Abstract

The study purpose is to gain insight into changing diverse management approaches to corporate philanthropy in a period that spans both from economic boom and recession. First, the authors present an overview of Spanish corporate philanthropy and compare it to U.S. corporate philanthropy. The authors find a significant gap between the U.S. and Spain’s corporate philanthropic spending as a percentage of profits and different trends between the two. A significant similarity is that the economic downturn is having a lower impact on spending than was predicted. The authors then focus on eight Spanish companies to explore how firms manage their philanthropy. The authors present a management model matrix that provides a framework for philanthropy management types and throws up divergent results for both society and companies. It seems that those companies that are managing philanthropy in a more sustainable way are not cutting their spending in this field despite falling profits.

Keywords

The recession that began in late 2007 may affect the field of corporate philanthropy (Cohen, 2009). The collapse of the financial and credit market is real, and the repercussions are dramatic. However, big U.S. corporations spent more on charity in 2008 despite worsening economic conditions and a slowdown in earnings (Brewster, 2008). Moreover, 55 CEOs from many of the world’s largest companies—IBM, General Electric and Coca-Cola—among others—stated during the Board of Boards CEO Conference that their corporate philanthropy would be on a par with 2008 (Fryer, 2009).

In Europe, Spanish companies are also facing great economic challenges as profits tumble and boards take a closer look at every aspect of the business. Against this gloomy background, many Spanish opinion leaders suggest the end of corporate philanthropy is nigh. Although Spain is the second largest philanthropic donor (Fundación de Estudios Financieros y Fundación, 2008), these analysts are convinced the slump will force companies to make drastic cuts in their spending in this field in 2009 (Caballero, 2008).

Nevertheless, some Spanish corporate philanthropy leaders say they will maintain their giving during the recession even if their profits are falling. During a recent conference, two corporate social responsibility (CSR) managers from two leading Spanish companies, BBVA—a financial services company—and Inditex—a fashion design, manufacturing, and distribution group—claimed that they plan to increase their contributions. BBVA and Inditex undertake philanthropic activities that impact directly on their core business. Their goal is to create social value for the community and benefits such as strengthening their business competences, enhancing their reputation, boosting employee morale, and finding new business models.

The purpose of this article is to gain insight into changing management approaches to corporate philanthropy as the economy goes through a boom-to-bust cycle. Exploring how the economic downturn is affecting corporate philanthropy will help furnish a better understanding of companies’ strategic thinking on corporate philanthropy.

Since our exploration is based on Spanish data, we first give an overview of Spanish corporate philanthropy and compare it to U.S. corporate philanthropy. This comparison will allow us to highlight any significant differences in the trends between the two groups. Then, we explore the following questions: Is Spanish corporate philanthropy similar to or different from U.S. corporate philanthropy? How do companies approach the management of their philanthropy?

To address these questions, we first review the literature on corporate philanthropy, focusing on its relationship with corporate success. Next, we explain the research methodology and introduce the sample companies. Then, we present the research findings and propose a conceptual framework for mapping companies’ philanthropy management. The article ends with some final comments and a discussion of the implications for future research.

Over the past few decades, there has been rapid growth in research on philanthropy and fundraising in the United States. This began with the pioneering works on philanthropy by Van Til (1990), Gronbjerg (1993), Burlingame (1997), and Sprinkel Grace (1997). One should also mention more tightly focused research on corporate philanthropy by Burlingame and Young (1996) and Himmelstein (1997). Those authors describe the efforts made by U.S. companies in this field, which date as far back as President Johnson’s war on poverty (Smith, 1994).

In an early contribution, Useem asserted that the single most important market factor underlying corporate philanthropy is the traditional measure of company success, its net income. In a similar vein, Cochran and Wood (1984) provided empirical evidence from U.S. companies to support the notion of a direct relationship between the level of company philanthropic donations and its financial performance. Also, McGguire, Sundgren, and Schneeweis (1988) maintained that corporate philanthropic contributions “may be especially sensitive to the existence of slack resources and that less profitable firms may be less willing to undertake socially responsible actions.” Adams and Hardwick’s (1998) study based on 1994 data from 100 U.K.-listed companies revealed that profitable companies tend to make larger donations than less profitable ones. Recently, based on a sample of 489 Fortune 500 companies, Crampton and Patten (2008) found differences in corporate contributions following the September 11, 2001, terrorist attacks in the United States correlated strongly with differences in firms’ profitability. The study provides evidence suggesting that even in the wake of catastrophic events, corporate giving is largely conditioned by financial concerns. In their article, authors cite earlier studies that find a significant positive relationship between firms’ short-term profitability and their charitable contributions (Galaskiewicz, 1997; Maddox & Siegfried, 1980; McElroy & Siegfried, 1985; Navarro, 1988; Useem, 1988).

However, corporate philanthropy is more than a byproduct of corporate success. It is used to stimulate success as well (Useem, 1988). Indeed, an emerging genre of work linked to corporate philanthropy looks at how giving is part of a firm’s overall strategy and strategic positioning. Campbell and Slack (2007) and Haley (1991) discussed charitable contributions in terms of “social currency” and suggested that contributions can be and are used to align corporations and environments and can serve as strategic resources. Mecson and Tilson (1987) suggested that philanthropy is often a vital component of corporate strategic management. Strategic philanthropy was later described by Thorne, Ferrell, and Ferrell (2003) as being the “synergistic use of a firm’s resources to achieve both organizational and social benefits” (p. 360). Therefore, if companies integrate philanthropy into their strategic goals, they will foster opportunities for creating value for their businesses while addressing important social needs. Hess, Rogovsky, and Dunfee (2002) argue that philanthropy is truly strategic for companies when they are able to use their businesses’ core resources to create social benefits and enhance their competitive advantages. Porter and Kramer (2002) assert that true strategic giving addresses important social and competitive issues where both the company and society benefit from the firm bringing its unique assets and expertise to bear. Exploiting their full potential to develop and implement solutions not only offers greater benefits to society but also helps companies set themselves apart from the competition, enhance their brands, motivate their staff, and strengthen their licenses to operate (Bruch & Walter, 2005; Epstein, 2005; Kramer & Kania, 2006; Marx, 1999). Various business cases have taken the same line. One such is Hoyt’s (2003) on Cisco Systems. The company has developed a philanthropic program that is integrated throughout the company, with a strategy that is consistent with the company’s business direction and corporate resources. As in its business endeavors, the company concentrates on efficient use of resources to achieve the best results and to align and reinforce its business and philanthropic strategies. Bonfiglioli, Moir, and Ambrosini (2006) described Microsoft’s activities in encouraging employability to show how these activities provide strategic advantage for the company.

Corporate philanthropy can increase consumer name recognition and employee productivity, cut R&D costs, help overcome regulatory obstacles, and generally improve profitability (Simon, 1995; Smith, 1994). Thus, corporate philanthropy can be seen as potentially having a positive impact on a firm’s sales, providing scope for greater revenue and bigger profits (Patten, 2008). Based on a survey of corporate philanthropy managers of U.S. firms, Saiia, Carroll, and Buchholtz (2003) found that some well-established corporate philanthropic programs are being run in a way that benefits the community by helping to better position the firm. In this context, top management teams are requiring greater strategic accountability in corporate philanthropic programs and professional standards in corporate spending on philanthropy. In a similar vein, Brammer, Millington, and Pavelin (2006) explored philanthropic management practices among large companies based in the United Kingdom. Their research revealed that decisions are mostly made by top managers, while management processes are assigned to a functional area inside the company. Lately, based on 14 in-depth interviews with decision makers in Canadian corporations, Foster, Meinhard, Berger, and Krpan (2009) identified distinct roles for corporations in their philanthropic activities. The majority of companies in their sample were categorized within the overarching context of investing in the community because of the business benefits reaped as a result.

Several authors argue that corporate philanthropy should be viewed as a strategic investment that may yield intangible returns, such as enhanced reputation, corporate culture, and legitimacy (Fombrun & Gadberg, 2000). Gadberg and Fombrun (2006) argue that corporate philanthropy can create ‘‘reputational capital.” Godfrey (2005) further argues that increased stocks of reputational capital provide insurance-like protection for the intangible asset values arising from companies’ relations with various stakeholders. Such relations include staff commitment to the firm, legitimacy with communities and governments, trust from suppliers and partners, and brand loyalty from customers. Godfrey notes that such relations are rare and valuable assets that are difficult for competitors to imitate and consequently leads to competitive advantage.

On the one hand, the business and social literature assumes that corporate philanthropy depends on having sufficient organizational slack (Seifert, Morris, & Bartkus, 2004). On the other hand, several scholars argue that corporate philanthropy is becoming more strategic and is expected to make a more direct contribution to the company’s profitability (Saiia et al., 2003).

The economic downturn means companies around the world are struggling to contain costs. Even in those companies that have escaped the worst of the crisis, the outlook remains uncertain and credit is tight (Cogman, Dobbs, & Giordano, 2009). The recession has put a great deal of pressure on CEOs and top managers, who are responding by trimming costs wherever possible. Financial responsibilities are of fundamental concern for businesses (Carroll, 1991). A firm must meet its financial requirements and maintain its competitive market position before discretionary expenditures such as corporate philanthropy can be made (Saiia et al., 2003). Following this line of argument, many experts claim that the crisis may herald a dramatic and irreversible decline in corporate philanthropy.

Nevertheless, one could argue companies take a strategic approach to philanthropy and will thus continue spending despite a slump in profits. By contrast, companies adopting a purely charitable form of corporate philanthropy may well decide to cut their expenditure. Put another way, companies that have integrated philanthropy into their operations and that carry out philanthropic programs serving the community and advancing the firm’s objectives will continue investing in them regardless of the financial challenges they face. When philanthropy is marginal to core business, charitable spending is likely to be cut back when the firm profits drop.

Previous scholars have developed classification frameworks to describe different approaches to corporate philanthropy. Austin (2003) presents philanthropy in organizations as linear, ranging from less to more involvement. Porter and Kramer (2002) focus on the outcomes achieved to classify some forms of corporate philanthropy as strategic. Others, such as Bruch and Walter’s (2005), use two dimensions to classify philanthropy in four categories, which are based on competences and market orientation. Kasper and Fulton (2006) have also developed a framework for helping companies in their philanthropy efforts. They focus on the degree of alignment between philanthropic efforts and the company strategy and on how responsive or proactive the company is in its approach to philanthropy. Foster et al. (2009) stress that though each framework differs in its focus, at least one of the dimensions identified includes motivation, implementation, or outcome. Also, these conceptual frameworks imply that it is possible for a company to move from one category to another. Alter’ s (2006) classification of business and social program activities is slightly different in that she talked about three models: the embedded social enterprises that also function as a sustainable program strategy, integrated social enterprises created as a funding mechanism to support the nonprofit’s operations, and external social enterprises that support their social programs through supplementary financing. Even this typology focuses on social enterprise; it guides in analyzing the extent to which philanthropy is integrated by firms.

Method

To support these propositions, we conducted a two-part study. First, we undertook a survey among large Spanish companies to gather data on corporate philanthropy and uncover the nature and size of their charitable spending. The data would help us to determine whether and to what extent these companies are resizing their philanthropic investments in the slump that began in late 2007. To put our findings in a broader context, we compared the firms in our sample with those of U.S. companies to highlight any significant differences in trends between the two groups. The United States was chosen for comparison purposes because its corporate philanthropy model is more advanced than that of European countries (Pasquero, 1991).

Quantitative research was carried out using the sample of 35 Spanish companies. The entire sample was drawn from the IBEX 35, the index made up by the 35 most liquid securities traded on the Spanish Market, used as a domestic and international benchmark and as the underlying index in the trading of derivatives. The selection of a security to be included on the IBEX 35 does not necessarily depend on the size of the companies, though a minimum market capitalization is required to be eligible for the IBEX 35. Many large companies that are regularly traded on the stock exchange belong to the IBEX 35, though not because of their size but owing to their liquidity. Thus, IBEX 35 include some of the biggest Spanish companies such Telefónica or Banco Santander but also much smaller ones. Most of the IBEX 35 companies are global companies. During the past decades, they have become established in overseas market initially focusing on Latin America. Later, their attention shifted to Europe, especially the United Kingdom, as well as the United States and Asia. This sample has been chosen because the bulk of corporate philanthropy is carried out by IBEX 35 companies and because these companies provide data on their philanthropic activities through their annual reports. As these companies are often used in economic forecasts, it is reasonable to assume that they may also be markers for trends in corporate philanthropy. The quantitative research covered disclosure of the relationship between philanthropy budgets and the financial performance for 2006, 2007, and 2008.

In all, 26 of the 35 companies in the index were included in the sample, the remaining 9 being ruled out because they do not undertake philanthropic activities, do not make any public reports, or did not answer our postal survey. The survey comprised two parts. The first was a tailored questionnaire containing specific requests for data not contained in the company’s reports. The second part contained a survey of the firms’ 2009 corporate philanthropy agenda and their views on how the crisis is affecting corporate philanthropy. The response rate was 46%—that is 16 of the original 35 companies answered. One company stated that it could not answer because it was rethinking its philanthropic policies.

In order to compare the downturn’s impact on Spanish and U.S. corporate philanthropic investments, we use the Giving in Numbers 2007, Giving in Numbers 2008 , and Giving in Numbers 2009 reports published by the Committee Encouraging Corporate Philanthropy (CECP). Those reports present survey findings on 155 companies.

We then conducted in-depth interviews with the CSR manager or the top decision maker in charge of corporate philanthropy in eight companies from the IBEX 35. The selection criteria was based on the Spanish Social Responsibility Observatory (2008) analysis on the quality and consistency of the information provided by companies on their philanthropic activities and on their corporate responsibility scores (an average of GRI, AA1000, NEF, NU, and Corporate Governance scores). We selected the highest-scoring company in each industrial category in the IBEX 35: renewable energy, transport, financial services, construction, consumer products, insurance, oil and gas operations, and communications. The purpose of the interviews was to analyze how leading companies undertake their philanthropic investments and to capture process elements that are missed by traditional quantitative methodologies. Field-based approaches and “Elite interviews” or “long interviews with decision makers” were carried out to give insights into decision makers’ understanding of the phenomenon, its meaning to them, and what they consider relevant (Dexter, 1970).

Leading players in general CSR fields were interviewed. Their ages ranged from 40 to 55, three of them were women, and they had been in their respective companies for at least 5 years. The interviews focused on each person’s own experience of the company’s philanthropic activities, trends in involvement, commitment and his or her appreciation of corporate philanthropy, and the landmark events in the company’s philanthropic activities.

The Current State of Corporate Philanthropic Investments in Spain and the United States

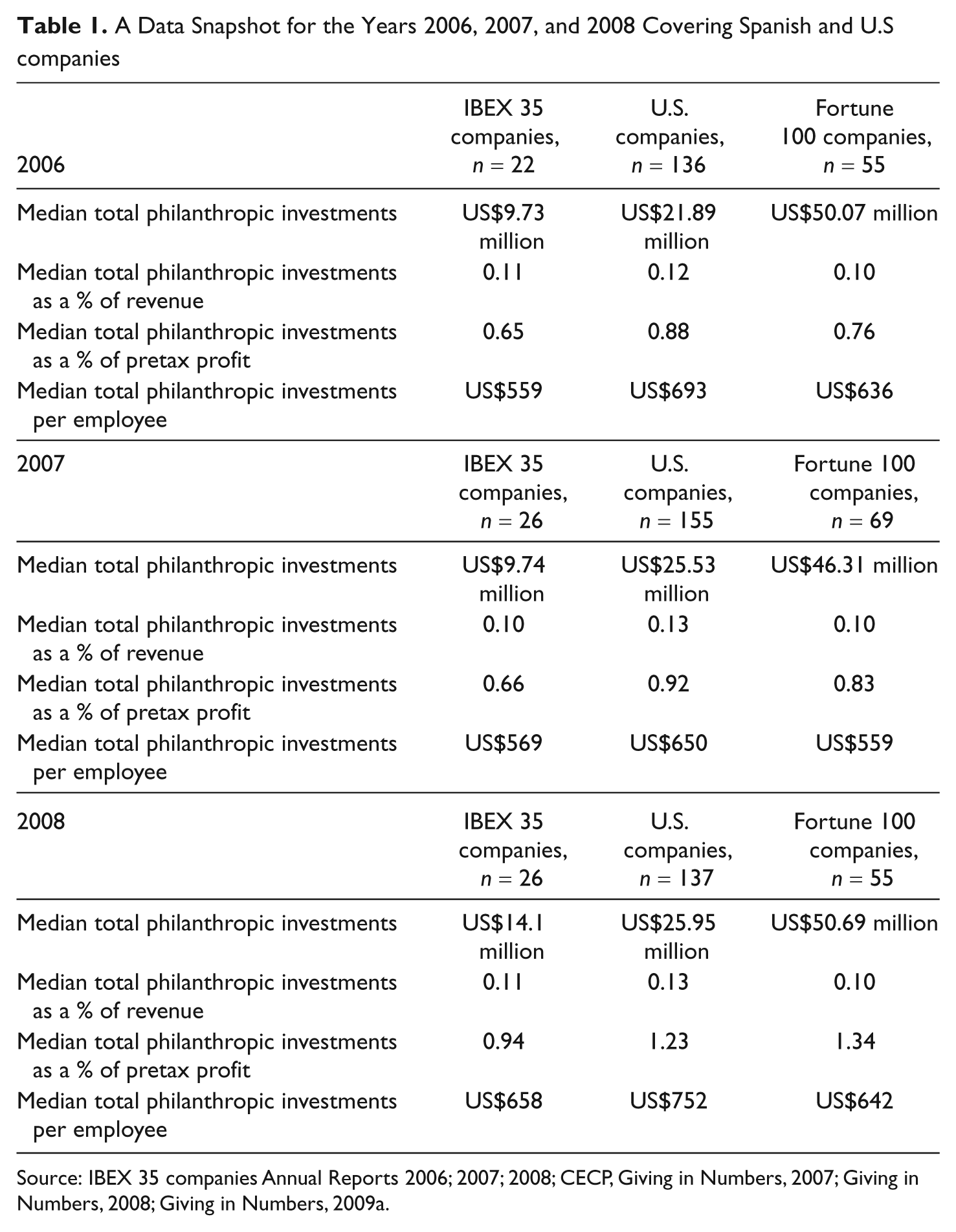

Some Spanish multinationals can stand comparison with their U.S. counterparts when it comes to philanthropic investments. The expression “corporate philanthropic investments” is used in this article to refer to a wide range of activities that companies assess and report such as cash donations, contributions that include in kind resources or donations in time. Take Spain’s BBVA Bank, with its reported US$95 million in philanthropic investments in 2007 and US$125 million in 2008. Among similar banks in the United States, Bank of America allocated US$200 million to philanthropic investments in 2007 and the same amount in 2008. These sums are stunning for European firms, which unlike their American counterparts have no long-standing philanthropic tradition as a result of the welfare-state culture that still prevails in Europe. However, in recent years, corporate philanthropy has become widespread in Spain, especially among large companies. Table 1 shows a snapshot of median findings for key data points from our survey, 2006, 2007, and 2008 company annual reports for IBEX 35 companies and the 2007, 2008, and 2009 editions of Giving in Numbers surveys for U.S. companies.

A Data Snapshot for the Years 2006, 2007, and 2008 Covering Spanish and U.S companies

In order to compare Spanish and U.S. philanthropic investments, we present data in U.S. dollars. Since Spanish companies report their figures in Euros, we used the annual exchanges rates for 2006, 2007, and 2008 Euros per U.S. Dollar provided by the OECD (Organization for Economic Cooperation and Development) in the Main Economic Indicators 2009 edition to convert Euros amounts to Dollar amounts.

Medians are used because they are less sensitive to extreme values than averages, which can be skewed by very high or very low values. In 2008, philanthropic investments per company ranged from US$1 million to more than US$160 million in our surveyed IBEX 35 companies. CECP found that the philanthropic investments per company ranged from US$600,000 to more than US$1,900 million in their U.S. companies survey. Table 1 shows that U.S. philanthropic investments are higher than Spanish philanthropic investments. However, the gap narrows when seen as a percentage of revenues, as a percentage of pretax profits and per employee.

The snapshot includes data from IBEX 35 companies, U.S. companies, and Fortune 100 companies since IBEX 35 companies not only have some specific characteristics that are very similar to those of U.S. companies but also possess some others that only Fortune 100 companies have. In 2008, IBEX 35 companies’ gross revenues ranged from US$1,000 million to more than US$89,000 million. In that matter, our data set is closer to U.S. companies data set where there is also a wide range of revenue levels. CECP found that revenues ranged from US$3,000 million to more than US$70,000 million in their 2008 U.S. companies survey. However, like Fortune 100—American largest businesses, IBEX 35 companies have a great visibility. These companies are point of reference and are considered markers for trends in many management issues.

Philanthropic Investments by Budget Source, by Program Area, and by Geography

Half of the IBEX 35 companies in our sample reported having a corporate foundation, but only 34% of philanthropic investments are made by corporate foundations and the remaining 66% are made directly by corporations. By contrast, 92% of Fortune 100 companies and 85% of the rest of U.S. companies have a corporate foundation through which a large proportion of their philanthropy is administered. Indeed, just 44% of U.S. philanthropic investments are made directly by corporations according to CECP reports.

Spanish companies and U.S. companies allocate a large share of their philanthropic investments budget to education, 26% for IBEX 35 companies, 27% for Fortune 100, and 28% for U.S companies. On average, a Spanish company allocates the largest share of its philanthropic budget to education while a U.S. company earmarks the same shares of its total philanthropic budget to health and social services and education. By comparison, a typical Spanish company allocates the second largest share of its budget, 19%, to culture programs, compared to just 7% in the case of U.S. companies. Spanish and Fortune 100 companies both earmark the third largest share of their philanthropic budgets to economic development (15% for IBEX 35 companies, 14% for Fortune 100 companies), whereas in U.S. companies economic development accounts for the fourth largest share (12%).

Year 2008 IBEX 35 companies, Fortune 100 companies, and U.S. companies average percentage of total philanthropic investments by program area (IBEX 35 companies, n = 20; Fortune 100 companies, n = 42; U.S. companies, n = 82)

Spanish companies spend a significantly higher percentage of their 2008 total philanthropic budgets internationally than their U.S. counterparts. The Spanish companies surveyed invested 41% of their total budget abroad in 2008, which represents a rise of 7 percentage points from 2007. By contrast, U.S. companies allocate about 12% of their budgets to international philanthropic investments. Specifically, Fortune 100 companies allocated 17% of their budget in 2007 and 18% in 2008. The rest of the U.S. companies allocated 12% in 2007 and 13% in 2008 to international philanthropic investments. This seems a widespread feature within the European Union. According to PiE (Philanthropy in Europe, 2006), Europe’s leading corporate foundations have greater international focus. As PiE’s ranking of the top 25 biggest spending European and U.S. corporate foundations reveals, 56% of the top 25 Europe’s corporate foundations give internationally, compared to 44% of the U.S. corporate funders.

Philanthropic Investments Trends and the Recession

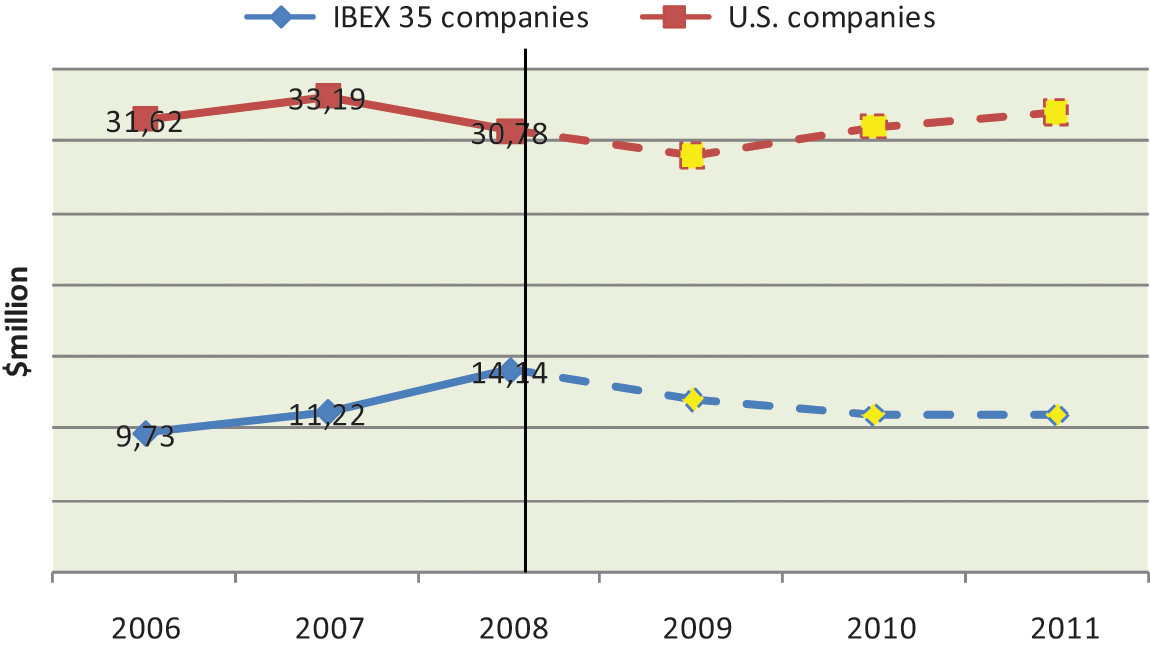

In order to make comparisons over time and observe trends in the real value of corporate philanthropic investments between 2006 and 2008, we adjusted the numbers for inflation. We used the Spanish GDP (gross domestic product) deflator provided by the OECD in the Main Economic Indicators 2009 edition to convert the amount of philanthropic investments to 2006 constant dollar value.

The following figures are based on a matched set of 22 IBEX 35 companies providing data from 2006 to 2008. This matched set is lower than the total number of companies reporting in 2007 because firms reporting for the first time in 2007 cannot be used to identify trends between 2006 and 2008. The CECP also relies on a matched-set data adjusted for inflation to analyze specific trends from one year to the next. In this case, the matched-set data for U.S. companies is 102.

Median total philanthropic investments per company—inflation adjusted (IBEX 35 companies, n = 22; U.S. companies, n = 102)

The median total philanthropic investment made by U.S. companies is more than twice the corresponding median for Spanish companies. This may be explained in part by the long philanthropic tradition in the United States. As can be seen, more than 80% of U.S. companies have established a corporate foundation through which a large proportion of their philanthropy is channeled. Many U.S. foundations are very long-lived and have accumulated considerable endowments, which provide an additional source of funding for corporate philanthropy (Brammer & Pavelin, 2005).

In 2008, Spanish philanthropic investments were 46% of the total philanthropic investments made by U.S. companies. However, the median philanthropic investments per Spanish company follows a rising trend showing an increase of 26% whereas the median philanthropic investments per U.S. company dropped by 7.8% from a peak in 2007 of US$33.19 million.

However, the 2008 median philanthropic investments per Spanish company may represent a peak before a decline in 2009. One explanation could be a 1-year lag between profits and philanthropic investment levels. Consequently, after the 2008 peak, median philanthropic investments may drop over the next few years. Since U.S. philanthropic investment reached a peak a year before the Spanish one, the upturn of philanthropic investments per U.S. company may also start before the Spanish one.

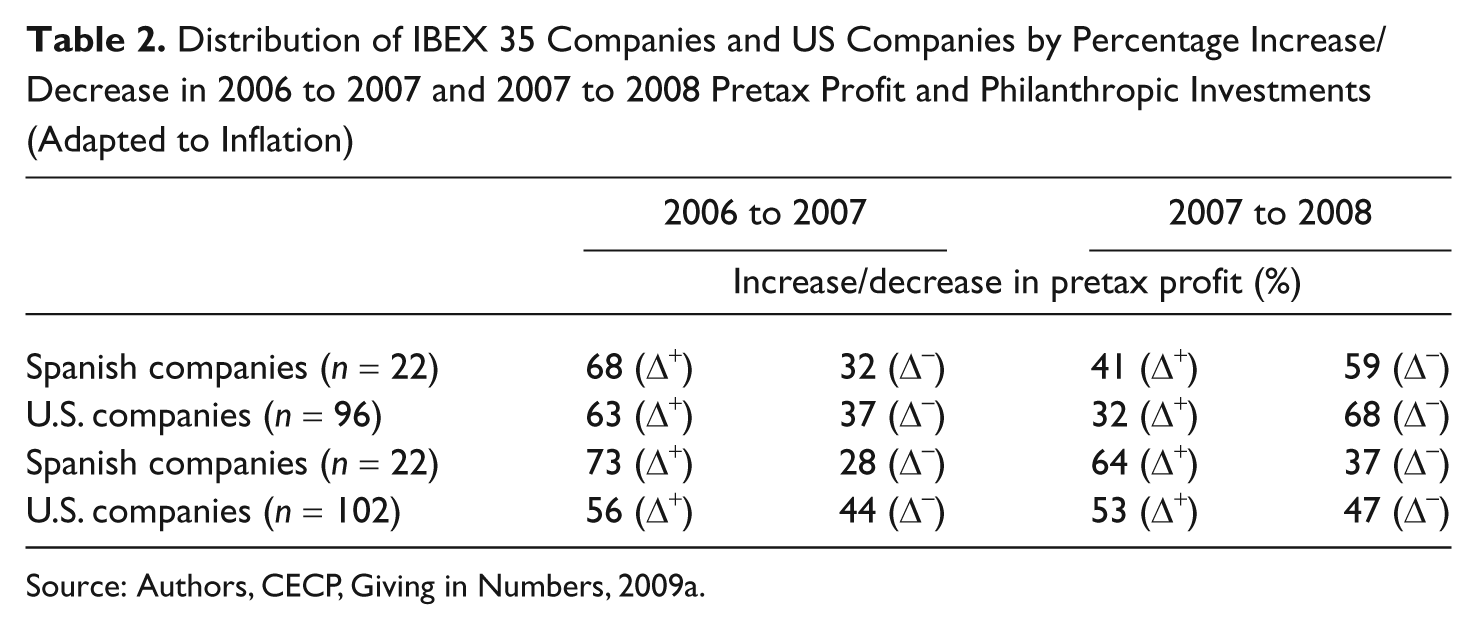

Table 2 provides an overview of how pretax profit changed from 2006 to 2008 for Spanish and U.S. companies. From 2006 to 2007, 68% of Spanish companies and 63% of U.S. companies saw an increase in their pretax profit. The trend then reversed. From 2007 to 2008, 59% of Spanish companies and 68% of U.S. companies saw profits fall.

Distribution of IBEX 35 Companies and US Companies by Percentage Increase/Decrease in 2006 to 2007 and 2007 to 2008 Pretax Profit and Philanthropic Investments (Adapted to Inflation)

Source: Authors, CECP, Giving in Numbers, 2009a.

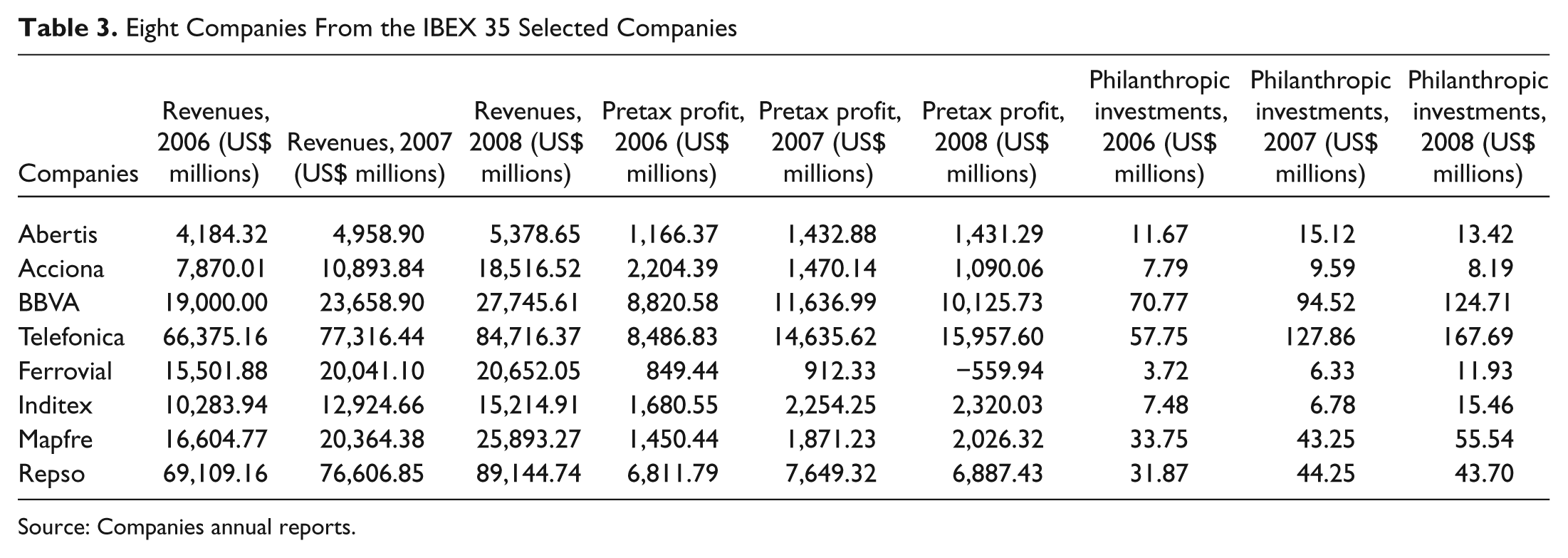

Eight Companies From the IBEX 35 Selected Companies

Source: Companies annual reports.

Table 2 also gives an overview of how philanthropic investments changed from 2006 to 2008 for Spanish and U.S. companies. From 2006 to 2007, 73% of Spanish companies and 56% of U.S. companies increased their philanthropic investments. Despite profit declines in Spanish and U.S. companies, more companies raised philanthropic spending from 2007 to 2008 than those cutting it; 64% of Spanish companies and 53% of U.S. companies increased their philanthropic spending.

The Outlook for 2009

In order to shed light how Spanish companies are refocusing their efforts in the recession, we made a survey among IBEX 35 companies. The survey focused on their 2009 corporate philanthropy agenda and their views on how the crisis is affecting corporate philanthropy. For U.S. companies, the data were obtained from the CECP 2009b report.

In answering the question, “How important should the economy be in determining philanthropic investments?,” 81% of our sample IBEX 35 companies considered that it should be important and 6% thought it should not be important. By contrast, all the U.S. companies surveyed by CECP (55 firms) considered that it should be important though they differed over how much.

To the question, “When considering a change in your company’s contributions, which constituency most influences your decisions?,” in the case of Spanish companies the most common answers were the board (29%) and senior managers (27%). According to the CECP, U.S. companies’ answers to the same question were their staff (51%) and their customers (29%).

Finally, when companies were asked what they considered to be the most important consideration in the current economic climate, 50% of the IBEX 35 companies in the sample thought that it was time to show that corporate philanthropy was crucial for business through its integration in the company’ strategic objectives. They felt that firms should focus their efforts on philanthropic activities that generate benefits for business and solve social problems;

37.5% of our IBEX 35 companies sample thought that it was time to broaden the traditional concept of noncash contributions by exploring new ways of contributing to the community, and 12.5% of our IBEX 35 companies sample thought that the recession will lead to big cuts in corporate philanthropy. In a similar vein, 56% of U.S. CEOs think it is most important for companies to refocus philanthropy on causes that are of key importance to the business strategy.

One of the most important aspects to highlight is the gap between U.S. and Spain corporate philanthropy investments. Although the gap has narrowed recently, it is still large. It would be worth tracking this gap over the next few years.

Comparing Spanish and U.S. corporate philanthropy is not something to be taken lightly. The welfare tradition is very different in both countries; there are many comparative studies that attempt to describe different forms the welfare state has taken (Esping-Andersen, 1990). The economic and political circumstances and the leaders and institutions of each country have all contributed toward shaping a particular brand of welfare state in each country. (Ashford, 1986). We must not forget that we are discussing two countries in which development of the welfare state is atypical (Flora & Heidenheiemer, 1987). Despite its increase since the time of the New Deal, social spending in the United States continues to account for a much smaller percentage of the GDP than in other Western countries. And Spain is atypical in that it began shaping its welfare state when most other industrialized countries were already reforming theirs (Heclo, 1987). The main difference between the systems in the United States and other countries is that U.S. system makes only a token attempt to enhance redistributive wealth; innovative policies are almost always introduced in response to crisis, and U.S. social services are often privately managed. Characteristic features of Spain’s welfare state are that it is becoming increasingly universal, that polices and their administration are becoming increasingly decentralized, and that it is being selectively privatized (Rodríguez Cabrero, 1998).

This explains the remarkable difference in where contributions are made, particularly health and culture. Indeed, the public health care systems of Spain differ significantly from that of the United States. Spanish state provides extensive coverage, with benefits including payments of doctors’ fees, hospitalization, and the cost of pharmaceutical products to most Spaniards. The United States, on the other hand, relies on two programs, Medicare and Medicaid, which target mainly the elderly and low-income households, respectively. A large U.S. population is not eligible for public funds or services (Alesina et al., 2001). Thus, the typical U.S. company allocates an important percentage of its philanthropic budget to health programs.

In congruence, this set of historical circumstances is reflected in the structure of the U.S. nonprofit sector. Indeed, the major institutions in the American nonprofit sector are heavily concentrated in the field of health care, which contains 46% of nonprofit employment. The nonprofit sector turns out to be a significant economic force in the United States, accounting for 6.9% of the country’s (Salamon et al., 1999).

The profusion of nonprofit organizations has been one of the defining features of the American experience at least since the early 1800s (Salamon et al., 1999). This is explained by a strongly individualistic cultural ethos that has produced deep-seated antagonism to concentrated power, whether political or economic. Strong economic interests have reinforced this cultural ethos in order to avoid government interference with business and to escape taxation beyond what was considered absolutely necessary. This has contributed to an “ideology of voluntarism” that has made support of voluntary approaches to social problem solving an important political issue and ideological symbol. A resulting pattern of social problem solving made it difficult for government to extend its reach without engaging the aid of private institutions, thereby subsidizing an extensive expansion of nonprofit activity (Sokolowski & Salamon, 1999).

The Spanish nonprofit sector has started gaining ground the last quarter of the previous century when the rapid economic development of Spain since 1975 has created many new demands for social services. Before that, the long and complicated history of Spain, with the prominent role of the Catholic Church and then the strong corporatist policies of the Franco dictatorship reduced the social and political space potentially available for many types of nonprofit organizations (Ruiz Olabuénaga et al., 1999). Nowadays, the nonprofit sector appears to be an important and growing economic force in Spain, accounting for 4% Spain’s GDP. It has a sizable presence in the fields of education and research, which accounts for 25.1% of nonprofit employment (Ruiz Olabuénaga et al., 1999).

Also, those differences between Spanish and U.S. corporate philanthropy may have arisen out of systematic differences in the institutional contexts within which the companies in our study operate. Particularly, tax law is an important consideration in explaining the differences between United States and Spain corporate philanthropy investments. American charitable contributions are generally tax deductible to the extent they do not exceed 10% of a corporation’s profits (Carroll & Joulfaian, 2005). Besides, there are tax benefits for contributions to certain types of organizations such as federally approved tax-exempt organizations—501c3 tax-exempt nonprofits—which may induce U.S. companies to prioritize 501c3 organizations from local NGOs in other countries for making their contributions. The institutional setting regarding Spanish corporate philanthropy is very recent and less developed than in the United States. In 2002, the Spanish government announced the 49/2002 law on tax system for nonprofits and tax incentives for philanthropy that permit corporation tax deductions. However, the law requires important reforms in order to match the U.S. model (Corbella, 2009).

Aside from these differences in institutional settings, there are also relevant disparities in other institutional dimensions as well as economic, social, and cultural factors that should be addressed in future work. For example, the U.S. individualistic cultural ethos has created a preference for contributing to community through individual action. For that reason, whereas in some Spanish companies the desire of founders have influenced corporate giving decisions, in the United States some of those same decisions may be shifted to the family foundations such as Bill and Belinda Gates Foundation or Howard Hughes Foundation. This American individual philanthropic tradition may explain also why in U.S. companies the major influences on giving decisions come from staff and customers whereas in Spanish companies it is from the board and senior managers. If the top managers in Spanish firms do not champion philanthropy, it would be difficult to involve employees and customers into it.

Corporate Philanthropy Management Models

As mentioned in the Method section, this part of the article focuses on a sample of eight large leading Spanish companies in the IBEX 35 index. Five of the eight companies studied are among those firms that have increased their philanthropic investments even though their pretax profits fell in 2008.

As mentioned in the literature review, some scholarly works have developed frameworks for classifying different approaches to corporate philanthropy. Since these works include the reasons for engaging in philanthropy, the strategic analysis, the implementation, and the outcomes expected, we focused our study on them. We have added a fifth factor to take account of the economic downturn. Our main findings of the in-depth interviews with eight IBEX 35 companies are summarized below (Urriolagoitia and Vernis, 2008, 2009).

Regarding the reasons driving corporate philanthropy, our eight companies recognized that, until a few years ago, they mostly donated money in response to a senior manager’s whim to contribute to a given cause. They also recognize that they started giving in response to a rising number of requests from nonprofit entities. Given this situation, companies decided to reformulate their philanthropy policies by diagnosing the situation and outlining new approaches. These changes took place very recently—most companies began the transformation processes in 2005-2006. For example, Repsol started by inventorying its philanthropic activities abroad and revising its corporate guidelines. To this end, it organized a Community Relationship Workshop with representatives from the 15 countries in which it operates.

After this review, a group of companies made the communication department responsible for their corporate philanthropy. Abertis recruited a new director who specializes in philanthropy and has set up a sponsorship committee, as has Acciona. A second group of companies, Mapfre and Telefónica, decided to put their corporate philanthropy in the hands of both the CSR department and the corporate foundation. Lastly, a third group of companies involve most of their departments. Although the CSR department is the main coordinator, philanthropic activities are embedded in the organization. Ferrovial has put its philanthropy on its business units’ agendas given that coordination mechanisms are part of the company’s organizational structure. BBVA business areas are engaged through its Corporate Responsibility and Reputation Committee, which comprises members from the 15 business areas; “we worked for five months crafting the CSR (corporate social responsibility) plan in which the corporate philanthropy strategy is an important part.” In addition to the corporate-level committee, this approach was replicated at country level.

The eight companies made very little strategic analysis before drawing up their corporate philanthropy policies and procedures. The companies admitted that before the change, they used to make ad hoc donations to several institutions in different areas, without adopting any general criteria. After the change, a group of companies—Abertis, Acciona, and Repsol—established a formal process for analyzing grant requests. This ensures their philanthropic investments are effective and deliver brand awareness and reputation. Abertis, whose core business is transport, chose road safety as the focus for its philanthropy in addition to social access, environmental conservation, and road safety education. The company views sponsorship as an opportunity to tie in its values and identity with its project partners.

Telefónica and Mapfre stand out for their analysis of broad social problems and their attempts to solve them. Both companies have dedicated a great deal of time and effort, even bringing in outside experts to ensure that their philanthropic investments focus on meeting the greatest needs. Their philanthropic activities are driven by core, enduring, and central organizational values and they are perceived as such by the community.

Telefónica redoubles its philanthropic efforts through its Foundation, focusing on education through information technology. A global strategy was formulated, as the Foundation not only operates in Spain but also in seven Latin American countries. Although each Foundation affiliate operates domestically on the basis of local issues, all share a global strategic focus, with the same mission, goals, and work methods.

BBVA, Inditex, and Ferrovial form another group. These companies focus their strategic analysis on finding out how to solve a social problem that affects directly their business. BBVA is transforming its Integration Scholarship Program into part of its core business. Basically, this program provides financial aid for educational purposes to underprivileged families in order to foster their social integration. The families receive financial aid through a bank account opened solely for that end. That way, they become familiar with retail bank services and are thus potential clients.

Our eight companies did not have any formal processes prior to overhauling their philanthropy policies and procedures. Since most of the philanthropic funds were one-off donations, execution was very informal. After the change, companies clustered again in three groups. Abertis, Acciona, and Repsol provide funding for medium-term nonprofit programs. For instance, Abertis has prepared a manual to guide sponsorship decisions, as has Acciona. This sets the requirements nonprofits must meet to be eligible for funding.

Mapfre and Telefónica form another group characterized by the provision of funds to nonprofit organizations and by the involvement of their corporate foundations. Those corporate foundations provide financial and expert support for implementing long-term philanthropic projects. Besides concentrating their philanthropic investments on a few far-reaching projects, Fundación Telefónica assesses long-term relationships with NGOs or similar organizations with great experience and specific knowledge of the social problem addressed. Fundación Telefónica believes that the key to its program’s success lies in its reliance on a specialized partner. Such reliance boosts legitimacy and ensures operating support.

For implementing their philanthropic investments, BBVA, Ferrovial, and Inditex get directly involved in providing all kinds of resources and tools. By engaging its employees and making use of their core competencies, expertise, and technological capabilities, these three companies have embedded their philanthropy in their business units’ agendas. Coordination mechanisms are part and parcel of the company’s organizational structure. BBVA has further integrated its philanthropy into its business through reporting to the board. This has led to managers realizing that the philanthropic program is a key tool for conducting business in Latin America. Inditex’s Social Council—a corporate body that outlines the company’s corporate social responsibility policies—plays a vital role in coordinating collaborative initiatives with various institutions. The council’s members are drawn from a variety of sectors, including nonprofit and academic ones.

Outcomes were paltry before the changes were made, and our eight companies had no expectations for either society or their business. Now, Abertis, Acciona, and Repsol take great pains to measure the impact of their philanthropic initiatives on both the society and the company. “It is a transparency requirement that guarantees that grantee organizations are reliable. We also ask them about their follow-up mechanisms and potential benefits for Abertis.”

Mapfre and Telefónica seek great social impact and enhancement of their reputation among their stakeholders. They have also developed specific indicators to measure the social impact of their philanthropic investments as well as indicators to monitor their reputation among different stakeholders.

BBVA, Inditex, and Ferrovial have incorporated social and economic impact measures into the company’s daily operation. Through its Integration Scholarship Program, BBVA has gained access to a great number of people who never use bank services. By improving living conditions for its workers, Inditex is boosting suppliers’ operating capabilities and its production chain. With its philanthropic project to improve health and living conditions in northeastern Tanzania, Ferrovial is building ties with developing nations that may offer investment opportunities in the future and help the firm diversify its business and expand in other countries. In short, all three companies are achieving social goals as well as generating a sustainable productive environment in geographical areas that are strategic to their businesses.

Most companies in our sample believe the first things companies ax in a recession is ad hoc charitable donations. “Those companies making one-off charitable donations are the first to turn off the tap. When business takes a dive, it is easy to freeze those kinds of gifts.” Against the backdrop of recession, Abertis, Acciona, and Repsol decided to cut back firm-wide spending, which included corporate philanthropy. Abertis and Repsol are planning to cut down their philanthropic investments for 2009. However, at the same time, these companies are working to seize opportunities for increased efficiency and for fostering a climate that allows new ideas to flourish, such as Abertis’ plans to set up volunteer programs. This initiative is part of Abertis’ efforts to build a corporate identity.

Despite the slump, Mapfre and Telefonica raised their philanthropic investments from 2007 to 2008 even though their profits fell. These companies are planning to increase their philanthropic spending next year whether or not they make bigger profits. Finally, BBVA, Inditex, and Ferrovial have increased their philanthropic investments even though their profits have fallen. They too plan to continue on the same track and do not consider the recession has any impact on their philanthropic investments. “When your philanthropy is integrated into the core business you will not shelve it just as you would not shelve the accounting department.”

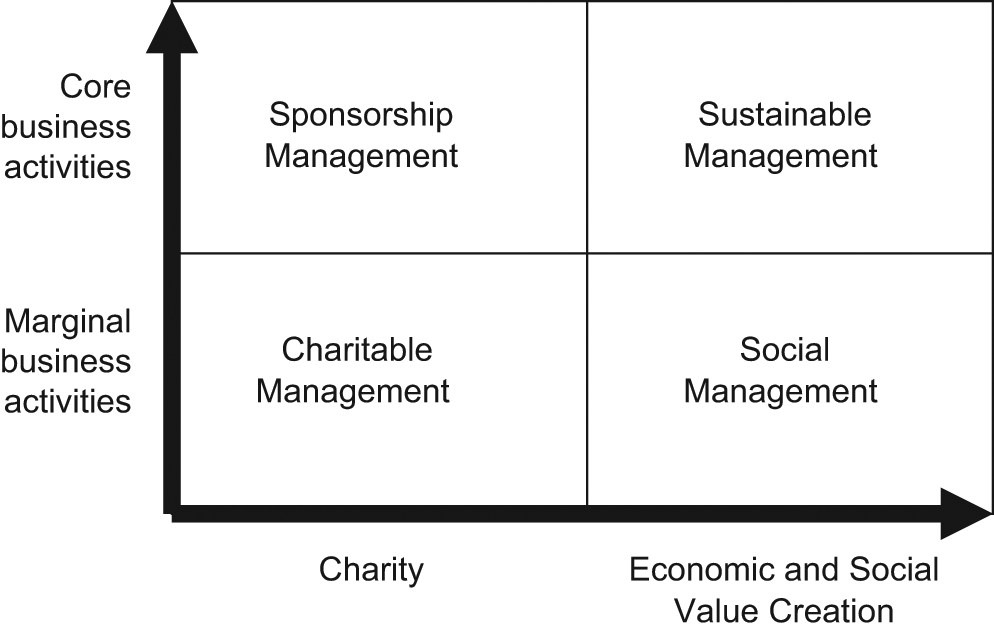

Given the features identified in our eight companies, we propose the matrix below to map companies’ philanthropy management. The vertical axis represents the extent to which a company’s philanthropic investments go to the core of its business. At one end, there are companies supporting any kind of philanthropic investments. At the other end, there are companies that seek to align their philanthropic activities with their knowhow and core operations.

The horizontal axis represents the extent to which corporate philanthropic activities create economic and social value. At one end, there are companies embarking on philanthropy solely for charitable purposes, showering society with gifts without expecting anything in return. At the other end, there are companies engaged in philanthropic activities that generate business benefits and social value. Figure 3 shows the matrix for corporate philanthropy management models.

Corporate philanthropy management models

The charitable model includes companies whose main reasons for contributing to society reflect the fleeting wishes of their shareholders or top managers and are a reaction to pressures from local NGOs or communities. These firms neither intend to help solve social issue nor reap any benefit for themselves. Before they transformed their philanthropy policies, the eight sample companies conducted a thorough diagnosis of their social activities. This highlighted the lack of clearly defined policies, coordination, and evaluations mechanisms. No precise decision-making criteria were found to explain contribution choices. Thus, one can infer that before their respective reviews, these companies followed the charitable model in dispensing their largesse. The companies fully realize that philanthropic funds dry up in a recession.

The sponsorship model matches companies that try to exploit synergies between their business and their philanthropic activities. These companies establish clearly defined decision-making criteria to ensure that their philanthropic investments are effective and provide brand awareness and reputation. A decisive factor for these companies is the synergy between their brand values and attributes and those of the grantee institutions. They have a formalized process to decide which organizations to support and how much money to give, but their strategic analysis still leads to responses to specific requests rather than the adoption of a proactive approach. The desired benefit is enhanced reputation and not improvement in the company’s ability to compete. The emphasis remains on fostering awareness rather than on creating value. These companies stress that the assessment of medium-term collaboration with grantees is the key to enhancing their corporate image and reputation. In order to attain their objectives, these companies build some organizational capabilities within their CSR departments. They usually put someone in charge of coordinating and monitoring the sponsorship relationships. Neither top managers nor the rest of the organizations get involved in the sponsorship activities. Companies adopting this approach are quick to cut their philanthropy budgets during a downturn. However, these companies also view changes in the global economy as an opportunity to start working on integrating their philanthropy strategy with company-wide business objectives.

The social model describes companies that have decided to make long-term investments to help solve a pressing social problem. They proactively develop their own projects—complex programs addressing social issues with a comprehensive, long-term approach. Such projects are consistent with the company’s mission and are tied to well-thought-out social objectives. This consistency is critical in order to build a stable and enduring presence in this social issue. Hence, their emphasis is on social value creation. However, those companies’ ability to compete is not improved since they do not draw on their core capabilities. The desired benefits for the company are reputation enhancement, shaping the corporate culture, or boosting staff motivation and commitment.

Under the social management model, corporate philanthropy contributes to broad, positive social outcomes. For such companies, philanthropic investments are a priority and of long-term importance. This is why they keep raising them even during recession.

The sustainable model encompasses leading Spanish companies that embark on philanthropic activities that directly affect their core business. Their purpose is to create social value for the community and economic benefits such as strengthening their business competences, entering new markets, or finding new business models.

The philanthropy strategy of these companies is a carefully constructed system of interdependent parts consistent with their CSR policies, processes, and activities. Moreover, all of these elements are aligned with their corporate strategy. The development of their philanthropy begins with the board of directors’ approval of the corporate strategy and builds on common pillars: value creation for their stakeholders, and social, environmental, and economic sustainability. Philanthropy is successfully linked with corporate strategy with the open involvement of the president of the company and through drivers such as CSR working committees involving business unit managers. As a result, a comprehensive view of philanthropy as an important dimension of CSR is articulated; focused social programs are established and social targets set for each business unit. Managers perceive social programs as a great opportunity for developing their core businesses. They make big efforts in planning, structuring, and nurturing a social project so that they can attain strategic objectives.

Those companies have instituted integrated governance systems that foster corporate philanthropy in coherence with other CSR activities. Those systems may include social boards, corporate directors, corporate and regional coordinators, and business unit accountability measurement and audits. Since corporate philanthropy is aligned with their business objectives, companies applying the sustainable management model do not see the recession having any impact on their philanthropic investments.

Corporate philanthropy is believed to vary by industry (Buchholtz et al., 1999; Seifert et al., 1994; Useem, 1988). Brammer and Pavelin (2005) suggest that industry-specific differences may be important and that these arise as responses to institutional or stakeholder pressures. Saiia et al. (2003) focus on differences in business exposure that create interindustry differences in the need to give and in the level of business visibility (Brown et al., 2007). Regarding our taxonomic categories, Spanish companies that match the sustainable model belong to the financial services, manufacturing, and retailing sectors. Financial companies have a strong local presence in the communities in which they do business as well as manufacturing companies that are large consumers of local raw materials or occupy significant real estate for the production and transport of goods. Accordingly, these highly visible companies integrate corporate philanthropy in their business agenda since they receive maximum benefit from each charitable dollar given. Spanish companies that adopt the sponsorship model belong to the infrastructure and construction sector and the oil and gas sector. Philanthropy should arguably have lower economic benefits for the company in industries with less visibility or significant environmental impacts because it fails to address the primary concerns of stakeholder groups (i.e., to reduce environmental impacts). For this reason, philanthropy is viewed by those industries as a brand-awareness expenses rather than value-creating investments. Moderately visible companies such as communications and insurance companies have adopted the social model since they have incentives to foster reputations for creating social value without the pressure to foster corporate philanthropy for going forward within their industry.

Conclusion and Further Research

This article provides an exploratory analysis of patterns in the philanthropic investments of the largest corporate philanthropists in Spain and in the United States in a period spanning from boom to bust. Our findings highlight significant similarities between Spanish and U.S corporate philanthropy: Basically, the recession is not affecting them as much as was predicted. However, there is still a gap between the U.S. and Spain corporate philanthropy investments as a percentage of pretax profits even if median philanthropic investments per Spanish company follow a rising trend. Also, it seems that companies that are managing philanthropy in a more sustainable way are not cutting their philanthropic investments despite sinking profits and rising uncertainty. Nevertheless, to find out the net effect of crisis we need to track corporate philanthropy trends over the next 3 years to determine the rise in corporate philanthropy.

A management model matrix has been developed where different philanthropy management types are determined by a combination of the degree of alignment with the core business activities and the value generated by these philanthropic activities both for society and companies.

In practical terms, the philanthropy management matrix may be a useful tool for managers to decide how to allocate company resources to philanthropic initiatives and to determine the outcomes desired for both society and the company. When positioning their philanthropy into one matrix’s side, managers may prioritize their strategic choices about where to go, be aware of the challenges the company may face, and set benchmarks.

Companies in the same industry often share philanthropic goals and focus areas, have overlapping stakeholders, and face similar business challenges. Therefore, longitudinal studies by industry would allow a thorough understanding of the corporate philanthropic investments trends at a global level.

Finally, our work links with research on business and nonprofits partnerships (Austin, 2003); thus it would be interesting to analyze in depth why private company executives engage in such partnerships in developing their corporate philanthropy.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.