Abstract

Are poor physical and financial health driven by the same underlying psychological factors? We found that the decision to contribute to a 401(k) retirement plan predicted whether an individual acted to correct poor physical-health indicators revealed during an employer-sponsored health examination. Using this examination as a quasi-exogenous shock to employees’ personal-health knowledge, we examined which employees were more likely to improve their health, controlling for differences in initial health, demographics, job type, and income. We found that existing retirement-contribution patterns and future health improvements were highly correlated. Employees who saved for the future by contributing to a 401(k) showed improvements in their abnormal blood-test results and health behaviors approximately 27% more often than noncontributors did. These findings are consistent with an underlying individual time-discounting trait that is both difficult to change and domain interdependent, and that predicts long-term individual behaviors in multiple dimensions.

Keywords

Are two of the great behavioral problems facing the developed world driven by the same underlying psychological factor? Insufficient retirement savings and chronic health problems are looming crises in most developed countries. Nearly 36% of Americans over the age of 20 years are obese (National Center for Health Statistics, 2012), and diabetes has become almost four times more prevalent since 1980 (Centers for Disease Control and Prevention, 2013). Similar disturbing trends exist for retirement planning. Almost half of all retirees have no retirement savings, and median savings for near-retirees (ages 55–64 years) are only $12,000 (Rhee, 2013). Previous research has suggested that both health and savings behaviors are related to time preferences (Chapman & Elstein, 1995), because they represent individuals choosing to forego future wealth or health in favor of immediate consumption. Empirical research overwhelmingly supports this argument. Individual time preferences influence health and financial behaviors, including gambling (Dixon, Marley, & Jacobs, 2003), drug use and smoking (Harrison, Lau, & Rutström, 2010; Kirby, Petry, & Bickel, 1999), diet choice (Huston & Finke, 2003), cancer control (Chapman, 2005), gym attendance (DellaVigna & Malmendier, 2006), creditworthiness (Meier & Sprenger, 2010, 2012), and financial savings (Ersner-Hershfield, Garton, Ballard, Samanez-Larkin, & Knutson, 2009).

Although intertemporal-choice problems in different domains (such as health and finance) frequently coexist in individuals, there is still debate about whether these domain-specific behaviors stem from common underlying time preferences or instead from separate domain-specific factors and motives, including impulsivity, compulsivity, inhibition, self-control (Ariely & Wertenbroch, 2002; Frederick, Loewenstein, & O’Donoghue, 2002; Laibson et al., 1998), and strength of connections with the future self (Bartels & Rips, 2010; Ersner-Hershfield et al., 2009). These many underlying factors are thought to explain why individuals frequently exhibit inconsistent intertemporal choices across domains (Chapman, 1996, 2005; Frederick et al., 2002).

In this article, we provide evidence that insufficient retirement savings and chronic health problems are at least partially driven by common time-discounting preferences. We used personnel and health data from eight industrial laundry locations to show that individual discounting differences appear to be domain interdependent—the previous decision of an employee to forego immediate income and contribute to a 401(k) retirement plan predicted whether he or she would respond positively to the revelation of poor physical health. Our approach was unique in exploiting a quasi-exogenous shock to employees’ health knowledge from a company-sponsored wellness plan to predict who was more likely to improve his or her health.

After controlling for differences in initial health, demographics, and job type, we found that retirement savings and health-improvement behaviors were highly correlated. Individuals who had previously chosen to save for the future by making 401(k) contributions improved their health significantly more than noncontributors did, even though there were few health differences between the two groups prior to program implementation. This distinction is important because although health and financial discounting appear to be domain independent at any given point in time, financial discounting predicts dynamic responses to health information. Although we could not directly measure discounting preferences as the mechanism driving both behaviors or conclusively rule out all alternative explanations, additional analyses supported this assertion and cast doubt on alternative explanations involving conscientiousness, advice taking, financial need, and life-expectancy considerations.

Method

The study took place at an industrial laundry company with facilities in multiple states. The company instituted an organization-wide wellness program that offered its employees annual biometric screenings from 2010 to 2012. The screenings were administered by nurses from a third-party employee-wellness-services company and included two parts: (a) a full panel of 42 blood tests and (b) a health-habits survey. Approximately 3 weeks after testing, packets were returned to employees detailing their health status, including their blood results (highlighting abnormalities), health-behavior scores, future health risks, and personalized suggestions for health improvement. Any individual with highly abnormal results was contacted by a nurse, who discussed the results with the individual and requested permission to forward them to the employee’s physician. Because the health data were provided directly to participants (and the researchers) by the company facilitating the wellness program, the laundry company never had access to its employees’ health information. This project was approved by the Washington University in St. Louis Institutional Review Board.

Subjects

Subjects were 414 workers employed between 2010 and 2012 in the laundry company’s corporate headquarters and in the seven nonunion plants that participated in the study. For participating in the program, participating employees received a small decrease in their health insurance premium (15%, which worked out to $1.75–$11 per month, depending on the employee’s salary).

Of the 414 individuals employed during the period of the study, 213 attended more than one screening, 158 attended only one, and 43 did not participate. Because our analysis required 2 years of testing to observe health improvements, we were able to analyze only those 213 employees with repeat participation. Of the 158 who participated only once, 126 were employed during a period that covered only one of the testing days, whereas 32 were employed during more than one testing day but did not participate in a second test. Although we do not have data on the reason for this nonparticipation, interviews with the company human-resources manager indicated that most of these 2nd-year nonparticipants were likely absent from the workplace on the testing day for personal or job-related reasons. For the 43 that chose never to participate, the human-resources manager stated that a fear of doctors, coverage under a spouse’s insurance plan, absence on the date of testing, and potential drug use were all reasons why individuals may have chosen not to participate. Of our final sample of 213 repeat participants, 208 (98%) initially had at least one abnormal blood finding, and 53 (25%) had at least one severely abnormal finding.

Although our selection process creates concern about sample-selection bias, we do not believe it significantly biased our results. There do not appear to be any systematic differences between repeat participants and single-time participants in the relationship between retirement contribution and initial health (we could not observe health changes for single-time participants because they participated in only one screening). Furthermore, repeat participants, single-time participants, and nonparticipants all have very similar observable characteristics. To support that sample-selection bias did not influence our results, we alternatively implemented Heckman selection models that controlled for the endogenous selection process. These results provided little evidence that any selection bias occurred, and controlling for selection did not significantly change the main results. We report these model results in the Supplemental Material available online.

Finally, we note that in 2012, the laundry company scaled back the wellness program and offered only the full range of blood tests to new participants while continuing to conduct diabetes and cholesterol tests, as well as the full survey, for all repeat participants. This change meant that we could observe only 2 years of full blood panels (and thus an annual change) for the 154 repeat participants who first tested in 2010 and not for the 59 repeat participants who first tested in 2011 but were not given the full blood panel in 2012. In contrast, our final data included either one or two values for annual change per individual for diabetes, cholesterol, and survey-based variables (e.g., high-risk factors), yielding 328 observations from 213 repeat participants.

Measure of financial discounting

We measured financial discounting using each individual’s chosen withholding percentage for his or her 401(k) defined-contribution retirement plan from immediately before implementation of the wellness program. Each employee designated paycheck withholding at hiring with the help of human-resources personnel. Employees can change contributions at any point, but the default contribution is 6% of the employee’s salary if no choice is made within 90 days of hiring. Although 78% of employees started with the default contribution, 17% of these individuals changed their allotment within 30 days after the initial 90-day period, 28% changed within 90 days, and 37% changed within 1 year. Retirement-program participation significantly increases future wealth because the company matches 50% of the tax-exempt employee contributions up to 6% of the employee’s salary. Despite this, many employees (55) chose not to withhold. Average salaries were just under $39,000, so each dollar withheld decreased immediate consumption. This trade-off drove the correlation between retirement savings and underlying time-discount rates observed in previous studies (e.g., Ersner-Hershfield et al., 2009). We placed employees into two groups on the basis of whether they decided to contribute: contributors (low time-discount rate) and noncontributors (high time-discount rate). The distribution of contributions was bimodal, with 74% of employees choosing to contribute.

Measures of health improvement

We measured both aggregate and specific health improvements for individual employees using differences between yearly health-test results. The first aggregate measure was the annual change in the number of categories with at least one abnormal blood finding. The health-testing company defined abnormal blood findings for 12 categories based on specific tests falling outside laboratory-designated normal ranges: diabetes, cholesterol, kidney, electrolytes, white blood cells, prostate, iron, blood calcium, cell balance, enzymes, thyroid, and overall blood count. The mean number of categories in which first-time participants had abnormal blood results was 2.72 (range = 0–7).

The second aggregate health measure was the annual change in the number of high-risk factors. The testing company included 15 biometric and self-reported risk factors: current smoker, no regular exercise, not using seat belts, heavy alcohol use, regular relaxation- or sleep-medication usage, life dissatisfaction, job dissatisfaction, poor physical-health perception, high stress score (3+ stress indicators from survey variables), high blood pressure (140/90+), high cholesterol (240+ mg/dL), low high-density-lipoprotein cholesterol (< 40 mg/dL), obesity (body mass index = 27+), frequent sick days (6+ per year), and chronic health problems, including heart disease, cancer, stroke, diabetes, asthma, or arthritis. The mean number of factors for which there was an annual change in first-time participants was 2.76 (range = 0–9). Our data included only one annual-change value for most blood tests but two annual-change values for high-risk factors, as well as diabetes and cholesterol measures. In addition to these aggregate measures, we also examined the change between screenings for each specific blood-test variable and high-risk factor.

Although our focus was on how financial discounting predicts health improvements following the revelation of poor-health information to workers, it is important to note that we observed few differences in the health of contributors and noncontributors at the initial screening. Although a few self-reported behaviors were significantly different across groups (see Table S1 in the Supplemental Material), such differences could easily be random given the large number of tests presented. The similarity in these initial results is important for at least four reasons. First, it shows that improvements across groups cannot be explained by higher potential to improve, which might stem from existing health problems. Second, it shows that people do not appear to be rationally matching expectations of life expectancy to retirement savings. Third, it suggests that people are not intentionally (or at least successfully) using retirement savings as a precommitment device to motivate better health. Finally, and perhaps most important, it is consistent with prior evidence that health and money are domain independent in contemporaneous behavior (Chapman & Elstein, 1995). This is critical because we examined domain interdependence in dynamic behavioral changes.

Results

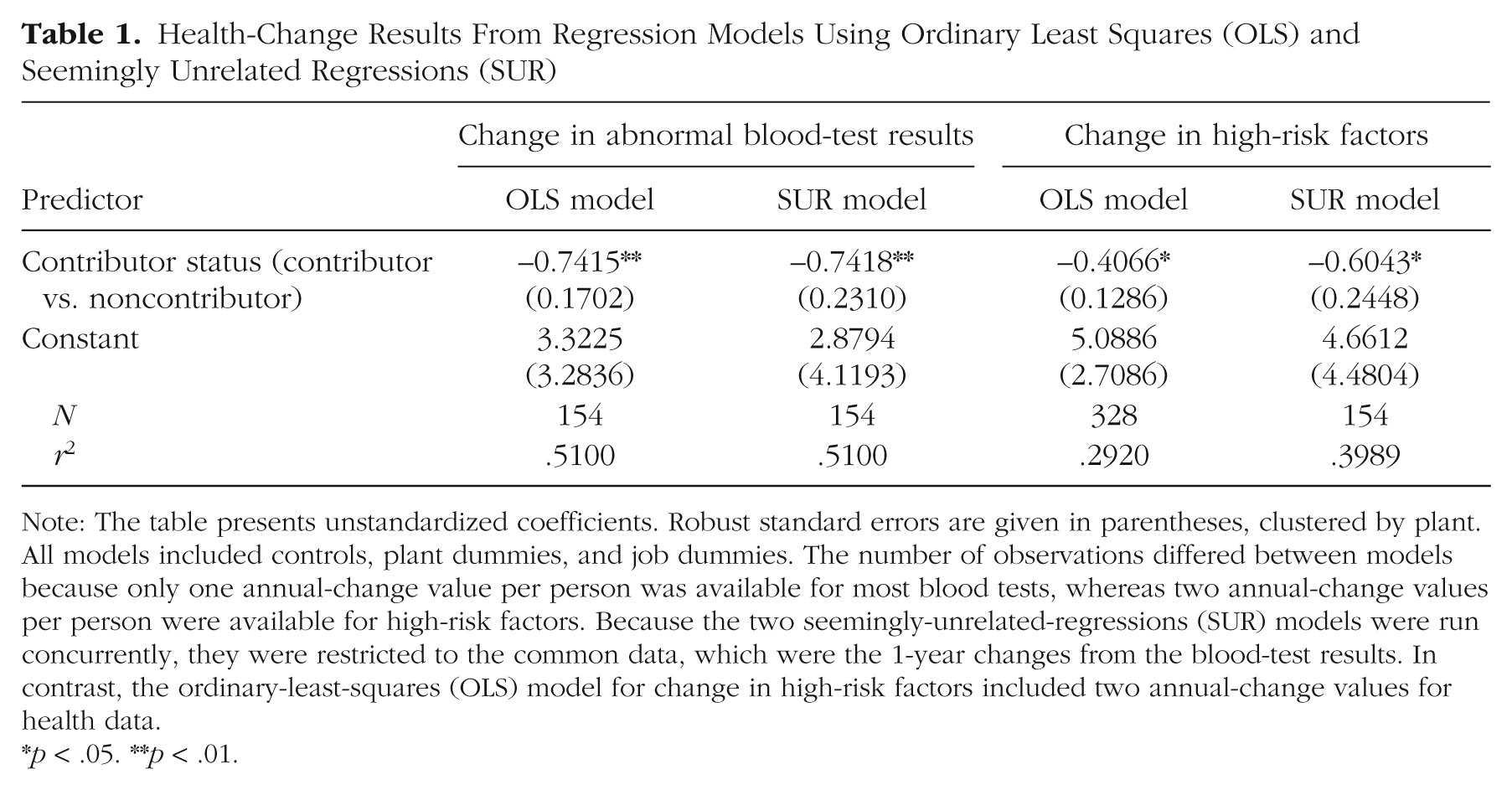

We used regression analysis to estimate how contributing to a 401(k) plan predicted health improvement between biometric screenings. Because both health improvement and 401(k) contributions can differ according to demographics and cognitive ability, we controlled for differences in initial health, personal and family health history, annual salary, number of federal tax exemptions claimed, gender, age, marital status, work location, and specific job. We estimated the average effect of contributing to a 401(k) plan on health improvement using ordinary least squares (OLS) and seemingly unrelated regressions (SUR), clustering standard errors by plant in OLS. High-risk-factor OLS regressions reflected up to two annual-change values per person, whereas abnormal-blood-count regressions and SUR models reflected one annual-change value per person—the 2010 to 2011 change. To control for different participant cohorts, we included year dummies and a dummy variable indicating the second time an individual participated.

Aggregate health measures

Figure 1 and Table 1 detail our main results. Figure 1 shows that, after we controlled for demographic risk factors, retirement contributors’ health improved after they receiving health information, whereas noncontributors continued to suffer health declines as they aged. Table 1 shows that abnormal test results decreased 0.74 (p < .01) more for contributors than for noncontributors, a 27% improvement from the mean of 2.72. High-risk factors for contributors decreased between 0.41 and 0.60 (p < .05) more than for noncontributors, a 15% to 22% improvement from the mean of 2.76. These results show that one or more abnormal blood-test findings returned to normal for, on average, three out of every four contributors, compared with comparable noncontributors, and a high-risk factor decreased for one out of every two contributors.

Mean number of health improvements as a function of retirement-contributor status, separately for individuals with abnormal blood-test results and high health-risk factors. The graph shows conditional means obtained using the ordinary-least-squares-predicted values estimated at the means of the control variables for each group. See the Results section for a list of control variables; see the Supplemental Material for further details. Error bars indicate 95% confidence intervals.

Health-Change Results From Regression Models Using Ordinary Least Squares (OLS) and Seemingly Unrelated Regressions (SUR)

Note: The table presents unstandardized coefficients. Robust standard errors are given in parentheses, clustered by plant. All models included controls, plant dummies, and job dummies. The number of observations differed between models because only one annual-change value per person was available for most blood tests, whereas two annual-change values per person were available for high-risk factors. Because the two seemingly-unrelated-regressions (SUR) models were run concurrently, they were restricted to the common data, which were the 1-year changes from the blood-test results. In contrast, the ordinary-least-squares (OLS) model for change in high-risk factors included two annual-change values for health data.

p < .05. **p < .01.

Specific health factors

We next tested whether the same health factors improved across individuals or whether the improved factors were specific to each individual. To do so, we first regressed those specific blood tests with the highest abnormality incidences on contributor: cholesterol (79%), diabetes (53%), and kidneys (31%). Figure 2 shows the percentage of improvement for each test. In contributors, hemoglobin-A1c and glucose-diabetes scores commonly improved. Hemoglobin A1c estimates the average level of blood sugar over a 2- to 3-month interval, and consistent readings of 5.7 or higher indicate prediabetes. Glucose readings indicate blood sugar at the time of sample collection, and values above 100 indicate an increased risk of diabetes. We found that in contributors, hemoglobin A1c decreased by 1.5% (p < .05) from a mean of 5.59, and glucose decreased by 2.1% (p < .05) from a mean of 98.7. Medical research suggests that such improvements can substantially affect health (Stratton et al., 2000), and our coefficients suggest a 1.8% risk reduction for diabetes and diabetes-related death and a 3.1% risk reduction in microvascular complications.

Mean percentage of improvement for contributors relative to noncontributors on nine blood-test results. The graph shows regression coefficients estimated using ordinary least squares. See the Results section for control variables. Data were limited to one annual-change value for blood urea nitrogen (BUN) and BUN/creatinine; two annual-change values were used for the other categories. Triglycerides and glucose were Winsorized at 2 standard deviations above the mean because of extreme outliers who may have not fasted prior to testing or recently consumed alcohol. Error bars indicate 95% confidence intervals. HDL = high-density lipoprotein, LDL = low-density lipoprotein, VLDL = very-low-density lipoprotein.

We also found that cholesterol significantly improved in contributors. This change has considerable implications for heart disease, which accounts for one in every four deaths in the United States (Kochanek, Xu, Murphy, Miniño, & Kung, 2011). We found that low-density lipoprotein (LDL) and very-low-density lipoprotein (VLDL) decreased 8% (p < .01) and 12% (p < .1) respectively, from means of 115 and 26 (compared with healthy limits of LDL < 99 and VLDL < 40), which suggests that the risk of heart and vascular disease decreased in contributors with high cholesterol. 1 Nearly all other tests had positive coefficient estimates but were not significant at the .10 level. Blood urea nitrogen (BUN) and BUN/creatinine, the two major kidney tests, showed considerable improvement but were not quite significant at the .10 level. This imprecise coefficient estimate is not surprising given the very few individuals with abnormalities that improved in each of these tests.

Specific high-risk factors

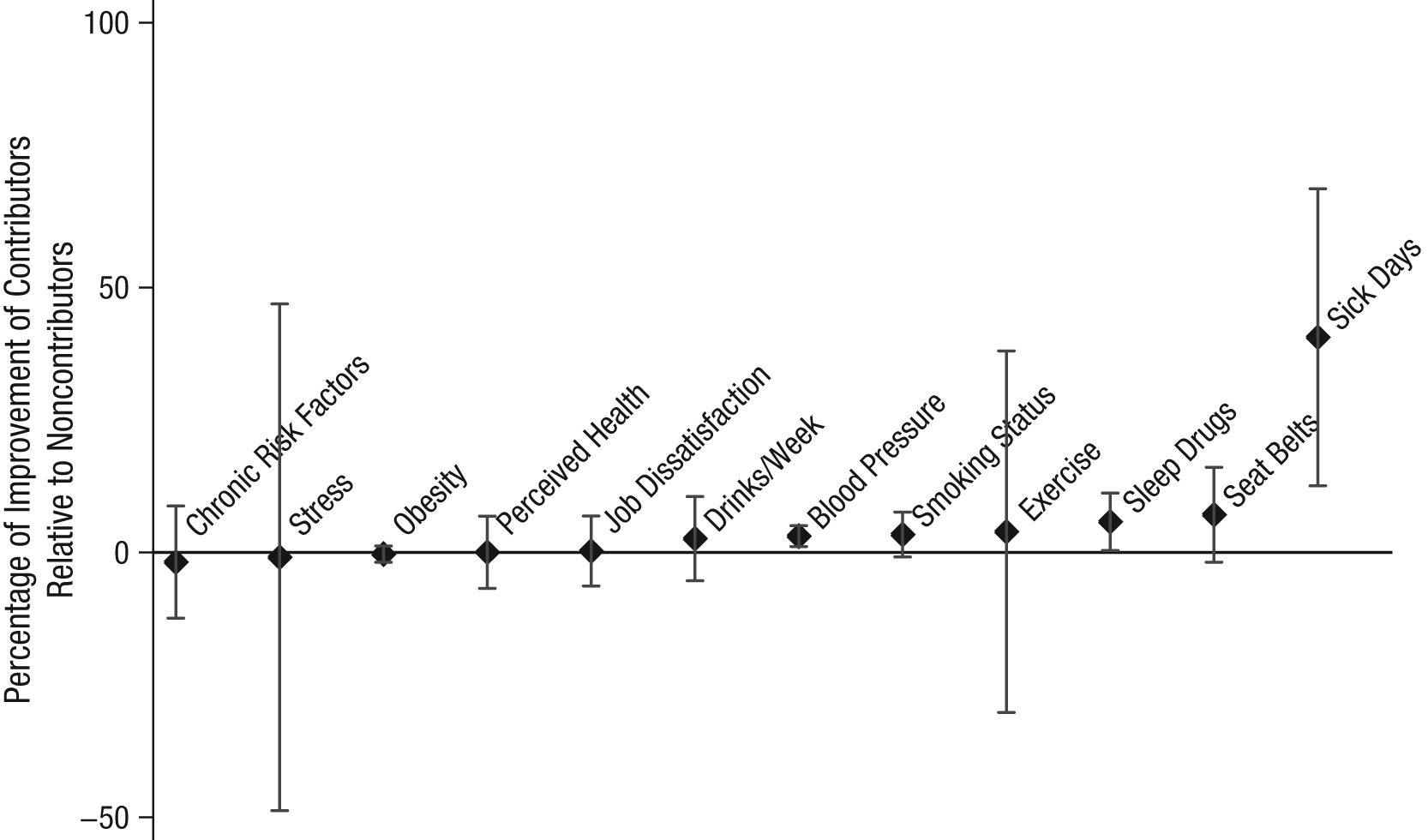

We also examined high-risk factors and found improvements for contributors (relative to noncontributors) in safety behaviors (seat-belt use), mental health (reduced sleep and use of anxiety medication), and risky lifestyle choices (smoking; Fig. 3). First, relative systolic blood pressure decreased 3.1 points (p < .1) more for contributors, a difference of 2.5% from a mean of 124, which reduces their risk of heart disease or stroke (National Institutes of Health, 1997). Second, safety behaviors improved more for contributors, including a 7% improvement in seat-belt use, reduced smoking, and reduced usage of sleep and relaxation medications, although these were not quite significant at the .10 level. Finally, and most striking, we found that the number of sick days reported was dramatically lower for contributors than for noncontributors, with a relative decrease of more than 40% (p < .05). This suggests that improving one’s health has significant spillover effects on society and business beyond the direct cost of poor health.

Mean annual percentage of improvement for contributors relative to noncontributors in 12 health-risk categories. The graph shows regression coefficients estimated using ordinary least squares. See the Results section for control variables. Cholesterol and high-density lipoprotein are presented in Figure 2. Error bars indicate 95% confidence intervals.

The often weak statistical significance of our estimates for individual health dimensions is not surprising, given our limited sample size and the infrequency of abnormal findings on some blood dimensions. The relationship between retirement contributions and health improvements was more easily observed on specific dimensions in which health problems are common, such as cholesterol and diabetes, and on more comprehensive measures, such as counts of abnormal blood findings and sick days. Taken together, our results suggest that overall health improved on many dimensions for contributors. The overall difference in health changes between contributors and noncontributors is clear, although each individual improved (or worsened) on unique dimensions. Perhaps most interesting is that the largest improvements occurred in areas that predict future health, but which do not significantly affect immediate health, such as prehypertension, prediabetes, and high cholesterol. This is consistent with health improvements reflecting a long-term perspective rather than short-term benefits.

Mechanism

Although our results are consistent with domain-interdependent time discounting, there are a number of potential alternative explanations. First, trait-level conscientiousness may drive both retirement savings and health-improvement behaviors. To test this alternative, we estimated the relationship between retirement contributions and two employee behaviors that indicate conscientiousness in other domains: punctuality and seat-belt use (see the Supplemental Material for details). Using logistic regression, we found little evidence that employees who are either frequently late (odds ratio = .87, p = .70) or do not use seat belts (odds ratio = .99, p = .99) exhibit different savings behavior from other employees. These results cast doubt on the hypothesis that trait-level conscientiousness drove the results.

Second, individual differences in the propensity to take advice (Koestner et al., 1999), especially from authority figures, may drive the two behaviors. In this explanation, contributors’ health may improve because they are more likely than noncontributors to take both financial and health advice. We addressed this by repeating our linear regression analysis on only those individuals who initially took advice from human-resources personnel at the time of hiring by withholding 6% of their paycheck (78% of employees), which eliminated those employees most likely to reject advice. Our results on this subsample were qualitatively similar to our main regression results (see the Supplemental Material), which suggests that even among employees who initially took advice by choosing the default contribution, later contribution choice predicted health improvements. This result, in conjunction with our previous finding on seat-belt use, casts doubt on the theory that advice taking was driving the results.

Third, it is possible that individuals chose not to contribute because of an urgent financial need and that this need also constrained their ability to invest in improving their health. Such severe immediate financial needs may arise either from a present-oriented focus leading to high debt levels, consistent with individuals discounting the future, or from unanticipated expenses such as medical costs. There are four reasons that we believe this alternative explanation does not explain our results. First, initial observable health levels were very similar between contributors and noncontributors. Given our comprehensive medical data, it is unlikely that there were systematic unobservable health problems creating such financial needs. Second, the company insurance plan is relatively inexpensive, with low premiums ($11–$34 monthly), low out-of-pocket maximums ($1,000 annually), and low copayments for medications ($9–$12) and doctor visits ($25). Third, the health program provided all participants with the opportunity to meet with nurses at no cost to receive health advice. Finally, individuals encountering unanticipated urgent financial needs can withdraw money from their retirement plan. Related to this concern, a worker’s spouse may also save for retirement. We repeated our SUR analysis, but this time we excluded married individuals, and we found very similar results to those for our full sample (abnormal blood test: β = −0.86, p < .05; high-risk factors: β = −0.47, p < .15).

Finally, one might argue that our regression results reflect employees strategically choosing their retirement plan in response to or in coordination with their health. This argument could be based on several mechanisms. First, employees could use retirement as a precommitment mechanism (e.g., Schwartz et al., 2014), by which the inability to retrieve wealth until later in life motivated them to improve their health after they received detailed information from the health program. We find this explanation unlikely for several reasons. As we noted earlier, we saw little evidence of initial health differences between contributors and noncontributors that would be expected if they were successfully using retirement saving to commit to improving their health. Moreover, because 401(k) contributions can be withdrawn without penalty at age 55 or in case of hardship (such as premature illness), such a commitment device would be effective only for individuals expecting to become ill and die rapidly before age 55 (and thus not be able to use a hardship withdrawal).

The second strategic mechanism would be if employees reduced their retirement savings in response to the health program reducing their perception of life expectancy. To test this alternative mechanism, we used historical data on all 401(k) contribution changes for employees. We compared 401(k) changes in the year after a health evaluation to changes in the previous year. For this alternative explanation to hold, we would expect individuals who received negative information to reduce their withholding amount. Using Mann-Whitney tests, we found little evidence, however, that the distribution (p = .83) of 401(k) changes was statistically different between the 2 years. Moreover, we found that people who did not take steps to improve their health were no more likely to switch (p = .93) following the revelation of negative health information than people who did take such steps (see the Supplemental Material). This suggests that precommitment and strategic retirement decisions are unlikely to explain our findings.

Although these analyses cast doubt on alternative explanations, our relatively small sample from one firm could not conclusively rule them out, nor did we have the opportunity to directly test time discounting experimentally. We therefore acknowledge that these alternative explanations may play some role in the correlation between retirement savings and health improvement. Other explanations may exist that we cannot test, such as individuals feeling more positively about their future selves and therefore investing in both future health and financial stability (Hershfield, 2011; Levy, Slade, Kunkl, & Kasl, 2002). We encourage future work to better disentangle these mechanisms, possibly by combining experimental designs with personnel and medical data from a much larger employer.

Discussion

Our analysis suggests that the same underlying psychological factors that are linked to retirement planning also predict health-improvement behaviors. Although we cannot directly identify the specific mechanism driving this relationship, our results are consistent with domain-interdependent time-discounting preferences. Our rich panel data and extensive demographic controls cast doubt on alternative mechanisms, such as advice taking, conscientiousness, and cognitive ability, although other mechanisms, such as self-efficacy expectations and views of the future self, may have influenced our results. Furthermore, we cannot discern whether these behaviors reflect rational or time-inconstant preferences, such as procrastination or self-control problems (Ariely & Wertenbroch, 2002; Vohs & Heatherton, 2000). This is an important focus for future research, given recent evidence that effort-related domains (such as health) may show more present bias than monetary domains (Augenblick, Niederle, & Sprenger, 2013). Finally, care should be used in generalizing our results, as they are based on a relatively small sample of repeat-participant, long-term employees.

These findings are important for four reasons. First, they suggest that for long-term and high-stakes decisions, discount rates can be interdependent across important domains. If this is the case, the efficacy of programs that target health improvements may be predicted by individual financial history and coordinating health and savings programs may improve efficiency and efficacy. It also implies that if time discounting can truly be changed through treatments such as power (Joshi & Fast, 2013) or commitment devices (Ariely & Wertenbroch, 2002), the benefits may spill over to influence intertemporal choices in other domains. Second, our results suggest that there are deliberate individual traits that are difficult to change and that influence long-term individual behaviors in multiple dimensions (Eigsti et al., 2006; Reuben, Sapienza, & Zingales, 2010). Third, we showed that even when current intertemporal choices appear to be independent across domains, current behavior in one domain may predict future changes in the other after information is provided to program participants. Finally, our results suggest that popular solutions to short-term decision framing, such as defaults, may be ineffective in changing long-term behaviors for certain classes of individuals.

Our study is unique in that time preferences on one high-stakes dimension, retirement, predicted the efficacy of behavioral-improvement programs on another critical dimension—health. This suggests that, at least for some individuals, discounting may not be as domain independent as previously thought. Although this seems to contradict earlier findings of domain independence (e.g., Chapman & Elstein, 1995), several differences in our study might explain this. First, our study used a quasi-exogenous shock to health information that links financial discounting to dynamic health responses rather than to cross-sectional behavior. This distinction is important because, as in previous studies, our findings offer little evidence of cross-sectional correlations between health and financial choices. Second, our study links high-stakes financial decisions with changes in a broad array of health behaviors and metrics, each with potentially different links to retirement savings. Health improvements on each dimension may require different behavioral commitments and personal traits, which would be consistent with multiple underlying factors affecting intertemporal health choices.

Footnotes

Acknowledgements

The authors thank Bart Hamilton, Ian Larkin, Stephan Meier, and Julia Minson, editor Gretchen Chapman, and three anonymous reviewers for their comments and suggestions. Managers at the laundry and wellness companies were invaluable to the project.

Declaration of Conflicting Interests

The authors declared that they had no conflicts of interest with respect to their authorship or the publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.