Abstract

This paper empirically examines the relationship between energy efficiency, CO2 emissions, foreign direct investment, exports, and real gross domestic product at both aggregate and disaggregate levels in Malaysia based on an autoregressive distributed lag approach. The annual data for the period of 1971–2013 are employed. The results indicate that energy efficiency Granger causes economic growth at the aggregate level, but not in each of the three main sectors (primary, secondary, and tertiary) of the economy. Another important finding of the study is that the export-led growth hypothesis is found to be valid in Malaysia at both the aggregate and disaggregate levels. The results of our study also confirm the fact that CO2 emissions do affect the overall economic performance and growth in all sectors, except for the primary sector. This finding implies that pollution from both secondary and tertiary sectors has led to economic growth in Malaysia. Moreover, it is also discovered that foreign direct investment does not have a significant impact on economic growth in Malaysia. The results of this study are essential for policymakers of Malaysia in designing appropriate policies in each sector that can lead to robust growth in the country. In addition to focusing on enhancing energy efficiency and promoting foreign direct investment, the policymakers should also start to look for alternative strategies to ensure long-term economic growth in the country.

Introduction

An accelerating global energy demand, particularly on fossil fuels over the years, has created enormous pressures on the environment. The burning of fossil fuels is the primary human activity that has led to climate change. The current extreme climatic condition that reduces food supply and threatens coastal cities could cause an additional 100 million people in the world to suffer from poverty by 2030. 1 According to the World Bank 1 and Niu et al., 2 efficient utilization of energy is one of the most effective ways to achieve the objective of carbon dioxide (CO2) reduction. Despite various international attempts (e.g., Kyoto Protocol) made so far to mitigate the problem of global warming, little success has been achieved in reducing greenhouse gases worldwide.

In many cases, the failure of these international climate change negotiations is mainly because developing countries are sceptical and reluctant to commit to binding emission constraints set as they fear of a trade-off between energy efficiency and economic growth. In other words, the developing nations are facing a dilemma of how to achieve continuous growth while reducing emissions simultaneously. As a developing nation, Malaysia encounters the same problems as other developing countries. The developing nations have been highly dependent on energy to support their robust economic growth over the past decades. However, in the case of Malaysia, the problem is unique in the sense that the economic growth has started to dampen since the Asian financial crisis in 1997. In the last two decades, the Malaysian economy was no longer able to achieve a growth rate of more than 7% as experienced before the crisis. 3 To restore its growth momentum, adequate and continuous supply of energy sources is essential as the country is currently experiencing a sharp increase in energy demand due to industrialization and a reduction in local reserves of energy sources.

Improving energy efficiency is one of the best ways to address the two significant challenges in Malaysia. First, due to rising energy demand and gradual depletion of local reserves of resources, including oil, the country would need to rely on imported energy sources, particularly coal for energy production. It is indeed risky to depend on the external supply of coal for 40% of the energy used in electricity production. 4 The dependence on imported coal could expose Malaysia to supply interruption and fluctuating coal prices. By improving energy efficiency, it is expected that the country's dependence on external resources can be minimized. Second, Malaysia has been relying on fossil-based energy sources such as coal and oil for energy production that have contributed to the emissions of greenhouse gases. According to Safaai et al., 5 285.73 million tonnes of CO2 will be emitted in Malaysia by 2020, 68.86% higher than in 2000, if nothing is done to reduce CO2 emissions. It is also predicted that CO2 emissions in the country will triple by 2030 as compared to its magnitude in 2004. 6 By increasing energy efficiency, a reduction in air pollution can be achieved by the country. 7

Given the above reasons of environmental protection and national security, it is vital for Malaysia to achieve high energy efficiency while moving towards the goal of becoming a high-income nation. However, the question is, can energy efficiency be achieved without retarding economic performance in Malaysia? If energy efficiency is not realized at the expense of economic growth, there would be no issue to implement both the environmental protection policies and growth strategies simultaneously in the country. Otherwise, the country would need to think of other alternatives to achieve the dual goals of a clean environment and steady economic performance.

Most of the previous studies about Malaysia have focused on the relationship between energy consumption and economic growth.8–13 To the best of our knowledge, there has never been a study examining the impact of energy efficiency on economic growth in Malaysia, particularly from the perspective of aggregate and disaggregate levels. Our study represents the first attempt in the literature to look into this relationship. Determination of the relationship between energy efficiency and economic growth by sectors is significant to realize what policies should be followed to improve economic performance in each of the sectors. Besides, to carry out a single-country time-series study involving only Malaysia can eliminate problems associated with cross-country studies. In particular, findings from panel studies provide merely a general understanding of the relationship among variables, thus making it more challenging to direct national policies. Malaysia is a country worth investigating as its economy is the second largest in Southeast Asia in terms of nominal gross domestic product per capita. 14 However, the environmental quality in the country has worsened substantially in recent decades. Based on these arguments, this study, therefore, attempts to fill the gap by investigating the impact of energy efficiency on the economic performance of Malaysia from both aggregate and disaggregate perspectives by considering CO2 emissions, exports and foreign direct investment (FDI) as control variables.

By using annual data of 1971–2013 to perform the analysis, we adopt an autoregressive distributed lag (ARDL) approach to explore the relationship between energy efficiency and economic growth in the presence of CO2 emissions, exports, and FDI at the aggregate level. Besides, the study also aims to examine the extent to which energy efficiency contributes to economic growth at the disaggregated level in Malaysia. As hardly any prior researches have studied the role of energy efficiency in economic growth from both aggregate and disaggregate levels, the results of our study are expected to contribute not only to policymakers but also to the academics. Specifically, the findings of this study are to provide useful insights and references to future research when it comes to investigating the energy-growth nexus, particularly from the perspective of disaggregate level.

The remainder of this article is structured as follows. The next section provides a literature review. Then it is followed by research methodology. The subsequent section provides a discussion on the empirical results. The final section concludes the article with the inclusion of policy implications.

Literature review

In recent years, the role of energy efficiency in affecting economic growth has received increased attention among the researchers. Investigating the relationship between economic growth and energy efficiency is crucial as an improvement in energy efficiency contributes to increased firms' productivity that will, in turn, lead to higher economic growth. According to a hypothesis by Porter and van der Linde, 15 energy efficiency may enhance productivity because firms can adopt new technologies and innovative processes following a saving in energy costs. Most importantly, improved energy efficiency is expected to reduce the environmental costs of higher economic growth. However, studies on the link between energy efficiency and economic growth remain scarce. Cantore et al. 16 examine the impact of energy efficiency on economic growth at both micro- (total factor productivity) and macro-level (overall economic growth) in 29 developing countries. Whether at micro- or macro-level, energy efficiency is found to lead to better economic performance. In other words, trade-off does not exist between energy efficiency and economic growth in low- and middle-income countries. Using micro data on Indian manufacturing industry, Sahu and Narayanan 17 find a positive relationship between firms’ energy efficiency and total factor productivity. In another paper by Recalde and Ramos-Martin, 18 a U-shaped curve is portrayed between energy intensity-the inverse of energy efficiency and economic development in Argentina from 1990 to 2003.

Besides, Kepplinger et al. 19 examine the determinants for energy intensities in the manufacturing sector using mixed-effect models in OECD and non-OECD countries. In general, it is discovered that GDP is negatively linked to energy intensity. More recently, Rajbhandari and Zhang 20 investigate the causal relationship between energy efficiency and economic growth in 56 middle-income countries for the period from 1978 to 2012. A bidirectional causality is discovered between lower energy intensity and higher economic growth. Another recent study by Bataille and Melton 21 examines the effect of energy efficiency on the economic performance of Canada from 2002 to 2012. The findings indicate that higher GDP is achieved with improved energy efficiency.

A vast amount of studies has been done on the growth-pollution nexus ever since the pioneering research by Grossman and Krueger. 22 Two possible relations are found. First, economic growth is revealed to be the cause of the pollution problem. Concerning this, numerous empirical studies have found an inverted U-shaped curve of pollution relative to income, which is known as “Environmental Kuznets Curve” (EKC). The EKC indicates that pollutant emissions tend to increase at lower levels of income and then reduce at higher levels of income. Some countries will enter into less polluting sectors by adopting cleaner technologies. This will help them to reduce pollution. Employing a panel dataset of 17 OECD countries, Bilgili et al. 23 find the existence of an inverted U-shaped relationship between economic growth and CO2 emissions. Likewise, Dong et al. 24 confirm the validity of the EKC hypothesis. The authors investigate the relationship between GDP and pollution for 14 Asia-Pacific countries from 1970 to 2016. Jalil and Mahmud 25 also support the inverted U-shaped link between economic growth and environmental degradation. By using Autoregressive Distributed Lag (ARDL) methodology, the paper looks into the growth-pollution nexus using China's time-series data from 1975 to 2005. Besides, Apergis and Ozturk 26 test the presence of the EKC hypothesis in 14 Asian countries from 1990 to 2011 using GMM methodology. The results indicate that the inverted U-shaped EKC does hold in the countries examined. Furthermore, Yii and Geetha 27 also support the existence of EKC in Malaysia, where the shrinkage of CO2 emissions occurred when economic development shifted to the service sector.

Second, pollution does have a significant impact on economic growth. Empirical evidence shows that CO2 emissions have either a positive or negative effect on economic growth.28–30 By using the Granger causality test, Coondoo and Dinda 28 suggest that the causal relationship between CO2 emissions and economic growth depends on country groups. For North America and Western Europe (developed countries), for instance, a unidirectional causality is found running from CO2 emissions to GDP. Similarly, Youssef et al. 30 reveal that GDP Granger causes CO2 emissions in a panel of 56 countries. Specifically, environmental degradation is found to cause a decline in economic growth in all income groups (i.e., low-, middle- and high-income) examined. Besides, Dinda 29 investigates the linkage between pollution and economic growth for 88 countries using panel data from 1960 to 1990. It is evident from the results that CO2 emissions tend to deter the global economy from growing.

Two possible reasons can be put forth in explaining the negative relationship between CO2 emission and economic growth based on the existing literature. First, some studies such as Stern et al. 31 and Lean and Smyth 32 argue that if the issue of environmental degradation is not taken care of, then negative externalities brought about by pollution problem may reduce human health and the quality of industrial equipment, and in turn lead to a decline in productivity in the long run. This is the reason why income declines as environmental degradation deteriorate. Another reason to explain the negative relationship between CO2 emissions and income has been pointed out by Coondoo and Dinda 28 who suggest that as income reaches a threshold level, decreasing emissions would be associated with income growth. Some specific conditions are required for the realization of this relationship. For countries to experience low emission with high growth, they may need to undergo a structural change from emission-intensive manufacturing to less emission-intensive services in the economy. Another condition under which the negative relationship may emerge is that the conventional fossil fuel is replaced with less polluting energy resources, even if a country's economy continues to be manufacturing-intensive.

There has been an abundance of research examining the relationship between FDI and economic growth. A study by Yao and Wei 33 using China as an example for newly industrializing economies proves that FDI and economic growth are positively related. With FDI, the productive efficiency of local firms in China has improved. This further leads to a shift in the production frontier towards the level of developed countries. Similarly, another study by Whalley and Xin 34 on China indicates that FDI has been the major contributor to economic growth. The findings of the study also suggest that Chinese GDP growth rate would be approximately 3.4 percentage points lower if there were no FDI inflows into the country. A more recent study by Amri 35 also finds that FDI does have a positive impact on GDP. The study inspects the FDI-growth nexus in 75 countries for the period between 1990 and 2010.

On the other hand, Herzer et al. 36 investigate the linkage between FDI and economic growth using a dataset of 28 developing countries. It is found that FDI is not a vital determinant of economic growth both in the short-run and long-run for most of the countries. Similarly, by applying cointegration test, Mah 37 examines the causal relationship between FDI inflows and economic growth in China and finds that FDI inflows do not lead to economic growth. Instead, economic growth is revealed to cause the FDI inflows. By employing a panel quantile regression model, Zhu et al. 38 examine the association between FDI and GDP in five selected ASEAN countries. It is revealed that FDI does not seem to be a significant factor influencing economic growth in these countries. In a nutshell, some studies report a positive while others show a negative or null effect of FDI on economic growth. The mixed results indicate that the relationship between FDI and economic growth remains controversial.

Another significant conclusion that can be drawn from the existing literature is that the impact of FDI varies from sector to sector in the economy. In general, the manufacturing sector receives the most benefits from FDI if compared to other sectors. As noted by Chakraborty and Nunnenkamp, 39 FDI contributes to different growth effects in different sectors in India. It is found that FDI and output are mutually reinforcing only in the manufacturing sector over the long-run, but not in primary and service sectors. Likewise, Akinlo 40 attempts to find out whether FDI contributes to growth in the extractive sector (such as oil subsector). The results indicate that FDI in the extractive sector does not lead to much growth.

Besides, hundreds of studies have examined exports-growth nexus. Based on the export-led growth hypothesis, exports lead to economic growth. Awokuse 41 discusses how export and import affect growth in three transitional economies (Bulgaria, Czech Republic, and Poland) and found that exports stimulate economic growth. Apart from that, using data for the period from 1971 to 2006, Lean and Smyth 32 investigate the causality among five variables, namely aggregate output, electricity consumption, exports, labour and capital in Malaysia. The results indicate that exports Granger cause economic growth that is consistent with the export-led-growth hypothesis. The findings are supported by Pistoresi and Rinaldi 42 who find evidence of the export-led growth hypothesis in Italy from 1863 to 2004 by employing cointegration analysis and causality tests.

Similarly, Sunde 43 suggests that exports stimulate economic growth in South Africa using the ARDL bounds testing approach. The export-growth hypothesis is also supported by Fatemah and Qayyum 44 who discover that export is a significant determinant of economic growth in Pakistan. However, the arguments for exports-led-growth hypothesis have been criticized by a group of researchers who believe in inwardly oriented trade policies instead of outward-oriented trade policies. For instance, Tang et al. 45 study the relationship between exports and GDP in Asia's Four Little Dragons by utilizing modified Wald causality test within the augmented vector autoregression framework. The results show that export-led growth is not stable in the four countries during the period of analysis. This implies that Asia’s Four Little Dragons should not rely on export for spurring long term growth in the economy. Likewise, a study by Gözgör and Can 46 who use panel non-causality test shows that the export-led growth hypothesis is not valid in 139 countries from 1970 to 2010.

The above literature review shows that there is a widespread consensus currently for considering energy efficiency, CO2 emission, FDI, and export as main factors affecting economic growth. Specifically, energy efficiency and pollution have been included in the growth models in recent years to complement those common factors found in the early growth models such as classical and neoclassical growth models. In this regard, the studies on the role of energy efficiency and CO2 emission in fostering economic growth have become a prominent line of research.

In the context of Malaysia, the consideration of energy efficiency and CO2 emission is vital because the country has been experiencing increased CO2 emission in recent years despite its steady economic growth. To reduce the emission, the country needs to improve its energy efficiency in order to achieve sustainable growth over the long run. Along with energy efficiency and CO2 emission, other two crucial stimulus factors of economic growth are included in the model. For example, FDI is selected because it has been on the upward trend over the last two decades, 47 making it a vital influence for economic growth in Malaysia. Besides, the export is selected because Malaysia adopts an export-oriented growth strategy.

Besides, it is also evident from the literature that inconclusive and mixed findings of the relationship between economic growth and each of the variables (i.e., energy efficiency, CO2 emission, FDI, and exports). These inconsistent findings exist because most of the existing studies of economic growth only emphasize on two or three variables which may suffer from omitted variable bias. Thus, this study moves a step further by incorporating more variables, namely CO2 emission, energy efficiency, FDI, and export into a single growth model. Among these variables, this study considers the critical factor of energy efficiency of which will contribute to the existing literature. The study will focus on whether this variable is vital to be included into the growth model or not. This study will enable us to obtain a broader view of factors influencing economic growth, particularly in Malaysia.

Research methodology

This study uses the annual data for Malaysian economic indicators over the period from 1971 to 2013. These data are obtained from the World Development Indicators (WDI), published by the World Bank. This study uses the GDP per capita based on 2010 constant prices in USD as the proxy for aggregate production.

For the disaggregated level, production sectors are categorized into primary, secondary, and tertiary sectors. The primary sector includes forestry, hunting, fishing, cultivation of crops, and livestock production. In Malaysia, agricultural activities expressively contribute to the growth of the economy. These activities position the foundation and become the driving force behind the national economy. Agriculture is the primary source to finance the development of the country and steadily assist in the transformation of the economy towards industrialization. 48 The secondary sector refers to industry-related activities. Lastly, the tertiary sector comprises of wholesale and retail trade, transport, government, financial, professional, and personal services such as education, health care, real estate services, bank service charges, import duties, and others. As a proxy for real GDP per capita in representing the disaggregate production, value-added per capita based on 2010 constant prices for each production sector is used. This variable is measured in U.S. dollar.

This study chooses net export of goods and services at constant price in 2010 (measured in U.S. dollar), the net inflow of foreign investment (measured in % of GDP), and carbon dioxide emission (measured in metric tonnes per capita) to seek whether these variables could contribute to a significant effect on the economic performance. Energy efficiency is further considered in our analysis by taking the ratio of real GDP per capita to energy consumption (measured in a kilogram of oil equivalent per capita). a

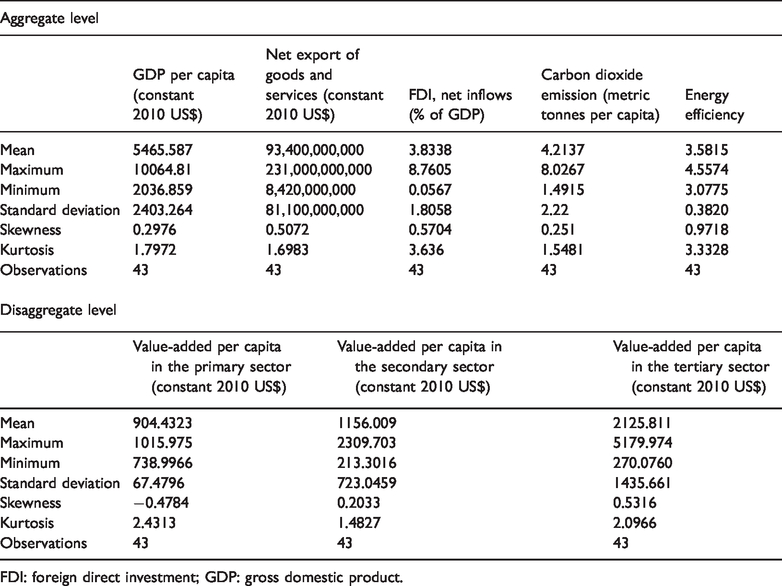

Table 1 shows the descriptive statistics of the variables used in this study. The mean of US$2125.811 for value-added per capita based on 2010 constant prices is found to be higher for the tertiary sector than primary and secondary sectors. It is also reported that energy efficiency provides the mean of 3.5815 with the maximum value of 4.5574. Looking at the skewness in aggregate and disaggregate levels, the statistics reveal that real GDP per capita, real value-added per capita for secondary and tertiary sectors are slightly skewed to the right, except for real value-added per capita in the primary sector. This positive skewness is also found for a net export of goods and services, FDI, carbon dioxide emission, and energy efficiency. All variables are converted into the natural logarithmic form. The reason is that it can reduce variation and induce stationarity in the variance-covariance matrix.

Descriptive statistics.

FDI: foreign direct investment; GDP: gross domestic product.

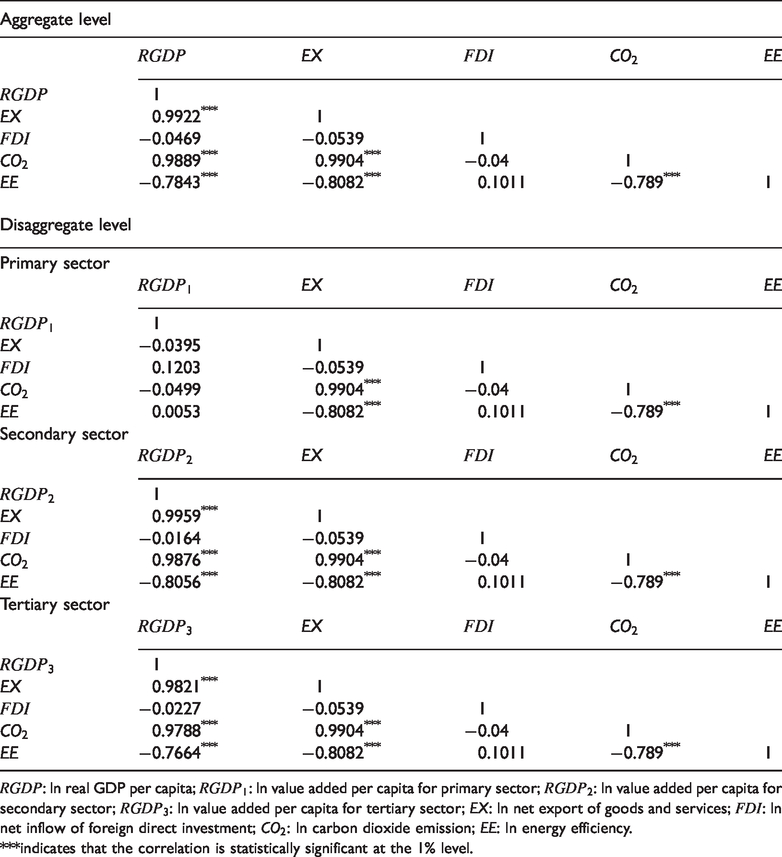

In Table 2, real GDP per capita for the aggregate level is positively correlated with the net export and CO2 emission. Besides, it is found that real GDP per capita is negatively correlated with energy efficiency at the aggregate level. The negative correlation is also found in the secondary and tertiary sectors. According to Kepplinger et al., 19 productivity growth in developing countries such as Brazil and India is not always achieved as a result of energy efficiency. In many cases, improved production is often obtained via a drop in energy efficiency or an increase in energy intensity. The same goes for Malaysia as a developing country. Only in the primary sector, energy efficiency and economic growth are found to be positively correlated. Similar results are obtained for secondary and tertiary sectors. Real GDP is found to have a positive correlation with net export and CO2 emission, respectively. The correlation between energy efficiency and real GDP remains negative due to energy consumption per capita is increasing more rapidly as compared to GDP per capita. This suggests that labour and capital in Malaysia are not fully utilized in optimizing energy use for production at the aggregate level. These relatively low skills among labours in accessing and using energy-related technologies are found in the manufacture and service-related activities.

Correlation coefficient matrix.

***indicates that the correlation is statistically significant at the 1% level.

Autoregressive distributed lag (ARDL) modelling approach is proposed by Pesaran et al. 49 There are four reasons for using this approach in our study. First, the ARDL model can be used for small sample size because it provides consistent estimators of the short-run parameters and super-consistent estimators of long-run parameters. 49 Second, the ARDL model does not restrict the order of integration of each variable, where it can be used to examine the existence of a long-run relationship among variables, whether the underlying regressors are I (0) or I (1). 49 Third, to assess short-run impacts directly and estimate long-run elasticities indirectly, lags of the dependent variable, lags of independent variables and contemporaneous variable are used in the model. Fourth, it is applicable when the independent variables are endogenous because it could simultaneously correct residual serial correlation. Following the modelling approach developed by Pesaran et al., 49 we perform the analysis with three steps for aggregate and disaggregate levels.

The first step is to examine the existence of a long-run relationship among variables by using the bounds test. Estimation of the error-correction version of the ARDL model (or an unrestricted error-correction model, UECM) is used to perform the testing. This model consists of short-run and long-run variables, which are in the first differenced and level form, respectively. The model is specified as equation (1).

Equation (1) is viewed as an ARDL

Pesaran et al. 49 develop a statistical table that consists of two sets of critical value for the F-statistic value at the significance level of 1%, 5%, and 10%. b With integrated order of a series whether zero or one, lower critical bound (LCB) is used for explanatory variables that follow an integrated order zero processes (I(0)), while upper critical bound (UCB) is used for explanatory variables that follow an integrated order one process (I(1)). They calculate critical values based on large sample sizes of 500 and 1000 observations, and 2000 and 40,000 replications, respectively. Narayan and Narayan 50 as well as Narayan 51 state that using the critical value of small sample size will lead to misleading results. To overcome such a problem, Narayan 51 uses a similar GAUSS code by Pesaran et al. 49 to generate a new set of critical values for small sample sizes ranging from 30 to 80 observations. c

Since the number of observations in the data in this study is small, Narayan’s 51 LCB and UCB are used to compare the computed test statistic value. If the F test statistic exceeds the UCB, the null hypothesis of no long-run relationship is rejected. This concludes in favour of the long-run relationship. If the F test statistic below the LCB, the null hypothesis is not rejected. If the F test statistic falls within the two bounds, the test will be inconclusive.

When cointegration is established, the second step is to obtain the long-run and short-run models based on the following tentative models for ARDL level relation (shown as equation (2)). The order of an ARDL

The long-run parameters are derived by using equation (3) to equation (7).

The resulted in the choice of ARDL

After obtaining the long-run relation, the error-correction model (ECM) in the first difference that associates with the long-run estimates is specified as equation (9).

The third step is to determine the short-run directions of causality by performing the Granger-causality test. To test the short-run causality, the null hypothesis is formed to state that set of new parameters for the first-differenced variables in equation (9) are equal to zero, indicating that no short-run causality exists between the variables. 52 The hypothesis testing is performed by using the F distribution. The rejection of the null hypothesis indicates that there exists a causal relationship between the variables in the short run.

Furthermore, one lagged error-correction term

Results and discussion

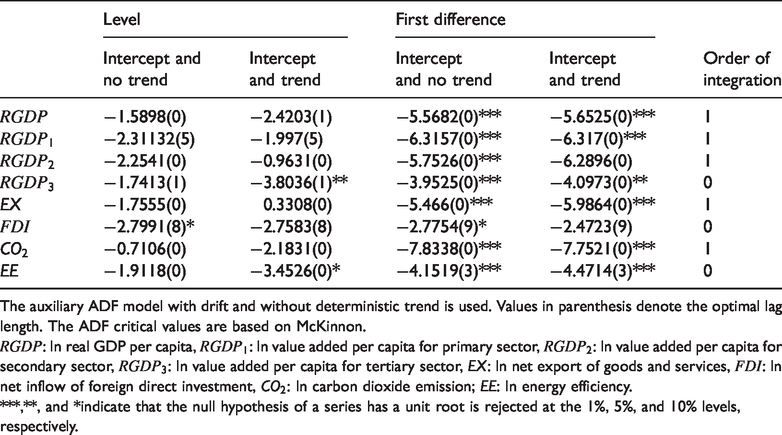

Table 3 presents the results of the unit root test. The results show that aggregate real GDP per capita, real value-added per capita in the primary sector, real value-added per capita in the secondary sector, net export and CO2 emission contains a unit root. Meanwhile, real value-added per capita in the tertiary sector, FDI and energy efficiency is found to be stationary at the level form.

Results of the augmented Dickey–Fuller unit root test.

The auxiliary ADF model with drift and without deterministic trend is used. Values in parenthesis denote the optimal lag length. The ADF critical values are based on McKinnon.

***,**, and *indicate that the null hypothesis of a series has a unit root is rejected at the 1%, 5%, and 10% levels, respectively.

The UECM of aggregate real GDP per capita and respective disaggregate real value-added per capita (equation (2a) to (2d)) are estimated. The robustness of the model is confirmed by Breusch-Godfrey serial correlation Lagrange multiplier (LM) and autoregressive conditional heteroskedasticity (ARCH) tests. These tests indicate that these models are free from autocorrelation and heteroskedasticity problems.

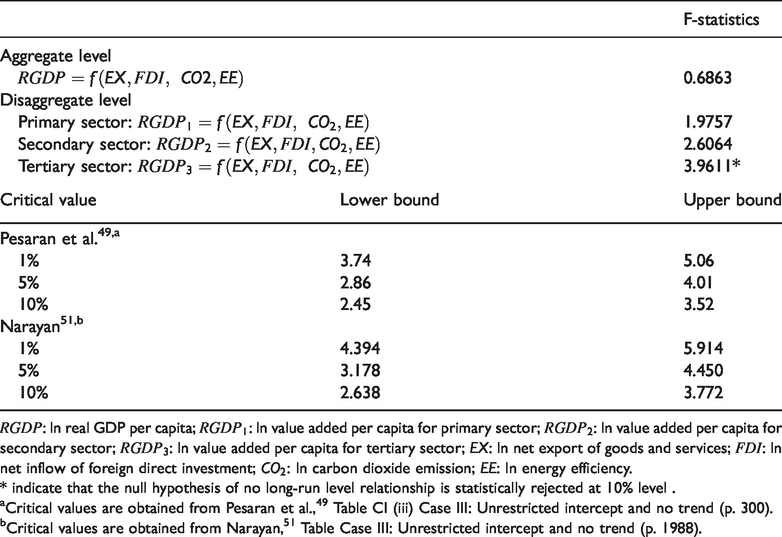

Based on the adequate model, the bounds cointegration is tested. Table 4 presents the results of the bounds cointegration based on aggregate real GDP per capita, real value-added per capita in the primary sector, real value-added per capita in the secondary sector and real value-added per capita in the tertiary sector. The computed F-statistic of 3.9611 for real value-added per capita in the tertiary sector is higher than the upper critical bound value at the 10% level from either Pesaran et al. 49 or Narayan, 51 indicating that there is a rejection of the null hypothesis of no cointegration. This suggests that the existence of steady-state long-run relationship among real value-added per capita in the tertiary sector, net export, FDI, CO2 emission, and energy efficiency.

Results of bounds test for cointegration analysis.

* indicate that the null hypothesis of no long-run level relationship is statistically rejected at 10% level .

aCritical values are obtained from Pesaran et al., 49 Table CI (iii) Case III: Unrestricted intercept and no trend (p. 300).

bCritical values are obtained from Narayan, 51 Table Case III: Unrestricted intercept and no trend (p. 1988).

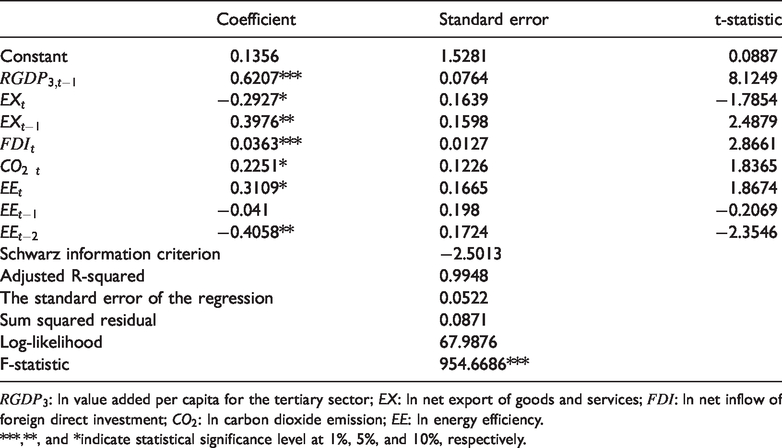

From the bounds testing, it demonstrates that the long-run relationship among variables is only established for the case of the tertiary sector. The ARDL (1, 1, 0, 0, 2) model is selected to fit the data of real value-added per capita in the tertiary sector. The results for this selected model are summarised in Table 5.

Results of ARDL (1, 1, 0, 0, 2) estimate for real value added per capita in the tertiary sector.

***,**, and *indicate statistical significance level at 1%, 5%, and 10%, respectively.

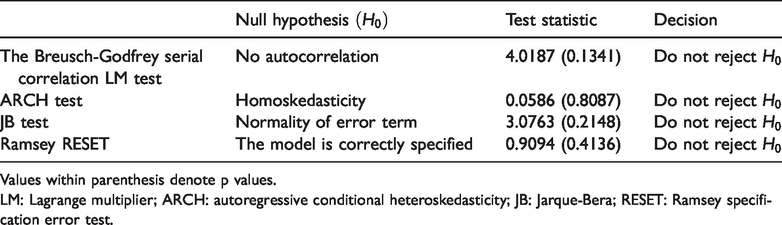

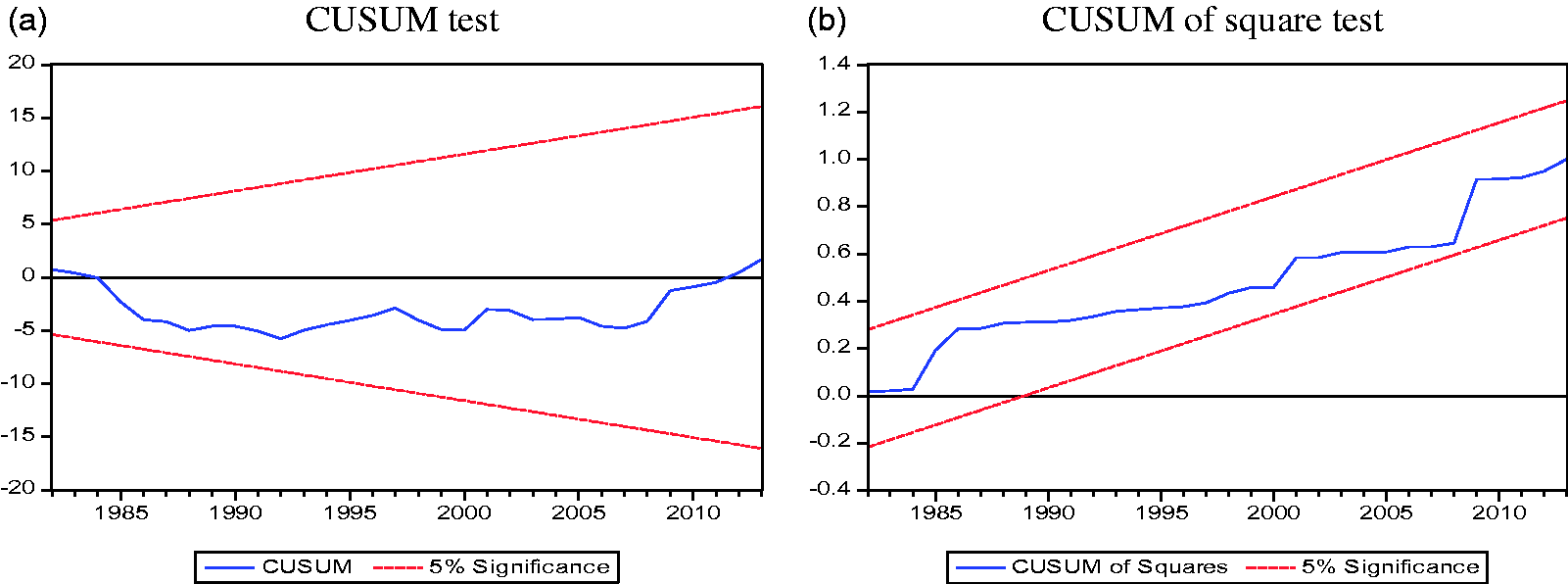

Table 6 shows the diagnostic testing of the selected model. The Breusch-Godfrey serial correlation LM test indicates that the model is free from the autocorrelation problem. The ARCH test indicates that the model is free from heteroskedasticity problem. Then, the Jarque-Bera test indicates that the error term of the model is normally distributed. Lastly, the Ramsey specification error test indicates that there is no functional form misspecification. Furthermore, plots of the cumulative sum (CUSUM) and CUSUM of square tests in Figure 1 indicate that there is no misspecification and structural instability of long-run and short-run estimated parameters in the sample period. This suggests that the model produces reliable estimation results.

Diagnostic testing for the equation of real value added per capita in the tertiary sector with ARDL (1, 1, 0, 0, 2).

Values within parenthesis denote p values.

LM: Lagrange multiplier; ARCH: autoregressive conditional heteroskedasticity; JB: Jarque-Bera; RESET: Ramsey specification error test.

Plot of cumulative sum (CUSUM) and CUSUM of square tests for the equation of real value added per capita in the tertiary sector.

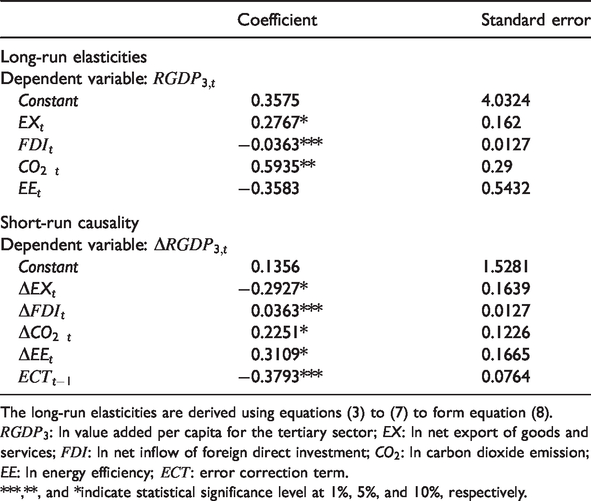

From the long-run model which explains the real value-added per capita in the tertiary sector, it is evident that net export enters with a positive and significant coefficient throughout, indicating that 1% increase of export leads to 0.2767% increase in real value-added per capita for the tertiary sector. The results indicate that export plays a vital role in encouraging the expansion of the tertiary sector in Malaysia. It is in line with the previous evidence such as Lean and Smyth, 32 Pistoresi and Rinaldi 42 and Sunde 43 who claim that export activities may help to enhance real GDP per capita. Most importantly, our result is also consistent with the government's plan of emphasizing on the development and growth of exports from the tertiary service sector as Malaysia aims to increase its share of exports from 12% in 2010 to 19% by 2020. As Malaysia is moving towards becoming a developed nation, exports from the service sector can serve as an engine of growth for the Malaysian economy. This is particularly true for service industries such as education, healthcare, travel, Islamic finance, and waste management, which have great potential for growth and export.

Meanwhile, an additional percentage increase in the net flow of investment significantly reduces the real value-added per capita for the tertiary sector by 0.0363%. This suggests that FDI does not help in promoting growth in the tertiary sector. Instead, it is harmful to the tertiary sector in Malaysia. Our finding is supported by Chakraborty and Nunnenkamp 39 and Duan et al. 38 who suggest that FDI does not play an essential role in contributing to output growth. However, it is contradictory with the findings of Amri 35 and Jayaraman et al., 53 who claims that FDI and economic growth are positively related. The positive linkage between FDI and economic growth can be explained by both the endogenous and exogenous growth theories. FDI can improve the host country’s economy through capital accumulation, the introduction of new goods and imported technologies (based on the view of exogenous-growth theory), and also by increasing the stock of knowledge in the host country via skill transfers based on the endogenous growth theory. According to OECD, 54 multinational companies (MNCs) who invest in the host country can generate positive externalities via technological transfer. Thus, the positive relationship between FDI and economic growth in the host country is based on the assumption that MNCs who invest are mainly from developed countries. MNCs from wealthy countries can invest hugely in R&D that can, in turn, lead to technological spillovers in the host country. Besides, the significantly positive relationship is often found in developed countries as FDI encourages capital accumulation and knowledge spillovers. For instance, Liu et al. 55 on the United Kingdom, Pegkas 56 on Eurozone countries and Sharma et al. 57 on European Union demonstrate that both variables are positively correlated.

For this study, the negative relationship between FDI and growth in the tertiary sector is expected as Malaysia is a developing country. Specifically, two possible reasons can explain the adverse effect of FDI on real value-added per capita in the tertiary sector in developing countries. First, local service firms may not be able to compete with foreign firms, leading to a reduction in economic productivity as foreign firms have a much lower cost of production, thus enabling them to steal demand from local firms. Second, the positive knowledge spillovers may not necessarily occur in the case of developing countries as they have insufficient skilled labours and underdeveloped financial markets. 58 Furthermore, Sen 59 and Thirlwall 60 argued that MNCs might bring negative technological spill-overs or transfer inappropriate technological know-how to the local firms via FDI. In such a case, the host country’s economic development could be retarded as a result of FDI. In short, the theoretical and empirical literature may provide different outcomes on the impact of FDI on economic growth. 61

For CO2 emission, its additional percentage change significantly increases the real value-added per capita by 0.5935% in the tertiary sector. The result is consistent with findings by Dinda 29 and Youssef et al. 30 who suggest that better economic performance can be achieved with a more polluted environment. This finding may also imply that the utilization of conventional fossil fuels is much more than the less-polluting energy sources in Malaysian tertiary sector. In 2014, fossil fuel energy consumption (% of total) in Malaysia was recorded as high as 96.63% according to the World Bank. The burning of fossil fuels such as coal, oil, and natural gas to produce electricity and power vehicles for the tertiary sector emit various types of pollutants, including CO2 into the atmosphere. The healthy development of the service industry in Malaysia translates into increased real value-added per capita in this sector. However, the result of long-run elasticities shows that the impact of energy efficiency on real value-added per capita is not significant for the tertiary sector. Energy efficiency has no relation to the real value-added per capita in the tertiary sector. In other words, production volume in the tertiary sector is not affected by its energy consumption per unit of output.

From the error-correction model, short-run impacts of net export, FDI, CO2 emission, and energy efficiency on real value-added per capita for the tertiary sector are further investigated. As indicated in Table 7, net export, CO2 emission, and energy efficiency are found to Granger cause the real value-added per capita for the tertiary sector at the 10% level, while FDI provides Granger causality to real value-added per capita at the 1% level.

Long-run elasticities and short-run causality of real value added per capita in the tertiary sector.

The long-run elasticities are derived using equations (3) to (7) to form equation (8).

***,**, and *indicate statistical significance level at 1%, 5%, and 10%, respectively.

In terms of the long-term disequilibrium (or imbalance) in the real value-added per capita,

For the tertiary sector, we determine how much of deviations from the long-run production in 1980, 1990 and 2000. To achieve the long-run production in the subsequent year, we would obtain how much of deviations in the value-added per capita from the tertiary sector should be corrected. For example, the error correction term in 1980 is found to be 0.1824. This indicates that real value-added per capita in 1980 is above its long-run equilibrium by 0.1824%. In the case of any internal shock or external shock to real value-added per capita, the tertiary sector would react its value-added per capita toward the long-term path in 1981 by decreasing 0.0692%. In 1990, the error correction term indicates that the real value-added per capita is above its long-run equilibrium by 0.0146%. To restore the equilibrium in 1991, its value-added per capita is required to decrease by 0.0055%. The shrinkage of value-added per capita in the tertiary sector to achieve the long-run equilibrium, supporting that Malaysia heavily relied on the agricultural and manufacturing sectors before 2000. Besides, the government services contributed to a large share of the tertiary sector in the mid of 1980s and 1990s as the economic activities were mainly pioneered and hedged by the government. The occurrence of the 1997 financial crisis led the government to deregulate and liberalize the tertiary sector such as selective capital controls, debt restructuring and recapitalization of the banking system.

However, the error correction term in 2000 indicates that the value-added per capita is below its long-run equilibrium by 0.1216%. To achieve long-run production at the end of 2001, the tertiary sector would increase its value-added per capita by 0.0461%. Such an adjustment during the period of 2000–2001 demonstrates that the country undertakes the short-term development planning for the stimulus of monetary and fiscal measures in driving industries' performance, especially Islamic banking, finance, telecommunication, and tourism. For example, the government implements the 2000 national strategy to eliminate direct participation and transform economic development into a public–private sector partnership. As a result, the Malaysian economy would grow as the financial sector resilient with profitability and support monetary policy.

Table 8 presents the results of dynamic short-run causality among the determinants of real GDP per capita for aggregate level as well as for the disaggregate level, primarily real value-added per capita in both primary and secondary sectors. This can be done by restricting the coefficient of an interesting variable with its lags equal to zero and testing the existence of Granger causality from such variable to real output (real GDP per capita and real value-added per capita). The rejection of the null hypothesis of no Granger causality indicates that an interested variable Granger causes real output.

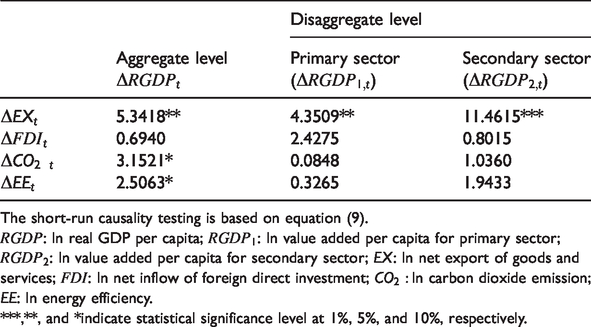

Results of short-run causality.

The short-run causality testing is based on equation (9).

***,**, and *indicate statistical significance level at 1%, 5%, and 10%, respectively.

For the aggregate level, the empirical results indicate that all variables significantly Granger cause real GDP per capita, except FDI. As net exports Granger cause real GDP per capita, it can be concluded that trade activities are essential in ensuring a stable and sustainable economy in Malaysia. Our finding is consistent with previous empirical studies such as Kubo, 62 Hye et al., 63 and Fatemah and Qayyum, 44 who also support the export-led growth hypothesis. A few reasons can be put forth to explain the positive relationship between exports and economic growth in Malaysia. First, export expansion stimulates the production of more goods for exports that makes the exploitation of economies of scale and the country's comparative advantages possible. Second, stiff foreign market competition encourages local firms to engage in technological innovation. Third, the foreign exchange earned from exports enables Malaysia to increase imports of capital goods and the latest technologies that, in turn, raise production and income. Besides, Granger causality is found running from CO2 emissions to GDP. Higher CO2 emissions tend to lead to better economic performance in Malaysia.

Our result does not seem to support the neo-classical assumption that economic growth is unaffected by the use of energy. 64 As a developing country, the demand for energy has been increasing over the years. This phenomenon does not only impact the environment but also contributes to robust economic growth in the country. It is also shown in Table 7 that energy efficiency Granger causes economic performance. The result confirms the previous evidence that energy efficiency tends to stimulate output growth in the economy.16,17,65 Our finding is also aligned with the national energy efficiency policy of Malaysia. It is stressed in the national energy efficiency policy that by boosting energy efficiency, waste can be minimized in order to contribute to sustainable growth in the economy.

For both primary and secondary sectors, all variables are found to be not significant to Granger cause real value-added per capita, except for net export. This indicates that net export is an essential determinant of real value-added per capita in the short run. The significance of exports can be proven by the fact that Malaysia has been relying on exports from the primary and secondary sectors for achieving impressive growth in the past decades. For instance, Malaysia's GDP grew by 5.9% in 2017, mainly attributed to an exceptional performance from exports. Exports from the primary and secondary sectors continue to be the primary source of income for Malaysia. Significant exports of Malaysia include petroleum products, electrical and electronics, chemicals, and palm oil.

Theoretical and practical facts underpinning the estimated output

From the theoretical point of view, the estimated output of this study is in contradiction to the conventional theories of growth such as classical and neoclassical models. The early theories emphasize the understanding of economic growth and attempt to find out the general factors affecting growth that could be applied at all times and in all countries. In particular, these theories focus on the importance of certain factors such as labour and capital for growth. Instead, our estimated output is aligned with the modern theories of growth, which suggest that conditions for growth change over time. Based on modern theories, the emphasis on the innovations will enhance the energy efficiency, in turn, stimulating economic growth. The initial impact is believed to be channelled to the tertiary sector the most which is in line with our results.

From a practical perspective, the estimated outcomes of our study are of great importance to the policymakers. Previously, the decision making about how to improve economic performance in Malaysia often did not take into consideration those factors which seem not crucial to growth such as CO2 emission and energy efficiency. Instead, the government's focus was more about the common factors affecting economic growth, such as inflation, capital stock, FDI, and export. However, in recent years, the Malaysian government starts to look into the effects of air pollution on the economy. Currently, the country is aiming to achieve sustainable economic development. For example, it realizes economic aspirations without compromising on environmental quality. Thus, the estimated output of our study is timely, and it can provide insightful policy directions to the government of Malaysia. For instance, our findings reveal the fact that only CO2 emission, energy efficiency, and export contribute to growth at the aggregate level, but not FDI. The results are indeed in line with the government's current efforts of gearing its policies towards increasing exports, improving energy efficiency, and adopting renewable energy sources in the country. In the meantime, the government needs to scrutinize the reason(s) for the fact that FDI does not contribute to growth. Furthermore, the estimated output at a disaggregated level can also provide hints to the government on the appropriateness of the current policies applied in each of the sectors in Malaysia.

Conclusion

Amid sluggish economic growth, Malaysia, as an energy-dependent country, encounters the dilemma of the trade-off between energy efficiency and economic growth. By using Granger causality test based on an autoregressive distributed lag (ARDL) modelling approach, this study empirically examines the relationship between energy efficiency and economic growth in the presence of CO2 emissions, exports, and FDI in Malaysia. Additionally, we are particularly interested to see the extent to which energy efficiency contributes to economic growth in each of the primary, secondary, and tertiary sectors.

Our results indicate that energy efficiency Granger causes economic growth at the aggregate level, but not in each of the three main sectors of the economy. It is also interesting to note from the correlation coefficient matrix that energy efficiency and real GDP are found to be negatively correlated. Therefore, further efforts and commitments should be given to other factors that might have been contributing to economic growth, such as small and medium enterprises, domestic investment, and local consumption in the country. However, it does not imply that we can neglect the importance of energy efficiency as it still helps to reduce environmental degradation in the country.

Another important finding of this study is that the export-led growth hypothesis is found to be valid in Malaysia at both the aggregate and disaggregate levels. This implies that export is not only playing an essential role in enhancing the overall economic performance, but also helping to improve the value-added per capita in the primary, secondary, and tertiary sectors. Thus, it is suggested that the policymakers should adopt the existing export-oriented policies continuously while coming up with new strategies that can further encourage exports.

The results of our study also confirm the fact that CO2 emissions do influence overall and sectoral growth, except in the primary sector. This indicates that pollution in the secondary and tertiary sectors has led to income growth in Malaysia. This phenomenon shows the substantial reliance on traditional energy such as fossil fuel in the process of Malaysian industrialization and transportation. The upward trend between CO2 emissions and economic growth is commonly related to energy consumption, where the intensive use of energy in the production or service line would incur the environmental externality that in turn, boosts the productivity. Even though CO2 emissions induce economic expansion, this does not mean that pollution can be used as a ‘tool' to obtain better growth. Instead, the government should attempt to embrace the concept of green economic growth, a strategy for Malaysia to realize sustainable development. Thus, it is suggested that the country should seriously consider using more renewable energy sources, particularly in secondary and tertiary sectors rather than fossil fuels, to achieve sustainable growth.

As FDI does not contribute to economic growth, it is time for the policymakers to relook into the absorptive capabilities of the country that include human capital, financial system, trade policy, and formal institutional frameworks. Only with excellent absorptive capabilities, the full benefits of FDI inflows can be obtained. Although the significance of energy efficiency and sectoral growth is investigated in this study, the future attempt can be conducted to determine the existence of asymmetric effect among the variables using more advanced analytical techniques. To further obtain more solid outputs, some advanced modelling such as Markov-switching and structural models can be used to capture the potential effect of regime-switching and structural breaks.

Footnotes

Acknowledgements

We would like to thank the Associate Editor and anonymous referees for their helpful suggestions and corrections on the earlier draft of our paper and upon which we have improved the content. This paper is the revised version of an earlier work presented at the 5th International Conference on Business, Accounting, Finance and Economics held at the Faculty of Business and Finance, Universiti Tunku Abdul Rahman (UTAR), Kampar Campus, Malaysia on 4 October 2017.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.