Abstract

In recent decades, wind energy has undergone significant progress, with the contribution of countries such as China, the United States, Germany and Spain standing out, although there is no single comprehensive model for promoting renewable energy worldwide. In Spain, the regions of Galicia, Castilla-La Mancha and Andalusia have led this process, with significant changes in their contribution depending on the economic situation and the varied legislative framework in force at any given time. Although wind energy is less harmful to the environment, it is not harmless, and environmental impact and its penalisation is one of the key elements in the applicable regulations. In the case of Spain, the three regions mentioned above, out of a total of seventeen, apply their own taxes to tax the environmental impact of wind energy. The aim of this paper is to describe and compare the wind tax applied in the aforementioned regions from 1995 to 2020; to characterise wind taxation socio-economically, and to assess the suitability of this type of taxation to tax the environmental impacts associated with wind energy activity in Spain. The differences in tax treatment are notable and it is observed that the concept of environmental impact has been anchored in the past and, today, older wind farms with less powerful wind turbines are those that bear a greater tax burden, while more modern, more powerful and larger wind farms (with a significant environmental, acoustic and visual impact) may even be exempt from taxation.

Introduction

Since the end of the 20th Century, renewable energies have been evolving rapidly worldwide, and wind power has been in the vanguard of this change, and it has been widely stated in the literature. This dynamic may be ascribed to a number of factors, but the foremost of these is undoubtedly the establishment of policies that aim to foment more sustainable development through the use of renewable energies.1–3 In terms of installed capacity, the proportion of wind power generation has risen from 9.5% in 2007 to 24.5% in 2020 (Figure 1).

World renewable energy installed capacity (on grid) (2007–2020) (%). Source: Author’s elaboration from IRENA. 4

Presently, the wind industry is playing an important role throughout the world since it is providing new employment opportunities, diversifying the sources of energy production, contributing significantly to sustainable development and helping to mitigate climate change.5–7 Wind energy is expected to play an increasingly important role worldwide, progress that will be driven by a combination of more intensive exploitation and technological improvements. 8 In spite of a systemic crisis and the consequent negative impact on the traditional model of financing renewable energy installations, the most recent reports,4,9 allow us to confirm the strength of the wind sector worldwide and a significant concentration of wind power generation within six countries (Figure 2).

World leader wind installed capacity countries (2007–2020) (%). Source: Author’s elaboration from IRENA. 4

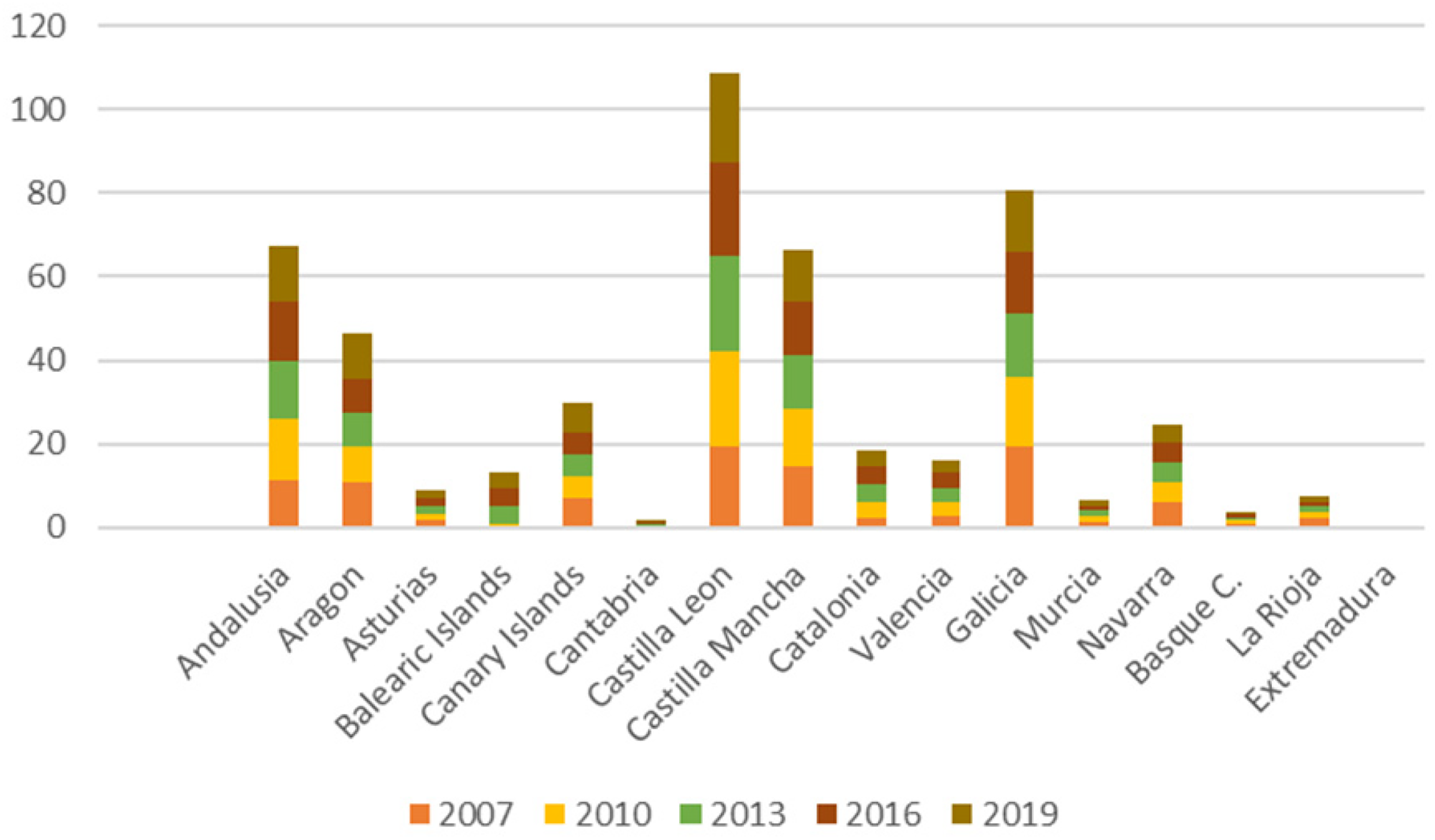

The applicable regulations and the wind development model followed by the pro-producer countries have not been unique, although the Danish model has served as a reference. In Spain, regulations affecting the generation of wind power vary considerably depending on the autonomous region. Three of these regions have been at the forefront of the development and evolution of wind power since 1995; Galicia, Castilla León, and Castilla-La Mancha. These are the regions whose wind power sector has evolved most notably and whose weight as a proportion of total Spanish production has been the greatest by far in recent years. In fact, the combined production of the four regions represents 70% of the total capacity for Spain in 2019 (Figure 3) and 65% of the installed wind turbines (Figure 4).

Wind installed farms in each of the Spanish regions (2007–2019 2 )(%). Source: Own elaboration from AEE 10 *. (*):In Figures 3 and 4, in relation to Extremadura, the values are not very significant, so they are not shown. In spite of this, we consider it important to include it in the list of regions, in order to see the disparate evolution shown.

The aim of this paper is multiple: (i) firstly, to describe and compare the wind tax applied in the three regions indicated, from 1995 to 2020, identifying the common elements and the differences. (ii) Then, to characterise the wind tax socio-economically. (iii) Finally, from a critical perspective, assess the suitability of this type of tax to tax the environmental impacts associated with wind energy wind energy activity in Spain, with an alternative proposal for policy makers to consider. The selection criteria for the three regions of analysis were the installed wind power capacity, their pioneering wind energy trajectory in Spain and the existence of a wind tax applicable in each region. From the analysis of the existing scientific literature, we have not identified any contributions that allow us to make a regional comparison, within the same country, on the differences generated by the same tax on the wind resource.

The novelty of this research lies in the socio-economic comparison of the three types of wind tax in Spain, as well as in the critical analysis of the capacity to penalise the environmental impacts associated with the wind business. However, it also has limitations, such as the lack of updated data on all the wind farms installed in the regions under study, the lack of tax data for each wind farm and the lack of historical data on the part of the tax revenue allocated to mitigate the environmental impact of wind energy. The novelty of this research lies in characterising the impact of the application of a wind tax, theoretically with the same purpose, but which presents notable differences in the three regions, demonstrating that the level of penalisation is very different.

Compared to fossil fuels, wind energy is the energy source that is most compatible with animals and human beings in the world. Wind energy is less harmful to the environment, and generates both positive and negative impacts (both in the construction and operation phases).12,13 The positive environmental impacts are mainly twofold 12 : (i) reduction of water consumption(conventional power plants use large amounts of water);and (ii) reduction of carbon dioxide emission (wind energy has zero direct air pollution). The negative impacts are associated to its construction and maintenance phases, and some wildlife impacts (impacts on wildlife with mortality from collisions with wind energy plant while the indirect impacts are avoidance, habitat disruption and displacement;noise impact;visual impact).14–16 To penalise the negative impacts generated, the public sector can act through various instruments, including taxes, whose application may be correct but not neutral, and may cause other undesired effects (paralyzing investments). There are several reasons that justify the existence of energy taxes, which can be roughly grouped in three main headings: revenue-raising motives, correction of environmental externalities, and capture of rents associated to natural resources that are used in energy production or consumption energy taxes.17,18 Thus, energy taxes can incorporate in their structure elements that are more or less closely related to the environmental damage caused, a characteristic that justifies their identification as environmental taxes, or energy-environmental taxes. The introduction of environmental taxes, particularly on energy, faces major political obstacles due to their impact on competitiveness, their impact on low-income citizens, their impact on world trade and existing subsidies. 19 The lack of a framework for environmental energy taxation with a supranational vision prevents this taxation from being at its optimum level, with only marginal changes in national, regional and local taxes. Energy-environmental taxation is one of the instruments available to political decision-makers to correct environmental externalities, although the use of these taxes—up to now—is below their real potential. The need to comply with the Paris agreement and be in a position to achieve the Sustainable Development Goals by 2030 20 requires an in-depth reflection on existing environmental taxes and their possible modulation in the immediate future to adapt them to reality. For example, electricity taxes often do not differentiate between different energy producing sources, generally not favouring cleaner energy sources and emission reductions. However, most countries encourage the green energy transition by taxing fuels more heavily than hydro, wind and solar, and energy use tends to be less carbon-intensive. 20

Thus, the countries that pioneered the use of green taxation began their tax reforms with a view to compensating for the revenue-raising potential of lowering other, more perceptible taxes, such as income tax, for example. After this first generation, a second wave of green tax reforms (GTRs) emerged, which moved towards compensating labour costs such as social security contributions, following the rise in energy taxes, in an attempt to influence the labour market. After the 2008 crisis, heterogeneity has taken over the third generation of green strategies (Figure 1), without much progress in the internalisation of environmental externalities, which is still a long way to go. 20 (Figure 5)

Green taxes reforms. Source: Author’s elaboration from Gago et al. 21

This reality is particularly striking in the Spanish case, where the absence of a national green tax strategy has been exploited by the Autonomous Regions to use environmental taxes for extra-fiscal purposes, with the aim not so much of raising revenue as of intervening in the economy. One of the most important areas of action of the regional government are those levied on the energy sector. Green decentralisation, which, a priori, does not necessarily have to be negative, works against a harmonisation that avoids the judicialisation of certain tax mechanisms that can play an essential role in environmental effectiveness. 22

The structure of paper is as follows. In Section “Literature review” we present the literature review. The analytical methodology used together with a description of the statistical information and the case study are in Section “Materials and methods”. The results we obtain are showed in Section “Results and discussion” and a discussion of their implications. The last section offers the key findings and policy implications that can be derived from the results.

Literature review

There is an extensive bibliography on factors related to the installation of wind farms: socioeconomic, environmental, energy, cultural, territorial, political, technical and technological. The importance of each factor may vary in different regions and the context.23–25 For this study, the characterisation of energy taxes applied to wind energy due the environmental impacts of wind development are the most important.

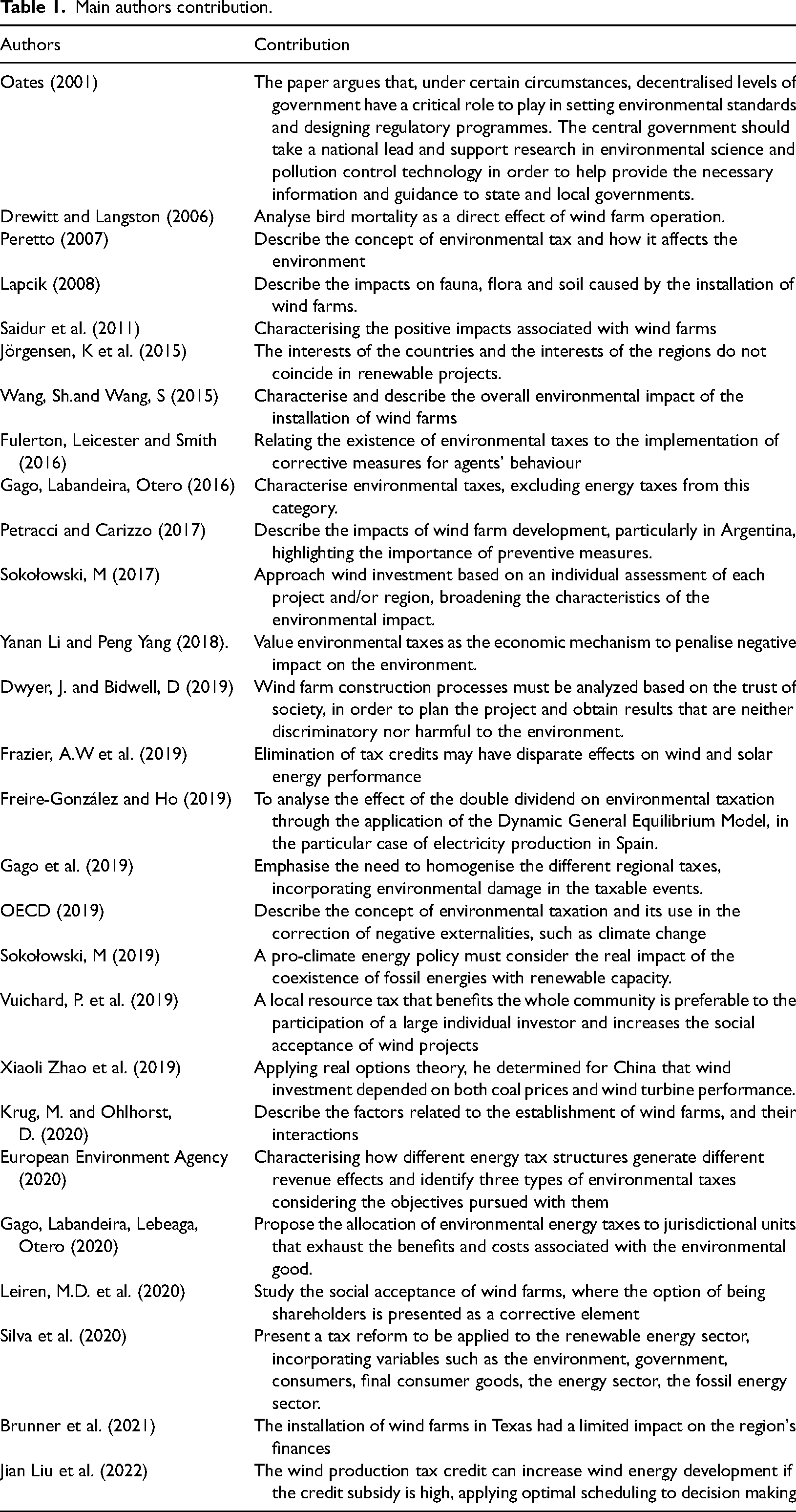

To understand this characterisation, it is necessary to start from the link between energy policy and the climate aid policy that countries wish to pursue. Countries that opt for a pro-climate energy policy start from an understanding of the implications between the coexistence of fossil fuels (desirable decreasing trend) and renewable capacities (increasing trend), 26 which can lead to discrepancies between objectives at the country and regional level, 27 as well as in the means of supporting the expansion of green energy. In the case of wind energy, investments require comprehensive regulatory frameworks, which allow for individual assessments according to the specific characteristics of the regions where wind farms are to be located in order to safeguard environmental impacts. 28 For example, real options theory has shown that in China, wind promotion policies are affected by the uncertainty associated with carbon prices and wind turbine performance due to weather conditions. 29 In Texas, the impact of wind farm installation was limited in improving the region's finances and citizens’ opportunities, with the exception of a modest increase in current spending. 30 Another figure to consider is tax credits (especially on production) that promote wind advancement, according to results obtained through optimal programming analysis, 31 although depending on the strength of the market they can also cause brakes on promotion. 32 In the field of taxation, Dwyer and Bidwell 33 highlight the importance of analyzing the process of wind farm promotion starting from the defense of the public interest, allowing its participation to integrate common interests and minimize the impact of externalities. In this sense, Vinchard et al. 34 highlight the effectiveness of a tax on local resources that benefits the entire community and reduces the presence of large individual financial investments led by international companies that do not care about the impact on the environment.

The bibliographical references on environmental taxes and/or energy taxes focus mainly on their application to fossil fuel electricity generation and, almost token stically, on renewable energies. It is this theoretical approach that will be used in this research. It is necessary to clarify the difference between environmental or environment-related taxes, energy taxes and energy-environmental taxes.

Environmental taxes are a useful tool to reduce environmental impacts associated with energy consumption and production, particularly global warming and climate change. 20 Typical environmental taxes in developed countries include air pollution tax, water pollution tax, noise tax, solid waste tax and garbage tax. Environmental taxes are the economic means of allocating the social costs of the environmental pollution and ecological destruction to the production costs and the market prices, and then distributing the environmental resources through the market mechanism. 35

The classification of environmental taxes is limited to the nature of the taxable events, which must be exclusively environmental, excluding energy taxes. The aim of this type of tax is to correct environmental damage and generate revenue that governments can use to reduce existing distortions, thus achieving an extra benefit or increase in non-environmental welfare. The theory of the double dividend arises, where the first dividend is given by the environmental improvement obtained, and the second represents all the additional changes in welfare generated by the use of the environmental revenue. 36

The European Environment Agency 19 states that there are three types of environmental taxes depending on their programmatic objectives, which generate different levels of effectiveness: (i) cost-covering taxes (to cover the costs of environmental services and pollution control measures; (ii) incentive taxes (to change the behaviour of producers and/or consumers; (iii) environmental taxes for fiscal purposes (to increase revenue). The main reasons put forward for the establishment of environmental taxes are the internalisation of externalities in the price of the goods, services and activities that produce them; the application of the “polluter pays” principle, integrating economic and environmental policies, encouraging changes in the behaviour of agents; the stimulation of innovation and structural changes; and to reinforce compliance with regulatory provisions. 37

Energy taxes are levied on energy products (gas, coal, petrol, etc.) and energies (electricity, nuclear, renewable, etc.) at the different stages from production to consumption and in various forms: general and specific taxes, taxes on energy produced and consumed, earmarked and non-earmarked taxes, etc. 38

Assessed the establishment of a tax that would penalise the production of electricity by coal-fired power plants, from the transport of the mineral to the consumption of that electricity (33). Among energy taxes, taxation on electricity increases the cost of electricity, reducing demand and thereby the associated environmental burdens. The concrete effects of electricity taxation depend on the configuration of the tax. Regarding Spain, some studies have analyzed the impacts of energy or carbon taxes using different methodologies,38,39 but not in the long-term context of renewable energy transitions. Applied to renewable energies, Silva et al. 40 propose a tax reform that incorporates as variables, the environment, government, consumers, final consumer goods, the energy sector, the fossil energy sector, and the renewable energy sector. Another authors 22 indicate that environmental energy taxes should preferably be allocated to jurisdictional units that exhaust the benefits and costs associated with the environmental good, so that they can generate competition between regions to increase environmental quality and attract citizens, thus increasing the benefits of fiscal policy. In Spain, there are four categories of environmental energy taxes applied at the regional or autonomous community level: (i) on atmospheric emissions; (ii) on installations and activities that have an impact on the environment; (iii) wind energy taxes; and (iv) taxes on dammed water. All of them are characterised by not defining the externality appropriately, not estimating adequately the social costs, not considering the spatial scope of the environmental damage taxed. Table 1 presents a compilation of the main theoretical contributions mentioned in this section.

Main authors contribution.

Materials and methods

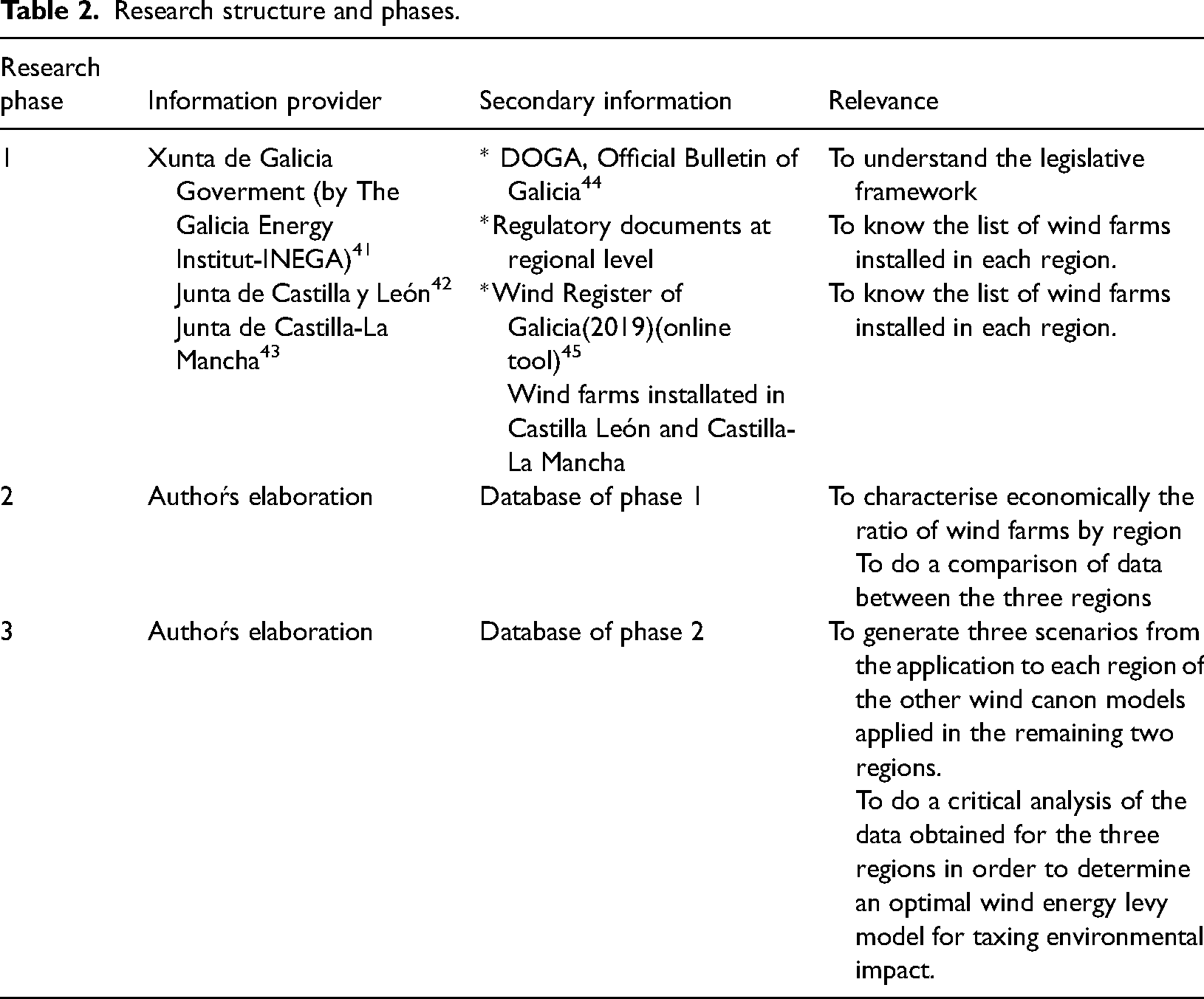

Analizing the factors that explain the win canon in Castilla León, Castilla-La Mancha and Galicia, and its adequacy to the “polluter pays” principle require the use of different quantitative and qualitative methods, and a theoretical approach was used, based on three consecutive and interdependent phases. The main source of information for this re-search paper came from the systematisation of data gathered from secondary sources and our analysis was based on publicly available data (see Table 2). The information is not homogeneous for the three regions, the main limitation for the analysis, because the official data for the three regions do not include the same variables, nor do they refer to the same period (for Castilla León and Galicia they correspond to the period 1995–2019, and for Castilla-La Mancha to the period 1995–2014) and there are two official data sources for Galicia, with non-coincident content.

Research structure and phases.

It has been necessary to carry out a more exhaustive study of the available information in the three phases proposed, especially for Galicia:

Phase 1: Summary of all wind farms installed in the three regions. In the case of Galicia, this was done by comparing the two official sources of information, the Register of wind farms (online tool) and the Wind farms installatd inform of Inega. Phase 2: socio-economic analysis of the samples of wind farms in the three regions, based on the applicable wind tax regulations in Castilla León, Castilla-La Mancha and Galicia. The variables under study were:

Name of wind farm City council or councils of location Province or provinces of location Total number of wind turbines in the wind farm Unit power of the wind turbine. This variable is important to have an approximation of the possible environmental impact by technology, visual impact and acoustic impact. Total power of the wind farm Unit tax rate: depending on the number of wind turbines in the wind farm and in accordance with the provisions of Law 8/2009, wind farms with more than three wind turbines will be taxed by wind tax, regardless of their technological capacity, size and age (€). Total fee: theoretical total fee for each wind farm, calculated for one calendar year of operation (€). Singular wind farms and corporate wind farms were not considered as it was not possible to obtain information for all of the above variables. Phase 3: comparative scenarios of wind farm fee adequacy. For each region, the wind tax model of the other two regions was applied to see the variations in the theoretical tax rate, and to assess which of the three regulations would be more realistic for taxing the environmental impact associated with wind activity.

Case study

Case study analyses provide the opportunity to develop a rich understanding of the characteristics and outcomes involved in the implementation of wind power taxes at a regional and local level.

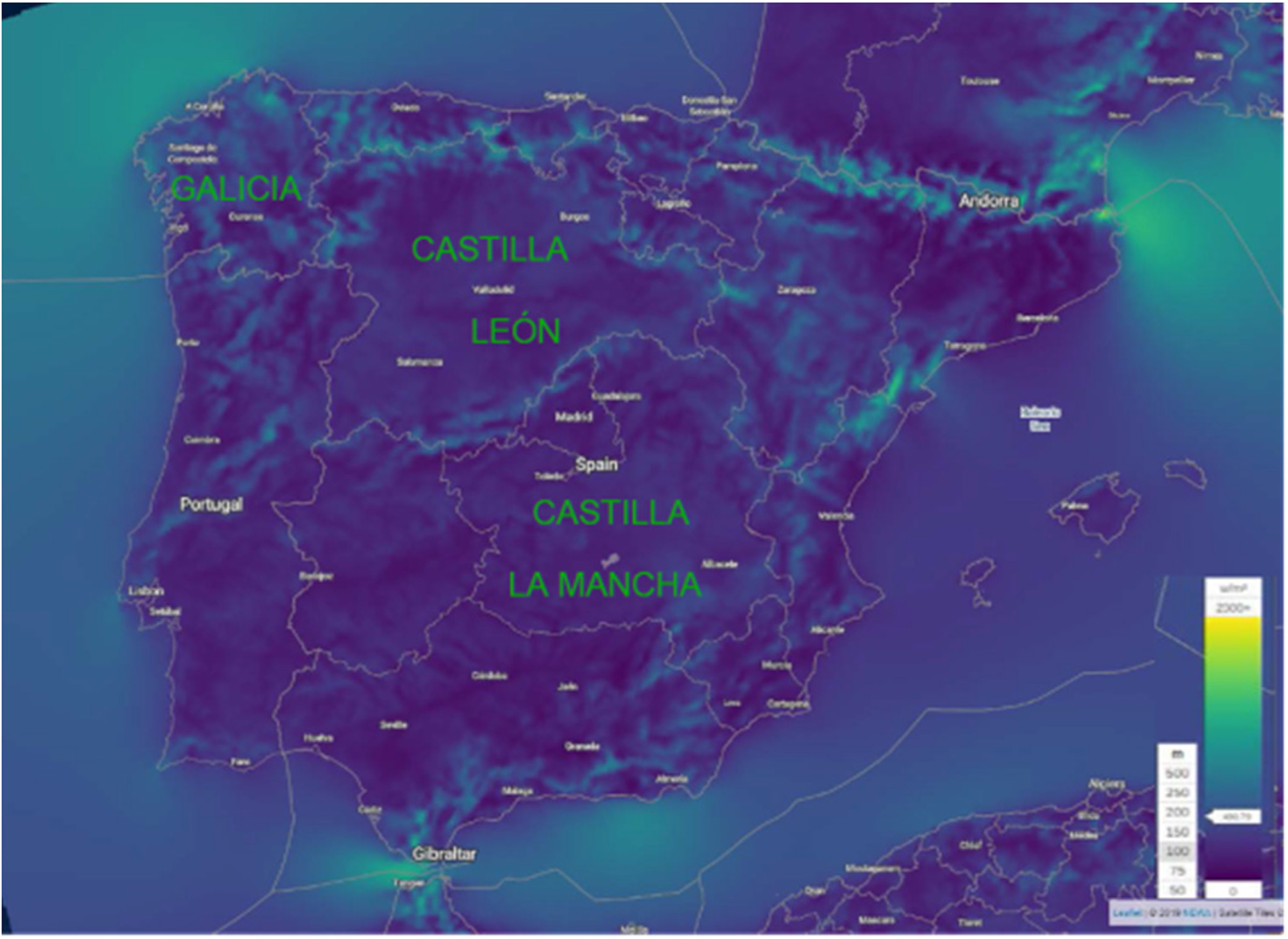

In Spain, the complexity of the energy system and also of the electricity mix (covered by much legislation but lacking integrated wind policy) and the optimal wind registers (onshore and offshore) led to an unequal growth of wind promotion in Spain, which was organised on a regional basis but had not been matched by policies for the whole sector (Figure 6).

Wind atlas of Spain and the regions of Castilla León, Castilla La Mancha and Galicia. Source: Author’s elaboration from New European Wind Atlas 46 .

The importance of the three selected regions is justified by the remarkable wind resources for industrial exploitation, so that from 2007 to the present (2021) (Tables 3 and 4), they have hosted between 59% and 53% of the installed wind power capacity in Spain, as well as between 53% and 48% of the installed wind farms. In the case study, a total of 483 wind farms were analysed for which information was available for all the variables considered, with 117 wind farms in Castilla-La Mancha, 138 wind farms in Galicia, and 238 wind farms in Castilla León.

Comparison of existing spanish regulations on wind energy taxation.

Fees applicable in the Castilla Leon wind farm levy.

Results and discussion

Comparison of regulations and economic assessment

The comparative analysis of the regulations highlights differentiating elements in the different parts of the regulations (Table 3), as well as three different scales for the calculation of the tax liability (Tables 4–6).

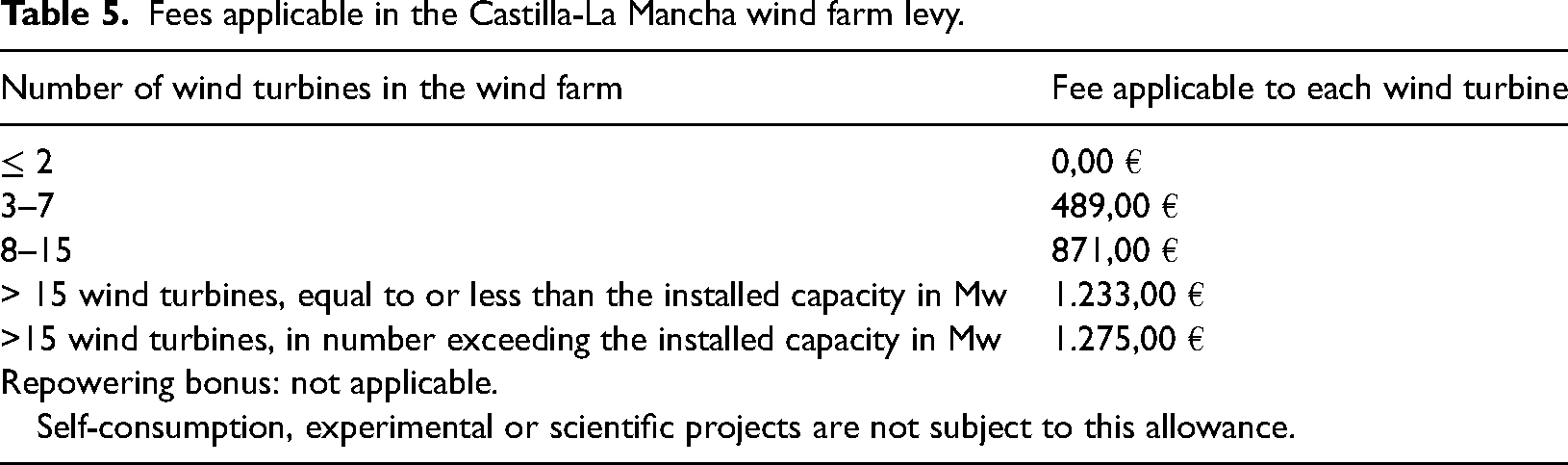

Fees applicable in the Castilla-La Mancha wind farm levy.

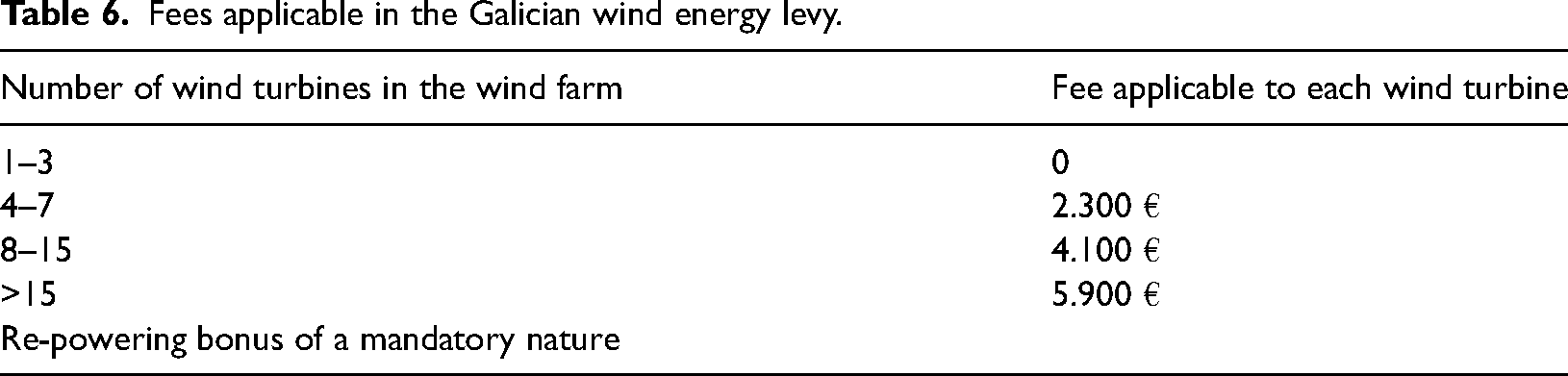

Fees applicable in the Galician wind energy levy.

The Castilla León wind tax 42 establishes that the tax rate will be calculated according to the power of each installed wind turbine, and according to the following scale (Table 4):

The Castilla-La Mancha wind tax 43 indicates that the tax rate will be calculated according to the number of wind turbines, and in the case of wind farms with a larger number of turbines, considering the total installed capacity (Table 5):

The Galicia wind tax 44 considers a scale depending on the number of wind turbines, with wind farms with four or more turbines being taxed (Table 6):

In Spain, the three existing wind taxes are different in their content, but not in their purpose. The Castilla León wind tax is an annual tax, which establishes that the objective of this tax is “the generation of visual and environmental effects and impacts caused by wind farms and fixed elements of high-voltage electricity supply located in the territory of the Community of Castilla León”. The Castilla-La Mancha wind tax was created with the aim of “…preserving cohesion, territorial balance and the natural environment, as a physical environment that supports the economic activity linked to the industrial use of wind, in its consideration as a protected legal asset, and in order to contribute to the development of a sustainable energy and economic model…”. Law 8/2009, of 22 December, regulates the use of wind energy in Galicia and creates the wind energy tax and the Environmental Compensation Fund. 44 The explanatory memorandum of this law states that the generation of renewable energy is not totally innocuous and the installation of wind turbines involves “easements, unavoidable burdens for the environment, the natural environment, the landscape and the habitat in which they are located, which in part becomes transformed not only as a result of the visual impact produced by the existence of wind turbines but also of other elements such as access roads and evacuation lines”.

One of the main differences is the established tax rate, since the regions of Galicia and Castilla-La Mancha use the criterion of the number of wind turbines (in Galicia it would affect wind farms with 4 or more wind turbines, and in Castilla-La Mancha it would affect wind farms with 3 or more wind turbines). This reality seems to collide with the functionality of the “polluter pays” principle, and contributes to reflect on whether the wind tax is a tax in which the energy factor or the environmental factor has a greater impact, as indicated in the introduction to this article. It should be recalled that it defines three types of environmental taxes depending on the objectives pursued, and that their existence internalises externalities in the price of the goods, services and activities that produce them; the application of the “polluter pays” principle.22,36 In this sense, by excluding from taxation wind farms with a smaller number of turbines, in the regions of Galicia and Castilla-La Mancha there is not a full application of the above-mentioned principle. On the other hand, the three wind taxes are environmental energy taxes, as established some authors 22 and in the three regions they stand out for not defining the externality appropriately, not incorporating the spatial scope of the environmental damage taxed, and causing an inadequate jurisdictional allocation with great uncoordination between the different regions; without achieving a clear modifi-cation of environmental behaviour. From an environmental perspective, the impact of the double dividend theory for the wind tax should be considered, even if it is difficult to determine the first dividend for the environmental improvement obtained, and the second dividend should be reinforced by all the additional welfare changes generated by the use of the environmental revenue (through the environmental compensation fund).

Analysis of the structure of wind farms

In the three regions analysed, and fundamentally for Galicia and Castilla-La Mancha, wind farms with a greater number of wind turbines and lower power (less than 900 kW) predominate, with a lower productive capacity and less visual impact compared to wind turbines with a power of more than 1200 kW. In Castilla León, the importance of wind turbines with a high production capacity, with a rated power equal to or greater than 2000 kW (Table 7), stands out, with a visual environmental impact equal to or greater than that of less powerful and older wind turbines.

Main parameters of wind farms installed in Castilla León, Castilla-La Mancha and Galicia.

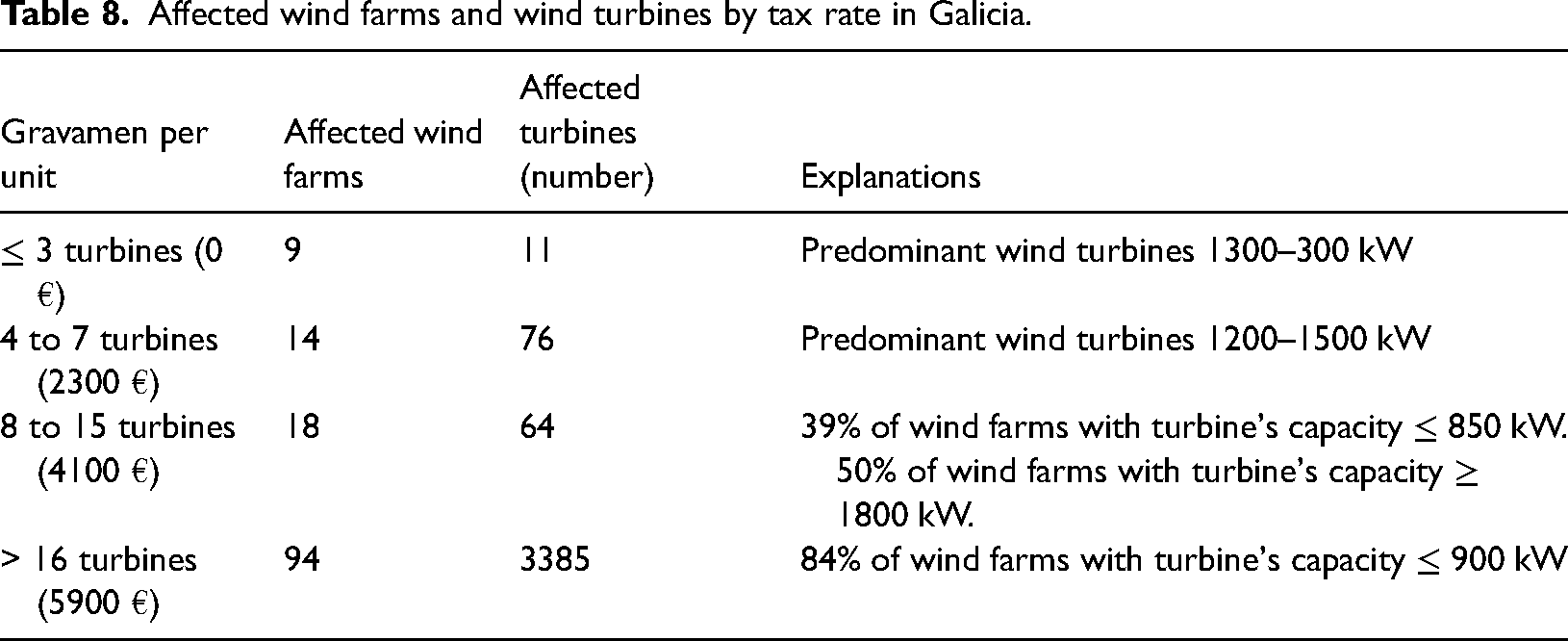

Due to the rapid development of wind energy in Galicia, especially up to 2007, the number of wind turbines installed was generally small (≤650 kW), but in significant numbers (Table 8). Thus, it can be deduced that 2168 wind turbines between 300 and 750 kW were installed, 61.7% of the total, and they were located in 46% of the wind farms, and in 60% of the affected municipalities. Only 25.2% of the wind farms operate large wind turbines (1500 kW or more), representing a lower number of installed wind turbines, with a total of 439 wind turbines (12.5%). However, these wind turbines have considerable dimensions, both in terms of diameter and shaft height, which contributes to their overall environmental impact, almost doubling the dimensions of a smaller and less productive wind turbine. Considering the period of analysis, it can be seen that 50.2% of the installed wind turbines have an average life of 22 years, corresponding to the oldest and least productive wind turbines.

Affected wind farms and wind turbines by tax rate in Galicia.

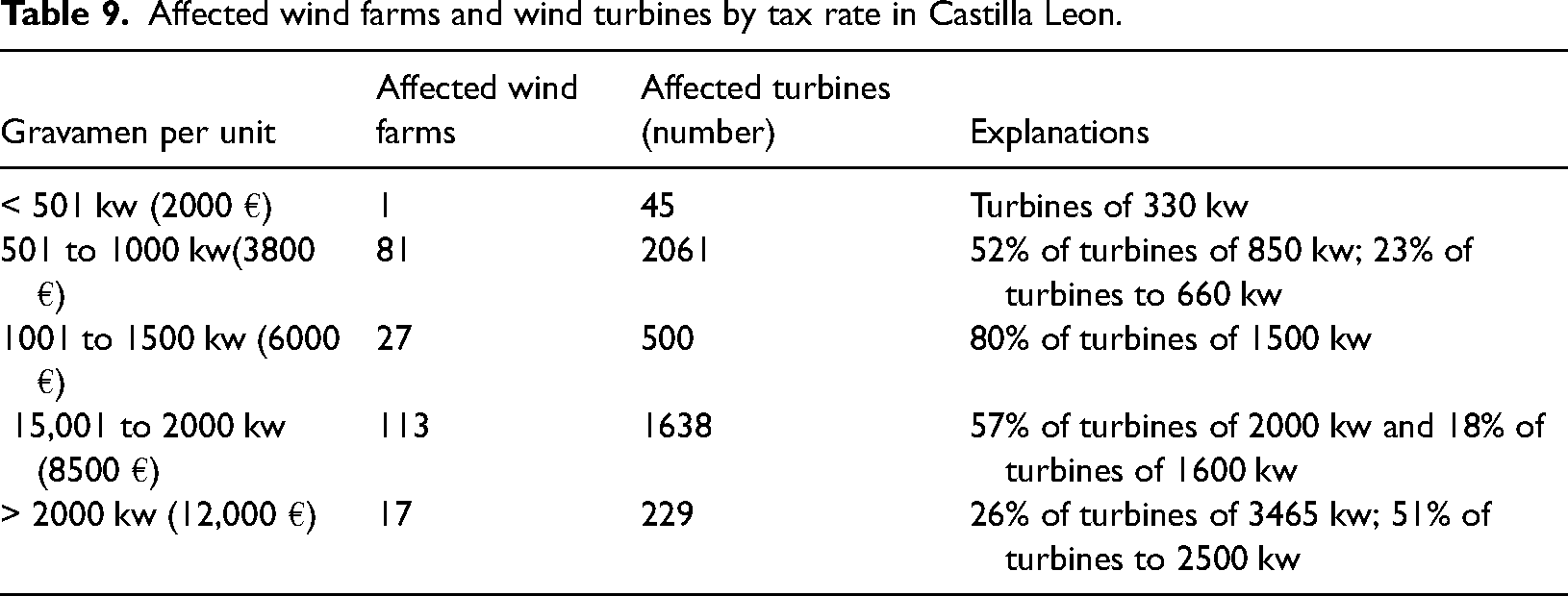

In the region of Castilla León, wind power expansion has been constant throughout the period. The presence of wind farms with wind turbines of higher production capacity and larger dimensions is noteworthy, although in general terms they are installations with fewer turbines (Table 9).

Affected wind farms and wind turbines by tax rate in Castilla Leon.

A similar situation can be seen in the region of Castilla-La Mancha, where wind farms with a higher number of wind turbines have a lower unit power, and therefore older and less productive turbines (Table 10).

Affected wind farms and wind turbines by taxation rate in Castilla-La Mancha.

Based on the above, it is also necessary to highlight how the power of the wind turbines affects the wind farms. Thus, Galicia stands out because 38% of the turbines are up to 660 kW, being present in 84% of the wind farms, and being the wind farms with the highest number of wind turbines. With the existing quota, it would be the oldest wind farms, with older, less productive and smaller turbines, which would be paying higher taxation. A similar situation can be seen in Castilla-La Mancha, a region where 33% of wind turbines are up to 660 kW and another 33% up to 850 kW. However, in the region of Castilla Leon, 26% of wind turbines have a unit power of up to 850 kW and 26% above 2000 kW. The new generation wind turbines are larger, more productive and have a greater visual and/or acoustic impact. It cannot be categorically stated that the most powerful and newest wind turbines are less noisy, and in many cases it is necessary to carry out checks through specific programmes (WindPRo). In this sense, the tax reform34,40 is relevant, in which the renewable energy sector is incorporated with all the variables of affectation highlighted and related to environmental impact, complemented with other regulations if necessary 1 .

Suitability scenarios on environmental impact

Considering the above, in order to assess the taxation capacity of the impact of wind farms by the three levies studied in this article, three scenarios are proposed consisting of a comparison of the application of the same levy to the three territories. Scenario 1 would apply the three levies to a selection of typical wind farms in Castilla-La Mancha (Table 11), scenario 2 would apply them to a selection of wind farms in Castilla León (Table 12) and scenario 3 would apply them to wind farms in the region of Galicia (Table 13). As there are differences in the definition of the three charges, it is possible to make a comparison that allows an approximation to an ideal model of wind power charges in terms of penalising environmental impact.

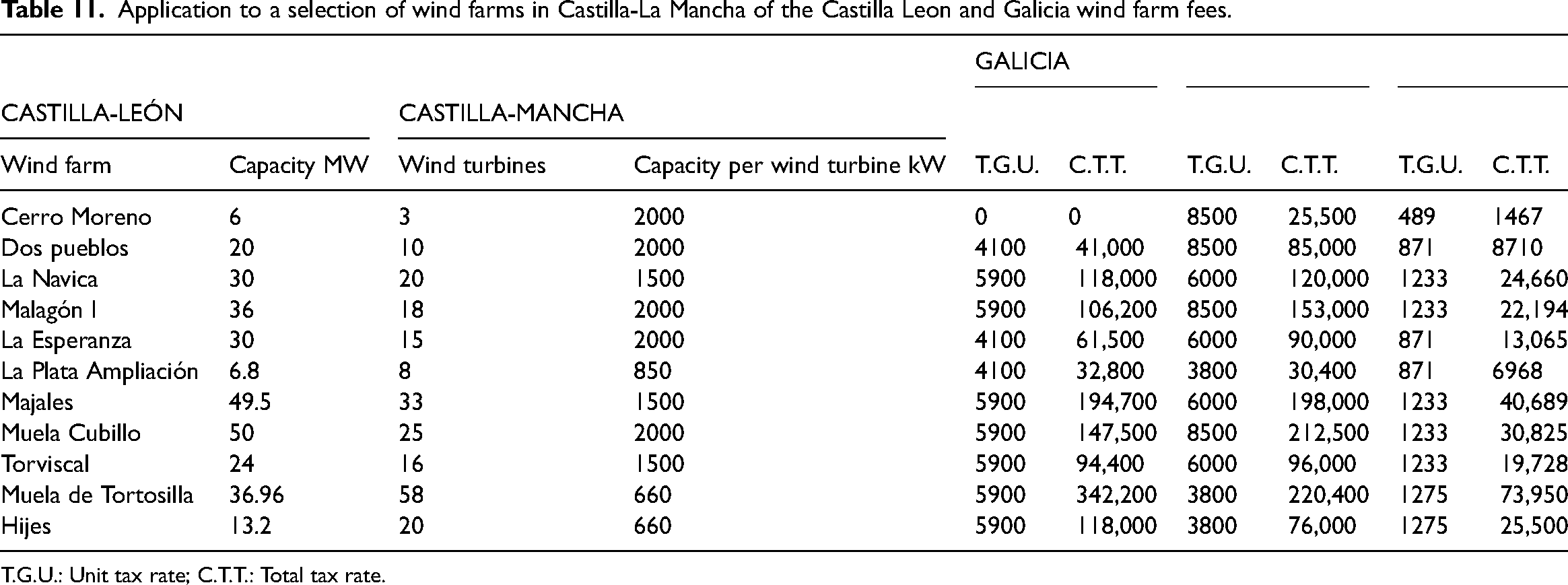

Application to a selection of wind farms in Castilla-La Mancha of the Castilla Leon and Galicia wind farm fees.

T.G.U.: Unit tax rate; C.T.T.: Total tax rate.

Application to a selection of wind farms in Castilla León of the Castilla-La Mancha and Galicia wind charges.

T.G.U.: Unit tax rate; C.T.T.: Total tax rate.

Application to a selection of wind farms in Castilla León of the Castilla-La Mancha and Castilla León wind charges.

T.G.U.: Unit tax rate; C.T.T.: Total tax rate.

The suitability scenarios reveal problems that have already been detected throughout the analysis. Scenario 1 (Table 11) would imply for the region of Castilla-La Mancha a significant increase in tax rates, as Galicia's wind tax has higher tax rates and Castilla León's wind tax would be applied to all wind farms, regardless of the number of total turbines. Scenario 2 (Table 12) would imply for the region of Castilla León a decrease in the tax rate when applying the Castilla-La Mancha levy, but an increase with the Galician model, which would be levied on wind farms with a higher number of turbines and lower power. Finally, Schedule 3 (Table 13) would imply for Galicia a decrease in the tax rate for wind farms with older and more wind turbines, but an increase for wind farms with more powerful turbines. In application of the “polluter pays” principle, it would be appropriate to consider a wind tax model that takes into account all wind farms, regardless of the number of wind turbines installed and also according to their unit power, together with wider safety distances.

Conclusions

The three regional regulations analyzed present notable differences, especially in the characteristics of the applicable fees (unit power, minimum number of turbines to be taxed, and number of turbines per tax bracket).

The collection capacity is also very disparate, and for example for the year 2019, the wind power fee in Castilla León was at least three times the revenue of the other two regions.

The characteristics of the wind farms analyzed are also not coincident among the three regions, highlighting:

in Galicia: the existence of wind farms with a unit power of less than 850 kW but with a high number of turbines, which bear a higher tax. The most current wind farms are made up of a smaller number of turbines of higher power, so they are either not taxed or are taxed less. The 84% of the wind farms subject to taxation have turbines of less than 900 kW; in Castilla León: wind farms are made up of turbines of more than 1500 to 2000 kW and there are also wind farms of less than 1000 kW; in Castilla-La Mancha: a mixed system is applied that combines number of turbines and power, highlighting wind farms with more than 1500 kW of unitary power and from 600 to 850 kW.

From the perspective of the policy makers, based on the scenarios foreseen for the “polluter pays”, it would be appropriate to consider a wind tax model that takes into account all wind farms, regardless of the number of wind turbines installed and also according to their unit power, together with wider safety distances. The establishment of the wind energy tax involves penalising the environmental impact of carrying out an environmentally friendly but not harmless energy activity. This requires less productivist action on the part of governments, which should apply comprehensive regulations to penalize and prevent impacts, on fossil energies and also clean energies. Special attention is needed to define “correct taxes”, to avoid or reduce undesired impacts over investments, competitiveness, citizens, regions, etc.

The need to penalise the process of implementing this renewable energy contrasts with the non-existence of such tax figures in the installation of other energy infrastructures and other larger infrastructures (motorways, airports, ports, dry ports), in which the environmental impacts and damage are nontorious and sometimes even harmful to the economic development of the municipalities in which they are located

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.