Abstract

One of the most pressing health issues in the United States is the persistent association between socioeconomic status (SES) and mental health. Individuals who are materially advantaged by their education, employment, annual income and wealth usually live longer, happier lives in this country than those with fewer material resources. The importance of this disparity has been a major push of the governmental program Healthy People 2010 (U.S. Department of Health and Human Services, 2000), which highlights SES as a major source for understanding health disparities. The key to such understanding is an adequate accounting of the resources that individuals and families may draw on to support their health statuses, as well as their concurrent financial liabilities.

This article contributes to the literature on SES and its association with mental health. It includes traditional measures of SES, including education, income and occupation, and adds often-called-for measures of wealth and assets. However, it is distinct in its attention to debt, which is notably absent from the usual range of indicators of socioeconomic position (Galobardes, Shaw, Lawlor, Lynch, & Davey Smith, 2006). All of these measures of SES lead to a better understanding of the fundamental social causes of disease (Link & Phelan, 1995). Unlike more proximate causes of problems with mental health, some dimensions of SES (such as income and wealth) have a lasting effect that serves as a resource or buffer against life’s hardships. Conversely, being in debt is a potential stressor that weakens one’s ability to deal with the stress at hand, and limits one’s ability over time to address a situation (Link & Phelan, 1995; Pearlin, 1989; compare Dwyer et al., 2011). Moreover, resources such as income accumulate over time; whereas, stressors related to debt could lead to cumulative disadvantage (Dannefer, 2003; Ferraro & Shippee, 2009). Focusing on mental health, our research reveals the unique significance of being in debt. The negative association between debt and mental health also holds up after accounting for early health problems and mental health two years past, reducing the possibility that these results are artifacts of social selection or “drift” processes (Dohrenwend et al., 1992).

The analyses consider three aspects of mental health that are plausibly associated with debt and other indicators of SES. Depression and anxiety represent internalizing affective responses to indebtedness or low SES. Owing money or possessing few economic resources can lead to concerns about the future, uncertainty, and worry. Adults may alternatively respond to such situations through externalizing behaviors, such as irritability and conflict with others, and a general state of anger. A great deal of research documents the association between SES and depressive symptoms, but there is less on anxiety or anger (Drentea, 2000; Collett & Lizardo, 2010; Schieman, 2003). As all of these SES measures accrue over life, whether it is in terms of cumulative advantage or disadvantage, we certainly expect to find relationships with depressive symptomatology and anxiety in this sample of older adults. We are not as sure about anger, which may be more sensitive to proximate causes, and may be more common in a younger, as compared to an older, sample. However, we wanted to test multiple SES measures with multiple mental health outcomes, in keeping with the fact that neither SES measures nor mental health measures are interchangeable (Horwitz, 2002; Lahelma, Laaksonen, Martikainen, Rahkonen, & Sarlio-Lähteenkorva, 2006).

The findings suggest that assessing the mental health significance of SES or socioeconomic position is incomplete when there is no consideration of debtor status. Research such as this is important both for the sake of better accounting for individuals’ socioeconomic position in society, and also because of growing wealth disparities and rising levels of debt (Blank & Barr, 2009; Pollack et al., 2007; U.S. Census Bureau, 2005, table 678). As consumer debt continues to rise in the U.S. (Garcia, 2007; Ritzer, 1995; Sullivan, 2009), it seems warranted to conclude that there an increasing need for health scholars to incorporate debt in the study of the SES health gradient.

SES, Wealth, Debt, and Mental Health

Overall, those with higher levels of SES have better mental health (Amone-P’olak et al., 2009; Cockerham, 2006; Laaksonen et al., 2009; Lahelma et al., 2006; Mirowsky & Ross, 2003b). Looking separately at the traditional components of SES, each aspect contributes to the association with mental health, though not equally. Education is arguably the most important source of the association, partly because additional education is linked to better pay and employment conditions (Mirowsky & Ross, 2003a). Income and occupational status also are independently associated with mental health in most studies, and the effects of very low income and economic hardship appear to be large and enduring (Laaksonen et al., 2009; Pudrovska, Schieman, Pearlin, & Nguyen, 2005; Reynolds & Ross, 1998).

Despite the significance of SES differences in mental health for social research and public policy, researchers increasingly recognize the limits of past efforts to measure the association. In particular, recent scholarship has exposed the inadequacy of traditional measures of SES (Lahelma et al., 2006; Shavers, 2007) and the need to include wealth (Braveman et al., 2005; Conley, 1999; Laaksonen, Rahkonen, Marikainen, & Lahelma, 2005; Pollack et al., 2007). Wealth potentially affords many indirect mental health advantages, ranging from its role as a buffer against sudden financial disruptions to the significance of wealth for residential options, health lifestyles (organic foods, health club memberships, etc.), and socially advantageous networks (Cockerham, 2005; Conley, 1999). It allows individuals to live in comfort and to insulate themselves from the hardships of the broader world (Keister, 2000).

A similar case can be made that the full significance of SES for mental health cannot be adequately measured without accounting for debt. Like wealth, debt is unevenly distributed and socially patterned. Debt levels are higher among younger adults, women, and middle income as compared to lower income households (Drentea, 2000; Drentea & Lavrakas, 2000; Princeton Survey Research Associates International, 2008; Keister, 2000; McCloud & Dwyer, 2011; Sullivan, Warren, & Westbrook, 2000). Debt varies by race/ethnicity, too, though the direction of the difference depends on whether one considers access to credit, debt levels, type of debt, or risk of defaulting (e.g., Garcia, 2007; Gray, 1997).

Excessive debt is in part harmful to psychological well-being because it wears away at one’s mental health. Debt and the stress surrounding debt have been found to be negatively associated with physical health (Drentea & Lavrakas, 2000; Munster, Ruger, Ochsmann, Letzel, & Toschke, 2009; O’Neill, Prawitz, Sorhaindo, Kim, & Garman, 2006), as well as mental health including anxiety and depression (Brown, Taylor, & Price, 2005; Drentea, 2000; Jacoby, 2002; Reading & Reynolds, 2001; Roberts, Golding, Towell, & Weinreb, 1999). In small sample studies, debt is associated with self destructiveness and self poisoning (Hatcher, 1994; Meltzer et al., 2011; Politano & Lester, 1997). Indebtedness has negative mental health consequences for various reasons, possibly including the perception of not being able to get out of debt or the potential shame and anxiety resulting from defaulting on loans or declaring personal bankruptcy (Manning, 2000; Sullivan et al., 2000). Carrying heavy debt loads and being called by collectors are considered stressful for most people (Princeton Survey Research Associates International, 2008).

In our study, debt is measured by whether someone has any debt. We consider debt as different from economic hardship—i.e., difficulty in meeting expenses. Those with hardship may accrue debt, but they also may not have any access to borrowing (Blank & Barr, 2009). Economic hardship is consistently associated with greater psychological distress, but indebtedness is not always so. Recently, Dwyer et al. (2011) reported that among some young adults taking on debt is positively associated with mastery or self-esteem. They argue that this may reflect their view of debt as an investment in pursuit of middle class status, rather than a burden. Thus, debt may be viewed positively as a tool in some cases, but we assume debt is stressful for older adults.

In the older and diverse sample we examine, we expect that debt will be associated with worse mental health on average.

Hypothesis 1: Being in debt will be associated with higher depressive symptomatology, anxiety and anger, controlling for traditional indicators of SES and wealth.

In addition, we assess whether the deleterious consequences of indebtedness vary according to the apparent ability to pay off debts.

Hypothesis 2: The positive association between debt and depressive symptomatology, anxiety, and anger will be greatest among those with the fewest assets.

Our research also improves on previous work in that we account for the possibility of social drift/selection. Although others have addressed causal order issues for some aspects of the SES and health gradient (e.g., Dohrenwend et al., 1992; Ross & Mirowsky, 1995), with few exceptions (Dwyer et al., 2011), extant research on debt and mental health has not been able to do this (e.g., Drentea, 2000). Thus, it is still unclear whether debt leads to poor mental health outcomes, or whether those with poor mental health are more likely to take on debt. Depressed, anxious, or anger-prone individuals may be more impulsive or overspend as a way to boost esteem or placate their problems and frustrations (Bauman, 1998; Bauman, 2001; Baumeister, 2002). We posit the opposite in the following hypothesis:

Hypothesis 3: Even after controlling for earlier mental health, debt will still have an effect on current mental health outcomes, indicating that the association between concurrent debt and mental health is not due to indebtedness caused by prior mental health problems.

Data and Method

Sample

The analyses use the Miami Disability Study, a two-wave panel study of Miami-Dade county residents of adults with and without physical disability. Ten thousand randomly selected households were screened with respect to age, sex, ethnicity, disability status, and language. The sampling frame was stratified to have even numbers of women and men, even numbers of those people screened as having a physical disability and those without a disability, and even numbers of Cubans, other Hispanics, African Americans, and non-Hispanic Whites. Computer-assisted interviews were completed in English or Spanish based on the respondent’s preference. A total of 1,986 first wave interviews were completed in 2000-2001 (success rate = 82%). Follow-up interviews were conducted approximately 2 years later (n = 1,513). We assess the association between debt and mental health in the follow-up interviews, controlling for baseline mental health using identical measures in the first wave of interviews. The analytic sample in this article is made up of 1,463 respondents. The oversampling of individuals with physical disabilities resulted in a greater proportion of older individuals than in the general population. The median age in the first wave sample was 59, compared to 35.6 years for the Miami-county population as a whole in 2000, thus the sample consists of predominantly older Floridians. The descriptive statistics we report are weighted to account for the stratified survey design of the study. Descriptive statistics were generated using STATA’s “svy” estimation procedures that use Taylor linearization to adjust the variance estimates (StataCorp, 2009). 1

Missing data was somewhat of an issue for the items tapping income and assets (nonresponse rates of 6%, 8%, and 9% for personal income, household income, and assets, respectively), but not debt (less than 1% missing). To reduce the potential bias from item nonresponse, we used multiple imputation techniques available in Stata (Royston, 2004; StataCorp, 2009). The ICE command in Stata generated 5 data sets that substituted missing values on income, assets, and other predictors with values imputed from regressing each on all observed variables. The slope coefficients in Tables 3 and 4 are averaged coefficients from the 5 data sets. We also tested the models without the imputed data, thus losing 310 cases. Results were substantively similar, and as such, we used the models with imputed data.

Measures

Depressive symptomatology

The 20-item version of the Center for Epidemiologic Studies Depression Scale (CES-D; Radloff, 1977) was administered to assess recent symptoms of depression in both the first and second waves of the study. Study participants were asked how often in the past month they experienced feelings such as loneliness, sadness, and hopelessness. The response options included not at all, occasionally, frequently and almost all the time (coded 0 to 3, respectively). Depression is equal to the sum of scores across the 20 items (Cronbach’s α = .88), then converted to a standard scale to facilitate comparisons across the three measures of mental health outcomes.

Feelings of anxiety

Five items assessed recent feelings of anxiety. The respondents were asked to what extent in the past month they felt over excited, tense, anxious, or worried over possible misfortunes. Responses included none, somewhat, moderately, and very much (coded 0 through 3, respectively). The scale of anxiety equals the standardized sum of scores (Cronbach’s α = .87).

Anger

Six items assessed recent feelings and expressions of anger. The respondents were asked to what extent over the past month they felt they stay angry, yell at people, feel like they are boiling inside, lose their temper, feel angry and get into fights and arguments. Responses included 5 = very much like me, 4 = much like me, 3 = somewhat like me, 2 = not much like me, and 1 = and not like me at all (Cronbach’s α = .88). Responses to the items were summed and then standardized.

Debtor status, credit card debt

Respondents were asked if they had “any debts including credit cards, store credit, a mortgage or home equity loan, a car loan or any other loan?” A dummy variable identifies those with any debt (coded 1) versus those with no debt (coded 0). Those who reported any debt (around 60% of the wave 2 sample) where then asked, “On average, how much debt do you usually carry on your credit cards each month after you make your payments?” Credit card debt is the monthly balance in dollars.

Debt stress

Two items ask how often the respondents worries about the total amount of debt they owe, and whether they are concerned about never being able to pay it off (Drentea & Lavrakas, 2000). The two Likert-type items were correlated at r = .87, and were combined in a standardized scale where higher values indicate greater feelings of anxiety related to debt. Though correlated positively with depression, anxiety, and anger, a factor analysis confirmed that these two indicators of debt stress load uniquely on a separate factor.

Income

Respondents were asked to estimate their total personal income before taxes, choosing from among 16 categories: 0 = none, 1 = less than US $5,000, 2 = $5,000 - 9,999, 3 = $10,000 - 14,999, 4 = $15,000 - 19,999, 5 = $20,000 - 24,999, 6 = $25,000 - 34,999, 7 = $35,000 - 44,999, 8 = $45,000 - 54,999, 9 = $55,000 - 64,999, 10 = $65,000 - 74,999, 11 = $75,000 - 84,999, 12 = $85,000 - 94,999, 13 = $95,000 - 114,999, 14 = $115,000 - 134,999, and 15 = $135,000 and above. The analyses used this ordinal measure of household income as if it were interval-level data, plus a squared term to capture nonlinearity in its association with debt and mental health. We also conducted sensitivity analyses that instead used measures that (a) imputed values of income based on category midpoints, (b) treated income as a categorical measure with “less than US$5,000” as the reference category, and (c) used household income instead of personal income. These analyses yielded substantively similar results.

Assets

Respondents were asked, “Suppose you needed money quickly, and you cashed in all of your checking and savings accounts, your stocks and bonds and real estate (other than your home). If you added up what you got, about how much would this amount to?” The response options were eight ordinal categories ranging from 0 = less than US$10,000 to 7 = more than US$1,000,000. (Sensitivity analyses confirmed that similar results were obtained if dollar values based on category midpoints were analyzed instead).

Homeownership

We identify homeowners with a dichotomous dummy measure (1 = owns home), and include a self-reported estimate of the value of the home in which respondents were asked how much money they would get for their home if they sold it. The eight ordinal response options were the same as those for assets, and again we verified that using the ordinal measure was not affecting the overall findings. Respondents who were not homeowners were coded 0 on the measure of home value.

Education

Educational attainment is measured as the highest grade of school or year of college completed.

Occupational status

We used the Nam-Powers occupational SES index based on the respondents’ current or longest held occupation. Scores on the Nam-Powers index represent “the approximate percentage of persons in the labor force who are in occupations having combined average levels of education and income lower than the given occupation, as of the 1990 Census” (Nam, 2000, p. 12). The analyses also control for current employment status, contrasting those who were retired, unemployed, or not in the labor force for other reasons (in this sample, this often was due to disability status) to respondents who were employed.

Controls

The regression analyses control for differences in mental health attributable to age (M = 59.2), racial/ethnic status (30.3% African American, 46.0% Hispanic, and 23.7% White), gender (53.9% women), employment status (45.1% employed, 36.9% retired, 2.3% unemployed, and 15.7% out of labor force), health insurance coverage (81.7% with insurance), marital status (47.1% married), physical disability status (28.0% with disability), and presence of dependent children in the household (40.0% with 1 or more), all of which are potentially associated with mental health. Health insurance and employment status were included to better isolate the mental health consequences of debt, although they could also be seen as other aspects of SES. The analyses contrast Hispanic and black respondents to Whites. Cubans and other Hispanics were combined because there was no substantive difference between them for any of the analyses. Some models also control for earlier health problems and the lagged value of the dependent variable as assessed in the first wave of the study, around two years earlier. The measure of early health problems is a count of major health problems that occurred before age 26, including physical disability, retrospective diagnoses of childhood conduct disorder or attention deficit or hyperactivity disorder, or having experienced an onset before the age 26 of major depression, generalized anxiety, social phobia, or panic disorders.

Results

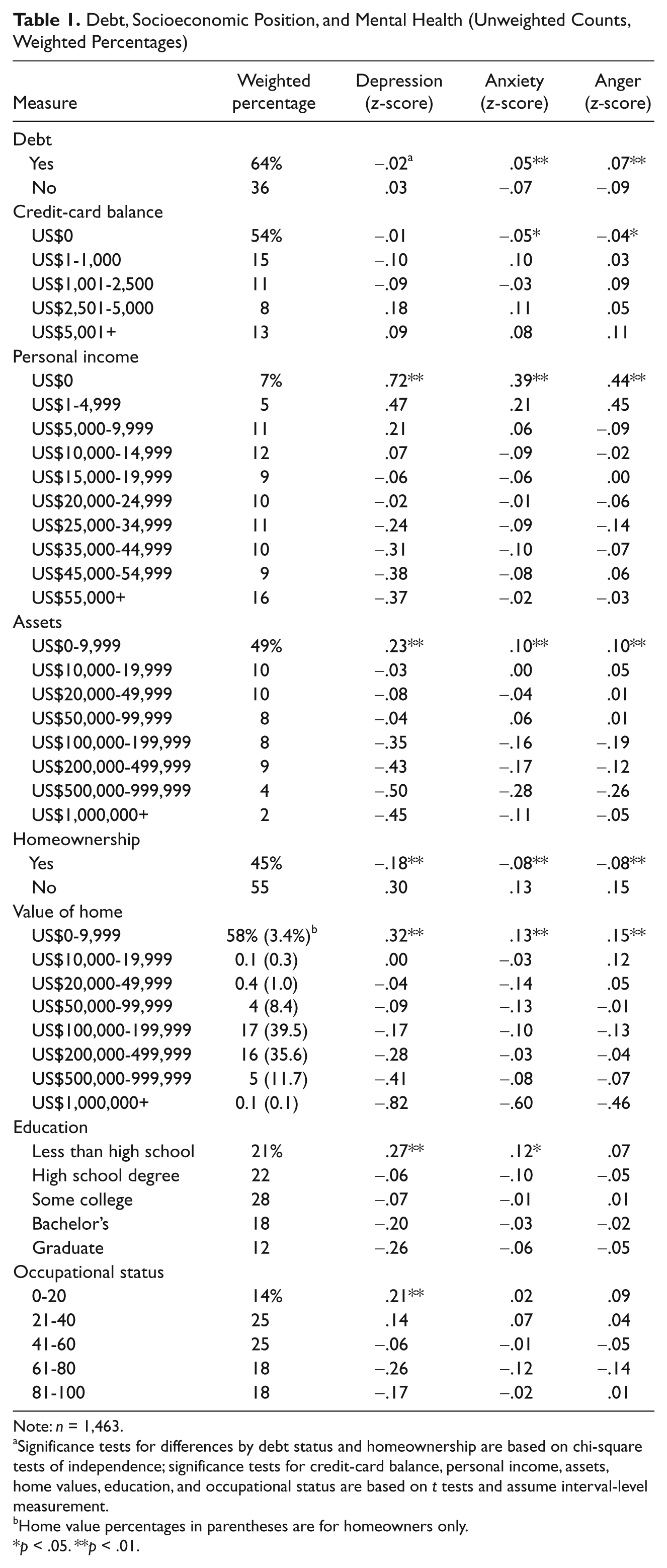

Table 1 presents overall distributions of debt and other aspects of SES, and also how mean levels of depression, anxiety, and anger vary across categories of these measures. Weighted percentages of debt and SES are reported in the left-hand column, and the other columns contain means of the standardized mental health measures by debt and SES. In Miami-Dade County, FL, 64% of adults are indebted to a bank, credit-card company, store, or other lending source. Just under half (46%) carry balances forward on a credit card, and some at very high levels. Thirteen percentage report having more than US$5,000 on their credit cards after making the monthly payment. There is also some preliminary support of Hypothesis 1, in that symptoms of anxiety and anger—but not depression—vary significantly by debtor status and amount of credit card debt. The differences are admittedly small; for example, debtors have anxiety symptoms that are .12 of a standard deviation greater than nondebtors (.05 – [–.07] = .12).

Debt, Socioeconomic Position, and Mental Health (Unweighted Counts, Weighted Percentages)

Note: n = 1,463.

Significance tests for differences by debt status and homeownership are based on chi-square tests of independence; significance tests for credit-card balance, personal income, assets, home values, education, and occupational status are based on t tests and assume interval-level measurement.

Home value percentages in parentheses are for homeowners only.

p < .05. **p < .01.

The other measures of SES in Table 1 show the considerable disparities in income and wealth in Miami-Dade, and that these are consistently associated with mental health. Adults who have no personal income report the greatest number of depressive symptoms, on average, a level that is around one standard deviation higher than those making at least US$55,000 per year (.72 – [–.37 = 1.09]). 2 Assets are more concentrated than personal income, where one half of Miami-Dade adults report having no wealth in the form of checking or savings accounts, stocks, bonds, or real estate. Likewise, homeowners report better mental health than nonowners, as do adults with more valuable homes relative to those with less valuable homes. This latter result only holds true for depressive symptoms when nonowners are removed from the bottom category; value of home among homeowners is not associated with anxiety or anger.

Education and occupational status are negatively associated with depressive symptomatology in Miami-Dade; and education, but not occupational status, predicts fewer symptoms of anxiety. Neither is associated with symptoms of anger. These results show the importance of examining multiple measures of mental health, as they differ by which SES indicator is analyzed.

As the traditional measures of SES appear to be associated with mental health more consistently, and with larger impact than debtor status and credit card debt, a crucial question is whether debtor status is redundant as a measure of SES. If the variance in debt overlaps to a great extent with the variance in income, wealth, education, and occupational status, then existing measures may not be lacking. To provide some insight into this question, we regressed debtor status on SES, employment status, and other control variables. We found that the association between the log odds of being in debt and income was parabolic, and therefore include a squared term for income in the equation. These logistic regression results are reported in Table 2.

Logistic Regression of Debtor Status

Source: Miami Disability Study, 2001.

Note: n = 1,463.

p < .05. **p < .01.

Notably, the various aspects of SES are not consistently associated with the odds of indebtedness. Some social and economic resources increase the risk, others decrease it, and many are not associated one way or the other. Personal income increases the odds of being in debt at low levels of income, then becomes protective against debt at an income of US$45,000 to US$55,000 (using the logit coefficients, the slope goes from positive to negative at

We next assess whether debt is consequential for mental health once other aspects of SES are accounted for. The regression analyses in Table 3 strongly affirm the unique contribution of debt to mental health (though not the amount of credit card debt, as mentioned earlier). Indebtedness increases symptoms of depression, anxiety, and anger, above and beyond the influences of income, wealth, education, occupational status, employment, various controls, and earlier mental health. The effects range between .14 and .17 of a standard deviation. Despite the modest magnitude of the coefficients, debt more consistently predicts mental health than any other standard indicator of SES. Thus, debt is “nonignorable” when assessing the significance of SES for mental health.

Regression of Depression, Anxiety, and Anger on Debt, Socioeconomic Status, and Controls

Source: Miami Disability Study, 2001.

Note: n = 1,463. Metric slopes with T-scores in parentheses.

p < .05. **p < .01.

Finally, we also looked at debt stress as a dependent variable, and not surprisingly found it strongly related to debtor status, and also that assets, being retired, and having health insurance were protective against debt stress, while having children, being physically disabled, or being White/Hispanic relative to black increased symptoms of debt stress, all else equal (not shown).

Other measures of SES affect mental health, but none as consistently as indebtedness. Symptoms of depression and anger, but not anxiety, decrease with income among lower income groups. However, the significant squared term suggests these associations reverse and become negative, at an income of around US$45,000 to US$55,000

What underlies the robust effect of indebtedness on depression, anxiety, and anger? Drentea (2000) found that the negative health impact of debt was largely due to anxiety over being able to pay it off. We added a measure of debt stress to the models in Table 3, and report the coefficients for debt stress and debt in Table 4 (coefficients for indicators of SES and controls not reported). Each unit increase in the scale of debt stress is predicted to increase depression, anxiety, and anger by .16, .14, and .10 standard deviations, respectively. Accounting for debt stress also explains the deleterious effects of indebtedness on mental health, reducing the coefficients for debtor status to nonsignificance in each case.

Regression of Depression, Anxiety, and Anger on Debt Stress, Debt, Socioeconomic Status, and Controls

Source: Miami Disability Study, 2001.

Note: Coefficients for socioeconomic status and controls not shown. n = 1,463. Metric slopes with T-scores in parentheses.

p < .05. **p < .01.

In additional analyses, we tested whether indebtedness had a larger negative impact on mental health for some subpopulations as compared to others, such as those with few assets compared to those with considerable assets. The results yielded no evidence that debt is less stress-producing for groups with more socioeconomic resources, further attesting to its unique and robust mental health significance.

Discussion and Conclusion

This article shows that future research on the SES health gradient would benefit from taking debt into account. Indebtedness is common, socially patterned, and consequential for mental health. In our sample of older adults, two-thirds were in debt and just under half carried balances on their credit cards. Similar to previous studies, we found that older age is protective against being a debtor (Drentea, 2000). Individuals who were older and retirees were less likely to have any debt. We also found that greater income is associated with less likelihood of being a debtor, whereas lower income increases the likelihood of debt. Higher occupational status, being married and African Americans also were more likely to be in debt. This research then corresponds with previous research showing that African Americans have higher debt levels (Garcia, 2007), but surprisingly we found no association between Hispanic ethnicity and being a debtor. Considering the large number of Hispanics in this sample, this finding is rather robust.

Turning to mental health, we found that debt matters for mental health above and beyond the traditional SES measures. In support of Hypothesis 1, being a debtor was associated with higher depressive symptomatology, anxiety and anger. Thus, the failure to include debt may result in an incomplete accounting of the SES health gradient, because debt is arguably as much a part of individuals’ socioeconomic positions as household income or employment. Furthermore, it was noteworthy how specific aspects of SES were not consistently associated with different mental health outcomes (the sole exception being indebtedness). These results resonate with Lahelma et al.’s (2006) study of Helsinki workers, where economic difficulties were much better predictors of depression and anxiety than were conventional SES indicators. The most important results in this article are that indebtedness is the only SES measure significantly related to all three mental health outcomes. That is, in modern society, indebtedness is a key component underlying the relationship between socioeconomic position and mental health.

We found no support for Hypothesis 2—the effect of debt on mental health did not vary by level of assets. We are not sure why the negative consequences of indebtedness do not vary by economic resources. Perhaps there is something truly unique about the imbalanced social relationship of being in debt to an individual, a store, or a financial institution. Alternatively, perhaps this is due to our data source’s relatively simple measures of assets. Future research should continue to examine this relationship.

We also extended past research by controlling for earlier mental health and early health problems up to age 25, thereby reducing concerns that the results are driven by social selection. We found support for Hypothesis 3—there were still independent effects of debt on the mental health outcomes after controlling for prior mental health. Thus, the association between debt and current mental health is not spuriously due to earlier mental health, lending support for (though not necessarily proving) a social causation interpretation.

Finally, additional analyses indicated that the association between debt and mental health is explained by debt stress. This suggests that debtors report greater symptoms of depression, anxiety, and anger in large part because they are worried about being able to pay off what they owe. Thus, as discussed at the beginning of this article, debtor status is stressful, and is associated with mental health. Among this sample of older adults, who were not raised in the debt-normative times of today, and who are living in a time when debt may be a necessary stepping stone to higher social class (Dwyer, McCloud, & Hodson, 2011), debt is associated with lower levels of mental health. It may be especially distressing for these older Americans because they associate worry and shame with debt (Sullivan et al., 2000). Similarly, they came of age during a time where they were ‘sold’ the American dream, but often could not fulfill it as easily as their parents had (Newman, 1993). Future research should further explore the stress of being in debt, and mental health professionals should consider debt as a possible stressor that can be alleviated through both mental health counseling, but also financial counseling, education, and debt relief.

As with all studies, ours has several limitations. For one, the measures of income and assets in these data are not dollar figure reports, but ordinal measures, meaning there is measurement error in the estimates we’ve reported. Also, credit card debt levels are generally underestimated (Zinman, 2009). Second, it’s unfortunate that debtor status and credit card debt-to-income ratio were only measured in the second wave. This prevents us from testing whether the recent onset of debt leads to mental health declines. Third, ideally we would have the dollar amount of all debt owed, not just credit card debt—this is perhaps the reason for the null findings associated with credit card debt levels. Fourth, these results are generalizable to Miami-Dade County, a single major metropolitan area that is unique from the U.S. general population in several important ways. However, due to the specificity of the sample, we also have a lot of detail on some subgroups of the U.S. population, such as among this older population of Whites, Hispanics and African Americans. This is also a strength of the article. Fifth, the measure of debt used in this study is a very general one, and future research should differentiate between secured and unsecured forms of debt as well as different types of debt within these broader categories (e.g., mortgages, credit card balances, vehicle loans, college loans etc.), as Dwyer and her colleagues do (2011). In addition, when studying those of lower SES, payday loans and the like are important. It is likely that the mental health consequences of debt vary by type, or even that different populations are more/less susceptible to anxiety from different forms of debt. Such analyses await better data. Finally, the data were collected in the early 2000s. Although more recent data would be desirable, associations between debt and mental health status were found, and it is rare to have a data set that includes this many measures of SES and mental health. Thus, this article provides a documentation of an important relationship which should be confirmed and elaborated in future work.

Studies of the SES gradient in mental health need to pay more attention to debt, especially if studying rates of anxiety, anger or depressive symptomatology. Therefore, we conclude that debt is an inextricable aspect of the SES gradient in mental health, and that it should be included in future mental health studies alongside the traditional indicators of SES. This is especially important, as a credit crisis rocked the first decade of the 21st century. The economic structure in the U.S. changed dramatically in this first decade, and more Americans have experienced economic stress in the recession. Furthermore, although these data are from the early 2000s, one could plausibly argue that the mental health effects that we found here prior to the crisis would only be stronger post crisis and recession. These economic and structural changes also affected individuals during a time of unrelenting growth in consumerism and consumption.

Although the economic crisis of the 2000s hit, it is unclear whether people’s desires changed much, though their realities may have changed. The theory of relative deprivation explains how those with lower SES will experience more mental distress due to the imbalance of the beliefs of what one ought to have, and what one can afford. In modern U.S. society, the messages of how one should experience life in terms of lifestyle choices is frequently incapable for what people with lower income and education can afford. The relative deprivation associated with lower SES could lead to more anxiety and depression among the lower classes of society (Åberg, Lundberg, & Burström, 2006; Bernburg, Thorlindsson, & Sigfusdottir, 2009; Schumaker, 2001). An effort to buy the lifestyle expected, thus increasing debt and diminishing wealth has a psychological toll. Future research should try to understand the nexus of debt, consumption desires and mental health.

Given the credit crisis of the 2000s, future research should continue to examine the stressful and distressing relationship between debt and mental health. We used both multiple measures of social status and of mental health to examine the relationships among variables. However, future research should also examine all possible sources and amounts of debt, including amount owed on homes, cars, educational loans and so on. Only then could we get an accurate assessment of affects on mental health.

Theorists have argued that the current era of harried complexity and increasing materialism in everyday life has increased levels of mental disorder (Bauman, 1998). Increasing wealth disparity and growing debt fall right into the nexus of materialism, consumerism, angst and mental disorder. This research adds to the call to expand the traditional measures of SES to include not only wealth but also debt.

Footnotes

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by grants RO1 DA13292 and RO1 DA016429 from the National Institute of Drug Abuse to R. Jay Turner, and from the NSF ADVANCE grant program at UAB awarded to Patricia Drentea.