Abstract

Many sales organizations today are focusing on their culture as a strategic tool, deciding what it should be, aligning with strategic goals, business strategy and sales compensation design. The culture of sales organization is comprised of fundamental principles and beliefs that are shared by its members and hence determines the norms that dictate how sales employees should think and behave. In addition to this, compensation systems promote behaviour of sales employees that ultimately becomes dominant behaviour in the sales organization. An effective sales performance supported by an appropriate compensation strategy and culture of sales organization plays a significant role in determining financial performance, enhancing valuation of the sales organizations and increasing competitive advantage in the market place. This research provides various frameworks and models for establishing relationship between organization culture and compensation structure and deriving its impact on sales performance. Study also provides numerous illustrations to calculate optimal compensation structure and corresponding organization culture to achieve maximum valuation of sales organization.

Introduction

The culture of a sales organization is composed of fundamental principles and beliefs that are shared by the members of the sales organization. It is an effective mechanism for controlling and managing sales employee behaviors when compared with organizational rules and regulations. The culture of a sales organization affects perceptions as well as behaviors of sales employees and contributes to the success or failure of the organization. Hence, culture determines the norms in sales organizations and dictates how sales employees should think and behave. The culture of sales organizations has become an important factor in explaining all aspects of organizational behavior as it influences how salespeople perceive and interpret a given situation, and consequently how they behave. Likewise, sales compensation systems also influence the behavior of sales employees and are intended to align their individual actions with organizational goals. Compensation systems influence the behavior of salespeople that ultimately becomes dominant behavior in the sales organization. Such behavior influences employees’ perceptions and beliefs about the value systems of the organization.

Sales Organization: An Unique Instance of Market Culture

The four dominant types of organizational cultures are (a) hierarchy, (b) clan, (c) adhocracy and (d) market. 1 Each of the four types of cultures has a different focus and orientation, as shown in Table 1.

Organization Culture and Its Attributes.

Source. Tabulated by the author.

Market culture is characterized by external focus (instead of internal focus) and control (instead of flexibility; Table 1). A sales organization is an unique case of market culture as it has external focus and control orientation. As market culture is externally oriented, it plays an important role in adapting organizations to their external environment. One of the important elements of market culture is the method of control of the salespeople’s behavior. A suitable and efficient way of control will depend significantly on the shared assumptions and values of sales employees in the sales organization. This is the reason why different methods of sales force control will be applied in different market cultures adopted by sales organizations. Sales force control systems allow sales organizations to align salespersons’ behaviors and objectives with organizational goals.

Market culture has high degree of formal control. Formal controls are written, management-initiated mechanisms that influence the probability that sales employees will behave in ways that support the stated marketing objectives of sales organizations. Two basic forms of formal control in sales organization are behavior control and outcome control. In behavior control, specific steps, procedures and processes are articulated that result in desired outcomes for realizing the goals, whereas in outcome control, desired performance outcomes or outputs of sales employees are articulated. 2

Behavioral control is exercised when the sales organization attempts to influence the means of achieving desired ends, and hence it is associated with high levels of sales manager monitoring, directing, evaluating and rewarding of sales activities and performance evaluation centered on the salesperson’s job inputs. 3 It involves considerable supervision and feedback of salespeople’s activities. Hence, in behavioral control, sales organizations prescribe what salespeople should do, describe that they should accomplish the quality of sales activities, and accordingly salespeople are evaluated and compensated based on their behavior and/or activities rather than the end results. Here, a sales manager holds sales employees responsible for following the prescribed process but does not hold them responsible for the outcome (e.g., a sales manager notifies a sales employee to follow certain procedures for new market development, but does not hold the sales employee responsible for the extent of new business generated).

In contrast, under an outcome-based control system, sales employees are responsible for their performance but free to decide the methods of achievement. Outcome control is exercised when performance standards are set, monitored and the results evaluated. In outcome control, sales managers give less monitoring and direction to salespeople, who are left alone to achieve results in their own way using their own strategies, and objective measures of results, such as sales volume, sales income and retained profits, rather than measures of salesperson behaviors, are used to evaluated and compensate salespersons. Outcome-based control typically relies on higher levels of salesperson financial performance and more limited sales manager control activities. 4 In outcome-based control, the sales manager does not need to know the causal mechanism for sales performance because responsibility for cause–effect knowledge has been delegated to the sales employee. For example, in outcome-based control, a sales manager notifies a sales employee to improve his or her sales output without specifying the process.

Sales Organization Culture: Process-Oriented Culture Versus Outcome-Oriented Culture

Sales organization culture is defined both in terms of its causes and effects such as process-oriented culture and outcome-oriented culture, respectively. Key features of process-oriented culture and outcome-oriented culture are given below.

Process-Oriented Culture

Sales organizations with process-oriented culture evaluate and reward what salespeople bring to the job in terms of their behavior. Sales organizations measure what salespeople actually do—their efforts, activities, hours, expenses and the like. In the process-oriented culture of sales organization, focus is on behavior control. It is achieved by the sales manager who has the authority over a certain number of sales employees. In the process-oriented culture, behavior-based control systems allow sales managers a great deal of control over the selling operation in terms of how salespersons should achieve results. 5 As such, a sales manager is supreme in this culture. In behavior control, the object of control is individual behavior of sales employees, that is, their actions and decisions, and the goal is to harmonize these actions and decisions with organizational goals. The sales manager supervises the progress of the sales-related work process, decisions and actions of the sales employees, through immediate contact and communication with them.

The sales manager gives instructions to the sales employees regarding how, when and what should be done and also solve the problems that emerge during the work process. Hence, it encourages centralization of decision making in sales organizations, since decisions about the manner of work are reached by the sales manager, and the sales employees only execute them. This method of control leaves little room for the sales employees to have the freedom of choice regarding the manner in which they will perform their work tasks. This culture implies a very low degree of autonomy or discretion of sales employees, and this is why it is a very restrictive mechanism of behavior control.

Such sales organizations also rely on a plethora of performance criteria, many of them subjective or difficult to observe. The major part of compensation in a process-oriented culture is fixed (capped salaries). In a process-oriented culture, much of the motivation of salespeople rests more on intrinsic rewards such as feelings of achievement, personal growth and the satisfaction of offering good service and less on extrinsic motivation.

A process-oriented culture is best under the following circumstances:

Salesperson lacks experience and requires direction and monitoring

Organizations need to strengthen brand/product or services

High nonsales priority for salespeople such as formulation of marketing strategy

Focus on new product/territory development, which contributes indirectly to current sales and directly to future sales

Difficult to design equity rule or variable pay formula for efforts of salespeople

Disadvantages of a Process-Oriented Culture

As behavior control is adopted by a sales organization in a process-oriented culture, it conforms to people’s natural instincts to create hierarchies, and hence creates far more overhead costs. Also, sales employees of a process-oriented culture tend to avoid uncertainty because of more emphasis on fixed pay in the compensation structure. 6

Outcome-Oriented Culture

Under an outcome-oriented culture, there is a very limited extent of sales managers’ monitoring, directing, evaluating and rewarding activities as sales managers often have minimal contact with their salespeople. As such a salesperson is supreme in this culture. Sales organizations with an outcome-oriented culture measure result or outcomes of sales and reward results. These results can take many forms: sales, margins, contributions to profit, share of customer wallet, market share, sales of new products, repeat business, on-time collection of receivables and so forth. An outcome-oriented culture does not allow the sales organization to reward specific selling efforts of strategic importance. It is difficult for the sales organization to direct selling efforts toward other strategic goals, such as selling to selected customer groups, pursuing relationship-building activities that do not result in an immediate sale or focusing on customer orientation as an organized strategy.

In the current business environment, the primary focus of sales efforts is to accurately determine and satisfy customer needs in order to create long-term orientation of salespeople toward their customers, or customer orientation. A high level of customer orientation reflects a high level of concern for the customer’s long-term needs, while a low level of customer orientation reflects a selfish concern for the achievement of short-term sales objectives. 7

Salespeople in an outcome-oriented culture enjoy considerable autonomy. The sales organization sees them as entrepreneurs who craft and execute personal strategies to find customers and fulfill sales targets. Sales employees of an outcome-oriented culture accept uncertainty and view it as a challenge. Salespeople place more importance on achieving sales targets than on pleasing their organization with behavior expectations.

An outcome-oriented culture is best under the following circumstances:

Customers need extensive information from salespeople

Over a period of time, customers have forged strong ties with salespeople

Salespeople’s skills and knowledge determine whether firm closes sales, as advertising or pricing budget not having much impact on sales

There are many ways to close a deal, so a sales organization does not want to impose a sales manager’s preferences on salespeople

Disadvantages of an Outcome-Oriented Culture

An outcome-oriented culture of a sales organization causes short-term orientation of salespeople that leads to unethical behavior. More reliance on incentives or variable pay creates a situation of “moral hazard.” Moral hazard as defined by agency theory is the tendency of a salesperson who is imperfectly monitored to engage in dishonest or otherwise undesirable behavior. Unethical relationships with customers cause the potential risk to the sales organization as it destroys the value of customers and reduces overall profitability. Sales organizations need to foster a salesperson’s ethical behavior not only because of the positive consequences to the salesperson in terms of higher job satisfaction but also because unethical sales behavior can cause disputes with customers, reduces customer trust, affects their long-term relationship with customers as well as overall value of the organization. With initial unethical sales practices by salespeople, frequency of buying, retention rate as well as average tenure of a customer will also decrease, thereby substantially reducing the profit margin and long-term viability of the sales organization. 8

Sales Performance: Impact of Customer Orientation and Sales Organization Culture

Sales organizations may differ in how they prioritize and what they define as important components of sales performance. To understand sales performance, it is important to explore how such a culture (process oriented vs. outcome oriented) influences the performance of the individual salesperson. Salesperson performance has two dimensions, comprising behavior performance (influenced by a process-oriented culture) and outcome performance (influenced by an outcome-oriented culture). Behavior performance consists of the behaviors employed by salespeople in meeting their job responsibilities (e.g., sales support). Outcome performance relates to the sales results and sales activities directly attributed to the salesperson (e.g., technical knowledge and sales presentation). 4

Effective sales performance requires sufficient sales activity by sales employees in terms of quantity as well as quality, and also requires proper allocation of such activity to customers, products and selling tasks. Sales activities performed by sales employees are greatly influenced by types of sales organization culture. The culture and compensation system design of a sales organization function as complementary elements in directing salespeople toward achieving the strategic goals of the sales organization. 9 Salespeople operating under a process-oriented culture are compensated by a relatively high portion of fixed pay (salary) compared to variable pay. In contrast, under an outcome-oriented culture, the salesperson’s variable pay (commission) accounts for the primary form of total compensation. 10 With the right quantity, quality and allocation of sales activity, and supported by an appropriate sales organization culture, that is, process-oriented or outcome-oriented culture, a sales force can produce the desired results.

In a process-oriented culture of sales organization, the main focus of control will be on behavior of sales employees, and hence it leads primarily to sales activity quality. A behavior-based sales control system adopted by a process-oriented culture should foster customer orientation because salespeople will be allowed to develop specific skills without being forced to sacrifice long-term objectives for immediate results. Salespeople’s customer orientation should increase when they receive behavioral feedback (which is typically higher in a process-oriented culture). The degree of customer orientation is also influenced by the quality of sales activity. Hence, a process-oriented culture facilitates “customer orientation” as it aims at identifying the customer’s interests, goals and other product-related needs.

By identifying and satisfying customer needs, customer-oriented salespeople create customer value. Thus, customers are likely to respond to increases in customer value through customer orientation by purchasing more. A salesperson’s customer orientation drives sales volume through increases in cross-buying, 11 customer retention 12 and immediate purchases. 13

However, adopting a process-oriented culture by a sales organization and subsequently customer-oriented behaviors also requires inputs in terms of substantial salespeople resources such as their efforts and time that may negatively affect revenues and profits (costs of customer orientation) and thus affect the financial performance of the sales organization. Salespeople wanting to increase their customer orientation need to reallocate how they spend their time. They are required to spend more time per customer, which reduces the total number of customers they can serve at all. These time requirements may affect a salesperson’s sales performance because they are associated with important opportunity costs.

The problem may be aggravated further if there is a flawed process for attracting and acquiring customers as it leads to selection of wrong customers. The organization that serves and retains such difficult-to-serve, chronically unhappy customers is making expensive mistakes as it drains its resources in the long term. Such customers cannot be profitably served and utilize a disproportionate amount of time of salespeople and also other resources of the sales organization. As such salespeople will have less time for acquiring potential customers.

Thus, increasing customer orientation means also increasing customer acquisition costs and shifting resources from customer acquisition to customer retention, which does not necessarily improve sales performance immediately. 14 This may also result in fewer sales opportunities and, thus, reduced salesperson performance. Thus, the salesperson’s customer orientation is a resource-intensive endeavor. 15 In particular, customer orientation costs arise from salesperson time and hence it also represents additional costs for the sales organization. The costs of implementing a customer-oriented selling may be higher than what salespeople realize. 16 The law of diminishing returns applies to the benefits of increasing customer orientation with regard to sales performance, whereas costs increase steadily. Hence, a high degree of process-oriented culture (with higher customer orientation) does not always imply higher sales performance.

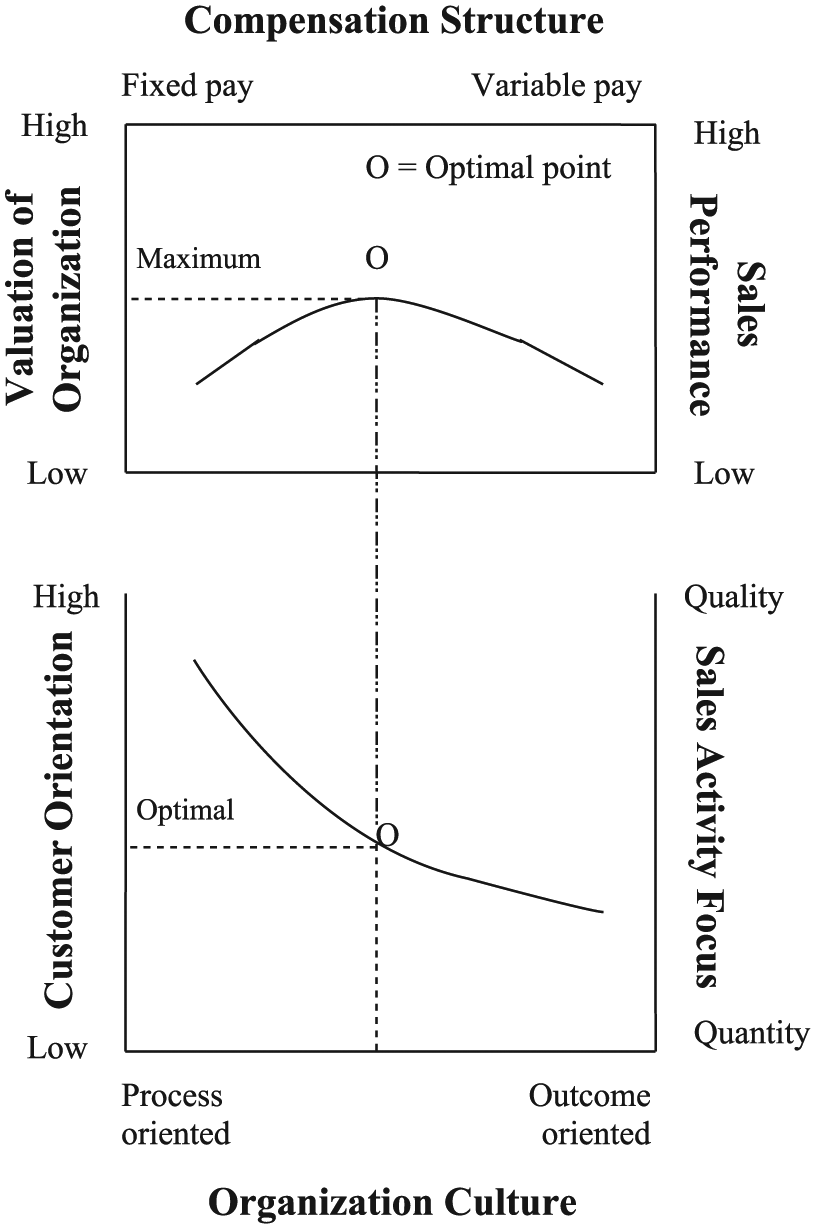

In a highly competitive environment, many sales organizations are searching for ways to reduce sales costs while maintaining performance. Hence, in a process-oriented culture reducing the behavior orientation of salespeople who are “too customer oriented” (focusing more on sales activity quality at the expense of activity quantity) promises to be a viable strategy. This leads to a situation where the focus of sales activity is more on quantity than quality (i.e., outcome-oriented culture). An outcome-oriented culture of sales organization leads to an incentive-driven compensation structure and focus on sales performance as it neglects the long-term customer relationship to a successful sale. Incentives affect outcome or results by influencing salespeople’s motivation and hence it leads primarily to sales activity quantity. Incentives can focus salespeople’s attention away from the content of their work to the consequences of it. However, incentives can have undesired consequences particularly when it comes to customer orientation or ethical behavior by salespeople as it encourages activity quantity at the expense of quality of sales activity. Hence, a high degree of outcome-oriented culture does not normally imply higher customer orientation as well as long-term sales performance (Figure 1).

Sales performance: Impact of customer orientation and organization culture.

To summarize, a high degree of customer orientation in a process-oriented culture results both in gain (benefits) and loss (costs). As customer-oriented behaviors trigger customer reactions, it positively affects revenues and profits through increased sales volumes and higher prices (benefits of customer orientation). However, customer-oriented behaviors also require inputs in terms of salesperson resources and firm resources that may negatively affect revenues and profits and, thus, salesperson financial performance (costs of customer orientation). As shown in Figure 1, there is an optimum level (Point “O”) with regard to customer-oriented behaviors in sales encounters.

Intuitively, the relationship between salesperson customer orientation and sales performance was thought to be positively linear. However, empirical research found a curvilinear, inverted-U relationship between salesperson customer orientation and sales performance, providing evidence that an optimum level of customer orientation behaviors exist. Research also found that approximately 30% of salespeople exhibit customer orientation levels that are higher than the optimum. Hence, customer-oriented behaviors are particularly effective in creating value if they help customers satisfy their core needs. Beyond that, increases in customer orientation add less value for the customer. 17

As shown in Figure 1, a process-oriented culture has a high degree of customer orientation with focus on sales activity quality. However, an outcome-oriented culture has a low degree of customer orientation with focus on sales activity quantity. Both process-oriented and outcome-oriented cultures when adopted fully result in low sales performance and accordingly lower valuation of the sales organization. Hence, the solution lies somewhere in middle of process-oriented and outcome-oriented cultures (i.e., mix of process-oriented and outcome-oriented cultures) where sales performance as well as valuation of sales organization is highest (optimal point “O” in Figure 1).

Firm Valuation: Impact of Organization Culture and Customer Orientation

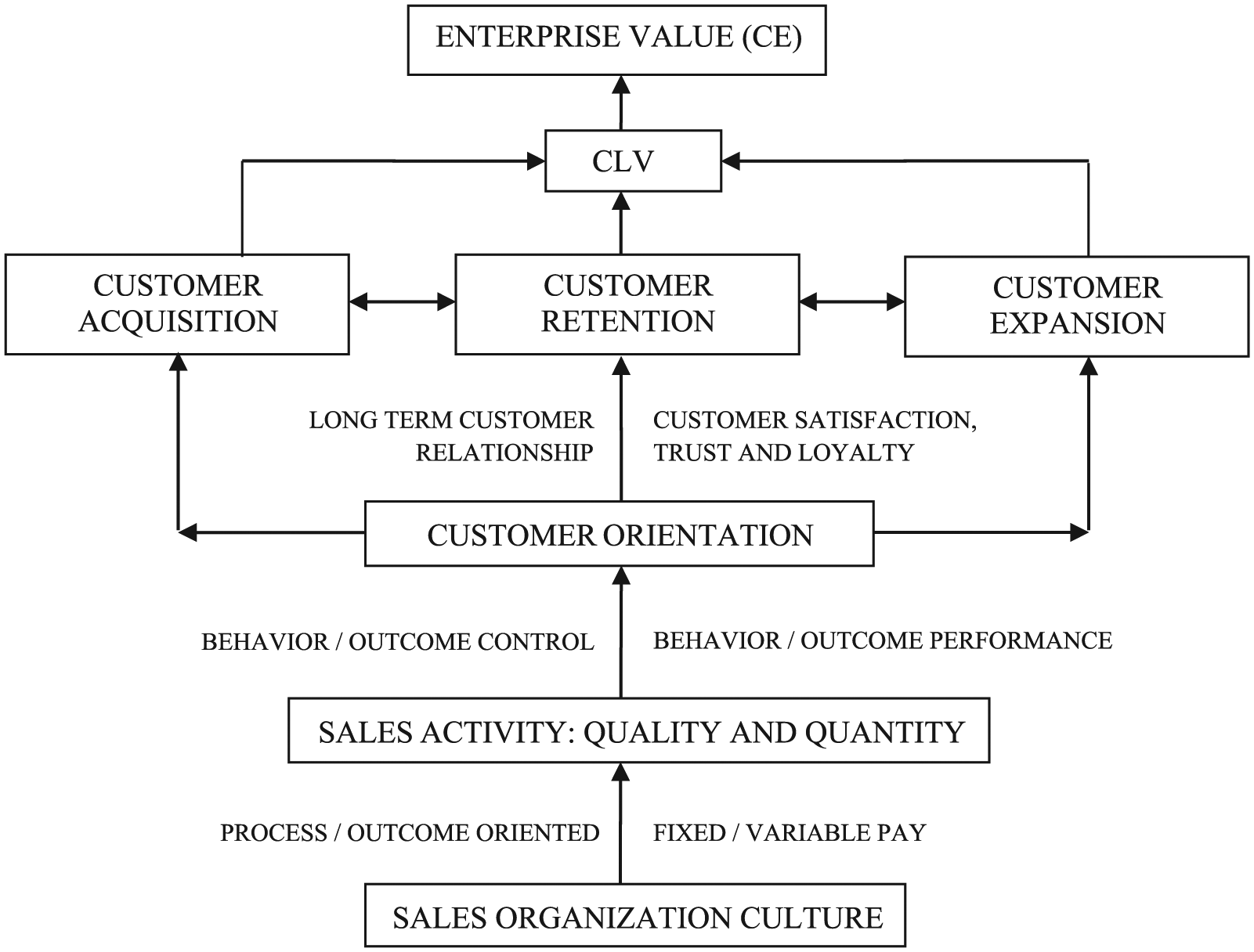

As the customer base forms an integral part of a sales organization’s overall value, valuing customers makes it possible to value the sales organization. The lifetime value of a customer (i.e., the customer lifetime value [CLV]) for an organization is the net revenues obtained from that customer over the lifetime of transactions with that customer minus the cost of attracting, selling and servicing the customer taking into account the time value of money. Thus, CLV reflects the present value of all expected future flows associated with the customer. 18 The framework shown in Figure 2 illustrates how the culture of sales organization influences sales performance in terms of sales activity quality and quantity, customer orientation and consequently CLV.

CLV: Impact of sales organization culture and customer orientation.

Customer retention (caused by increased customer satisfaction, trust and loyalty), customer expansion (caused by cross-selling and up-selling) and customer acquisition (cost affected by focus of sales activity, i.e., quality vs. quantity depending on types of sales organization culture) are directly related to CLV. The CLV of a customer represents the amount the customer will contribute to the bottom line of the organizations over the span of the business relationship with them. 19 The CLV concept simply suggests that it is also important to focus on the quality of customers organizations acquire, not just the number of customers. According to a prior research, 20% of a company’s customers make 150% to 300% of the company’s total profit, 60% to 70% of the customers breakeven (their CLV equals zero) and 10% to 20% of the customers lose from 50% to 200% of the company’s total profit. 20

If a sales organization is able to build deep, committed and meaningful relationships with their customers through customer orientation, it enhances their loyalty and they will keep a relationship with the sales organization for a longer period of time, and such committed customers generate higher CLV for the sales organization. However, there should be an optimal level of customer orientation as shown in Figure 1. Very high level of customer orientation at the cost of higher customer acquisition cost will also result in suboptimal performance with lower CLV.

A organization having a process-oriented culture has a higher retention rate of customer as well as customer acquisition cost, whereas an outcome-oriented culture has a low retention rate of customer as well as customer acquisition cost. 21 Thus, CLV is also influenced by types of organization culture. The valuation of an organization can be depicted in the form of Customer Equity (CE) as it is a good proxy of overall organization value. 22 CE is defined as the total of the CLV (customer lifetime value) of all the organization’s current and potential customers. 23

CE seeks to assess the value of not only a firm’s current customer base but also its potential or future customer base and represents the entire operating cash flow of a firm. This is because operating assets provide cash flows only, if they are used to create products and services that are purchased by customers. 24 Consequently, CE and all cash flows generated from nonoperating assets yield the overall value of a firm. The CLV represents such a profound supplier-oriented understanding of customer value. A supplier-oriented point of view for customer value is defined as the customer’s economic value to the company, a definition that differs from the frequently employed demand-oriented definition of customer value as the company’s or its products’ value for the customer. 25

As shown in Figure 2, the culture of an organization affects firm valuation. The CLV is an appropriate metric to assess the overall value of a firm, because the long-term value of customers is a more stable and relevant metric of firm value than financial metrics like market capitalization. Sales organization culture influences customer orientation, which in turn affects customer acquisition, customer retention and customer expansion, and ultimately impact CLV, CE or valuation of the firm.

Mix of Process-Oriented Culture and Outcome-Oriented Culture: An Optimal Solution

In a sales organization, culture should be considered as a strategy, because it influences the various activities (and the extent to which they are performed) of salespeople and comprise an organization’s strategy for managing salespeople. The culture of any sales organization is the product of its management control system: the policy that governs the way a sales organization trains, monitors, supervises, motivates and evaluates salespeople. It signals what the management expects from its salespeople and conveys to salespeople which trade-offs the sales organization would prefer them to make when inevitable conflicts arise between focusing on higher customer satisfaction and focusing on higher sales volume.

Sales organizations can develop sales goals of different time frames such as short term versus long term to reflect various types of organization culture such as outcome-oriented culture versus process-oriented culture. The appropriate compensation scheme is not the same for each strategy. Sales organizations with a long-term approach design a compensation plan based on parity compensation, which typically is implemented with a higher proportion of fixed pay (salary) in the pay mix, as it allows them to better control behavior or the way the sales force does its selling and moves the risk away from the salesperson to the sales organization. Sales organizations with a short-term sales goals however are unlikely to see much benefit in accepting the risk from salespeople. They are likely to buy results rather than their behavior. Therefore, as sales organizations choose the equity rule, salespeople will not respond positively to a long-term directive since they want the best performance results possible in the short term in order to get the biggest share of rewards.

Strategy suffers and execution fails when sales organizations do not help salespeople manage the tension between serving the need of immediate payoff with focus on higher sales volume (short-term objective) and serving the need of customers with focus on higher customer orientation (long-term objective). It is because a sales organization’s controls (behavior vs. outcome control) are in conflict with one another. This misalignment invariably creates problems in sales functions.

A process-oriented culture is facilitated by monitoring as there is a high level of managerial intervention and deployment of subjective measures of inputs. In a process-oriented culture, sales organizations may dictate how salespeople make sales (new accounts or repeat business due to higher customer satisfaction), implying that their job is not only about meeting sales quota but also about the ways to achieve it. An outcome-oriented culture is influenced by the incentive plan design as there is little monitoring and managerial direction. An outcome-oriented culture rewards salespeople for what they produce, thus encouraging them to do whatever it takes to achieve the sales target.

The two culture types are at extremes, and many sales organizations function quite well somewhere in the middle, where the benefits of a process-oriented culture and the benefits of an outcome-oriented culture are in some sort of equilibrium. Indeed, this is where most sales organizations should be. Figure 3 shows sales organization culture with optimal performance.

Sales organization culture: Various types.

Illustration

To get an optimal sales organization culture with a corresponding compensation plan where the firm has maximum valuation, various scenarios of organization culture (such as wholesome process-oriented culture, outcome-oriented culture and varying degrees of outcome- vs. process-oriented culture) are considered. In these different scenarios, it is assumed that contribution margin and promotion costs remain unchanged. However, customer retention rate and customer acquisition costs vary according to various cultures. Table 2 provides customer buying behavior data for a sales organization along with related the financial matrix. The total number of customers considered for the sales organization in this illustration is 10,000.

Customer Buying Behavior Data and Financial Matrix.

Source. Table developed by the author.

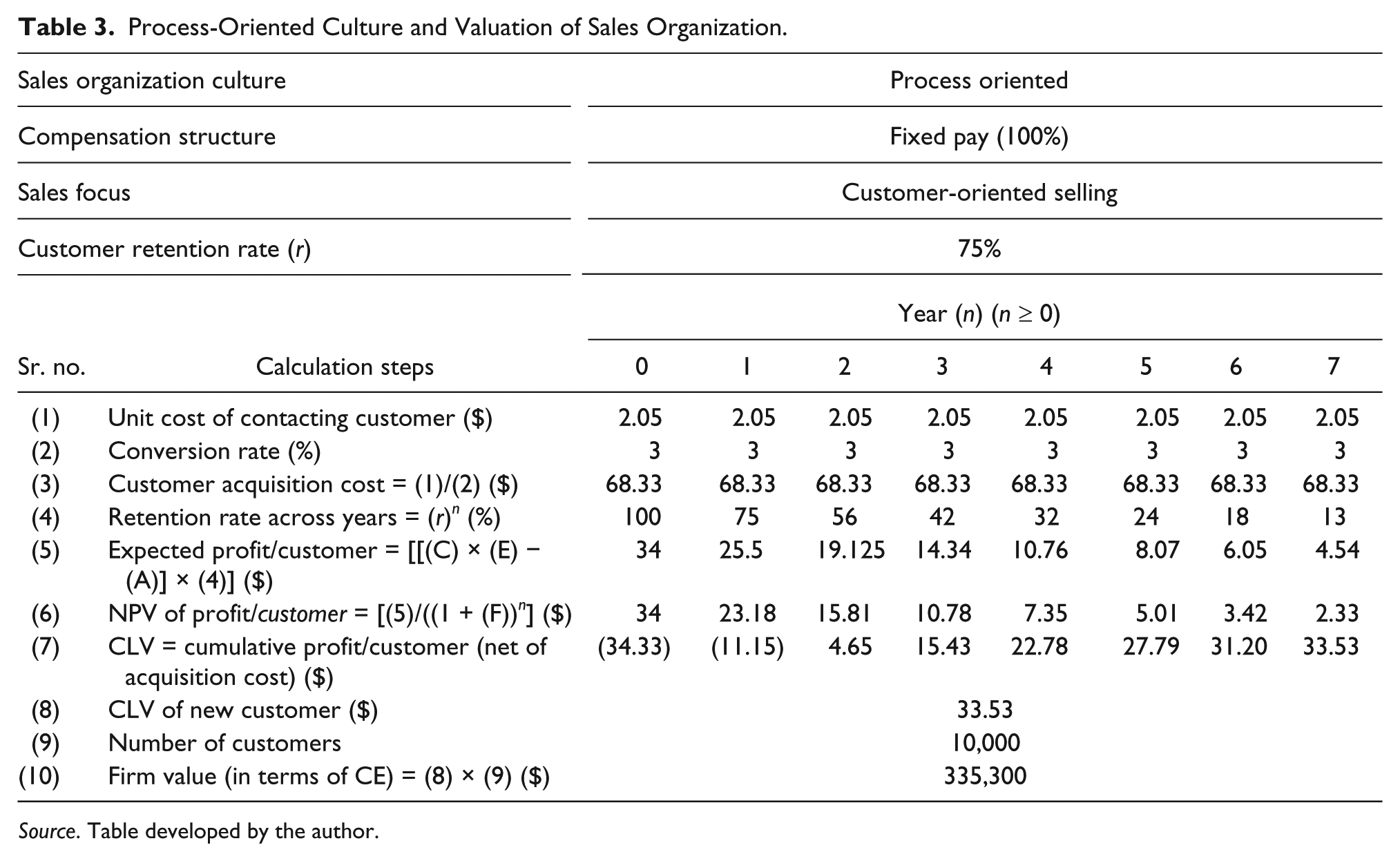

Table 3 shows the process-oriented culture (with salary focus) of a sales organization with an appropriate compensation strategy. It also shows calculation for CLV, CE and ultimately firm value.

Process-Oriented Culture and Valuation of Sales Organization.

Source. Table developed by the author.

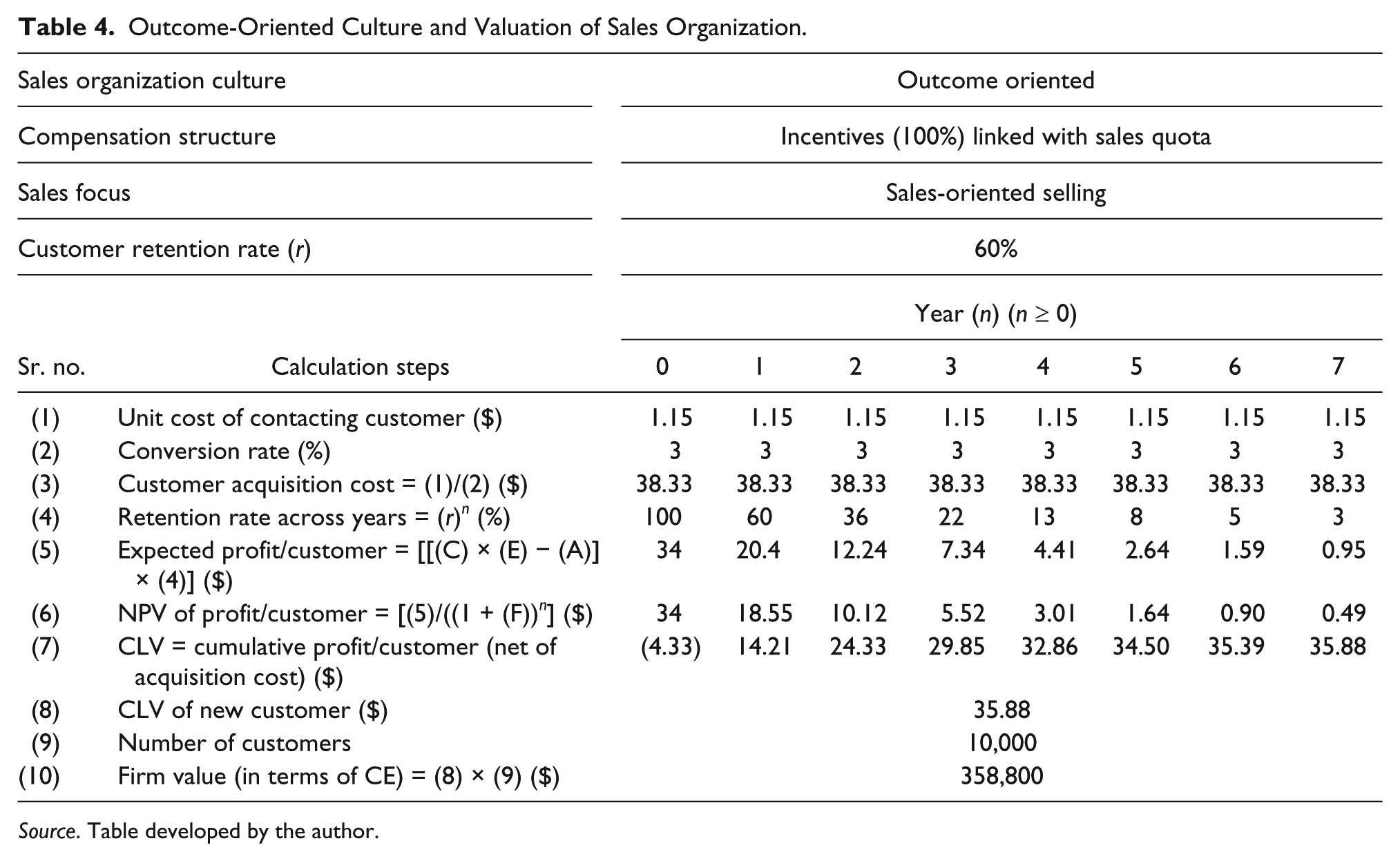

Table 4 shows the outcome-oriented culture (with incentive focus) of a sales organization with appropriate compensation strategy. It also shows calculation for CLV, CE and ultimately firm value.

Outcome-Oriented Culture and Valuation of Sales Organization.

Source. Table developed by the author.

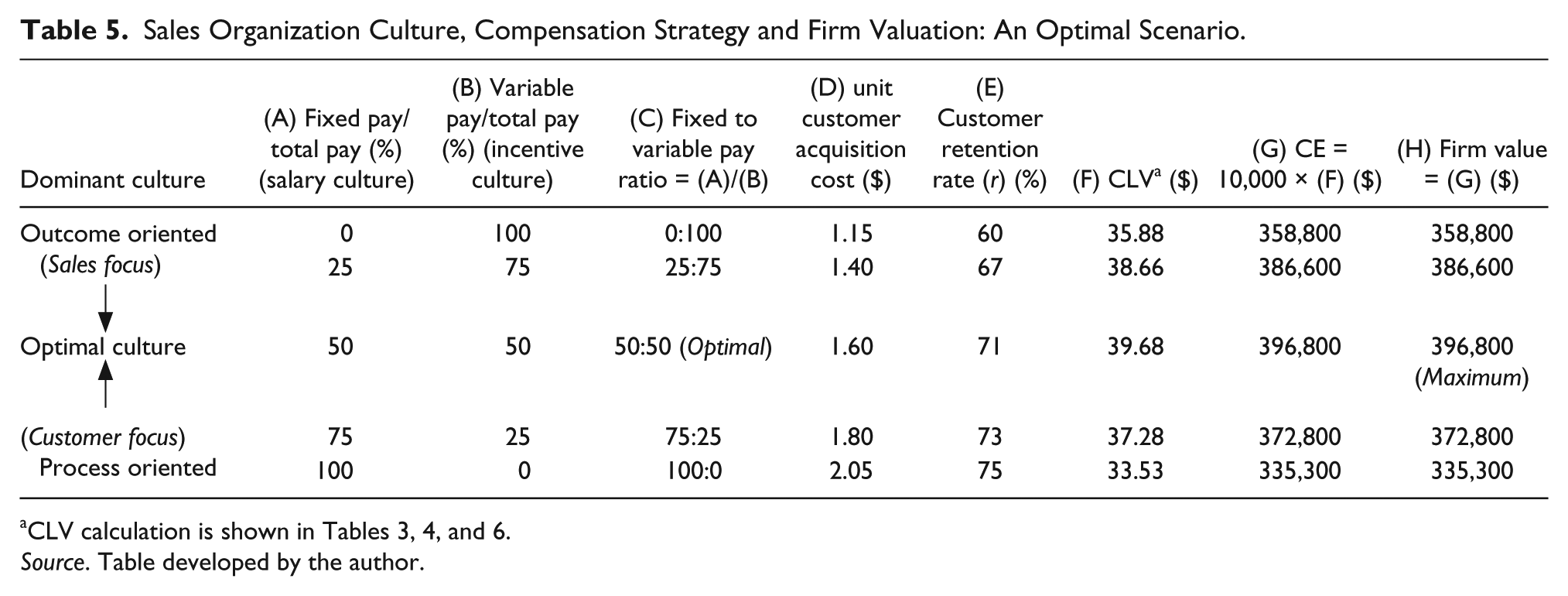

Similarly, valuation of a sales organization is calculated for varying degrees of outcome-oriented culture and process-oriented culture (Table 5).

Sales Organization Culture, Compensation Strategy and Firm Valuation: An Optimal Scenario.

Source. Table developed by the author.

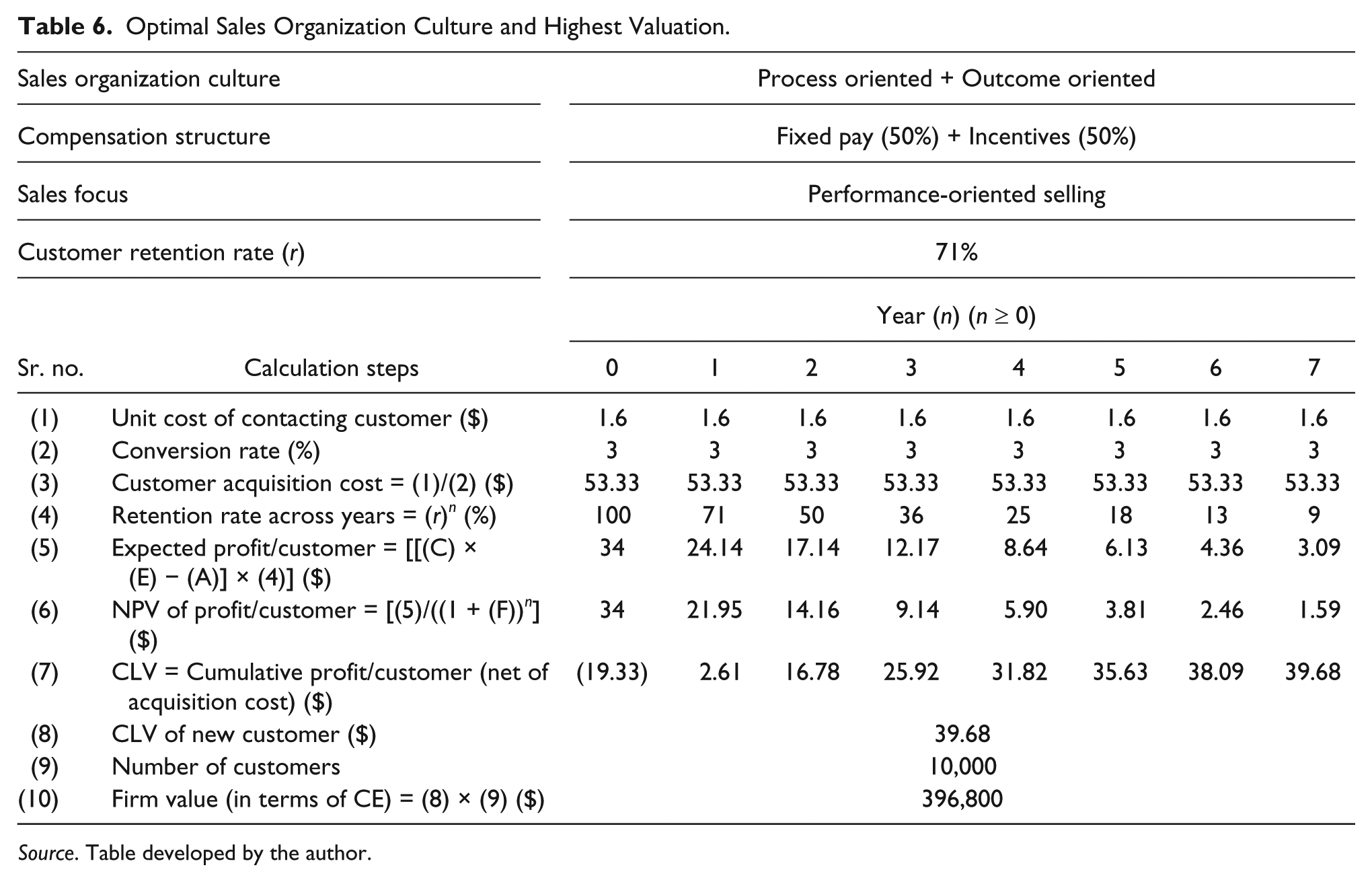

It is evident from the Table 5 that in a performance-enhancing organization culture (with optimal mix of outcome-oriented as well as process-oriented culture), the valuation of a sales organization is maximum. A detailed calculation for such a performance-enhancing organization culture is given in Table 6. An organization having such a culture has the optimal balance of fixed and variable pay in its compensation structure. In this strong positive culture, the sales organization has an optimal level of customer retention rate as well as customer acquisition cost and accordingly the valuation of the sales organization is maximum (Table 5).

Optimal Sales Organization Culture and Highest Valuation.

Source. Table developed by the author.

The relationship of sales organization culture and valuation as calculated in this illustration is shown as a chart in Figure 4. It also shows the optimal point where the valuation of the sales organization is maximum. At this point the sales organization has an optimal culture with the corresponding optimal pay mix.

Sales organization culture and valuation: An optimal scenario.

Conclusions

Many sales organizations today are focusing on their culture as a strategic tool, deciding what it should be, aligning with strategic goals, business strategy and sales compensation design and transitioning to the desired culture. A process-oriented culture focuses on behavior controls and emphasizes sales behaviors, whereas an outcome-oriented culture focuses on outcome controls and emphasizes sales outcomes. An effective sales performance supported by an appropriate compensation strategy and culture of the sales organization plays a significant role in determining financial performance, enhancing valuation of the sales organization and increasing competitive advantage in the market place.

Sales organization culture has a direct influence on customer acquisition cost due to varying sales performance (sales activity with quality focus as in behavior-based control or quantity focus as in an outcome-based control) as well as customer retention rate due to varying levels of customer orientation (a process-oriented culture has higher degree of customer orientation compared with an outcome-oriented culture). Process-oriented culture and outcome-oriented culture are very different and hence produce very different results. Hence, no culture is best in all circumstances as it also depends on the design of a compensation plan. Few sales organizations should be inculcating wholesale process-oriented culture or outcome-oriented culture. However, trying to do both at the same time does not work.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.