Abstract

In recent years, the emergence of new legal forms allowing for-profit firms to incorporate with a formal commitment to both profit and social purpose has disrupted the traditional American business-charity dichotomy. The arrival of these hybrid firms can be expected to affect the functioning of markets and poses a potential challenge to the role played by large nonprofits that provide quasi-public services such as education and health care. We construct duopoly models of competition between a nonprofit firm and either a traditional for-profit firm or a hybrid firm, simultaneously choosing output levels of a homogeneous good. We show that when the nonprofit competes with a hybrid firm it becomes less competitive in the sense that its output level contracts, it raises less net revenue with which to fund charity care, and it is more easily driven out of the market.

Keywords

Confronting the array of organizational forms available to social enterprise, Dennis Young, Elizabeth Searing, and Cassady Brewer developed the concept of the social enterprise zoo (Young et al., 2016). Their framework directs our attention not only to the striking variety of social enterprise organizations but also to the importance of the “habitats” in which these organizations operate and of the “zookeepers” who curate them. In the United States, the biodiversity has traditionally clustered in the nonprofit domain but, in recent decades, an expansion of legal forms is encouraging the for-profit incorporation of social enterprises. The zoo metaphor reminds us that this curated change in the “habitat” can have consequences for existing enterprises in the nonprofit sector.

Diverse in its makeup, the nonprofit sector contains organizations whose public purposes include advocacy, innovation, service delivery, individual expression, citizen engagement, and the creation of social capital (Frumpkin, 2002; Moulton & Eckerd, 2012). Among nonprofits whose public purpose is service delivery are organizations that provide quasi-public services, that is, services that combine a public purpose with a private benefit that consumers are willing to pay for (James, 1990). Important examples of quasi-public services provided by commercial nonprofits include education and health care. Because markets for these services already attract both for-profit and nonprofit service providers, it is interesting to wonder how these markets and the nonprofits that serve them might be affected by the arrival of for-profit firms incorporated with a social purpose.

We use a mathematical model to address a “habitat” question for this sort of commercial nonprofit: What might be the consequences for a nonprofit that currently shares a market with a traditional for-profit firm if it finds itself competing instead against a hybrid for-profit firm with a legally declared social purpose? For example, would we expect the service-delivery nonprofit to reach more paying customers, or fewer? Does changing the type of organization that shares the nonprofit’s market affect the publicness of the nonprofit, reducing the resources it devotes to its purely public purpose while its customers enjoy lower prices? Does it matter whether the nonprofit has commitments to its workers or other stakeholders that give it a cost disadvantage, or alternatively that it enjoys a cost advantage thanks to donors and mission-driven workers and volunteers?

In the U.S. context, these are important questions. Among public charities with revenues of at least $50,000 in 2013, 72% of revenue was generated as fees for service (Urban Institute, 2015). In many markets, including hospitals, nursing homes, education, and day care, large nonprofits regularly compete with for-profit firms. How a commercial nonprofit functions can be affected by who its competitors are: a recent paper in this journal, for example, found that nonprofit hospitals were more willing than for-profits to invest in the early adoption of electronic medical recordkeeping, but the difference was attenuated where nonprofit hospitals were in greater competition with for-profit hospitals (Freedman & Lin, 2018). In a comprehensive review of earlier literature on nonprofit hospitals, Schlesinger and Gray (2006) conclude, The presence of nonprofit providers influences the behavior of for-profit organizations, and vice versa. The more for-profit hospitals in a locality, the more nonprofit hospitals (1) respond aggressively to revenue-increasing opportunities, (2) adopt profitable services, (3) discourage admissions of unprofitable patients, and (4) reduce resources devoted to treating the patients they do admit. (pp. 294–295)

In other words, the presence of for-profit competitors seems to reduce the publicness of the nonprofit hospitals.

We begin with an overview of the emergence in the United States of new legal forms combining profit-seeking with social purpose, and the scholarship that addresses them. Next, we review the theoretical literature on nonprofit competition in mixed markets and trace the line of inquiry that we build upon.

We model the objective function of a hybrid firm as including, in contrast to for-profit firms, an altruistic component, as well as being consistent, in contrast to nonprofits, with accountability to shareholders. We allow the hybrid firm’s production costs to differ from those of the for-profit or nonprofit firm, in light of its access to equity markets and also in light of socially conscious firms’ potential access to donations and grants, subsidies and tax breaks, and mission-driven employees and volunteers.

We also describe our nonprofit and traditional for-profit firms, and the market in which our firms compete. We are especially interested in large commercial nonprofits such as hospitals, nursing homes, and schools; these nonprofits care about the well-being of their paying customers as well as the well-being of clients served at no charge (or other public purposes pursued with net revenues generated in the commercial market). These institutions tend to be large relative to their local markets and, to capture this, we look at competition in markets with just two producers.

We showcase three results of the model. These address a profit-seeking firm’s motive to pursue a customer-facing social purpose, and the nonprofit firm’s willingness and ability to serve paying customers versus clients who cannot pay. We conclude with a discussion of the results and directions for future research. The mathematical derivations and proofs are presented in the appendix.

The Arrival of Mission-Oriented For-Profit Legal Forms in the United States

In the United States, most large mission-driven enterprises incorporate as nonprofits. The defining features of a nonprofit firm are its avowed charitable or social purpose, the favorable tax treatment that comes with nonprofit status, and, central to economists’ modeling of nonprofit behavior (Hansmann, 1980), the “nondistribution constraint” dictating that net revenues must be directed to its charitable purpose and not to the enrichment of shareholders.

Until recently, and in contrast to businesses in many other countries, incorporated profit-seeking firms in the United States were more or less tightly bound by what we might call a “nonredistribution constraint”: Shareholders could mount legal challenges if value was directed away from them to other stakeholders or to social purposes. This view of American business was famously articulated by Nobel laureate Milton Friedman in 1970 in the New York Times: “[T]here is one and only one social responsibility of business—to use its resources and engage in activities designed to increase its profits . . . without deception or fraud” (Friedman, 1970).

During the next 40 years this would relax, with many states adopting constituency statutes allowing management to consider stakeholders other than shareholders. But it was not until the benefit corporation was introduced in 2010 that a primarily profit-seeking business could formally incorporate with a declared social purpose. Whereas low-profit, limited-liability corporations (L3Cs) were designed to give nonprofit firms greater access to capital markets, 1 benefit corporations and similar incorporation options, now widely available in the United States (Feldman, 2021), “transform standard for-profits into dual-mission entities” with a required “purpose of creating general public benefit” and are permitted to declare a commitment to a “specific public benefit” in their charter (Brakman Reiser & Dean, 2017, p. 53). Reporting requirements include a benefit report on their activities in support of non-shareholder constituencies and any mission specified in their charter.

Primarily profit-seeking but with an avowed social purpose, these hybrid firms’ commitment to multiple goals creates a problem of trust when managers cannot commit to a particular division of resources between the pursuit of public purpose and profit. One possible advantage of having an increasingly broad array of hybrid forms available—enterprises may choose their state of incorporation and requirements vary across states—is that entrepreneurs might be able to use their choice of form to signal their intended balance between “mission and margin,” thereby resolving the trust problem. This seems not to be the case: Brakman Reiser and Dean (2017) document the ways in which fiduciary standards, reporting requirements, and penalties for noncompliance all fall short of committing the hybrid firm to a particular mission-margin balance.

There is a cynical reason to think that incorporation as a hybrid of the benefit-corporation type might be attractive to investors and create less of a trust issue between shareholders and other constituencies than nonprofit scholars have anticipated. As we discuss in the next section, formal models of imperfect competition suggest that there are circumstances under which public-facing missions such as “expanding community access to affordable health care” can increase the profits of profit-seeking firms. In other words, markets for quasi-public services may attract profit-seekers with pseudo-public motives.

Competition Between For-Profit and Nonprofit Firms

Nonprofit scholars first modeled mathematically the case in which nonprofit firms enter into competition with for-profits as a side venture to generate money for their organization (James, 1983), such as a hospital leasing parking spaces to neighboring businesses, trading off the distastefulness of the commercial activity against the funding it provides. Attention shifted to nonprofits’ principal markets of operation as nonprofit scholars documented differential behavior between for-profit and nonprofit firms, for example as providers of care in nursing homes, psychiatric facilities, and facilities for the mentally handicapped (Weisbrod, 1988). Harrison and Lybecker (2005) focus our attention on the motives of nonprofit hospitals by modeling a market in which a for-profit hospital competes with a nonprofit hospital, allowing the nonprofit hospital to maximize a weighted average of profit and either output, quality, or charity care. Stenbacka and Tombak (2020) consider the importance of cost differentials between standard-quality and high-quality medical treatments in a world in which universal health insurance offers payment for the standard-quality option and the nonprofit hospital cares about the well-being of the customers it serves, demonstrating that the size of the cost differential can determine which hospital provides the high-quality treatment. Moon and Shugan (2020) consider a hospital market in which a for-profit competes with a nonprofit that maximizes a combination of profit and output; they generate results consistent with the empirical observation that the more profitable hospitals providing more premium specialty medical services are likely to be nonprofits. 2

While many papers focused on the hospital industry, another strand of literature was interested in the “unfair competition” between a tax-paying for-profit and a tax-exempt nonprofit firm operating in the same market. Liu and Weinberg (2004) use a duopoly model to demonstrate that it is not the tax advantage so much as it is the nonprofit’s objective function that, ironically, leads it to generate more profit than its profit-seeking rival. Sansing (2000) explores the conditions under which a joint venture between a taxable for-profit and a nonprofit might be more socially efficient than competition between them. He constructs a Nash duopoly model in which the firms simultaneously choose their production levels of a homogeneous good. The nonprofit maximizes a combination of the profit it earns to fund its social purpose and the net value received by all customers served in the market, that is, consumer surplus; the for-profit firm seeks to maximize profit. Lien (2002) and Ferreira (2009) build on this model to consider the effects of the tax rate faced by the for-profit firm when demand is uncertain. Lien also modifies the model to allow the nonprofit to be concerned with the total surplus generated in the market, that is, the sum of consumer surplus, tax revenue, and after-tax profits. Goering (2008) and Flores and García (2016) show that if the nonprofit’s costs are high relative to its competitor’s, the nonprofit’s altruism might actually lead to a reduction in social welfare.

Kaneda and Matsui (2003) point out that, if the two firms have the same costs, the nonprofit with its concern for consumer surplus ends up making more profit than the firm that sets out to maximize profit, not because of its tax advantage but because of its altruistic concern for customers in the market. Kopel and Brand (2012) explore the conditions under which a socially concerned firm such as a nonprofit will earn higher profit than an explicitly profit-maximizing one. They find that deviating from profit maximization by putting a weight on consumer well-being increases shareholder value, but only up to a point. They note that hybrid organizational forms provide a potential avenue for achieving that profit.

When Lien (2002) allows the nonprofit’s altruism to extend to a concern with social efficiency, encompassing not only consumer surplus but also the profit and tax revenue generated in the market, he is allowing it the broad scope we might more naturally associate with a public enterprise. We model the nonprofit as having a more focused public purpose, such as the availability of health care or education, with no concern for the profits of its competitors and the taxes they generate, and indeed we see this as a fundamental distinction between a public enterprise and a private nonprofit enterprise. Similarly, we question whether a profit-seeking firm will have a public concern as broad as that of the nonprofit firm. We extend this literature on duopolistic competition by modeling the hybrid firm as having a narrower social concern, the consumer surplus going to its own customers, in contrast to the nonprofit’s concern with the total consumer surplus produced in the market.

The advent of the benefit corporation gives a for-profit duopolist the option of reincorporating as a hybrid firm with a customer-facing component of its objective function, a move with the potential to expand its market share and with expanded market share to increase its profits. What might competition against this sort of hybrid firm rather than a standard profit-maximizer mean for a commercial nonprofit who shares a market with it? To analyze this question, we model a hybrid firm that is primarily but not exclusively profit-seeking, and accountable to shareholders for both profit and social purpose.

Modeling Competition Between a Commercial Nonprofit and a Hybrid Firm

In this section, we model competition between a commercial nonprofit and a hybrid for-profit competitor of the sort represented by the benefit corporation, using competition between a nonprofit and a traditional for-profit as a point of comparison.

Each firm’s choice of how much to produce will depend on its objectives, its costs, and its constraints, and we consider these in turn. The firm’s choice also depends on the production decision of its competitor, because this affects the market price. We assume they compete in a market with just two firms and that, in equilibrium, their decisions are such that, given what the other firm is doing, each firm is doing the best it can. In the language of game theory, we seek Nash equilibria in a single-period simultaneous two-player game of quantity choice with a homogeneous good, tweaking the standard Cournot duopoly model to include our mission-sensitive firms. For simplicity, each firm faces constant average cost, 3 and market demand is linear.

We assume that the commercial nonprofit maximizes a weighted sum of all consumer surplus generated in the market and its own profit. Consumer surplus captures the benefits accruing to the market’s paying customers as the difference between the maximum amount they would have been willing to pay for the goods or services they purchased and the amount they actually paid, and we refer to this piece of the nonprofit’s utility function as intra-market altruism (IMA). Profit is assumed to be spent on mission-related activities that generate no revenue; this piece of the utility function is referred to as extra-market altruism (EMA).4,5

The central example of the mission-related activities funded by profit is the provision of the nonprofit’s commercial service at no charge to persons who cannot afford to participate in the market: Hospitals and health clinics provide charity care and schools give scholarships, for example. The only restriction of the model on the nature of this extra-market altruism is that it is assumed not to affect the market demand of paying customers or the nonprofit’s costs. This implies that profit cannot be spent on anything that materially changes quality in the eyes of paying customers, or to provide a public good that affects their demand for the purchased service. In the language of quasi-public goods, this is the assumption that consumers’ demand for the private aspects of the good is not affected by the provision of the public aspects of the good. This restriction rules out some interesting possible cases: For example, well-to-do families might be willing to spend more to send their children to a college whose generous financial aid brings together a diverse student body. The nonprofit may, however, devote its profits to a mission-related aspect of its services that does not affect consumers’ willingness to pay, funding a public good such as basic research or a dimension of quality that consumers are unwilling to pay for. For example, nonprofit hospitals may be early adopters of electronic recordkeeping and nonprofit colleges may devote considerable resources to periodically redesigning their general education programs, even though the value of their efforts is unseen by patients, students, and their families.

Finally, we assume that our nonprofit firm’s spending is limited by its revenues. In practice, donations allow a commercial nonprofit to spend more on its extra-market altruism than just its net revenue. For simplicity, we set the level of donations, grants, and so on at zero.

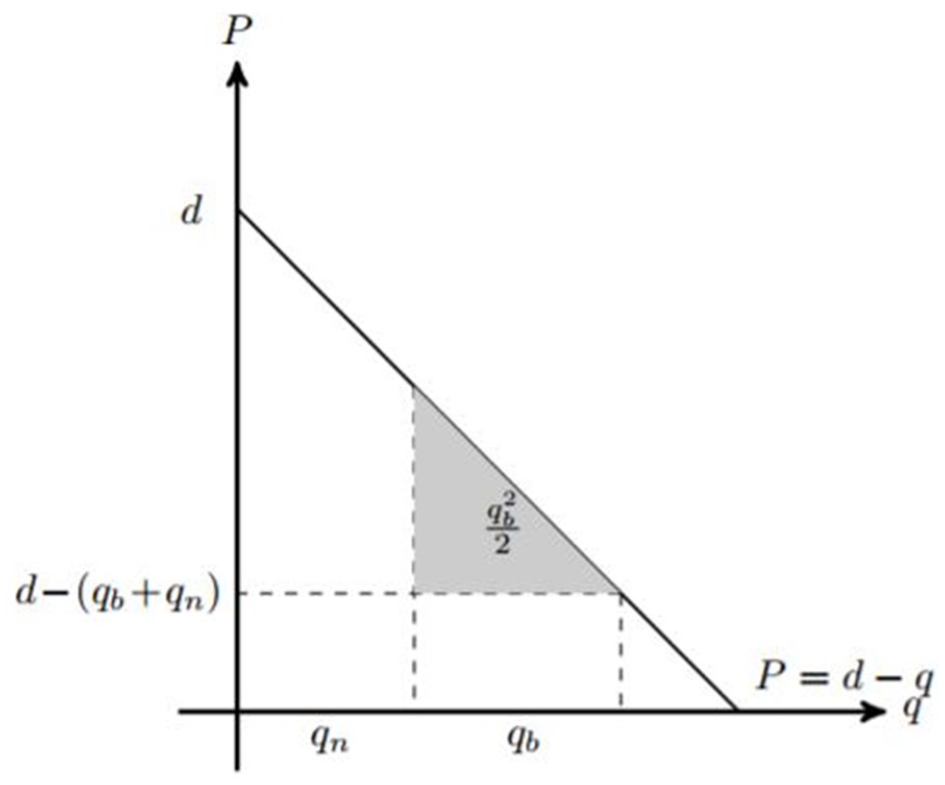

The hybrid firm, like the nonprofit, has an objective function that includes both profit and a measure of consumer surplus. Profit is divided between return to shareholders and the financing of extra-market altruism; EMA is attractive because contributions to social causes are readily documented and can address a wide range of social purposes. Consumer surplus is attractive in part because its pursuit increases market share. Because we are interested in hybrid firms of the benefit corporation sort, primarily profit-seeking but with an avowed social purpose, we constrain the hybrid to weigh profit at least as heavily as consumer surplus in its objective function. Because the hybrid must document its contribution to its declared social purpose, we model it as caring about its own contribution to consumer surplus, taking as given the amount of output produced by its nonprofit rival. Graphically, the consumer surplus that enters the hybrid’s objective function is the shaded triangle in Figure 1.

The hybrid firm’s addition to consumer surplus

The traditional for-profit firm is assumed to maximize profit. We allow its constant per-unit cost of production to differ from those of its nonprofit and hybrid counterparts, reflecting potential differences in taxes and subsidies, access to financing, stakeholder commitments that affect costs, and so forth.

More formally, we consider a model in which firms compete in a market with linear inverse demand p = d – q, where q is the sum of the firms’ output sold in the market. Firms make their quantity choices simultaneously; the objective functions of the nonprofit, benefit corporation, and traditional for-profit firm, respectively, are:

where

In the Technical Appendix, we solve for Nash equilibria in simultaneous, one-period games in which the firms choose their level of output. We consider in turn the cases in which (1) the nonprofit firm has the market to itself, (2) the nonprofit competes against a standard for-profit firm, and (3) the nonprofit competes with a benefit corporation. These models yield the results that are discussed next.

Results

Nonprofit Monopoly

Before discussing market equilibria when a nonprofit competes with a for-profit or a hybrid firm of the benefit corporation type, we briefly consider the case of a nonprofit facing no competition at all. When a nonprofit firm maximizes a weighted sum of the consumer surplus of the customers in its market and the profit generated to fund charitable services, and is not allowed to operate at a loss, we get

Result 1

If the nonprofit monopoly places sufficient weight on consumer surplus, it will operate at the efficient level, producing where price equals marginal cost and consumer surplus is maximized, even though the nonprofit places positive weight on the ability to provide charitable services.

When firms are profit maximizers, monopoly is a well-known source of market inefficiency. The commercial nonprofit’s concern with consumer surplus is a natural countervailing force, and if the nonprofit cared only about consumer surplus then we would expect it to operate at the efficient level, which maximizes consumer surplus. We note that even when a nonprofit firm places positive weight in its objective function on the provision of charitable services, it will limit its activities to its commercial ones if its weight on consumer surplus is greater than or equal to the weight on dollars raised for charity care. The converse does not apply: If the nonprofit firm places even a little weight on consumer surplus, it will deviate from the profit-maximizing level of output that would raise the most funds for charity care.

Competition Between a Commercial Nonprofit and a Profit-Maximizing Firm

This is the case that has been developed by others (Goering, 2008; Kopel & Brand, 2012; Lien, 2002; Sansing, 2000) and it serves as a benchmark below in our analysis of competition between a nonprofit firm and a hybrid firm of the benefit corporation type. The case is interesting in its own right, however, because one result is of great interest to a discussion of hybrid firms. As explored by Kaneda and Matsui and by Kopel and Brand (Kaneda & Matsui, 2003; Kopel & Brand, 2012), if the for-profit and nonprofit firm have the same costs of production, the nonprofit firm will generally make more money than the for-profit firm. This happens because the nonprofit’s concern with consumer well-being causes it to increase the quantity it produces: In equilibrium, the nonprofit has a larger share of the market—and of its profits—than does the for-profit firm. In other words, “Firms whose realized profits are the largest are not generally those that have the profit maximization objective” (Kaneda & Matsui, 2003).

What, then, is a would-be profit-maximizer to do? Incorporating as a nonprofit is no help, because of the nondistribution constraint. But incorporating as a hybrid firm with some commitment to intra-market altruism provides an approach to maximizing profit. However, too much IMA will expand production too much, depressing both firms’ profits: “[I]t pays off to take stakeholder interests into account, but not too much” (Kopel & Brand, 2012, p. 982). This is the sort of hybrid firm that the benefit corporation represents, primarily focused on profit but with room for management to show concern for customers.

Brakman Reiser and Dean (2017) caution that the double bottom line creates trust and commitment problems for the hybrid enterprise as its various constituents prefer different balances between profit and mission (Brakman Reiser & Dean, 2017). The economics literature on mixed-market competition adds an interesting wrinkle to this line of inquiry. The savvy profit-centered investor may realize that a formal commitment to “expanding community access and keeping prices down” or some similar nod to consumer surplus can pave the way to increased profits. Our model of the benefit corporation, which collapses to the case of a traditional profit-maximizer as its emphasis on intra-market altruism goes to zero, allows us to formalize this argument that the benefit corporation seems well suited to addressing the management challenges facing would-be profit maximizers who find themselves in competition with a nonprofit firm (Goering, 2007; Kopel & Brand, 2012).

Result 2

If a traditional profit-maximizing firm sharing a market with a nonprofit firm can, without increasing its per-unit costs, reincorporate as a benefit corporation and thereby create a credible commitment to a small enough level of concern with the consumer surplus it generates, it has an incentive to do so, because its profit will increase.

Competition Between a Commercial Nonprofit and a Benefit Corporation

Just as a nonprofit firm’s interest in consumer surplus increases its market share when competing against a profit-maximizing firm, the benefit corporation’s intra-market altruism takes market share away from a nonprofit competitor while expanding the overall quantity produced. As the nonprofit’s competitor places more value on the consumer surplus it generates, it increases its output. The nonprofit responds by decreasing its output to protect its net revenue, but never by more than the competitor increased its output, so the net effect is increased or constant total market output.

These observations build the intuition for the effect of a change in the nonprofit’s competitor’s intra-market altruism on the nonprofit’s influence both within and outside the market:

Result 3

Suppose that in a nonprofit-hybrid duopoly, the hybrid firm’s emphasis on intra-market altruism increases. This causes the nonprofit’s level of output to fall, and its profit, if positive, to decrease as well.

This is our central result: When its competitor becomes more altruistic within the market, the nonprofit becomes more limited in its own altruistic impact, producing less and raising less money to fund charity care. In this sense, the nonprofit has a greater impact when competing against a traditional for-profit firm than when competing against a hybrid firm. 6

It does not follow, however, that a nonprofit will necessarily prefer to share a market with a traditional for-profit firm rather than with a hybrid firm. This is because we allow our nonprofit to have a broad commitment to social well-being, caring about a social purpose and not just its own contribution to it. Whether it is better off competing against a traditional for-profit or alternatively a hybrid firm will depend on the relative cost advantages of the different firms and on the extents to which intra-market altruism motivates the hybrid firm and the nonprofit itself.

Discussion and Directions for Future Research

When a commercial nonprofit shares a market with a hybrid firm, our model suggests that it matters a great deal what the nature of the two firms’ altruistic concerns are. If the nonprofit operates in a market solely to generate profit to support charitable activities, the nonprofit is best off if its hybrid competitor is also interested only in social purposes unrelated to the market’s paying customers. In this case, the hybrid’s altruism has no impact on its behavior in the market it shares with the nonprofit: Both the nonprofit and the hybrid behave as if they were profit maximizers. The consumers in the market may actually be made worse off by being served by these altruistically minded firms than if they were served by profit maximizers: If nonprofits and hybrids operate at higher costs than traditional for-profit firms, perhaps because both have costly commitments to their workers or suppliers, these higher costs can lead to an equilibrium with higher price and less output than would have been provided by a traditional for-profit duopoly.

A hybrid firm of the sort represented by the benefit corporation, principally profit-seeking but with a declared public purpose, can represent a more powerful presence than a traditional for-profit firm when competing with a nonprofit firm. As hybrid firms increase their level of intra-market altruism, nonprofits experience decreases in both the quantity they sell and the amount of net revenue they generate for charitable purposes. The hybrid firm’s interest in producing consumer surplus is unambiguously bad news for a nonprofit that is wholly concerned with generating net revenue to fund charity care.

The type of nonprofit that should most welcome the arrival of hybrid firms is the nonprofit that operates in a market because it is centrally concerned with the welfare of the customers in that market. Early childhood education facilities, nursing homes for low-income elderly, drug rehabilitation centers, and family-planning clinics are examples of service delivery nonprofits that are devoted to the well-being of their customers and might plausibly applaud the expansion of the capacity of other service providers in their area.

While the welfare of paying customers for these important services is increased by its competitor’s intra-market altruism, the nonprofit’s ability to provide charity care is curtailed. It follows that, if the amount of profit that the hybrid corporation devotes to charity care is sufficiently small, the emergence of hybrid firms will redistribute welfare from those outside the market to paying customers within the market. In industries such as health care and education, this has the potential to exacerbate inequalities between the insured and uninsured, and those who can and cannot afford to pay tuition.

Besides their paying customers and their clients receiving charitable services, nonprofit organizations may honor costly commitments to the well-being of other stakeholders, such as their workers or their suppliers, and costly commitments can give a cost advantage to their competitors. Intra-market altruism alone is not sufficient to drive a nonprofit out of the market: to monopolize the market, its competitor must have a cost advantage over the nonprofit organization. However, it can be shown that the required cost advantage over the nonprofit is smaller in the case of a hybrid firm that displays intra-market altruism than in the case of a traditional for-profit competitor. The model cautions that the arrival of competitors with a concern for consumer surplus may limit the nonprofit’s ability to make costly commitments to the well-being of other stakeholders.

This analysis suggests avenues for future research, both formal and applied. We model producers as simultaneous quantity choosers who care about consumer surplus; there may be important contexts in which nonprofits strategically choose quality, care about quantity, are able to move first, and so on. A firm’s extra-market altruism might be allowed to affect the demand for its product, perhaps serving as a virtue-signaling advertisement.

We model the hybrid for-profit firm as accountable to shareholders by restricting their claims of consumer surplus creation to the extra surplus created when the hybrid’s output is added to the nonprofit’s output. Because the hybrid’s social purpose may be distinct from the market in which it operates, we model the hybrid’s extra-market altruism as irrelevant to the nonprofit. In specific settings, other assumptions may be of interest.

We have focused on the consequences for commercial nonprofits of competition with hybrid firms. Pivoting to questions of economic efficiency, it can be shown (see Result 4 in the Technical Appendix) that, unless the nonprofit firm has a cost advantage, the economic surplus generated in the commercial market unambiguously increases with the hybrid’s emphasis on intra-market altruism. If a for-profit firm can reincorporate as a hybrid without increasing its per-unit costs of production, it follows that more economic surplus is generated in the commercial market when the nonprofit competes with a hybrid firm than with a purely for-profit firm. While this result may be of interest in its own right, understanding the broader implications for efficient (not to mention equitable or just) resource allocation will generally involve modeling the firms’ charitable uses of the money raised in the commercial market (Eckel & Steinberg, 1993).

Scholars have explored the impacts on an organization’s publicness—the degree to which its commitments, behaviors, and governance resemble those of public institutions—of the sector in which the organization is located and the resources available in its environment (Bozeman, 1987; Moulton & Eckerd, 2012). In our model, in accordance with publicness theory, allowing a for-profit firm to reincorporate as a public-facing benefit corporation increases its publicness: it serves more customers at a lower price, and it undertakes charitable activity. Function follows form. What is intriguing, and not generally stressed in publicness or resource theory, is that the organizational forms of these other organizations have implications for the functioning of nonprofit organizations themselves. While anyone familiar with the American crises of medical bankruptcy and student loan debt is likely to agree that lowering prices and expanding access to medical care and higher education are in the public interest, market transactions between buyer and seller are quintessentially private-sector behaviors. Our nonprofit organization, finding itself sharing a market with the more public-facing benefit corporation, faces incentives to behave less publicly, scaling back the resources it devotes to its public purposes beyond the well-being of its paying customers. While this particular reaction is driven by the structure of our model, the lesson is general: in thinking about the influence of an organization’s environment on its behavior, it can pay to look beyond resources and regulations to its rivals as well.

A similar caution applies to the study of mission drift. Mission drift is defined as “a process of organisational change, where an organisation diverges from its main purpose or mission” (Cornforth, 2014). It is often attributed to “founder’s syndrome” as the sway of an influential founder recedes, to resource dependency on a primary revenue source, to changes in the regulatory environment, or to a shift in the organization’s values that emerges from the tension between the logic of the market and the logic of social purpose (Cornforth, 2014). In our model, as its competitor adopts a hybrid form, the nonprofit reduces its level of charity care while serving its paying customers at a reduced price. This changed behavior on the part of the nonprofit looks like mission drift when in fact its competitor’s mission drift has changed the nonprofit’s best strategy for pursuing its unchanged mission. A change in strategies may reflect a change in mission or it may instead reflect a successful navigation of changes in the environment in which an enterprise functions. Our analysis underscores the importance of market conditions—or, in the parlance of the nonprofit zoo, the importance of habitat—to the study of mission drift in social enterprises.

Footnotes

Technical Appendix

Author’s Note

The authors thank Al Slivinski and four anonymous referees as well as the editors of this journal for their insightful comments on earlier drafts. We gratefully acknowledge financial support from Pomona College.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors gratefully acknowledge research support from Pomona College.