Abstract

Sales organizations need to closely scrutinize the role of their sales force and its overall compensation costs. If organizations adapt to the changing internal and external environment, they are likely to be more successful and profitable. The sales force compensation plan should be compatible with the changing nature of the job, depending on stages of economic cycle. The economic life cycle stages are likely to be a key determinant of sales compensation strategies and their effectiveness in achieving organizational goals. Sales organizations must design a compensation strategy based on sales efforts and market dynamics according to economic cycle. Sales organizations must reassess their sales force structure and associated compensation plan across the economic cycle. This article illustrates economic as well as a noneconomic analysis for optimal choice between direct sales reps and independent reps. Various frameworks provided in this article will help managers of sales organizations in effectively managing compensation costs across the economic cycle.

Introduction

Sales force compensation costs represent a major portion of total costs for most sales organizations. To improve profitability, many sales organizations have begun to closely scrutinize the role of their sales force and its overall compensation costs. An important issue for human resources (HR), working with the sales manager, is the design of the pay structure. The core question is the mix of fixed (salary) versus variable (commission/incentives).

If organizations are able to adapt to changing circumstances, they are likely to be more successful and profitable. The organization must adjust its overall systems and practices to fit with the changing external and internal environment. 1 Accordingly, the sales force compensation strategy should in turn be adjusted to support the structure of the sales organization as well as respond to external environmental factors such as customers, territory, competitive response and stages of economic life cycle. Rebalancing the fixed and variable compensation components offers HR/compensation managers the flexibility needed to deal with market variability and external changes, particularly the economic cycle. Economic life cycle stages have been shown to be a key determinant of compensation strategies.

The structure of the sales organization must be well organized if it is to efficiently and effectively sell the products and services that satisfy customer needs. Sales force structure decisions influence how customers see the organization and affect the selling skills and knowledge level required of salespeople, which in turn affect recruitment, training and compensation structure. Each sales organization must structure its sales force to fit the unique needs of the customers, the organization as well as its management. If the sales force structure is adaptive, the sales organization can react quickly to market dynamics without a major structural overhaul and disruption of the selling process. The effective sales force structure adapts to evolving business needs. As sales force structuring is considered an art, there are no empirically developed algorithms to guide sales force structure decisions.

Direct Sales Force Versus Independent Reps

Sales outsourcing refers to shifting a sales organization’s sales activities in part or as a whole to an independent third party in order to limits its risk exposure by using external resources. One of the most important reasons why sales organizations outsource the sales function is turning fixed costs of a sales organization into variable costs. Sales employees who contract their services are called “indirect sales force,” “manufacturers’ representatives”’ or “independent reps,” whereas those who are employed directly by the sales organization are often called “in-house” or “direct” sales force.

Direct sales forces are employees of the company whose products they sell. They can be further classified as inside or outside sales reps. Inside reps almost always operate from within the company premises, performing sales calls and sales support functions. Conversely, outside reps perform their duties outside the company, and their job involves traveling and visiting customers. Independent reps will make up a portfolio of products that are complementary but not competitive.

Sales organizations with complex, heterogeneous and high-margin products with a long sales cycle are more efficient staffed with direct sales reps. In contrast, a large number of geographically distributed and widely dispersed customers, who frequently order small quantities, will be more efficiently served by several independent reps. Since independent reps carry multiple products and are well known in their territory, they are frequently able to penetrate a geographical market more quickly. There is a considerable debate on the use of direct sales force vis-à-vis independent reps based on various micro and macro factors. Hence, this research focuses on this question and studies the impact of economic cycle on choice of sales force structure.

Sales Force Structure Across the Economic Cycle: Key Features

An economic cycle is the upward and downward movements of the levels of gross domestic product (GDP) and refers to the phase of expansions and contractions in the level of economic activities (business fluctuations) around its long-term growth trend.

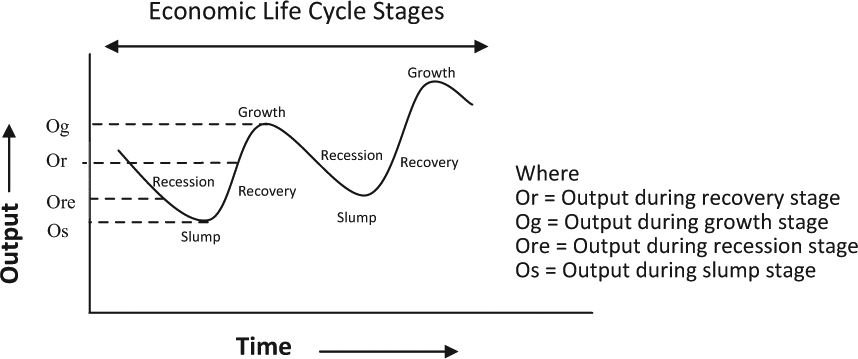

Figure 1 illustrates the four distinct stages of the economic cycle: “Growth” stage as the economy expands, then a turning point when the expansion stops and “Recession” starts with downward movement as GDP begins to decline, then the fall of GDP accelerates during “Slump” and finally another turning point that marks the end of the contraction and a “Recovery” or upturn begins in which the economy once again expands. As shown in Figure 1, GDP output changes across the economic life cycle, and accordingly an organization’s sales will also vary. During a recession as well as a slump stage (or contraction phase), output remains low. Similarly, during recovery as well as growth stages (expansion phase) of life cycle, output is higher. Outputs during recovery and growth stages are considerably higher as compared to recession and slump stages of economic life cycle. The stages of economic cycle are explained below.

Typical stages of economic life cycle.

Recovery Stage

As consumer confidence grows, leading to increased borrowing and spending during recovery stage, firms increase output and build up stock levels. Ultimately, spare capacity is exhausted, new investment occurs and hiring increases. In the recovery stage, the firm seeks to grow the existing market for its products. During recovery, the organization needs a versatile and high performance sales force to face a more competitive environment. Hence, such sales organizations may opt for direct sales personnel if (a) it can attract and hold talented sales force talents, (b) the market is highly concentrated geographically or (c) it has very few customers or sales volume is large enough that sales organizations can afford to employ a large direct sales force. In this scenario, a direct sales force serves sales organizations with great effectiveness.

Growth Stage

In the growth stage, the firm seeks to build brand preference and increase market share. The main strategy of the firm in the growth stage is to penetrate deeper into existing segments and develop new ones, for higher growth rates. The growth stage is characterized by a rapidly growing economy and organizations trying to expand their niche in the market place. The organization has achieved a degree of success if (a) the previous concern for survival has largely been overcome and (b) the organization is actively involved in exploiting opportunities. During the growth stage, the organization focuses on increasing product demand and market share. Large new investment is likely in this period. During this stage, the organization is growing in products, customers, sales volumes, geographic contact and number of sales employees.

When the business is growing at a faster rate, the sales force structure that works is different from what works, during the recovery stage. In the growth stage with high sales volume, the overall cost of direct sales personnel is less than the cost of independent reps; consequently a direct sales force is preferred. As products are established in the growing market and repeat sales become a larger proportion of overall sales, customers will require increased service and support, adding to the sales force’s workload. At this point, companies need to consider shifting to specialist sales personnel.

Recession Stage

In the recession stage, the growth in sales diminishes. The primary objective at this point is to defend market share while maintaining profit levels. Firms mainly focus on efficiently serving and retaining existing customers. When product demand is uncertain, employing a direct sales force is a risk. Hence, deployment of independent reps can help sales organizations better manage the business risk since they fail to perform as expected; their compensation costs in the form of commissions are minimal.

The sales organization in a recession or slump stage is challenged to grow the business, as it faces considerable uncertainty about the future. In this stage of the economic cycle, outsourcing is the preferred option for the sales organization. Independent reps are likely to be more effective than direct sales force as they are skilled and experienced and create synergy for customers as they offer multiple product lines. Independent reps can afford to call on small accounts because they have multiple lines, have established contacts and relationships and are less costly relative to a direct sales force. In this stage, products and services start to lose their advantage, and profit margins erode. Organizations emphasize increasing the efficiency and effectiveness of the sales force.

Slump Stage

During this stage, the organization begins to struggle as markets dry up and product demand decreases. Organizations emphasize cost reduction and efficiency improvement, protect critical customer relationships and exit unprofitable segments. This stage is characterized by a decrease in organization’s resource base. Organizations experience reductions in market share, reduced product demand and even steep financial losses. In this situation, organizations should use independent reps to service the most profitable, loyal and strategically important customers while discarding unprofitable product lines or territories. By using less expensive selling resources, the sales organization can continue selling efficiently to selected customer segments. Hence, to preserve profitability, sales organizations should rely on independent reps or selling partners to cover some market segments. In this stage of the economic cycle, improving the efficiency of the sales process is critical.

Business Risk and Operating Leverage Across the Economic Cycle

Choosing the proper balance of direct sales reps versus independent reps depends on customer and/or product characteristics as well as stages of economic life cycle. Certain stages of economic cycle are suited to a direct sales force, while others to independent reps or indirect channel partners. The more influence a salesperson has on the sale, the more important is a direct sales force for the sales organization.

The recession and slump stages of the economic cycle are characterized by low growth and low profit potential while the recovery and growth stages are characterized by high growth and higher profit potential. In the recession stage, there is lot of uncertainty and business risk.

Business risk is a central determinant of an organization’s present value as it affects risk-adjusted future profits. It is affected by various parameters such as price, variable costs, operating costs and the stability of demand. 2 Business risk has a negative impact on the operation or profitability of a given organization. A business risk can be the result of internal conditions as well as some external factors. Internal conditions such as higher operating fixed costs affect an organization’s value by increasing the variability of returns. Among the external factors that can create business risk, one of the most predominant risks is that of a change in demand for the firm’s goods and services. 3

As business risk is high during the recession and slump stages, sales organizations should keep low operating leverage (Figure 2). The degree of operating leverage is a function of the organization’s cost structure in terms of the relationship between fixed costs and total costs. An organization that has high operating leverage (high fixed costs relative to total costs) will also have higher variability in earnings before interest and taxes than a similar organization with low operating leverage. The higher the operating leverage (fixed costs/total costs), the more profits will vary with changing sales revenues.

Relationship of business risk and operating leverage across economic cycle.

In the growth stage, the organization’s operating income increases at an increased rate while uncertainty and business risk moderate. Similarly, during the recovery stage, uncertainty is low and business risk is also low. In the recession and slump stages, uncertainty and business risk are high again. As a result, during periods of low business risk, high operating leverage is preferred, while during periods of high business risk, low operating leverage is preferred. Accordingly, independent reps are preferred in the recession and slump stages while direct sales forces are preferred in recovery and growth stages of the economic life cycle. Deployment of independent reps will decrease operating leverage for a sales organization, as independent reps work on a commission-only basis. Since a direct sales force represents fixed costs, its deployment will increase operating leverage. By reducing the business risk, the cost of capital is also reduced, thus increasing the economic value of the firm. 4 Hence, the independent reps are most preferred choice for the sales organization when the business environment is uncertain.

Redesigning Sales Force Structure According to Job Challenges

The sales force compensation plan should be compatible with the changing nature of the job. As the role of the sales force changes considerably during various stages of economic cycle, so must the structure of the sales force. Understanding the impact of the economic cycle provides insight into the changing role of the sales force as the characteristics and requirements of the selling efforts shift during different stages of economic cycle. When an economy shifts to an expansion phase following a recession or slump, it will open up new markets for organizations requiring the sales force to sell differently.

During the recovery stage, the sales organization is looking to expand the existing customer base and markets, while during the growth stage, they focus efforts on penetrating the market and persuade customers to buy the organization’s products and services. Hence, during an expansion, sales revenue and volume expand and profitability improves. During this period, the sales force needs to represent multiple products, markets, territories and selling activities. At the same time, sales efforts are targeted to extend the products offered and involve new customers, market or territory acquisition or expansion and increasing market share.

Assured monetary rewards for conducting the difficult selling task of acquiring new customers and expanding to new territories are necessary to attract and retain effective sales talent. Hence, in this stage, sales organizations rely more on direct sales force. At this point, organizations need to motivate sales personnel with increased fixed pay. In such a case, as the role of sales force is more differentiated from each other, the sales force would be motivated by relatively higher proportion of fixed pay in compensation structure.

A higher level of job challenge is negatively associated with the ratio of variable to fixed pay. Hence, for more challenging jobs where sales performance becomes difficult to observe, organizations rely proportionately less on variable pay and more on fixed pay. Moving to a compensation structure that is higher in salary and lower in variable pay will help organizations in motivating their sales force. Thus, during in the recovery and growth stage, direct sales force with higher proportion of fixed pay is advocated (Figure 3).

Relationship of job challenges and sales force structure across economic cycle.

During recession or slump stage of economic cycle, sales revenue and volume remain stagnant or turn down and profitability also declines. Consequently, the organization focuses on survival and reducing sales costs. During the recession stage, it is important for sales force to defend the brand as it is not the time to add new products. During slump stage, they emphasize maintaining or growing existing business accounts. During both stages, the sales force is focused on maintaining existing market share by servicing established accounts. Hence, to minimize increased risk during a business contraction, firms should reduce fixed pay and maximize the use of variable pay, which is a cost only when a sales rep achieves certain results.

With variable, rather than fixed compensation, maintaining financial stability should be a less risky proposition. This is especially important during a contraction phase. In such a case, sales organizations rely more on independent reps as their compensation includes mainly variable pay. Hence, there is need to alter the sales force compensation plan according to changing role of sales force. Rebalancing of fixed and variable pay can provide an opportunity for HR managers to link compensation costs to different stages of the economic cycle.

Types of Sales Force Structure: Generalist Versus Specialist Sales Roles

Planning the effective sales force structure involves finding the right balance between generalized and specialized sales roles. Generalists are typically deployed in sales organizations that are managing hard-to-cut cost during recession stage of economic life cycle or trying to survive in the slump phase of economic life cycle.

During the recession stage, independent reps are the best choice. However, for large accounts that buy on contract, independent reps are usually less effective than direct sale force. 5 Hence, sales organizations may employ a small contingent of in-house direct sales force to service very large or key sales accounts, while permitting smaller accounts to be serviced by independent reps. Most sales forces during a recession comprise a relatively small number of direct sales force who sell a narrow product line to a limited number of target market segments along with larger proportion of independent reps (Figure 4).

Sales force structure and sales roles across economic life cycle.

Similarly, during the slump stage of the economic cycle, products are more efficiently handled by independent reps or channel partners since their costs are lower and less fixed. During recovery and growth stages of economic cycle, a direct sales force is preferred. In the growth stage, sales personnel have to call on prospects in a broader set of markets as their product portfolio expands because of the upbeat economy. This presents sales organizations with two challenges related to managing the sales force: specialization as well as size.

In a generalist sales organization, each representative or account manager sells an organization’s entire, but usually limited, product line to customers who typically are all in the same industry, thus providing a single point of business contact to customers. With a generalist sales force, salespeople would be expected to engage in all types of sales activities for all of the products and to sell to all of the customers. In a specialist sales force structure, salespeople would be expected to engage in a limited set of selling activities for only a portion of the organization’s products and would be selling only to a certain group of customers.

Sales forces specialize in different ways such as by product, customer, geography or function within the sales process and industry-vertical. Specialization by industry is recommended when a sales force with a deep industry knowledge represents a competitive advantage over a generalist sales force structure. Product specialization is most effective when vast knowledge is required to sell the product in the market. Product specialists are technical experts who know the products inside out.

When the sales force is customer specialized, it is more market driven and able to focus on select customer groups. Specialization by geography is the least complicated specialization and focuses on geographic territories. Sales force specialization by function is illustrated by the difference between the “Hunter” and “Farmer” roles of the sales force. Hunters typically focus on new sales, while farmers cultivate current customer relationships. Depending on stages of the economic cycle, a sales force structure may contain a mixture of generalist and specialist roles.

Direct Sales Force Versus Independent Reps: An Economic Analysis

Organizations must use their resources and capabilities to cope with and exploit their environment in order to attain competitive advantage. One method for moving toward a competitive advantage is to create strategies that anticipate and respond to environmental changes. Use of variable pay to protect a firm against declining profits is also one of the way firms can attain competitive advantage.

The direct sales force is difficult to set up, slow to get up to speed and treated predominantly as a fixed cost that includes salespeople, sales managers and information systems. Overhead costs of the direct sales force includes base salaries, 401(k)s, stock options, taxes and other fringe benefits, training costs, travel and other selling expenses and sales management overhead.

On the other hand, since independent reps are paid commission on realized sales, they represent variable costs. Outsourcing the sales function converts the largely fixed costs of a sales organization into mostly variable costs. Commissions paid to independent reps are a fraction of sales. Thus, if the product doesn’t sell, costs are minimal.

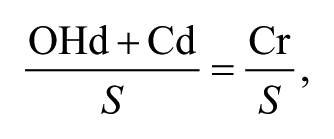

The decision to engage direct sales force or independent reps is generally influenced by the cost of serving the same level of sales. Sales organizations use independent reps until their sales are large enough for them to afford a direct sales force. The convergence of direct sales force cost and commissions paid to independent reps plays an important role in the initial decision of a sales organization as it determines the path of least total costs. Such convergence is viewed in the terms of selling cost and sales revenue and is stated by following formula:

where

OHd = Overhead cost of the direct sales force

Cd = Variable pay (Commission) of direct sales force

Cr = Commission of independent reps

S = Sales revenue

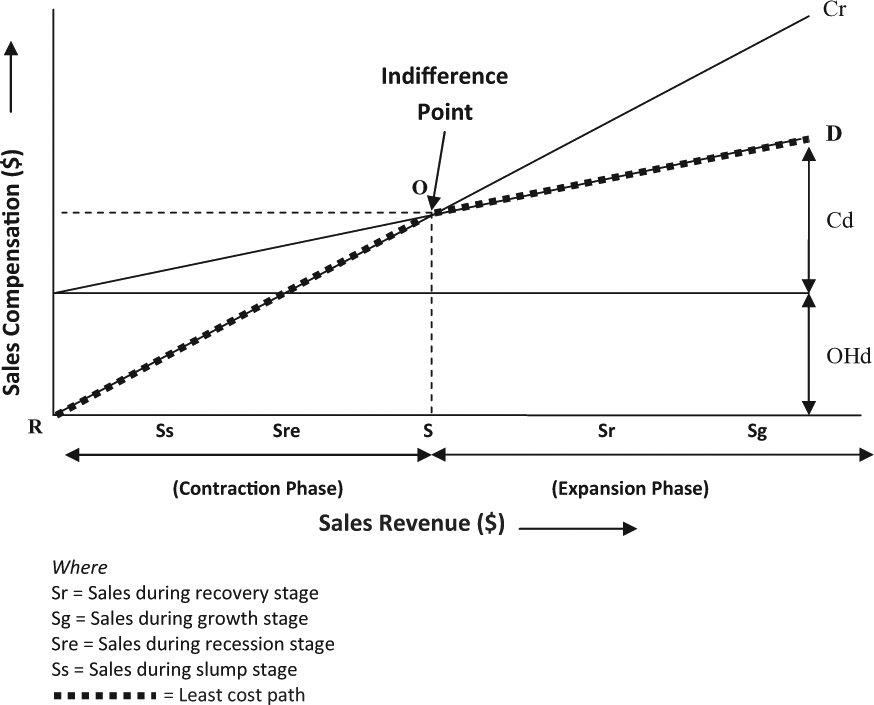

When this relationship is diagrammed as shown in Figure 5, it can be seen that the cost of independent reps (Cr) rises in direct proportion to increases in sales (S) as sales costs of independent reps are primarily in the form of commissions (Cr). Figure 5 represents the convergence of direct sales force costs and the commissions of independent reps for mixed pay plan (variable pay along with base salary) of direct sales force. For a mixed pay plan, the cost of direct sales force includes sales overhead, such as base salaries and overhead costs of sales support (OHd) as well as commission (Cd) paid to the direct sales force. The two cost lines would converge at point “O,” where the cost of the two sales force strategies would be equal (OHd + Cd = Cr). The point “O” is also called as indifference point or break point and shows equilibrium of the sales commission (variable pay) paid to the independent reps versus selling costs associated with a direct sales force.

Sales force structure and compensation cost across economic life cycle.

Therefore, based on a purely economic analysis, during a period of low sales such as in either a recession or a slump stage (contraction phases), a sales organization would use independent reps to gain sales at a lower cost as denoted by line RO and would continue using independent reps as long as their commission costs (Cr) remained lower than the costs associated with a direct sales force (OHd + Cd). As shown in Figure 5, the least cost paths are RO and OD whereas the cost of direct sales force is OHd + Cd.

Once the sales organization’s sales volume is high enough, as in recovery and growth stages (expansion phases), so that the commissions or variable pays paid to the independent reps (Cr) for that volume are greater than the total fixed cost and variable costs (OHd + Cd) that the sales organization estimates for a direct sales force, the sales organization should switch to a direct sales force to save money.

Hence, if sales exceeded point “O,” then the sales organization would convert sales force structure to a direct sales force to maintain the lower economic costs as denoted by line OD. After reaching the indifference point “O,” the sales organization will switch over to a direct sales as cost line OD represents the least cost path. Thus, when sales revenue is high (as in recovery and growth stages of economic life cycle) and above the indifference point, a direct sales force is deployed, and when sales revenue is low and below the indifference point, independent reps are used.

Sales organizations should be large enough and with enough volume to justify deploying a direct sales force adequate to provide intensive coverage of all geographic markets. Otherwise, they may be spread too thinly for optimum territory coverage. Hence, when sales organizations in a recession or slump stage cannot afford the fixed costs of a larger direct sales force, independent reps are a better choice as they are paid for results only, which enhances cash flow and profitability. This single evaluation, however, reflects only the economic aspect of the sales force structure decision.

Organizations should not choose direct sales force or independent reps in sales force structure based on these criteria only. Other important noneconomic factors in selecting a sales force structure are their relative performance in sales coverage/sales generation and the costs/revenue effects during the process of switching from independent reps to direct sales force and vice versa.

Direct Sales Force Versus Independent Reps Across the Economic Cycle: An Optimal Scenario

As calculated in the following illustration, relying on independent reps instead of direct salespeople results in an increase in variable costs, a decrease in fixed costs, along with a decrease in operating leverage and breakeven point (BEP).

The BEP is no loss–no profit situation. Independent reps (who work on commission or variable compensation) also help reduce the BEP, making it possible to be profitable faster. Hence, the breakeven quantity and operating leverage will be lower for the sales organization that has used independent reps instead of direct sales force, as calculated in following example. If the cost of coordination with independent reps is not considered in the calculations, then fixed costs will be zero and subsequently BEP will also be zero (Table 1).

Sales Force Structure and Financial Performance: Various Scenarios.

Source. Calculated by author.

Illustration

To illustrate, the impact of sales force structure on operating leverage and BEP assumes that a sales organization considers both options of employing direct sales force and independent reps as shown in Table 1. The sales organization in the “Direct Sales Force” option employs internal sales employees on mixed pay plan (fixed pay: $22,000 and commission: 2%) while in the other option with “Independent Reps,” the sales organization deploys independent reps on commission-only basis (at 12.24% commission on sales). The indifference point or break point occurs at sales volume of 70,000 units. At this point, the cost of the direct sales force and the cost of independent reps are equal (cost to sales ratio will be same for both the options; Scenario 1, Table 1). Below the indifference point, the cost of a direct sales force will be higher than the cost of independent reps (Scenario 2, Table 1). Above the indifference point the cost of independent reps will be higher than cost of the direct sales force (Scenario 3, Table 1). The area below the indifference point shows the contraction phase of an economic cycle while the area above the indifference point shows an expansion phase. As independent reps are self-employed, there are no overhead costs attributable to the sales organization. Hence, in comparison to direct sales force, the “Independent Reps” option of sales organization has a lower degree of operating leverage and lower market risk and its profits vary less with changes in sales volume.

A critical requirement of such an economic analysis is a complete and precise estimation of the total fixed costs associated with the direct sales force as well as accurate forecasting of sales revenue. In the earlier illustration, certain assumptions were made. It was assumed that a direct sales force can achieve an increase in sales volume with no increase in the number of salespeople. Such analysis is a cost-based steady-state analysis. It means that sales organization had either considerable slack resource at the beginning or a large improvement in the sales organization’s selling efficiency over a time.

It is also assumed that fixed costs associated with independent reps are zero. However, independent reps are not without fixed costs as some minimum amount of fixed costs are still incurred. In reality, the cost curve will not vary directly with sales volume as considered in the illustration. Essentially, fixed costs of sales will increase with increase in sales as fixed costs are not fixed at a given level in perpetuity. In fact, fixed costs are only semifixed as they are static only within a range of relevant factors, such as sales volume or the number of customers. As the relevant factors increase or decrease, the associated fixed costs become unfixed as investments must be increased or reduced, with costs fixed again at the new higher or lower level.

Overhaul of Existing Sales Force Structure: Some Considerations

As sales increase, the decision to modify the sales force structure shift should be based on many factors along with the cost economics. If the switch is from independent reps to direct sales personnel, the sales organization will lose the benefit of long-term continuity with customers and may result in customers shifting their allegiance to competitors. Compared to independent reps, a direct sales force provides less territory coverage, thereby affecting sales range and reach. A decision to shift from independent reps to direct sales force made purely on economics analysis can backfire. The qualitative factors such as special relationships of the sales force with customers, trade-offs between control and flexibility, the impact of short-term sales loss resulting from such a switch and so on should also be considered.

Unless there are compelling reasons for a sales organization to change from independent reps to sales force and vice versa, it is better to maintain the sales force structure. After a thorough review of all economic and noneconomic factors, if a sales organization decides to switch from independent reps to direct sales, it should be done all at once, and such transition should be completed as quickly as possible as is risky and time-consuming. Converting to a direct sales force from independent reps is a slow, expensive process that incurs high initial costs; it requires a considerable commitment of overhead and takes time to generate returns. Therefore, organizations that demand quick returns on investment may hesitate to convert to direct sales force from independent reps.

Discussion and Research Implications

To succeed in the long term, sales organizations must reevaluate their sales force structure to reflect the economic cycle. Sales force structure decisions are important for a sales organization as consequences of such decision errors are likely to affect a sales organization not just in current year but also for many years to come. Sales force structure is related to compensation management, distribution channels and territory management. No matter how well the sales organization hires and trains their sales force, inefficient sales force structure will prevent sales forces from reaching full productivity and optimal profitability.

It is hard for sales organizations to isolate the effect of the sales force from other effects in the marketplace that might cause sales to go up or down. These effects include pricing, advertising, sales promotions, along with changes in distribution, market needs and the actions of competitors. Despite the many variables, a sales force is a strategic lever for improving sales growth, market share and profitability. A sales force represents an expensive but important human asset when it sustains full productivity in the market place. In times of recession and/or cost cutting, the use of independent reps typically increases. After the economic downturn of 2001, Intel, Texas Instruments, Cirrus Logic and Hunt Wesson modified their sales force structure and switched from direct sales force to independent reps for some or all of their major product lines. 6

The decision whether to serve a sales territory with independent reps or a direct sales forces should be evolutionary in nature as an organization and its markets change, the appropriate configuration of the sales force should also change. There are many strategic issues in the selection of sales force structure: fixed versus variable cost to sales ratio, type of sales territories (dominant vs. marginal), availability of trained and experienced sales force, product characteristics and order size, short term versus long term selling approach, channel relationship and stability of relationships. 7

Conclusion

Sales force structure refers to the differing roles that an internal sales force (direct sales force) and external selling partners (independent reps) should play. The sales force structure is critical because it determines how quickly salespeople respond to market opportunities, influences their performance and affects revenues, compensation costs and profitability. A sales organization that does not adopt an evolving sales force strategy as it passes through the different stages of the economic life cycle is placing itself at considerable risk.

The economic cycle provides an opportunity to design a compensation strategy based on sales efforts and market dynamics. Although sales organizations devote considerable time and money to manage their sales forces, few give much thought to how the sales force structure needs to change over the economic life cycle. This article focuses on the key economic and noneconomic factors to guide the choice of direct sales force and independent reps across the economic life cycle.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.