Abstract

Introduction

The public health sector is complex, unpredictable, and characterized by unique elements. Citizens, not shareholders, are primary stakeholders as healthcare is mostly funded by general taxation. 1 Community and lobbying groups are increasingly requiring non-financial information disclosure. In response, Public Healthcare Organisations (PHOs) have introduced several social initiatives over the past decades to improve corporate performance. 2 Sustainability budgeting and reporting are essential for meeting stakeholder needs and enhancing transparency, helping organisations to measure, disclose and communicate sustainability actions whilst ensuring accountability. Furthermore, PHOs arguably have greater moral obligations to report on sustainability issues, as they provide services in the public interest. 3 Sustainability accounting and reporting are key tools for disclosing social impacts on reference communities 4 and improving accountability and transparency. Indeed, according to the Global Reporting Initiative, Sustainability reporting is the practice of publicly disclosing an organization’s most significant economic, environmental and/or social impacts, and hence its contributions – positive or negative – toward the goal of sustainable development. The United Nations (UN) 2030 Agenda and Sustainable Development Goals (SDGs) were introduced in 2015 for organisations to measure and communicate performance in environmental and social terms. SDGs are more prevalent in the private than the public sector 5 with limited adoption in the public sphere, particularly healthcare, often focused on SDG3 ‘Good health and well-being’. 6 Studies show attitudes toward sustainability reporting vary by country priorities and integration of sustainability with state-specific issues, thus the adoption of sustainability reporting and SDG integration in the public sector needs to be observed at country level. 7 Italy has a regionally decentralised healthcare system with different governance and organisational mechanisms, thus representing a natural experiment to study sustainability accounting and reporting adoption attitudes. 8 This study examines whether and how the Italian healthcare context has embraced sustainability accounting and reporting practices, and the role played by institutional pressures, by checking if the specific sector has developed those pressures that move organisations towards the adoption of sustainability disclosure, as stated in the institutional theory. 9

In this light, this study critically observes the contents of the official healthcare programming and reporting documents of the Italian National Healthcare System and the strategic integration of the SDGs. A substantive commitment to transparency, a symbolic response to external legitimacy pressures, or if the institutional response remains absent. Understanding these dynamics is crucial, as the Italian ‘natural experiment’ can reveal how regional governance diversity influences the depth and quality of sustainability reporting, potentially offering a scalable model for other fragmented public sectors.

In line with these premises, our Research Questions are:

Theoretical framework

Institutional theory

Institutional theory suggests that organisations adopt sustainability reporting in response to various pressures, including peer influence, to achieve conformity within their organisational field. 10 Pressures can be coercive, mimetic, cognitive, normative, or internal. Coercive pressures arise from the need to comply with regulations to avoid penalties, such as mandatory sustainable accounting and reporting systems. 11 Research indicates that countries with specific sustainability regulations report higher adoption rates. However, for state-owned enterprises in Europe, mandatory reporting regulations appear to have little impact on the propensity for sustainability reporting. 12 Mimetic pressure drives organisations to align with others in their sector to achieve comparable or superior performance. It occurs when organisations adopt successful practices from their peers rather than developing independent solutions. Literature highlights that coercive and mimetic pressures significantly influence accounting and reporting practices in public sector administrations, which are more susceptible to these pressures than private or non-profit organisations. 13 Cognitive pressure arises from adherence to shared beliefs or models regarded as ‘correct’, shaping decision-making through mental models that influence evaluations and organisational choices. 14 Cognitive schemas significantly influence decision-making, with the adoption of sustainability reporting mediated by the perceptions of strategic decision-makers. 15 Normative pressure reflects values, conventions and societal expectations driven by professionals, academics, institutions and influential organisations. Internal personnel expectations may reinforce this pressure; market-driven companies tend to prioritise non-financial reporting, whilst socially driven organisations focus on socially oriented practices. 16 Internal institutional pressure involves employees influencing sustainability reporting by requiring non-financial disclosures, serving as stakeholders with specific information needs, or advocating for internal processes to align with external expectations, thereby impacting high-level decisions. 17 In healthcare, personnel may prioritize tangible actions over reporting, given their focus on patient care. Few researchers have explored Institutional Theory in sustainability reporting adoption, highlighting the need for further studies on institutional context as a key driver. 18 There is also growing interest in approaches and frameworks for sustainability reporting. Public healthcare organisations often employ bottom-up approaches, focusing on community-specific issues without standardised practices, whereas top-down approaches align with international standards and comparable metrics. Framework discussions emphasise the integration of sustainability and financial reports, as standalone reports are less valued in performance evaluation unless integrated with financial data. Integrated reporting, which combines financial and non-financial information, is increasingly recognised as enhancing public sector sustainability reporting. 19

The case study

The Italian Healthcare System (IHS) is based on the universal Beveridge model; healthcare services are provided and financed by the government through general taxation. Since the 1990s, legislative reforms in Italy have transferred political, administrative, fiscal and financial healthcare responsibilities to 19 regions and two autonomous provinces (APs). The IHS operates at national, regional, and local levels. The central government sets core health benefits and allocates resources via taxation. Regional governments oversee health plans, strategies, budgets, and service quality. Local Health Authorities (LHAs) provide primary, secondary, and tertiary care through direct services or outsourcing to public or private providers, including hospitals and research facilities (IRCCS). 20 All LHAs annually publish their budget forecasts and their financial statements according to the law 118/2011 21. 21 Italy transposed the European Directive 2014/95/EU into national law through Legislative Decree No. 254 of 30 December 2016. In line with the novel Corporate Sustainability Reporting Directive (CSRD) 22, the Italian government has transferred the Directive into the national Legislative Decree No. 125 of 6 September 2024. Although no specific obligations exist for PHOs, national standards for public sector social reporting were established by the Gruppo di Studio per il Bilancio Sociale (GBS).

Method

Research protocol and data collection

The researchers employed document analysis as a qualitative research method of data collection and analysis 22 which involves a systematic process of reviewing, evaluating, and synthesising data from documents. The Research team obtained the most recent list of healthcare organisations from the Italian Ministry of Health website2 and included all PHOs in the analysis. Two researchers visited the official websites of these organisations to check for the presence of social reporting and financial documents. The first step involved visiting the ‘Transparent Administration’ section of the websites. The second step utilized the webpages’ search bars to locate social reporting documents using keywords such as “sustainability report,” “mandate report,” or “social report.” This was supplemented by a third step of using search engines to find eports by searching for the healthcare organisation’s name combined with the keywords mentioned. Forecast budgets and financial statements were downloaded from the ‘Bilanci’ section within the ‘Transparent Administration’ area. Sustainability reports and budget/financial statements are referred to as ‘monitoring reports’ and were analysed together, as they follow the same reporting structure according to Law 118/2011. The researchers explored 790 organizations’ websites. Furthermore, 21 regional websites were surfed to search for regional programming socio-sanitary plans (hereafter “regional programming reports”). Italian PHOs and regional authorities represent the unit of analysis, while regional programming and monitoring reports the unit of measurement. When plans were not available on the websites, they were obtained from the AGENAS (the Ministry’s technical agency) website3. Documents that could not be accessed or read (non-navigable) were excluded from the analysis. The exclusion of non-navigable documents was necessary to ensure the linguistic software (NVivo) could perform an accurate automated content analysis. Including non-readable files would have introduced “silent data” gaps, potentially skewing the frequency counts and pattern recognition. Despite these exclusions, the final sample remains representative of the current disclosure state of the Italian National Healthcare System, as it reflects the information actually accessible to stakeholders. The research team analysed programming and monitoring documents to examine how regional reports incorporate SDGs and sustainability in annual/long-term plans and during monitoring. Once sustainability concerns were identified, the researchers explored their connection to the financial dimension of healthcare organisations at both stages. The researchers excluded documents published before SDGs launch (2015), alongside the European Directive 2014/95/EU. The 2015–2022 period was chosen due to the normative pressure from both the SDGs publication and the Directive. The year 2022 marks a key milestone with the Corporate Sustainability Reporting Directive (CSRD), which mandates organisations to report on environmental and social impacts and requires third-party assurance of the information disclosed. 23 This is expected to lead to a significant increase in reporting and a shift from economic to governance-focused sustainability disclosure. In terms of methodological robustness, the adoption of temporal, technical, and substantive thresholds ensures contextual relevance to the post-2030 Agenda era, maintains analytical precision by allowing accurate NVivo processing, and guarantees data reliability by focusing exclusively on official governance documents accessible to stakeholders.

Data analysis

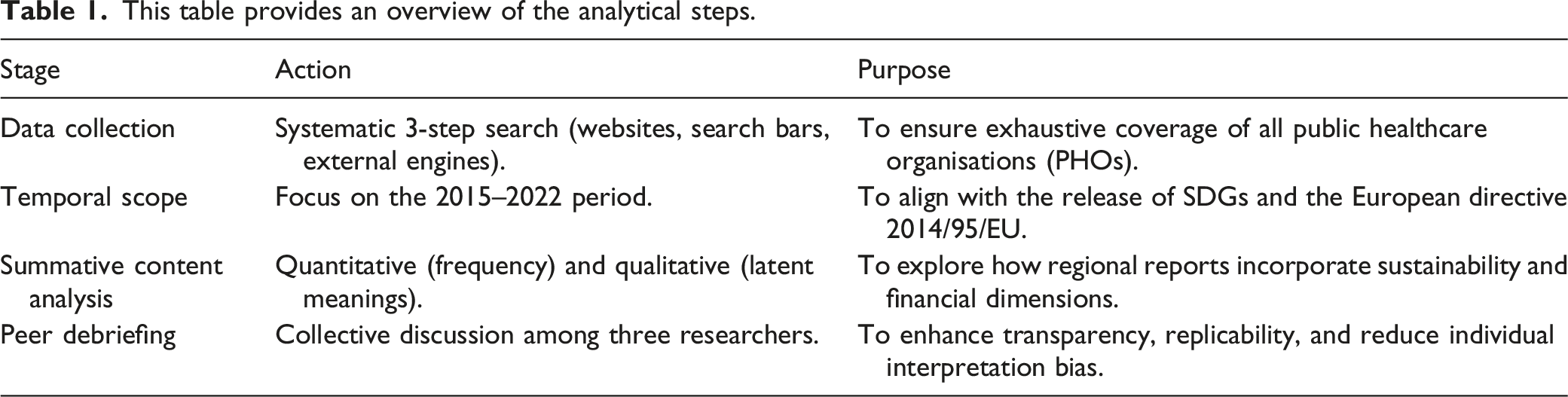

This table provides an overview of the analytical steps.

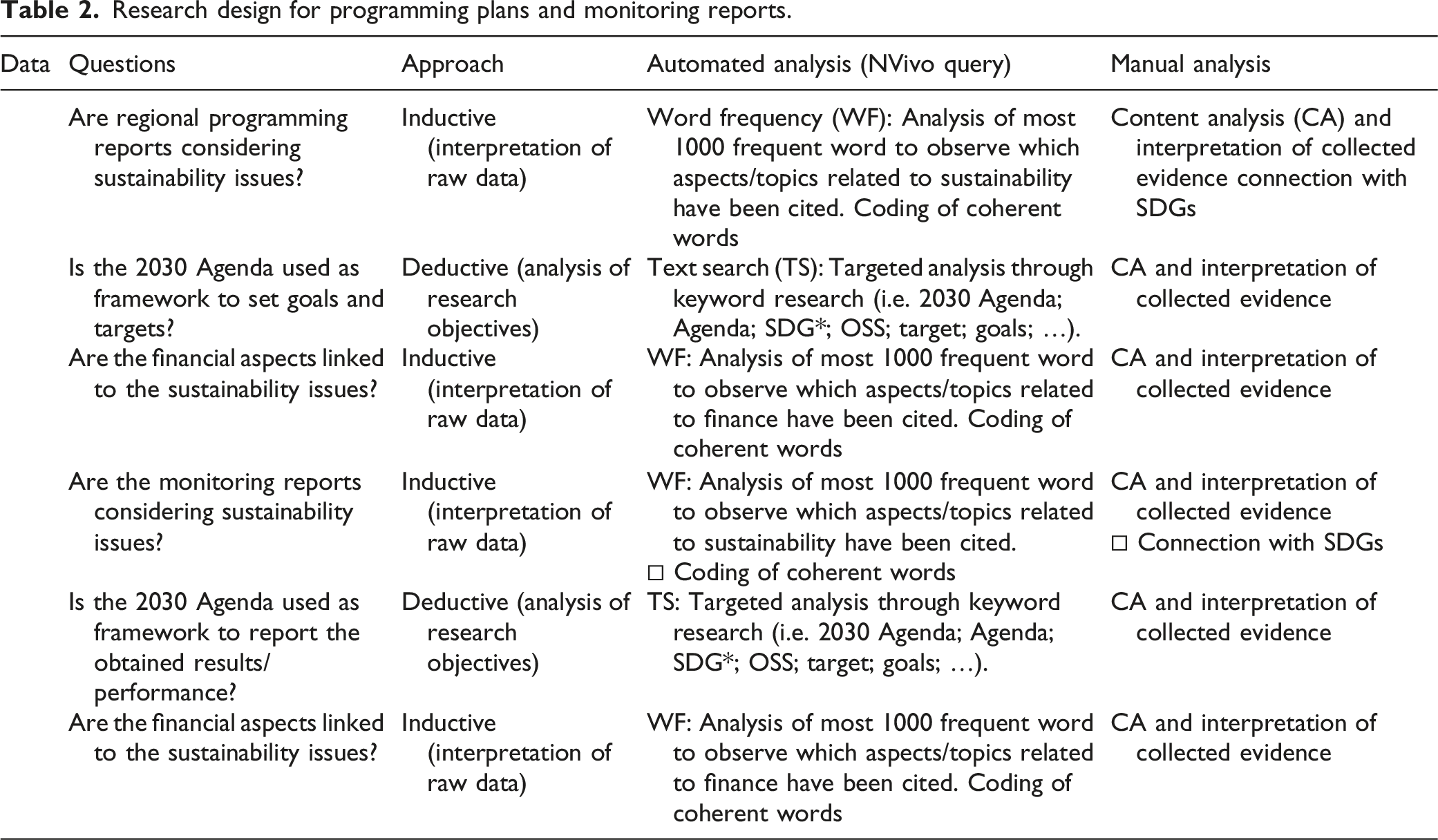

Research design for programming plans and monitoring reports.

Results

Results of the empirical analysis

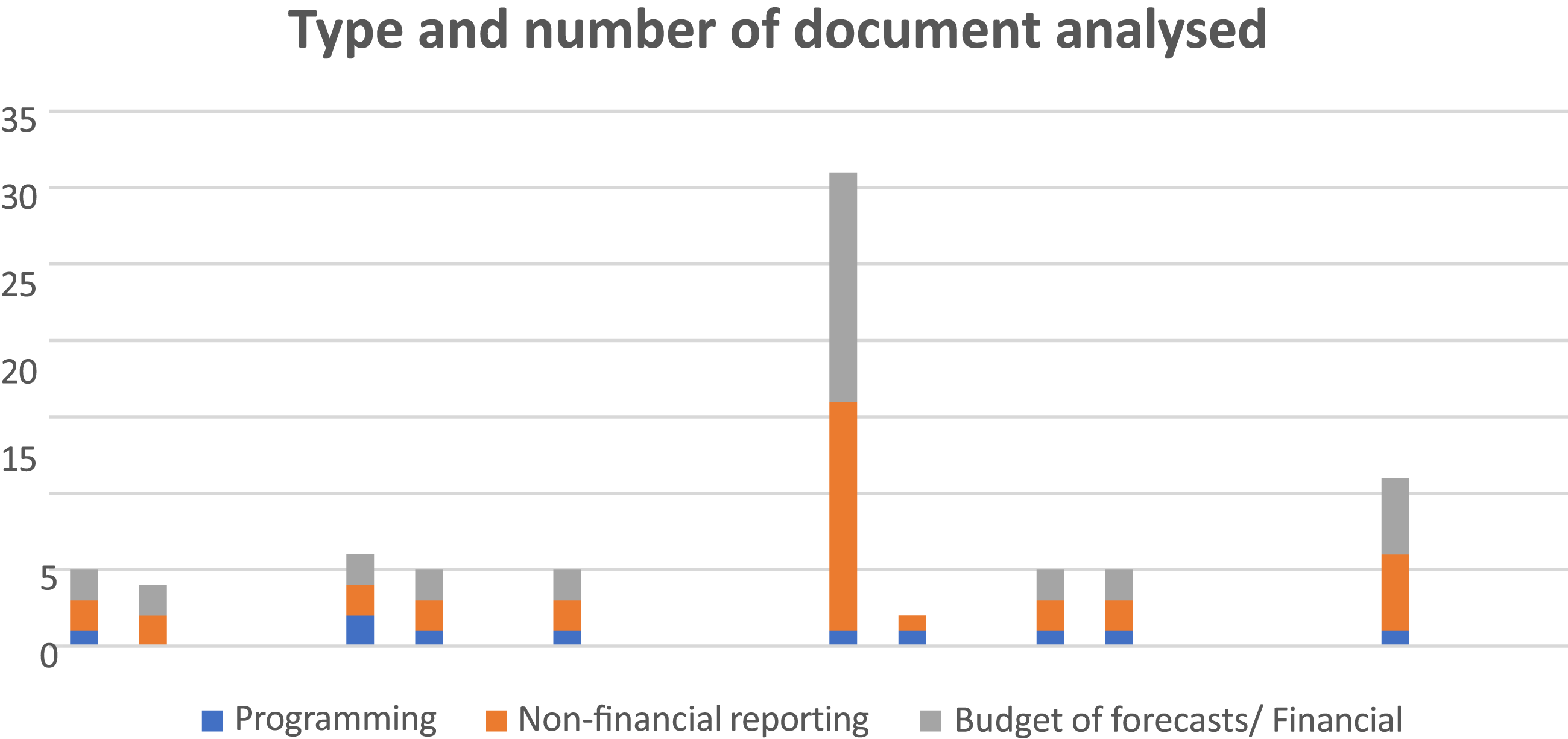

The researchers analysed 80 documents in total: 10 from the regional programming phase and 70 from the corporate monitoring phase (Figure 1). Although the research team visited 811 websites, 568 organisations did not publish the documents (568/811 = 70%). For a further 183 organisations (183/811 = 23%) the material retrieved was non-navigable or even obsolete (not referring to the period selected for the analysis 2012–2015). Documents analysed come from 60 organisations including regional authorities (9/60 = 15%), LHAs (45/60 = 75%) and university hospitals (6/60 = 1%). This result is in line with past literature on the topic.

26

As reported in the methods section, Italian public healthcare organisations and regional authorities represent the unit of analysis, whilst regional programming and monitoring reports the unit of measurement of this study. Type and number of document analysed.

Results of the empirical analysis.

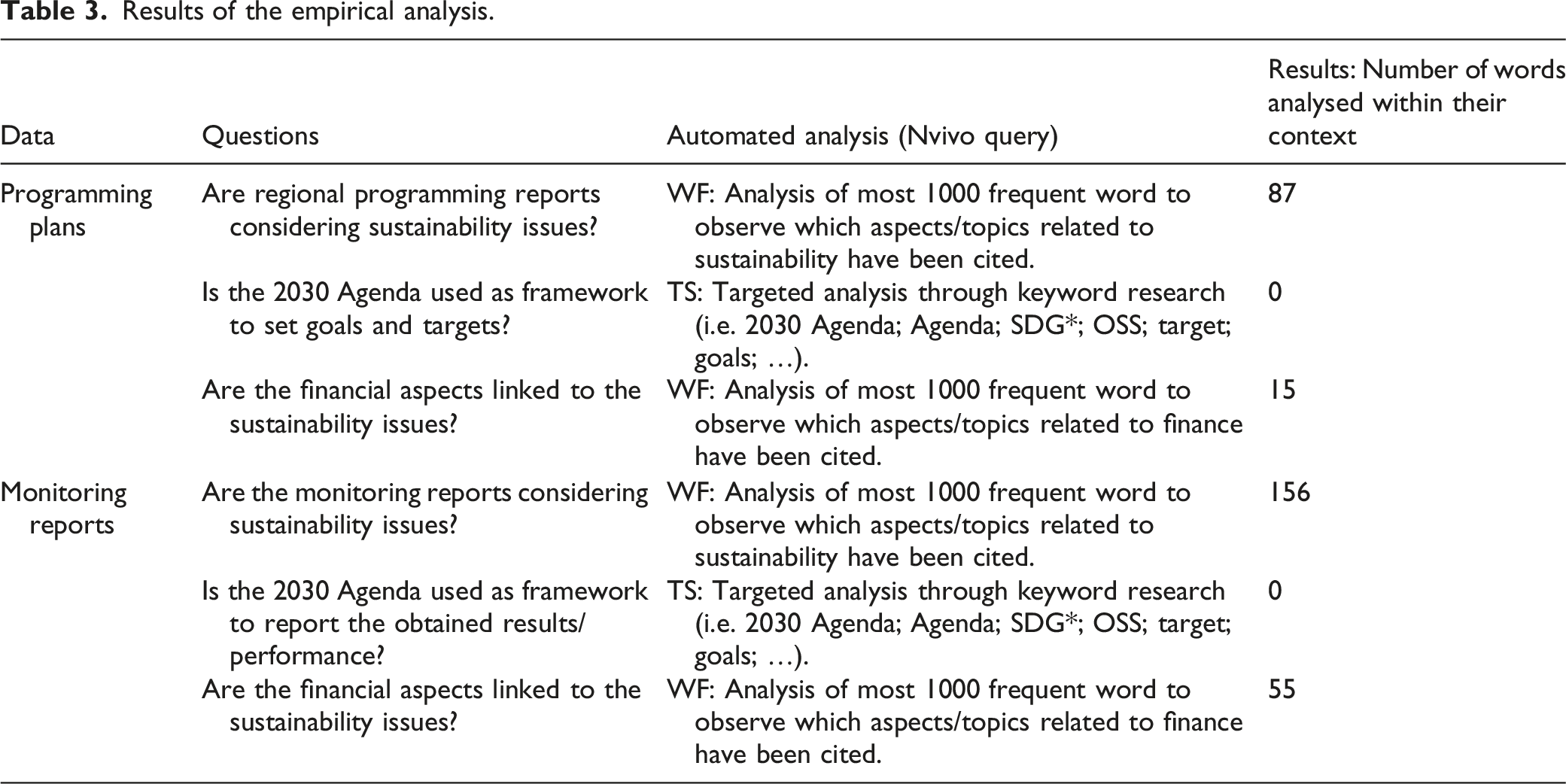

The programming documents contained 87 sustainability-related words, whereas the monitoring reports contained 156 sustainability-related words. These findings are partly attributable to the numerical difference between the two document clusters. However, further insights emerge from analysing which SDGs were potentially addressed by the identified words.

Programming level results

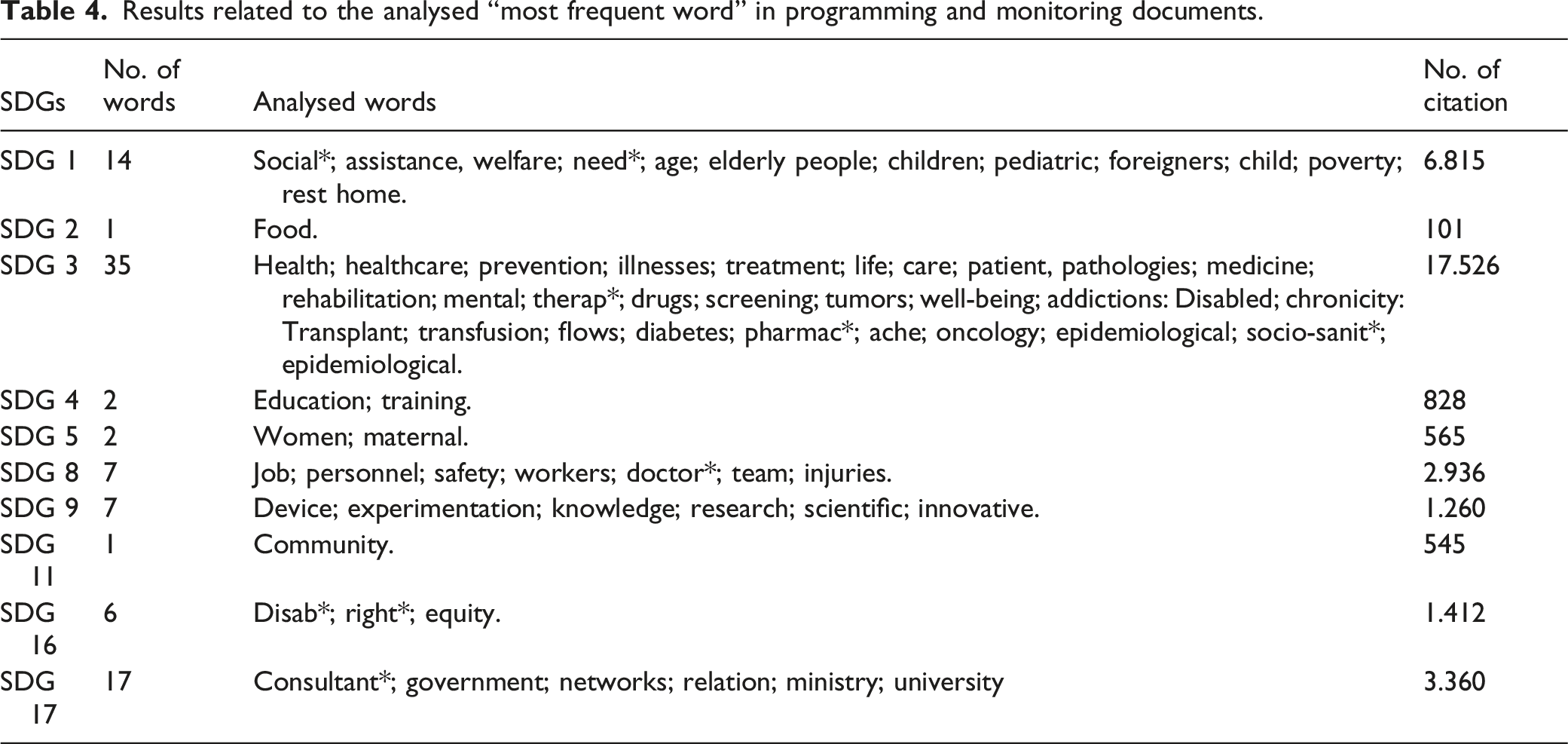

Results related to the analysed “most frequent word” in programming and monitoring documents.

Potential connections emerged between the content of programming documents and the SDGs. The classification through the SDGs lens has the scope to understand how the organisations could contribute consciously to the achievement of a more sustainable scenario. Specifically, poverty (SDG 1) was discussed primarily in terms of equitable access to services and support (Targets 1.3 and 1.4), whilst food security (SDG 2) was discussed in terms of access to food and nutritional quality. Education was linked to workforce development and training, whilst gender equality was addressed through maternal health (Target 5.6); the economic growth (SDG 8) has been linked to all the work-related aspects such as safe and secure working environment or the full and productive employment (Target 8.5 and 8.8). All the content related to innovation, research have been linked with Build resilient infrastructure, promote inclusive and sustainable industrialisation and foster innovation (SDG 9). Moreover, the researchers found connection with the access affordable and basic services (SDG 11), and with the inclusivity and equality (SDG 16). Finally, the programming documents have discussed the importance of their relations with the university, with governments and with local networks (SDG 17).

Monitoring level results

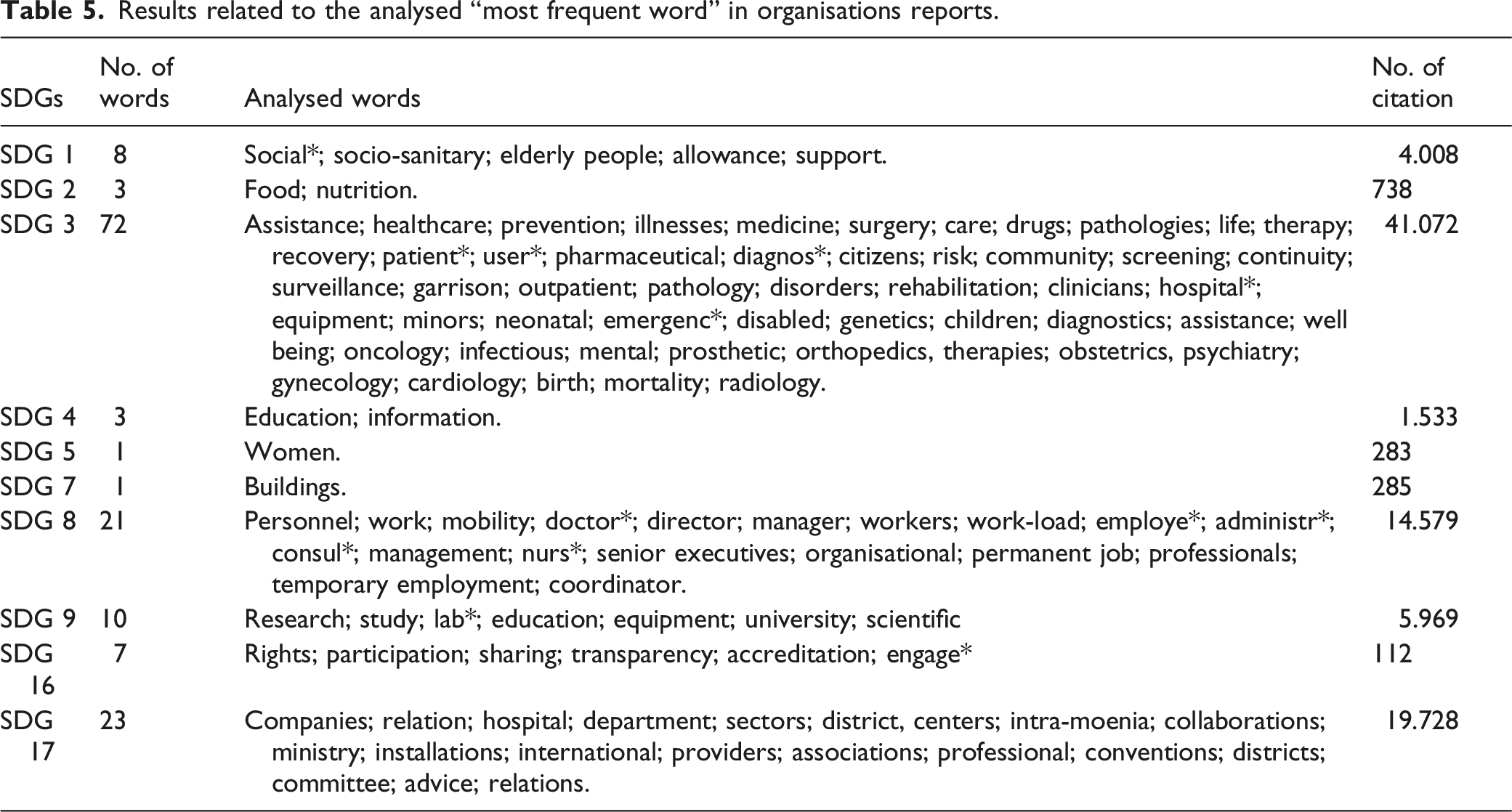

Results related to the analysed “most frequent word” in organisations reports.

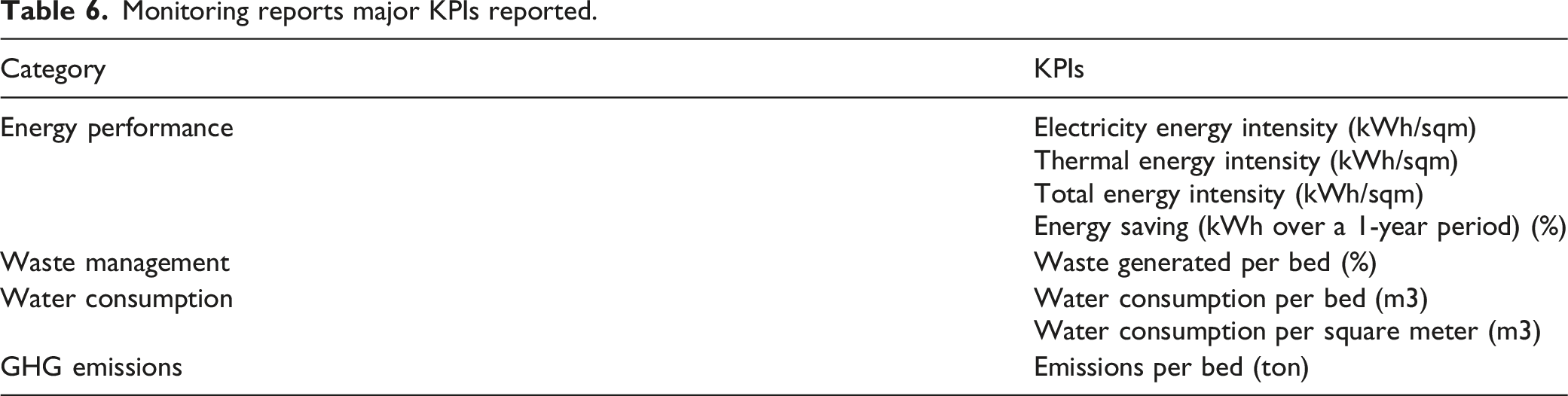

Notably, monitoring reports included environmental key performance indicators (KPIs). The main KPI categories were: energy performance, waste management, water consumption and greenhouse gas emissions.

Monitoring reports major KPIs reported.

Sustainability and finance

None of the 70 financial terms were used in relation to sustainability. Analysis revealed that these terms focused exclusively on financial performance, without connection to sustainability topics. Furthermore, budget forecasts and financial statements strictly adhered to the legal requirements of Law 118/2011, and did not reference how energy efficiency improvements might reduce resource consumption or carbon dioxide emissions. Financial documents reported hospital costs solely in terms of heating expenditure, electricity consumption and other utilities, as noted in previous literature. 29 Our findings indicate that financial topics remain disconnected from sustainability aspects, despite the potential for sustainable practices to offer financial benefits. Law 118/2011 mandates the harmonisation of accounting systems and budget plans for regions, local authorities, and healthcare organisations, but it does not address sustainability issues. To date, no amendments to the legislation have been discussed or approved regarding sustainability reporting. Furthermore, no additional sustainability-related documents are required from healthcare organisations as supplements to legally mandated financial reports. At the monitoring level, it is challenging to frame results within a framework that was overlooked at the planning stage.

Discussion

This study reveals a significant decoupling between the operational existence of sustainability themes and their formal reporting. Although content analysis identified a substantial number of sustainability-related terms (243) across programming and monitoring documents, these remain fragmented and largely disconnected from international standards such as the SDGs and the 2030 Agenda. Critically, the findings reveal a complete absence of integration between financial data and non-financial performance metrics, as evidenced by the lack of correlation between the 70 financial terms analysed and sustainability initiatives.

This suggests that, although Italian public healthcare organisations are addressing sustainability issues implicitly, the absence of a structured accounting framework prevents the translation of these efforts into transparent, strategic disclosure, leaving sustainability as an implicit rather than explicitly managed institutional objective. The primary finding is the absence of institutional pressures that would promote or facilitate the development of sustainability reports or the incorporation of sustainability issues and SDGs. While the data suggest a lack of formal pressure, these findings should be interpreted within the specific boundaries of the Italian regionalized context. This ‘decoupling’ may not reflect a total absence of commitment, but rather a transitional phase where informal practices have yet to be formalized into the structured reporting frameworks typical of the public sector. According to the literature, organisations are motivated by coercive pressure to conform to normative standards and avoid penalties. 30

Healthcare organisations are not required to produce sustainability reports under the NFRD or CSRD. There is no regulatory obligation to address global priorities like the 2030 Agenda, which does not exert coercive pressure. While healthcare organisations must create programming plans, these plans lack references to sustainability and do not integrate trends from the private sector. Normative bodies could drive this shift through specific regulatory requirements. Additionally, many programming documents replicate previous versions with minimal modifications. Some regions have extended their plans without substantive revisions, making it impossible to incorporate subsequently introduced frameworks such as the SDGs. The 2030 Agenda appears not to be utilised as a reporting framework. Consequently, it is unlikely that monitoring reports will incorporate references to institutional frameworks such as the 2030 Agenda that are disregarded at the programming level. Historically, Italian PHOs have published few sustainability reports. Despite Italy’s multi-level healthcare system, individual organisations independently determine their social reporting and sustainability initiatives. There is no coordinated national or regional strategy for hospital sustainability; instead, the landscape is fragmented, with individual initiatives left to the discretion of a few practitioners who have developed a specific sensitivity to the issue.31,32

The second lacking pressure is the mimetic one. Such pressure should drive organisations to align with others operating in the same sector to achieve or exceed comparable performance levels. 11 This pressure can create a virtuous cycle amongst competing organisations. However, sustainability reporting and the use of the SDGs as a framework are predominantly found in the private sector. As the literature shows 32, PHOs do not view themselves as competitors to private organisations nor feel compelled to emulate them, resulting in a lack of mimetic pressure in this sector. Sustainability is typically managed by local organisations rather than through high-level planning. In contrast, other countries, such as Portugal, include sustainability in national plans that are cascaded down (e.g., the Sustainability and Resilience in the Portuguese Health System). 33 This case serves as a relevant benchmark because it demonstrates how a centralized ‘top-down’ mandate can effectively integrate sustainability into a national health strategy. Unlike the fragmented Italian approach, the Portuguese model creates a direct link between national policy goals and local hospital performance, providing a clear regulatory roadmap that triggers both coercive and mimetic responses.

An ongoing debate concerns the impact of mandatory or strongly recommended non-financial information disclosure. Whilst mandatory disclosure promotes transparency and accelerates reporting, it may shift organisational priorities towards satisfying stakeholder interests without considering shareholder concerns.

The third institutional pressure that may be lacking is the cognitive pressure, likely tied to healthcare organisations’ mission. The adoption of shared mental models and beliefs considered “correct” or “valid” 30 is closely linked to the core mission of healthcare, which prioritizes patient care above all else. This focus results in reduced emphasis on other sustainability dimensions, such as environmental impact, reflecting limited awareness of broader sustainability issues. Although PHOs often underperform on environmental sustainability, they typically excel in social performance, particularly in relation to societal well-being. Some hospitals utilise social reports to highlight their social contributions. Social reporting is more prevalent in regions where healthcare is predominantly publicly provided rather than private. No social reports were identified for public hospitals in Lazio, Calabria and Campania, where private providers play a significant role in healthcare delivery. 3 This discrepancy may be attributable to limited resources in these regions, which face economic constraints and centralised governance. 34 Literature suggests that economic capacity can influence organisational sustainability practices and SAR initiatives, while adopting sustainability practices may enhance long-term financial sustainability.

The normative pressure is related to the social and cultural expectations that shape organisations. Normative pressures are absent, likely owing to the primary mission of hospitals. Stakeholders generally expect efficient healthcare services, even if this requires greater resource consumption. Public focus tends to prioritise outcomes such as lives saved and diseases treated, whilst other sustainability aspects remain secondary concerns. Finally, internal institutional pressure is driven by individuals within organisations advocating for the adaptation of practices to external expectations. This pressure can influence high-level strategic decisions. In healthcare, professionals prioritise clinical activities over administrative work, which may create internal barriers that impede the development of sustainability reporting practices.

Conclusions

This paper provides a comprehensive analysis of sustainability accounting and reporting in the Italian public healthcare sector. It examines whether official programming and monitoring documents address SDGs and sustainability, and assesses financial forecasts and consolidated statements to evaluate the sector’s integration of sustainability considerations.

The exploratory analysis reveals that Italian public healthcare organisations do not typically adopt sustainability accounting and reporting systems. Most documents are one-time reports, geographically concentrated, and do not reference SDGs. Furthermore, financial forecasts and consolidated statements comply with legal requirements but lack connections to SDG indicators. Additionally, our findings highlight a stronger emphasis on the social dimension of sustainability, particularly health and well-being issues. Social SDGs receive twice the number of references compared to environmental or economic SDGs. This focus aligns with the core mission of healthcare organisations, which prioritises social impact and public health. These findings align with legitimacy theory, which suggests that organisations disclose non-financial information to establish legitimacy and address stakeholder interests. By contrast, the economic and environmental dimensions of sustainability have received less emphasis.

However, public hospitals have significant potential to contribute to sustainable development. Efficient resource use, such as water and energy conservation, could reduce waste and positively impact financial outcomes. Moreover, the adoption of renewable energy sources could support SDGs 6 and 7. Enhanced waste management strategies could reduce waste generation, whilst collaboration with other stakeholders on circular economy principles would support SDG 12. Attention to working conditions and the role of women in public health could also contribute to SDGs 5 and 8. In theory, all SDGs could be addressed through targeted initiatives, many of which are already in place but are not systematically monitored or reported.

Systematic reporting on the impact of targeted initiatives could yield significant management benefits. It would consolidate sustainability best practices and support performance measurement using SDG-aligned indicators, supporting budget systems that prioritise sustainability. This supports the proposition that SDG-aligned organisational budgeting strengthens health-related SDG implementation at broader governance levels. Improvements could align healthcare governance levels and financial processes across organisations to enable a sustainability-driven approach. Italian public sector harmonisation has prioritised standards whilst neglecting sustainability. Revising principles to encompass all sustainability dimensions and aligning budgets with SDGs would support long-term planning and progress monitoring. From a policy perspective, our findings highlight an urgent need for Italian regulators to bridge the gap between the accounting requirements of Law 118/2011 and the evolving EU landscape. As the CSRD begins to set new transparency benchmarks, Italian PHOs risk institutional obsolescence unless they transition toward an integrated reporting model that treats sustainability as a core financial determinant.

From a methodological perspective, this study offers a significant contribution by demonstrating the effectiveness of a hybrid qualitative approach that integrates automated text search queries and words frequency analysis using NVivo. This framework provides a replicable and scalable model for analysing large volumes of institutional documents where manual content analysis would be impractical. By employing targeted queries to identify references to the 2030 Agenda and SDGs, the research establishes a systematic methodology for detecting ‘policy-practice decoupling’ in public sector reporting. To further validate this approach, future research should apply this text search-based methodology across different national and cultural contexts. Such comparative extensions could test the transferability of the method across diverse healthcare systems and generate insights into whether identified reporting gaps represent a localised issue or a global systemic trend. A limitation is the outdated sustainability content on public organisations’ websites, which reveals a significant communication gap. Future research could analyse monitoring reports prepared under the CSRD and identify best practices amongst healthcare providers. Promoting double materiality could strengthen the linkage between sustainability and financial performance. Comparative studies examining public and private providers across different contexts could identify effective and transferable practices.

Footnotes

Acknowledgements

The authors would like to express their sincere gratitude to the academic colleagues that provided valuable insights during the research.

Consent for publication

All participants were informed in writing that the findings may be published.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: On behalf of all the authors, I confirm that: The authors have no relevant financial or non-financial interests to disclose. The authors have no conflicts of interest to declare that are relevant to the content of this article. All authors certify that they have no affiliations with or involvement in any organisation or entity with any financial interest or non-financial interest in the subject matter or materials discussed in this manuscript. The authors have no financial or proprietary interest in any material discussed in this article.