Abstract

There is a large literature examining the effect of taxes and tax concessions on local economic development. The last comprehensive review of taxes and economic development, however, was Wasylenko’s review in 1997, which mostly examined the location response of firms. Subsequent to the last major review of the literature, empirical work in this area sought to address endogeneity concerns that plagued previous studies, resulting in a series of compelling new studies. This article reviews the empirical literature on tax-based economic development incentives produced since Wasylenko’s 1997 review and covers property tax (including tax increment financing and business improvement districts); spatially targeted and zone-based tax concessions; firm-specific incentives; and corporate income taxes. The review focuses on academic studies that employ modern program evaluation or quasi-experimental techniques and U.S.-based policies.

Estimates suggest that the value of state and local economic development incentives in the United States is between $45 billion and $90 billion annually (Bartik, 2017). 1 These incentives include a broad range of options—corporate income tax concessions, regulatory concessions, direct grants, targeted infrastructure improvements, employment tax credits, property tax abatements, and refundable tax credits, among others. Taxes and tax concessions play an outsized role in state and local economic development compared to most other policies, like customized job training. 2 There is a large literature examining the effect of taxes and tax concessions on local economic development, but no recent comprehensive review of this literature. The last comprehensive review of taxes and economic development was Wasylenko (1997), 3 which mostly examined the location response of firms. 4

In commentary on Wasylenko (1997), Bartik (1997) called for more studies that make use of natural experiments to study taxes and tax incentive policies, citing endogeneity as a primary concern with the studies available at that time. The primary difficulty in studying how taxes and tax incentives impact local economic development is that they are a result of local economic conditions, making variation in the policies directly correlated with outcomes of interest regardless of actual policy effects. Bartik’s critique has become a driving force in the empirical work on taxes and economic development, as is lucidly described (in reference to the capitalization of property taxes) by Elinder and Persson (2017, p. 19): Most of the earlier studies on property tax capitalization analyze local or regional cross-sectional variation in property tax rates. There are two fundamental identification problems with that approach, and these problems have been known and discussed since the seminal paper by Oates (1969). First, a higher tax rate implies higher tax revenues and consequently higher quality of public goods. Higher quality of public goods puts upward pressure on house prices, making it difficult to isolate the effect of the tax separately. Controlling for public goods quality has been the main concern so as to avoid biased estimates, but this task has proven difficult. Second, when local governments set their tax rate, areas with higher house prices, all else equal, are able to set a lower tax rate to collect a given amount of tax revenues. This creates a simultaneity bias between the property tax rate and house prices.

Following the general trend in empirical microeconometric research occurring over the past few decades (Angrist & Pischke, 2010), much of the literature on local economic development and taxes has focused on the use of natural experiments to address endogeneity concerns. 5 The newer literature examining the economic development effects of taxes, especially the capitalization effects of property taxes, relies on examining policy changes that can be categorized as natural experiments to deal with estimation problems. Tax policy can be thought of as a natural experiment if there is a “transparent exogenous source of variation in the explanatory variable” Meyer (1995, p. 151). Natural experiments break the endogenous relationship between outcomes and policy and allow for unbiased estimation of the effects of tax policy on local economies.

Not all policy changes can be thought of as natural experiments, and within the natural experiment framework there are differing methodologies—each with different assumptions, strengths, and weaknesses. 6 The most believable natural experiment approaches employ policy changes with two key elements: being unanticipated (or having features that are unanticipated) and varying across an otherwise homogenous population (allowing for treatment and comparison groups). Meyer (1995) made the point that the movement toward using natural experiments has the benefit of pushing researchers to consider the source of variation in the policies they study, and how it may relate to other factors, improving the quality of overall research.

In the years since Bartik’s (2017) commentary, a vast literature on taxes and tax incentives has emerged, much of it designed to confront the problem of endogeneity using natural experiment approaches to evaluation. This article reviews the modern literature on the effect of tax policy on state and local economic development. 7 It is rare in the literature to find studies of taxes that examine an outcome not directly related to the type of tax studied—property tax studies tend to examine property values; corporate income tax studies tend to examine corporate investment. This review covers tax-based policies in the areas of property tax (including tax increment financing (TIF) and business improvement districts [BIDs]), spatially targeted and zone-based tax concessions, firm-specific incentives, and corporate income taxes. The review covers a host of economic outcomes studied in the literature including business location, employment, income/poverty, and property values. The review focuses on academic studies that employ modern program evaluation or quasi-experimental techniques and examines U.S.-based policy, 8 essentially the work that has answered Bartik’s (1997) call to take endogeneity seriously.

By reviewing, summarizing, and in some cases highlighting the research on taxes and economic development from the past 20 years of academic research, I hope to inform both future researchers in this area and the policy-making community. As the trend in economics research more generally shifted toward rigorous empirical methods during this period, researchers have uncovered evidence that is useful for policy making. The output from the research covered here and the ongoing research effort in this area should be part of informing policy makers about the wisdom of using tax policy as an economic development tool.

Criteria and Procedure for Review and Trends in Publication

The first selection criteria for this review was to narrow down economic development policies to a set of taxes and tax-based incentives. The review covers tax-based policies in the areas of property tax (including TIF and BIDs), spatially targeted and zone-based tax concessions, firm-specific incentives, and corporate income taxes. I choose to examine these policies because they make up the primary toolkit used by U.S. state and local governments to encourage economic development. Additionally, these taxes and tax incentives primarily link economic activity and policy to a place rather than to a group of people, typically the target of redevelopment policy. Notably, I do not cover the economic effects of individual income taxes, as I view those policies as linked to people. 9

The second selection criteria was to examine research that answers Bartik’s (2017) call to take endogeneity seriously. For this criteria, papers needed to meet one of two standards: (a) demonstrate the use of strictly exogenous variation in tax policy, or (b) demonstrate the use of plausibly exogenous tax variation in tax policy and the proper use of quasi-experimental evaluation methods (including difference-in-differences, regression discontinuity, instrumental variables, and synthetic control methods). For the first qualifying criteria, strictly exogenous is defined as a tax policy that, by its own application and administration, is generated orthogonally from the outcome of interest. The gold standard for strictly exogenous would be random assignment of tax policy, which is almost never the case in practice. Examples of the strict criteria could be a policy generated from a higher level of government and bestowed on a local economy without regard to local conditions, or a rule that limits the generosity of the tax policy for reasons that are unrelated to local economic conditions (such as through a budget constraint). For the second qualifying criteria, I relax the strict exogenous definition and allow for plausibly exogenous policy variation but require the proper use of a quasi-experimental method to aid in identification. The proper qualifier indicates that the paper successfully implements the method, performs proper validity and robustness checks, and applies appropriate data. The second criteria are necessarily subjective, especially in the case of the proper qualifying criteria. For example, there are many papers that apply difference-in-differences estimation, but the quality of the difference-in-differences estimate is determined by the selection of the comparison group and examining pretrend differences between comparison and treated groups (among other things).

The search process for finding research that met the two criteria above moved as follows. First, I did an exhaustive article-by-article examination of the top economics journals in public finance and urban/regional economics. This included the National Tax Journal (NTJ), Journal of Urban Economics (JUE), Regional Science and Urban Economics (RSUE), Journal of Public Economics (JPubE), American Economic Journal: Economic Policy (AEJP), and the Journal of Regional Science (JRS). Notably, this review is not restricted to publications in these journals, but these journals were used to perform an exhaustive search. These journals were chosen because they are widely discussed as the top journals in the field of economics and regularly publish studies about taxes and economic development. I examined each issue of these journals beginning in 1998 and ending in 2018 and looked for articles that met the selection criteria. In addition to exhaustively examining these journals, I also used both EconLit and Google Scholar to search for relevant terms, such as “[type] tax economic development”; articles published in any economics journal could potentially be included within this search. On finding an article that met the selection criteria, I again used Google Scholar to view articles that cited the chosen article to browse for other potential pieces of research that met the selection criteria. Papers that were on topic, but that did not meet the selection criteria, were not reviewed.

Tables 1, 2, and 3 list the primary papers that comprised this review. Table 1 summarizes the studies of property taxes and property tax-based policies (BIDs in this case). Table 2 summarizes the studies of zone-based tax incentives. Table 3 summarizes the studies of firm-specific tax incentives and corporate tax studies. Note that while the studies listed in Tables 1 through 3 make up the core of the review, there are many other important (and compelling) related studies discussed in the text. Notably, individual studies of TIF are excluded from the tables but are discussed in the text, as they are aptly covered by other review papers.

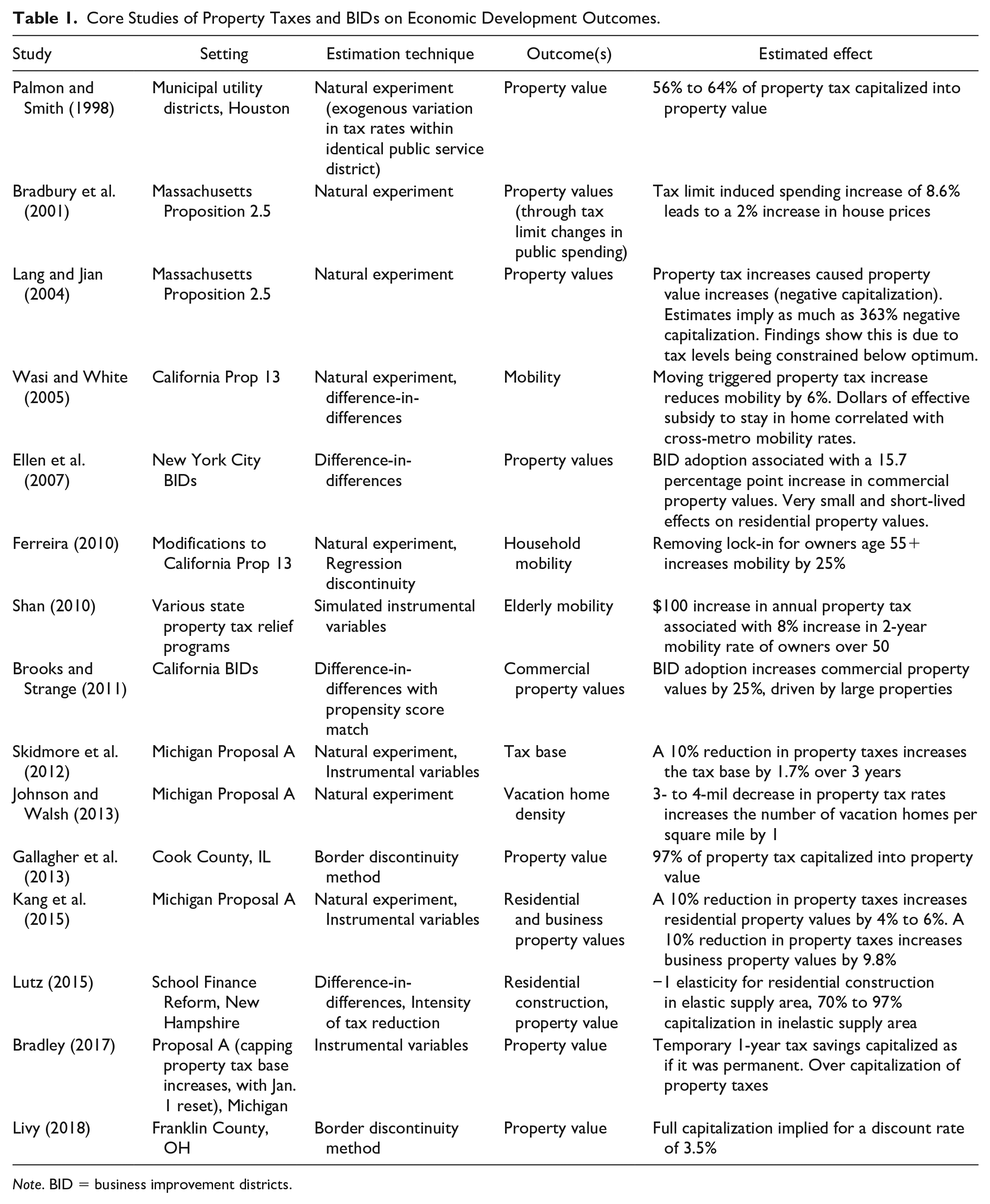

Core Studies of Property Taxes and BIDs on Economic Development Outcomes.

Note. BID = business improvement districts.

Core Studies of Zone-Based Tax Incentives and Economic Development Outcomes.

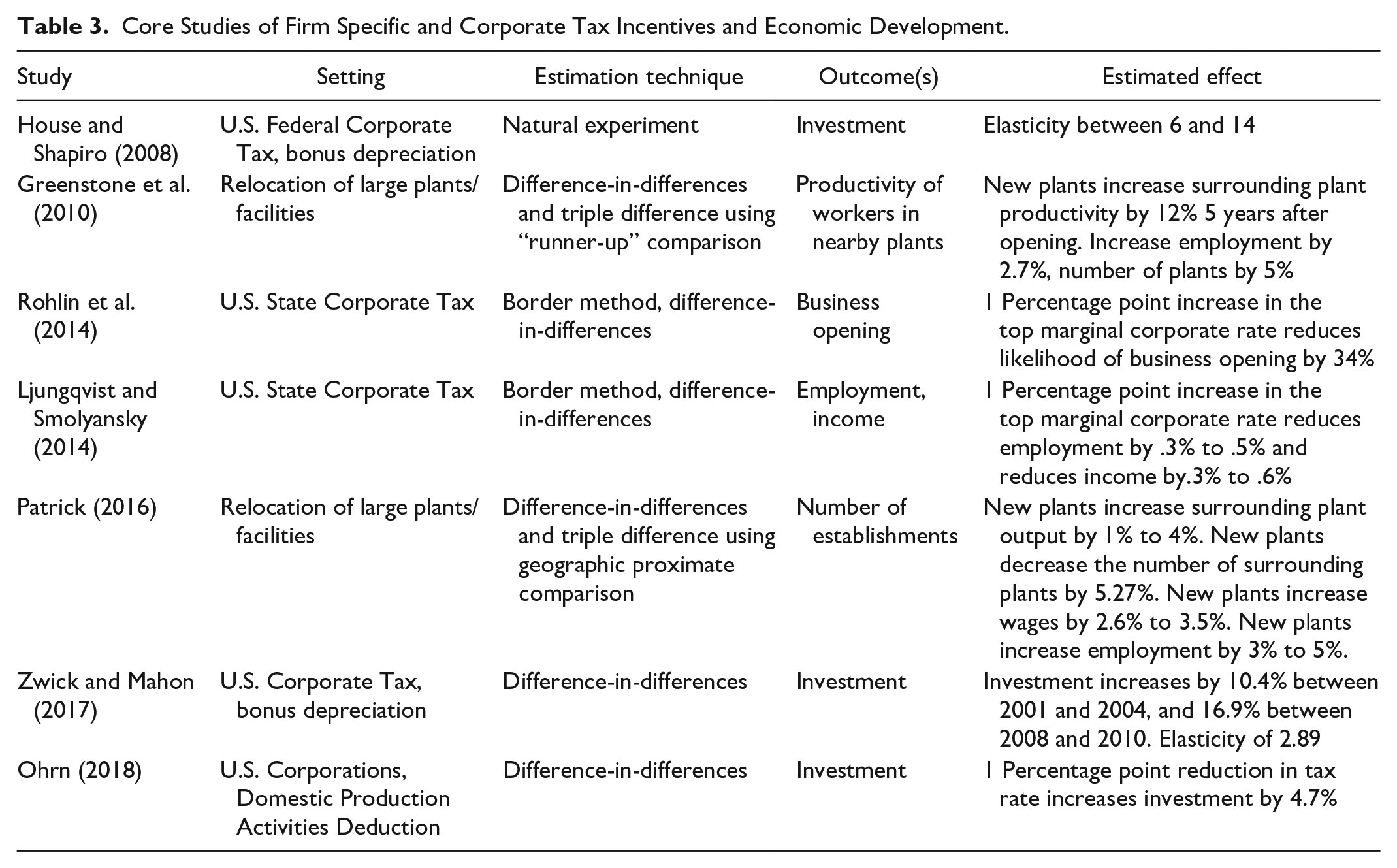

Core Studies of Firm Specific and Corporate Tax Incentives and Economic Development.

Of the 35 core studies in this review, 19 were published in the journals where an exhaustive review was completed. Regional Science and Urban Economics published the largest number of core studies, with 7 over the 1998 to 2018 period, followed by JUE (5), JPubE (4), AEJP (2), and JRS (1). The NTJ did not publish a study included in the core list during this time period, although that journal published several important studies discussed here, including Brooks (2007), Greenbaum and Landers (2014), and Patrick (2014). Also, among the 35 core studies, 6 were published in top economics general-interest journals, including the Journal of Political Economy (2), the American Economic Review (3), and the Review of Economics and Statistics (1). The remaining 10 core studies were published in a variety of outlets, including Economic Development Quarterly, the Brookings-Wharton Papers on Urban Affairs, Public Finance Review, and Real Estate Economics.

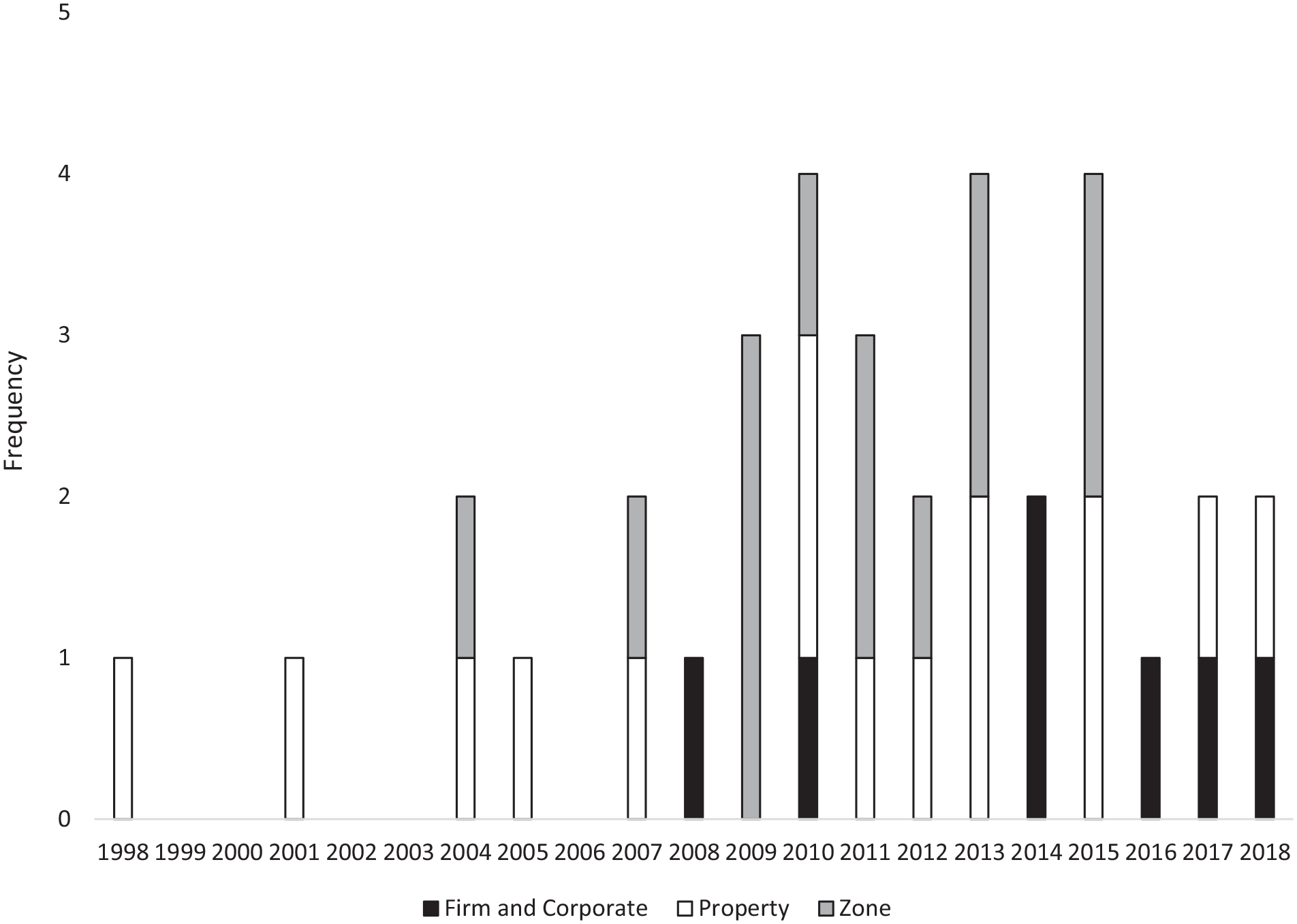

Figure 1 shows a histogram of the core studies across the period reviewed by publication date and categorized into types (firm and corporate, property, zone). The histogram indicates that there were very few studies that met the selection criteria before the mid-2000s, and stark growth in the number of published studies happening between 2009 and 2015. This is a function of both the number of studies in the field and the selection criteria. As quasi-experimental methods have become more commonly used by researchers, the number of studies that meet the selection criteria has grown. Notably, there is a decline in the number of studies beginning in 2015, driven by a dearth of studies on zone-based incentives. It remains to be seen if this trend will continue into the 2020s.

Histogram of core studies by type.

Across types of taxes and incentives, there are noticeable differences in publication trends. Studies of property taxes and incentives published between one and two articles per year in the sample period (with some years of zero publication in the first part of the period). Studies of zone-based incentives became quite common between 2009 and 2015 but were uncommon before and after that time window. Studies of firm-specific incentives and corporate taxes were dormant up until 2008 but have since been published at a rate of about one per year.

Besides the aforementioned increase in the use of quasi-experimental methods during this period, there are also likely policy changes driving the time trends in research. The advent of the federal Empowerment Zone (EMZ) program in the mid-1990s, as well as several state-level programs around the same time, seems to have at least partially induced the uptick in zone-based studies that occurs beginning in 2009. More recently, the dramatic expansion of offering individual firm subsidies and corporate tax relief seems to precede the uptick in academic research in these areas.

Property Taxes and Incentives

The economic development effects of property taxes, or from various forms of property tax relief, are typically measured in the form of capitalization into property values, although some newer studies also examined mobility and construction. 10 There exists a vast pre-2007 literature on the capitalization of property taxes and property tax relief beginning with Oates (1969), and aptly summarized by Yinger et al. (1988), Guilfoyle (2000), and Sirmans et al. (2008). These reviews both concluded that the empirical literature broadly suggested incomplete capitalization of property taxes into property values, although some studies suggested full capitalization.

While capitalization is not necessarily a stated economic development goal (as might be the case with employment), it represents an important outcome for several reasons. First, changing property values indicates that something about the location has also changed. A typical spatial equilibrium model would point to changes in the employment market or local amenities as being reflected in the value of property. Second, land represents the most inelastic of factors, and in any simple model of tax/subsidy incidence, it is the inelastic factor that will absorb changes to taxes/subsidies. This effect should be heightened for policies that are explicitly targeted to place. Third, capitalization effects of policy point to specific beneficiaries from policy changes—landowners. While there may be simultaneous effects in other markets, if policy becomes capitalized, it is landowners who will benefit from the change.

The endogeneity critique outlined in the beginning of this article has played a central role in the literature on the economic development (and capitalization) effects of property taxes. Most of the earlier literature tried to solve this issue by estimating two-stage least squares (2SLS) models, where the first stage explains differences in property tax rates and the second uses the predicted values of property tax rates to explain property values (or another economic outcome of interest). A well-identified 2SLS model would require that there is a factor driving changes in the property tax rate that is orthogonal to house prices (or any outcome of interest), but there is not a strong case for this important criterion in much of the pre-2000 literature. As discussed earlier, this review focuses on the studies that have best dealt with endogeneity concerns.

Post-1997 U.S.-Based Studies

The modern literature on the economic effects of property taxes, summarized in chronological order by Table 1, essentially starts with Palmon and Smith (1998). Capitalization rates reported in Table 1 refer the present value of the tax change that is reflected in current prices, where full or complete capitalization is 100%. If a percentage is reported, then researchers made a choice about how the discount rate applied to future tax liabilities; in other cases, researchers reported the discount rate that is implied if full capitalization exists. Palmon and Smith studied capitalization across municipal utility districts in the suburbs of Houston, TX. Palmon and Smith relied on variation in tax rates within an identical public service district. This study related how property tax rates vary among a cross section of 501 homes sold in 1989 and found that between 56% and 64% of tax differences are capitalized into home prices.

There are two reasons the Palmon and Smith (1998) study begins this review of the literature. First, its publication date places it immediately after the most recent comprehensive literature review. Second, and more important, it lays out a case for why the variation in property taxes in the study may be separate from the variation in public services, offering the ability to identify a pure tax capitalization effect. While there are reasons to find the Palmon and Smith study convincing, there is also good reason that the literature on the economic development effects of property taxes did not end there. First, there are likely to be some differences in public services across the study area of the Houston suburbs; moreover, Palmon and Smith did not make much of a case to show that public services are uniform. Second, the sources of variation in property taxes used in the study could easily be correlated directly with house price or correlated with other factors that change house prices. Finally, the study is of a small area of one city in the United States and the results may not be externally valid. Perhaps because of these reasons, this literature has continued throughout most of the last 20 years.

The 2000s brought a continued focus on sources of exogenous variation from natural experiments to study the economic effects of property taxes. Many of these modern studies focused on major reforms to state policy to limit property tax payments: Massachusetts Proposition 2½, California Proposition 13, and Michigan’s Proposal A. Other studies employed emerging tools from the program evaluation literature, such as difference-in-differences and border discontinuity methods.

Some of the first papers in the modern literature examined Massachusetts Proposition 2½, a measure that reduced effective property tax rates to 2.5% and limited the future growth in property tax revenues to 2.5%. 11 Bradbury et al. (2001) presented evidence that suggested Proposition 2½ was binding for many municipalities in Massachusetts—they pointed out that over half of municipalities had effective tax rates higher than the limit at the time the limit was voted into law. The fact that Proposition 2½ was implemented statewide in Massachusetts (making it exogenous to any individual municipality) and was binding for only a subset of municipalities (creating comparison and treatment areas) make it a viable natural experiment to study the economic effects of property taxes.

Bradbury et al. (2001) and Lang and Jian (2004) used Massachusetts Proposition 2½ to study the effects of property taxes on property values. These papers used different windows of data to study these effects but are otherwise quite similar. Both papers showed increases in property values in municipalities that were able to increase tax revenues (expenditures). In the context of the Proposition 2½ reform, this indicates that the law was holding the level of public goods/services (and corresponding tax collections) below what residents of municipalities preferred. The Proposition 2½ studies represent an earlier use of a natural experiment but do not fully separate the effects of property taxes from local spending, and so do not offer a pure estimate of tax capitalization.

While most of the studies of the economic effect of property taxation examined capitalization, there are several excellent studies that examine the mobility effects of property taxes. Chronologically, most of the mobility studies were published after the Proposition 2½ studies and before a series of excellent studies that also examined property value effects. The modern literature on how property taxes effect mobility begins with Wasi and White (2005), who used California’s Proposition 13 as a natural experiment combined with a difference-in-differences estimation strategy. Proposition 13, voted into law in 1978, mandates a property tax rate of 1% plus the cost of paying interest on locally issued bonds. Besides mandating the rate of property tax, Proposition 13 also mandates that properties are assessed at their market value at the time of purchase and that assessment growth cannot be more than 2% per year.

Proposition 13 dramatically increased property taxes for new owners of a home, as moving triggers a reassessment of property values on the purchased property. Wasi and White (2005) found that Proposition 13 caused the average tenure for homeowners in California to increase by 6%, with stronger negative effects on in-migrants to California. Wasi and White (2005) also found that the implicit subsidy for homeowners to stay in their homes varied across markets, and that the size of the subsidy was further correlated with declining mobility.

Ferreira (2010) used amendments to Proposition 13 to further study how property taxes effect mobility. Ferreira (2010) made use of amendments that allow homeowners age 55 or older to transfer the value of their property to a new property, but the provision does not apply to younger homeowners. 12 Using a regression discontinuity design, Ferreira (2010) documented a significant jump in the probability that a California homeowner moves after age 55 relative to before that age. The property tax benefit associated with being able to transfer value (thus reducing property tax burden) at age 55 results in a 25% higher mobility rate among 55-year-old homeowners compared with 54-year-old homeowners.

The California property tax preferences for older homeowners are not unique—many states offer property tax relief programs that are based on age or other characteristics like income. Shan (2010) documented the many state and local property tax preferences that depend on a resident’s age (as well as income and home value, among other characteristics) and studies how these policies affect mobility among the elderly using a simulated instrumental variables strategy. 13 Shan (2010) showed that a $100 increase in annual property taxes is associated with an 8% increase (0.73 percentage points on a base of 9%) in the mobility rate for homeowners older than age 50.

In addition to the statewide property tax reforms in Massachusetts and California, Michigan underwent a major reform in the mid-1990s in the form of Proposal A. The property tax reform in Michigan has also been the subject of several studies that use it in a natural experiment framework to determine the economic effects of the property tax. Proposal A, implemented as a school finance reform, imposed a 5% limit (or the inflation rate, if it is lower) on the growth of taxable property value and a maximum statutory mil rate for a principle residence. 14 However, values of sold properties are assessed at the acquisition value, creating a disincentive for mobility.

Skidmore et al. (2012) studied how the property tax limits imposed by Proposal A effected the property tax base in the communities of southeast Michigan using the exogenous change in tax rates from the statewide reform as an instrument for local tax rates. Skidmore et al. found that a community’s tax base, as measured by the aggregate property value over a 3-year period, is sensitive to the property tax rate. They estimated that for every 10% decrease in the property tax rate, the tax base would grow by 1.7%. Kang et al. (2015) further studied Proposal A, examining the potential for differential response to school spending and property taxes by businesses and residents. Using the same methodology as Skidmore et al. (2012), Kang et al. (2015) found that residential property values were more sensitive to school spending than property tax rates, but business property values were more responsive to tax rates than school spending. They also pointed out that business property values respond more to tax rate increases than residential property values.

Johnson and Walsh (2013) also studied Michigan’s Proposal A but examined how the differential property tax provisions for vacation homes effects vacation home density. By examining vacation home density, Johnson and Walsh further decoupled the link between most public services and the taxes collected, as vacation homeowners should not care about things like school quality (although they may care about other local public goods). Johnson and Walsh’s results showed that a 3- to 4-million decrease in the property tax rate is associated with an increase of 1 vacation home per square kilometer.

In a unique contribution to the literature on property tax capitalization, Bradley (2017) investigated the role that cognitive bias may play in the process. Like other papers in this literature, Bradley (2017) used Michigan’s Proposal A as a natural experiment, but instead of the aggregate data used by other studies, applied microdata on homes sold in Ann Arbor, MI. Bradley pointed to a unique feature of Proposal A that gives homebuyers a temporary tax advantage before their home is assessed at acquisition value for tax purposes—that the taxable value of the home is reset on January 1st of each year. This feature means that a buyer will temporarily pay property taxes based on the prior assessed value for the year they purchase the home (the taxable value will be further below acquisition value for homes the longer it has been since the home sold). Bradley used this temporary tax savings to show that homebuyers are overly sensitive to the temporary tax savings: for every $1 increase in temporary tax savings, the sales price increases by $29. The size of the price increase from the temporary tax savings makes it appear as though buyers are capitalizing a permanent tax savings instead, or that buyers fail to recognize the temporary nature of the tax savings. This result implies that cognitive bias may play a role in how and to what extent property taxes are capitalized into home prices.

In a compelling study, Lutz (2015) examined a 1999 school finance reform in New Hampshire to estimate the effect of property taxes on both residential home construction and capitalization. Lutz was the first modern empirical paper to consider both the price and quantity response to property taxation simultaneously, pointing out that the supply of housing should drive expected capitalization effects of a change in property taxes. To address the primary concern of endogeneity between property taxes, prices, and building, Lutz relied on the nature of the school finance reform in New Hampshire. The reform came as a series of grants to municipalities based on the per-pupil property wealth, which were then used to fund property tax reductions, creating an exogenous change in the property tax burden across municipalities but holding public services constant. Lutz found that a 15% reduction in local property taxes (induced by the grant allocation) causes an increase of 11% to 22% in residential construction, implying an elasticity between −.73 and −1.46. Perhaps most interestingly, Lutz found that the building response is not evident within 50 miles of Boston (covering the major suburban areas of the state), but that the property tax cuts in that area were capitalized into home prices. As predicted by the relative supply elasticities between denser suburban areas and the more sparsely populated areas of the state, only limited capitalization takes place outside of the 50-mile ring around Boston.

Outside of the studies that rely on law changes as direct natural experiments, there are two studies that used variation created by property tax differences that occur at municipal borders to identify the effect of property taxes on property values. This method is referred to as the border discontinuity method; 15 the idea is that areas close to, but on opposite sides of, a municipal boundary are identical (or at least similar) except for a difference in property taxes. If this is true then comparing the sales prices of similar homes close to the municipal border, but on opposite sides, allows an unbiased estimate of property tax capitalization.

Gallagher et al. (2013) applied the border discontinuity method to school-district boundaries in Cook County, IL (excluding Chicago). The design of the study goes further than applying the border method to all district boundaries, instead using only boundaries within a city that divides by school district. In addition to applying the border method at specific boundaries, the authors highlighted that public services can be better controlled for using the sale of small homes, as these homes are less likely to be occupied by families with children and thus the buyers will not be interested in school quality. After taking all these precautions to isolate the effect of school district property taxes, Gallagher et al. (2013) found that these taxes are nearly fully capitalized into home values (97%).

In another application of the border method, Livy (2018) examined capitalization in Franklin County, OH. This study is unique in that the environment allows the researcher to use properties sold within the same school district, but with different applicable tax rates. The research also employed a large data set of home sales across a long period where tax changes occur, allowing the use of property fixed effects and local neighborhood effects. Livy’s results suggested that, for standard discount rates, property tax differences are fully capitalized into a home’s sales price.

Although taxes are the focus of this review and the modern literature on the economic development effects of property taxes satisfyingly disentangles their effects from the effect of public services, most policy inextricably links the two. There is an enormous literature examining the capitalization effects of local school quality, which in many ways mirror the tax capitalization literature. Nguyen-Hoang and Yinger (2011) reviewed the literature on school quality capitalization that came out between 1999 and 2011 and summarized the results as “house values rise by 1-4 percent for a one-standard deviation increase in student test scores” (p. 46). The literature on both general local public goods (such as mass transit options) and school quality continues to grow, with most newer studies following a natural experiment or quasi-experimental approach. These results should be considered in tandem with empirical work that isolates the effect of property taxes.

Limiting property taxes that pay for valuable services causes property values to decline—it is not just that people want lower property taxes, they want public services provided in a cost-effective way. Property taxes also cause some degree of mobility, and these estimates are likely reflective of an “all else equal” approach, suggesting that if property taxes and public services are not in line then residents may relocate to find a better tax/service bundle. The literature that best identifies a pure tax effect (holding public services and other characteristics constant) on property values shows that property tax differences become fully capitalized into property values. To understand how initial characteristics may influence this result (especially local demand and supply elasticities), and if there is any room for property taxes to directly affect other economic outcomes of interest, more studies that follow natural experiments would be useful.

Employment Effects: Results From Traditional Studies

There is only a sparse post-1997 literature on the effects of property taxes on employment—noticeably little modern work has even attempted to make this link. Considering the findings from the capitalization literature this may not be surprising, if property taxes are fully realized in property values there may be no room for other economic effects. It is also worth noting that the studies examining the employment effects of property taxes use more traditional methods of estimation, attempting to control for other factors and estimating a regression model but do not make use of exogenous variation in tax rates created by a natural experiment. All these studies also examine a single metropolitan area and would be subject to the criticism that their results would differ if a similar policy were implemented in a different area (if the policy interacts with the local economy to produce a differential effect on the population of interest).

Mark et al. (2000) examined the effect of personal and business property taxes (as well as sales taxes) on employment growth in the Washington, D.C. metro area. This study estimated the employment effects of local taxes using a municipality fixed-effects model and the changes in tax rates occurring over the 1969 to 1994 period. The results in Mark et al. (2000) showed that a 1 percentage point increase in the personal property tax rate reduces annual employment growth by 2.44 percentage points, or that the elasticity is −2.12. The study also found that corporate income tax rates and commercial property tax rates are not related to employment growth. The authors noted that, outside of the fixed effects, the model does not control for public services like education, which may cause bias estimates of tax effects.

In a study of the Chicago metropolitan area, Dye et al. (2001) examined how the property tax rate and property tax classification 16 contribute to employment growth. The authors used data from 109 municipalities across the 1991 to 1996 period. They used a model with county-level fixed effects, and also controlled for a host of other factors but notably not the level of local public services. Their results showed that raising the tax rate on commercial property by 1 percentage point results in a 1.1 to 1.8 percentage point decrease in employment. Dye et al. (2001) found no independent effect of classification on employment outside of the tax rate effect.

Bollinger and Ihlanfeldt (2003) studied the mix of tax incentives in Atlanta, including commercial/industrial property tax abatements, residential construction/rehabilitation abatements, and job tax credits. They were interested in the effect of these policies on the share of regional employment within the Atlanta area. They used census tract-level data and controlled for other demographic and economic factors of areas outside of taxes but did not employ a natural experiment approach. They found that having a commercial/industrial policy in a census tract is associated with an 80-job increase over a decade. Notably, they used areas within the same metropolitan area as the basis for comparison for policy-treated tracts; these areas may be a poor comparison area as they could be subject to spillover effects from the policies.

Non-U.S. Studies

Outside of studies that examine U.S. policy, there are a host of studies that examine the economic redevelopment effects of property taxes and tax abatements in other countries. There are two studies that stand out, in particular, for employing modern methods of identification—Duranton et al. (2011) and Elinder and Persson (2017). Although the focus of this review is on U.S.-based studies, these papers offer a basis for comparison to the U.S. case and a look into how a different economic environment may interact with property tax policies.

Duranton et al. (2011) examined the effects of a nonresidential property tax in the United Kingdom. This tax is described as imposed on all property uniformly but with differing rates, with the revenues not used for local services. Although empirical work does not rely on a natural experiment that reforms the tax, the authors used variation through both time and across jurisdictional borders (in combination with instrumental variables) to create plausibly exogenous variation in the policy to identify the economic effects. Duranton et al. (2011) estimated the employment elasticity with respect to the nonresidential property tax rate to be approximately −1, but that there are essentially no effects on firm entry/exit from the property tax. The primary result was statistically significant in the authors preferred specification and was robust to some but not all the specification checks in the paper. The results of the Duranton et al. (2011) study are in line with the Chicago and Atlanta U.S. studies that suggested a large effect of business property taxes on employment.

In another European study, Elinder and Persson (2017) examined the capitalization effects of a cut to the national property tax in Sweden. They employed a natural experiment approach, using a reform that lowered the national property tax rate from 1% to 0.75% of the taxable value and capped the annual tax liability (the annual cap was binding for about half of all properties). The Swedish reform took place in 2008 and created a differential tax benefit for properties that increased rapidly for properties with tax liability that was previously lower than the annual cap. The authors estimated a difference-in-differences model around the national reform, using the price path of properties below the cap to create a counterfactual for the price path of properties above the cap. Unlike in the U.S. studies that suggested nearly complete capitalization, Elinder and Persson (2017) found evidence to suggest that the property tax cut was capitalized at between 1/3 to 1/2 of full rate for properties in the top 5% of value, but detected no appreciable capitalization beyond those effects. The authors suggested that the differential capitalization across the distribution of homes was likely driven by scarcity of land in the top segment of the market, large tax reductions in the top segment being quite salient, and the buyers of these homes being relatively more financially literate.

Tax Increment Financing

Much of the literature examining economic development effects of general property taxes focuses on large-scale state reforms; however, economic development is often not the intended outcome of these reforms. A property tax policy that is typically intended to impact economic development is TIF. The idea of a TIF is to designate a special district where the taxable value of properties is frozen (or potentially reduced) for the purposes of standard property tax collection, while the incremental property value appreciation is taxed to finance an economic development project. TIFs are implemented with the “but for” distinction, indicating that the TIF is only allowed if the economic development project would not have occurred “but for” the special tax treatment. Often, local government bonds will be issued to fund the economic development project and repaid with TIF-generated revenues. Merriman (2018) summarized the use of TIF across U.S. states, reporting at least one active TIF district in all states except Arizona (where they are not allowed) and Delaware. Merriman (2018) also reported that many states have several hundred 17 or even thousands 18 of active TIFs, and that there was $37 billion of debt associated with TIFs between 2000 and 2014. 19

The idea behind TIFs directly funding economic redevelopment is clear; however, it is challenging to discern the actual economic impact of the policy for several reasons. The first comes directly from the but for distinction of TIFs. While TIFs are supposedly not to be designated unless the economic development project would not have happened without the TIF, knowing the counterfactual is not possible (would the developer have made the investment even without the TIF?). Second, because evaluators will not know what would have happened in the TIF-designated area in the absence of the policy, they need to estimate this using a comparison area. Finding a comparison area that follows the path that the TIF area would have taken requires an area that is otherwise similar to the TIF district, but that is not subject to spillover effects from the TIF itself, characteristics that may be difficult to measure. Third, it is possible that TIFs are chosen in areas that will be trending differently than comparison areas. Finally, evaluators must deal with policy overlap from other federal, state, and local policies that can interact with the TIF (e.g., zoning policy, other tax policy, and enterprise/EMZs).

A large literature has emerged on the economic development impact of TIFs. In the most comprehensive review to date, Merriman (2018) offered the most recent review of 31 empirical studies of TIFs occurring between 1994 and 2017. Most of the reviewed studies used data generated pre-2000, although a few of the newer studies used data up to 2013. Merriman (2018) offered the following summary judgement of the empirical TIF literature: 42 percent of the studies—13 total—have positive results. Of the remaining 18 studies, 5 have negative results, 8 have neutral results, and 5 have mixed results. The neutral results suggest that TIF did little or nothing to stimulate economic development, so these studies might be viewed as an argument against the use of TIF. . . . the most recent studies, which tend to have the strongest data and best methodologies, are much less positive than earlier studies. Taken together, this review of the rigorous evaluation literature suggests that in most cases, TIF has not accomplished the goal of promoting economic development. (p. 52)

Merriman (2018) suggested there is evidence that TIF has positive effects in some cases, although this does not seem to be a function of location as even studies of the same TIF locations produce mixed findings.

Greenbaum and Landers (2014) also offered a review of the economic development effects of TIF. This older review of the empirical work on TIFs does not include studies published after 2014, excluding many of the studies that Merriman (2018) found to be the most credible and that have the least positive findings. Given this exclusion of the newer empirical work, it is not surprising that Greenbaum and Landers (2014) found the literature on TIFs to be more positive. Greenbaum and Landers (2014) suggested that “the majority of the studies find evidence of some positive associations between TIF districts and growth in property values” (p. 661) but that, “papers examining economic development outcomes finds less clear evidence of positive associations with TIF” (p. 662). Most of the studies categorized as studying economic development focused on employment as the outcome.

The vast empirical literature exists on the economic development effects of TIF broadly points toward a case that it is not an effective economic redevelopment tool; however, it seems reasonable to call for improvements in the existing empirical work before making a final judgement. The continued advance of quasi-experimental methods, especially the synthetic control method, offer a way to improve the construction of a counterfactual for what would have happened in TIF areas in the absence of TIF that would offer unbiased estimates of economic development effects. The end of TIF in California offers a large-scale change to the use of TIF that could also be useful in constructing empirical work using a natural experiment. 20

Business Improvement Districts

Designing special property tax districts with the goal of economic development is not unique to TIFs. Another increasingly common policy is BIDs. A BID is a locally formed collection of business operators and property owners that vote to levy a tax on themselves and use the proceeds for provision of local public goods. 21 The exact process of forming a BID differs across areas, but the idea that a BID creates a new tax (and spending) jurisdiction based on geography is the common characteristic. 22 BIDs differ from TIFs in that they are typically smaller in scale, do not typically take on debt, and they do not directly divert revenues that would be collected by the regular property tax.

Empirical work on the economic development effects of BIDs is extremely thin, consisting of only a few studies—two that estimated the effect of BIDs on property values, Ellen et al. (2007) and Brooks and Strange (2011), and another on local criminal activity (Brooks, 2008). One reason the empirical literature on the economic development effects of BIDs may be sparse is that it began to emerge as the level of sophistication in empirical work was rising rapidly, allowing researchers to predict the shortcomings of using standard methods. Estimating the effects of BIDs on economic outcomes comes with the standard problems encountered in the general property tax and TIF literatures, with the added complication that BIDs are voluntary; so by definition they are endogenously formed (because they are the result of voting by local businesses that demand public service improvements and corresponding taxes).

With the challenges to estimating the effects of BIDs in mind, Ellen et al. (2007) examined the effect of BID adoption in New York City on both commercial and residential property values using a difference-in-differences approach. Results of the study showed that BID implementation in New York City is associated with a 15.7 percentage point increase in commercial property values, 23 and that the effect on residential property values was likely small, short lived, and largely driven by the anticipation effects of the BID.

As part of a larger theoretical and empirical investigation into multiple aspects of BIDs, Brooks and Strange (2011) also estimated the effect of BIDs on commercial property values. 24 The study controlled for neighborhood by year to absorb time-varying neighborhood heterogeneity (an improvement over standard difference-in-differences estimation), and compared properties in BIDs with properties in three different comparison areas—places that were almost BIDs, places that are within 1 kilometer of a BID, and a sample that is propensity score matched to be the most similar to BIDs. Brooks and Strange (2011) found that, relative to areas that were almost BIDs, commercial properties increased in BIDs by 25%, on average, across all sizes of property, and that this effect was completely driven by properties in the top half of the square footage distribution. The propensity score estimated effect largely confirms this pattern, although the magnitudes of the property value increase are slightly smaller.

The property value increases documented from BID adoption imply they are effectively delivering the local public services they promise at an acceptable value for participants. Evidence that this is in fact the case comes from Brooks (2008), in her study of BID adoption and criminal activity in Los Angeles. Brooks used a variety of strategies to control for both neighborhood and time-varying effects, as well as matching to an appropriate comparison area to estimate the effects of BID adoption on crime. Her results showed that BIDs are quite effective at reducing crime, that adoption came with a 6% to 10% reduction in crime, and that this was robust across the various specifications. Brooks also calculated that even in the case that BIDs are only spending on crime reduction (an extreme case), they reduced violent crimes in a cost-effective way (the cost of reducing crime is lower than the social benefit).

BIDs and the empirical work on them to date are interesting because they both mirror the property tax in important ways. Like the property tax, BIDs are meant to finance valuable local public services. Like the empirical work on the property tax, the empirical work on BIDs shows that the services provided are valuable to those that consume them—when tax collection is in line with service provision the public is satisfied; when it is out of line, adjustments are made in the form of mobility or price capitalization.

Conclusions From Property Tax and Related Literature

Property taxes and tax concessions tend to be fully capitalized into property values. The literature that best divorces pure property tax effects from public service contributions all shows complete, near complete, or in one case overcapitalization. However, limiting property taxes that pay for valuable public services causes property value declines: The literature shows that it is not merely lower taxes that matter—citizens demand value and efficiency in public service provision. This literature should continue to follow the trend of outstanding contributions of the last 10 years and use natural experiments in property tax changes and related policies to identify the effects of the property tax across areas with different market characteristics and to examine outcomes related to capitalization, like mobility and building activity.

The empirical literature that exists on the economic development effects of TIF broadly points toward a conclusion that TIF is not an effective economic redevelopment tool. This literature is less developed than the general property tax literature, and it seems reasonable to call for improvements in existing empirical work before making a final judgement on the general idea of TIFs. The literature on BIDs is much more positive than the literature on TIFs, although it relies on only a few high-quality studies. Like the empirical work on the property tax, the empirical work on BIDs shows that the public services provided are valuable to those that consume them—when tax collection is in line with service provision the public is satisfied, when it is out of line adjustments are made in the form of mobility or price capitalization.

Spatially Targeted and Zone-Based Tax Concessions

Zone-based tax concessions are part of a broader set of place-based policies intended for redevelopment of poor or blighted (mostly urban) areas. Much like TIFs, a zone is typically carved out of an area from an existing jurisdiction to be given preferential treatment. 25 Unlike TIFs, zones are typically paid for out of general revenues and typically this funding comes from a higher level of government (e.g., the U.S. federal government funds local zones in cities). Another distinguishing characteristic of zones is that, while they are geographically distinct areas, these areas are typically chosen because of the characteristics (e.g., poverty rates, unemployment, income) of the people that live in the area (Neumark & Simpson, 2015). Zones also typically include other types of area-based assistance outside of tax concessions, such as grants, infrastructure spending, and offering social services to residents.

Peters and Fisher (2002) reviewed the early empirical literature on zones, focusing on U.S. state programs. In summarizing the state of the literature at that time, Peters and Fisher (2002) concluded: Given the paucity of enterprise zone studies, it seems highly unlikely that a broad research consensus on the impact of enterprise zones on growth will be possible for some time to come. The conclusions of the extant literature do point in quite contrary directions; however, the vast majority of the recent literature suggest that enterprise zones have little or no positive impact on growth. (p. 48)

The papers discussed by Peters and Fisher (2002) were all published in or before 2000, and none of them examined the larger-scale zone programs (California’s enterprise zones [EZs] or the federal EMZ). Since the Peters and Fisher (2002) review, there has been a plethora of studies examining the economic development effects of zone-based policy. Many of these studies employ the rigorous quasi-experimental research methods that have become common in the program evaluation literature.

Neumark and Simpson (2015) provided an extensive review of the modern literature on zone-based incentives, focusing on studies based in the United States and Europe, and highlighted several studies of large state programs and the federal program. Neumark and Simpson have a pointed discussion of the California EZ program, focusing on the contribution of Neumark and Kolko (2010),

26

where they summarized the results as follows: Across a variety of specifications, there is no evidence that enterprise zones affect employment. The estimates are small, statistically insignificant, and negative as often as they are positive. The statistical power of the evidence is modest, as the confidence intervals for the estimated employment effects are rather large . . . estimates do not exhibit any evidence of leading or lagged effects, but instead cement the view that enterprise zones in California did not affect employment . . . in the analysis accounting for the overlap between state enterprise zones and redevelopment areas or federal zones, there is similarly no evidence that enterprise zones have positive employment effects, whether or not they are combined with these other local policies. (p. 31)

The most rigorous evaluations of other state EZs come from studies of the Colorado (Billings, 2009) and Texas (Freedman, 2013) programs. Each of these studies used a quasi-experimental approach in estimating the impact of a state program, with Billings (2009) using a border-matching approach and Freedman (2013) using a regression discontinuity approach. There are also studies that used conditional difference-in-differences estimation to estimate the effects of state EZ programs. Rogers and Tao (2004) compared treated areas with qualified areas in Florida, and Bondonio and Greenbaum (2007) conditioned on a propensity score (the probability of becoming treated) combining programs across several U.S. states.

Billings (2009) matched business establishments in EZ areas with establishments outside of EZ areas, using a sample where both are close to the border of the zone. This matching is intended to produce a set of control establishments that is the most similar to actually EZ-treated establishments, and that is subject to the most similar local economy but does not receive a preferred tax treatment. Billings found that the Colorado EZ tax credits have no influence on business establishment location, meaning that new businesses are not more likely to start in the zone area than they are in the comparison area. Billings found that employment at new establishments increased by between 1.5 and 1.75 employees as a result of the EZ tax credits, but most results showed no effect at existing establishments.

In an extremely compelling study, Freedman (2013) used a regression discontinuity design to estimate the effect of the Texas EZ program on various economic development outcomes. Freedman’s empirical work relied on the rules for how an area qualifies for EZ status to help identify the effect of the program independent of other factors. Census blocks in Texas were automatically assigned to be EZ areas if they had a poverty rate higher than 20%. Freeman used the automatic assignment of blocks than happens at 20% and the fact that blocks within a small bandwidth of 20% are observably similar to estimate the effects of the program. Freedman found that the annual growth rate for residents of EZ areas is 1% to 2% higher than areas that were just short of the poverty-qualifying threshold, resulting in 35 to 42 resident jobs during the time of the program.

27

Freedman also documented a slight increase in EZ population, reductions in poverty, and greater house price appreciation using the regression discontinuity design. In concluding what his results implied about EZ programs, Freedman (2013) suggested the following caveats: . . . the EZ program in Texas is different from those of most other states, where in general localities must apply for EZ status . . . it would be misguided to assume that if one were to expand EZ coverage to include more affluent communities, it would have similar effects in those areas. . . . finding positive effects of the program does not immediately imply that it is cost- effective. . . . of the jobs created or preserved are lower- paying positions. This, combined with cost- of- living increases in EZs, would tend to erode any improvement in overall welfare owing to the program. (p. 342)

Freedman’s caveats point out that even for a compelling empirical study the link between results of an existing program and future policy is difficult to make. One potential way to improve on the viability of using empirical results to inform economic development policy is to examine a program that has uniform benefits but reaches a wide range of areas. One such program is the federal EMZ program.

The federal EMZ program is based on the zone concept—offering a series of tax incentives to employers locating in designated areas. Unlike state programs, the benefits of the federal program are largely uniform and designated areas exist across state boundaries. This offers the advantage of studying a similar set of incentives across a group of treated areas that is heterogenous. The federal EMZ program offered a wage tax credit based on employee and employer location within a designated area in the following cities: Atlanta, Baltimore, Chicago, Detroit, New York, Philadelphia, and Camden. EMZs were also given an allotment of Social Services Block Grants and some smaller tax incentives for capital investment. See Hanson (2009) for full details about EMZ designation and incentives.

There are several studies of the federal EMZ program including Hanson (2009), Hanson and Rohlin (2011a), Hanson and Rohlin (2011b), Hanson and Rohlin (2013), Busso et al. (2013), and Reynolds and Rohlin (2015). Hanson (2009) and Busso et al. (2013) studied the primary effects of the EMZ program on several economic development outcomes, while the other studies examined aspects like differential effects across the income distribution and by business type, and spillover effects. There is also work by Ham et al. (2011) that examined both the federal EMZ and state EZ programs simultaneously.

The Hanson (2009) and Busso et al. (2013) studies used different methodologies to study the federal EMZ and came to different conclusions about the effects of the program. Busso et al. (2013) compared the outcomes for EMZ-designated areas with outcomes in places that applied for EMZ status but were rejected and places that later became EMZ areas using a difference-in-differences design. The primary results from Busso et al. (2013) suggested a substantial positive effect of the EMZ program—a statistically significant 21% increase in jobs in EMZ neighborhoods. Using an alternative data set that allowed the researchers to distinguish between place of residence and place of work, Busso et al. (2013) found that most of the job growth was concentrated among residents of EMZ areas (although the effect is not precise). In addition to employment effects, Busso et al. (2013) also estimated a 12% increase in wages for residents living in the EMZ and a 30% increase in residential housing values (although this effect is not precise in the preferred specification). In concluding about the results of their work, Busso et al. (2013) suggested, The conclusion of our welfare analysis is that the EZ program appears to have successfully transferred income to a small spatially concentrated labor force with modest deadweight losses aside from the usual cost of raising the funds for the subsidy itself. We caution however that our study provides only a short run evaluation of the EZ program. . . . The responses of firms, population, and prices may well differ substantially over longer periods of time, if EZ subsidies in fact persist over such horizons. . . . Finally, we emphasize that many of our empirical results are imprecise and should not necessarily be expected to generalize to later round and future zones. Additional zones targeting less heavily distressed communities may yield larger distortions as such communities may be closer substitutes with surrounding areas. . . . While we find it plausible that the mix of large block grants and wage credits accompanying EZs would yield different results than their smaller state level predecessors, more work is necessary to disentangle the effectiveness of various combinations of spatial subsidies.” (p. 931)

Hanson (2009) used a different methodology and different data than Busso et al. (2013) to study the federal EMZ program. Noting the potential for an EMZ evaluation to be biased due to selection of treated zones from a pool of applicants, Hanson (2009) implemented an instrumental variables strategy, using membership and tenure on the House of Representatives Ways and Means committee as a source of variation driving EMZ selection. Along with instrumenting, Hanson (2009) also implemented a triple-difference estimation strategy, comparing EMZ areas and their larger city with the change in applicant areas and their larger city. The primary assumption behind this strategy was that Ways and Means membership and tenure do not directly influence local economic outcomes except through EMZ designation. Hanson (2009) presented evidence that this assumption might be valid. The findings in Hanson (2009) suggested no effect of the EMZ program on resident employment of poverty rates, but a large effect on residential property values—increasing them by $100,000 over the course of a decade.

Other research examining the federal EMZ suggested that impoverished residents did not benefit from the program and that the areas became more attractive to higher income residents, with most of the benefits accruing to neighborhoods in EMZ that were relatively more attractive prior to designation (Reynolds & Rohlin, 2015). Hanson and Rohlin (2011b) presented evidence that the EMZ program had a differential affect across firms in different sectors of the economy, with the share of firms in service and retail increasing at the expense of firms in transportation, finance, insurance, and real estate. Hanson and Rohlin (2011a) suggested that new firms enter the EMZ area, but that the magnitude of this effect is small—only about 20 new firms enter EMZ areas and at a cost of entry of $19 million per firm. Hanson and Rohlin (2013) examined the potential for the EMZ program to induce a spillover effect on surrounding neighborhoods (or economically similar neighborhoods). Hanson and Rohlin (2013) found that areas adjacent to or economically similar to EMZ areas experienced a loss of both firms and employment, with the magnitude of the loss roughly equivalent to estimated gains in the zone.

Non-U.S. Studies of Zone-Based Policies

Although the focus of this review is on U.S.-based studies, there is a high concentration of compelling work on zones that examines the French EZ program (Zones Franches Urbaines or ZFU). The French ZFU program exempts firms from paying the wage tax if they hire 20% of their labor force locally from the designated area (Gobillon et al., 2012). Gobillon et al. (2012) estimated that the ZFU program had a small, modest effect on the probability of an unemployed resident obtaining a job. Their preferred specification suggested that the ZFU program was responsible for 10 new transitions between being unemployed and finding work. Briant et al. (2015) studied how the ZFU program may have interacted with the local geography, examining whether there is a differential effect across areas by their degree of spatial isolation. Using a difference-in-differences research design Briant et al. (2015) found that the ZFU program increased the inflow of business establishments by 16% in less-isolated areas, while there was no measurable effect on the most-isolated areas.

Contrary to the small findings in Gobillon et al. (2012), follow-up work by Mayer et al. (2017) found that ZFUs have a substantial effect on employment, increasing employment by 24%. Mayer et al. also found that ZFUs are responsible for increases in firm entry, but that this is largely caused by diversion of firms from neighboring unsubsidized areas. While the estimated effects on employment are large, it is unclear what the net effects of the ZFU policy would be, considering the diversion of firms from neighboring areas. In the most recent work on ZFUs, Gobillon and Magnac (2016) implemented an evaluation of the ZFU program using the synthetic control method. This method is particularly attractive for the study of zone-based policies as it largely eliminates the concern of finding a comparison area with a parallel trend prior to policy implementation. Synthetic control estimates of the effect of the ZFU program on unemployment are much less precise than the small positive effects estimated in Gobillon et al. (2012), and are in fact of the opposite sign, casting doubt on the previous findings.

Conclusions From the Spatially Targeted and Zone-Based Literature

Overall, the best description of the empirical findings in the zone-based literature is “mixed.” It seems that for every positive finding for a particular program, there is an offsetting null or negative finding. These differences come despite the ever-increasing sophistication of empirical methodology to address bias in estimation. In summarizing the literature on zone-style policies, Neumark and Simpson (2015) came to a similar conclusion, stating the following: . . . it is very hard to make the case that the research establishes the effectiveness of enterprise zones in terms of job creation or welfare gains, although there clearly are some studies pointing to positive effects. Further progress requires effort to figure out what features of these programs can make them more effective, following on some early efforts in this direction in the existing research. Second, although there has been a slew of new studies in the past few years—and even many studies focusing on the same program—there has not been enough of an attempt to reconcile the disparate evidence. This kind of careful, often painstaking work may well help sharpen the findings from a research literature in which the findings remain rather disparate. (p. 46)

It seems the most appropriate conclusion to draw from the empirical research on zone-based policies is that more research needs to be done.

Firm-Specific Subsidies and Corporate Taxes

Tax incentives for economic development seem to be increasingly focused on the attraction of a single large firm. With each passing year, the popular press reports on a new firm (or firms) that localities are attempting to entice locate (or stay) in their district. Recent examples include Amazon’s HQ2, Foxconn, Boeing, Alcoa, and Intel, among many others. Mattera and Tarczynska (2013) estimated that state and local governments have spent $64 billion on incentive packages over the past 35 years. The academic literature on large-scale, firm-specific subsidies and tax breaks is shockingly thin, despite the attention these incentives receive in the press and the dollars that are spent on them.

In a recent review of literature on state and local economic development incentives, Bartik (2018) categorized 34 studies to determine the percentage of incentivized firms that were induced to make a location, expansion, or retention decision because of the incentive program. Bartik (2018) examined a wide range of policies including grants, payroll credits, property tax abatements, sales tax credits, and wage credits. In determining an appropriate response to use for his summary, Bartik carefully classified each study by the likely bias in the estimation. This is an interesting exercise in its own right, as it sheds light on the state of the literature. Bartik (2018) suggested that of the 34 studies, only 7 have no obvious bias (23 are bias toward a positive finding and 4 biased toward a negative finding). Across the studies that Bartik (2018, abstract) examined, he concluded that “typical incentives probably tip somewhere between 2 percent and 25 percent of incented firms toward making a decision favoring the location providing the incentive.”

There are two recent studies of large-scale, firm-specific subsidies that use quasi-experimental or natural experiment methods: Greenstone et al. (2010) and Patrick (2016). 28 Both of these studies estimated the effect of a large new manufacturing facility using a sample of plant relocations between 1982 and 1993 from the magazine Site Selection. Importantly, this is a select sample, both in terms of the type of business being relocated (manufacturing), the period chosen, and the fact that the relocation was covered by an international media outlet. Both studies used a difference-in-differences methodology, with the primary difference between them being how the researchers constructed a counterfactual for what would have happened in the area where the subsidized firm relocates. In both cases, this is done through the choice of comparison areas. In the Greenstone et al. (2010) case, they relied on comparing winning areas to areas that were runners-up in the competition to land the new firm. In the Patrick (2016) case, a comparison group was intentionally constructed by matching to geographically close areas that have similar observable characteristics as the winning area.

Greenstone et al. (2010) generally found large positive effects of the relocating facility on the local economy. Their primary estimates suggested that productivity at surrounding facilities increased by 12% after 5 years, with larger effects at facilities that share labor and technology characteristics. In addition to positive effects on the productivity of surrounding workers, Greenstone et al. (2010) also estimated positive effects on other firms entering the area (an increase of 12.5%) and on worker wages (an increase of 2.7%).

Importantly, although Greenstone et al. (2010) estimated a large average effect on the surrounding facilities, they also pointed out that for individual plants the effect varied substantially. Showing a series of case studies, Greenstone et al. found that the average effect at 18 of the 45 facilities was to decrease productivity at surrounding plants, while the average effect at another 12 of the 45 was statistically indistinguishable from zero. Thus, the large positive effect in the aggregate is driven by positive effects at only 25 of the 45 plants, and among those only 13 had positive effects that were statistically significant at conventional levels.

In a compelling counterweight to the results presented in Greenstone et al. (2010), Patrick (2016) made the case that using runner-up areas to construct a counterfactual for areas where plants locate will cause biased results. Patrick (2016) demonstrated that pretreatment outcomes and covariates differ greatly across the comparison and treatment areas used by Greenstone et al., potentially causing bias. Patrick (2016) also pointed out that the institutional features of the process for reporting runner-up areas in the Site Selection publication may induce bias. Finally, Patrick (2016) investigated the possibility that Site Selection misidentified the correct runner-up location and found evidence that it did so in only 2 of 9 cases.

After documenting that the Greenstone et al. (2010) identification strategy may suffer from severe flaws, Patrick (2016) outlined an alternative estimation strategy. Her primary estimates relied on matching places that had similar population, highway access, proximity to a metropolitan area, working-age population, and earnings, and were in geographic proximity to the actual firm location. Patrick presented evidence that her matched sample of comparison areas closely resembled the sample of locations where firms actually choose to locate. Patrick essentially found the opposite effects found in Greenstone et al. demonstrating that, if anything, large subsidized firms relocating to an area have a negative effect on the number of other business establishments (most specifications report a finding close to zero). Patrick also found a much smaller effect on surrounding firms that are operating, showing only a 1% to 4% increased subsidized area manufacturing output. Despite these negative findings, Patrick did find substantial wage gains (2.6% to 3.5%) and employment gains (3% to 5%) for residents where large firms relocate, although these estimates included gains from the subsidized firm. Finally, Patrick also found that places where a heavily subsidized new firm relocates have increased taxes and levels of government debt.

Corporate Income Taxes

In addition to firm-specific incentives and targeting by geography, lowering corporate tax rates or offering investment incentives to all firms can be used to induce economic activity. There is a fairly large body of evidence on the effect of corporate taxes (and nontargeted investment incentives), and much of it is designed around modern natural or quasi-experimental estimation strategy. I review some of the more recent and most compelling evidence here as a basis to compare broad corporate tax policy with the more targeted approaches already discussed.

Studies on the economic development effects of corporate tax policy can be broken into two broad categories—those that examine rates and those that examine special incentives (such as bonus depreciation). The most compelling studies that examined corporate tax rates used variation in U.S. state rates: Ljungqvist and Smolyansky (2014) and Rohlin et al. (2014). Of the studies that examined special incentives, three examined bonus depreciation—House and Shapiro (2008), Zwick and Mahon (2017), Garrett et al. (2019)—and the other examined the domestic production activities deduction (DPAD) —Ohrn (2018).

Ljungqvist and Smolyansky (2014) examined the effect of corporate tax rates on employment applying the border method using data on resident-based employment and incomes. Ljungqvist and Smolyansky compared counties that straddle state borders where corporate tax policy changes on one side and not the other. They examined 271 corporate tax changes over 1970 to 2010. The border approach allows the researchers tight control over other changes to the local economy that may be prompting corporate tax changes, limiting concerns of endogeneity bias in estimation. Ljungqvist and Smolyansky found that a 1 percentage point increase in the top marginal corporate tax rate reduced employment by 0.3% to 0.5%. They also pointed out that corporate tax changes are not symmetric; that is, they did not find employment effects from cutting the top marginal corporate tax rate unless that change happened during a recession. Along with employment changes, Ljungqvist and Smolyansky also demonstrated that a 1 percentage point increase in the top marginal corporate tax rate resulted in an income decline of 0.3% to 0.6% (but that cutting corporate taxes does not have a corresponding positive effect unless that policy happens during a recession).

Using data on business location and employment, Rohlin et al. (2014) also used the border method to examine state corporate tax rates. Rohlin et al. examined how corporate tax rates affect the propensity for a business to open on either side of the border when one state changes policy. To bolster the link between policy and the outcome of interest, the researchers examined borders that have a reciprocal tax agreement so that both sides of the border are likely to have a labor market that is common. Using this strategy, Rohlin et al. found that a 1 percentage point increase in the top marginal corporate tax rate reduces the likelihood of a business starting by 34%, with larger effects in the manufacturing and service sectors.

Most of the studies that examined special corporate incentives focused on their effects on business investment, with Garrett et al. (2019) making the link between business investment and employment. All of these studies examined the U.S. aggregate economy, although some of them looked at effects across industry and size of firm. House and Shapiro (2008) used the 2002 and 2003 implementation of bonus depreciation to study the effect of lowering the effective capital tax on investment. 29 They found a strong investment response to bonus depreciation that implies an elasticity between 6 and 14. Zwick and Mahon (2017) extended the analysis in House and Shapiro to include later years of policy and examined the effect by size of firm. Zwick and Mahon also found a significantly large effect of bonus depreciation: It increased investment between 10.4% and 16.9% (depending on the year of the policy experiment). They also found that small firms respond more strongly to the policy than large firms. Ohrn (2018) examined the investment response from the DPAD, a policy that allows firms to deduct some of their manufacturing income from regular taxable income. Ohrn used the implementation of the DPAD in 2005 as a natural experiment in a difference-in-differences framework to study the effects on investment. He found that a DPAD-induced 1 percentage point reduction in the corporate tax rate increases investment by 4.7%.