Abstract

The paper reports on a study of the comparative stability of foreign owned manufacturing firms in Wales, using as a framework the Welsh Register of Manufacturing Employment which records details of regional manufacturing entry and exits since 1966. The paper is set in the context of competing claims on the more transformative effects of inward investment with some stressing that notions of a ‘new regionalism’ in Wales have been unjustly founded on assumptions about the transforming effects of foreign investment. There is also a problem of a paucity of research showing how foreign investment had been involved in evolutionary processes of regional economic change. The paper shows that a more complete appreciation of the role of inward investment needs to consider not only its role in job creation but also the relative stability of the investment and jobs attracted. The paper reveals how analysis of plant birth and deaths also links through to perspectives offered by evolutionary economic geography, and how patterns of entry and exit might work to influence the economic trajectories of a disadvantaged region such as Wales.

Introduction

The activity of foreign manufacturing subsidiaries across the UK regions has been widely studied, with several papers having examined the embeddedness of foreign manufacturing in the regions (see, for example, Phelps et al., 2003). Embeddedness is multi-faceted and can include issues such as the intensity of buyer–supplier linkages of foreign plants, and the types of functions undertaken within these plants (for a discussion of these issues in relation to foreign capital see Munday et al., 1995; Welsh Government, 2009; see also Wren and Jones, 2009). However, the embeddedness of foreign plants also embraces the longevity and stability of activity supported.

This paper examines patterns of the entry and exit of foreign firms into and from the Welsh economy. Earlier analyses of foreign manufacturing stability and survival have been hindered, in part, by limits on data availability. However, Wales has an official database (Welsh Register of Manufacturing Employment) providing details of regional manufacturing entry and exits between 1966 and the mid-2000s. This offers an opportunity to examine foreign manufacturing entry and exit rates in Wales and builds upon an evidence base of relatively few UK studies (but see Jones and Wren, 2006; McCloughan and Stone, 1998; Stone and Peck, 1996; Wren and Jones, 2009).

The paper is set within the context of debates on how far inward investment across the UK regions, including Wales, has had a transforming effect in terms of improving regional economic development prospects. Examining the stability of the foreign sector, we believe, provides an answer to part of this puzzle. The paper addresses three questions: first, whether the evidence from Wales reveals that survival rates of foreign owned manufacturing firms are significantly higher than those for domestic firms; second, whether there is variation in survival rates in foreign manufacturing companies through different time periods; and third whether survival rates of foreign manufacturing plants vary in terms of employment size, industry sector and location within Wales.

The second section sets the analysis of foreign manufacturing stability in the context of regional debates in Wales (and other UK regions) on how far the presence of inward investment has had long term transforming beneficial effects on the regional economy. The third section reviews literature on foreign firm survival linking this through to issues of foreign ownership, age, size, timing of entry, industry and location. The fourth describes the database used for the analysis, and examines entry and exit rates of foreign manufacturing subsidiaries. The fifth section describes the method used to explore the comparative survival rates of foreign manufacturing subsidiaries, and discusses the results from the analysis. The final section concludes.

Why examine the stability of the foreign manufacturing sector?

Wales is an interesting lens through which to examine issues concerning the stability of foreign manufacturing plants. Research has highlighted the success of Wales in attracting inward investment (Hill and Munday, 1994). Tewdwr-Jones and Phelps (2000) considered Welsh advantages over other regions in terms of the inward investment process, and how the land use planning system had been used in the promotion and ‘gazumping’ in the location tournament process. However, while the Welsh Assembly and other devolved UK administrations may have had processual advantages in terms of bidding for mobile capital investments, there is a question as to whether these advantages are reflected in dynamic changes levered for the Welsh economy through new inward investment.

Accounts of the role of inward investment in Wales have been broadly positive, with research pointing to effects in terms of new jobs, higher exports and spillovers of new knowledge and techniques to indigenous firms (for a review see Welsh Government, 2009). However, regional claims of the more transformative effects of inward investment to Wales have been questioned. Indeed, the 1990s saw a significant policy shift towards the development of indigenous firms, and the role of the Welsh Development Agency (WDA) increasingly scrutinised with regard to overseas marketing (Welsh Government, 2009). Concerns about the role of inward investment were also voiced by authors such as Lovering (1999), who showed that the notion of a ‘new regionalism’ in Wales had been unjustly founded on assumptions about the transforming effects of foreign manufacturing investment. These notions had been ‘accompanied’ by a paucity of research showing how foreign investment had been involved in evolutionary processes of economic change in Wales. Indeed, Lovering (1999) questioned WDA activity on inward investment and claims of a resulting regional manufacturing renaissance: “The endlessly repeated claim that inward investment into Wales has had a transformative influence on the regional economy as a whole is entirely lacking in evidence. Over the decade to 1995 foreign direct investment created net very few jobs indeed (it is not possible to say exactly how few because no systematic research has ever been conducted.” (Lovering, 1999: 381)

Lovering shows the need for a more critical examination of the contribution of inward investment as opposed to a tendency merely to celebrate new inward investment. Others had also commented on longer term developmental concerns. Williams et al. (1992), for example, commenting on Japanese inward investment in the UK regions, showed that such investments featured lower value added functions and might have been better characterised as ‘warehouses’ rather than factories (see also Munday et al., 1995).

The context for our study is thus the historical concerns about the role of inward investment in regional economic development, concerns about the potentially transitory nature of selected investments, and then how far policy resources can be developed not merely to attract foreign firms but rather to make operations more sustainable through repeat investment. Analysis of the stability of foreign owned firms and their role in the evolutionary development processes should then be part of the wider policy evaluation process, and the discussion of how policy towards inward investors may have to evolve to bring about longer term developmental benefits. In this respect Phelps and Fuller (2000) showed that it could be important for policy resources to be used to cultivate the allegiance of capital. Phelps and Fuller revealed that the pro-competitive disengagement by government with regard to attracting inward investment may sit uneasily with policies that seek to improve the embeddedness of foreign capital. In particular, the need for significant levels of aftercare for inward investors might be seen as an admission that large sums committed in location tournaments have only succeeded in attracting enterprises to areas where they struggle to be successful because more weighty matters of regional production conditions have been ignored in decisions about location. More generally, Welsh Government (2009) highlighted a need for policymakers to question how well location marketing policies concerning inward investors were integrated into overall regional economic development strategy in Wales.

A corollary of this more critical appraisal of inward investment policy is that a more detailed appreciation of the role of inward investment needs to consider not only its role in job creation, but also the relative stability of the investment and jobs attracted. For example, Essletzbichler (2007) showed that it was a better understanding of the driving forces of job creation and destruction in British areas which was important for appropriate policy responses, and that net employment change figures can work to mask significant levels of job creation and destruction. An important question then is whether the relatively high inward investment job creation rates claimed for Wales are ‘marred’ by relatively high levels of foreign plant exit. Essletzbichler (2007) makes the key point that high rates of entry and employment are not necessarily the most important processes for generating net employment growth. Regions that are potentially transformed by the presence of foreign multinationals might also be characterised by low rates of foreign exit.

The analysis of the birth and deaths of plant in a region also connects to perspectives offered by evolutionary economic geography, and the processes through which regions transform themselves, and the processes by which the economic landscape, the spatial organisation of economic production, distribution and consumption, is transformed over time (Boschma and Martin, 2007). Geroski (1995) argues that understanding rates of exit and entry is important in examining the evolution of industry populations over time. Essletzbichler and Rigby (2007) showed that competition between agents based on the evolutionary factors of variety, selection and retention can work to produce distinct economic regions. Arguably, foreign owned firms are among the most significant agents in regions; patterns of entry and exit among such firms could work to influence the economic trajectories of a region such as Wales. Martin and Sunley (2006) also showed that it is unclear why selected areas become locked into development paths that lose dynamism, while other areas are better able to reinvent themselves through new development phases. Here, then, some regions find it more difficult than others to ‘shake free’ of their industrial history. In the context of these perspectives from evolutionary economic geography, the entry and exit of foreign firms in Wales could have important longer term effects – a matter of particular pertinence given the current focus of economic concerns in Wales on the long term persistence of a low skills equilibrium, low average productivity levels, and low levels of business spending on R&D (Welsh European Funding Office, 2013).

Wales is therefore a particularly interesting example for examining entry and exit of foreign plant. Our analysis addresses a challenge from Lovering (1999) for more detailed research to examine claims on the worth of the foreign-owned sector to the Welsh economy. It is believed that our findings may assist in the development of appropriate regional development policy, and provide insights into the forces driving the development path of the region, this in the context of persistent socio-economic disadvantage experienced by some parts of industrial Wales.

Foreign manufacturing entry and exit

There is a substantial body of work in the US, Europe and the UK that has addressed manufacturing exits. Key issues examined include the impact of general exits on national productivity, employment restructuring and employment change. Here, however, we focus the review on themes of ownership, industry, plant size, age and location, examined later through the empirical work.

Foreign ownership

The relative and absolute survival rates of foreign subsidiaries have been considered in a number of research studies in the UK and Ireland. This research has been linked to levels of public support given to inward investors and long-standing concerns – going back to the 1960s and 1970s – that subsidies and other types of assistance might attract more transient cost sensitive investment to peripheral areas. One consequence of this latter is that the attraction of weakly embedded foreign capital could deepen the ‘branch plant syndrome’. McAleese and Counahan (1979) examined the statistical relationship in Ireland between foreign plant size, marketing autonomy and employment performance. They concluded, from a study of exit rates, that multinational enterprises were no more footloose than their domestic counterparts. Studies analysing historical employment statistics for the UK regions also revealed greater stability in the foreign sector at times of domestic economic problems (see Hill and Munday, 1994; Welsh Government, 2009). Stone and Peck (1996), using an analysis of components of change, examined the stability of foreign-owned manufacturing plants across four UK regions, including Wales. One of their conclusions was that regional inward investment success was not determined merely by the opening of new foreign plants, but included consideration of strong performances in other components of change such as closures, acquisitions, exits and in-situ changes.

Another study focusing on the foreign sector in the UK was that of McCloughan and Stone (1998) who undertook a duration analysis of 252 plants in the North East region between 1970–1993 estimating the contribution of plant level characteristics seen to affect survival rates. They revealed that greenfield entrants were characterized by a lower risk of failure than acquisition entrants. This was linked to factors such as problems in integrating acquired subsidiaries, acquisition being a root to industry rationalisation, and new greenfield entrants having access to up to date technology and being more likely to benefit from employment and capital subsidies.

More recent detailed research has also taken place in the North East region. Jones and Wren (2006) found that the overall probability of longer duration of survival of inward investors was greater for plants pledging more than 50 jobs and in plants that were involved with the regional development agency. A key theme in this research was factors affecting prospects for re-investment, with the study revealing that the probability of reinvestment increased then decreased with plant size, and increased based on whether or not firms had received financial assistance. Wren and Jones (2009) examined 265 plants with foreign ownership in the North East that started operating after 1985. The study used a proportional hazards model to analyse plant survival behaviour; it was found that, in comparison to domestic plants, foreign-owned plants had higher exit rates. Importantly, however, in an analysis of reinvestment patterns and impacts on survival duration, Wren and Jones found little support for re-investment as a source of plant embeddedness.

To summarise: the issue of ownership is identified as one potential factor affecting survival duration of plants in UK regions. The evidence from Wales on foreign and domestic firm employment trends during the recent past (see Welsh Government, 2009) leads to the prior that foreign firms may be characterised by better survival rates than domestically owned firms. However, the nature of the data available to this study limits the avenues that can be pursued within the theme of ownership. For example, international research deals with the expected significance of issues such as mode of entry/type of investment (i.e. greenfield, or through merger and acquisition) in influencing survival outcomes (see for example, Li, 1995). The nature of the data used later in the present paper make it difficult to comment on how this factor would affect survival duration in Wales.

Age, entry date and size

Wren and Jones (2009) showed that the size and age of a plant are expected to be factors explaining the survival duration of foreign subsidiaries. These factors could have a strong effect on trends in re-investment and the size of a foreign subsidiary might affect its ability to secure new funding and re-investment. Size might link to the level of sunk costs committed, and the ability of a foreign subsidiary to compete with other subsidiaries for subsequent rounds of investment in new products (see Phelps and Fuller, 2000).

Li (1995) revealed that the exit rate of foreign owned firms increased with the age of the operation – but only up to a certain point. Li used the term ‘honeymoon effect’ to describe this pattern, showing that the initial resources used to support the subsidiary could insulate it from early failure. Age of plant might also link to the experience of the host nation with multinational firms, and this has also been shown to affect survival prospects (see, for example, Delios and Beamish, 2001).

Both the age and size of subsidiaries have also been important themes in other UK studies. For example, McCloughan and Stone (1998) explored whether the hazard function facing foreign firms in the North East region displayed negative duration dependence; that is, the longer the foreign plant survives, the lower its risk of failure becomes. They contend that this might be the case because foreign firms use their ownership advantages gradually and suggest that the possibility existed of foreign firms developing new ownership advantages post-entry. In addition, in a study by Evans et al. (2009) of foreign firm exits in Wales for the period 1985–2007, analysis of the hazard rate revealed that the date of entry into Wales was a factor in survival duration.

Industry effects

Earlier empirical work internationally and in the UK would also suggest that exit (and entry) rates vary across industry types. The fact that foreign subsidiaries differ in terms of product life cycle position could also give rise to variation in exit rates by industry. In Wales, for example, there have been noticeable periods of displacement of more labour intensive manufacturing sectors such as electrical engineering to locations in Eastern Europe and further afield due to the relative cost competitiveness of these latter areas (Welsh Government, 2009).

More generally, Driffield (1999) studied a series of industry-specific factors associated with foreign manufacturing entry and exit and revealed that higher rates of exit were connected with low profitability, low overall industry growth and low net capital. Driffield also found that foreign firms were unlikely to exit industries where such firms possessed a strong productivity advantage.

Location

The location of plants may also have an effect on exit rates. There might be an expectation that firms locating in assisted areas, or assisted parts of regions, could be more marginal (i.e. more grant dependent), and thus have lower survival rates. This has been an underlying theme of a series of analyses of the relative employment stability of foreign owned plants, and the longer term value for money in using policy resources in the form of grants and subsidies to foreign investors (see earlier). Assisted areas offering higher levels of grants and subsidies may suffer from not having the wider infrastructure of skills and suppliers needed to embed foreign firms. However, Jones and Wren (2006), in their study of inward investment in the North East of England, did show that the probability of reinvestment increases where firms have received grant funding.

In this paper, dealing with experience in Wales, we are only able to explore whether there are differences in exit rates between plants in areas receiving different levels of assistance. However, spatial data in greater detail on plant location could shed light on more subtle location issues, including whether firms have plants co-located on the same site, whether plants are co-locating close to similar industrial activity and whether plants that exit subsequently relocate to other parts of the region (see for example, Wren and Jones, 2009 for a discussion of these types of issues).

Foreign manufacturing in Wales

General background

Foreign manufacturing has a long history in Wales, with the first recorded firm (Monsanto) arriving in 1895. By 1974 foreign owned manufacturing employed an estimated 53,000 people. North American firms dominated foreign inward investment into Wales until the 1970s (Davies and Thomas, 1976). The quantity of European and Japanese manufacturing investments in the Welsh total increased sharply in the 1980s. There was a shake-out in Welsh manufacturing after 1980 and, by 1984, foreign owned manufacturing employment had fallen to around 40,000, but rose steadily after this reaching an estimated 75,000 by 1996. Munday (2000) showed that employment and output in the foreign owned manufacturing sector in Wales was relatively stable in the 1980s and 1990s; but underlying that stability was a growing number of foreign takeovers of domestic firms (see also Phelps (1997) for further analysis of the embeddedness of the foreign sector in the Welsh economy).

Wales was relatively successful in attracting foreign direct investment in the 1980s (Hill and Munday, 1994). Over the whole period since 1980, Welsh Government (2009) reveals that it was expansion projects that comprised the largest share of total foreign projects success, followed by new projects. In total Wales is estimated to have secured almost 1500 overseas inward investment projects between 1984 and 2007, with an estimated £13.5bn of planned capital investment, and almost 100,000 planned new jobs and 70,000 safeguarded jobs (Welsh Government, 2009; for recent commentary on Welsh inward investment trends see Crawley et al., 2012).

Data on foreign manufacturing exits

The main sources of statistical data for examining foreign direct investment trends into Wales are the Census of Production (for the period until 1997) the Annual Business Inquiry (from 1998) and the Inter-Departmental Business Register and the Business Register and Employment Survey after 2008. These tend to focus on employment and output indicators and provide little information on the life duration of foreign plants.

There are, however, additional data sources. One is the Welsh Register of Manufacturing Employment (WRME), initially compiled by the Welsh Office, and most recently by the Welsh Government, before being discontinued in the mid-2000s. The WRME maintained a record of manufacturing plants with more than 10 employees at a single site in Wales. The information recorded on WRME was collected at the end of each calendar year using a postal survey and telephone follow-up. Additional updating in-year was undertaken using a range of statistical and administrative sources such as the Census of Employment, Census of Production, Inter-Departmental Business Register (IDBR) and Dun & Bradstreet data.

The primary variables recorded on WRME are employment, industry, initial country of ownership, existence or not of the plant as part of a multi-plant enterprise, location, and opening and closure dates. In some cases (partial) data are also available on the type of opening, being a New Branch, the new plant being opened by an enterprise with other manufacturing units already in operation, being a Transfer, formation of the new plant corresponding or not to a closure of one or more existing plants, being an Enterprise New to Manufacturing (ENM), and the new plant being opened or not by an enterprise previously not having other plants within the regional manufacturing sector.

To make full use of the time series and cross-section dimensions of the WRME data a complete list of records was extracted, resulting in records on 6372 plants with at least one year’s worth of data. 1

Manufacturing plant entry and exit 1966-2003

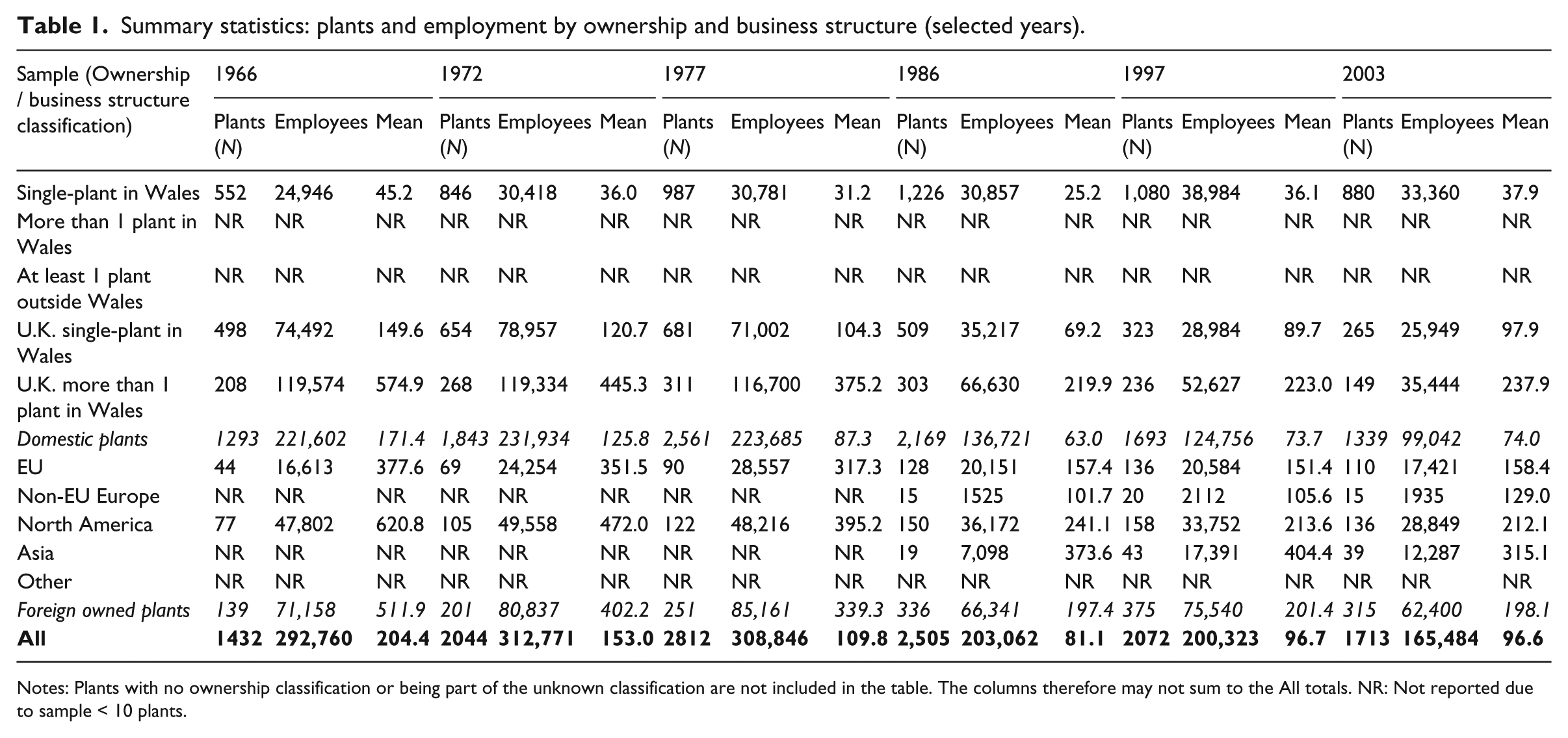

In what follows we summarise some of the findings from an analysis of the WRME database. Selected material here is derived from an initial analysis undertaken by Paull (2007). 2 From the 6372 records taken from the WRME, data on 6115 domestic and foreign plants remained for the analysis after some cleaning for incomplete records. Table 1 reveals the composition of the records for selected years between 1966 and 2003. Across all years of the dataset the primary geographies of origin for the recorded foreign owned plants are the European Union and North America (in 2003 providing 34.9% and 43.2% of foreign owned plants, respectively), with plants owned by Asian companies additionally providing a notable component. Over the full time period there is evidence of a trend towards an increased relative representation for foreign owned manufacturing plants, rising from 9.7% of total plants in 1966 to over 18% since 1997.

Summary statistics: plants and employment by ownership and business structure (selected years).

Notes: Plants with no ownership classification or being part of the unknown classification are not included in the table. The columns therefore may not sum to the All totals. NR: Not reported due to sample < 10 plants.

Examination of the estimated mean average size by employee numbers (see Table 1) suggests that Welsh-owned single-plants have tended to have the smallest mean size. The data also suggest a trend of declining mean plant size for both domestic and foreign owned plants during the period from 1966 to the mid-1980s, in the case of domestic owned plants falling from 171.4 employees in 1966 to 63.0 employees in 1986 and for foreign owned plants from 511.9 in 1966 to 197.4 in 1986 before both stabilising at a mean plant size of around 70 employees and 200 employees, respectively. The similarity in the percentage decline of mean plant sizes is an interesting feature, perhaps suggestive of wider-ranging factors concerning changes in manufacturing technologies and production; however, this is a question requiring more detailed research and is not specifically addressed in this study.

The data on recorded total stock of plants show an increase from 1432 plants in 1966 to a peak of 2812 in 1977. After this there was a fairly persistent decline, with the stock of plants reaching 1713 plants by 2003. However, the data on foreign-owned plants in the database show a very different pattern. In 1966 there were 139 records for plant on the database. With the exception of a few years in which foreign plant numbers fall, the trend was steadily upwards until 1991, when there were 394 foreign plants recorded. Between 1991 and 2000, numbers of foreign plants hovered around 370 before falling more sharply in the period 2000–2003. At the end of that period there were 315 foreign plants on the database.

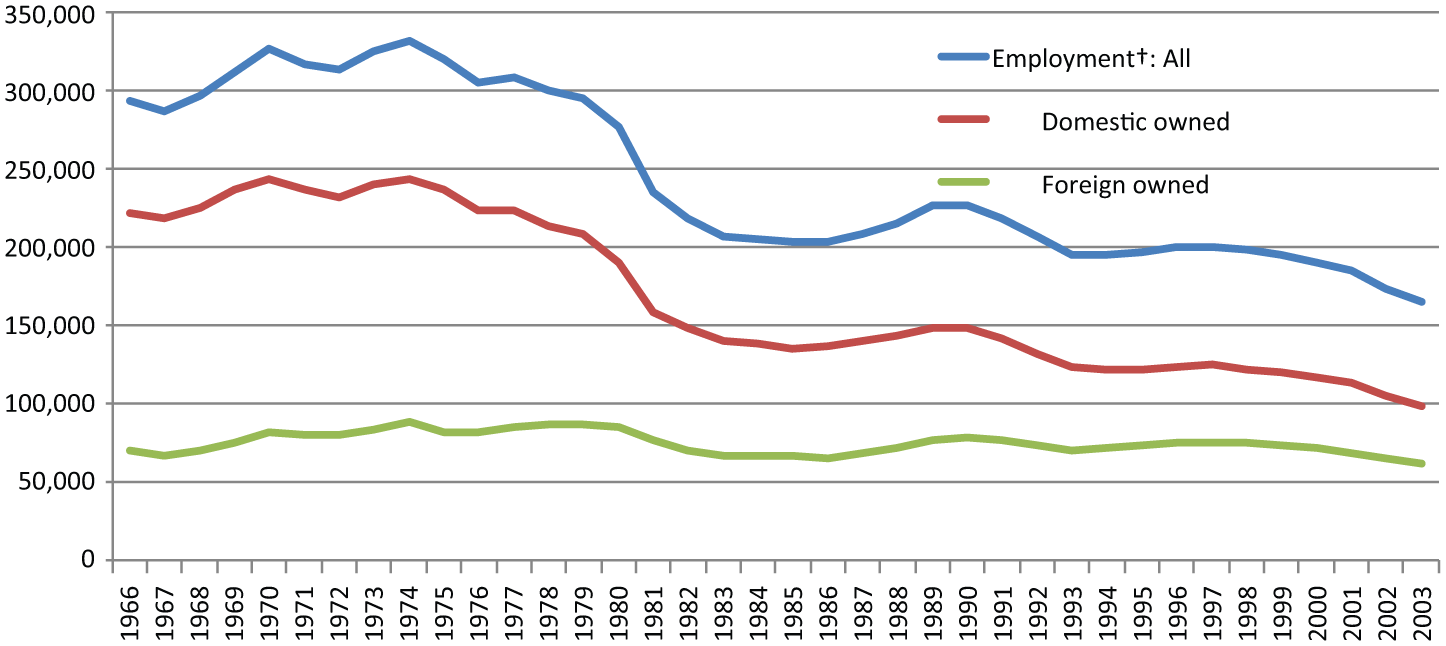

Figure 1 summarises the aggregate time series of employee numbers on the database. This exhibits a general increase from the initial 1966 base period of 292,760 employees (but falling to 286,706 in 1967) to peaks of 327,245 employees in 1970, followed by a modest decline until 1972, before rising again to a peak of 332,353 employees in 1974. A generally modest rate of decline then follows until around 1979, followed by a significant sharp fall in recorded employment reaching 207,137 employees during the recession of the early 1980s, representing a decline of 37.7% between the peak of 1974 and 1983. The data from 1983 onwards exhibit some measure of greater stability, with a period of employment recovery from 1986 to around 1989, reaching 227,656 employees, before reverting to a more general pattern of decline which, according to these data, had perhaps accelerated slightly since around the end of the late 1990s.

Estimated employment in foreign-owned and domestic plants in Wales (Source: WRME database 1966–2003).

Of interest is the role of foreign manufacturing industry employment in the total. In 1966, employment in the foreign-owned sector was a little over 71,000: this reached nearly 89,000 in 1974 and still stood at over 86,000 in 1980. During the early 1980s there was a major shakeout in all manufacturing in Wales and during the period 1983–1986 around 67,000 people were employed in the foreign owned plants. Thereafter there was steady growth until 1990. Foreign manufacturing employment totalled over 70,000 employees through the 1990s, but there was a noticeable decline in employee numbers after 1998. However, Figure 1 reveals that the contribution of foreign manufacturing to total manufacturing employment tends to have increased through time until 2003. For example, on average through the 1970s foreign manufacturing employment was 27% of total employment, in the 1980s it was 32%, and 39% in the 1990s.

As noted earlier, in addition to the growth or decline in employment in incumbent plants, the observed size distribution on the WRME database is also likely to be influenced by the entry of new plants and exit of existing plants. From the cleaned WRME dataset, information on opening dates was only available for 4662 plants (of which 739 plants were recorded as having opened before 1966) with records for 3252 plant closing dates. To address these data gaps the available information was supplemented by additional estimates using the observed data on beginning and final years of employment for each individual plant time series as proxies for opening and closing dates. Plants without a closure date and with employment information in 2003 were assumed to have remained in operation. Where no such information was entered for a plant it was assumed that the plant closed during 2003. Although it may be that for some plants this simply represented a single point of missing data in 2003 rather than closure, no other appropriate treatment is obviously available in the absence of further information.

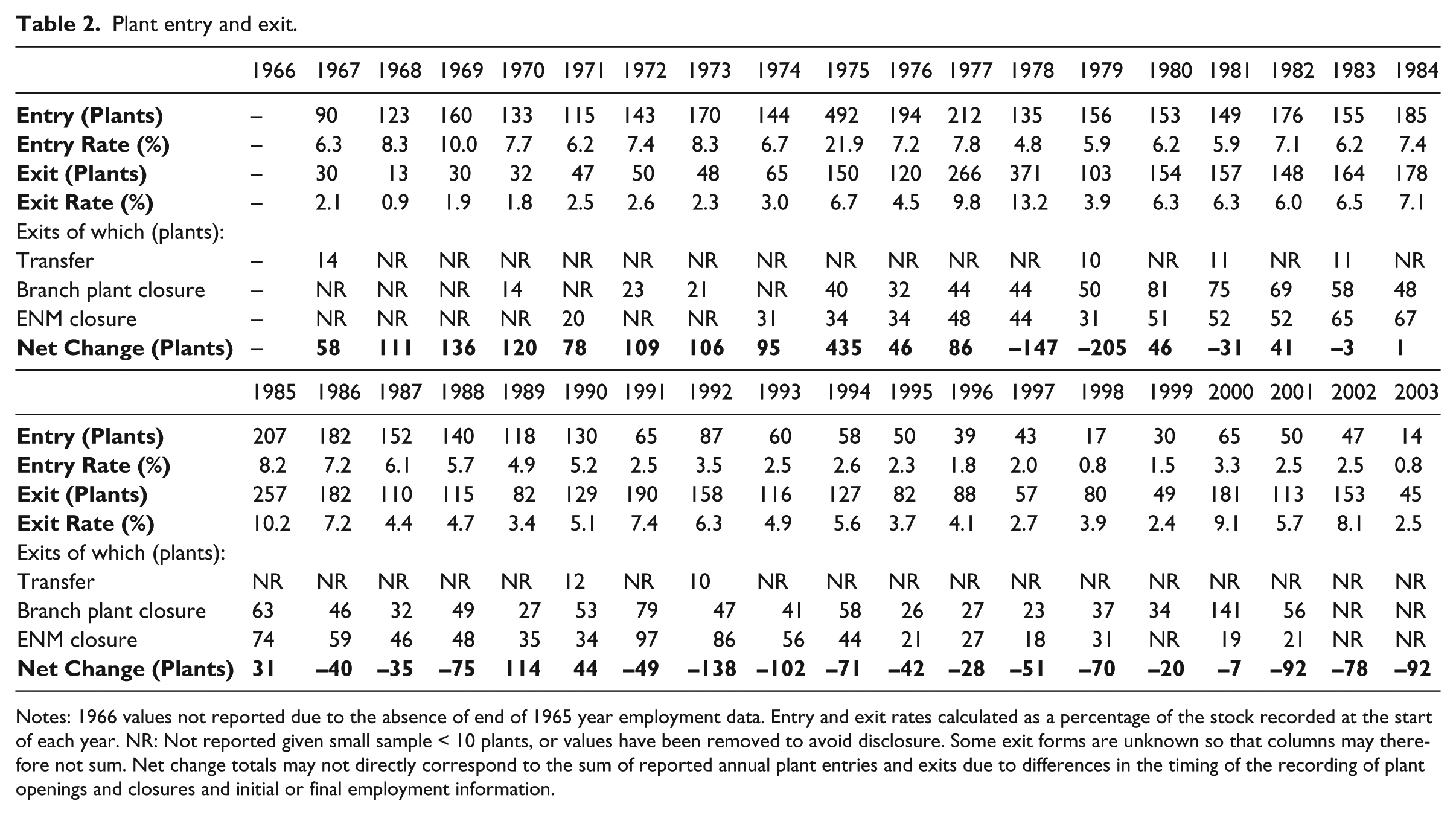

Examination of the data on constructed plant entry, presented in Table 2, suggests some volatility, peaking at a high of 492 newly recorded plants in 1975 (a year with an unusually high number of recorded plants with employee numbers below the more than 10 employees official threshold) 3 and reaching a low of just 14 recorded new plants in 2003.

Plant entry and exit.

Notes: 1966 values not reported due to the absence of end of 1965 year employment data. Entry and exit rates calculated as a percentage of the stock recorded at the start of each year. NR: Not reported given small sample < 10 plants, or values have been removed to avoid disclosure. Some exit forms are unknown so that columns may therefore not sum. Net change totals may not directly correspond to the sum of reported annual plant entries and exits due to differences in the timing of the recording of plant openings and closures and initial or final employment information.

In the case of the latter figure relating to plant exit in 2003, this could also reflect specific data collection issues in the final years of operating the dataset and with the series being discontinued shortly afterwards. However, the plant entry figure has been consistently below 100 since 1991. Excluding the year 1975, the entry rate (measured as a percentage of plant stock) was generally stable throughout the 1970s to the mid-1980s, at around 6%–8%. However, from around 1987 onwards a notable decline in entry rates is observed, falling from 6.1% to around 1.5%–3.5%, perhaps reflecting changes in technologies and market conditions in some parts of the manufacturing sector in Wales.

Plant exits exhibited an increase from the late 1960s to a peak, in 1978, of 371 plants exiting, since when there has been some volatility with further peaks in 1985 (257 exits), in 1991 (190 exits) and in 2000 (181 exits). Exit rates also exhibit volatility, ranging from a low of 0.9 % in 1968 to highs of 13.2% in 1978 and 10.2% in 1985. The data suggest greater volatility in plant exit rates than entry rates, which, again, may reflect to some extent the structural changes in the manufacturing sector experienced during this time period (1978 to 1985). This could also reflect closures linked to changes in the economic cycle; for example, high exit rates occurred in the late 1970s and early 1980s during a recessionary period. However, the data on periods of high exit rates do not always correlate well with periods when the UK experienced recession. Pike (1999), in a study of the North East of England, revealed that an effect of inward investment arriving in waves could be associated with periods of regional economic stability, but then periods of instability. For example, it is possible that firms which enter as a wave also exit in similar waves. This pattern appears to have occurred with much of the Japanese investment that entered Wales in the early 1980s in response to tariff pressures (Munday et al., 1995), but which subsequently relocated to Eastern Europe and further afield in response to the availability in those territories of cheaper labour costs, and with selected products entering the decline stages of their product cycles.

From 1966 until 1977 the numbers of recorded annual plant exits were lower than plant entries, resulting in a positive net effect on the stock of plants. Between the years 1978 and 1990 the picture was more mixed in terms of the net contribution to plant stock, with particularly significant net plant losses in 1977 and 1978. In every year after 1990 the recorded stock of manufacturing plants has been in decline.

Closer inspection of plant entry and exit by size-classes showed that plant entry was primarily into the smaller size-classes, including into the size-classes below the WRME recording threshold, especially in the period 1975–1977. The constructed data on plant exits by size-class indicate a very limited exit of larger plants, with most exits (in absolute terms) occurring in the smaller size-classes, particularly around or just above the official recording size threshold.

Examination of industry-level entry across the full time period (post-1966) of the dataset showed a relative concentration in Fabricated Metal Products, providing 588 new entrants, Other Machinery and Equipment (484 new entrants), Furniture (383 new entrants) and Rubber and Plastic Products (381 new entrants). Similarly, plant exits were highest in Fabricated Metal Products, where 569 plants exited, and Other Machinery and Equipment (470 exited). Such information clearly suggests some consistency with regard to those industries having the highest levels of entry and exit. Constructed data on entry and exit rates by industry in many cases provided very small samples, precluding any significant analysis from being presented.

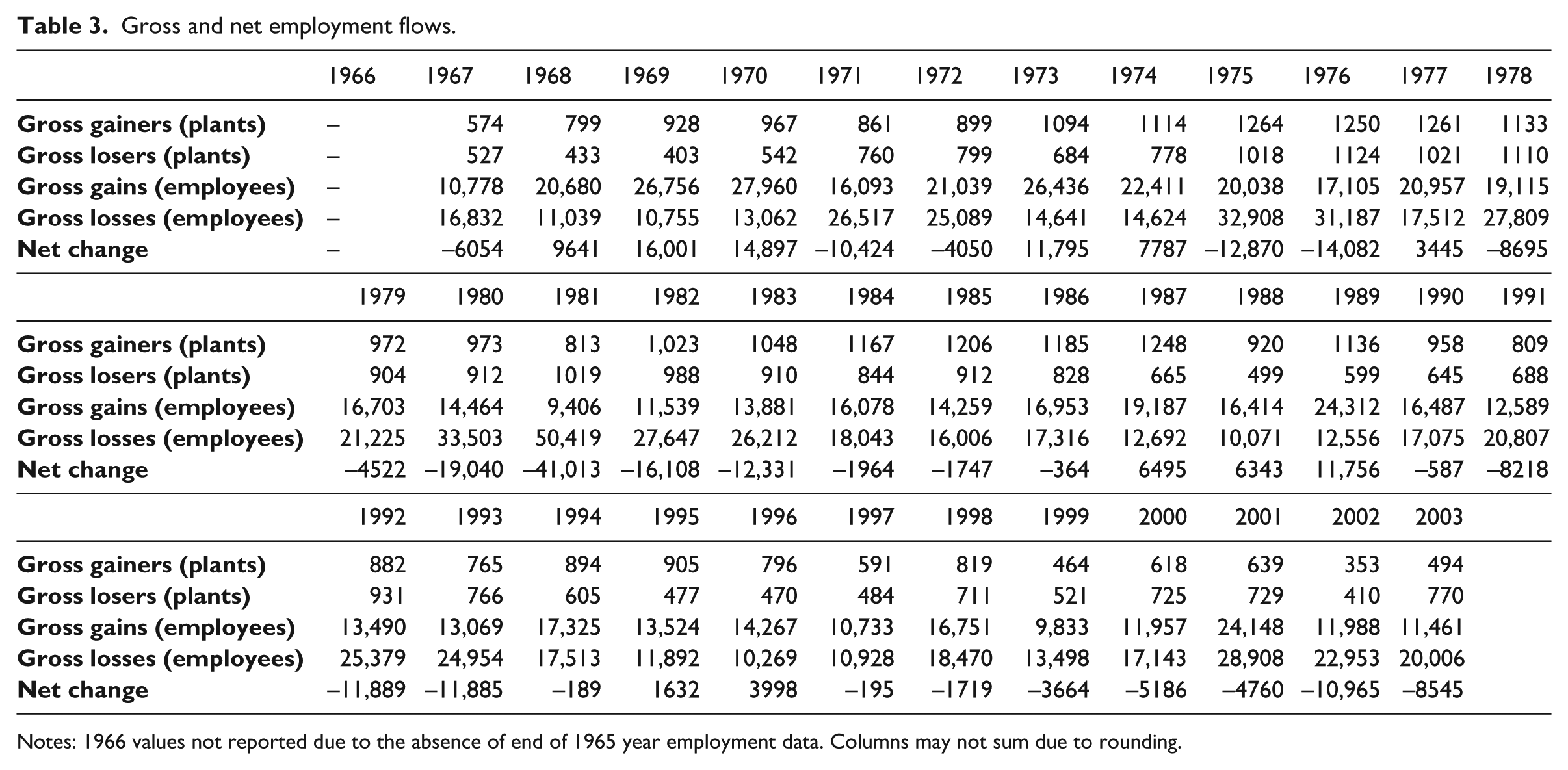

Bringing together the data on plant entry and exit and the changes in employment in incumbent plants, gross and net employment flows were constructed for the time period 1967–2003 (1966 not being examined due to the absence on information on the initial stock of plants and employment for the beginning of that year). Given the problem in some cases of matching precisely the opening and closure dates with initial and final employment records, a full decomposition of components of change, into the effects of entry, exit, expansion and contraction, is difficult: the discussion here considers gross and net flows – gross gains in employment arising from the contribution of entry and plant expansions, and gross losses from contractions and plant exits, the net flow being the sum of these effects.

The data, set out in Table 3, indicate significant annual gross gains and losses in employee numbers with the gross employment flows being considerably larger than the net flows recorded for each year, both gross flows generally being above 10,000 employees. Over the whole time period the average employment gains were 16,762 per annum with average losses of 20,202, a net average loss of 3,440 jobs each year. However, it is not the case there has been an even and continuous process of net employment erosion within the manufacturing sector in Wales. Interestingly, however, in almost every year of the data (except for 1981, 1992 and each of the years after 1999) the number of plants experiencing increased employee numbers exceeded the number of plants exhibiting reduced employee numbers.

Gross and net employment flows.

Notes: 1966 values not reported due to the absence of end of 1965 year employment data. Columns may not sum due to rounding.

Comparison of the gross gains and losses data indicate short periods of intensive employment shakeout in 1971, 1975–1976, 1980–1983, in the early 1990s and again in the early 2000s. The net employment effects were over 100,000 job losses in the period 1978–1983, a further net loss of almost 32,000 jobs between 1991–1993 and over 33,000 jobs lost in the period 1999–2003. The fall in gross gains to a low of 9406 employees, in combination with the increase in gross losses of over 50,000 employees in 1981, had a particularly significant effect, reducing overall recorded manufacturing employment by over 41,000 employees in that year.

Estimation and analysis

Having described general trends in the WRME dataset the analysis now switches to consider whether foreign firms in this dataset exhibited stronger survival rates than other firms, and what factors might account for this. To examine the effect of ownership on plant/firm survival, a Cox proportional hazard model is used. This specifies the hazard function as

where

The variables used are derived from the data discussed above. The dependent variable is the survival rate based on the length of time the plant/firm has operated in Wales. The explanatory variables include firm ownership measured as a series of dichotomous variables according to whether the plant/firm is foreign owned (‘Foreign’), Welsh owned (‘Wales’), other UK owned (‘UK’) or if ownership is not known (‘Own NK’). UK-owned firms are taken as the reference group in the more detailed analysis of ownership patterns. There is some expectation that the ’Own NK’ category in WRME data may be acting in the same way as a micro firm dummy, with 97% of the firms categorised as not known employing 10 people or fewer, and with 71% employing 5 people or fewer. The prior here, following the review, is that firms which are foreign owned will be characterised by better survival rates and thus lower hazard ratios than domestically owned firms. There are also dichotomous variables for whether the plant/firm was located in an Intermediate or Development Area within Wales (‘INT AREA’ and ‘DEV AREA’ respectively) and describing 23 separate manufacturing industry groups in terms of two digit Standard Industrial Classification (2003). Regarding location, there is some expectation that firms locating in assisted areas (locations where they receive subsidies) could be more marginal through time (i.e. more grant dependent) and thus have lower survival rates. The review has also highlighted that industry affiliation can have an affect on the likelihood of survival (Driffield, 1999). For example, over the period under consideration there has been displacement of more labour-intensive manufacturing sectors such as electrical engineering to locations in Eastern Europe and further afield due to the relative cost-competitiveness of these territories.

The explanatory variables also include the level of employment in the plant/firm. There is some evidence from our review that employment size can affect the likelihood of survival in different ways. For example, Phelps and Fuller (2000) showed that the propensity for repeat investment at a given subsidiary could be associated with factors such as the extent of sunk costs, which could be linked to subsidiary size. We experimented with a series of employment variables, including average employment size during the life of the plant/firm, minimum and maximum employment levels, and initial employment size. Log and quadratic specifications were also examined. In each case there was little variation in the underlying results as a result of different definitions of employment used. In what follows, where the employment variable (‘EMPLOY’) is reported it reflects average employment during plant life. Finally, there is a created variable measuring the age of the plant/firm since its inception (‘AGE’): while for many plants/firms this coincides with years of survival, this is not always the case.

Table 4 presents the results from a series of different specifications of the hazard regressions covering the whole of the period 1966-2003. Model 1 of Table 4 shows that foreign owned plants have a significantly lower hazard ratio (0.41) and therefore better survival rate than domestically owned plants/firms. In Model 2 the issue of ownership is further disaggregated. In comparison to rest of UK owned plants/firms foreign firms have a hazard ratio of just 0.30 indicating a significantly better chance of survival. Interestingly Welsh owned plants/firms are more likely to have survived during the period than those where the ownership is located elsewhere in the UK. This might suggest that the latter are especially prone to closure during economic downturns as operations are maintained at headquarter locations. Finally plants/firms where ownership is not known in the data are found to have significantly lower survival rates than those in the other ownership categories. As noted above this category is likely to contain a number of very small plants and the result may reflect the susceptibility to closure of these plants over time.

Basic hazards 1966–2003.

Note: Log L gives the maximised log-likelihood value. LR gives the likelihood ration test value. *p < 0.01; **p < 0.05.

In order to consider the relatively better survival rates for foreign owned firms/plants, a number of additional explanatory variables are included. In the first place we examine whether the success of the foreign owned plants is related to employment size (Model 3). Here the variable ‘EMPLOY’ reflects average employment in the plant/firm during its life time. The inclusion of this variable, acting as proxy for the size of plants/firms, has very little effect on the hazard ratio for any of the ownership groups. The results suggest that larger plants/firms survive longer than smaller ones and this explains, albeit marginally, the favourable performance of foreign plants/firms. In contrast, it is the smaller Welsh-owned firms that have better survival rates compared to their UK-owned counterparts.

In contrast, the addition of the ‘AGE’ variable in Model 4 works to improve the hazard ratio for foreign owned firms to 0.23. There is a suggestion here that older foreign firms may have better survival prospects, having overcome the liability of foreignness and then successfully using their ownership advantages over longer periods (see McCloughan and Stone, 1998). There would also seem to be a similar advantage to locally owned firms.

Finally, dummy variables to capture whether a plant/firm locates in a grant assisted area are added, in Model 5. There is some indication, perhaps surprisingly, that plants/firms located in these areas have better survival rates than those located in areas where regional incentives are not available. However, the inclusion of these variables has little effect on the hazard ratio for foreign plants/firms or indeed that of either of the other two ownership groups.

The conclusion from Table 4 is therefore that ownership is important as far plant/firm survival is concerned and that the inclusion of other important influences on the likelihood of survival does little to counter that finding. Moreover, there is evidence that foreign-owned plants are more likely to survive over time than other plants/firms. Indeed, even when the specification in Model 5 of Table 4 was supplemented with 23 industry dummies (detailed results not shown here) the hazard ratio for foreign ownership was little changed (0.26): a further conclusion, therefore, was that the relatively better survival duration of foreign firms in Wales was not due to industry sector specific effects. There is a suggestion from this analysis that foreign firms are more likely to be found in sectors such as chemicals, office machinery and medical equipment which had better overall survival prospects over the period than those in sectors such as clothing and leather, and basic metals and fabricated metals products.

Finally, the analysis focused on the stability of the foreign-owned plant hazard ratio over different time periods defined to capture different complete economic cycles over the period (see HM Treasury, 2005). Five time periods were selected and the final specification in Table 4 is used in each case. Looking first at the earliest period 1966–1971 (see Table 5), the survival rates for foreign plants are marginally higher than for UK-owned plants/firms, but this result was found not to be significant. Indeed, there is little evidence to suggest that ownership patterns have an effect on the likelihood of firm survival during this period.

Foreign firm hazard ratio through time.

Note: Log L gives the maximised log-likelihood value. LR gives the likelihood ration test value. *p < 0.01; **p < 0.05.

In contrast, over the period 1972–1977 foreign-owned plants are found to have better survival rates, with a hazard ratio of 0.62, although locally-owned firms have a slightly higher risk of closure than those where ownership is outside Wales but in the rest of the UK. Over the remaining three periods the foreign-owned firms continue to reveal lower hazard ratios, as do Welsh-owned firms. The stronger survival rates overall for foreign owned plants thus reflect their performance during the 1980s and beyond.

Conclusions

This study reveals that foreign-owned manufacturing in Wales is associated with better survival prospects than domestic and indigenous regional firms, and that findings on better survival are robust in the context of a series of size, industry and age effects. The study also reveals that the relatively lower hazard ratio is a consistent feature of the foreign manufacturing sector over time. A limitation of this study relates to the unfortunate discontinuation of the WRME database shortly after 2003: it would have been very interesting to explore the relative hazard ratio during the most recent, global recessionary period (i.e. from 2007).

We argued in the opening section that Wales was a useful lens through which to examine questions of foreign sector stability. Much had been made of the success of Welsh historical inward investment and its role in achieving a manufacturing renaissance, albeit with some authors such as Lovering (1999) questioning its role in transformative regional development processes. There are also debates on the balance of policy resources, between attracting new capital and improving the allegiance of foreign capital. Our results reveal that on one facet of embeddedness linked to stability and survival the foreign manufacturing sector performs relatively well. This might be taken as evidence in favour of the use of monies to support new inward investment. However, the opening part of the paper also showed that embeddedness covers other factors, such as the functions undertaken in foreign subsidiaries and the buyer–supplier linkages, maintained by foreign firms, which include a means by which knowledge passes from multinational to domestic enterprises. While the results show that relatively high levels of historical inward investment success are not marred by a lack of stability in foreign plants, there is still a question of the nature and quality of the stock of foreign manufacturing plant.

In this respect the methods adopted in our paper focus on what can be more easily quantified in terms of entry and exit. Lovering (1999) revealed the challenge to develop the evidence base on the contribution of inward investment. The methods adopted in this paper can only take us part-way to developing this evidence base in full. For example, the earlier review showed that other factors, such as the level of local decision making capacity in inward investors, the types of occupations supported, and embeddedness in terms of local supply chain linkages, are also expected to be important in assessing how far inward investment is developing to transform the region. There is then a challenge here for deeper analysis to reveal more about the changing characteristics of the stock of inward investment in Wales. This would need to progress using more qualitative methods such as in-depth case studies. In summary a survival analysis only disentangles one part of the puzzle relating to how far inward investment into a regional economy might or might not be transformative.

Moreover, following from the perspectives offered from evolutionary economic geography, the survival analysis only provides some insights into what exactly is being reproduced in the region through foreign entry and foreign exit, with other characteristics of the stock (that is, in terms of depth of function, and local linkages) having a strong influence on the economic trajectory of the region, locking the region into one development path (see Martin and Sunley, 2006).

In this respect one regional challenge identified has been to try to attract firms which score well on other facets of embeddedness, including a need to attract more ‘HQ-type’ operations in the region (see Welsh Government, 2009). Indeed, government inquiries initiated in 2012 into how far Wales might gain tax-varying powers could link closely to the potential to gain more higher value added ‘HQ-type’ functions in local foreign manufacturing firms (Silk Commission, 2012).

In conclusion, the paper inevitably raises a challenge for more research to be undertaken in Wales to understand the connection between inward investment and the evolutionary trajectory of the region.

Footnotes

Acknowledgements

We are very grateful to the Welsh Government for access to data in the Welsh Register of Manufacturing Employment (WRME), without which it would not have been possible to complete this analysis.