Abstract

This article is the first to study a nexus between financialization and circularity performance in the European region. To reflect the circularity performance, we use six different measures, including the amount of municipal waste, the number of circularity patents, the amount of circular material used, the rate of recycling waste, the rate of recycling biowaste, and the rate of recycling e-waste. By using various econometric techniques (namely a panel-corrected standard errors [PCSE] model, a feasible generalized least square estimates [FGLS] model, and the two-step General Method of Moment [the two-step GMM), our study indicates that financialization is an enabler for circularity. However, these results are only statistically significant for the financial institution's development, while the financial market has a positive yet insignificant impact on circularity performance. The development of the financial institution is reported to increase municipal waste and the amount of recycling biowaste and e-waste, thus promoting the path toward the circular economy. To shed light on the financialization-circularity nexus, we use the different dimensions of financialization dynamics and report heterogeneous influences on the different issues of circularity performance. Furthermore, the results from the dynamic fixed effects (DFE) in the autoregressive distributed lag (ARDL) method suggest that the impact of financial development only becomes apparent in the long term.

Introduction

The circular economy (CE) is promoted by many firms worldwide, including those based in the European Union (EU). Approximately 600 billion euros in financial gains could be achieved within the EU's manufacturing sector each year due to CE-type economic transformations. 1 Finland could gain 2.5 billion euros annually through circular economies; as a result, the world economy would benefit by one trillion dollars annually, as stated by McKinsey. 1 Sustainable environmental and economic growth is recommended in conjunction with circular economies. 2

A key component of modern economies’ sustainability is reducing energy consumption and pollution emissions.3–5 This can be achieved through the development of the financial system. It has been well documented for decades that the development of finance has contributed greatly to creating investment opportunities in developing countries 6 and developed countries. 7 Moreover, developed economies have improved their economic performance due to the increase in financial development. These countries have, however, raised environmental concerns about environmental issues as a result of the demand for steadily increasing energy. Thus, this study aimed to provide updated information that may assist in promoting a sustainable environment by examining how financial development affects the energy system and ecological quality, then the path toward the circular economy. Our study focuses on the case of European countries.

Research has demonstrated that financial development can have a variety of effects on the energy system and ecological quality. The interrelationship between environmental quality and financial development has been the subject of numerous empirical studies in recent years. The majority of them correlate to their specific case, nevertheless. By examining Tunisian annual time-series data, Kwakwa 8 examined the linkages between the trinity of financial development, urbanization, and energy use, for instance. Specifically, Shahbaz et al. 9 studied the impact of trade, financial development, and GDP on emissions of carbon dioxide in Indonesia. A study conducted by Islam et al. 10 examines how financial development affects the consumption of energy in Malaysia. Another study conducted in South Africa by Shahbaz et al. 9 investigated the long-run nexus of economic growth, trade openness, financial development, and coal consumption. Komal and Abbas 11 explored the linkages among financial development, energy, and economic growth by employing Pakistan data, while Tang and Tan 12 investigated the nexus of financial development, foreign direct investment, and consumer price index utilizing data from Malaysia. The study by Zhao and Yang 13 examined the association between CO2 emissions, financial development, energy use, and growth in Chinese provinces using the panel DOLS and FMOLS. There is a great deal of variation in the conclusions about the interrelationship between these two crucial aspects. It has been suggested by Karanfil 14 that previous studies’ mixed results are caused by endogeneity, primarily caused by variable omission. Briefly, this study's novelty can be summarized in the following way. As a starting point, prior studies have concentrated on one aspect of financialization, specifically the stock market total value traded in terms of GDP or stock market capitalization in terms of GDP. Notable, rather than the impacts of financialization on ecological improvements, its importance in helping countries pursue the goal of being a circular economy, which would be set as their priority, has been kept silent thus far. Due to a lack of relevant information, no article explores the link between financialization and circularity.

The first process through which the development of finance affects the environment is energy consumption. 7 In addition to encouraging investments in environmentally sustainable technologies, financial development also reduces carbon emissions. Energy conservation and sustainability can be promoted in homes, for example, by using energy-saving appliances.14,15 It is also possible that investments can increase energy consumption as a result of financial development, thereby negatively affecting the environment. Second, a potential mediator of growth of the financial sector and emissions from carbon dioxide is the increase in trade flows. 16 For example, commerce can promote eco-friendly technology investments, which help promote the sustainability of the environment. In addition, foreign direct investment (FDI) can have an impact on the environment. Through green technologies, FDI can open the door for the interchange of information and knowledge necessary to enhance the quality of the environment. 17 Lastly, financial development can impact carbon emissions by increasing economic activity. As a result of manufacturing activity spikes, emissions from waste disposal increase as productivity increases as well as the original technology used.

According to Kristensen and Mosgaard, 18 there is no single, widely accepted methodology to measure the circular economy. There have been some attempts over the years. However, an analysis of the literature indicates that most of the considered indicators focus on a single aspect, usually inputs and outputs, or only consider a few aspects of circularity. 19 According to Kristensen and Mosgaard, 18 recycling, end-of-life management, and regeneration are trend topics for circularity indicators, while few studies have addressed dismantling, extending the useful life, maximizing resources, or recycling for reuse. Scheepens et al. 20 developed an LCA-based metric to measure circularity in products, but the methodology focuses on reducing externalities rather than measuring circularity. In Genovese et al., 21 a lifecycle perspective was used to compare supply chain performance in the chemical and food sectors in order to integrate the circular economy within sustainable principles. Maio and Rem 22 developed the Circular Economy Index (CEI), which takes into account environmental and economic factors. The CEI focuses on the recycling process, excluding the recovery of materials. A CE performance indicator for industrial products was developed by Cayzer et al. 23 A performance indicator based on longevity has been developed by Franklin-Johnson et al., 24 that is, the length of time that a resource is kept in use. Di Maio et al. 25 demonstrated the difference between the resource efficiency of a process and of a product within supply chains from a lifecycle perspective.

There are several ways in which the findings of our study fill the gaps in the literature. The study is the first empirical examination of the impact of countries' financial development performance and their circularity. Therefore, this study contributes to the existing knowledge regarding the environmental influences of financialization by providing a comprehensive analysis of the link between financialization and circularity. Following Nham and Ha, 26 we use a variety of measures in this article to evaluate the performance of circularity. These measures include the amount of municipal waste, the number of circularity patents, the amount of circular material used, the rate of recycling waste, the rate of recycling biowaste, and the rate of recycling e-waste. Analyses of the sample of countries in Europe during the 2011–2019 period are conducted using a variety of techniques and empirical strategies. We select this database since the comprehensive measures of circularity are only available in this region. Other measures are quite old and do not reflect a completely diverse dimension of the circularity performance. After conducting various tests for cross-sectional dependence and stationarity of the studied series, we examine the relationship between financialization and circularity using a panel-corrected standard errors (PCSE) model in the following section. The feasible generalized least square estimates (FGLS) model is employed to further verify our findings by taking into account heteroscedasticity. An application of the two-step General Method of Moment (the two-step GMM) is considered to resolve an endogeneity issue. In addition, the dynamic fixed effects (DFE) estimator is applied to the autoregressive distributed lag (ARDL) method to measure both the short- and long-run effects. As indicated by Ha 27 and Ha and Thanh, 28 the DFE-ARDL method can be used to address both time-fixed effects and country-fixed effects.

In the remainder of the article, the organization is as follows. In the second section, we present a literature review and develop hypotheses, followed by the third section, which introduces the model, data, and estimation method. In the fourth section, the empirical study's results are presented. In the fifth section, we conclude the article by providing conclusions and policy implications.

A review of the literature

Theoretical framework

Grossman and Krueger 29 proposed the Environmental Kuznets Curve to explain the link between financial development and the environment. According to the original theory, economic growth initially leads to environmental degradation. Environment quality improves when per capita income reaches a certain level. 7 Critics argue that the EKC hypothesis ignores the potential role that financial development could contribute to improving the environment, although a substantial amount of empirical study has been conducted on it. 7 It was suggested by Tamazian et al. 30 that an economic market that is stable could be used to finance green energy, which could be environmentally beneficial. Some stock market studies have also suggested that it will help protect the environment by lowering manufacturing costs, expanding financial networks, facilitating the investment of capital for environmentally sustainable infrastructure, and maintaining viability over the long term. According to some studies, the growth of the financial sector can attract foreign direct investment (FDI) and innovation in environmental research. 7 According to a study by Zhang, 31 the development of finances can assist in investments in energy preservation and technologies that contribute to environmental sustainability. 6 However, some researchers have argued that growth in the financial sector may contribute to an increase in carbon discharge.31,32 Because an efficient financial system may enhance investment and increase energy consumption but may also harm the environment, as argued by Sadorsky. 33

Empirical evidence

Financial development and ecological quality

Discussions about climate change have focused on the effects of global warming on humans in recent years. Global environmental change is believed to be caused primarily by greenhouse gases (GHGs) originating from anthropogenic activities. In terms of GHG emissions, CO2 emissions account for 75% and are considered to be the main culprit. Most empirical studies attribute the principal cause of environmental degradation to GHG emissions, especially CO2. Recent studies by Vo et al. 34 confirm that energy consumption leads to pollution unilaterally. The long-term impact of the energies of fossil fuels and renewable energies on CO2 emissions was remarkable in these studies. The bi-directional relationship between these two variables has also been confirmed by Adewuyi and Awodumi. 35 As a proxy for air pollution, carbon dioxide emissions are generally considered the most appropriate. Because a better understanding of global warming is necessary and important, the interrelationships between financial growth, economic expansion, and the emissions of CO2 have recently attracted the attention of many researchers.

There have been mixed and uneven outcomes in research on the connection between carbon emissions and financial development. Vo and Zaman, 36 for instance, examined how energy demand relates to carbon emissions across 101 nations in the context of financial development between 1995 and 2018. Using the generalized technique of moments (GMM), the authors report that all countries studied experienced decreased carbon emissions as a consequence of financial development. For the Asian Pacific Economic Cooperation nations during the period 1970 and 2016, Zaidi et al. 37 used a constantly updated bias-corrected approach and Westerlund cointegration techniques to explore the dynamic of carbon emissions and financial development. According to this research, financial development dramatically lowered carbon emissions. For the BRIC countries of Brazil, Russia, Indonesia, and China (from 1992 to 2004), Tamazian et al. 30 examined the connections between environmental degradation and financialization. The authors found that financial development slowed environmental deterioration. Boutabba 38 demonstrated that financial development in India contributes to the degradation of the environment. In Pakistan, Shahbaz et al. 39 examined the asymmetries of financialization's effects on the quality environment and found that it impairs the environment in a negative way. From 1960 to 2007, Ozturk and Acaravci 40 investigated the correlation between carbon emissions, trade, and financialization in Turkey and concluded that under long-term circumstances, financialization did not significantly influence carbon emissions. Mahdi Ziaei 41 used a vector autoregressive model to research the relationship between energy use, carbon emissions, and financialization within 12 East Asian, Oceania nations, and 13 Europe from 1989 to 2011 and found that the stock market had an impact on both the environment and energy utilization. A significant factor in decreasing carbon emissions in Africa is financial access, according to Adams and Klobodu, 42 who investigated the causes of the degraded environment with a tendency from the financialization perspective. According to Rjoub et al., 43 financialization plays a moderating role in the determinants of carbon emissions, using canonical cointegrating regression, Hanck and Bayer cointegration, and can contribute to a sustainable environment in Turkey. Usman et al. 44 evaluated financial inclusion's impact on ecological footprints in 15 of the largest emitted nations and concluded that both financialization and energy renewal are responsible for greatly deteriorating the environment. Using apparently unrelated regression and GMM, Khan et al. 45 analyzed the link between energy use and financialization on carbon emissions for 128 nations from 1990 to 2017. They proved that financialization had a favorable influence on carbon emissions. A study by Lv and Li 46 examined the spatially impacted carbon emissions of financialization in 97 nations over the four years between 2000 and 2014 and found that financialization adversely influenced carbon emissions. In a study of the linkages between environmental quality and financialization in South Asian economies between 1990 and 2014, Tahir et al. 47 pointed out that carbon emissions were a result of financialization.

Even though the link between CO2 emissions and financial development has been thoroughly researched, the conclusions are inconclusive and vary dramatically across studies. 14 Thus, our analysis encompasses two interpretations of the research question. The following section provides a brief overview of two different lines of research on environmental degradation and financial development. These research strands are examined in the following sections. CO2 emissions are inhibited by financial development, according to the 1st group of discussions. The development of the finance strand suggests that green FDI technologies are largely attracted via financial development. Farhani and Solarin 48 and Kahouli 49 illustrate the effect of these advanced technologies on improving energy efficiency. According to Mielnik and Goldemberg, 50 FDI results in greater R&D engagements and slows global warming. According to Wang and Jin, 51 FDI's decontamination effects are highly dependent on domestic companies’ willingness to comply with pollution controls. Based on these studies, it is likely that environmental quality will continue to improve in the future. Aside from that, they also emphasize the need to rein in environmental pollution through the efficiency of financial markets.

Tamazian et al. 30 analyze Brazilian, Russian, Indian, and Chinese (BRIC) financial development, ecological degradation, and economic growth by applying various panel methodologies. As a result of financialization and economic growth, pollution of air has been reduced. Chinese provincial data provide evidence that the development of finance is positively correlated with CO2 emissions. 13 In addition to promoting environmental technologies and improving firms’ financial accessibility, financial development also serves as a catalyst for green innovations. In Indonesia, Malaysia, and South Africa, Shahbaz et al. 9 demonstrate that domestic credit to the private area reduces pollution both in the long term and short term. Based on a sample of 53 countries from 1999 to 2008, Chang 52 uses panel threshold regression to assure the technical impact of financial development. According to Bekhet et al., 53 economic growth is correlated with carbon dioxide emissions and financial development for the Gulf Cooperation Council (GCC). By utilizing the impulse response-VAR and ARDL, the results show that financialization has a positive influence on emissions of carbon dioxide in Kuwait, Oman, and Qatar. To analyze the connection between tourism, the development of finance, and emissions of CO2, Vo et al. 6 found that financial development stimulates tourism and reduces the emissions of CO2. Nonlinearity and the absence of significant control variables explain the inconclusive relationship between financialization and ecological degradation.

According to Karanfil, 14 previous studies have produced mixed results due to the omission of crucial variables. As trade liberalization and the integration of financial markets increased in the latter period, Abbasi and Riaz 54 revealed that pollution effects were reduced. The results of the Pakistan dataset suggest that the EKC relationship between ecological degradation and the economy's growth depends on financial development. In their study, Zaidi et al. 55 highlight two issues that are often resolved in an improper manner in previous studies, which can lead to ambiguous outcomes. First, important variables are omitted. There is a possibility that important factors are overlooked. Second, in the panel data, there are also unobserved shocks and heterogeneous slopes, as well as cross-sectional dependence. Estimates may be biased if those problems are not captured or are dealt with improperly. The relationship between the development of finance in Saudi Arabia and environmental degradation is inverted U-shaped, according to Mahalik et al. 56 Environmental pollution and financial development can be correlated quadratically using ARDL bound testing and Bayer–Hanck's cointegration test According to Adom et al., 57 financial development can negatively or positively affect environmental quality depending on the technical and scale effects. According to Baloch et al., 58 in OECD countries, there is a nonlinear association between financialization, ecological degradation, and economic growth. A shift toward environmentally friendly energy technologies has remarkable effects on pollution reduction.

According to Park et al., 59 two effects can be decomposed into the directional effects of financialization on ecological degradation. First, in emerging markets, the scale effects of rapid development of finance or growth are often dominant. Second, as a result of the suppression of scale effects and the reduction of pollution, the inhibiting effects only become noticeable after a certain level of financial growth has been reached. Furthermore, other studies have been conducted on relevant topics. A study by Bekun et al. 60 examines the association between the consumption of energy and the growth of the economy in South Africa from 1960 to 2016 by taking into account the external effects of capital, labor, and CO2 emissions. According to empirical evidence, energy consumption drives economic growth in an inverted U-shape. Approximately 15.2 percent of CO2 emissions would increase when gross product consumption increases by one percent. A second study by Bekun et al. 60 analyzed CO2 emissions, resource rents, and nonrenewable and renewable energy from 1996 to 2014 using the pooled mean group ARDL. Reliance on natural resource rent would be detrimental to the environment if adequate and timely management options are not provided. In addition, there is empirical evidence that supports the hypothesis that GDP growth is correlated with the use of renewable and nonrenewable energy in the EU.

The environmental degradation in BRICS countries is likely caused by coal rents, the low quality of regulations, and the economy growing faster, according to Adedoyin et al. 61 In order to move toward sustainability, the authorities need to adopt stringent energy-related regulations based on the pooled mean group—ARDL for panel data from 1980 to 2014. Etokakpan et al. 62 analyze the new Turkish policies in a separate study. An unprecedented wave of globalization has sped up the country's growth. Researchers found a long-term relationship between growth, globalization, the consumption of energy, and the emissions of CO2 based on Bayer and Hanck cointegration tests and autoregressive distributed lags. According to the findings, economic growth in Turkey is neither sustainable nor eco-friendly. Despite this, Turkey's energy use is efficient because it reduces both short-term and long-term environmental pollution. According to Emir and Bekun, 63 Romania's GDP has a positive relationship with energy intensity because of the feedback effect between energy intensity and GDP. For the period 1990–2014, autoregressive distributed lag and Granger causality tests are used. There is a bidirectional relationship between the growth of the economy and energy intensity, according to the empirical results. Furthermore, the findings suggest that Romania's economic growth is unsustainable.

Energy consumption and ecological quality nexus

Energy use has been studied by prior scholars with different outcomes in regard to its intermediary role in the relationship between finance-carbon emissions. Karanfil 14 demonstrated, for example, that financial development can contribute to promoting sustainability and declining energy use. In her study of short-run and long-run causality between financial development and energy use, Kahouli 49 concluded that energy consumption is a one-way Granger cause of financial development. Adekoya et al. 64 contended that the development of finance could lead to increasing investments in green technologies that provide sustainability for the environment. For the period 1953 to 2006, Jalil and Feridun 65 used an Autoregressive Distributed Lag Model to explore the influence of financialization on energy use and economic growth in China and showed that financialization contributed to decreasing environmental pollution. The study by Shen et al. 66 evaluated the link between carbon emissions and financialization through the use of green investments as a mediating factor, exploring a positive connection between financialization and economic growth. Using data spanning from 1980 to 2008, Al-mulali and Sab 67 researched the linkages between energy use and carbon dioxide emissions and concluded that financialization promotes energy-saving projects and contributes to reducing environmental threats. With a multivariate time series analysis, Islam et al. 10 evaluated the link between finance and energy use in Malaysia and found that consumption has both long- and short-term effects on financialization. The dynamic relations between environmental degradation, energy use, and financial development in the OECD nations from 1990 to 2017 were modeled by Baloch et al. 68 and concluded that financial development promotes energy innovation while improving the environment's quality. An OECD panel of 35 countries was examined by Ozcan et al. 69 to examine the dynamics of environmental degradation, economic growth, and energy consumption, between 2000 and 2014. The authors found that economic growth and energy consumption contributed significantly to the degradation of the environment in OECD nations.

A review of the studies concluded that three key issues were contributing to the lack of agreement. First, inappropriate proxies have been used for measuring financial development, which has resulted in differences in the outcome. Another problem is the failure to determine mechanisms by which the environmental impact of financial development can occur. The final causes are measurement error, reverse causality, and sampling bias since endogeneity control is lacking.

In this article, we then fill these gaps by providing a more comprehensive analysis of the link between financialization and circularity. Instead of considering a single dimension of financialization and circularity, we employ measures that cover different issues of financialization and circularity. Specifically, this article utilizes the measures of circularity performance, which has characteristics such as low pollution emissions, low energy consumption, waste elimination, and increased efficiency, while we consider the financial depth, financial access, and financial efficiency of the financial market and financial institutions. Our article is expected to provide theoretical reasoning and empirical support to examine the role of financialization on circularity more comprehensively. To confirm the findings, we also use various econometric techniques that deal with the potential issue of heterogeneity and endogeneity.

Empirical methodology

The model used to investigate the nexus of financialization (FIN) and circularity performance (CIR) can be presented as follows:

Measures of circularity performance (CIR)

As contended by Murray et al., 70 CIR has features such as low pollution emissions, low energy consumption, waste elimination, and increased efficiency. Based on the circular economy approach, there are two types of cycles: technical and biological ones. In the technical cycles, materials, products, and components remain on the market as long as possible by repairing, reusing, re-manufacturing, and recycling. In the biological cycles, nontoxic materials can be directly restored into the biosphere. It is important to note that restoration is a crucial component of such an approach, as it allows CIR to be both preventative and active in repairing past damage. 70 However, a review of the literature indicates that most of the indicators considered are based on metrics that are based on a single aspect. 71

Following Nham and Ha,25 this article uses various measures to capture diverse dimensions of circularity. Six distinct measures are used to reflect the level of circularity, which European countries obtain. These measures consist of the number of patents associated with recycling and secondary raw materials (CIR_PA); a generation of municipal waste per capita (kilograms per capita) or municipal waste (CIR_MW); the share of circular material use or circular material usage (CIR_MA) measured as (%); and the recycling share of all waste excluding major mineral waste or recycling waste performance (CIR_RW). Regarding recycling waste performance, we explicitly consider the recycling share of biowaste and e-waste (CIR_RB and CIR_RE, respectively) performance. Variables taken from European Statistics (Eurostat) are for the period starting from 2012 to 2019.

Measures of financial development

Financial development is a multidimensional process. We need to overcome the shortcomings of single indicators as proxies for financial development by using measures originally developed by Svirydzenka.

72

Financial development is defined as a combination of depth (the size and liquidity of markets), access (the ability of individuals and companies to access financial services), and efficiency (ability of institutions to provide financial services at low cost and with sustainable revenues, and the level of activity of capital markets). This broad multidimensional approach to defining financial development follows the matrix of financial system characteristics developed by Čihák et al.

73

Specifically,

Control variables

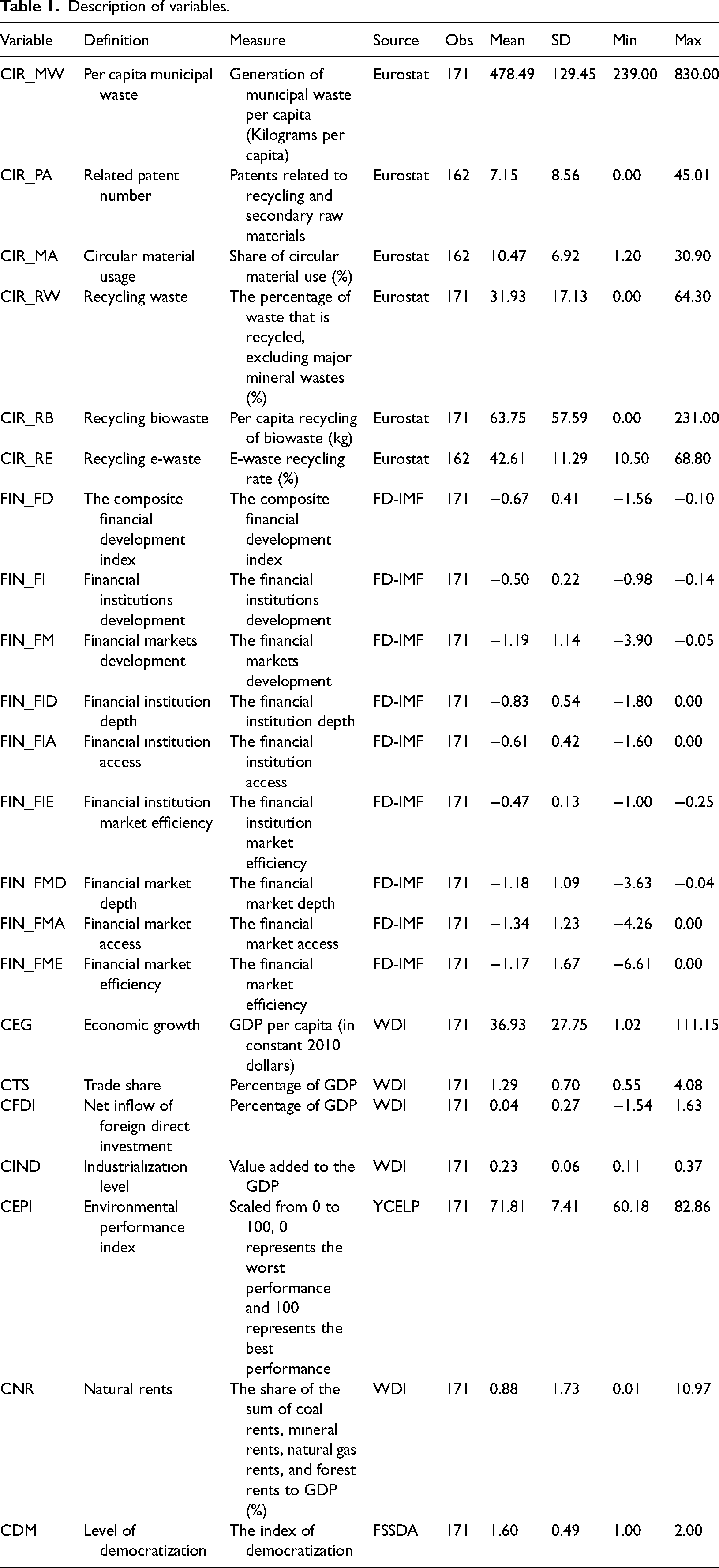

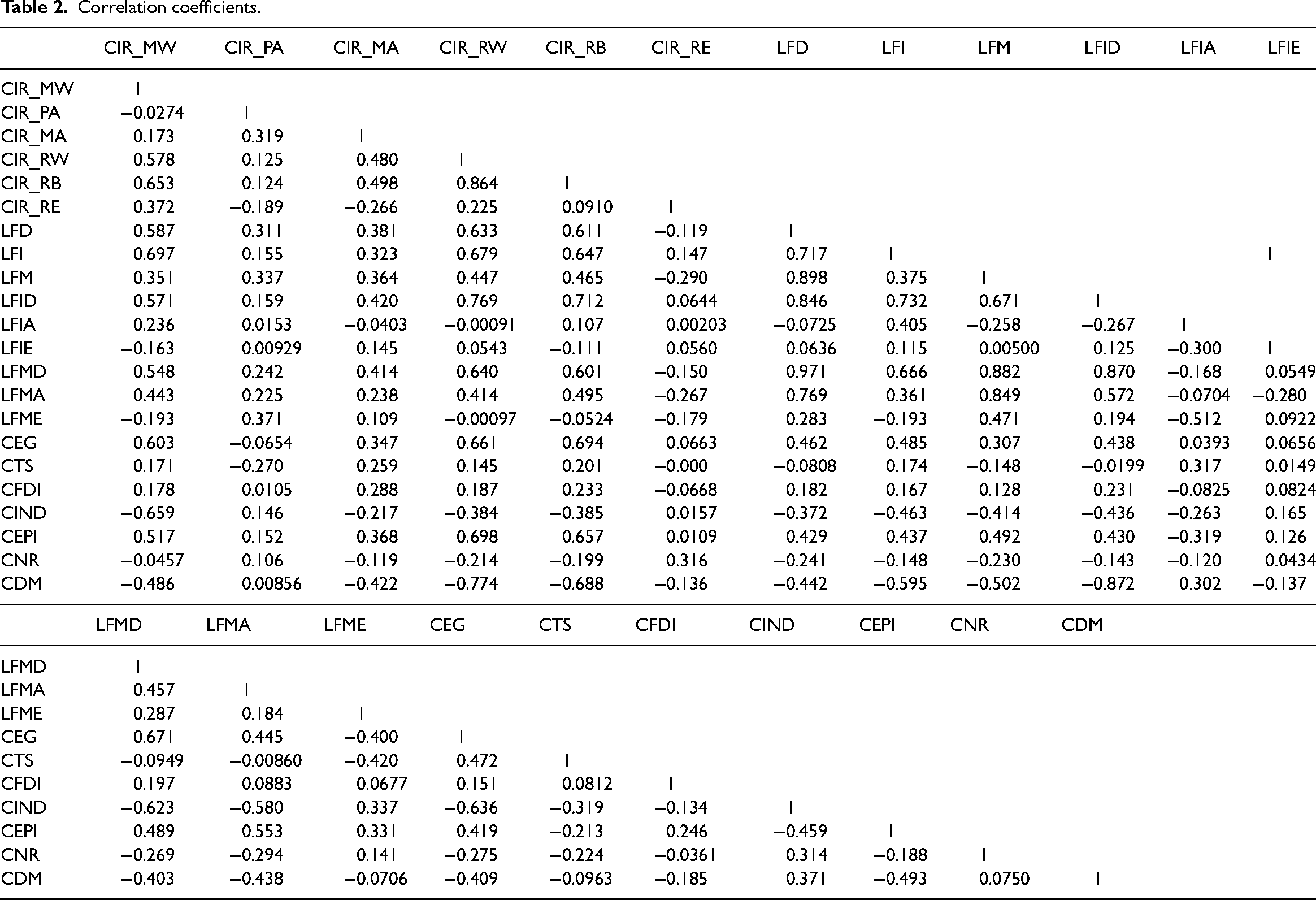

Literature-based empirical studies, especially Nham and Ha25 and Sun et al., 74 were used to determine the explanatory variables. We have taken the economic growth level (CEG), the share of trading activities (CTS), the level of industrialization (CIND), and the level of democratization (CDM) as explanatory variables. According to Nham and Ha,25 the importance of net foreign direct investment (CFDI) is also incorporated into the model. Natural rent (NR) and environmental performance index (CEPI) are included as explanatory variables. Table 1 summarizes the variable and statistical description of all considered variables. A correlation matrix is presented in Table 2, which indicates a positive correlation between financialization and circularity.

Description of variables.

Correlation coefficients.

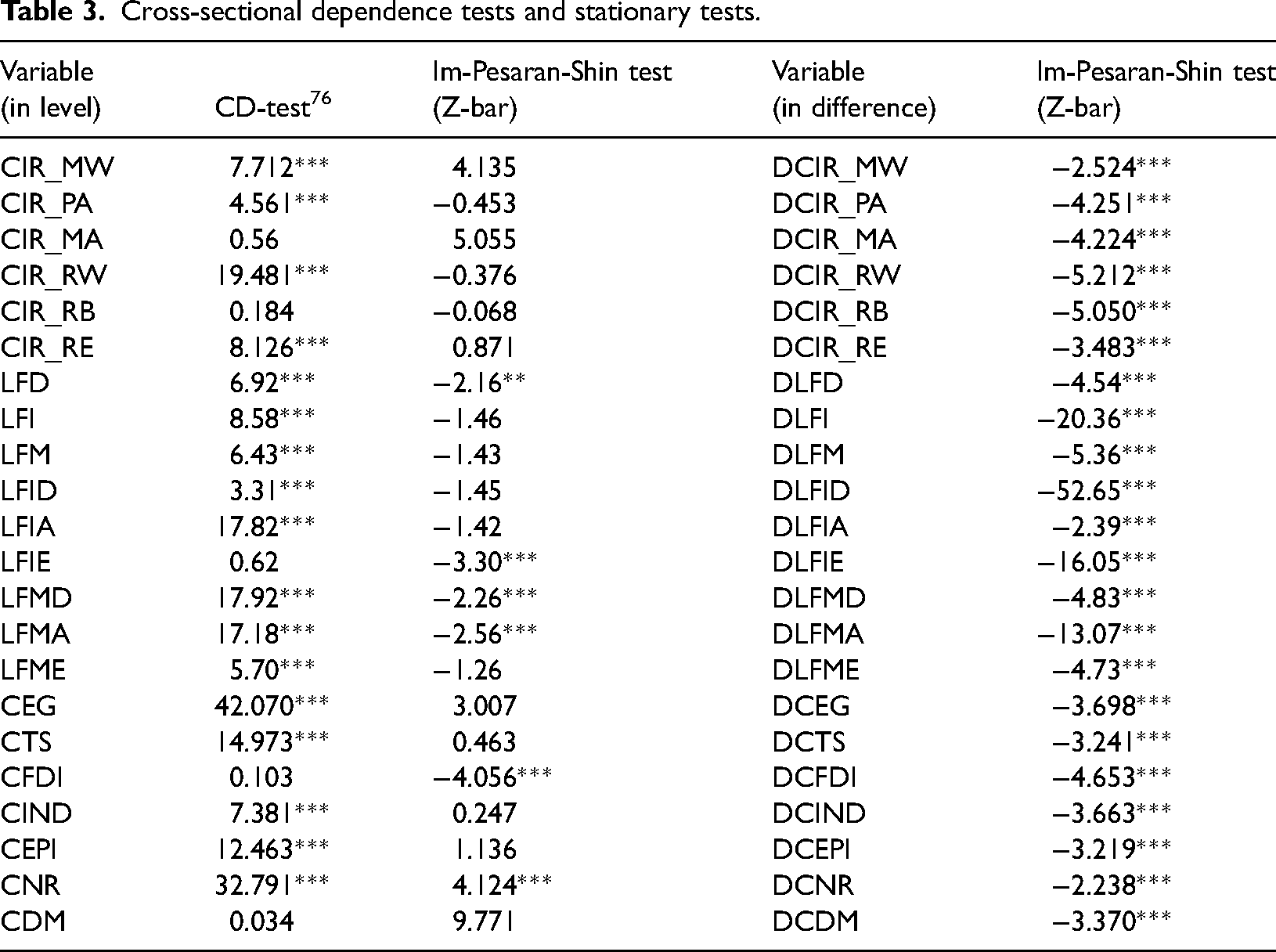

The following steps are followed in the conduct of a cross-sectional dependence (CD) test We validate the presence of CD in the data by using the cross-sectional dependence tests. Based on the properties of our used database, we apply the method developed by Pesaran. 75 The stationarity of our studied series is checked by using adequate methods. We select unit root tests developed by Im et al. 77 as recommended by Ha. 27 According to Table 3, some variables do not become stationary after the first level of difference, however, others become stationary at the second level of difference. To investigate the economic complexity-circularity nexus for the data with CD and stationarity of the first-difference variables, the panel-corrected standard error (PCSE) model is the most appropriate empirical approach.27,78–81

Cross-sectional dependence tests and stationary tests.

In addition, we replicated our estimates using different statistical models, including the Feasible Generalized Least Squares (FGLS) that address the issue of heterogeneity, 27 and the two-step system GMM, which are designed to deal with the potential issue of endogeneity in Equations 1 and 2.28–82 Notably, the effects of the project over the short and long term are also assessed. Accordingly, the autoregressive distributed lag (ARDL) method developed by Pesaran and Smith 83 is employed. Hence, we have used a dynamic fixed-effects estimation (DFE) to account for causal relationships between variables and heteroscedasticity across countries due to the potential presence of endogeneity. 84

Empirical results

Economic complexity and environmental innovation

Environmental innovation activities

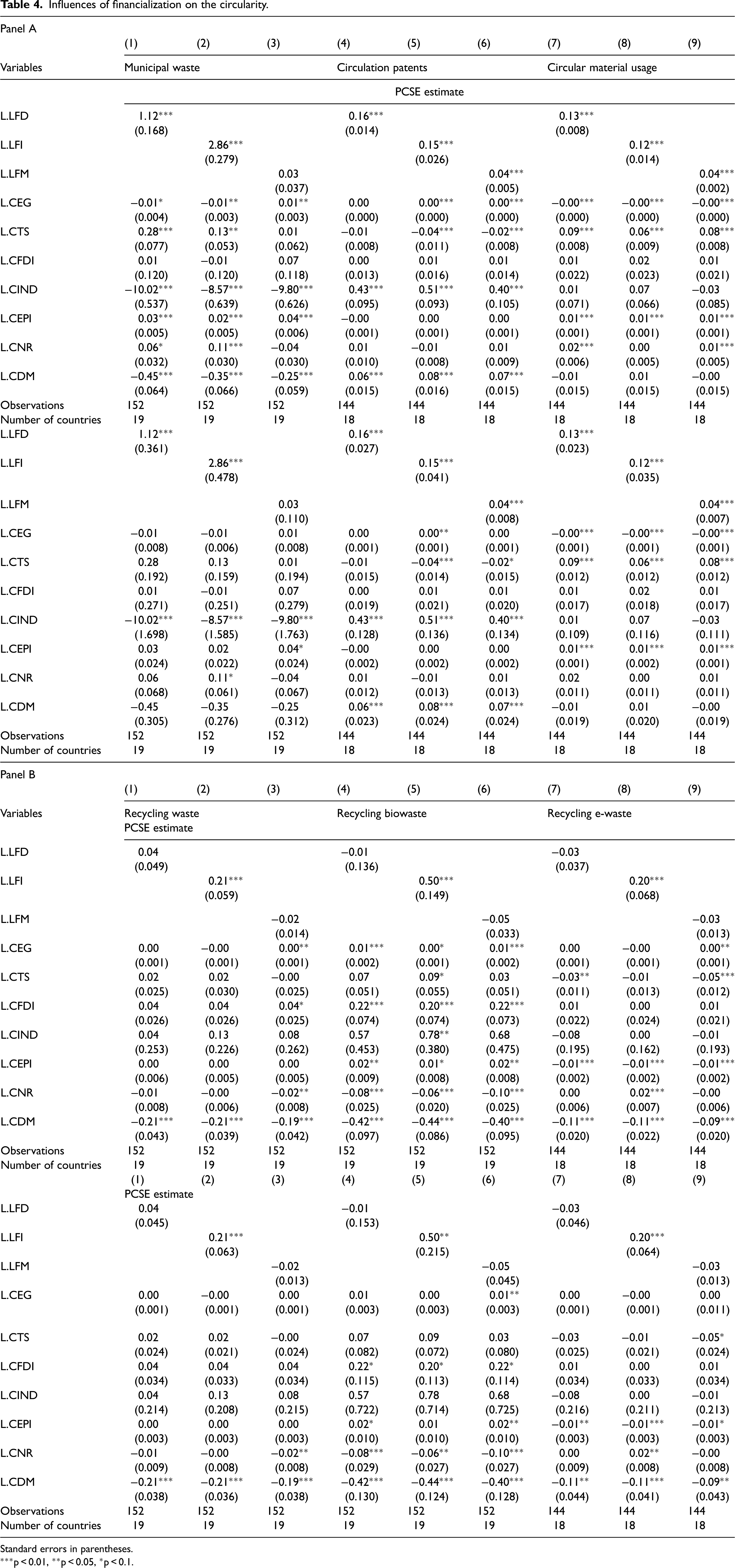

Regarding the PCSE and FGLS estimations, Table 4 indicates the impact of financialization on economic circularity in the total sample. For the PCSE estimation, financialization has a positive influence on the three aspects of economic circularity, including circulation patents and circular material usage, yet in terms of municipal waste, the action causes more problems. While these results are only statistically significant for almost all parts of financialization, the financial market (FM) has a positive yet insignificant impact on municipal waste. Therefore, along with a rise in financialization comes the increment of municipal waste, circulation patents, and circular material usage. The increment of municipal waste is predicted as financialization could result in the need for more resources to accumulate capital. Aligned with previous findings on the impact of financialization and environmental qualities,85,86 the financial institution's development is reported to increase municipal waste. While consumption leads to waste, the solution to deal with such issues is proposed and implemented. In exposure to the global capital, the changes in capital accumulation along with/ or with the restructuring of the political and economic preeminent of the financial market have led to various programs and interventions.87,88 The impact of the financialization process is also consistent with Langley 89 as evidence for the expansion of formerly implemented economy circulations is found to be enabled. Investment is seen as more than just lubricating the national economic machine but is also a critical environmental intervention that will permit the dynamic, entrepreneurial, and emergent forces of economic circularity.

Influences of financialization on the circularity.

Standard errors in parentheses.

***p < 0.01, **p < 0.05, *p < 0.1.

For the control variables, economic growth (CEG) has a statistically significant yet weak negative impact on municipal waste while having no impact on circulation patents or circular material usage. While the level of industrialization (CIND) and the level of democratization (CDM) posit a significantly negative impact on municipal wastes, while increasing the number of circulation patents, circulation material usage receives no significant influence. Results of trade share (TS), environment performance index (CEPI), and natural rent (CNR) reveal that although the three variables increase municipal waste, this trio also contributes to increasing circular material usage. Among all control variables, CFDI was recorded to have no impact on any economic circularity aspects. Findings from the FGLS estimation illustrate the same results in the PCSE.

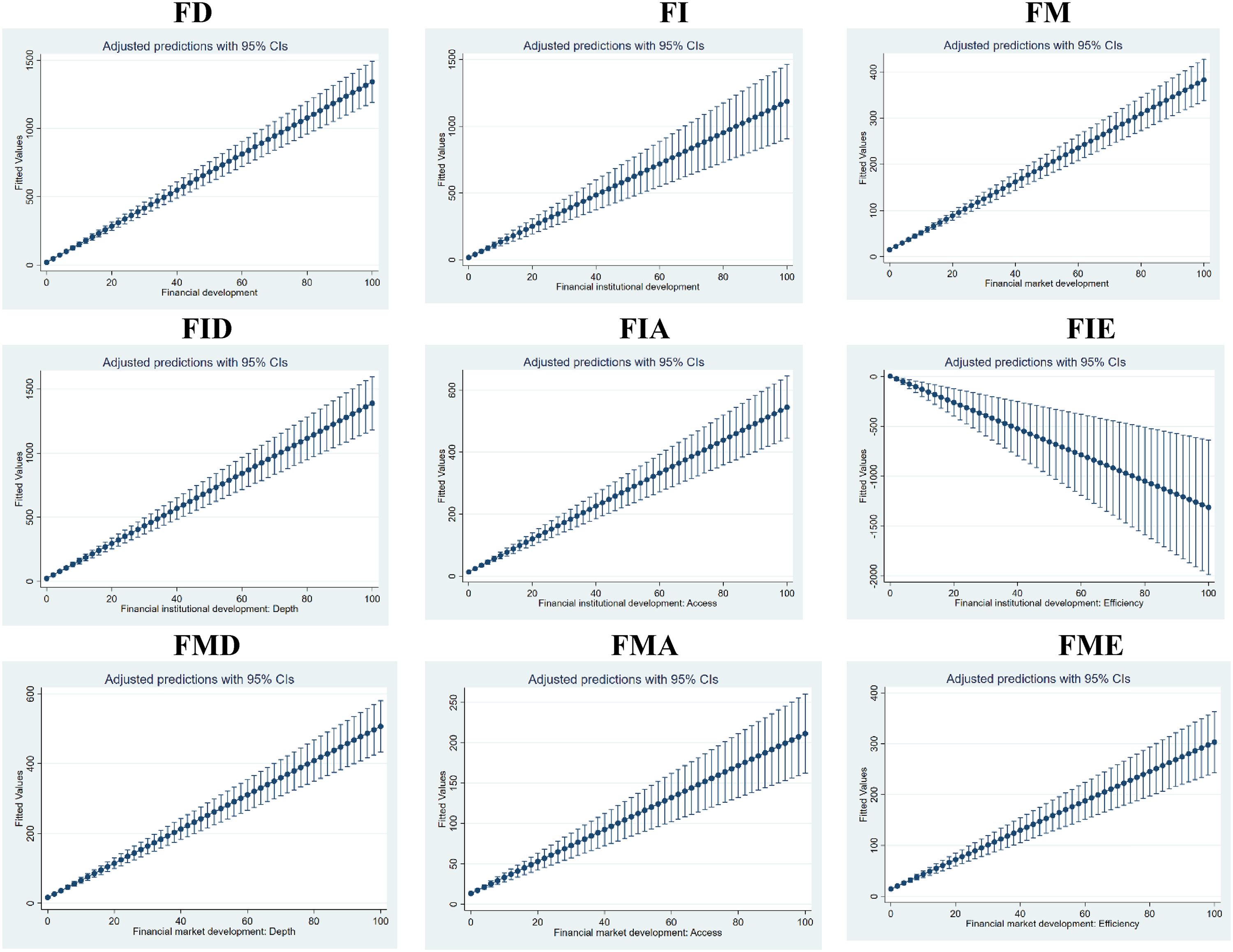

The results from Table 4 indicate that financialization can increase municipal waste yet in terms of circulation patents and circular material usage. However, as observed that different financialization dynamics propose different outcomes and influences, Table 5 offers a closer look at the influences of distinct dimensions of financialization on circularity in terms of depth, access, and efficiency. As for financialization depth, this dimension contributes to more municipal waste. However, consistent with the previous analysis, this dimension also promotes circularity patents and circular material usage. Although the recycling waste performance is not affected or has a statistically insignificant impact from financialization depth, the performance of recycling e-waste marks a positive influence. On the other hand, this dimension results in a negative influence on recycling biowaste.

Influences of distinct dimensions of financialization on the circularity.

Standard errors in parentheses.

***p < 0.01, **p < 0.05, *p < 0.1.

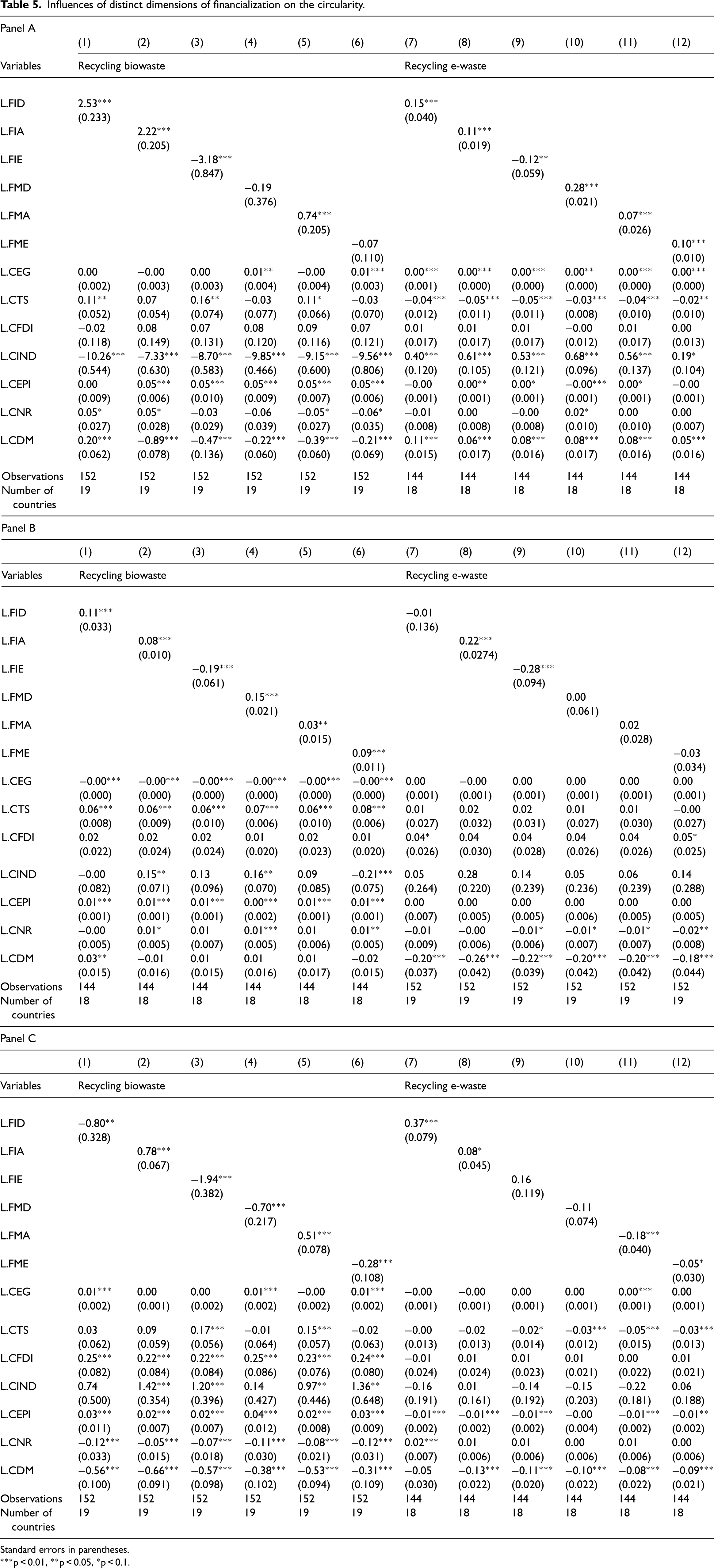

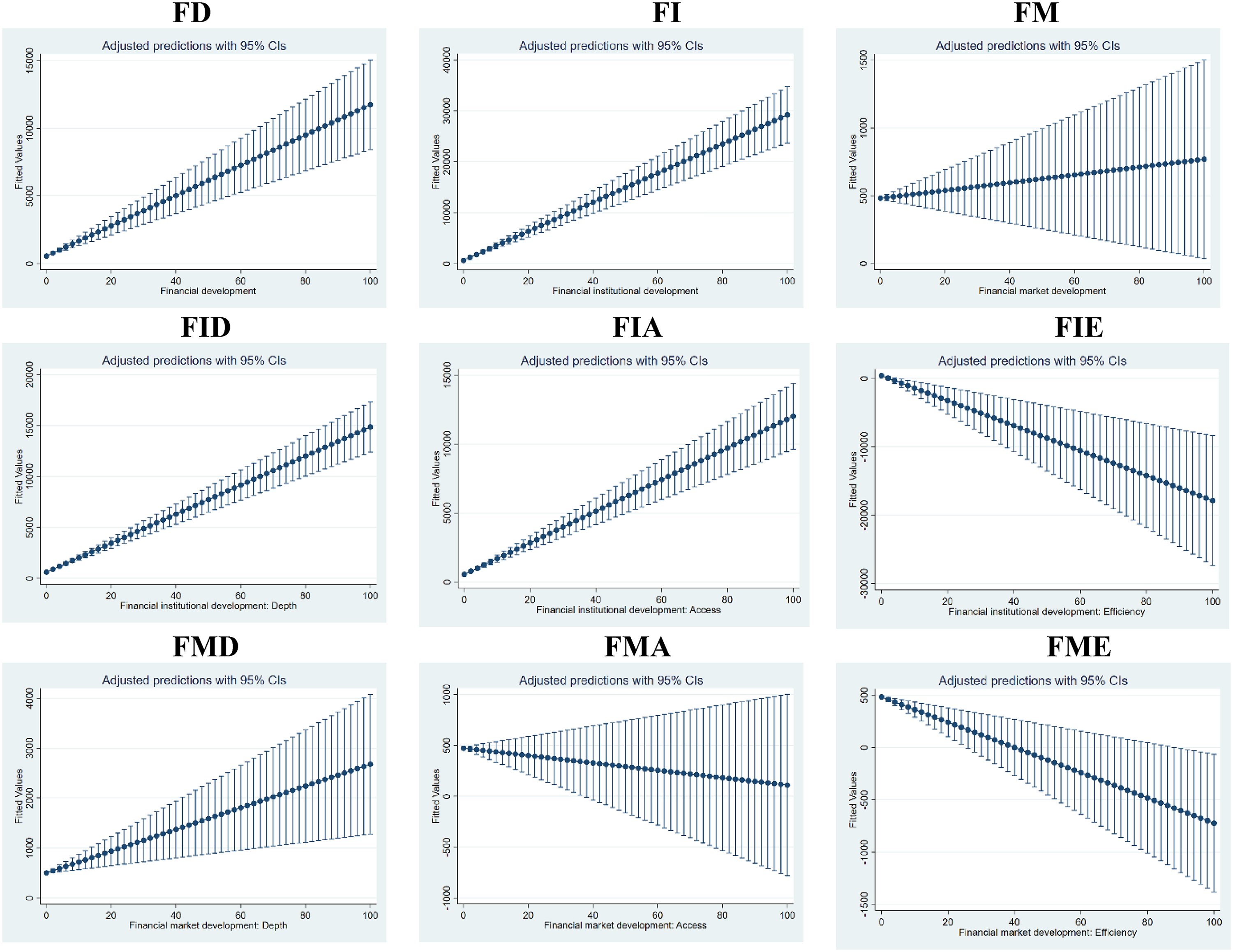

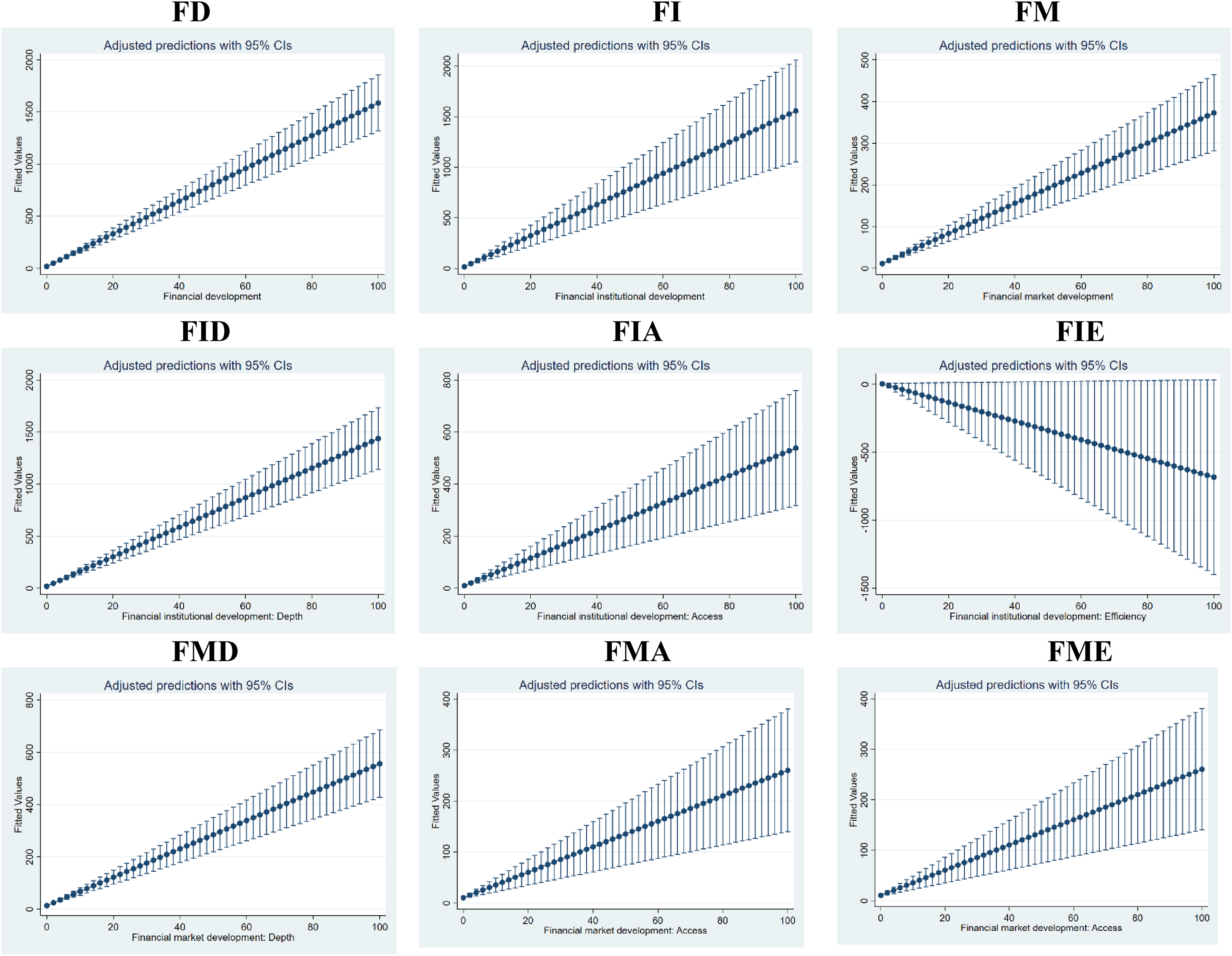

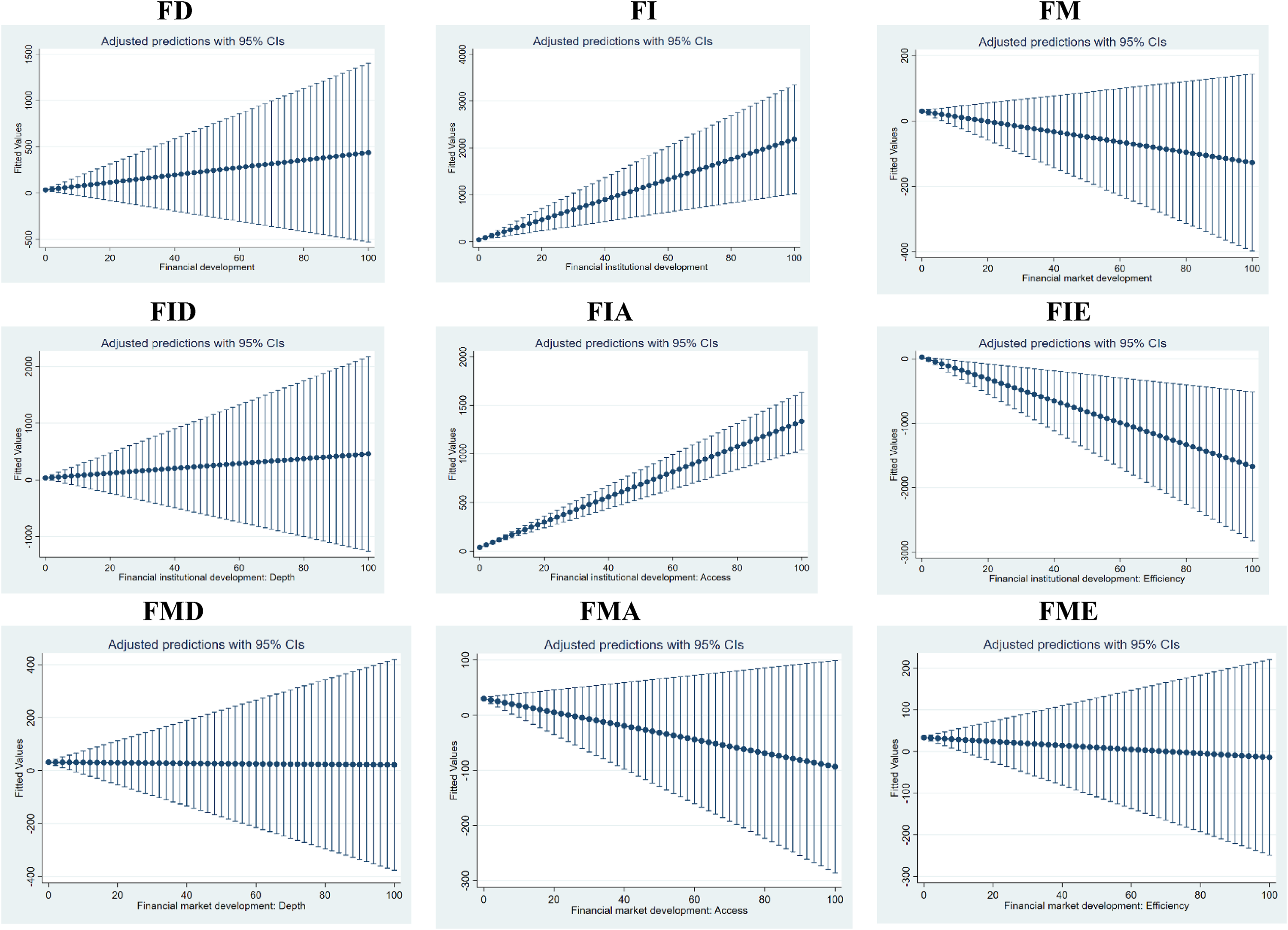

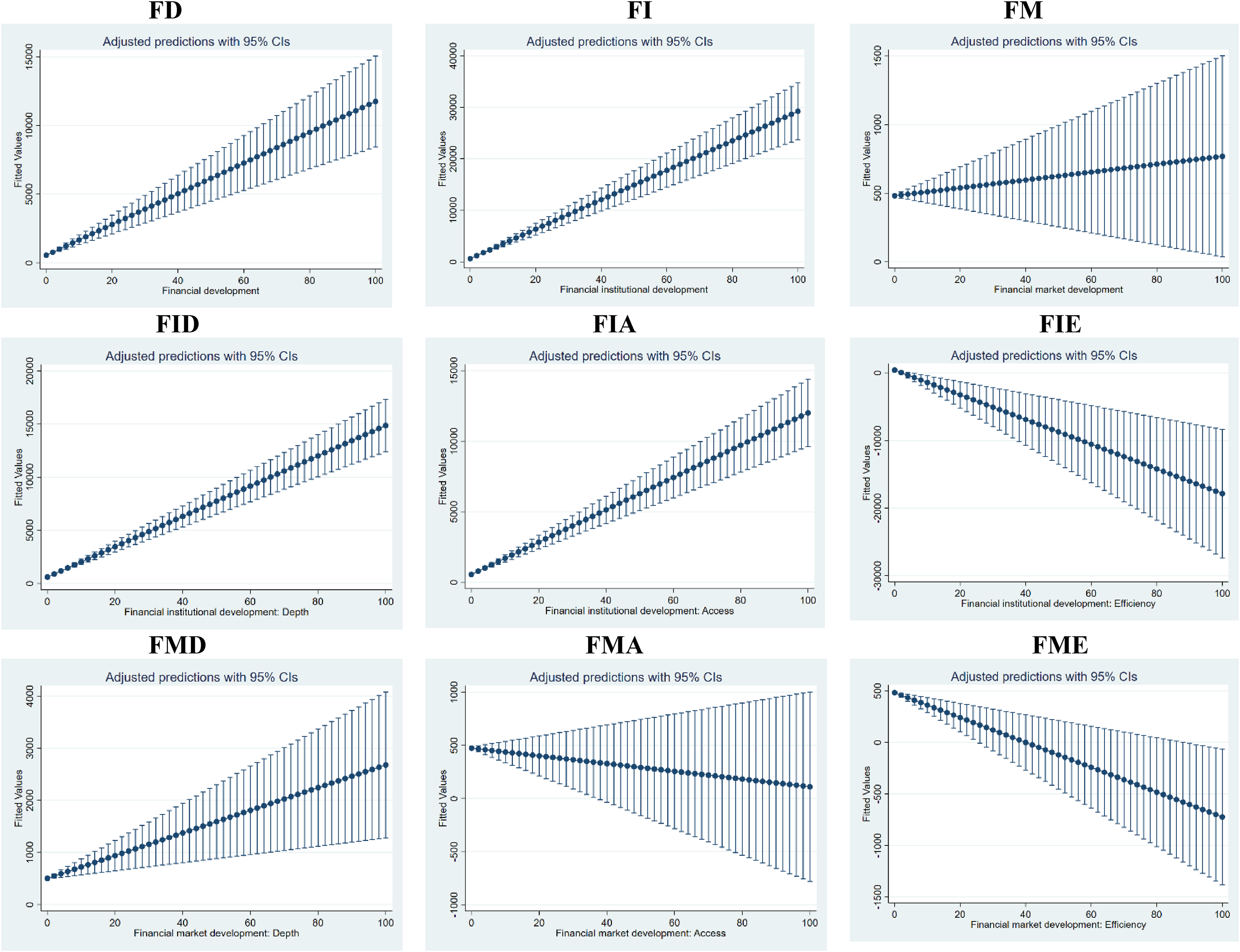

Next, we observe the accessibility of financialization and its influences on economic circularity. Access to financialization leads to an increment in municipal waste yet also increases all other aspects such as circulation patents, circular material usage, and the recycling performance of waste, bio waste, and e-waste. However, the development of financialization all results in the increment of waste. When looking at financialization efficiency, this dynamic reduces municipal waste while increasing bio-waste and e-waste recycling performance. However, this also results in fewer circulation patents, less circular material usage, and decreasing waste recycling performance. In scrutinizing the financial market, regarding the depth of the market, municipal waste, performance of recycling waste, and performance of recycling e-waste report no significant impact, while circulation patents and circular material usage report a positive impact and the performance of recycling biowaste endure a negative influence. Market accessibility increases municipal waste, circulation patents, circular material usage, and biowaste recycling performance while reducing the performance of recycling waste and e-waste. As for market efficiency, while the effect on municipal waste and waste recycling performance is insignificant, circular patents and circular material usage have a positive effect. Moreover, market efficiency also negatively impacts the performance of both biowaste and e-waste. To demonstrate our findings, we use the predictive margin figure to portray the margin of financialization and circularity in Figure 1.

Predictive margin of financialization and circularity (A) municipal waste.

(B) circulation patents. (C) circular material usage. (D) recycling waste. (E) recycling biowaste. (F) recycling e-waste.

Robustness check

Short-run and long-run effects: ARDL model

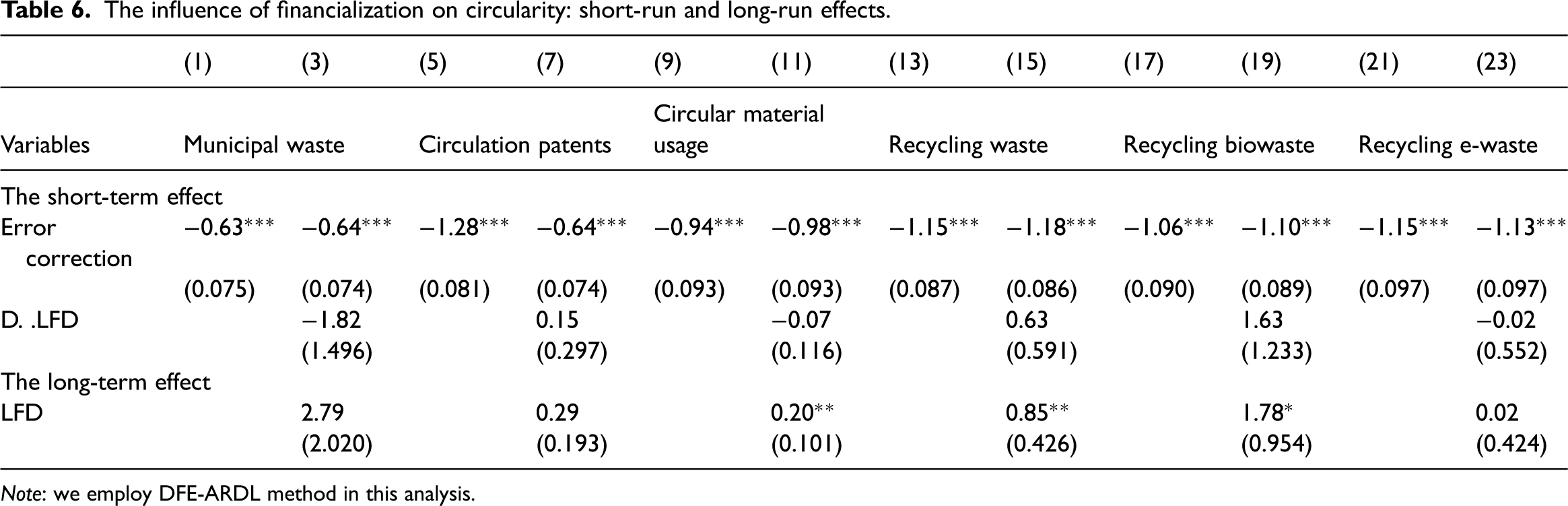

In the subsequent analysis, we concentrate on measuring the effect of financialization on economic circularity in the short and long term, and we report the results in Table 6. The results show that, in the short term, financialization has no significant impact on all aspects of economic circularity. However, in the long term, financialization affects three dimensions of economic circularity. Specifically, there is an increase or a positive influence on circular material usage, recycling waste, and recycling bio-waste. In other words, in the long run, countries with a better performance in the financial system are more likely to engage in using circular material while favoring increasing the performance of recycling waste (including biowaste). However, municipal waste is observed to have little to no impact. “Technical obsolescence” (the depletion of the improvement margin for subsequent technological efficiency increases) or a decreasing return on pollution-reduction technology might explain this impact. 90 According to recent studies, 91 there is actual evidence that pollution grows despite rising incomes, which contradicts the original EKC concept. Therefore, it can be stated from our findings that although financialization develops, municipal waste reduction is not observed. However, along with such development, focus on long term is witnessed in increasing circular material usage and recycling performance of waste and biowaste.

The influence of financialization on circularity: short-run and long-run effects.

Note: we employ DFE-ARDL method in this analysis.

Endogeneity control: two-step GMM

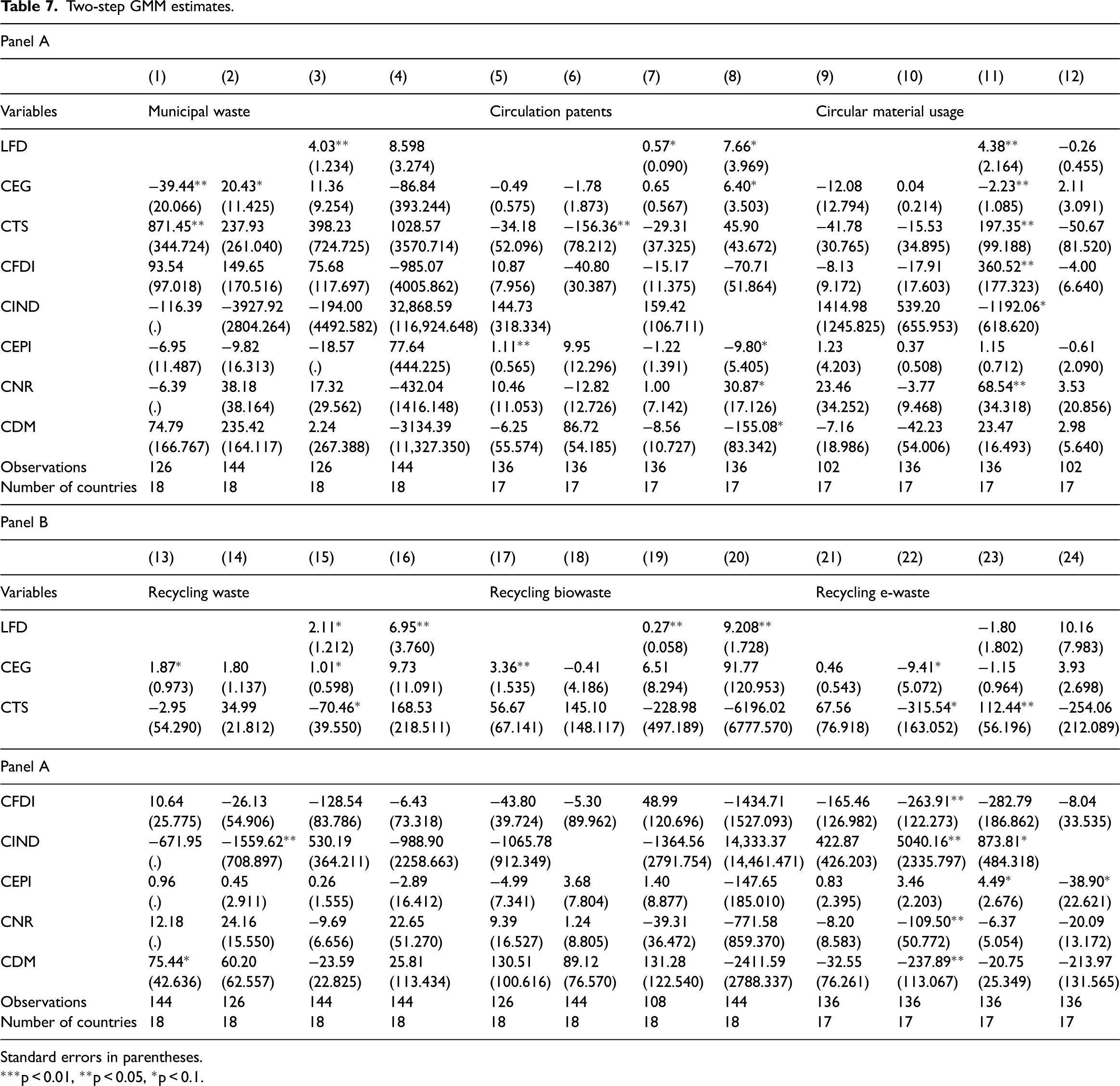

Next, we utilize two-step GMM estimates as endogeneity seems to be one of the article's drawbacks. The results are outlined in Table 7. For the financial development index, LFD can be observed to have little to no significant impact on the performance of recycling e-waste. However, for the rest of the circular economic dimensions, LFD appears to be statistically significant results. For municipal waste, financialization results in an increment of municipal waste. However, circulation patents, circular material usage, and recycling performance for both waste and biowaste also increase. This aligns with the previous analysis. For control variables, most of the variables mark to be insignificant.

Two-step GMM estimates.

Standard errors in parentheses.

***p < 0.01, **p < 0.05, *p < 0.1.

Conclusions

The first article examines the relationship between financialization and circularity performance in the European region. To reflect the circularity performance, we use six different measures. These measures include the amount of municipal waste, the number of circularity patents, the amount of circular material used, the rate of recycling waste, the rate of recycling biowaste, and the rate of recycling e-waste. Our study provides evidence that the expansion of previously implemented economy circulations has been enabled. Despite the fact that these results are only statistically significant for almost all aspects of financialization, financial markets appear to have a positive yet insignificant impact on circularity performance. The development of financial institutions is reported to increase municipal waste and the amount of recycling biowaste and e-waste, thus facilitating the transition to a circular economy. We use the different financialization dynamics to shed light on the nexus between financialization and circularity. We report heterogeneous outcomes and influences on different aspects of circularity performance. Moreover, the effects of financial development are more likely to be evident over the long term. The findings are robust and reliable when we take into account heterogeneity, fixed effects, and endogeneity.

Theoretical contributions

In this article, we propose a theoretical framework for extending our understanding of the relationship between financialization and circularity. In our view, the diverse dimensions of financial development, including financial markets and financial institutions, play a crucial role in promoting the circular economy. While previous studies consider a single dimension of circularity performance without delving into other dimensions, our article is expected to provide theoretical reasoning and empirical support to examine the role of financialization on circularity more comprehensively. We utilize circularity performance measures, which have characteristics such as low pollution emissions, low energy consumption, waste elimination, and increased efficiency. We also employ an inclusive measure of financial development, which can encompass the various aspect of financialization, including financial depth (i.e., size and liquidity of markets), financial access (i.e., the ability of individuals and companies to access financial services), and financial efficiency (i.e., the ability of institutions to provide financial services at low cost and with sustainable revenues, and the level of activity of capital markets). Consequently, our study contributes to the literature on the financialization-circularity nexus.

Practical implications

On the policy front, authorities should concentrate on the development of the financial system as a critical resource to promote circularity performance. Governments, global organizations, industry associations, and the world's leading enterprises, who are responsible for ensuring that the path toward the circular economy, is financially supported strategically, rapidly, and responsibly. It is imperative that we achieve our ambitious climate goals in order to save our planet and achieve our ambitious climate goals. One of the best ways to circularize the economy is to create new opportunities based on the development of the financial system in both the financial markets and financial institutions. These policies should focus on an improvement of the size and liquidity of markets, the ability of individuals and companies to access financial services, the ability of institutions to provide financial services at low cost and with sustainable revenues, and the level of activity of capital markets. The stability and development of the financial sector play a critical role in enhancing a country's comparative advantage to compete and seize the opportunity and advantages of circularity. Our findings also suggest that the path toward the circular economy can be promoted if the governments of these countries should propose financial support policies or policies to help countries mitigate financial pressure, such as a reduction in tax, an extension of a tax payment period, or a decrease in interest rate. However, we also want to emphasize that this positive influence will result in the long term rather than the short term. Therefore, we recommend investing in developing financial institutions and markets to facilitate the performance of circularity. These policies should be implemented consistently and for a sufficiently long period.

Limitations and further research directions

There are two limitations to this study that could be interpreted as limitations. To begin with, we analyzed archival data gathered exclusively for the European Union area. Although circularity has been accelerated in this area, it is vital to consider the role of financialization in enhancing circularity in developing areas as well. Developing economies are characterized by a low level of financial development and aim to move toward a circular economy. However, the surveys adhered to strict guidelines to gather information about various forms of circularity or simply the current level of circularity performance in developing economies. Second, there may be channels through which financialization influences circularity. These channels may be the level of economic development, economic complexity performance, and the effectiveness of government policies. These channels will be taken into account in the study, which is expected to provide more insightful lessons for economists and policymakers in designing policies to promote the circular economy. Future research may need to explore data sources to gather more information about circularity in developing countries and examine the role of financialization in this area.

Footnotes

Author Contributions

Le Thanh Ha contributed to all stages of preparing, drafting, writing, and revising this review article. Le Thanh Ha made a substantial, direct, and intellectual contribution to the work during different preparation stages. Le Thanh Ha read, revised, and approved the final version of this manuscript.

Compliance with ethical standards

Disclosure of potential conflicts of interest. Research involving human participants and/or animals. Informed consent.

Consent for publication

Not applicable

Data availability statement

Data available on request due to privacy/ethical restrictions.

Ethics approval and consent to participate

Not applicable.

Declaration of conflicting interests

The author(s) declares that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This article was supported by National Economics University.

Appendix

Countries in the sample.

| EU countries | ||

|---|---|---|

| Austria | Hungary | Portugal |

| Belgium | Iceland | Slovak Republic |

| Bulgaria | Ireland | Slovenia |

| Czech Republic | Italy | Sweden |

| Denmark | Lithuania | |

| Spain | Luxembourg | |

| Estonia | Latvia | |

| United Kingdom | Malta | |

| Greece | The Netherlands | |

| Croatia | Poland | |