardino (population 210,000) filed for Chapter 9 protection in August 2012. It bypassed the neutral evaluation process by declaring a “fiscal emergency” to head off litigation by its creditors. The city stopped making its biweekly $1.2 million employer contributions to CalPERS and as of the end of November 2012 owed $6.9 million. CalPERS has filed objections to San Bernardino’s bankruptcy, claiming that it was a ruse to avoid its creditors and that it had not developed a plan of adjustment. If San Bernardino succeeds in its filing for Chapter 9 eligibility, it may bring CalPERS to the table as a creditor for the first time. At the end of November 2012, CalPERS filed a legal motion with the bankruptcy court to lift the Chapter 9 automatic stay to allow it to sue San Bernardino for its arrears. 10

Analysis and Conclusion

Although their details and approaches differ, the issues in the Stockton and the San Bernardino cases are similar. Are pension funds—specifically CalPERS—“creditors” in Chapter 9 bankruptcy cases that must be consulted and eventually subjected to the government’s plan of adjustment? If they are, CalPERS and, by extension, other cost-sharing pension plans in California and nationwide will be subject to potentially large losses as cash-strapped local governments attempt to escape their pension debt. If they are not creditors, the full cost of the recovery plan will fall on the bondholders, other creditors and insurers.

In the Stockton case, an insurer is contesting the city’s eligibility for Chapter 9 protection because it had not negotiated with CalPERS. In the San Bernardino case, the city unilaterally ceased making contributions to CalPERS because of a fiscal emergency. CalPERS has petitioned the bankruptcy court to lift the automatic stay to allow it to sue San Bernardino in order to force it to resume contributions and pay its arrears. And in December 2012, a powerful group of bondholders and the company that insured the bonds, National Public Finance Guarantee Corp., filed a protest with the bankruptcy court objecting to CalPERS efforts to sue the city. 11

If CalPERS prevails, it will push all of the cost of the recovery plan onto the bondholders, other creditors and insurers, who will almost certainly demand that the pension fund be brought into the Chapter 9 consultations as a condition of cooperating in the plan of adjustment. Remember, it is not necessary that all creditors approve the recovery plan.

CalPERS fallback position is to place San Bernardino’s proportionate share of the pension plan assets in a separate fund or account and continue to pay benefits to the city’s retirees until those funds are depleted. This may conflict with provisions of the California state constitution and statutory law. It also assigns some of the cost and risk of financial restructuring to the city employees and retirees who have a right to those benefits under state law. To the extent that costs are shifted to current employees and retirees, it also violates a widely held assumption that vested pension benefits are inviolate.

On another level, the issue may boil down to whether federal law (Chapter 9) takes precedence over state constitutional and statutory law. It usually does. If so, CalPERS will eventually be drawn into the Chapter 9 recovery plan process of Stockton, San Bernardino and various other local governments that are party to its cost-sharing multiple-employer plans.

This is not a small problem. In California alone, there are 58 counties and 429 cities and a multitude of special districts and other local entities. In addition to CalPERS’ over 1,500 cost-sharing local governments, the 20 “1937 Act” counties provide similar pension services to local entities within their jurisdictions. Beginning 2013 for public pension plans, and 2014 for employers/governments, the new GASB rules take effect. The “perfect storm” of existing large unfunded liabilities; the lower (blended) discount rates, market valuation of assets and curtailed amortization periods; along with the requirement that cost-sharing employers report the proportionate share of the unfunded liabilities, will push a lot of local governments into Chapter 9 bankruptcy. Moody’s proposed changes will further exacerbate things.

Meanwhile, the litigation concerning Stockton and San Bernardino will progress. Whatever the outcomes at the bankruptcy court level, it is highly likely that one or both of the cases will be appealed to the Ninth Circuit and to the U.S. Supreme Court. Although the litigation may take years to unfold, whatever the courts eventually decide, state and local government pension plans will be profoundly affected.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.