Abstract

In Hungarian libraries, the development of financial literacy (FL) is either not present at all or is very low in intensity. The Hungarian government strategy does not involve libraries in FL development. Based on the dissemination of information and digital literacy, there are numerous good examples worldwide proving that libraries, reaching all of their users, can effectively take part in financial education and, built thereon, business development and business information services. This can increase their social recognition and even supplement their funding. In 2022, for the first time in the country, the authors conducted a survey among Hungarian librarians to assess the current situation, to identify what hinders the expansion of services related to FL, and what tasks should be performed and what innovations should be introduced in libraries. The survey also seeks to define which fields of competence are to be acquired by librarians. It also reveals the forms of external professional cooperation that are necessary to organise library programmes strengthening financial awareness. The results provide valuable information not only for Hungary, but also internationally, since they showcase the challenges that the library system of a former socialist country in Europe faces after three decades of market economy in this current, market- and profit-oriented world.

Keywords

Introduction

The financial crises of the 21st century, the pandemic, the ongoing war in Ukraine, and the resulting, ever deepening economic recession all increase the value of measures aimed at improving the population’s financial literacy (FL). The economic recession of 2008 already highlighted that those with lower levels of FL are more likely to make financial mistakes, and have a harder time handling an economic crisis (Hung et al., 2009). Therefore, the skills, knowledge, and competences which can help people be more successful even in financially difficult situations are increasingly important not only at a micro- or macroeconomic level, but also from a societal (social and equal opportunity) point of view.

The UN’s first sustainable development goal is eradicating poverty. In achieving this goal, FL has a vital role, which libraries can also support with their work, since they already take part in education, and in the creation and mediation of culture.

There are several models for the development of FL, similarly to how society has diverse expectations related to financial education. The international driving force behind developing FL is the OECD International Network on Financial Education (INFE), created in 2008, which encompasses more than 285 state institutions from 130 countries. Its document repository contains expert materials, surveys, etc., one of the most recent being the EU/OECD-INFE financial competence framework for adults (FINCOMP) (OECD, n.d.). The efforts of member states are in line with the goals of the OECD-INFE. Every country built a different strategy to develop FL fitting their own society and culture. The Hungarian government accepted the strategy for improving financial awareness (Pénzügyi tudatosság fejlesztésének stratégiája, n.d.) in 2017, which is available not only in the form of an expert document, but through the complex website named Be Smart With Money (Okosan a pénzzel, n.d.) as well. It can be concluded that the strategy does not involve Hungarian libraries when it comes to achieving its goals, even though the authors’ study clearly supports that it is necessary to expand the financial services of Hungarian libraries. According to the OECD’s international survey from 2020 (Kiril, 2020) monitoring the adult population and assessing FL by awarding points in three categories (financial knowledge, financial behaviour, financial attitude), Hungary is placed in the lower middle section.

It is a well-known cliché that libraries cannot be replaced by the internet, therefore, libraries also have certain duties in improving (digital) FL (Ballestra et al., 2016; Faulkner, 2022a, 2022b; Keller et al., 2015). Financial education covering all social classes requires access to information and critical thinking. Users will continue to turn to libraries for reliable sources, from which they can acquire information necessary for making financial decisions (Kraus, 2015). The most common sources of financial information are the internet and the family (Ballestra et al., 2016), but as a 2015 survey from the US clearly states, the library is also a possible basic institution for financial information. (Barack, 2015)

Literature review

Libraries get involved with the primarily non-formal education of FL-related knowledge in various ways all over the world. Nowadays, it is mostly the development of information literacy and the guaranteeing of equal opportunities which are in the forefront of research and programmes, especially the library adaptations of the UN’s sustainable development goals (SDGs) (IFLA, 2018). There is abundant literature on the library aspects of developing FL. The authors’ recent summary examines, based on an international literature analysis, the library results achieved over the past decade in the field of developing FL (Kiszl and Winkler, 2022). Further current studies also analyse national strategies (Faulkner, 2022a), services (Faulkner, 2022b) and the characteristics of certain countries (Yap et al., 2022).

Successful programmes are aimed at the two target audience groups of financial awareness development: library users and librarians (the training of trainers). The American Library Association (ALA) offers a complex programme to develop FL using the toolkit of libraries, with the cooperation of several external cooperating organisations, but especially with the partnership of the Financial Industry Regulatory Authority (FINRA) Investor Education Foundation. The Financial Literacy Education in Libraries: Guidelines and Best Practices for Service was published in 2014 (RUSA, 2014). The Financial Literacy Interest Group (FLIG) blog of the ALA Reference and User Services Association (RUSA) provides up-to-date information on the subject (ALA, n.d.a). The Financial Literacy in Public Libraries: A Guide for Building Collections collects LibGuide sources (books, websites, databases) and provides professional support for librarians (ALA, n.d.b). The complex Smart Investing @ Your Library programme (ALA, n.d.c) operates with the professional and financial cooperation of the FINRA Foundation, and its pillar aimed at children is Thinking Money for Kids. The former travelling exhibition was transferred to the virtual space out of necessity due to the pandemic, and lives on as an online game, thereby fitting the current gamification trend. The volume published by the ALA provides 16 library model programmes (Welch and Hogan, 2020), and in 2011 the ALA got involved with the Money Smart Week programme as well (ALA, 2012).

The process of developing teaching material, webpage collections, and curricula related to FL development programmes is not necessarily the responsibility of each and every library. The New York Public Library, for example, took on this task, and many other libraries may follow in their footsteps. Librarians can profit from their webpage Money Matters Pro (New York Public Library, n.d.a), and their users can benefit from the platform Money Matters (New York Public Library, n.d.b). In the public library project of New York there are also committed directors and colleagues, and partners who recognised the mutual benefits of cooperating with libraries (McDonough, 2014). The same can be seen at the Wells Fargo-sponsored initiative available for locals, the New York StartUP! Business Plan Competition (New York StartUP! Business Plan Competition, n.d), which is aimed at business development and, more specifically, encouraging the foundation of startups. In Europe, the economic development service system of the British Library Business & IP Centre (Business and IP Centre, The British Library, n.d.) is worth mentioning.

Programmes supporting businesses, however, can only be truly effective for a target audience with adequate awareness about their personal finances. To summarise, the successive steps in economic development are:

developing digital literacy;

developing FL;

supporting new businesses (even startups), business development.

Hungary had a centrally planned, Soviet style economy before the 1990s, which had an impact on the everyday life of libraries as well. The change of the political system, that is, the transition to a market economy led to a promising period, a good library-related example being the Entrepreneurial Information Project (Vállalkozói Információs Projekt, VIP), but this was followed by years of stalling and isolation. National library strategies and the programmes linked to their implementation barely involved the topic of FL and business information, if at all (Kiszl et al., 2018). Among educational institutions, the Institute of Library and Information Science of the Faculty of Humanities of Eötvös Loránd University in Budapest has been prioritising the education and research of financial knowledge, financial awareness and business development for more than two decades without interruption, and there is no accredited further education programme available in this field (Kiszl, 2021). There are public library best practices to mention from nearby European countries as well: The Finlit – A Model for Non-Formal Education of Adult Library Users (Bon et al., 2021) was created with the cooperation of Bulgaria, Poland, Romania, and Slovenia. This is one of the reasons which made this survey topical in Hungary.

Methodology

The survey was conducted in May–June of 2022 with the software Survio. The questionnaire was sent to the participants via the largest Hungarian librarian mailing list (Katalist), two large Hungarian Facebook groups for librarians, and by directly contacting the leaders of Hungarian librarian organisations. The idea for assembling the questions was provided by the content on the Manager Tools of the ALA Smart Investing @ Your Library website (Smart Investing @ Your Library, n.d.b).

One third of those who visited the page completed the questionnaire; a possible explanation is that there were 42 questions, and it took 5–10 minutes for the majority (50%) to complete, 10–30 minutes for 30% of the respondents, and even longer for the rest. The questionnaire was admittedly long, and its completion required quite a long time. During testing, the excessive number of questions was raised as an issue, but the goal of the survey was to gain a deeper understanding, therefore, the authors decided to keep the long questionnaire instead of a shortened one which could have generated a more favourable completion ratio.

One third of the respondents are between the ages of 50 and 59 years, the second largest age group is of those between 40 and 49 years, followed by half as many 30–39-year-olds, and then a nearly identical number of 20–29-year-olds and respondents above 60. 80.9% of the respondents are women, 16.8% are men, and 2.3% did not wish to answer. According to the authors’ judgement, this fits the age and gender composition of Hungarian librarians.

Seventy-eight percent of the respondents have relevant professional qualification, 71% of whom did not study economics during their librarian training. The most frequently mentioned subjects by those who studied economics were macro- and microeconomics and library management.

Among the 256 respondents, only one person (0.39%) is not working in a library at the time of the research; this reflects the authors’ intention to survey colleagues currently actively working in libraries. Altogether 36% of them work in Budapest, 12% in Pest County, while Fejér, Bács-Kiskun, and Heves Counties are represented above 5%, the rest being under. Based on the 2021 data of KultStat (the abbreviation in Hungarian for Kulturális Statisztika, in English: Cultural Statistics), there are 3213 librarians currently employed in Hungary (Könyvtári Intézet, n.d.) [The harmonised time series database of library statistics]. This research is therefore not representative, which may be considered as a potential limitation of the study. Nevertheless, through using the technique of self-selection (or volunteer) sampling (Jupp, 2006), the results of the study provide important and useful information, since those completing the questionnaire are the most suitable participants, that is, ones who, possessing adequate knowledge, experience, and interest, could or wished to voice relevant opinion on the topic. This was an important criterion, since FL as a topic is typically outside the scope of (foreign to) the professional activities of Hungarian librarians.

The distribution of the respondents’ place of employment according to library types: 30% work in city libraries with county-wide scope; 23% in municipality/city libraries; 22% in higher education libraries; nearly 9% in national specialised libraries; and 6.6% in school libraries. The remaining 9.4% work either in the national library, in workplace libraries, or in religious ones. The answers, therefore, cover a wide range of institutions.

Nearly one-third of the respondents are library directors, which means they are represented in a high number. Most of the respondents (26.6%) work in reference service, while the following three biggest categories are those of bibliographers/cataloguing librarians, (professional) information service providers, and collection managers (between 10% and 15%).

Our examination focuses on FL exclusively. As it is emphasised, financial consultancy is generally not among the tasks of librarians (Kiszl, 2021).

Results

Nearly half of the respondents stated that there is no colleague in their library familiar with financial topics. This percentage is quite high, but it should be considered that more than one respondent could be from the same library. In one-third of the respondents’ institutions there is at least one colleague skilled in finances, and 10% could not provide an answer to this question.

Eight out of 10 librarians stated that there is no material related to finances on their library’s website (source collection, programme recommendations, etc.), and there were no programmes organised related to finances over the past 5 years either in the library or at an external venue. Those four librarians who indicated that they organised local trainings related to finances mentioned the topics of taxes (3 responses), consumer protection and fraud (1 response), and children and money (1 response). The few projects implemented at external venues had similar topics.

The responding librarians are not convinced but believe that their library might be able to find cooperating partners who could help implementing financial educational programmes: the average response was 3 on a scale of 1–5. One third of the respondents have little confidence that their library could organise financial awareness raising programmes which would meet the library users’ expectations; another third are undecided (3 on a scale of 1–5); and the remaining 40% indicated that their library could probably organise such an event.

Forty-four percent of the respondents do not believe that, and 38% are undecided whether their library’s employees could answer finance-related questions asked by their users. Only 17% of the respondents gave a decidedly positive answer (4 or 5). The average result was 2.6, which also proves that it is essential to address this topic.

The respondents stated that their library’s employees might not be able to provide assistance in more complex finance-related problems even with the help of external sources or other institutions. The average result was 2.9, which shows that they have little confidence in their colleague’s competence in this field.

The next question, however, shows that the respondents gave a 2.78 rating on average to how well they know their library’s finance-related collection and programmes. This answer should be taken into consideration when evaluating those preceding it.

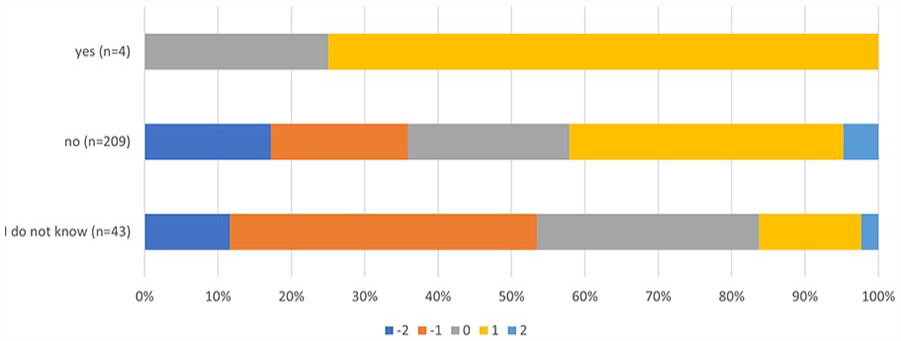

After inquiring about financially savvy colleagues, the question represented in Figure 1 was aimed at evaluating how competent the respondents themselves are in answering questions related to finances. Negative and positive answers were given in nearly equivalent proportions of approximately 40%–40%, while the remaining 24% of the respondents are uncertain which side they belong to.

Assessing own competences in FL-related questions.

Fifteen percent of the respondents participated in professional training covering financial topics over the past 5 years. Half of them received further education, 36% used online sources, and 21% attended higher education programmes. The remaining respondents attended professional conferences, webinars, other trainings, and 7.9% completed in-library training. One limitation of the research is that the depth of these trainings cannot be established.

The survey also inquired about the topics in which they would consider receiving training. More than 30% indicated the categories Children and Money, Household Budget Planning and Record Keeping, and Bank Services and Savings; between 20% and 30% indicated Pension Planning, Free Services for Those in Financial Difficulty, Consumer Protection and Fraud, and Investments; and every fifth respondent also marked Taxes as an answer. This establishes the major directions of competence development.

Related to the issue of library information service and requesting assistance, the questionnaire contained the question How often do library users request information sources and assistance in financial topics? 34.7% of the respondents indicated that they do not know, or they do not remember, while nearly 50% stated that no questions are asked on this topic. Based on these responses it can be established that approximately 15% of the respondents were asked questions related to finance. Figure 2 illustrates the answers without the options I do not know and I do not remember.

Frequency of FL questions by users.

The next question was aimed at assessing the level of the librarians’ awareness of initiatives supporting FL development in Hungary. One quarter of the respondents have heard of at least one relevant programme, and there was no significant difference between the responses of library directors and employees.

The authors also wished to get information on Hungarian initiatives supporting financial awareness development. The names most often mentioned were the Hungarian National Bank (14) and András Fáy’s Foundation (10), Pénz7 [Money Week] (8), the State Audit Office (7), the Pénziránytű [Money Compass] Foundation (7), and Okosan a pénzzel [Be Smart With Money] (5). Although they are not prominent individually, the respondents also mentioned initiatives of educational institutions; advertisements, websites and consultation services of banks; books; and periodicals (both online and printed).

Only 6.6% have heard about foreign initiatives; more than half of those giving an affirmative answer, 11 respondents, could name a specific programme. For example, British Library (11), Money Smart Week (4), Thinking Money (2), Smart Investing @ Your Library (1).

No more than 5% of the respondents could mention any national or international library initiatives supporting business development. Seven of them named the British Library, two the IFLA, and Hungarian examples included a rural municipality library (Justh Zsigmond Town Library) and Eötvös Loránd University.

To the question Why do you think it is necessary for libraries to participate in the development of financial awareness?, 178 free-text responses were received. The authors classified the individual answers to three clearly definable groups which could include numerous responses. There was one respondent whose answer fit two of the created categories. Thirty-four percent of the respondents believe that the development of financial awareness is one of the responsibilities of libraries; 30% believe it could be one of the responsibilities of libraries, and it would be worth making efforts; and another approximately 30% stated that there would be a user demand for this library role, and this is why efforts should be made. Seventy percent of the respondents believe that it is necessary for libraries to get involved in financial awareness development. Besides the already existing demand therefor, the respondents identified further reasons as well, for example, the library’s information mediating and digital competency developing role, and its ability to reach a wide audience. Those who do not believe the libraries’ involvement to be necessary mostly stated that ‘this is not what our duty is/this is not our responsibility’, and other recurring arguments included the lack of competence and capacity, limited funding and prestige, weariness and burnout.

Nearly two-thirds of the respondents think that the social status of libraries would improve if they assumed the roles included in this research: education and information service related to financial awareness; two-thirds of the respondents, however, believe that the funding of libraries would not improve by assuming the roles included in this research: education and information service related to financial awareness.

Involvement in business development is not considered necessary by the majority (54%) of the respondents. Fifty-three percent of them, however, still believe that if libraries got involved in business development (e.g. information service provided to startups), it could improve their operation and make them more effective.

Three quarters of the respondents think that it is necessary to teach subject related to economics, FL, and business development in higher education librarian training.

The most useful tools for developing financial awareness, according to the respondents, are (1) model projects (introducing good practices), support materials prepared for programme planning, (2) online resource collections (LibGuide), (3) librarian training and the further training of library directors.

Analysis

Seventy-eight percent of the respondents have a relevant higher education degree, but there is no relation between the year of graduation and the year of birth, as Figure 3 shows. During their higher education studies, only 28% of the respondents studied economics.

Year of birth and graduation of respondents.

The number of respondents with degrees is not distributed evenly throughout the examined periods. Most of the respondents graduated between 2000 and 2009, but, as Figure 4 clearly shows, the number of those graduates who studied economics increased decade by decade. Due to the limited number of years passed in the current decade (2020–2022), there will most likely be a significant and continuous increase over these five decades, especially because Eötvös Loránd University, the largest Hungarian university training institution, has been prioritising teaching economics since the millennium.

Librarian graduates who studied economics.

The economics knowledge acquired by librarians during their years in higher education can be compared to how competent they believe themselves to be in answering finance-related questions. The fact that someone completed a subject on economics in higher education does not imply that they feel competent in providing information on financial matters (for these two indicators: r = 0.069, p = 0.331). Therefore, it can be established that those who received training in economics consider themselves confident in a higher proportion, but the two lower categories are still nearly identical.

Whether librarians feel competent does not follow from whether their library’s page contains FL-related material. It can be said, however, that if there is such material to be found, and if the librarian is aware of it, there is a higher chance that they feel competent. This can be due to several reasons. For example, where such material is published, colleagues work on this subject; there are related leadership intentions; the topic has been covered; or related programmes have been organised.

Sixteen percent of the respondents did not know whether their workplace offered any trainings or programmes related to finance over the past 5 years. If someone knew about a training their library offered on the topic of financial knowledge, it seemingly made them more confident in their own competences in related information service. Unfortunately, only four persons reported on such trainings, therefore, the answers suggest a trend, but the sample size is too small to assume that a greater number would bring the same results. Figure 5 shows that the most uncertain respondents were the most likely to answer I do not know to the question on trainings provided by their library.

Library FL programmes and librarians’ FL competence.

Overall, the respondents assessed their own competence to be higher than that of their colleagues at their library when they answered the question on their own and their colleagues’ competences in financial matters. It is intriguing to see in Figure 6 that there is quite a high number of respondents who are confident in their own competence (33%). This raises the question whether everyone assessed their colleagues compared to their own level of competence, but there was only a slight positive relation between the two sets of responses.

Colleagues’ and own competences in answering FL questions.

When the confidence level in their own competence is compared to the answers on their colleagues, it is visible that most respondents consider themselves more competent than they do their colleagues (41%), and nearly the same number believed their own and their colleagues’ level of competence to be the same (35%). One quarter of the respondents believe that their colleagues are more competent than them.

If the responses to the two questions are analysed in a structured manner, meaning that those who assess their own competence to be the same are grouped together, and then it is examined how competent these groups consider their colleagues, it can be established that, on average, those who are more confident in their own competence are more likely to believe the same about their colleagues, and the uncertain respondents are more likely to think that their colleagues are the same.

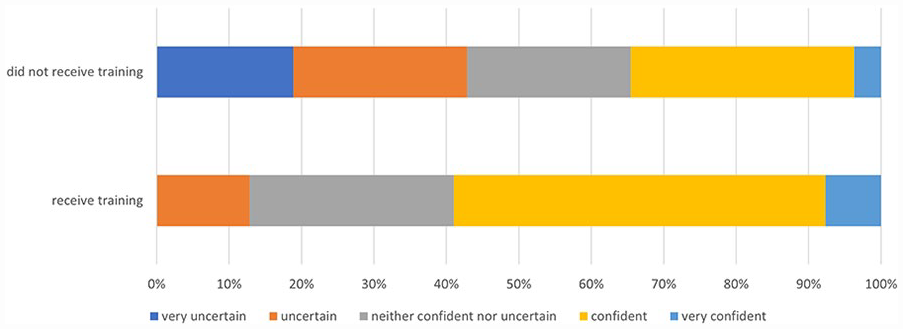

If someone participated in a finance-related professional training over the past 5 years, did that increase their confidence in their ability to answer questions related to finances? The responses strongly suggest that it did. Not one respondent who received such training stated that they are very uncertain, and only 12% of them chose uncertain. Among those who did not receive such training, the proportion of those uncertain was a lot higher, and the proportion of being confident or very confident was a lot lower. This means that there could be a link between receiving training and how competent each person feels. Unfortunately, only 15% of the respondents participated in such a training, but Figure 7 shows the differences between the two groups.

Finance trainings and librarians’ FL competence.

There was no connection found between participation in trainings and the number of questions raised by readers in the library. Most of the respondents did not receive such questions or do not know whether the library receives any. Based on the results, in most cases the participation in trainings was not motivated by the readers’ needs.

According to those who receive finance-related questions based on their answer given to the question How often do library users request information sources and assistance in financial topics?, and could identify how often this happens, it is not typical to receive these questions on a daily basis, but there is interest. The answers show that nearly 70% of the respondents received the latest question a month ago or receive FL-related questions even more regularly (weekly or even daily). Neither library users nor policy makers consider libraries significant partners in Hungary when it comes to FL and financial information, but, based on the results, there is a demand among users.

If the responses to this same question (How often do library users request information sources and assistance in financial topics?) are examined classified into groups, it can be established that in libraries where there is someone familiar with financial topics, related questions were asked more frequently. However, the existence or lack of FL material available on the library’s website shows a considerably less distinctive pattern, meaning that the content of the website is less indicative of the number of questions they receive. Respondents from libraries where there were FL trainings organised over the past 5 years generally could not say when they last received a question on this topic. Those libraries, however, where there were absolutely no finance-related questions asked, did not organise any trainings.

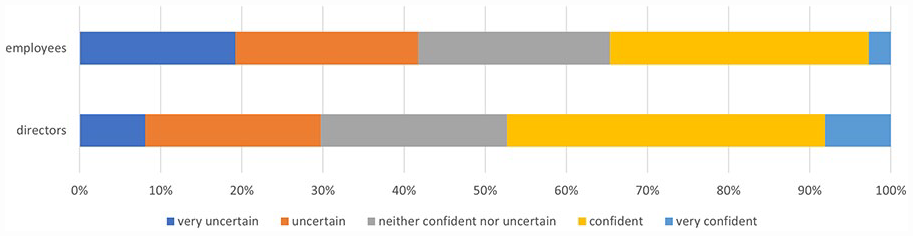

According to Figure 8, the confidence level of library directors and employees in answering questions differ; directors were more likely to choose more confident options, but this could also be a result of managerial attitude.

FL competences of library directors and employees.

Regarding the questions on the improvement of the libraries’ social standing and their possibly increased funding, the results vary about assuming a role in the development of financial awareness. Nearly the same number of respondents believe that both the social standing and the funding would improve; that social standing would, but funding would not improve; and that neither social standing nor funding would improve. The most outstanding is the extremely low number of those who believe that assuming these projects would not improve the libraries’ social standing, but it would improve their funding (Figure 9).

Improving social standing and funding with FL library services.

Those who believe that assuming educational and information service roles would improve the libraries’ social standing consider it more necessary for libraries to participate in the development of financial awareness. There is a positive relationship between the two datapoints (r = 0.655, p = 0.001).

Summary

Based on the answers, and taking national characteristics into consideration, the necessary Hungarian library development demands could be defined, and the obstacles to innovation could be identified as well. First, the project components of Smart Investing @ Your Library which are the most easily applicable in Hungary should be considered:

online further education programmes on the topic of developing FL specifically for librarians (Smart Investing @ Your Library, n.d.e).

a guide on identifying and convincing external cooperating partners in order to develop and operate services (Smart Investing @ Your Library, n.d.a).

the national adaptation of the 16 model programmes already successful in American libraries (Smart Investing @ Your Library, n.d.d).

more conscious collection management related to personal finance (Collection Management for Personal Finance and Investing Resources (Smart Investing @ Your Library, n.d.b).

marketing activities focused on FL (Smart Investing @ Your Library, n.d.c).

initiatives aimed exclusively at children (application developed from the Thinking Money for Kids travelling exhibition due to Covid19 (ALA - FINRA, n.d.), a guide on expansion (ALA - FINRA, n.d.), a collection on programme ideas (ALA, n.d.c), gamification solutions.

The research findings support that it is inevitable for libraries to be the venues for non-formal trainings on finance and business development, since they can reach all social classes, are physically present in all villages and cities, and are constantly available remotely. The conditions for this for different types of libraries:

appearing in the nationwide strategy created by the governance of this sector, in accordance with the Digital Welfare Programme and Hungary’s Digital Educational Strategy (DOS - Magyarország Digitális Oktatási Stratégiája - Digitális Jólét Program, n.d.), with the principles laid down in the national strategy for financial awareness, and with the strategic objectives of consumer protection, culture, etc.;

central methodology support based on international best practices (professional organisations to be named later and/or Library Institute);

involving external professional and funding partners (see below);

a change of perspective by the representatives of the library sector (complex, diversified element: its conditions include a pay reform, attractive career guidance, developing the organisational culture, preventing burnout, etc.);

acquiring funding (grants from state, civil, or market economy sources, or a combination thereof);

continuous modernisation of librarian training (universities) and further education (Library Institute) with the cooperation of external partners.

In Hungary, all of the above needs to be completed in line with the national strategy Okosan a pénzzel!, by seeking cooperation opportunities with the National Financial Awareness Working Group: State Audit Office, Ministry of Interior, Central Statistical Office, Ministry of Culture and Innovation, the Hungarian State Treasury, the National Bank of Hungary, Pénziránytű Foundation, Ministry of Finance, Ministry of Technology and Industry.

In addition to those listed above, potential partners to libraries include commercial banks (e.g. K&H Vigyázz, kész, pénz! [Ready, Set, Money!]) and their foundations (e.g. OTP András Fáy Foundation), the network of professional chambers (e.g. Hungarian Chamber of Trade and Industry), other financial institutions for mediation (e.g. insurance companies), professional organisations (e.g. Hungarian Banking Association), the civil sector (e.g. Econventio Kerekasztal Közhasznú Egyesület [Ecoventio Roundtable Non-profit Association]), national events (e.g. Pénz7). In the United States of America, the ALA is the engine of the initiatives; in Hungary, this could be the Association of Hungarian Librarians and the Alliance of Libraries and Information Institutes. The achievement of higher education goals could be coordinated by the Board of University Library Directors.

When it comes to the support of developing FL via library tools, the competence development of librarians has a key role. Taking into account the results of the National Impact of Library Public Programs Assessment (Shepard et al., 2019), the following competences are essential for effective librarian work. (Hard) competences built on each other, directly contributing to the development of national economy: (1) digital literacy, (2) FL, (3) business/entrepreneurial competencies. Additional (soft) library and information science competences: (1) source knowledge, (2) searching, (3) cooperation (with users and external partners), (4) fundraising, (5) learning (lifelong learning), (6) time management, (7) ethics, (8) adoption of best practices (event planning), (9) adaptability (conflict management) competences (Kiszl, 2022).

Therefore, financial education is a possible way out in order to, among other goals, recover the tattered social standing and perceived usefulness of the librarian profession and the libraries’ reputation among their maintainers.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the János Bolyai Research Scholarship of the Hungarian Academy of Sciences and the ÚNKP-22-5 New National Excellence Programme of the Ministry for Culture and Innovation from the source of the National Research, Development, and Innovation Fund.